Dr Aaron G. Grech Central Bank of Malta & London School of Economics 19 th February 2015 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Dr Aaron G. Grech

Central Bank of Malta & London School of Economics

19th February 2015

1

Why provide incentives for voluntary personal

retirement schemes?

A review of practices across the EU

The incentives provided in Malta

Remaining issues

2

Economic theory argues that taxation and tax exemptions hurt economic efficiency as they distort behaviour from its optimal path.

Since state pension generosity is set to decline, economic theory suggests that forward-looking individuals will save more anyway.

A strand of economic research argues that fiscal incentives do not generate new saving, but rather a movement of saving from taxed to untaxed products.

So why should Government intervene?

3

Insufficient retirement income: Retirement income is

more important than other saving, and yet individuals

are less likely to do it due to myopic behaviour.

Individuals are not well-informed on state pensions.

Moral hazard: The existence of means-tested benefits

may lead people to under-save. By providing incentives

to save, the Government is redressing this issue.

Need to increase saving: Given ageing, the Government

needs to intervene to favour a larger capital base to

improve future potential output and income. Saving

helps us get a share in foreign countries’ future growth. 4

International evidence on the effectiveness of tax

incentives to increase national saving is mixed. In

particular, many studies have shown that a shift to a

funded system does not automatically raise saving.

However the case of Malta is not the same. The state

system results in diminishing provision as the effective

social security rate is declining. Meanwhile, the

household saving rate has nearly halved since the 1990s.

Moreover a lot of savings are very liquid (about a third

are currency or savings accounts) with very low return.

Most long term savings tend to give lump sums.

5

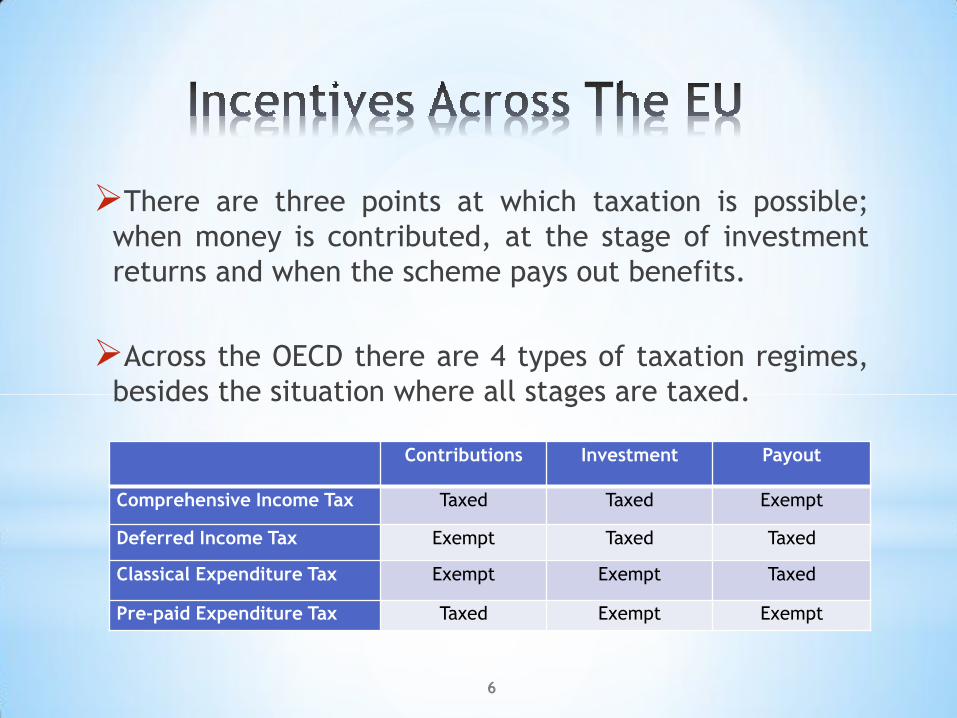

There are three points at which taxation is possible;

when money is contributed, at the stage of investment

returns and when the scheme pays out benefits.

Across the OECD there are 4 types of taxation regimes,

besides the situation where all stages are taxed.

6

Contributions Investment Payout

Comprehensive Income Tax Taxed Taxed Exempt

Deferred Income Tax Exempt Taxed Taxed

Classical Expenditure Tax Exempt Exempt Taxed

Pre-paid Expenditure Tax Taxed Exempt Exempt

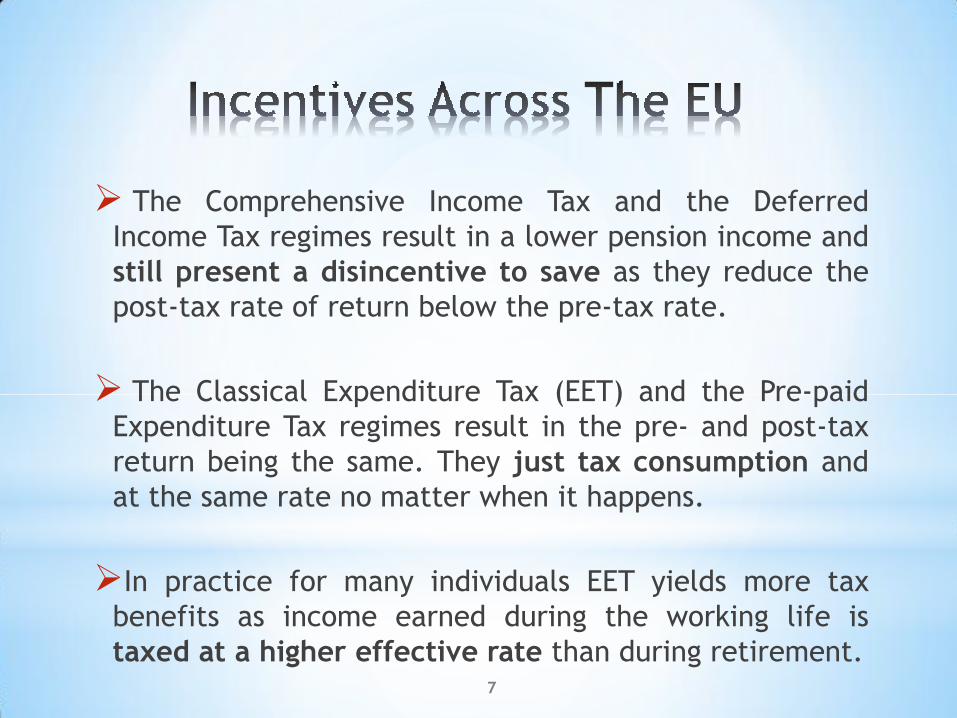

The Comprehensive Income Tax and the Deferred

Income Tax regimes result in a lower pension income and

still present a disincentive to save as they reduce the

post-tax rate of return below the pre-tax rate.

The Classical Expenditure Tax (EET) and the Pre-paid

Expenditure Tax regimes result in the pre- and post-tax

return being the same. They just tax consumption and

at the same rate no matter when it happens.

In practice for many individuals EET yields more tax

benefits as income earned during the working life is

taxed at a higher effective rate than during retirement.

7

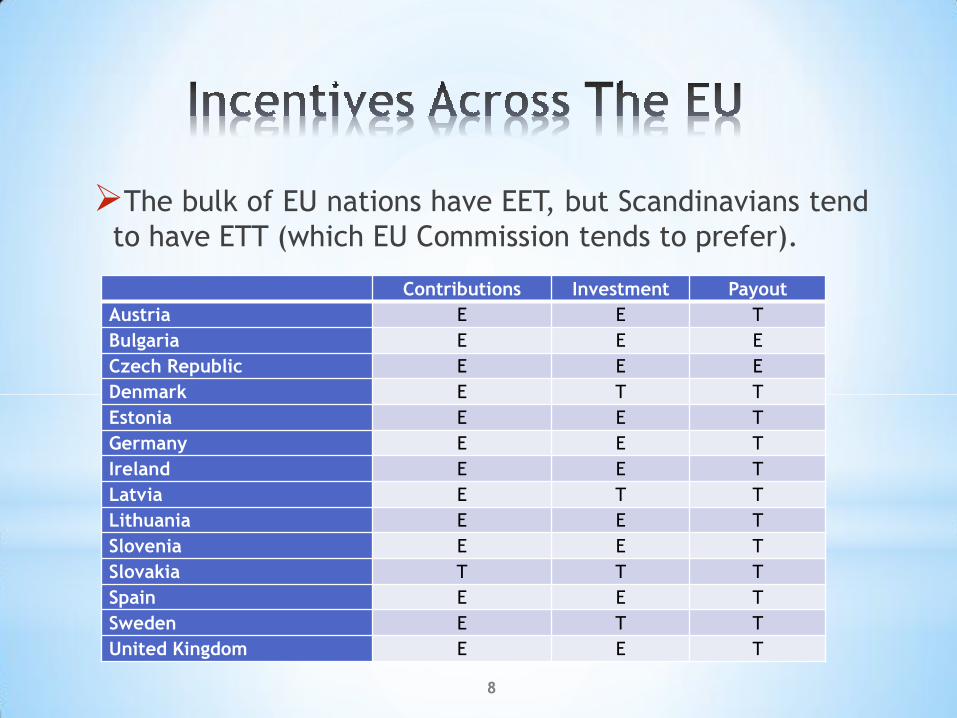

The bulk of EU nations have EET, but Scandinavians tend

to have ETT (which EU Commission tends to prefer).

8

Contributions Investment Payout

Austria E E T

Bulgaria E E E

Czech Republic E E E

Denmark E T T

Estonia E E T

Germany E E T

Ireland E E T

Latvia E T T

Lithuania E E T

Slovenia E E T

Slovakia T T T

Spain E E T

Sweden E T T

United Kingdom E E T

Countries set restrictions on contributions in order to

control tax avoidance or for distributional issues. There

is significant variation in contribution limits.

9

Annual Contribution Limit

Austria €2,260

Belgium €810

Czech Republic €960

France 10% of income

Germany €12,000

Hungary €400

Ireland 15% of income

Italy €5,150

Netherlands €1,040

Portugal €400

Slovakia €400

Spain €7,200

United Kingdom €51,000

Besides providing tax incentives, there are two other

policies that have been put in place, especially to help

participation among those on low income, who tend to

be young and therefore those who should be saving.

Some countries like Sweden and the UK have made

personal pensions quasi-mandatory or mandatory, for

instance by auto-enrolling new workers into schemes.

Typically this requires a default scheme run by the State.

In others, such as Germany and Austria, there is heavy

State subsidisation for certain contributions, through

matching contributions or direct subsidies.

10

Till the launch in 2014 of Government’s Supporting

Retirement Saving (SRS) incentive scheme, most long

term savings in Malta were either taxed at all stages or,

in the case of lump sum products, were TTE.

SRS has two components. The first is the provision of a

15% tax credit on contributions to a personal retirement

scheme (PRS) up to a maximum of €1,000 a year.

Investment income on such schemes is tax-free.

The second component is the introduction of Individual

Saving Accounts (ISAs), which are interest-bearing

schemes to which one can contribute up to €1,000 a

year. Interest earned on these schemes is tax-free.

11

For savings products to be deemed a PRS, they need to

fulfil 5 criteria:

Operate under the Retirement Pensions Act or

similar legislation like the Insurance Business Act;

Benefit payments shall not start earlier than age

50 or later than 70;

Only up to 30% of assets to be given as lump

sum, the rest through annuity or drawdown;

Are subject to specified investment restrictions

under the Retirement Pensions Act;

Need to set transparent charges and send

regular information to savers.

12

Why go for 15% tax credit?

Those on high incomes are already saving. It is

unfair to provide better incentives to them than to

those on lower income. Only those earning more

than €25,000 (150% average wage) pay an effective

tax rate more than 15%. The scheme increases the

minimum tax threshold by €1,000 for savers.

Why go for a €1,000 annual contribution limit?

This amounts to about 6.3% of the average wage,

and would result in a pension pot that would

deliver a replacement rate of about 9% of average

wages at retirement (the reduction in state

pension generosity after the 2007 reform).

13

Amongst the main concerns faced by individuals

(especially those on low incomes) when buying pension

products is that they will not be able to access funds.

To allay this fear ISAs are being introduced. Individuals

will be able to save without entering into long-term

commitments. They would be getting a tax exemption

on the 15% withholding tax on interest income.

The hope is that in time these individuals will feel more

confident and transfer their savings into a PRS. ISAs are

one of the most popular savings products abroad.

14

Should there be additional conditions on PRSs so that

more individuals feel confident about them?

In a consultation exercise, financial sector groups

were asked about issues such as provision of

guarantees and capping of fees. There was a general

consensus that the financial sector would find these

conditions onerous and there is no need for them.

Should contribution limits increase?

While the current level is appropriate, it will be

important to ensure that the limits are revised from

time to time to remain relevant.

15

Should ISAs be extended to cover capital gains?

At this stage this seems premature and could harm

the development of PRSs.

Should contributions also be allowed for family

members?

Current legislation allows someone who pays the

married rate to also contribute for their partner.

However contributions for children are not allowed.

What about State or Employer contributions?

At this stage this seems premature but this is an

option which will be kept under review, especially

for low income earners.

16

After 35 years of absence, there are now all the

conditions for private pensions to be re-established in

Malta. This area constitutes the major missing piece of

the Maltese financial services sector.

The sector’s development will depend on the financial

industry offering adequate products that win the trust

of Maltese savers who have grown used to low-return,

low-risk and easy-access financial products.

The concerted efforts of all stakeholders could result in

retirement provision becoming more diversified, ensuring

a better income for future pensioners and less

pressure on future taxpayers.

17

Related Documents