Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Abstract

This report provides information on consolidating critical balance sheet components during cooperative mergers. It discusses the implications of combiningassets and liabilities and provides information and examples on various meth-ods of consolidating member equities. Several case studies of cooperatives thathave merged are included. They provide actual examples on how equities werecombined during mergers, consolidations, and acquisitions.

Key Words: Merger, plan, equity, assets, liabilities

Consolidation of Balance Sheet ComponentsDuring Cooperative Mergers

James J. WadsworthDavid S. ChesnickAgricultural EconomistsU.S. Department of AgricultureRural Business and Cooperative Development Service

RBCDS Research Report 139

March 1995

Cooperatives or cooperative leaders studying merging or in the midst of merg-ing are likely to confront some difficult issues when planning to consolidatemajor balance sheet components-assets, liabilities, and equity. This reportdescribes the implications and presents information and examples on methodsfor consolidating these important financial elements.

This information was obtained from: (1) literature by noted authors on coopera-tive mergers; (2) intra-agency development of examples and relevant informa-tion; and (3) case studies of several fanner cooperatives recently involved inmergers.

This report is intended to aid cooperative leaders and others interested in (a)better understanding financial aspects involved in mergers, and (b) developinga plan to combine major balance sheet components for the merger, consolida-tion, or acquisition being considered.

The authors thank the six cooperatives that participated as case-study subjects.Their contributions were essential for this report.

For brevity, the term “merger” is used throughout the report rather than specify-ing merger, consolidation, and acquisition in every instance.

The portions of this report that refer to the tax implications of mergers do notrepresent official policy of the U.S. Department of Agriculture, the InternalRevenue Service, the U.S. Department of the Treasury, or any other govem-ment agency. Hence, this report is not providing tax recommendations.Cooperatives studying or interested in tax issues of mergers should seek professional/legal tax advice.

Contents

Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

Consolidating Balance Sheet Components . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Assets and Liabilities ....................................................................................... 2

Assets ....................................................................................................... 2

Liabilities ................................................................................................... 4

Member Equities ............................................................................................... 4

Allocated Equity ......................................................................................... 5

Unallocated Equity..................................................................................... 5

Equity Redemption Plans ......................................................................... 6

Alternatives for Consolidating Equity ................................................................. 6

Examples-Hatfield, et al. Report ............................................................ 6

Immediate Payoff .............................................................................. 6

Delayed Payoff .................................................................................. 6

Prorate Old Equity ............................................................................ 7

Reassignment to Unallocated Reserves .......................................... 8

Equity Reevaluation .......................................................................... 8

Base Capital Plan ........................................................................... 10

Handling Inactive Patrons ............................................................... 10

Other Alternatives ................................................................................... 11

Transfer Stock ................................................................................. 11

Exchange Stock ............................................................................. 11

Group Old Equity ............................................................................. 11

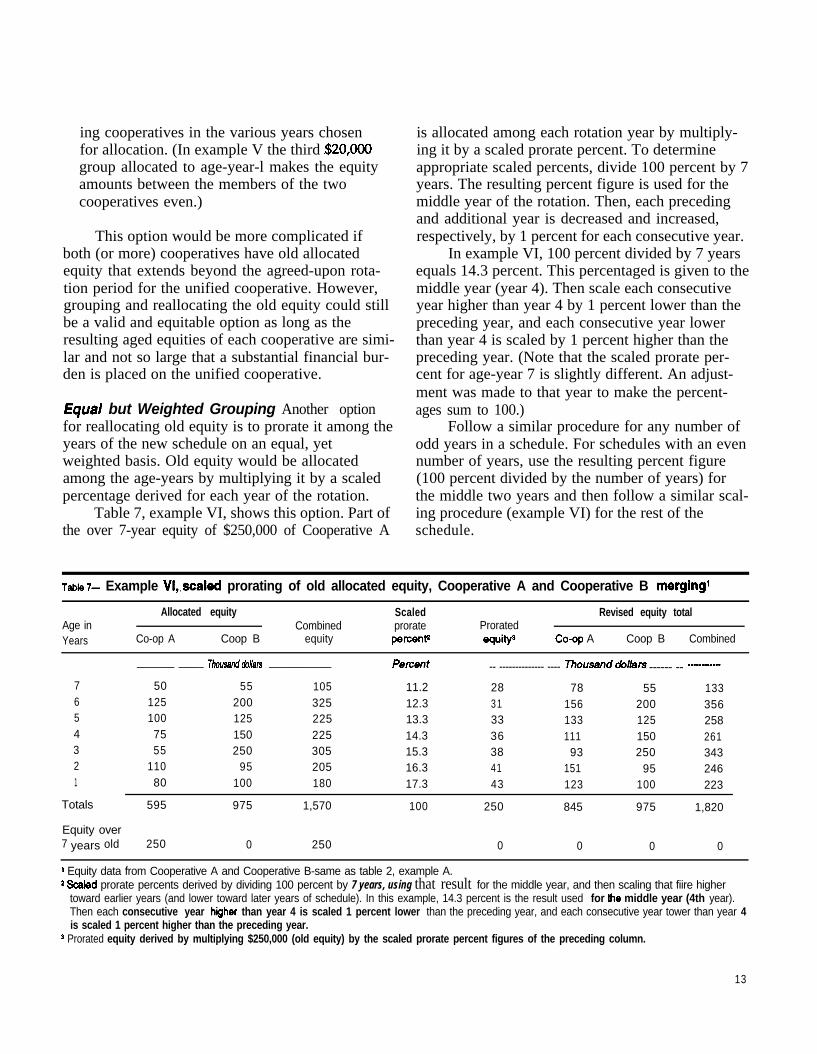

Equal but Weighted Grouping ......................................................... 13

Percentage-of-All-Combined Equities ............................................ 14

Acquisitions ............................................................................................ 15

Summary ................................................................................................ 16

ii

Contents

Cooperative Examples of Combining Equity .................................................. 16

Merger-Different Size and Strength ..................................................... 16

Consolidation-Different Size and Strength ........................................... 17

Acquisition 1 -Different Size and Strength ............................................ 17

Acquisition 2Cimilar Size and Strength ............................................... 17

Recent Case Study Examples ................................................................ 18

Case Study I-Cooperatives 0 and P ............................................ 18

Case Study II-Cooperatives Q and R ........................................... 20

Case Study III-Cooperatives S and T .......................................... 20

Case Study IV-Cooperatives U and V .......................................... 22

Case Study V-Cooperatives W and X .......................................... 22

Case Study VI-Cooperatives Y and Z .......................................... 23

Summary ............................................................................................... 23

Other Financial Issues ................................................................................... 24

Evaluating Equity ................................................................................... 24

Tax Considerations ................................................................................ 24

Summary and Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

References . . ..*.............*.................................. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Appendix Adlossary of Terms/Concepts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

Appendix B-Case Study Survey Questions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Highlights

Cooperative leaders pursuing merger will benefit by developing and following anorganized plan to carry them through the process. Part of this plan entails thecareful study of the characteristics and structure of the participating coopera-tives’ assets, liabilities, and equity. Major questions need to be answered per-taining to those structures:

l What are the assets, what will be needed, and what are they worth?

l How should assets be evaluated (book or appraised value)?

l How do debt-to-asset ratios compare?

l Must assets be sold to retire debt?

l Are liabilities at similar levels and structured the same?

l What types of equities do the cooperatives have?

l What are the redemption plans?

l Are the cooperatives current in redeeming equity?

l What alternatives are available for consolidating member equities?

l What redemption plan will best suit the unified cooperative?

These and other questions should be addressed in the merger plan. Doing sowill require a thorough examination of each cooperative’s balance sheet andfinancial characteristics. Every merger is different depending on the attributes ofeach cooperative, what precipitated the merger, and what each cooperative hasto offer a unified organization.

Handling member equity is, perhaps, the most difficult financial issue in a merg-er. Member investment needs to be respected and protected. Alternatives forcombining equity must take that into consideration.

Not all alternatives for combining equity provide complete member equality.Develop alternatives and assess attributes of each to narrow the field to themost suitable alternative given the conditions and the overall situation of the par-ticipating cooperatives.

This report contains 21 alternatives or examples for combining equity. Elevenare described in general. Ten are examples from cooperatives that participated

iv

in a merger. Cooperatives considering merger may use them to help develop afield of alternatives.

Cooperatives usually don’t face the same problems in acquisitions as they do inmergers. While member financial interests and their patronage still must berespected, the acquiring cooperative usually dictates most actions taken to com-bine assets, liabilities, and member equity, especially if the cooperative beingacquired is financially weak. In any event, acquisitions are gaining in popularitygiven the relative ease by which the applicable transactions can be completed.

Cooperatives considering merger must work to let members know that theirinterests are being represented and protected and that their financial stake in theunified cooperative is important.

The new or unified cooperative should emerge with an equity capitalization andredemption program that closely adheres to the “user-owned cooperative princi-ple-the equity structure should reflect current patterns of usership. Cooperativeleaders should adhere to that precept in developing the merger plan.

V

Consolidation of Balance Sheet ComponentsDuring Cooperative Mergers

James J. WadsworthDavid S. ChesnickAgricultural Economists

B alance sheet characteristics of cooperativesinvolved in a merger are rarely identical.

Problems often arise when organizations with differ-ent depreciable assets, liabilities, types of equity, andequity redemption programs attempt to combinetheir assets and equities into a single organization.

Asset evaluation, liability realignment, andequity transfer during cooperative mergers are deli-cate issues and must be handled in an equitable ormutually agreeable manner.

In a merger, one or more business organiza-tions absorb another firm. The survivor maintainsits identity. Many of its organizational features areoperated on an expanded basis, given its increasedsize and capacities. Consolidation combines two ormore business organizations into a new organiza-tion. In an acquisition, the assets of one cooperativeare purchased by another.

This report examines and clarifies the alterna-tive methods for evaluating and consolidating criti-cal balance sheet components during mergers, con-solidations, and acquisitions. The report providesreferences for cooperatives involved in planningand negotiating a merger, and/or for those interest-ed in the types of financial structural changes thatresult from the consolidation of cooperative balancesheets during mergers.

Mergers result in expanded assets, realignedliabilities, and transferred and consolidated memberequities. Cooperative members involved in mergershave a personal stake in the methods used to evalu-ate and consolidate these critical financial elements.

This report has seven sections. The first is ageneral plan for consolidating major balance sheetcomponents during a cooperative merger. The sec-ond describes the appraisal of cooperative assetsand handling liabilities, while the third analyzesand describes alternatives for consolidating mem-ber equities-some summarized from another liter-ature source and some developed.

The fourth section provides some generalalternatives for consolidating equity, examples bor-rowed from other literature and other developedexamples. The fifth section includes case studies ofcooperatives that have merged, some originatingfrom a past study and some from recent case stud-ies. Section six discusses some financial issues per-taining to merger. Section seven summarizes thereport and discusses implications of the findings.

CONSOLIDATING BALANCE SHEETCOMPONENTS

Cooperative leaders contemplating or activelypursuing merger will benefit by developing andfollowing an organized plan that will carry the par-ticipants through the merger process. A well-developed plan for merger indicates steps to followand the components or elements in each step.1

Part of the plan should include strategies forconsolidating the balance sheet components of theparticipating cooperatives. A joint merger or studycommittee evaluates all implications of consolidat-ing the participants’ balance sheets and providesrecommendations to the boards of directors aboutthe most suitable strategies for completing the task.

Initial phases of those studies often involveoutside consultants. Later phases of merger propos-als usually involve a range of complex issues thatrequire the outside assistance from legal counsel,accountants, and occasionally professional media-tors.

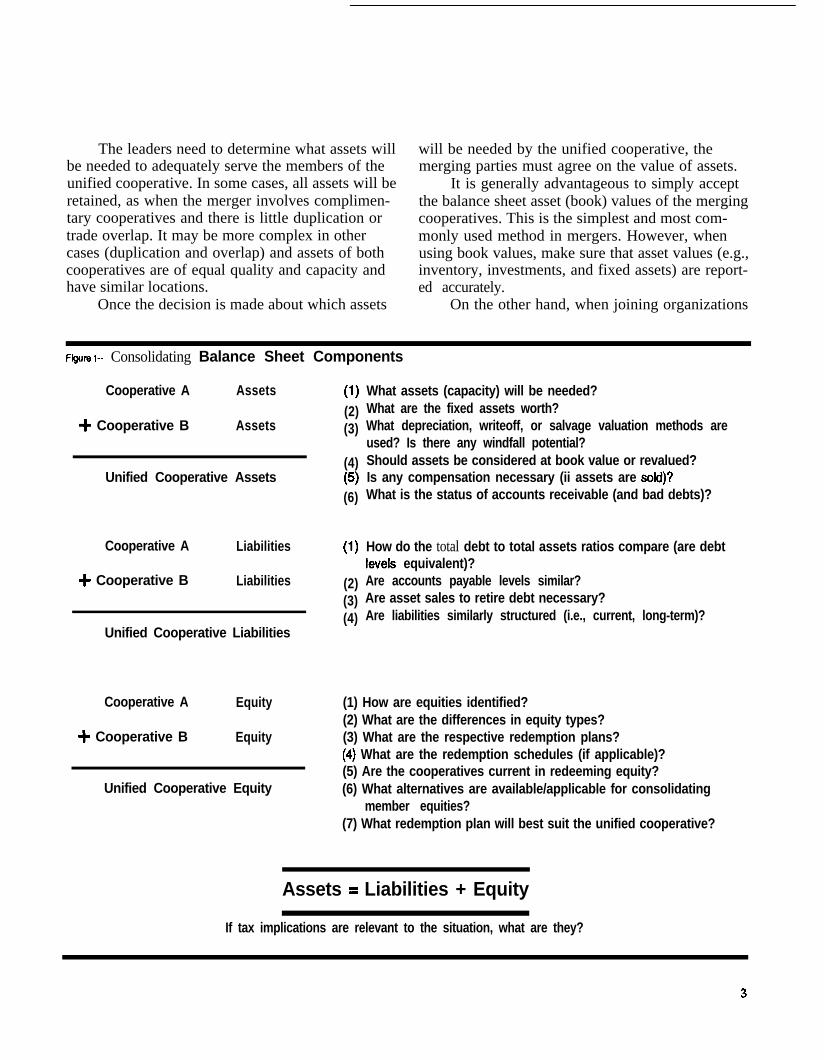

This part entails careful study of the character-istics and structure of participants’ assets, liabili-ties, and equity (figure 1). The figure portrays the

1 See Swanson (ACS Research Report 43-MergingCooperatives: Planning, Negotiation, and Implementation)for general information, guidelines, and step-by-step pro-cedures for merging cooperatives.

consolidation of assets, liabilities, and equities oftwo cooperatives into a single organization.

The variations and implications of consolidat-ing these major financial elements can be compli-cated. To limit disruption to the merger process,financial consolidations should be handled careful-ly. In proceeding with merging these components, anumber of questions, such as those included in fig-ure 1, need to be answered in their regard.

Successfully answering these and other moredetailed questions requires a thorough understand-ing of the characteristics of each merger partici-pant’s financial statements. Thus, financial state-ments must be carefully examined by the mergercommittee.

The final plan or strategies for consolidatingthe financial elements may vary according to thestatus of the cooperatives contemplating merger.For example, cooperatives with a similar financialstructure and similar financial strength and perfor-mance will find it relatively easy to consolidatefinancial elements.

On the other hand, consolidating the financialelements of cooperatives with significantly differ-ent structures and financial strengths may be moredifficult. If one cooperative is financially strong andthe other in danger of bankruptcy, the strongercooperative may feel that the equity position of theweaker one should be adjusted in relation to cur-rent financial predicament in terms of debt and theprobability of future losses without the merger.

Other circumstances may require special plansfor financial consolidation-(a) the cooperativeshave similar levels of financial success, but one isrelatively larger than the other, (b) the cooperativeshave similar financial performance, but one hassuperior operating assets in superior locations, (c)the cooperatives have a similar financial structure,but one owns property with windfall potential, (d)the cooperatives have different types of equityinstruments or revolvement periods vary, etc. Suchdifferences must be considered when planning theconsolidation of financial (balance sheet) compo-nents of merging cooperatives.

A merger plan must examine possible taximplications associated with the various aspects offinancial consolidation. Different methods for con-

2

solidating financial elements may have different taximplications. This may be especially true whencooperatives are merging across State lines, orwhen asset disposal returns windfall profits.

The mission of a merger is to create synergies,and at the very least, a financially and operational-ly sound cooperative that enhances the economicwell-being of owner-members. A merger shouldproduce greater economies of scale, less businessduplication, a greater resource base from which tooperate, and an expanded member base from whichto derive and achieve broader market penetration,greater leadership abilities, and expanded capital-ization.

The merged cooperative also has an opportu-nity for a new beginning by following importantcooperative financial principles and practices,regardless of whether or not the participants com-pletely followed them before the merger.

In other words, the merged organization has arenewed opportunity to improve or continueadherence to the “user-owned” cooperative princi-ple regarding member capitalization, financial poli-cies, and equity redemption. The members musthave a substantial financial stake in their coopera-tive and the equity structure should reflect currentpatterns of usership.

ASSETS AND LIABILITIES

AssetsAs cooperative leaders examine the value and

quality of assets involved in a merger, questionsinvariably arise (figure 1):

(1)(2)(3)

(4)

(5)

(6)

What assets (capacity) will be needed?What are the fixed assets worth?What depreciation, writeoff, or salvage valua-tion methods are used? Is there windfall poten-tial?Should assets be considered at book value orrevalued?Is any compensation necessary (if assets aresold)?What is the status of accounts receivable (andbad debts)?

The leaders need to determine what assets willbe needed to adequately serve the members of theunified cooperative. In some cases, all assets will beretained, as when the merger involves complimen-tary cooperatives and there is little duplication ortrade overlap. It may be more complex in othercases (duplication and overlap) and assets of bothcooperatives are of equal quality and capacity andhave similar locations.

will be needed by the unified cooperative, themerging parties must agree on the value of assets.

It is generally advantageous to simply acceptthe balance sheet asset (book) values of the mergingcooperatives. This is the simplest and most com-monly used method in mergers. However, whenusing book values, make sure that asset values (e.g.,inventory, investments, and fixed assets) are report-ed accurately.

Once the decision is made about which assets On the other hand, when joining organizations

F~~II~S I-- Consolidating Balance Sheet Components

Cooperative A

+ Cooperative B

Assets

Assets

(1)(2)(3)

Unified Cooperative Assets(4)(6)(6)

Cooperative A Liabilities

+ Cooperative B Liabilities

Unified Cooperative Liabilities

(1)

(2)(3)(4)

What assets (capacity) will be needed?What are the fixed assets worth?What depreciation, writeoff, or salvage valuation methods areused? Is there any windfall potential?Should assets be considered at book value or revalued?Is any compensation necessary (ii assets are sokl)?What is the status of accounts receivable (and bad debts)?

How do the total debt to total assets ratios compare (are debtlevels equivalent)?Are accounts payable levels similar?Are asset sales to retire debt necessary?Are liabilities similarly structured (i.e., current, long-term)?

Cooperative A Equity

+ Cooperative B Equity

Unified Cooperative Equity

(1) How are equities identified?(2) What are the differences in equity types?(3) What are the respective redemption plans?(4) What are the redemption schedules (if applicable)?(5) Are the cooperatives current in redeeming equity?(6) What alternatives are available/applicable for consolidating

member equities?(7) What redemption plan will best suit the unified cooperative?

Assets = Liabilities + Equity

If tax implications are relevant to the situation, what are they?

3

use considerably different methods for deprecia-tion, debt writeoff, salvage valuation, or have prop-erties of possible windfall potential, proceduresother than the general acceptance of book valuesmay be necessary. Other procedures include evalu-ating assets on a liquidation basis, collateral basis,or appraisal basis.

The evaluation of assets of the cooperativescontemplating merger must reflect member-equityvalues. If book values are used, member-equity val-ues also can be accepted. However, if assets are val-ued by appraisal or some other method, then mem-ber-equity values may have to be adjusted.

Reevaluation of assets and member equitymay negatively impact some member good-will.Therefore, reevaluation must be done fairly and itsimpact well communicated to members.

When compensation for assets of one of themerging cooperatives is necessary (e.g., assets aresold or their value is appreciably high) the form ofcompensation must be negotiated. Compensationcan be in cash, stock, notes, debentures, or bookcredit. Cash payments may be made in a lump sumor over a period of years.

LiabilitiesMerger questions related to the examination of

liabilities include (figure 1):

(1) How do the total debt to total assets ratios com-pare (are debt levels equivalent)?

(2) Are accounts payable levels current and simi-larly structured?

(3) Must assets be sold to retire debt?(4) Are liabilities similarly structured (i.e., current,

long term)?

Real differences in liabilities and long-termdebt obligations can pose problems for mergingcooperatives. However, differences must be ana-lyzed in relative terms. The merger committee oranalysts should start by examining the ratios oftotal debt (total liabilities) to total assets.

Ratio differences may indicate a possiblesource of friction between members of the partici-pating cooperatives. If friction occurs, one methodof alleviating the problem is to dispose of some of

the assets from the cooperative(s) with greater debtto reduce the debt burden.

However, the outcome of such action (the saleof assets) must be carefully examined. First, towhom are the assets being sold. Will competitors bebidding on assets.7 If so, how will such a sale affectthe unified cooperative’s operations? Second, criti-cal assets must not be sold simply to alleviate a dif-ference in debt-the capacity of the assets thatremain after sale must be sufficient to meet the uni-fied organization’s needs.

Therefore, in some cases, debt levels may haveto be transferred as they are (or paid off in someother manner) so that the unified organizationkeeps the physical assets it needs to operate.

There is usually little concern when debt loadsand structures are relatively similar. In most cases,such debt can be consolidated and/or restructuredin a mutually agreeable manner.

Current liabilities should also be examined. Ifthere are major relative differences in current liabil-ity categories-deposits received, advance pay-ments, trade acceptances, notes payable, short-termloans, and current portions of long-term debt-thereasons for such differences must be clarified and acourse of action set for resolving or accepting dif-ferences.

MEMBER EQUITIESMember equity must be carefully examined

during cooperative mergers. Member equity pro-vides the definition and direct measure of mem-bers’ investment and, thus, ownership in theircooperative. Data from 1991 (ACS Research Report124-Equity Redemption and Member EquityAllocation Practices of Agricultural Cooperatives)indicate that equity made up 49 percent of assetsfor those cooperatives with active equity redemp-tion programs (table 1). For those with inactiveequity redemption programs (where equity is sub-ject to but not redeemed) and those whose equity isnot subject to redemption, equity made up 44 per-cent of assets. This ownership in their cooperativemakes members particularly interested in how theirequity is handled (i.e., transferred/exchanged) in amerger.

4

gable I- Equity redemption practices of agriculturalcooperatives, 19911

Percent

Active redemption programs

Total equity to total assets

Unallocated equity to total equity

Inactive redemption programs

Total equity to total assets

Unallocated equity to total equity

49

21

44

15

Systematic programs only 16Special programs only 34

Systematic and special programs 26

Subtotal 76

No equity redemption program 10

Not subject to equity redemption 14

Total 100

t Rathhone and Wissman (ACS Research Report 124).

Figure 1 lists seven questions pertaining. toconsolidating members’ equity:

(1)(2)(3)(4)

(5)

(6)

(7)

How are equities identified?What are the differences in equity types?What are the respective redemption plans?What are the redemption schedules(if applicable)?Are the cooperatives current in redeemingequity?What alternatives are available/applicable forconsolidating member equities?What redemption plan will best suit the unifiedcooperative?

Cooperative leaders negotiating a mergermust determine how to handle differences in equitytypes and what equity instruments should be usedby the unified cooperative. They will also need toexamine alternatives for consolidating equity andredeeming equity, and work out various relatedissues.

Allocated EquityEquity capital in a cooperative is either allocat-

ed or unallocated. Allocated equity is capitalassigned proportionally to each member on thebasis of the patronage or business the member con-ducts with the cooperative.

Allocated equity is acquired in several differ-ent ways: (1) by direct investment from members(common stock, preferred stock), (2) through aretained patronage allocation (i.e., preferred stock,allocated equity), or (3) through per-unit retains.Conversely, unallocated equity is capital retainedby the cooperative that is not assigned or designat-ed to specific member accounts.

Cooperatives involved in mergers may havedifferent allocated equity profiles. In some, equitiesmay be accrued and labeled differently.Redemption plans and schedules may be at differ-ent stages. Others may carry old allocated equity ofinactive, retired, or deceased members. Differencesin the equity profiles of merging cooperatives mayor may not cause problems. Small differences canusually be overcome easily. On the other hand,variations in redemption schedules and/or thepresence of old allocated equity may create conflictbetween the members of merging cooperatives.

Unallocated EquityWhile not assigned to a member’s account,

unallocated equity makes up varying amounts oftotal equity in cooperatives. In 1991, unallocatedequity made up 21 percent of total equity for coop-eratives with active redemption programs. Forthose cooperatives with inactive redemption pro-grams, unallocated equity made up 15 percent oftotal equity (table 1).

Even though not individually assigned, mem-bers have a vested interest in how unallocated equi-ty is handled. This is especially true when onecooperative has a much larger unallocated accountin relation to its allocated equities than the othercooperative(s). It may be prudent to transfer someunallocated equities from the cooperative with therelatively larger amount into associated memberallocated accounts. However, such a procedurerequires careful study and administration.

5

Equity Redemption PlansThere are three types of systematic equity

redemption programs in agricultural cooperatives:revolving fund plan, base capital plan, and percent-of-all-equities plan. There are also special programsactivated by events that occur to individual mem-bers, such as when they die, retire from farming, orreach a prescribed age.

In 1991,76 percent of all cooperatives hadsome type of active equity redemption program, 10percent had no program, and 14 percent were notsubject to equity redemption (table 1). These datasuggest that cooperatives discussing merger arelikely to have either different or no equity redemp-tion programs. Such differences can lead to prob-lems if each cooperative feels its program or policyis superior.

Members of a cooperative current in redeem-ing its equity may be reluctant to merge their equi-ty on an equal basis with a cooperative that is notcurrent. In other words, members of a cooperativein a more current equity position may be reluctantto dilute their equity by assuming the redemptionburden of a cooperative in a less current position.While the concern of members in such a situation isunderstandable, it is important to carefully examinethese differences and reach an agreeable solution.

If one (or more) of the merging cooperatives issignificantly behind in redeeming its equity, a planshould be devised to either reallocate the old equityinto a current equity rotation schedule or pay it off.On the other hand, if merger participants are cur-rent in redeeming member equity and have similarredemption programs, then the major issues toaddress are how to unite the equities and phase-inthe equity redemption program chosen for the uni-fied cooperative.

To alleviate potential problems, leaders of eachcooperative should openly analyze positive andnegative aspects of each plan. The program ulti-mately chosen should be a current-user based plansupported by the members. Of course, the level ofsupport members exhibit will likely be tied to howwell they perceive that their leaders analyzed eachplan and handled respective differences in redemp-tion schedules and/or outstanding equity

Merger participants should develop and imple-

ment an equity structure for the emerging coopera-tive that reflects current patterns of usership andthen adhere to it. Farmers benefitting from the coop-erative today should be those who finance it.

If old allocated equity of inactive, retired, ordeceased members is still on the books of the coop-eratives studying merger, then a strategy should bedeveloped to retire or pay it off.

ALTERNATIVES FOR CONSOLIDATINGEQUITY

There are numerous ways to consolidate equi-ties during cooperative mergers. This section pro-vides information and examples, in a general sense,pertaining to several methods of consolidating themember equity of cooperatives being merged. Otherinformation pertaining to mergers, consolidations,and acquisitions is also included in this section.

Examples-Hatfield, et al. ReportA report by Hatfield, et al. (Consolidation of

Allocated Equity for Merging Cooperatives PreviouslyOperating on a Revolving Fund, 1986), describes sixoptions for consolidating the equity of cooperativesin different stages of redemption: immediate pay-off, delayed payoff, prorate old equity, reassign-ment to unallocated reserves, equity reevaluation,and base capital plan. The options are describedhere and examples provided where applicable.

hmediate PayoH In this option, the survivingcooperative pays all allocated equity older than apredefined date. That date, prescribed by themerging cooperatives, corresponds to the age-inyears-that the oldest allocated equities are to be inthe unified cooperative. For example, if thecooperatives agree to 7 years, all allocated equityolder than that would be considered old equity andimmediately paid. All allocated equity is broughtinto the merger as is. No concern is given to theamount or actual status (age) of the equity.

Delayed Payoff This option is similar to theimmediate payoff. Existing equity levels arebrought into the merged cooperative. Thedifference is that the old allocated equity (as set bythe predefined date) is paid off at some specified

6

rate (e.g., 2 or 3 years at a time), on a delayed basis(e.g., per fiscal year), and not all at once. Thedelayed payments are continued until all the oldallocated equity has been redeemed (up to thepredefined date).

Hatfield, et al. noted the disadvantage of thesetwo options is that they may be inequitable, espe-cially if a significant difference exists in revolve-ment periods and amounts of old allocated equity.Also, the pressure put on cash reserves may weak-en the capital structure of the unified cooperative(although more so in the immediate payoff planthan in the delayed plan). These options shouldonly be considered when leaders are assured thatthe unified cooperative will not be left with insuffi-cient net worth and financial strength once themerger is completed.

The advantage is that they are likely to be well

perceived in a public relations light-especially tothose members whose cooperatives are on equalfooting in equity redemption, and to those mem-bers whose cooperative is behind in equity redemp-tion in relation to its merger partner(s). However,members of a cooperative further along in equityredemption may not agree with the good-will ges-ture.

Prorate Old Equity The old equity of the mergingcooperatives is prorated over a revolvementschedule. If there is a significant difference betweenthe age of each cooperative’s equity, this option willnot be equitable to the parties involved. Thecooperative more current and with less old equitywill be paying part of the old equity of the otherpartners.

Table 2 (example I) shows prorating old equity.

Table 2- Example 1, prorating old allocated equity, Cooperative A and Cooperative B merging

Ahcated equity Revised equity totalAge in Combined 7-year totals Proratedyears’ Coop AZ Coop 93 equity4 equiW Coop A’ Co-opB@ Combined0

_______ _ _________ Tjwusa& &l/am ___ ______________ Percent _____________________ l=hol/eanrj r&&n --------------------

7 50 55 105 7 17 67 55 122

6 125 200 325 21 52 177 200 377

5 100 125 225 14 35 135 125 260

4 75 150 225 14 35 110 150 260

3 55 250 305 19 48 103 250 353

2 110 95 205 13 33 143 95 238

1 80 100 180 12 30 110 100 210

Totals 595 975 1,570 100 250 845 975 1,820

Equity over7 years old 250 0 250 0 0 0 0

SOURCE: Hatfii, et al., p6. (modified example)1 Cooperatfve B is on a 7-year revolving fund plan and current, and Cooperative A does not have a member redemption plan or has neverredeemed allocated equity.2 Allocated equity of Cooperative A-last 7 years and total allocated equity over 7-years old.1 Allocated equity of Cooperative B-last 7 years.4 Allocated equity from Cooperative A and Cooperative B added together for each year, overall, and old equity.5 Combined equity in each year of the 7-year period divided by the total of the 7 years.a The $250 old outstanding equity of Cooperative A multiplied by the corresponding percent data in the preceding column.7 Revised equity of Cooperative A-original allocated equity (2nd column) plus prorated old equity.8 Cooperative B revised equity the same as previously because there was no old equity.e Combined revised equity total of Cooperative A and Cooperative 9.

7

In this example, Cooperative A has allocated equitymore than 7 years old, while Cooperative B isredeeming equity on a 7-year revolvement cycle.The older allocated equity of Cooperative A($250,000) is prorated over the latest 7 years to coin-cide with the redemption schedule of CooperativeB. The equity is prorated by multiplying total allo-cated equity older than year 7 by the percentage incolumn 5 of table 2 (combined equity for each yearas a percent of 7-year combined total) for each yearof the 7-year period.

The resulting amount is then added to theequity of Cooperative A for redemption in the cor-responding year. While example I shows the totalamount of old equity of Cooperative A being pro-rated, actually, the old equity of each member ofCooperative A is being prorated.

This plan brings the older equity of one coop-erative into the shorter revolving cycle of the othercooperative. Spreading the old equity redemptionobligation over a number of years softens the finan-cial burden of trying to redeem significant equityamounts all at once.

Example A-I shown in appendix table 1 is sim-ilar to example I except that both Cooperative Aand Cooperative B have old equity prorated. Thiscase assumes that a 9-year revolving fund is chosen(both cooperatives were revolving on a longerschedule at the time of merger) for the unifiedcooperative. Thus, the old equity of each coopera-tive is prorated over the 9-year schedule.

This option shortens the period of equity rota-tion of one or both cooperatives in example I andexample A-I. However, when cooperatives havesignificantly different equity profiles prior to themerger, such as in example I, the plan is not equi-table to all members.

Reassignment to Unallocated Reserves Thisoption also alleviates the equity redemptiondifferences of Cooperative A and Cooperative B.The less current cooperative-Cooperative A-absorbs an amount of equity (recent equity) equalto its old equity (amount older than the agreed-upon 7 years) and crediting it to unallocatedreserves of the unified cooperative. Cooperative A(as used in the previous example) would deduct

$250,000 from its recent 7-year allocated equity total($595,000; the deduction could be prorated over the7-year rotation schedule) and the unifiedcooperative would be credited with $250,000 inunallocated reserves (table 3-example II).

To account for the loss of recent equity, eachpatron of Cooperative A could be issued a capitalloss statement equal to the amount deducted fromhis/her recent equity portion. However, this exer-cise still results in the need to account for the$250,000 old equity (greater than 7 years). One solu-tion is to bring it into the 7-year-redemption sched-ule. Prorating this amount over the most recent 7years in the same manner as presented in example I(table 2) leaves the unified cooperative with com-bined equity of $1,820,000 as shown in the last col-umn of table 3, including the $250,000 of unallocat-ed reserve.

Hatfield, et al. point out that this option treatsall members fairly and equitably because it placesthe responsibility for older unredeemed equity onthe cooperative with the older equity.

Equify Reevaluation An interesting formula isprovided in this option. The book values of themerging cooperatives’ allocated equity are adjustedaccording to appraised values of that equity. Theseconversion ratio formulas are used to adjust bookvalues in this option:

Conversion ratio formula for Cooperative A:

A, = Aa/AbBa/Bb

Conversion ratio formula for Cooperative B:

B, =Ba/Bb

Aa/Ab

A and B represent Cooperatives A and B whilea = appraised value,b = book value, andr I reevaluation multiplier.

8

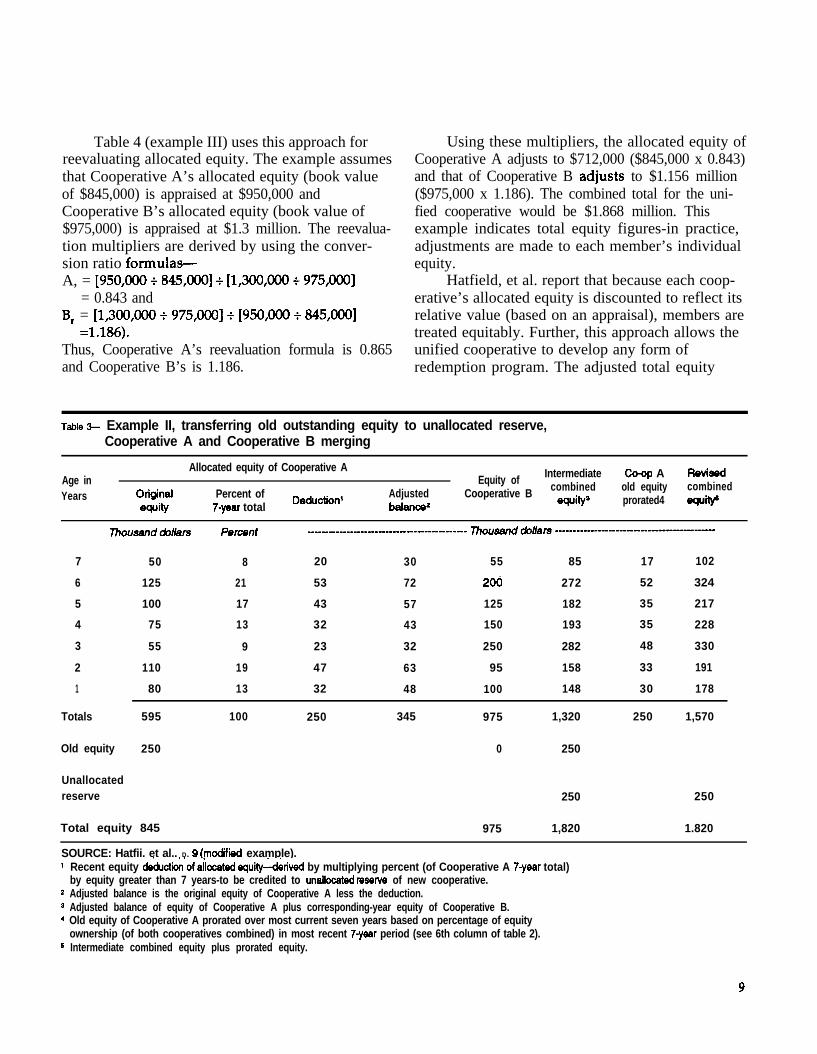

Table 4 (example III) uses this approach forreevaluating allocated equity. The example assumesthat Cooperative A’s allocated equity (book valueof $845,000) is appraised at $950,000 andCooperative B’s allocated equity (book value of$975,000) is appraised at $1.3 million. The reevalua-tion multipliers are derived by using the conver-sion ratio formulas-A, = [950,000 + 845,000] + [1,300,000 + 975,000]

= 0.843 andB, = [1,300,000 + 975,000] + [950,000 + 845,000]

=1.186).Thus, Cooperative A’s reevaluation formula is 0.865and Cooperative B’s is 1.186.

Using these multipliers, the allocated equity ofCooperative A adjusts to $712,000 ($845,000 x 0.843)

.and that of Cooperative B adlusts to $1.156 million($975,000 x 1.186). The combined total for the uni-fied cooperative would be $1.868 million. Thisexample indicates total equity figures-in practice,adjustments are made to each member’s individualequity.

Hatfield, et al. report that because each coop-erative’s allocated equity is discounted to reflect itsrelative value (based on an appraisal), members aretreated equitably. Further, this approach allows theunified cooperative to develop any form ofredemption program. The adjusted total equity

gable S- Example II, transferring old outstanding equity to unallocated reserve,Cooperative A and Cooperative B merging

Age inYears

Allocated equity of Cooperative A Intermediate RevissdEquity of Co-op A

OIigilIal Percent of Deduction1 Adjusted Cooperative B combined old equity combined

equity 7-year total balance2 equity3 prorated4 equity6

7 50 8 20 30 55 85 17 102

6 125 21 53 72 200 272 52 324

5 100 17 43 57 125 182 35 217

4 75 13 32 43 150 193 35 228

3 55 9 23 32 250 282 48 330

2 110 19 47 63 95 158 33 191

1 80 13 32 48 100 148 30 178

Totals 595 100 250 345 975 1,320 250 1,570

Old equity 250 0 250

Unallocatedreserve 250 250

Total equity 845

SOURCE: Hatfii. et al.. D. 9 lmociifii example).

975 1,820 1.820

Recent equity ckkction’of skated equity-hhived by multiplying percent (of Cooperative A 7-year total)by equity greater than 7 years-to be credited to unalloceted msetve of new cooperative.Adjusted balance is the original equity of Cooperative A less the deduction.Adjusted balance of equity of Cooperative A plus corresponding-year equity of Cooperative B.Old equity of Cooperative A prorated over most current seven years based on percentage of equityownership (of both cooperatives combined) in most recent 7-year period (see 6th column of table 2).Intermediate combined equity plus prorated equity.

9

TEW c Example iii, adjusting allocated equity basedon conversion ratio formula, Cooperative Aand Cooperative B merging

Coopwaive A Coopmative B Combined totals

Thousand &Uars

Book value 845 975 1,820Appraised value1 950 1,300 2,250

Conversion ratio* 0.843 1.188

Adjusted equity3 712 1,158 1,858

Source: Ha&Id, et al., p.11 (modified example).l Appraised velues assumed for example purposes.* Conversion ratio derived by conversion ratio formula (see text).3 Ac@sted equity is cbrived by multiplyiig equity at book value by

conversion ratio.

could be divided equally to fit into an equityredemption schedule, or it could be converted to abase-capital plan, or a percentage-of-all-equitiesplan.

The basis of this alternative is the appraisalprocess. It must consider each cooperative’s poten-tial for deriving positive returns as well as the con-dition of the fixed assets. A cooperative may showa capital loss in the reevaluation process due to adecline in property values or earning power (asCooperative A did in example III).

Base Capita/ P/an Under this plan, a total equityrequirement is determined for the unified,cooperative. Each member would be obligated tohold equity in the unified cooperative based onhis/her business volume during the year.

Each member’s annual business volumewould be divided by the total business volume ofthe unified cooperative (a 3- or S-year average forinstance) to find a basis. The resulting basis-per-cent (i.e., relative proportion of cooperative use andthus, equity requirement)-for each member wouldbe multiplied by the unified cooperative’s totalequity requirement to derive each member’srequired equity investment.

Then, a comparison between each member’srequired equity investment and current equity

holding in his/her pre-merger cooperative wouldbe made to determine if the member is over- orunder-invested. Equity of over-invested memberswould be retired while under-invested memberswould make up the equity deficiency (some combi-nation of direct cash payment, retained earnings,capital retains, and/or the purchase of equity froman over-invested member). The investment wouldbe adjusted annually according to the individual’spatronage and the cooperative’s capital needs.

This method for consolidating equity may bethe easiest to administer in situations where thereare significant differences in the amounts of mem-ber equity between the pre-merger cooperatives.However, Hatfield, et al. point out that pre-mergerinequities will continue to exist unless there is astock reevaluation. If stock is revalued, inequitiescan be corrected.

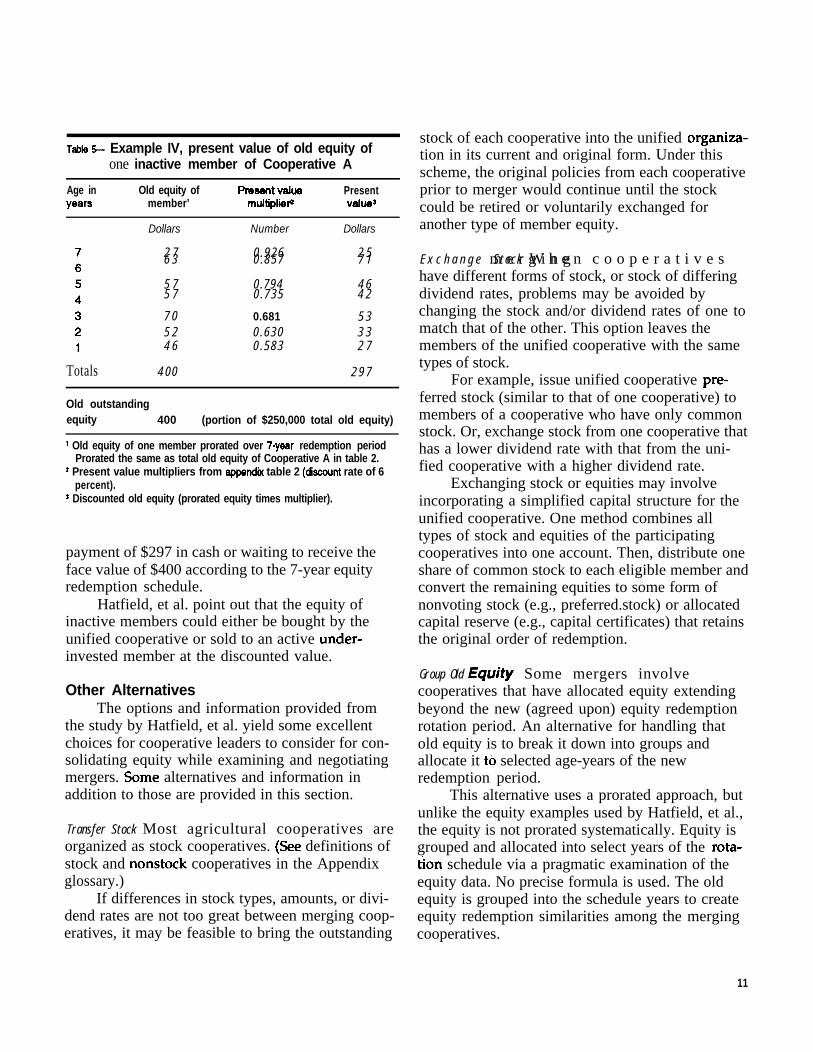

Handling inactive Patrons Hatfield, et al. alsopresented a buyout option for paying off the equityof inactive patrons. In contrast to leaving inactivepatron equity in the unified cooperative forredemption in the chosen schedule, inactivepatrons may receive a lump-sum payment for theirallocated equities. After reaching agreement of adiscount rate, the present value of future equitypayments from the revolving fund plan would becalculated and the total paid in lump sum.

This procedure gives the inactive member theoption of immediately receiving cash for his/herequity at a discounted rate rather than having itplaced in the equity revolvement rotation of theunified cooperative for later redemption.

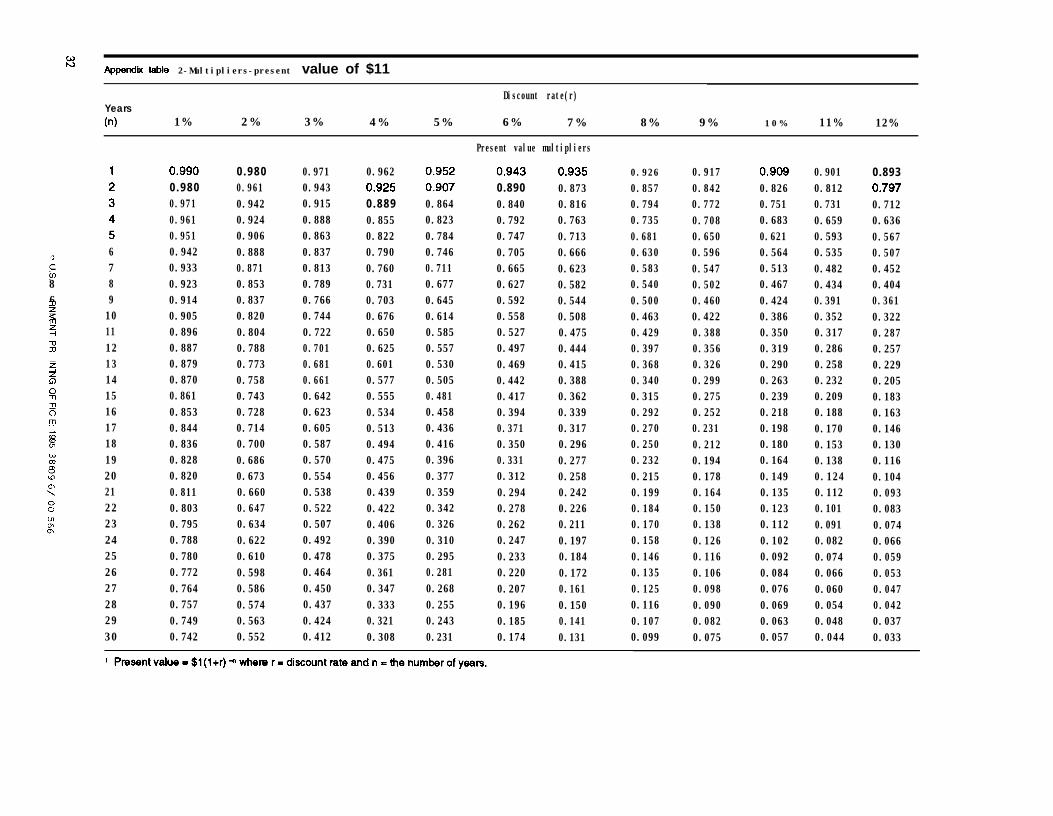

Table 5 (example IV) illustrates this situation.One member of Cooperative A has old equity of$400 that is prorated over the 7-year redemptionperiod. To discount the equity, the prorated amountfor each year is multiplied by the present valuemultiplier for the established discount rate (e.g., 8percent) and for the appropriate time period.(because the equity from year 7 would be redeemedin year 1, the corresponding multiplier would befound by using 8 percent and 1 year.) Followingthis pattern for all 7 years results in a discountedtotal value of $297 for the member. Thus, this mem-ber would have the option of receiving a lump sum

10

we s- Example IV, present value of old equity ofone inactive member of Cooperative A

Age inYears

Old equity of PIwent VahJemember’ multipliiF

Dollars Number

PresentVdlW

Dollars

stock of each cooperative into the unified organiza-tion in its current and original form. Under thisscheme, the original policies from each cooperativeprior to merger would continue until the stockcould be retired or voluntarily exchanged foranother type of member equity.

2 7 0 . 9 2 6 2 56 3 0 . 8 5 7 7 1

5 7 0 . 7 9 4 4 65 7 0 . 7 3 5 4 2

7 0 0.681 5 35 2 0 . 6 3 0 3 34 6 0 . 5 8 3 2 7

4 0 0 2 9 7

E x c h a n g e m e r g i n g c o o p e r a t i v e sS t o c k W h e nhave different forms of stock, or stock of differingdividend rates, problems may be avoided bychanging the stock and/or dividend rates of one tomatch that of the other. This option leaves themembers of the unified cooperative with the sametypes of stock.

For example, issue unified cooperative pre-Totals

Old outstandingequity 400 (portion of $250,000 total old equity)

’ Old equity of one member prorated over 7-year redemption periodProrated the same as total old equity of Cooperative A in table 2.

* Present value multipliers from appendii table 2 (&count rate of 6percent).

3 Discounted old equity (prorated equity times multiplier).

payment of $297 in cash or waiting to receive theface value of $400 according to the 7-year equityredemption schedule.

Hatfield, et al. point out that the equity ofinactive members could either be bought by theunified cooperative or sold to an active under-invested member at the discounted value.

Other AlternativesThe options and information provided from

the study by Hatfield, et al. yield some excellentchoices for cooperative leaders to consider for con-solidating equity while examining and negotiatingmergers. Some alternatives and information inaddition to those are provided in this section.

Transfer Stock Most agricultural cooperatives areorganized as stock cooperatives. (See definitions ofstock and nonstock cooperatives in the Appendixglossary.)

If differences in stock types, amounts, or divi-dend rates are not too great between merging coop-eratives, it may be feasible to bring the outstanding

ferred stock (similar to that of one cooperative) tomembers of a cooperative who have only commonstock. Or, exchange stock from one cooperative thathas a lower dividend rate with that from the uni-fied cooperative with a higher dividend rate.

Exchanging stock or equities may involveincorporating a simplified capital structure for theunified cooperative. One method combines alltypes of stock and equities of the participatingcooperatives into one account. Then, distribute oneshare of common stock to each eligible member andconvert the remaining equities to some form ofnonvoting stock (e.g., preferred.stock) or allocatedcapital reserve (e.g., capital certificates) that retainsthe original order of redemption.

Group Old Equity Some mergers involvecooperatives that have allocated equity extendingbeyond the new (agreed upon) equity redemptionrotation period. An alternative for handling thatold equity is to break it down into groups andallocate it t0 selected age-years of the newredemption period.

This alternative uses a prorated approach, butunlike the equity examples used by Hatfield, et al.,the equity is not prorated systematically. Equity isgrouped and allocated into select years of the rota-t’ion schedule via a pragmatic examination of theequity data. No precise formula is used. The oldequity is grouped into the schedule years to createequity redemption similarities among the mergingcooperatives.

11

The equities of Cooperative A andCooperative B-used in the previous examplesfrom Hatfield, et al. (table 2, example I)-could begrouped. Table 6 (example V) shows that the$250,000 of old equity of Cooperative A is arbitrari-ly broken into three groups ($65,000, $165,000, and$20,000). These groups are allocated into three age-years (4,3, and 1, respectively) of the 7-year rota-tion schedule. The net result is that the old equityof Cooperative A is grouped and distributed intothe chosen 7-year equity rotation schedule relativeto the distribution of Cooperative B equity in theschedule.

This option allows old equity of CooperativeA to be reallocated into the new 7-year equityredemption rotation period. However, the equity isgrouped and placed into age-years that will resultin the old equity being redeemed in future years.While this goes somewhat against the principle thatcurrent users be current financers, it is more equi-table to the members of Cooperative B. The older

equity of Cooperative A is placed in later revolvingyears.

This equity grouping and allocation could alsobe done in other ways. In essence, the precise typeof distribution followed is irrelevant as long as bothcooperative memberships are satisfied with theresults. However, two rules should be followedwhen using this option to ensure that the equitygrouping and subsequent allocations are logicallymade:

(1) Avoid allocating any equity groupings intothe oldest equities (front years of the schedule)that will be redeemed during the unified coop-erative’s first few years of operation-thisavoids placing an additional financial burdenon the unified cooperative. (In table 6, exam-ple V, no groups are allocated to scheduleyears 7,6, and 5.)

(2) Develop equity group sizes relative toequity amount differences between the merg-

we IZ- Example V, grouping and reallocating old allocated equity, Cooperative Aand Cooperative B merging’

Allocated equity Revised equity totalsAge in Grouped equityyears Coop A C-WB Coop AZ Co+p A Coop B

Thousand dollars

Combined

7 5 0 5 5 5 0

6 125 2 0 0 125

5 100 125 100

4 75 150 6 5 140

3 55 2 5 0 165 2 2 0

2 110 9 5 110

1 60 100 2 0 100

Totals 595 9 7 5 2 5 0 645Equity over 7years old 2 5 0 0 0 0

Grouping of old equity:Group 1 6 5Group 2 165Group 3 2 0

1 Equity data from same cooperatives in table 2.* Pragmatic grouping of old equity of Cooperative A and reallocation among years 4,3, and 1.

5 5 105

2 0 0 3 2 5

125 225

150 290

2 5 0 4 7 0

9 5 205

100 200

9 7 5 1,820

0 0

12

ing cooperatives in the various years chosenfor allocation. (In example V the third .$20,000group allocated to age-year-l makes the equityamounts between the members of the twocooperatives even.)

This option would be more complicated ifboth (or more) cooperatives have old allocatedequity that extends beyond the agreed-upon rota-tion period for the unified cooperative. However,grouping and reallocating the old equity could stillbe a valid and equitable option as long as theresulting aged equities of each cooperative are simi-lar and not so large that a substantial financial bur-den is placed on the unified cooperative.

E9ua/ but Weighted Grouping Another optionfor reallocating old equity is to prorate it among theyears of the new schedule on an equal, yetweighted basis. Old equity would be allocatedamong the age-years by multiplying it by a scaledpercentage derived for each year of the rotation.

Table 7, example VI, shows this option. Part ofthe over 7-year equity of $250,000 of Cooperative A

is allocated among each rotation year by multiply-ing it by a scaled prorate percent. To determineappropriate scaled percents, divide 100 percent by 7years. The resulting percent figure is used for themiddle year of the rotation. Then, each precedingand additional year is decreased and increased,respectively, by 1 percent for each consecutive year.

In example VI, 100 percent divided by 7 yearsequals 14.3 percent. This percentaged is given to themiddle year (year 4). Then scale each consecutiveyear higher than year 4 by 1 percent lower than thepreceding year, and each consecutive year lowerthan year 4 is scaled by 1 percent higher than thepreceding year. (Note that the scaled prorate per-cent for age-year 7 is slightly different. An adjust-ment was made to that year to make the percent-ages sum to 100.)

Follow a similar procedure for any number ofodd years in a schedule. For schedules with an evennumber of years, use the resulting percent figure(100 percent divided by the number of years) forthe middle two years and then follow a similar scal-ing procedure (example VI) for the rest of theschedule.

gable 7- Example Vl,.scalad prorating of old allocated equity, Cooperative A and Cooperative B merging’

Allocated equity Scaled Revised equity totalAge in Combined prorate ProratedYears Co-op A Coop B equity Pe-nP equiW Coop A Coop B Combined

_________ ______ Thousand &,/jam _______________ Penxnt __ ______________ ____ Thoum,j &//a,-~ ______ __ __._________

7 50 55 105 11.2 28 78 55 1336 125 200 325 12.3 31 156 200 3565 100 125 225 13.3 33 133 125 2584 75 150 225 14.3 36 111 150 2613 55 250 305 15.3 38 93 250 3432 110 95 205 16.3 41 151 95 2461 80 100 180 17.3 43 123 100 223

Totals 595 975 1,570 100 250 845 975 1,820

Equity over7 years old 250 0 250 0 0 0 0

1 Equity data from Cooperative A and Cooperative B-same as table 2, example A.z Scaled prorate percents derived by dividing 100 percent by 7 years, using that result for the middle year, and then scaling that fiire higher

toward earlier years (and lower toward later years of schedule). In this example, 14.3 percent is the result used for the middle year (4th year).Then each consecutive year higher than year 4 is scaled 1 percent lower than the preceding year, and each consecutive year tower than year 4is scaled 1 percent higher than the preceding year.

3 Prorated equity derived by multiplying $250,000 (old equity) by the scaled prorate percent figures of the preceding column.

13

While this option may not be equitable to allmembers (those of Cooperative B), it may be palat-able because of the way it distributes a higher pm-portion of the old equity (such as Cooperative A)toward the later years of the redemption rotationschedule.

Percentage-of-All-Combined Equities Thisoption is analogous to the Percentage-of-All-Equities redemption plan used by manycooperatives.

The cooperative would redeem a percentage ofall outstanding allocated equities. All memberswould receive the same percentage of their equitiesregardless of when they were originally allocated.The percent figure used for redemption would bedetermined by the board of directors, given the uni-fied cooperative’s financial performance and capitalneeds. Members would receive an equity redemp-tion derived from a percentage of their total equityaccounts included in the combined equities of theunified cooperative. Equity would be redeemedannually or as determined by the board.

All combined equity would be redeemed bythe percentage-of-all-combined equities plan beforeany new allocated equity, accumulated from theoperations of the unified cooperative, would beredeemed. Once all past equity is redeemed, the

ia~e e- Example VII, percentage of all combinedequities plan

Cooperative A Cooperative B Combined

Thousand Dollars

EquityAookvalue 845 975 1,820

Equity-adjusted’ 950 1,300 2,250

Equity redeemabld 1 3 5 ( 6 % )

1 Equity adjusted following valuation of assets.2 Equity redeemable after first year of operation--percent of all

combined equity plan, subject to financial performance and equityrequirements. (Each member would receive 6 percant of equitieshe/she has alkcated in combined equity.)

new equity could be similarly redeemed or arevolving fund established.

Table 8, example VII, shows this option usingthe same‘two cooperatives in the previous exam-ples. After appraisal, Cooperative A’s $845,000 ofallocated equity is adjusted to $950,000 andCooperative B’s $975,000 is adjusted to $1.3 millionfor a combined equity total of $2.255 million (eachmember of Cooperative A would have his/herequity adjusted by a multiplier of 1.12($950,000/$845,000). Those in Cooperative B wouldhave their equity adjusted by a multiplier of 1.33($1.3 million/$975,000).

In the first year of operation, the board makes$135,000 available for redemption. This amount,applied against the combined adjusted equity total,is 6 percent. Thus, each member would have 6 per-cent of equity redeemed (equity in the adjustedcombined equity total). This procedure would befollowed each year until all the combined equity isredeemed.

In this example, assets shown were revalued.This illustrates that this option fits well with merg-ers that involve asset reevaluation. Equity is adjust-ed to reflect asset values provided by the reevalua-tion and then combined. This option also applies tosituations where no assets or equity are revalued.

The major factor to consider in using thisoption is its fairness or unfairness to members,given that all their equities will be combined intoone grouping without regard to original dates ofissuance.

The Percentage-of-All-Combined Equity planis easy to administer and understand. It can also befinancially beneficial. Annual redemption of thecombined equities would not be predeterminedbased on historically allocated sums but ratherdetermined on the unified cooperative’s mostrecent financial performance and capital require-ments.

The disadvantage is that if equity is revaluedat higher levels for both cooperatives, such as inexample VII, then the unified cooperative will beresponsible for redeeming higher levels of equitythan originally prescribed.

14

AcquisitionsAcquisition characteristics distinguish them

from merger and consolidation transactions. In anacquisition, one cooperative purchases the assets ofanother. The cooperative being acquired is dis-solved and ceases to exist. The acquiring coopera-tive assumes the assets, and sometimes the liabili-ties.

The board of directors of the acquiring cooper-ative must vote whether or not to proceed with thetransaction. A full vote of the members is notrequired. However, members of the cooperativebeing acquired generally must vote on liquida-tion/voluntary dissolution. While a full member-ship vote is not necessary for the acquiring cooper-ative, lack of membership support may inhibitfuture operations of the unified cooperative. Thus,it is in everyone’s interest that directors of theacquiring cooperative proceed with the transactiononly with sound member support. A strong direc-tor-to-member communication program will berequired.

When cooperatives aspire to combine assetsthrough an acquisition, consolidation of critical bal-ance sheet components requires careful negotiationand analysis, just as in a merger or consolidation.Members of both cooperatives have a vested inter-est in how the transaction is completed. Often, theassets of the cooperative being acquired will bereevaluated (e.g., market value).

To speed the process, the acquiring coopera-tive may find it practical to assume the liabilities ofthe other. However, the acquiring cooperative is notrequired to assume the liabilities of the dissolvingcooperative. But, the dissolving cooperative cannotbe folded until it pays its liabilities, so the acquiringcooperative often assumes them. The liabilities canbe assumed as is or be restructured. Restructuringmay be advisable when the cooperative being pur-chased is in poor financial health.

Equity instruments will be issued to the mem-bers of the cooperative being acquired. This is usu-ally done in relation to the value of assets and mayalso be contingent on outstanding liabilities thatmust be assumed and the future earning potentialof the cooperative being acquired.

The acquiring cooperative may issue equity

certificates, stock (preferred, common), bonds,notes, equity credits, nearly any kind of financialinstrument, to the members of the acquired cooper-ative as part of the transaction. The type issued willusually depend on what acquiring cooperative cur-rently uses and the circumstances pertaining to themember equity of the cooperative being acquired(i.e., equity age and type).

Equity is often transferred during an acquisi-tion by issuing new equity credits (e.g., stock, cer-tificates) to the new members in exchange for theequity they hold in their cooperative. The exchangerate may depend on specific factors (e.g., assetsvalue, equity level) associated with the acquisitiontransaction. The simplest case will involve coopera-tives with similar types of equity. A simpleexchange can be made. However, in some cases anacquiring cooperative may wish to issue differenttypes of equity instruments to different members ina way that makes the equity capitalization plan ofthe acquiring cooperative more fair to members.For example:

Issue stock and debenture bonds. Cooperative A isacquiring Cooperative B. Cooperative A has a 7-year equity redemption schedule while its partnerhas not redeemed equity in many years.Cooperative A issues one share of common (voting)stock and preferred stock (its primary memberequity instrument) to Cooperative B’s current-usermembers in exchange for their accrued equity.Cooperative A then issues debenture bonds (withgiven due dates) to the inactive members ofCooperative B in exchange for their accrued equity.

This allows the current-user members ofCooperative B to participate in Cooperative A’sequity capitalization and redemption program andprovides a way to retire the old equity ofCooperative B’s inactive members. Their equity willbe redeemed in the form of debenture bonds thatbecome due in the future. Most cooperatives allowmembers to cash in debenture bonds before theyare due.

Acquisitions are disruptive, particularly to themembers of the dissolving cooperative who mayfeel a severe sense of loss. For this reason, it isimportant that the interests of all members effected

15

be respected and protected by the individualboards as the transaction is completed.

SummaryThe six alternatives described earlier as devel-

oped by Hatfield, et al., provide sound examples ofconsolidating the equity of merging cooperatives.

The first four options should be includedamong equity combination considerations of coop-eratives with revolving fund plans (or cooperativesthat have no set redemption plan but are willing toimplement a revolving fund plan). The last twooptions should be included among equity combina-tion considerations of cooperatives with base capi-tal, percentage of all equities, or other special plans.Of course, the last two options also could be usedby cooperatives with revolving funds.

Five additional alternatives are described inthe second part of this section. The first two alter-natives involve the simple transfer and exchange ofstock. The third and fourth should be considered bycooperatives with revolving fund plans or whosemerger plan involves implementing a revolvingfund. The fifth alternative would fit any merger sit-uation. The example corresponding to this alterna-tive indicates that equity is adjusted to reflect assetreevaluation. The other four alternatives could bemade more equitable to members of merging coop-eratives by adjusting members’ equity in accor-dance with an asset reevaluation.

Acquisition, another way to combine coopera-tives, is a popular alternative to merger and consol-idation. The authority granted to the acquiringcooperative via the acquisition makes difficultasset-utilization, financial, personnel, and otheroperational decisions a little easier to carry out.

COOPERATIVE EXAMPLES OF COMBININGEQUITY

Up to this point, general information andexamples of consolidating member equity amongmerging cooperatives have been presented, somefrom previous studies and some developed. Whilethey demonstrate different methods, they don’tindicate precisely how cooperatives complete mem-ber equity transfers/exchanges during actual merg-ers.

This section provides some examples and casestudies of actual cooperative mergers, consolida-tions, and acquisitions. Ten cases are described.Four originate from a report by Haskell (FCSResearch Report 8-Results and Methods of FourMergers By Local Farm Supply Co-ops) completedin 1970. The others stem from a survey of recentlymerged cooperatives.

In the first four case examples, two farm sup-ply cooperatives participated in each merger. Theyare identified as Cooperative A or Cooperative B.

Merger-Different Size and StrengthA relatively larger and stronger Cooperative A

merged with Cooperative B. After the merger,Cooperative A assumed operation of all facilitiesand services previously operated by Cooperative B.Cooperative A became the unified cooperative andassumed all assets, debts, and other liabilities ofCooperative B.

The shares of common stock, share credits,deferred patronage refunds, and patrons’ equityreserves held by members of Cooperative B wereconverted, at par value, into shares and partialshares of common stock of Cooperative A (the uni-fied cooperative). Preferred stock was carried intothe unified cooperative at par value.

Cooperative B was 9 years behind CooperativeA in stock redemption prior to the merger, so twoalternative redemption methods were described inthe merger plan.

Alternative 2. The board of directors of the unifiedcooperative could call stock for redemption orretirement in the order of issuance by years. Theoldest outstanding stock would be called first.Whenever common stock of Cooperative A issuedprior to the effective date of merger would becalled for redemption or retirement, the board ofdirectors would also call a proportionate share ofstock issued to common stockholders ofCooperative B, in the order of issuance by years.Further, no common stock of the unified coopera-tive issued after the effective date of the mergerwould be retired until all common stock issued byCooperative B prior to the effective date had beenretired.

16

Alternative 2. The board of directors of the unifiedcooperative could retire common stock after thedate of merger on the basis of a percentage of allthe common stock outstanding. In this event, thesame percentage of the stock of each commonshareholder would be called at the same time,regardless of issue date.

Consolidation-Different Size and StrengthIn this case, a smaller but more financially

sound Cooperative A was consolidated with aslightly weaker Cooperative B. The existence ofCooperatives A and B ended and a new cooperativeemerged. The unified (surviving) cooperativeassumed ownership and operation of all facilitiesand services of the original cooperatives.

The plan of consolidation contained specificarrangements concerning the conversion of stockand stock credits of the original cooperatives tostock and allocated reserves of the unified coopera-tive.

Cooperative A had preferred stock, first issue(6 percent cumulative dividend), preferred stock,second issue (5 percent cumulative dividend), andpatronage common stock and credits (no divi-dends). Cooperative B had preferred stock (5 per-cent noncumulative dividend) and patronage com-mon stock and credits (no dividends).

An owner of stock and/or stock credits ineither original cooperative could determine thesecurities (i.e., of those offered) of the unified asso-ciation that he/she would receive for presentlyheld stock. All exchanges were completed on a dol-lar-fordollar basis as to stated or par amounts.

The consolidated cooperative offered pre-ferred stock (5 percent noncumulative dividend)and 6 percent debenture bonds due in 15 years.Bonds could be exchanged within 3 months fromthe effective time of merger for preferred stock at 5percent noncumulative dividend.

Acquisition l-Different Size and StrengthA stronger and slightly larger Cooperative A

acquired Cooperative B, a smaller cooperativeexperiencing management and financial difficulties.

Cooperative A purchased all of CooperativeB’s plant facilities and equipment, supplies, furni-

ture, fixtures, office equipment, accounts receivable,contracts, leases, and interests in all real and per-sonal property, all at book values.

Cooperative B agreed to exert all possibleeffort to assure transfer of at least 75 percent of itsoutstanding preferred stock held by its members tothe surviving association at par value. Preferredstockholders of Cooperative B would receive nodividends that had been passed. At its option,Cooperative A could void the transaction if 75 per-cent of the stock had not transferred.

Acquisition 24imilar Size and StrengthIn this case Cooperative A acquired

Cooperative B. Both were about the same size andstrength but there was a sharp contrast in the typesof businesses and services they offered.Cooperative A (surviving) assumed operation of allfacilities and services of Cooperative B.

The shares of common stock of Cooperative Bwere converted into shares of common stock of theunified cooperative at par value. The unified coop-erative ended up with common stock at $5 a shareentitling each holder to one vote, and nonvotingcommon stock with a par value of $5 a share.Dividends on both types were eligible for declara-tion by the board of directors out of any net savingsnot distributable as patronage refunds.

Preferred stockholders of Cooperative B wereapportioned one or more subordinated promissorynotes bearing interest at 4 percent a year, andmaturing in 20 years from issue date. Promissorynotes were in the principal amount of the par valueof the preferred stock so exchanged. No dividendswere to be paid on the outstanding preferred stockof Cooperative B for any year beginning on or afterthe effective date of consolidation, whether or notthe stock had been surrendered in exchange for apromissory note.

The oldest outstanding common stock ofCooperative B was issued 18 years prior to mergerand 21 years in Cooperative A. To deal with stock-holders of both cooperatives equitably, the unifiedcooperative retired all of the common stock issued18 years prior to merger. Next came stock issued 20years prior to merger followed by 17 years, 19years, and 21 years. Thereafter, stock issued 16

17

years prior and in any subsequent years was retiredin the order of issuance. This stock redemptionsequence is clarified as follows:(1) Stock issued 18 years prior-Cooperative B’s

oldest stock and Cooperative A’s 18th yearstock.

(2) Stock issued 20 years prior-Cooperative Astock.

(3) Stock issued 17 years prior--stock from bothcooperatives.

(4) Stock issued 19 years prior-Cooperative Astock.

(5) Stock issued 21 years prior--Cooperative A’soldest stock.

(6) Stock issued 16 years prior-stock from bothcooperatives.

(7) Stock issued 15 years prior, followedby 14,13, etc.

The stock redemption gap between membersof each cooperative would be equal following theredemption of stock reflected in the 5th sequence(stock issued 21 years prior).

Recent Case Study ExamplesThis section includes six case studies of farmer

cooperatives that have merged in recent years. Twocooperatives were involved in each merger. Theywere asked several questions pertaining to thefinancial aspects of the merger (see Appendix B).

In all but one case, a committee was appointedto study and negotiate various aspects of the merg-er. The average committee size was nine.Participants consisted largely of directors and man-agement personnel from both cooperativesinvolved. A couple committees also had attorneysand other outside individuals. In one case, accoun-tants were used. One case study subject indicatedthat the committee performed very well, two indi-cated that it performed well, and the others said itperformed okay.

The first case study is described in detail whilethe others are summarized.

Case Study &Cooperatives 0 and P TWO

relatively small cooperatives were consolidated andadopted a new name. A 1Zmember committeenegotiated merger issues. Member support was

moderate. (The cooperatives identified membersupport as strong, moderate, weak, or none.)

The unified cooperative had assets of about$3.8 million. Pie-merger data showed:

Cooperative 0

Sales of about$3.3 million.

Assets of about$2.2 million.

Low debt; short-termdebt-to-asset ratio of14 percent; limitedlong-term debt.

Membership commonstock, certificates ofindebtedness.

No set redemptionprogram; redeemedequity at boarddiscretion.

Cooperative P

Sales of about$2.2 million.

Assets of about$1.6 million.

Low debt; short-termdebt-to-asset ratio ofabout 17 percent;no-long-term debt.

Common stock, pre-ferred stock, pre-ferred stock A.

No set redemptonprogram; redeemedequity at boarddiscretion

Excess equipment assets were sold at bookvalue and the proceeds used to pay off some exist-ing debt. Common stock from both cooperativeswas exchanged for unified cooperative commonstock (par value $10) to members of the participat-ing cooperatives (0 and P). The conversion had tobe made within 30 days after the consolidation.Members who neither wished to join nor converttheir common stock could surrender that stock forcash payment. Stock surrenders also had to bemade within 30 days.

The cooperatives developed and followed aplan for transferring equities. Records were exam-ined to determine equity amounts. The board ofdirectors of the unified cooperative (within 60 daysof consolidation) determined the allocated and totalequities of each constituent cooperative.

For Cooperative 0, the amounts of allocatedpatronage equities consisting of qualified, nonqual-ified, and certificates of indebtedness were deter-mined as well as the total amount of Cooperative 0

equities less the face value of outstanding member-ships (the difference being total Cooperative 0equities).

For Cooperative P, the amount of preferredstock A and preferred stock was determined as wellas the total patrons’ equities less membership orcapital stock (the difference being total CooperativeP equities).

After stock determination, the board of direc-tors allocated to Cooperative 0 equity holders aportion of the total equities of Cooperative 0 notalready allocated. Total Cooperative 0 equitydivided by allocated Cooperative 0 equity had toequal total Cooperative P equity divided byCooperative P stock. This ratio was calculated:

Total Cooperative 0 equity Total Cooperative P equity

Allocated Cooperative 0 equity = Allocated Cooperative P stock

Thus, equal proportions of allocated equitiesof Cooperative 0 and Cooperative P to total equi-ties of Cooperative 0 and Cooperative P werebrought into the consolidation. BecauseCooperative O’s ratio was larger than CooperativeP’s, some of Cooperative O’s unallocated equitywas allocated to its members to make the ratiossimilar.

Table 9 shows this procedure. In the example,

the allocated equity to total equity ratios are notequal. Cooperative O’s ratio is 1.25 whileCooperative P’s is 1.22. To make the ratios equal,$27,400 of Cooperative 0 unallocated equity istransferred to Cooperative 0 allocated equity. Theequities were allocated to members’ allocated equi-ty accounts on a basis similar to that of the mem-bers’ original equity allocations made over the 5-year period immediately preceding the effectiveconsolidation date.

The equities of Cooperative 0 membersbrought into the merger were then converted topreferred stock of the unified cooperative. Eachdollar of equity was converted to one share of pre-ferred stock (par value $1).

Each share of preferred stock (par value $1)held by the members of Cooperative P was convert-ed to a similar share with the unified cooperative.The same procedure was followed for preferredstock A of Cooperative P.

Remaining unallocated equities of Cooperative0 and Cooperative P became a part of the unifiedcooperative’s unallocated reserve to be unallocated,permanent capital.

After consolidation, the equity capital struc-ture of the unified cooperative consisted of capitalstock-shares of common stock (par value of $10)designating membership and voting rights, andpreferred stock A and preferred stock-two classes

T&I~ 4- Case study I, member equity transfer of Cooperative 0 and Cooperative PI

Prior to merger At mergeP

co-op 0 coop P ~OpO co-op P Unifii Co-op

DOliflrS

Allocated equity3 1.055,oOO 787,200 1,082,400 787,200 1,869,OOO

Unallocated equity 265 ,000 172,800 237 ,600 172,800 410 ,400

Total equity 1,320,OOO 960,000 1,320,000 960 ,000 2,280,OOO

Ratio 41.25 1.22 1.22 1.22 1.22

1 Numbers are hypothetical, for example purposes. Assumptions: total equity to total assets = 60 percent and for Cooperative P unallocatedequity to total equity = 18 percent and unallocated equity to total assets = 11 percent.