1 ( ) , , . . . 102410028 . & ( , ) 20102012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 181

1

991260983105 983123983124983125983108983129 983119983118 983110983113983118983105983118983107983113983105983116 983120983109983122983110983119983122983117983105983118983107983109 983105983118983105983118983116983129983123983113983123991261

(983127983113983124983112 983122983109983110983109983122983109983118983107983109 983124983119 983115983109983123983119983122983105983117 983107983109983117983109983118983124)

983105 983120983154983151983146983141983139983156 983154983141983152983151983154983156 983155983157983138983149983145983156983156983141983140 983156983151 983114983137983159983137983144983137983154983148983137983148 983118983141983144983154983157 983124983141983139983144983150983151983148983151983143983145983139983137983148 983125983150983145983158983141983154983155983145983156983161 983112983161983140983141983154983137983138983137983140 983142983151983154 983156983144983141

983137983159983137983154983140 983151983142 983140983141983143983154983141983141

983117983105983123983124983109983122 983119983110 983106983125983123983113983118983109983123983123 983105983108983117983113983118983113983123983124983122983105983124983113983119983118

983106983161

983117983126983113983115983122983105983117 983123983113983118983111983112

983122983141983143 983118983151 102419831090028

983125983150983140983141983154 983156983144983141 983111983157983145983140983137983150983139983141 983151983142

983120983154983151983142 983115983126983123 983122983105983114983125

983108983141983152983137983154983156983149983141983150983156 983151983142 983117983137983150983137983143983141983149983141983150983156 983123983156983157983140983145983141983155

983111983151983147983137983154983137983146983157 983122983137983150983143983137983154983137983146983157 983113983150983155983156983145983156983157983156983141 983151983142 983109983150983143983145983150983141983141983154983145983150983143 amp 983124983141983139983144983150983151983148983151983143983161

(983105983142983142983145983148983145983137983156983141983140 983156983151 983114983137983159983137983144983137983154983148983137983148 983124983141983139983144983150983151983148983151983143983145983139983137983148 983125983150983145983158983141983154983155983145983156983161 983112983161983140983141983154983137983138983137983140)

983112983161983140983141983154983137983138983137983140

20109830852012

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 281

2

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 381

3

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 481

4

DECLARATION

I hereby declare that the project entitled ldquoA study on financial performance

analysis aatt KKeessoorraamm CCeemmeennttrdquo submitted in partial fulfillment of the requirements for

award of the degree of MBA at Gokaraju Rangaraju Institute of Engineering and

Technology affiliated to Jawaharlal Nehru Technological University Hyderabad is

an authentic work and has not been submitted to any other UniversityInstitute for

award of any degreediploma

MVIKRAM SINGH

(10241e0028)

MBA GRIET

HYDERABAD

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 581

5

ACKNOWLEDGEMENT

Firstly I would like to express our immense gratitude towards our institution

Gokaraju Rangaraju Institute of Engineering amp Technology which created a great

platform to attain profound technical skills in the field of MBA thereby fulfilling our most

cherished goal

I would thank all the finance department of Kesoram specially Mr MURTHY ASST

Manager Finance for guiding me and helping me in successful completion of the project

I am very much thankful to our Prof KVS RAJU (Internal Guide) sir for extending

his cooperation in doing this project

I am also thankful to our project coordinator Prof S RAVINDRA CHARY for

extending his cooperation in completion of Project

I convey my thanks to my beloved parents and my faculty who helped me directly or

indirectly in bringing this project successfully

M VIKRAM SINGH

(102419831090028)

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 681

6

INDEX

SNo Contents Page No

Chapter-1 1-8

Introduction

Need of the Study

Objectives of the Study

Methodology of the Study

Limitations of the Study

Chapter-2 9-28

Industry Profile

Company Profile

Chapter-3 29-38

Review of Literature

Chapter-4 39-68

Data Analysis And Interpretation

Chapter-5 69-71

Findings

Suggestions

Chapter-6 72-75

Annexure

Bibliography

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 781

7

CHAPTER-I

INTRODUCTION

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 881

8

Introduction-

The term lsquofinancial performance analysis also known as analysis and interpretation

of financial statementsrsquo refers to the process of determining financial strength and

weaknesses of the firm by establishing strategic relationship between the items of the

balance sheet profit and loss account and other operative data

ldquoFinancial performance analysis is a process of evaluating the relationship between

component parts of a financial statement to obtain a better understanding of a firmrsquos

position and performance

The purpose of financial analysis is to diagnose the information contained in

financial statements so as to judge the profitability and financial soundness of the firm Just

like a doctor examines his patient by recording his body temperature blood pressure etc

Before making his conclusion regarding the illness and before giving his treatment A

financial analyst analyses the financial statements with various tools of analysis before

commenting upon the financial health or weaknesses of an enterprise

The analysis and interpretation of financial statements is essential to bring out the

mystery behind the figures in financial statements Financial statements analysis is an

attempt to determine the significance and meaning of the financial statement data so that

forecast may be made of the future earnings ability to pay interest and debt maturities (both

current and long term) and profitability of a sound divided policy

Financial performance refers to the act of performing financial activity In broader sense

financial performance refers to the degree to which financial objectives being or has been

accomplished It is the process of measuring the results of a firms policies and operations in

monetary terms It is used to measure firms overall financial health over a given period oftime and can also be used to compare similar firms across the same industry or to compare

industries or sectors in aggregation

In short the firm itself as well as various interested groups such as managers

shareholders creditors tax authorities and others seeks answers to the

Following important questions

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 981

9

1 What is the financial position of the firm at a given point of time

2 How is the financial performance of the firm over a given period

Of time

These questions can be answered with the help of financial analysis of a firm Financial

analysis involves the use of financial statements A financial statement is an organized

collection of data according to logical and conceptual framework 50 consistent accounting

procedures Its purpose is to convey an understanding of some financial aspects of a

business firm It may show a position at a moment of time as in the case of a balance sheet

or may reveal a series of activities over a given period of time as in the case of an income

statement

Thus the term lsquofinancial statementsrsquo generally refers to two basic statements

The balance sheet and the income statement

The balance sheet shows the financial position (condition) of the firm at a given point of

time It provides a snapshot and may be regarded as a static picture

ldquoBalance sheet is a summary of a firmrsquos financial position on a given date that

Shows total assets = total liabilities + ownerrsquos equityrdquo

The income statement (referred to in India as the profit and loss statement) reflects the

performance of the firm over a period of time

ldquoIncome statement is a summary of a firmrsquos revenues and expenses over a specified period

ending with net income or loss for the periodrdquo

However financial statements do not reveal all the information related to the financial

operations of a firm but they furnish some extremely useful information which highlights

two important factors profitability and financial soundness Thus analysis of financial

statements is an important aid to financial performance analysis Financial performance

analysis includes analysis and interpretation of financial statements in such a way that it

Undertakes full diagnosis of the profitability and financial soundness of the business

ldquoThe analysis of financial statements is a process of evaluating the relationship between

component parts of financial statements to obtain a better understanding of the firmrsquos

position and performancerdquo

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1081

10

Need for Study

Need Of Financial Management Study To Diagnose The Information Contain In

Financial Statement So as To Judge the Profitability and Financial Position of the

Firm

Financial Analyst Analyses The Financial Statements With Various Tools Of

Analysis Before Commanding Upon The Financial Health Of The Firm

Essential to Bring Out the History

Significance and Meaning of the Financial Statements

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1181

11

Objectives

1 To understand the financial statements of Kesoram cement

2 To study the change in assets and liabilities of the company

3 To study the liquidity position of the firm

4 To study the financial health of the company using ratio analysis

5 To study the profitability of the company

6 To offer suggestions to the company

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1281

12

Significance of Financial Performance Analysis

Interest of various related groups is affected by the financial performance of a firm

Therefore these groups analyze the financial performance of the firm The type of analysis

varies according to the specific interest of the party involved

Trade creditors interested in the liquidity of the firm (appraisal of firmrsquos liquidity)

Bond holders interested in the cash-flow ability of the firm (appraisal of firmrsquos capital

structure the major sources and uses of funds profitability over time and projection of

future profitability)

Investors interested in present and expected future earnings as well as stability of these

earnings (appraisal of firmrsquos profitability and financial condition)

Management interested in internal control better financial condition and betterperformance (appraisal of firmrsquos present financial condition evaluation of opportunities in

relation to this current position return on investment provided by various assets of the

company etc)

Research Methodology

Research Design

This is a systematic way to solve the research problem and it is important

component for the study without which researches may not be able to obtain the format A

research design is the arrangement of conditions for collection and analysis of data in a

manager that aims to combine for collection and analysis of data relevance to the research

purpose with economy in procedure

Meaning of Research Design

The formidable problem that follows the task of defining the research problem is the

preparation of design of the research project popularly known as the research design

decision regarding what where when how much by what means concerning an inquiry of

a research study constitute a research design A research design is the arrangement of

conditions for collection and analysis of data in a manager that aims to combine for

collection and analysis of data relevance to the research purpose with economy in

procedure

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1381

13

Sources of Data

Data we collected based on two sources

Primary Data

Secondary Data

Primary Data

The Primary Data Are Those Informationrsquos which are Collected afresh and for the

First Time And Thus Happen to Be Original in Character

Secondary Data

The secondary data are those which have already been collected by some other agency and

which have already been processed The sources of secondary data are annual reports

browsing internet through magazines

1 It includes data gathered from the annual reports of Kesoram

2 Articles are collected from official website of Kesoram

Methodology Used

Types Of Financial Statements Adopted

Following Two Types of Financial Statements Are Commonly Used in

Analyzing the Firmrsquos Financial Position

a Balance Sheet

b Income Statements

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1481

14

Limitations of Financial Statement

Each Project Gives Rise to Its Own Unique Risks And Hence Possess Its Own Unique

Challenges

1 Only Interim Reports

Only interim statements donrsquot give a final picture of the concern The data given in

these statements is only approximate The actual position can only be determined when the

business is sold or liquidated

2 Donrsquot Give Extra Position

The Financial Statements Are Expressed In Monetary Values So They Appear To

Give Final And Accurate Position The Values Of Fixed Assets In The Balance Sheet

Neither Represent The Value For Which Fixed Assets Can Be Sold Nor The Amount Which

Will Be Required To Replace These Assets

3 Historical Costs

The Financial Statements Are Prepared On The Basis Of Historical Costs Or

Original Costs The Value of Assets Decreases with the Passage of Time Current Price

Changes Are Not Taken Into Account The Statements Are Not Prepared Keeping In View

The Present Economic Conditions The Balance Sheet Loses The Significance Of Being An

Index Of Current Economic Realities

4 Act of non monitory factors Ignored

There are certain factors which have a bearing on the financial position and

operating results of the business but they donrsquot become a part of these statements because

they canrsquot be measured in monetary terms Such factors may include in the reputation of the

management

No Precision

The precision of financial statement data is not possible because the statements deal with

matters which canrsquot be precisely stated The data are recorded by conventional procedures

followed over the years Various conventions postulates personal judgments etc

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1581

15

CHAPTER-II

INDUSTRY PROFILE

amp

COMPANY PROFILE

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1681

16

Industry Profile

In the most general sense of the word cement is a binder a substance which

sets and hardens independently and can bind other materials together The word cement

traces to the Romans who used the term opus caementicium to describe masonry whichresembled concrete and was made from crushed rock with burnt lime as binder The

volcanic ash and pulverized brick additives which were added to the burnt lime to obtain a

hydraulic binder were later referred to as cementum and cement Cements used in

construction are characterized as hydraulic or non-hydraulic

The most important use of cement is the production of mortar and concretemdashthe bonding of

natural or artificial aggregates to form a strong building material which is durable in the

face of normal environmental effects

Concrete should not be confused with cement because the term cement refers only to the dry

powder substance used to bind the aggregate materials of concrete Upon the addition of

water andor additives the cement mixture is referred to as concrete especially if aggregates

have been added

It is uncertain where it was first discovered that a combination of hydrated non-hydraulic

lime and a pozzolan produces a hydraulic mixture (see also Pozzolanic reaction) but

concrete made from such mixtures was first used on a large scale by engineers They used

both natural pozzolans (trass or pumice) and artificial pozzolans (ground brick or pottery) in

these concretes Many excellent examples of structures made from these concretes are still

standing notably the huge monolithic dome of the Pantheon in Rome and the massive Baths

of Caracalla The vast system of Roman aqueducts also made extensive use of hydraulic

cement The use of structural concrete disappeared in medieval Europe although weak

pozzolanic concretes continued to be used as a core fill in stone walls and columns

Modern cement

Modern hydraulic cements began to be developed from the start of the Industrial Revolution

(around 1800) driven by three main needs

Hydraulic renders for finishing brick buildings in wet climates

Hydraulic mortars for masonry construction of harbor works etc in contact with sea water

Development of strong concretes

In Britain particularly good quality building stone became ever more expensive during a

period of rapid growth and it became a common practice to construct prestige buildings

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1781

17

from the new industrial bricks and to finish them with a stucco to imitate stone Hydraulic

limes were favored for this but the need for a fast set time encouraged the development of

new cements Most famous was Parkers Roman cement This was developed by James

Parker in the 1780s and finally patented in 1796 It was in fact nothing like any material

used by the Romans but was ldquoNatural cement made by burning septaria - nodules that are

found in certain clay deposits and that contain both clay minerals and calcium carbonate

The burnt nodules were ground to a fine powder This product made into a mortar with

sand set in 5ndash15 minutes The success of Roman Cement led other manufacturers to

develop rival products by burning artificial mixtures of clay and chalk

John Smeaton made an important contribution to the development of cements when he was

planning the construction of the third Eddystone Lighthouse (1755-9) in the English

Channel He needed a hydraulic mortar that would set and develop some strength in the

twelve hour period between successive high tides He performed an exhaustive market

research on the available hydraulic limes visiting their production sites and noted that the

hydraulicity of the lime was directly related to the clay content of the limestone from

which it was made Smeaton was a civil engineer by profession and took the idea no

further Apparently unaware of Smeatons work the same principle was identified by Louis

Vicat in the first decade of the nineteenth century Vicat went on to devise a method of

combining chalk and clay into an intimate mixture and burning this produced an artificial

cement in 1817 James Frost working in Britain produced what he called British cement

in a similar manner around the same time but did not obtain a patent until 1822 In 1824

Joseph Aspdin patented a similar material which he called Portland cement because the

render made from it was in color similar to the prestigious Portland stone

All the above products could not compete with limepozzolan concretes because of fast-

setting (giving insufficient time for placement) and low early strengths (requiring a delay of

many weeks before formwork could be removed) Hydraulic limes natural cements and

artificial cements all rely upon their belite content for strength development Belite

develops strength slowly Because they were burned at temperatures below 1250 degC they

contained no alite which is responsible for early strength in modern cements The first

cement to consistently contain alite was made by Joseph Aspdins son William in the early

1840s This was what we call today modern Portland cement Because of the air of

mystery with which William Aspdin surrounded his product others (eg Vicat and I C

Johnson) have claimed precedence in this invention but recent analysis of both his concrete

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1881

18

and raw cement have shown that William Aspdins product made at North fleet Kent was a

true alite-based cement However Aspdins methods were rule-of-thumb Vicat is

responsible for establishing the chemical basis of these cements and Johnson established

the importance of sintering the mix in the kiln

William Aspdins innovation was counter-intuitive for manufacturers of artificial cements

because they required more lime in the mix (a problem for his father) because they required

a much higher kiln temperature (and therefore more fuel) and because the resulting clinker

was very hard and rapidly wore down the millstones which were the only available grinding

technology of the time Manufacturing costs were therefore considerably higher but the

product set reasonably slowly and developed strength quickly thus opening up a market for

use in concrete The use of concrete in construction grew rapidly from 1850 onwards and

was soon the dominant use for cements Thus Portland cement began its predominant role

It is made from water and sand

Types of modern cement

Portland cement

Cement is made by heating limestone (calcium carbonate) with small quantities of other

materials (such as clay) to 1450degC in a kiln in a process known as calcination whereby a

molecule of carbon dioxide is liberated from the calcium carbonate to form calcium oxide

or lime which is then blended with the other materials that have been included in the mix

The resulting hard substance called clinker is then ground with a small amount of gypsum

into a powder to make Ordinary Portland Cement the most commonly used type of cement

(often referred to as OPC)

Portland cement is a basic ingredient of concrete mortar and most non-speciality grout The

most common use for Portland cement is in the production of concrete Concrete is a

composite material consisting of aggregate (gravel and sand) cement and water As a

construction material concrete can be cast in almost any shape desired and once hardened

can become a structural (load bearing) element Portland cement may be gray or whitePortland cement blends

These are often available as inter-ground mixtures from cement manufacturers but similar

formulations are often also mixed from the ground components at the concrete mixing plant

Portland blast furnace cement contains up to 70 ground granulated blast furnace slag

with the rest Portland clinker and a little gypsum All compositions produce high ultimate

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 1981

19

strength but as slag content is increased early strength is reduced while sulfate resistance

increases and heat evolution diminishes Used as an economic alternative to Portland

sulfate-resisting and low-heat cements

Portland fly ash cement contains up to 30 fly ash The fly ash is pozzolanic so that

ultimate strength is maintained Because fly ash addition allows lower concrete water

content early strength can also be maintained Where good quality cheap fly ash is

available this can be an economic alternative to ordinary Portland cement

Portland pozzolan cement includes fly ash cement since fly ash is a pozzolan but also

includes cements made from other natural or artificial pozzolans In countries where

volcanic ashes are available (eg Italy Chile Mexico and the Philippines) these cements

are often the most common form in use

Portland silica fume cement Addition of silica fume can yield exceptionally high

strengths and cements containing 5-20 silica fume are occasionally produced However

silica fume is more usually added to Portland cement at the concrete mixer

Masonry cements are used for preparing bricklaying mortars and stuccos and must not be

used in concrete They are usually complex proprietary formulations containing Portland

clinker and a number of other ingredients that may include limestone hydrated lime air

entrainers retarders water proofers and coloring agents They are formulated to yield

workable mortars that allow rapid and consistent masonry work Subtle variations of

Masonry cement in the US are Plastic Cements and Stucco Cements These are designed to

produce controlled bond with masonry blocks

Expansive cements contain in addition to Portland clinker expansive clinkers (usually

sulfoaluminate clinkers) and are designed to offset the effects of drying shrinkage that is

normally encountered with hydraulic cements This allows large floor slabs (up to 60 m

square) to be prepared without contraction joints

White blended cements may be made using white clinker and white supplementary

materials such as high-purity metakaolin

Colored cements are used for decorative purposes In some standards the addition of

pigments to produce colored Portland cement is allowed In other standards (eg ASTM)

pigments are not allowed constituents of Portland cement and colored cements are sold as

blended hydraulic cements

Very finely ground cements are made from mixtures of cement with sand or with slag or

other pozzolan type minerals which are extremely finely ground together Such cements can

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2081

have the same physical characteristics as normal cement but with 50 less cement

particularly due to their increased surface area for the chemical reaction Even with

intensive grinding they can use up to 50 less energy to fabricate than ordinary Portland

cements

Non-Portland hydraulic cements

Pozzolan-lime cements Mixtures of ground Pozzolan and lime are the cements used by the

Romans and are to be found in Roman structures still standing (eg the Pantheon in Rome)

They develop strength slowly but their ultimate strength can be very high The hydration

products that produce strength are essentially the same as those produced by Portland

cement

Slag-lime cements Ground granulated blast furnace slag is not hydraulic on its own but is

activated by addition of alkalis most economically using lime They are similar to

pozzolan lime cements in their properties Only granulated slag (ie water-quenched glassy

slag) is effective as a cement component

Super sulfated cements These contain about 80 ground granulated blast furnace slag

15 gypsum or anhydrite and a little Portland clinker or lime as an activator They produce

strength by formation of ettringite with strength growth similar to a slow Portland cement

They exhibit good resistance to aggressive agents including sulfate

Calcium aluminate cements are hydraulic cements made primarily from limestone and

bauxite The active ingredients are monocalcium aluminate CaAl2O4 (CaO middot Al2O3 or CA in

Cement chemist notation CCN) and mayenite Ca12Al14O33 (12 CaO middot 7 Al2O3 or C12A7 in

CCN) Strength forms by hydration to calcium aluminate hydrates They are well-adapted

for use in refractory (high-temperature resistant) concretes eg for furnace linings

Calcium sulfoaluminate cements are made from clinkers that include yeelimite (Ca4

(AlO2)6SO4 or C4A3 in Cement chemists notation) as a primary phase They are used in

expansive cements in ultra-high early strength cements and in low-energy cements

Hydration produces ettringite and specialized physical properties (such as expansion or

rapid reaction) are obtained by adjustment of the availability of calcium and sulfate ionsTheir use as a low-energy alternative to Portland cement has been pioneered in China

where several million tonnes per year are produced Energy requirements are lower because

of the lower kiln temperatures required for reaction and the lower amount of limestone

(which must be endothermically decarbonated) in the mix In addition the lower limestone

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2181

21

content and lower fuel consumption leads to a CO2 emission around half that associated

with Portland clinker However SO2 emissions are usually significantly higher

Natural Cements correspond to certain cements of the pre-Portland era produced by

burning argillaceous limestones at moderate temperatures The level of clay components in

the limestone (around 30-35) is such that large amounts of belite (the low-early strength

high-late strength mineral in Portland cement) are formed without the formation of

excessive amounts of free lime As with any natural material such cements have highly

variable properties

Geopolymer cements are made from mixtures of water-soluble alkali metal silicates and

aluminosilicate mineral powders such as fly ash and metakaolin

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2281

22

COMPANY PROFILE

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2381

23

Kesoram Cement Industry is one of the leading manufacturers of cement in India It is a day

process cement Plant The plant capacity is 826 lakh tones per annum It is located at

Basanthnagar in Karimnagar district of Andhra Pradesh Basanthnagar is 8 km away from

the Ramagundam Railway station linking Madras to New Delhi The Chairman of the

Company is BKBirla

History

The first unit at Basanthnagar with a capacity of 21 lakh tones per annum

incorporating humble suspension preheated system was commissioner during the year 1969

The second unit was setup in year 1971 with a capacity of 21 lakh tones per annum went on

stream in the year 1978 The coal for this company is being supplied from Singgareni

Collieries and the power is obtained from APSEB The power demand for the factory is

about 21 MW Kesoram has got 2 DG sets of 4 MW each installed in the year 1987

Kesoram Cement has setup a 15 KW captor power plant to facilitate for

uninterrupted power supply for manufacturing of cement at 24th

august 1997 per hour 12

mw actual power is 15 mw

The Company was incorporated on 18th October 1919 under the Indian Companies Act

1913 in the name and style of Kesoram Cotton Mills Ltd It had a Textile Mill at 42

Garden Reach Road Calcutta 700 024 The name of the Company was changed to Kesoram

Industries amp Cotton Mills Ltd on 30th

August 1961 and the same was further changed to Kesoram Industries Limited on 9th July

1986 The said Textile Mill at Garden Reach Road was eventually demerged into a separate

company

The First Plant for manufacturing of rayon yarn was established at Tribeni District

Hooghly West Bengal and the same was commissioned in December 1959 and the second

plant was commissioned in the year 1962 enabling it to manufacture 4635 metric tons perannum (mtpa) of rayon yarn This Unit has 6500 metric tons per annum (mtpa) capacity as

on 3132009

The plant for manufacturing of transparent paper was also set up at the same location at

Tribeni District Hooghly West Bengal in June 1961 It has the annual capacity to

manufacture 3600 metric tons per annum (mtpa) of transparent Paper

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2481

24

The Company diversified into manufacturing of cast iron spun pipes and pipe fittings at

Bansberia District Hooghly West Bengal with a production capacity of 45000 metric tons

per annum (mtpa) of cast iron spun pipes and pipe fittings in December 1964

The Company subsequently diversified into the manufacturing of Cement and in 1969

established its first cement plant under the name Kesoram Cement at Basantnagar Dist

Karimnagar (Andhra Pradesh) and to take advantage of favorable market conditions in

1986 another cement plant known as Vasavadatta Cement was commissioned by it at

Sedam Dist

Gulbarga (Karnataka) The cement manufacturing capacities at both the plants were

augmented from time to time according to the market conditions and as on 3132009

Kesoram Cement and Vasavadatta Cement have annual cement manufacturing capacities of

15 million metric tons and 41 million metric tons respectively

The Company in March 1992 commissioned a plant at Balasore known as Birla Tyres in

Orissa for manufacturing of 10 lakh mtpa automotive tyres and tubes in the first phase in

collaboration with Pirelli Ltd UK a subsidiary company of the world famous Pirelli

Group of Italy - a pioneer in production and development of automotive tyres in the world

The capacity at the said plant was further augmented during the year by 19 MT per day

aggregating to 271 MT per day production facility The Greenfield Project of 257 MT per

day capacity in the State of Uttarakhand with a capex of about Rs760 crores commenced

the commercial production in phases during the financial year 2008-09The Company as on

3132009 had the manufacturing capacities of 371 million tyres 295 million tubes and

153 million flaps per annum in the Plants including at Uttarakhand Plant It has small

manufacturing capacities of various Chemicals at Kharda in the State of West Bengal also

It has the annual manufacturing capacities of 12410 mtpa of Caustic Soda Lye 5045 mtpa

of Liquid Chlorine 6205 mtpa of Sodium Hypochlorite 8200 mtpa of Hydrochloric Acid

3200 mtpa of Ferric Alum 18700 mtpa of Sulphuric Acid and 1620000 m3pa of purified

Hydrogen Gas

The Company is a well-diversified entity in the fields of Cement Tyre Rayon Yarn

Transparent Paper Spun Pipes and Heavy Chemicals with two core business segments ie

Cement and Tyres

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2581

25

In Spun Pipes amp Foundries a unit of the Company work suspended from 2nd May 2008

still commences till further notice

The Company as of now is listed on three major Stock Exchanges in India ie Bombay

Stock Exchange Ltd Mumbai Calcutta Stock Exchange Association Ltd Kolkata and

National Stock Exchange of India Ltd Mumbai and at the Societe de la Bourse de

Luxembourg Luxembourg

A further expansion upto 165 million tons of cement per annum in Vasavadatta Cement at

Sedam in Karnataka as unit IV at the same site is in progress with a 175 MW Captive

Power Plant involving a capital expenditure of about Rs 78350 crores (including the cost

of Captive Power Plant)

The commercial production of cement in the aforesaid unit IV has commenced in June

2009 The work for the further expansion in the Tyres Section at Uttarakhand for radial

tyres with 100 MT per day capacity and bias tyres with 125 MT per day capacity involving

an estimated aggregate capital outlay of about Rs 840 crores is under progress The Board

has further approved a Motor Cycle Tyre Project of 70 MT per day capacity at the same site

involving a capital outlay of Rs190 crore The civil construction of both the Projects is in

full swing The commercial production in both the Projects is likely to start by December

2009 January 2010

Birla Supreme in popular brand of Kesoram cement from its prestigious plant of

Basantnagar in AP which has outstanding track record In performance and productivity

serving the nation for the last two and half decades It has proved its distinction by bagging

several national awards It also has the distinction of achieving optimum capacity

utilization

Kesoram offers a choice of top quality portioned cement for light heavy

constructions and allied applications Quality is built every fact of the operations

The plant lay out is rational to begin with The limestone is rich in calcium

carbonate a key factor that influences the quality of final product The day process

technology uses in the latest computerized monitoring overseas the manufacturing process

Samples are sent regularly to the bureau of Indian standards National council of

construction and building material for certification of derived quality norms

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2681

26

The company has vigorously undertaking different promotional measures for

promoting their product through different media which includes the use of news papers

magazine hoarding etc

Kesoram cement industry distinguished itself among all the cement factories in

Indian by bagging the National Productivity Award consecutively for two years ie for the

year 1985-1987 The federation of Andhra Pradesh Chamber amp Commerce and Industries

(FAPCCI) also conferred on Kesoram Cement An award for the best industrial promotion

expansion efforts in the state for the year 1984 Kesoram also bagged FAPCCI awarded for

ldquoBest Family Planning Effort in the staterdquo for the year 1987-1988

One among the industrial giants in the country today serving the nation on the

industrial front Kesoram industry ltd has a checked and eventful history dating back to the

twenties when the Industrial House of Birlarsquos acquired it With only a textile mill under its

banner 1924 it grew from strength to strength and spread its activities to newer fields like

Rayon Transparent paper pipes Refractors tyres and other products

Looking to the wide gap between the demand and supply of vital commodity

cement which play in important role in National building activity the Government of India

had de-licensed the cement industry in the year 1966 with a review to attract private

entrepreneur to augment the cement production Kesoram rose to the occasions and divided

to set up a few cement plants in the country

Kesoram cement undertaking marketing activities extensively in the state of Andhra

Pradesh Karnataka Tamilnadu Kerala Maharashtra and Gujarat In AP sales Depts are

located in different areas like Karimnagar Warangal Nizamabad Vijayawada and Nellore

In other states it has opened around 10 depots

The market share of Kesoram Cement in AP is 705 The market share of the

company in various states is shown as under

STATES MARKET SHARE

Karnataka 409

Tamilnadu 094

Kerala 029

Maharashtra 281

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2781

27

Process and Quality Control

It has been the endeavor of Kesoram to incorporate the Worldrsquos latest technology in

the plant and today the plant has the most sophisticated

X-ray analysis

Fully computerized XRF and XRD X-RAY Analyzers keep a constant round the

clock vigil on quality

Supreme performance

One of the largest Cement Plants in Andhra Pradesh the plant incorporate the latest

technology in Cement - making

It is professionally managed and well established Cement Manufacturing Company

enjoying the confidence of the consumers Kesoram has outstanding track record in

performance and productivity with quite a few national and state awards to its credit

BIRLA SUPREME the 43 Grade Cement is a widely accepted and popular brand

in the market commanding a premium

However to meet the specific demands of the consumer Kesoram bought out the 53

grade BIRLA SUPREME ndash GOLD which has special qualities like higher fineness quick-

setting high compressive strength and durability

Supreme Strength

Kesoram Cement has huge captive Limestone Deposits which make it possible tofeed high- grade limestone consistently its natural Grey colour is anion- born ingredient

and gives good shade

Both the products offered by Kesoram ie BIRLA SUPREME-43 Grade and

BIRLA SUPREME-GOLD-53 Grade cement are outstanding with much higher

compressive strength and durability

The following characteristics show their distinctive qualities

Comprehensive

Strength

Opc 43

grls 8112

1989

Birla

Supreme 43

grade

Opc 43 gr

Is 1226987

Birla

Supreme

Gold 53 gr

3 days mpa Min 23 31 + Min 27 38+

7 days mpa Min 23 42+ Min 37 48+

28 days mpa Min 43 50+ Min 53 60+

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2881

28

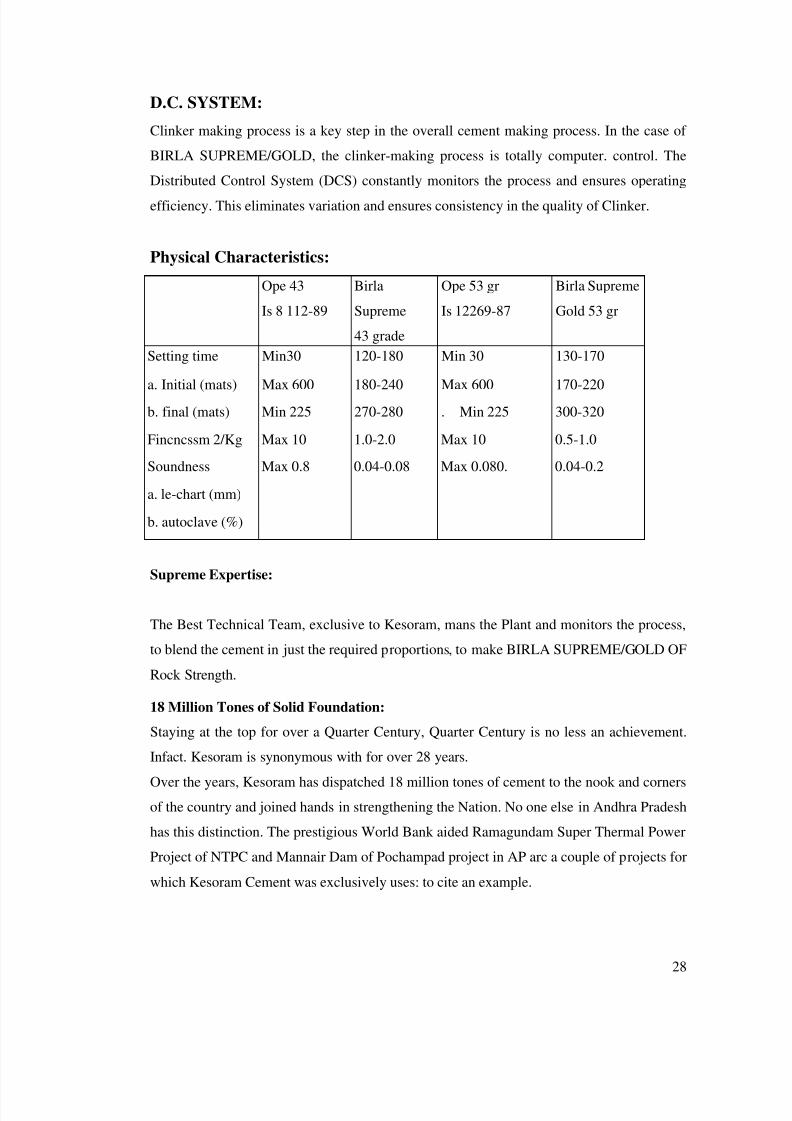

DC SYSTEM

Clinker making process is a key step in the overall cement making process In the case of

BIRLA SUPREMEGOLD the clinker-making process is totally computer control The

Distributed Control System (DCS) constantly monitors the process and ensures operating

efficiency This eliminates variation and ensures consistency in the quality of Clinker

Physical Characteristics

Ope 43

Is 8 112-89

Birla

Supreme

43 grade

Ope 53 gr

Is 12269-87

Birla Supreme

Gold 53 gr

Setting time Min30 120-180 Min 30 130-170

a Initial (mats) Max 600 180-240 Max 600 170-220

b final (mats) Min 225 270-280 Min 225 300-320

Fincncssm 2Kg Max 10 10-20 Max 10 05-10

Soundness Max 08 004-008 Max 0080 004-02

a le-chart (mm)

b autoclave ()

Supreme Expertise

The Best Technical Team exclusive to Kesoram mans the Plant and monitors the process

to blend the cement in just the required proportions to make BIRLA SUPREMEGOLD OF

Rock Strength

18 Million Tones of Solid Foundation

Staying at the top for over a Quarter Century Quarter Century is no less an achievement

Infact Kesoram is synonymous with for over 28 years

Over the years Kesoram has dispatched 18 million tones of cement to the nook and cornersof the country and joined hands in strengthening the Nation No one else in Andhra Pradesh

has this distinction The prestigious World Bank aided Ramagundam Super Thermal Power

Project of NTPC and Mannair Dam of Pochampad project in AP arc a couple of projects for

which Kesoram Cement was exclusively uses to cite an example

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 2981

29

Chemical Characteristics

Opc 43 gr

Is 81 132-989

Birla

Supreme

43 grade

Ope 53 gr

Is 12269-

87

Birla

Supreme

Gold 53 gr

Loss on inflection Max 5 lt16 Max 40 lt15

Insoluble residue Max 20 lt08 Max 20 lt 06

Magnesium oxide Max 60 lt 13 Max 60 lt 13

Lime saturation factor 066-102 08-09 08-102 088-09

Alumna iron ratio MinO66 15-17 MinO66 15-17

Sulfuric anhydride Max 253 16-20 Max 2 53 16-20

Alkalis Chlorides Max 005 Max 001 Max 005 Max 04

Kesoram Cement - advantages

Helps in designing sleeker and more elegant

Structures giving greater flexibility in design concept

Due to its fine quality super fine construction can be achieved Its gives maximum

strength at Minimum use of cement with water in the water cement ratio especially the 53

grade Birlas supreme-gold

Feathers in Kesorams cap

Kesoram has outstanding track record achieving over 100 capacity utilization I

productivity and energy conservation It has proved its distinction by bagging several

national and state awards noteworthy being

NATIONAL

1 National productivity award for 1985-86

2 National productivity award for 1986-87

3 National award for mines safety for 1985-86

4 National award for mines safety for 1986-875 National award for energy conservation 1989-90

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3081

30

STATE

1 AP State productivity award for 1988

2 State award for best industrial management 1988-89

3 Best industrial productivity award of FAPCCI (federation of AP chamber of

commerce and industry) 1991

4 Best management award of the state Govt 1993

5 FAPCCI award for the workers welfare 1995-96

ISO 9002

All quality systems of Kesoram have been certified under ISO 90021S 4002 which

proves the worldwide acceptance of the products

All quality systems in production and marketing of the product have been certified by BIS

under ISO 90021S 14002

The first unit was installed at basanthnagar with a capacity of 25 ndashlakhs TPA (tones per

annum) incorporating humble supervision preheated system during the year 1969

The second unit followed suit with added a capacity of 2 lakhs TPA in 1971

The plant was further expanded to 9 lakhs by adding 25 lakhs tones in august 1978 113

lakhs tones in January 1981 and 087 lakhs tones in September 1981

Power

Singareni collieries make the supply of coal for this industry and the power was

obtained from AP TRANSCO The power demand for the factory is about 21MW Kesoram

has got 2-diesel generator seats of 4 MW each installed in the year 1987

Kesoram cement now has a 15MWcaptive power plant to facilities for uninterrupted

power supply for manufacturing of cement

Performance

The performance of kersoram cement industry has been outstanding achieving over

cent percent capacity utilization all through despite many odds like power cuts and which

most 40 was wasted due to wagon shortage etc

The company being a continuous process industry works round the clock and has

excellent records of performance achieving over 1005 capacity utilization

Kesoram has always combined technical progress with industrial performance The

company had glorious track record for the last 27 years in the industry

Technology

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3181

31

Kesoram cement uses most modern technology and the computerized control in the

plant A team of dedicated and well- experienced experts manages the plant

The quality is maintained much above the bureau of Indian standards

The raw materials used for manufacturing cement are

Lime stone

Bauxite

Hematite

Gypsum

Environmental and Social Obligations

For environmental promotion and to keep ndashup the ecological balance this section

has planted over two lakhs trees on social obligation front this section has undertaken

various social welfare programs by adopting ten nearly villages organizing family welfare

campus surgical camps animal health camps blood donation camps children immunization

camps seeds training for farmers etc were arranged

Welfare and Recreation Facilities

For the purpose of recreation facilities 2 auditoriums were provided for playing

indoor games cultural function and activities like drama music and dance etc

The industry has provided libraries and reading rooms About 1000 books are available in

the library All kinds of newspaper magazines are made available

Canteen is provided to cater to the needs of the employees for supply of snacks tea

coffee and meals etc

One English medium and one Telugu medium school are provided to meet the

educational requirements

The company has provided a dispenser with a qualified medical office and

paramedical staff for the benefit of the employees The employees covered under ESI

scheme have to avail the medical facilities from the ESI hospital

Competitions in sports and games are conducted every year for august 15th

Independence Day and January 26th republic day among the employees

Electricity

The power consumption per ton of cement has come down to 108 units against 113

units last year due to implementation of various energy saving measures The performance

of captive power plant of this section continues to be satisfactory Total power generation

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3281

32

during the year was 84 million units last year This captive power plant is a major role in

keeping power costs with in economic levels

The management has introduced various HRD programs for training and

development and has taken various other measures for the betterment of employeersquos

efficiency

The section has installed adequate air pollution control system and equipment and is

ISO14001 such as Environment management system is under implementation

Awards

Kesoram cement bagged many prestigious awards including national awards for

productivity technology conservation and several state awards since 1984 The following

are the some of important awards

AWARDS OF KESORAM CEMENT

No Year Awards

National

State

1 1989-90 Management award community

Development

State

2 1991 Energy conservation may day award of the

Govt

State

3 1991 Pundit Jawaharlal Nehru rolling trophy for

best

State

4 1993 National productivity effort Indira Gandhi

national award

State

5 1994 Best management award State

6 1994-

1995

Best industrial rebellion award State

7 1995 Rural development by chief minister

Environment and mineral conservation

award

State

8 1995 Best industrial rebellion award State

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3381

33

9 1995-

1996

Best effort of an industrial unit to

development rural economy shriSRRungta

award for social

National

10 1996 Awareness for best rural development

efforts

State

11 1999 Best workers welfare best family welfare

award

State

12 2001 First prize for mine environment amppollution

control for the 3rd

year in succession

State

13 2002 Vana mithra award from AP Govt State

14 2003 Company has got OHSAS-18001 State

15 2005 Certification from DNV New Delhi State

16 2006 Award for pollution control and

environmental protection FAPCCI award

for best rural development in the state

State

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3481

34

Products of the organization

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3581

35

CHAPTER-III

LITERATURE REVIEW

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3681

36

Introduction

Financial Performance Analysis

The term lsquofinancial performance analysis also known as analysis and interpretation of

financial statementsrsquo refers to the process of determining financial strength and

weaknesses of the firm by establishing strategic relationship between the items of the

balance sheet profit and loss account and other operative data

ldquoAnalyzing financial statementsrdquo by Metcalf and Titard

ldquoFinancial analysis is a process of evaluating the relationship between component

parts of a financial statement to obtain a better understanding of a firms position and

performancerdquo by Myers

Financial Performance

The word lsquoPerformance is derived from the word lsquoparfourmenrsquo which means lsquoto dorsquo lsquoto

carry outrsquo or lsquoto renderrsquo It refers the act of performing execution accomplishment

fulfillment etc In border sense performance refers to the accomplishment of a given task

measured against preset standards of accuracy completeness cost and speed In other

words it refers to the degree to which an achievement is being or has been accomplished In

the Words of Frich Kohlar ldquoThe performance is a general term applied to a part or to all the

conducts of activities of an organization over a period of time often with reference to past or

projected cost efficiency management responsibility or accountability or the like Thus not

just the presentation but the quality of results achieved refers to the performance

Performance is used to indicate firmrsquos success conditions and compliance

Financial performance refers to the act of performing financial activity In broader

sense financial performance refers to the degree to which financial objectives being or has

been accomplished It is the process of measuring the results of a firms policies and

operations in monetary terms It is used to measure firms overall financial health over a

given period of time and can also be used to compare similar firms across the same industry

or to compare industries or sectors in aggregation

The purpose of financial analysis is to diagnose the information contained in financial

statements so as to Jude the profitability and financial soundness of the firm Just like a

doctor examines his patient by recording his body temperature blood pressure etc Before

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3781

37

making his conclusion regarding the illness and before giving his treatment a financial

analyst analysis the financial statements with various tools of analysis before commenting

upon the financial health or weaknesses of an enterprise

The analysis and interpretation of financial statements is essential to bring out the

mystery behind the figures in financial statements Financial statements analysis is an

attempt to determine the significance and meaning of the financial statement data so that

forecast may be made of the future earnings ability to pay interest and debt maturities (both

current and long term) and profitability of a sound divided policy

Types of financial analysis-

Financial analysis into different categories depending upon

(1) The material used and

(2) The method of operation followed in the analysis or the modus operandi of

analysis

Types of financial analysis

On the basis of material used on the basis of modus operandi

External Internal Horizontal Vertical

Analysis Analysis Analysis Analysis

1 On the basis of material used - According to material used financial analysis canbe of two types

External analysis

Internal analysis

External analysis-

This analysis is done by outsiders who do not have access to the detailed internal

outsiders include investors potential investors Creditors Potential Creditors Government

Agencies Credit Agencies and General Public For financial analysis these external parties

to the firm depend almost entirely on the published financial statements

Internal analysis-

This analysis is undertaken by the persons namely executives and employees of the

organization or by the officers appointed by government or court who have access to the

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3881

38

books of account ( internal accounting records) and other information related to the

business

2 983119983150 983156983144983141 983138983137983155983145983155 983151983142 983149983151983140983157983155 983151983152983141983154983137983150983140983145983085

According to the modus operandi financial analysis can also be of two types

a Horizontal analysis

bVertical analysis

Horizontal analysis-

Horizontal analysis refers to the comparison of financial data of a company for several

years The figures for this type of analysis are presented horizontally over a number of

columns The figures of the various years are compared with standard or base year a base

year is year chosen as beginning point This type of analysis is also called lsquodynamicanalysisrsquo as it is based on the data from year to year rather than on data of any one year The

horizontal analysis makes it possible to focus attention on items that have changed

significantly during the period under view

b Vertical analysis-

Vertical analysis refers to the study of relationship of the various items in the financial

statements of one accounting period In this types of analysis the figures from financial

statement of a year are compared with a base selected from the same yearrsquos statement

Methods of financial analysis-

The following methods of analysis are generally used-

1 Comparative Statements

2 Trend Analysis

3 Common-Size Statements

4 Funds flow Analysis

5 Cash Analysis

6 Ratio Analysis

7 Cost-volume-Profit Analysis

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 3981

39

Comparative statements-

The comparative financial statements are statements of the financial position at

different periods of time the elements of financial position are show in a

Comparative Statement provides an idea of financial position at two or more

periods Generally two financial statements (balance sheet and income statement) are

prepared in comparative form for financial analysis

The Comparative Statement May Show-

1 Absolute figures (rupee amounts)

2 Changes in absolute figures ie increase or decrease in absolute figures

3 Absolute data in terms of percentages

4 Increase or decrease in terms of percentages

The Two Comparative Statements Are-

1 Comparative balance sheet and

2 Income statement

1 983107983151983149983152983137983154983137983156983145983158983141 983138983137983148983137983150983139983141 983155983144983141983141983156983085

The comparative balance sheet analysis is the study of the trend of the same items group of

items and computed items in two or more balance sheets of the same business enterprise on

different dates The change in periodic balance sheet items reflect the conduct of a business

the change can be observed by comparison of the balance sheet at the beginning and at the

end of a period and these changes can help in forming an opinion about the progress of an

enterprise

Guide Lines for Interpretation of Comparative Balance Sheet-

While interpreting comparative balance sheet the interpreter is expected to study the

following aspects-

1 Current financial position and liquidity position

2 Long-term financial position

3 Profitability of the concern

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 4081

40

Common Size Statement-

The common-size statements balance sheet and income statement are show in

analytical percentages The figures are shown as percentages of total assets total liabilities

and total sales The total assets are taken as 100 and different assets are expressed as a

percentage of the total similarly various liabilities are taken as a part of total liabilities

Common Size Balance Sheet-

A statement in which balance sheet items are expressed as the ratio of each asset to

total assets and the ratio of each liability is expressed as a ratio of total liabilities is called

common size balance The common size balance sheet can be used to compare companies

of differing size The comparison of figures in different periods is not useful because total

figures may be affected by a number of factors It is not possible to establish standard norms

for various assets The trends of figures from year to year may not be studied and even they

may not give proper results

Trend Analysis of Balance Sheet-

Trend analysis is Very important tool of horizontal financial analysis

This analysis enables to known the change in the financial function and operating efficiency

in between the time period chosen

By studding the trend analysis of each item we can known the direction of changes and

based upon the direction of changes the options can be changed

Trend =Absolute Value of item in the statement understudy 100

Absolute Value of same item in the base statement

Ratio Analysis

Ratio analysis is used as a technique of analyzing the financial information contained in the

balance sheet and profit and loss accounts for a more meaningful understanding of the

financial position and performance of a firm

The relationship between two accounting figures expressed mathematically is known as a

financial ratio A ratio helps the analyst to make qualitative judgment about the firmrsquos

financial position and performance

Several ratios can be calculated from the accounting data contained in the financial

statements The parties which generally undertake financial analysis is short ndashterm

creditors long-term creditors owner and management In view of the requirements of the

various ratios ratios are classified into the following four important categories

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 4181

41

Liquidity ratios

Leverage ratios

Activity ratios

Profitability ratios

Liquidity Ratios

It is extremely essential for a firm to be able to meet its obligations as they become due

Liquidity ratios measure the ability of the firm to meet its current obligations A firm should

ensure that it does not suffer from lack of liquidity and also that it does not have excess

liquidity The failure of a company to meet its obligations due to lack of sufficient liquidity

will result in a poor creditworthiness loss of creditorsrsquo confidence or even in legal tangles

resulting in the closure of the company A very high degree of liquidity is also bad idle

assets earn nothing The firmrsquos funds will be unnecessarily tied up in current assets

Therefore it is necessary to strike a proper balance high liquidity and lack of liquidity

The most common ratios which indicate the extent of liquidity or lack of it are

Current ratio

Quick ratio

Other ratios include Cash ratio Interval Measure and Net working capital ratio

Current Ratio

The current ratio is calculated by dividing current assets by current liabilities

Current assets

Current ratio = --------------------------

Current liabilities

Current ratio is a measure of the firmrsquos short term solvency It indicates the availability of

current assets in rupees for every one rupee of current liability A ratio of greater than one

means that the firm has more current assets than current claims against the Current ratio of

2 to 1 or more is considered satisfactory Current ratio represents a margin of safety for

creditors

Quick Ratio

Quick ratio also known as acid-test ratio establishes a relationship between quick assets and

the current liabilities Cash is the most liquid asset It is calculated by dividing quick assets

by current liabilities

Quick ratio = Quick Assets Current Liabilities

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 4281

42

(Quick Assets = Current assets ndash Inventory)

One defect of the current ratio is that it fails to convey any information on the composition

of the current assets of the firm A rupee of cash is considered equivalent to a rupee of

inventory of receivables But it is not so A rupee of cash is more readily available to meet

current liabilities than a rupee of say inventory This implies the usefulness of the current

ratio

The Acid ndashtest ratio measures the firmrsquos ability to convert its current assets quickly into

cash in order to meet its current liabilities

A quick ratio of 1 to 1 is considered to represent a satisfactory current financial condition It

is an important index of the firmrsquos liquidity

Leverage Ratios

Leverage ratios identify the source of a firmrsquos capital ndashowners or outside creditors

Financial leverage refers to the use of debt in financing non-current assets If the return on

assets exceeds the cost of debt the leverage is successful ndash ie it improves return on equity

Debt ndashEquity Ratio

The Debt ndash Equity is determined to analyze the soundness of the long term financial

policies of the organization It is also known as ldquoInternal External Equity Ratiordquo

It is calculated as follows

Debt ndash Equity Ratio = Total long term debt Share holders funds

Equity Ratio

This ratio is also called as proprietary ratio establishes a relationship between share holderrsquos

funds to total assets of company Equity Ratio is calculated by dividing share holders fund

by total assets

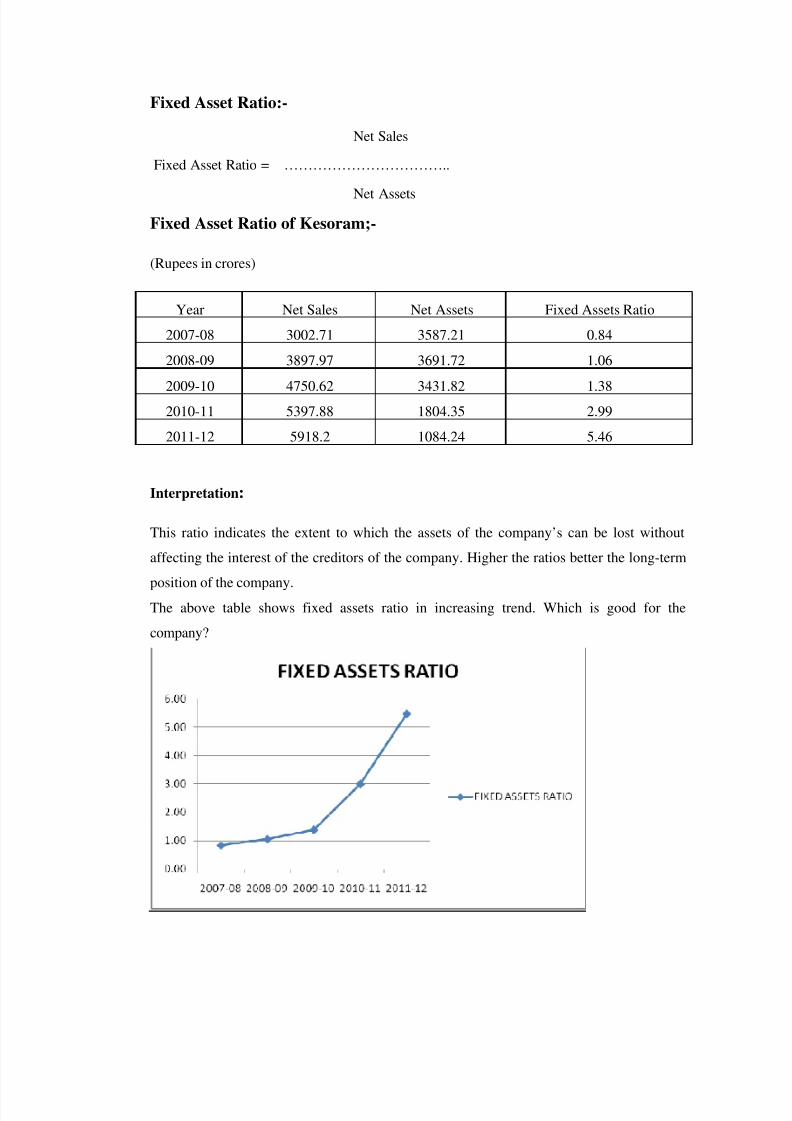

Fixed Asset Ratio

This ratio indicates the extent to which the assets of the companyrsquos can be lost without

affecting the interest of the creditors of the company Higher the ratios better the long-term

position of the company

Activity Ratios

They are primarily used for studying a firmrsquos working capital situation A well managed

firm should have good activity ratios

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 4381

43

Working Capital Turnover Ratio

The working capital turnover ratio indicates whether or not working capital has been

effectively used in making sales

Working capital turnover = Sales Net current assets

Inventory Turnover Ratio

This ratio also known as Stock Turnover Ratio establishes the relationship between costs of

goods sold or net sales during the given period and the average amt of stock held during the

period This ratio reveals the number of times finished stock in turnover during a given

accounting period

Higher the ratio the better is it because it shows the finished stock is rapidly turned

in to sales On the other hand a low stock turnover ratio is not desirable because it reveals

the accumulation of stock

Debtors Turnover Ratio

This ratio indicates the velocity of debt collection of a company In other words it shows

the number of times average turnover during a year

A Higher Debtor Turnover Ratio indicates a more efficient is the management towards

debtors and low ratio ratio implies inefficient management of debtors

Total Assets Turnover Ratio

The asset turnover ratio indicates how efficiently management is employing Assets

Total Assets Turnover Ratio = Sales Total Assets

Profitability Ratios

Profitability ratios are the ratios which measure a firmrsquos overall effectiveness as revealed by

the returns generated on sales and investment

General Profitability Ratios

1 Gross Profit Ratio

2 Net profit Ratio

3 Operating or Expenses Ratio

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 4481

44

Gross Profit Ratio

Gross profit Ratio measures the relationships to net sales and is usually represented as a

percentage It is a good measure of profitability

The gross profit ratio indicates the extent to which selling price of goods per unit may

decline without resulting in losses on operation Higher the gross profit betters the result

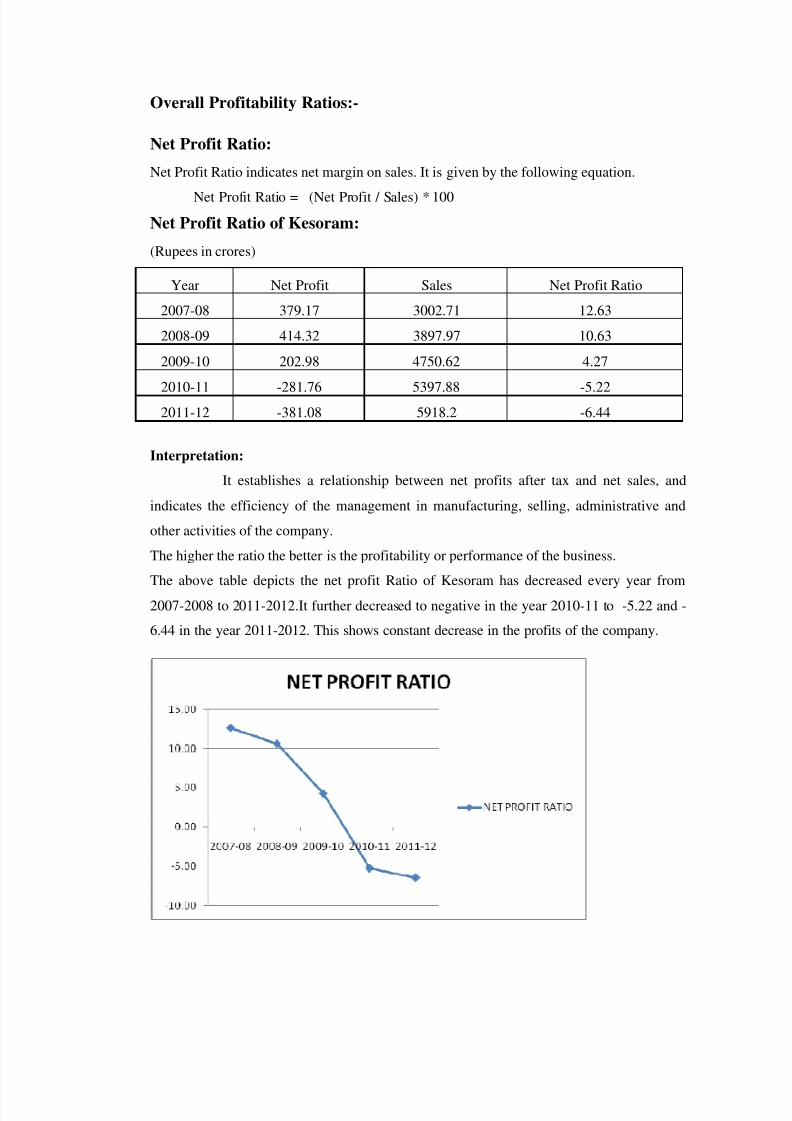

Net Profit Ratio

Net Profit Ratio indicates net margin on sales It is given by the following equation

Net Profit Ratio = (Net Profit Sales) 100

Operating or Expenses Ratio

This ratio is complimentary of Net Profit Ratio The more the net profit the less the

Operating Ratio Operating costs include the cost of direct materials direct labors and otheroverheads viz are generally excluded from operating costs A comparison of the Operating

Ratio will indicate whether the cost efficiency is high or low in the figure of sales This less

the ratio it depicts the efficiency of the management

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 4581

45

CHAPTER IV

DATA ANALYSIS amp INTERPRETATION

8102019 A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance hellip

httpslidepdfcomreaderfulla-study-a-study-on-financial-performance-analysis-with-reference-to-kesoram 4681

46

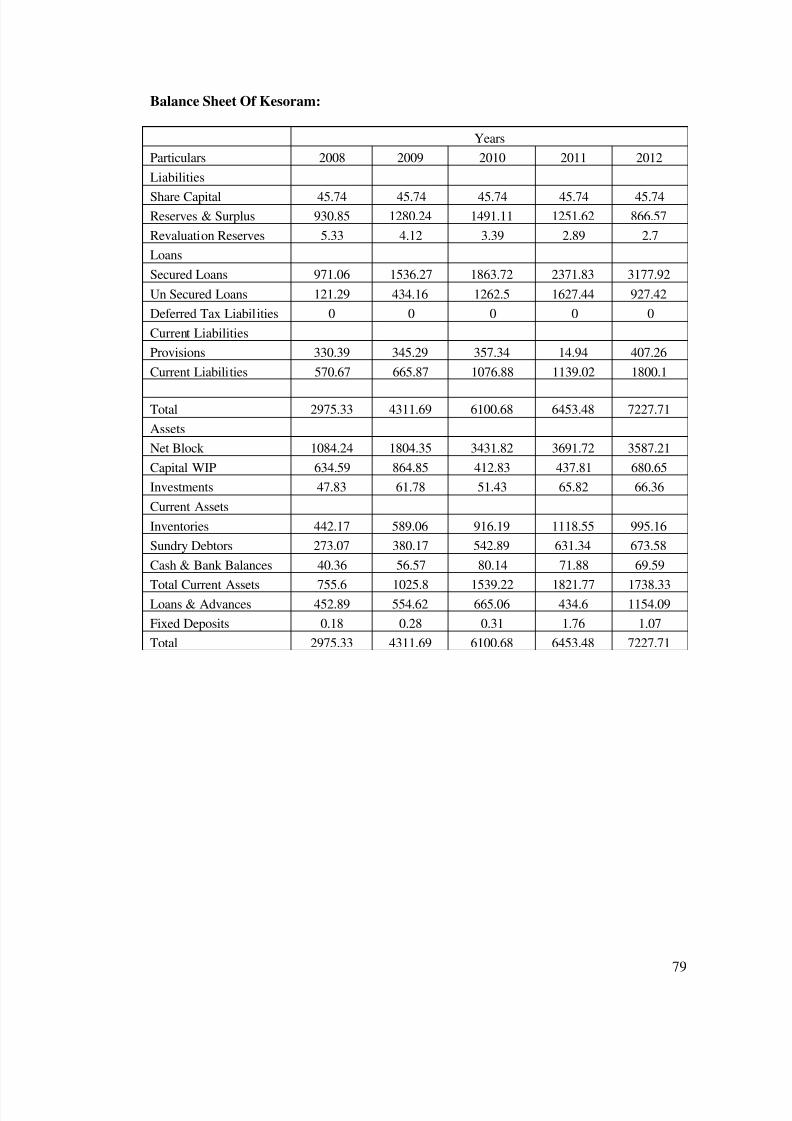

Comparative Balance Sheet of Kesoram in the Year between 2008-2009

(Rupee in crores)

Years Changes

Particulars 2008 2009 In Rupees In Percentage

Liabilities

Share Capital 4574 4574 000 000

Reserves amp Surplus 93085 128024 34939

Revaluation Reserves 533 412 -121 -2270

Loans

Secured Loans 97106 153627 56521 5821

Un Secured Loans 12129 43416 31287 25795

Deferred Tax Liabilities 000 000 000 000

Current Liabilities

Provisions 33039 34529 1490 451

Current Liabilities 57067 66587 9520 1668

Total 297533 431169 133636 4491

Assets

Net Block 108424 180435 72011 6642

Capital Wip 63459 86485 23026 3628

Investments 4783 6178 1395 2917

Current Assets

Inventories 44217 58906 14689 3322

Sundry Debtors 27307 38017 10710 3922

Cash amp Bank Balances 4036 5657 1621 4016

Total Current Assets 75560 102580 27020 3576

Loans amp Advances 45289 55462 10173 2246

Fixed Deposits 018 028 010 5556

Total 297533 431169 133636 4491