ACA Best Practices: Annual Healthcare Reporting & Strategic Employee Communications (Form 1095-C) ADP Workforce Now ® Current Version

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACA Best Practices: Annual Healthcare Reporting & Strategic Employee Communications (Form 1095-C)

ADP Workforce Now® Current Version

3

Our Speakers

© Copyright 2015 ADP, LLC. Proprietary Information.

John JankeSr. Director of Program Management, ACAADP, LLC

John is a Certified Healthcare Reform Specialist and has been an ADP Associate for more than 30 years. For the past 4 years, he has been leading the ACA Program for ADP Major Accounts and often speaks on this topic at ADP and industry events. He is widely regarded as an ACA subject‐matter expert.

Mary serves as VP in ADP’s HCM Strategic Advisory Services group. As a communications expert, she is responsible for consulting with clients to provide strategy, advice, insight and practical communications solutions to help drive change. She also leads ADP’s HCM Strategic Communications group, a team that develops communications for clients. Mary brings 19 years of dynamic, innovative and well‐rounded marketing leadership with documented success in communications, marketing, public relations, branding, events, and employee programs.

Mary SchaferVice President, HCM Strategic CommunicationsADP, LLC

4

This presentation is not: Legal Advice The Final Word on Health Care Reform A Political Opinion

Disclaimer

ADP DOES NOT PRACTICE LAW OR GIVE LEGAL ADVICE

ADP STRONGLY RECOMMENDS THAT CLIENTS OBTAIN QUALIFIED LEGAL COUNSEL PRIOR TO MAKING ANY DECISIONS

5

How prepared is your company/organization to effectively manage the complexity of Annual Reporting? Not at all SlightlyModerately Very Extremely

Polling Question #1

5© Copyright 2015 ADP, LLC. Proprietary Information.

6

In this webinar, we will review several topics: Understanding the Annual Reporting Requirements

Workforce Now Sources of Data for Forms 1095‐C and 1094‐C

Explanation and Examples of Form 1095‐C: Employer‐Provided Health Insurance Offer and Coverage

Explanation and Examples of Form 1094‐C: Transmittal of Employer‐Provided Health Insurance Offer and Coverage Information Returns

Webinar Program

7

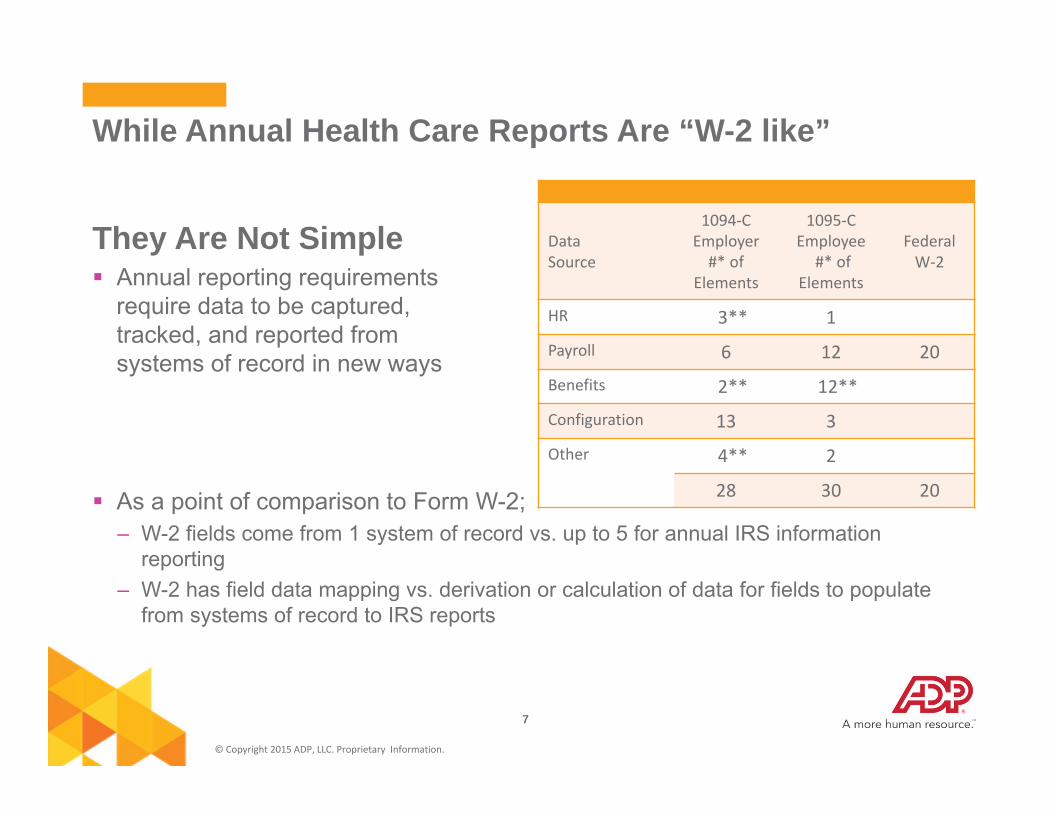

They Are Not Simple Annual reporting requirements

require data to be captured, tracked, and reported from systems of record in new ways

As a point of comparison to Form W-2;– W-2 fields come from 1 system of record vs. up to 5 for annual IRS information

reporting – W-2 has field data mapping vs. derivation or calculation of data for fields to populate

from systems of record to IRS reports

While Annual Health Care Reports Are “W-2 like”

© Copyright 2015 ADP, LLC. Proprietary Information.

DataSource

1094‐C Employer#* of

Elements

1095‐C Employee

#* ofElements

Federal W‐2

HR 3** 1

Payroll 6 12 20

Benefits 2** 12**

Configuration 13 3

Other 4** 2

28 30 20

8

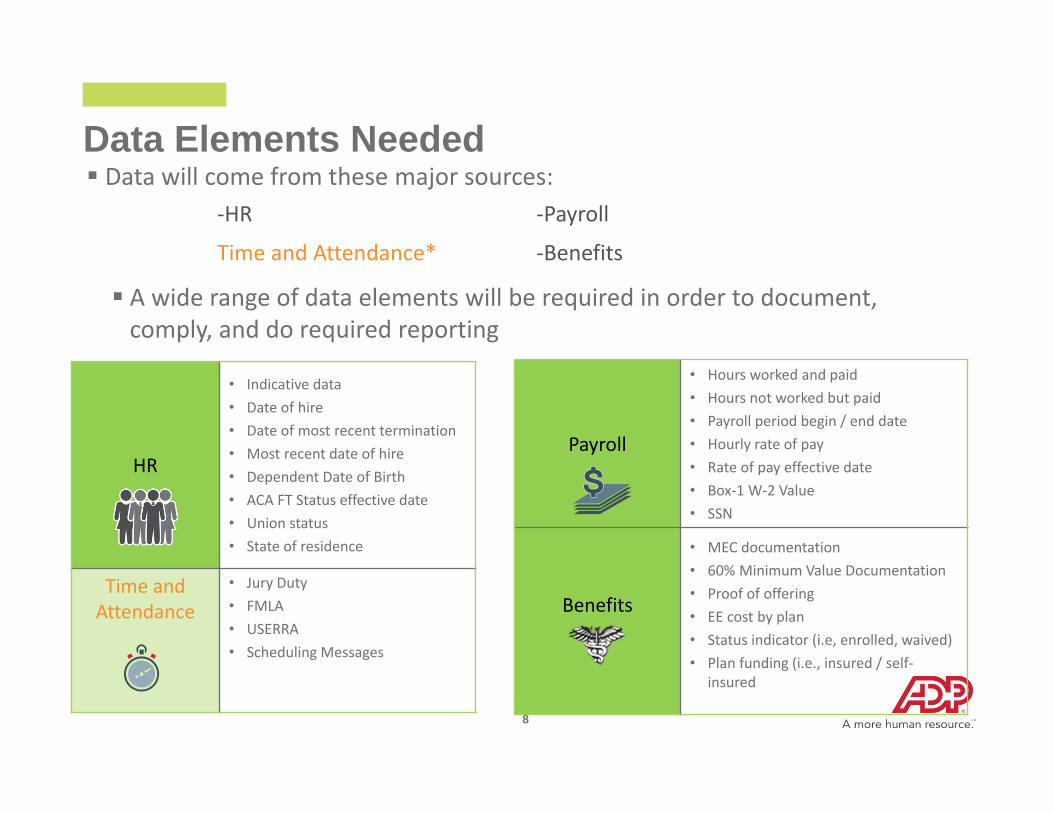

Data Elements Needed Data will come from these major sources:

HR

• Indicative data• Date of hire• Date of most recent termination• Most recent date of hire• Dependent Date of Birth• ACA FT Status effective date• Union status• State of residence

Time and Attendance

• Jury Duty• FMLA• USERRA• Scheduling Messages

Payroll

• Hours worked and paid• Hours not worked but paid• Payroll period begin / end date• Hourly rate of pay• Rate of pay effective date• Box‐1 W‐2 Value• SSN

Benefits

• MEC documentation• 60% Minimum Value Documentation• Proof of offering• EE cost by plan• Status indicator (i.e, enrolled, waived)• Plan funding (i.e., insured / self‐

insured

‐HR ‐Payroll

Time and Attendance* ‐Benefits

A wide range of data elements will be required in order to document, comply, and do required reporting

9

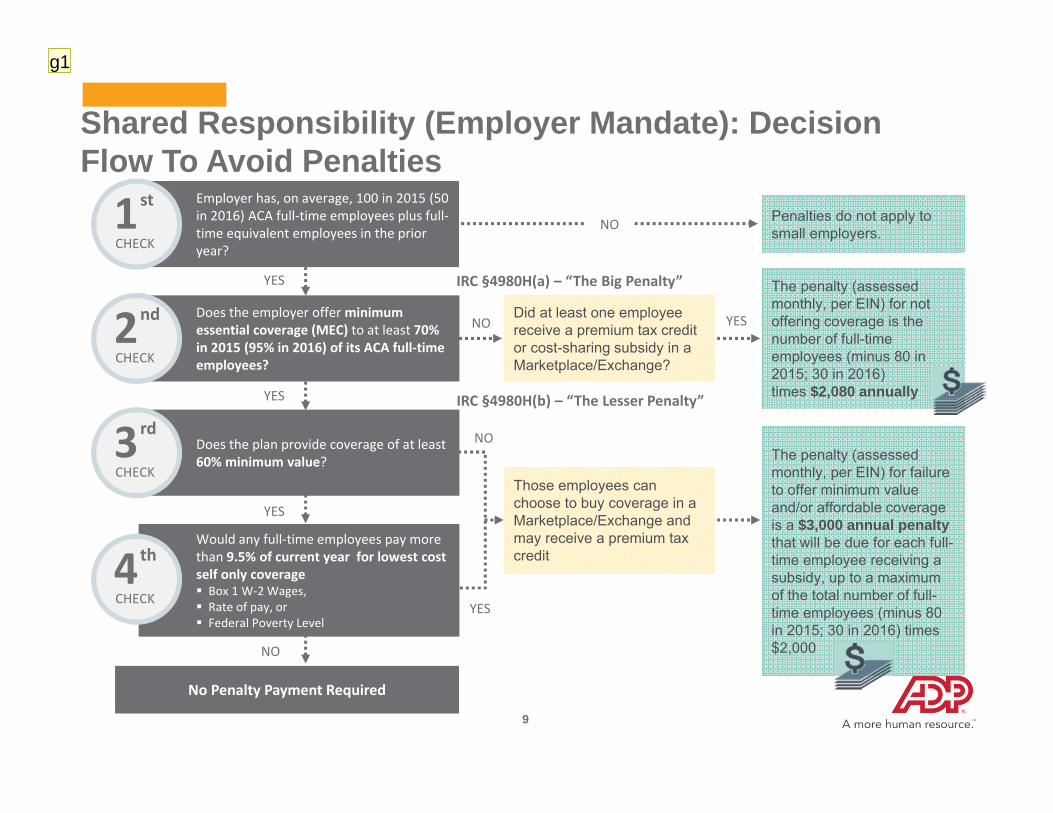

Did at least one employee receive a premium tax credit or cost-sharing subsidy in a Marketplace/Exchange?

Those employees can choose to buy coverage in a Marketplace/Exchange and may receive a premium tax credit

The penalty (assessed monthly, per EIN) for not offering coverage is the number of full-time employees (minus 80 in 2015; 30 in 2016) times $2,080 annually

The penalty (assessed monthly, per EIN) for failure to offer minimum value and/or affordable coverage is a $3,000 annual penalty that will be due for each full-time employee receiving a subsidy, up to a maximum of the total number of full-time employees (minus 80 in 2015; 30 in 2016) times $2,000

Penalties do not apply to small employers.

No Penalty Payment Required

Employer has, on average, 100 in 2015 (50 in 2016) ACA full‐time employees plus full‐time equivalent employees in the prior year?

1st

CHECK

Does the employer offer minimum essential coverage (MEC) to at least 70% in 2015 (95% in 2016) of its ACA full‐time employees?

2nd

CHECK

Does the plan provide coverage of at least 60% minimum value?

3rd

CHECK

Would any full‐time employees pay more than 9.5% of current year for lowest cost self only coverage Box 1 W‐2 Wages, Rate of pay, or Federal Poverty Level

4th

CHECK

YES

YES

YES

NO

NO

NO YES

NO

YES

IRC §4980H(a) – “The Big Penalty”

IRC §4980H(b) – “The Lesser Penalty”

Shared Responsibility (Employer Mandate): Decision Flow To Avoid Penalties

g1

Slide 9

g1 In the first Check - it is not 50 full-time "plus" 50 Full-time equivalents - it is 50 full-time employees INCLUDING full-time equivalent employees. greenji, 9/16/2015

10

What do employers need to know about Affordable Care Act reporting?Under the Affordable Care Act (ACA), Applicable Large Employers (ALEs) are required to take some new actions.

These employers must file information returns with the IRS and also provide statements to full‐time employees about health coverage the employer offered or to show the employer didn’t offer coverage.

Information reporting was voluntary for calendar year 2014. All applicable large employers are required to report health coverage information for the first time in early 2016 for calendar year 2015.

11

What is an Applicable Large Employer?

An Applicable Large Employer (ALE) is an employer with 50 or more full‐time employees – including full‐time equivalent (FTE) employees

A full‐time employee is defined by ACA as working 30 hours per week and/or 130 hours per month

• ALE’s with 50‐99 full‐time employees (including FTE employees) will not be penalized for non‐compliance with Employer Shared Responsibility requirements in 2015, but are required to provide 1095‐C forms to full‐time employees and file a copy with the IRS

• ALE’s with 100 or more full‐time employees (including FTE employees) are also subject to other the Employer Shared Responsibility requirements in 2015, and can be penalized for non‐compliance

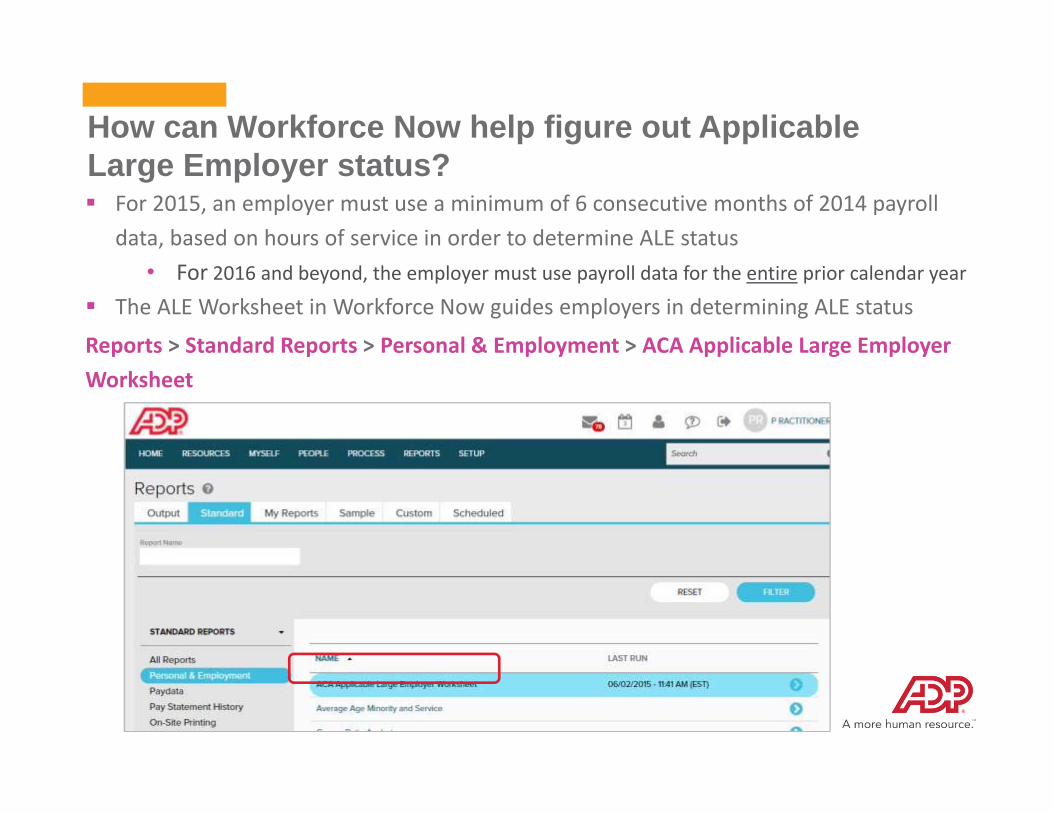

12

How can Workforce Now help figure out Applicable Large Employer status? For 2015, an employer must use a minimum of 6 consecutive months of 2014 payroll

data, based on hours of service in order to determine ALE status• For 2016 and beyond, the employer must use payroll data for the entire prior calendar year

The ALE Worksheet in Workforce Now guides employers in determining ALE status

Reports > Standard Reports > Personal & Employment > ACA Applicable Large Employer Worksheet

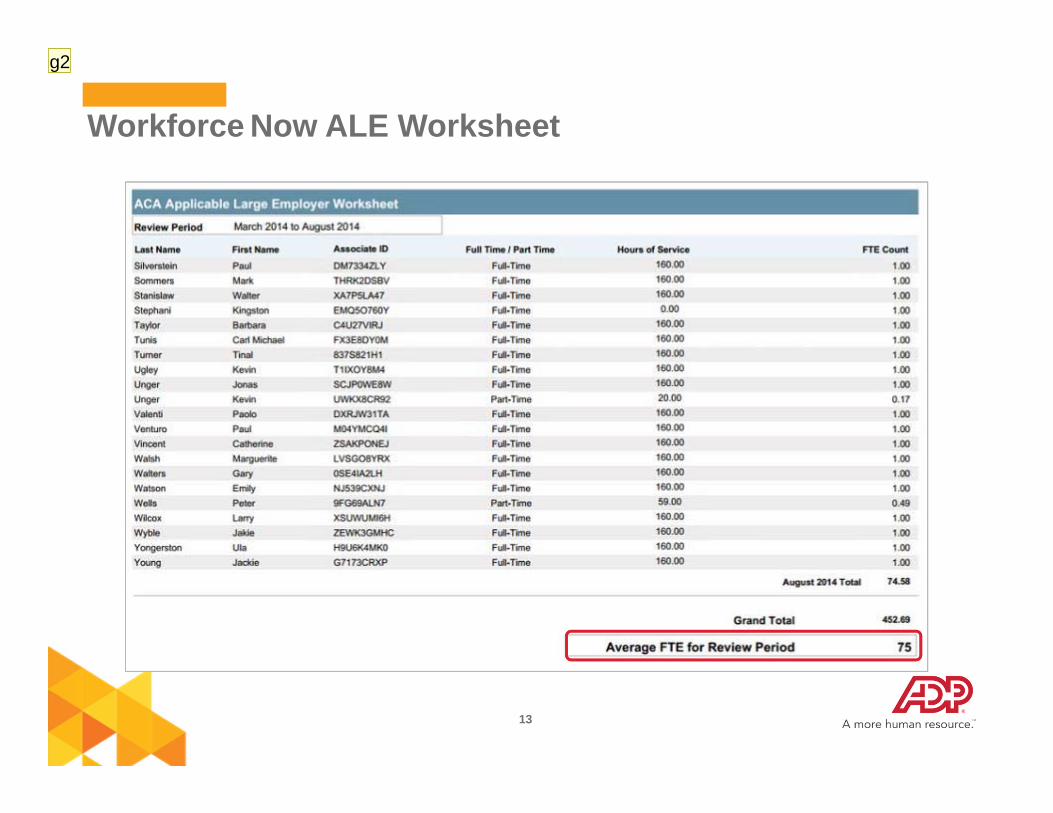

13

Workforce Now ALE Worksheet

g2

Slide 13

g2 Note that there is a new rule where clients can exclude any veterans from this number if the veteran receives govt health insuarnce like TRICARE or VA coverage. Just in case it comes up. Law was just signed in July. greenji, 9/16/2015

14

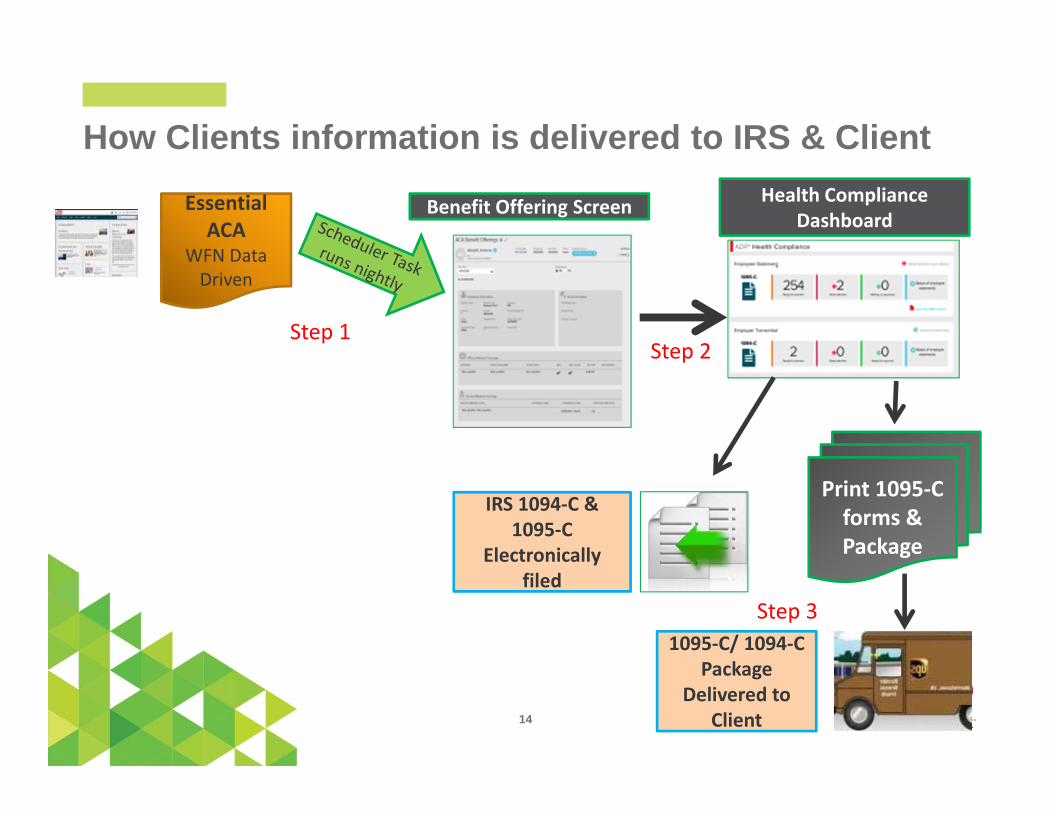

How Clients information is delivered to IRS & Client

Benefit Offering ScreenEssential ACA

WFN Data Driven

Health Compliance Dashboard

IRS 1094‐C & 1095‐C

Electronically filed

Print 1095‐C forms & Package

1095‐C/ 1094‐C Package

Delivered to Client

Step 1Step 2

Step 3

15

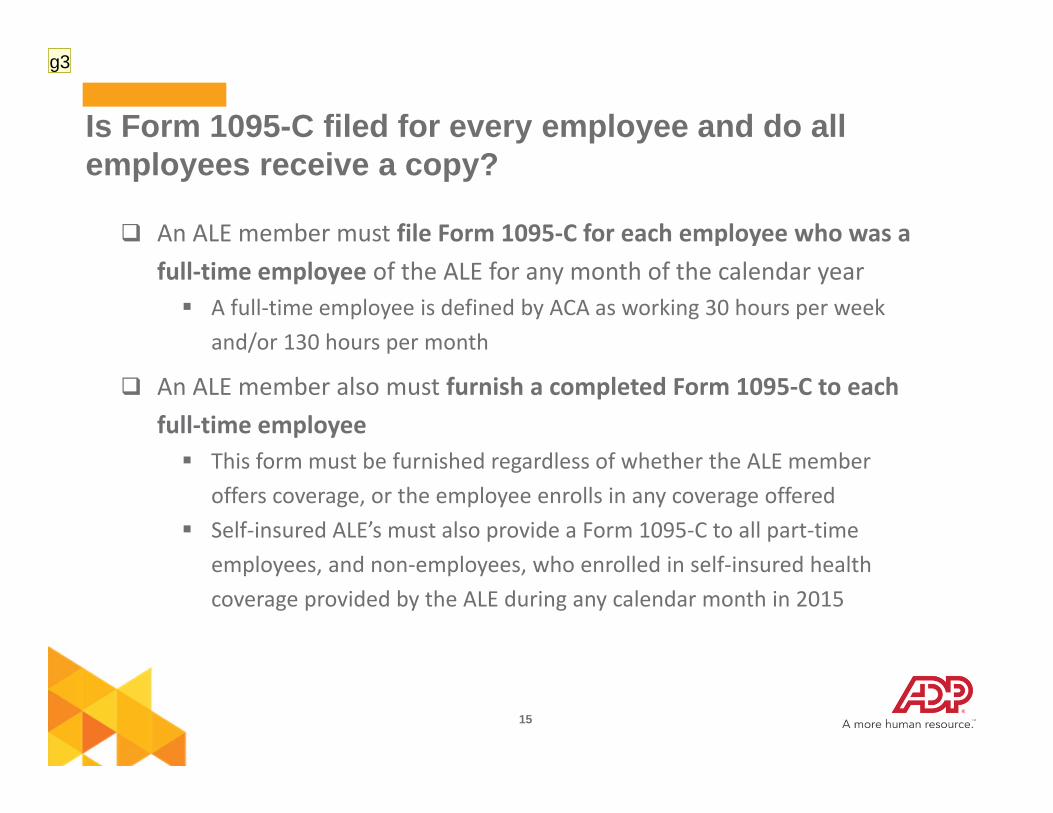

Is Form 1095-C filed for every employee and do all employees receive a copy?

An ALE member must file Form 1095‐C for each employee who was a full‐time employee of the ALE for any month of the calendar year A full‐time employee is defined by ACA as working 30 hours per week

and/or 130 hours per month

An ALE member also must furnish a completed Form 1095‐C to each full‐time employee This form must be furnished regardless of whether the ALE member

offers coverage, or the employee enrolls in any coverage offered Self‐insured ALE’s must also provide a Form 1095‐C to all part‐time

employees, and non‐employees, who enrolled in self‐insured health coverage provided by the ALE during any calendar month in 2015

g3

Slide 15

g3 ADP is not supporting any of the alternative reporting method - including these substitute forms. greenji, 9/16/2015

16

How can Workforce Now help determineFull-Time Employee Status?There are several tools in Workforce Now: Measurement Periods to establish employee status ACA Look‐Back Worksheet to review ACA full‐time or part‐time status

on a month‐by‐month basis

New Employees: Employees “reasonably expected” to work 30 hours or more per week, or 130 hours or more

per month, need to be offered coverage within the first 3 months of employment Employees not “reasonably expected” to work 30 hours or more per week, or 130 hours or

more per month, can be included in Initial Measurement Periods (IMP) to determine full‐time or part‐time status

Ongoing Employees: Employees need to be included in Standard Measurement Periods (SMP) to determine full‐

time or part‐time status

17

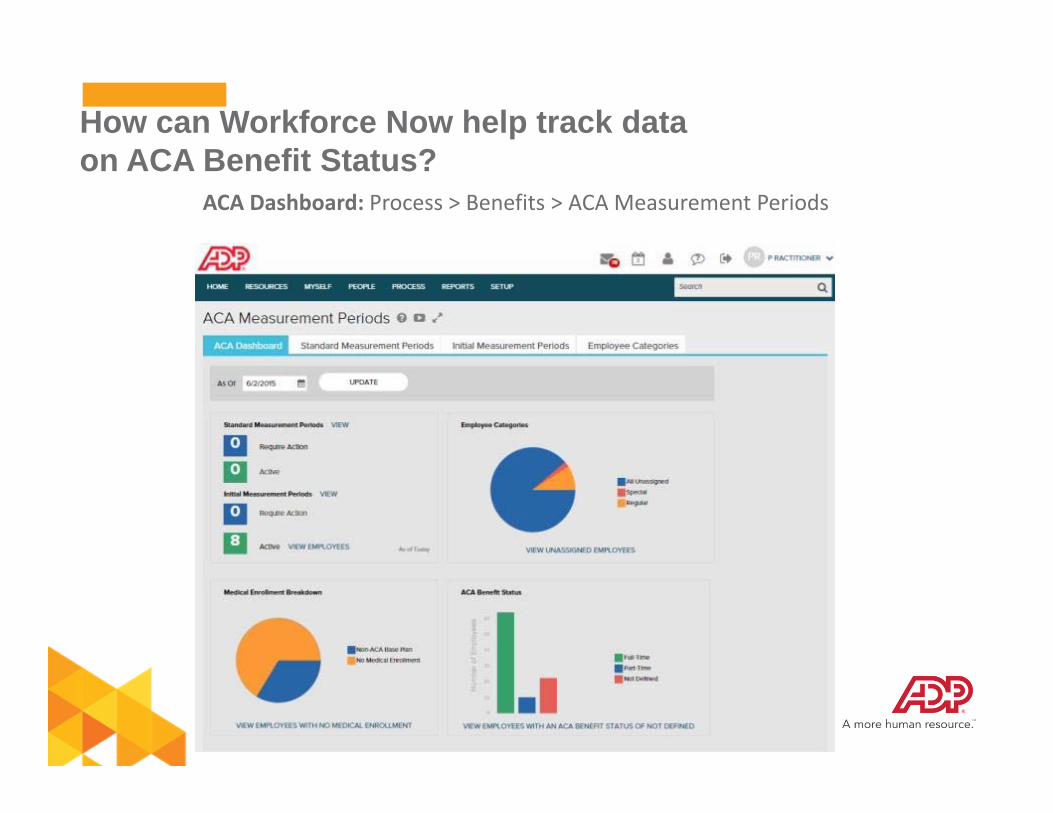

How can Workforce Now help track dataon ACA Benefit Status?

ACA Dashboard: Process > Benefits > ACA Measurement Periods

18

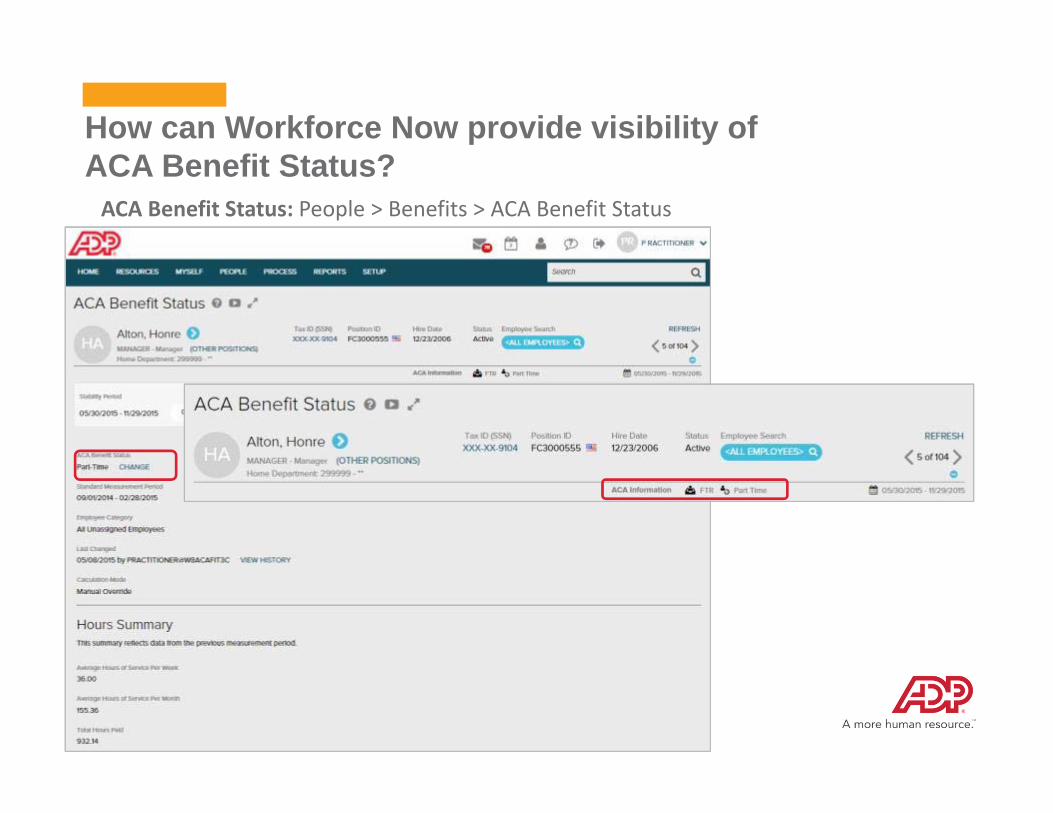

How can Workforce Now provide visibility of ACA Benefit Status?ACA Benefit Status: People > Benefits > ACA Benefit Status

19

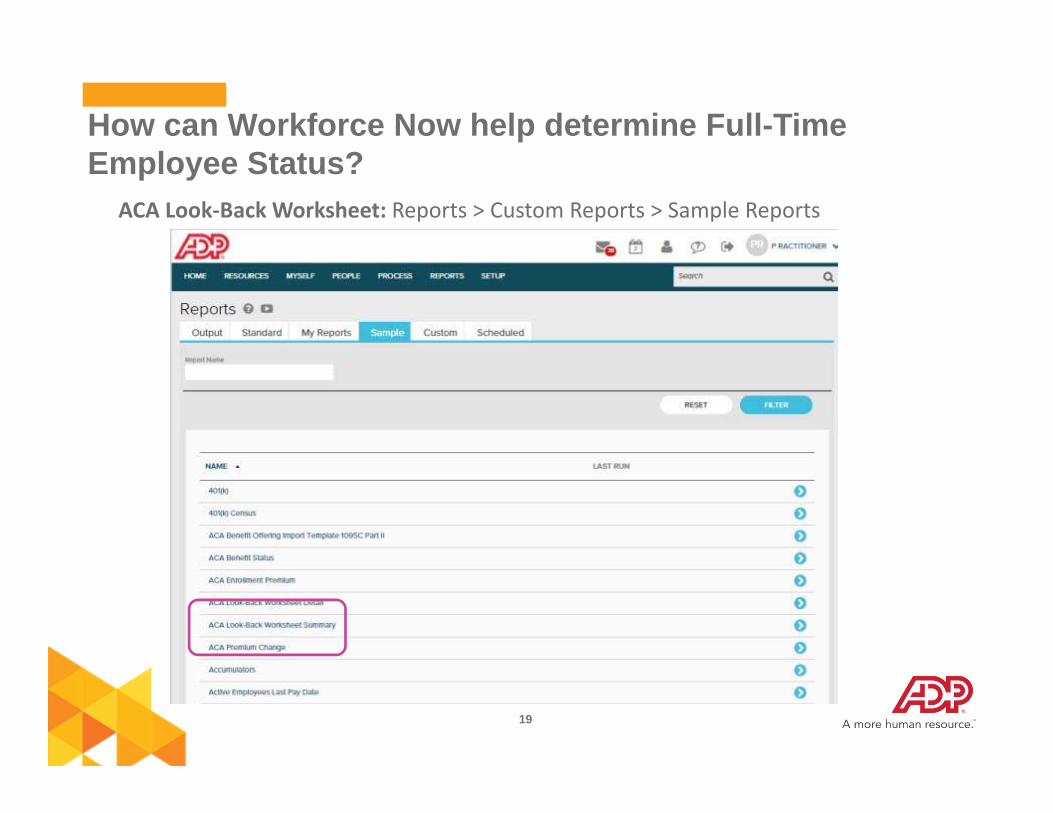

How can Workforce Now help determine Full-Time Employee Status?

ACA Look‐Back Worksheet: Reports > Custom Reports > Sample Reports

20

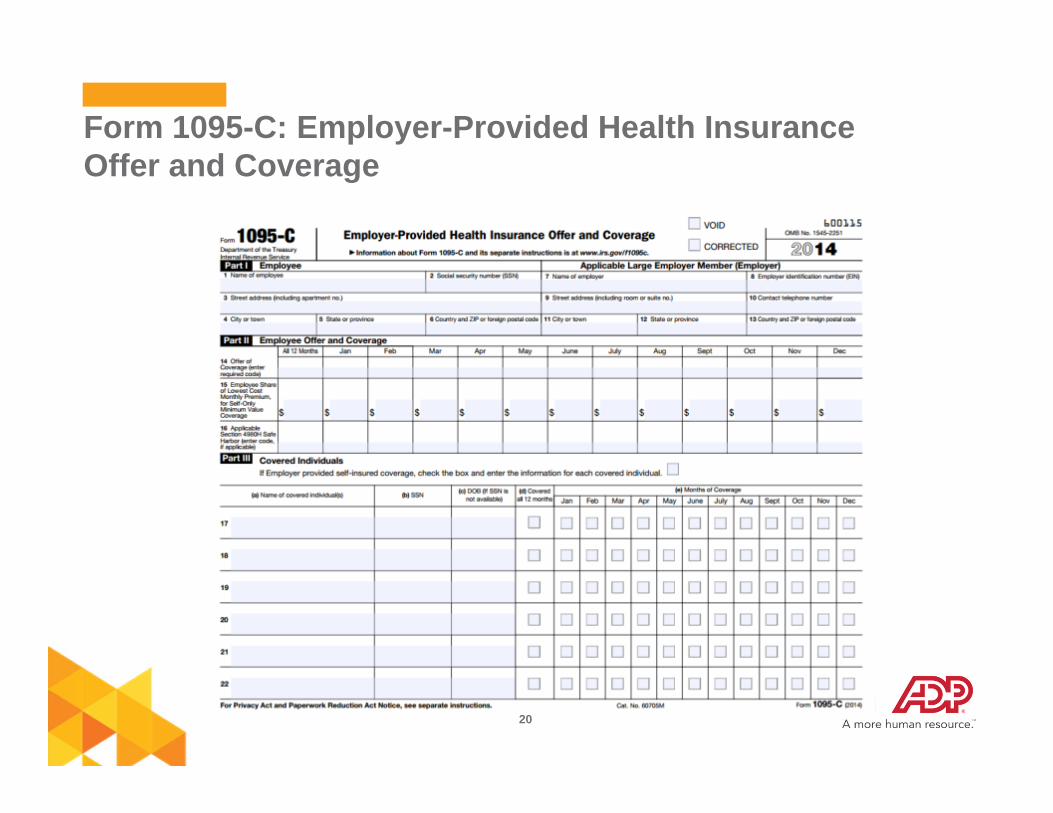

Form 1095-C: Employer-Provided Health InsuranceOffer and Coverage

21

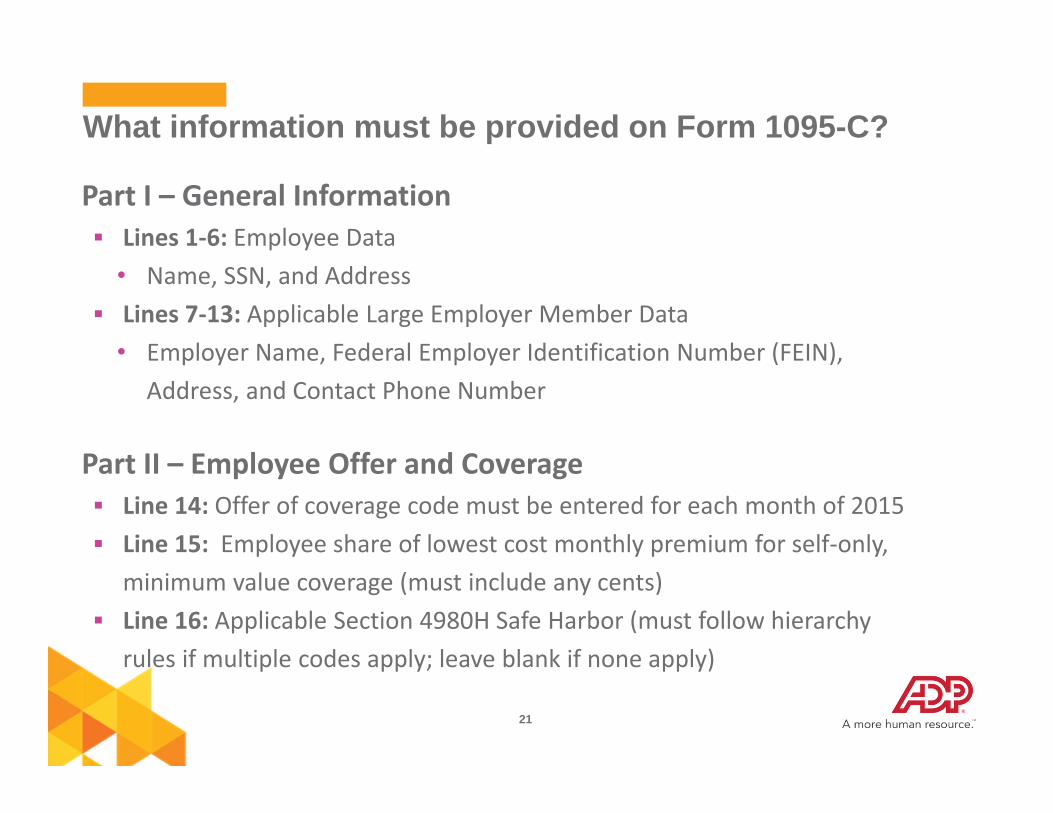

Part I – General Information Lines 1‐6: Employee Data

• Name, SSN, and Address Lines 7‐13: Applicable Large Employer Member Data

• Employer Name, Federal Employer Identification Number (FEIN), Address, and Contact Phone Number

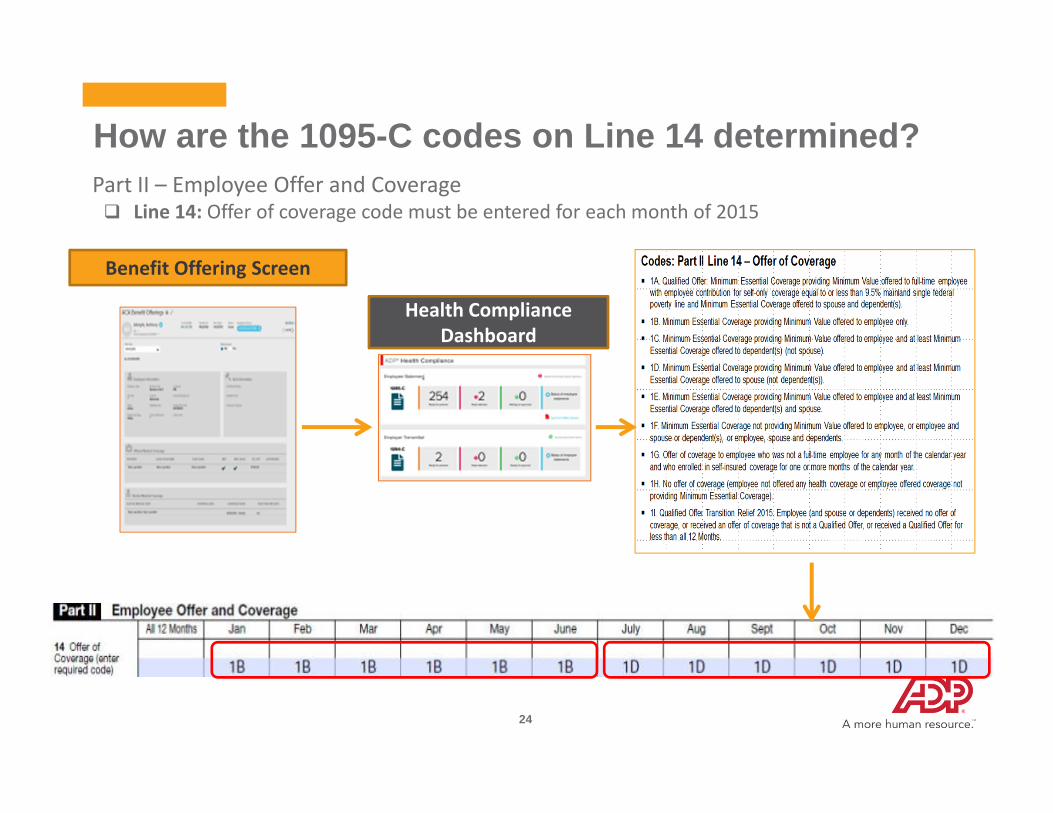

Part II – Employee Offer and Coverage Line 14: Offer of coverage code must be entered for each month of 2015 Line 15: Employee share of lowest cost monthly premium for self‐only,

minimum value coverage (must include any cents) Line 16: Applicable Section 4980H Safe Harbor (must follow hierarchy

rules if multiple codes apply; leave blank if none apply)

What information must be provided on Form 1095-C?

22

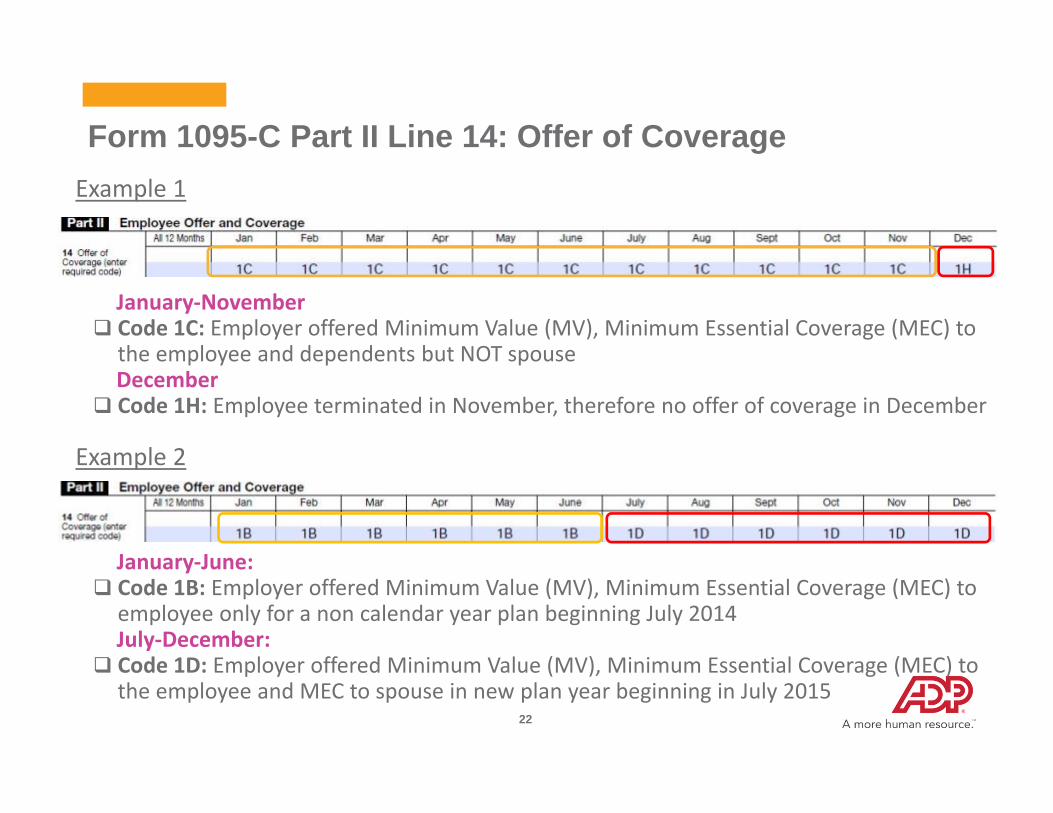

Example 1

January‐November Code 1C: Employer offered Minimum Value (MV), Minimum Essential Coverage (MEC) to

the employee and dependents but NOT spouseDecember

Code 1H: Employee terminated in November, therefore no offer of coverage in December

Example 2

January‐June: Code 1B: Employer offered Minimum Value (MV), Minimum Essential Coverage (MEC) to

employee only for a non calendar year plan beginning July 2014July‐December:

Code 1D: Employer offered Minimum Value (MV), Minimum Essential Coverage (MEC) to the employee and MEC to spouse in new plan year beginning in July 2015

Form 1095-C Part II Line 14: Offer of Coverage

23

Setup > Benefits > Plan Setup: Plan Class Details

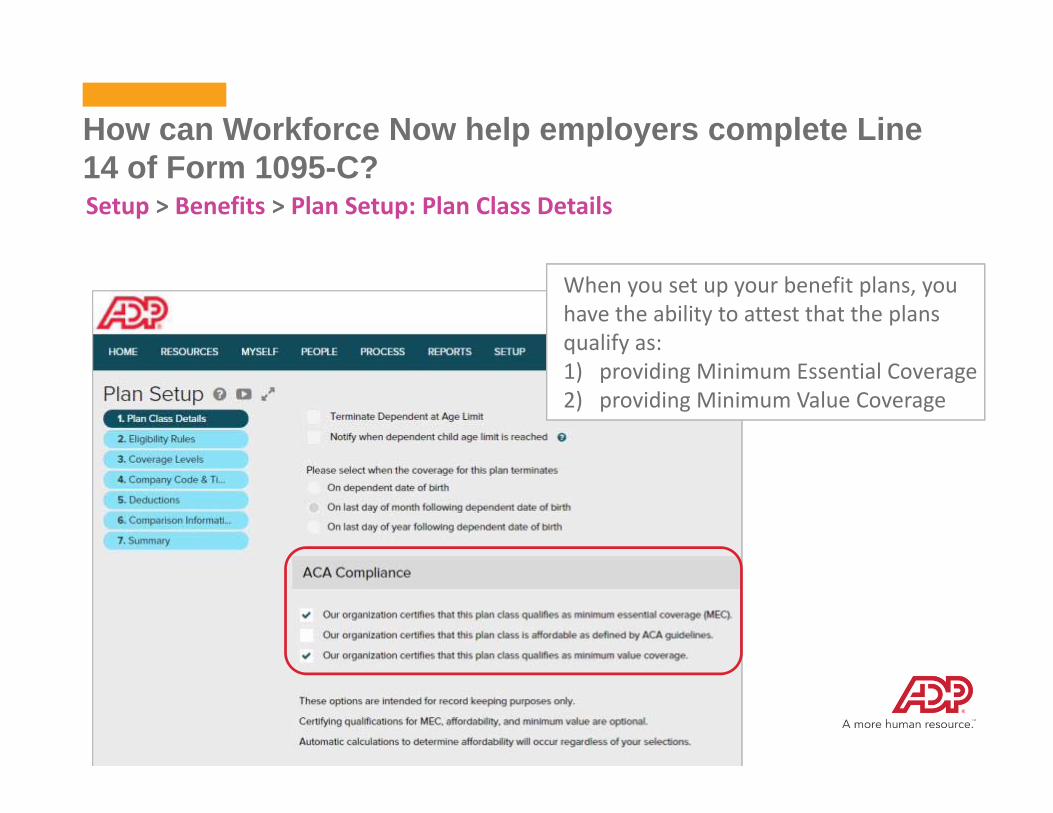

How can Workforce Now help employers complete Line 14 of Form 1095-C?

When you set up your benefit plans, you have the ability to attest that the plans qualify as: 1) providing Minimum Essential Coverage2) providing Minimum Value Coverage

24

How are the 1095-C codes on Line 14 determined?Part II – Employee Offer and Coverage Line 14: Offer of coverage code must be entered for each month of 2015

Benefit Offering Screen

Health Compliance Dashboard

25

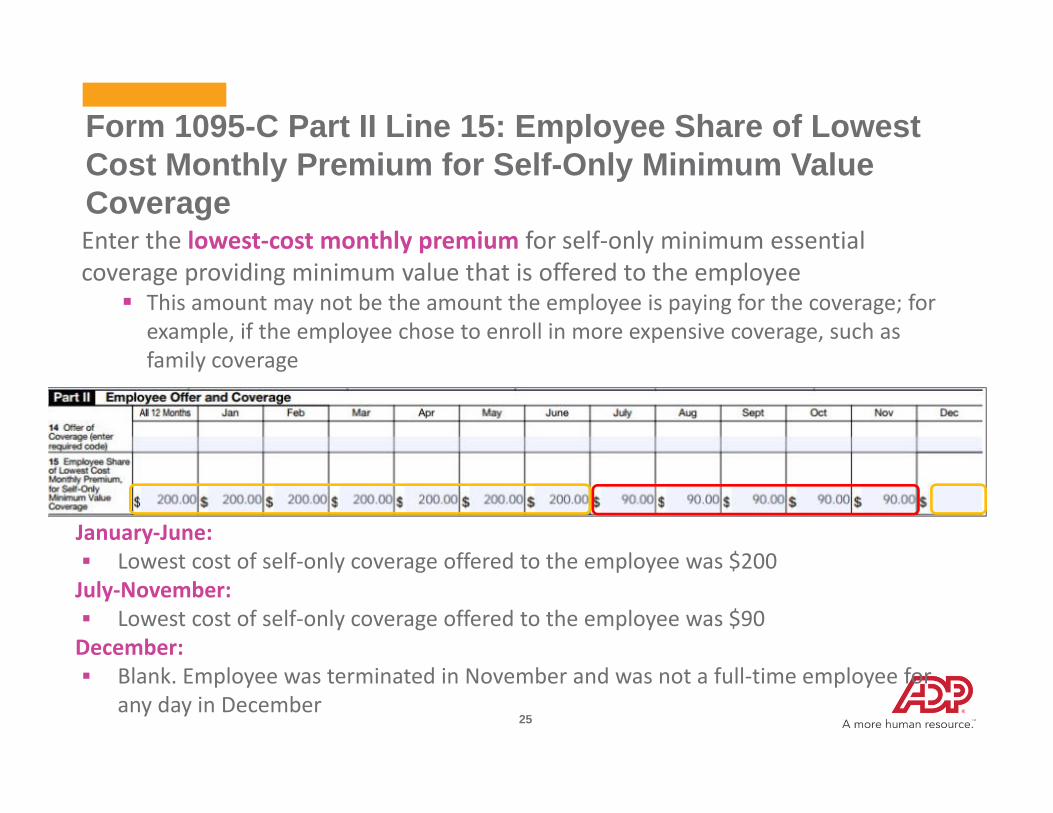

Enter the lowest‐cost monthly premium for self‐only minimum essential coverage providing minimum value that is offered to the employee This amount may not be the amount the employee is paying for the coverage; for

example, if the employee chose to enroll in more expensive coverage, such as family coverage

January‐June: Lowest cost of self‐only coverage offered to the employee was $200July‐November: Lowest cost of self‐only coverage offered to the employee was $90December: Blank. Employee was terminated in November and was not a full‐time employee for

any day in December

Form 1095-C Part II Line 15: Employee Share of Lowest Cost Monthly Premium for Self-Only Minimum Value Coverage

26

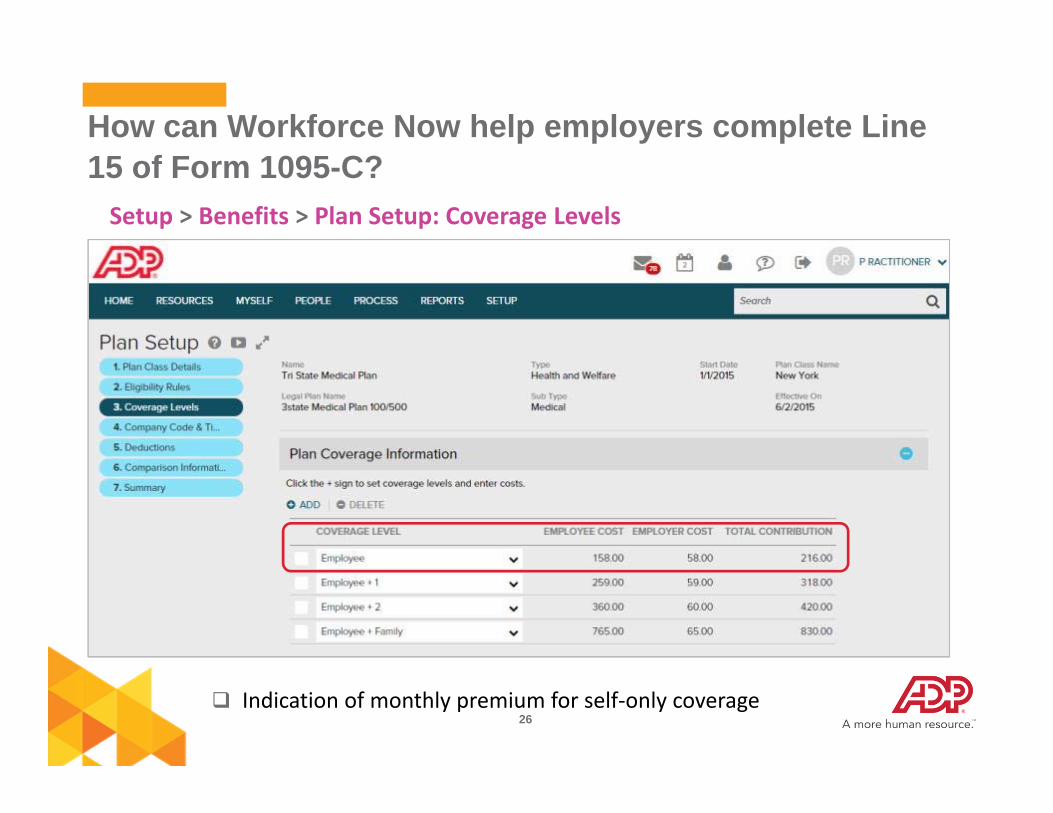

Setup > Benefits > Plan Setup: Coverage Levels

Indication of monthly premium for self‐only coverage

How can Workforce Now help employers complete Line 15 of Form 1095-C?

27

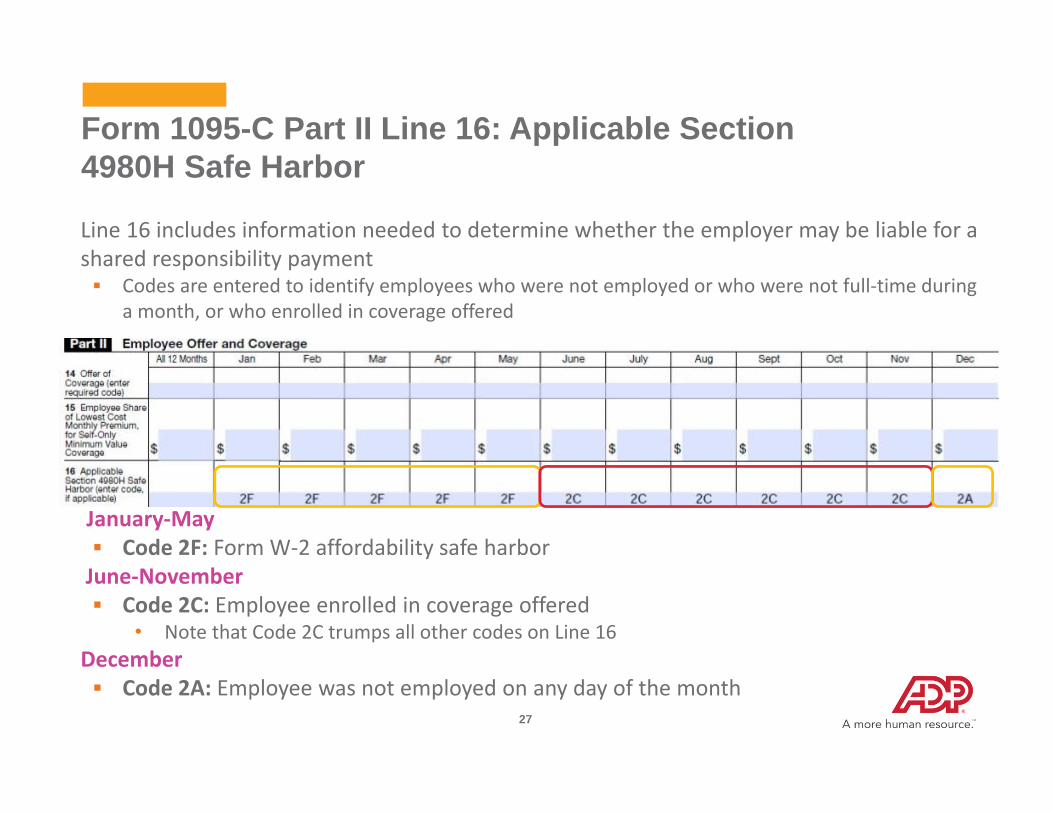

Line 16 includes information needed to determine whether the employer may be liable for a shared responsibility payment Codes are entered to identify employees who were not employed or who were not full‐time during

a month, or who enrolled in coverage offered

January‐May Code 2F: Form W‐2 affordability safe harborJune‐November Code 2C: Employee enrolled in coverage offered

• Note that Code 2C trumps all other codes on Line 16December Code 2A: Employee was not employed on any day of the month

Form 1095-C Part II Line 16: Applicable Section 4980H Safe Harbor

28

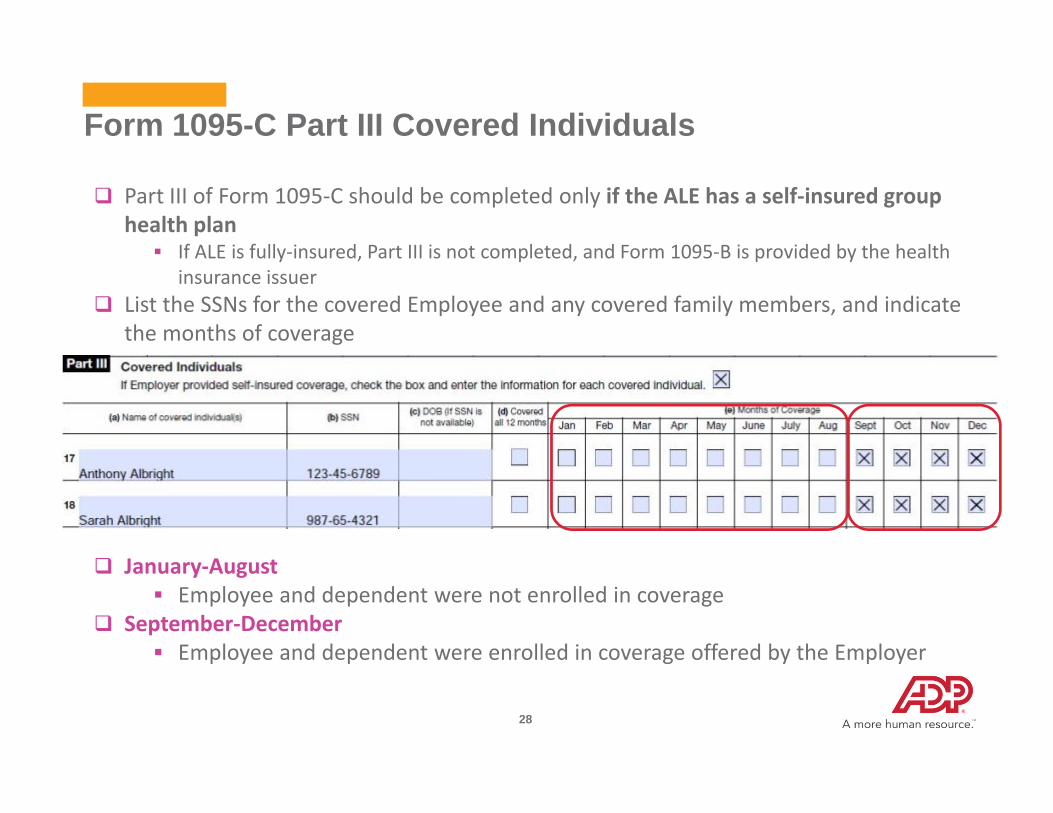

Form 1095-C Part III Covered Individuals

Part III of Form 1095‐C should be completed only if the ALE has a self‐insured group health plan If ALE is fully‐insured, Part III is not completed, and Form 1095‐B is provided by the health

insurance issuer List the SSNs for the covered Employee and any covered family members, and indicate

the months of coverage

January‐August Employee and dependent were not enrolled in coverage

September‐December Employee and dependent were enrolled in coverage offered by the Employer

29

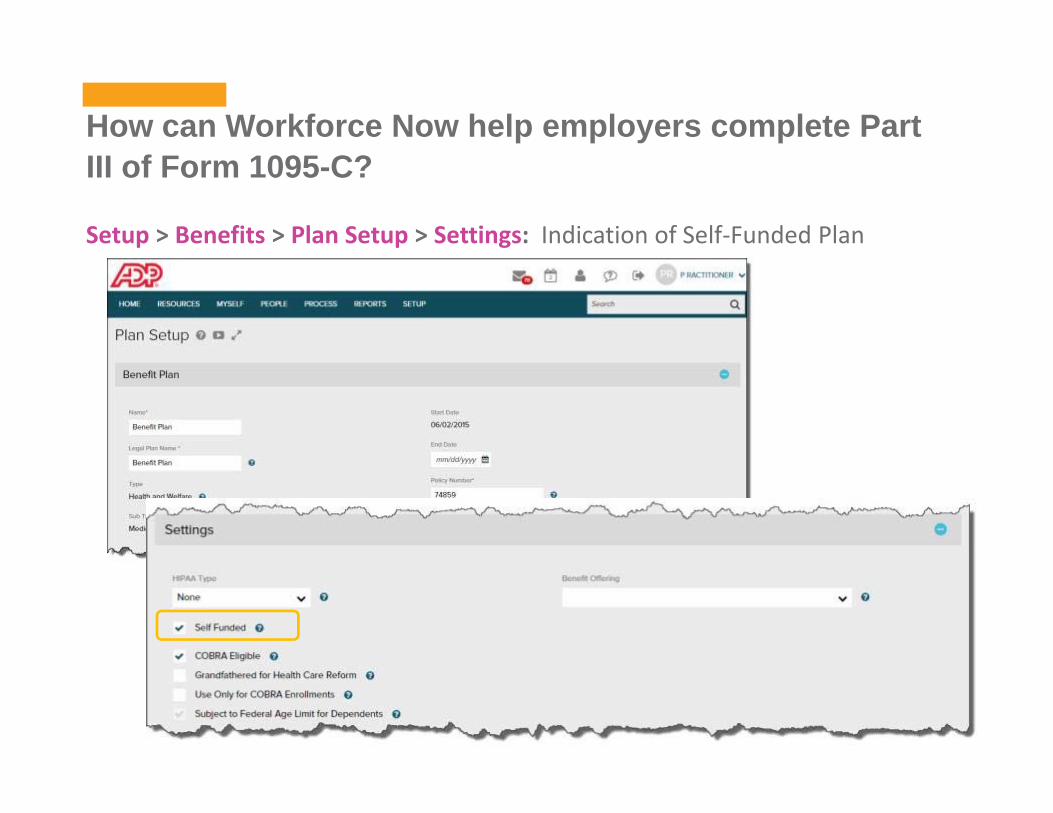

Setup > Benefits > Plan Setup > Settings: Indication of Self‐Funded Plan

How can Workforce Now help employers complete Part III of Form 1095-C?

30

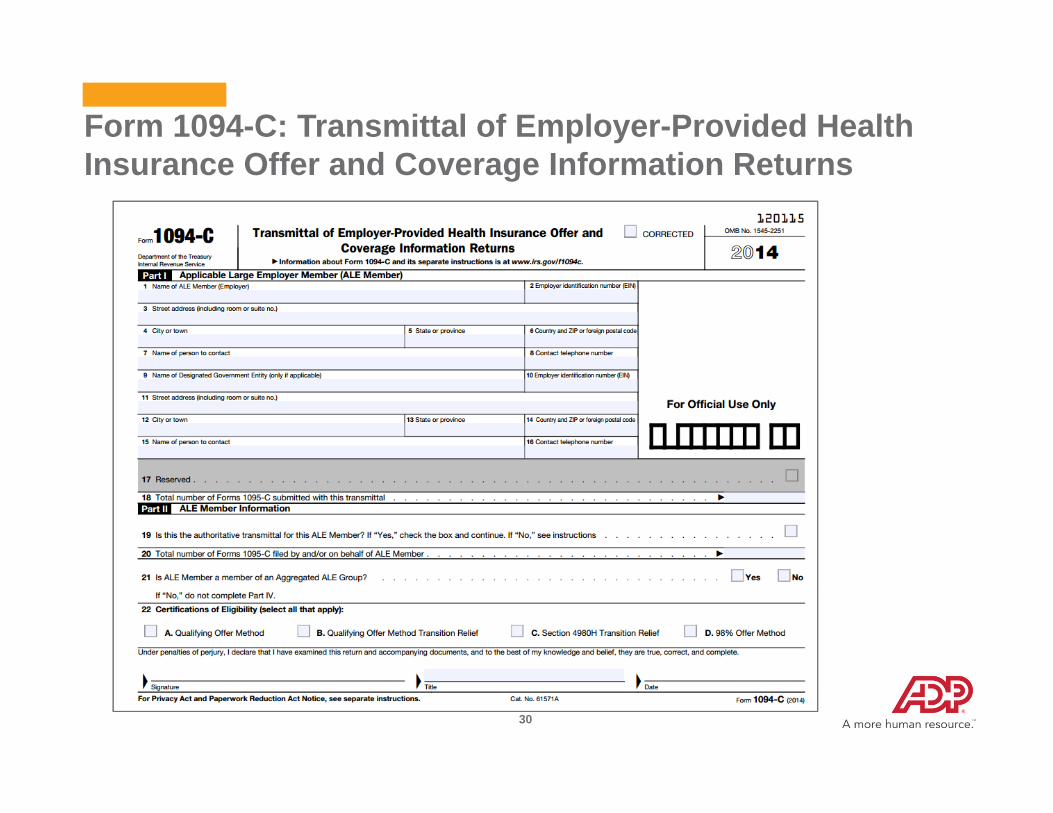

Form 1094-C: Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns

31

An ALE is required to file a Form 1094‐C even if the ALE does not offer health coverage to its employees Separate reporting of 1094‐C must be submitted for each Federal Employer

Identification Number (FEIN) associated with an ALE Separate reporting by FEIN is required even if several related ALEs using

different FEINs are covered under the same health plan If an Aggregated ALE Group includes multiple FEINs, each FEIN for each

member of the group must be listed in Part IV

Note: An Aggregated ALE Group refers to a group of ALE Members treated as a single employer under section 414(b),(c), (m) or (o) of the Internal Revenue Code.

ADP recommends that employers consult with outside counsel to determine if they are members of an Aggregated Group of ALEs.

Will all employers need to complete Form 1094-C?

32

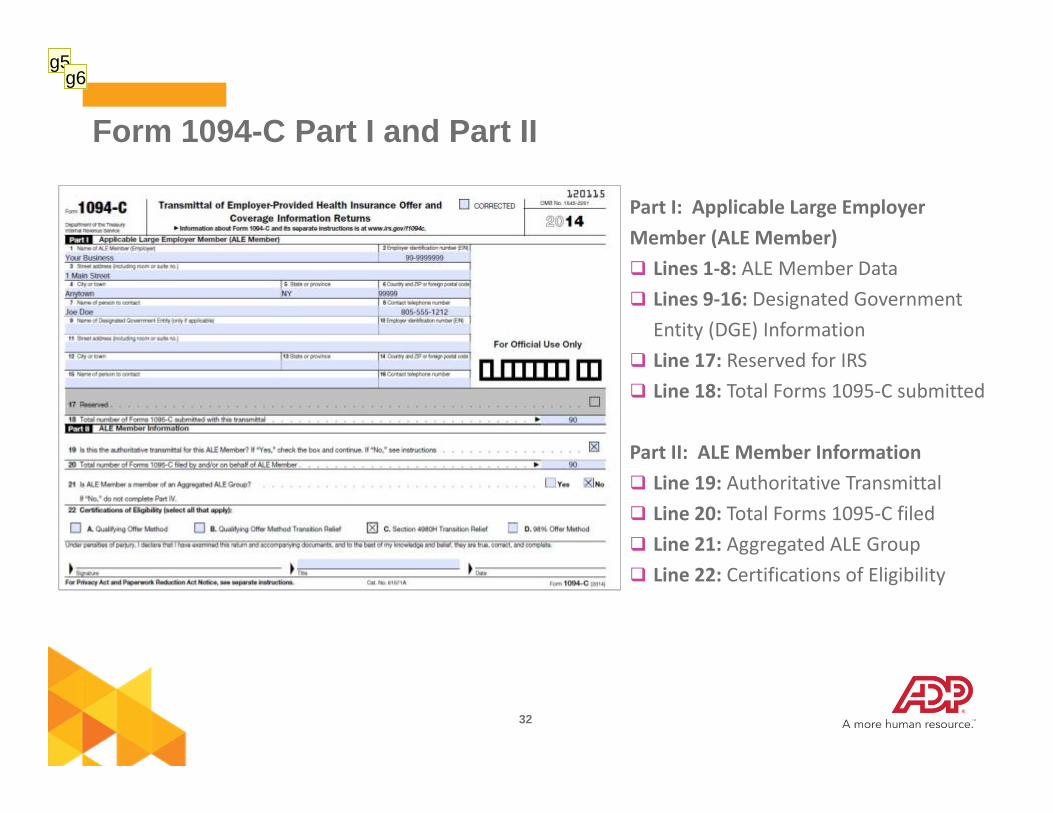

Form 1094-C Part I and Part II

Part I: Applicable Large Employer Member (ALE Member) Lines 1‐8: ALE Member Data Lines 9‐16: Designated Government

Entity (DGE) Information Line 17: Reserved for IRS Line 18: Total Forms 1095‐C submitted

Part II: ALE Member Information Line 19: Authoritative Transmittal Line 20: Total Forms 1095‐C filed Line 21: Aggregated ALE Group Line 22: Certifications of Eligibility

g5g6

Slide 32

g5 John - It's not really that an employer should consult with outside counsel to determine if they are part of a DGE. It is more that if theDGE is going to file on behalf of another FEIN, then the IRS wants to know that. So, let's say a state runs the plan and is going to report for the municipalities that participate in the plan. The State would be the DGE and should fill out this information, but the employer they are reporting on should go in the top. so, they should know if they are a DGE filing for other entities or not. You may not want to say anything. greenji, 9/16/2015

g6 You know that ADP HC is only filing one authoritative transmittal, right. The idea is that you don't have to fill out all of Form 1094-C unless it is the authoritative transmittal. greenji, 9/16/2015

33

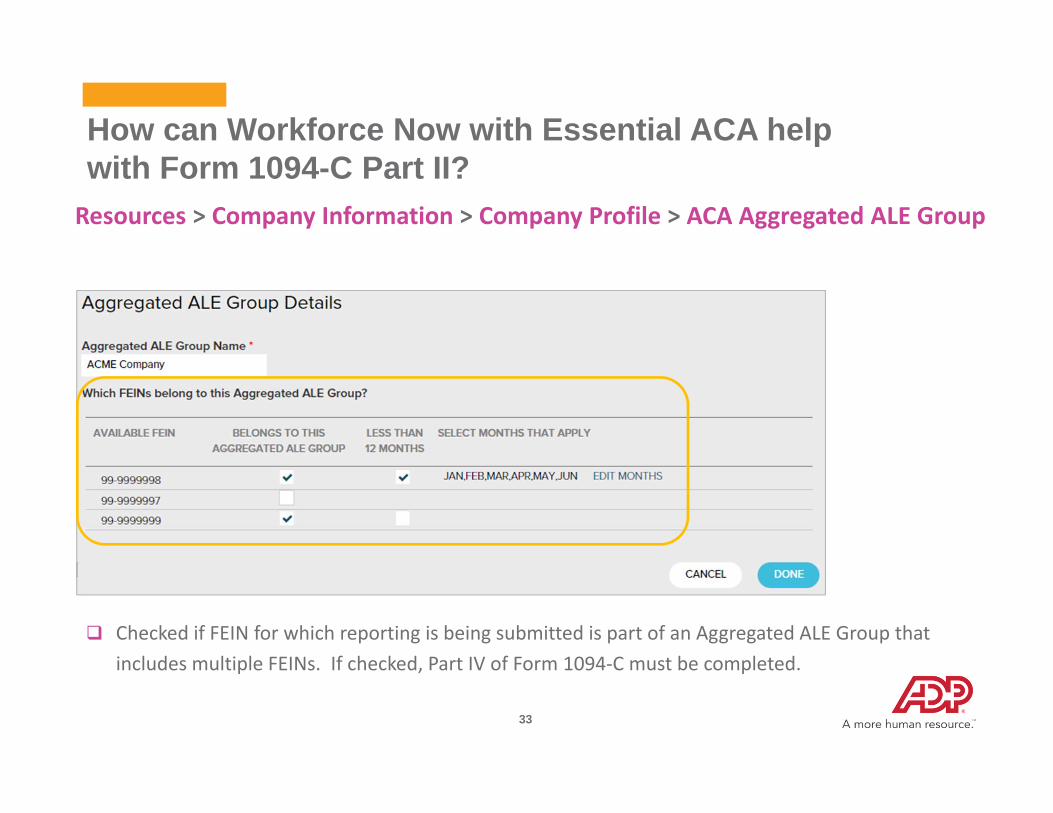

Resources > Company Information > Company Profile > ACA Aggregated ALE Group

Line 21: Is ALE Member a member of an Aggregated ALE Group?

Checked if FEIN for which reporting is being submitted is part of an Aggregated ALE Group that includes multiple FEINs. If checked, Part IV of Form 1094‐C must be completed.

How can Workforce Now with Essential ACA help with Form 1094-C Part II?

34

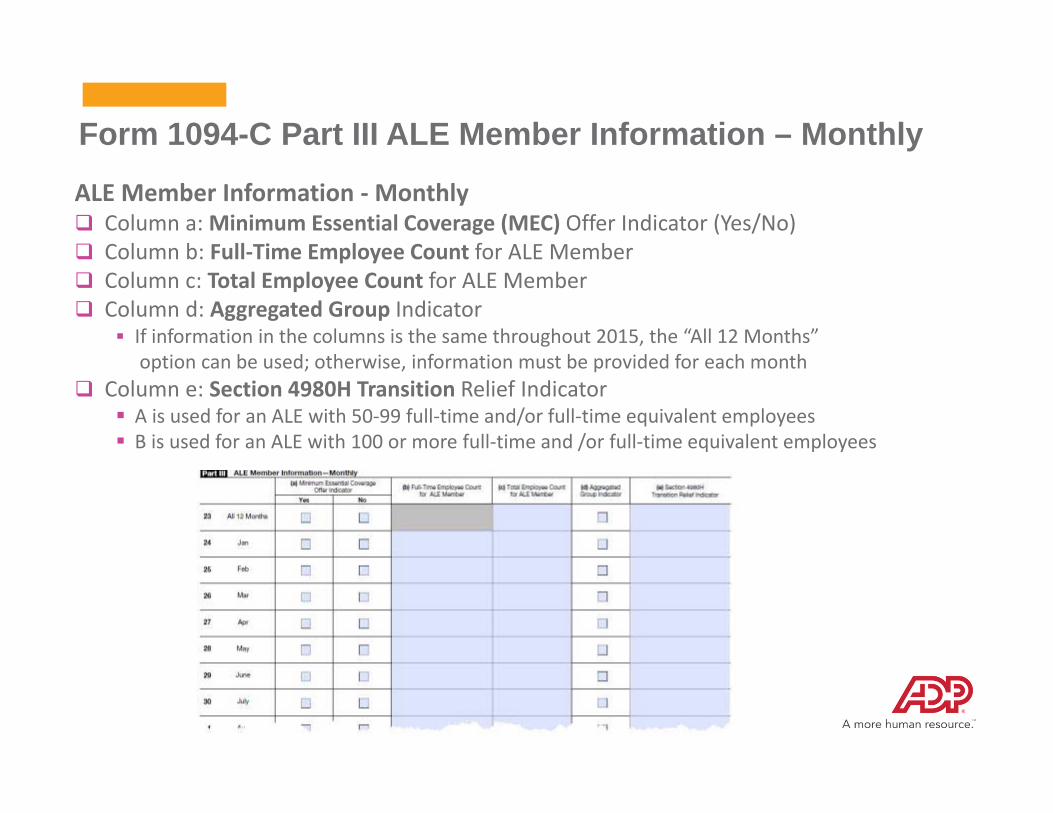

ALE Member Information ‐Monthly Column a: Minimum Essential Coverage (MEC) Offer Indicator (Yes/No) Column b: Full‐Time Employee Count for ALE Member Column c: Total Employee Count for ALE Member Column d: Aggregated Group Indicator

If information in the columns is the same throughout 2015, the “All 12 Months”option can be used; otherwise, information must be provided for each month

Column e: Section 4980H Transition Relief Indicator A is used for an ALE with 50‐99 full‐time and/or full‐time equivalent employees B is used for an ALE with 100 or more full‐time and /or full‐time equivalent employees

Form 1094-C Part III ALE Member Information – Monthly

35

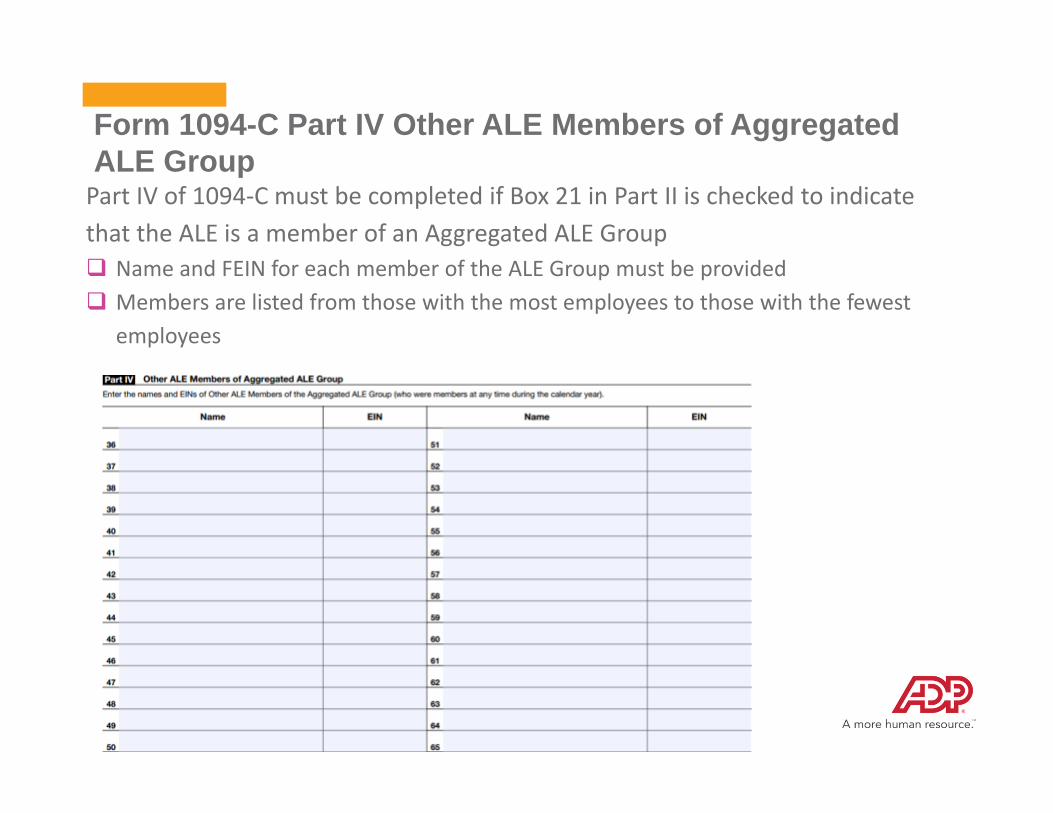

Part IV of 1094‐C must be completed if Box 21 in Part II is checked to indicate that the ALE is a member of an Aggregated ALE Group Name and FEIN for each member of the ALE Group must be provided Members are listed from those with the most employees to those with the fewest

employees

Form 1094-C Part IV Other ALE Members of Aggregated ALE Group

36

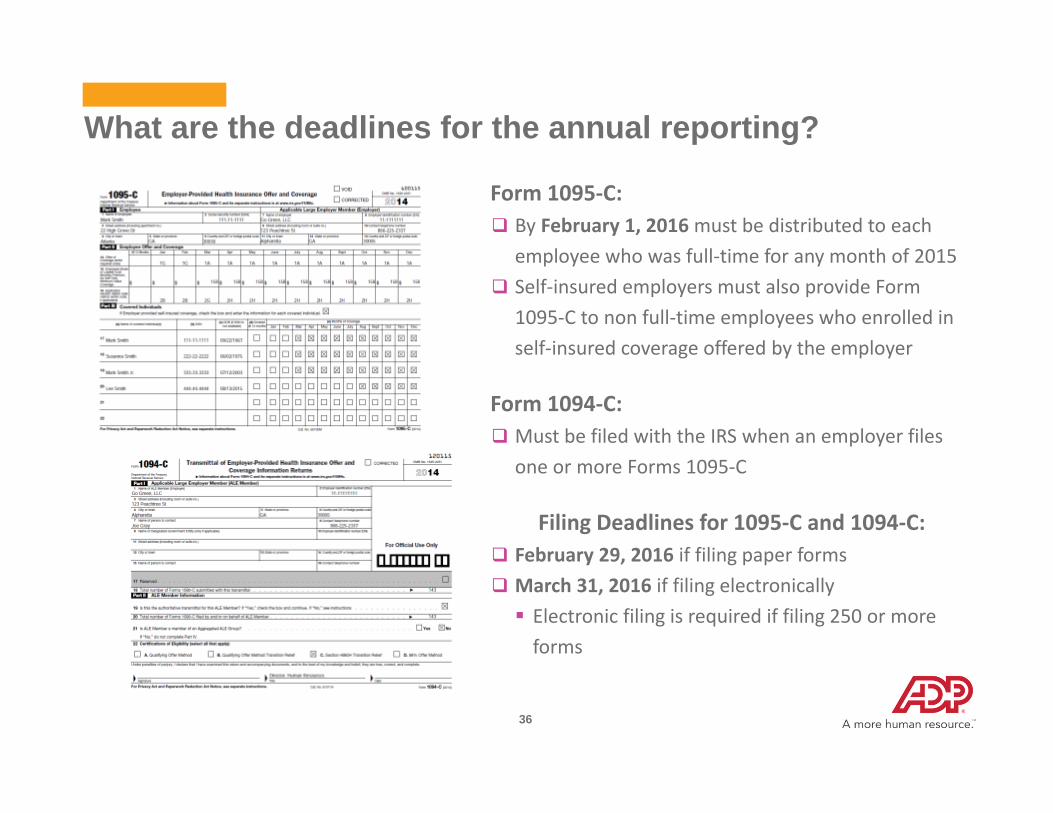

Form 1095‐C: By February 1, 2016must be distributed to each

employee who was full‐time for any month of 2015 Self‐insured employers must also provide Form

1095‐C to non full‐time employees who enrolled in self‐insured coverage offered by the employer

Form 1094‐C: Must be filed with the IRS when an employer files

one or more Forms 1095‐C

Filing Deadlines for 1095‐C and 1094‐C: February 29, 2016 if filing paper forms March 31, 2016 if filing electronically Electronic filing is required if filing 250 or more forms

What are the deadlines for the annual reporting?

37

Q&A

38

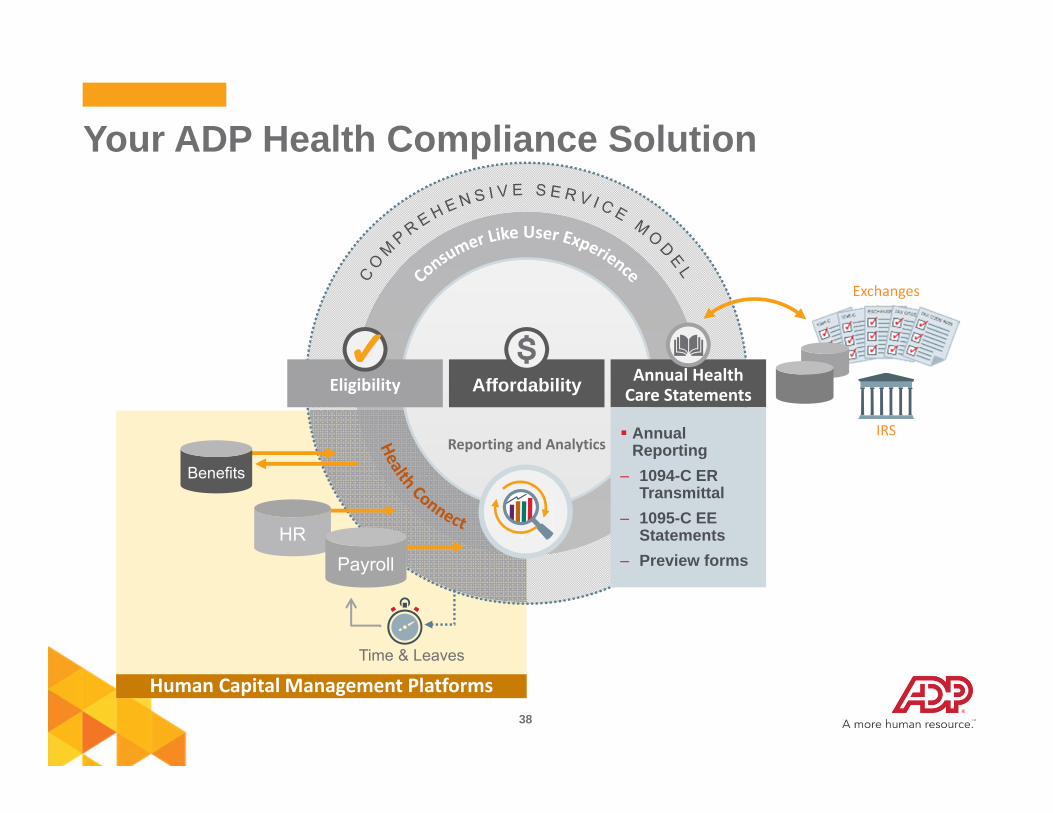

Your ADP Health Compliance Solution

Human Capital Management Platforms

IRS

Exchanges

Annual Health Care StatementsAffordabilityEligibility

Reporting and Analytics

Time & Leaves

Annual Reporting

‒ 1094-C ER Transmittal

‒ 1095-C EE Statements

‒ Preview forms

Benefits

HRPayroll

39

Will your company be managing Form 1095-C and 1094-C requirements using: Internal resources only Outsourcing this process A combination of both internal and outsourced resources Not sure at this time

Polling Question #2

39© Copyright 2015 ADP, LLC. Proprietary Information.

40

41

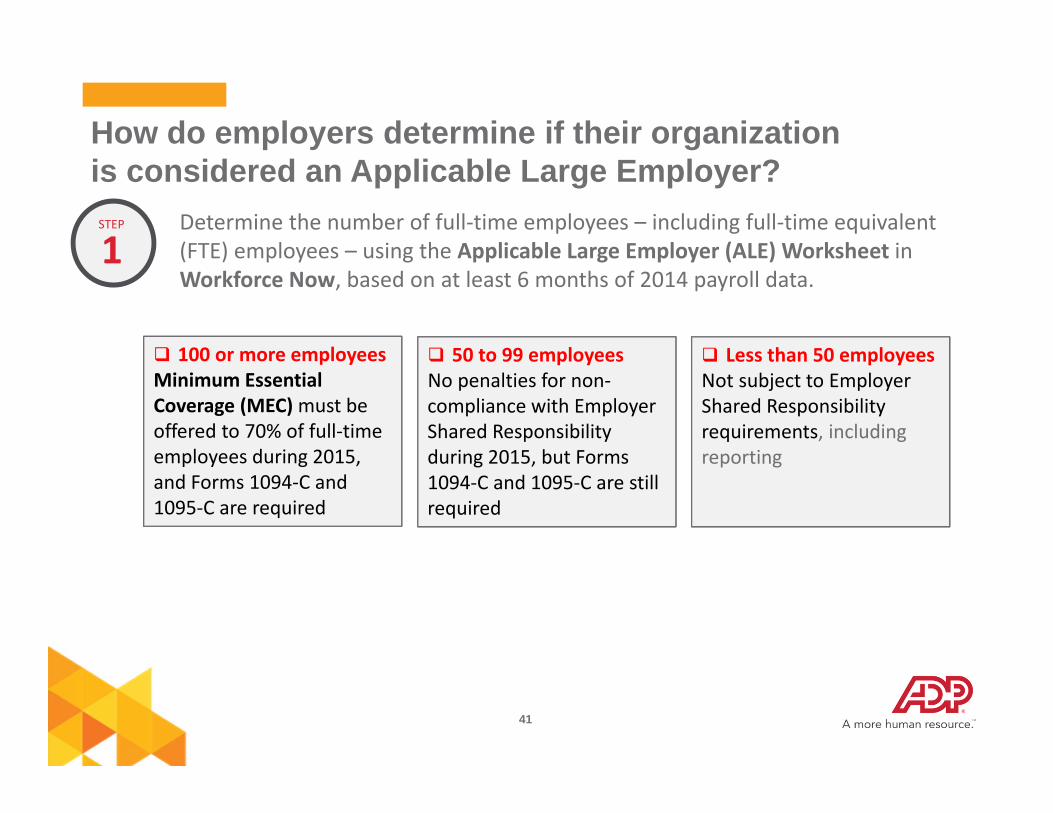

How do employers determine if their organization is considered an Applicable Large Employer?

1STEP Determine the number of full‐time employees – including full‐time equivalent

(FTE) employees – using the Applicable Large Employer (ALE) Worksheet in Workforce Now, based on at least 6 months of 2014 payroll data.

100 or more employeesMinimum Essential Coverage (MEC) must be offered to 70% of full‐time employees during 2015, and Forms 1094‐C and 1095‐C are required

50 to 99 employeesNo penalties for non‐compliance with Employer Shared Responsibility during 2015, but Forms 1094‐C and 1095‐C are still required

Less than 50 employeesNot subject to Employer Shared Responsibility requirements, including reporting

42

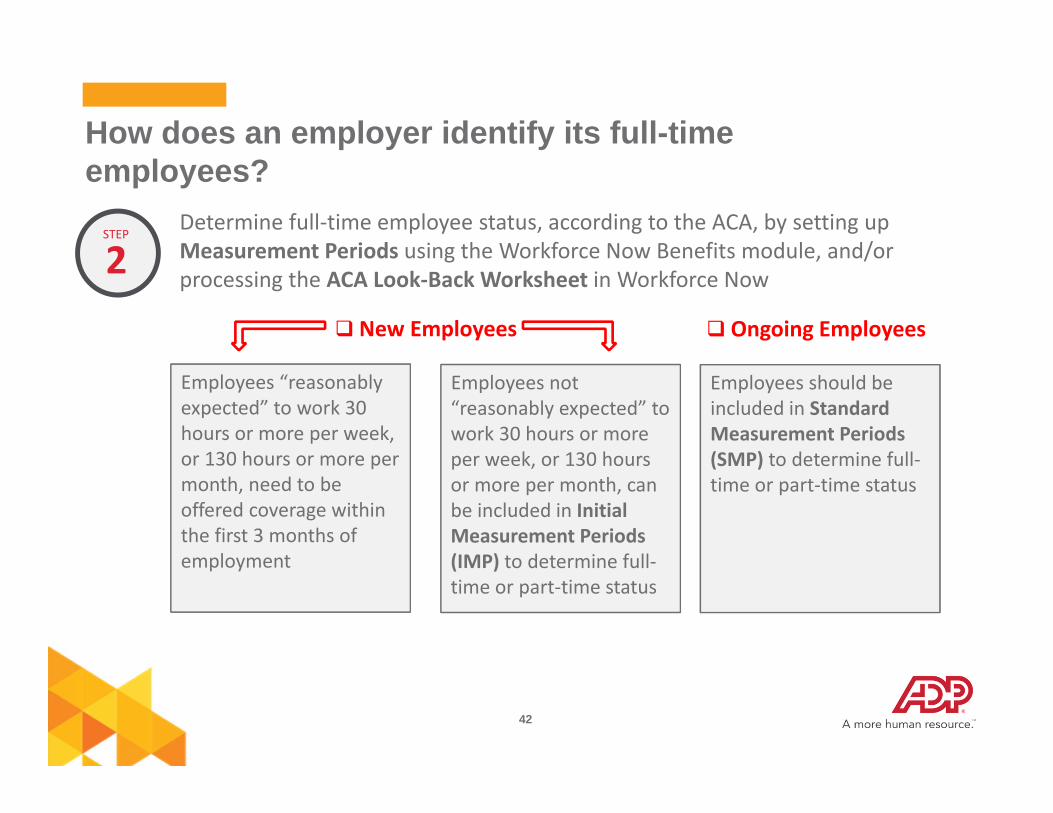

How does an employer identify its full-time employees?

2STEP

Determine full‐time employee status, according to the ACA, by setting up Measurement Periods using the Workforce Now Benefits module, and/or processing the ACA Look‐Back Worksheet in Workforce Now

Employees “reasonably expected” to work 30 hours or more per week, or 130 hours or more per month, need to be offered coverage within the first 3 months of employment

Employees not “reasonably expected” to work 30 hours or more per week, or 130 hours or more per month, can be included in Initial Measurement Periods (IMP) to determine full‐time or part‐time status

Employees should be included in Standard Measurement Periods (SMP) to determine full‐time or part‐time status

New Employees Ongoing Employees

43

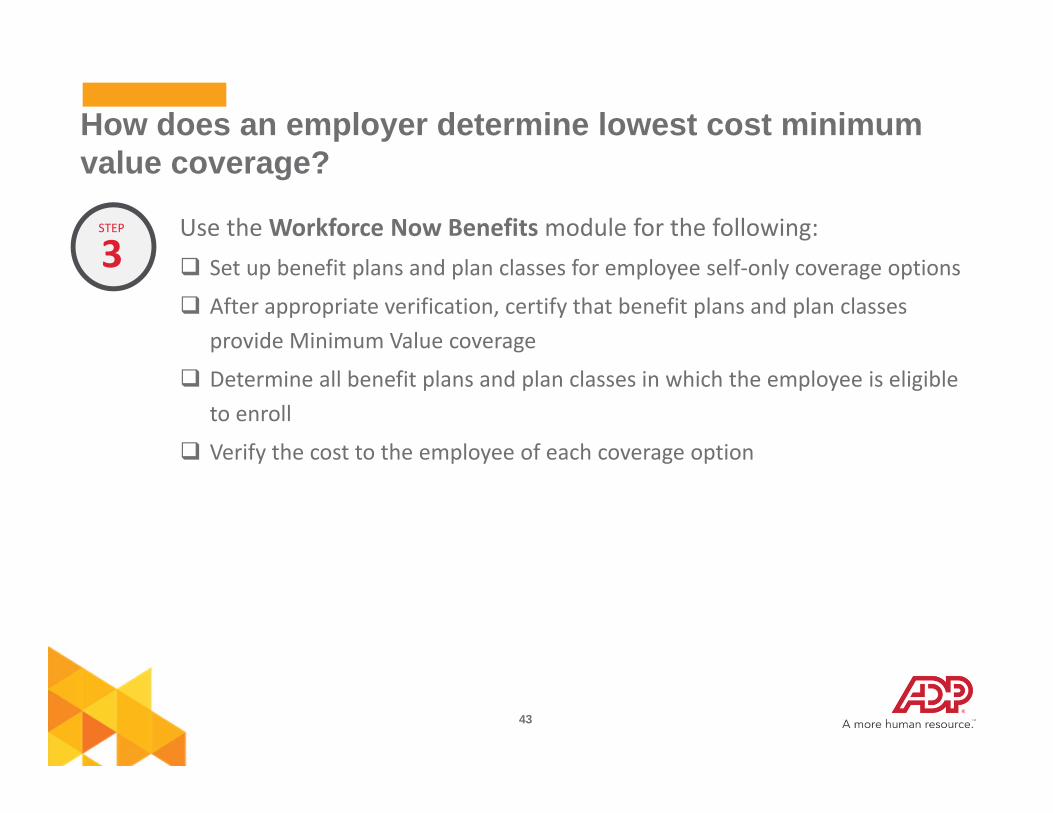

How does an employer determine lowest cost minimum value coverage?

3STEP Use the Workforce Now Benefitsmodule for the following:

Set up benefit plans and plan classes for employee self‐only coverage options

After appropriate verification, certify that benefit plans and plan classes provide Minimum Value coverage

Determine all benefit plans and plan classes in which the employee is eligible to enroll

Verify the cost to the employee of each coverage option

44

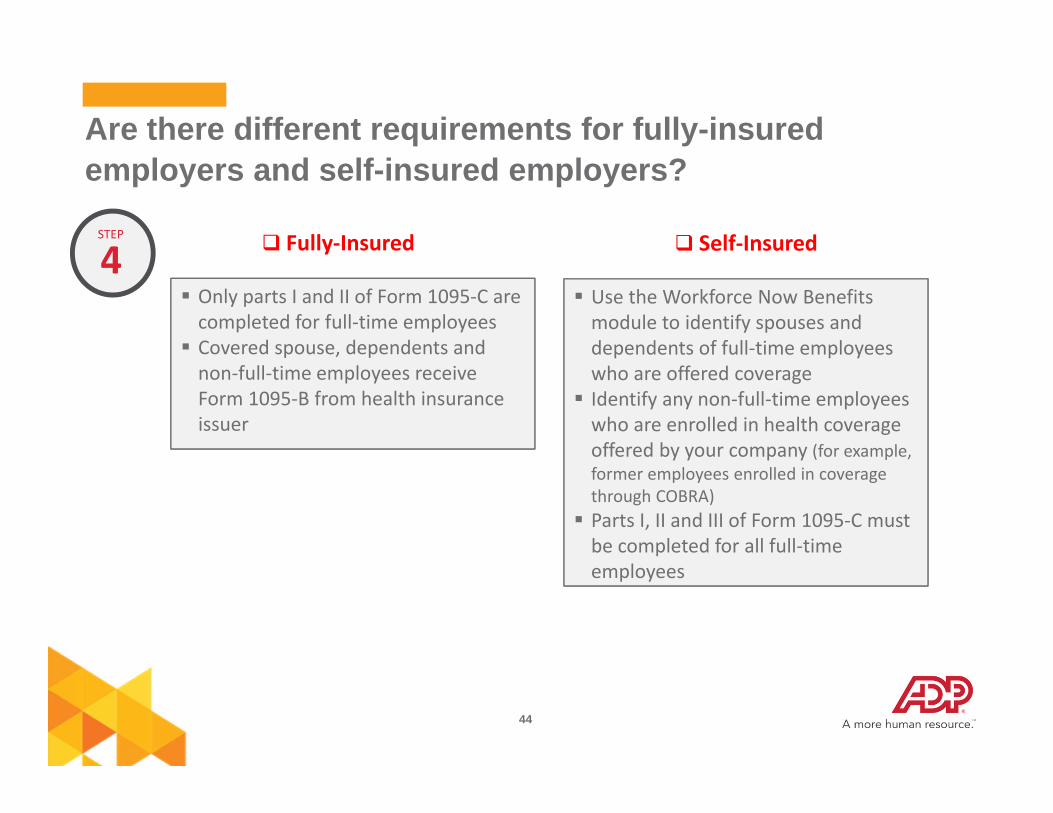

Are there different requirements for fully-insured employers and self-insured employers?

4STEP

Only parts I and II of Form 1095‐C are completed for full‐time employees Covered spouse, dependents and non‐full‐time employees receive Form 1095‐B from health insurance issuer

Use the Workforce Now Benefits module to identify spouses and dependents of full‐time employees who are offered coverage Identify any non‐full‐time employees who are enrolled in health coverage offered by your company (for example, former employees enrolled in coverage through COBRA) Parts I, II and III of Form 1095‐C must be completed for all full‐time employees

Fully‐Insured Self‐Insured

45

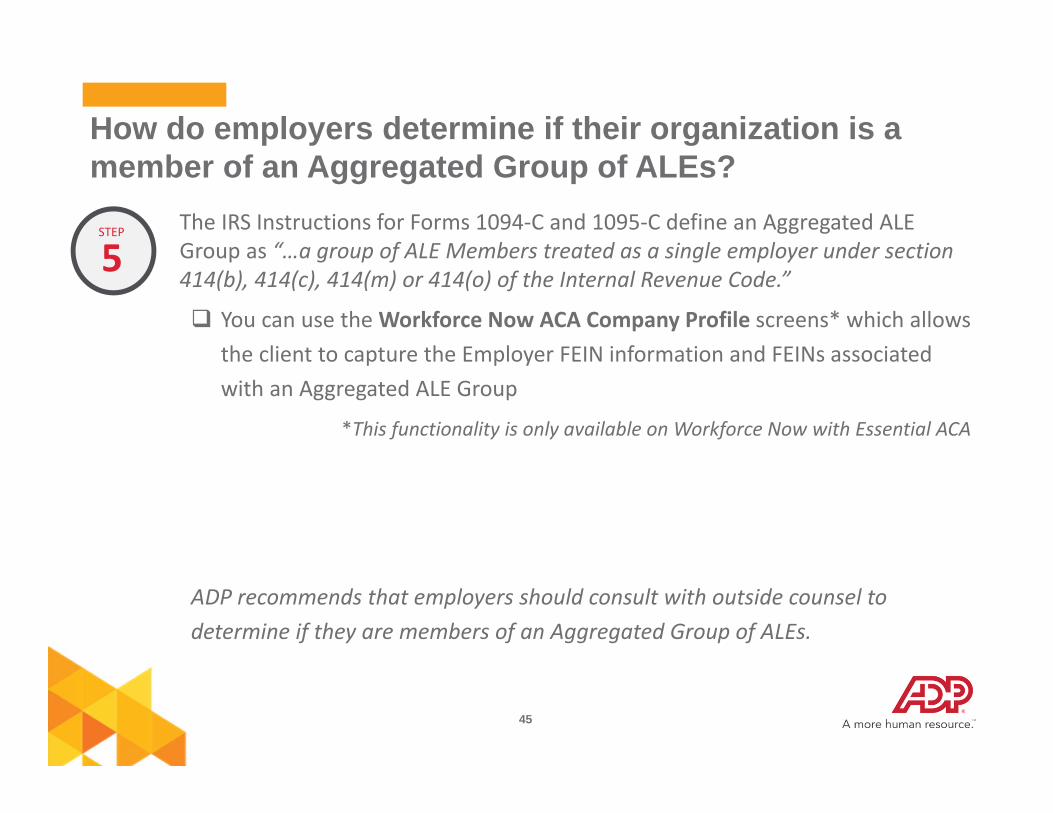

How do employers determine if their organization is a member of an Aggregated Group of ALEs?

5STEP The IRS Instructions for Forms 1094‐C and 1095‐C define an Aggregated ALE

Group as “…a group of ALE Members treated as a single employer under section 414(b), 414(c), 414(m) or 414(o) of the Internal Revenue Code.”

You can use the Workforce Now ACA Company Profile screens* which allows the client to capture the Employer FEIN information and FEINs associated with an Aggregated ALE Group

*This functionality is only available on Workforce Now with Essential ACA

ADP recommends that employers should consult with outside counsel to determine if they are members of an Aggregated Group of ALEs.

46

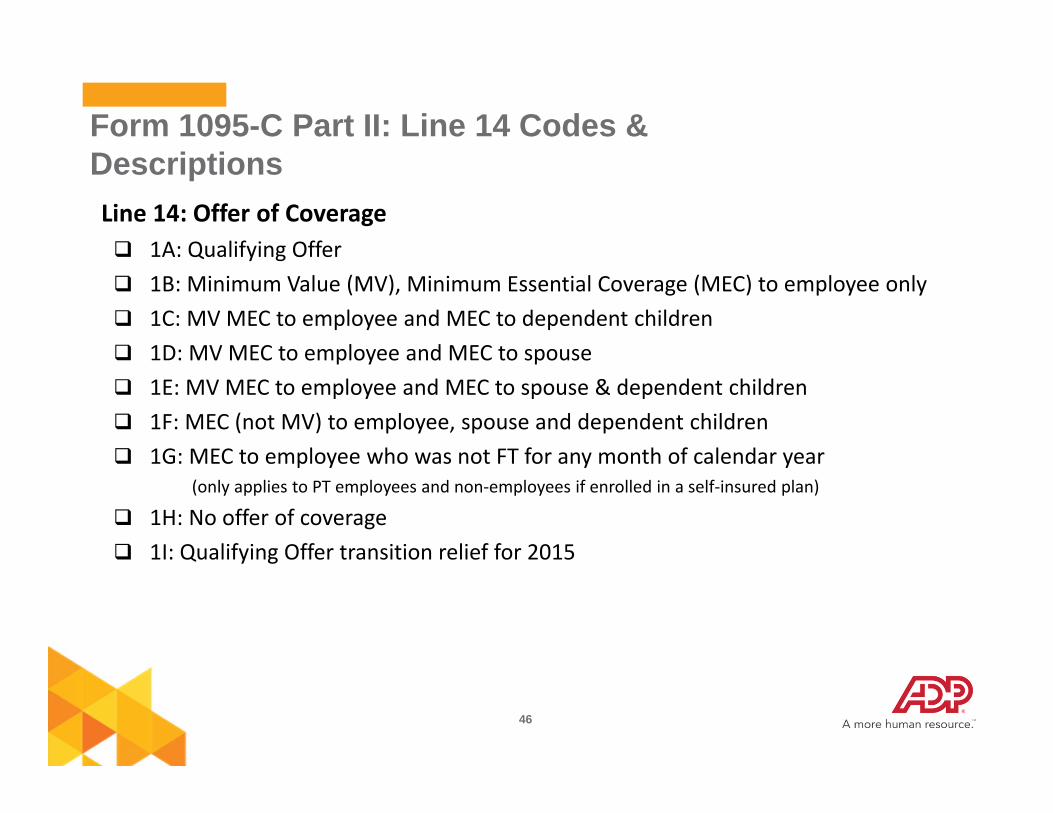

Form 1095-C Part II: Line 14 Codes & Descriptions Line 14: Offer of Coverage 1A: Qualifying Offer 1B: Minimum Value (MV), Minimum Essential Coverage (MEC) to employee only 1C: MV MEC to employee and MEC to dependent children 1D: MV MEC to employee and MEC to spouse 1E: MV MEC to employee and MEC to spouse & dependent children 1F: MEC (not MV) to employee, spouse and dependent children 1G: MEC to employee who was not FT for any month of calendar year

(only applies to PT employees and non‐employees if enrolled in a self‐insured plan)

1H: No offer of coverage 1I: Qualifying Offer transition relief for 2015

47

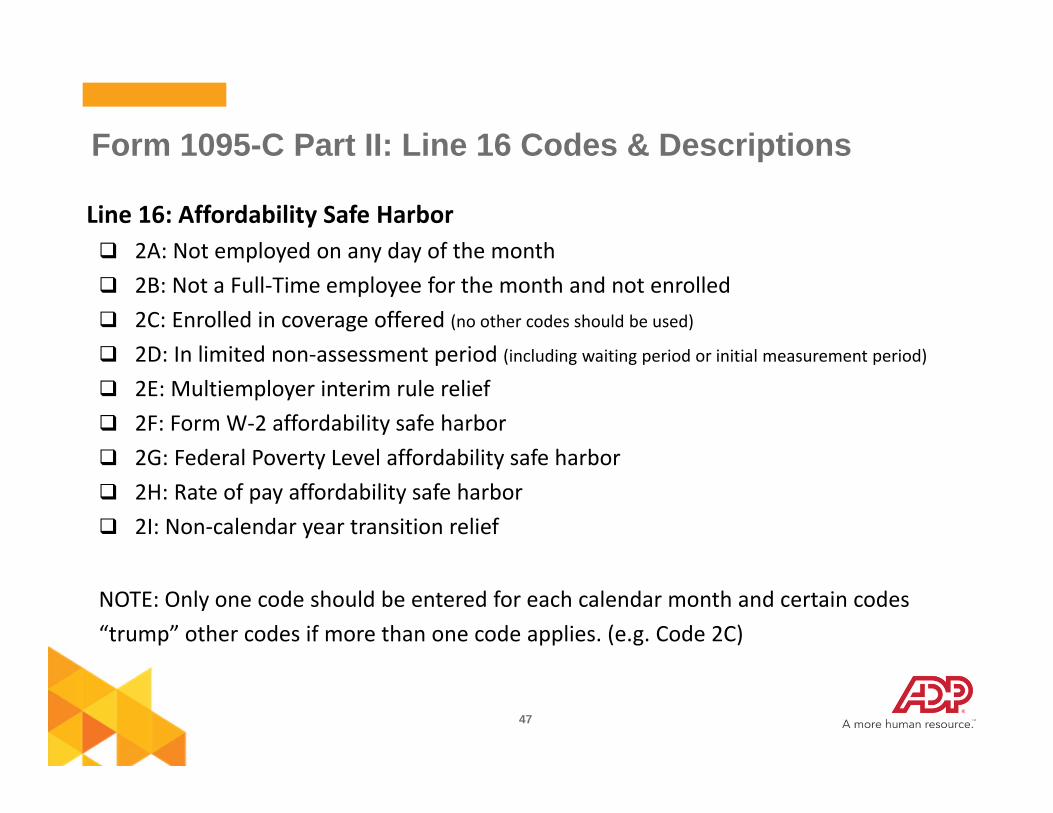

Form 1095-C Part II: Line 16 Codes & Descriptions

Line 16: Affordability Safe Harbor 2A: Not employed on any day of the month 2B: Not a Full‐Time employee for the month and not enrolled 2C: Enrolled in coverage offered (no other codes should be used) 2D: In limited non‐assessment period (including waiting period or initial measurement period)

2E: Multiemployer interim rule relief 2F: Form W‐2 affordability safe harbor 2G: Federal Poverty Level affordability safe harbor 2H: Rate of pay affordability safe harbor 2I: Non‐calendar year transition relief

NOTE: Only one code should be entered for each calendar month and certain codes “trump” other codes if more than one code applies. (e.g. Code 2C)

48

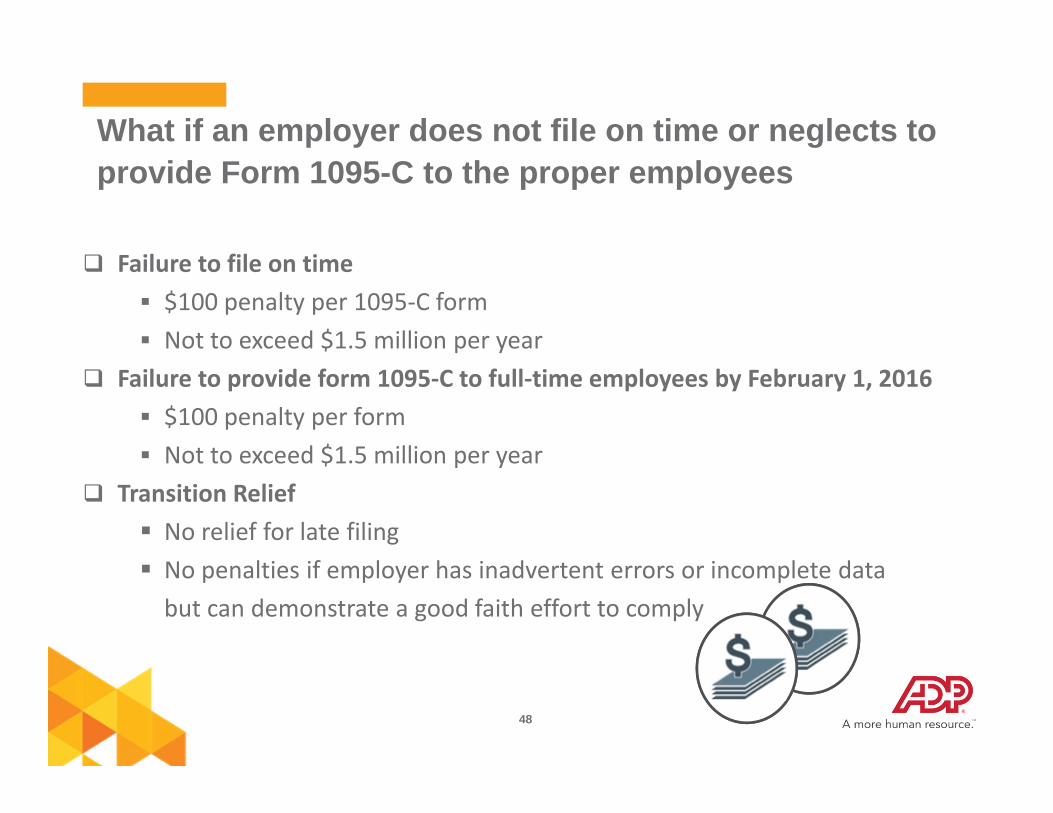

Failure to file on time $100 penalty per 1095‐C form Not to exceed $1.5 million per year

Failure to provide form 1095‐C to full‐time employees by February 1, 2016 $100 penalty per form Not to exceed $1.5 million per year

Transition Relief No relief for late filing No penalties if employer has inadvertent errors or incomplete databut can demonstrate a good faith effort to comply

What if an employer does not file on time or neglects to provide Form 1095-C to the proper employees?

Communications and Annual ReportingMary SchaferVice President, HCM Strategic CommunicationsADP, LLC

50

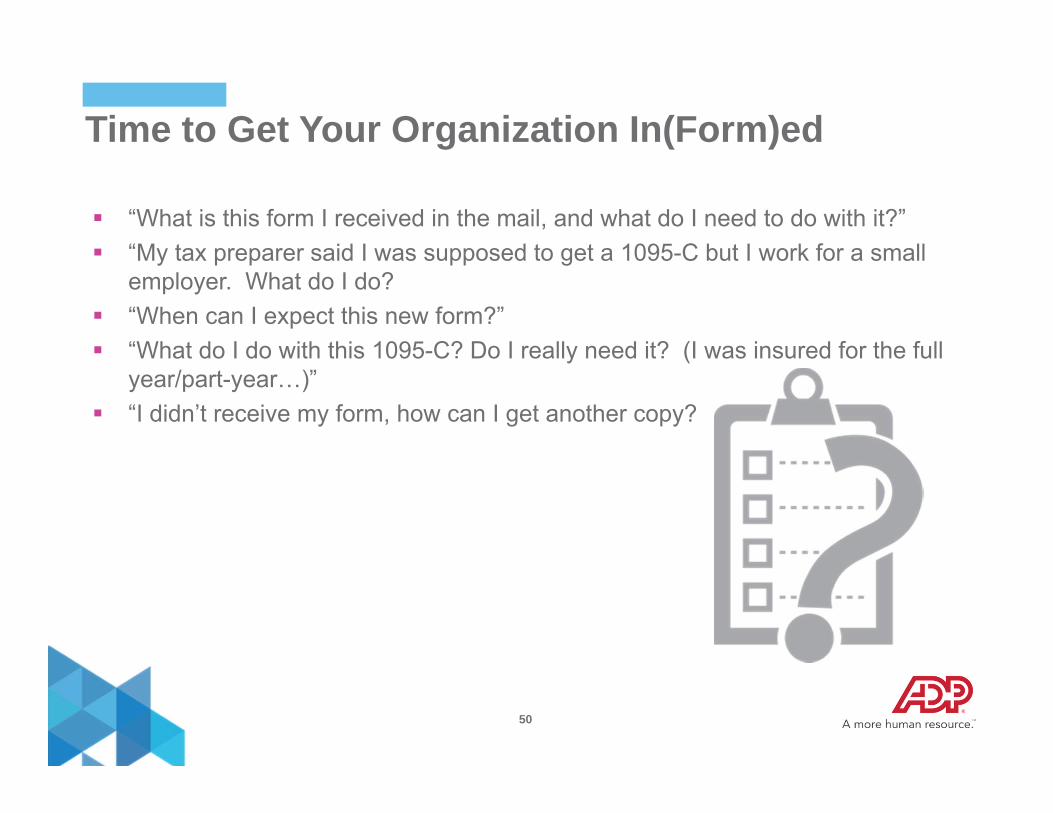

“What is this form I received in the mail, and what do I need to do with it?” “My tax preparer said I was supposed to get a 1095-C but I work for a small

employer. What do I do? “When can I expect this new form?” “What do I do with this 1095-C? Do I really need it? (I was insured for the full

year/part-year…)” “I didn’t receive my form, how can I get another copy?

Time to Get Your Organization In(Form)ed

51

• How prepared do you feel your company is to issue Form 1095-C to your employees by February 1, 2016?

Extremely Very Somewhat Not very Not at all

Polling Question #3

52

“No strategy” is NOT a strategy. You need a plan because:

Your full-time employees will receive Form 1095-C for the first time in January 2016

They need to know what it is, what it means and what to do with it

What Are You Communicating?

53

Audience: Who Do You Need to Reach?

Target Audiences

COBRA Beneficiaries

Retirees

New Hires /Full Time

Former Full Time

Employees

Any Covered Employee*

Full Time Employees

*varies depending on whether the plan is insured or self insured

54

Reduce confusion

Decrease calls and inquires to you and your team

Reduce requests for duplicate forms

Provide your employees with information they need to file their 2015 taxes

Provide an opportunity to paint the big picture about ACA and your organization’s strategy

Proactive Communications Can Help

55

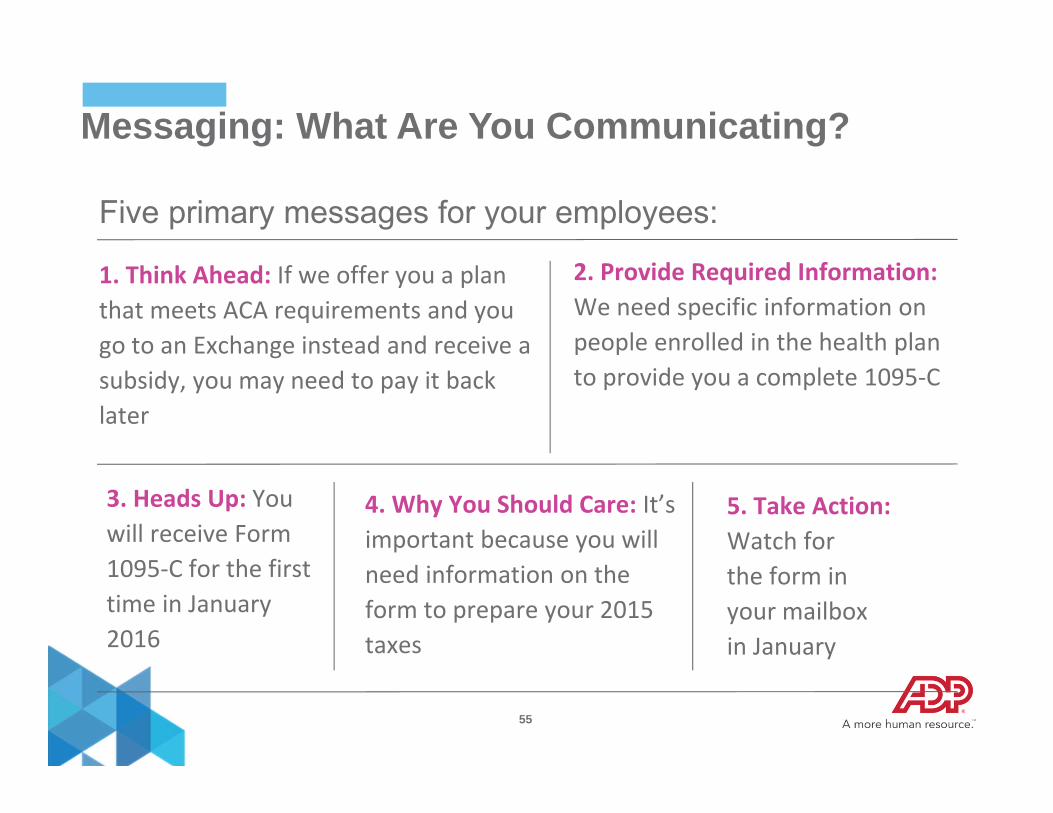

Five primary messages for your employees:

Messaging: What Are You Communicating?

3. Heads Up: You will receive Form 1095‐C for the first time in January 2016

1. Think Ahead: If we offer you a plan that meets ACA requirements and you go to an Exchange instead and receive a subsidy, you may need to pay it back later

2. Provide Required Information: We need specific information on people enrolled in the health plan to provide you a complete 1095‐C

5. Take Action: Watch for the form in your mailbox in January

4. Why You Should Care: It’s important because you will need information on the form to prepare your 2015 taxes

56

Home Mailer (i.e. postcard) Email Company Intranet Posters Manager Meetings Videos & Webinars Newsletter FAQs

Use a Variety of Communications Vehicles

57

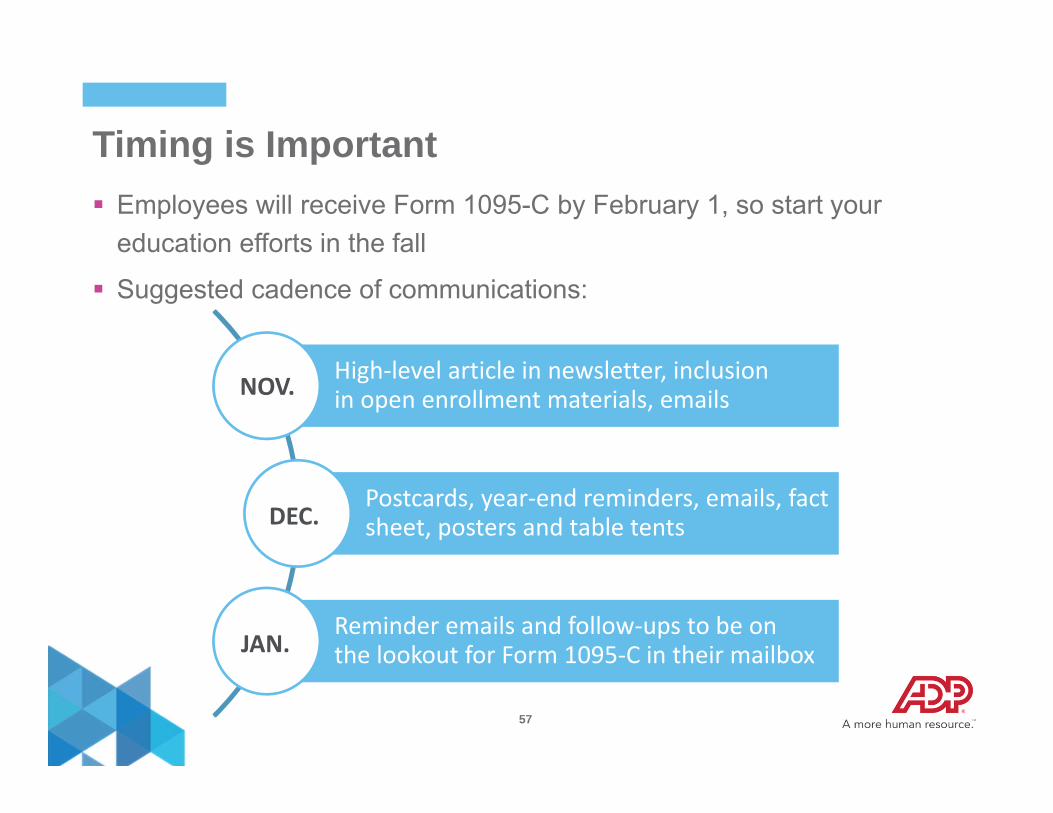

Employees will receive Form 1095-C by February 1, so start your education efforts in the fall

Suggested cadence of communications:

Timing is Important

High‐level article in newsletter, inclusion in open enrollment materials, emails

Postcards, year‐end reminders, emails, fact sheet, posters and table tents

Reminder emails and follow‐ups to be on the lookout for Form 1095‐C in their mailbox

NOV.

DEC.

JAN.

58

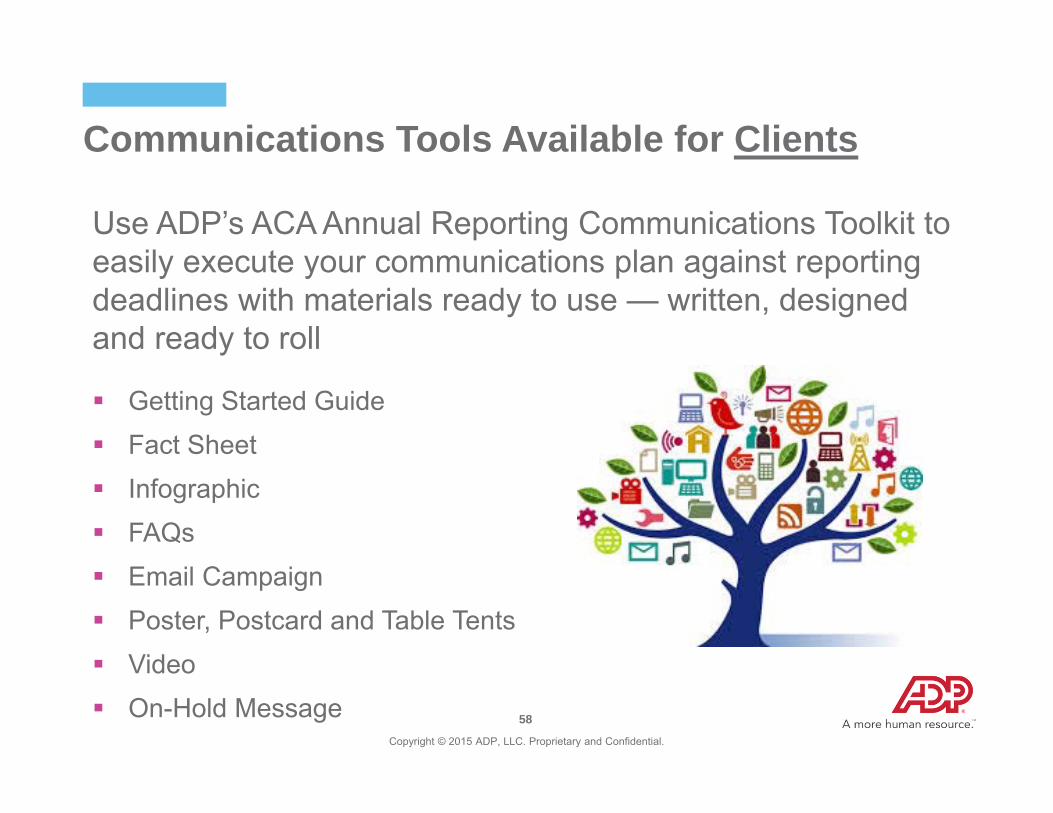

Communications Tools Available for Clients

Use ADP’s ACA Annual Reporting Communications Toolkit to easily execute your communications plan against reporting deadlines with materials ready to use — written, designed and ready to roll

Getting Started Guide Fact Sheet Infographic FAQs Email Campaign Poster, Postcard and Table Tents Video On-Hold Message

Copyright © 2015 ADP, LLC. Proprietary and Confidential.

59

1. Be clear and concise

2. Understand your employees

3. Use multiple channels

4. Provide context

5. Make it personal

Takeaways: Communications Best Practices

60

Takeaways: Communications Best Practices

61

Thank YouThis session has been certified for 1 HRCI credit.

To subscribe to ADP’s Eye on Washington regulatory email alerts visit: www.adp.com/eyeonwashington

Please visit www.adp.com/acafaqs for a list of ACA Frequently Asked Questions or www.adp.com/health-care-reform for additional ACA insights.

Before taking any actions on the information contained in this presentation, employers and plan sponsors should review this material with internal This material is subject to change and is provided for informational purposes only and nothing contained herein should be taken as legal opinion, legal advice, or a comprehensive compliance review. The ADP Logo and ADP are registered trademarks of ADP, LLC. All other trademarks and service marks are the property of their respective owners. Copyright © 2015 ADP, LLC. ALL RIGHTS RESERVED.

63

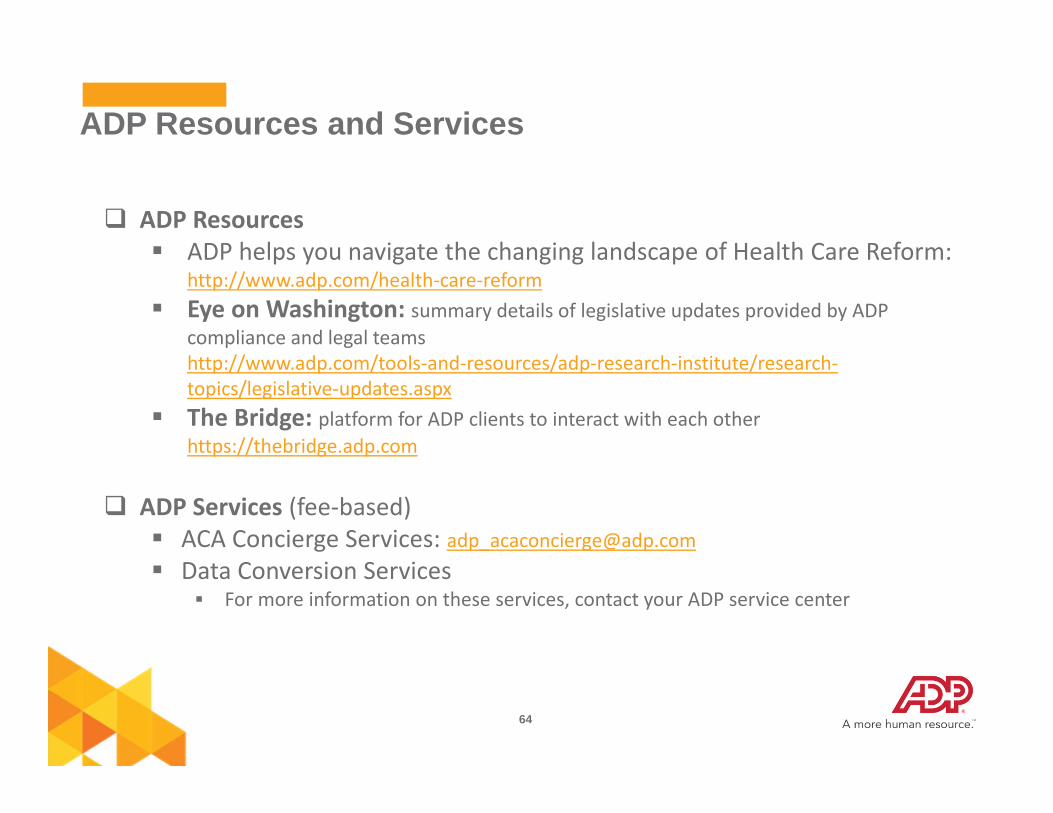

Appendix

64

ADP Resources ADP helps you navigate the changing landscape of Health Care Reform:

http://www.adp.com/health‐care‐reform Eye on Washington: summary details of legislative updates provided by ADP

compliance and legal teamshttp://www.adp.com/tools‐and‐resources/adp‐research‐institute/research‐topics/legislative‐updates.aspx

The Bridge: platform for ADP clients to interact with each otherhttps://thebridge.adp.com

ADP Services (fee‐based) ACA Concierge Services: [email protected] Data Conversion Services

For more information on these services, contact your ADP service center

ADP Resources and Services

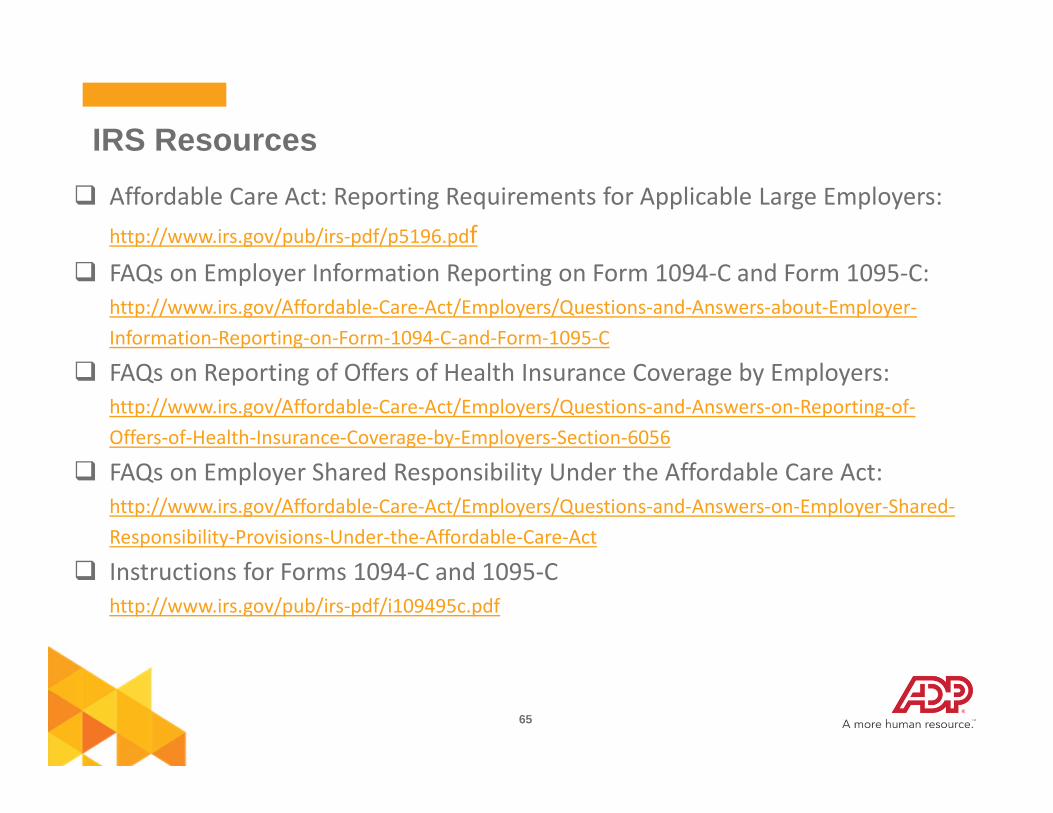

65

IRS Resources Affordable Care Act: Reporting Requirements for Applicable Large Employers:

http://www.irs.gov/pub/irs‐pdf/p5196.pdf FAQs on Employer Information Reporting on Form 1094‐C and Form 1095‐C:

http://www.irs.gov/Affordable‐Care‐Act/Employers/Questions‐and‐Answers‐about‐Employer‐Information‐Reporting‐on‐Form‐1094‐C‐and‐Form‐1095‐C

FAQs on Reporting of Offers of Health Insurance Coverage by Employers: http://www.irs.gov/Affordable‐Care‐Act/Employers/Questions‐and‐Answers‐on‐Reporting‐of‐Offers‐of‐Health‐Insurance‐Coverage‐by‐Employers‐Section‐6056

FAQs on Employer Shared Responsibility Under the Affordable Care Act: http://www.irs.gov/Affordable‐Care‐Act/Employers/Questions‐and‐Answers‐on‐Employer‐Shared‐Responsibility‐Provisions‐Under‐the‐Affordable‐Care‐Act

Instructions for Forms 1094‐C and 1095‐C http://www.irs.gov/pub/irs‐pdf/i109495c.pdf

Related Documents

![ACA Annual Reporting [Infographic]](https://static.cupdf.com/doc/110x72/55cb9a98bb61ebdd728b4587/aca-annual-reporting-infographic.jpg)