“A STUDY OF BANKRUPTCY POSITION OF ALOK INDUSTRIES LTD.” Project Report submitted to UNIVERSITY OF CALICUT In partial fulfillment of the requirement for the award of the degree of BACHELOR OF COMMERCE (PROFESSIONAL) Submitted by ASWATHI RAJEEVU (CCASBCP027) Under the supervision of Ms. TEENA THOMAS DEPARTMENT OF COMMERCE CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA MARCH 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

“A STUDY OF BANKRUPTCY POSITION OF ALOK

INDUSTRIES LTD.”

Project Report submitted to

UNIVERSITY OF CALICUT

In partial fulfillment of the requirement for the award of the degree of

BACHELOR OF COMMERCE (PROFESSIONAL)

Submitted by

ASWATHI RAJEEVU

(CCASBCP027)

Under the supervision of

Ms. TEENA THOMAS

DEPARTMENT OF COMMERCE

CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA

MARCH 2021

CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA

CALICUT UNIVERSITY

DEPARTMENT OF COMMERCE

CERTIFICATE

This is to certify that the project report entitled “A STUDY OF

BANKRUPTCY POSITION OF ALOK INDUSTRIES LTD.” is a bonafide

record of project done by ASWATHI RAJEEVU, Reg. No. CCASBCP027,

under my guidance and supervision in partial fulfillment of the requirement for

the award of the degree of BACHELOR OF COMMERCE (PROFESSIONAL)

and it has not previously formed the basis for any Degree, Diploma and

Associateship or Fellowship.

PROF. K.O.FRANCIS Ms. TEENA THOMAS

Co-ordinator Project Guide

DECLARATION

I, ASWATHI RAJEEVU, hereby declare that the project work entitled

“A STUDY OF BANKRUPTCY POSITION OF ALOK INDUSTRIES LTD.”

is a record of independent and bonafide project work carried out by me under the

supervision and guidance of Ms. Teena Thomas, Assistant Professor,

Department of Commerce, Christ College, Irinjalakuda.

The information and data given in the report is authentic to the best of my

knowledge. The report has not been previously submitted for the award of any

Degree, Diploma, Associateship or other similar title of any other university or

institute.

Place: Irinjalakuda Aswathi Rajeevu

Date: CCASBCP027

ACKNOWLEDGEMENT

I would like to take the opportunity to express my sincere gratitude to all people

who have helped me with sound advice and able guidance.

Above all, I express my eternal gratitude to the Lord Almighty under whose

divine guidance; I have been able to complete this work successfully.

I would like to express my sincere obligation to Rev.Dr. Jolly Andrews,

Principal-in-Charge, Christ college Irinjalakuda for providing various facilities.

I am thankful to Prof. K.O.Francis, Co-ordinator of B.Com (Professional), for

providing proper help and encouragement in the preparation of this report.

I am thankful to Ms. Teena Thomas, Class teacher for her cordial support,

valuable information and guidance, which helped me in completing this task

through various stages.

I express my sincere gratitude to Ms. Teena Thomas, Assistant Professor, whose

guidance and support throughout the training period helped me to complete this

work successfully.

I would like to express my gratitude to all the faculties of the Department for

their interest and cooperation in this regard.

I extend my hearty gratitude to the librarian and other library staffs of my college

for their wholehearted cooperation.

I express my sincere thanks to my friends and family for their support in

completing this report successfully.

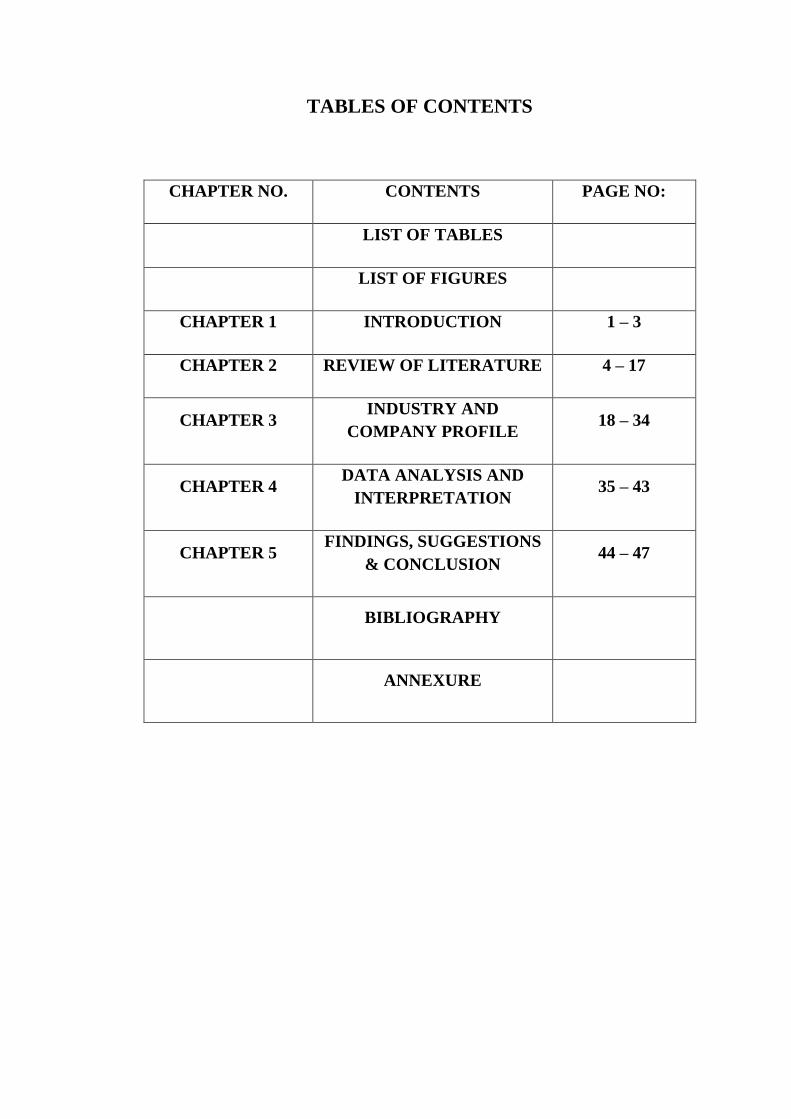

TABLES OF CONTENTS

CHAPTER NO. CONTENTS PAGE NO:

LIST OF TABLES

LIST OF FIGURES

CHAPTER 1 INTRODUCTION 1 – 3

CHAPTER 2 REVIEW OF LITERATURE 4 – 17

CHAPTER 3 INDUSTRY AND

COMPANY PROFILE 18 – 34

CHAPTER 4 DATA ANALYSIS AND

INTERPRETATION 35 – 43

CHAPTER 5 FINDINGS, SUGGESTIONS

& CONCLUSION 44 – 47

BIBLIOGRAPHY

ANNEXURE

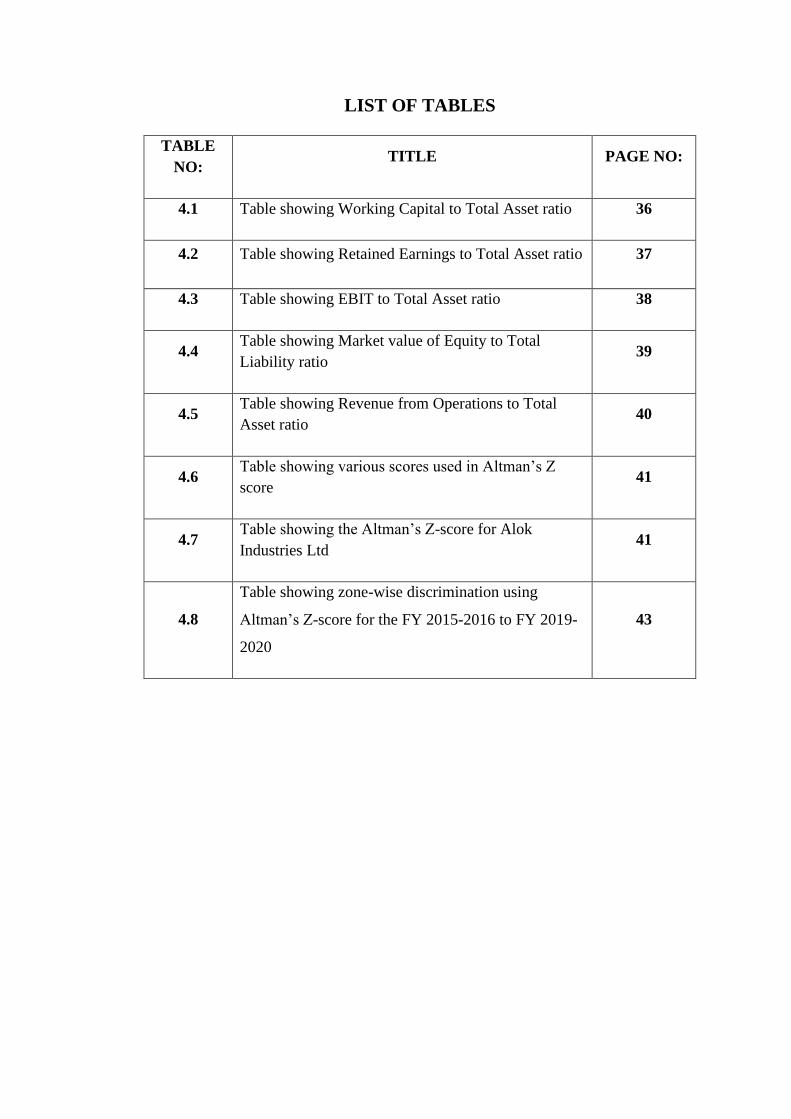

LIST OF TABLES

TABLE

NO: TITLE PAGE NO:

4.1 Table showing Working Capital to Total Asset ratio 36

4.2 Table showing Retained Earnings to Total Asset ratio 37

4.3 Table showing EBIT to Total Asset ratio 38

4.4 Table showing Market value of Equity to Total

Liability ratio 39

4.5 Table showing Revenue from Operations to Total

Asset ratio 40

4.6 Table showing various scores used in Altman’s Z

score 41

4.7 Table showing the Altman’s Z-score for Alok

Industries Ltd 41

4.8

Table showing zone-wise discrimination using

Altman’s Z-score for the FY 2015-2016 to FY 2019-

2020

43

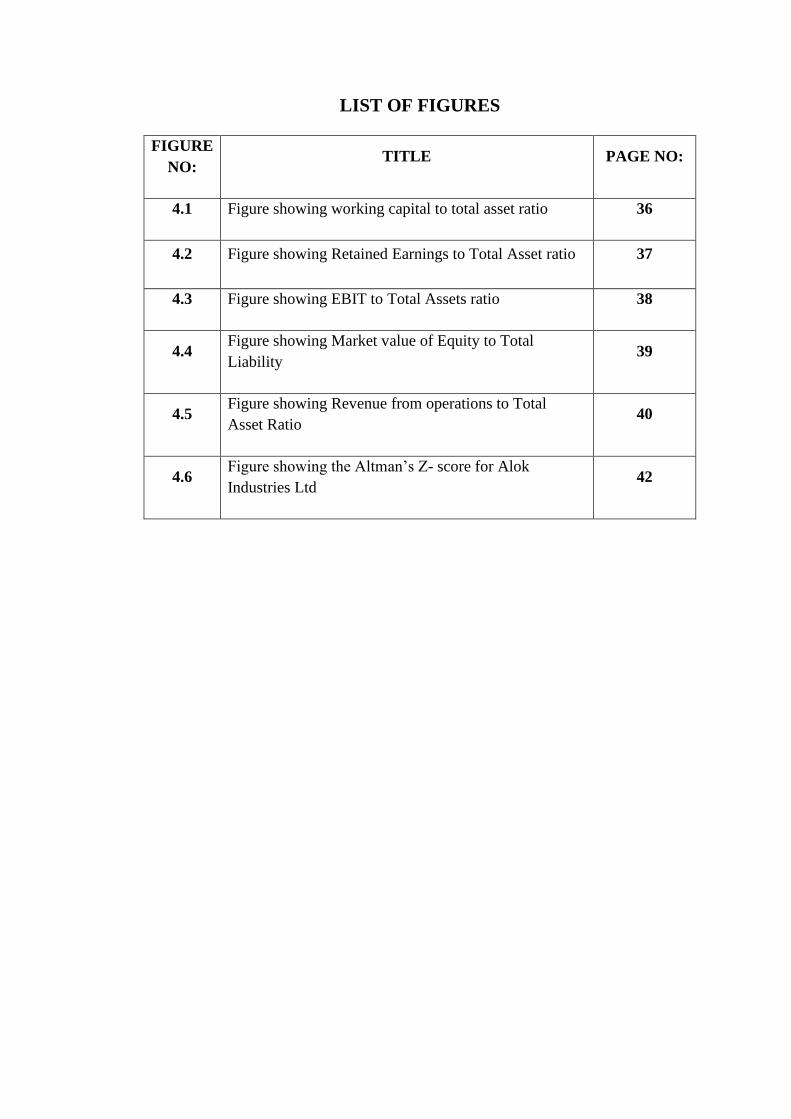

LIST OF FIGURES

FIGURE

NO: TITLE PAGE NO:

4.1 Figure showing working capital to total asset ratio 36

4.2 Figure showing Retained Earnings to Total Asset ratio 37

4.3 Figure showing EBIT to Total Assets ratio 38

4.4 Figure showing Market value of Equity to Total

Liability 39

4.5 Figure showing Revenue from operations to Total

Asset Ratio 40

4.6 Figure showing the Altman’s Z- score for Alok

Industries Ltd 42

CHAPTER Ⅰ

INTRODUCTION

1

1.1 Introduction

Most of the organizations exist with an objective of profit maximization. To

achieve profit maximization objective, firm needs strong internal & external

support. The failure of internal support system such as effective utilization of

funds, labour, material etc & external support system such as economic, political

& socio-cultural conditions results in Bankruptcy of the organization.

Bankruptcy is a situation where the firm’s total liabilities exceed total assets.

The real net worth of the firm is, therefore negative. This leads to reduced sales,

increased cost & losses, ineffective competition etc. Ultimately firm will be

under distress stage. Under such situations it becomes difficult for investors &

lenders to analyze the financial performance of the organization.

Financial longevity of a business is a concern to internal and external

stakeholders. Internal stakeholders might be interested in whether skills are

transferable, while external stakeholders might be concerned directly with their

investment or profits. Predicting if a Business will do well or go bankrupt has

led to propagation of various theories. Knowing how to determine the financial

health of a company is a vital business skill. Having a clear picture of financial

health can help in making more informed decisions about an organization’s

direction and how resources are allocated. Similarly, if a company plan to attract

investors or seek financing, one needs to speak up and present the business’s

financial health. Financial health of a company or a firm plays a pivotal role in

every organization in the world.

Several bankruptcy models for example, logit analysis, recursive portioning

algorithm and neural networks are available but still Altman’s model is

considered to be superior and pervasively applied by researchers all over the

world in the present days. This study is an attempt to examine the bankruptcy

position of Alok Industries Ltd using Altman’s Z-score.

2

1.2 Statement of Problem

Financial Risks show the possibility of losses arising from the failure to achieve

financial objectives. These risks are not necessarily independent of each other.

The importance of these risks will vary from one company to another in relation

to the company’s size, nature, functional sector etc. The main aim of this study

is to test and understand the bankruptcy position of the chosen company.

1.3 Scope of study

The project is conducted in order to know the bankruptcy position of the Alok

Industries Ltd. It helps in understanding and evaluating bankruptcy position of

the company.

1.4 Significance of study

Financial distress is a global phenomenon that affects companies across all

sectors of the economy .The significance of predicting bankruptcy is

fundamental in assessing the financial condition of a company and prospects in

its operations. This study offers a better insight into the bankruptcy position of

the sample company.

1.5 Objectives of the Study

• To analyse ratios such as working capital to total assets, retained

earnings to total assets, EBIT, market value of equity to total liabilities

and sales to total assets.

• To examine the bankruptcy position of Alok Industries Ltd.

• Improve the knowledge of bankruptcy prediction of companies.

1.6 Research Design

1.6.1 Nature of Study

The study is Analytical in nature.

3

1.6.2 Nature of Data

The study mainly uses secondary data. It includes financial variables and

accounting information such as ratios including working capital to total assets,

retained earnings to total assets, EBIT, market value of equity to total liabilities

and sales to total assets.

1.6.3 Sources of Data

The study uses secondary data. Secondary sources include annual reports,

official websites of the chosen companies, a number of research papers including

Asian Journal of Management Research, International Journal of Advanced

Science and Technology, working papers and financial dailies.

1.6.4 Period of Study

The period of study is from 2015 to 2020.

1.7 Tool for Analysis

Altman’s Z-Score

1.8 Chapterization

Chapter 1: Introduction

Chapter 2: Review of Literature

Chapter 3: Industry Profile and Company Profile

Chapter 4: Data Analysis and Interpretation

Chapter 5: Finding Conclusion and Suggestions

CHAPTER Ⅱ

REVIEW OF LITERATURE

4

2.1 Introduction

This section deals with review of literature which is divided into two parts

namely, Conceptual and Empirical Literature. Conceptual Literature includes

various theories and concepts used in the study. Empirical Literature mainly

includes reviews on earlier studies.

2.2 Conceptual Review

2.2.1 Meaning of Bankruptcy

The word bankruptcy is derived from Italian banca rotta, literally meaning

"broken bench" but more idiomatically "broken bank", since bankers

traditionally dealt from wooden benches. A folk etymology alleges that Italian

bankers' benches were smashed if they defaulted on payment, but this is often

dismissed as a legend.

A legal declaration that one is unable to pay one's debts and thus needs to have

debts forgiven or reorganized. That is, bankruptcy is a legal proceeding in whic

h a person or corporation has become insolvent, and therefore cannot pay his/h

er/its obligations. Most of the time, the person or corporation files this declarati

on with a bankruptcy court, though in some cases the creditors may do so them

selves.

2.2.2 Bankruptcy in India

The Parliament of India in the first week of May 2016 passed Insolvency and

Bankruptcy Code 2016 (New Code). Earlier a clear law on corporate bankruptcy

did not exist, even though individual bankruptcy laws have been in existence

since 1874. The earlier law in force was enacted in 1920 called the Provincial

Insolvency Act.

The legal definitions of the terms bankruptcy, insolvency, liquidation and

dissolution are contested in the Indian legal system. There is no regulation or

5

statute legislated upon bankruptcy which denotes a condition of inability to meet

a demand of a creditor as is common in many other jurisdictions.

Winding up of companies was in the jurisdiction of the courts which can take a

decade even after the company has actually been declared insolvent. On the other

hand, supervisory restructuring at the behest of the Board of Industrial and

Financial Reconstruction is generally undertaken using receivership by a public

entity.

2.2.3 Salient Features of Insolvency and Bankruptcy Code 2016

1. Resolution of Insolvency:

The Insolvency and Bankruptcy Code, 2016 lays down the separate insolvency

resolving procedures for companies, individuals as well as partnership

companies. It is possible to initiate the procedure either by the creditors or the

debtors. The code lays down a maximum time period for completing the

insolvency resolution procedure for individuals and corporates. In the case of a

company, the procedure must be fully completed in one hundred and eighty days,

which can later be stretched by ninety days only when a large percentage of

creditors permit or agree. On the other hand, in the case of start-ups (aside to the

partnership companies), small organizations as well as other organizations

(having less than Rs 1 crore worth of assets), the resolution procedure would be

fulfilled within a period of ninety days of initiating the required that can be

further stretched by as many as 45 days.

2. Regulator of Insolvency:

The Code lays down that the Insolvency and Bankruptcy Board of India shall

oversee the proceedings related to insolvency in the nation and also regulate all

the organizations that have been registered by the board. The Insolvency and

Bankruptcy Board shall consist of ten members, which would also include the

6

representatives of the Law and Finance ministries as well as the RBI (Reserve

Bank of India).

3. Licensed Insolvency Professionals:

The management of insolvency procedure shall be done by licensed insolvency

professionals. They would also exercise control on the debtor’s assets at the time

of the insolvency procedure.

4. Insolvency and Bankruptcy Adjudicator:

The Code has introduced two distinct tribunals for overseeing the procedure

resolving insolvency, for companies and individuals. These are (i) the National

Company Law Tribunal for organizations and Limited Liability Partnership

companies; as well as (ii) the Debt Recovery Tribunal for overseeing insolvency

resolution for individuals as well as partnership firms.

5. Procedure:

An insolvency plea is given to the authority that adjudicates (in corporate

debtor’s case it is NCLT) by operation or financial creditors or the corporate

debtor. The plea can be accepted or rejected in a maximum time period of

fourteen days. In case the plea gets acceptance then the tribunal will have to

quickly appoint an IRP or Insolvency Resolution Professional for drafting a plan

of resolution within a period of 180 days (that can be extended by ninety days).

Following this, the court would initiate the process of resolving corporate

insolvency. For that particular period, the company’s directors shall remain

suspended whereas the promoters shall have no say in the company management.

The Insolvency Resolution Professional can seek help of the management of the

company for handling everyday operations. In case the CIRP is unable to revive

the organization, then the process of liquidation shall be initiated.

7

6. Amendments:

Certain individuals are prohibited from providing any plan of resolution in case

there are any defaults. Hence, wilful defaulters, management or promoters of

company in case there is any non-performing outstanding debt for more than a

year, as well as directors who have been disqualified cannot submit any plan.

Apart from this, the bill also places a restriction on the selling of a defaulter’s

property to any such individuals at the time of liquidation.

2.2.4 Causes of Bankruptcy

1. Market Conditions

Poor conditions in overall economy and the specific market in which a business

operates are common causes of bankruptcy. The economy tends to follow a

boom and bust cycle of rapid expansion followed by lulls or recessions. During

bust periods, consumer confidence and spending tend to decline, which can

lead to low revenue. Companies involved in specific niche markets can also be

susceptible to shifts in consumer preferences. For example, a small business

owner that owns a music store might be forced to close shop if customers start

buying digital downloads instead of CDs. Competition from larger companies

is another market factor that can cut into the revenue of small companies and

lead to bankruptcy.

2. Financing

Financing is one of the primary challenges that small businesses face. Many

business owners take out loans to help finance their operations. If a business

struggles, his lender may not be willing to grant additional funding, which

could lead to bankruptcy. Even if an owner can secure more financing to keep

his company afloat in the short-term, high debt makes it more difficult for a

company to be profitable because it has to pay interest on the debt.

8

3. Poor Decision Making

Lack of planning and level-heading thinking can lead to hasty decisions and

business failure. For example, a business owner might spend time and money

developing a product that she believes in without surveying customers and

studying production costs to gauge whether the product could be profitable.

Even if the product is useful, it might not be financially viable from a business

standpoint. Lack of education and experience in finance and management can

increase the likelihood of poor decisions, but no company is immune to making

mistakes.

4. Other Causes

Bankruptcy can result from a host of other underlying problems that inhibit

profitability. Some other factors that can contribute to bankruptcy include poor

business location, loss of key employees, lawsuits raised by competitors and

personal issues like illness or divorce. Unforeseen disasters and criminal

activity like floods, storms, fires, theft and fraud can also cause hardships that

lead to bankruptcy.

2.2.5 Procedure for Bankruptcy

A plea for insolvency is submitted to the adjudicating authority (NCLT in case

of corporate debtors) by financial or operation creditors or the corporate debtor

itself. The maximum time allowed to either accept or reject the plea is 14 days.

If the plea is accepted, the tribunal has to appoint an Interim Resolution

Professional (IRP) to draft a resolution plan within 180 days (extendable by 90

days). following which the Corporate Insolvency Resolution process is initiated

by the court. For the said period, the board of directors of the company stands

suspended, and the promoters do not have a say in the management of the

company. The IRP, if required, can seek the support of the company's

management for day-to-day operations. If the CIRP fails in reviving the company

the liquidation process is initiated.

9

Insolvency and bankruptcy code bill was introduced in the Indian parliament by

the NDA government in 2015 but got final clearance in May 2016 parliament

session. It was believed that this bill will resolve all the banking issues present

in the economy. The main reason to introduce this bill was to fasten up the long

insolvency process which it did. After this bill, the insolvency process for the

company is 180 days with an extension of 90 days, and for startups and small

companies, it is 90 days with an extension of 45 days. The question is will it

resolve all banking issues and the answer is no, as India's banking industry is

going through a very difficult phase. Banks are merging up due to bad loans and

all this hustle can't be simplified with this bill. IBC will only bad debts that are

disclosed. Undisclosed bad loans or bad loans that get disclosed after the victim

absconds remain untouched. And there are many incidents in past years in which

creditors flew away from the country after being unable to pay off the loan that

they took. But, the IBC did improve the economic system and the impact can be

seen - the economy is clearly stabler

2.2.6 Meaning of Altman’s Z score

Altman Z score, is a tool that helps to measure the financial distress or

bankruptcy. It was published by Edward I Altman in the year 1968. Altman’s

idea of developing a formula for predicting bankruptcy started at the time of

the Great Depression when businesses experienced a sharp rise in incidences of

default. The Z score model is mainly designed to measure the financial health of

the company in terms of financial distress or bankruptcy. The model uses the

formulae based on the information found in the profit and loss account and

balance sheet of the organization.

2.2.7 History of the Altman Z-Score

NYU Stern Finance Professor Edward Altman developed the Altman Z-score

formula in 1967, and it was published in 1968. Over the years, Altman has

continued to revaluate his Z-score over the years. From 1969 until 1975, Altman

looked at 86 companies in distress, then 110 from 1976 to 1995, and finally 120

10

from 1996 to 1999, finding that the Z-score had an accuracy of between 82% and

94%.

In 2012, he released an updated version called the Altman Z-score Plus that one

can use to evaluate public and private companies, manufacturing and non-

manufacturing companies, and U.S. and non-U.S. companies. One can use

Altman Z-score Plus to evaluate corporate credit risk. The Altman Z-score has

become a reliable measure of calculating credit risk.

2.2.8 Components of Altman’s Z-score

Altman’s Z-score model combines five financial ratios to predict the probability

of a company becoming insolvent in the next two years.

The following are the key financial ratios that make up the Z-score model:

1. Working Capital to Total Assets

Working capital is the difference between the current assets of a company and

its current liabilities. The value of a company’s working capital determines its

short-term financial health. A positive working capital means that a company

can meet its short-term financial obligations, and still make funds available to

invest and grow. In contrast, negative working capital means that a company will

struggle to meet its short-term financial obligations because there are inadequate

current assets.

X1 = working capital

total assets

2. Retained Earnings to Total Assets

The retained earnings/total assets ratio shows the amount of retained earnings or

losses in a company. If a company reports low retained earnings to total assets

ratio, it means that the company is financing its expenditure using borrowed

funds rather than funds from its retained earnings. It increases the probability of

11

a company going bankrupt. On the other hand, a high retained earnings to total

assets ratio shows than a company uses its retained earnings to fund capital

expenditure. It shows that the company achieved profitability over the years, and

it does not need to rely on borrowings.

X2 = retained earnings

total assets

3. Earnings Before Interest and Tax to Total Assets

EBIT, a measure of a company’s profitability, refers to the ability of a company

to generate profits solely from its operations. The EBIT/Total Assets ratio

demonstrates a company’s ability to generate enough revenues to stay profitable

and fund ongoing operations and make debt payments.

X3 = earnings before interest and taxes

total assets

4. Market Value of Equity to Total Liabilities

The market value, also known as market capitalization, is the value of a

company’s equity. It is obtained by multiplying the number of outstanding shares

by the current price of stocks. The market value of the equity/total liabilities ratio

shows the degree to which a company’s market value would decline when it

declares bankruptcy before the value of liabilities exceeds the value of assets in

the balance sheet. A high market value of equity to total liabilities ratio can be

interpreted to mean high investor confidence in the company’s financial strength.

X4 = market value of equity

total liabilities

12

5. Sales to Total Assets

The sales to total assets ratio shows how efficiently the management uses assets

to generate revenues vis-à-vis the competition. A high sales to total assets ratio

is translated to mean that the management requires a small investment to

generate sales, which increases the overall profitability of the company. In

contrast, a low or falling sales to total assets ratio means that the management

will need to use more resources to generate enough sales, which will reduce the

company’s profitability.

X5 = sales

total assets

The Altman’s Z-score formula is written as follows:

▪ Original Z-score component definitions

X1 = working capital / total assets

X2 = retained earnings / total assets

X3 = earnings before interest and taxes / total assets

X4 = market value of equity / total liabilities

X5 = sales / total assets

Z-score bankruptcy model:

Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + 1X5

Zones of discrimination:

Z > 2.99 – "safe" zone

1.81 < Z < 2.99 – "grey" zone

Z < 1.81 – "distress" zone

13

2.2.9 Advantages

• The Z Score highlights factors contributing to a company’s financial

health and uncovers emerging trends that indicate improvements or

deterioration in financial condition.

• The Z Score is a critical tool business managers use to assess financial

health.

• It helps managers align business strategies with capital allocation

decisions and provide transparency of financial condition to lenders and

equity capital providers.

• The Z Score is an effective tool to demonstrate credit worthiness to

bankers and soundness of business model to investors.

• The scoring system uses fives financial ratios that are calculated on the

basis of even financial data which is easily available from the balance

sheet and income statement of any company.

• It is a quantitative model that can be mapped with the credit scoring model

which is more of a mix of quantitative and qualitative measures.

• Being a quantitative model, it is very easy to draw insights from the

outcome.

• Investors usually use it to measure the solvency of a company in order to

decide whether to invest or not in that company.

2.2.10 Disadvantages

• One of the major disadvantages of the model is that it can only forecast

the likelihood of failure; only if the company is comparable to its

database. For instance, a restaurant typically exhibits a negative working

capital cycle and as such the model may end up indicating high

bankruptcy risk which is not true.

• The scoring system does not work well for new or emerging companies

as their earnings are too low and will end up indicating high risk.

14

• The model fails to incorporate the benefits of good cash flow

management.

• A misleading company financial will result in misleading Z score.

15

2.3 Empirical Literature

John Stephen Grice and Robert Wingram(2001). This study examines three

research questions using recent sample data: (1) Is Altman's original model as

useful for predicting bankruptcy in recent periods as it was for the periods in

which it was developed and tested by Altman? (2) Is the model as useful for

predicting bankruptcy of non-manufacturing firms as it is for predicting

bankruptcy of manufacturing firms? (3) Is the model as useful for predicting

financial stress conditions other than bankruptcy as it is for predicting

bankruptcy? The results are consistent with negative answers to questions one

and two and a positive answer to question three.

Hayes et al. (2010). As a result of the findings, the suggestion is that further

exploration of Altman’s Z score, and alternative formulas, is necessary to refine

this potentially useful tool in order to develop a predictive collection of tools

useful in predicting not only bankruptcy, but financial distress in a variety of

firms in a variety of contexts.

Gnyana Ranjan Bal(2015) The paper applied Altman’s Z-score to predict

corporate bankruptcy of select FMCG Companies. By applying Z-score and

select liquidity ratios the study concludes that the investors can use this model to

analyze financial position of the companies. In case of the select data, Z-score of

all companies for current year shows sound financial position and less chances

of bankruptcy in near future.

Lubawa, G. & Louangrath, P. (2016). The study used the Altman Z-score for

the privately held firms as the standard for evaluation. Multiple loans have

theoretical support in the literature. This paper claims that lenders stands to gain

more in case of default when there are multiple lenders.

16

Manjusha Senapati and Saptarshi Ghosa (2016) The model was tested for

some stressed industries/companies and was found to capture the underlying

distress. Distressed bank debt for the sample companies was found to be

increasing since 2011-12.

Soumya Agarwal and Guru Gobind Singh (2018). The empirical results

suggest the Z” Score model is a reliable predictor of current position of Top 5

Public Sectors Banks in India. The Z” Score has predicted the banking failures

successfully but a number of factors could suggest that the analysis was

somewhat biased. The Z” Score is only valid five years prior to bankruptcy.

Panigrahi Ashok(2019).This study uses Altman's 'Z' Score Model to test the

financial distress of a few selected pharmaceutical companies. This model has

been applied in several financial distress and bankruptcy studies with satisfactory

results.The result shows that the average Z-Score of the pharmaceutical industry

is 5.90 during the period of study. It clearly indicates that the pharmaceutical

industry has a healthy financial position because Z-Score is much above the cut-

off scores i.e. 1.8.

Apoorva D.and, Sneha Prasad Curpod(2019).Seven companies have been

selected to check the efficiency and accuracy of this model. As per this model,

bankruptcy of these companies could be predicted three years prior to the

occurring of the event in India. In conclusion, Altman Z score can be applied for

Indian companies; however the same is not 100% accurate.

Bracegirdle, Stewart.(2019).The Altman z-score bankruptcy model is used as

the statistical tool for determination of bankruptcy in the sample of independent

17

oil and gas companies. It was found that for the most part, the larger companies

did indeed experience less risk of bankruptcy, but the findings were inconclusive.

Prof. Vandana Samba and Dr. Vani Harpanahalli. (2020). The research paper

focuses on four financial ratio’s indicators of Altman Z-score in order to predict

or ascertain the financial distress and the bankruptcy position of the company.

By observing the Z-score model for prediction of bankruptcy resulted in “Grey

Zone” which means the company is almost near bankruptcy.

CHAPTER Ⅲ

INDUSTRY AND COMPANY

PROFILE

18

3.1 Introduction

This chapter deals with Industry Profile and Company Profile of Alok Industries

Ltd.

3.2 Industry Profile of Alok Industries Ltd.

3.2.1 Textile industry

The textile industry is primarily concerned with the design, production and

distribution of yarn, cloth and clothing. The raw material may be natural, or

synthetic using products of the chemical industry.The textile industry in India

traditionally, after agriculture, is the only industry that has generated huge

employment for both skilled and unskilled labour in textiles. The textile industry

continues to be the second-largest employment generating sector in India. It

offers direct employment to over 35 million in the country. India is first in global

jute production and shares 63% of the global textile and garment market. India

is second in global textile manufacturing and also second in silk and cotton

production. 100% FDI is allowed via automatic route in textile sector. Rieter,

Trutzschler, Saurer, Soktas, Zambiati, Bilsar, Monti, CMT, E-land, Nisshinbo,

Marks & Spencer, Zara, Promod, Benetton, and Levi’s are some of the foreign

textile companies invested or working in India.India’s textiles sector is one of

the oldest industries in the Indian economy, dating back to several centuries.

The industry is extremely varied, with hand-spun and hand-woven textiles

sectors at one end of the spectrum, while the capital-intensive sophisticated mills

sector on the other end. The decentralised power looms hosiery and knitting

sector forms the largest component in the textiles sector. The close linkage of

textiles industry to agriculture (for raw materials such as cotton) and the ancient

culture and traditions of the country in terms of textiles makes it unique in

comparison to other industries in the country. India’s textiles industry has a

capacity to produce wide variety of products suitable for different market

segments, both within India and across the world.

19

India is among the world's largest producers of Textiles and Apparel.The

domestic textiles and apparel industry contributes 2% to India’s GDP, 7% of

industry output in value terms and 12% of the country’s export earnings.The

textiles and apparel industry in India is the second-largest employer in the

country providing direct employment to 45 million people and 60 million people

in allied industries.India has also become the second-largest manufacturer of

PPE in the world. More than 600 companies in India are certified to produce

PPEs today, whose global market worth is expected to be over $92.5 bn by 2025,

up from $52.7 bn in 2019.

3.2.2 Industry Scenario

• FDI in the textiles and apparel industry has reached up to $3.45 bn

during 2020

• Exports in the textiles and apparel industry are expected to reach $300

bn by 2024-25 resulting in a tripling of Indian market share from 5% to

15%.

• The textiles and apparel industry can be broadly divided into two

segments - yarn and fibre and processed fabrics and apparel. The domestic

textiles and apparel market was estimated at US$ 100 billion in FY19.

The textile industry has around 4.5 crore workers including 35.22 lakh

handloom workers all over the country. In FY19, growth in private

consumption was expected to create strong domestic demand for textiles.

Growth in demand is expected to continue at 12% CAGR to reach US$

220 billion by 2025.

• Cotton production in India reached 36.04 million bales in FY20. During

FY19, production of fibre in India stood at 1.44 million tonnes (MT) and

reached 1.60 MT in FY20 (till January 2020), while that for yarn, the

production stood at 4,762 million kgs during same period.

20

• India is the world's second largest exporter of textiles and clothing.

Increased penetration of organised retail, favourable demographics, and

rising income level are likely to drive demand for textiles. Cloth

production stood at 63.34 billion square meters in FY20 (till January

2020).

• India’s textiles and apparel export is expected to increase to US$ 82.00

billion by 2021 from US$ 22.95 billion in FY20 (till November 2019).

• Rising Government focus and favourable policies is leading to growth

in the textiles and clothing industry. The Ministry of Textiles is

encouraging investment through increasing focus on schemes such as

Technology Up-gradation Fund Scheme (TUFS). In Union Budget 2020-

21, the Government has allocated Rs. 761.90 crore (US$ 109.01 million)

for Amended Technology Upgradation Fund Scheme (A-TUFS). The

Cabinet Committee on Economic Affairs (CCEA), Government of India

has approved a new skill development scheme named 'Scheme for

Capacity Building in Textile Sector (SCBTS)'. The Government

announced a special package to boost export by US$ 31 billion, create

one crore job opportunities and attract investment worth Rs. 80,000 crore

(US$ 11.93 billion) during 2018-2020. Cumulative FDI (Foreign Direct

Investment) inflow in the textiles sector stood at over US$ 3.45 billion

between April 2000 to June 2020.

• In Union Budget 2020-21, the Government of India has allocated around

Rs. 3,515 crore (US$ 502.93 million) to the Ministry of Textiles and Rs.

80 crore (US$ 11.45 million) for the scheme on Integrated Textile Parks.

The Ministry of Textiles has announced Rs. 690 crore (US$ 106.58

million) for setting up 21 readymade garment manufacturing units in

seven states for development and modernisation of Indian textile sector.

National Technical Textiles Mission is proposed for a period from 2020-

21

21 to 2023-24 at an estimated outlay of Rs. 1,480 crore (US$ 211.76

million).

• The National Handloom Development Programme has been allocated

Rs. 388.21 crore (US$ 55.55 million), whereas, the Integrated Processing

Development Scheme has received Rs. 50 crore (US$ 7.15 million) in

Union Budget 2020-21.

• On July 17, 2020, Khadi and Village Industries Commission (KVIC)

inaugurated the first-of-its-kind footwear training center in Delhi to train

the marginalized community of leather artisans.

• In May 2020, the Ministry of Textiles urged textile entrepreneurs to

reorient themselves and diversify their manufacturing skills to suit the

global demand amid the coronavirus pandemic.

3.2.3 Government Initiatives

Indian government has come up with several export promotion policies for the

textiles sector. It has also allowed 100% FDI in the sector under the automatic

route.

Initiatives taken by Government of India are:

• Defence Research and Development Organisation (DRDO) is helping

the Indian textile industry to produce yarns and eliminate dependence

on import of Chinese and other foreign clothing for military uniforms.

• In October 2020, the Cabinet Committee on Economic Affairs chaired

by Mr. Narendra Modi approved mandatory packaging of 100% food

grains and 20% sugar in jute bags. Under the Jute Packaging Materials

(Compulsory Use in Packing Commodities) Act, 1987, the

government is required to consider and provide for the compulsory

use of jute packaging materials for supply.

22

• Government launched production linked incentive scheme to provide

incentives for manufacture and export of specific textile products

made of man-made fibre.

• On September 2, 2020, the Union Cabinet approved signing an MOU

between textile committee, India and M/s Nissenken Quality

Evaluation Centre, Japan, for improving quality and testing Indian

textiles and clothing for the Japanese market. This India-Japan pact on

cooperation in textiles will facilitate Indian exporters to meet the

requirements of Japanese importers as per the latter’s technical

regulations.

• Under Union Budget 2020-21, a National Technical Textiles Mission

is proposed for a period from 2020-21 to 2023-24 at an estimated

outlay of Rs. 1,480 crore (US$ 211.76 million).

• In 2020, New Textiles Policy 2020 is expected to be released by the

Ministry of Textiles.

• The Directorate General of Foreign Trade (DGFT) has revised rates

for incentives under the Merchandise Exports from India Scheme

(MEIS) for two subsectors of Textiles Industry - readymade garments

and made-ups - from 2% to 4%.

• The Government of India has taken several measures including

Amended Technology Up-gradation Fund Scheme (A-TUFS),

estimated to create employment for 35 lakh people and enable

investment worth Rs. 95,000 crore (US$ 14.17 billion) by 2022.

• Integrated Wool Development Programme (IWDP) was approved by

Government of India to provide support to the wool sector, starting

from wool rearer to end consumer, with an aim to enhance quality and

increase production during 2017-18 and 2019-20.

23

3.2.4 Market Size

India’s textiles industry contributed 7% of the industry output (in value terms)

in FY19. It contributed 2% to the GDP of India and employed more than 45

million people in FY19. The sector contributed 15% to India’s export earnings

in FY19.

Textiles industry has around 4.5 crore employed workers including 35.22 lakh

handloom workers across the country.The domestic textiles and apparel market

stood at an estimated US$ 100 billion in FY19.

The production of raw cotton in India is estimated to have reached 36.04 million

bales in FY20. During FY19, production of fibre in India stood at 1.44 million

tonnes (MT) and reached 1.60 MT in FY20 (till January 2020), while that for

yarn, the production stood at 4,762 million kgs during same period.

3.2.5 Production Overview

India is the second largest producer of fibre in the world and the major fibre

produced is cotton. Other fibres produced in India include silk, jute, wool,

and man-made fibers. 60% of the Indian textile Industry is cotton based. The

strong domestic demand and the revival of the Economic markets by 2009 has

led to huge growth of the Indian textiles industry. In December 2010, the

domestic cotton price was up by 50% as compared to the December 2009 prices.

The causes behind high cotton price are due to the floods in Pakistan and China

. India projected a high production of textile (325 lakh bales for 2010 -11). There

has been increase in India's share of global textile trading to seven percent in five

years. The rising prices are the major concern of the domestic producers of the

country.

• Man Made Fibres: This includes manufacturing of clothes

using fibre or filament synthetic yarns. It is produced in the

large power loom factories. They account for the largest sector

of the textile production in India. This sector has a share of 62%

24

of the India's total production and provides employment to

about 4.8 million people.

• The Cotton Sector: It is the second most developed sector in

the Indian Textile industries. It provides employment to a huge

number of people but its productions and employment is

seasonal depending upon the seasonal nature of the production.

• The Handloom Sector: It is well developed and is mainly

dependent on the SHGs for their funds. Its market share is

13% of the total cloth produced in India.

• The Woolen Sector: India is the 7th largest producer of the

wool in the world. India also produces 1.8% of the world's total

wool.

• The Jute Sector: The jute or the golden fibre in India is mainly

produced in the Eastern states of India like Assam and West

Bengal. India is the largest producer of jute in the world.

• The Sericulture and Silk Sector: India is the second largest

producer of silk in the world. India produces 18% of the world's

total silk. Mulberry, Eri, Tasar, and Muga are the main types of

silk produced in the country. It is a labour-intensive sector.

25

3.3 Company Profile of Alok Industries Ltd.

3.3.1 History and Evolution

Alok was established in 1986 as a private limited company, with our first

polyester texturising plant being set up in 1989. We became a public limited

company in 1993. Over the years, we have expanded into weaving, knitting,

processing, home textiles and garments. And to ensure quality and cost

efficiencies we have integrated backward into cotton spinning and

manufacturing partially oriented yarn through the continuous polymerisation

route. We also provide embroidered products through Grabal Alok Impex Ltd.,

our associate company. That is how Alok evolved into a diversified manufacturer

of world-class home textiles, garments, apparel fabrics and polyester yarns,

selling directly to manufacturers, exporters, importers, retailers and to some of

the world’s top brands.

Alok has a strong foothold in the domestic retail segment through a wholly

owned subsidiary, Alok H&A Limited, under the cash & carry model that offer

garments and home textiles at attractive price points.Alok also has an

international presence in the retail segment through its associate concern, Grabal

Alok (UK) Limited. This entity owns more than 200 outlets across England,

Scotland and Wales vending value for money ranges for menswear,

womenswear, childrenwear, footwear, homeware and accessories.In addition,

Alok has also invested in premium commercial/residential projects across

Mumbai through its wholly owned subsidiaries.

3.3.2 Vision

To be the world's best integrated textile enterprise, driven by research &

innovation, with a leadership position across products & markets, while

exceeding customer & stakeholder expectations.

26

3.3.3 Mission

• Be a knowledge leader & an innovator in our business

• Maximise people :development initiatives

• Optimise use of all resources

• Become a process driven organisation

• Exceed compliance and global quality standards

• Actively explore potential market & products

• Offer innovative, customised and value-added services to our customers

• Be an ethical, transparent and responsible global organization

3.3.4 Values

1. Customer Satisfaction

We will be attuned to market needs; wherever possible, we will anticipate market

needs; we will respond quickly to changes in customer requirements; we will be

completely focused on quality; we will keep delivery commitments on time and

every time; we will develop new products and processes that will go beyond

customer satisfaction to achieve customer delight.

2. Passionate About Excellence

Excellence is non-negotiable in every aspect of our business process. Superior

quality of performance is critical to our business growth and success. We will

constantly strive to exceed expectations: be it internal or external.

3. Develop Human Capital

We will empower, energise and inspire our people to perform beyond their best;

we will create empowered teams that take informed decisions; we will recognise

and leverage skills and strengths of various teams; we will enable sharing of

knowledge; we will create an adequate 'bench strength' that will take care of

changes in business scenarios.

27

4. Fair To All

All our actions will be determined by fairness; we shall be fair to our

customers, vendors, shareholders, all our business partners and society at large.

Fairness is not just sticking to the letter of the law or the contract but

appreciating its spirit and basing all our actions on being fair to the spirit of that

understanding.

5. Concern For The Environment And The Community

We will take the utmost care of our environment and the communities in which

we operate; we shall nurture our environment and its natural resources and shall

ensure that none of our actions deplete or pollute them; we will encourage

initiatives that create environmental sustainability and help in community

development

6. Safety And Health

We will provide a safe workplace. We will promote the health and well-being of

our people and their families. We will encourage healthy work habits and a

'work-life' balance. We believe that working safely and protecting the health of

our people is 'working smart' and creates greater and more sustainable wealth.

7. Responsible Corporate Citizen

We recognise that we have our responsibilities towards the society in which we

operate. We commit ourselves to be a responsible corporate citizen; our

activities should not only create shareholder.

3.3.5 Human Resource

At Alok, the role of the HR team is structured to meet the needs of the

organization. As a successful organization, Alok is becoming more adaptive,

resilient, quick to change direction and customer-centered. Within this

28

environment, the HR team is a strategic partner, an employee sponsor or

advocate and a change mentor.

1. Strategic Partner:

In the role as a strategic partner, the HR team contributes to the development of

and the accomplishment of the organization-wide business plan and objectives.

The HR business objectives are established to support the attainment of the

overall strategic business plan and objectives. This strategic partnership impacts

HR services such as the design of work positions; hiring; reward, recognition

and strategic pay; performance development and appraisal systems; career and

succession planning; and employee development.

2. Employee Advocate:

As an employee sponsor or advocate, the HR function plays an integral role in

organizational success via knowledge about and advocacy of people. This

advocacy includes expertise in how to create a work environment in which

people will choose to be motivated, contributing, and happy.

3. Change Champion:

The constant evaluation of the effectiveness of the organization results in the

need for the HR team to frequently champion change. Both knowledge about and

the ability to execute successful change strategies makes the HR team a key

catalyst to bring about change in the organization. This a critical attribute to

minimize employee dissatisfaction and resistance to change.

29

3.3.6 Corporate Social Responsibility(Sustainable Growth)

Alok Industries' focus on activities related to sustainability is at the core of its

long term goal of being a leader in providing sustainable and integrated textile

solutions. The sustainability programmes includes interventions in prevention of

environmental degradation, promotion of energy conservation and stress on

community development.

Environment

On the environment protection front the thrust is on green development. This

includes promoting green procurement to minimize environmental degradation

through mitigation of environmental impact on Climate Change and pollution of

Air, Water and Soil. At Alok, waste recycling is actively pursued across all its

processes by establishing long term contractual relations with vendors,

contractors and agencies with established credentials on waste recycling. The

endeavour is to demonstrate environmental leadership and influence the industry

and citizens at large to encourage use of environmental friendly products,

processes and services. The Company is emerging as a model in the region for

Waste management by supporting innovation, development of new technologies

and creation of demand in the mainstream society for environmental friendly

products and services.

The Company increasingly uses ethical fibres like Organic cotton (cotton grown

without the use of external synthetic agricultural inputs like fertilizers and

pesticides and helps conserve the environment from the harmful effects of the

use of hazardous agro chemicals) and Better cotton from Better Cotton Initiative

(BCI) (involves educating the cotton growers to adopt the Best Management

Practices in cotton cultivation). This is not only leading to helping conserve the

fragile environment threatened today by indiscriminate use of agro chemicals

and pesticides but will also help farmers get a decent farm earnings sustain their

livelihoods.

30

In addition, the Company has 'best in class' ETP system established for primary,

secondary and tertiary treatment of effluents and reverse osmosis plant to

optimize water conservation. It also has "Green Zones" around all facilities and

encourages planting of saplings to conserve ecological balance. The Company

has strived to minimize air pollution from its plants and units by installing

Selective Catalytic Reduction (SCR) systems in the exhaust of the DG sets which

reduce oxides of Nitrogen. Alok encourages the use of recycled products and has

set up a recycled polyester unit with an initial 10 tons per day of capacity to

recycle polyester and polyester yarn waste, flakes and PET bottles to produce

100% recycled polyester fibre.

Energy Management

Alok is committed to:

• Achieve the lowest Specific Energy Consumption per unit of product,

thereby minimizing Greenhouse emissions, solid waste and water

pollution.

• Attain sustainable development by continuously improving Energy

Conservation and Energy efficiency throughout the production cycle.

• Prevent wastage of energy in any mode - steam, water, air or power - by

efficient and most optimal use of resources.

• Comply with all applicable legislations, and best practices on Energy

Management Community Development

Alok is a Fair Trade (FLO) certified company and value the fair price concept

across the value chain. Since the textile chains have resource poor growers as the

weak link at the far end of the chain, Alok initiated and has been instrumental in

31

few of the well known Organic & Fair Trade cotton projects in India and abroad

where in a premium is paid to the marginal Organic and Fair Trade cotton

growers. Alok buys back their farm produce to enable them effectively integrate

with the market and remain sustainable in a highly volatile cotton business. Alok

partnered with Zameen Organic in an effort to form a golden textile value chain

which included a farmer owned Organic & Fair Trade Company.

Similarly, cotton made in Africa (CMiA) is another important variant of

sustainable cotton type Alok is into and supplies its quality products to

sophisticated markets in parts of Europe. Alok has been playing a key role in a

very ambitious Organic & Fair Trade cotton project in West Africa which has

the world's top lingerie brand on board.Corporate Social Responsibility (CSR)

initiatives are integral to operations at the plants. Alok has started a public school

with CBSE Board in Silvassa. It employs tribal women on weaving looms and

garment/made up stitching machines after intensive training and orientation. The

Company has a Private Public Partnership with Silvassa Administration for

converting the Government owned Industrial Training Institute into a centre of

excellence.

3.3.7 Group Companies

In April 2007, Alok acquired 60% of the equity of Mileta a.s, a ‘top of the line’

integrated textile entity situated in the Czech Republic; subsequently, Alok has

raised its stake in the company to 79.80%. Mileta is one of the premium textile

enterprises in Europe, manufacturing handkerchiefs, shirting fabrics, table linen,

bed linen and other premium products. Mileta exports most of its production to

Europe, North and South America, Africa, Middle East, Far East and

Australia.The Mileta acquisition brings significant synergies to both entities.

While Alok has access to Mileta’s premium-product technology and penetrates

deeper into high-end European markets, Mileta now has a strong support base

and easy access to India.Mileta’s brands – Mileta, Erba, Cottonova, Lord Nelson

and Wall Street – have high recall. Alok has launched some of these brands –

32

Erba (for handkerchiefs) and Lord Nelson (for premium shirting) – in the Indian

market. Cottonova bed linen is now also being manufactured in Alok’s plants

and being exported.

3.3.8 Board Of Directors

1. Siddharth Achuthan, Chairman of the Board (Non-Executive,

Independent Director)

Siddharth Achuthan (DIN: 00016278) is a Commerce and Law graduate from

the Mumbai University, a fellow member of the Institute of Chartered

Accountants of India and an associate member of the Institute of Company

Secretaries of India. Mr. Siddharth Achuthan was associated with Deloitte,

Haskins & Sells for over 4 decades and served as Partner for 33 years. He has

vast and varied experience in the field of Audit of domestic as well as

multinational companies in sectors such as Manufacturing, Hospitality,

Technology and Non-Banking Financial Services. Presently, he is on the Board

of M/s. Reliance Industrial Infrastructure Limited and M/s. Indiabulls Housing

Finance Limited.

2. Anil Rajbanshi (Non-Executive, Non Independent Director)

Anil Rajbanshi (DIN: 03370674) is the Member of the National Committee of

Textiles of CII and FICCI. He represents Reliance and SRTEPC in Textiles

Committee and represents Reliance Industries Limited at Sasmira. He has many

years of experience of working with major fibre producers and has been involved

with the Indian Man-made fibre textiles industry since 1989. Mr. Anil Rajbanshi,

is the Ex-Chairman of The Synthetic & Rayon Textiles Export Promotion

Council and is a long Standing Member of Committee of Administration of the

Council (SRTEPC).He is the Senior Executive Vice President & Head Corporate

Affairs of PETCHEM at M/s. Reliance Industries Limited. He is the Director of

Recron (Malaysia) Sdn Bhd, a Reliance Group company that operates world’s

largest integrated textile complex. He was knighted by Government of Malaysia

in 2008.

33

3. Hemant Desai (Non-Executive, Non Independent Director)

Hemant Desai (DIN: 00008531) is a Member of Board of Governors, Auro

University, a deemed University in Surat, Gujarat. Mr. Hemant Desai is

Managing Director, Gujarat Chemical Port Ltd. (GCPL), a joint venture of

Reliance Industries Limited (RIL) and Six PSUs of Govt. of Gujarat. GCPL has

modern port infrastructure and facilities for handling 5 MMTPA of liquid

hydrocarbons, cryogenic petrochemicals and chemicals.He is part of the core

leadership team at RIL for the past more than three decades. He is Advisor and

Mentor, Reliance Group leading diverse corporate initiatives of Petrochemicals

Complex at Hazira and Dahej, Man-made fibres business, Jamnagar Refinery

and SEZ, its related industrial infrastructure of Power, Ports, Petroleum and Gas

Pipelines, Petro-Retail outlets. He is also actively involved with RIL’s fast

growing Consumer businesses of Retail, Jio 4G and Broadband .He is

spearheading various business and public institutions as Chairman of: Hazira

Area Industries Association (HAIA) (Hazira has attracted investments worth

US$ 27 Bn), Board of Management of Hazira Notified Area and Gujarat Captive

Jetty Association.

4. Venkataraman Ramachandran (Non-Executive, Non Independent

Director)

Venkataraman Ramachandran (DIN: 02032853) is a Commerce graduate from

the Bharathiar University and an associate member of the Institute of Chartered

Accountants of India, the Institute of Cost Accountants of India and the Institute

of Company Secretaries of India. He has over 25 years of work experience in

audit, accounting, finance, taxation and corporate law functions across various

sectors such as manufacturing, telecommunications, technology and

infrastructure. He has been associated with the Reliance group since 2004.

34

5. Samir Chawla (Non-Executive, Non Independent Director)

Samir Chawla (DIN: 03499851) holds PGDM from IIM Calcutta and B.Tech.

from IIT Kanpur. Mr. Samir Chawla has over 26 years of experience in Banking

and Financial Services Sector and is associated with JM Financial Asset

Reconstruction Company Limited (JMFARC) since October 2017. Prior to

JMFARC, for 4 years, he had a venture which helped companies in

restructurings.

6. Rahul Dutt (Non-Executive, Independent Director)

Rahul Dutt (DIN: 08872616) is a legal professional with bachelor’s degree in

Law from the Government Law College, Mumbai (2000). He has a master’s

degree with distinction in Law from the UK (University of Leicester, 2001). He

is a member of the Bar Council of Maharashtra & Goa, and a partner in the

Mumbai office of the law firm M/s. Khaitan & Co. He was recognized as a

Notable Practitioner for expertise in Corporate M&A by Asia Law Profile.He

has over 15 years' work experience with focus on mergers and acquisitions, joint

ventures, infrastructure, technology licensing and business contracts across

various sectors such as petrochemicals, petro-marketing, telecommunications,

retail, and sports.

7. Mumtaz Bandukwala (Non-Executive, Independent Director)

Mumtaz Bandukwala (DIN: 07129301) is commerce and law Graduate and has

been a practicing Solicitor since the last almost 30 years. Her specialization has

mainly been in Companies Act and Securities laws. She has handled several

mergers and private equity investments in companies in India. She has also

handled arbitrations and property matters. Presently, she is practicing as a partner

of M/s. Junnarkar & Associates, Advocates, Solicitors and Notary.

CHAPTER Ⅳ

DATA ANALYSIS AND

INTERPRETATION

35

4.1 Introduction

This chapter consists of ratio analysis, calculation of Z-score, comparing

discriminations and data interpretation.

4.2 Research Methodology

This study is analytical in nature and the sample selected for the study is that of

Alok Industries Ltd. Secondary data have been used to conduct the respective

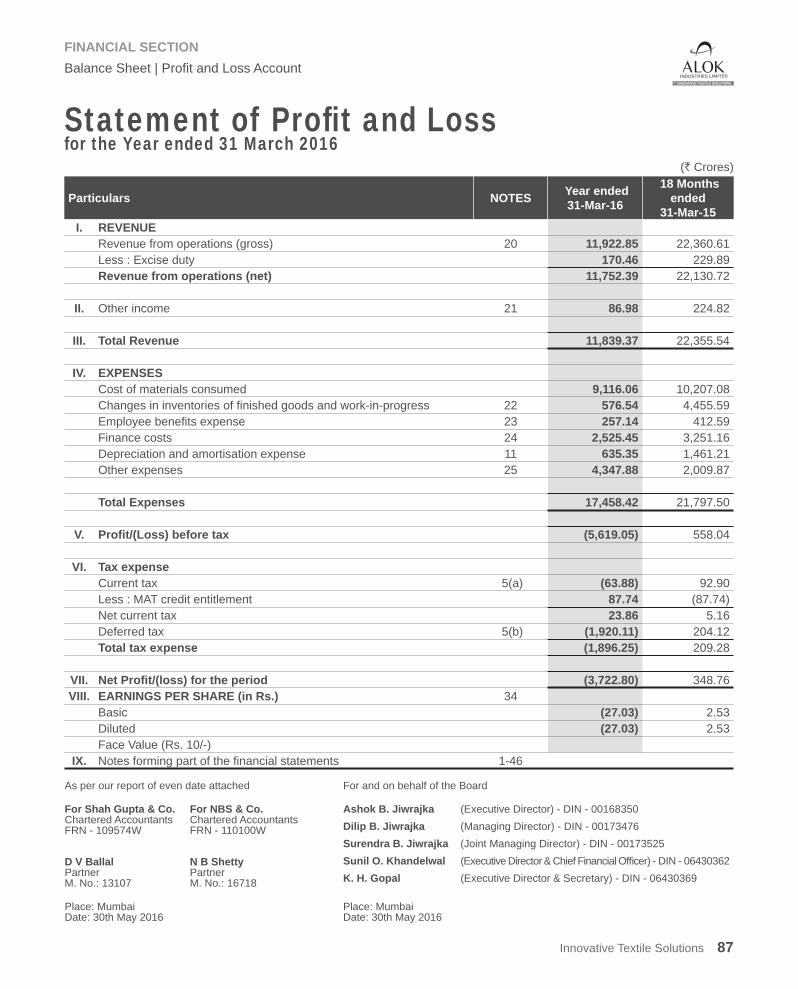

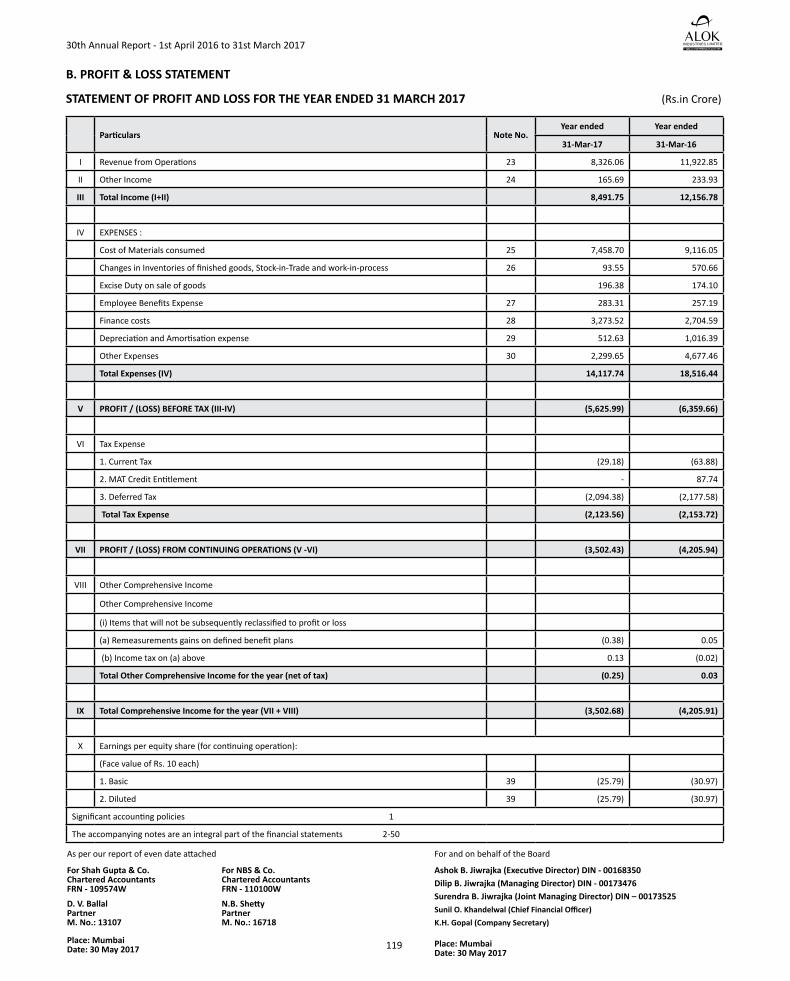

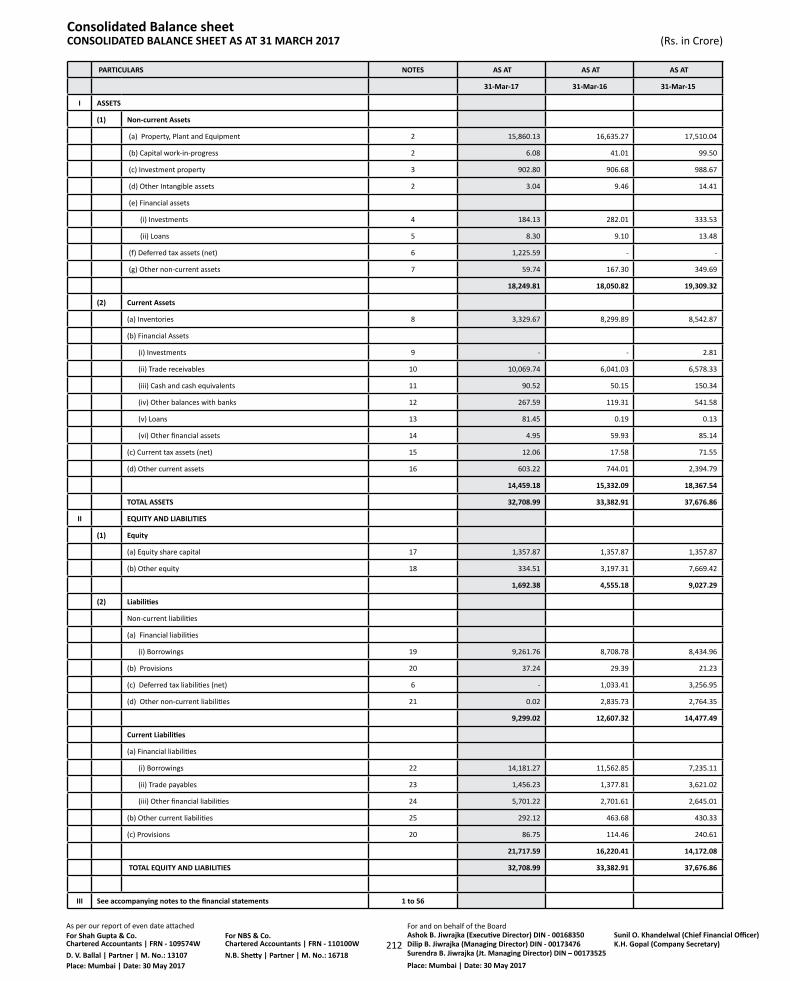

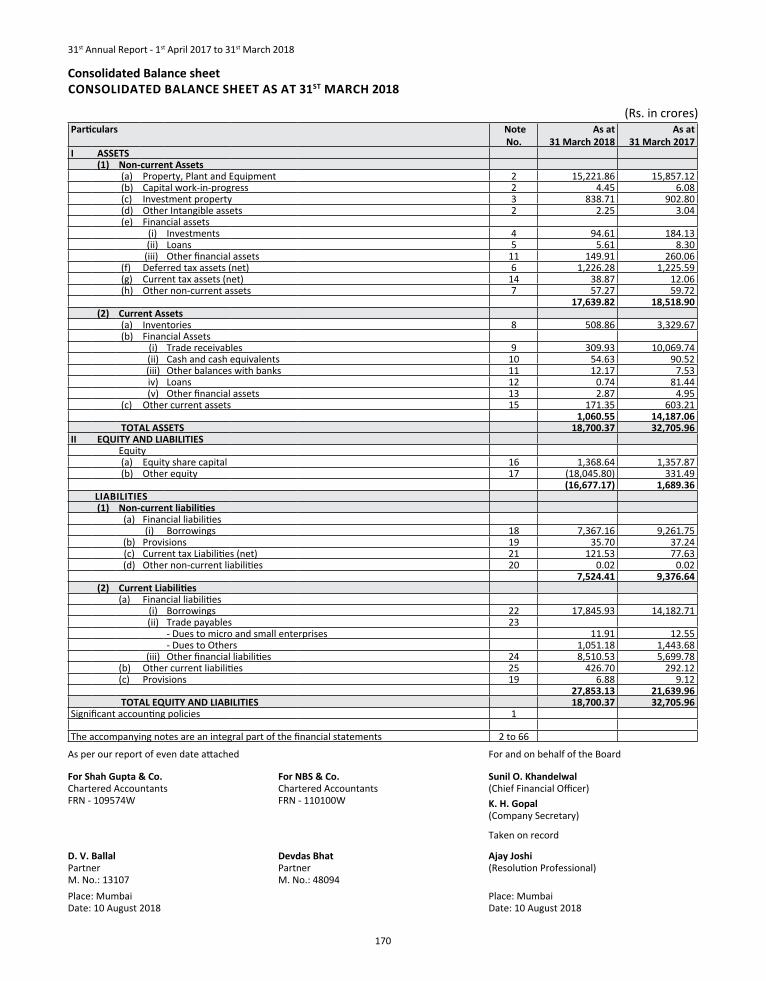

study. The data for the analysis was largely collected from the annual reports of

the sample company. Annual Reports were downloaded from the official website

of Alok Industries Ltd. Data from the financial year 2015-16 to 2019-20 were

analyzed and Altman’s Z score was applied to arrive at the respective

interpretation and analysis.

Following ratios have been used for analysis:

1. Working Capital to Total Assets

X1 = working capital

total assets

2. Retained Earnings to Total Assets

X2 = retained earnings

total assets

3. Earnings Before Interest and Tax to Total Assets

X3 = earnings before interest and taxes

total assets

4. Market Value of Equity to Total Liabilities

X4 = market value of equity

total liabilities

5. Sales to Total Assets

X5 = sales

total assets

36

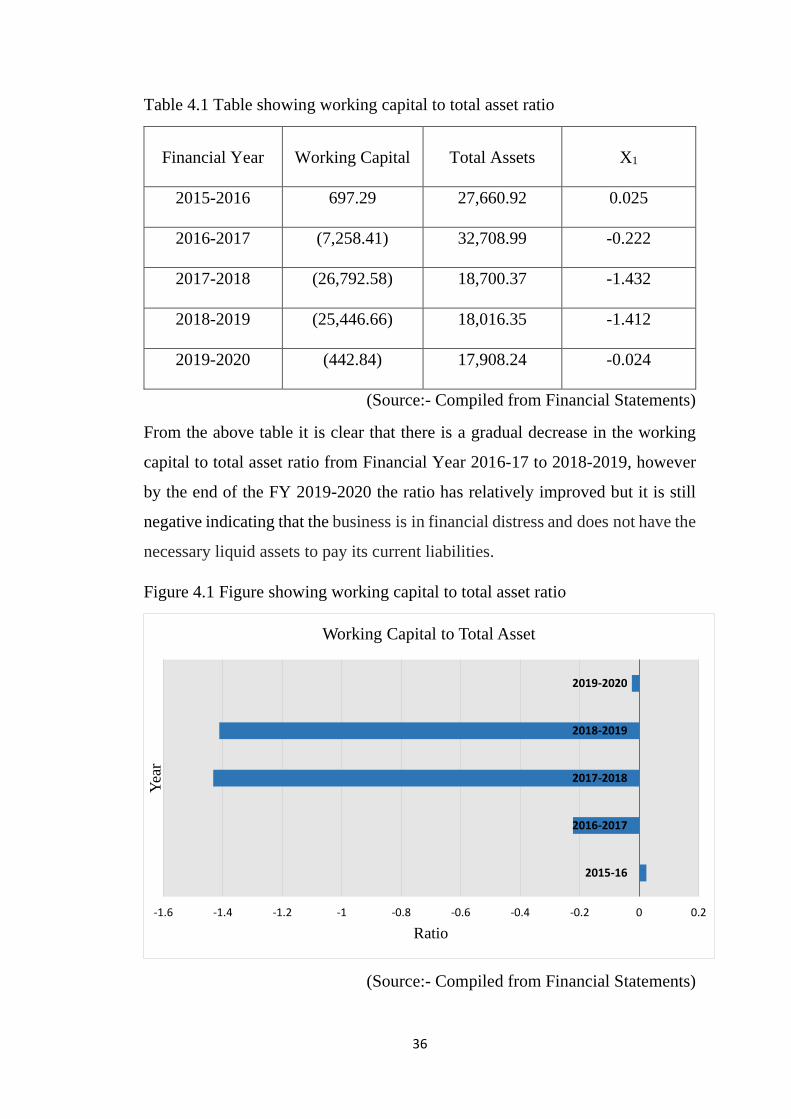

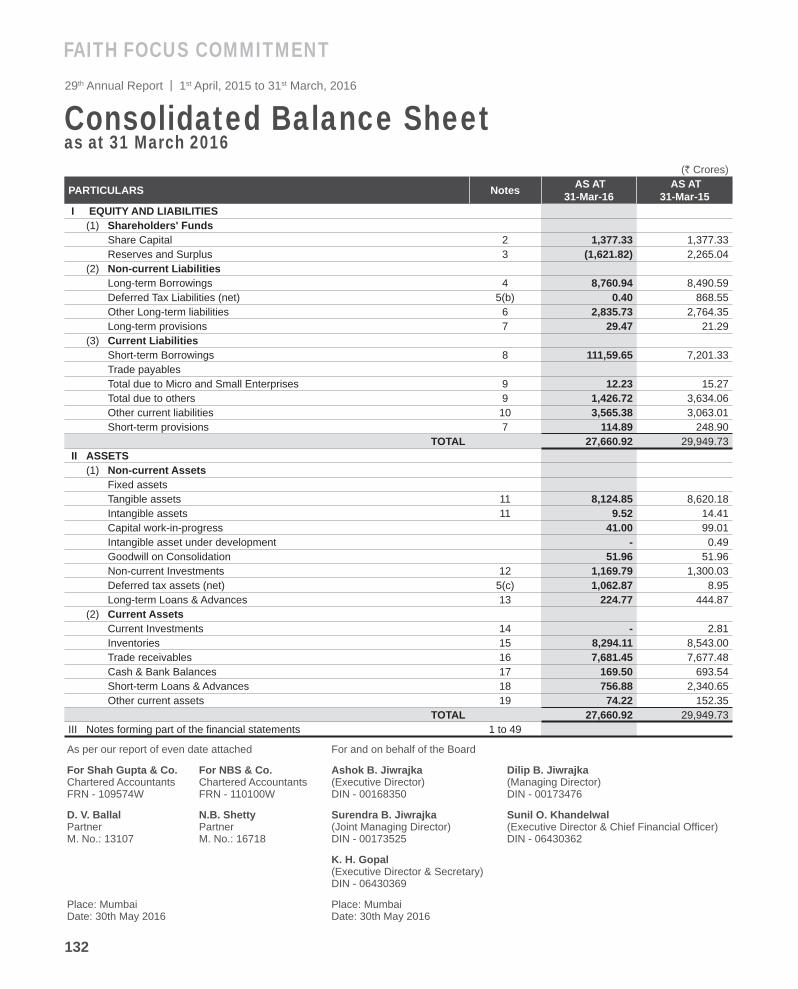

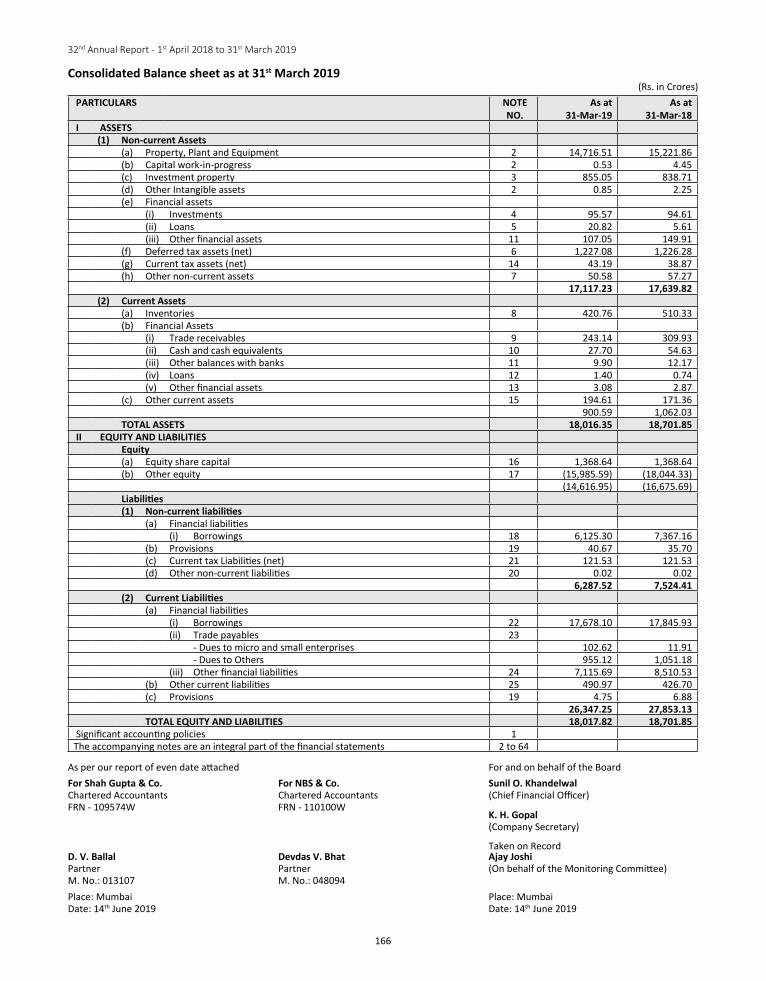

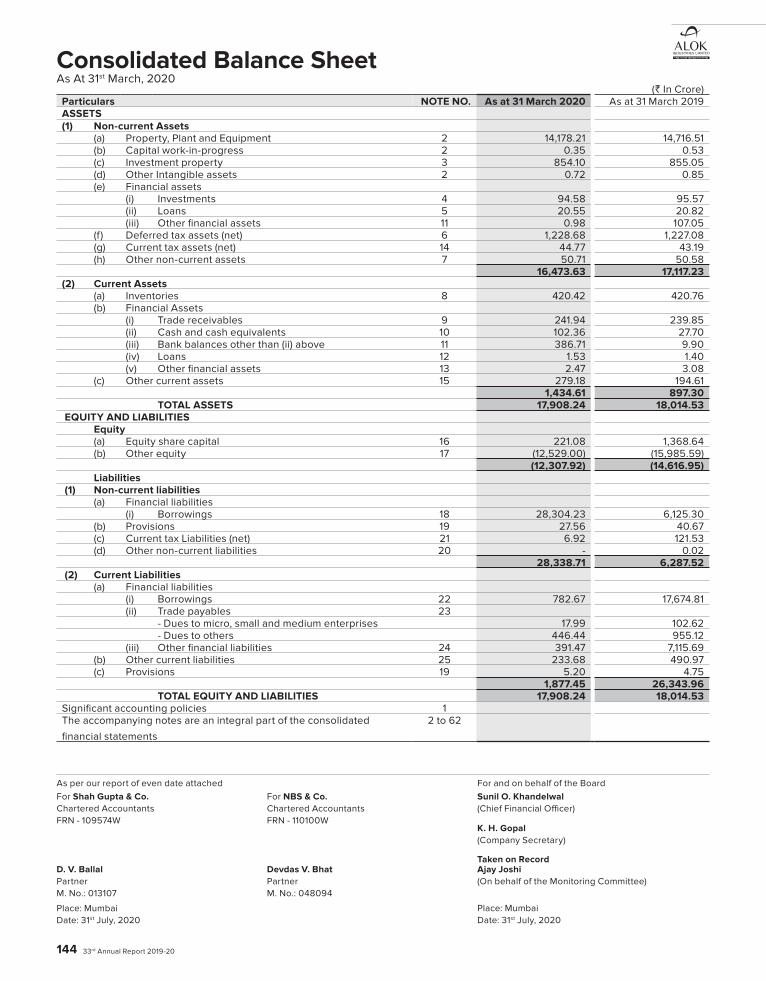

Table 4.1 Table showing working capital to total asset ratio

Financial Year

Working Capital

Total Assets

X1

2015-2016

697.29

27,660.92

0.025

2016-2017 (7,258.41)

32,708.99

-0.222

2017-2018 (26,792.58)

18,700.37

-1.432

2018-2019 (25,446.66)

18,016.35

-1.412

2019-2020 (442.84)

17,908.24

-0.024

(Source:- Compiled from Financial Statements)

From the above table it is clear that there is a gradual decrease in the working

capital to total asset ratio from Financial Year 2016-17 to 2018-2019, however

by the end of the FY 2019-2020 the ratio has relatively improved but it is still

negative indicating that the business is in financial distress and does not have the

necessary liquid assets to pay its current liabilities.

Figure 4.1 Figure showing working capital to total asset ratio

(Source:- Compiled from Financial Statements)

-1.6 -1.4 -1.2 -1 -0.8 -0.6 -0.4 -0.2 0 0.2

2015-16

2016-2017

2017-2018

2018-2019

2019-2020

Ratio

Yea

r

Working Capital to Total Asset

37

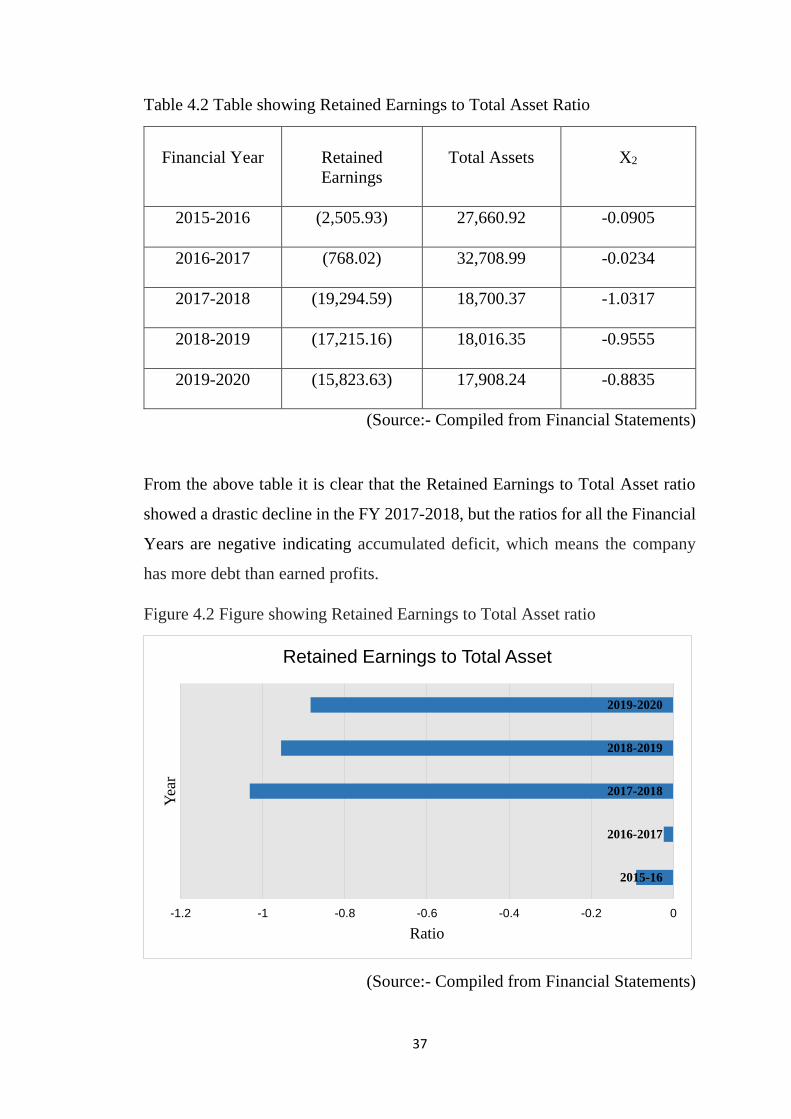

Table 4.2 Table showing Retained Earnings to Total Asset Ratio

Financial Year

Retained

Earnings

Total Assets

X2

2015-2016

(2,505.93)

27,660.92 -0.0905

2016-2017 (768.02)

32,708.99

-0.0234

2017-2018 (19,294.59)

18,700.37

-1.0317

2018-2019 (17,215.16)

18,016.35

-0.9555

2019-2020 (15,823.63)

17,908.24

-0.8835

(Source:- Compiled from Financial Statements)

From the above table it is clear that the Retained Earnings to Total Asset ratio

showed a drastic decline in the FY 2017-2018, but the ratios for all the Financial

Years are negative indicating accumulated deficit, which means the company

has more debt than earned profits.

Figure 4.2 Figure showing Retained Earnings to Total Asset ratio

(Source:- Compiled from Financial Statements)

-1.2 -1 -0.8 -0.6 -0.4 -0.2 0

2015-16

2016-2017

2017-2018

2018-2019

2019-2020

Ratio

Yea

r

Retained Earnings to Total Asset

38

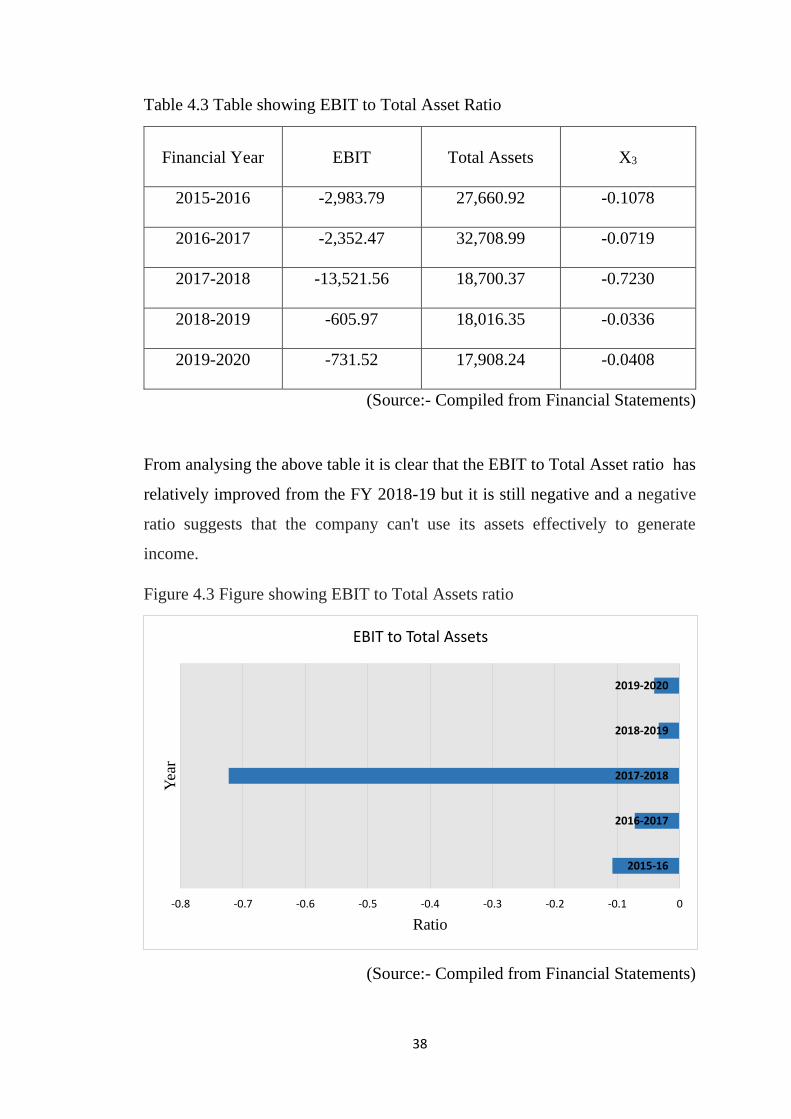

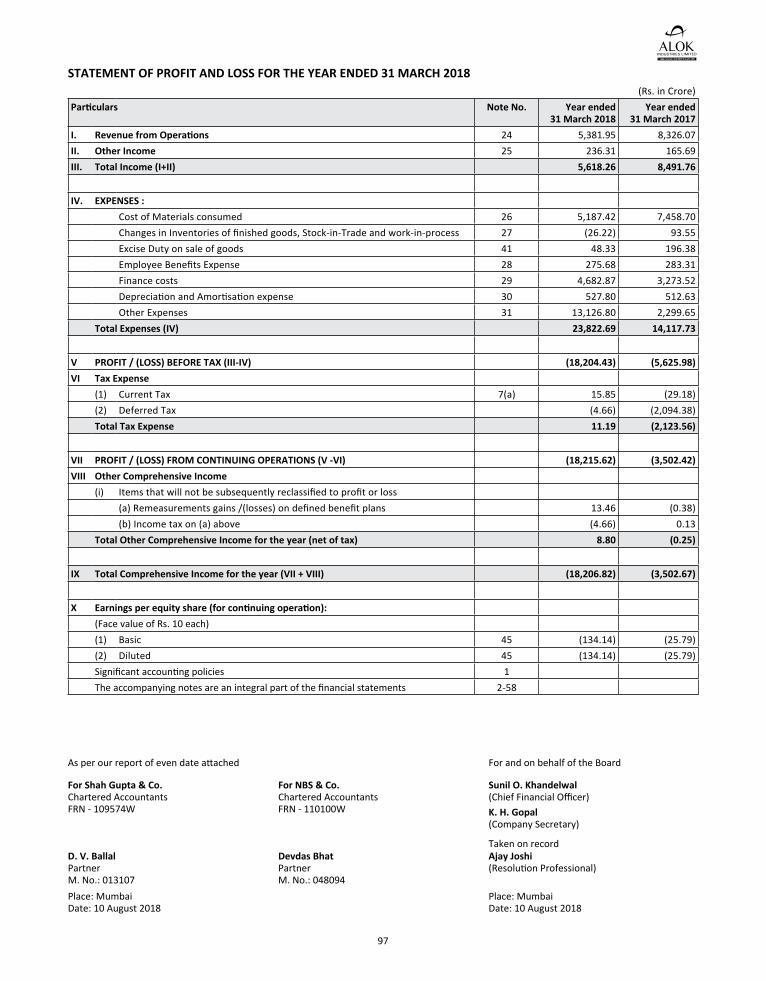

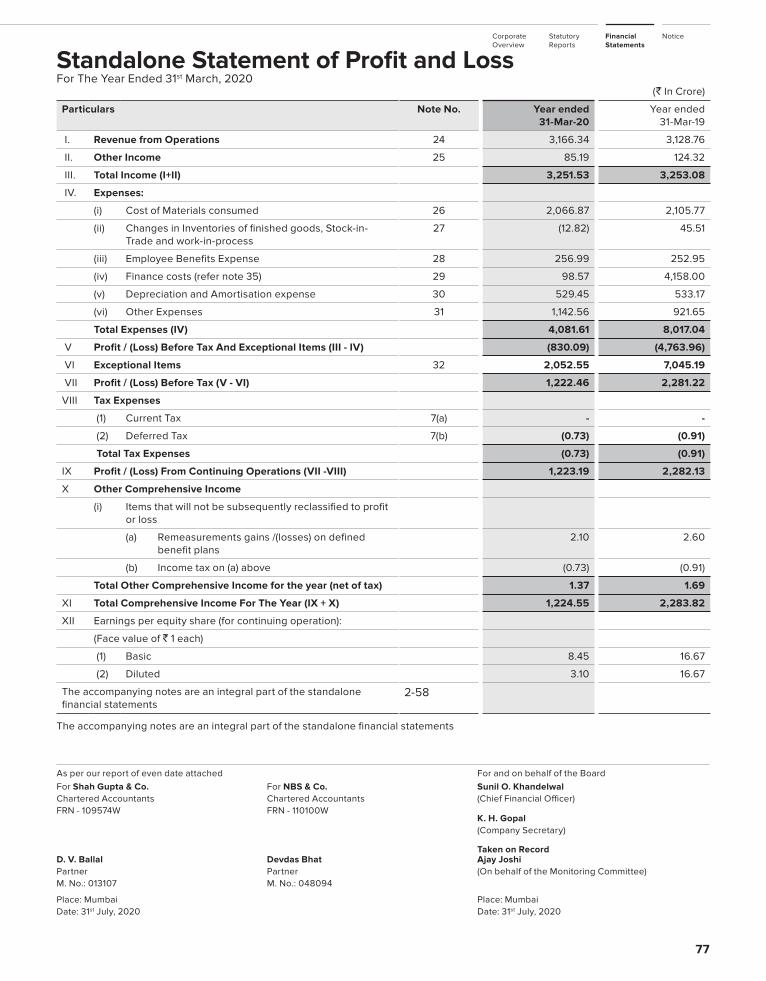

Table 4.3 Table showing EBIT to Total Asset Ratio

Financial Year

EBIT

Total Assets

X3

2015-2016

-2,983.79

27,660.92

-0.1078

2016-2017 -2,352.47

32,708.99

-0.0719

2017-2018 -13,521.56

18,700.37

-0.7230

2018-2019 -605.97

18,016.35

-0.0336

2019-2020 -731.52 17,908.24

-0.0408

(Source:- Compiled from Financial Statements)

From analysing the above table it is clear that the EBIT to Total Asset ratio has

relatively improved from the FY 2018-19 but it is still negative and a negative

ratio suggests that the company can't use its assets effectively to generate

income.

Figure 4.3 Figure showing EBIT to Total Assets ratio

(Source:- Compiled from Financial Statements)

-0.8 -0.7 -0.6 -0.5 -0.4 -0.3 -0.2 -0.1 0

2015-16

2016-2017

2017-2018

2018-2019

2019-2020

Ratio

Yea

r

EBIT to Total Assets

39

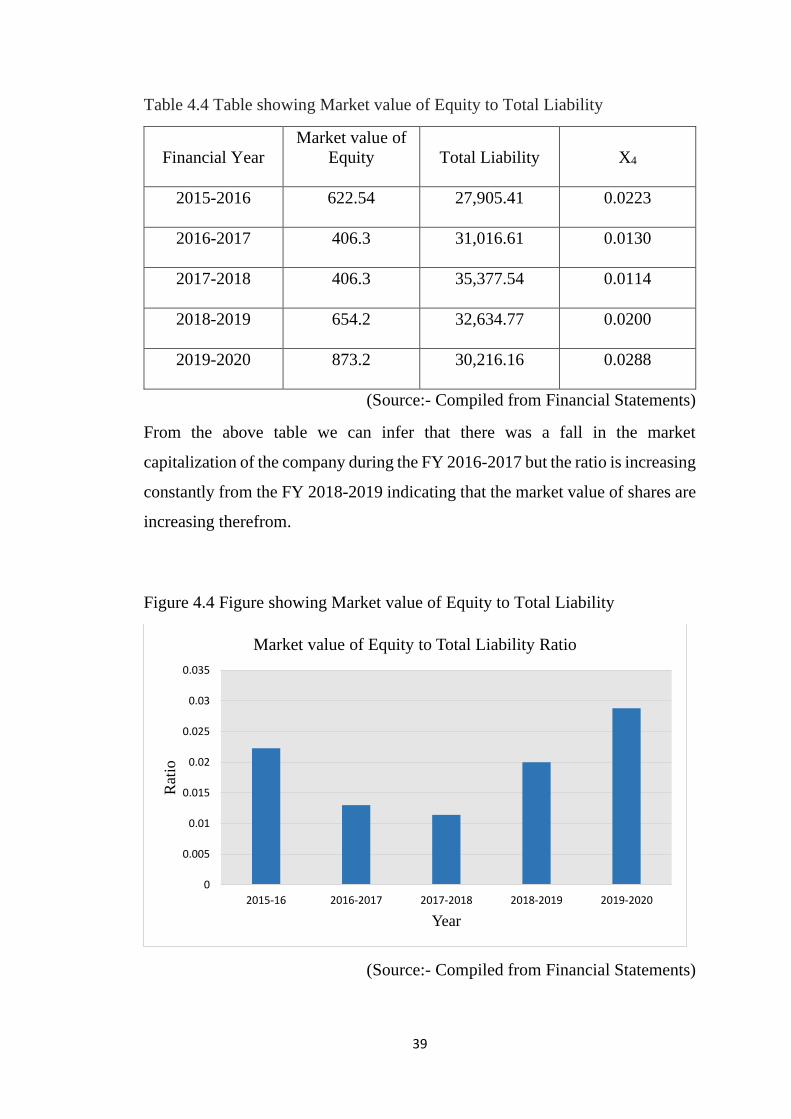

Table 4.4 Table showing Market value of Equity to Total Liability

Financial Year

Market value of

Equity

Total Liability

X4

2015-2016

622.54

27,905.41

0.0223

2016-2017 406.3

31,016.61

0.0130

2017-2018 406.3

35,377.54

0.0114

2018-2019 654.2

32,634.77

0.0200

2019-2020 873.2

30,216.16

0.0288

(Source:- Compiled from Financial Statements)

From the above table we can infer that there was a fall in the market

capitalization of the company during the FY 2016-2017 but the ratio is increasing

constantly from the FY 2018-2019 indicating that the market value of shares are

increasing therefrom.

Figure 4.4 Figure showing Market value of Equity to Total Liability

(Source:- Compiled from Financial Statements)

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

2015-16 2016-2017 2017-2018 2018-2019 2019-2020

Rat

io

Year

Market value of Equity to Total Liability Ratio

40

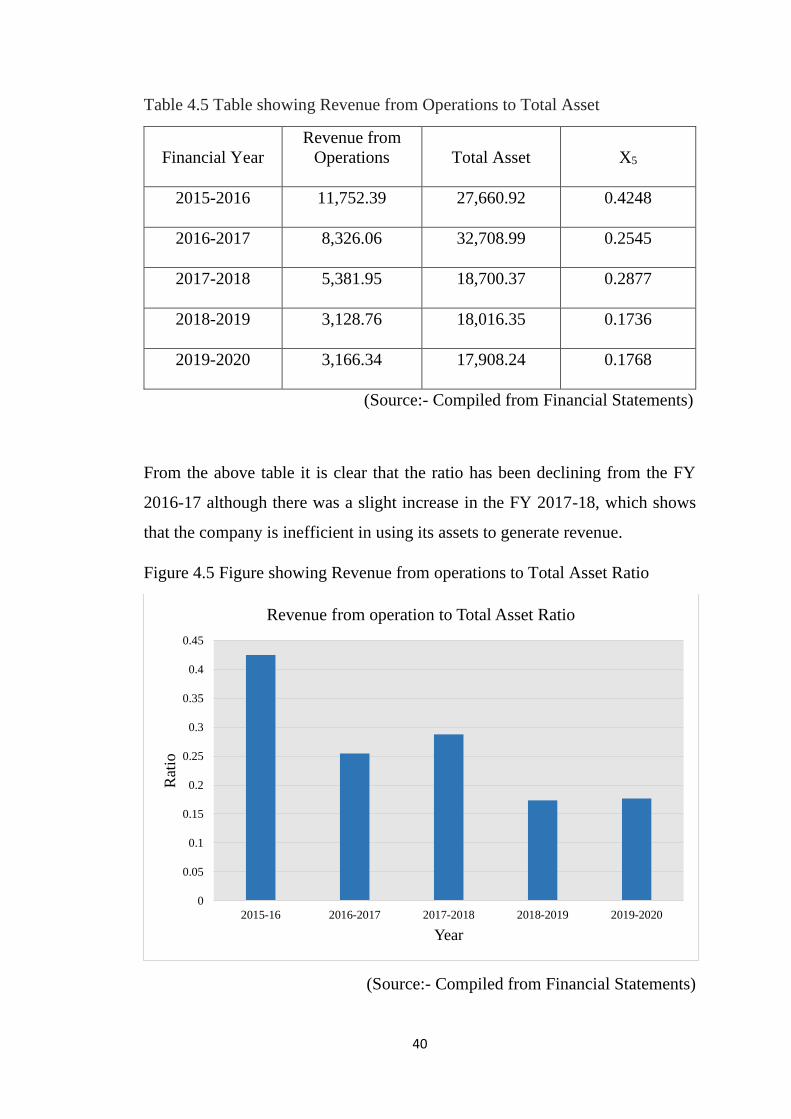

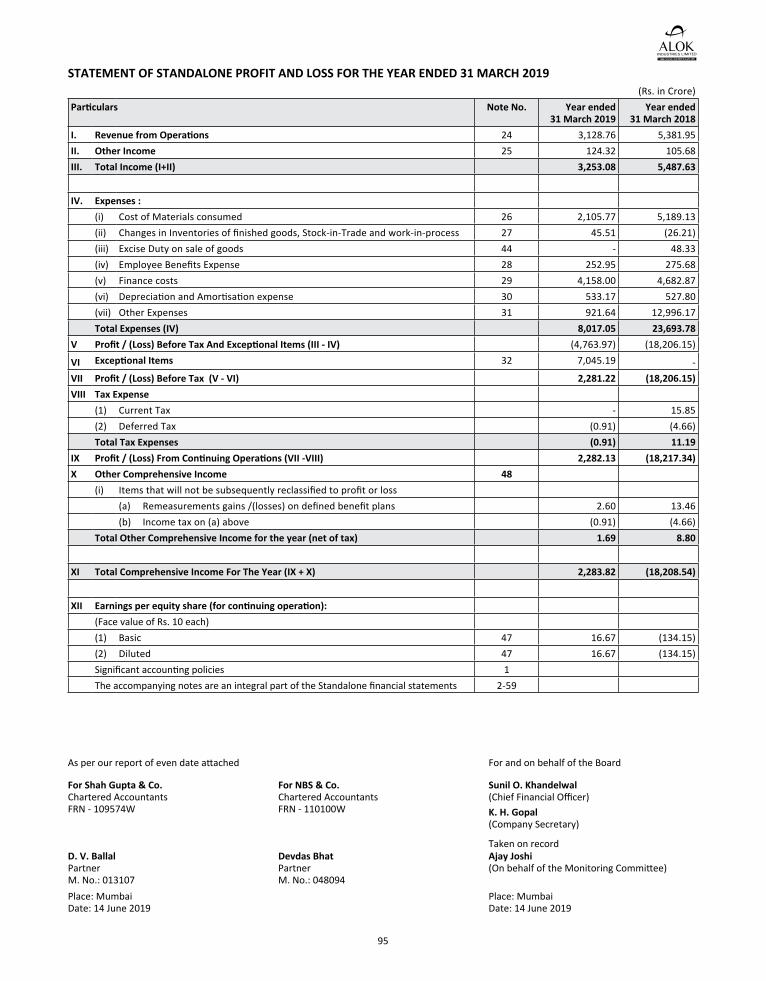

Table 4.5 Table showing Revenue from Operations to Total Asset

Financial Year

Revenue from

Operations

Total Asset

X5

2015-2016

11,752.39

27,660.92

0.4248

2016-2017 8,326.06

32,708.99

0.2545

2017-2018 5,381.95

18,700.37

0.2877

2018-2019 3,128.76

18,016.35

0.1736

2019-2020 3,166.34

17,908.24

0.1768

(Source:- Compiled from Financial Statements)

From the above table it is clear that the ratio has been declining from the FY

2016-17 although there was a slight increase in the FY 2017-18, which shows

that the company is inefficient in using its assets to generate revenue.

Figure 4.5 Figure showing Revenue from operations to Total Asset Ratio

(Source:- Compiled from Financial Statements)

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

2015-16 2016-2017 2017-2018 2018-2019 2019-2020

Rat

io

Year

Revenue from operation to Total Asset Ratio

41

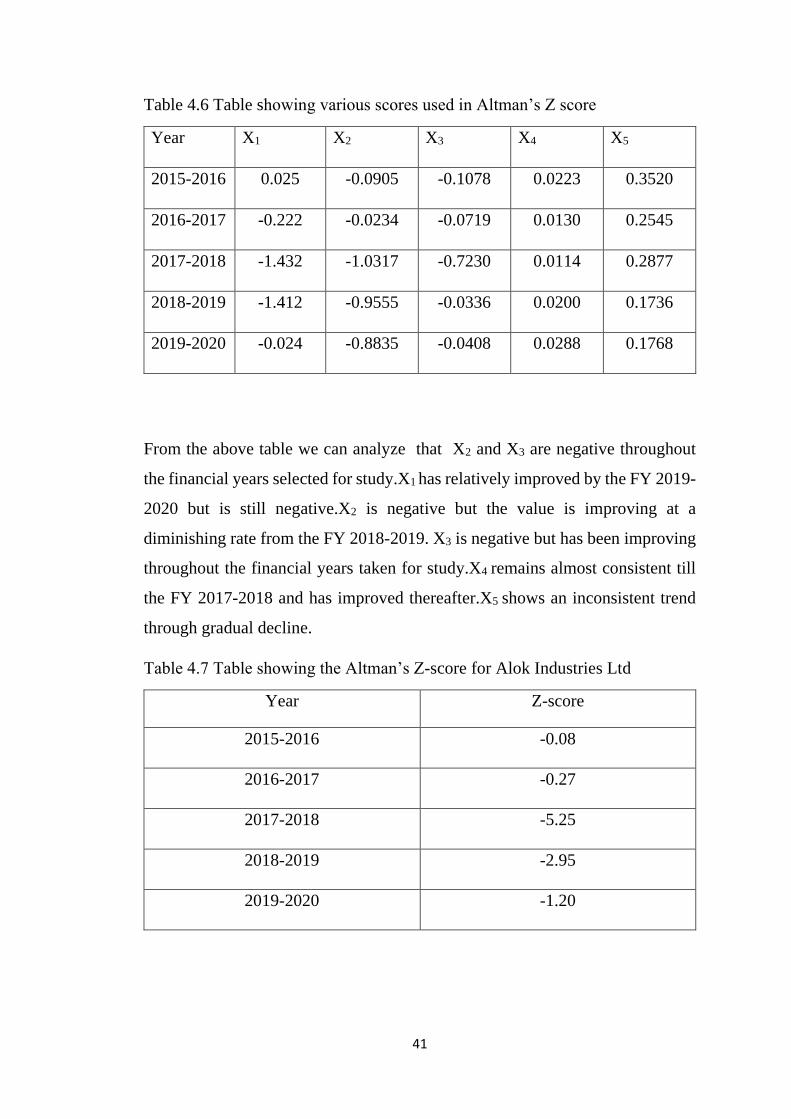

Table 4.6 Table showing various scores used in Altman’s Z score

Year X1 X2 X3 X4 X5

2015-2016 0.025

-0.0905

-0.1078

0.0223

0.3520

2016-2017 -0.222

-0.0234

-0.0719

0.0130

0.2545

2017-2018 -1.432

-1.0317

-0.7230

0.0114

0.2877

2018-2019 -1.412

-0.9555

-0.0336

0.0200

0.1736

2019-2020 -0.024

-0.8835

-0.0408

0.0288

0.1768

From the above table we can analyze that X2 and X3 are negative throughout

the financial years selected for study.X1 has relatively improved by the FY 2019-

2020 but is still negative.X2 is negative but the value is improving at a

diminishing rate from the FY 2018-2019. X3 is negative but has been improving

throughout the financial years taken for study.X4 remains almost consistent till

the FY 2017-2018 and has improved thereafter.X5 shows an inconsistent trend

through gradual decline.

Table 4.7 Table showing the Altman’s Z-score for Alok Industries Ltd

Year Z-score

2015-2016 -0.08

2016-2017 -0.27

2017-2018 -5.25

2018-2019 -2.95

2019-2020 -1.20

42

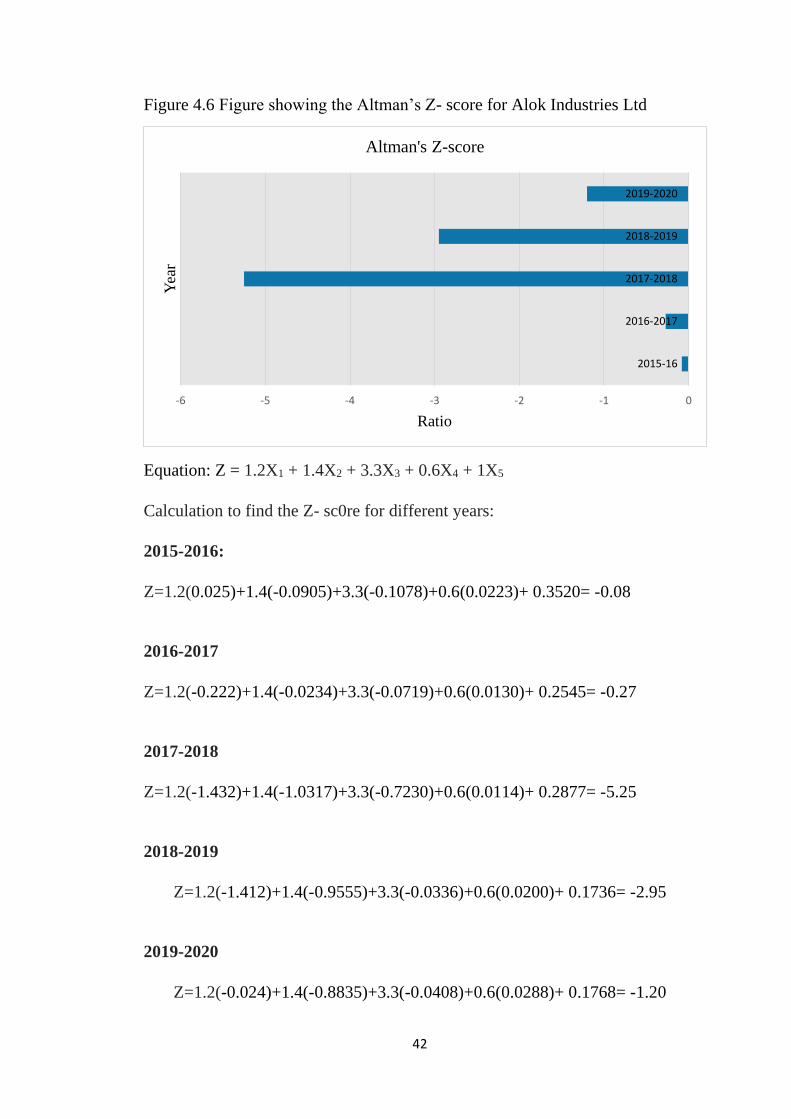

Figure 4.6 Figure showing the Altman’s Z- score for Alok Industries Ltd

Equation: Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + 1X5

Calculation to find the Z- sc0re for different years:

2015-2016:

Z=1.2(0.025)+1.4(-0.0905)+3.3(-0.1078)+0.6(0.0223)+ 0.3520= -0.08

2016-2017

Z=1.2(-0.222)+1.4(-0.0234)+3.3(-0.0719)+0.6(0.0130)+ 0.2545= -0.27

2017-2018

Z=1.2(-1.432)+1.4(-1.0317)+3.3(-0.7230)+0.6(0.0114)+ 0.2877= -5.25

2018-2019

Z=1.2(-1.412)+1.4(-0.9555)+3.3(-0.0336)+0.6(0.0200)+ 0.1736= -2.95

2019-2020

Z=1.2(-0.024)+1.4(-0.8835)+3.3(-0.0408)+0.6(0.0288)+ 0.1768= -1.20

-6 -5 -4 -3 -2 -1 0

2015-16

2016-2017

2017-2018

2018-2019

2019-2020

Ratio

Yea

r

Altman's Z-score

43

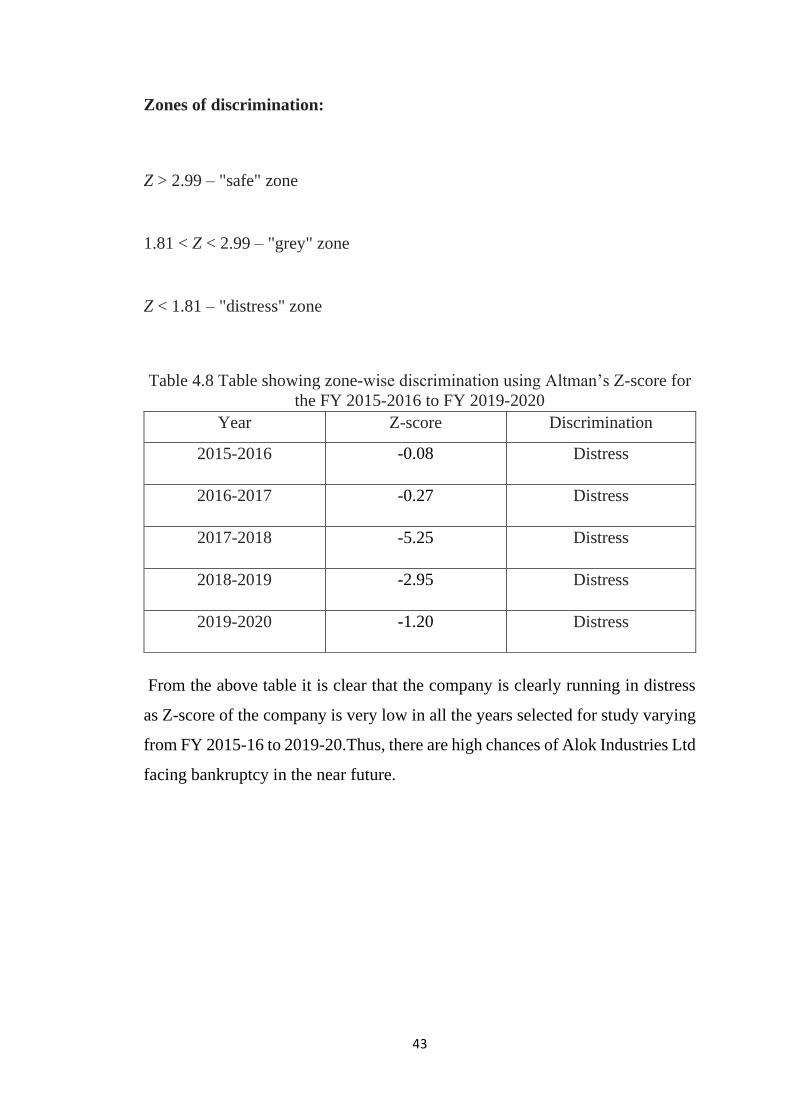

Zones of discrimination:

Z > 2.99 – "safe" zone

1.81 < Z < 2.99 – "grey" zone

Z < 1.81 – "distress" zone

Table 4.8 Table showing zone-wise discrimination using Altman’s Z-score for

the FY 2015-2016 to FY 2019-2020

Year Z-score Discrimination

2015-2016 -0.08

Distress

2016-2017 -0.27

Distress

2017-2018 -5.25

Distress

2018-2019 -2.95

Distress

2019-2020 -1.20

Distress

From the above table it is clear that the company is clearly running in distress

as Z-score of the company is very low in all the years selected for study varying

from FY 2015-16 to 2019-20.Thus, there are high chances of Alok Industries Ltd

facing bankruptcy in the near future.

CHAPTER Ⅴ

FINDINGS, SUGGESTIONS AND

CONCLUSION

44

5.1 Introduction

This chapter includes major findings of the study, conclusions and

suggestions to avoid a bankruptcy situation for Alok Industries Ltd.

5.2 Findings

• The first ratio, which shows the relation between working capital to

total asset is negative (figure 4.1).From further analysis, it is clear that

there is a gradual decrease in the working capital to total asset ratio

from Financial Year 2015-16 to 2018-2019, however by the end of the

FY 2019-2020 the ratio has relatively improved but it is still negative

indicating that the business is in financial distress and does not have

the necessary liquid assets to pay its current liabilities. So there are

problems with liquidity and hence a possibility to go bankrupt.

• The second ratio depicts the relation between the retained earnings of

the company and its total assets (figure 4.2). Retained Earnings to

Total Asset ratio showed a drastic decline from the FY 2017-2018, but

the ratios of all the Financial Years are negative indicating

accumulated deficit, which means the company has more debt than

earned profits. Thus, the company is facing difficulty in accumulating

earnings due to losses indicating the possibility of bankruptcy.

• The third ratio shows the relation between EBIT to total asset(figure

4.3). From analysis it was clear that the EBIT to Total Asset ratio is a

negative ratio and this suggests that the company can't use its assets

effectively to generate income. This also indicates poor operating

efficiency and financial leverage. Thus this ratio also supports the

notion of bankruptcy.

45

• The fourth ratio shows the relationship between market value of equity

to total liabilities(figure 4.4). From analysis we can infer that there

was a drastic fall in the market capitalization of the company during

the FY 2016-2017 but the ratio is increasing constantly from the FY

2018-2019 indicating that the market value of shares are increasing

therefrom. This ratio does not support bankruptcy as it is increasing

every year.

• The fifth ratio shows the relationship between revenue from

operations to total assets(figure 4.5). From analysis it is clear that the

ratio has been declining from the FY 2016-17 although there was a

slight increase in the FY 2017-18. This shows that the company is

inefficient in using its assets to generate revenue and thus, this ratio

supports the possibility of bankruptcy.

• The only ratio which gives positive sign to the company is the market

value of equity to total liabilities ratio, but this ratio alone cannot be

taken as an indicator of better position of the company.

• To accurately inspect the bankruptcy position of any company,

Altman’s Z-score must be calculated. From calculating and checking

the Z-score it is clear that the company is clearly running in distress

in all the years selected for study varying from FY 2015-16 to 2019-

20.As per the discriminations of Altman if the Z-score is less than 1.8,

the company is running in distress. It is difficult to overcome this

distress thus, we can presume that the company will face bankruotcy

in the upcoming years.

46

5.2 Suggestions

• It is advisable to attract the customers by giving offers, to attain more

profit in the upcoming years.

• Liquidity position of the company should be improved. It can be increased

by increasing the working capital of the company.

• It is recommended to improve the revenue from operation because it is

the backbone of the company.

• Market value of equity leads to increased credibility. Thus, it is advisable

to increase the market value of shares.

• Prioritize Debt Repayments.

47

5.3 Conclusion

The purpose of this study was to apply Altman’s Z-score model on Alok

Industries Ltd. Preliminary results show that the model correctly identified Alok

Industries Ltd. as a financially unstable company with Z-score below 1.81 in all

years of observation. After observing the discriminations we can conclude that

the company is clearly running in distress as Z-score of the company is very low

in all the years selected for study varying from FY 2015-16 to 2019-20. Thus,

there are high chances of Alok Industries Ltd facing bankruptcy in the near

future.

BIBLIOGRAPHY

Books

❖ Dr. K venugopalan, “Business Research Methods”, Calicut university Central co-

operative stories ltd. No.4347 Calicut University, 2016.

❖ A Vinod, “ Accounting for Management”, Calicut university Central co-operative

stories ltd. No.4347 Calicut University, 2017.

Journals

❖ John Stephen Grice, R. W. (2001). Tests of the generalizability of Altman's

bankruptcy prediction model. Journal of Business Research, 54(1), pp.53-61.

❖ Hayes, S., Hodge, K., & Hughes, L. (2010). Efficacy of Altman's Z to predict

Bankruptcy. Economic and Business Journal:Inquiries and Perspectives, 3(1),

pp.122-134.

❖ Gnyana Ranjan Bal. (2015). Prediction of financial distress using Altman Z-score:

a study of select FMCG companies. Indian Journal of Applied Research, 5(9),

pp.129-131.

❖ Lubawa, Galinoma & Louangrath, Paul. (2016). Using Altman Z-Score to Assess

the Financial Effects of Multiple Loans on SMEs. International Journal of Research

& Methodology in Social Science,2(1), pp.63-86.

❖ Senapati, M., & Ghosal, S. (2016). Modelling Corporate Sector Distress in India.

RBI Working Paper Series, (10), pp.1-22.

❖ Agarwal, S., & Singh, G. (2018). Altman Z score with reference to Public Sector

Banks in India. International Journal of Research and Analytical Reviews, 5(4),

pp.955-963.