ACA (Obamacare) Impact On Individuals Chapter 3 1 Premium Tax Credit (PTC) 2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACA (Obamacare)

ImpactOn Individuals

Chapter 31

Premium Tax Credit

(PTC)

2

3

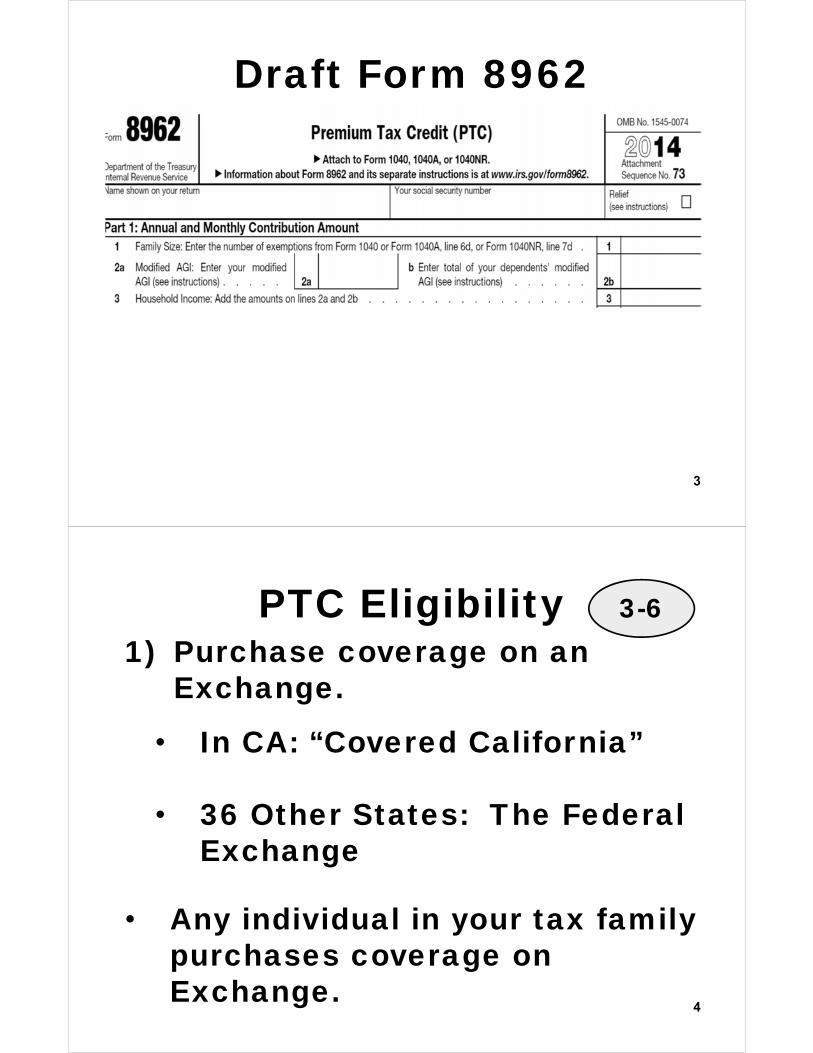

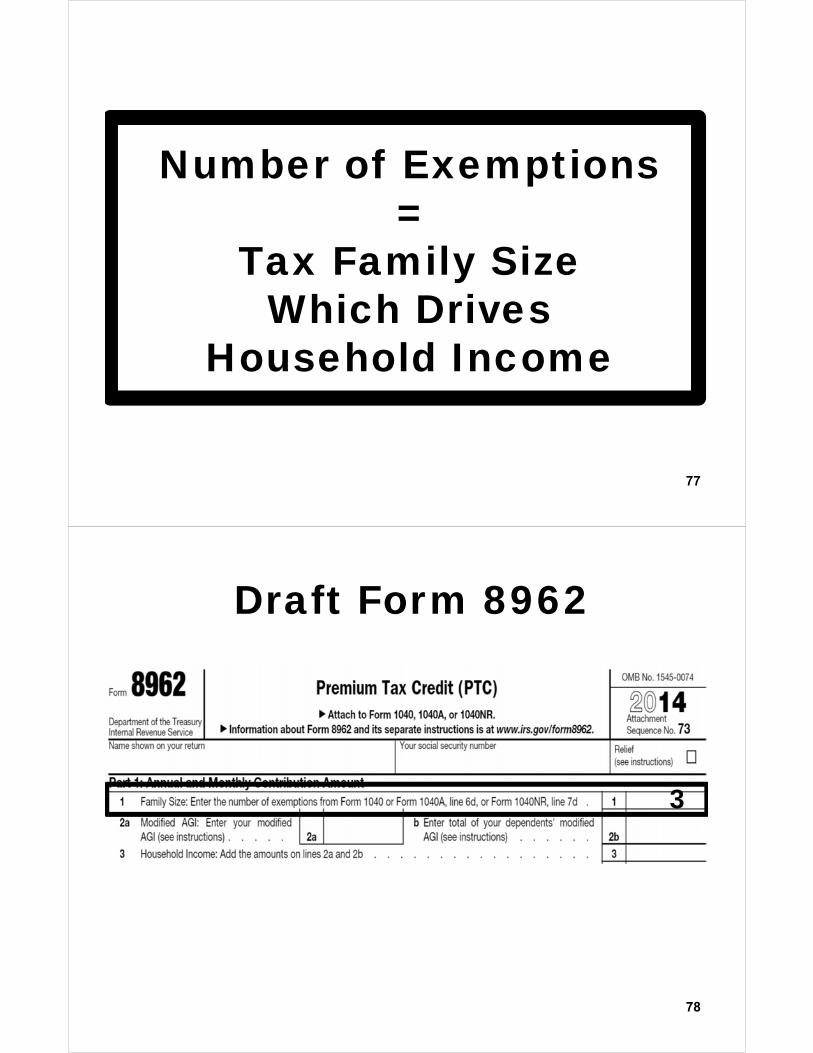

Draft Form 8962

4

PTC Eligibility1) Purchase coverage on an

Exchange.

• In CA: “Covered California”

• 36 Other States: The Federal Exchange

• Any individual in your tax family purchases coverage on Exchange.

3-6

5

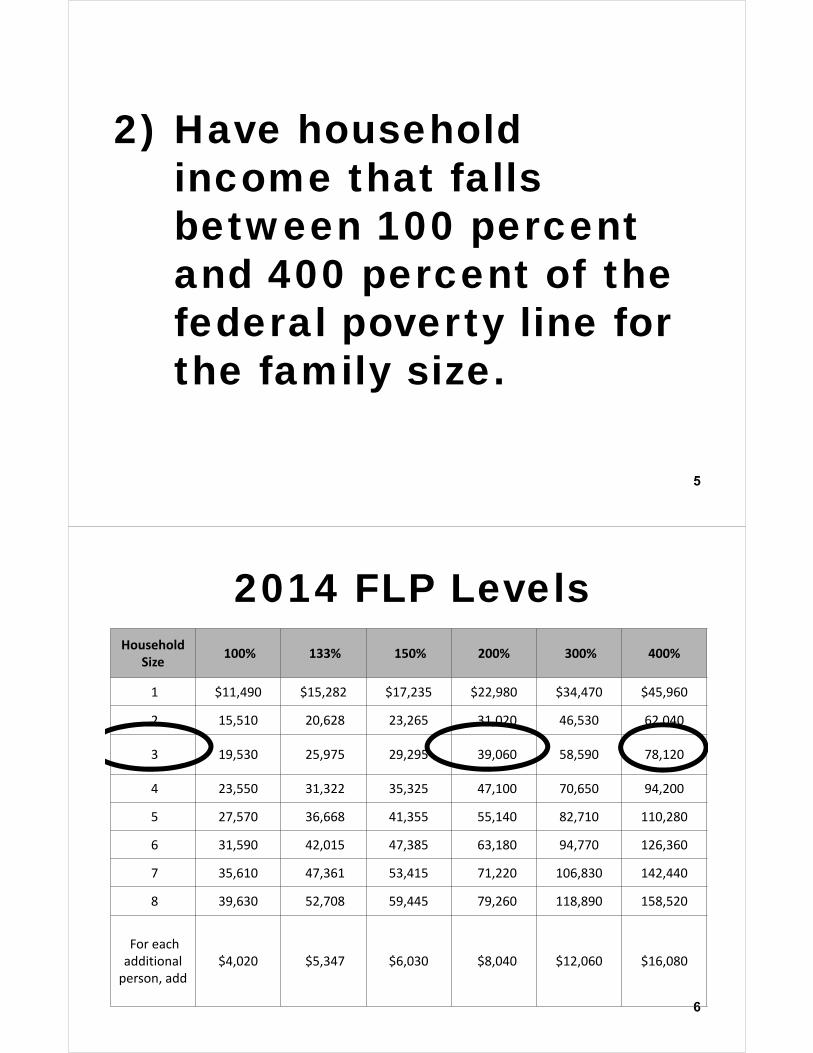

2) Have household income that falls between 100 percent and 400 percent of the federal poverty line for the family size.

6

Household Size

100% 133% 150% 200% 300% 400%

1 $11,490 $15,282 $17,235 $22,980 $34,470 $45,960

2 15,510 20,628 23,265 31,020 46,530 62,040

3 19,530 25,975 29,295 39,060 58,590 78,120

4 23,550 31,322 35,325 47,100 70,650 94,200

5 27,570 36,668 41,355 55,140 82,710 110,280

6 31,590 42,015 47,385 63,180 94,770 126,360

7 35,610 47,361 53,415 71,220 106,830 142,440

8 39,630 52,708 59,445 79,260 118,890 158,520

For each additional person, add

$4,020 $5,347 $6,030 $8,040 $12,060 $16,080

2014 FLP Levels

7

Individual Market

Medicaid/Medical

PTCHI < 400% of FPL

HI > 100% of FPL

The Exchange

8

3) Are not able to get affordable coverage through an eligible employer health plan that provides minimum value.

9

But if an individual enrolls in the employer health insurance, then

no PTC even if it is unaffordable or lacks

minimum value

An employer-sponsored plan is “affordable” to taxpayer, spouse, and

dependents if employee cost

for self-only coverage does not exceed 9.5% of your household income.

10

11

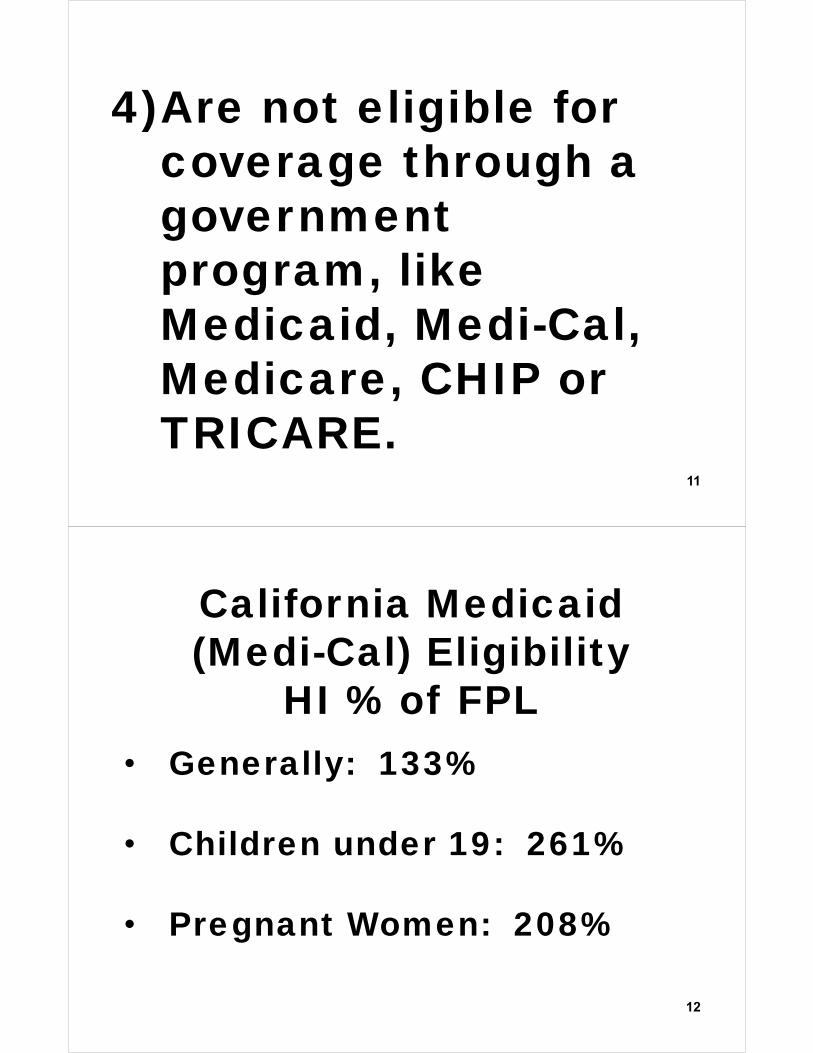

4)Are not eligible for coverage through a government program, like Medicaid, Medi-Cal, Medicare, CHIP or TRICARE.

12

California Medicaid (Medi-Cal) Eligibility

HI % of FPL• Generally: 133%

• Children under 19: 261%

• Pregnant Women: 208%

13

MEC Eligibility Relief

Notice 2014-71 prevents a pregnant woman from losing eligibility for the PTC as a result of the pregnancy, merely because she is eligible for, but DOES NOT enroll in, the Medicaid or CHIP coverage:

14

No Similar ReliefFor a Child’sEligibility for

Medicaid

15

5) Cannot be claimed as a dependent by another person.

16

6) Do not file a Married Filing Separately (MFS) tax return with an exception for victims of domestic abuse and spousal abandonment who are allowed to claim the PTC using the MFS filing status.

17

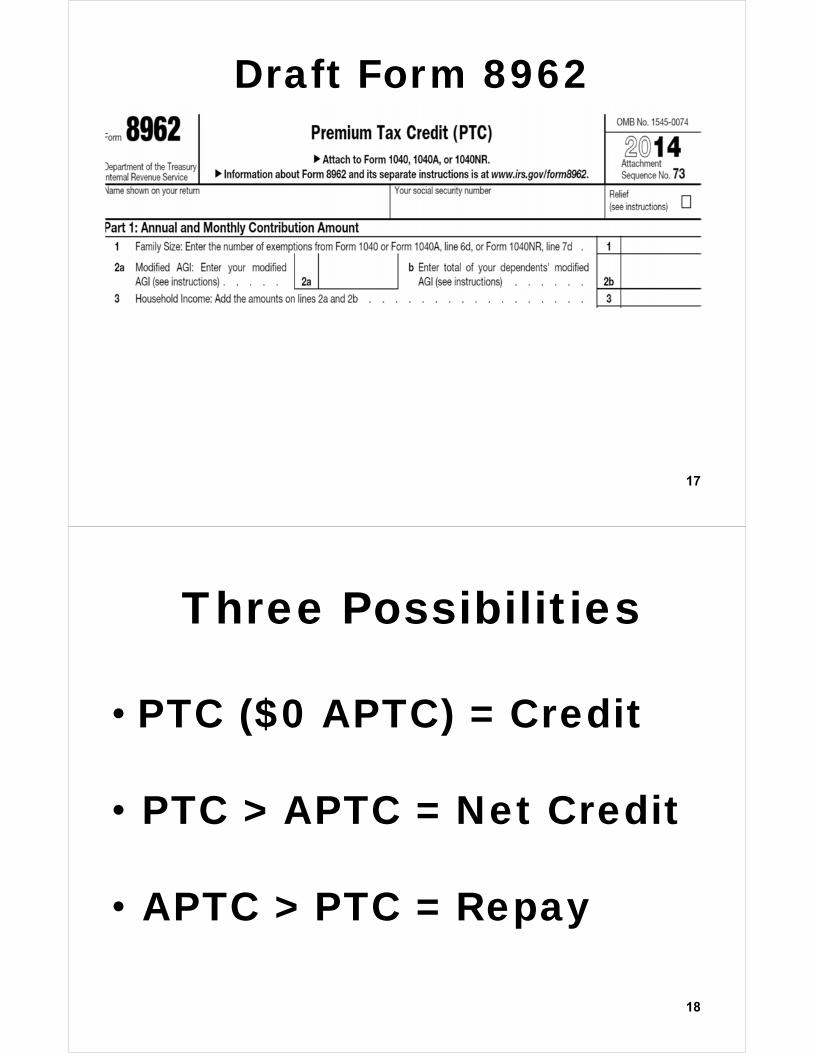

Draft Form 8962

18

Three Possibilities

• PTC ($0 APTC) = Credit

• PTC > APTC = Net Credit

• APTC > PTC = Repay

Refund

19

PTC > APTC = Form 1040 Line 69

20

APTC > PTC =

Form 1040 Line 46

Repay

21

Family of Three Facts

• H and W both age 35• CA ZIP 94506• One dependent child

(age 10) • File MFJ• Purchase a bronze plan

via Covered California

22

NoAdvance

PTC

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%MAGI

P

$4,848 PTC

$7,954 PTC

$2,460 PTC

24

H&W’s MAGI

Is $78,121

P

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%

P

$4,848 PTC

$7,954 PTC

$2,460 PTC $0 PTC $78,121 400.0005%

26

Contribute $1to deductible

IRA by unextended due

date of Form 1040

$78,121 400.0005$0 PTC

P

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

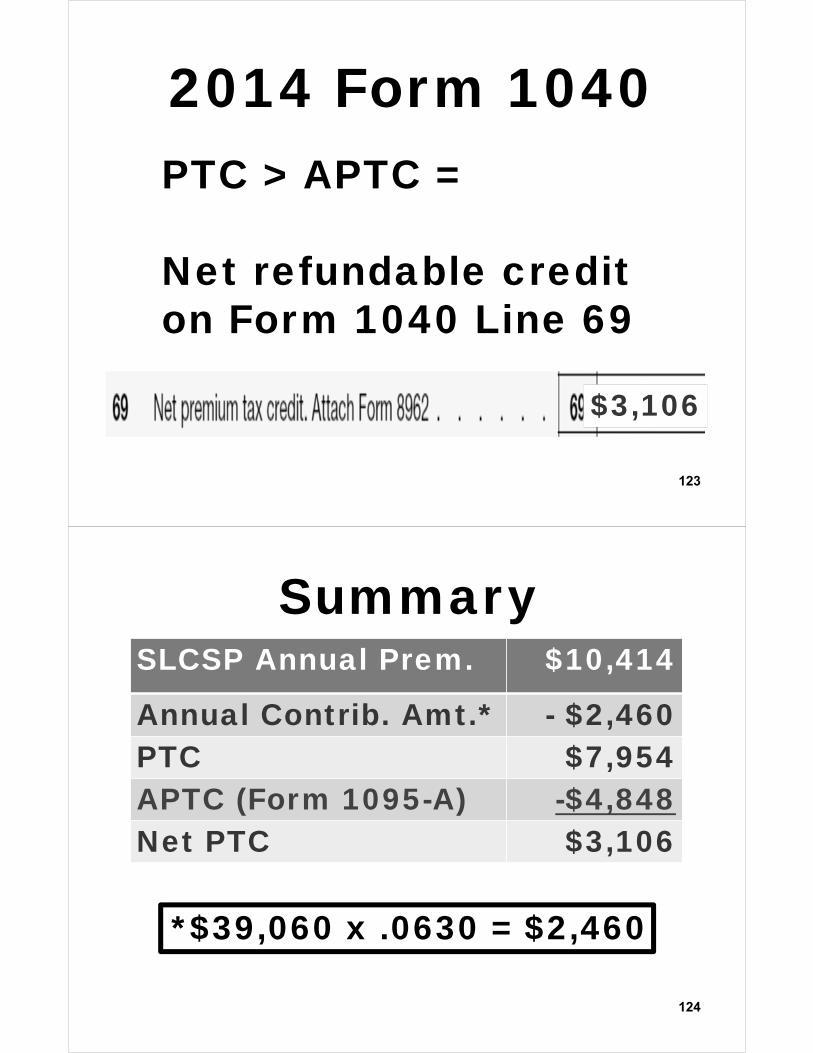

$78,120 400%

P

$4,848 PTC

$7,954 PTC

$2,460 PTC

PTC $2,460

28

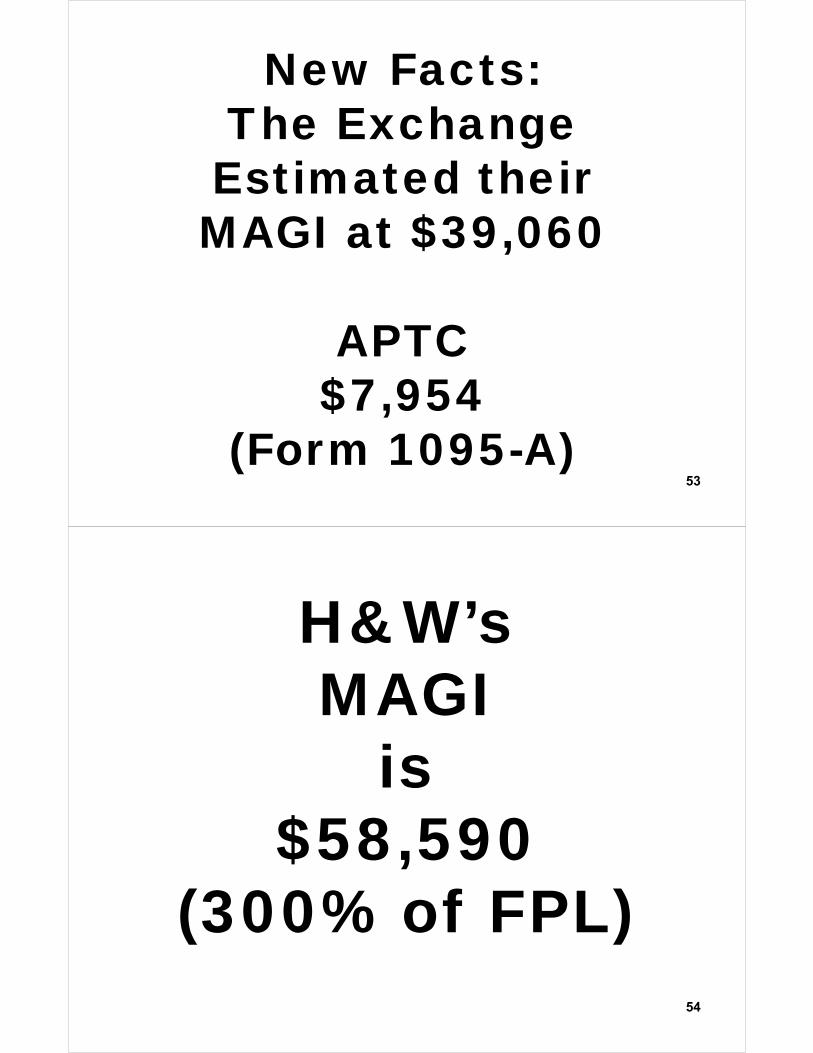

New Facts:The Exchange Estimated their MAGI at $39,060

APTC$7,954

(Form 1095-A)

P

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%

P

$4,848 PTC

$7,954 APTC

$2,460 PTC $0 PTC $78,121 400.0005%

Repay $7,954

30

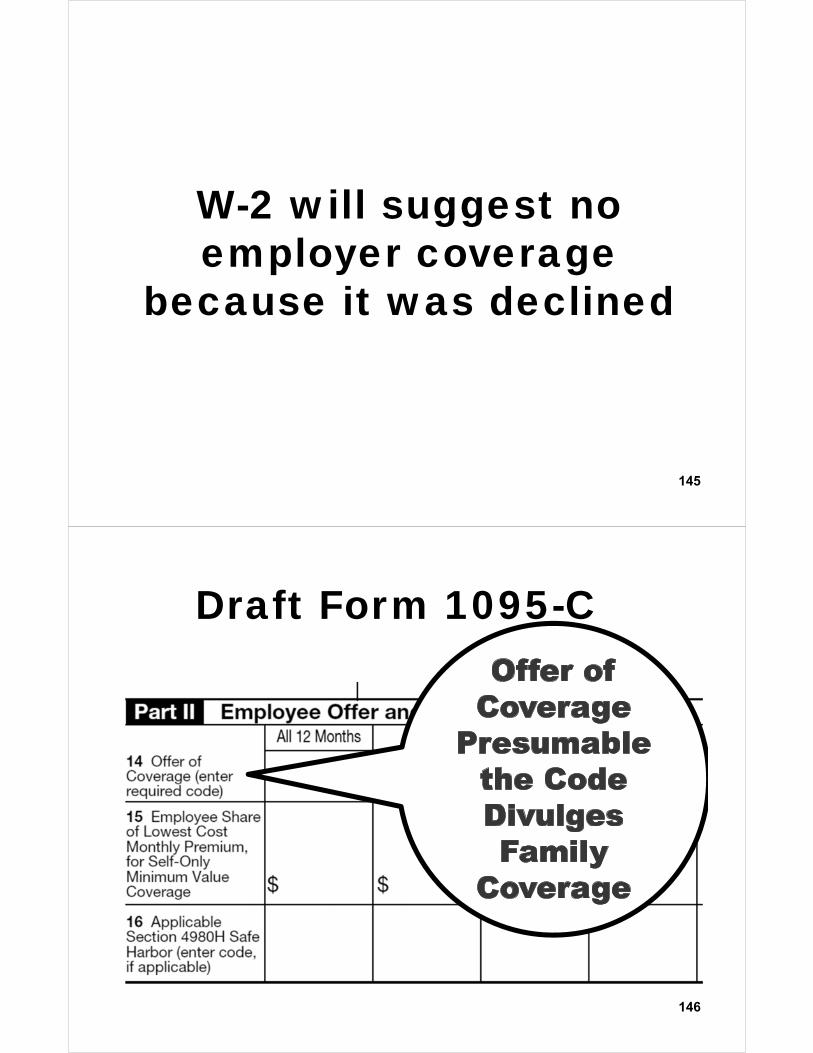

Contribute $1to deductible IRA

PTC $2,460But….

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%MAGI

P

$7,954 APTC

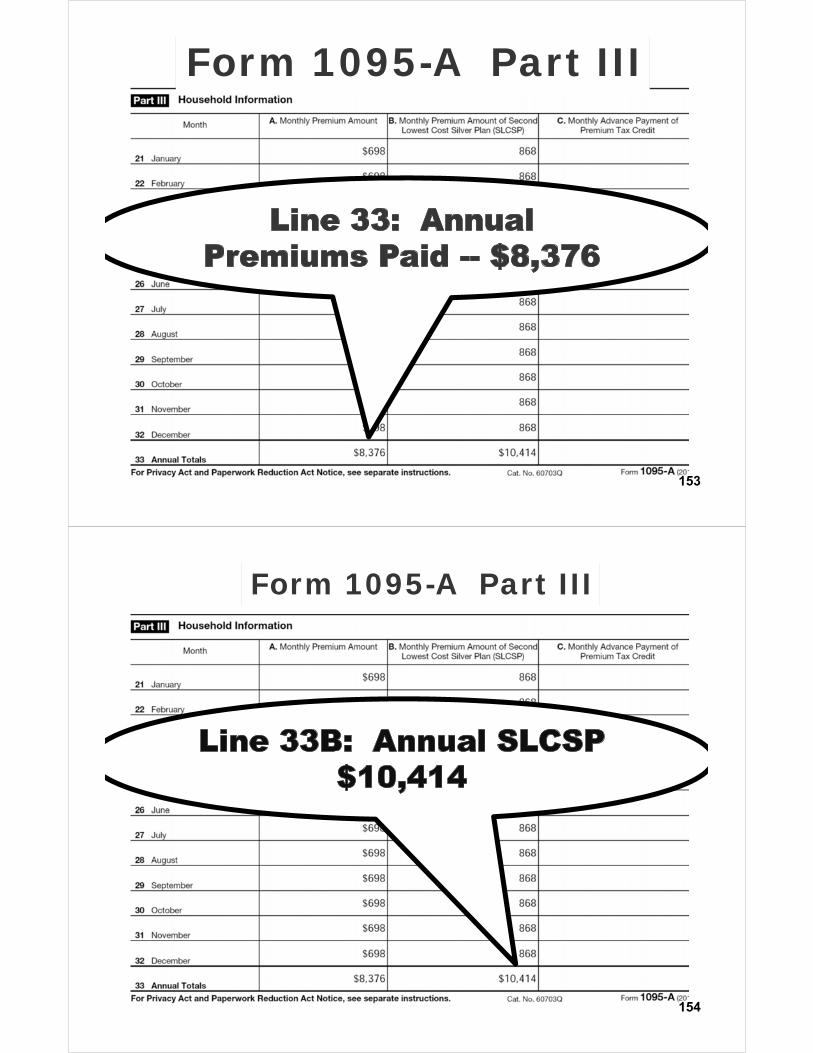

$2,460 PTC

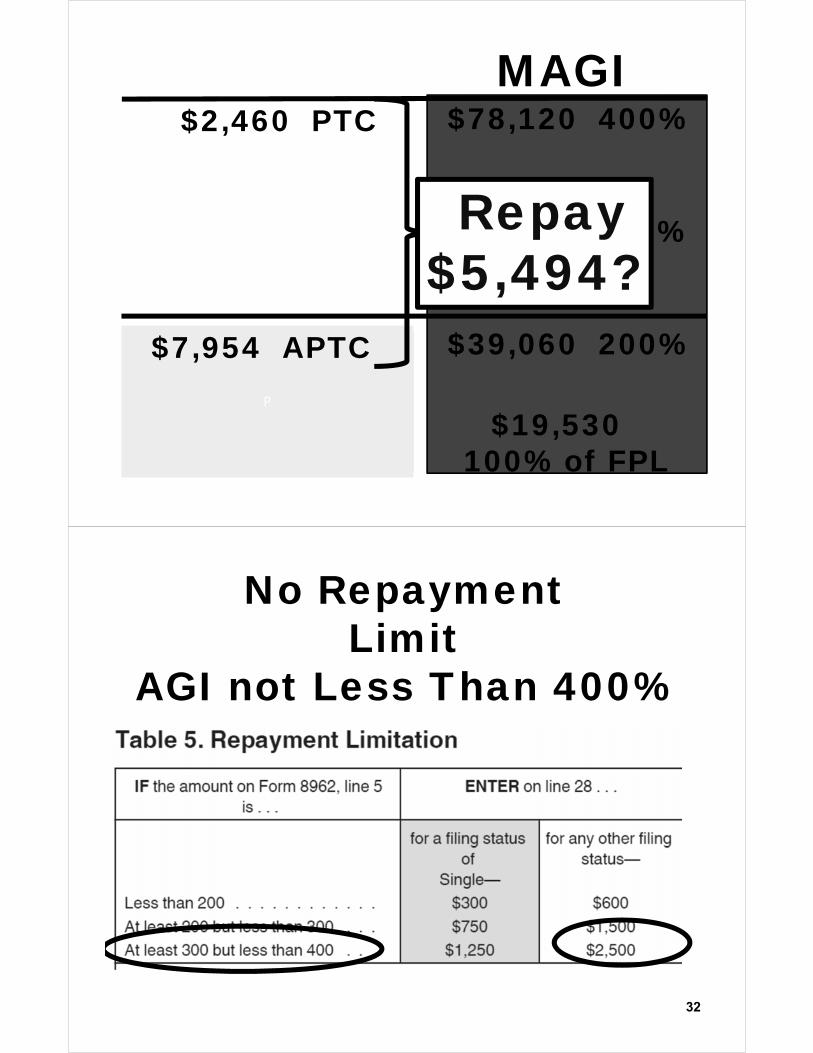

Repay $5,494?

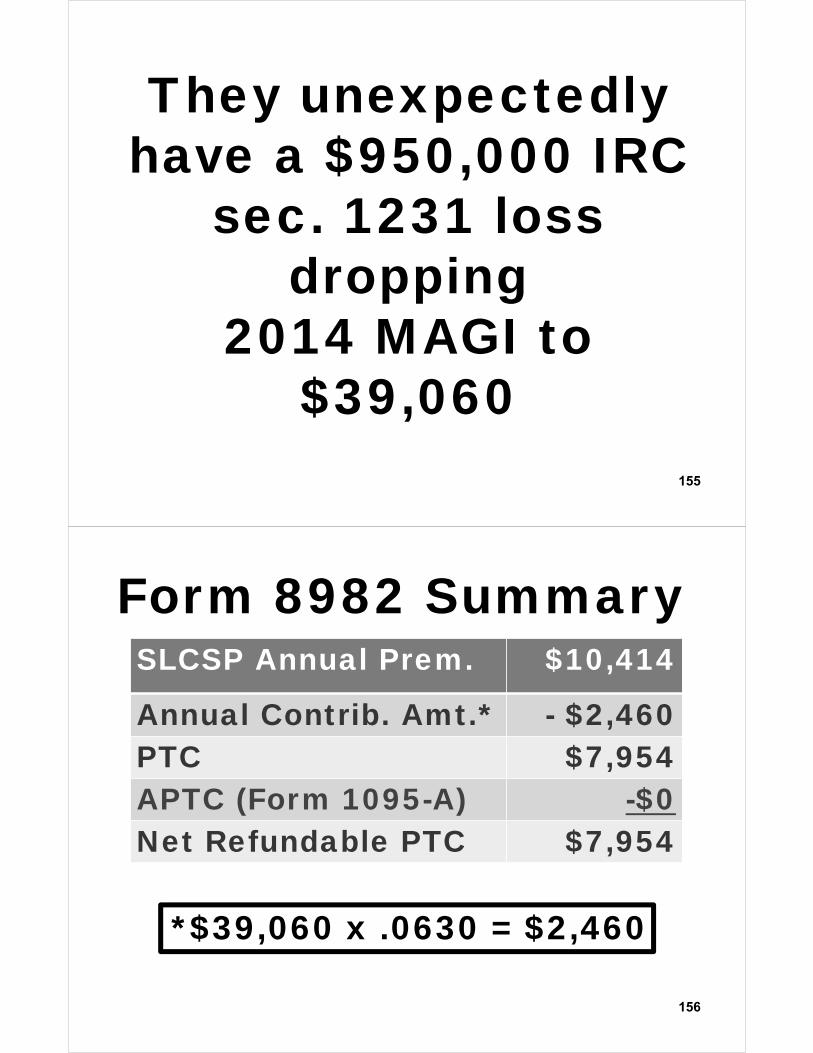

32

No RepaymentLimit

AGI not Less Than 400%

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%MAGI

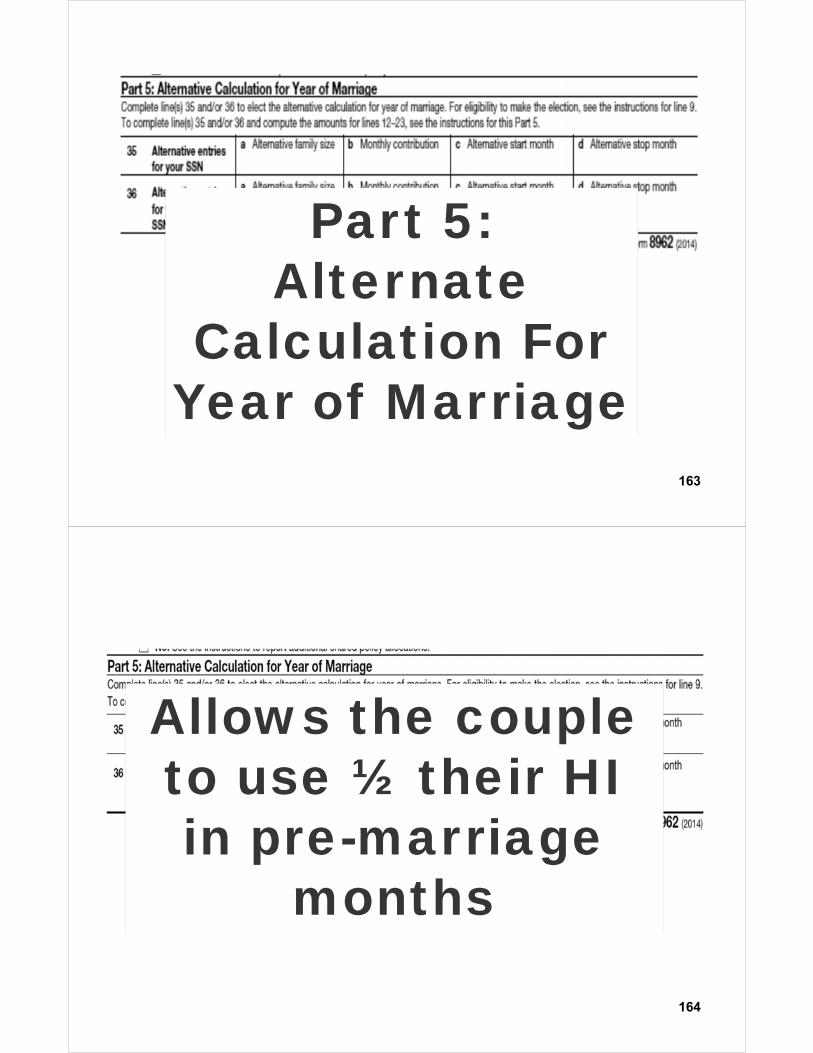

P

$7,954 APTC

$2,460 PTC

Repay $5,494

34

Contribute $2 (not $1)

to deductible IRA

PTC $2,460Plus $2,500 Limit

35

RepaymentLimit of $2,500

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,119 400%MAGI

P

$7,954 APTC

$2,460 PTC

Repay $5,494$2,500

37

$2 IRA Contribution Saves $5,454

($7,954 - $2,500)

38

What if $5,001 is Contributed to IRA reducing actual HI to

$73,120(374% of FPL)

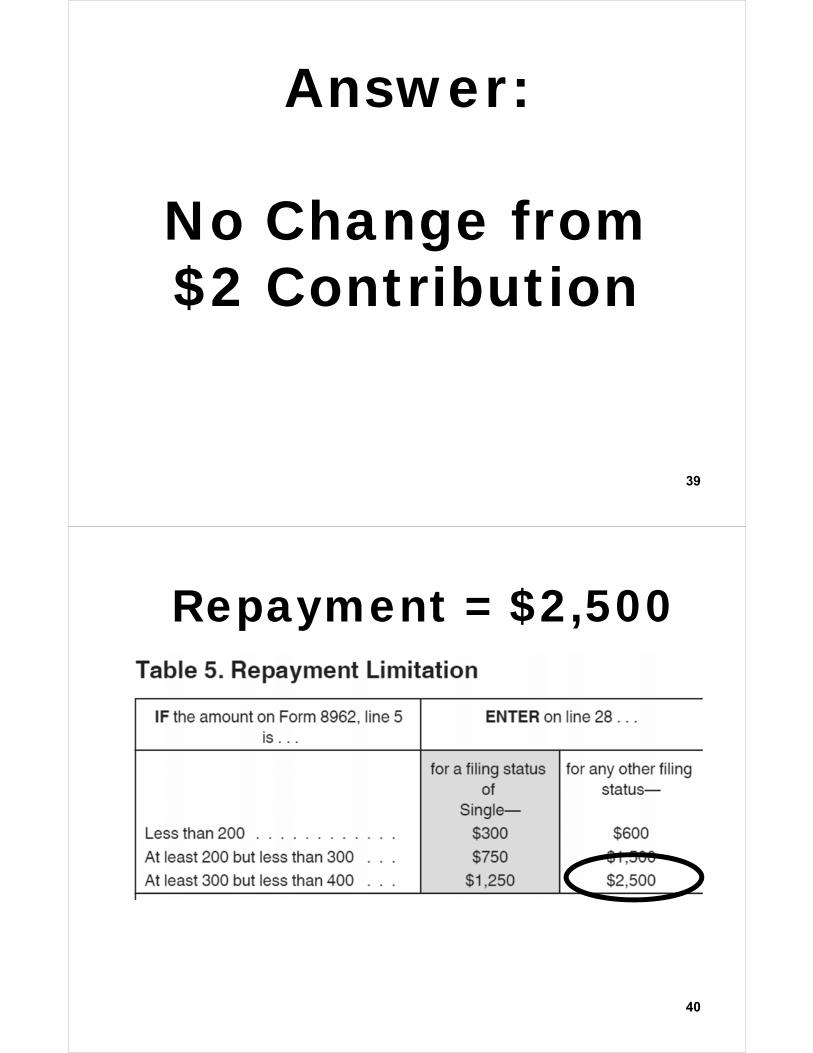

39

Answer:

No Change from $2 Contribution

40

Repayment = $2,500

41

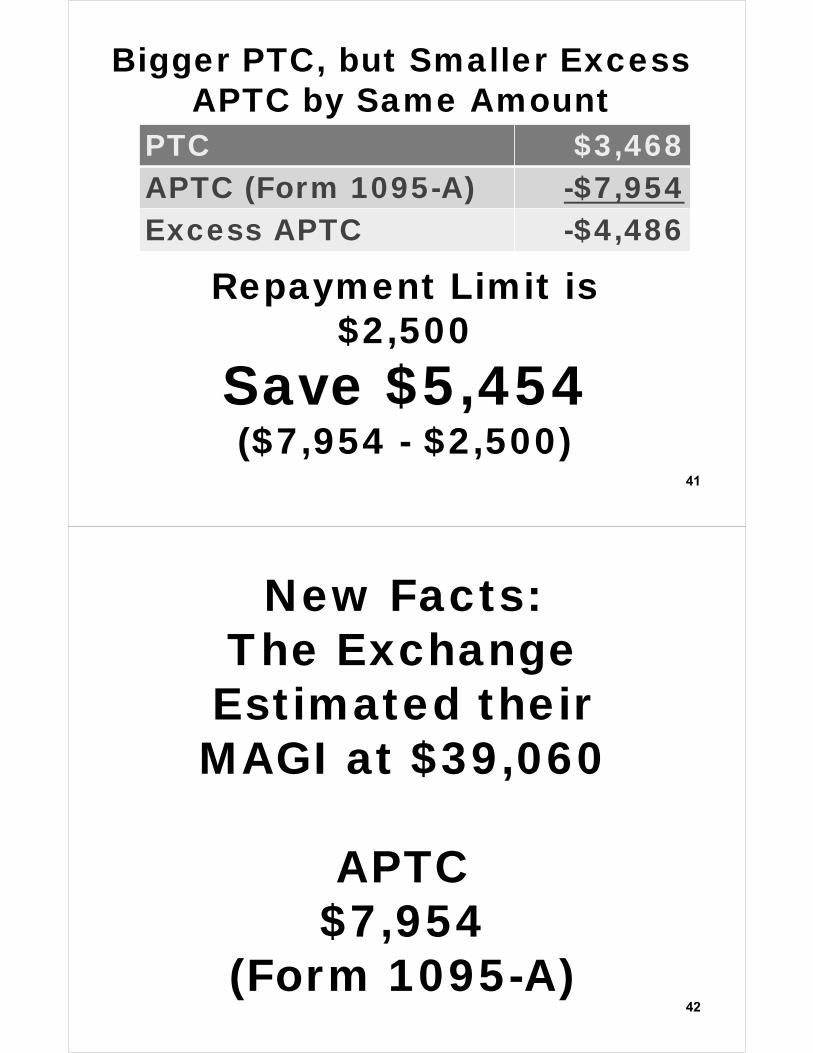

PTC $3,468APTC (Form 1095-A) -$7,954Excess APTC -$4,486

Repayment Limit is $2,500

Save $5,454 ($7,954 - $2,500)

Bigger PTC, but Smaller Excess APTC by Same Amount

42

New Facts:The Exchange Estimated their MAGI at $39,060

APTC$7,954

(Form 1095-A)

43

H&W’s MAGI

is $83,121

($5,001 over 400% of FPL)

P

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%

P

$4,848 PTC

$7,954 PTC

$2,460 PTC $0 PTC $83,121

Repay $7,954

45

Now, a $5,002 IRA contribution

reduces HI to $78,119

(slightly below400%)

46

$5,002 IRA Contribution Saves $5,454

($7,954 - $2,500)

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,119 400%MAGI

P

$7,954 APTC

$2,460 PTC

Repay $2,500

48

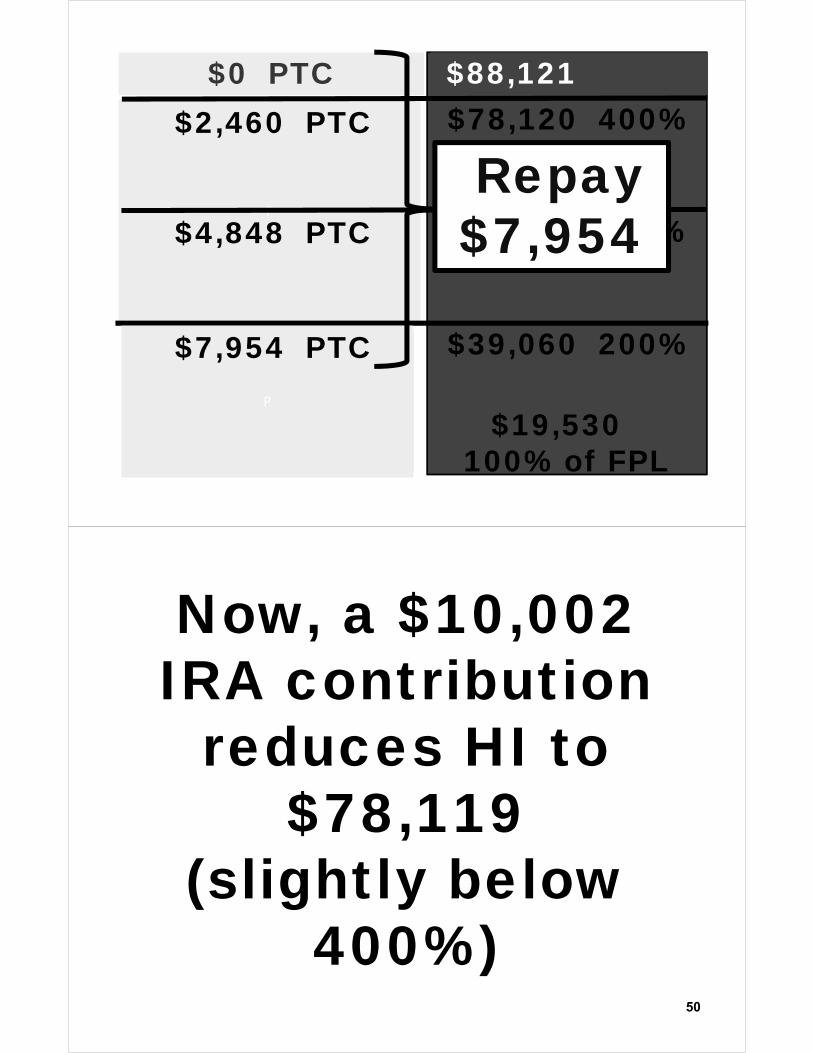

H&W’s MAGI

is $88,121

($10,001 over 400% of FPL)

P

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%

P

$4,848 PTC

$7,954 PTC

$2,460 PTC $0 PTC $88,121

Repay $7,954

50

Now, a $10,002 IRA contribution

reduces HI to $78,119

(slightly below400%)

51

$10,002 IRA Contribution Saves $5,454

($7,954 - $2,500)

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,119 400%MAGI

P

$7,954 APTC

$2,460 PTC

Repay $2,500

53

New Facts:The Exchange Estimated their MAGI at $39,060

APTC$7,954

(Form 1095-A)

54

H&W’s MAGI

is $58,590

(300% of FPL)

P

PP

$19,530 100% of FPL

$39,060 200%

$58,590 300%

$78,120 400%

P

$4,848 PTC

$7,954 APTC

$2,460 PTC

Repay $3,106

Or $2,500

56

$1,500 RepaymentLimit

If AGI Less Than 300%

57

Contribute $1to deductible IRA

Save $1,000

Repayment Limited to $1,500

58

$1,500 RepaymentLimit

If AGI Less Than 300%

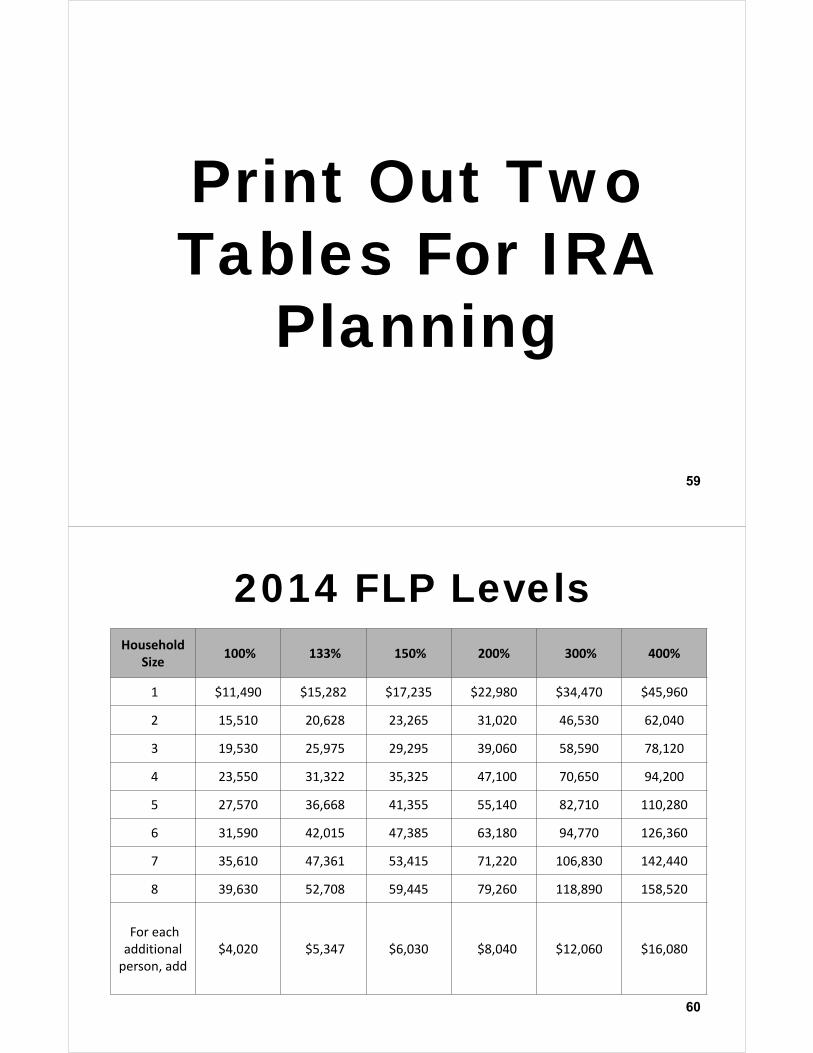

Print Out Two Tables For IRA

Planning

59

60

Household Size

100% 133% 150% 200% 300% 400%

1 $11,490 $15,282 $17,235 $22,980 $34,470 $45,960

2 15,510 20,628 23,265 31,020 46,530 62,040

3 19,530 25,975 29,295 39,060 58,590 78,120

4 23,550 31,322 35,325 47,100 70,650 94,200

5 27,570 36,668 41,355 55,140 82,710 110,280

6 31,590 42,015 47,385 63,180 94,770 126,360

7 35,610 47,361 53,415 71,220 106,830 142,440

8 39,630 52,708 59,445 79,260 118,890 158,520

For each additional person, add

$4,020 $5,347 $6,030 $8,040 $12,060 $16,080

2014 FLP Levels

61

62

Draft Form 8962

Reconcile PTC and APTC

on Form 8982

PTC =

63

1) SLCSP* minus contribution amount, or

2) If less, the premium paid*

*Exchange Provides on Form 1095-A

64

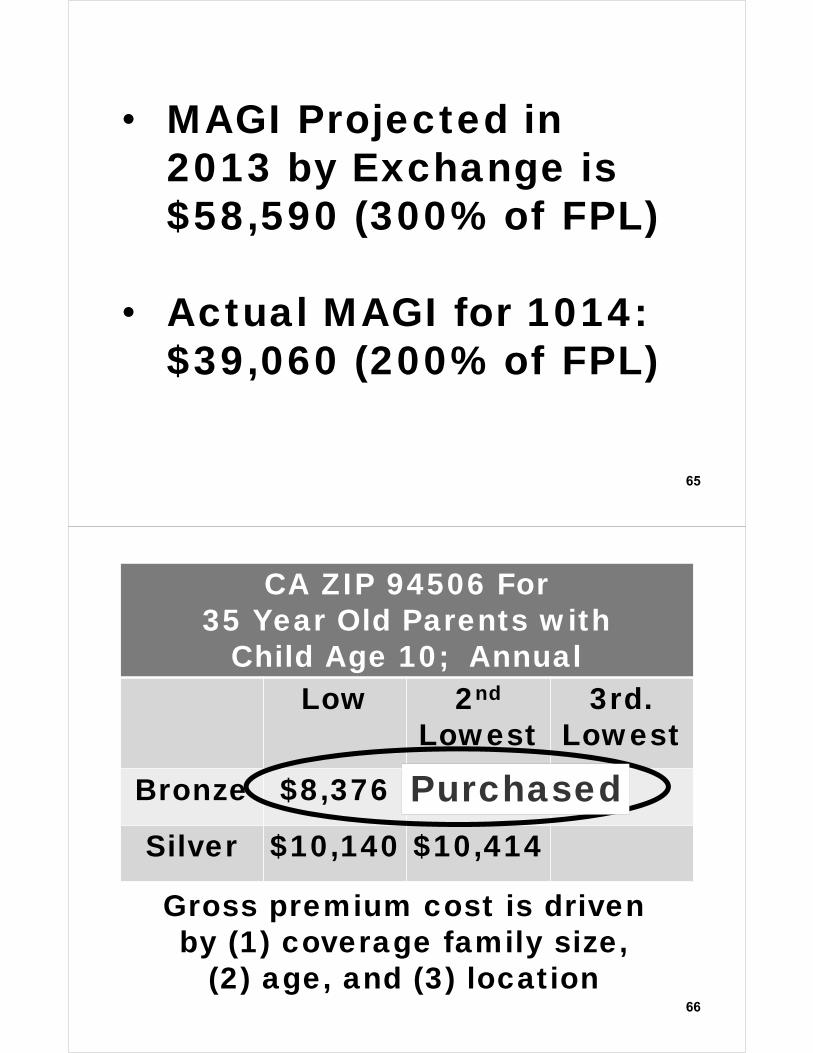

Family of Three Facts

• H and W both age 35• CA ZIP 94506• One dependent child

(age 10) • File MFJ• Purchase a bronze plan

via Covered California

65

• MAGI Projected in 2013 by Exchange is $58,590 (300% of FPL)

• Actual MAGI for 1014: $39,060 (200% of FPL)

CA ZIP 94506 For 35 Year Old Parents with

Child Age 10; AnnualLow 2nd

Lowest3rd.

Lowest

Bronze $8,376

Silver $10,140 $10,414

66

Purchased

Gross premium cost is driven by (1) coverage family size,

(2) age, and (3) location

67

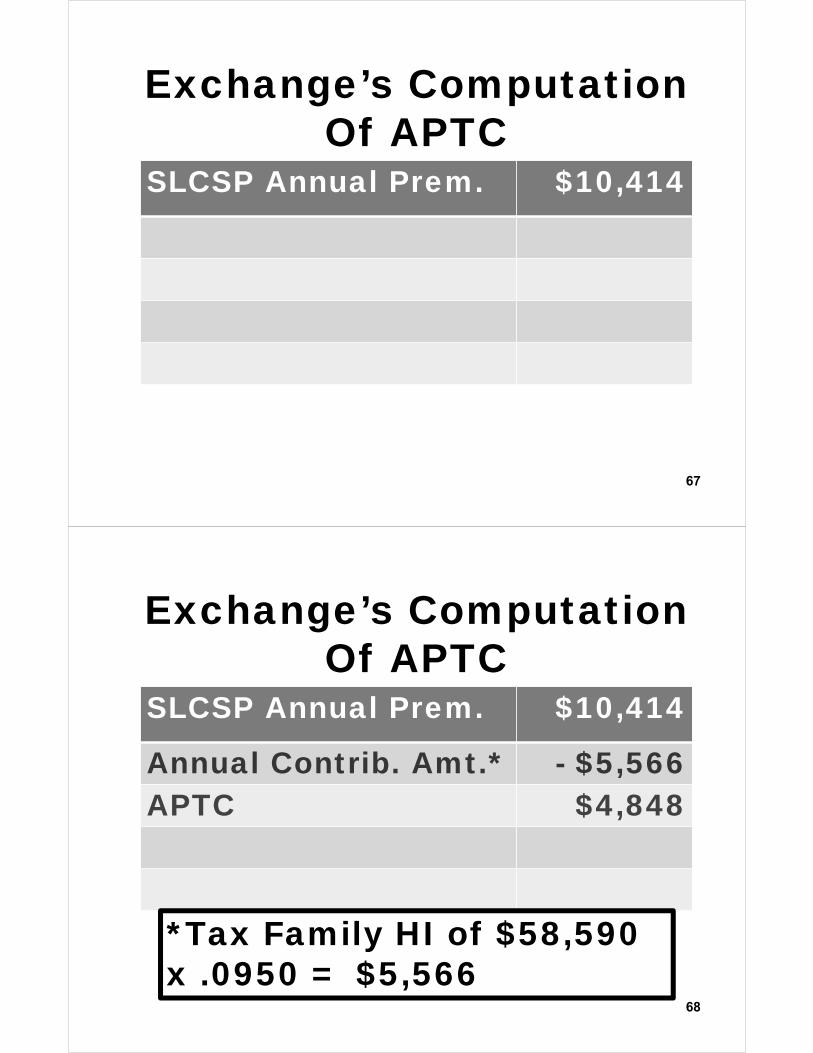

SLCSP Annual Prem. $10,414

Exchange’s ComputationOf APTC

68

SLCSP Annual Prem. $10,414

Annual Contrib. Amt.* - $5,566APTC $4,848

*Tax Family HI of $58,590 x .0950 = $5,566

Exchange’s ComputationOf APTC

69

Form 1095-A

70

Form 1095-A Part III

MonthlyPremium Amount

Annual Premium Amount

71

Form 1095-A Part III

MonthlySLCSP

For Coverage

Family

AnnualSLCSP

72

Form 1095-A Part III

MonthlyAPTC

AnnualAPTC

73

Part 1Lines 1 through 8:

Eligibilityand

Contribution Amount

74

Draft Form 8962

75

x

76

Draft Form 8962

77

Number of Exemptions =

Tax Family SizeWhich Drives

Household Income

78

Draft Form 8962

3

79

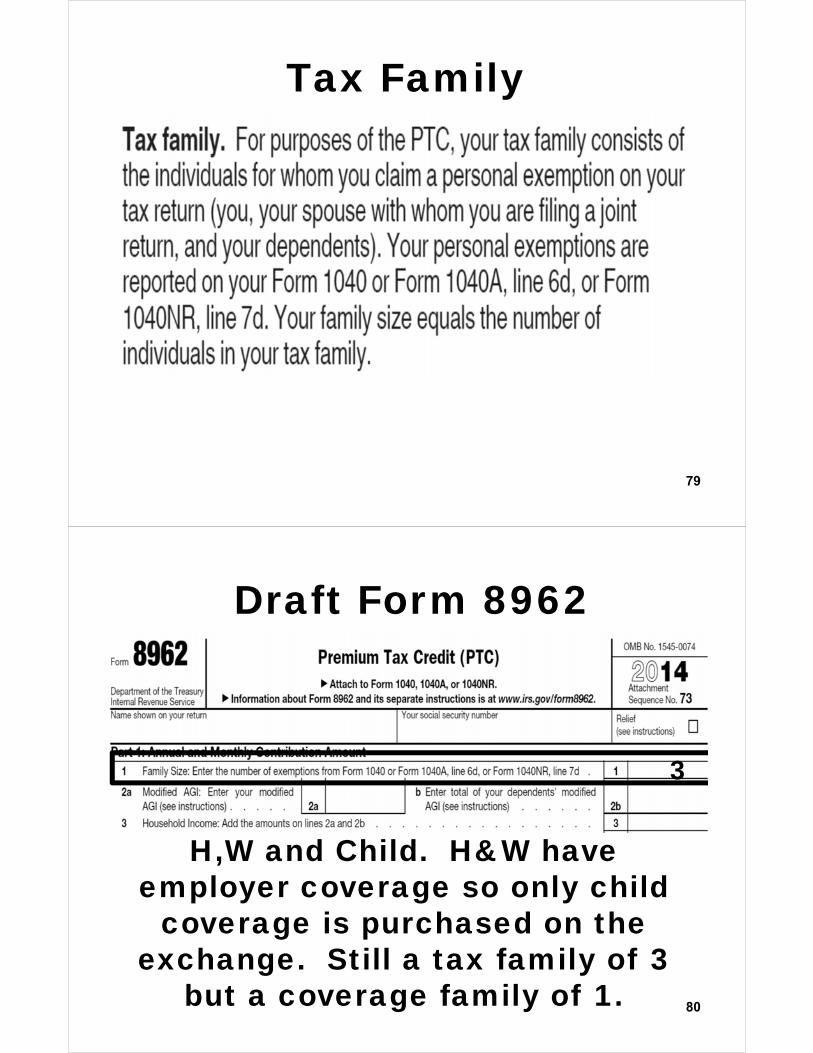

Tax Family

80

Draft Form 8962

3

H,W and Child. H&W have employer coverage so only child

coverage is purchased on the exchange. Still a tax family of 3

but a coverage family of 1.

81

Draft Form 8962

3

Line 3 = Household Income

Household Income = Modified AGI of Taxpayer

and Dependents

82

Draft Form 8962

3Line 2a: Your Modified AGI

AGI + excluded foreign earned income + tax exempt interest +

excluded social security benefits

83

3

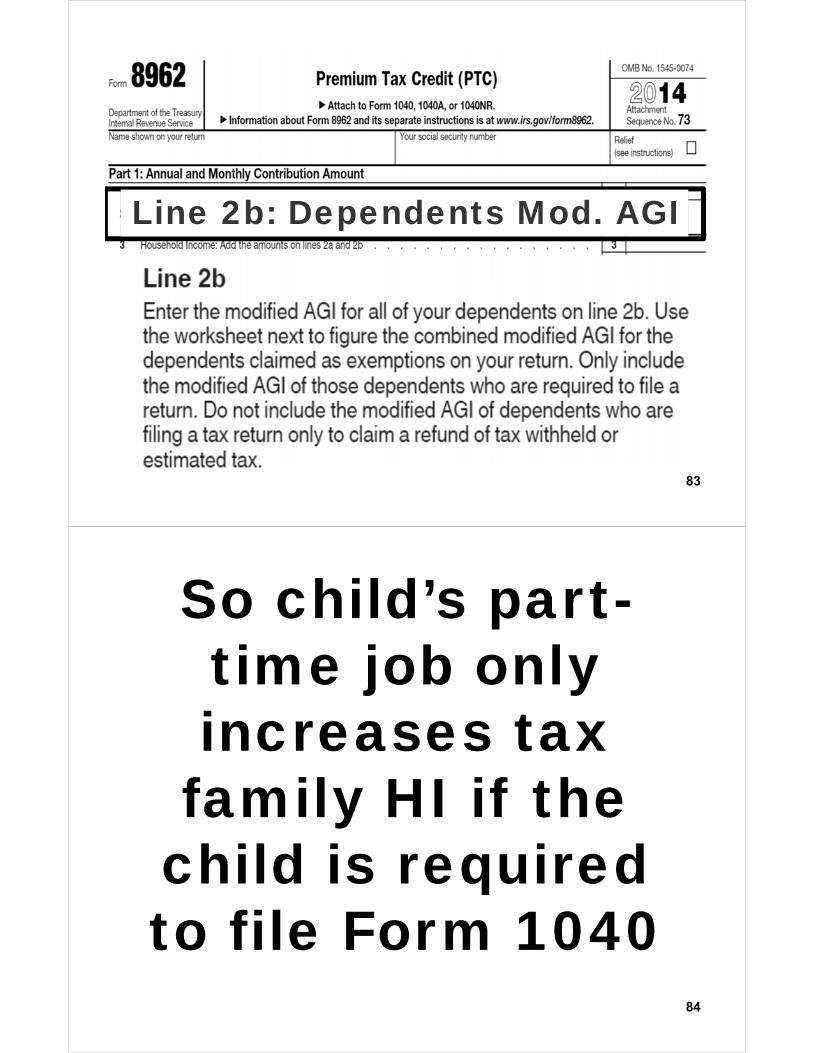

Line 2b: Dependents Mod. AGI

84

So child’s part-time job only increases tax family HI if the

child is required to file Form 1040

85

Draft Form 8962

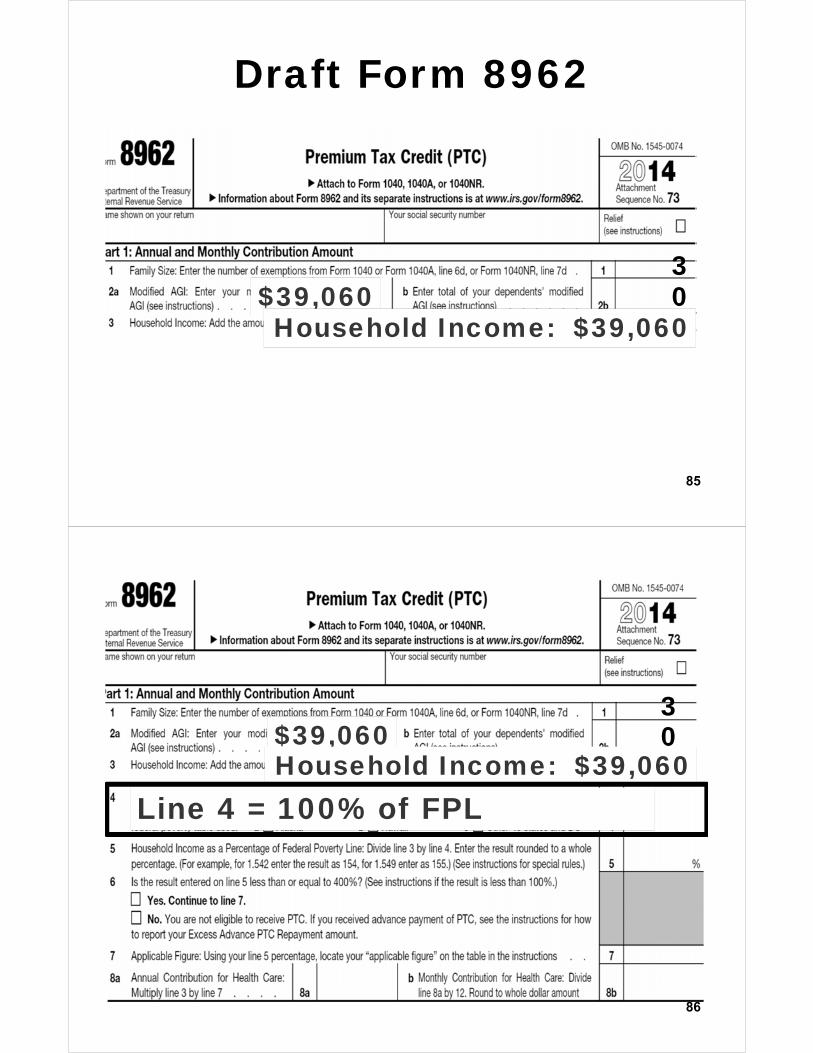

3$39,060 0Household Income: $39,060

86

3$39,060 0Household Income: $39,060

Line 4 = 100% of FPL

87

88

3$39,060 0Household Income: $39,060

x100% of FPL $19,530

89

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

90

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

91

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%Is Line 5 less < 400%?

92

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

If Yes Continue to Line 7

93

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

If NO: No PTC and Pay Back APTC For ALL Individuls “in your tax family”

94

Modify Facts:• H,W and Child. All year, H&W

have employer coverage but child coverage is purchased on the exchange.

• If MAGI exceeds 400% of FPL, then pay back APTC for child whether or not the child filed a federal income tax return.

95

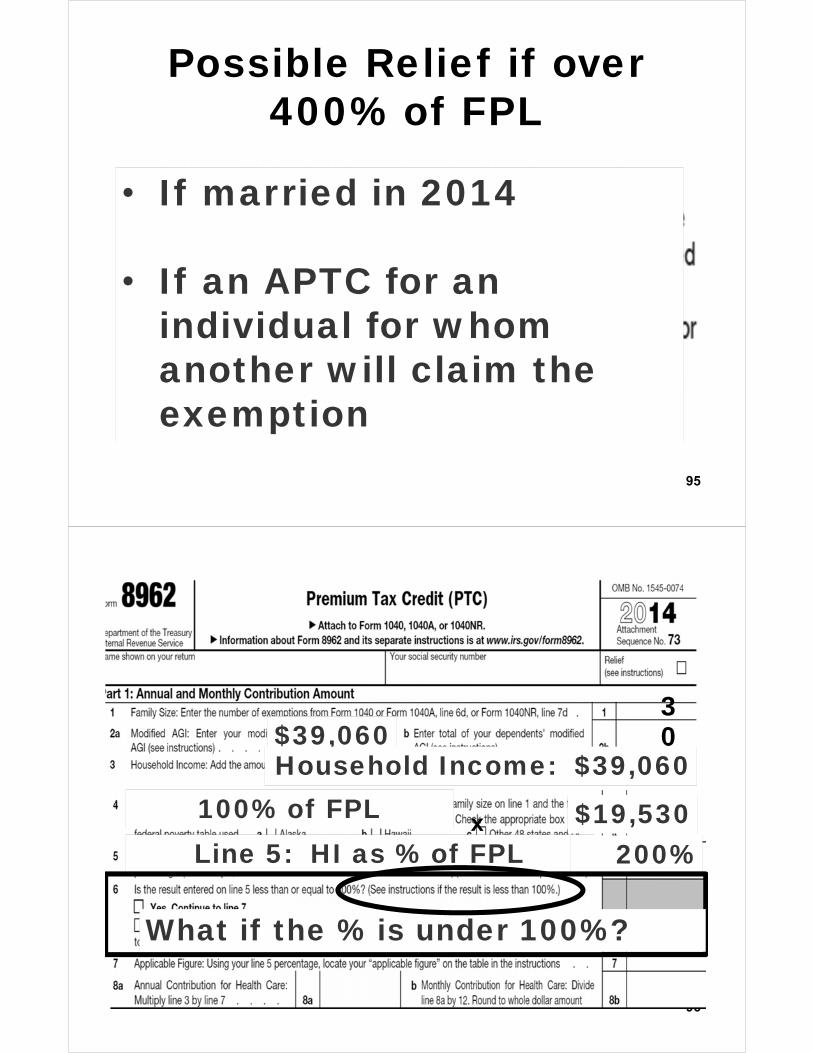

Possible Relief if over 400% of FPL

• If married in 2014

• If an APTC for an individual for whom another will claim the exemption

96

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

What if the % is under 100%?

97

Two Ways to Can Get PTC if Under 100% of FPL:

1)Marketplace estimated HI

between 100% and 400%

of FPL + APTC, but

Actual % is Below 100%

98

2)

Lawful NRA not EligibleFor Medicaid/Medi-Cal

99

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

x

100

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

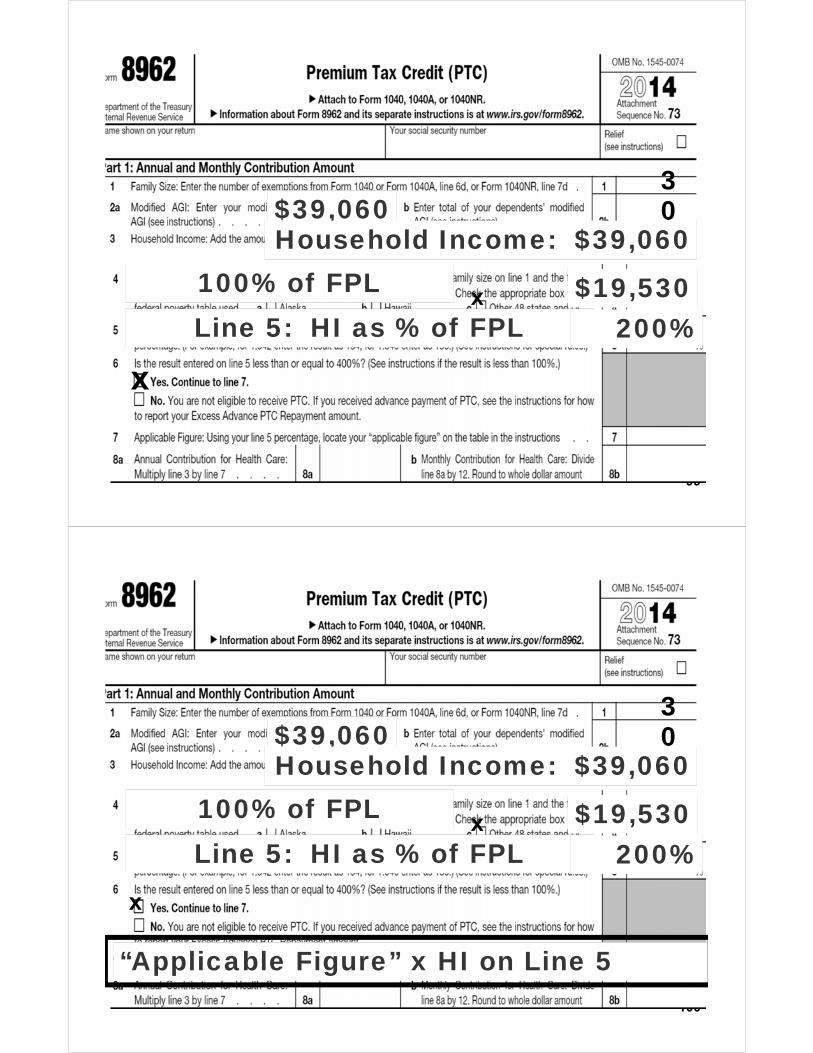

x

“Applicable Figure” x HI on Line 5

101

Form 8962 Page 6Line 7 Applicable Figure

LL.0630

Higher HI % of FPL=

Higher Applicable Figure

102

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

x200%

.0630

103

3$39,060 0Household Income: $39,060

x100% of FPL $19,530Line 5: HI as % of FPL 200%

x

Annual Contribution ÷ 12

104

3$39,060 0Household Income: $39,060

x100% of FPL $19,530

Line 5: HI as % of FPL 200%x

200%

.0630÷ 12 = $205 $39,060 x .0630 = $2,460

105

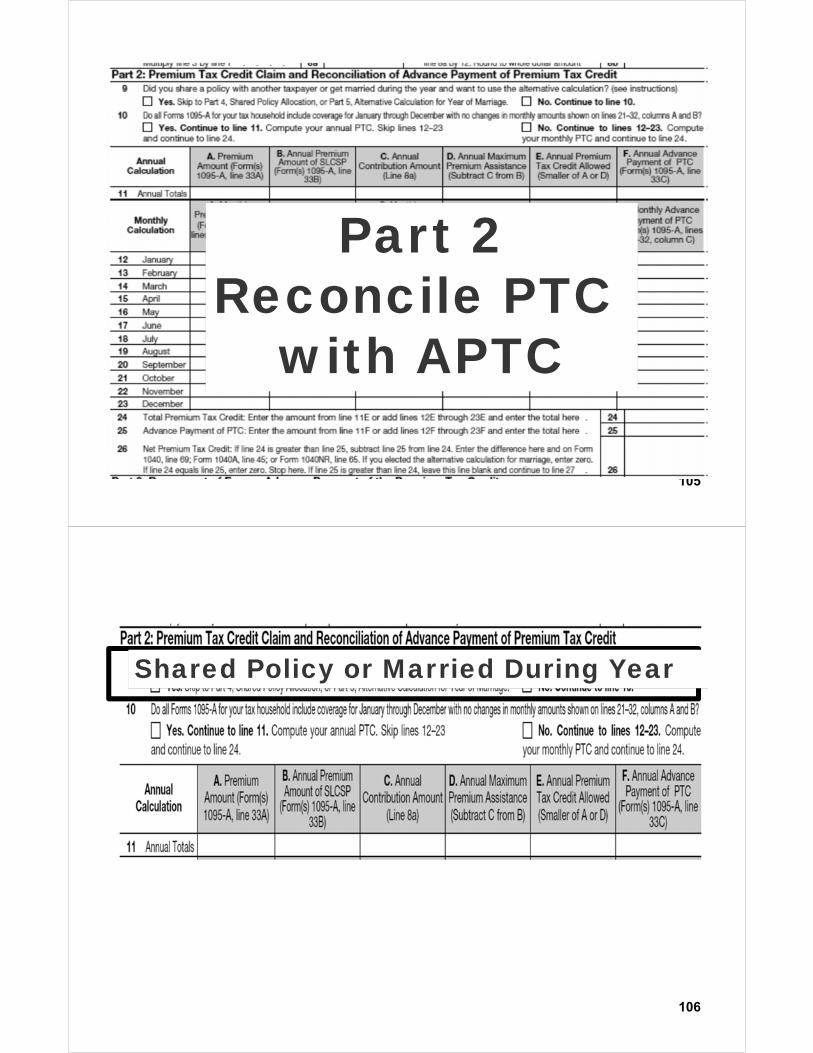

Part 2Reconcile PTC

with APTC

106

Shared Policy or Married During Year

107

x

108

Are Forms 1095-A Monthly Amounts the Same?

x

109

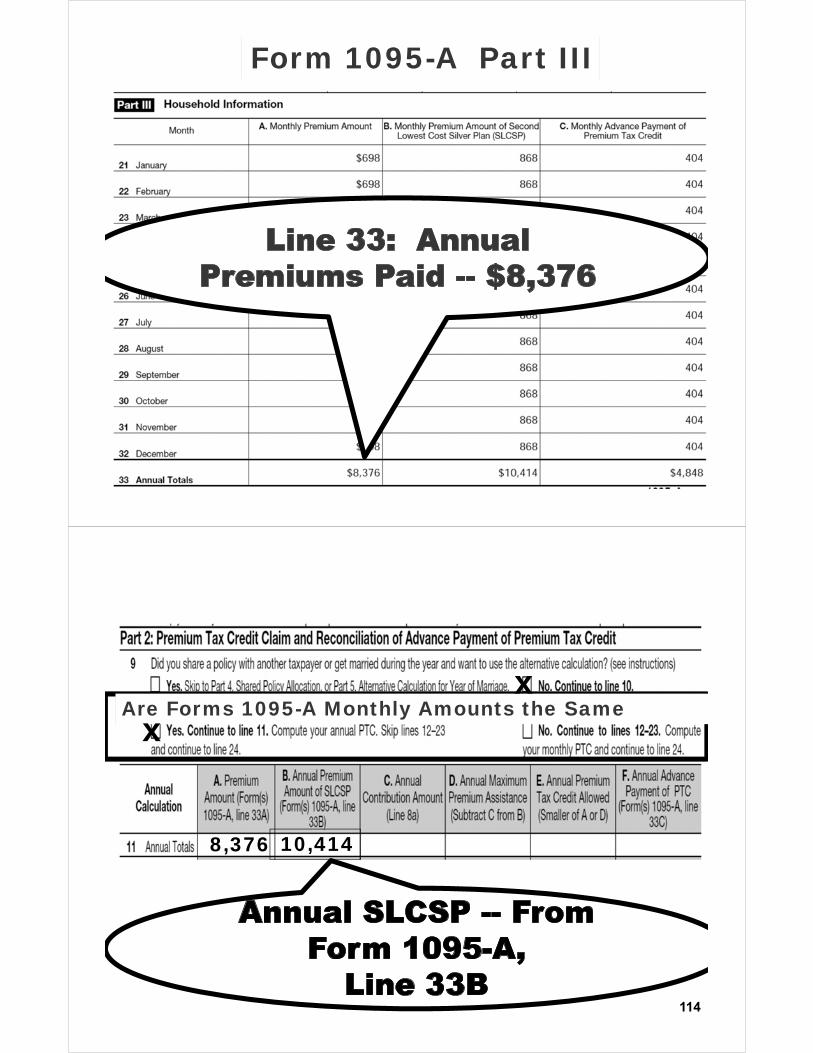

Form 1095-A Part III

All Part III Columns are filled-in with the

same amount each month

110

Form 8982 Monthly Calculation

111

Are Forms 1095-A Monthly Amounts the Samex

x

112

Are Forms 1095-A Monthly Amounts the Same

8,376

xx

113

Form 1095-A Part III

114

Are Forms 1095-A Monthly Amounts the Same

8,376 10,414

xx

115

Form 1095-A Part III

116

SLCSP Annual Prem. $10,414

Annual Contrib. Amt.* - $5,566APTC $4,848

*Tax Family HI of $58,590 x .0950 = $5,566

Exchange’s ComputationOf APTC

117

Are Forms 1095-A Monthly Amounts the Same

8,376 10,414 $2,460

xx

118

Are Forms 1095-A Monthly Amounts the Same

8,376 10,414 $2,460 7,954

xx

119

Are Forms 1095-A Monthly Amounts the Same

8,376 10,414 $2,460 7,954 7,954

xx

120

Are Forms 1095-A Monthly Amounts the Same

8,376 10,414 $2,460 7,954 7,954 4,848

x

121

Form 1095-A Part III

122

PTC = $7,954APTC = $4,848

L 24 Exceeds L 25: Net PTC = $3,106

2014 Form 1040

123

PTC > APTC =

Net refundable credit on Form 1040 Line 69

$3,106

124

SLCSP Annual Prem. $10,414

Annual Contrib. Amt.* - $2,460PTC $7,954APTC (Form 1095-A) -$4,848Net PTC $3,106

*$39,060 x .0630 = $2,460

Summary

125

Form 1095-A

126

The Monthly SLCSP

On Form 1095-AMay Not

Be Correct Due to Coverage Family

Changes ora Move

127

128

The SLCSP Is Based Upon

the Coverage Family

Here, coverage family of three

129

What if our Tax Family of Three

Becomesa

Coverage Family of

One?

130

Modified Facts:Same as above except, midyear,

H&W are covered by H’s employer insurance, so H&W’s Exchange

insurance is canceled July 1 but Child (C) is not covered by the

employer policy so C keeps his/her individual Marketplace Policy

Exchange Projected HI $58,590Actual HI of $39,060

131

The SLCSP Is Based Upon

the Coverage Family

of 1

132

Exchange Reports Coverage Family on

Form 1095-A, Part IIBeginning and Ending Dates

133

July through December

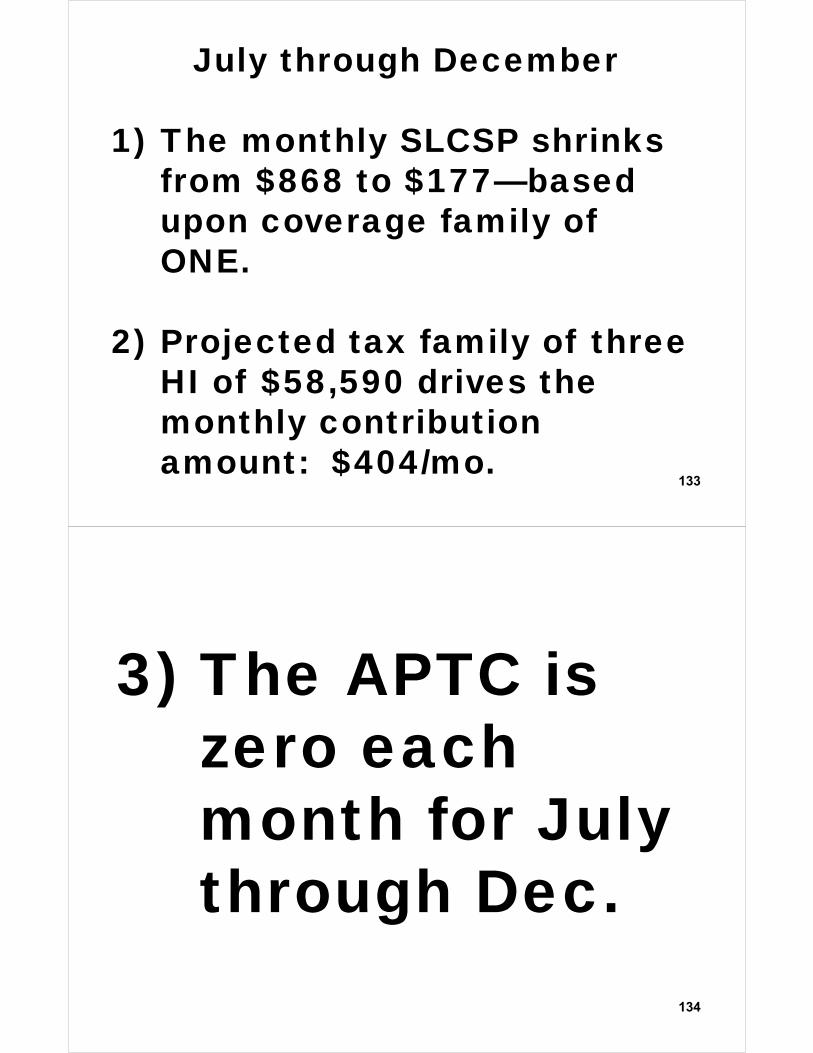

1) The monthly SLCSP shrinks from $868 to $177—based upon coverage family of ONE.

2) Projected tax family of three HI of $58,590 drives the monthly contribution amount: $404/mo.

134

3) The APTC is zero each month for July through Dec.

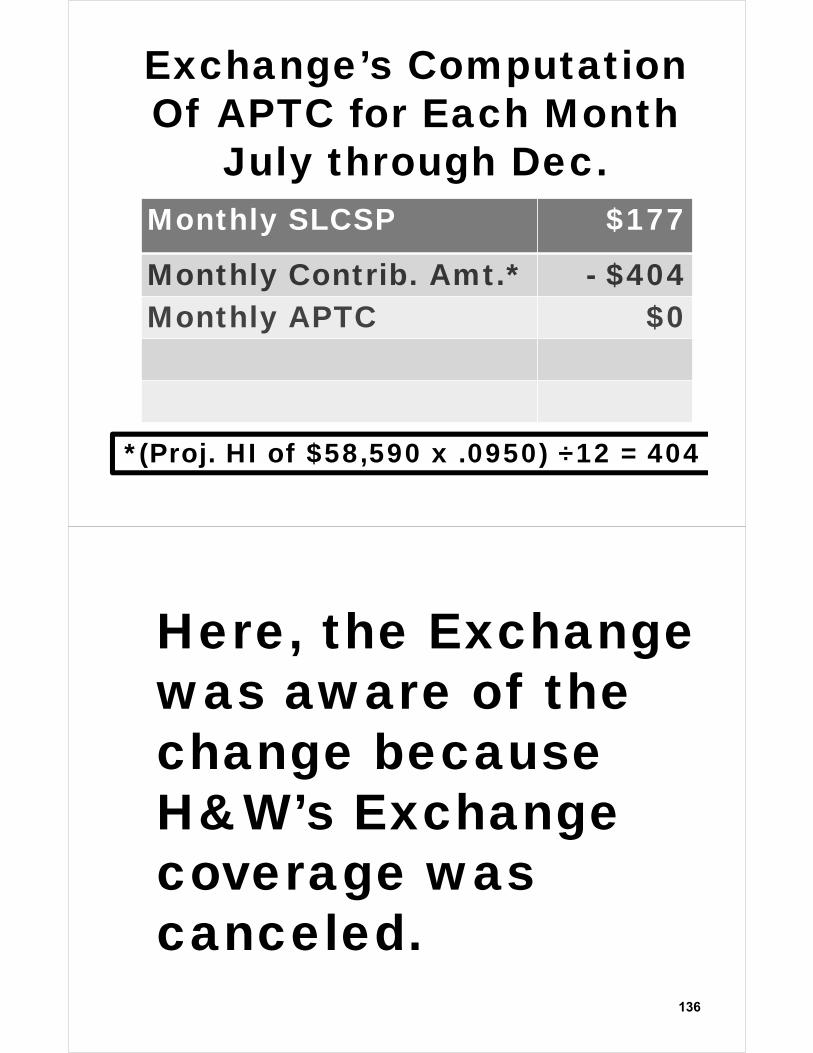

Monthly SLCSP $177

Monthly Contrib. Amt.* - $404Monthly APTC $0

*(Proj. HI of $58,590 x .0950) ÷12 = 404

Exchange’s ComputationOf APTC for Each Month

July through Dec.

136

Here, the Exchange was aware of the change because H&W’s Exchange coverage was canceled.

137

Form 1095-A Part III

$404$868JanThruJune

JulyThruDec.

$130

MonthlyPremium

$698

MonthlySLCSP

MonthlyAPTC

$177 $0

138

Form 8962 Part 2

Enter Monthly InfoFrom Form 1095-A

Monthly SLCSP $868

Monthly Contrib. Amt.* - $205Monthly Maximum PTC $663

Monthly PTC in Jan thru June

*(HI of $39,060 x .0630) ÷ 12 = $205

Monthly SLCSP $177

Monthly Contrib. Amt.* - $205Monthly Maximum PTC $0

Monthly PTC in July thru Dec.

*(HI of $39,060 x .0630) ÷ 12 = $205

141

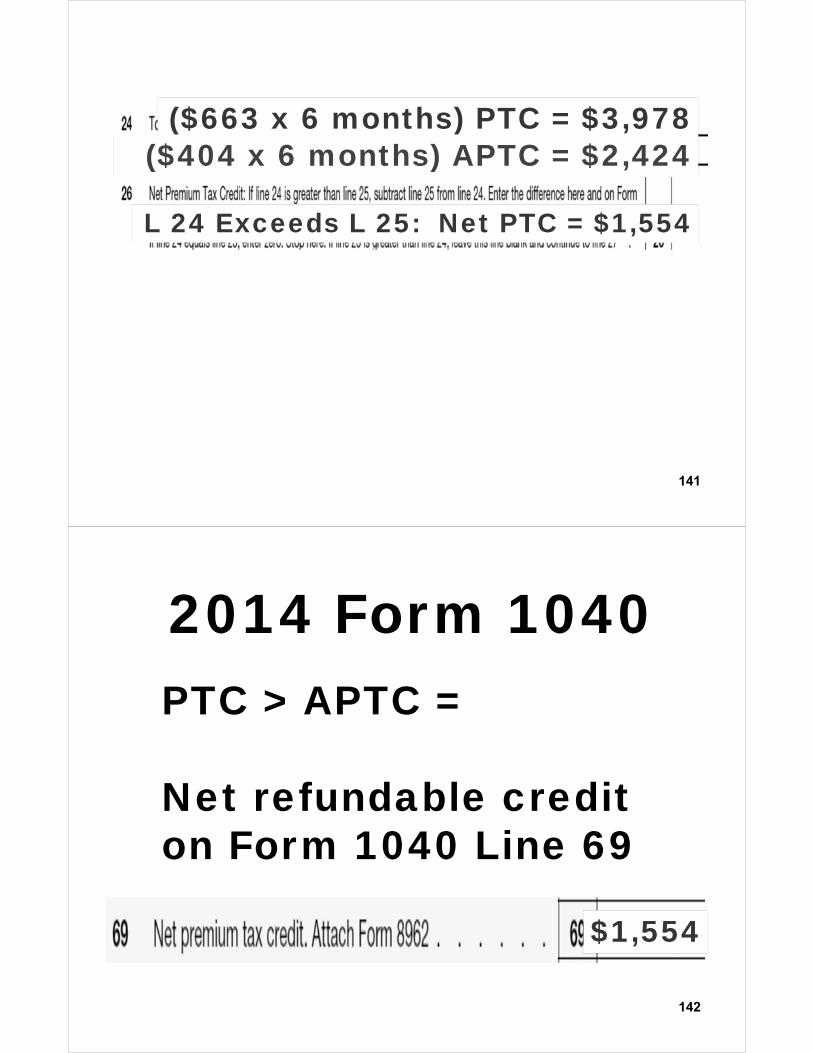

($663 x 6 months) PTC = $3,978($404 x 6 months) APTC = $2,424

L 24 Exceeds L 25: Net PTC = $1,554

2014 Form 1040

142

PTC > APTC =

Net refundable credit on Form 1040 Line 69

$1,554

143

What if an employee with a new 2014 job and a tax family of 3

declines “affordable” (self-only) coverage, and purchases family coverage on the exchange, in

order to get the premium credit but does not tell the Exchange or IRS on Form 8962 about the

employer coverage.

144

Will the exchange or IRS know that none of the members of the family

qualified for the APTC or the PTC?

No Form 1095-B or C for2014

145

W-2 will suggest no employer coverage

because it was declined

146

Draft Form 1095-C

147

148

Optional Form

In 2014

And Only ALEsIn 2015+

149

New FactsNo

AdvancePTC

150

H&W & C’s MAGI

Was Projected at $1,000,000 but they

purchased family health insurance on the

exchange

Family Net Worth $10 Mil.

151

Are they eligible for the PTC?

What will Form 1095-A Look

Like?

152

Form 1095-A Part IIINeither their premiums nor

their SLCSP are based upon HI.But no APTC

153

Form 1095-A Part III

154

Form 1095-A Part III

155

They unexpectedly have a $950,000 IRC

sec. 1231 loss dropping

2014 MAGI to $39,060

156

SLCSP Annual Prem. $10,414

Annual Contrib. Amt.* - $2,460PTC $7,954APTC (Form 1095-A) -$0Net Refundable PTC $7,954

*$39,060 x .0630 = $2,460

Form 8982 Summary

157

Part 3Repayment of Excess APTC

158

Part 4:Shared

Policy Allocation

159

160

One Insurance Policy:

Two Tax Families and two coverage

families (of 3 and 1)

161

Premium $15,000

Gary’s SLCSP is $12,000 (for 3)

Jim’s SLCSP is $6,000 (for 1)

162

Gary

Jim’s SSN

.67

163

Part 5:Alternate

Calculation For Year of Marriage

164

Allows the couple to use ½ their HI in pre-marriage

months

165

Rev. Proc. 2014-41 (July 25, 2014)

Self-Employed Health Insurance

Deduction and PTC

3-52

166

Guidance on and examples of the

calculation methods a taxpayer may use to resolve the circular

relationship between the IRC sec. 162(l)

deduction and the PTC.

167

Cost-sharing subsidies lower deductibles and the total out-of-pocket costs under the plan:

• HI must not exceed 250% of federal poverty level.

• Must purchase a silver plan.

Related Documents