INTERNSHIP REPORT ON A STUDY ON STATUTORY LABOUR COMPLIANCES WITH REFERENCE TO UKN PROPERTIES PRIVATE LIMITED By SHUBHA S USN: 1NZ14MBA60 Submitted to VISVESVARAYA TECHNOLOGICAL UNIVERSITY,BELGAUM In the partial fulfilment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under The Guidance of, Internal Guide External Guide Ms. ARADHANA YADAV Mr. SUNDARESH M (Professor, Dept. of Management) (GM-HR Admin & logistics) DEPARTMENT OF MANAGEMENT STUDIES NEW HORIZON COLLEGE OF ENGINEERING OUTER RING ROAD, MARATHALLI BANGALORE -560103 BATCH: 2014-2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTERNSHIP REPORT ON

A STUDY ON STATUTORY LABOUR COMPLIANCES WITH

REFERENCE TO UKN PROPERTIES PRIVATE LIMITED

By

SHUBHA S

USN: 1NZ14MBA60

Submitted to

VISVESVARAYA TECHNOLOGICAL UNIVERSITY,BELGAUM

In the partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under The Guidance of,

Internal Guide External Guide

Ms. ARADHANA YADAV Mr. SUNDARESH M

(Professor, Dept. of Management) (GM-HR Admin & logistics)

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING

OUTER RING ROAD, MARATHALLI

BANGALORE -560103

BATCH: 2014-2016

ACKNOWLEDGEMENT

I am thankful to NEW HORIZON COLLEGE OF ENGINEERING , BANGALORE for

gain knowledge in the masters degree programme with also doing a project by get

experience.

I have gained knowledge, small experience, learned a lot and become more matured as an

individual in the UKN Company.

I would like to thank Dr. MANJUNATH, Principle of new horizon college of engineering,

Bangalore for giving me a opportunity to do a project in the company to gain experience by

submitting the project report.

My humble gratitude to Dr. SHEELAN MISHRA, head of the department of management

studies, Bangalore. doing a project work in the UKN company who helped me out by

giving me their valuable suggestions.

I am deeply indebted to my project Guide. Dr. ARADHANA YADAV for giving me their

valuable time, advise, guidance, encouragement & help during the course of my project.

To begin with I Acknowledge & Express my Gratitude to HR department – Mr.

SUNDARESH, GM – HR, Admin & Logistics, Mr. SUNIL KUMAR, HR& Admin , Mr.

SATEESH KUMAR, Compliance Officer. UKN Properties Pvt Ltd. Bangalore for the

support & guidance which they rendered in spite of their highly busy schedule.

And last but not the least I am thankful to all of my friends & my parents who helped me a

doing a project.

SIGNATURE

SHUBHA.S

1NZ14MBA60

TABLE OF CONTENT

CHAPTER PARTICULARS

PAGE

NO.

EXECUTIVE SUMMARY

CHAPTER-1 1-7

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

1.10

INTRODUCTION ABOUT THE INTERNSHIP

TOPIC CHOOSEN FROM THE STUDY

STATEMENT OF THE PROBLEM

NEED OF THE STUDY

OBJECTIVES OF THE STUDY

SCOPE OF THE STUDY

METHODOLOGY

REVIEW OF LITERATURE

HYPOTHESIS

LIMITATIONS OF THE STUDY

CHAPTER-2 8-15

2.1

2.2

2.2.1

2.2.2

2.2.3

2.2.4

2.2.5

2.2.6

INDUSTRY PROFILE

COMPANY PROFILE

VISION,MISSION,QUALITY POLICY

SERVICE PROFILE

NATURE OF BUSINESS CARRIED

COMPANY COMPETITORS

FUTURE GROWTH &PROSPECTUS

SWOT ANALYSIS

CHAPTER-3 CONCEPTUAL FRAMEWORK ON STATUTORY

LABOUR COMPLIANCES

16-31

CHAPTER-4 DATA ANALYSIS AND INTERPRETATION

32-82

CHAPTER-5 FINDINGS,SUGGESTIONS,CONCLUSION

83-84

CHAPTER-6 BIBLIOGRAPHY

ANEXTURE

LIST OF TABLES

SL.NO TABLE.NO NAME OF THE TABLE PAGE.NO

1 4.11. working conditions * employee benefits

32

2 4.1.2 welfare activities * working environment

33

3 4.1.3 welfare activities * statutory compliances

34

4 4.1.4 welfare activities * social benefits

35

5 4.1.5 welfare activities * job description

36

6

4.1.6 working conditions * working environment

37

7

4.1.7 working conditions * satisfaction of facility

38

8 4.2.1 Gender of the respondents 39

9 4.2.2 Percentage of respondents from different Age

groups

41

10 4.2.3 Experience of the employees

43

11 4.2.4 Respondents shows company rules & regulations

45

12 4.2.5 Satisfaction about the job description

47

13 4.2.6 Eligible for ESI & EPF

49

14 4.2.7 Working conditions inside the company

51

15 4.2.8 Employee benefits provided by the organization

53

16 4.2.9 Maternity benefits provided by the organization

55

17 4.2.10 Deduction of employees professional tax

57

18 4.2.11 Employer providing holiday for sickness

59

19 4.2.12 Working environment provided by the organization

61

20 4.2.13 Benefits for the employees

63

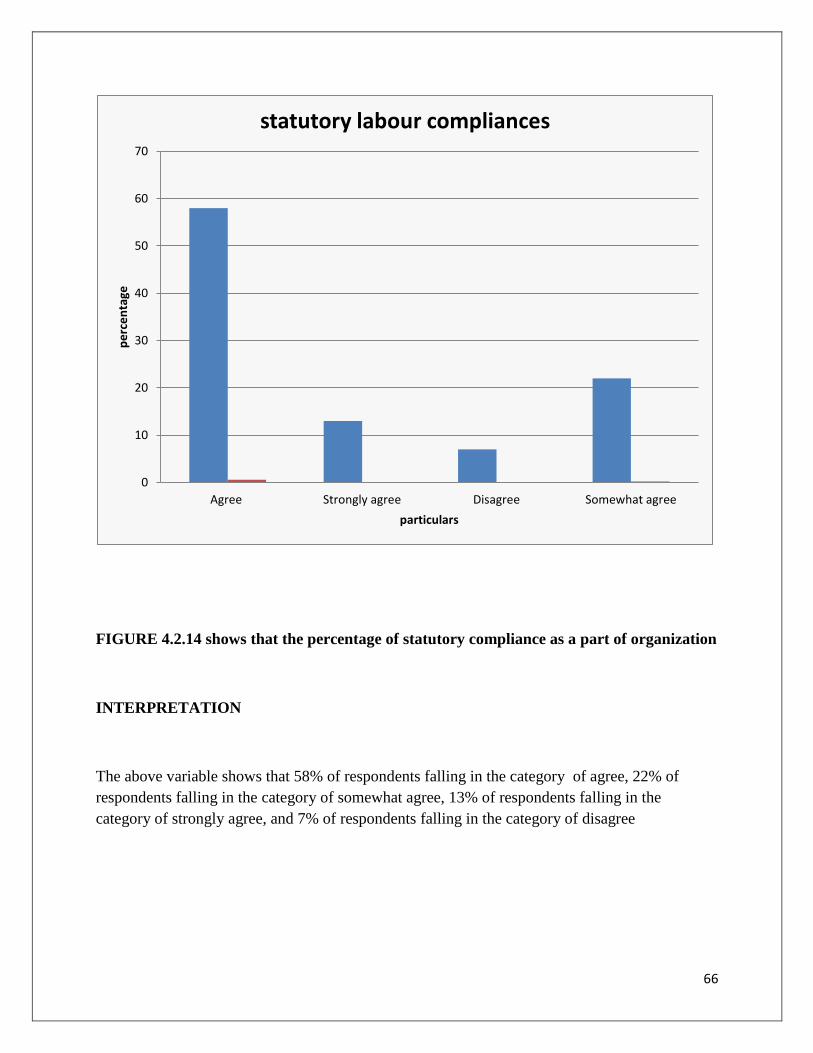

21 4.2.14 Statutory labour compliance is a part of organization

65

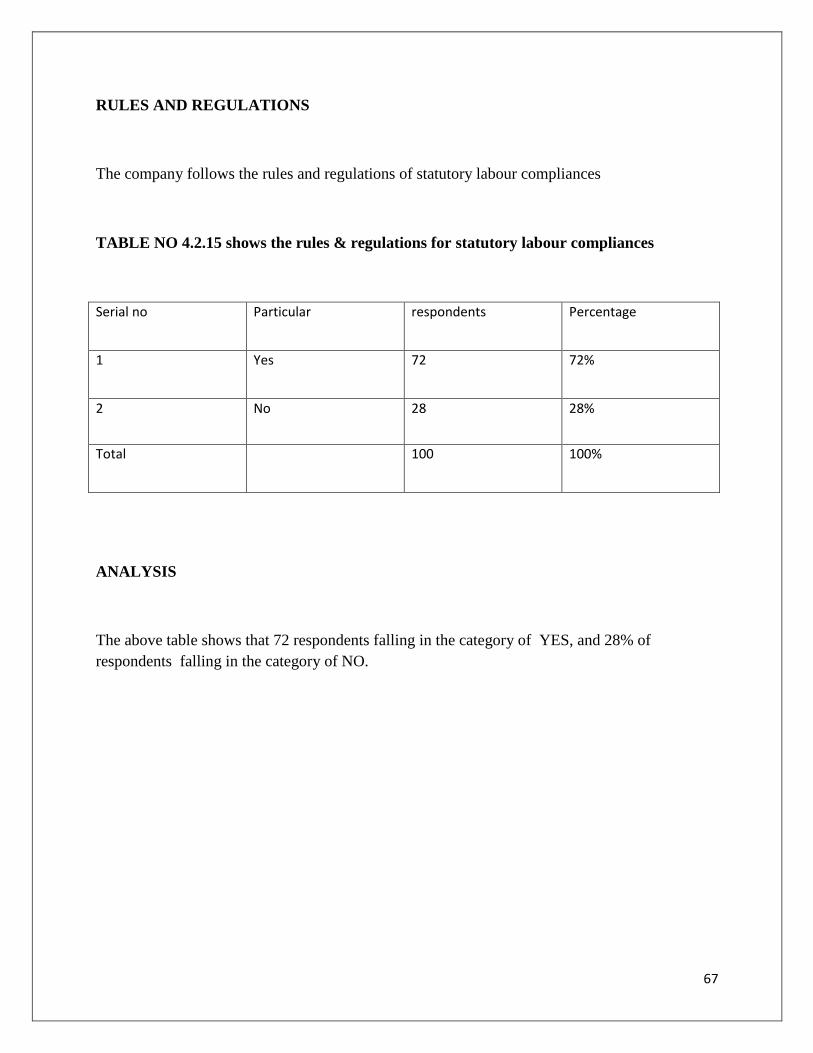

22 4.2.15 Rules & regulations of statutory labour compliances 67

23 4.2.16 Social & saving benefits provided by the organization

69

24 4.2.17 Employees insurance scheme

71

25 4.2.18 Pension gets in the period of retirement

73

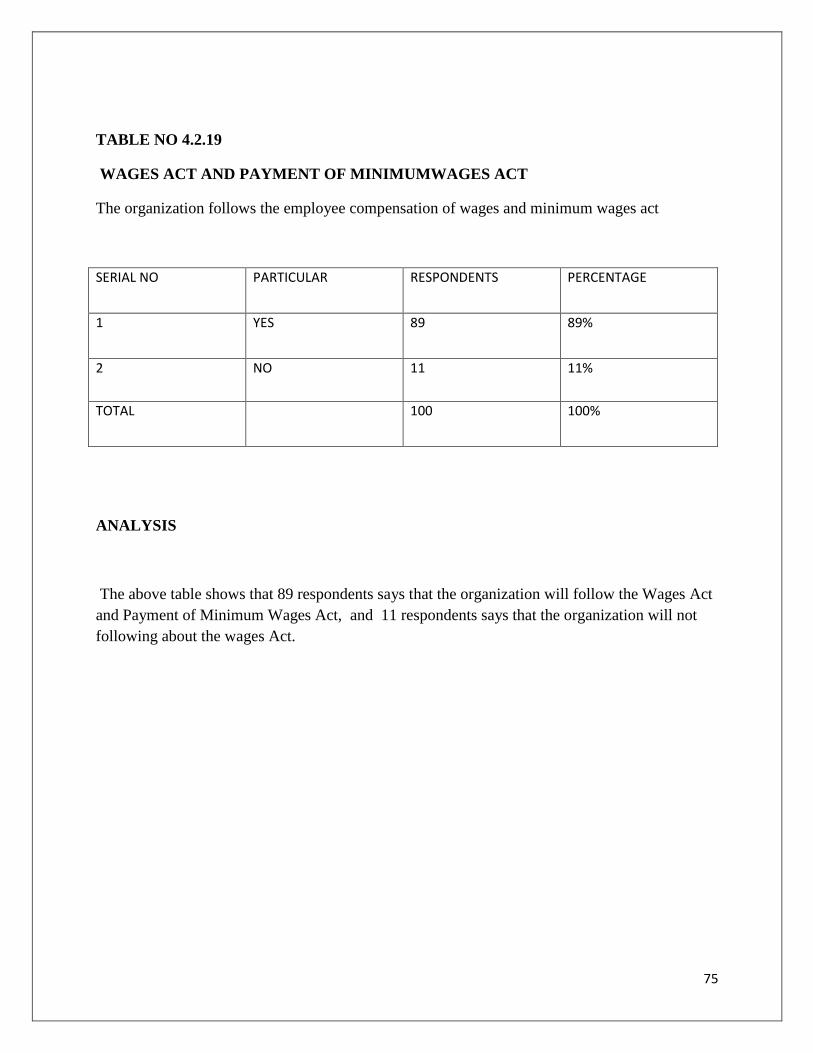

26 4.2.19 Payment of wages & minimum wages act

75

27 4.2.20 Deductions of ESI, EPF & Renewal process

77

28 4.2.21 Satisfaction of facilities provided by the organization

79

29 4.2.22 Facilities of employees welfare activities 81

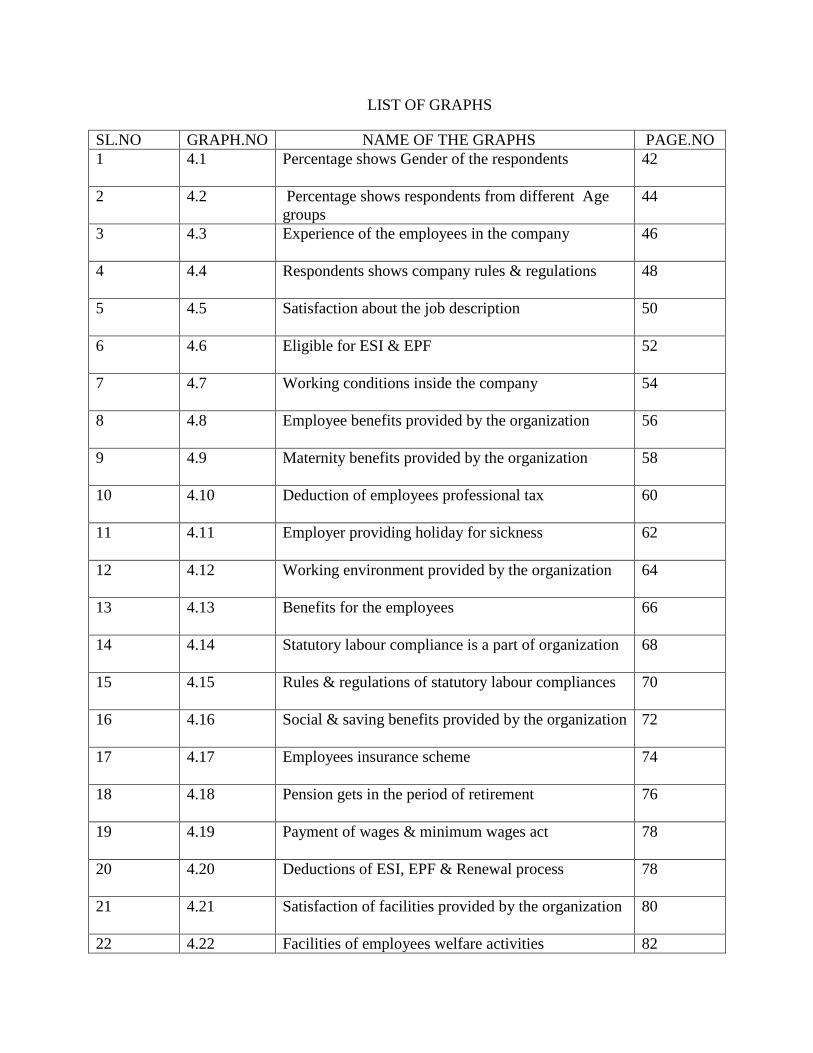

LIST OF GRAPHS

SL.NO GRAPH.NO NAME OF THE GRAPHS PAGE.NO

1 4.1 Percentage shows Gender of the respondents

42

2 4.2 Percentage shows respondents from different Age

groups

44

3 4.3 Experience of the employees in the company

46

4 4.4 Respondents shows company rules & regulations

48

5 4.5 Satisfaction about the job description

50

6 4.6 Eligible for ESI & EPF

52

7 4.7 Working conditions inside the company

54

8 4.8 Employee benefits provided by the organization

56

9 4.9 Maternity benefits provided by the organization

58

10 4.10 Deduction of employees professional tax

60

11 4.11 Employer providing holiday for sickness

62

12 4.12 Working environment provided by the organization

64

13 4.13 Benefits for the employees

66

14 4.14 Statutory labour compliance is a part of organization

68

15 4.15 Rules & regulations of statutory labour compliances

70

16 4.16 Social & saving benefits provided by the organization

72

17 4.17 Employees insurance scheme

74

18 4.18 Pension gets in the period of retirement

76

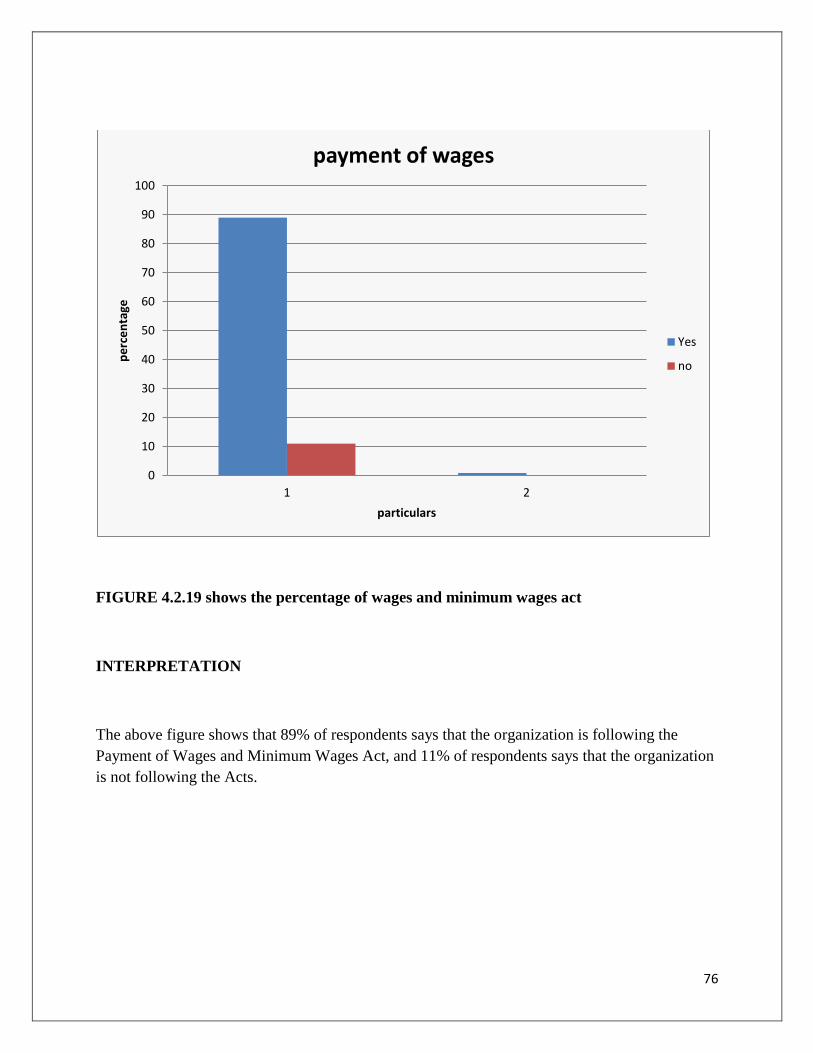

19 4.19 Payment of wages & minimum wages act

78

20 4.20 Deductions of ESI, EPF & Renewal process

78

21 4.21 Satisfaction of facilities provided by the organization

80

22 4.22 Facilities of employees welfare activities 82

EXECUTIVE SUMMARY

The project report explains about the study done for the purpose of project and company This

study is on the “Statutory Labour Compliances” in UKN Properties Pvt Ltd, Whitefield,

Bangalore. The review helps to gain a goal sight. All details are covered in a summarized form.

Introduction of the study contains introduction about the internship, Topic chosen for the study,

Need for the study, Objectives of the study, Scope of the study, Methodology adopted, Literature

review and limitation of the study.

The data collected by two sources i.e. Primary and secondary data. Primary data collected with

the direct interactions with the officials and secondary data was collected with the help of past

records, company websites and other source of information etc.

Industry profile also prepared to know how the Real Estate sector came into existence and the

development in India.

Company profile contains Vision, and Mission and Quality Policy, Service profile, Competitors

information, SWOT analysis, future plans.

While preparing this report it has been tried to reveal the insights of the study and a few

recommendations and suggestions were also prescribed based on the observations and findings.

I have also applied few research tools like questionnaire and survey methods to obtain the

information from the respondents and thereby have analyzed the factor by using Bar chart.

As part of my project programme I got a chance to work at this area for a period of 10 weeks.

During this period I have learned about this company and its work environment.

1

CHAPTER – 1

1.1 INTRODUCTION ABOUT THE INTERNSHIP

INTRODUCTION OF STATUTORY LABOUR COMPLIANCES:-

The internship is about a statutory compliances, it is necessary for all small and large

companies in the world to keep their businesses secure from a legal problem. An increase

knowledge of the statutory labor compliances is important to minimize the problem associated

with the noncompliance of statutory requirements.

In today‟s competitive and legal business world, it is most important for employers to manage

statutory labour compliances. every country has many types of compliance needs.

There are number of statutory requirements for Indian companies and companies have to spend a

significant amount of time in their payroll management to ensure that they are compliant with

the legal regulations. If companies fall to adhere to statutory compliances, they may have to face

heavy penalties and problems which are several times more than complying with legal

guidelines.

MEANING OF STATUTORY LABOUR COMPLIANCES:-

Statutory compliance refers to the legal framework within which organizations should operate,

to treatment of their employees.

Every country has several hundreds of federal and state labor laws that companies need to align

with. This list is forever being added to.

The company‟s effort and money goes into ensuring compliance to these laws which could deal

with a range of problems, with the payment of minimum wages to maternity benefit or

professional taxes.

Therefore dealing with statutory compliance requires for companies to the well- versed with the

various labor regulations in their country operation.

2

DUTIES OF AUTHORITIES :-

Statutory compliances is very essential to each & every organization in India. We have to

maintain all kinds of workers like managers, staffs, skilled, unskilled, executives & any kind of

workers in every month under the Karnataka shops & establishment act, the employees pension

scheme 1995the inspectorates of factories act 1947, the minimum wages act,

The Payment of the wages act 1936, the payment of the gratuity act 1972, the payment of the

bonus act 1965, the equal remuneration act 1976, the maternity benefit act 1961, the trade unions

act, the workmen compensation act, the intermigration act, the building of constructions workers

act, the professional tax & service tax act.

Statutory compliances is one of the main important thing in hr department & applicable to all

kinds of establishments. As per act we have to maintain statutory labour compliances in the

company.

ROLES & RESPONSIBILITIES :-

1) Collecting workers details.

2) ESI card issued to the workers.

3) Smart card process.

4) Submitting ESI returns

5) Maintaining ESI returns & ESI paid Challns file

6) Preparing PF nomination forms

7) PF settlement case

8) PF death claim process

9) PF slip process

10) EPF Records- monthly, annual returns submitting to the PF office.

11) Attendance statements checking

12) Visiting to the EPF office, ESI regional office, branch offices, labour office for

submission of records & getting about new notifications, implement matters.

13) Visiting to every projects for verifying workers attendance register, in time out time,

drinking water, rest room etc.

14) Advising to all contractors for maintaining labour statutory compliances under labour

laws.

3

CONTRACTORS – RESPONSIBILITIES :-

All contractors are working under principle employer at the site. What ever happened at the

working place principle employer is the hole responsible because all contractor workers working

at employer place. So we need to take care of all workers include company workers also at the

site.

We have to prepare labour compliances for contractors also under contract labour act, BOCW

Act, PF Act, ESI Act, WCA Act, Professional Act, Bonus Act, equal remuneration act & labour

welfare fund act.

Every month all contractors without fail they have to give labour compliances along with bill to

the principle employer. Below list has given what all records to be producing to the principle

employer

1.2 TOPIC CHOOSEN FOR STUDY :

UNDERSTANDING OF STATUTORY LABOUR COMPLIANCES

1.3 STATEMENT OF THE PROBLEM:

A failure to pay the ESI / EPF of employees, from the company due to the under maintenance of

the employees registers, and facing problem in the inspection.

And also working environment provided by the company.

1.4 NEED OF THE STUDY

To find the labour welfare which helping and providing good industrial relation

To find out the employees satisfaction towards the welfare actions

To know on the facilities provided by the company

4

1.5 THE OBJECTIVES OF THE STUDY :

To study the methods of a statutory compliances with HR with the special reference to

UKN Properties pvt.ltd

To identify the specific sectors or avenues for employees statutory compliances

To study the welfare facilities provided by the organization

To suggest the improvement for quality of working environment

1.6 SCOPE OF THE STUDY :-

The learning is to come across out a satisfaction of the employees, whether the organization is

providing Necessary statutory compliances for employees and also health, safety, and welfare

measures in UKN Properties Pvt. Ltd. Bangalore. This study improves the employees facilities

provided by the organization and making good payroll system.

1.7 METHODOLOGY:-

To satisfy the objectives of my study. I have taken both into thought the primary & secondary

data.

1.7.1 THE PRIMARY DATA:

The primary data is used from beginning to end Questionnaire methods for collecting

employees information of various departments in the organization.

The data is collected specially for project at pass and directly during questionnaire and

personal communication.

1.7.2 THE SECONDARY DATA:

The data is collect from the company information and files.

The data is also collected by books, internet, articles and employers

5

1.8 REVIEW OF LITERATURE :-

According to Ashwathappa (2010)

In his book HRM "talked about the differed styles of settlement and administrations given to

representatives as far as pay for time not worked, protection edges, pay advantages, annuity

arranges and so on.., conjointly specified the approaches to advantage the advantages and

administrations inside of the higher strategy.

According to Sathishkumar L and Nataraj (2009)

have expressed that there is a pressure between the part of exchange unions and specialists'

congresses, which parallels the strains talked about in the Dutch circumstance. Branine examines

the opposing effect of the work market changes Chinese specialists and shows how the Chinese

State has responded to the negative effect of the change by passing a surge of work laws

intended to minimize modern distress.

Sathishkumar L and Nataraj V (2008)

have discovered that the goals of the work strategy changes appear to be just in part

accomplished and advance improvements in these regions will be of hobby and worry to

mechanical relations scholastics all through the world. In seeking after them we ought to be

aware of the proposal from Watson that the main regimens orders of the sociologies ought to be

utilized to look at the occupation relationship instead of attempting to raise Human Resource

Management or Industrial Relations to the status of isolated controls.

According to Binoyjoseph, and josephinjodey (2009)

in his articles examines has bring up , the structure of the welfare states on a government

disability fabric. Bosses, government, and the exchange unions have done a great deal to elevate

to the improvement of the working conditions.

6

According to Maruthimuthu k, (2003),

has watched that the general impression is that an environment of fulfillment wins on grounds,

however there is degree for changes in specific regions like amusement offices, and reward. With

usage of inventive plans and upgrades, better work administration relationship might be built up

and kept up in future.

Report on the National labour commission (2002),

Administration of India, made suggestions in the region of work welfare measures which

incorporate government managed savings, amplifying the utilization of the Provident Fund, tip

and unemployment protection and so forth. Shobha Mishra and Manju Bhagat, in their

"Standards for Successful Implementation of Labor Welfare Activities", expressed that work

truancy in Indian commercial ventures can be lessened, all things considered, by procurement of

good lodging, wellbeing and family mind, bottle, instructive and preparing offices and

procurement of welfare exercises. The standard for effective execution of work welfare exercises

is only an augmentation of majority rule

According to David (2001)

Robinson in his book, of individual/human asset administration says the an assortment of

settlement and administrations given by the organization to their laborers. The legitimately

fundamental administrations and settlement contain standardized savings premium, joblessness

remuneration, representatives pay and circumstance inability programs. They feel that cost of the

picked advantages offered seems, by all accounts, to be developing.

According to Michel (2001)

His book, human resource organization and human relations says that the acquirements of intra-

divider painting welfare offices help in improving the way of work of delegate thusly incredible

human relations will make among different carders of representatives.

7

1.9 HYPOTHESIS :-

The acts following by the organization of the employees works as an agent for the growth

of and also motivates the employees to perform well employee work is the value able

outcome of sound of statutory labour organization.

Ensures healthier growth of organization in terms of business & motivation among

managers.

The acts in UKN makes the employees safety and facilities

1.10 LIMITATIONS OF THE STUDY :-

Because of the high busy schedule of employees it was difficult to interact with the

company

Employees feel uncomfort to answer the questions about the welfare measures

Employer rejected some questions about the organizational activities because of the

confidential

8

CHAPTER – 2

2.1 INDUSTRY PROFILE :-

UKN PROPERTIES PVT LTD.

Land or building advancement or property improvement, is a multilevel business, doing

movements that ranges beginning the remodel and liberate of vacant structures to the buy of

unfinished area and the suggest of better land or building to others. varying over belief on paper

into real property. Land improvement if single in relative to development, though numerous

engineers likewise build.

construct the structure, and rent manage, and at last suggest it. Designers employment with

various partners along every progression of this procedure, including modelers, engineers,

surveyors, city organizers, assessors, contractual workers, renting specialists and that's just the

beginning. Organizations in this industry go after administration contracts the world over. The

sorts of temporary workers fluctuate as per each phase of the business cycle. In the early part of a

monetary rise, transportation interest will get, raising framework spending. Once a recuperation

has grabbed hold, business pick up certainty and acknowledge money for development. In testing

times, rivalry in this area can be savage. At the point when both government and business is rare,

contract value rivalry warms up, forcing net revenues. The boundaries to section in this industry

are high, given the size and many-sided quality of ventures and capital financing required.

The greater part of individuals from the Heavy Construction Industry are Capital concentrated.

Be that as it may, the organizations don't for the most part convey substantial obligation troubles.

Administration are entirely traditionalist. In fact, obligation proportions are regularly under 30%.

A couple organizations primarily engaged of giving administration and building administrations,

are most work concentrated. Most development undertakings are long haul, and income is

genuinely simple to foresee, as are profit, through the business cycle. Rich income guarantees the

subsidizing of everyday operations.

In great times, abundance money is put aside for inward and outside extension. Amid testing

periods, some money might go toward obligation retirement and regular stock buybacks in

backing of the offer cost. For the most part, these organizations are not known not liberal payers

of profits. We alert preservationist speculators that overwhelming Construction stocks can be

fairly unpredictable in times of vulnerability. The UKN Properties Pvt Ltd is one of the main

manufacturers of Bangalore, which has effectively finished numerous private ventures. The

9

UKN is a Leading Real Estate Company that has been built up to satisfy the expanding

development needs. The organization is good to go to accomplish an apex position in the Indian

Real Estate. The business house is a group of inventive personalities and experts to strive to

convey life to the artful culminations that are best in the business sector and all the innovators.

With inventive designing, incredible engineering and stunning completion, each undertaking for

the organization is class definer. The organization pushing forward with the mission of finishing

consumer loyalty, quality control and giving worth to your well deserved cash.

2.2 COMPANY PROFILE :-

INTRODUCTION OF A COMPANY

The UKN is motivated by a logic of element structures and unequivocally expressiveness. UKN

makes properties that are grand, yet grounded in a comprehension of human settings and

profound engagement with contemporary materials and procedures.

In the previous decade, we've connected these standards to Create Commercial, Retail,

Residential, and Hospitality Buildings that are tastefully inspiring and additionally especially

useful and eventually, empathetic.

Our group is experienced, excited and focused on working with you to make structures that serve

human needs, while hoisting human experience. To summarize the working with you to make

structures that serve human needs, while raising human experience. To reword the American

Architect and visionary Louis Kahn, we start with the unlimited and use quantifiable intends to

make something that, at last, should be inconceivable – putting resources into vastness.

HISTORY OF A COMPANY :-

The organization UKN PROPERTIES PVT LTD was begun in the year 1997 under the

organizations demonstration 1956. The company‟s registered office is on Residency Road and

the corporate office is at sigma soft tech park, Whitefield, Bangalore. Mr. Gautam U Nambisan

is the main promoter and chairman of UKN Properties Pvt Ltd. Under his leadership the

company undertook various residential and commercial projects independently and also with the

other partners many of which are exclusively for top executives of software companies and also

high net worth individuals. The company employs more than 100 people and has approximately

10

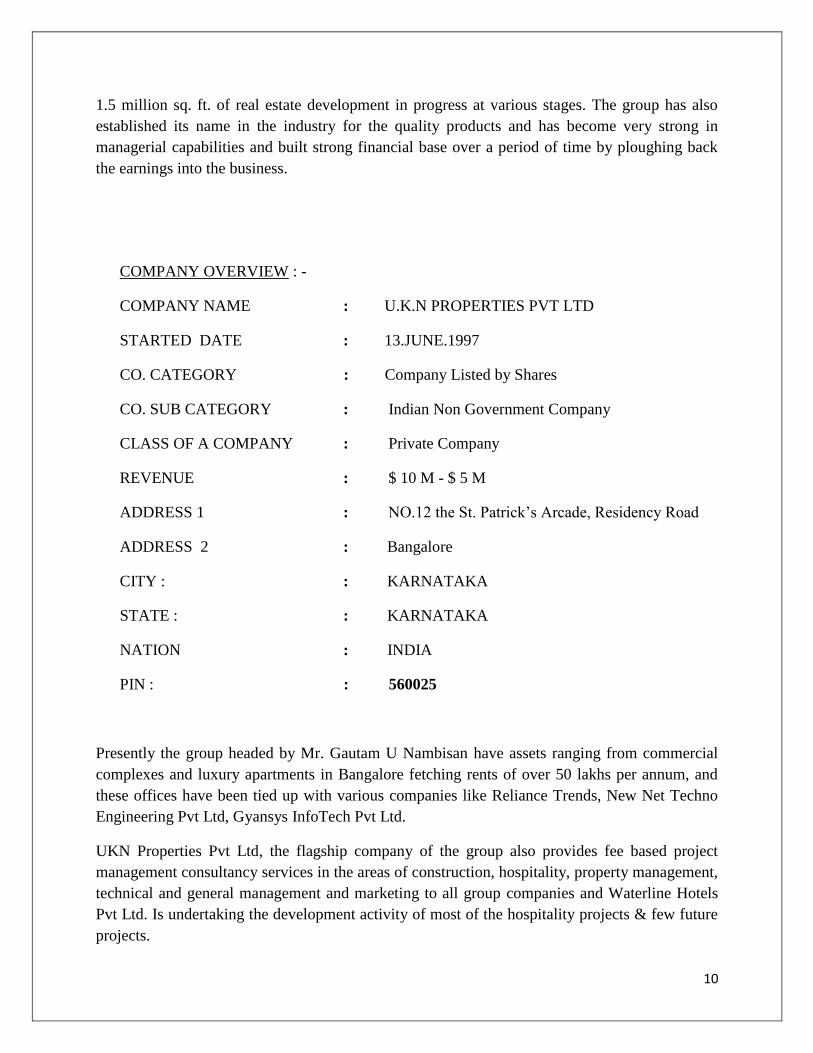

1.5 million sq. ft. of real estate development in progress at various stages. The group has also

established its name in the industry for the quality products and has become very strong in

managerial capabilities and built strong financial base over a period of time by ploughing back

the earnings into the business.

COMPANY OVERVIEW : -

COMPANY NAME : U.K.N PROPERTIES PVT LTD

STARTED DATE : 13.JUNE.1997

CO. CATEGORY : Company Listed by Shares

CO. SUB CATEGORY : Indian Non Government Company

CLASS OF A COMPANY : Private Company

REVENUE : $ 10 M - $ 5 M

ADDRESS 1 : NO.12 the St. Patrick‟s Arcade, Residency Road

ADDRESS 2 : Bangalore

CITY : : KARNATAKA

STATE : : KARNATAKA

NATION : INDIA

PIN : : 560025

Presently the group headed by Mr. Gautam U Nambisan have assets ranging from commercial

complexes and luxury apartments in Bangalore fetching rents of over 50 lakhs per annum, and

these offices have been tied up with various companies like Reliance Trends, New Net Techno

Engineering Pvt Ltd, Gyansys InfoTech Pvt Ltd.

UKN Properties Pvt Ltd, the flagship company of the group also provides fee based project

management consultancy services in the areas of construction, hospitality, property management,

technical and general management and marketing to all group companies and Waterline Hotels

Pvt Ltd. Is undertaking the development activity of most of the hospitality projects & few future

projects.

11

ABOUT :- GAUTAM NAMBISAN- Chairman, UKN PROPERTIES PVT LTD

Mr. Gautam Nambisan is a Young business visionary with a recognition in inn administration

and undertaking different prestigious private business friendliness and resort extends freely and

as joint endeavors. He has created ability in the venture advancement, arranging, fund and

promoting. The association has likewise created to meet the continually expanding requests of

the developing business. His capacity to manufacture organizations together with vital

accomplices and sharp eye for point of interest is understood.

Under the stewardship of Mr.Gautam Nambisan the gathering is included different multi-million

dollar private and business activities of more than 5 million sft. Al Bangalore and Kerala He is

autonomously developing top of the line resorts, inns, private activities, and shopping centers in

different urban communities in south India.

“ LUXURY SHOULD COME IN SMALL NUMBERS ”- said Gautam Nambisan, Chairman of

UKN company.

2.2.1 VISION AND MISSION QUALITY POLICY :

VISION AND MISSION

CORPORATE VALUES OF AN Organization

1. ENDURING – as a complete, Ukn‟s primary giving and a lot of significantly, a durable

relationship.

2. PRICE CREATION – Ukn remains for formation of qualities for different partners like

house proprietors, clients, business accomplices, specialists, merchants staff and partners.

3. CLEAR – to make trust, Ukn has faith in being clear as an association by and large its

operations right from the declarations of a benefit to its consummation.

4. DISTINCTIVE – the sole on account of emerge from the culmination is by being

particular and best in class arrangements at every phase of an undertaking, be it's an open

lodging venture or a blended use office.

12

QUALITY POLICY :

UKN is a leading real estate and hospitality development company based in Bangalore, having

debt-free land holdings in Bangalore, Kerala and Tamil Nadu, currently developing over

2.5million sq. ft. in these locations.

Real Estate Development Products

MIRAYA characterizes our work and outline theory that motivates the customary and

contemporary. Miraya is UK's ultra extravagance home offering with very much determined

outline and top of the line specification. Whitefield is the hub of our developments at Bangalore

and waterfront locations in Kerala. Miraya product offering linked with mixed use of hospitality

& ultra luxury deliver superior value and returns. We limit the development to a maximum of 87

units as we believe luxury comes with limited numbers. UKn carefully selects the

land/partnerships for design development & joint developments. Through joint developments,

UKn has a track record of providing superior values and revenues to our partners.

BY UKN

By UKn is the luxury product designed to cater the needs of our customers. Our products like :

Esperanza has remarkable courtesies, regard for the most modest subtle element solace

and accommodation, astutely – arranged loft designs and excellent perspective of nature.

It is a cutting edge wonder of eco – living flawlessly mixed into the urban scene

exquisitely created homes intended to give the ideal mix of space and way of life. Euro

styling and outline yet remembering Indian sensibilities at all levels from basis to plan

and rises.

Belvista has an expansive living area which gives approach to roomy outside porches

with a characteristic beat spilling out of space to live with vertical patio nurseries.

Sumptuous tiled floors to living regions and exquisite avoiding grapple the rooms, while

luxuriously designed crown cut timber entryways include profundity and measurement

Interlaken : it themes to the concept of “ use of space” . supremely comfortable

residences, planned living zones that change the space into a home – proprietor's

pleasure. The exemplary European style is an unpretentious feeling outlined with a

repeating theme of wood steady platte of common materials.

13

HOSPITALITY

ALiLA oversees one of a kind city inns and resorts in the Asia Pacific locale. The Hallmark of

ALiLA is in vogue, unwinding situations and magnificent cordiality that makes a one of a kind

visitor experience, ceaselessly reclassified to mirror the absolute best of a contemporary way of

life.

2.2.2 SERVICE PROFILE :-

The UKN is a service provider residential, commercial building construction and construction

project services to the customers.

They provide quality service to customers

2.2.3 NATURE OF THE BUSINESS CARRIED :-

UKN Properties Pvt Ltd deals in construction / leading construction /real estate company in

Bangalore. The UKN properties also suitable for Commercial, Retail, Hospitality, Residential

Buildings. The company is managing long term relationships with customers they develop a

solutions that they enrich the way of people work, learn, live & play. It is a spirit of innovation

The projects of a company namely

14

MAJOR PROJECTS OF UKN :-

UKN RESIDENCE PROPERTIES Namely :

1. The BELVISTA

2. The ESPERANZA

3. The MIRAYA ROSE

4. The MIRAYA GRANT

5. The INTERLAKEN

6. THE BELVEDERE

7. The MIRAYA GARDEN

8. The MIRAYA PARK

These are the projects carried out by the company UKN.

2.2.4 COMPANY COMPITITORS :-

Some of the competitors

1. KRISTAL GROUP

2. VAISHANVI GROUP

3. DAADYS BUILDERS PVT LTD

4. PRESTIGE ESTATE PROPERTIES PVT LTD

2.2.5 FUTURE GROWTH & PROSPECTS :-

Planning For Big Projects

2.2.6 SWOT ANALYSIS OF THE COMPANY :-

STRENTHS of the UKN

UKn company always looks a new and situation of the art solutions at every phase of

a project.

UKn provides safe & healthy work environment for its employees.

UKn took a part of social responsibility, the company is doing a socially responsible

activities

Availability of skilled manpower

Strong departmentalization structure in the organization

Good co-ordination between the employees

15

WEAKNESSES of the UKN

High amount of money need to be invested in hospitality projects

Limitations for banks to fund real estate & hospitality projects

Existing workforce (laboures) takes longer time to adopt to the changing skill

requirements

Scarcity of skilled resources

Initial huge investment in hospitality sector

OPPORTUNITIES of the UKN

Growth of the market

Huge demands for affordable cost of the residence

New IT will constructed nearby locale

anticipated new link road

THREATS of the UKN

Large number of competitors

Economic downturn

Increase the cost of land, labour, resources

Government policies

16

CHAPTER – 3

3.1 CONCEPTUAL FRAMEWORK ON STATUTORY LABOUR COMPLIANCE

MEANING AND DEFINITION OF LABOUR WELFARE

Labour welfare is an essential measurement of mechanical connection, it incorporates general

welfare offices intended to fare thee well a prosperity of representatives and with a specific end

goal to expand their expectation for everyday comforts . it can likewise gave by the legislature,

non-government offices and exchange unions.

Welfare has been for the most part acknowledged by bosses as a social right to gain offices along

these lines, the administration additionally impedance and acquaints enactment from time with

time to get the consistency giving such luxuries. The mediation of the state, in any case, is just to

enlarge the territory of its relevance.

Work welfare incorporates the setting up of least attractive guidelines of procurement of offices

like wellbeing, therapeutic help, sustenance, protection, garments, training, professional stability

diversion and so forth such offices empowers the specialist and his gang life and the social life.

Work welfare enhances the wellbeing, security, welfare and general prosperity of the specialists.

It is stood up to those exercises which are embraced statutory or something else, inside the

modern specialists and their relatives e.g. entertainment medicinal, instructive washing,

showering, transport offices, bottles and crèches, and so forth hence, the term work welfare

covers the specialists as well as their families.

DEFINITIONS

• The ILO season confined at NEW DELHI in the year 1947 characterized "work welfare

is an administrations offices and civilities, which might be set up in, exercises to empower

persons utilized in that to make their work in solid, and well disposed foundation and to give

them offices conductive to great physical condition and great assurance"

17

• M. Joshi felt the work welfare "alludes to every one of the endeavors which a

representatives in abundance of the base standard of working conditions settled by production

lines act and the far beyond the procurement of social enactment giving against mischance,

maturity, affliction and the unemployment"

• The board of trustees of work welfare (1969) characterized work welfare "alludes such

administrations, offices and luxuries as a satisfactory bottles, rest and diversion offices, clean and

medicinal offices, course of action for travel and for the work and from convenience of

specialists utilized at a separation from their homes and such different administrations, comforts,

and such offices including standardized savings measures as an add to enhance the conditions

under which laborers are utilized"

SCOPE OF LABOUR WELFARE

Labour welfare is the self-spurred idea that gains new extents with the adjustments in the

surroundings of the business. It was as an early a 'Whitley commission watched' welfare is one of

which should fundamentally be versatile, bearing a some what distinctive translation in one

nation from each other, as indicated by the diverse social traditions, the level of industrialization

and an instructive advancement of a specialists.

The Rage advisory group (1946) watched that we wish to incorporate welfare activities anything

accomplished for scholarly, moral, physical, monetary improvement of specialists whether by

boss, government or different offices, well beyond gave by law or under some agreement and

what is ordinarily far beyond given by law or under some agreement and what is typically

expected as a major aspect of the agreement for administrations. the study group, the

administration of India in 1960 to inspect work welfare conduct then existing, partitioning the

whole scope of these exercises into 3 bunches they are

i. Welfare inside of the regions of a foundations medicinal guide, containers, creches,

supply of drinking water and so on..,

ii. Welfare external surface the foundation procurement for indoor and open air

entertainment, lodging, visual guidelines, grown-up instruction and so forth..,

iii. Social security

18

CLASSIFICATION OF WELFARE MEASURES

1. Statutory welfare measures

2. Non statutory welfare measures

1. Statutory : it must be given regardless of the measure of a foundation, say, drinking

water. Furthermore, those which must be given subject to the job of a predetermined number of

individuals, e.g.., crèche additionally a piece of statutory welfare conveniences.

2. Non – statutory : in the event of a specific luxuries, there are no base standard set down

as in the circle of lodging, amusement, transport, medicinal and instructive offices. This is left to

the prudence of the business.

1. STATUTORY

Procurements For Factories Act Regarding Labor Welfare Area 42 to 49 of the processing plants

act, 1948 has contain procurements identifying with welfare of work. Sec42 to 45 apply to all

production lines regardless of various laborers utilized. Sec 46 to 49 Are pertinent to processing

plants utilizing more than a predefined number of specialists.

These procurements are talked about beneath :

Washing facilities (sec.42) :

in each processing plant :

a) adequate and suitable pleasantries for washing might be given and kept up to the

utilization of laborers

b) Separate and enough offices might be accommodated the utilization of male and female

specialists

c) The offices might be helpfully open and should be kept clean.

19

Facilities for capacity and drying clothing(sec.43) :

The legislature might have the appreciation of any production line, class, or depiction of

manufacturing plants, make rules requiring the procurements in that of suitable spots for a

continuing garments not worn amid working hours and for the drying of a wet attire.

First-help appliances(sec.44) :

there might be in each production line be given and kept up to be prepared available amid every

single working hour emergency treatment boxes or pantry furnished with the concurred

substance, and the quantity of a such boxes or an organizers to be given and kept up should not

be under one each one hundred and fifty laborers commonly utilized at any one time in the

industrial facility.

Canteens (sec.46) :

The state government have might decides requiring that in any predefined production line

wherein more than two hundred and fifty specialists are a normally utilized, a container or a

flasks should be given and be kept up by an occupier for the utilization of their laborers.

Shelters, rest rooms, and lounges( (sec-47) :

In each plant wherein more than one hundred and fifty laborers are normally utilized, sufficient

and suitable asylums of rest rooms and a suitable lounge, with procurement for drinking water

specialists can eat suppers brought be them, should be given and kept up to the utilization of

specialist.

Crèches (sec.48) :

In each processing plant wherein more than 30 ladies specialists are usually utilized, there should

be given and kept up a suitable spaces for the utilization of youngsters under the gage of six

years of a such laborers.

Welfare officers (sec.49) :

in each processing plant wherein five hundred or more specialists are usually utilized, the

occupier should be utilized in the manufacturing plant such various welfare officers as might be

a recommended.

20

2. NON-STATUTORY

Economic administrations :

the workers are frequently need cash for buy of a bike, bike, T.V.., fan, sewing machine, and so

on.., to raise their standard of clearing out. The business might be propel then the cash which

would be a paid back by the workers as a regularly scheduled payments to be deducted from

their pay rates. The workers might likewise be prompted to develop their own an assets for future

possibilities.

Recreational administrations :

The administration might give, for recreational offices. More pleasing casual climate is to

advanced through the contacts and the connections developed in the recreational occasions. The

administration might be accommodate indoor amusements like table tennis in a typical space for

workers. The instance of a major associations, administration might likewise organize a play

areas for outside diversions and incorporate the specialists to plan groups to play a matches with

other comparable groups.

Facilitative Services :

These are an accommodations which the workers commonly require, for example,

i. Housing Facilities :

Some association develop a pads for their workers and give to be the same either free or at an

ostensible rent. At times, money pay are given while in different cases, advances are progressed

to the workers to empower them to build or buy their own particular houses or pads.

ii. Medical Facilities :

the physical condition is one of the preeminent possessions for the representatives and it is

however typical that there might be an a few wounds as a result of mishaps while working. So

medical aid offices must be accommodated inside of the manufacturing plant area. Likewise,

restorative framework is by and large in operation under which a pay of medicinal costs really

21

caused is permitted. The association might likewise concurred specialists from whom the

representatives might get benefits on account of need.

iii. Educational Facilities :

the instructive offices might be given by the association to the workers youngsters by opening of

a school for them.

iv. Washing Facilities :

the required to accommodate wash bowls and washing comforts to be an advantageously

reachable to every one of the laborers which ought to be a slick, appropriately partitioned and

screened for the utilization of male and the female workers.

v. Leave Travel Concession :

the associations discount real admissions acquired by worker in under-taking a visit the length of

with his or her wife and the minor youngsters once amid the specific.

DIFFERENT ACTS APPLICABLE IN “UKN PROPERTIES PVT LTD ”

ACTS APPLIACABLE IN UKN PROPERTIES PVT LTD:-

The CONTRACT LABOUR (R & A) ACT

The PAYMENT OF WAGES ACT

The MINIMUM WAGES ACT

The EMPLOYEES‟ STATE INSURANCE ACT

The PAYMENT OF BONUS ACT

The EMPLOYEES PROVIDENT FUND & M.P ACT

The MATERNITY BENEFIT ACT

The LABOUR WELFARE FUND

REQUIREMENTS UNDER DIFFERENT LABOUR LAWS:-

the establishment of UKN properties of a companies are mandatory to meet the terms with the

provisions of the following acts/rules in their day to working.

22

THE CONTRACT LABOUR ( R & A ) ACT, 1970

INTRODUCTON :-

The agreement work (Regulation and Abolition) act, 1970 has been authorized to control the

administration of agreement work in distinct foundations and for matter connected therewith.

The Act accommodates the foundation of Central and State recommended sheets to prompt the

stressed governments on matters emerging out of the association of the demonstration.

SCOPE OF THE ACT:-

The act may also called contract labour (R & A) ACT,1970

It come into power on such date as the center government might, by notice in the

overseer periodical, name and diverse dates might be designated for uncommon

procurements of this demonstration

It applies:

To every foundations in which twenty or more workers are utilized or were utilized on

any day of the prior twelve months as contract work;

To each temporary worker who utilizes or who utilized on any day of the prior twelve

months twenty or more laborers

This act is applicable for construction company, construction of residential

apartments, hotels, complex commercial building & build the buildings.

In project wise & site wise we need to concentrate on principle employer,

contractors & subcontractors what actually they are maintaining statutory labour

records under labour laws.

In project there is a different working activities going in the site like painting

work, shuttering work, bar bending work, fabrication work etc. like these works

are taken by contractors. contractors are working at the site by labours. Those

labours records should be maintain by each and every contractors.

In our company 4 projects like Esperanza phase-2. Belvista, Miraya rose and

Interlaken.

Principle employer should have a contract labour licence for each projects.

In each project we have to maintain labour compliances both principle employer

and contractors & sub contractors as per contract labour act.

23

The contractor shall maintain following registers in the prescribed formats under the act:-

1. Register in form

2. Accident register ( under regulation 66 of ESI general regulations ) if ESI is applicable

3. Register of employees employed by the contractor

4. Employment card

THE PAYMENT OF WAGES ACT, 1936

BEGINNING:-

With the expansion of industry in India, inconveniences identifying with pay of wages to

individuals utilized in industry took a frightful pivot. The mechanical units are not make

installment of wages to their specialists were compelled to raise their heads against their usage.

In 1926, our Indian government kept in touch with the neighborhood governments to set up the

circumstance with perspective to the postponements which happened in the remuneration of

wages to the general population utilized in trade. questions so gathered was set before the

imperial commission on work which was designated in 1929. On the announcement of the

commission, our Indian government rethought the point and in February, 1933 the installment of

wages bill, 1933, was bring the administrative gathering and conveyed with the end goal of

evoking conclusions. A proposal for the position of the bill to a select board of trustees was

assigned yet the movement couldn't be passed and the bill to a pick council was tabled however

the movement couldn't be passed and the bill fizzled. In 1935 the installment of a wages bill,

based upon a same standards as the prior bill of 1933 yet altogether reexamined was presented in

the authoritative get together on fifteenth February, 1935. The bill was alluded to the select

council. The select panel realistic its report on second September, 1935. Joining the proposals of

the top quality board, the installment of wages bill, 1935 was again presented in the authoritative

get together. The installment of wages bill, 1935 having been gone by authoritative gathering got

its benefits on 23 April. 1936. It went ahead law book as The Payment of a Wages Act, 1936.

MEANING OF WAGES:-

Compensation implies all remuneration ( whether by the method of pay, remittances or else )

communicated in states of cash or capable of being so talked which would, if the states of

business, express or masked, were fulfilled, be payable to a man working in admiration of his

occupation or of work done in such job, and incorporates:

24

1) Any installment to be paid under any prize or understanding between the gatherings or

request of a court;

2) Any installment to which the individual utilized is allowed in appreciation of additional

time work or occasions or any leave period;

3) Any additional installment payable under the states of livelihood ( whether called reward

or by the whatever other name);

The contractor shall maintain following registers in the arranged formats under the act:-

1. Register of the wages

2. Register of the fines

3. Register of the deductions & the advances

MINIMUM WAGES ACT, 1948

INTRODUCTION:-

Minimum wage is one provides not only for exposed provisions of time, but also the

preservations of a good organization of the employee. minimum wage is a setting up machinery

gathering was held at Geneva for the period of 1928 and the declaration of that was personified

in articles 223 to 228 of the international labour code to symbolize thing of minimum wages in a

case of trades or parts of trades, such a bonds are extremely low. The initial aim of a minimum

wages act is to avoid development of labour in industries.

minimum wages act enables both of the central and the state government to attach minimum

rate of wages allocated to a employees in a elected number of sweated industries.

DEFINITIONS :-

EMPLOYER : „employer‟ means several individual who employs directly or from side to side

someone else or whether for himself or whatever other individual, one or more workers in any

25

calendars livelihood in the admiration of a base rates of wages contain settled under this

demonstration and incorporates :

In a modern unit, any individual named as a chief of the mechanical unit under the

processing plants act, 1948.

Alternately the recorded business under the force of any Indian government. The

individual or power designated by such government for the administration and control of

representatives or where no individual or power is so delegated, the highest point of the

office.

EMPLOYEE : the „employee‟ means an individual who is working for appoint or payment to

do every work expert or uneducated, guide or office in a programmed service in respect of the

wages has been fixed. The term includes :

The contractor shall maintain following registers in the prescribed formats under the act:-

1. Wages slips

THE EMPLOYEE’S STATE INSURANCE ACT, 1948

INTRODUCTION :-

This act called as a Employees state insurance act, 1948

It is applicable to complete India

It arrive interested in strength on such dates as the central government may, by

announcement in the authorized Gazette, sign up,

OBJECTIVES OF THE ACT :-

This ACT gives assured payback to employees like sickness, motherhood and service

harm and to construct requirements for definite extra theme in family member thereto as

the opening to this act reflects.

To change a plan of socio-economic welfare & creation of detailed requirements in value

of it.

To give social and economic fairness to the poor labour group of the property.

ESI also provides for labour benefit that includes welfare behavior done, moral, physical,

& intellectual profitable betterment of workers whether by employers, or by

26

management or by other agency for the development of worker‟s values of living &

encouragement of their social & economic wee-being.

CONTRIBUTION OF ESI Scheme :-

The Employees payment of 1.75% of a wages (employees are earning up to a 50 rupees

per day are to be exempted from the payment of their contribution).

The Employer‟s payment should be 4.75% of wages.

Social precautions gain For ESIC :-

The Sickness benefit

The Maternity benefit

The Medical benefit

The Dependent‟s benefits

The Funeral expenses

The Disablements benefits

It is one of the benefit to the workers.

ESI will deduct on gross wages include basic, da, hra, education allowances,

travelling allowance, other allowances, medical special allowance & OT wages

also.

ESI Government decided up to whoever getting salary within Rs.15000/- those

workers only to get benefits from the government. New circulation will coming

like ceiling wages extended from Rs.15000/- to Rs.25000/- on accounting year

2014-2015. Rs.25000/- implemented with effect from April-2014.

We have 5years of SI benefits-leave benefit, maternity benefit, funeral benefit,

dependents benefits, and sickness benefits.

The Employee payment 1.75%, the Employer payment 4.75%. totally 6.5% we

have to pay in each month to the state bank of India.

The SBI – this bank only collect ESI Contribution both shares because

government has given authorized for receiving Contribution. So, every month

with in 25th

we need to pay otherwise interest & damages will come. Delay

payment 12% interest & damages will come.

In ESI every employee should have ESI insurance number thorough online by

using website called www.esic.in

We have 2 type of half yearly for submit to the department.

a. April to September

b. October to March

27

Half yearly returns should be submitted to the related ESI Branch office. April to

September – this period returns submission last date 11th

, October. Octobrt to

march – this period returns submission last date 11th

, may in Form.no.5 along

with ESI paid challans & covering letter attested by employer.

Inspection book, ESI accident register, Form-T Register to be maintaining under

ESI Act.

The contractor shall maintain following registers in the prescribed formats under the act :-

1. Registers of employees contributions (form 7)

2. Accident Register

3. Inspection Book

4. Wherever ESI is not applicable, insurance policy under workmen‟s compensation to be

taken for each employee to cover the death & permanent disability.

THE PAYMENT OF BONUS ACT, 1965

INTRODUCTION :-

Bonus is a impression referring to ex gratia payment or bounty or a payment by way of gift.

Normally the term bonus implies an extra payment over and above what is due to the person

concerned given as a voluntary gift. Bonus is also one method of sharing profits with the

workers. the concept of bonus has undergone considerable change. The obligation to pay a bare

minimum extra irrespective of the financial results has turned bonus into an additional statutory

payment by an employer to his employees.

The contractor shall maintain following registers in the prescribed formats under the act :-

1. A, B & C Register

28

EMPLOYEES PROVIDENT FUND & M.P ACT, 1952

INTRODUCTION :-

The employees‟ provident fund & miscellaneous provisions act, 1952 is one of the important

social security legislations. It is enacted as a measure of social justice and should be understood

liberally so has to confirm benefit on the employees to the maximum extent.

The introduction to the act states that the objective of this act is to provide further establishment

of provident fund, pension fund, and deposit-linked insurance fund for employees in factories

and other establishment.

OBJECTIVES OF THE ACT:-

To provide security to the working class and to inculcate amount workers the spirit of

savings by gainfully employed.

To create some prerequisite for the opportunity of the developed employee after his

leaving or for his dependents in case of his early death and inculcating the habit of saving

among the workers.

To give timely monitory help to industrial employees and their family when they are in

suffering and or not capable to create family and social obligations and to keep them in

old age, disablement, early death of the wage earner and in some other contingency.

Employees provident fund is the one of the social benefit & savings for the employees in

every kind of establishments.

If workers are crossed more than 20 we need to take EPF registration from the

department.

PF will deduct on Basic & DA @ 12% employee & employer. Government has decided

maximum up to 6500/- we have to pay EPF. More than 6500/- also we have to pay option

to pay EPF that is depending up on company management.

This is every month process it means that we have to pay EPF contribution every month

to the government. Employees contribution 12%, employer contribution 12%,

administrative charges 1.61%, totally 25.61% we have to pay in every month to the SBI

SBI – this bank only collect EPF Contribution both shares because government has given

authorization for receiving Contribution. So, every month with in 15th

we need to pay otherwise

interest and damages will come. Delay payment 12% interest & damages will come

29

As per EPF Act we need to submit monthly, annual returns to the department,

maintaining registers also on every month.

Within 25th

of every month we have to submit monthly returns in Form.No 12A,5,10 PF

paid Challan along with covering letter attested by employer.

Every year 30th

April we have to submit Annual Returns in Form.No-6A , 3A, &

Reconciliation Statement along with covering letter attested by employer.

In EPF every employees should have a separate EPF Account Number thorough online

by using website called www.employeesewa or www.epfindia.com

PF Holders dependents also get a pension in case of PF Holder is death

8.5% interest will given by Central Government on Employees Contribution & Employer

Contribution.

The contractor shall maintain following registers in the prescribed formats under the act :-

1. Form 3A monthly contribution statement

2. Inspection book

MATERNITY BENEFIT ACT, 1961

INTRODUCTION :-

motherhood disables a women employee from responsibility any work for the period of the few

weeks without delay previous and next child birth. In order to keep the health of the mother and

the child, it is needed that she be freed from life form busy in work during this period. with the

appearance of the scheme of wage labour in industrial activities, many employers tend to finish

the services of the women employees when they set up that maternity interfere with the

performance of ordinary duties by them. Many women employees, so, had to go on leave without

pay through this stage in order to maintain their service; many others had to stand a important

damage to keep their good association during the period of pregnancy, which was harmful to the

health of together the mother and the child.

Maternity help legislation was undertaken in categorize to allow the women employees to carry

on the social purpose of child bearing without undue strain on their health, and loss of wages.

Therefore, maternity benefit act, 1961, aims at providing payment of cash maternity benefit for a

certain period before and after detention, allowance of leave, and certain other related services.

OBJECTIVES OF THE ACT :-

To control the pay of women workers in definite establishments for definite specified

periods before and after child delivery.

30

To give installment of maternity advantages to ladies specialists at the rate of normal day

by day compensation figured on the premise of the wages payable to her for the days on

which she has worked amid the three timetable months quickly going before the date

from which she absented herself because of maternity.

To accommodate certain advantages if there should be an occurrence of unnatural birth

cycle, untimely conception, or sickness emerging out of pregnancy.

To ensure the poise of parenthood and the respect of another individual's introduction to

the world by accommodating full and sound upkeep of the ladies and her tyke at this vital

time when she is not working.

The contractor shall maintain following registers in the prescribed formats under the act.

1. Form-A Register

LABOUR WELFARE FUND

INTRODUCTION :-

Work welfare is a critical measurement of mechanical connection, work welfare incorporates

general welfare offices intended to deal with prosperity of representative's and keeping in mind

the end goal to build their expectation for everyday comforts.

It can likewise gave by government, non government offices and exchange unions.

HISTORY OF Labour LAW :-

In India the work welfare began now and again amid the first world war (1914-1918) till then

prosperity of specialists in processing plants was not really thought by anyone.

Indian Labor Organization has assumed an extremely noteworthy part for work welfare Shaped

by Indian focal government and state governments for welfare of work in businesses.

DIFINITION :-

As indicated by Arthur James…

Work welfare implies anything accomplished for the solace and change, scholarly and social, of

the representatives over and over the wages paid which is not a need of the business.

31

OBJECTIVES :-

Work law gives social solace to representatives

It gives scholarly change of workers.

To manufacture stable workforce

To make workers lives great and worth living

To give sound and legitimate working conditions

To guarantee prosperity of representatives and families

The contractor shall maintain following registers in the prescribed formats under the act:-

1. Rs.3/- to be deducted from each employee other than Manager and Executives and

company has to add Rs.6/-

2. & make payment before 31st January

32

CHAPTER 4

DATA ANALYSIS AND INTERPRETATION

4.1 TESTING OF HYPOTHESIS

H0. There is no association between the welfare measures of the employees.

H1. There is a association between the welfare measures of the employees.

4.1.1 working conditions * employee benefits

Crosstab

Count

employee benefits Total

excellent good satisfactory poor

welfare

activities

Yes 9 16 42 15 82

no 1 4 8 5 18

Total 10 20 50 20 100

Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 1.287a 3 .732

Likelihood Ratio 1.301 3 .729

Linear-by-Linear

Association .597 1 .440

N of Valid Cases 100

a. 3 cells (37.5%) have expected count less than 5. The

minimum expected count is 1.80.

The above testing of hypothesis was tested by using chi-square test with the help of statistical

package SPSS.20, it was tested with 5% level of significance. The above tables show the cross

tabulation and chi-square results. In the table the p value is 0.732 which is greater than 0.05,

therefore there is an evidence to accept the null hypothesis. Hence there is no significance

difference between the employee benefits.

33

4.1.2 welfare activities * working environment

Crosstab

Count

working environment Total

excellent good satisfactory poor

welfare

activities

yes 14 26 33 9 82

no 4 4 7 3 18

Total 18 30 40 12 100

Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 1.065a 3 .785

Likelihood Ratio 1.055 3 .788

Linear-by-Linear

Association .041 1 .840

N of Valid Cases 100

a. 2 cells (25.0%) have expected count less than 5. The

minimum expected count is 2.16.

The above testing of hypothesis was tested by using chi-square test with the help of statistical

package SPSS.20, it was tested with 5% level of significance. The above tables show the cross

tabulation and chi-square results. In the table the p value is 0.785 which is greater than 0.05,

therefore there is an evidence to accept the null hypothesis. Hence there is no significance

difference between the working environment in welfare activities provided by the organization.

34

4.1.3 welfare activities * statutory compliances

Crosstab

Count

statutory compliances Total

agree strongly

agree

Disagree somewhat

agree

welfare

activities

yes 45 8 7 22 82

no 5 5 0 8 18

Total 50 13 7 30 100

Chi-Square Tests

Value Df Asymp. Sig.

(2-sided)

Pearson Chi-Square 8.919a 3 .030

Likelihood Ratio 9.652 3 .022

Linear-by-Linear

Association 2.429 1 .119

N of Valid Cases 100

a. 2 cells (25.0%) have expected count less than 5. The

minimum expected count is 1.26.

The above testing of hypothesis was tested by using chi-square test with the help of statistical

package SPSS.20, it was tested with 5% level of significance. The above tables show the cross

tabulation and chi-square results. In the table the p value is 0.030 which is greater than 0.05,

therefore there is an evidence to accept the null hypothesis. Hence there is no significance

difference between the statutory compliances in welfare activities.

35

4.1.4 welfare activities * social benefits

Crosstab

Count

social benefits Total

agree disagree 12

welfare

activities

yes 63 18 1 82

no 13 5 0 18

Total 76 23 1 100

Chi-Square Tests

Value df Asymp. Sig.

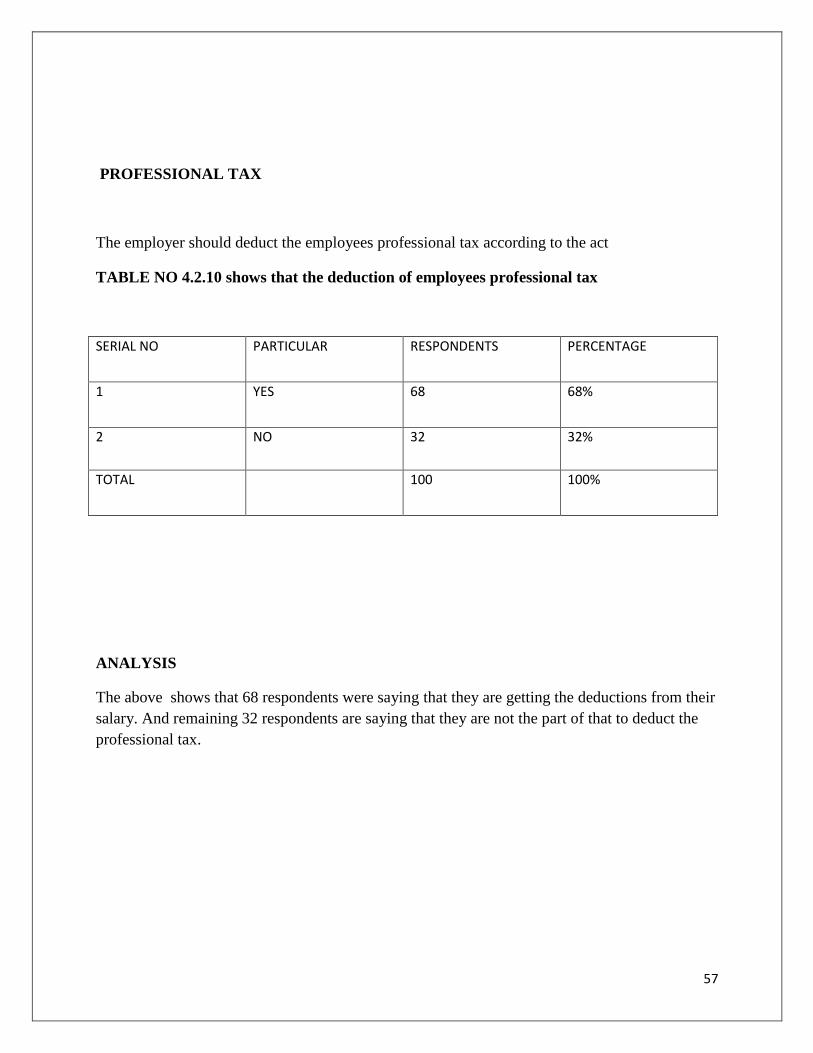

(2-sided)

Pearson Chi-Square .479a 2 .787

Likelihood Ratio .646 2 .724

Linear-by-Linear

Association .064 1 .801

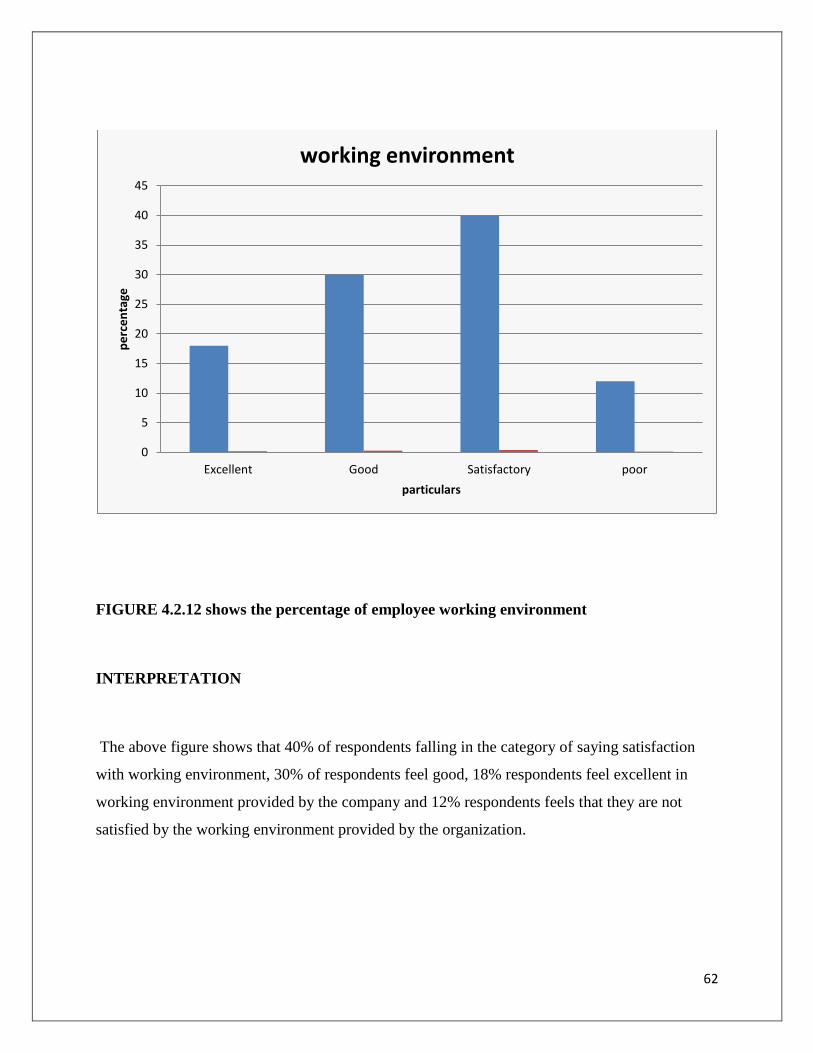

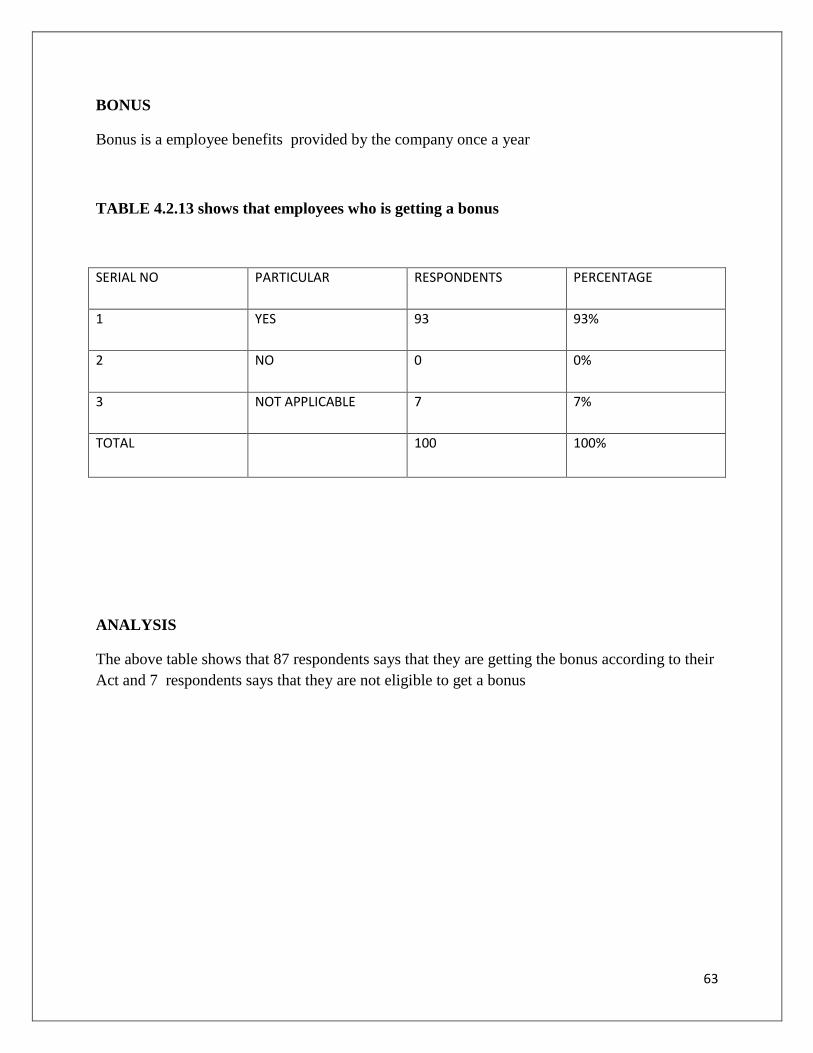

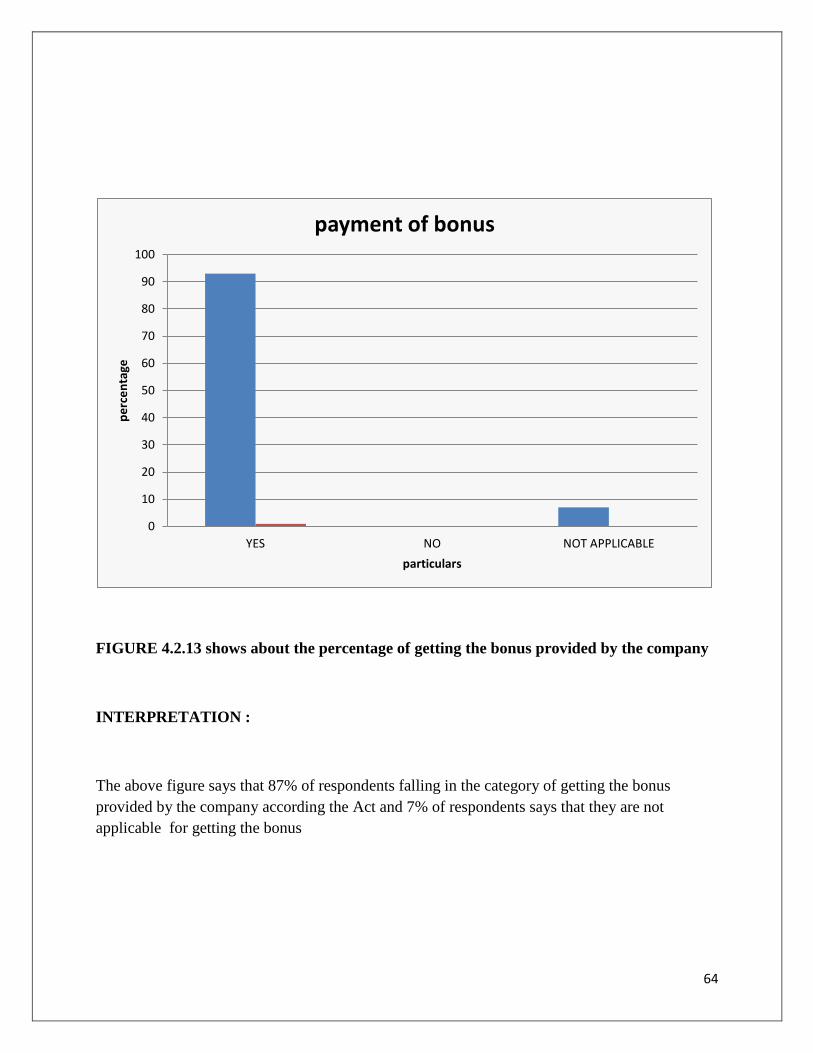

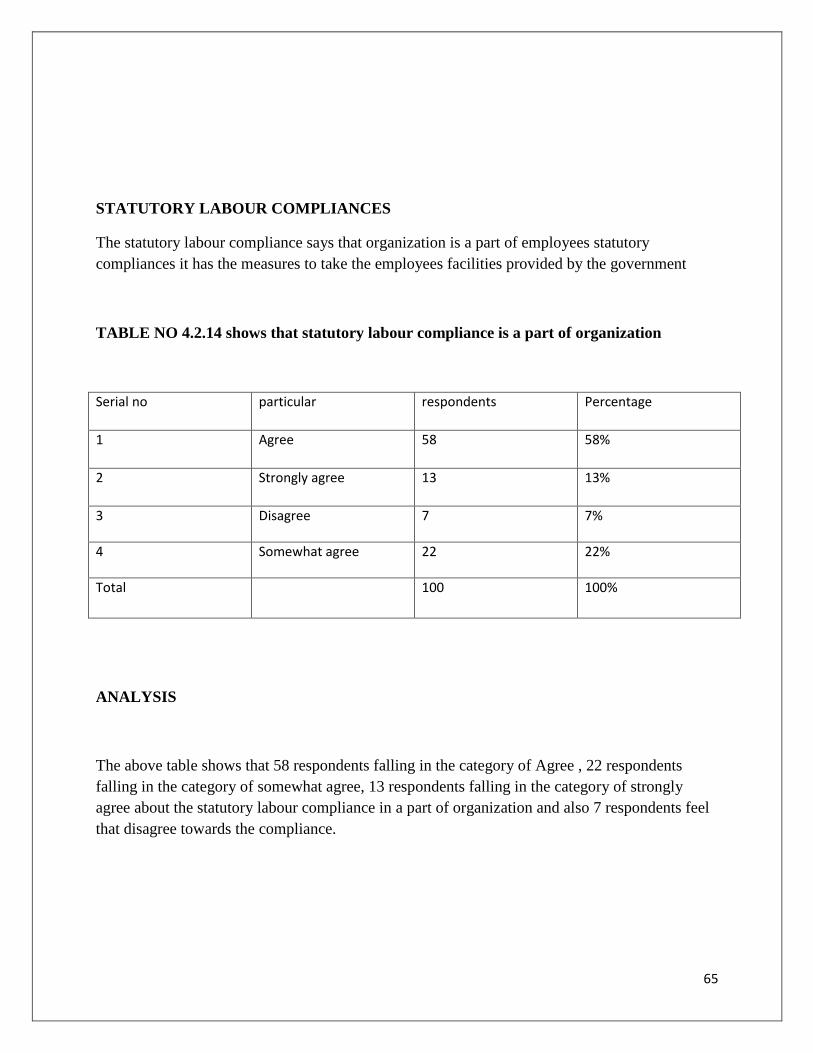

N of Valid Cases 100

a. 3 cells (50.0%) have expected count less than 5. The

minimum expected count is .18.

The above testing of hypothesis was tested by using chi-square test with the help of statistical

package SPSS.20, it was tested with 5% level of significance. The above tables show the cross

tabulation and chi-square results. In the table the p value is 0.787 which is greater than 0.05,

therefore there is an evidence to accept the null hypothesis. Hence there is no significance

difference between the social benefits in welfare activities.

36

4.1.5welfare activities * job description

Crosstab

Count

job description Total

very

satisfied

satisfied neutral

welfare

activities

yes 10 43 29 82

no 2 6 10 18

Total 12 49 39 100

Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 2.657a 2 .265

Likelihood Ratio 2.628 2 .269

Linear-by-Linear

Association 1.513 1 .219

N of Valid Cases 100

a. 1 cells (16.7%) have expected count less than 5. The

minimum expected count is 2.16.

the above testing of hypothesis was tested by using chi-square test with the help of statistical

package SPSS.20, it was tested with 5% level of significance. The above tables show the cross

tabulation and chi-square results. In the table the p value is 0.265 which is greater than 0.05,

therefore there is an evidence to accept the null hypothesis. Hence there is no significance

difference between the job description. In welfare activities.

37

4.1.6working conditions * working environment

Crosstab

Count

working environment Total

excellent good satisfactory poor

working

conditions

Excellent 7 13 18 6 44

Good 3 8 11 5 27

Satisfactor

y 6 5 8 1 20

Poor 2 4 3 0 9

Total 18 30 40 12 100

Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 6.368a 9 .703

Likelihood Ratio 7.315 9 .604

Linear-by-Linear

Association 2.375 1 .123

N of Valid Cases 100

a. 8 cells (50.0%) have expected count less than 5. The

minimum expected count is 1.08.

the above testing of hypothesis was tested by using chi-square test with the help of statistical

package SPSS.20, it was tested with 5% level of significance. The above tables show the cross

tabulation and chi-square results. In the table the p value is 0.703 which is greater than 0.05,

therefore there is an evidence to accept the null hypothesis. Hence there is no significance

difference between the working environment in welfare activities.

38

4.1.7 working conditions * satisfaction of facility

Crosstab

Count

satisfaction of facility Total

housing

facilities

medical

policy

conductive

working

conditions

all the

above

working

conditions

Excellent 8 31 2 3 44

Good 4 19 0 4 27

Satisfactor

y 4 14 0 2 20

Poor 1 7 0 1 9

Total 17 71 2 10 100

Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 4.094a 9 .905

Likelihood Ratio 4.828 9 .849

Linear-by-Linear

Association .089 1 .765

N of Valid Cases 100

a. 11 cells (68.8%) have expected count less than 5. The

minimum expected count is .18.

the above testing of hypothesis was tested by using chi-square test with the help of statistical

package SPSS.20, it was tested with 5% level of significance. The above tables show the cross

tabulation and chi-square results. In the table the p value is 0.905 which is greater than 0.05,

therefore there is an evidence to accept the null hypothesis. Hence there is no significance

difference between the satisfaction of facilities in working environment.

39

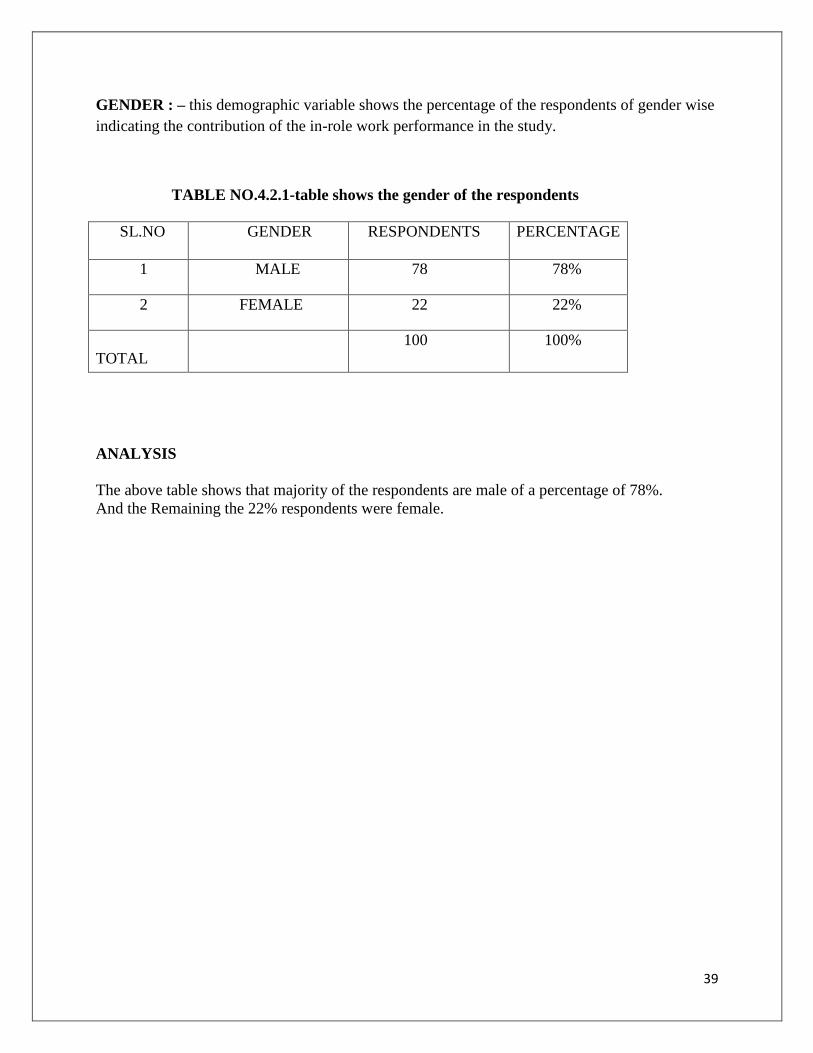

GENDER : – this demographic variable shows the percentage of the respondents of gender wise

indicating the contribution of the in-role work performance in the study.

TABLE NO.4.2.1-table shows the gender of the respondents

SL.NO GENDER RESPONDENTS PERCENTAGE

1 MALE 78 78%

2 FEMALE 22 22%

TOTAL

100 100%

ANALYSIS

The above table shows that majority of the respondents are male of a percentage of 78%.

And the Remaining the 22% respondents were female.

40

Figure 4.2.1: the figure showing the percentage of gender of the respondents

INTERPRETATION

The above table shows that the respondents in this study is comprises of 72% are falling in the

gender of male and 22% falling in the age gender of female.

0

10

20

30

40

50

60

70

80

90

1 2

pe

rce

nta

ge

particulars

Gender

MALE

FEMALE

41

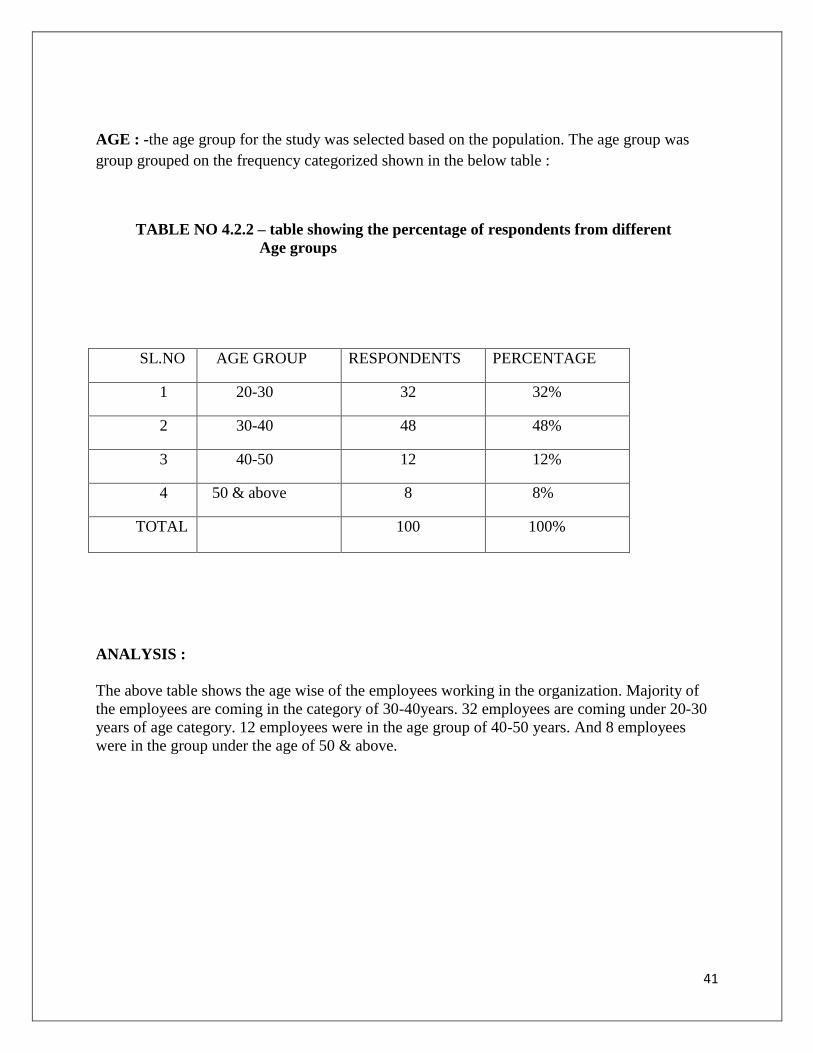

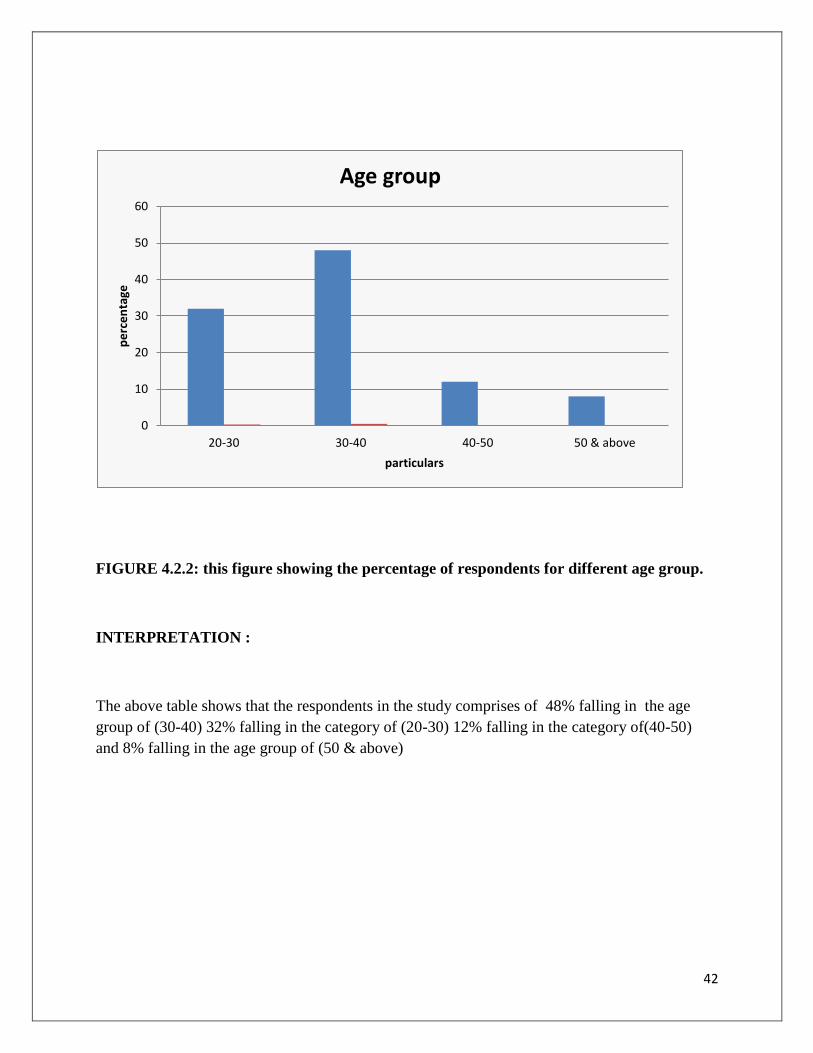

AGE : -the age group for the study was selected based on the population. The age group was

group grouped on the frequency categorized shown in the below table :

TABLE NO 4.2.2 – table showing the percentage of respondents from different

Age groups

SL.NO AGE GROUP RESPONDENTS PERCENTAGE

1 20-30 32 32%

2 30-40 48 48%

3 40-50 12 12%

4 50 & above 8 8%

TOTAL 100 100%

ANALYSIS :

The above table shows the age wise of the employees working in the organization. Majority of

the employees are coming in the category of 30-40years. 32 employees are coming under 20-30

years of age category. 12 employees were in the age group of 40-50 years. And 8 employees

were in the group under the age of 50 & above.

42

FIGURE 4.2.2: this figure showing the percentage of respondents for different age group.

INTERPRETATION :

The above table shows that the respondents in the study comprises of 48% falling in the age

group of (30-40) 32% falling in the category of (20-30) 12% falling in the category of(40-50)

and 8% falling in the age group of (50 & above)

0

10

20

30

40

50

60

20-30 30-40 40-50 50 & above

pe

rce

nta

ge

particulars

Age group

43

YEAR OF EXPERIANCE

The selected year of experience for the study was based on the population. the year of experience

was grouped based on the frequency categorized shown in the table

TABLE NO 4.2.3 showing the experience of the respondents

SL.NO YEARS RESPONDENTS PERCENTAGE

1 0-3 YEARS 32 32%

2 3-5 YEARS 38 38%

3 5-7 YEARS 19 19%

4 7 & ABOVE YEARS 11 11%

TOTAL 100 100%

ANALYSIS :

The above table shows that the 38 respondents are falling in the experience of 3-5 years. 32

respondents are falling in the experience of 0-3 year. 19 respondents are coming under the

category of 5-7 years and 11 respondents are falling in he experience of 7 & above years.

44

FIGURE 4.2.3: this figure showing the percentage for respondents for different years of

experience.

INTERPRETATION :

The above variable shows that the respondents in this study is comprises of 38% falling in the

experience of (3-5 year) 32% falling in the experience of (0-3year) 19% falling in the experience

of (5-7 year) 11% falling in the experience of (7 & above years).

0

5

10

15

20

25

30

35

40

0-3 YEARS 3-5 YEARS 5-7 YEARS 7 & ABOVE YEARS

pe

rce

nta

ge

years of experiance

45

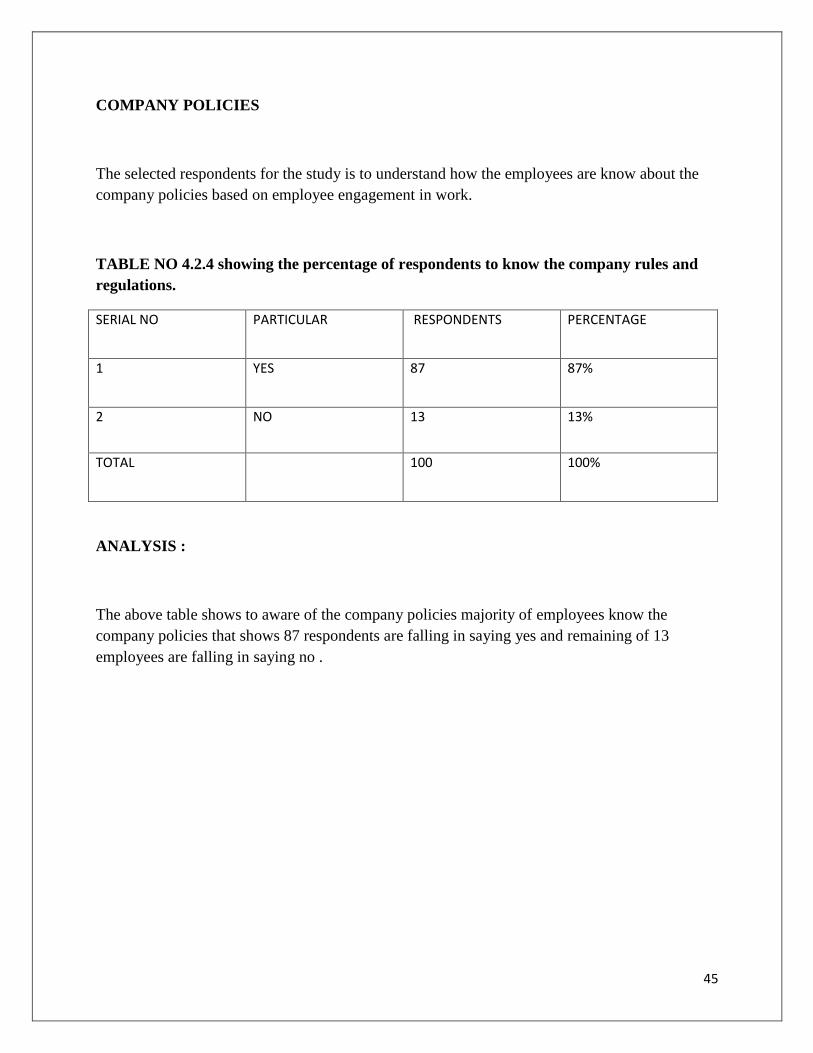

COMPANY POLICIES

The selected respondents for the study is to understand how the employees are know about the

company policies based on employee engagement in work.

TABLE NO 4.2.4 showing the percentage of respondents to know the company rules and

regulations.

SERIAL NO PARTICULAR RESPONDENTS PERCENTAGE

1 YES 87 87%

2 NO 13 13%

TOTAL 100 100%

ANALYSIS :

The above table shows to aware of the company policies majority of employees know the

company policies that shows 87 respondents are falling in saying yes and remaining of 13

employees are falling in saying no .

46

FIGURE NO 4.2.4 showing the percentage of respondents to aware the company policies.

INTERPRETATION :

The above variable shows that the respondents in this study comprises of 87% falling in the

category of to aware the company policies and 13% falling in the category they are not known

about the company policies.

JOB DESCRIPTION :

0

10

20

30

40

50

60

70

80

90

100

pe

rce

nta

ge

particualrs

company policies

Yes

no

47

In this study job is considered as the employees are how description is related to the job. The job

description is designed based on the nature of the work the employees are comfort.

TABLE NO 4.2.5 shows the significant factor of the job description.

SERIAL NO PARTICULAR RESPONDENTS PERCENTAGE

1 VERY SATISFIED 12 12%

2 SATISFIED 49 49%

3 NEUTRAL 39 31%

4 DISSATISFIED 0 49%

TOTAL 100 100%

ANALYSIS :

the above table shows that 49 respondents are satisfied with their job. 39 respondents are neutral

with their job description and remaining 12 respondents are very satisfied in their job

description.

48

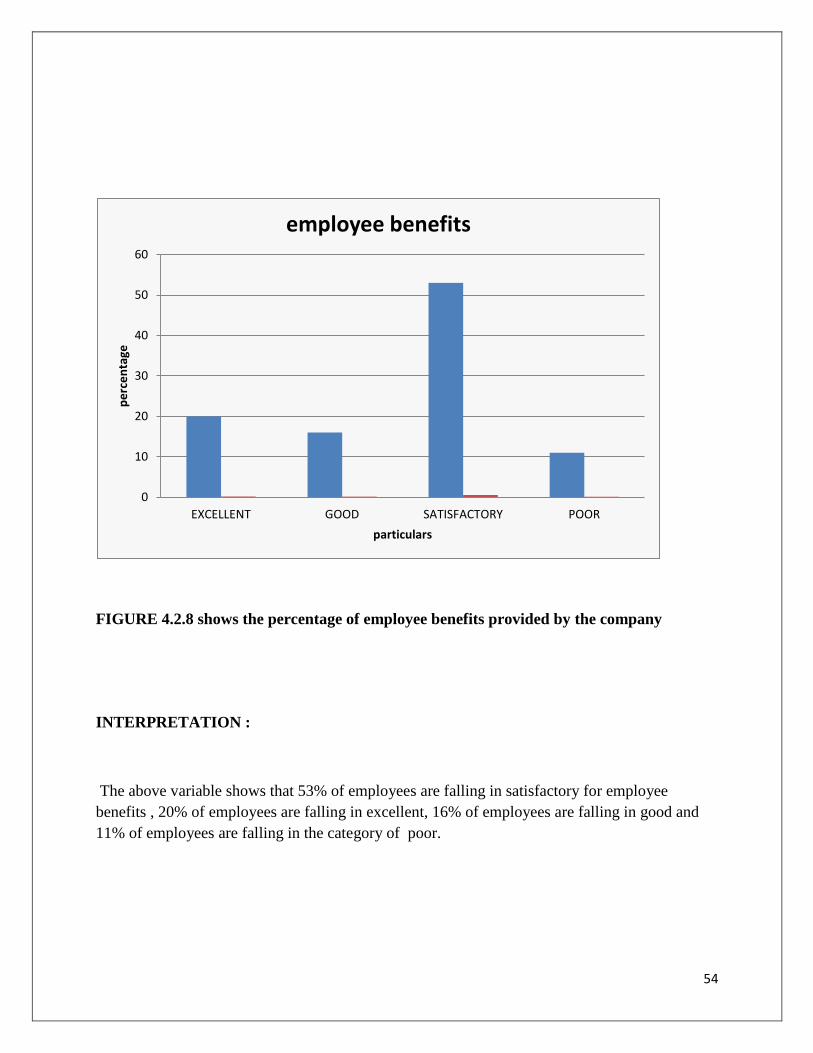

FIGURE NO 4.2.5 shows the significant of job description

INTERPRETATION :

The above variable shows that the respondents are 49% satisfied with their job description 39%

respondents are feeling neutral and 12% respondents are feeling very satisfied with their job

description.

ELIGIBLE FOR ESI & EPF

0

10

20

30

40

50

60

Very satisfied satisfied Neutral Dissatisfied

pe

rce

nta

ge

particulars

job description

49

In this study the employees are eligible to get a ESI and EPF which is deducting by the employer

If the employees are eligible they get the facilities for ESI schemes. It shows the employees

satisfaction with their work environment.

TABLE NO 4.2.6 shows the that deduction of ESI AND EPF for eligible employees

SERIAL NO PARTICULAR NO.OF RESPONDENTS PERCENTAGE

1 YES 70 70%

2 NO 0 0%

3 NOT APPLICABLE 30 30%

TOTAL 100 100%

ANALYSIS:

The above table shows that 70 of employees are eligible to get the ESI and EPF schemes are

deducting from the employer side and remaining employees are not required for the deduction of

ESI.

0

10

20

30

40

50

60

70

80

Yes No Not applicable

pe

rce

nta

ge

particulars

Chart Title

50

FIGURE 4.2.6 showing the employer is deducting ESI & EPF for the eligible employees

INTERPRETATION :

the above variable shows that the respondents in this study is comprises of 70% falling in getting

the ESI and EPF deductions and remaining employees of 30% of respondents are not applicable