1 A Premier Mid-Tier Zinc Producer Trevali Mining Corporation – Corporate Presentation TSX: TV BVL: TV | www.trevali.com | September 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

A Premier

Mid-Tier Zinc Producer

Trevali Mining Corporation – Corporate Presentation

TSX: TV BVL: TV | www.trevali.com | September 2017

Disclaimer1

21Please refer to Appendix: Disclosures for important items relating to the resource estimates and production plans.

Certain statements contained in this document, including, without limitation, those concerning the economic outlook for the mining industry, expectations regarding

metal prices and production, the potential acquisition transaction described herein (the “Transaction”) and the expected benefits thereof, the commercial

operations of certain of Trevali Mining Corporation’s (“TV”) projects, and its liquidity and capital resources and expenditures, contain certain forward-looking

statements regarding TV’s economic performance, financial condition as well as assumptions regarding normal operating conditions, cost guidance and production

guidance with respect to its operations, including pro forma operations, and assuming completion of the Transaction. Although TV believes that the expectations

reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly,

results could differ materially from those set out in the forward-looking statements as a result of, among other factors, changes in economic and market conditions,

success of business initiatives, changes in the regulatory environment and other government actions, fluctuations in metal prices and exchange rates, and

business and operational risk management. TV undertakes no obligation to update publicly or release any revisions to these forward-looking statements to reflect

events or circumstances after the date of the annual report. All subsequent written or oral forward-looking statements attributable to TV or any person acting on its

behalf are qualified by the cautionary statements herein.

Trevali's production plan at the Caribou Mine is based only on measured, indicated and inferred resources, and not mineral reserves, and does not have

demonstrated economic viability. Trevali’s production plan at the Santander Mine is based only on measured, indicated and inferred mineral resources, and not

mineral reserves, and does not have demonstrated economic viability. Production plans at the Rosh Pinah and Perkoa mines are based on both proven and

probable reserves in addition to measured, indicated and inferred resources. Mineral resources that are not mineral reserves do not have demonstrated economic

viability. Inferred mineral resources are considered too speculative geologically to have the economic considerations applied to them that would enable them to be

categorized as mineral reserves, and there is therefore no certainty that the conclusions of the production plans and Preliminary Economic Assessment (PEA) will

be realized. Additionally, where Trevali discusses exploration/expansion potential herein, any potential quantity and grade is conceptual in nature and there has

been insufficient exploration to define a mineral resource and it is uncertain if further exploration will result in the target being delineated as a mineral resource.

There can be no assurance that the Transaction will be successfully completed as it will be subject to the satisfaction of a number of conditions including, without

limitation, Trevali shareholder approval and Transaction financing.

Zinc: Demand and Supply

3

➢ Global zinc demand continues to rise (from 2-4%

per year, approx. 280,000-560,000 tonnes/year) -

driven by GDP growth, urbanization & infrastructure

development, and as a “mid-cycle” commodity with

expanding markets for consumer goods

(automobiles, appliances, etc.)

➢ Primary zinc supply is in deficit following the

closures of a number of global marquee mines

(Brunswick 12, Century and Lisheen) over that past

few years, plus production cutbacks from major

producers

➢ Consensus forecast of significantly tightening zinc

market over the next several years

➢ Benchmark zinc smelter treatment charges (“TCs”)

dropped significantly in 2016, and even further in

2017 down to approx. US$172/tonne with no

smelter price participation (0% escalators) – a drop

from approx. US$260/tonne realized price in Q4-

2016

➢ Wood Mackenzie forecasting US$1.23/lb

(US$2700/tonne) zinc long-term price

➢ Zinc smelters scaling back/curtailing refined zinc

metal production due to concentrate shortages

Global zinc inventories (LME & SHFE) are approaching an 8-year low while prices are

forecast to increase

A Premier Zinc Producer

4

● Santander zinc mine in Peru in fourth year of commercial production and has delivered

consistent, strong operational performance

● Caribou zinc mine in Canada successfully achieved commercial production in 2016

Production in

Peru and

Canada

● 2017 YTD average daily trading volume of approximately 4 million sharesStrong trading

liquidity

➢ A Global Pure-Play Zinc Producer – Strong zinc leverage with

approximately 85% of revenue derived from zinc production*

➢ Successfully brought two zinc mines into production and acquired two

additional producing zinc mines to become a Global Top-10 Zinc Producer

➢ Zinc production now to take advantage of zinc deficits now

➢ Strong organic growth potential at all projects

➢ Proven management and technical teams

Please refer to Appendix: Disclosures for important items relating to the resource estimates, PEA and production plans.*Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost

guidance.

● Completely refinanced balance sheet significantly reduces cost of capital

● Increased covenant flexibility to pursue additional growth opportunities

● Glencore a cornerstone, strategic shareholder (25.6%)

Strengthened

Position

● Recently acquired the Rosh Pinah mine in Namibia and Perkoa mine in Burkina Faso

from Glencore

● More than a 150% increase in Trevali’s forecast annual zinc production - creating a

Global Top-10 Zinc Producer

Acquired

additional zinc

mines in Africa

5

Transforms Trevali

into a Premier

Intermediate Zinc

Company

Significantly

Increases Production

Scale While

Maintaining Attractive

Margins

Enhances Cash Flow

Generation and

Maintains

Conservative Balance

Sheet

Creates Platform for

Future Growth

➢ Significantly enhances Trevali’s position as the “go-to” name for zinc exposure

➢ Increases capital markets profile with market capitalization of plus-C$1 billion

➢ Enhances asset diversification with four producing assets across global platform

➢ Maintains conservative balance sheet with strong free cash flow generation*

➢ More than doubles Trevali’s 2017E production to approx. 410* million lbs. Zn and approx. 470* million lbs. ZnEq

➢ Maintains current operating margins and attractive leverage to zinc prices

➢ Increases leverage to zinc with zinc representing about 85%* of total metal production revenue

➢ Completely refinanced balance sheet significantly reduces cost of capital and increases covenant flexibility to

pursue potential M&A opportunities

➢ Low cost debt (terms of LIBOR + 3-4% and 5-year term)

➢ Transaction more than doubles Trevali’s projected 2017E EBITDA

➢ Maintains conservative balance sheet and low debt-to-EBITDA ratio

➢ Increases scale and creates a platform to enable future growth

➢ Positions Trevali to compete for world’s best zinc / base metal assets from a position of strength

➢ Further builds on long standing strategic relationship, with Glencore becoming a cornerstone investor (25.6%) in

Trevali

➢ Addition of Glencore’s industry leading operating and management teams

Glencore African Zinc Mines Acquisition: Benefits to Trevali

Shareholders*

Attractive Transaction

Economics

➢ Transaction is expected to be accretive to existing Trevali shareholders on a projected cash flow* per share and

projected NAV* per share basis at spot prices

Source: Company data, management estimates.

Analysis shown on attributable basis using mid-point of guidance; based on spot pricing of US$1.30/lb Zn, US$1.05/lb Pb, US$2.70/lb Cu, US$1,235/oz Au, and US$17.85/oz Ag.

Perkoa reflects effective 100% interest based on current LOM.*Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost guidance.

6

603

570

463

406 405

326

263 255 244

232

174 166 163 163 156

1% 16% 19% 14% 68% 74% 11% 86% 11% 20% 7% n.a. 20% 7% 3% 20% 3% 2% 73%

Glencore Vedanta Teck Boliden Volcan Milpo MitsuiMining

ProFormaTrevali

DowaHoldings

LundinMining

Goldcorp SociedadMinera El

Brocal

Hudbay Nyrstar South32 KAZMinerals

SouthernCopper

GrupoMéxico

Trevali

2,412 1,854 1,459 726

Source: Company data, FactSet, SNL

Analysis shown on consolidated basis using 2016 actual production in million lbs; excludes MMG due to mine shutdown in 2016; excludes Hindustan Zinc due to consolidation by

Vedanta; Teck excludes refined zinc production/sales.

Zinc % of total revenue calculated based on zinc production at an assumed price of US$0.93/lb Zn for 2016 divided by total revenue; Glencore % based on industrial metals revenue.

Trevali based on attributable 2017E metrics due to expected ramp-up. Represents forward looking information (including metal/commodity price forecasts); assumes normal operating

conditions, achievement of production and cost guidance.

Trevali Moves to 8th Largest Zinc Producer Globally1

1

FY2016 Zinc % of Total Revenue (%)

FY2016 Zinc Production (mm lb)

Trevali is projected to sit in the middle of the C1

cost curve1

7

Source: Trevali data, Glencore data and management estimates

Analysis shown on attributable basis using mid-point of 2017 guidance and full year production.

Perkoa reflects effective 100% interest based on current LOM. Caribou commenced commercial production on July 1, 2016.*Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost guidance.

2016 Zinc

Production

Perkoa, Burkina Faso

➢ Producing since 2013

➢ 2017E zinc production guidance of 165-170* million payable lb

➢ 2017E total site cash cost guidance of US$95-100/tonne* milled

➢ 2017E AISC guidance of US$0.83-0.87/lb* Zinc

Rosh Pinah, Namibia

➢ Producing since 1969

➢ 2017E zinc production guidance of 80-84* million payable lb

➢ 2017E total site cash cost guidance of US$45-50/tonne* milled

➢ 2017E AISC guidance of US$0.68-0.72/lb* Zinc

Santander, Peru

➢ Producing since 2013

➢ 2017E zinc production guidance of 52-56* million payable lb

➢ 2017E total site cash cost guidance of US$35-40/tonne* milled

➢ 2017E AISC guidance of US$0.66-0.70/lb* Zinc

Caribou, Canada

➢ Producing since 2015

➢ 2017E zinc production guidance of 90-93* million payable lb

➢ 2017E total site cash cost guidance of US$55-60/tonne* milled

➢ 2017E AISC guidance of US$0.84-0.88/lb* Zinc

Caribou68 mm lb

Caribou*90-93 mm lb

Santander61 mm lb

Santander*63-65 mm lb

Rosh Pinah*80-84 mm lb

Perkoa*165-170 mm lb

129 mm lb

2016 2017E

398-412* mm lb

Production and Cost Profile*

2017E Zinc

Guidance

~215%

Trevali Capital Structure

81 Details of outstanding options and warrants can be found in the Appendix: Options and Warrants

TSX:TV | BVL(Lima):TV | US-OTCQX: TREVF

Trevali one-year share price performance

Share Capital

(as of Sept 18, 2017, C$1.41/share)

Shares issued/outstanding: 823 million

Shares fully diluted: 837 million

Market Capitalization: C$1.2 billion

Stock Options1: 11 million

Warrants1: 2.8 million

Trevali Management & Directors

9

DR. MARK CRUISE – PRESIDENT & CEO

Base metal deposit specialist with over 20-years project experience from grass-roots

exploration through resource definition to permitting and production in Europe and the

America’s on behalf of Pasminco Exploration, Anglo American and TSX-listed

companies. Geology Ph.D. on the Irish zinc-lead orefield and was a member of Anglo

American’s Lisheen Zinc-Lead Mine feasibility/technical team in Ireland. Co-founded

Trevali in 2007 to position the Company for anticipated global Zn deficits.

PAUL KELLER, P.ENG. – CHIEF OPERATING OFFICER

28 years of mine operations experience in Canada, most recently as Manager of

Technical Services for a major Canadian mining contractor where he led a team of

engineers and designers on various mining contracts for major mining companies.

Paul began his career with Rio Algom and has also worked in various management

roles with Barrick Gold's Hemlo mine in operations, engineering and maintenance.

ANNA LADD, CMA – CHIEF FINANCIAL OFFICER

Over 15 years experience in the finance and mining industry. Served as VP Finance

and CFO of Sulliden Gold, Crowflight Minerals, Kria Resources and other privately

held exploration companies, in addition to senior positions with mining companies

including Kinross Gold Corporation and has also worked in Thompson and Sudbury

operations for Vale Inco. Ms. Ladd is a Certified Public Accountant and received her

Masters of Arts in Economics from Queen's University, and a Bachelor of Commerce

degree in Finance from the University of British Columbia.

DANIEL MARINOV – VP OF EXPLORATION

Over 24 years of international experience in exploration and underground mining,

and has held senior management roles with Rio Tinto and Anglo American (including

project manager at Anglo's Michiquillay porphyry Cu-Au-Mo deposit in Peru).

STEVE STAKIW – VP CORPORATE COMMUNICATIONS

Over 25 years of geology/mining industry and research/finance market experience.

Steve has held a senior management role with a leading mining research and

investment publication and has consulted to resource-focused investment funds.

DR. MARK CRUISE, PRESIDENT, CEO & DIRECTOR

DAVID HUBERMAN, CHAIRMAN & DIRECTOR

Experienced lawyer specializing in corporate, commercial, banking, securities,

regulatory and mining law. Director of Ivanhoe Mines Ltd. (renamed Turquoise Hill

Resources) from 2003-2012 and its Chairman from 2011-2012.

CHRIS ESKDALE, DIRECTOR

Global Head Industrial Zinc for Glencore Plc.

DAN MYERSON, DIRECTOR

Manages Glencore’s Canadian zinc business and has worked closely with Trevali at

both the corporate and operations level, specifically facilitating technical support to the

Caribou operations.

MIKE HOFFMAN, DIRECTOR - OPERATIONS

Over 25 years global mine development experience including Vice President

Operations at Yamana Gold, Desert Sun and Goldcorp.

CATHERINE GIGNAC, DIRECTOR

Geologist and mining analyst with over 25 years experience at mining companies and

several global brokerage firms (UBS, RBC and Merrill Lynch Canada) as well as

independent firms (Wellington West, Loewen Ondaatje McCutcheon and Dundee).

DAVID KORBIN, DIRECTOR

Chartered Accountant and former Director of Callinan Royalties Corporation,

Turquoise Hill Resources Ltd. (formerly Ivanhoe Mines) and Ivanhoe Mines Australia.

Previous managing partner of Deloitte Touche LLC and also was a Director of

Seaspan Corporation and Chairman of it’s Audit Committee.

ANTON DRESCHER, DIRECTOR

Certified Management Accountant with extensive public company board and officer

experience.

Directors

10

Analysis shown on attributable basis using mid-point of guidance; based on spot pricing of US$1.30/lb Zn, US$1.05/lb Pb, US$2.70/lb Cu, US$1,235/oz Au, and US$17.85/oz Ag.

Perkoa reflects effective 100% interest based on current LOM.*Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost guidance.

High-Quality Diversified Assets in Mining-Friendly Jurisdictions

Rosh Pinah

(Namibia)

Perkoa

(Burkina Faso)

Caribou /

Halfmile-Stratmat

(Canada)

Santander

(Peru)

Ruttan

(Canada)

Heath Steele

(Canada)

Zinc Mines

Projects / Other Assets

2017E Attributable Production* (mm lb Zn Eq.)

Caribou128 27%

Santander85

18%Rosh Pinah

90 19%

Perkoa168 36%

Gergarub

(Namibia)

Peru

11

12

● 2,000 tonne-per-day Zinc-Lead-Silver mine and mill complex in

the Central Peruvian Polymetallic Belt

● 2016 production statistics:

▪ 89% Zinc recovery producing 61.3 million payable lbs

▪ 86% Lead recovery producing 19.3 million payable lbs

▪ 71% Silver recovery producing 813,807 payable ozs

● 2016 site cash costs of US$0.32/lb ZnEq1 (payable produced)

or US$34.17/tonne (includes mining, milling and site G&A).

Total (all in) cash cost of US$0.75/lb ZnEq1 (payable produced)

includes site costs plus smelting, refining, freight, royalty and

sustaining capex.

● 2017 metal production guidance:

▪ Zinc – 52-57 million payable pounds

▪ Lead – 12-14 million payable pounds

▪ Silver – 700,000-900,000 payable ounces

▪ Total site cash costs of US$35-40/tonne milled

● Significant exploration potential to expand current resource; all

the deposits remaining open; successful, ongoing drill program

Santander Mine, Peru

Please refer to Appendix: Disclosures for important items relating to the resource estimates and production plans.

* Mineral Reserves (Proven & Probable) included in Mineral Resources1ZnEq Payable Pounds Produced = ((Zn Payable lbs Produced x Zn Price)+(Pb Payable lbs Produced x Pb

Price)+(Cu Payable lbs Produced x Cu Price)+(Au oz Payable Produced x Au Price)+(Ag oz Payable Produced x Ag

Price))/Zn Price.

Location Peru

Ownership 100% controlled

Type of deposit Carbonate Replacement Deposit

Primary metals Zn, Pb, Ag

Processing Standard milling with flotation recovery

End product Zn and Pb-Ag concentrates

Infrastructure Underground mining operation, 2,000 tonne-per-

day processing mill, tailings facility and camp

Santander mine, mill, and infrastructure, Peru

Resource Tonnes Zn (%) Pb (%) Ag (oz/ton)

Proven &

Probable*2,540,000 4.51 0.69 1.09

Measured &

Indicated3,800,000 4.85 0.83 1.23

Inferred 12,000,000 4.22 0.23 0.56

13

1

Santander Mine Development Workings

1

New Brunswick, Canada

14

15

● 3,000 tonne-per-day Zinc-Lead-Silver mine and mill complex in

the Bathurst Mining Camp of New Brunswick, Canada

● 2016 production statistics*:

▪ 77% Zinc recovery producing 36.7 million payable lbs

▪ 58% Lead recovery producing 13.8 million payable lbs

▪ 36% Silver recovery producing 402,067 payable ozs

● 2016 site cash costs of US$0.45/lb ZnEq1 (payable produced) or

US$56.39/tonne (includes mining, milling and site G&A). Total

(all in) cash cost of US$0.92/lb ZnEq1 (payable produced)

includes site costs plus smelting, refining, freight, royalty and

sustaining capex

● 2017 production guidance:

▪ Zinc – 90-93 million payable pounds

▪ Lead – 30-32 million payable pounds

▪ Silver – 800,000-900,000 payable ounces

▪ Total site cash costs of US$55-60/tonne milled

● Deposit remains open to depth

* Declared commercial production July 1/2016

Caribou Mine - Bathurst Mining Camp, New BrunswickLocation Bathurst Mining Camp, New Brunswick

Ownership 100% controlled

Type of deposit VMS polymetallic

Primary metals Zn, Pb, Ag, Cu, Au

Processing Standard milling with flotation recovery

End product Zn, Pb-Ag and planned Cu-Au concentrates

Infrastructure 3,000 tonne-per-day underground mining

operation and processing mill

Caribou mine and milling complex, Bathurst, New BrunswickPlease refer to Appendix: Disclosures for important items relating to the resource estimates and

production plans.1ZnEq Payable Pounds Produced = ((Zn Payable lbs Produced x Zn Price)+(Pb Payable lbs

Produced x Pb Price)+(Cu Payable lbs Produced x Cu Price)+(Au oz Payable Produced x Au

Price)+(Ag oz Payable Produced x Ag Price))/Zn Price.

Resource Tonnes Zn% Cu% Pb% Ag (g/t) Au (g/t)

Measured &

Indicated7,230,000 6.99 0.43 2.93 84.4 0.9

Inferred 3,660,000 6.95 0.32 2.81 78.3 1.2

16

▪ Seven zones in the deposit and

remains open

▪ Copper feeder zones never

previously targeted

▪ Recent deep drilling encountered

massive sulphides approx. 450

metres below current defined

resource

▪ Historic deep holes encountered

significant mineralized intervals

(including DDH076 with 5.8 metres

of 8.4% Zn, 3.9% Pb, 0.3% Cu, 147

g/t Ag and 1.2 g/t Au)

Caribou Exploration Upside

Resources of Caribou Deposit

Tonnes Zn% Cu% Pb% Ag (g/t) Au (g/t)

Measured &

Indicated7,230,000 6.99 0.43 2.93 84.4 0.9

Inferred 3,660,000 6.95 0.32 2.81 78.3 1.2

Please refer to Appendix: Disclosures for important items relating to the resource estimates and production plans.

Namibia

17

18

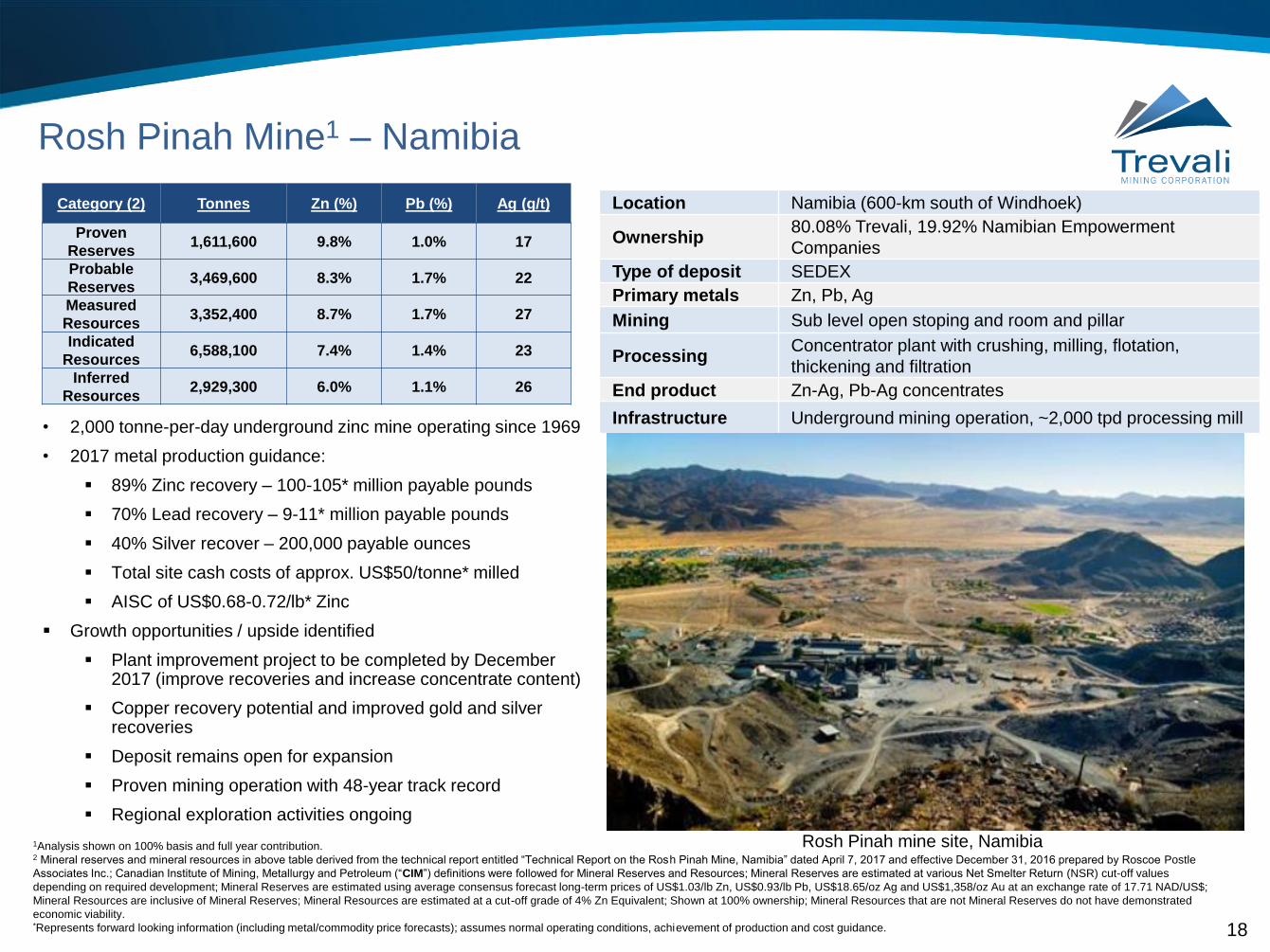

Category (2) Tonnes Zn (%) Pb (%) Ag (g/t)

Proven

Reserves1,611,600 9.8% 1.0% 17

Probable

Reserves3,469,600 8.3% 1.7% 22

Measured

Resources3,352,400 8.7% 1.7% 27

Indicated

Resources6,588,100 7.4% 1.4% 23

Inferred

Resources2,929,300 6.0% 1.1% 26

1Analysis shown on 100% basis and full year contribution. 2 Mineral reserves and mineral resources in above table derived from the technical report entitled “Technical Report on the Rosh Pinah Mine, Namibia” dated April 7, 2017 and effective December 31, 2016 prepared by Roscoe Postle

Associates Inc.; Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) definitions were followed for Mineral Reserves and Resources; Mineral Reserves are estimated at various Net Smelter Return (NSR) cut-off values

depending on required development; Mineral Reserves are estimated using average consensus forecast long-term prices of US$1.03/lb Zn, US$0.93/lb Pb, US$18.65/oz Ag and US$1,358/oz Au at an exchange rate of 17.71 NAD/US$;

Mineral Resources are inclusive of Mineral Reserves; Mineral Resources are estimated at a cut-off grade of 4% Zn Equivalent; Shown at 100% ownership; Mineral Resources that are not Mineral Reserves do not have demonstrated

economic viability.*Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost guidance.

Rosh Pinah mine site, Namibia

• 2,000 tonne-per-day underground zinc mine operating since 1969

• 2017 metal production guidance:

▪ 89% Zinc recovery – 100-105* million payable pounds

▪ 70% Lead recovery – 9-11* million payable pounds

▪ 40% Silver recover – 200,000 payable ounces

▪ Total site cash costs of approx. US$50/tonne* milled

▪ AISC of US$0.68-0.72/lb* Zinc

▪ Growth opportunities / upside identified

▪ Plant improvement project to be completed by December 2017 (improve recoveries and increase concentrate content)

▪ Copper recovery potential and improved gold and silver recoveries

▪ Deposit remains open for expansion

▪ Proven mining operation with 48-year track record

▪ Regional exploration activities ongoing

Location Namibia (600-km south of Windhoek)

Ownership80.08% Trevali, 19.92% Namibian Empowerment

Companies

Type of deposit SEDEX

Primary metals Zn, Pb, Ag

Mining Sub level open stoping and room and pillar

ProcessingConcentrator plant with crushing, milling, flotation,

thickening and filtration

End product Zn-Ag, Pb-Ag concentrates

Infrastructure Underground mining operation, ~2,000 tpd processing mill

Rosh Pinah Mine1 – Namibia

19

Rosh Pinah Exploration Potential*

*Outside of the currently delineated reserves and resources, the exploration potential quality and grade is conceptual in nature and there has been insufficient exploration to define additional

mineral resources. It is uncertain if further exploration will result in the target being delineated as a mineral resource.

Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost guidance.

▪ Located on the same underexplored belt as Skorpion, Black

Mountain and Gamsberg

▪ Limited historic exploration – discovery of Gergarub (EM target)

▪ Several quality targets remain

▪ Significant exploration potential remains on EPL2616

▪ Underground exploration activities ongoing – main mining zone –

WF3

▪ Open to the NW

Satellite image of Rosh Pinah and surrounding projects, Namibia

• Drilling from the known to the unknown and extending existing ore

lenses laterally e.g.: North of WF3.

• Low to medium potential targets exist as depth extensions of current ore

bodies, e.g. the down-plunge extensions of the AAB, S1S and WF3.

Burkina Faso

20

21

• 2,000 tonne-per-day underground zinc mine commenced

production in 2013

• 2017 metal production guidance:

▪ 92% Zinc recovery – 165-170* million payable pounds

▪ Total site cash costs of US$95-100/tonne* milled

▪ AISC of US$0.83-0.87/lb* Zinc

• Simple metallurgy – high zinc recoveries (plus-90%)

• Strong CSR receiving recognition for 2 national awards for

community development and significant contribution to

community health program

• Significant exploration potential on 4 adjacent properties /

historical gold occurrences assayed

Perkoa mine infrastructure, Burkina Faso

Location Burkina Faso

Ownership 90% Trevali, 10% Government of Burkina Faso

Type of deposit VMS

Primary metals Zn

Mining Transversal and retreat

Processing Concentrator plant with crushing, milling, flotation,

thickening and filtration

End product Zn concentrate

Infrastructure Underground mining operation, ~2,000 tpd

processing mill

Category (2) Tonnes Zn (%)

Proven Reserves 1,700,000 15.8

Probable Reserves 780,000 13.7

Measured Resources 3,040,000 15.5

Indicated Resources 1,220,000 12.4

Inferred Resources 1,640,000 12.9

1Analysis shown on 100% basis and full year contribution.2Mineral reserves and mineral resources in above table derived from the technical report entitled “Technical Report on the Perkoa Mine, Burkina Faso” dated April 7, 2017 and effective December 31, 2016 prepared by Roscoe Postle

Associates Inc.; CIM definitions were followed for Mineral Reserves and Resources; Mineral Reserves are estimated at an NSR cut-off value of $100/tonne inclusive of capital expenditure, incremental stopes greater than US$78/tonne

are included based on individual financial analysis; Mineral Reserves are estimated using an average consensus forecast zinc price of US$0.99 per pound and a €/US$ exchange rate of 1.11; Shown at 100% ownership; Mineral

Resources are inclusive of Mineral Reserves; Mineral Resources are estimated at a cut-off grade of 5% Zn; Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability).*Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost guidance.

Perkoa Mine1 – Burkina Faso

22

Perkoa Exploration Potential*

Perkoa 3D Model illustrating planned resource conversion

and expansion drilling*

Regional geophysics highlighted 46 conductors for follow-up screening

▪ Mineralization remains open at depth

▪ Drill testing in progress

▪ Regionally – 46 EM anomalies identified for follow-up

▪ Licenses never explored for base metals – gold only

*Outside of the currently delineated reserves and resources, the exploration potential quality and grade is conceptual in nature and there has been insufficient exploration to define additional

mineral resources. It is uncertain if further exploration will result in the target being delineated as a mineral resource.

Represents forward looking information (including metal/commodity price forecasts); assumes normal operating conditions, achievement of production and cost guidance.

23

Halfmile Mine - Bathurst Mining Camp, New Brunswick

Location Bathurst Mining Camp, New Brunswick

Ownership 100% controlled

Type of deposit VMS polymetallic

Primary metals Zn, Pb, Ag, Cu, Au

Processing Standard milling with flotation recovery

End product Zn, Pb-Ag and Cu-Au concentrates

Infrastructure Fully permitted and developed underground

mining operation

Resource Tonnes Zn% Pb% Cu% Ag (g/t) Au (g/t)

Indicated 6,262,043 8.13 2.58 0.22 30.8 n/a

Inferred 6,078,200 6.69 1.83 0.14 20.5 n/a

• Fully permitted underground mine with production levels in

place

• Halfmile Mine developed in 2011 with trial underground

mining/production in 2012 of over 100,000 tonnes of material

processed on a toll-basis through the Brunswick 12 Mill -

providing metallurgical/recovery data

• Produced quality, saleable concentrates (Zn, Pb-Ag and Cu-

Au) averaging:

53.7% Zn concentrate

45.8% Pb concentrate (with 680 g/t Ag)

27% Cu concentrate (with 325 g/t Ag and 2.7 g/t Au)

• Significant exploration upside beyond Upper and Lower Zones

that host current resource

• Remains open for expansion -- 3D seismic survey indicates a

large, deep reflector (Deep Zone) that returned multiple,

mineralized drill intercepts including:

5.7 m of 9.88% Zn, 2.33% Pb and 3.9 m of 9.42% Zn, 1% Pb

4.5 m of 10.61% Zn, 1.41% Pb and 0.22% Cu

6 m of 9.61% Zn, 1.93% Pb

5 m of 9.77% Zn, 3.46% Pb and 4.8 m of 7% Zn, 2.27% Pb

• PEA study underway on potential combined Halfmile-Stratmat

development plan

Source: Company data, resource is NI 43-101 compliant. Please refer to Appendix: Disclosures for important items relating to the resource estimates and production

plans.

24

• Multi-lens zinc-lead-silver-copper-gold rich volcanogenic

massive sulphide

• Near-surface sulphide body remains open for expansion

along strike and at depth

• Multi-phase 30,000-metre drill program has returned

results including: Hole RST-752 intersecting 26.75

metres grading 7.42% Zn, 1.37% Pb, 1.26% Cu, 94.2 g/t

Ag and 2.45 g/t Au

• Discovery of new multi-lens zones of copper-gold

mineralization including: Hole ST-793 intersecting 5.7

metres of 15.9% Zn, 7% Pb, 0.54% Cu and 98 g/t Ag

plus a higher-grade copper zone of 35 metres of 2.36%

Cu, both in the S-5 Lens; Hole ST-769 returned 9.2

metres of 7% Zn and 3.8% Pb in the S-1 Zone

• PEA study underway on potential combined Halfmile-

Stratmat development plan

Stratmat Deposit - Bathurst Mining Camp, New Brunswick

Source: Company data, resource is NI 43-101 compliant. Please refer to Appendix: Disclosures for important items relating to the resource estimates and production plans.

Location Bathurst Mining Camp, New Brunswick

Ownership 100% controlled

Type of deposit VMS polymetallic

Primary metals Zn, Pb, Ag, Cu, Au

Processing Potential standard milling with flotation recovery

Potential end

productPotential Zn, Pb-Ag and Cu-Au concentrates

Infrastructure In permitting stage, drill delineated deposit

Resource Tonnes Zn% Pb% Cu% Ag (g/t) Au (g/t)

Indicated 4,700,000 5.31 2.07 0.41 48.5 0.6

Inferred 2,400,000 4.76 2.07 0.70 38.8 0.4

24

25

2007➢ Trevali established to identify, acquire and develop zinc assets

➢ Acquired Santander Zinc project in Peru

2008 ➢ Discovered significant new Zn-mineralized zones at Santander

2009➢ Initial Santander resource estimate

➢ MOU agreement with Glencore to develop Santander

2010 ➢ Finalized agreement with Glencore for mine development at Santander

2011➢ Acquired Halfmile and Stratmat zinc deposits in New Brunswick

➢ Permitted and commenced development at both Santander and Halfmile mines

2012

➢ Trial mining commenced at Halfmile Mine in New Brunswick

➢ Commence construction at Santander Mine in Peru

➢ Acquired Caribou Mine and Mill in New Brunswick

2013 ➢ Commenced operations and commissioning at Santander Mine

2014

➢ Declared Commercial Production at Santander Mine

➢ Positive Preliminary Economic Assessment (PEA) study on Caribou Mine

➢ Santander Mine production exceeds 2014 guidance

2015

➢ Commenced operations and commissioning at Caribou Mine

➢ Discovered multiple new zones of high-grade Zn-Pb-Ag mineralization at Santander Mine

➢ Santander Zinc Mine production exceeds 2015 guidance

2016

➢ Declared Commercial Production at Caribou Zinc Mine

➢ Expanded new zones of high-grade Zn-Pb-Ag mineralization at Santander Mine

➢ Record annual zinc production from Santander Mine in 2016

2017➢ Invests in Caribou Mine future with new mining fleet

➢ Transformational acquisition of Perkoa and Rosh Pinah zinc mines from Glencore

Appendix: Trevali - Track Record of Successful Execution

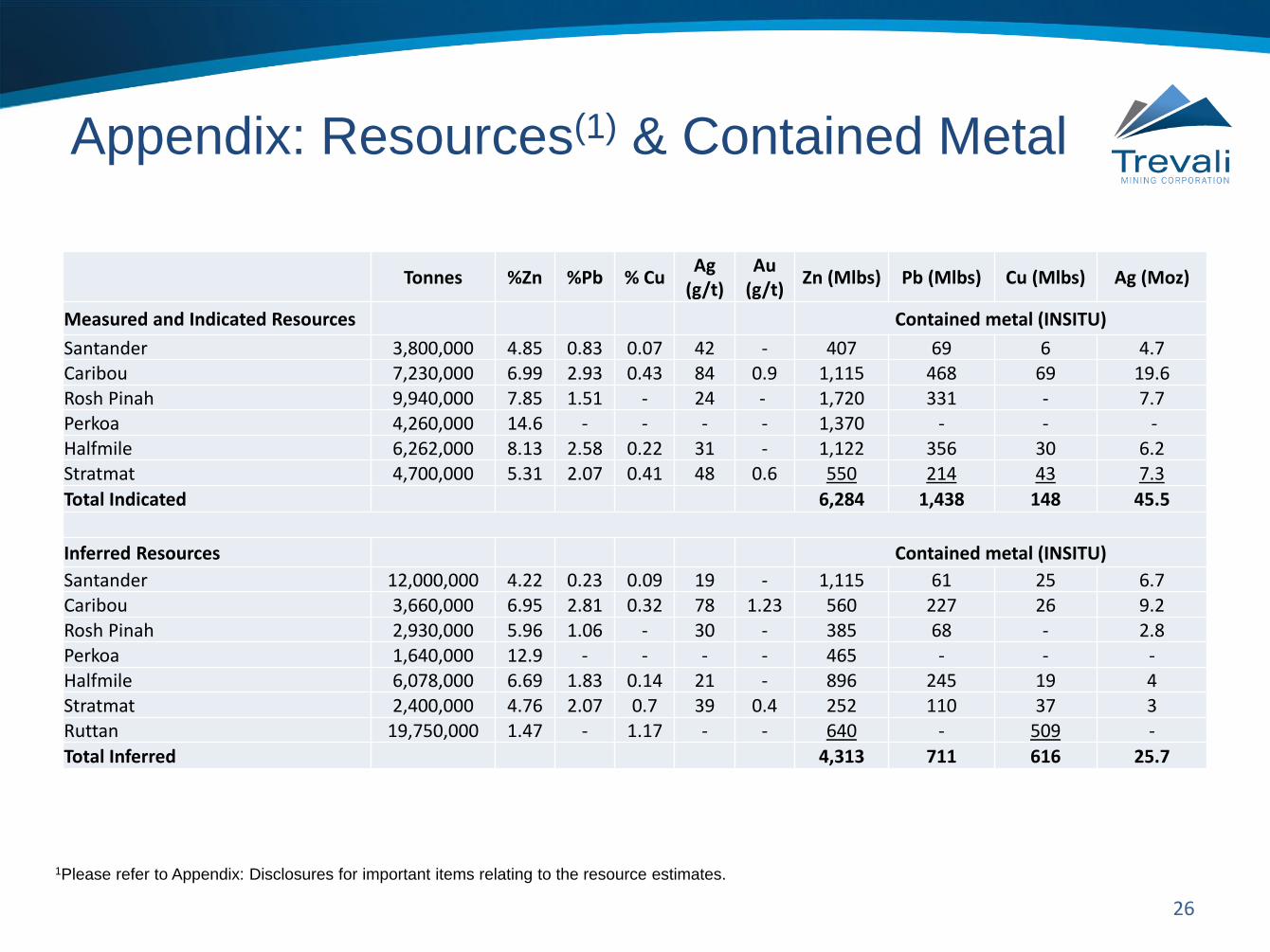

Appendix: Resources(1) & Contained Metal

26

1Please refer to Appendix: Disclosures for important items relating to the resource estimates.

Tonnes %Zn %Pb % CuAg

(g/t)Au

(g/t)Zn (Mlbs) Pb (Mlbs) Cu (Mlbs) Ag (Moz)

Measured and Indicated Resources Contained metal (INSITU)

Santander 3,800,000 4.85 0.83 0.07 42 - 407 69 6 4.7Caribou 7,230,000 6.99 2.93 0.43 84 0.9 1,115 468 69 19.6Rosh Pinah 9,940,000 7.85 1.51 - 24 - 1,720 331 - 7.7Perkoa 4,260,000 14.6 - - - - 1,370 - - -Halfmile 6,262,000 8.13 2.58 0.22 31 - 1,122 356 30 6.2Stratmat 4,700,000 5.31 2.07 0.41 48 0.6 550 214 43 7.3

Total Indicated 6,284 1,438 148 45.5

Inferred Resources Contained metal (INSITU)

Santander 12,000,000 4.22 0.23 0.09 19 - 1,115 61 25 6.7Caribou 3,660,000 6.95 2.81 0.32 78 1.23 560 227 26 9.2Rosh Pinah 2,930,000 5.96 1.06 - 30 - 385 68 - 2.8Perkoa 1,640,000 12.9 - - - - 465 - - -Halfmile 6,078,000 6.69 1.83 0.14 21 - 896 245 19 4Stratmat 2,400,000 4.76 2.07 0.7 39 0.4 252 110 37 3Ruttan 19,750,000 1.47 - 1.17 - - 640 - 509 -

Total Inferred 4,313 711 616 25.7

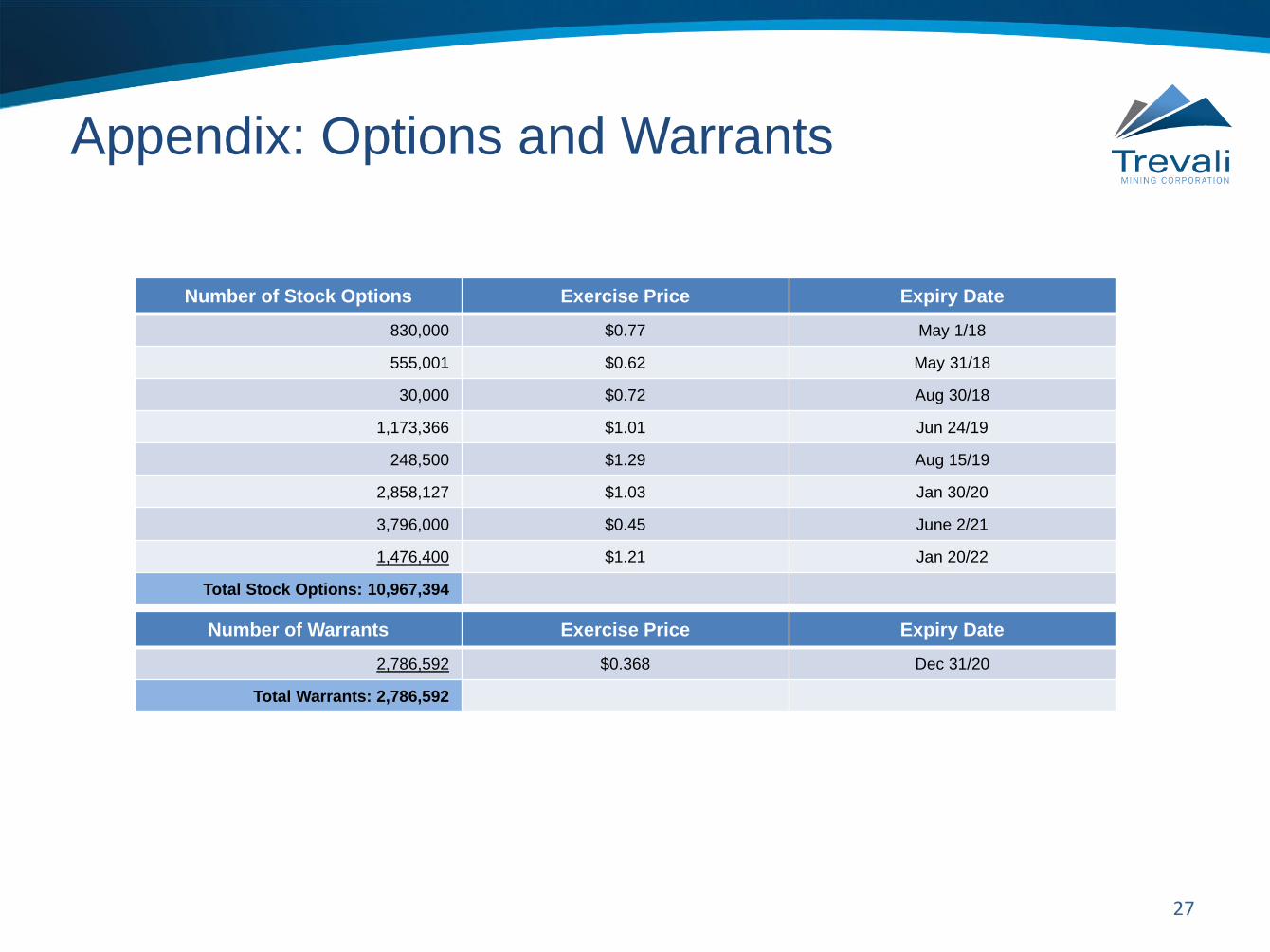

Appendix: Options and Warrants

27

Number of Warrants Exercise Price Expiry Date

2,786,592 $0.368 Dec 31/20

Total Warrants: 2,786,592

Number of Stock Options Exercise Price Expiry Date

830,000 $0.77 May 1/18

555,001 $0.62 May 31/18

30,000 $0.72 Aug 30/18

1,173,366 $1.01 Jun 24/19

248,500 $1.29 Aug 15/19

2,858,127 $1.03 Jan 30/20

3,796,000 $0.45 June 2/21

1,476,400 $1.21 Jan 20/22

Total Stock Options: 10,967,394

Appendix: Mining Analyst Coverage

28

Firm Analyst Location

BMO Capital Markets Alex Terentiew Toronto, Canada

Cormark Securities Inc. Stefan Ioannou Toronto, Canada

Eight Capital Jacques Wortman Toronto, Canada

GMP Securities L.P. Ian Parkinson Toronto, Canada

Haywood Securities Inc. Pierre Vaillancourt Toronto, Canada

Kallpa Securities S.A.B Sebastian Cruz Lima, Peru

Paradigm Capital Inc. Jeff Woolley Toronto, Canada

Scotiabank Orest Wowkodaw Toronto, Canada

TD Securities Inc. Craig Hutchison Toronto, Canada

The above investment firms and equity analysts provide research reports on Trevali Mining Corporation. Any opinions, estimates,

forecasts or other analyses, including prior or future Trevali performance from any source is the opinion of the writer and is theirs

alone and does not represent the opinions, estimates or forecasts of Trevali or its management. Trevali does not, by any

reference, imply any endorsement of, or concurrence with, such information, conclusions or recommendations. Trevali does not

distribute research reports.

29

EurGeol Dr. Mark D. Cruise, Trevali's President and CEO, and a qualified person as defined by NI 43-101, has reviewed the scientific and technical

information that forms the basis for this presentation. Dr. Cruise is not independent of the Company as he is an officer, director and shareholder.

Trevali's production plan at the Caribou Mine is based only on measured, indicated and inferred mineral resources, and not mineral reserves, and does

not have demonstrated economic viability. Trevali’s production plans at the Perkoa Mine, Rosh Pinah Mine and Santander Mine are based on both

proven and probable reserves and on measured, indicated and inferred mineral resources; mineral resources by definition do not have demonstrated

economic viability. Inferred mineral resources are considered too speculative geologically to have the economic considerations applied to them that

would enable them to be categorized as mineral reserves, and there is therefore no certainty that the conclusions of the production plans and

Preliminary Economic Assessment (PEA) will be realized. Additionally, where Trevali discusses exploration/expansion potential, any potential quantity

and grade is conceptual in nature and there has been insufficient exploration to define a mineral resource and it is uncertain if further exploration will

result in the target being delineated as a mineral resource.

The Santander resource estimate was independently estimated by the Company’s consultant Arseneau Consulting Services Ltd. The resource

estimates were prepared by and under the supervision of Dr. Gilles Arseneau, an appropriate "independent qualified person" as this term is defined in

National Instrument 43-101. Dassault Systemes Geovia Gems version 6.7 (Gems) software was used to review and modify the geological solids

provided by Trevali, prepare assay data for geostatistical analysis, construct the block model, estimate metal grades and tabulate mineral resources.

The Geostatistical Software SAGE2001 was used for geostatistical analysis and variography. A cut-off-grade of US$40 was utilized which is the

nominal base-case estimated grade of material that can be mined and processed considering all applicable costs. For reference, the Company’s

Santander 2017 site cash cost guidance (mining, milling and site G&A) is US$35-$40 per tonne. The mineral resources identified in Table 1 are based

on Ordinary Kriged (OK) capped values inside 5-by-5-by-5-metre blocks for the Magistral deposits and 10-by-10-by-5-metre blocks for the Puajanca

and Santander Pipe deposits. Assays were capped prior to compositing and assays were composited to 2 metres for the Magistral and Puajanca

deposit and 3.5 metres for the Santander deposit. Resource estimates for Santander Pipe and Puajanca South are unchanged from 2012 but have

been updated to reflect 2016 metal prices. The US dollar value cut-off is based on the formula:

Dollar Value = ((Ag Price x Ag Recovery x Ag Grade) + (Pb Price x Pb Recovery x Pb Grade)+(Zn Price x Zn Recovery x (Zn Grade)). Price for silver is

($16.50/oz) and that for Pb ($0.95), Zn ($1.15) and Cu ($2.50) is per pound. A recovery of 74% was applied to Ag, 85% for Pb, 89% for Zn and 0% for

Cu for calculating the dollar value formula. Santander zinc equivalent is calculated by dividing the dollar value by the zinc price.

Caribou resource estimate was completed by SRK Consulting (Canada) Inc. in January 2013. The tabled resource estimate utilizes a 5% zinc

equivalent (ZnEQ) cut-off grade. ZnEq=((Cu Grade*Cu Price*Cu Recovery)+(Pb Grade*Pb Price*Pb Recovery)+(Zn Grade*Zn Price*Zn Recover)+(Au

Grade*Au Price*Au Recovery)+(Ag Grade*Ag Price*Ag Recovery))/Zn Price. In calculating ZnEq, SRK Consulting (Canada) Inc. utilized the long term

metal prices provide by Energy & Metals Consensus Forecast. Price for Au is $1470 per ounce, Ag is $26 per ounce, Cu is $3.39 per pound, Pb is

$1.18 per pound, and Zn is $1.14 per pound. A recovery of 83% was applied to Zn, 71% was applied to Pb, 57% was applied to Cu, 45% was applied

to Ag, and 40% was applied to Au. The pounds of metal are in-situ and have not had any mining factors applied to them.

Appendix: Disclosures I

30

Caribou PEA study was conducted in accordance with the definitions in Canadian National Instrument 43-101. SRK Consulting (Canada) Inc. was the

lead independent consultant, with contributions from other independent consultants commissioned by Trevali – Holland & Holland Consulting and

Stantec Consulting. The base case Caribou Mine Project PEA uses price assumptions of US$1.00/lb zinc, US$1.00/lb lead, US$3.00/lb copper,

US$21.00/oz silver and US$1,200/oz gold. These prices are based on a review of consensus price forecasts from financial institutions and similar

studies that recently have been published. The PEA is considered preliminary in nature and includes economic analysis that is based, in part, on

inferred mineral resources. Inferred mineral resources are considered too speculative geologically to have the economic considerations applied to them

that would allow them to be categorized as mineral reserves, and there is no certainty that the results will be realized. Mineral resources are not

mineral reserves because they do not have demonstrated economic viability.

Halfmile Deposit resource estimate completed by Tetra Tech Wardrop and prepared by Tim Maunula, P.Geo. and Christopher Moreton, Ph.D., P.Geo.

Stratmat Deposit resource estimate completed by SRK Consulting (Canada) Inc. and prepared by Dr. Gilles Arseneau, P.Geo.

Rosh Pinah mineral reserves and mineral resources are derived from the technical report entitled “Technical Report on the Rosh Pinah Mine, Namibia”

dated April 7, 2017 and effective December 31, 2016 prepared by Roscoe Postle Associates Inc.; Canadian Institute of Mining, Metallurgy and

Petroleum (“CIM”) definitions were followed for Mineral Reserves and Resources; Mineral Reserves are estimated at various Net Smelter Return

(NSR) cut-off values depending on required development; Mineral Reserves are estimated using average consensus forecast long-term prices of

US$1.03/lb Zn, US$0.93/lb Pb, US$18.65/oz Ag and US$1,358/oz Au at an exchange rate of 17.71 NAD/US$; Mineral Resources are inclusive of

Mineral Reserves; Mineral Resources are estimated at a cut-off grade of 4% Zn Equivalent; Shown at 100% ownership; Mineral Resources that are not

Mineral Reserves do not have demonstrated economic viability.

Perkoa mineral reserves and mineral resources are derived from the technical report entitled “Technical Report on the Perkoa Mine, Burkina Faso”

dated April 7, 2017 and effective December 31, 2016 prepared by Roscoe Postle Associates Inc.; CIM definitions were followed for Mineral Reserves

and Resources; Mineral Reserves are estimated at an NSR cut-off value of $100/tonne inclusive of capital expenditure, incremental stopes greater

than US$78/tonne are included based on individual financial analysis; Mineral Reserves are estimated using an average consensus forecast zinc price

of US$0.99 per pound and a €/US$ exchange rate of 1.11; Shown at 100% ownership; Mineral Resources are inclusive of Mineral Reserves; Mineral

Resources are estimated at a cut-off grade of 5% Zn; Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability).

Appendix: Disclosures II

31

In Canada, an issuer is required to provide technical information with respect to mineralization, including reserves and resources, if any, on its mineral

exploration properties in accordance with Canadian requirements, which differ significantly from the requirements of the SEC applicable to registration

statements and reports filed by U.S. companies pursuant to the U.S. Securities Act or the U.S. Securities Exchange Act of 1934, as amended. As such,

information contained in this presentation concerning descriptions of mineralization under Canadian standards may not be comparable to similar

information made public by U.S. companies subject to the reporting and disclosure requirements of the SEC.

The terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with

Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and

Petroleum (the “CIM”) — CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These

definitions differ from the definitions in Industry Guide 7 (“Industry Guide 7”) under the U.S. Securities Act. Under Industry Guide 7 standards, a “final”

or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to

designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and

required to be disclosed by NI 43-101; however, these terms are not defined terms under Industry Guide 7 and are normally not permitted to be used in

reports and registration statements filed with the SEC. You are cautioned not to assume that any part or all of mineral deposits in these categories will

ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their

economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category.

Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. You

are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained

ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that

does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this presentation containing descriptions of any mineral deposits may not be comparable to similar information

made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and

regulations thereunder. You are cautioned that the reserves presented in this presentation while in compliance with Canadian standards and

regulations, may not meet the requirements of reserve disclosure under SEC guidelines.

Appendix: Cautionary Note Regarding United States Laws

Contact Information

32

TREVALI MINING CORPORATION

1400-1199 West Hastings Street

Vancouver, BC, V6E 3T5, CANADA

Phone: 1-604-488-1661

Fax: 1-604-408-7499

www.trevali.com

CONTACT:Steve Stakiw

Vice President, Investor Relations and Corporate Communications

Direct phone:1-604-638-5623

A member of the

Related Documents