Fraud in a Downturn A review of how fraud and other integrity risks will affect business in China in 2009

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Fraud in a DownturnA review of how fraud and other integrity risks will affect business in China in 2009

2 Fraud in a downturn

Contents

Introduction

Fraud and integrity risks in 2009

The strategy of the enlightened organisation

Conclusion

3

10

18

22

Fraud in a downturn 3

Introduction

The impact of the global economic slowdown is challenging even our most robust institutions. Those charged with the governance of some of the world’s largest companies have had to focus on short term measures to address the risk of corporate failure. The dilemma organisations face is how best to manage recovery in the short term, while not losing sight of the need to maximise shareholder value and to maintain and develop services over the medium and long term.

As the global economy declines and China feels the impact of this, new threats emerge. The failure of Bernard L. Madoff Investment Securities LLC illustrates very well how, as economic conditions decline, allegations of fraud, previously undetected, emerge from the shadows. Possibly the only positive aspect of the credit crunch is that, as providers of finance retrench and seek return of loan finance or investment capital, fraudulent borrowing or fraudulent investment management is revealed, thereby capping the losses that have occurred.

When economic survival is threatened (either for the organisation or for the individual) the line separating acceptable and unacceptable behaviour can, for some, become blurred. In addition, fraud and other economic crime have become a focus of criminal activity over the past five years; criminal organisations that profit from fraud view the current economic conditions as an opportunity, not a threat.

There are aspects of the economy in the emerging markets, and specifically in China, which can be a catalyst for fraud to occur, due to the structure of supply chains, management, legal systems as well as cultural differences.

This paper considers whether fraud and integrity threats are changing during this period of economic downturn and, if so, how. It considers in detail particular areas of risk in relation to China, and highlights, looking forward, the issues that boards of directors and audit committees need to beware of in 2009: the frauds that may emerge and the likely regulatory response. Finally, we describe the strategies enlightened organisations are implementing to manage short term risks and to enhance stakeholder value in the longer term.

4 Fraud in a downturn

The perfect storm

The Fraud Triangle, developed by the criminologist, Dr. Donald Cressey, describes three conditions that are commonly found when fraud occurs. The perpetrators experience some Incentive or Pressure to engage in misconduct. There must be an Opportunity to commit fraud and the perpetrators are often able to Rationalise or justify their actions. The global economic decline is such that each of these three factors (Incentive / Pressure, Opportunity and Rationale) is present as never before.

There are specific characteristics in the China market which can expose organisations with China operations to an even greater risk of fraud, by acting as a catalyst to increase incentive/pressure, opportunity or rationalisation.

Incentive / PressureWhile fraud could, from a legal perspective, be perpetrated by a company, the steps taken to commit fraud are always the actions of individuals. It is sometimes assumed that people commit fraud for personal gain and in particular to obtain money. People are said, for example, to ‘cook the books’ in order to earn the large year end bonus. The reality is far more complex. Personal gain is often a factor – in other instances it is personal reputation, pressure from above or a desire to help the organisation succeed that can be the principle motivation.

Avoidance of loss, whether it be future income, job security, power or prestige can be a strong motivator. As people lose their jobs, and those still in employment feel ever more threatened, the pressure to commit fraud will increase. The great majority of people are fundamentally honest and, as such, are not tempted by wrongful personal gain. However, when someone’s livelihood is at stake, or the future of a company rests on obtaining a new order from a potential customer, some people will feel more acutely the pressure to do the wrong thing: to pay the bribe that secures the company’s financial future or to look the other way while others do so.

In China, the high growth rate of the economy, and the structure of business ownership can create additional risks with regards to the incentive / pressure to commit fraud:

!FRAUD RISK

OpportunityAttitude /

rationalism

Incentive / pressure

Fraud in a downturn 5

High growth rate of the economyThe speed of China’s economic growth is unprecedented in history. While the large developed economies of the west have gone into recession, recent OECD figures for China still estimate 6–7% growth in 20091. In recent years, investors have poured capital into China with the expectation of capitalising on these high growth rates. As these growth targets filter down through senior management and to operational staff, this can result in staff at all levels being subjected to extreme pressure to deliver. As China feels the purse strings tightening due to decreased exports and high domestic saving, the incentive/pressure for company executives to find other ways to meet their targets is likely to increase.

Structures of ownershipMany industry sectors of the economy in China remain largely state controlled, including banking, energy, mining and healthcare. Aside from the 150 or so large corporations that report directly to the central government, there are also a much larger number which fall into a grey area, including partly owned subsidiaries of large state owned organizations, companies owned by local and municipal governments and those which retain a state holding company as one of their minority shareholders2. Organizations operating in China thus need to be cautious when dealing with local companies that they are fully compliant with international anti-bribery legislation for example the Foreign Corrupt Practices Act which prohibits the offer or gift of anything

of value to a foreign official. A business associate who may in other societies be regarded as a private individual representing a private company, may in China be viewed as a “foreign official” in the eyes of the US Department of Justice. Furthermore, there is a potential for increased incentive/pressure to pay bribes when lines are blurred between government administration and business management creating a conflict of interest, despite the Central Communist Party policy of zhengqi fenkai (separation of government functions and business operations).

OpportunityThe word “crisis” in Chinese weiji is made up of two characters, one meaning “danger” and the second “opportunity”. The world is in a state of perpetual change, and with change comes opportunity. What is new, however, is how the economic downturn is forcing the pace of change. This can create opportunities for potential fraudsters to take advantage of. Organisations looking to reduce costs must now do so with little time to reflect. Programmes and projects are being cut at short notice. People are being let go without sufficient time for employers to reflect on the longer term consequences.

1 Dow Jones Newswires: OECD Economic Growth to Slow More Than Expected in ’09, 20 March 2009, Dow Jones & Company, Inc.

2 Reassessing China’s State-Owned Enterprises - McKinsey Quarterly, 7/8/2008

6 Fraud in a downturn

As change happens, gaps in the control system can and will appear. With fewer people employed there will be less scope for the segregation of duties that is a key component of internal control in relation to fraud. Checks and balances put in place to maintain control will be abandoned. Procedures whose purpose was to detect anomalies will be suspended.

In China, the nature of supply chains and often blurry legal boundaries can significantly increase the opportunity to commit fraud, as outlined below:

Supply chain disparitySupply chains in developing countries such as China are often more complex and fragmented than those in developed countries, not least in China because of its sheer size and geographical diversity. In order to achieve market penetration and distribute to large numbers of heterogeneous markets in often remote regions, there is a heavy reliance on distributors, dealers, agents and other middlemen, which can mean that maintaining full control over the production and distribution process from raw material to delivery of the end product can be more complex and thus more susceptible to manipulation. This can significantly increase the opportunity to commit fraud.

Legal issues and the localization of controlThe PwC global economic crime survey (2007) highlights a perceived complexity in the legal system

in China and a perception of high levels of corruption3. While the central government is publicly very active in fighting corruption and encouraging clean business4, what is often found in China is a situation of “clean water, dirty pipes”, i.e. the clean policy poured into the system at the top in Beijing is not necessarily what is happening further down the line. Well connected local courts can act in a way that protects their own interests rather than really encouraging transparent and clean business5. Furthermore, the fact that the law comes from a series of often ambiguous and vague statutes as opposed to a system of common law can lead to inconsistency in its application. These factors combine to contribute to an increase in both the opportunity, as well as the rationalisation to commit fraud.

RationalisationThe third element of the fraud triangle is the ability of individuals, be they front line operations staff or members of the board of directors, to rationalise the fraudulent act. To illustrate what we mean by this we have set out below some examples of rationalisation, with a particular emphasis on themes that will emerge as the economic downturn persists.

“Everyone pays bribes to make sales in that country, there is no other way.”

3 PricewaterhouseCoopers Global Economic Crime Survey, 2007 4 Commercial Bribery and Liability, China Law and Practice, 10 Feb 2009,

Euromoney Institutional Investor PLC5 The Economist Intelligence Unit, 27 February 2009

Fraud in a downturn 7

“If the city bankers can keep their million dollar bonuses, why can’t I have a piece of the action?”

“Cooking the books or ‘creative accounting’ is not fraud, it is just bending the rules.”

“This company is fundamentally sound – if I have to cross the line to get us through the next six months, so be it.”

“I was entitled to a bigger bonus than I received, so made up a bit of the difference via expense claims.”

In difficult economic times the capacity for people to rationalise fraud and corruption increases.

The rationalisation aspect of the fraud triangle can be expanded to incorporate the idea of differential association. This is the idea that criminal behaviour is learnt in interaction with other persons in a process of communication6. In this respect, the culture of an organisation, and cultural norms of a country can play a significant part in creating a rationalisation for committing a crime. In China, some cultural and social characteristics could potentially increase the risk of rationalisation of fraud:

Cultural differences and historical legaciesIn China, there is a strong reliance on the fostering of close personal relationships, or guanxi in order to achieve business goals. It is often perceived as essential to have relationships with government and in the supply/distribution chain which are based on a form of mutual individual benefit. Whilst globally, maintaining good relationships with suppliers and customers is essential for developing a sustainable business, in China there is a risk that the maintenance of these relationships can be prioritised above the objective achievement of a business goal.

It has been suggested that one reason for this China specific cultural norm is a hangover in business mindset from the days of the state run economy where the entire welfare system in China had devolved to the work unit and employees were reliant on the leaders of their work unit for nearly every aspect of their lives. The factory leaders themselves had strong vested interests to protect, and the cultivation of local government officials was one means by which they protected them7. In the earlier days of the state run economy, in many cases the only way to get ahead was to cultivate these personal relationships. This remains significant in recent times, and as it becomes increasingly difficult to make ends meet, and increased pressure is experienced by individuals, organisations and families, the reliance on relationships is likely to become more prevalent, and increasingly may be viewed as an essential part of self protection.

6 Association of Certified Fraud Examiners Manual 2008, 4.206 7 Perkowski, Jack, Managing the Dragon : How I’m Building a Billion Dollar

Business in China, Crown Business, New York, 2008

8 Fraud in a downturn

Disparate wealth and an increasing divideAlthough China’s predominantly state owned banks have not been exposed to the slowdown in the financial markets as much as their western counterparts, and there has not been as much public anger at the high rewards for seemingly poor performance in these banks as in the west, there is increasing discontent among the populace amid the severe economic downturn about the ever widening wealth gap in China. Estimates have suggested that workers in the lowest paid industries earn a tenth of those in the highest paid8, without even taking into account the vast disparities of wealth between urban and rural areas. As pressure increases to meet targets, the particularly large differences in earnings between senior staff and a lower level unskilled worker could significantly increase the rationalisation of fraud.

Intellectual propertyAlthough there has been progress made with regards to intellectual property rights, substantial improvements still remain a long way off9. These risks can be highlighted particularly if production is outsourced or if trademarked higher quality products are made alongside lower quality products intended for the local market. There has been headway made in recent infringement cases, but this still remains a significant

fraud risk in China. The ongoing rationalisation for this type of fraud can be found on the streets of all large Chinese cities where counterfeit goods from DVDs to mobile phones, from luxury watches to clothing brands can readily be found in abundance.

From a demand side, as disposable income decreases during the financial crisis, consumers may more readily favour cheaper, counterfeit goods, rather than legal alternatives. Furthermore, companies experiencing cost pressures may cut corners with regards to licenses and royalty payments, particularly in areas where cheap copies are readily available, such as in the software market. Looking from the supply side, research and development budgets may be hit by cost cuts, creating an increased rationalisation to reverse engineer or copy existing products, rather than expend resource on developing own brand products. The significant reduction in demand for China’s exports10 may add to the risk of intellectual property violations, as struggling outsourced production companies or Joint Ventures which previously manufactured goods for export may move towards the manufacture of lower quality imitations for the domestic market in order to survive.

8 Financial Industry Executives Asked to Take Pay Cut as Salary Gap Widens Further in China, Global Insight Daily Analysis, 10 April 2009 9 Economist Intelligence Unit, February 200910 Xinhua Net 25 April 2009

Fraud in a downturn 9Fraud in a downturn 9

10 Fraud in a downturn

1. How vulnerable is the organisation to financial statement fraud?

Collusive fraud involving senior management in collaboration with third parties is notoriously difficult to identify. Adequate segregation of duties and responsibilities helps mitigate the risk but, as noted earlier in this paper, as costs are cut segregation of duties in some organisations is beginning to break down. Where senior management collude with others to provide evidence in support of balances in the financial statements, material fraud can be almost impossible for auditors to detect. Audit committees should consider whether internal controls and processes are sufficiently robust to prevent accounting fraud and ask some key questions:

• Istheethicaltoneatthetopappropriate?• Areremunerationsystemsdrivingtheright behaviours for our senior people?• Arethesegregationofkeydutiesandresponsibilities still adequate following any cost cutting initiatives?

• Dowehaveanadequatewhistleblowerhotlineand would employees speak up if they had concerns? • Howwellresourcedisinternalaudit?• Doesinternalaudithavethenecessaryfraud detection experience?• Arethereportinglinescorrectforfunctionssuchas finance and internal audit?• Dowehavethenecessaryfinancialskillsto challenge the numbers?

Significant accounting frauds often run undetected for a number of years. Inflated revenue (through incorrect revenue recognition), keeping liabilities off - balance sheet and the over statement of fair valued assets (or understatement of associated provisions) are the most likely to arise. Frauds that emerge in 2009 will have started in 2008 or even earlier with the economic downturn acting as the catalysts that result in the detection of the wrongdoing. As Warren Buffet so memorably, put it: “you only find out who is swimming naked when the tide goes out”11.

Fraud and integrity risks in 2009

We have discussed the likely influence of the economic downturn on fraud in 2009, and particular high risk areas in China. Given these circumstances, what are the likely effects on corporates, investors, regulators and government? The questions below are ones that we believe boards and audit committees should be asking themselves and key stakeholders:

11 Letter to the shareholders of Berkshire Hathaway Inc., 28 February 2002

Fraud in a downturn 11

2. Is the organisation at risk of regulatory scrutiny for bribing public officials?

Many companies (or at least their senior employees) continue to believe it is necessary to pay bribes (or to use agents who have the right contacts at the right price) in order to compete, especially in emerging markets such as China, as discussed in the previous section. As a result, many of the recent high-profile investigations by US regulators have touched these markets. In addition to overseas regulators signalling their intentions to clamp down hard on corruption, the PRC regulators have also been active. The regulatory framework around bribing of public officials in China has been in place since entering the WTO, however, actions taken by PRC authorities have focused mainly on the recipients of bribery as can be seen in a recent case involving BNP Paribas where a high ranking official in the PRC Ministry of Finance was jailed for taking bribes.

While many companies have taken steps to create the right global anti-corruption policies, too few have put the right processes and controls in place to prevent corruption occurring. There remains significant opportunity within some global organisations to engage in bribery (e.g. via ‘consulting’ payments or benefits in kind), incentive (to win new business) and ability to rationalise (it’s ‘market practice’) also remain high.

3. How much are fraud losses in the supply chain and through revenue leakage costing our business?

We continue to be surprised by how few organisations understand what fraud is actually costing their businesses. Too few retailers have reliable data on stock shrinkage. It remains relatively rare for businesses to have a proper understanding of the fraud risks within their procurement process or to have designed controls to address these risks.

Fraud losses will continue to run at high levels in 2009. Some commentators put the estimate of losses from fraud at 7% of revenue12. We consider this figure to be high as an estimate of the impact on fraud on businesses in general, but we recognise that some companies will experience significant frauds that result in losses at this level. We see continuing opportunity for significant fraud losses as many organisations continue to underestimate avoidable fraud losses and fail to develop adequate controls.

12 Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse

12 Fraud in a downturn

4. How well do we know the people we do business with?

More and more, organisations are being held accountable for the actions of the parties they contract with. Regulators are prosecuting companies and their directors and officers for the inappropriate actions of business partners such as distributors and sales agents. Companies cannot simply ignore the actions of business partners, who may be willing to pay bribes in order to achieve sales, but many still do. As discussed in the previous section, this can be a particular problem in China, where many businesses may regard these kinds of payments as a cultural norm.

Risks lie not just in the sales channel but also in the supply chain. Organisations in many industries have suffered reputational damage due to fraudulently concealed unethical practices arising in the supply chain including through:

• theuseofchildlabourbysubcontractors• thefailureofsubcontractorstoproperlyvet employees working with children and in other sensitive industries• subcontractorssourcingmaterialsfrom inappropriate sources

• non-compliancewithlabourlaws,especiallyin China with the introduction of the new labour law in 2008• financialfailuresorpressuresimpactingonthe partners’ abilities to perform• undisclosedrelatedpartytransactions

Some organisations are beginning to address these risks and are using Corporate Intelligence techniques to conduct integrity due diligence on business partners, but others are not. We see continuing high levels of opportunity for this type of fraud. Many organisations face significant reputational risk from inadequate due diligence and monitoring controls in relation to business partners in the sales channel and supply chain in 2009.

Fraud in a downturn 13

5. Is the organisation at risk of a significant data theft?

In the past, discussions around fraud, integrity and asset losses have tended to focus on cash, tangible assets (e.g. stock/inventory) and financial securities. Nowadays, people are more and more concerned with their data leakage and theft. In 2008, the leakage of personal data of 40,000 pregnant women in Shenzhen was widely reported.

To date, most serious losses of personal data appear to be the result of mishap, not serious fraud or misconduct, although there have been some exceptions. Criminal organisations have for some time recognised the value of personal data and, while bank account details continue to have a black market value, there will be a significant risk of theft.

We see the principal threat arising from the opportunity resulting from the inadequacy of control. In our experience, many organisations have begun to put arrangements in place to improve data security. However, not enough is being done to address the risk of deliberate theft by criminal organisations working in collusion with permanent, short term or temporary staff to infiltrate organisations and circumvent existing control systems.

6. How robust are the controls in our treasury and banking operations?

We tend to think of rogue traders as a threat faced only by investment banks. In fact, many organisations use hedging strategies in their treasury function or trade in energy or other commodities. The losses reported by Société Générale in 2008 were, perhaps, an early warning of impact of a declining economy on the heightened risk of fraud and irregularity. As in so many cases, it appears that problems escalated as Jerome Kerviel, the trader at the centre of the case, contrived to trade beyond his authority level. In China, while the state owned banks may be unwilling to enter into more risky hedging strategies, there is a system of underground lending in the private equity sector which is poorly regulated13.Many rating and loan guarantee companies also operate in an opaque and unprofessional way, and there is a general lack of industry standards in this area14.

In 2009 we see increased opportunity for rogue traders to operate undetected as control environments weaken. There are also significant influences that will provide pressures or incentives for some staff to trade beyond the limit of their authority and rationalise their actions.

13 Squeezed Middlemen; Chinese loan guarantors were key to the rise of small and medium-size businesses—until they got overextended, Forbes, 2009 14 China urged to revamp rating, credit guarantee system, Industry Updates, China Daily, 3 March 2009

14 Fraud in a downturn

In addition, as companies sail ever closer to banking covenant breaches, the temptation to ‘massage the numbers’ provided to its banks (even if only designed to ‘tide us over for couple more months before that new contract is renewed’) will increase.

Asset based lending has allowed companies to obtain debt finance while enabling lenders to secure lending against specified company assets. The range of assets against which debt can be secured ranges from the more traditional (stock/inventory, debtors, property, plant and equipment) through to the more unusual such as intellectual property assets (trademarks, patents, franchise and design rights). As credit becomes ever harder to obtain, we see a significant increase in the incentives and pressures of borrowers who are facing difficult trading conditions to commit frauds and also the ability of at least some borrowers to rationalise their actions. We also see the pressures on the asset based lenders to control their own costs which then restrict the resources they can apply to counter this threat.

7. Are we at risk of breaching competition laws?

In China, the new Anti-Monopoly Law took effect on August 1, 2008 after more than 10 years of drafting. It covers monopolistic agreements among business operators, abuse of dominant market positions by business operators, and concentration of business operators that may eliminate or restrict competition. It also provides significant penalties and remedies in the event of violations, which in some cases could be up to 10% of the sales revenue from the previous year.

The introduction of this new legislation further increases the regulatory challenges facing companies in China, and may require companies to be pro-active in managing compliance to minimize the risk of associated financial or reputational damage.

Fraud in a downturn 15

8. Are we putting the organisation at risk through the way we recruit?

We anticipate that the number of people providing misleading information in order to obtain employment will rise as competition for jobs becomes more intense, especially in China where competition for the top jobs is fierce, and even high calibre university graduates are struggling to find jobs due to a surge in university admissions over the past few years15. Providing false qualifications or references, withholding information that may be detrimental to an application including hiding criminal convictions are common examples of the lengths that some people are willing to go to in order to obtain employment.

The economic decline will, for some individuals, increase their motivation and ability to rationalise this type of fraud. We also foresee increasing opportunity for recruitment fraud: as back office headcount is reduced, resources currently being devoted to pre-employment screening may be cut back.

Which industries could be affected the most? Unlike in previous recessions, this downturn appears to be hitting the services sector as hard as manufacturing, or even harder. Service providers including banks, law firms and accountants all face increased threat levels.

In addition, In China, the new Labour Law which took effect on January 1, 2008 could make it increasingly difficult to dismiss staff, especially where concerns of inappropriate behaviour exist but can not be clearly proven.

9. How reliable is the non-financial data we provide to our stakeholders and regulators?

We have seen numerous instances of ‘non-financial’ fraud in recent years, involving the deliberate misrepresentation of disclosed information, such as non-financial performance data. The recent milk scandal in China, where protein levels of infant milk were inflated by using the industrial chemical melamine, demonstrates the risk in this area.

We see the principal threat of this type of fraud arising from the ability of some organisations and particular employees to rationalise the misstatement of non-financial data – often this type of behaviour is considered as harmless poetic license to achieve a particular objective, rather than the fraud on taxpayers or service users that it often amounts to.

15 The Economist, 11 April 2009: Where will the students go?

16 Fraud in a downturn

10. If a crisis occurred, how well prepared are we to react?

We expect both the foreign and domestic regulators to continue their adoption of a more pro-active approach to the detection and investigation of fraud and regulatory breaches in 2009. Companies are now expected to report, at an early stage, if a regulatory breach, fraud or corruption is identified.

Companies will need to be ‘investigation ready’, i.e. they will need to have policies in place regarding the conduct of investigations and will be expected to know where data is stored and how it can be speedily retrieved.

As well as criminal prosecutions, regulators are making more use of their ability to seek civil penalties in order to dispose of some cases. In seeking to resolve investigations in this way, regulators will take into account:

• therigourwithwhichanorganisationreactedto an alleged incident including the thoroughness and independence of any internal investigation;• thequalityandcomprehensivenessofthe organisation’s controls; and • thecooperationaffordedthembythecompany.

11. Do we have adequate directors and officers (D&O) insurance?

Notwithstanding the best internal controls, compliance programmes and ‘fire-drills’, it is sensible to ensure that every company carries sufficient D&O insurance to protect its officers and directors in the event of inward litigation and claims. Any exposure of the company to North America, especially via a US listing, significantly increases the risks of class action litigation whilst US regulatory investigations by the SEC or DOJ tend to be quite memorable for all the wrong reasons!

Prudent boards and audit committees will want to ensure via their broker that they have adequate insurance coverage.

Fraud in a downturn 17

18 Fraud in a downturn

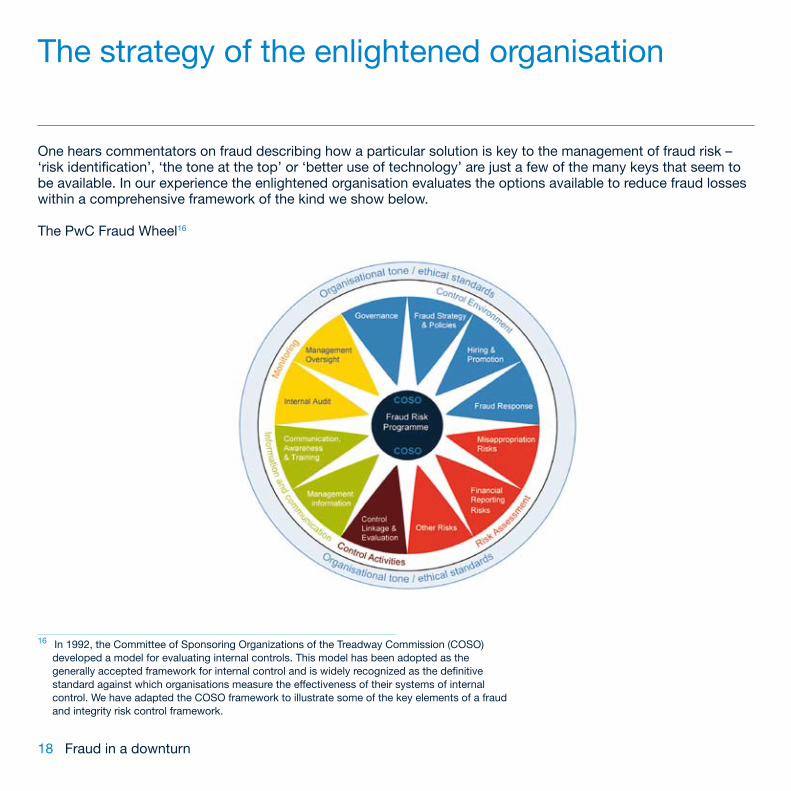

One hears commentators on fraud describing how a particular solution is key to the management of fraud risk – ‘risk identification’, ‘the tone at the top’ or ‘better use of technology’ are just a few of the many keys that seem to be available. In our experience the enlightened organisation evaluates the options available to reduce fraud losses within a comprehensive framework of the kind we show below.

The PwC Fraud Wheel16

The strategy of the enlightened organisation

16 In 1992, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) developed a model for evaluating internal controls. This model has been adopted as the generally accepted framework for internal control and is widely recognized as the definitive standard against which organisations measure the effectiveness of their systems of internal control. We have adapted the COSO framework to illustrate some of the key elements of a fraud and integrity risk control framework.

Fraud in a downturn 19

Each organisation must determine how best to implement a fraud and integrity risk strategy. We set out below some of the questions those charged with governance need to ask, and receive answers to, in order to obtain some comfort that a sound strategy is in place:

• Organisational tone – what steps are being taken to be certain that the right tone at the top permeates down through the organisation? Does our remuneration strategy, including bonus arrangements, support the organisation’s ethical stance, or undermine it?

•Governance – are we receiving sufficient information and asking enough questions to have a sound strategic oversight of fraud risks, losses and prevention programmes. What are we doing personally to promote an anti-fraud culture?

•Fraud and integrity policies – do we have the right policies and practices in place (code of conduct, fraud policy, whistle-blowing, conflicts of interest, fraud response) and, more importantly, are they adequately publicised, promoted and enforced?

•Hiring and promotion – how much do we know about the people we recruit or promote to positions of responsibility? Is there anything else we should know before we bring them in or promote them?

•Risk assessment – what are the key fraud and integrity risks? Who is making this assessment and what information is the assessment based on? Has anyone thought through the fraud and integrity risks arising from the people we do business with, i.e. our sales agents, distributors, joint venture partners and supply chain?

•Control linkage and evaluation – is the control system designed principally to identify errors or is it sufficiently robust to prevent or detect fraud, corruption or other misconduct risks? Are we using best practice unpredictable controls, including spot checks and data mining to help both detect and deter potential fraudsters? Do we have a reliable, trusted whistle blowing programme (it is an essential anti-fraud and corruption control)?

•Management information – do our middle and senior management have the information they need to manage fraud and integrity risks? A sound information system will include reliable fraud loss reporting as well as data on ongoing internal investigations and whistle blowing activity.

•Communication and training – do our people receive proper communication and training? Are operational and finance staff an effective first line of defence against fraud and integrity risks? Have staff been trained to identify fraud and integrity risks in their business areas and to develop preventative and detective controls that really work?

20 Fraud in a downturn

•Management oversight – do senior management monitor fraud, corruption and other integrity based threats and take action where needed? Senior management should monitor compliance with key policies and the delivery of training programmes around business ethics.

•Gatekeeper functions – are teams working together in the right way to reduce fraud, corruption and other integrity risks? Are gatekeeper functions such as loss prevention teams, in-house legal, security, internal audit and the compliance function working together to deliver an effective fraud and integrity risk strategy?

•Fraud and corruption response – how well do we deal with allegations of fraud and corruption, when they arise? Are we conducting thorough, independent investigations and taking action where appropriate? How do we ensure that lessons learned from the investigation are implemented across the company, and not only in the area affected by the fraud?

The strategy of the enlightened organisation (Cont.)

Fraud in a downturn 2121 Fraud in a downturn

22 Fraud in a downturn

The economic downturn is changing the nature and scale of fraud and integrity risks that organisations face. The speed of change is such that opportunities to commit fraud will be prevalent. More people will feel real pressure to ‘cross the line’ or to look the other way while others do so. In addition, the falling economic tide will expose more frauds that have been ongoing whilst economic conditions were good. Although there are many competing priorities for those charged with governance to consider, in our view Boards of Directors would be wise to reflect carefully on the changing landscape of fraud and other integrity risks.

A number of risks in the current business environment in China expose businesses with Chinese operations to a heightened risk of fraud. Boards and senior management need to additionally consider business structures and cultural factors when developing a comprehensive anti–fraud program. These inherent risks in the business environment are likely to have an even higher impact as companies are hit by decreasing exports, cost pressures and supply problems.

It is for those charged with governance to take the lead on fraud and integrity issues. Employees look to the Board and senior management to set the tone and unless the senior commitment is there, change will not happen and the benefits of reducing fraud and other integrity risks will not be realised.

The good news is that effective fraud risk management more than pays for itself. Companies across industry sectors are desperate to find ways to reduce cost. Attacking fraud, waste and abuse offers a huge cost savings opportunity for a relatively low investment.

The challenge organisations face is that there is no single ‘key’ to stopping fraud. Organisations need to develop a strategy that enables the deployment of appropriate measures to manage this increasing risk. The strategy needs to be owned by those charged with governance, otherwise it will not succeed, and needs to involve people from across the organisation. Most large organisations have mature legal, compliance and internal audit functions. But these are one step removed from where the fraud and misconduct occur. Front line operations and finance personnel need to become effective first and second lines of defence.

Conclusion

Fraud in a downturn 23

About PwC fraud risk specialists

PwC China and Hong Kong fraud risk specialists play a lead role in the lifecycle of fraud and other avoidable losses, providing fraud control consulting services, reactive investigative services and proactive remedial and compliance services to clients.

Our international network comprises partners and staff who specialise in areas such as investigations, fraud risk management, avoidable loss identification & mitigation, cost control, anti-money laundering, anti-bribery & corruption and corporate intelligence. The fraud risk specialists are supported by a team of forensic technologists who provide data mining and electronic discovery type services.

Contacts

China and Hong Kong

John Donker is a partner in PwC Forensic Services and leads the PwC Forensic Services practice in Hong Kong and China. His work involves providing advice to clients and their legal advisors involved in dispute or potential dispute situations and carrying out forensic fact finding investigations.

Tel: +852 2289 2411E-mail: [email protected]

Jean Roux is the partner responsible for PwC Forensic Services in Shanghai and has specialized in forensic investigations since 1987. He has been involved in numerous investigations covering a wide variety of industries including financial services, retail, manufacturing and public sector organizations. More than 40 of these cases have proceeded to either court or formal disciplinary tribunals where he has given evidence.

Tel: +86 (21) 2323 3988E-mail: [email protected]

Brian Cheung is the partner responsible for PwC Forensic Services in Beijing. Brian has over 20 years’ professional accounting and advisory experience in China, Hong Kong and Canada. Brian has extensive experience in investigating fraud and asset misappropriation in China and providing advisory services to clients in relation to business disputes and debt recovery in China.

Tel: +86 (10) 6533 2228E-mail: [email protected]

This is printed on Magno Satin which is made from totally chlorine free process and fibre from well managed forestry with 20% pre-consumer waste. Magno Satin is ISO 14001 and EMAS certified.

www.managinginadownturn.comThis publication has been prepared by PricewaterhouseCoopers for general guidance on matters of interest only, and is not intended to provide specific advice on any matter, nor is it intended to be comprehensive. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers firms do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. If specific advice is required, or if you wish to receive further information on any matters referred to in this publication, please speak with your usual contact at PricewaterhouseCoopers or those listed in this publication.

© 2009 PricewaterhouseCoopers. All rights reserved. PricewaterhouseCoopers refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

Contacts (Cont.)

Brian McGinley is an Associate Director in PwC Forensic Services in Beijing. He has been with PwC Forensic Services since 1998 and has a depth of experience in a range of financial investigations and commercial disputes. His investigations experience includes investigations into management and employee fraud, procurement fraud, asset misappropriation, ponzi schemes, financial statement fraud and investigations into alleged breaches of the United States Foreign Corrupt Practices Act.

Tel: +86 (10) 6533 7363E-mail: [email protected]

Duncan Fitzgerald is a partner in our Systems and Process Assurance practice and is responsible for our Internal Audit and Corporate Governance practice in Hong Kong and China. He is also responsible for coordinating our Internal Audit Services in Asia. Duncan spends the majority of his time working with clients in Hong Kong on internal control, fraud control and risk management related issues.

Tel: +852 2289 1190E-mail: [email protected]

Philip Lau is a partner in our Systems and Process Assurance practice and is responsible for our Internal Control related services in Beijing and North China. He spends a significant amount of time helping clients address IT internal control related concerns together with China listing internal control requirements. Philip’s clients include both local and multinational clients.

Tel: +86 (10) 6533 2118E-mail: [email protected]

Jasper Xu is a partner in our Systems and Process Assurance practice and is based in Shanghai. He is responsible for our Internal Audit services in Central China and works with both local and multinational clients (MNCs). Jasper focusses on Internal Audit outsourcing, particularly for MNCs addressing their China related risks (including fraud control risks).

Tel: +86 (21) 2323 3405E-mail: [email protected]

Cimi Leung is a partner in our Systems and Process Assurance practice and is responsible for our services in Southern China. Cimi has significantly developed our practice in the last 2 years and has teams dedicated to providing Internal Audit and Corporate Governance, Internal Control listing compliance and IT internal control services.

Tel: +86 (20) 3819 2997E-mail: [email protected]

John Tracey is a partner in PwC Forensic Services in the UK. He specialises in the investigation of complex fraud, corruption and other integrity issues. John leads PwC’s Fraud Risks and Controls practice in the UK, advising clients on how best to manage fraud and integrity risks.

Tel: +44 121 265 5783E-mail: [email protected]

Related Documents