A Tale of Two Countries: Sovereign Default, Trade, and Terms of Trade Grace W. Gu * August 3, 2015 (click here for the latest version) Abstract Sovereign defaults are associated with income and trade reductions and terms- of-trade deterioration. This paper develops a two-country model to study the inter- actions between foreign-debt default risk, income, trade, and terms of trade. Debt crises are costly because they adversely affect the vertical integration of production between the creditor and the borrower. Consequently, trade flows change due to income losses and home bias in consumption. The defaulter’s terms of trade also deteriorate endogenously, which accelerates its income and trade losses. The model produces procyclical imports, exports, and terms of trade, and other empirical fea- tures of Mexicos business cycles and default episodes. Keywords: sovereign default, terms of trade, real exchange rate, trade, DSGE. JEL code: F34 - F41 - F44 * Gu: Department of Economics, UC Santa Cruz, Engineering 2 Building, Room 463, Santa Cruz, CA 95060, [email protected]. I thank Laura Alfaro, Yan Bai, Paul Bergin, George Bulman, Michael Dooley, Fabio Ghironi, Michael Hutchinson, Ken Kasa, Ken Kletzer, Huiyu Li, Eswar Prasad, Katheryn Russ, Ina Simonovska, Alan Spearot, Viktor Tsyrennikov, Carl Walsh, Beiling Yan, Vivian Yue, as well as many others, for their incredibly helpful discussions. This paper has also benefited from comments from conference/seminar participants at Cornell, AEA-Boston, UC Davis, UC Riverside, UC Santa Barbara, UC Santa Cruz, Santa Clara Univ, Atlanta Fed, Peking Univ, Tsinghua Univ, San Francisco Fed, and NBER Summer Institute.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A Tale of Two Countries:

Sovereign Default, Trade, and Terms of Trade

Grace W. Gu∗

August 3, 2015

(click here for the latest version)

Abstract

Sovereign defaults are associated with income and trade reductions and terms-

of-trade deterioration. This paper develops a two-country model to study the inter-

actions between foreign-debt default risk, income, trade, and terms of trade. Debt

crises are costly because they adversely affect the vertical integration of production

between the creditor and the borrower. Consequently, trade flows change due to

income losses and home bias in consumption. The defaulter’s terms of trade also

deteriorate endogenously, which accelerates its income and trade losses. The model

produces procyclical imports, exports, and terms of trade, and other empirical fea-

tures of Mexicos business cycles and default episodes.

Keywords: sovereign default, terms of trade, real exchange rate, trade, DSGE.

JEL code: F34 - F41 - F44

∗Gu: Department of Economics, UC Santa Cruz, Engineering 2 Building, Room 463, Santa Cruz, CA95060, [email protected]. I thank Laura Alfaro, Yan Bai, Paul Bergin, George Bulman, Michael Dooley,Fabio Ghironi, Michael Hutchinson, Ken Kasa, Ken Kletzer, Huiyu Li, Eswar Prasad, Katheryn Russ,Ina Simonovska, Alan Spearot, Viktor Tsyrennikov, Carl Walsh, Beiling Yan, Vivian Yue, as well asmany others, for their incredibly helpful discussions. This paper has also benefited from comments fromconference/seminar participants at Cornell, AEA-Boston, UC Davis, UC Riverside, UC Santa Barbara,UC Santa Cruz, Santa Clara Univ, Atlanta Fed, Peking Univ, Tsinghua Univ, San Francisco Fed, andNBER Summer Institute.

1 Introduction

Sovereign debt default events are associated with three empirical regularities: (a) deep

recessions, (b) a decline in international goods trade, and (c) deteriorating terms of trade

and real exchange rates. Recent evidence shows that, across countries, default episodes

have on average been accompanied by a GDP drop of 5 percent below trend, a bilateral

trade value decline of 8 percent, and real depreciation of 30-50 percent.1 However, these

three phenomena have not been addressed simultaneously by existing sovereign default

models. This paper fills the gap by studying how foreign-debt default risk and occurrences

endogenously interact with income, terms-of-trade, and international goods trade through

production vertical integration in a two-country DSGE model.2

The model features four key elements. First, the model has default risk and occur-

rences (as in Eaton and Gersovitz, 1981; Aguiar and Gopinath, 2006; Arellano, 2008; and

Mendoza and Yue, 2012). The second key element is consumption home bias in both

countries. In the model, I show that as the borrower country’s default risk increases

with debt, its budget constraint tightens and its terms of trade deteriorate due to home

bias and reduced world relative demand for its final good. Deterioration in the terms

of trade prevents the borrower country from real appreciation that could have eased the

debt burden denominated in the creditor country’s final good. Thus, the default risk

increases further. In this way, the default risk interacts with the terms of trade and the

real exchange rate prior to a sovereign default.

The third key element of the model is vertical integration of production, where some

firms in the creditor country import an intermediate good from the borrower country to

produce a final good.3 The last key element of the model is a default penalty through the

vertical integration. When a large adverse productivity shock causes the borrower country

to default, the event triggers an efficiency loss in the creditor-country firms’ operations

regarding the intermediate good input from the defaulting country, which causes the

demand for the intermediate good to decline.

Empirical analyses indicate such efficiency loss exists. Specifically, this paper finds

that Canadian output was negatively affected by Mexican default events and the size of

1See Rose (2005), Cuadra and Sapriza (2006), Reinhart and Rogoff (2011), and Mendoza and Yue(2012).

2As illustrated in the model and result sections of this paper, the two-country model differs from asmall open economy model in offering unique insights about bond market equilibrium pricing and theimpact of a sovereign default on a creditor country’s income.

3Here the vertical integration is narrowly defined. It does not include activities where creditor countryfirms export an intermediate good to borrower country. Mendoza and Yue (2012) use this latter channelfor a default penalty.

1

the impact increases with an industry’s dependency on Mexican inputs. Moreover, the

efficiency loss in vertical integration is also consistent with other papers’ empirical findings

that foreign firms’ activities (e.g., FDI, offshoring, and other global sourcing) are more

severely damaged than domestic firms’ in a crisis country, possibly due to crisis-elevated

trade costs, information asymmetry, and risk aversion (e.g., Brennan and Cao, 1997; Tille

and van Wincoop, 2008; Milesi-Ferretti and Tille, 2010; and Broner, Didier, Erce, and

Schmukler, 2013).4

The decline in foreign demand for the intermediate good upon default in the model

generates an income loss additional to that from the initial adverse productivity shock in

the defaulting country. Its wealth declines relative to the creditor country’s because its

overall income loss exceeds the gain from not repaying the debt. This reduces the world

relative demand of the defaulting country’s final good, due to home bias in consumption.

Therefore, its terms of trade and real exchange rate deteriorate, taking a third toll on

income and trade. In this way, the model builds an endogenous terms-of-trade mechanism

by which a sovereign default amplifies the effects of adverse productivity shocks on the

borrower country’s income and trade.5

This paper contributes to the literature by examining the role of vertical integration

for both creditor and borrower countries during sovereign debt crises. In particular, it in-

corporates the impact of sovereign default on creditor-country firms’ vertically integrated

production activities with the defaulting country. This produces a sovereign-default cost

to both the creditor and the borrower countries, which affects their debt contract.

The second contribution of this paper is that it studies the endogenous consequences

of a sovereign default to income, trade, terms of trade, and real exchange rate, and thus

how they affect the incentives to default. For one thing, the model captures reductions

in trade flows during default episodes, which have been well studied in the empirical

literature (e.g., Rose, 2005), but not in the theoretical literature. Modeling this stylized

fact helps us understand how a country’s consumer preferences regarding home goods and

imports affect its propensity to default (Rose and Spiegel, 2004; Rose, 2005).6

For another, this paper endogenizes terms of trade and real exchange rate in a sovereign

4Moreover, Fuentes and Saravia (2010) find that a default event can reduce FDI inflows by 72 percent.Aizenman and Marion (2004) also document that greater supply uncertainty reduces the expected incomefrom vertical FDI.

5It is worth emphasizing that, as in previous sovereign default models, this paper’s default also arisesin equilibrium as an optimal decision of a benevolent government.

6Past empirical research suggests that less outward-oriented sovereigns are more willing to default.Therefore, if a sovereign government internalizes its citizens’ desire for imported goods, we can begin toconsider how a country’s reduced desire for foreign goods can spur defaults, or how we can motivate thecountry to service its debt on time.

2

default model. It captures their two-way interaction with default risk prior to sovereign

default occurrences. During sovereign default events, it also captures the terms of trade

and real exchange rate deteriorations as they contribute to a defaulting country’s income

and trade losses. For instance, for 45 sovereign default episodes in 27 developing countries

over the period 1977-2009, on average at least half of the defaulting countries’ losses of

output and export value came from real depreciation.7 Therefore, the terms of trade and

real exchange rate in my model results in an endogenous penalty on income and trade

upon default. That is, unlike many previous sovereign default models, this model does

not rely on an exogenous endowment loss.8

In a quantitative exercise, I apply the model to the Mexican debt crises in the 1980s

and the country’s business cycles for the period of 1981Q1-2012Q4.9 This model generates

three empirical features of emerging markets’ business cycles and their sovereign default

episodes. First, it delivers countercyclical trade balances and procyclical trade flows.

Second, the model supports high bond spreads that are also countercyclical. Third, the

model accounts for terms-of-trade deterioration, real depreciation, and trade flow and

GDP declines during and right after a sovereign default.

To further study the role of terms of trade in affecting income, I examine the model

results where GDP and trade losses are partially due to terms-of-trade deterioration and

partially due to volume changes, as in the data. I also evaluate the welfare of both

countries, as the welfare of the creditor country is often left out of existing sovereign

default models. This reveals that upon default, both countries’ welfare declines, but

higher vertical integration and maintaining healthy foreign business environment reduce

their post-default welfare losses.

In explaining the cyclical movements of trade balances and terms of trade, this paper

is related to other studies in the international business cycle literature.10 But many of

them ruled out actual default events in equilibrium, unlike this model. Thus this paper is

closely related to sovereign debt literature (e.g., Grossman and Van Huyck, 1988; Kletzer

and Wright, 2000; Alfaro and Kanczuk, 2005), especially to previous quantitative small-

7The relevant figure is not included in this version of the paper due to space limitation, but is availableupon request. All data are real, logged, and HP-filtered. Raw data sources are detailed in the Appendix.

8It is similar to Mendoza and Yue (2012), where their model endogenizes output losses by a productionefficiency loss due to a default-triggered decline of trade credit to import inputs.

9I chose Mexico for this two-country model because Mexico has a relatively large open economy amongthe countries that have recently defaulted, as well as relatively large vertically integrated sectors involvedin foreign production, including its maquiladora sector (Zlate, 2012).

10These include but are not limited to works by Backus, Kehoe, and Kydland (1992, 1994), Mendoza(1995), Stockman and Tesar (1995), Heathcote and Perri (2002), Kehoe and Perri (2002), Kose (2002),Broda (2004), Iacoviello and Minetti (2006), Bodenstein (2008), and Raffo (2008).

3

open-economy sovereign default models, such as those by Aguiar and Gopinath (2006),

Arellano (2008), and Mendoza and Yue (2012), based on Eaton and Gersovitz (1981).

They have made significant contributions to endogenizing default risk (and income), as

well as to accounting for key empirical patterns of developing countries’ business cycles

and default episodes. However, those models do not focus on default-triggered changes

to trade flows and the terms of trade.

A few recent sovereign default papers (Cuadra and Sapriza, 2006; and Bleaney, 2008;

Popov and Wiczer, 2014) have examined the roles of exogenous terms-of-trade shocks and

exogenous terms-of-trade default penalty in small open economy models. The inclusion of

endogenous terms of trade and real exchange rate distinguishes this paper from them. Na,

Schomitt-Grohe, Uribe, and Yue (2014) also include endogenous exchange rate but focus

on optimal exchange rate policy. Like the model in this paper, their model achieves con-

current default and depreciation. However, their depreciation is driven by wage rigidity

and the government’s intention to reduce unemployment, whereas this model’s deprecia-

tion is associated with consumption home bias and changes to trade flows. Most recently,

Asonuma (2014) has also endogenized the real exchange rate in a two-country sovereign

default model, but through a different mechanism in endowment economies.11 In this

paper, I use production economies to incorporate richer business cycle fluctuations.

In addition, this paper complements the vast literature about international trade and

financial crises with incomplete markets, especially for emerging economies (e.g., Mendoza

2002, 2003, 2010). More specifically, it fits in the existing strand that focuses on the

connection between international trade and sovereign defaults, and the strand on the

connection between trade and exchange rate.

In the former strand, which consists largely of empirical studies, Rose (2005) docu-

ments that a default can reduce real bilateral trade value (in USD) by 8 percent for an

extended period after the event. However, it remains unclear why trade declines. The

four hypotheses – trade sanctions, trade credit collapse, asset seizures, and reputation –

are commonly mentioned, but the empirical evidence supporting them remains ambigu-

ous (Martinez and Sandleris, 2011; Tomz and Wright, 2013). One exceptional theoretical

model is proposed by Bulow and Rogoff (1989), who apply creditors’ seizures of a de-

faulting country’s exports. This paper instead incorporates vertical integration and terms

of trade to examine the interaction between trade and sovereign defaults. In the latter

strand of literature on trade and exchange rate, this paper is related to works by Bald-

win and Krugman (1989), Alessandria, Kaboski, and Midrigan (2010), Engel and Wang

11Asonuma (2014) uses traded and non-traded goods to generate real depreciation in his model, similarto the idea proposed by Arellano and Kocherlakota (2014).

4

(2011), Drozd and Nosal (2012), and Alessandria, Pratap, and Yue (2014). My model

differs by endogenizing default risk in interest rates.

The remainder of this paper is organized as follows. Section 2 describes the model

environment, equilibrium, and mechanisms. Section 3 provides the model calibration and

quantitative results. Section 4 concludes.

2 Model

2.1 Environment

In this section, I describe a dynamic model of two countries with endogenous sovereign

default, terms of trade, real exchange rate, and risk averse agents. In the model, the two

countries (i = 1, 2) trade one-period discount bonds, produce two unique final goods (j =

1, 2), respectively, and consume both through trade. The two final goods are imperfect

substitutes with constant elasticity, and cij stands for country i’s consumption of final

good j. pj stands for the final good j’s price, and country 1’s final good price p1 is

normalized to 1. I assume that the nominal exchange rate between the two countries is

1, and thus the real exchange rate is the ratio of country 2’s over country 1’s aggregate

price index. When the ratio decreases, country 2 experiences real depreciation.

I set country 1 to be the creditor who never defaults and has constant productivity

e1; country 2 is the borrower who has an option to default on its sovereign bonds and

faces stochastic productivity e2 that follows a Markov chain.12 Creditor country 1 has a

fixed amount of capital, k1, which can be paired either with a fixed amount of domestic

labor n1 to produce the final good 1, or with an imported intermediate good produced by

borrower country 2’s labor to produce the same final good 1. I use k1 to denote capital

used with domestic labor, km to denote that used with imported intermediate inputs, and

k1 + km = k1.13 Borrower country 2 has a fixed amount of labor, n2. It is divided into nm

who produce intermediate inputs for creditor country 1, and n2 = n2 − nm who produce

final good 2 with domestic capital k2.

12One way to interpret the creditor country’s constant productivity is that it always can smooth itsproduction through other financial channels that are not in this model, regardless of the situation in thebond market with the borrower country. Moreover, since the creditor country never defaults, it is not ofinterest in this paper to complicate the model results by including its productivity shocks. It would beof future research interest, however, to study the spillover effects when a creditor country’s productivityshocks trigger a borrower country’s sovereign default.

13Another setup is creditor country 1’s imported intermediate good and domestic labor directly sub-stitute each other imperfectly as inputs, and produce final good 1 with capital. Similar results areexpected, but it emphasizes the role of labor substitution in the creditor country, whereas the currentsetup emphasizes the role of capital allocation and has the flexibility to alternatively interpret km as FDI.

5

Three reasons stand out for this asymmetric model setup, where creditor country 1

allocates capital and borrower country 2 allocates labor and produces the intermediate

good for exporting. First, many of the countries that have recently defaulted are devel-

oping or emerging economies, where labor tends to be abundant and is used to produce

intermediate goods for export, through vertical FDI, offshoring, and other global sourcing

activities. Second, even though creditor country 1 does not produce intermediate goods,

its domestic labor input is an imperfect substitute for the imported intermediate good

and can be considered as creditor country 1’s own implicit intermediate inputs.

Third, the impact of a sovereign default on the demand for borrower country 2’s

intermediate good exports serves as one of the default penalties in the model. Even

though the data show defaulting countries’ intermediate good imports are also usually

damaged, I extract it from this paper because the inclusion makes it difficult to single

out the impact of the intermediate good export reduction upon default as a penalty,

which is the focus of this paper. The current setup keeps the model tractable, yet retains

a connection to reality. However, it is interesting to include more channels of global

integration in future research.14

It is also worth noting that borrower country 2 produces the intermediate good only

for export, not for domestic use. It is to distinguish the globally integrated production

activities from purely domestic activities in the borrower country. Because the two types

of activities are affected differently by crises, according to empirical studies mentioned in

the introduction. Meanwhile, we can consider those intermediate goods for domestic use

to be embedded in the value of borrower country 2’s final good 2.

In the bond market, a non-state-contingent one-period bond denominated in the cred-

itor country’s final good 1 is traded between the two countries. The bond is denoted

as bi for country i’s asset holdings. The borrower country’s default can be triggered by

negative productivity shocks and can happen along the equilibrium. The two countries

hold their own beliefs/concerns about borrower country 2’s default probabilities, while the

actual default probabilities are endogenous to debt holding and fundamental. Risk-averse

creditors in country 1 are willing to offer debt contracts that in some states may result in

a default by charging a high interest rate. Hence, equilibrium interest rates reflect the two

countries’ concerns about the default probabilities, as well as the creditor’s consumption

changes and risk aversion (Lizarazo, 2013).

The timing of this model is as follows. Both countries start off with initial sovereign

bond assets. After they observe the current productivity shock, borrower country 2 decides

14Mendoza and Yue (2012) use a default-triggered intermediate good import reduction as the defaultpenalty and reach a similar output-loss result as this paper does.

6

whether to repay its debt. If it does not default, bond market equilibrium determines the

bond price and the next period’s quantity. If it defaults, both countries enter financial

autarky and return with a certain probability, and creditor country 1 firms’ operations

with the intermediate good from borrower country 2 suffer from an efficiency loss. Then

accordingly, both countries reallocate their capital and labor. And last, production, trade,

and consumption take place. The following sections describe the model specifications.

2.2 Country 1: Creditor

Creditor country 1 has two types of agents: representative firms, and households.

2.2.1 Firms

Firms hire domestic workers n1, rent capital from households, choose capital allocation

{k1, km}, and decide how many intermediate good inputs to import from borrower coun-

try 2.15 Firms’ goal is to maximize their profits, taking wage w1, capital rent r1, and

intermediate good price pm as given:

Π1 = maxn1,qm,k1,km

{e1n

α11 k

1−α11 − w1n1 − r1k1 + e1(εqm)α3k1−α3

m − pmqm − r1km}

(1)

The first three terms are the profit the firms gain from using domestic labor n1 to

produce final good 1. The last three terms are the profit the firms gain from using

intermediate inputs εqm to produce final good 1, after deducting intermediate good costs

and capital rents. ε symbolizes the firms’ efficiency of operating with the intermediate

good from borrower country 2. When the borrower country is not in default, ε = 1. When

the borrower country is in default, a small portion of its intermediate good used by country

1’s firms is lost in operation. More specifically, during default episodes ε = min(ε e2e2, 1),

where 0 < ε < 1 and e2 is borrower country 2’s average productivity. This formulation

has four indications.

First, creditor country 1 firms’ production using the foreign intermediate good suffer

from an additional efficiency loss on top of the defaulting country’s negative aggregate

productivity shock that lowers its intermediate good production in the first place.16 This

15The model results would not be different if country 1’s firms internalize the production decision ofthe intermediate good sector in borrower country 2. The arrangement would be similar to that used inthe global sourcing literature (Antras and Helpman, 2004). But the current setup helps the model clarifythat the default-triggered efficiency loss is on the creditor country firms’ operations, not directly on thedefaulting country firms and their intermediate good production and exports.

16Unless the aggregate productivity in defaulting country 2 is already lower than εe2. The modelcalibration ensures that min(e2) > εe2.

7

setup reflects the empirical findings that foreign firms’ activities (e.g., FDI, offshoring,

and other global sourcing) are more severely damaged than domestic firms’ activities

in a crisis country, as evidenced by but not limited to Brennan and Cao (1997), Tille

and van Wincoop (2008), Milesi-Ferretti and Tille (2010), and Broner, Didier, Erce, and

Schmukler (2013).

Second, the default-triggered efficiency loss lies only in the foreign operations of country

1’s firms, not in defaulting country 2’s firms, given that the latter are already subject

to the negative aggregate productivity shocks that trigger sovereign defaults. Hence, the

model assumes that default events and efficiency losses in ε do not directly affect the

supply of the intermediate good. It is country 1 firms’ demand of the intermediate good

that is directly affected, possibly due to defaulting country 2’s worsened foreign business

environment and/or crisis-elevated trade costs and information asymmetry that cause

country 1 firms’ marginal cost of operating with the imported intermediate good to rise.

Third, the efficiency loss is applied only to country 1 firms’ production using im-

ported inputs from the defaulting country, not to their production using domestic inputs,

for which this paper provides empirical support. In the regression analysis, Mexico is

used for the defaulting country and Canada for the creditor country, as in the model

calibration. I collect Canadian monthly output data on 13 manufacturing industries for

the period from January 1981 to October 2012. After controlling for crisis-impacts from

the U.S., Canadian business cycles, and industry-specific trends and other factors, I find

negative impacts of Mexican sovereign default episodes on Canadian manufacturing out-

puts. Moreover, a Canadian industry that uses more Mexican inputs is more negatively

affected by those default episodes than an industry that uses less Mexican inputs. See

the Appendix for more details.

Last, the formulation of ε generates efficiency losses and default penalties that increase

with defaulting country 2’s productivity state, such that, all else being equal, the borrower

country has a larger incentive to default at a lower productivity state. This is consistent

with previous sovereign default models (Arellano, 2008).

2.2.2 Households

Households in creditor country 1 supply fixed amounts of capital k1 and labor n1 to the

firms. They use the proceeds from firms for consumption to maximize a standard time-

separable utility function E[∑∞

t=0 βt1U(c11t, c12t)], where 0 < β1 < 1 is the discount factor

and U(.) is a one-period utility function that is continuous, homothetic, strictly increasing

and concave, and satisfies the Inada conditions. More specifically, based on Krugman

8

(1980), I use an additive separable utility function U(c11t, c12t) = ρ1cθ111t + (1 − ρ1)cθ112t,

where 0 < ρ1, θ1 < 1. The elasticity of substitution is constant at 11−θ1 . This utility

function assumes independence between the domestic final good and the imported final

good in marginal utility, and brings tractability and computability to this model.

Households also choose how many of the one-period non-state-contingent bonds issued

by borrower country 2 to purchase, given the bond price q. Hence, their expected lifetime

utility depends on borrower country 2’s default decisions. When the borrower country

does not default in the current period, the creditor country households’ optimization

problem can be written recursively as:

V1c(s, b1) = maxb′1,c11,c12

U(c11, c12) + β1[

∫s′ /∈D1(b′2)

V1c(s′, b′1)dF1(s′|s) +

∫s′∈D1(b′2)

V1d(s′)dF1(s′|s)]

(2)

where b′i is country i tomorrow ’s bond asset holding, and s is the aggregate state of the two

economies. F1 and D1 are creditor country 1 households’ beliefs about borrower country

2’s productivity process and default set, respectively, which I explain in the next section.

The household problem is subject to:

w1n1 + r1k1 + b1 = c11 + p2c12 + qb′1. (3)

where q = β1

∫s′ /∈D1(b

′2)∂V ′1c/∂b

′1dF1(s′|s)

λ1, and λ1 is the multiplier of the budget.

When a default happens, bond assets are set to zero, both countries undergo financial

autarky, and only with a certain probability 0 < φ < 1 can they resume bond trading.

Some may argue that it is not realistic to also exclude the creditor from the interna-

tional financial market. But since the creditor country has no productivity shock, its

consumption losses from the bond market exclusion are reduced. The creditor country’s

constrained maximization problem becomes:

V1d(s) = maxc11,c12

{U(c11, c12) + β1E1[φV1x(s′, 0) + (1− φ)V1d(s

′)]} (4)

where V1x = [V1d(s) or V1c,b1(s)|borrower country 2 defaults or not]. The problem is

subject to

w1n1 + r1k1 = c11 + p2c12. (5)

Given the above setup, I calculate creditor country 1’s GDP as the gross production

9

of final good 1 minus the cost of the imported intermediate good, i.e., e1nα11 k

1−α11 +

e1(εqm)α3k1−α3m − pmqm. Note that its GDP value and volume are the same in the model

because its final good price is p1 = 1.

2.3 Country 2: Borrower/Defaulter

Country 2 has four types of agents: intermediate good firms, final good firms, households,

and a government.

2.3.1 Intermediate Good Firms

Intermediate good firms produce intermediate good inputs for creditor country 1 firms’

final good 1 production. They decide how many domestic workers to hire, nm, and labor

is the only input needed for the intermediate good production. I assume the production

to be linear in nm and associated with the country’s aggregate productivity e2. The firms

maximize the following profit:

maxnm{pme2nm − p2wmnm} (6)

Note that the supply of the intermediate good is not directly affected by ε, even though

the equilibrium quantity is. From the first order condition, we have pm = p2wme2

.

2.3.2 Final Good Firms

Country 2’s final good firms rent capital k2, hire domestic workers n2 to produce final

good 2. They maximize the following profit:

maxn2,k2{p2e2n

α22 k

1−α22 − p2w2n2 − p2r2k2} (7)

where w2 is domestic sector wage.

2.3.3 Households

Households in borrower country 2 supply labor n2 and capital k2. They derive income

from two sources: wages from producing the intermediate good for creditor country 1, and

wages and capital rent from domestic final good firms. Their utility is a standard time-

separable homothetic function of a consumption bundle E[∑∞

t=0 βt2U(c21t, c22t)], where

0 < β2 < 1 is the discount factor. Similar to creditor country 1, the one-period utility

function is specified as U(c21t, c22t) = (1 − ρ2)cθ221t + ρ2cθ222t, where 0 < ρ2, θ2 < 1. The

10

elasticity of substitution is constant at 11−θ2 . As in Mendoza and Yue (2012), households

do not borrow directly from abroad, but the government chooses a debt policy internalizing

the utility of households, taking as given the wages and the capital rent.

2.3.4 Government

Country 2’s sovereign government issues one-period non-state-contingent discount bonds,

so the asset market is incomplete. It cannot commit to repaying its debt, it compares the

value of repaying debt V2c and that of default V2d and chooses the option that provides

the greater value, that is:

V2x(s, b2) = max {V2c(s, b2), V2d(s)} (8)

The nondefault value is given by the choice of (b′2, c21, c22) that maximizes the following

problem, taking wages, capital rent, p2, and bond price q as given:

V2c(s, b2) = maxb′2,c21,c22

U(c21, c22) + β2[

∫s′ /∈D2(b′2)

V2c(s′, b′2)dF2(s′|s) +

∫s′∈D2(b′2)

V2d(s′)dF2(s′|s)]

(9)

subject to

p2w2n2 + p2r2k2 + p2wmnm + b2 = c21 + p2c22 + qb′2. (10)

where F2 and D2 are the government’s beliefs about its country’s productivity process

and default set, respectively. q = β2

∫s′ /∈D2(b

′2)∂V ′2c/∂b

′2dF (s′|s)

λ2, and λ2 is the multiplier of the

budget constraint. It is worth noting that here the government takes q as given, which

differs from previous small open economy sovereign default models, where the borrower

follows a bond price schedule set by the creditor and understands its debt choice can affect

the bond price accordingly.

In the event of a default triggered by an adverse productivity shock to the borrower

country, the foreign demand for the defaulting country’s intermediate good declines due to

an efficiency loss in foreign firms’ operations with those inputs. Meanwhile, both countries

enter financial autarky as their bond assets are set to zero, and return to bond trading with

probability 0 < φ < 1. There is no other direct penalty, such as exogenous endowment

loss or trade sanctions.17 However, in equilibrium the defaulting country does suffer other

17There lacks empirical evidence in the literature that other countries impose trade sanctions on de-faulting countries (Martinez and Sandleris, 2011; Tomz and Wright, 2013).

11

endogenous losses, as discussed in the mechanism section. Taking into account all the

consequences of a sovereign default, the borrower country’s default value is as follows:

V2d(s) = maxc21,c22

{U(c21, c22) + β2E2[φV2x(s′, 0) + (1− φ)V2d(s

′)]} (11)

subject to

p2w2n2 + p2r2k2 + p2wmnm = c21 + p2c22 (12)

The definitions of the actual default set D and the actual probability of default are

standard from Eaton-Gersovitz type models (also see Arellano, 2008). Default set D at

each current debt level b2 is a collection of exogenous states when borrower country 2’s

government strategically chooses to default to maximize its value:

D(b2) = {s ∈ S : V2c(s, b2) < V2d(s)} (13)

Because no one can be certain about the aggregate state tomorrow, the actual default

probability π is the sum of all the probabilities of tomorrow’s states where the borrower

country will choose to default, given the debt level:

π(s, b′2) =

∫s′∈D(b′2)

f(s, s′)ds′ (14)

This default probability exists whether or not the borrower or the creditor country con-

siders the default risk when issuing or purchasing bonds. It is possible for two countries

to have different beliefs/concerns about the actual default set or the actual default prob-

ability. That is, π1(s, b′2) =∫s′∈D1(b′2)

f1(s, s′)ds′, π2(s, b′2) =∫s′∈D2(b′2)

f2(s, s′)ds′, and

{D,D1,D2} and {π, π1, π2} are not necessarily equal to each other, respectively. More

discussion about the two countries’ beliefs about the default probability is in the equilib-

rium bond price section.

Given the above setup, I calculate borrower country 2’s GDP value as the gross pro-

duction of final good 2 plus the intermediate good exports, p2e2nα22 k

1−α22 + pme2nm, and

its GDP volume as e2nα22 k

1−α22 + e2nm.

2.4 Equilibrium

Finally, in equilibrium all goods, capital, labor, and bond markets clear for both countries

in default and nondefault regimes. Also, in the borrower country, the intermediate good

sector per-worker wage is equal to the wage paid in its domestic production sector, so

12

that there is no labor flowing between the two sectors. The equilibrium conditions are

formulated and defined as follows:

b1′(s, b1) + b2

′(s, b2) = 0 in nondefault regime, (15)

or b1′(s, b1 = 0) = 0 & b2

′(s, b2 = 0) = 0 in default regime (16)

and n1 = n1, k1 + km = k1, n2 + nm = n2, k2 = k2, wm = w2, (17)

e1nα11 k

1−α11 + e1(εqm)α3k1−α3

m = c11 + c21, e2nα22 k

1−α22 = c12 + c22, e2nm = qm. (18)

Definition 1 A recursive competitive equilibrium is defined as a set of functions for (a)

creditor country 1’s capital allocation and borrower country 2’s labor allocation; (b) both

countries’ household consumption policy c and saving policy b′; (c) welfare value V at

default and nondefault regimes; and (d) the law of motion for the aggregate state s, such

that: (i) the borrowing and lending policies satisfy the problem’s first-order conditions;

(ii) the two countries’ value functions satisfy Bellman Equations; (iii) r1, r2, pm, p2 and

q clear the capital, goods, and bond markets; (iv) wm and w2 stabilize labor flows between

the two sectors in borrower country 2; and (v) the law of motion is consistent with the

stochastic processes of e2.

Borrower country 2’s terms of trade are calculated using unit value index, as in the

World Bank data; and its real exchange rate is two countries’ CPI ratio using Laspeyres

price index.18 More specifically, they are calculated as follows:

TOT2t =

(pt2ct12+ptmq

tm)/(ct12+qtm)

(p02c012+p0mq

0m)/(c012+q0m)

pt1ct21/c

t21

p01c021/c

021

(19)

REXR2t = NEXR(pt2c

022 + pt1c

021)/(p0

2c022 + p0

1c021)

(pt2c012 + pt1c

011)/(p0

2c012 + p0

1c011)

(20)

2.4.1 Mechanism

This section summarizes the important mechanisms in this model. First of all, prior to

a default, how is default risk linked with trade and the terms of trade? As the borrower

country accumulates debt, its default risk and the equilibrium bond interest rate rise.

The higher cost of debt reduces the borrower country’s available funds for consumption

relative to the creditor country’s; thus, owing to home bias in both countries, the world

18The qualitative results do not change if using Paasche price index.

13

relative demand of final good 2-to-1 decreases.19 Decreasing relative demand of final good

2-to-1 puts downward pressure on the relative price p2, preventing the borrower country

from improving terms of trade to ease its budget constraint and debt burden. Hence, when

the terms of trade deteriorate because of higher default risk, in turn, the deterioration

increases the borrower country’s default risk.

Once a large enough adverse productivity shock causes borrower country 2 to default,

the mechanism affecting income, trade, and terms of trade works as follows. The default

triggers an efficiency loss to the creditor country firms’ operations using the defaulting

country’s intermediate good, which has several effects. First, the demand of the interme-

diate good declines, resulting in a lower pm. Second, creditor country 1’s firms have to

reallocate capital away from combining with the imported intermediate good, and towards

its domestic labor to produce final good 1. This decreases creditor country 1’s marginal

product of capital, as well as its capital rents.

Third, in the defaulting country 2, fewer workers are hired in the intermediate good

sector, so some workers have to shift to domestic production of final good 2, since this

model has no unemployment.20 The labor shifting enables the defaulting country to

produce and export more of its own final good 2 despite the initial adverse productivity

shocks than the country would be able to without such labor shifting. In addition, the

lower demand for labor and the overflow of workers into the domestic good sector lowers

the defaulting country’s wage in both sectors.21 The reduced labor income contributes to

the sovereign default costs.

Overall, owing to the initial adverse productivity shock and the additional wage re-

duction, the defaulting country’s income declines even though it does not repay the debt.

When its available funds for consumption declines relative to the creditor country’s, the

world relative demand of final good 2-to-1 decreases, again because of two countries’ home

bias preferences in consumption. Therefore, the defaulting country’s terms of trade and

real exchange rate deteriorate, which in turn induces more losses to its income, purchasing

power, and trade values.

In particular, from both countries’ households’ first order conditions (Eq. 21) and

budget constraints, we can see how the defaulting country’s wealth share in the world

19As proven in the Appendix, consumption home bias in both countries is a sufficient condition toreduce the world relative demand of final good 2 when the country’s world wealth share declines. Themore home biased the two countries are, the more the relative demand decreases.

20Usually high unemployment occurs during default episodes, but for my calibrating country Mexico,the unemployment rate has been relatively low in comparison with international standards, because ofits informal sectors.

21In general, emerging markets’ wage fluctuations are more volatile than developed countries’, whiletheir employment fluctuations are less volatile, as documented by Li (2011).

14

affects the world relative demand of final good 2-to-1 (RD, Eq. 22):

p2 =ρ2

1− ρ2

(c21

c22

)1−θ2 , p2 =1− ρ1

ρ1

(c11

c12

)1−θ1 (21)

RD ≡ c12 + c22

c11 + c21

=S2( 1

g2− 1

g1) + 1

g1

1− p2g1

+ S2(p2g1− p2

g2)

(22)

where S2 =GDP2+b2−qb′2GDP1+GDP2

is the wealth share of borrower country 2 in the world, g1 =

( p2ρ11−ρ1 )

11−θ1 + p2, and g2 = [p2(1−ρ2)

ρ2]

11−θ2 + p2. If the two countries’ households have exactly

the same preferences towards the two final goods, i.e., g1 = g2, then the world wealth

share has no effect on the world relative demand. In this model, because there is home

bias in both countries making g1 > g2, all else being equal, the world demand of final good

2 (i.e., c12 + c22) is positively related to S2, while that of final good 1 (i.e., c11 + c21) is

negatively related to S2. Therefore, the world relative demand of final good 2-to-1, RD,

increases with borrower country 2’s wealth share in the world S2. The above is generalized

in the following proposition.

Proposition 1 (1.1) If g1 > g2, then all else being equal the world relative demand of

final good 2-to-1, RD, is positively related to borrower country 2’s wealth share in the

world S2, i.e. ∂RD∂S2

> 0. (1.2) In other words, if the sum of the two countries’ home goods

expenditure shares is strictly larger than 1, i.e., c11GDP1+b1−qb′1

+ c22p2GDP2+b2−qb′2

> 1, then all

else being equal ∂RD∂S2

> 0.

Proof. See Appendix.

As default risk increases or during default episodes, borrower country 2’s wealth share

in the world declines, which causes the world relative demand of final good 2-to-1 to de-

crease. This reduces the relative price of final good 2, p2, and borrower country 2’s real

exchange rate.22 Together with lower pm, its terms of trade also deteriorate. This mech-

anism becomes stronger as g1 increases, or g2 decreases, i.e., as either country becomes

more home biased in consumption.

Proposition 2 When g1 > g2, ∂RD∂S2

increases with g1 and decreases with g2.

Proof. See Appendix.

From Eq. 21, we can also see that as p2 decreases when default risk increases or during

default episodes, borrower country 2’s consumption shifts towards the home good (i.e.,

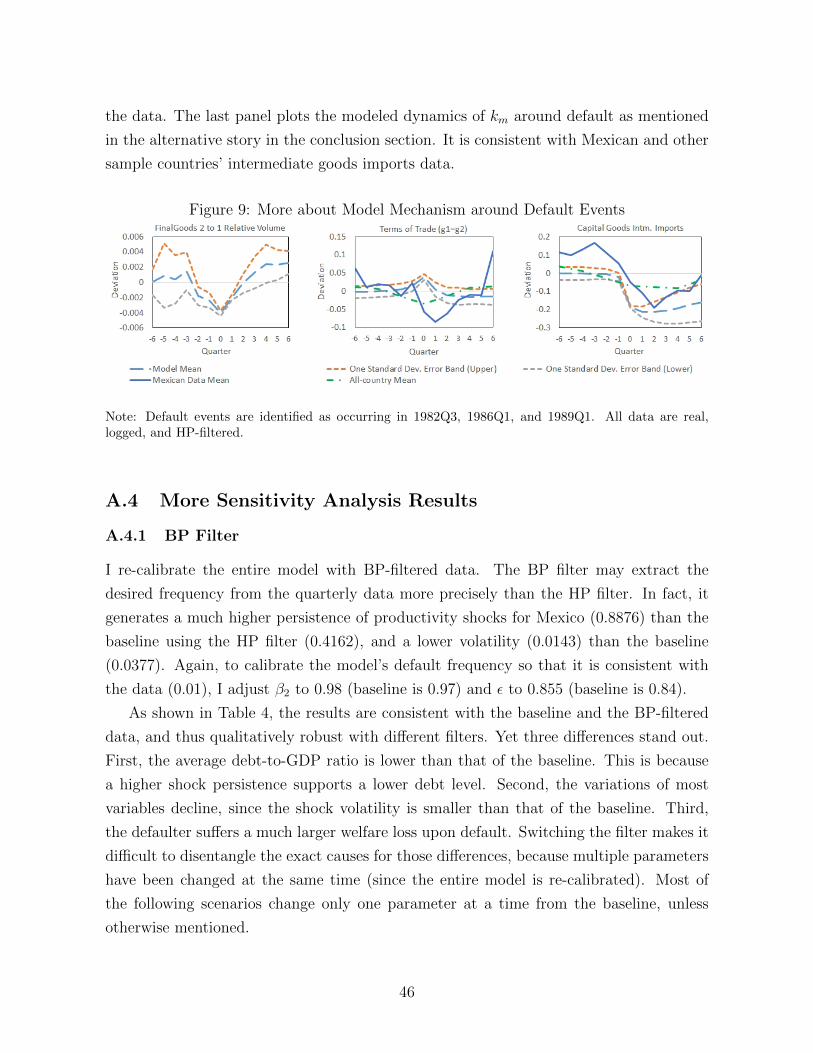

22In equilibrium, the world relative quantity of final good 2-to-1 declines, as shown by the first panelin Appendix Figure 9.

15

c21c22

declines), while creditor country 1’s shifts towards the foreign good (i.e., c11c12

declines).

Hence, trade flows change.

To summarize, the main costs to the creditor when the borrower defaults are the

missed debt repayment, and the production loss caused by an efficiency loss in using

imported intermediate inputs from the defaulting country. These constrain the creditor

country’s budget. However, the creditor gains from more favorable terms of trade and real

appreciation that allow it to import more of the borrower country’s final good. For the

borrower country, the main costs upon default are wage losses, lower purchasing power,

and no access to the international bond market for consumption smoothing. It gains by

forgoing the debt repayment.

2.4.2 Equilibrium Bond Price

This section illustrates how bond prices are determined in the model. Figure 1 plots

bond price q against creditor country 1’s asset level tomorrow b′1 (i.e., borrower country

2’s borrowing tomorrow) for a given productivity state s and current asset level of the

creditor country, b1 (i.e., the borrower country’s current borrowing). In a simpler case

without default risk, the bond price is determined by the following equation in equilibrium:

q∗(b, b′, s) = β1

E1∂U∂c′11

λ1

= β2

E2∂U∂c′21

λ2

(23)

where λ1 = ∂U∂c11

and λ2 = ∂U∂c21

. The first equation is creditor country 1’s bond demand

function, and the second equation is borrower country 2’s bond supply function. As shown

in the left panel of Figure 1, the bond demand curve and bond supply curve (dashed lines)

are close to linear and intersect at point E1.23 Point E1 pins down the market equilibrium

bond price and tomorrow’s bond quantity.

If the current bond holding b1 is at a higher level, as in the right panel of Figure 1, then

bond demand curve will shift up (to the thicker dashed line) because of a lower current

marginal utility of domestic consumption (i.e., λ1), according to Equation 23. Meanwhile,

bond supply curve will shift down because of a higher current marginal utility of imported

consumption (i.e., λ2). The resulting new intersect point E1′ provides a larger equilibrium

bond quantity and a slightly lower price, depending on the two countries’ risk aversion.

Now let’s consider default risk. In equilibrium, bond demand and supply curves take

into account the borrower’s and the creditor’s perspectives on default probability, respec-

23Even in this risk-free bond case, the bond supply and demand curves are not exactly linear, becauseof the agents’ risk aversion.

16

Figure 1: Bond Price (given aggregate productivity state s)

Note: Dashed lines indicate that neither country considers default risk; solid lines indicate that bothcountries consider default risk but borrower country 2 is more optimistic about its repayment probability.The x-axis in the above plots is b′1. As b′1 is positive (right hand side) and becomes larger, borrowercountry 2 accumulates more and more debt.

tively, as in the following equations:

q∗(b, b′, s) = β1

∫s′ /∈D1(b′2)

∂U∂c′11∂U∂c11

dF1(s′|s) = β2

∫s′ /∈D2(b′2)

∂U∂c′21∂U∂c21

dF2(s′|s) (24)

When the two countries believe that default probability increases significantly, both

the demand and supply curves imply lower bond prices. It is reflected by the solid lines in

the left panel of Figure 1, given current b1, both curves bend downward as tomorrow’s b′1

(i.e., country 2 tomorrow’s borrowing) becomes larger. In particular, for borrower country

2, the intuition is that, taking default probability into account, the government knows it

has to lower the bond price in order to issue more bonds. But, as proven by Arellano

(2008), there is a lower bound for bond price q, up to which a borrower country is willing

to take on debt. That is, for any bond price q below a certain threshold, a borrower

country is able to issue less bond with a higher price q to finance the same amount of

consumption (of final good 1). Hence, the bond supply curve terminates at the lower

bound for q. The result is a different equilibrium point from the no-default-risk case, at

E2: both the equilibrium bond quantity and price are lower than those at E1.

Again, if the current bond holding is at a higher level, as indicated by the solid lines in

the right panel of Figure 1, then creditor country 1’s bond demand curve will shift upward

and borrower country 2’s bond supply curve will shift downward. The new intersect point

E2′, again, provides a larger equilibrium bond quantity and a lower price. However, owing

to the default risk, the increase in the bond quantity is much smaller and the decrease in

17

Figure 2: Default Probability Beliefs and Bond Price

Note: Here I assume that the creditor country always has the correct belief/concern about the defaultset and probability, i.e., D1 = D and π1 = π. Case (1) depicts the bond supply curve if borrowercountry 2 does not consider default probability when issuing bonds, used as baseline. Case (2)depicts the bond supply curve if the borrower country does consider default probability and is moreoptimistic about its repayment probability, or less concerned about default risk, than the creditorcountry is. Case (3) depicts the bond supply curve if the borrower country considers default probabilityand has the same belief or is more pessimistic about its repayment probability than the creditor country is.

the bond price is much larger than in the no-default-risk case.

However, Figure 1 only shows one special case of the two countries’ beliefs/concerns

about default probabilities, i.e., the bond supply curve starts to bend downward at a higher

bond quantity (b′1) than the bond demand curve does. It implies that when the bond is

initially issued, the borrowing government is more optimistic about making repayments,

or less concerned about default risk, than the creditor country is. The level of b′1 at

which the supply and demand curves start to bend down may differ depending on the

countries’ beliefs or concerns about the default probability. This issue does not arise in

small open economy sovereign default models because the borrowing government chooses

bond according to a price schedule following the creditor country’s bond demand curve.

Figure 2 shows three possible relations between the bond supply and demand curves,

assuming that the creditor country always has the correct belief about default risk and

default probability, i.e., D1 = D and π1 = π. The thick solid line (1) depicts the bond

supply curve when borrower country 2’s government does not consider default probability

when issuing bonds, i.e., D2 = ∅ or π2 = 0. It can be interpreted as follows: even though

the government aims to maximize the households utility in the long run, it is myopic on

debt repayments. Here I emphasize the timing of “when issuing bonds”, not after the

issuance. In reality, whether and when a borrower country’s government is not concerned

about sovereign default risk is difficult to verify. But given many countries’ serial default

events, it is possible that their governments learned little about their own default risk

18

from the past or were not concerned about the risk when issuing new bonds. A unique

equilibrium is guaranteed in case (1).

The thin solid line (2) depicts the bond supply curve when the borrower country does

consider default probability but is more optimistic about its repayment probability, or less

concerned about the default risk, than the creditor country is. This case also yields at least

one equilibrium.24 The dashed line (3) depicts the bond supply curve when the borrower

country considers default probability and has the same belief or is more pessimistic about

its repayment probability than the creditor country is, i.e., π = π1 ≤ π2 for each (s, b′2).

That is, the bond supply curve starts to bend down at the same time or earlier than the

bond demand curve does. This case, however, does not guarantee an equilibrium as in the

graph; the borrowing government may ration the supply of bonds. It is of future research

interest to investigate this case and look for the zone of such bond rationing.

This paper focuses on case (1) and (2), since they provide at least one equilibrium in

the bond market. I first solve case (1) as the baseline, then the optimistic borrower model

in case (2). In particular, for case (2) I specify that the borrowing government believes

its country has a higher steady-state productivity than the actual level that the firms and

the creditor country know. That is, all the agents in the model share the same default sets

D1 = D2 = D, but have different beliefs about default probabilities π = π1 > π2, since the

borrowing government is more optimistic about productivity on average. In reality, this

situation may stem from a developing country government’s overly optimistic perspective

on the country’s growth. Other scenarios can generate case (2) as well; I use the above

specification for its simplicity.25 I expect case (1) and case (2) to generate similar results.

3 Quantitative Results

3.1 Baseline Calibration

In this section, I study the quantitative implications of the model by conducting numerical

simulations at the quarterly frequency and using a baseline calibration based on the data,

largely from Mexico and Canada. Table 1 shows the calibrated parameter values.26

24The equilibrium is unique as long as line (2) does not bend down to cross the bond demand curveagain. It depends on the slope of both curves. When both countries hold the same beliefs about thestandard deviation and the transition probabilities of the borrower’s productivity shocks, the equilibriumis unique.

25For example, the borrowing government may not be concerned about default risk until its debt levelreaches a certain level.

26U.S. is Mexico’s number 1 trade partner and creditor, while Canada is also among the top 6 since1980s.

19

Table 1: Parametrization

Calibrated Parameter Value Target StatisticsBond market

re-entry probability φ = 0.083 Dias and Richmond (2007)Creditor country 1 home bias ρ1 = 0.94 0.99, Canadian (CA) consumption share

of non-Mexican goodsBorrower country 2 home bias ρ2 = 0.82 0.70, Mexican (MX) home goods

consumption shareCreditor country 1 elasticity

of substitution θ1 = 0.25 1.33, advanced economy intratemporal elasticityBorrower country 2 elasticity

of substitution θ2 = 0.60 2.50, emerging economy intratemporal elasticityCreditor country 1 domestic

production labor share α1 = 0.63 From OECD data for CABorrower country 2 domestic

production labor share α2 = 0.45 From OECD data for MXIntermediate good share

in final good 1 production α3 = 0.54 CA&MX average labor share in productionCreditor country 1 labor endowment n1 = 2.5 Average CA-to-MX employment ratioCreditor country 1 capital endowment k1 = 18.19 0.65, average FDI-to-GDP ratio for MXBorrower country 2 labor endowment n2 = 1 Normalized to 1Borrower country 2 capital endowment k2 = 1 Normalized to 1Creditor country 1 productivity e1 = 2.8557 2, average CA-to-MX GDP ratioBorrower country 2 productivity steady state E(e2) = 1 Normalized to 1Borrower country 2 autocorrelation of TFP ρ = 0.4162 From production functionBorrower country 2 std. dev. of TFP shocks σ = 0.0377 From production functionCreditor country 1 discount factor β1 = 0.99 1%, US government bond interest rateParameter by Simulation Value Target StatisticsBorrower country 2 discount factor β2 = 0.97 1%, quarterly default frequency for MXIntm. good sector efficiency loss upon default ε = 0.84 -0.18, average intm. goods export income

deviation from trend upon default for MX

The probability that both countries reenter the international financial market after a

default is 0.083, which implies that the borrower country stays in exclusion for an average

of three years after default. This is the estimate obtained by Dias and Richmond (2007)

for the median duration of exclusion periods. It is also consistent with the finding by

Gelos, Sahay, and Sandleris (2011) and is applied by Mendoza and Yue (2012).

The parameters ρ1 and ρ2 in the model control the degree of home bias in consumption.

According to the World Bank (WDI), the average share of domestic products in final

consumption for Canada and Mexico for the period 1981-2012 is 0.6 and 0.7, respectively.

Hence, I use Mexico’s 0.7 in calibrating ρ2 such that, at steady state, borrower country

2’s domestic good share in final consumption is 0.7. As for Canada, not all 40 percent of

its final consumption is from Mexico. Since Mexico accounts for on average 2.4 percent of

Canadian imports over the same sample period, I calibrate ρ1 such that, at steady state,

20

creditor country 1’s domestic good share in final consumption is 0.99.

The next two parameters θ1 and θ2 have to do with the elasticity of substitution

between domestic good consumption and imported good consumption for developed and

developing countries.27 The literature provides a large range of estimates for the elasticity

of substitution. Backus, Kehoe, and Kydland (1994) document that U.S. elasticity is

between 1 and 2; values in this range are commonly used in empirical trade models.

Their benchmark model adopts a value of 1.5. Later authors have used similar values,

e.g., Chari, Kehoe, and McGrattan (2002), Bergin (2006), and Ruhl (2008). A recent

paper by Feenstra, Luck, Obstfeld, and Russ (2014) also find point estimates for the

macro elasticity exceeding unity in almost all industries.

However, few papers have studied the Armington elasticity for developing countries.

Ostry and Reinhart (1992) find the elasticity of substitution between traded and nontraded

goods in the range of 1.22 to 1.27, and significant regional differences, with less-developed

countries displaying higher values. Yet, the cross-country comparison of Armington elas-

ticities remains unclear. This paper does not take a stand on the value of the elasticity.

As a starting point, I adopt 1.33 as the elasticity of substitution for the creditor coun-

try to match that for developed countries on average, and a higher value of 2.5 for the

borrower country to indicate that less-developed countries may have a higher elasticity of

substitution between home and foreign goods as they do for traded and nontraded goods.

In sensitivity analyses, I explore other values for the elasticities.

The labor share in the final good production is set at 0.63 for Canada and 0.45 for Mex-

ico, which are the average labor income shares using annual data for the period 1981-2009

(1981-2008 for Canada) from OECD Statistics. The input share of imported intermediate

good to produce final good 1 is the average labor share in final good production of Canada

and Mexico. I vary this parameter value in sensitivity analysis as well.

The capital and labor endowments of borrower country 2 are normalized to 1. Hence,

creditor country 1’s labor size is n1 = 2.5 to match the average CA-to-Mexico employment

ratio for 1981Q1-2012Q4. Creditor country 1’s capital endowment k1 is chosen such that,

at steady state, its capital used with the intermediate good, km, is 65 percent of borrower

country 2’s GDP. This is approximated by the average of FDI-to-GDP ratio for Mexico

during 1981Q1-2012Q4, assuming the majority of the FDI to Mexico is vertical. However,

it is important to note that this approximated target is by no means a complete calibration

for the actual amount of foreign capital used with Mexican intermediate goods to produce

foreign final goods.

27Without default risk, θ1 and θ2 also determine the values for the elasticity of intertemporal substi-tution for both countries. But with default risk, the intertemporal elasticity decreases with the risk.

21

The only productivity shock in the model is to borrower country 2’s productivity e2,

whose steady state is normalized to 1. It follows an AR(1) process:

log e2,t = ρ log e2,t−1 + ηt

with η being iid and following N(0, σ2). I estimate the process using the model’s pro-

duction functions, and HP-filtered Mexican data for GDP, (average) capital stock, and

employment in both the domestic sector and the FDI sector for 1981Q1-2012Q4. Using

the method proposed by Tauchen and Hussey (1991), I construct a Markov approximation

to this process with 5 states of productivity realization for e2. For creditor country 1,

its constant productivity e1 is calibrated to be 2.8557, so that at steady state the CA-

to-Mexico GDP ratio is 2, equal to the average CA-to-Mexico GDP ratio for 1981-2011,

according to IMF annual data.

Both U.S. and Canadian treasury bills bear real interest rates that are below 1 percent

on average; hence we have β1 = 0.99. Last, the targets for setting β2 and ε are quarterly

frequency of Mexican defaults and the loss in Mexican intermediate goods exports upon

default. Mexico’s quarterly default frequency is 1%, since it had eight default episodes

between 1828 and 2012 according to Reinhart (2010). In the later sections, to study

the dynamics around Mexican sovereign defaults during the 1980s, I include more such

episodes from Paris Club data for the sample period 1981Q1-2012Q4. They are 1982Q3,

1986Q1, and 1989Q1. At the onset of these most recent sovereign default episodes, Mex-

ico’s intermediate goods export value, on average, was about 18 percent below trend.

Given these two targets, the simulated procedure yields β2 = 0.97 and ε = 0.84.

I solve the model with a discretized state space of 5 realizations for borrower country

2’s productivity and 107 points for asset holdings. The model is considered to be solved

when the convergence distance diminishes to 1.0000e − 06. In the following sections, I

first examine the properties of the calibrated model and then study the simulated results,

both over business cycles and around default events.

3.2 Policy Functions

The properties of bond quantity and its price in the baseline model are in line with other

sovereign default papers. The left plot in Figure 3 graphs the next-period assets for

the borrower country against its current assets, in a high-productivity state and a low

productivity state in the current period. As the borrower country accumulates debt (to

the left of the bottom axis), its marginal borrowing capacity diminishes. Moreover, when

22

the country is in a low-productivity state, its bond function starts to flatten out at a lower

current debt amount than it would in a high-productivity state. That is to say, all else

being equal, a higher productivity state supports a higher debt level.

Figure 3: Policy Functions

The right plot in Figure 3 graphs the bond price functions. It shows that the bond

price decreases with the debt level (i.e., interest rate rises). Across productivity states,

the bond price is significantly higher for a high-productivity state, which implies that

interest rates are countercyclical.

3.3 Cyclical Movements

This section starts the assessment of the quantitative performance of the model by com-

paring moments from the data with moments from the model’s dynamics. To compute

the latter, I feed borrower country 2’s productivity process into the model and conduct

1,000 simulations, each with 600 periods. Then I truncate the first 100 observations and

use the rest to compute the statistics of the model results.

Table 2 compares the moments produced by the baseline model and optimistic bor-

rower model with those from Mexican data and from Mendoza and Yue (MY, 2012). All

the data used in this model are quarterly from 1981Q1 to 2012Q4. The data sources

are provided in the Appendix. Note that Mendoza and Yue (2012) calibrate their model

partially to Argentine data and partially to Mexican data.

As explained earlier, to guarantee the existence of bond market equilibrium, on one

hand, the baseline model assumes that the borrowing government is unconcerned about

default probability (i.e., D1 = D, π1 = π, and D2 = ∅ or π2 = 0, as case (1) in Figure

3). On the other hand, the optimistic borrower model assumes that the government does

23

Table 2: Statistical Moments of Borrower Country 2’s Business Cycles

Statistics Data Baseline M&Y Optimistic(2012) Borrower∗

Average debt/GDP ratio (in percent) 74.94 27.44 22.88 27.43Average bond spreads (in percent) 4.35 4.59 0.74 4.59Bond spreads std. dev. (in percent) 4.71 2.44 1.23 2.48Real exchange rate std. dev. (in percent) 17.30 ∗∗∗1.99 n.a. 2.03Terms of trade std. dev. (in percent) 6.21 ∗∗∗3.87 n.a. 3.95Dom. product con. std. dev./GDP std. dev. 1.23 0.96 n.a. 0.96Total consumption std. dev./GDP std. dev. 1.12 1.09 1.05 1.09Trade balance/GDP std. dev. (in percent) ∗∗2.08 1.40 n.a. 1.41Correlation with GDP

Bond spreads −0.39 −0.92 −0.17 −0.92Real exchange rate 0.53 ∗∗∗0.54 n.a. 0.55Terms of trade 0.25 ∗∗∗0.49 n.a. 0.50Trade balance/GDP ∗∗ − 0.65 −0.20 −0.54 −0.19Total exports 0.21 0.85 n.a. 0.85Intermediate good exports 0.18 0.85 n.a. 0.85Total import 0.75 0.92 n.a. 0.92Wage 0.65 0.88 n.a. 0.87GDP volume 0.65 0.79 n.a. 0.79Default occurrence −0.14 −0.24 −0.09 −0.24Default duration −0.39 −0.64 n.a. −0.64

Correlation with bond spreadsReal exchange rate −0.76 ∗∗∗ − 0.78 n.a. −0.79Terms of trade −0.13 ∗∗∗ − 0.77 n.a. −0.77Trade balance/GDP ∗∗0.30 0.50 0.15 0.50Total exports −0.02 −0.63 n.a. −0.63Intermediate good exports −0.08 −0.65 n.a. −0.64Total import −0.28 −0.91 n.a. −0.91Wage −0.35 −0.68 n.a. −0.68GDP volume −0.19 −0.52 n.a. −0.51Default occurrence 0.18 0.26 n.a. 0.26Default duration 0.56 0.86 n.a. 0.86

Note: All data in the table are HP-filtered, except bond spreads and default occurrence and duration.

All data are in real terms and at quarterly frequency. Bond spreads are calculated over U.S. government

bond real interest rates that are sometimes negative. ∗Under optimistic borrower case, the government

believes E(e2) = 1.04 with all else being the same as the baseline calibration. That is, the government-

perceived average productivity is about one standard deviation higher than the actual level. ∗∗Mexican

bilateral trade balances with Canada exhibit similar statistics as Mexican total trade balances’ statistics,

except with smaller magnitudes. ∗∗∗I use Laspeyres price index for CPI and real exchange rates, and unit

value index for terms of trade. Under Paasche price index, the correlations and standard deviations of

real exchange rates remain the same or increase slightly without switching signs.

24

consider default probability but believes its country has a higher steady-state productivity

than the actual level that the firms and the creditor country know (i.e., D1 = D2 = Dbut π = π1 > π2, as case (2) in Figure 3). More specifically, The borrowing govern-

ment believes E(e2) = 1.04 with all else being the same as the baseline calibration; that

is, the borrowing government perceived average productivity is about one standard de-

viation higher than the actual level. Although these two cases differ in the borrower’s

belief/concerns regarding default risk, they have similar results, as expected and illus-

trated in Figure 3. Unless otherwise stated, the analysis for the rest of this paper is based

on the baseline model results.

Table 2 shows that this model produces a debt-to-GDP ratio of about 27 percent

on average, while matching the 1 percent default frequency observed in the data. The

result that the debt-to-GDP ratio is lower than the data is common in the literature of

strategic sovereign default models. There are several main factors impacting this ratio

in the model, including the two countries’ discount factors, beliefs on default probability,

sovereign default costs, and risk aversion. In particular, risk aversion limits this model’s

ability to generate data-matching debt-to-GDP ratios (Lizarazo, 2013). However, it does

help my model support a data-consistent average bond spread, on which I elaborate below.

Model statistics for bond spreads are tricky in that during default periods the model

has no finite interest rate. I report in Table 2 the modeled bond spread statistics for

business cycles, with the infinite interest rates during default episodes being replaced by

the average Mexican counterpart from the data (10 percent). The mean of bond spreads

is close to the data. Here, the bond price reflects not only the expected return due

to the probability of default, but also compensation to risk-averse creditors for bearing

sizable consumption risk.28 On average about a third of the interest rate is attributed

to the risk premium from creditor’s risk aversion. 29 The impact of risk aversion on

the risk premium decreases relative to the impact of default risk as the borrower country

approaches a default. Therefore, unlike many previous studies using small open economies

with risk-neutral investors, this model breaks the close link between the probability of

default and bond pricing by including the creditor country’s welfare loss and risk aversion.

Meanwhile, the modeled volatility of bond spreads is smaller than the data.

In the model, the volatility of terms of trade is closer to the data than the volatility

28As explained in the next section, the creditor country suffers a long-lasting welfare decline once theborrower country defaults. The impact of the creditor country’s welfare loss on bond spreads followsa similar rationale of “rare disaster” as in Barro (2006) and Gabaix (2008), and is consistent with thefindings of Lizarazo (2013).

29To estimate that, I calculate the bond price without default risk as q(b, b′, s) = β1E1

∂U∂c′11λ1

, given thecurrent model result b′.

25

of real exchange rates is. When default risk increases or during default episodes, even

though the borrower country’s terms of trade deteriorate and its CPI declines, the creditor

country also adjusts its consumption towards the cheaper imported final good. It results in

a lower CPI for the creditor country as well, causing the borrower country’s real exchange

rate does not decline as much as its terms of trade do. Meanwhile, in the data, both the

terms of trade and the real exchange rate are influenced by many other factors during

business cycles, such as policies in trade, money supply, and nominal exchange rate, which

this model does not take into account.

Domestic good consumption is smoother in the model than in the data because of

borrowing, home bias preference, and labor movement from the intermediate good sec-

tor to the domestic sector during default crises. These three factors support domestic

good production and their consumption in spite of adverse productivity shocks. Total

consumption is less smoothed than domestic good consumption in the model on account

of the variations in imports and terms of trade over business cycles. It is also slightly

more volatile than output, as in the data. The volatility of trade balances is lower in the

model than in the data. Other sovereign default models have generated similar results.

For example, Aguiar and Gopinath (2007) produce a trade balance standard deviation of

0.95, Arellano (2008) 1.5, and Yue (2010) 2.81.

Next, Table 2 shows that this model does a good job of delivering the correlation

between GDP value and bond spreads, as well as their correlations with other variables.

It yields a negative correlation between bond spreads and GDP, consistent with the data,

because bonds have a higher default risk in bad states. As in Mendoza and Yue (2012), this

model produces countercyclical default risk in a setting where both income and default

risk are endogenous and affect each other, unlike in the models of sovereign default alone

or of business cycles alone.

However, this model distinguishes itself from Mendoza and Yue (2012) in that the

endogenous income and default risk interact through the movement of terms of trade. In

my model, both the terms of trade and the real exchange rate have a positive relation to

GDP and a strong negative relation to bond spreads, which is also consistent with the data.

As explained in the model mechanism section, when the borrower country accumulates

debt, the default risk and the interest rate rise, resulting in the country’s terms-of-trade

deterioration. This prevents real appreciation from easing its budget constraint and from

helping it to pay back debt that is denominated in the creditor country’s final good.

Therefore, default risk is further elevated to raise the bond interest rate. Once an adverse

productivity shock causes the borrower country to default, the country is penalized by an

additional income loss from a wage decline, causing its terms of trade and real exchange

26

rate to deteriorate sharply. This takes a third toll on the defaulting country’s income.

This mechanism, in which increased debt and default risk raise the real interest rate,

deteriorate terms of trade, real exchange rate, and income, explains the modeled relations

between GDP value, bond spreads, terms of trade, and real exchange rates. It also explains

the model-generated negative relation between trade balances and GDP, while producing

a positive relation between trade balances and bond spreads. These are consistent with

the stylized business cycle features in Mexico and other developing countries.

More important, the model also delivers procyclical trade flows and a negative relation

between trade flows and bond spreads consistently with the data, which have not been

captured by previous sovereign default models. During downturns, the value of both

imports and exports declines, partly because of the deterioration in the terms of trade.

Furthermore, the model predicts a correlation between the borrower country’s exported

intermediate good and its GDP or bond spreads, qualitatively in line with the correlations

observed in the Mexican data. More broadly, the business cycle correlations between

output and intermediate goods export value differ across countries but are usually positive.

For instance, using annual growth data (1988-2013), I compute the correlation for 16

countries for which I have intermediate goods export data. On average, the correlation

between output growth and intermediate goods export growth is 41 percent.30

As discussed earlier, the wage in borrower country 2 declines with productivity and

even more so during sovereign default episodes. It is confirmed by the model results, where

the wage strongly positively correlates with GDP and negatively with bond spreads, as

in the data and the findings of Li (2011).

In addition, this model disentangles the default-related loss of GDP volume in GDP

value. As I show in the next section, during default periods, about two thirds of GDP

value loss in the model is due to lower GDP volume, while the other third is attributable

to real depreciation. In Table 2, even though GDP value is positively correlated with

GDP volume, it is not a perfect correlation–only 65 percent in the data and 79 percent in

the model. The real exchange rate and terms of trade do play a role in explaining GDP

value changes in both the model and the data. Also, consistent with the data, the model

generates declining GDP volume when bond spreads increase over business cycles.

Last, I report in Table 2 the correlations between default and output, and between

default and bond spreads. In particular, the onset of a default event is positively correlated