1 COOPETITION IN ASEAN A study exploring the possibility of Coopetition in the Telecommunications Industry in ASEAN (ABS Learning Team Project) LT B 11 Bhatia, Ananta Chandra, Kislay Eufemio, Jose Carlo Govindarajan, Santosh Pangalilingan, Diana Shirolkar, Sagar

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

COOPETITION IN ASEAN A study exploring the possibility of Coopetition in the Telecommunications Industry in ASEAN

(ABS Learning Team Project)

LT B 11

Bhatia, Ananta

Chandra, Kislay

Eufemio, Jose Carlo

Govindarajan, Santosh

Pangalilingan, Diana

Shirolkar, Sagar

2

Introduction

The objective of this study is to explore the possibility of Coopetition between the leading players of the Telecommunication industry in the ASEAN region. Coopetition is a business strategy based on a combination of cooperation and competition, derived from an understanding that business competitors can benefit when they work together. In highly segmented industries with strong network effects, such as the information technology industry, cooperation and competition, or Coopetition, may be the only way to conduct business. Because of strong network effects it is often difficult in the information technology industry to get new products off the ground. In addition, the market demands more and more interoperability and this requires technical standards. However, the establishment of technical standards by competitive market forces in and of themselves is usually a rocky road. Frequently, it leads many incipient companies down the road to bankruptcy and established companies down the road of product abandonment before their contributions can get any wind in their sails. Many years of fruitless, cutthroat competition in which no clear winner emerges inhibits the overall health of the market, in terms of company profitability and in terms of interoperability and high customer investments which often become stranded once a clear winner does emerge. New strategies are needed to avoid this undesirable situation. Coopetition, which has its theoretical foundations in game theory, does just that.

The companies we are focusing on to are SingTel from Singapore and Smart Communications from the Philippines. SingTel and Smart Telecom could initiate collaboration to lead the effort for the following:

1. To create ASEAN wide telecom infrastructure sharing to reduce their capital investment and operational costs and thus offer cheaper telecom services

2. To create a common standard for mPayment (mobile payment) across ASEAN which would facilitate inter operator mobile financial transactions

Gradually, the other major telecom players from the ASEAN region could join this collaborative effort and push for an ASEAN wide implementation that benefits them all. The ASEAN Economic Council Blueprint calls for such a Coopetition among the various firms across the region to achieve a greater economic integration.

The ASEAN 2015 Vision

The ASEAN region was formed in 1967 to address political and security concerns. Due to the effects of globalization on cross border movement of goods, services, capital and labour, the emergence of China and India as economic powerhouses and the Asian financial crisis of 1997, economic integration became the focal point for ASEAN. In 2007, a goal was set to create the ASEAN Economic Council by 2015. The AEC would establish ASEAN as a single production base characterized by free flow of goods, services, investment, skilled labour and freer flow of capital. The following are the AEC areas of cooperation:

a) human resources development and capacity building b) recognition of professional qualifications c) closer consultation on macroeconomic and financial policies d) trade financing measures; enhanced infrastructure and communications connectivity

3

e) development of electronic transactions through e-ASEAN f) integrating industries across the region to promote regional sourcing g) enhancing private sector involvement for the building of the AEC

Specifically, for the Telecommunications industry, the following pieces from the AEC Blueprint is the most relevant:

Information Infrastructure Development: Efforts have been made to facilitate interconnectivity and technical interoperability among ICT systems, leveraging an existing national networks and evolving these into a regional information infrastructure. Equal emphasis has been given in improving trust and confidence in the use of the internet and security of electronic transactions, payment and settlements

The proposed actions to achieve the aforementioned are as follows:

i. Facilitate high-speed connection among all national information infrastructure by 2010 and implement ICT measures as identified in the VAP;

ii. Intensify capacity building and training programmes for national Computer Emergency Response Teams (CERTs) and strengthen its capacity, cooperation and the coverage of the region’s cyber-security network, including expanding the ASEAN CERT Incident Drills to include ASEAN’s Dialogue Partners in 2007;

iii. Encourage the participation of all stakeholders (people, communities, enterprises and public administrations) in utilisation and development of ICT applications and services on the regional information infrastructure;

iv. Support sectoral ICT applications (initially in key sectors such as customs, logistics, transport, content industry) to improve their effectiveness and productivity;

v. Expand the number of ASEAN countries participating in the ASEAN MRA for telecommunications equipment; and

vi. Deepen regional policy and regulatory framework to deal with the opportunities and challenges in the area of Next Generation Networks, including the interoperability of

E-Commerce: To lay policy and legal infrastructure for electronic commerce and enable on-line trade in goods with ASEAN through the implementation of the e-ASEAN Framework Agreement based on common reference frameworks.

The proposed actions to achieve the aforementioned are as follows:

i. Adopt best practices in implementing telecommunications competition policies and fostering the preparation of domestic legislation on e-commerce;

ii. Harmonise the legal infrastructure for electronic contracting and dispute resolution; iii. Develop and implement better practice guidelines for electronic contracting, guiding

principles for online dispute resolution services, and mutual recognition framework for digital signatures in ASEAN;

iv. Facilitate mutual recognition of digital signatures in ASEAN; v. Study and encourage the adoption of the best practices and guidelines of regulations

and/or standards based on a common framework; and

4

vi. Establish a networking forum between the businesses in ASEAN and its Dialogue Partners as a platform for promoting trade and investment.

The proposed actions to be taken for realizing the ASEAN 2015 vision pertaining to ICT reveals that ICT companies being one of the key stakeholders must lead the effort and they would be supported by governmental bodies of the member states and ASEAN.

The Telecommunications Industry

The telecommunications Industry in the ASEAN region is worth around 50 billion USD. The telecom industries of the nations of Cambodia, Laos, Myanmar and Brunei are tiny compared to the other six and have a much smaller share of the overall market (Refer to exhibit 1).

The following are some of the key issues faced by the Telecommunications industry today:

1. Growth and Profitability problem: The telecommunications industry, after reaching a certain teledensity, faces the issues of growth and profitability. Say, a nation has a mobile penetration level of 106%, which means that the number of mobile connections per capita has already exceeded one. Not to mention that a plain vanilla mobile connection has become a commodity of sorts. Therefore, the operators need to think of new areas for achieving growth and staying profitable. Solution: The telecom operators have come up ingenious ideas to provide value added services to customers to increase their revenues and profitability. One such service is mobile payment. Mobile payment, also referred to as mobile money, mobile money transfer, and mobile wallet generally refer to payment services operated under financial regulation and performed from or via a mobile device. Instead of paying with cash, check, or credit cards, a consumer can use a mobile phone to pay for a wide range of services and digital or hard goods. Although the concept of using non-coin-based currency systems has a long history, it is only recently that the technology to support such systems has become widely available. In developing countries mobile payment solutions have been deployed as a means of extending financial services to the community known as the "unbanked" or "underbanked," which is estimated to be as much as 50% of the world's adult population, according to Financial Access' 2009 Report "Half the World is Unbanked". These payment networks are often used for micropayments. The use of mobile payments in developing countries has attracted public and private funding by organizations such as the Bill and Melinda Gates Foundation, USAID and Mercy Corps. But one of the major problems with mobile payment is the lack of a common standard across the telecom operators of the region, user readiness and infrastructure development. As of now the mPayment services are restricted to urban areas only and not all handsets support mPayment service. Unless the mPayment system is truly interoperable, it will never reach its full potential. Imagine the lack of interoperability between banks which would result in non exchange of funds between 2 competing banks. In such a case, the banking industry as a whole would fail to provide us with the benefit of easily carrying out financial transactions. In order to create an

5

acceptable standard of mobile payment that would allow inter operator mobile financial transactions, the major telecom operators would have collaborate. Telcos should plug into an ecosystem of partners rather than going it alone. Access to regulatory insights, market expertise, and speed to market far outweigh concerns about dividing up the potential revenue pie or user base. It is a situation which clearly demands Coopetition, collaborate before you compete. Capital Expenditure Problem: As traffic over both wireless and fixed networks continue to grow at an explosive rate, Telco’s struggle to keep pace with the increasing demand. The investment in infrastructure cannot happen at the same pace as the increase in demand and instances of substandard network performance are more frequent. The nature of the underlying technology of the telecommunications industry is such that the equipment needs frequent upgrades. Most of the equipment needs to be upgraded before the investment is recovered by the firm. Given the competitiveness in the industry, it becomes imperative for firms to upgrade or lose out.

Solution: To counter the problem of the increased demand on telecom infrastructure and the frequent need for upgrades, telecom operators can resort to sharing of the infrastructure. In the telecom industry, the installation costs and the maintenance costs of its infrastructure form a major part of the costs of a telecom company. Infrastructure sharing is already prevalent in certain parts of the world. The degree and method of infrastructure sharing can vary in each country depending on regulatory and competitive climate. Sharing of infrastructure if a very good example of Coopetition as the major telecom companies who are competitors come together to reduce their fixed costs by sharing them and then compete for market share. The sharing of infrastructure allows companies to exercise economies of scale and save of their investment costs while avoiding duplication. Once the load of network deployment is take off the firm, it can focus on product innovation, improved customer service and better commercial offerings. The sharing of telecom infrastructure can also bring down the operating costs which can be passed on to customers.

6

Company Profiles SingTel Established in 1992, SingTel is an integrated domestic telecommunication service provider. SingTel is the leading domestic fixed, mobile and broad-band operator. SingTel was listed on the Singapore Stock Exchange in 1993 and is now the supplier of communications services in more than 20 countries. SingTel provides a wide range of services including national fixed-line services, mobile services (via SingTel Mobile), broad-band, IP and internet access, and international phone services. Also, SingTel operates ADSL network across the island and has four satellites earth station. SingTel has huge investment in strategic regional markets such as India, Indonesia, the Philippines, Thailand and Bangladesh. Singapore is still looking to invest in other potential markets in the region. All these investments are carried out by its international unit, SingTel International (STI), which accounts for over 50% of the group’s revenue. Temasek Holdings, the Singapore government’s investment arm is the dominant owner of SingTel with 56.3% of its stake. Smart Communications Established in 1991, Smart Communications is now the leading mobile operator with 36.9 million subscribers as of March 2009, accounting for 52% of market share. Smart Communications is a wholly owned subsidiary of PLDT. It has a GMS network with 8,678 base stations (March 2009) covering 99% of the population. The network also supports Piltel’s prepaid GMS service Talk N Text, and acquired CURE, a wireless start-up company. Smart Communications is one of the four 3G service providers in the Philippines. Services include TV streaming, music and video clip downloads and video calling. It reported in 2006 that it had 350,000 3G users. Smart Communications also provides a wide range of mobile and wireless broad-band services. ASEAN Integration and the Telecommunications Industry

The imminent economic integration of the ASEAN region has opened up the doors to new opportunities for the Telecommunications Industry in a huge way. Essentially, the goal of the ASEAN integration is to create a stronger, unified economic region and raise the quality of life of the 600 million ASEAN citizens. The ICT Industry has and will continue to play a pivotal role in the accomplishment of this goal. Research has shown that a 10% increase in broadband penetration boosts GDP by an average of 1.3% and a 10% increase in teledensity results in 0.7% increase in GDP. Case studies illustrate the potential savings in different markets: In India, for example, an estimated 240,000 towers are needed over the next three years. Analysis indicates that capital expenditure savings could reach US$4 billion if operators achieve double tenancy on deployed sites by 2010.In one Middle Eastern example, two competing operators require an average of 3,500 towers each to achieve optimal coverage. Should they decide to share 50 percent of their towers, they could reach Capex savings in the range of US$250 million over the next three years. Finally, in one fixed-network sharing case, multiple cost components would be affected and optimized if two or more operators share their network. Set-up costs could be reduced by as much as 40 percent, and utilization costs could be reduced by 20 percent. Imagine

7

the impact of such kind of savings on the overall economic growth of a region where capital is not that easy to come by. The importance of Telecommunications to realize the ASEAN vision cannot be overstated. Telecommunication infrastructure sharing could accelerate the rate at which mobile and internet access increases across the ASEAN region while making it cheaper at the same time. The multi-ethnic, multicultural and varied socioeconomic make-up of the ASEAN region provides varied mPayment opportunities to businesses. Businesses involved in the m-payment sector, whether through the provision of m-payment platforms or the sale of goods and services that are available for purchase via mobile transactions, can find a range of mobile consumers across ASEAN, with the region home to over 500 million mobile phone subscribers. Mobile money transfer services have especially caught on in countries with large migrant worker populations, with India, Malaysia and Indonesia some of the leading regional markets in this regard. Businesses able to offer person-to-person transfers and remittances services can unlock value among large populations, with the combined value of remittances inflows of these three countries amounting to US$71.1 billion in 2011. Countries with large rural populations also offer businesses rapid growth in the take-up of m-payments, as banking and fixed telecom services are typically highly skewed in favour of urban residents. Countries such as China, India and the Philippines with especially large rural populaces can drive demand for mobile transactions that substitute the lack of localised services. In general, the benefits of m-payments are considerable. Mobile operators increase their added-value revenues through new commercial offerings; banks reduce cash-handling and labour costs, while retailers accelerate transaction times and therefore push through more sales of goods and services. According to trade sources, global m-payment transaction value will surpass US$172 billion in 2012. Therefore, mPayment standardization efforts taken by two leading players such as SingTel and Smart would further the cause of ASEAN Economic Integration. Environment Analysis of ASEAN

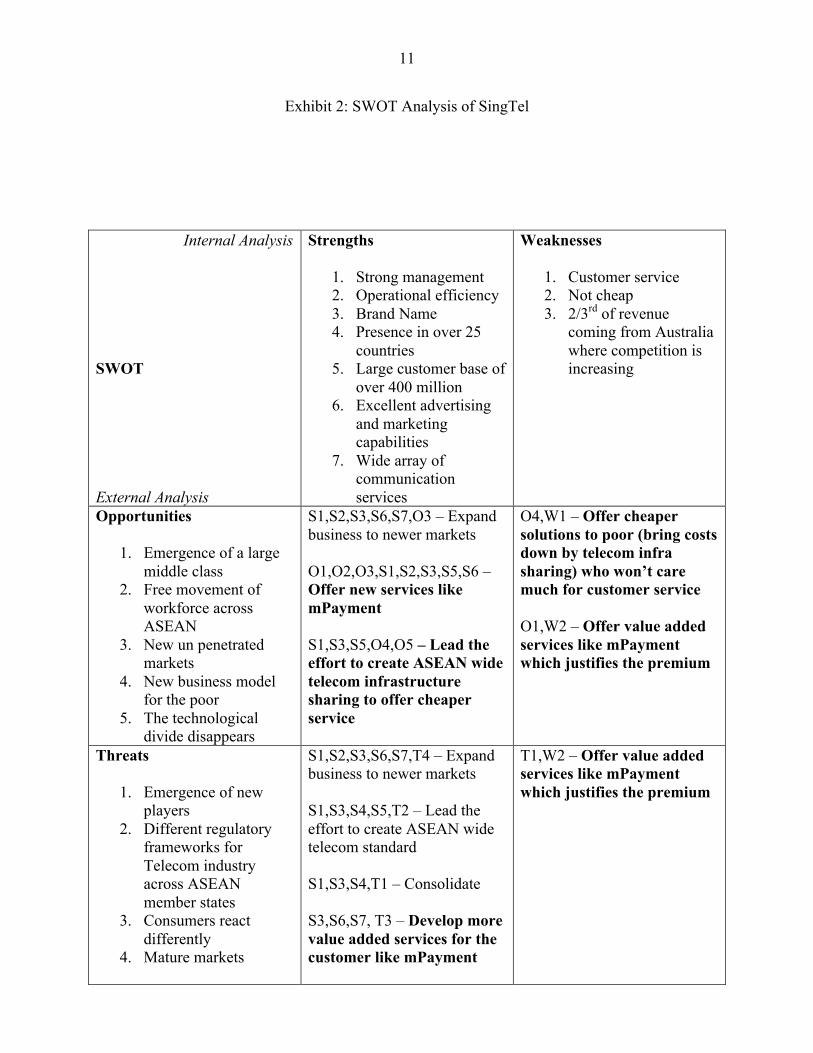

We conducted a SWOT of SingTel and Smart communications and a PESETL analysis of the ASEA region to assess how feasible our proposal is.

Please refer to exhibits 2 and 3 for a SWOT analysis of SingTel and Smart. The strategic options that emerge from SWOT reveal that the collaboration for telecom infrastructure sharing and implementing a common mPayment standard would be a judicious choice for the firms to sustain long term growth and contribute towards the ASEAN economic integration.

The following is a PESTEL analysis to assess whether the environment is favourable for the two companies, SingTel and Smart to collaborate and eventually compete.

1. POLITICAL a. With the exception of Singapore, the other ASEAN nations are marred by

corruption to varying degrees b. There is an increasing solidarity among the ASEAN member states for achieving

the challenging task of ASEAN economic integration c. The region has ties to India, a nation with a very well developed ICT Industry

which has already benefited from telecom infrastructure sharing and is experimenting with mPayment from which cooperation can be sought.

8

2. ECONOMIC a. The regulations(pertaining to mPayment and telecom infrastructure sharing) are

country specific b. There is no single point of ASEAN information c. The ASEAN region is economically disparate. Singapore is a developed nation;

Thailand, Philippines, Indonesia, Brunei, Malaysia and Vietnam are developing economies while Cambodia, Laos and Myanmar are the least developed of them all.

d. The region is home to the most promising countries from an economic growth perspective and is witnessing an increase in the middle class population

3. SOCIAL a. The region does not have a common language or culture which makes

collaboration challenging b. There is an increase in usage of mobile devices c. There is a need for services for the unbanked (mPayment) d. There is a need for a new business model for the poor, the bottom of the pyramid

4. TECHNOLOGICAL a. The region is home to some of the top players in the ICT Industry in Asia b. The technological divide is narrowing as communications technology gets

cheaper and more accessible 5. ENVIRONMENTAL

a. The ASEAN region is committed to sustainable and environment friendly development. Telecom infrastructure sharing will reduce the energy consumption and increase asset utilization as resources are shared, thus is more eco friendly.

6. LEGAL a. The country regulations are not aligned to ASEAN roadmaps b. There is no ASEAN court of justice or any such supranational organization to

settle disputes amongst the ASEAN member states

The PESTEL analysis reveals that while certain factors favour collaboration amongst telecommunication companies in different ASEAN nations, certain others make the task challenging. However, the overall climate seems to be conducive given that the economic integration of the region is important and the nations are working towards achieving that goal.

The Coopetition Framework

We have established the grounds for Coopetition between the two firms. The following diagram outlines the value net for the two firms. The same value net is applicable to both the firms because they are from the same industry.

The following shows the application of the P.A.R.T.S. framework (the framework proposed by Branderburger and Nalebuff):

1. Players: The following are the players involved: a. Company

i. Telecom companies such as SingTel and Smart Communications b. Customers

i. The existing and potential customers of the telecom companies

9

c. Suppliers i. The suppliers of telecom equipment

ii. The suppliers of mobile POS systems d. Substitutors

i. Non mobile communication devices ii. Cash and credit card

e. Complementors i. Mobile device manufacturers like Samsung, Nokia etc.

ii. Mobile OS designers like Google, Apple etc.

2. Added Value: Added values are what each player brings to the table. SingTel and Smart

both are leading providers of telecom services. Individually, they are strong contenders. But, if they collaborate on telecom infrastructure sharing and mPayment standardization, they would increase the overall value of all the players involved and not just their own. It would make the industry more cost efficient and open up new revenue streams.

3. Rules: As of now, each player has been individually upgrading and expanding its infrastructure network. The rule has been to play on your own. Similarly, Telcos have come up with their own mPayment system which customers can use to transact but only within their network and subscriber base. The existing rules in the marketplace limit the benefits everyone can enjoy from the game. Infrastructure sharing promises to bring down the operational costs and Capex requirements for all players. A service like mPayment needs the network effect working in its favour for it to become widespread

SingTel(&(Smart(Communica2ons(

Customers(

Mobile(device(manufacturers,(Mobile(OS(designers,(App(designers(&(sellers,(

Financial(Ins2tu2ons(Retail(Stores(for(Mpayment(

Suppliers:(Telecom(equipment(vendors(and(landowners,(

mobile(POS(prviders(

Subs2tutors(:(Non(mobile(communica2on(devices,(Cash(and(credit(card(((mPayment)(

10

and popular. Collaboration effectively changes the rules of the game as having a wider network or your own standard of mPayment will not guarantee success.

4. Tactics: Tactics influence the way players perceive the uncertainty and thus mould their behaviour. The proposed collaboration requires an unprecedented level of cooperation among the firms. Firms like SingTel and Smart will have to lift the fog that shrouds telecom infrastructure sharing and mPayment standardization. They will have to demonstrate to each other and other potential stakeholders about the long term benefits of collaboration. Given the complexity of the exercise, it is imperative that the benefits such as decrease in operational costs and capital investment and the potential increase in revenues through mPayment transactions are clearly visible and measurable to all, thereby encouraging more players to join the effort.

5. Scope: Telecom infrastructure sharing essentially involves the vertical disintegration of the firms such that the business pertaining to network management is carved out and many such units are consolidated together as a one unified region wide network management company. This move will create a greater economy of scale for the newly formed entity. Introduction of mPayment standardization promises to broaden the scope of the firms by increasing their share of revenues from this part of their business. The network infrastructure linkage is being removed from the game while mPayment linkage as a value added service is being expanded. As the scope of the telecom firms shrink vertically but increase horizontally, the scope of the game changes.

Exhibit 1: Total Telecommunications Market (2011): US$48.93 Billion (Mobile and Fixed Services Voice and Data Revenue)

11

Exhibit 2: SWOT Analysis of SingTel

Internal Analysis SWOT External Analysis

Strengths

1. Strong management 2. Operational efficiency 3. Brand Name 4. Presence in over 25

countries 5. Large customer base of

over 400 million 6. Excellent advertising

and marketing capabilities

7. Wide array of communication services

Weaknesses

1. Customer service 2. Not cheap 3. 2/3rd of revenue

coming from Australia where competition is increasing

Opportunities

1. Emergence of a large middle class

2. Free movement of workforce across ASEAN

3. New un penetrated markets

4. New business model for the poor

5. The technological divide disappears

S1,S2,S3,S6,S7,O3 – Expand business to newer markets O1,O2,O3,S1,S2,S3,S5,S6 – Offer new services like mPayment S1,S3,S5,O4,O5 – Lead the effort to create ASEAN wide telecom infrastructure sharing to offer cheaper service

O4,W1 – Offer cheaper solutions to poor (bring costs down by telecom infra sharing) who won’t care much for customer service O1,W2 – Offer value added services like mPayment which justifies the premium

Threats

1. Emergence of new players

2. Different regulatory frameworks for Telecom industry across ASEAN member states

3. Consumers react differently

4. Mature markets

S1,S2,S3,S6,S7,T4 – Expand business to newer markets S1,S3,S4,S5,T2 – Lead the effort to create ASEAN wide telecom standard S1,S3,S4,T1 – Consolidate S3,S6,S7, T3 – Develop more value added services for the customer like mPayment

T1,W2 – Offer value added services like mPayment which justifies the premium

12

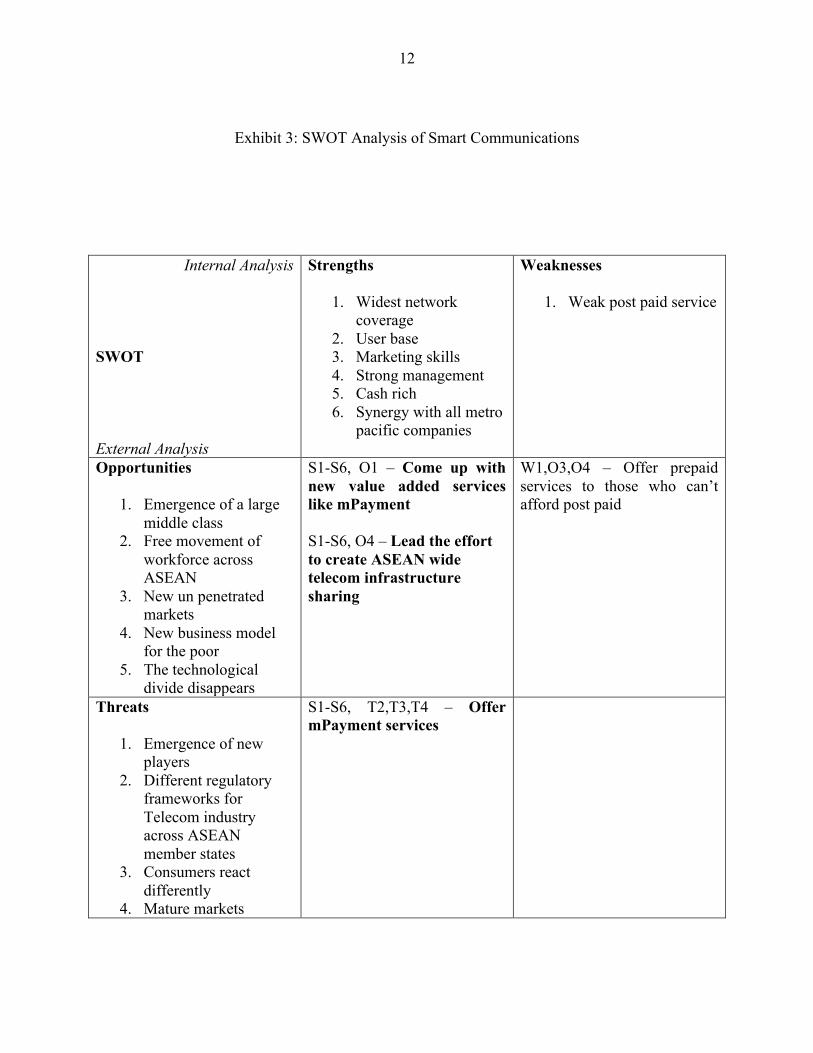

Exhibit 3: SWOT Analysis of Smart Communications

Internal Analysis SWOT External Analysis

Strengths

1. Widest network coverage

2. User base 3. Marketing skills 4. Strong management 5. Cash rich 6. Synergy with all metro

pacific companies

Weaknesses

1. Weak post paid service

Opportunities

1. Emergence of a large middle class

2. Free movement of workforce across ASEAN

3. New un penetrated markets

4. New business model for the poor

5. The technological divide disappears

S1-S6, O1 – Come up with new value added services like mPayment S1-S6, O4 – Lead the effort to create ASEAN wide telecom infrastructure sharing

W1,O3,O4 – Offer prepaid services to those who can’t afford post paid

Threats

1. Emergence of new players

2. Different regulatory frameworks for Telecom industry across ASEAN member states

3. Consumers react differently

4. Mature markets

S1-S6, T2,T3,T4 – Offer mPayment services

13

Telecom Infrastructure Sharing: Proof of concept

In the telecom industry, the installation costs and the maintenance costs of its infrastructure form a major part of the costs. Infrastructure sharing is already prevalent in certain parts of the world. The degree and method of infrastructure sharing can vary in each country depending on regulatory and competitive climate. Sharing of infrastructure if a very good example of Coopetition as the major telecom companies who are competitors come together to reduce their fixed costs by sharing them and then compete for market share. The sharing of infrastructure allows companies to exercise economies of scale and save of their investment costs while avoiding duplication.

This practice of infrastructure sharing is something that will benefit the ASEAN if implemented. It will be the best possible example of Coopetition. Instead of individually bearing the costs of the humongous infrastructure and trying to recover it from operations. Companies could decide to share the infrastructure. One way of doing it would be a company bearing the initial costs and then the other pay it on usage basis. The other would be to find a third party who would set up this infrastructure and charge the telecom companies that would pay on usage. The companies could also decide to share the costs of infrastructure and then utilize the infrastructure to compete with each other.

This option has been tried in India in 2007 and has been successfully in place since then. A company called Indus towers was set up by 3 major stake holders Vodafone Group (42%), Bharti Infratel (42%) and Aditya Birla Group (16%). These three telecom players pooled in the resources to set up this company that was incorporated and had a separate management. The job of this company was to set up passive infrastructure across the country. This infrastructure would be shared by these telecom companies in their day to day operations . This is the best example of Coopetition as the companies first come together to set up the basic infrastructure and then compete with each other for market share and profit.

Indus Towers owns 1,09,539 mobile phone towers across 15 circles out of the 22 telecom circles of India. The basic purpose of the company is to provide shared telecom infrastructure to the founding companies and provide scale benefits to these companies in the process. Indus towers, earns its profits by charging members for tower infrastructure usage. Despite lack of complementary capabilities this alliance is sustainable.

The main reason for this model to work in India are:

• Better Return on investments through increased efficiency

• Favorable environment

14

• Shared Risks

The shared risks is another major reason why this arrangement makes sense for these companies.

The analysis of this arrangement of Indus is as follows :

Strengths - Reduced operating costs and capital expenditure - Enhanced value creation for all partners - Reduced financial and political risk - Raised barriers of market entry to the new players - Existing distribution and sales networks -Crisis handling with co-operation

Weaknesses - Huge investments in research and development - Challenges faced in rural set-up

- Increased pollution and radiations - Network coverage no more a competitive advantage for any partner

Opportunities - Access to global markets & the growing demand - Growth rates and profitability - New acquisitions - Faster access to the rural markets - Financial support by the Government to set up towers -Growth in wireless subscriber base & tele-density

Threats - Potential conflicts in the corporate objectives of the partners - Failure to adhere to international standards of emission attracts retaliation from the environmentalists

The Road Ahead for Indus :

• Mobile Phone Operators were concerned with operational performance and strove to maximize tower ownership, preferred being self-dependent as far as rollouts were concerned

• Tower Operators: Endeavoured to improve tower tenancy which determined their success. Also they required skills to manage multiple customers

• Key Challenge : Reconciliation of completely differing mindset of mobile phone operators and tower operators.

15

Modified Redding Framework:

A modified Redding framework of coordination-order-meaning accounts for the ASEAN factors in firm-level structures and systems for coordinating and exchange, institutions, and culture. This will highlight the main factors that will decide whether coopetition and alliances will work.

Culture –

To explain the culture similarities and differences in two selected countries / companies, we used Hofstede’s theory of cultural dimensions and GLOBE (Global Leadership and Organizational Behaviour Effectiveness). (Source: http://geert-hofstede.com/countries.html)

16

Hofstede’s theory of cultural dimensions –

Hofstede’s theory measures degree of similarity / difference within countries on five dimensions

I. Power distance (PDI) – “This dimension expresses the degree to which the less powerful members of a society accept and expect that power is distributed unequally”. (Source: http://geert-hofstede.com/countries.html). Higher score indicates more hierarchical culture; where as a low score indicates equality in power. From the power scores for Singapore and the Philippines, Philippines has more hierarchical culture.

II. Individualism versus collectivism (IDV) – The high side of this dimension, called Individualism, can be defined as a preference for a loosely-knit social framework in which individuals are expected to take care of themselves and their immediate families only. Its opposite, Collectivism, represents a preference for a tightly-knit framework in society in which individuals can expect their relatives or members of a particular in-group to look after them in exchange for unquestioning loyalty. Form the scores Singapore has more collectivism. (Source: http://geert-hofstede.com/countries.html)

III. Masculinity versus femininity (MAS) – “The masculinity side of this dimension represents a preference in society for achievement, heroism, assertiveness and material reward for success”. Society at large is more competitive. “Its opposite, femininity, stands for a preference for cooperation, modesty, caring for the weak and quality of life. Society at large is more consensus-oriented.” (Source: http://geert-hofstede.com/countries.html)

17

From the score, Filipinos are more individual performers where as Singaporeans take decision collectively. The score in MAS also confirms the PDI score.

IV. Uncertainty avoidance (UAI) –“The uncertainty avoidance dimension expresses the degree to which the members of a society feel uncomfortable with uncertainty and ambiguity. A higher score indicates more rigid and orthodox society; where as low score means a flexible society”. (Source: http://geert-hofstede.com/countries.html) From the score in UAI for both countries it is very clear that, Singaporeans are open for changes; whereas Filipinos do not like the changes.

V. Long-term versus short-term orientation (LTO) – “The long-term orientation dimension can be interpreted as dealing with society’s search for virtue. Societies with a short-term orientation generally have a strong concern with establishing the absolute Truth.” (Source: http://geert-hofstede.com/countries.html) From the scores, it is clear that the Singaporeans are more believe that truth depends very much on situation, context and time. They show an ability to adapt traditions to changed conditions, a strong propensity to save and invest thriftiness, and perseverance in achieving results.

The Global Leadership and Organizational Behaviour Effectiveness –

The Global Leadership and Organizational Behaviour Effectiveness Research Project (GLOBE) is an international group of social scientists and management scholars who study cross-cultural leadership. Based on similarities in cultural values and beliefs, GLOBE researchers have divided the participating societies into 10 cultural clusters. Each cluster is rated on six different styles of leadership scales as given below.

• The performance-oriented style (called "charismatic/value-based" by GLOBE) stresses high standards, decisiveness, and innovation; seeks to inspire people around a vision; creates a passion among them to perform; and does so by firmly holding on to core values. (Source: http://www.inspireimagineinnovate.com/PDF/GLOBEsummary-by-Michael-H-Hoppe.pdf)

• The team-oriented style instills pride, loyalty, and collaboration among organizational members; and highly values team cohesiveness and a common purpose or goals. (Source: http://www.inspireimagineinnovate.com/PDF/GLOBEsummary-by-Michael-H-Hoppe.pdf)

• The participative style encourages input from others in decision-making and implementation; and emphasizes delegation and equality. (Source: http://www.inspireimagineinnovate.com/PDF/GLOBEsummary-by-Michael-H-Hoppe.pdf)

• The humane style stresses compassion and generosity; and it is patient, supportive, and concerned with the well-being of others. (Source:

18

http://www.inspireimagineinnovate.com/PDF/GLOBEsummary-by-Michael-H-Hoppe.pdf)

• The autonomous style is characterized by an independent, individualistic, and self-centric approach to leadership. (Source: http://www.inspireimagineinnovate.com/PDF/GLOBEsummary-by-Michael-H-Hoppe.pdf)

• The self-protective (and group-protective) style emphasizes procedural, status-conscious, and 'face-saving' behaviours; and focuses on the safety and security of the individual and the group. (Source: http://www.inspireimagineinnovate.com/PDF/GLOBEsummary-by-Michael-H-Hoppe.pdf)

Singapore falls under the CONFUCIAN ASIA cluster while Philippines falls under the SOUTHERN ASIA cluster.

CONFUCIAN ASIA CLUSTER –High on in group collectivism, institutional collectivism and performance orientation

SOUTHERN ASIA CLUSTER – High on Humane orientation and in group collectivism

Order –

1. Financial Capital

• Financial Capital (Philippines) – The main sources of capital are relatives and friends. The banks are only secondary due to their tighter credit policies and volatile interest rates. There are also a few major banks and even fewer that can grant a lot of loans.

• Financial Capital (Singapore) - Angel investment is a significant source of capital. In fact, Singapore offers tax investment schemes for private investors. Singapore accounted for 52% of all private equity investments in Southeast Asia. Singapore is the financial hub in Southeast Asia being home to almost all the large banks in the world.

2. Human Capital –

• Singapore - Human Capital in Singapore is concentrated in managerial levels.

19

(source:)

20

• Philippines – Laborers and unskilled workers comprise about one-third of the total employed population.

Trust : -

Singapore -

• Based on a survey conducted by Straits Times, Singapore had the highest trust in government of any country in the world with 72% of the respondents having a high trust rating on the country’s institutions.

• Only 19 per cent of respondents said they trusted business leaders to tell the truth in a difficult situation compared to the 60 per cent of those who trusted businesses overall. Similarly, only 23 per cent of the Singaporeans polled said they trusted government leaders to tell the truth, versus the 72 per cent who said they trusted the Government to do what is right as an institution.

• "Individual leaders are not getting the credit for the stability and strength of their institutions, which are perhaps already deemed stable, but do take the blame when things go wrong,"

21

Philippines –

• Church is the most trustworthy Philippine Institution, business least trustworthy in the Philippines

• For the Church to keep the people's trust, respondents said it has to provide spiritual guidance, be a role model of holiness, and maintain its separation from the state

• According to the survey, how business treats its internal stakeholders is the most important driver of trust. Providing fair wages and salaries was ranked the highest concern by all respondents, followed by offering quality but fairly priced products, showing concern for society, and paying proper taxes.

Coordination:

The Singaporeans are high on uncertainty avoidance and are long term oriented. Being a developed country, they have all their basic needs satisfied and have a higher per capita. The country is high on in group collectivism, institutional collectivism. The country is very performance oriented. These traits of the workforce combined with the abundant educated human capital and financial capital makes Singapore a great ally. In all the country is a completely developed and has technologically advanced business systems. On the down side that fact that the country is small and this well developed means that the country does not have the luxury of cheap workforce and labor also is low on humane orientation.

On the other hand a country like Philippines is high on PDI. The Power distance is the extent to which the less powerful members of organizations and institutions (like the family) accept and expect that power is distributed unequally." Cultures that endorse low power distance expect and accept power relations that are more consultative or democratic. This country is high on MAS but has moderate educated human capital and financial capital.

The implementation of the proposed idea is going to be quite a task and given the state the region is in right now, it would be wise to gradually increase the effort and number of involved players. There will be resistance to change from virtually all stakeholders. The firms will face their own organizations, the competitors, the regulators and other governmental bodies. To begin with, the telecom industry players from the nations of Singapore, Philippines, Malaysia and Indonesia should start coopeting. A study conducted by SGE (Singapore Entrepreneurs) reveals that Singapore and the Philippines top Southeast Asia in terms of mobile payment readiness and therefore collaboration between the leading telecom operators of these nations would be the best foot forward to achieve mPayment standardization and telecom infrastructure sharing. The other nations should join at a later date, when the idea has materialized into something concrete. In order to achieve the ASEAN vision, it is incredibly important that the leading firms in the region take the initiative to create a region wide platform for cooperation. The essence of Coopetition is to think win-win and not win-lose. If SingTel and Smart lead effort

22

for infrastructure sharing and mPayment standardization, they will be changing the Telecom game for the greater good.

These countries complement each other perfectly. What one of them lacks is in abundance in the other. Coordination of these two nations in various fields like telecom will work positively for both the nations.

23

Sources and References

Web Articles

1. http://www.booz.com/global/home/what-we-think/industry-perspectives/display/2013-telecommunications-industry-perspective?pg=all

2. http://en.wikipedia.org/wiki/Telecom_infrastructure_sharing 3. http://www.asean.org/news/asean-secretariat-news/item/12th-asean-ministerial-meeting-

on-the-environment-and-8th-meeting-of-the-conference-of-the-parties-to-the-asean-agreement-on-transboundary-haze-pollution

4. http://www.asean.org/ 5. http://www.bharti-infratel.com/cps-portal/web/benefits.html 6. http://www.cio-asia.com/blogs/featured-blogs/blog-making-mobile-payments-pay-off-in-

asia/ 7. http://en.wikipedia.org/wiki/Mobile_payment 8. sgentrepreneurs.com/2012/05/10/singapore-tops-mobile-payments-readiness-index-

philippines-second-in-southeast-asia/ 9. www.wikipedia.com/Indiantelecom 10. Strategic alliances on telecom infrastructure- Article times of India.

Papers and Industry Reports

1. Top ten risks in telecommunications 2012 by Ernst and Young 2. TELECOMMUNICATION SECTOR IN ASEAN: “ASEAN ECONOMIC

INTEGRATION AND ITS IMPLICATIONS FOR LABOUR IN THE REGION” by Steven Truong Trong Vu (National University of Singapore, NUS)

3. Regional Focus: Asia Pacific Home to a Large Mobile Payments Market - Euromonitor International 02 January 2013

4. Telecom Infrastructure Sharing - Regulatory Enablers and Economic Benefits – Booze & Co.

5. World Economic Forum – Global Information Technology Report 2013 6. The right game – Using game theory to shape strategy by Brandenburger and Nalebuff 7. The socio-economic impact of mobile financial services – the BCG Group 8. The IMD Competitiveness Roadmap: 2012-2050 9. ASEAN Economy Community Blueprint – ASEAN 10. ASEAN ICT Master Plan – TELMIN (ASEAN) 11. Mobile communication and the impact on economic development by Harald Gruber and

Pantelis Koutroumpis

Books

1. Economics of Strategy by David Besanko, David Dranove, Mark Shanley and Scott Schaefer

Related Documents