A Real Intertemporal Model with Investment Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 1 / 30

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A Real Intertemporal Model with Investment

Economics 3307 - Intermediate Macroeconomics

Aaron Hedlund

Baylor University

Fall 2013

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 1 / 30

Introduction

We have looked at static models with production but no savings, andwe have looked at dynamic models with savings but no production.

Now we construct a dynamic model with production to studyinvestment, business cycles, fiscal/monetary policy, etc.

Three economic actors:1 A representative consumer makes consumption/savings decisions and

supplies its labor.

2 A representative firm hires labor and makes production andinvestment decisions.

3 The government engages in government spending using tax revenuesand borrowed funds.

Three markets: labor market, credit market, goods market.

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 2 / 30

The Representative Consumer

The consumer’s budget constraints are given by

C1 + Sp1 = w1(h − l1) + π1 − T1

C2 = w2(h − l2) + π2 − T2 + (1 + r)Sp1

The intertemporal budget constraint is

C1 +C2

1 + r= w1(h − l1) + π1 − T1 +

w2(h − l2) + π2 − T2

1 + r

Consumers solve

maxC1,l1,C2,l2

u(C1, l1) + βu(C2, l2)

subject to

C1 +C2

1 + r= w1(h − l1) + π1 − T1 +

w2(h − l2) + π2 − T2

1 + r

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 3 / 30

The Representative Consumer

Optimality conditions:

Within-period decisions:

{ul (C1,l1)uC (C1,l1) = MRSC1,l1 = w1

ul (C2,l2)uC (C2,l2) = MRSC2,l2 = w2

Intertemporal decisions:uC (C1, l1)

βuC (C2, l2)= MRSC1,C2 = 1 + r

C1 +C2

1 + r= w1(h − l1) + π1 − T1 +

w2(h − l2) + π2 − T2

1 + r

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 4 / 30

Current Labor Supply

Factors affecting current labor supply, Ns1 = h − l1:

1 The current real wage: We will assume that the substitution effectdominates, i.e. ↑ w1 ⇒↓ l1 ⇔↑ Ns

1 .

2 The real interest rate: Intertemporal substitution of leisure just asfor consumption. Note that our existing solution conditions imply

ul(C1, l1)

βul(C2, l2)= MRSl1,l2 =

w1(1 + r)

w2

We will assume that the substitution effect dominates, i.e.↑ r ⇒↓ l1 ⇔↑ Ns

1 . Note that higher future wages ↑ w2 ⇒↑ l1 ⇔↓ Ns1 .

3 Lifetime wealth: Consumption and leisure are normal goods, so higherlifetime wealth (↑ π, ↓ T , etc.) causes reduced labor supply.

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 5 / 30

Labor Supply

NS(rL) NS(rH) NS (r)

NS (r) H L

Higher real interest rates increase labor supply (left) while higherlifetime wealth decreases labor supply (right).

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 6 / 30

Consumption Demand

Cd(r)

Cd(rH )

Cd(rL ) Slope = MPC

The marginal propensity to consume measures how muchconsumption increases when aggregate income Y increases by 1.

Higher real interest rates reduce current consumption (right).

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 7 / 30

The Representative Firm

Output Y1 = z1F (K1,N1) and Y2 = z2F (K2,N2).

The firm invests some of its output in capital accumulation:

K2 = (1− d)K1 + I1

Profits π1 = Y1 − w1N1 − I1 and π2 = Y2 − w2N2 + (1− d)K2.

The representative consumer owns the firm and receives profits asdividend income.

The firm maximizes the present value of dividend income,V = π1 + π2

1+r .

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 8 / 30

The Representative Firm

The firm solves

maxN1,I1,N2

z1F (K1,N1)− w1N1 − I1

+z2F (

K2︷ ︸︸ ︷(1− d)K1 + I1,N2)− w2N2 + (1− d)

K2︷ ︸︸ ︷[(1− d)K1 + I1]

1 + r

Optimality conditions:

Within-period decisions:

{z1FN(K1,N1) = MPN(K1,N1) = w1

z2FN(K2,N2) = MPN(K2,N2) = w2

Investment decision: z2FK (K2,N2)︸ ︷︷ ︸MPK (K2,N2)

−d = r

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 9 / 30

Optimal Investment Schedule

r =

Re

al In

tere

st R

ate

r =

Re

al In

tere

st R

ate

I1 = Investment in New Capital I1 = Investment in New Capital

rL

I1 H

z2FK(K2,N2) – d

rH

I1 L

z2FK(K2,N2) – d

H

z2FK(K2,N2) – d

L

Diminishing MPN and MPK ⇒ downward sloping I d and Nd .

Higher expected TFP or lower current capital cause increased I d .

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 10 / 30

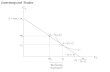

Investment and Credit Market Imperfections

Suppose the borrowing interest rate is r + x , where the spread x is thedefault premium from limited commitment/asymmetric information.

Firms that borrow choose investment to satisfy

z2FK (K2,N2)− d = r + x ⇔ r = z2FK (K2,N2)− d − x

r =

Re

al In

tere

st R

ate

I1 = Investment in New Capital

z2FK(K2,N2) – d – xL

z2FK(K2,N2) – d – xH

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 11 / 30

Investment and the Interest Rate Spread

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 12 / 30

Investment and the Interest Rate Spread

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 13 / 30

Competitive Equilibrium

A competitive equilibrium is prices r , w1, w2; household allocationsC1, Ns

1 , C2, Ns2 ; firm allocations K1, Nd

1 , I1, Nd2 ; and allocations for

the government G1, G2, T1, T2 such that:1 C1, Ns

1 , C2, and Ns2 solve the household’s optimization problem.

2 Nd1 , I1, and Nd

2 maximize discounted profits V = π1 + π2

1+r , given K1.

3 The government’s budget constraint is satisfied: G1 + G2

1+r = T1 + T2

1+r .

4 Labor market clearing: Nd1 = Ns

1 and Nd2 = Ns

2 .

5 Credit market clearing: Sp1 + Sg

1 = 0⇔ Sp1 = B1 where

Sp1 = w1N

s1 + π1 − T1 − C1 and B1 = −Sg

1 = G1 − T1.

6 Goods market clearing: C1 + I1 + G1 = z1F (K1,Nd1 ) and

C2 + G2 = z2F (K2,Nd2 ) + (1− d)K2 where K2 = (1− d)K1 + I1.

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 14 / 30

Walras’ Law

Walras’ law states that we have a redundant market clearingcondition, i.e. (1) – (3) + any two of (4) – (6) automatically implythe third market clearing condition.

Here we show (1) – (3), (4), and (6) ⇒ (5). From (6) and (2),

C1 + I1 + G1 = z1F (K1,Nd1 )⇒ C1 = z1F (K1,N

d1 )− I1 − G1

⇒ C1 = w1Nd1 + z1F (K1,N

d1 )− w1N

d1 − I1︸ ︷︷ ︸

π1

−G1

Using Ns1 = Nd

1 from (4), the household budget constraint from (1),and B1 = G1 − T1 from (3) gives

C1 = w1Ns1 + π1 − (B1 + T1)⇒ B1 = w1N

s1 + π1 − T1 − C1︸ ︷︷ ︸

Sp1

⇒ B1 = Sp1

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 15 / 30

Equilibrium Conditions

Household optimality:

Within-period decisions:

ul (C1,h−Ns

1 )

uC (C1,h−Ns1 )

= w1

ul (C2,h−Ns2 )

uC (C2,h−Ns2 )

= w2

Intertemporal decisions:uC (C1, h − Ns

1 )

βuC (C2, h − Ns2 )

= 1 + r

C1 +C2

1 + r= w1N

s1 + π1 − T1 +

w2Ns2 + π2 − T2

1 + r

Profit maximization:

Within-period decisions:

{z1FN(K1,N

d1 ) = w1

z2FN(K2,Nd2 ) = w2

Investment decision: z2FK (K2,Nd2 ) − d = r

Government budget constraint: G1 + G21+r

= T1 + T21+r

.

Market clearing: Nd1 = Ns

1 and Nd2 = Ns

2 (labor); C1 + I1 + G1 = z1F (K1,Nd1 ) and

C2 + G2 = z2F (K2,Nd2 ) + (1 − d)K2 (goods).

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 16 / 30

Labor Market Clearing and Output Supply

Higher r causes Ns1(w1; r) to shift right. Market clearing N1 increases,

causing higher Y1 = z1F (K1,N1). Thus, Y s1 (r) is upward-sloping.

N1

N1

Y1

w1 N1(w1)

d

w1 L

w1 H

N1 L N1 H

N1 L

N1 H

Y1 H

Y1 L

Y1 (r) s

rL

rH

Y1 L Y1

H

r

Y1

N1(w1 ; rL) s

N1(w1 ; rH) s

Y1 = z1F(K1 ,N1)

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 17 / 30

Goods Market Clearing and Output Demand

Higher r reduces the demand for goods because of lower C1(Y1; r)and I1(r). Thus, the goods market clearing Y1 decreases.

Output demand curve Y d1 (r) is downward-sloping.

De

man

d f

or

Per

iod

1 G

oo

ds

r =

Re

al In

tere

st R

ate

Y1 = Period 1 Income Y1 = Period 1 Income

Y1 (r) d

Y1 H

Y1 L

C1(Y1 ; rH) + I1(rH) + G1

C1(Y1 ; rL) + I1(rL) + G1

rH

rL

Y1 H

Y1 L

Y1 H

Y1 L

45° line

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 18 / 30

Equilibrium

w

1 =

Pe

rio

d 1

Re

al W

age

r =

Re

al In

tere

st R

ate

N1 = Period 1 Employment Y1 = Period 1 Output

r

Y1 (r) d

N1(w1 ;r) s

N1 Y1

w1

Y1(r) s N1(w1)

d

By construction, Nd1 = Ns

1 everywhere on Y s1 and C1 + I1 + G1 = Y1

everywhere on Y d1 .

Thus, all markets clear when r adjusts to cause Y s1 (r) = Y d

1 (r).

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 19 / 30

Effects of Higher Government Spending – Output Demand

Higher G1 ⇒ higher T1 and/or T2. Suppose Y1 ⇒ Y1 + ∆Y .

Net change in household disposable income ∆Y −∆T = ∆Y −∆G .

C1(Y1; r) + MPC (∆Y −∆G )︸ ︷︷ ︸C1(Y1+∆Y−∆G ;r)

+I1(r) + G1 + ∆G = Y1 + ∆Y ⇒ ∆Y = ∆G

De

man

d f

or

Per

iod

1 G

oo

ds

r =

Re

al In

tere

st R

ate

Y1 = Period 1 Income Y1 = Period 1 Income

Y1 (r) d

Y1 Y1 + ΔY

C1(Y1 ; r) + I1(r) + G1

C1(Y1 ; r) + MPC(ΔY – ΔG) + I1(r) + G1 + ΔG

Y1

45° line

Y1 + ΔY

Y1 (r) = Y1 (r) + ΔG d ~ d

C1(Y1 + ΔY – ΔG; r)

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 20 / 30

Effects of Higher Government Spending – Output Supply

The negative wealth effect of ∆T causes Ns1 to shift to the right.

N1

N1

Y1

w1 N1(w1)

d

w1

N1

N1

Y1

Y1 (r) s

r

Y1

r

Y1

N1(w1 ; r) s

Y1 = z1F(K1 ,N1)

Y1 ~

N1 ~

N1 ~

Y1 ~

w1 ~

N1(w1 ; r) s ~

Y1 (r) s ~

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 21 / 30

Effects of Higher Government Spending – Equilibrium

w1 =

Pe

rio

d 1

Re

al W

age

r =

Re

al In

tere

st R

ate

N1 = Period 1 Employment Y1 = Period 1 Output

r

Y1 (r) d

N1(w1 ;r) s

N1 Y1

w1

Y1(r) s N1(w1)

d

Y1 (r) s ~

Y1 (r) = Y1 (r) + ΔG d ~ d

Y1 + ΔG

N1(w1 ;r) s ~

N1(w1 ;r ) s ~ ~

w1 ~

r ~

Y1 ~ N1

~

Small negative wealth effect on Ns1 ⇒ small relative increase in Y s

1 .

Output Y1 increases, but ∆Y < ∆G because higher r crowds out C1

and I1. Summary: ↑ r , ↑ Y1, ↓ C1, ↓ I1, ↑ N1.

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 22 / 30

Effects of Lower Initial Capital – Output Demand

Lower K1 increases MPK next period, z2FK ((1− d)K1 + I1,N2) ↑.

Firms increase I1, driving MPK back down until MPK − d = r . Thus,Y d

1 shifts to the right.

De

man

d f

or

Per

iod

1 G

oo

ds

r =

Re

al In

tere

st R

ate

Y1 = Period 1 Income Y1 = Period 1 Income

Y1 (r) d

Y1

C1(Y1 ; r) + I1(r) + G1

C1(Y1 ; r) + I1(r) + G1

Y1

45° line

Y1 (r) d ~

~

Y1 ~

Y1 ~

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 23 / 30

Effects of Lower Initial Capital – Output Supply

Lower K1 decreases MPN this period, z1FN(K1,N1) ↑.

Labor demand Nd1 shifts to the left, causing Y s

1 to shift to the left.

N1

N1

Y1

w1

N1(w1) d

w1

N1

N1

Y1

Y1 (r) s

r

Y1

r

Y1

N1(w1 ; r) s

Y1 = z1F(K1 ,N1)

Y1 ~

N1 ~

N1 ~

Y1 ~

w1 ~

Y1 (r) s ~

N1(w1) d ~

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 24 / 30

Equilibrium Effects of Lower Initial Capital: Case 1

w1 =

Pe

rio

d 1

Re

al W

age

r =

Re

al In

tere

st R

ate

N1 = Period 1 Employment Y1 = Period 1 Output

r

Y1 (r) d

N1(w1 ;r) s

N1 Y1

w1

N1(w1) d

Y1 (r) s

Y1(r) s ~

Y1 (r) d ~

r ~

Y1 ~

N1(w1 ;r ) s ~ N1(w1)

d ~

N1 ~

w1 ~

Summary: ↑ r , ↑ I1, ambiguous Y1, N1, and C1.

Labor supply shifts to the right in the new equilibrium because of thehigher interest rate, i.e. Ns

1(w1; r̃) > Ns1(w1; r).

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 25 / 30

Equilibrium Effects of Lower Initial Capital: Case 2

w1 =

Pe

rio

d 1

Re

al W

age

r =

Re

al In

tere

st R

ate

N1 = Period 1 Employment Y1 = Period 1 Output

r

Y1 (r) d

N1(w1 ;r) s

N1 Y1

w1

N1(w1) d

Y1 (r) s Y1(r)

s ~

Y1 (r) d ~

r ~

Y1 ~

N1(w1 ;r ) s ~

N1(w1) d ~

N1 ~

w1 ~

Output increases above because the demand effect from higherinvestment outweighs the supply effect from lower labor demand.

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 26 / 30

Effects of Higher Present TFP z1 – Output Supply

Higher z1 increases MPN this period.

Labor demand Nd1 increases, causing Y s

1 to shift to the right.

N1

N1

Y1

w1

N1(w1) d

N1

Y1 (r) s

r

Y1

r

Y1

N1(w1 ; r) s

Y1 = zLF(K1 ,N1)

Y1 ~

N1 N1 ~

N1 ~

Y1

Y1 ~

w1

w1 ~

Y1 (r) s ~

N1(w1) d

~

Y1 = zHF(K1 ,N1)

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 27 / 30

Effects of Higher Present TFP z1 – Equilibrium

w1 =

Pe

rio

d 1

Re

al W

age

r =

Re

al In

tere

st R

ate

N1 = Period 1 Employment Y1 = Period 1 Output

r

Y1 (r) d

N1(w1 ;r) s

N1 Y1

w1

N1(w1) d Y1 (r)

s

Y1(r) s ~

r ~

Y1 ~

N1(w1 ;r ) s ~

N1(w1) d ~

N1 ~

w1 ~

No effect on C1(Y1; r), I1(r), or G1, and thus no change in Y d1 .

Summary: ↓ r , ↑ Y1, ↑ C1, ↑ I1, ↑ N1. Labor supply shifts to the left,i.e. Ns

1(w1; r̃) < Ns1(w1; r).

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 28 / 30

Effects of Higher Future TFP z2 – Output Demand

Higher z2 increases MPK and MPN next period.

Firms increase I1 because of higher MPK . Also, higher MPN increasesw2, causing C1 to increase (C smoothing). Thus, Y d

1 shifts right.

De

man

d f

or

Per

iod

1 G

oo

ds

r =

Re

al In

tere

st R

ate

Y1 = Period 1 Income Y1 = Period 1 Income

Y1 (r) d

Y1

C1(Y1 ; r) + I1(r) + G1

C1(Y1 ; r) + I1(r) + G1

Y1

45° line

Y1 (r) d ~

~

Y1 ~

Y1 ~

~

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 29 / 30

Effects of Higher Future TFP z2 – Equilibrium

w1 =

Pe

rio

d 1

Re

al W

age

r =

Re

al In

tere

st R

ate

N1 = Period 1 Employment Y1 = Period 1 Output

r

Y1 (r) d

N1(w1 ;r) s

N1 Y1

w1

N1(w1) d

Y1 (r) s

Y1 (r) d ~

r ~

Y1 ~

N1(w1 ;r ) s ~

N1 ~

w1 ~

No effect on Nd1 or Ns

1 , and thus no change in Y s1 .

Summary: ↑ r , ↑ Y1, ↑ N1, ↑ I1, ambiguous C1 because higher w2 andY1 (+) and higher r (−). Labor supply shifts to the right.

Econ 3307 (Baylor University) A Real Intertemporal Model with Investment Fall 2013 30 / 30

Related Documents