Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Contents

Cover

Series

TitlePage

Copyright

Dedication

Foreword

Preface

Acknowledgments

AbouttheAuthor

Chapter1:Introduction1.1LESSONSFROMACRISIS1.2FINANCIALRISKANDACTUARIALRISK1.3SIMULATIONANDSUBJECTIVEJUDGMENT

Chapter2:InstitutionalBackground2.1MORALHAZARD—INSIDERSANDOUTSIDERS2.2PONZISCHEMES2.3ADVERSESELECTION

2.4THEWINNER'SCURSE2.5MARKETMAKINGVERSUSPOSITIONTAKING

Chapter3:OperationalRisk3.1OPERATIONSRISK3.2LEGALRISK3.3REPUTATIONALRISK3.4ACCOUNTINGRISK3.5FUNDINGLIQUIDITYRISK3.6ENTERPRISERISK3.7IDENTIFICATIONOFRISKS3.8OPERATIONALRISKCAPITAL

Chapter4:FinancialDisasters4.1DISASTERSDUETOMISLEADINGREPORTING4.2DISASTERSDUETOLARGEMARKETMOVES4.3DISASTERSDUETOTHECONDUCTOFCUSTOMERBUSINESS

Chapter5:TheSystemicDisasterof2007–20085.1OVERVIEW5.2THECRISISINCDOSOFSUBPRIMEMORTGAGES5.3THESPREADOFTHECRISIS5.4LESSONSFROMTHECRISISFORRISKMANAGERS5.5LESSONSFROMTHECRISISFORREGULATORS5.6BROADERLESSONSFROMTHECRISIS

Chapter6:ManagingFinancialRisk6.1RISKMEASUREMENT6.2RISKCONTROL

Chapter7:VaRandStressTesting7.1VARMETHODOLOGY7.2STRESSTESTING7.3USESOFOVERALLMEASURESOFFIRMPOSITIONRISK

Chapter8:ModelRisk8.1HOWIMPORTANTISMODELRISK?8.2MODELRISKEVALUATIONANDCONTROL8.3LIQUIDINSTRUMENTS8.4ILLIQUIDINSTRUMENTS8.5TRADINGMODELS

Chapter9:ManagingSpotRisk9.1OVERVIEW9.2FOREIGNEXCHANGESPOTRISK9.3EQUITYSPOTRISK9.4PHYSICALCOMMODITIESSPOTRISK

Chapter10:ManagingForwardRisk10.1INSTRUMENTS10.2MATHEMATICALMODELSOFFORWARDRISKS10.3FACTORSIMPACTINGBORROWINGCOSTS10.4RISKMANAGEMENTREPORTINGANDLIMITSFORFORWARDRISK

Chapter11:ManagingVanillaOptionsRisk11.1OVERVIEWOFOPTIONSRISKMANAGEMENT11.2THEPATHDEPENDENCEOFDYNAMICHEDGING11.3ASIMULATIONOFDYNAMICHEDGING

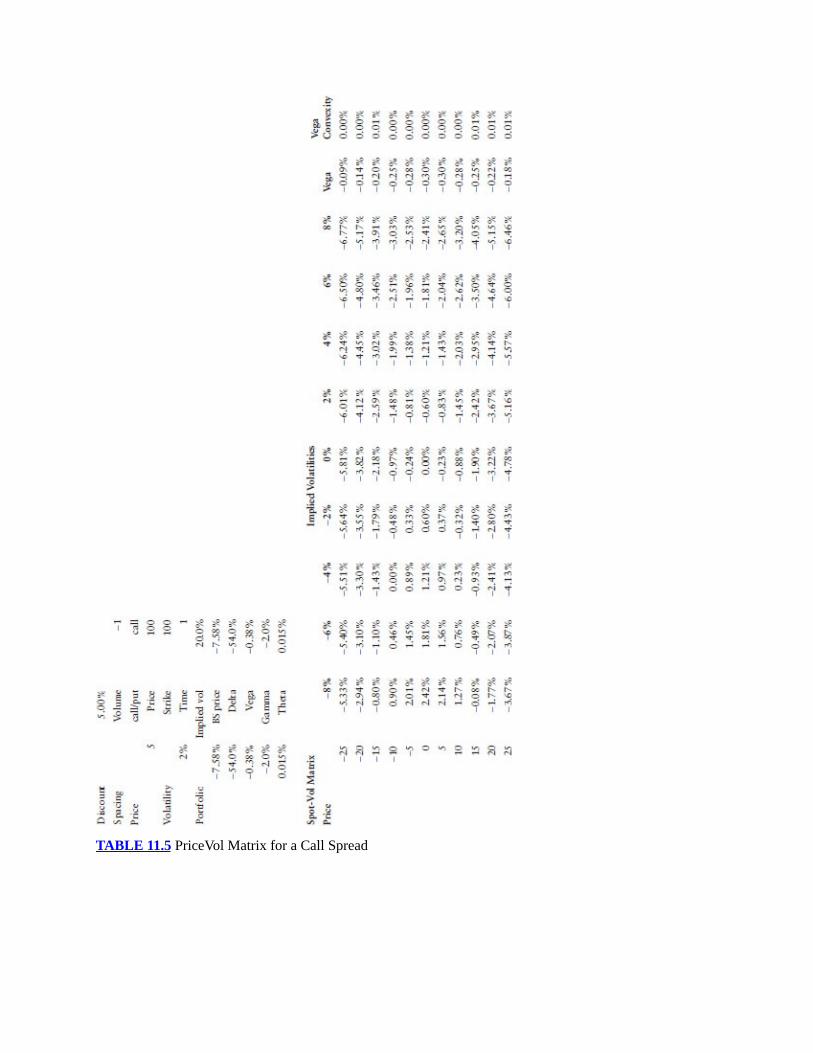

11.4RISKREPORTINGANDLIMITS11.5DELTAHEDGING11.6BUILDINGAVOLATILITYSURFACE11.7SUMMARY

Chapter12:ManagingExoticOptionsRisk12.1SINGLE-PAYOUTOPTIONS12.2TIME-DEPENDENTOPTIONS12.3PATH-DEPENDENTOPTIONS12.4CORRELATION-DEPENDENTOPTIONS12.5CORRELATION-DEPENDENTINTERESTRATEOPTIONS

Chapter13:CreditRisk13.1SHORT-TERMEXPOSURETOCHANGESINMARKETPRICES13.2MODELINGSINGLE-NAMECREDITRISK13.3PORTFOLIOCREDITRISK13.4RISKMANAGEMENTOFMULTINAMECREDITDERIVATIVES

Chapter14:CounterpartyCreditRisk14.1OVERVIEW14.2EXCHANGE-TRADEDDERIVATIVES14.3OVER-THE-COUNTERDERIVATIVES

References

AbouttheCompanionWebsite

Index

Founded in 1807, John Wiley & Sons is the oldest independent publishingcompanyintheUnitedStates.WithofficesinNorthAmerica,Europe,Australia,andAsia,Wiley is globally committed to developing andmarketing print andelectronic products and services for our customers' professional and personalknowledgeandunderstanding.TheWileyFinanceseriescontainsbookswrittenspecifically for financeand

investmentprofessionalsaswell as sophisticated individual investorsand theirfinancial advisors. Book topics range from portfolio management to e-commerce, risk management, financial engineering, valuation, and financialinstrumentanalysis,aswellasmuchmore.Foralistofavailabletitles,visitourWebsiteatwww.WileyFinance.com.

Coverimage:JohnWiley&Sons,Inc.Coverdesign:©TomFewsteriStockphoto,©samxmegiStockphoto

Copyright©2013byStevenAllen.Allrightsreserved.PublishedbyJohnWiley&Sons,Inc.,Hoboken,NewJersey.

PublishedsimultaneouslyinCanada.TheFirstEditionofthisbookwaspublishedin2003byJohnWiley&Sons,Inc.Nopartofthispublicationmaybereproduced,storedinaretrievalsystem,ortransmittedinanyformorbyanymeans,electronic,mechanical,photocopying,recording,scanning,orotherwise,exceptaspermittedunderSection107or108

ofthe1976UnitedStatesCopyrightAct,withouteitherthepriorwrittenpermissionofthePublisher,orauthorizationthroughpaymentoftheappropriateper-copyfeetotheCopyrightClearanceCenter,Inc.,222RosewoodDrive,Danvers,MA01923,(978)750-8400,fax(978)646-8600,orontheWebatwww.copyright.com.RequeststothePublisherforpermissionshouldbe

addressedtothePermissionsDepartment,JohnWiley&Sons,Inc.,111RiverStreet,Hoboken,NJ07030,(201)748-6011,fax(201)748-6008,oronlineat

http://www.wiley.com/go/permissions.LimitofLiability/DisclaimerofWarranty:Whilethepublisherandauthorhaveusedtheirbesteffortsinpreparingthisbook,theymakenorepresentationsorwarrantieswithrespecttotheaccuracyorcompletenessofthecontentsofthisbookandspecificallydisclaimanyimpliedwarrantiesofmerchantabilityor

fitnessforaparticularpurpose.Nowarrantymaybecreatedorextendedbysalesrepresentativesorwrittensalesmaterials.Theadviceandstrategiescontained

hereinmaynotbesuitableforyoursituation.Youshouldconsultwithaprofessionalwhereappropriate.Neitherthepublishernorauthorshallbeliableforanylossofprofitoranyothercommercialdamages,includingbutnotlimited

tospecial,incidental,consequential,orotherdamages.Forgeneralinformationonourotherproductsandservicesorfortechnical

support,pleasecontactourCustomerCareDepartmentwithintheUnitedStatesat(800)762-2974,outsidetheUnitedStatesat(317)572-3993orfax(317)572-

4002.Wileypublishesinavarietyofprintandelectronicformatsandbyprint-on-

demand.Somematerialincludedwithstandardprintversionsofthisbookmaynotbeincludedine-booksorinprint-on-demand.Ifthisbookreferstomedia

suchasaCDorDVDthatisnotincludedintheversionyoupurchased,youmaydownloadthismaterialathttp://booksupport.wiley.com.Formoreinformation

aboutWileyproducts,visitwww.wiley.com.LibraryofCongressCataloging-in-PublicationData:

Allen,Steven,1945–Financialriskmanagement[electronicresource]:apractitioner'sguideto

managingmarketandcreditrisk/StevenAllen.—2nded.

1onlineresource.Includesbibliographicalreferencesandindex.

DescriptionbasedonprintversionrecordandCIPdataprovidedbypublisher;resourcenotviewed.

ISBN978-1-118-17545-3(cloth);978-1-118-22652-0(ebk.);ISBN978-1-118-23164-7(ebk.);ISBN978-1-118-26473-7(ebk.)1.Financialriskmanagement.2.Finance.I.Title.

HD61658.15'5—dc23

2012029614

ToCarolineForallthewaysshehashelpedbring

thisprojecttofruitionAndformuch,muchmore

Foreword

RiskwasaloteasiertothinkaboutwhenIwasadoctoralstudentinfinance25years ago. Back then, risk was measured by the variance of your wealth.Loweringriskmeant loweringthisvariance,whichusuallyhadtheunfortunateconsequenceofloweringtheaveragereturnonyourwealthaswell.In those halcyon days, we had only two types of risk, systemic and

unsystematic.Thelatteronecouldbeloweredforfreeviadiversification,whiletheformeronecouldonlybeloweredbytakingahit toaveragereturn.Inthatidyllic world, financial risk management meant choosing the variance thatmaximizedexpectedutility.Onemerelyhad tosolveanoptimizationproblem.Whatcouldbeeasier?I started to appreciate that financial riskmanagement might not be so easy

when I moved from theWest Coast to the East Coast. The NewYork–basedbanksstartedcreatingwholedepartmentstomanagefinancialrisk.Whydoyouneeddozensofpeopletosolveasimpleoptimizationproblem?AsItalkedwiththedenizensofthosedepartments,Inoticedtheykeptintroducingtypesofriskthatwerenotinmyfinanciallexicon.Firsttherewascreditrisk,atermthatwasto be differentiated from market risk, because you can lose money lendingwhetheramarketexistsornot.Fine,Igotthat,butthencameliquidityriskontop ofmarket and credit risk. Just as Iwas struggling to integrate these threetypesofrisk,peoplestartedworryingaboutoperationalrisk,basisrisk,mortalityrisk,weatherrisk,estimationrisk,counterpartycreditrisk,andeventheriskthatyourmodelsforalltheseriskswerewrong.Ifmodelriskexisted,thenyouhadtoconcedethatevenyourmodelformodelriskwasrisky.Sincetheproposedsolutionforallthesenewriskswerenewmodelsandsince

the proposed solution for the model risk of the new models was yet moremodels, it was no wonder all of those banks had all of those people runningaroundmanagingallofthoserisks.Well,apparently,notquiteenoughpeople.AsIwrite thesewords, themedia

arehavingafielddaydenouncingJPMorgan'sroughly$6billionlossrelatedtotheLondonwhale'sill-fatedforayintocreditdefaultswaps(CDSs).As the flagbearer for theTVgeneration, Ican'thelpbut thinkof revivinga

1970s TV show to star Bruno Iksil as the Six Billion Dollar Man. As eye-popping as these numbers are, they are merely the fourth largest trading loss

since the first editionof this bookwas released. Ifwe ignoreBernieMadoff's$50 billion Ponzi scheme, the distinction for the worst trade ever belongs toHowieHubler,wholost$9billiontradingCDSsin2008foranotherbankwhosenameI'drathernotwrite.However,ifyoureallyneedtoknow,thenhere'sahint.The present occupant of Mr. Hubler's old office presently thinks that riskmanagementisacomplicatedsubject,verycomplicatedindeed,andhastoadmitthatasimpleoptimizationisnottheanswer.Sowhatistheanswer?Well,whenthe answer to a complicated question is nowhere to be found in the depths ofone's soul, then one can always fall back on asking the experts instead. TheDanishscientistNielsBohr,oncedeemedanexpert,saidanexpertis,“Apersonthathasmadeeverypossiblemistakewithinhisorherfield.”Asanexpertinthefieldofderivativesecuritiesvaluation,IbelieveIknowa

fellow expert when I see one. Steve Allen has been teaching courses in riskmanagement at New York University's Courant Institute since 1998. SteveretiredfromJPMorganChaseasamanagingdirectorin2004,cappinga35-yearcareerinthefinanceindustry.Giventhewidepraiseforthefirsteditionofthisbook, theauthorcouldhaverestedonhis laurels,comfortedby theknowledgethat thewisdomof theages iseternal. Instead,hehas taken ituponhimself towriteasecondeditionofthistimelessbook.Most authors in Steve's enviable situationwould have contented themselves

withexploiting thecrisis toelaborateonsomeextendedversionof“I toldyouso.”Instead,Stevehasaddedmuchinthewayoftheoreticaladvancesthathavearisenoutofthenecessityofensuringthathistorydoesnotrepeatitself.Theseadvances in turnraise the increasingdegreeofspecializationwesee inside theriskmanagementdepartmentsofmodern financial institutionsand increasinglyin the public sector aswell.Alongwith continued progress in the historicallyvitalproblemofmarking tomarketof illiquidpositions, there is an increasingdegreeofrigorinthedeterminationofreservesthatariseduetomodelrisk, inthelimitsusedtocontrolrisktaking,andinthemethodsusedtoreviewmodels.Thenecessityoftestingeveryassumptionhasbeenmadeplainbythestressthatthe crisis has imposed on our fragile financial system. As the aftershocksreverberate around us, we will not know for many years whether the presentsafeguardswillservetheirintendedpurpose.However,thetimingforanupdatetoSteve'sbookcouldnotbebetter.Itrulyhopethatthecurrentgenerationofriskmanagers,whethertheybegrizzledorgreen,willtakethelessonsontheensuingpagestoheart.Oursharedfinancialfuturedependsonit.

PeterCarr,PhDManagingDirectoratMorganStanley,GlobalHeadofMarketModeling,and

ExecutiveDirectorofNewYorkUniversityCourant'sMastersinMathematicalFinance

PrefaceThis book offers a detailed introduction to the field of risk management asperformedat large investmentandcommercialbanks,withanemphasison thepracticesofspecialistmarketriskandcreditriskdepartmentsaswellastradingdesks.Alargeportionofthesepracticesisalsoapplicabletosmallerinstitutionsthatengageintradingorassetmanagement.The aftermath of the financial crisis of 2007–2008 leaves a good deal of

uncertainty as to exactlywhat the structure of the financial industrywill looklikegoingforward.Someofthebusinesscurrentlyperformedininvestmentandcommercialbanks,suchasproprietarytrading,maymovetootherinstitutions,atleast in some countries, based on new legislation and new regulations.But inwhatever institutional setting this business is conducted, the riskmanagementissues will be similar to those encountered in the past. This book focuses ongenerallessonsastohowtheriskoffinancialinstitutionscanbemanagedratherthanonthespecificsofparticularregulations.Myaiminthisbookistobecomprehensiveinlookingattheactivitiesofrisk

management specialists aswell as tradingdesks, at the realmofmathematicalfinanceaswellasthatofthestatisticaltechniques,and,mostimportant,athowthesedifferentapproachesinteractinanintegratedriskmanagementprocess.This second edition reflects lessons that have been learned from the recent

financialcrisisof2007–2008(formoredetail,seeChapters1and5),aswellasmanynewbooks,articles,andideasthathaveappearedsincethepublicationofthefirsteditionin2003.Chapter6onmanagingmarketrisk,Chapter7onvalueat risk (VaR) and stress testing, Chapter 8 onmodel risk, and Chapter 13 oncreditriskarealmostcompletelyrewrittenandexpandedfromthefirstedition,andanewChapter14oncounterpartycreditriskisanextensiveexpansionofasectionofthecreditriskchapterinthefirstedition.Thewebsiteforthisbook(www.wiley.com/go/frm2e)willbeusedtoprovide

bothsupplementarymaterialstothetextandcontinuousupdates.Supplementarymaterials will include spreadsheets and computer code that illustratecomputations discussed in the text. In addition, there will be classroom aidsavailable only to professors on theWiley Higher Education website. Updateswill include an updated electronic version of theReferences section, to alloweasycut-and-pastelinkingtoreferencedmaterialontheweb.Updateswillalsoinclude discussion of new developments. For example, at the time this book

wenttopress,thereisnotyetenoughpublicinformationaboutthecausesofthelarge trading losses at JPMorgan's London investment office to allow adiscussionofriskmanagementlessons;asmoreinformationbecomesavailable,I will place an analysis of riskmanagement lessons from these losses on thewebsite.This book is divided into three parts: general background to financial risk

management, the principles of financial risk management, and the details offinancialriskmanagement.

Thegeneralbackgroundpart(Chapters1through5)givesaninstitutionalframeworkforunderstandinghowriskarisesinfinancialfirmsandhowitismanaged.Withoutunderstandingthedifferentrolesandmotivationsoftraders,marketers,seniorfirmmanagers,corporateriskmanagers,bondholders,stockholders,andregulators,itisimpossibletoobtainafullgraspofthereasoningbehindmuchofthemachineryofriskmanagementorevenwhyitisnecessarytomanagerisk.Inthispart,youwillencounterkeyconceptsriskmanagershaveborrowedfromthetheoryofinsurance(suchasmoralhazardandadverseselection),decisionanalysis(suchasthewinner'scurse),financetheory(suchasthearbitrageprinciple),andinoneinstanceeventhecriminalcourts(thePonzischeme).Chapter4providesdiscussionofsomeofthemostprominentfinancialdisastersofthepast30years,andChapter5focusesonthecrisisof2007–2008.Theseserveascasestudiesoffailuresinriskmanagementandwillbereferencedthroughoutthebook.Thispartalsocontainsachapteronoperationalrisk,whichisnecessarybackgroundformanyissuesthatariseinpreventingfinancialdisastersandwhichwillbereferredtothroughouttherestofthebook.Thepartonprinciplesoffinancialriskmanagement(Chapters6through8)firstlaysoutanintegratedframeworkinChapter6,andthenlooksatVaRandstresstestinginChapter7andthecontrolofmodelriskinChapter8.Thepartondetailsoffinancialriskmanagement(Chapters9through14)appliestheprinciplesofthesecondparttoeachspecifictypeoffinancialrisk:spotriskinChapter9,forwardriskinChapter10,vanillaoptionsriskinChapter11,exoticoptionsriskinChapter12,creditriskinChapter13,andcounterpartycreditriskinChapter14.Aseachrisktypeisdiscussed,specificreferencesaremadetotheprincipleselucidatedinChapters6through8,andadetailedanalysisofthemodelsusedtopricetheserisksandhowthesemodelscanbeusedtomeasureandcontrolriskispresented.

Sincethe1990s,anincreasedfocusonthenewtechnologybeingdevelopedto

measureandcontrol financial riskhas resulted in thegrowthofcorporatestaffareasmannedbyriskmanagementprofessionals.However, thisdoesnotimplythatfinancialfirmsdidnotmanageriskspriorto1990orthatcurrentlyallriskmanagement is performed in staff areas. Senior linemanagers such as tradingdesk and portfolio managers have always performed a substantial riskmanagementfunctionandcontinuetodoso.Infact,confusioncanbecausedbythetraditionofusingthetermriskmanagerasasynonymforaseniortraderorportfolio manager and as a designation for members of corporate staff areasdealingwith risk.Although this book covers riskmanagement techniques thatareusefultobothlinetradingmanagersandcorporatestaffactingonbehalfofthefirm'sseniormanagement,theneedsoftheseindividualsdonotcompletelyoverlap.Iwilltrytoalwaysmakeacleardistinctionbetweeninformationthatisuseful to a trading desk and information that is needed by corporate riskmanagers,andexplainhowtheymightintersect.Books and articles on financial risk management have tended to focus on

statistical techniques embodied inmeasures such as value at risk (VaR).As aresult, risk management has been accused of representing a very narrowspecialty with limited value, a view that has been colorfully expressed byNassim Taleb (1997), “There has been growth in the number of ‘riskmanagement advisors,' an industry sometimes populated by people with anamateurish knowledge of risk. Using some form of shallow technical skills,these advisors emit pronouncements on such matters as ‘risk management'without a true understanding of the distribution. Such inexperience andweaknessbecomemoreapparentwiththevalue-at-riskfadortheoutpouringofbooksonriskmanagementbyauthorswhonevertradedacontract”(p.4).Thisbookgives amorebalancedaccountof riskmanagement.Less than20

percentof thematerial looksatstatistical techniquessuchasVaR.Thebulkofthebookexaminesissuessuchasthepropermark-to-marketvaluationoftradingpositions,thedeterminationofnecessaryreservesagainstvaluationuncertainty,the structuringof limits tocontrol risk taking, and the reviewofmathematicalmodels and determination of how they can contribute to risk control. Thisallocation of material mirrors the allocation of effort in the corporate riskmanagementstaffareaswithwhichIamfamiliar.Thisisreflectedinthestaffingofthesedepartments.Morepersonnelisdrawnfromthosewithexperienceandexpertise in trading and building models to support trading decisions than isdrawnfromastatisticaloracademicfinancebackground.Althoughmanyreadersmayalreadyhaveabackgroundintheinstruments—

bonds, stocks, futures, and options—used in the financial markets, I havesupplieddefinitionseverytimeIintroduceaterm.Termsareitalicizedinthetextat thepoint theyaredefined.Anyreader feeling theneedforamore thoroughintroduction tomarket terminology should find the first nine chapters ofHull(2012)adequatepreparationforunderstandingthematerialinthisbook.Mypresentationofthematerialisbasedbothontheoryandonhowconcepts

areutilizedinindustrypractice.IhavetriedtoprovidemanyconcreteinstancesofeitherpersonalexperienceorreportsIhaveheardfromindustrycolleaguestoillustrate these practices. Where incidents have received sufficient previouspublicscrutinyoroccurredlongenoughagothatissuesofconfidentialityarenotaconcern,Ihaveprovidedconcretedetails.Inothercases,Ihavehadtopreservethe anonymity of my sources by remaining vague about particulars. Mypreservation of anonymity extends to a liberal degree of randomness inreferencestogender.Athoroughdiscussionofhowmathematicalmodelsareused tomeasureand

control risks must make heavy reference to the mathematics used in creatingthese models. Since excellent expositions of the mathematics exist, I do notpropose to enter intoextensivederivationsof results that can readilybe foundelsewhere. Instead, I will concentrate on how these results are used in riskmanagement and how the approximations to reality inevitable in anymathematicalabstractionaredealtwithinpractice.Iwillprovidereferencestothe derivation of results. Wherever possible, I have used Hull (2012) as areference,sinceitistheoneworkthatcanbefoundontheshelfofnearlyeverypractitionerinthefieldofquantitativefinance.Although the material for this book was originally developed for a course

taughtwithinamathematicsdepartment,Ibelievethatvirtuallyallofitsmaterialwillbeunderstandabletostudentsinfinanceprogramsandbusinessschools,andtopractitionerswithacomparableeducationalbackground.Akeyreasonforthisis that whereas derivatives mathematics often emphasizes the use of moremathematicallysophisticatedcontinuous timemodels,discrete timemodelsareusually more relevant to risk management, since risk management is oftenconcerned with the limits that real market conditions place on mathematicaltheory.This book is designed to be used either as a text for a course in risk

managementorasa resource for self-studyor reference forpeopleworking inthefinancialindustry.Tomakethematerialaccessibletoasbroadanaudienceaspossible, I have tried everywhere to supplement mathematical theory with

concreteexamplesandhavesuppliedspreadsheetsontheaccompanyingwebsite(www.wiley.com/go/frm2e) to illustrate these calculations.Spreadsheetson thewebsite are referenced throughout the text and a summary of all spreadsheetssuppliedisprovidedinthe“AbouttheCompanionWebsite”sectionatthebackofthebook.Atthesametime,Ihavetriedtomakesurethatallthemathematicaltheorythatgetsusedinriskmanagementpracticeisaddressed.Forreaderswhowant to pursue the theoretical developments at greater length, a full set ofreferenceshasbeenprovided.

Acknowledgments

The views expressed in this book are my own, but have been shaped bymyexperiences in the financial industry. Many of my conclusions about whatconstitutesbestpracticeinriskmanagementhavebeenbasedonmyobservationof and participation in the development of the risk management structure atJPMorgan Chase and its Chemical Bank and Chase Manhattan Bankpredecessors.Thegreatestinfluenceonmyoverallviewofhowfinancialriskmanagement

shouldbeconductedandonmanyofthespecificapproachesIadvocatehasbeenLesleyDanielsWebster.Myclose collaborationwithLesley tookplaceover aperiodof20years,duringthelast10ofwhichIreportedtoherinherpositionasdirector of market risk management. I wish to express my appreciation ofLesley'sleadership,alongwiththatofMarcShapiro,SuzanneHammett,BlytheMasters,andAndyThreadgold,forhavingestablishedthestandardsofintegrity,openness, thoroughness, and intellectual rigor that have been the hallmarks ofthisriskmanagementstructure.ThroughoutmostoftheperiodinwhichIhavebeeninvolvedinthesepursuits,

Don Layton was the head of trading activities with which we interacted. Hisrecognition of the importance of the risk management function and strongsupport for a close partnership between riskmanagement and trading and thefreedom of communication and information sharing were vital to thedevelopmentofthesebestpractices.Throughtheyears,myideashavebenefitedfrommycolleaguesatChemical,

Chase, JPMorgan Chase, and in consulting assignments since my retirementfrom JPMorgan Chase. At JPMorgan Chase and its predecessors, I wouldparticularly like to note the strong contributions that dialogues with AndrewAbrahams,Michel Araten, Bob Benjamin, Paul Bowmar, George Brash, JuliaChislenko,EnricoDellaVecchia,MikeDinias, FawazHabel,BobHenderson,JeffKatz,BobbyMagee,BlytheMasters,MikeRabin,BarrySchachter,VivianShelton,PaulShotton,AndyThreadgold,MickWaring,andRichardWisehaveplayed in the development of the concepts utilized here. In my consultingassignments,IhavegainedmuchfrommyexchangesofideaswithRickGrove,Chia-Ling Hsu, Neil Pearson, Bob Selvaggio, Charles Smithson, and othercolleagues at Rutter Associates, and Chris Marty and Alexey Panchekha at

Bloomberg. In interactionswith riskmanagers atother firms, I havebenefitedfrommyconversationswithKenAbbott,JohnBreit,NoelDonohoe,andEvanPicoult.ManyofthetradersIhaveinteractedwiththroughtheyearshavealsohad a major influence on my views of how risk management should impactdecision making on the trading desk and the proper conduct of relationshipsbetween traders and riskmanagement specialists. I particularly want to thankAndy Hollings, Simon Lack, Jeff Larsen, DinsaMehta, Fraser Partridge, andDonWilsonforprovidingmewithprototypesforhowtheriskmanagementoftrading should be properly conducted and their generosity in sharing theirknowledge and insight. I also wish to thank those traders, who shall remainanonymous here, who have provided me equally valuable lessons in riskmanagementpracticestoavoid.This book grew out of the riskmanagement course I created as part of the

MathematicsinFinanceMSprogramatNewYorkUniversity'sCourantInstituteofMathematicalSciences in1998.Forgivingme theopportunity to teachandfor providing an outstanding institutional setting in which to do it, I want tothank the administration and faculty of Courant, particularly Peter Carr, NeilChriss, Jonathan Goodman, Bob Kohn, and Petter Kolm, with whom I haveparticipated in the management of the program, and Caroline Thompson,GabrielleTobin,andMelissaVacca, theprogramadministrators. Ihavegainedmany insights that have found their way into this book by attending othercourses in theprogram taughtbyMarcoAvellaneda, JimGatheral,BobKohn,andNassimTaleb.Ken Abbott began participating in the risk management course as a guest

lecturer, later became my co-teacher of the course, and now has fullresponsibilityfor thecoursewithmyparticipationasaguest lecturer.ManyoftheinsightsinthisbookhavebeenlearnedfromKenorgeneratedaspartofthedebates and discussions we have held both in and out of the classroom. Thestudentsinmyriskmanagementcoursehavehelpedclarifymanyoftheconceptsinthisbookthroughtheirprobingquestions.IparticularlywanttothankKarimBeguir,whobeganasmystudentandhassincegraduatedtobecomeaFellowofthe program and a frequent and valued contributor to the risk managementcourse.Severalofhisinsightsarereflectedinthesecondeditionofthebook.Ialsowish to thankOtelloPadovaniandAndreaRaphael,studentswhobecamecollaborators on research that appears on the website for the book(www.wiley.com/go/frm2e). Mike Fisher has provided greatly appreciatedsupportasmygraduateassistantinhelpingtoclarifyclassassignmentsthathave

evolvedintoexercisesinthisbook.Thedetailedcommentsandsuggestions Ihave received fromNeilChrisson

large portions of thismanuscript far exceed the norms of either friendship orcollegiality. In numerous instances, his efforts have sharpened both the ideasbeing presented and the clarity of their expression. I alsowish to thankMichAraten, Peter Carr, BobbyMagee, Barry Schachter, Nassim Taleb, and BruceTuckman for reading the text and offering helpful comments. For the secondedition, I would like to thank Ken Abbott and Rick Grove for reading newchaptersandofferinghelpfulsuggestions.I alsowish to extendmy thanks toChuck Epstein for his help in finding a

publisher for this book. Bill Falloon, Meg Freeborn, and Michael Kay, myeditors at JohnWiley & Sons, have offered very useful suggestions at everystageof theediting.AtMacAllisterPublishingServices,AndyStonewasveryhelpfulasproductionmanagerandJeanneHenningwasathoroughandincisivecopyeditorforthefirsteditionofthisbook.TheindividualtowhombothIandthisbookowethegreatestdebtismywife,

CarolineThompson.Thenumberofwaysinwhichherbeneficialinfluencehasbeenfeltsurpassmyability toenumerate,butIat leastneedtoattemptabriefsample.ItwasCarolinewhointroducedmetoNeilChrissandfirstplantedtheidea ofmy teaching at Courant. She has been a colleague ofNeil's, JonathanGoodman's,andmineinthecontinueddevelopmentoftheCourantMathematicsinFinanceMSprogram.Fromthestart,shewasthestrongestvoiceinfavorofbasingabookonmyriskmanagementcourse.Atfrequentbottlenecks,onboththe first and second editions,when I have beendaunted by an obstacle tomyprogress that seemed insurmountable, it was Caroline who suggested theapproach,organizedthematerial,orsuggestedthejointeffortthatovercamethedifficulty.Shehasmanagedallaspectsoftheproductionformat,andstyleofthebook, including efforts from such distant ports as Laos, Vietnam, India, andHolland.

AbouttheAuthor

SteveAllen isa riskmanagementconsultant, specializing in riskmeasurementand valuation with a particular emphasis on illiquid and hard-to-value assets.Until his retirement in 2004, he was Managing Director in charge of riskmethodology at JPMorgan Chase, where he was responsible for modelvalidation, risk capital allocation, and the development of new measures ofvaluation,reserves,andriskforbothmarketandcreditrisk.Previously,hewasin charge ofmarket risk for derivative products at Chase. He has been a keyarchitectofChase'svalue-at-riskandstresstestingsystems.Priortohisworkinrisk management, Allen was the head of analysis and model building for allChasetradingactivitiesforovertenyears.Since1998,Allenhasbeenassociatedwith theMathematics in FinanceMasters' program at New York University'sCourant Institute ofMathematical Sciences. In this program, he has served asClinical Associate Professor and Deputy Director and has created and taughtcoursesinriskmanagement,derivativesmathematics,andinterestrateandcreditmodels. He was a member of the Board of Directors of the InternationalAssociation of FinancialEngineers and continues to serve as co-chair of theirEducationCommittee.

CHAPTER1

Introduction

1.1LESSONSFROMACRISISI began the first edition of this book with a reference to an episode of thetelevision series Seinfeld in which the character George Costanza gets anassignmentfromhisbosstoreadabooktitledRiskManagementandthengiveareport on this topic to other business executives.Costanza finds the book andtopicsoboringthathisonlysolutionistoconvincesomeoneelsetoreaditforhim and prepare notes. Clearly, my concern at the time was to write aboutfinancial riskmanagement in away thatwould keep readers from finding thesubject dull. I could hardly have imagined then that eight years later DemiMoore would be playing the part of the head of an investment bank's riskmanagement department in a widely released movie,MarginCall. Even lesscouldIhaveimaginedtheterribleeventsthatplacedfinancialriskmanagementinsuchaharshspotlight.Myconcernnowisthattheglobalfinancialcrisisof2007–2008mayhaveled

totheconclusionthatriskmanagementisanexcitingsubjectwhosepractitionersand practices cannot be trusted. I have thoroughly reviewed the material Ipresented in the first edition, and it still seems to me that if the principles Ipresented,principlesthatrepresentedindustrybestpractices,hadbeenfollowedconsistently, a disaster of themagnitudewe experiencedwould not have beenpossible. In particular, the points Imade in the first edition about using stresstestsinadditiontovalueatrisk(VaR)indeterminingcapitaladequacy(seethelast paragraphs of Section 7.3 in this edition) and the need for substantialreservesanddeferredcompensationforilliquidpositions(seeSections6.1.4and8.4 in this edition) still seem sound. It is tempting to just restate the sameprinciplesandurgemorediligenceintheirapplication,butthatappearstoocloseto the sardonic definition of insanity: “doing the same thing and expectingdifferent results.” So I have looked for places where these principles needstrengthening(you'llfindasummaryinSection5.4).ButIhavealsoreworkedtheorganizationofthebooktoemphasizetwocoredoctrinesthatIbelieveare

thekeystotheunderstandingandproperpracticeoffinancialriskmanagement.The first core principle is that financial risk management is not just risk

management as practiced in financial institutions; it is risk management thatmakesactiveuseoftradinginliquidmarketstocontrolrisk.Riskmanagementisa discipline that is important to a wide variety of companies, governmentagencies,andinstitutions—oneneedonlythinkofaccidentpreventionatnuclearpower plants and public healthmeasures to avoid influenza pandemics to seehowcriticalitcanbe.Whiletheriskmanagementpracticedatinvestmentbanksshares some techniques with risk management practiced at a nuclear facility,thereremainsonevitaldifference:muchof theriskmanagementat investmentbankscanutilizeliquidmarketsasakeyelementinriskcontrol;liquidmarketsareofvirtuallynousetothenuclearsafetyengineer.Myexpertiseisinthetechniquesoffinancialriskmanagement,andthatisthe

primarysubjectof thisbook.Somerisksthatfinancialfirmstakeoncannotbemanagedusingtradinginliquidmarkets.Itisvitallyimportanttoidentifysuchrisksandtobeawareofthedifferentriskmanagementapproachesthatneedtobe taken for them.Throughout the book Iwill be highlighting this distinctionandalsofocusingonthedifferencesthatdegreeofavailableliquiditymakes.Asshorthand, I will refer to risk that cannot be managed by trading in liquidmarketsasactuarialrisk, since it is the typeof risk thatactuariesat insurancecompanies have been dealing with for centuries. Even in cases that must beanalyzedusingtheactuarialriskapproach,financialriskmanagementtechniquescan still beuseful in isolating the actuarial risk and in identifyingmarketdatathat can be used as input to actuarial risk calculations. I will address this ingreaterdetailinSection1.2.The second core principle is that the quantification of risk management

requiressimulationguidedbybothhistoricaldataandsubjectivejudgment.Thisis a common feature of both financial risk and actuarial risk.The timeperiodsimulatedmayvarygreatly,fromvalueatrisk(VaR)simulationsofdailymarketmoves for very liquid positions to simulations spanning decades for actuarialrisk.ButIwillbeemphasizingsharedcharacteristicsforallofthesesimulations:thedesirabilityoftakingadvantageofasmuchhistoricaldataasisrelevant,theneedtoaccountfornonnormalityofstatisticaldistributions,andthenecessityofincludingsubjectivejudgment.MoredetailsontheserequirementsareinSection1.3.

1.2FINANCIALRISKANDACTUARIALRISK

Themanagementoffinancialriskandthemanagementofactuarialriskdosharemanymethodologies,apoint thatwillbeemphasized in thenextsection.Bothrely on probability and statistics to arrive at estimates of the distribution ofpossible losses. The critical distinction between them is the matter of time.Actuarialrisksmaynotbefullyresolvedforyears,sometimesevendecades.Bythe timethe trueextentof losses isknown, theaccumulationofriskmayhavegone on for years. Financial risks can be eliminated in a relatively short timeperiodbytheuseofliquidmarkets.Continuousmonitoringofthepriceatwhichrisk can be liquidated should substantially lower the possibility of excessiveaccumulationofrisk.Two caveats need to be offered to this relatively benign picture of financial

risk.Thefirstisthattakingadvantageoftheshortertimeframeoffinancialriskrequires constant vigilance; if you aren't doing a good job ofmonitoring howlarge your risks are relative to liquidation costs, you may still acquire moreexposurethandesired.ThiswillbedescribedindetailinChapter6.Thesecondis the need to be certain that what is truly actuarial risk has not beenmisclassifiedasfinancialrisk.Ifthisoccurs,itisespeciallydangerous—notonlywillyouhavethepotentialaccumulationofriskoveryearsbeforetheextentoflosses is known, but in not recognizing the actuarial nature, you would notexercise thecaution that theactuarialnatureof the riskdemands.Thiswillbeexamined more closely in Sections 6.1.1 and 6.1.2, with techniques formanagementofactuarialriskinfinancialfirmsoutlinedinSection8.4.Ibelievethatthisdangerousmuddlingoffinancialandactuarialriskwasakeycontributortothe2007–2008crisis,asIargueinSection5.2.5.Ofcourse, it isonlyanapproximationtoviewinstrumentsasbeingliquidor

illiquid.Thevolumeof instrumentsavailablefor tradingdifferswidelybysizeand readiness of availability.This constitutes the depth of liquidity of a givenmarket.Oftenafirmwillbefacedwithachoicebetweentherisksofreplicatingpositions more exactly with less liquid instruments or less exactly with moreliquidinstruments.Onethemeof thisbookwillbe thetrade-offbetweenliquidityriskandbasis

risk.Liquidityriskistheriskthatthepriceatwhichyoubuy(orsell)somethingmaybesignificantly lessadvantageousthanthepriceyoucouldhaveachieved

undermoreidealconditions.Basisriskistheriskthatoccurswhenyoubuyoneproduct and sell another closely related one, and the two prices behavedifferently.Let's lookatanexample.Supposeyouareholdingalargeportfolioofstocksthatdonottradethatfrequentlyandyouroutlookforstockpricesleadstoadesiretoquicklyterminatetheposition.Ifyoutrysellingthewholebasketquickly, you face significant liquidity risk since your sellingmay depress theprices atwhich the stocks trade.An alternativewould be to take anoffsettingposition inaheavily traded stock futurescontract, suchas the futurescontracttiedtotheStandard&Poor's™S&P500stockindex.Thislowerstheliquidityrisk,but it increasesthebasisrisksincechangesinthepriceofyourparticularstockbasketwillprobablydifferfromthepricechangesinthestockindex.Oftentheonlywayinwhichliquidityriskcanbereducedistoincreasebasisrisk,andtheonlywayinwhichbasisriskcanbereducedistoincreaseliquidityrisk.Theclassificationofriskasfinancialriskoractuarialriskisclearlyafunction

of the particular type of risk and not of the institution. Insurance againsthurricane damage could be written as a traditional insurance contract byMetropolitan Life or could be the payoff of an innovative new swap contractdesigned byMorgan Stanley; in either case, itwill be the same risk.What isrequiredineithercaseisanalysisofhowtradinginliquidmarketscanbeusedtomanage the risk. Certainly commercial banks have historically managedsubstantial amounts of actuarial risk in their loan portfolios. And insurancecompanies have managed to create some ability to liquidate insurance riskthroughthereinsurancemarket.Evenindustrialfirmshavestartedexploringthepossible transformation of some actuarial risk into financial risk through thetheory of real options. An introduction to real options can be found in Hull(2012,Section34)andDixitandPindyck(1994).A useful categorization to make in risk management techniques that I will

sometimesmakeuseof,followingGumerlock(1999),istodistinguishbetweenrisk management through risk aggregation and risk management through riskdecomposition.Riskaggregationattemptstoreduceriskbycreatingportfoliosofless than completely correlated risk, thereby achieving risk reduction throughdiversification.Riskdecompositionattemptstoreduceariskthatcannotdirectlybepricedinthemarketbyanalyzingitintosubcomponents,allorsomeofwhichcan be priced in the market. Actuarial risk can generally be managed onlythroughriskaggregation,whereasfinancialriskutilizesbothtechniques.Chapter7 concentrates on risk aggregation,while Chapter 8 primarily focuses on riskdecomposition;Chapter6addressestheintegrationofthetwo.

1.3SIMULATIONANDSUBJECTIVEJUDGMENT

Nobodycanguaranteethatallpossiblefuturecontingencieshavebeenprovidedfor—thisissimplybeyondhumancapabilitiesinaworldfilledwithuncertainty.But it is unacceptable to use that platitude as an excuse for complacency andlack of meaningful effort. It has become an embarrassment to the financialindustry to see thenumberof events that aredeclared “once in amillennium”occurrences,basedonananalysisofhistoricaldata,when theyseeminfact totake place every few years. At one point I suggested, only half-jokingly, thatanyone involved in riskmanagementwhoused thewordsperfectandstorm inthe same sentence should be permanently banned from the financial industry.More seriously, everyone involved in riskmanagementneeds tobe aware thathistorical data has a limited utility, and that subjective judgment based onexperienceandcarefulreasoningmustsupplementdataanalysis.Thefailureofriskmanagerstoapplycriticalsubjectivejudgmentasacheckonhistoricaldataintheperiodleadingtothecrisisof2007–2008isaddressedinSection5.2.5.Thisbynomeansimpliesthathistoricaldatashouldnotbeutilized.Historical

data,ataminimum,suppliesacheckagainst intuitionandcanbeused tohelpformreasonedsubjectiveopinions.Butriskmanagersconcernedwithprotectinga firm against infrequent but plausible outcomes must be ready to employsubjectivejudgment.Letusillustratewithasimpleexample.Supposeyouaretryingtodescribethe

distributionofavariableforwhichyouhavealotofhistoricaldatathatstronglysupportsanormaldistributionwithameanof5percentandstandarddeviationof 2 percent. Suppose you suspect that there is a small but nonnegligiblepossibility that therewill be a regime change thatwill create a very differentdistribution.Let'ssayyouguessthereisa5percentchanceofthisdistribution,which you estimate as a normal distribution with a mean of 0 percent andstandarddeviationof10percent.If all you cared about was the mean of the distribution, this wouldn't have

much impact—lowering themean from5percent to4.72percent.Even ifyouwereconcernedwithbothmeanandstandarddeviation,itwouldn'thaveahugeimpact: the standard deviation goes up from 2 percent to 3.18 percent, so theSharpe ratio (the ratio of mean to standard deviation often used in financialanalysis)would drop from2.50 to 1.48.But if youwere concernedwith how

largealossyoucouldhave1percentofthetime,itwouldbeachangefromagain of 0.33 percent to a loss of 8.70 percent. Exercise 1.1will allow you tomake these and related calculations for yourself using the Excel spreadsheetMixtureOfNormalssuppliedonthebook'swebsite.This illustrates the point that when you are concerned with the tail of the

distributionyouneedtobeveryconcernedwithsubjectiveprobabilitiesandnotjustwithobjectivefrequencies.Whenyourprimaryconcernisjustthemean—oreventhemeanandstandarddeviation,asmightbetypicalforamutualfund—thenyourprimaryfocusshouldbeonchoosingthemostrepresentativehistoricalperiodandonobjectivefrequencies.Whilethisexamplewasdrawnfromfinancialmarkets,theconclusionswould

look very similar ifwewere discussing an actuarial risk problem like nuclearsafetyandweweredealingwithpossibledeathsratherthanfinanciallosses.Thefact that risk managers need to be concerned with managing against extremeoutcomes would again dictate that historical frequencies need to besupplementedbyinformedsubjectivejudgments.Thisreasoningisverymuchinlinewiththeprevailing(butnotuniversal)beliefsamongacademicsinthefieldsofstatisticsanddecisiontheory.AgoodsummaryofthecurrentstateofthinkinginthisareaistobefoundinHammond,Keeney,andRaiffa(1999,Chapter7).Rebonato (2007) isa thoughtfulbook-length treatmentof these issues fromanexperienced and respected financial risk manager that reaches conclusionsconsistentwiththosepresentedhere(seeparticularlyChapter8ofRebonato).Theimportanceofextremeeventstoriskmanagementhastwootherimportant

consequences.Oneisthatinusinghistoricaldataitisnecessarytopayparticularattentiontotheshapeofthetailofthedistribution;allcalculationsmustbebasedon statistics that take into account any nonnormality displayed in the data,including nonnormality of correlations. The second consequence is that allcalculations must be carried out using simulation. The interaction of inputvariables in determining prices and outcomes is complex, and shortcutcomputationsforestimatingresultsworkwellonlyforaverages;assoonasyouarefocusedonthetailsofthedistribution,simulationisanecessityforaccuracy.Theuseof simulationbasedonbothhistoricaldata and subjective judgment

andtakingnonnormalityofdataintoaccountisarepeatedthemethroughoutthisbook—in the statement of general principles inSection6.1.1, applied tomoreliquid positions throughout Chapter 7, applied to positions involving actuarialrisk inSection8.4, andapplied to specific riskmanagement issues throughoutChapters9through14.

EXERCISE1.1TheImpactofNonnormalDistributionsonRisk

UsetheMixtureOfNormalsspreadsheettoreproducetheriskstatisticsshowninSection1.3(youwillnotbeabletoreproducetheseresultsprecisely,duetotherandomelementofMonteCarlosimulation,butyoushouldbeabletocomeclose).Experimentwithraisingtheprobabilityoftheregimechangefrom5percentto10percentorhighertoseethesensitivityoftheseriskstatisticstotheprobabilityyouassigntoanunusualoutcome.Experimentwithchangesinthemeanandstandarddeviationofthenormaldistributionusedforthislower-probabilityeventtoseetheimpactofthesechangesontheriskstatistics.

CHAPTER2

InstitutionalBackgroundAfinancialfirmis,amongotherthings,aninstitutionthatemploysthetalentsofa variety of different people, each with her own individual set of talents andmotivations. As the size of an institution grows, it becomesmore difficult toorganize these talents and motivations to permit the achievement of commongoals.Evensmallfinancialfirms,whichminimizethecomplexityofinteractionof individuals within the firm, must arrange relationships with lenders,regulators,stockholders,andotherstakeholdersinthefirm'sresults.Since financial risk occurs in the context of this interaction between

individualswith conflicting agendas, it shouldnot be surprising that corporateriskmanagersspendagooddealoftimethinkingaboutorganizationalbehavioror that their discussions aboutmathematicalmodels used to control risk oftenfocuson theorganizational implicationsof thesemodels. Indeed, ifyou takearandomsampleof theconversationsof senior riskmanagerswithina financialfirm,youwill findasmanyreferences tomoralhazard,adverseselection,andPonzischeme(termsdealingprimarilywithissuesoforganizationalconflict)asyouwillfindreferencestodelta,standarddeviation,andstochasticvolatility.Foranunderstandingoftheinstitutionalrealitiesthatconstitutetheframework

inwhich risk ismanaged, it is best to startwith the concept ofmoral hazard,whichliesattheheartoftheseconflicts.

2.1MORALHAZARD—INSIDERSANDOUTSIDERS

ThefollowingisadefinitionofmoralhazardtakenfromKotowitz(1989):Moral hazardmay be defined as actions of economic agents inmaximizingtheir own utility to the detriment of others, in situationswhere they do notbear the full consequences or, equivalently, do not enjoy the full benefits oftheiractionsduetouncertaintyandincompleteorrestrictedcontractswhichpreventtheassignmentoffulldamages(benefits)totheagentresponsible....Agents may possess informational advantages of hidden actions or hiddeninformation or there may be excessive costs in writing detailed contingent

contracts. . . .Commonlyanalyzedexamplesofhiddenactionsareworkers'efforts,whichcannotbecostlesslymonitoredbyemployers,andprecautionstakenbytheinsuredtoreducetheprobabilityofaccidentsanddamagesduetothem, which cannot be costlessly monitored by insurers. . . . Examples ofhidden information are expert services—such as physicians, lawyers,repairmen,managers,andpoliticians.In the context of financial firm risk, moral hazard most often refers to the

conflict between insiders and outsiders based on a double-edged asymmetry.Information is asymmetrical—the insiders possess superior knowledge andexperience.Theincentivesarealsoasymmetrical—theinsidershaveanarrowersetofincentivesthantheoutsidershave.Thisthemerepeatsitselfatmanylevelsofthefirm.Let's begin at the most basic level. For any particular group of financial

instruments that a firmwants to deal in,whether it consists of stocks, bonds,loans, forwards, or options, the firm needs to employ a group of expertswhospecialize in this group of instruments. These experts will need to have athoroughknowledgeof the instrument thatcan rival theexpertiseof the firm'scompetitors in this segment of the market. Inevitably, their knowledge of thesectorwillexceedthatofotheremployeesofthefirm.Evenifitdidn'tstartthatway,theexperiencegainedbyday-to-daydealingsinthisgroupofinstrumentswill result in information asymmetry relative to the rest of the firm. Thisinformation asymmetry becomes even more pronounced when you considerinformation relative to theparticular positions in those instruments intowhichthefirmhasentered.Thefirm'sexpertshavecontractedforthesepositionsandwillcertainlypossessafarmore intimateknowledgeof themthananyoneelseinsideoroutside the firm.Agenericnameusedwithin financial firms for thisgroupofexperts is the frontoffice.A largefrontofficemaybedividedamonggroupsofspecialists: thosewhonegotiate transactionswithclientsof thefirm,whoareknownassalespeople,marketers,orstructurers;thosewhomanagethepositionsresultingfromthesenegotiatedtransactions,whoareknownastraders,positionmanagers,orriskmanagers;andthosewhoproduceresearch,models,or systems supporting the process of decision making, who are known asresearchersortechnologists.However,thisgroupofexpertsstillrequiresthebackingoftherestofthefirm

inordertobeabletogeneraterevenue.Someofthisdependencemaybeaneedtousethefirm'sofficesandequipment;specialistsinareasliketax,accounting,law,andtransactionsprocessing;andaccesstothefirm'sclientbase.However,

theseareservicesthatcanalwaysbecontractedfor.Thevitalneedforbackingisthefirm'sabilitytoabsorbpotentiallossesthatwouldresultifthetransactionsdonotperformasexpected.AforcefulillustrationofthisdependenceisthecaseofEnron,whichin2001

wasadominantforceintradingnaturalgasandelectricity,beingapartytoabout25 percent of all trades executed in thesemarkets. Enron's experts in tradingthese products and the web-enabled computer system they had built to allowclients to tradeonlinewerewidely admired throughout the industry.However,when Enron was forced to declare bankruptcy by a series of financing andaccountingimproprietiesthatwerelargelyunrelatedtonaturalgasandelectricitytrading,theirdominanceinthesemarketswaslostovernight.Why?Thetradersandsystemsthatweresowidelyadmiredwerestillinplace.

Their reputationmayhavebeendamaged somewhat basedon speculation thatthecompany'sreportingwasnothonestanditstradingoperationwasperhapsnotas successful as had been reported. However, this would hardly have beenenoughtoproducesuchalargeeffect.Whathappenedwasanunwillingnessoftrading clients to deal with a counterparty that might not be able to meet itsfuturecontractualobligations.Without thebackingof theparentfirm'sbalancesheet,itsstockholderequity,anditsabilitytoborrow,thetradingoperationcouldnotcontinue.So now we have the incentive asymmetry to set off the information

asymmetry. The wider firm, which is less knowledgeable in this set ofinstruments than the group of front-office experts,must bear the full financiallossifthefrontoffice'spositionsperformbadly.Themoralhazardconsistsofthepossibility that the front officemay bemorewilling to risk the possibility oflarge losses in which it will not have to fully share in order to create thepossibilityof largegains inwhich itwillhaveafullshare.Andtherestof thefirmmaynothavesufficientknowledgeofthefrontoffice'spositions,duetotheinformationasymmetry,tobesurethatthishasnotoccurred.What are some possible solutions? Could a firm just purchase an insurance

contractagainsttradinglosses?Thisishighlyunlikely.Aninsurancefirmwouldhave even greater concerns aboutmoral hazard because it would not have asmuchaccesstoinformationasthosewhoareatleastwithinthesamefirm,evenif they are less expert.Could the firmdecide to structure the pay of the frontoffice so that it will be the same no matter what profits are made on itstransactions,removingthetemptationtotakeexcessiverisktogeneratepotentiallargegains?Thefirmcould,butexperienceinfinancialfirmsstronglysuggests

theneedforupsideparticipationasanincentivetocallforththeeffortsneededtosucceedinahighlycompetitiveenvironment.Inevitably,thesolutionseemstobeanongoingstruggletobalancetheproper

incentivewiththepropercontrols.Thisistheveryheartofthedesignofariskmanagementregime.Ifthefirmexercisestoolittlecontrol,theopportunitiesformoralhazardmayprovetoogreat.Ifitexercisestoomuchcontrol,itmaypassupgoodprofitopportunitiesifthosewhodonothaveasmuchknowledgeasthefrontofficemakethedecisions.Totrytoachievethebestbalance,thefirmwillemployexpertsinriskmanagementdisciplinessuchasmarketrisk,creditrisk,legalrisk,andoperationsrisk.Itwillsetupindependentsupportstafftoprocessthetradesandmaintaintherecordsofpositionsandpayments(thebackoffice);report positions against limits, calculate the daily profit and loss (P&L), andanalyzethesourcesofP&Landrisk(themiddleoffice);andtakeresponsibilityfortheaccuracyofthefirm'sbooksandrecords(thefinancefunction).However,thetwo-sidedasymmetryofinformationandincentivewillalwaysexist,asthepersonnel in these control and support functions will lack the specializedknowledgethatthefrontofficepossessesintheirsetofinstruments.The two-sided asymmetry that exists at this basic level can be replicated at

other levels of the organization, depending on the size and complexity of thefirm.The informationaldisadvantageof themanagerof fixed-incomeproductsrelative to the front office for European bonds will be mirrored by theinformationaldisadvantageofthemanagerofalltradingproductsrelativetothemanageroffixed-incomeproductsandthefirm'sCEOrelativetothemanagerofalltradingproducts.Certainly, the two-sided asymmetry will be replicated in the relationship

betweenthemanagementof thefirmandthosewhomonitor thefirmfromtheoutside.Outsidemonitorsprimarilyrepresentthreegroups—thefirm'screditors(lendersandbondholders),thefirm'sshareholders,andgovernments.Allthreeofthesegroupshaveincentivesthatdifferfromthefirm'smanagement,astheyareexposedtolossesbasedonthefirm'sperformanceinwhichthemanagementwillnotfullyshare.Theexistenceof incentive asymmetry for creditors is reasonablyobvious. If

thefirmdoeswell,thecreditorsgettheirmoneyback,buttheyhavenofurtherparticipationinhowwellthefirmperforms;ifthefirmdoesverybadlyandgoesbankrupt, thecreditorshavesubstantial,possiblyeventotal, lossoftheamountlent.Bycontrast,thefirm'sshareholdersandmanagementhavefullparticipationwhenthefirmperformswell,butliabilityinbankruptcyislimitedtotheamount

originallyinvested.WhenweexaminecreditriskinSection13.2.4,thiswillbeformallymodeledasthecreditorssellingaputoptiononthevalueofthefirmtotheshareholders.Sincealloptionscreatenonlinear(henceasymmetric)payoffs,wehaveaclearsourceofincentiveasymmetryforcreditors.It is less clear whether incentive asymmetry exists for shareholders. In

principle, their interests are supposed to be exactly aligned with those of thefirm's management, and incentives for management based on stock value areused to strengthen this alignment. In practice, it is always possible thatmanagement will take more risk than shareholders would be completelycomfortablewithinthehopeofcollectingincentive-basedcompensationingoodperformanceyears thatdoesnothave tobereturnedinbadperformanceyears.Kotowitz(1989)quotesAdamSmithfromWealthofNations:“Thedirectorsofsuchcompanies,however,beingmanagers ratherofotherpeople'smoney thanoftheirown,itcannotwellbeexpected,thattheyshouldwatchoveritwiththesameanxiousvigilancewithwhichthepartnersinaprivatecompanyfrequentlywatchovertheirown.”Government involvement arises from the asymmetric dangers posed to the

health of theoverall economyby the failure of a financial firm. If an implicitgovernmentguarantee isgiven to rescue large financial firms frombankruptcy(the notion of “too big to fail”), then moral hazard is created throughmanagement'sknowledgethat itcantry tocreateprofitopportunities, inwhichthegovernmenthasonly limitedparticipation through taxes,by takingrisksoflossesthatwillneedtobefullyabsorbedbythegovernment.Ifthegovernmentisnotwillingtopreventthefailureoflargefinancialfirms,thenitwillwanttoplacerestrictionsontheexternalitiesthatthosefirmscancreatebynothavingtobear their share of the cost to the overall economy of a firm's potentialbankruptcy.Inallthreecasesofmoralhazardinvolvingoutsidemonitors,theinformation

asymmetry is even more severe than when the information asymmetry takesplacewholly inside the firm. Seniormanagement and its riskmonitors are atleast on the premises, are involved in day-to-day business with more juniormanagers, andcanutilize informalmeasures, suchas the rotationofmanagersthroughdifferentsegmentsofthefirm,toattempttodiffusebothincentivesandknowledge. Outsidemonitors will have only occasional contact with the firmandmustrelymostlyonformalrequirementstoobtaincooperation.Letus lookat someof theoutsidemonitors that creditors, shareholders, and

governmentsrelyon:

Inadditiontotheirowncreditofficers,creditorsrelyonratingagenciessuchasMoody'sInvestorsServiceandStandard&Poor's(S&P)toobtaininformationaboutandmakejudgmentsonthecreditworthinessofborrowers.Shareholdersandcreditorsrelyoninvestmentanalystsworkingforinvestmentbankersandbrokeragefirmstoobtaininformationaboutandmakejudgmentsonthefutureearningsprospectsandsharevaluesoffirms.Althoughneitherratingagenciesnorinvestmentanalystshaveanyofficialstandingwithwhichtoforcecooperationfromthefirmstheyanalyze,theirinfluencewithlendersandinvestorsinbondsandstocksgivesthemtheleveragetoobtaincooperationandaccesstoinformation.Governmentscanusetheirregulatorypowerstorequireaccesstoinformationfromfinancialfirmsandemploylargestaffstoconductexaminationsofthefirms.Forexample,fortheU.S.government,theFederalReserveSystemandtheComptrolleroftheCurrencyconductexaminationsofcommercialbanks.AsimilarfunctionisperformedbytheSecuritiesandExchangeCommission(SEC)forinvestmentbanks.Creditors,shareholders,andgovernmentsallrelyonindependentaccountingfirmstoconductauditsofthereliabilityofthefinancialinformationdisclosuresthatarerequiredofallpubliclyheldfirms.

Over the years, many critical questions have been raised about how trulyindependentthejudgmentoftheseoutsidemonitorsreallyis:

Creditratingagencieshavebeenaccusedofbeingtooslowtodowngraderatingsinresponsetoadversechangesinafirm'sfinancialconditionbecausetheirsourceofrevenuecomesfromthefirmswhosedebttheyrate.Similarly,independentauditorshavebeensuspectedofbeingtoodeferentialtothefirmstheymonitorsincethesefirmsaretheoneswhopaytheirauditfeesandhirethemforconsultingservices.Thefearisthatthedesireformorerevenuewillbluntobjectionstocompanieschoosingaccountingmethodsthatcasttheirresultsinafavorablelight.Investmentbankshaveabuilt-inconflictofinterestfromcompetingforthebusinessofthefirmswhoseperformancetheirinvestmentanalystsaremonitoring.Ithaslongbeennotedthatanalysts'buyrecommendationsfaroutnumbersellrecommendations.Accusationshavebeenleveledthatgovernmentregulatoryagenciesaremoreconcernedwithprotectingtheinterestsofthefirmsbeingmonitoredthanwithprotectingthepublicinterest.Thesechargeshaveparticularforce

whenpersonnelflowfreelybetweenemploymentintheregulatoryagenciesandinthefirmstheyregulate.

All of these criticisms seemed to be coming to a head in 2002 amid thescandals involving the now-defunct auditing firmofArthurAndersen,Enron'sdeclarationofbankruptcyonly aweekafterbeing rated investmentgrade, andthemassive declines in the stock values of technology firms highly touted byinvestment analysts. Some useful reforms have been undertaken, such asforbiddingauditingfirmstosellconsultingservicestofirmstheyauditandnotallowing the bonuses of investment analysts to be tied to investment bankingfeescollectedfromclientswhosestockstheycover.However,thebasicsourcesofconflictofinterestremain,andinvestorsandlenderswillcontinuetoneedtoemployaskepticalfilterwhenutilizinginputfromoutsidemonitors.Although the conflicts between insiders and outsiders due to the two-sided

asymmetryofmoralhazardcannotbeeliminated,afrankunderstandingbybothsides can lead to a cooperative relationship. In a cooperative relationship,insiderswillacknowledgetheneedtohaveoutsidersexercisecontrolsandwillvoluntarily share information and knowledge with outsiders. In a cooperativerelationship,outsiderswillacknowledgetheirneedtolearnfromtheinsidersandwilleasecontrolsinresponsetoatrackrecordofopenness,althoughbothmustrecognize the need to always have some level of controls (the ancient folkwisdom states that “I trustmygrandmother, but I still cut the cardswhen shedeals”).A lack of understanding of moral hazard can lead to an uncooperative

relationshipfueledbymutualresentmentsbetweenaninsider,suchasatraderorstructurer,with an outsider, such as a corporate riskmanager or regulator.Aninsiderwhodoesnotunderstandthepurelysituationalneedtohavesomeonelessknowledgeable“lookovermyshoulder”willattribute it toaninsultinglackofpersonal trust, an arrogant assumption of more knowledge than the otherpossesses,orasimpledesirebytheoutsidertocreateajoborgrabpower(whichisnottosaythatsomeofthesemotivationsdonotexistinreality,mixedinwiththeneedtocontrolmoralhazard).Theinsider'sresponsewillthenprobablybetowithhold information, obfuscate, andmislead,whichwill drive the outsider toevencloserscrutinyandmorerigidcontrols,whichisclearlyaprescriptionforavicious circle of escalation. An outsider who lacks an understanding of thesituation may defensively try to pretend to have more knowledge than heactually has or may denigrate the knowledge of the insider, which will onlyexacerbateanysuspicionsoftheprocesstheinsiderhas.

Moralhazardhaslongbeenakeyconceptintheanalysisofinsurancerisks.Atypical example would be an insurance company's concern that an individualwhohaspurchasedinsuranceagainstautotheftwillnotexerciseasmuchcareinguardingagainsttheft(forexample,parkinginagarageratherthanonthestreet)as one who has not purchased insurance. If the insurance company coulddistinguishbetweenindividualswhoexerciseextracareandthosewhodon't,itcouldsellseparatecontracts to the twotypesof individualsandprice theextralosses into just the type sold to those exercising less care. However, theinformation advantage of an individual monitoring his own degree of carerelativetotheinsurancecompany'sabilitytomonitoritmakesthisprohibitivelyexpensive.Sotheinsurancecompanyneedstosettleforcrudermeasures,suchasestablishingadeductiblelossthattheinsuredpersonmustpayintheeventoftheft,therebyaligningtheinterestsoftheinsuredmorecloselywiththeinsurer.Ithasbecomeincreasinglycommonformoralhazardtobecitedinanalysesof

theeconomicsoffirmsingeneral,particularlyinconnectionwiththeimpactofthe limited liability of shareholders willing to take larger gambles. Theshareholdersknowthatif thegamblesucceeds,theywillavoidbankruptcyandshareintheprofits,butwillsuffernogreaterlossinalargebankruptcythaninasmallerone.ToquoteW.S.Gilbert:Youcan'tembarkontradingtootremendous,It'sstrictlyfairandbasedoncommonsense,Ifyousucceed,yourprofitsarestupendous,Andifyoufail,popgoesyoureighteenpence.

(fromGilbertandSullivan'sUtopia,Limited)A firm's creditors can exercise somecontrol over their actions andmightbe

able to forbid such gambles, assuming they have sufficient knowledge of thenature of the firm's investments.This iswhere the informational advantage ofthemanagersoverthecreditorswithrespecttothefirm'sinvestmentscomesin.What sort of actions can we expect from a trader based on the concept of

moral hazard? We can certainly expect that the trader may have a differentdegreeof riskaversion than thefirm'smanagement,since traders'participationinfavorableresultsexceedstheirparticipationindownsideresults.Taleb(1997,66)referstothisasthetrader“owninganoptiononhisprofits”andstatesthatinsuch circumstances “it is always optimal to take asmuch risk as possible.Anoptionisworththemostwhenvolatilityishighest.”Thiswillprobablybecomeevenmorenoticeableifthetraderhasbeenhavingapooryear.Knowingthatshe

isheadedtowardaminimalbonusandpossibledismissalmayinclinethetraderto swing for the fencesand takea large risk.The traderknows that if the riskturns out favorably, it might be enough to reverse previous losses and earn abonus.Ifitturnsoutpoorly,then“youcan'tgetlessthanazerobonus”and“youcan't get fired twice.” (You can damage your reputation in the industry, butsharing information about a trader's track record between competitor firmscannotbedonethatefficiently—moreinformationasymmetry.)Forthisreason,firmsmayseverelycutthetradinglimitsofatraderhavingapooryear.Beyond thedifferences in risk aversion,moral hazard can even result in the

perverse behavior (for the firm) of having a trader willing to increase riskexposure when faced with a lower expected return. Consider the followingadvicetotradersfromTaleb(1997,65):Howaggressiveatraderneedstobedependshighlyonhisedge,orexpectedreturnfromthegame:Whentheedgeispositive(thetraderhasapositiveexpectedreturnfromthegame,asisthecasewithmostmarketmakers),itisalwaysbesttotaketheminimumamountofriskandletcentrallimitslowlypushthepositionintoprofitability.Thisistherecommendedmethodformarketmakerstoprogressivelyincreasethestakes,inproportiontotheaccumulatedprofits.Inprobabilityterms,itisbettertominimizethevolatilitytocash-inonthedrift.Whentheedgeisnegative,itisbesttobeexposedaslittleaspossibletothenegativedrift.Theoperatorshouldoptimizebytakingasmuchriskaspossible.Bettingsmallwouldensureaslowandcertaindeathbylettingcentrallimitcatchuponhim.

The mathematics and economic incentives that this advice is based on arecertainlysound.Itisadvicethatisknowntoeverygambler(oroughttobe)andiswellfoundedinstatisticaltheory.Whentheoddsareinyourfavor,placemanysmallbets;whentheoddsareagainstyou,placeonelargebet.Essentially,whentheoddsareagainstyou,youareattemptingtominimizethelengthoftimeyouare playing against the house since you are paying a tax, in the form of anexpectedloss,fortheprivilegeofplaying.However,although thismakesperfecteconomicsensefromtheviewpointof

the individual trader, it is hardly the strategy the firmemploying these traderswouldwant to see them follow.The firm,whoseP&Lwill be the sumof theresultsofmanytraders,wouldliketoseetraderswithanegativeexpectedreturn

not takeanypositionsatall rather thanhavethesebe the traders takingonthemostrisk.Totheextentthefirm'smanagementcanfigureoutwhichtradershavea negative edge, it will restrict their risk taking through limits and thereplacementofpersonnel.However,theindividualtradershavetheinformationadvantageinknowingmorethanthefirmabouttheirexpectedreturns.Theyalsohave the asymmetrical incentive to take larger risks in this case, even thoughdoing sowill probablyhurt the firm.The traderswill notderivemuchbenefitfrom the firmdoingwell if theydonot contribute to that result, but theywillbenefitiftheydoincreasetheirriskandwinagainsttheodds.Moral hazard helps to explain the valuation that investors place on the

earningsvolatilityof financial firms.Youcould argue that firms shouldworryjust about the expectedvalueandnot aboutvolatility, since themarket shouldplacea riskpremiumonlyon risk that it cannothedgeaway (an investorwhowants less risk will just take the stock with the highest expected return anddiversify by mixing with government bonds). However, empirical evidenceshows that themarketplacesa stiffdiscountonvariable tradingearnings.Thereasonmaybeinformationasymmetry.Itishardforoutsiderstotellwhetherafirmis takingsoundgambles tomaximizeexpectedvalueor ismaximizing itsinsiders'optiononone-waybets.Perold(1998)states:Iviewfinancial intermediariesasbeingspecial inseveralways:First, thesefirms are in credit-sensitive businesses, meaning that their customers arestrongly risk-aversewith respect to issuerdefaultoncontractuallypromisedpayoffs. (For example, policyholders are averse to having their insuranceclaimsbesubjecttotheeconomicperformanceoftheissuingfirm,andstrictlyprefertodobusinesswithahighlyratedinsurer.)Thecreditworthinessoftheintermediary is crucial to its ability to write many types of contracts, andcontractguaranteesfeatureimportantlyinitscapitalstructure.Second,financialfirmsareopaquetooutsiders.Theytendtobeinbusinessesthat depend vitally on proprietary financial technology and that cannot beoperatedtransparently.Inaddition,thebalancesheetsoffinancialfirmstendtobeveryliquid,andaresubjecttorapidchange.Financialfirms,thus,aredifficult to monitor, and bear significant deadweight costs of capital.Guarantorsfacecostsrelatedtoadverseselectionandmoralhazard....Third, financial firms are also internally opaque. Information tends to beprivateatthebusinessunitlevel,orevenatthelevelofindividualemployeessuchastraders.Efficientmanagementofthesefirmsthusinvolvessignificant

use of performance-related compensation to mitigate against monitoringdifficulty.Moralhazardcancreateabattlegroundoverinformationbetweeninsidersand

outsiders.Insidersarefearfulthatanyinformationobtainedbyoutsiderswillbeusedasatooltotightencontrolsoverinsiders'actions.Insiderscanbeexpectedto have an inherent bias against tighter controls, partly because narrowing therange of actions available leads to suboptimal solutions and partly becauseincentive asymmetry makes riskier action more rewarding to insiders than tooutsiders. One of the most common ways in which insiders can misleadoutsidersabouttheneedforcontrolsistermedaPonzischeme.

2.2PONZISCHEMESIn its original meaning, a Ponzi scheme is a criminal enterprise in whichinvestors are tricked into believing that theywill receive very high returns ontheirinvestments,buttheearlyinvestorsarepaidoutathighratesofreturnonlywiththepaymentscomingfromthecashinvestedbylaterinvestors.Theillusionofhighreturnscanbeprettyconvincing.Afterall,youcanactuallyseetheearlyinvestors receiving their high returns in cash, and the conmen running theseschemes can produce very plausible lies about the purported source of thereturns. As a result, the pace of new investment can be intense, enabling theillusionofprofit tobemaintainedovera fairly long timeperiod. It'saviciouscycle—theeagernessofnewinvestorstoplacemoneyintheschemeleadstotheheightenedabilitytomakeinvestmentsappearhighlyprofitable,whichleadstoevengreatereagernessofnewinvestors.However,ultimately,anyPonzischememust collapse, as there is no ultimate source of investment return (in fact,investmentreturnisquitenegative,astheflowofnewinvestmentmustalsobepartially diverted to the criminals profiting from it). Ponzi schemes are alsosometimescalledpyramidschemesandbearacloseresemblancetochainletterfrauds.WhenIwrotetheimmediatelyprecedingparagraphforthefirsteditionofthis

book in 2003, I felt the need to thoroughly explain what a Ponzi scheme is.Today,itisprobablynotnecessary,asBernieMadoffhasregrettablygivenusallanexhaustivelessoninhowaPonzischemeisrun.TheoriginalmeaningofPonzischemeshasbeenbroadenedbyriskmanagers

to include situations in which firms are misled as to the profitability of a

business linebytheinadequatesegregationofprofitsonnewlyacquiredassetsandreturnsonolderassets.Let's consider a typical example. Suppose a trading desk has entered into

marketinganewtypeofpath-dependentoption.Thedeskexpectssubstantiallymore customer demand for buying these options than for selling them. Theyintend tomanage the resulting riskwith dynamic hedging using forwards andmorestandardoptions.Aswewillseewhendiscussingpath-dependentoptionsinSection12.3,itisverydifficulttotrytoestimateinadvancehowsuccessfuladynamichedgingstrategyforpath-dependentoptionswillbe.Insuchcircumstances,thepricingoftheoptiontotheclientmustbebasedon

an estimate of the future cost of the dynamic hedging, applying someconservatismtotrytocovertheuncertainty.Let'sassumethatatypicaltradehasaseven-yearmaturity,andthatthecustomerpays$8millionandthefirmpays$5 million to purchase the initial hedge. Of the remaining $3 million, we'llassumethatthedeskisestimatingdynamichedgingcostsof$1millionoverthetwo years, but the uncertainty of these costs leads to setting up a $2 millioninitialallowance(orreserve)tocoverthehedgingcosts,leaving$1milliontobebookedasup-frontprofit.Suppose the tradingdeskhasmadea seriouserror inpredicting thehedging

costs,andthehedgingcostsactuallyenduparound$5million,leadingtoanetloss of $2 million on every transaction booked. You may not be able to doanything about deals already contracted, but you would at least hope to getfeedbackfromthelossesencounteredonthesedealsintimetostopbookingnewdealsorelseraiseyourpricetoamoresustainablelevel.ThisshouldhappenifP&Lreportingisadequatelydetailed,soyoucanseethelossesmountinguponthehedgingofthesetrades(thisiscalledhedgeslippage).However, it isoftendifficult tokeep trackofexactlyhowtoallocateaday's

tradinggainsandlossestothebookofdealsbeinghedged.Youwanttoatleastknow that trading losses are occurring so you can investigate the causes. Themost severe problem would be if you didn't realize that trades were losingmoney.Howcouldthishappen?IfP&Lreportingisnotadequatelydifferentiatedbetween the existing business and new business, then the overall tradingoperation can continue to look profitable by just doing enough new business.Every time a new deal is booked, $1million goes immediately into P&L.Ofcourse,themoredealsthatarebooked,thelargerthehedginglossesthatmustbeovercome, so evenmore new trades are needed to swamp the hedging losses.TheresemblancetoaPonzischemeshouldnowbeobvious.

One key difference is that in its original meaning, the Ponzi scheme is adeliberate scam. The financial situation described is far more likely to arisewithoutanydeliberateintent.However,thoseinthefrontoffice,basedontheircloseknowledgeofthetradingbook,willoftensuspectthatthissituationexistsbeforeanyoutsidersdo,butmaynotwanttoupsettheapplecart.Theywouldbejeopardizingbonusesthatcanbecollectedupfrontonpresumedearnings.Theymayalsobewillingtotaketheriskthattheycanfindawaytoturnthesituationaroundbasedontheirgreaterparticipationinfutureupsidethanfuturedownside.Theymaychoose tohide thesituation fromoutsiderswho theysuspectwouldnot give them the latitude to take such risks. So moral hazard can turn anaccidentallyoriginatedPonzischemeintoonethatisveryclosetodeliberate.As a historical footnote, the Ponzi scheme derives its name from Charles

Ponzi,aBoston-basedswindlerof the1920s(though itwasnot thefirstPonzischeme—William “520 Percent”Miller ran one in Brooklyn around 1900; anexcellent1905playbyHarleyGranville-Barker,TheVosey Inheritance,whichhas been revived frequently over the past decade, revolves around a lawyerspecializing in trusts and estates trying to train his son to take over themanagement of hisPonzi scheme).The following account ofCharlesPonzi isdrawnfromSifakis(1982):[Ponzi]discoveredhecouldbuyupinternationalpostal-unionreplycouponsat depressed prices and sell them in theUnited States at a profit up to 50percent. It was, in fact, a classic get-rich-slowly operation, and as such, itboredPonzi.Sohefiguredoutabettergimmick.Ponzi figured out that telling people hewasmaking themoney and howhe

couldmake itwas just as good as actuallymaking it.He advertised a rate ofreturnof50percentinthreemonths.Itwasanofferpeoplecouldn'trefuse,andmoneystartedtocomerollingin.WhenPonzi actually started paying out interest, a deluge followed.Ononemonumentaldayin1920,Ponzi'sofficestookinanincredible$2millionfromAmerica'snewestgamblers,thelittlepeoplewhosqueezedmoneyoutofbankaccounts, mattresses, piggy banks, and cookie jars. There were days whenPonzi's office looked like a hurricane had hit it. Incoming cash had to bestuffed in closets, deskdrawersandevenwastebaskets.Of course, themorethatcamein,themorePonzipaidout.As long as new funds were coming in, Ponzi could continue to make

payments.However, aswith all pyramid schemes, the bubble had to burst. A

newspaper published some damaging material about his past, including timespentinprison.Newinvestorsstartedtohesitate.Ponzi'sfragileschemecollapsed,sinceitrequiredanunendingflowofcash.Hisbooks,suchastheywere,showedadeficitofsomewherebetween$5and$10million,orperhapsevenmore.Nooneeverknewforsure.

2.3ADVERSESELECTIONLet'sreturntothesituationdescribedpreviously.Supposeouraccountingisgoodenough to catch the hedge slippage before it does toomuch damage.We stopbookingnewdealsofthistype,butwemayfindwehavebookedadisturbinglylargenumberofthesedealsbeforethecutoff.Ifourcustomershavefiguredoutthedegree towhichweareunderpricing the structurebeforewedo, then theymaytrytocompleteasmanydealsastheycanbeforewewiseup.Thispatternhas frequently been seen in the financialmarkets. For example, the last firmsthatfiguredouthowtocorrectlypricevolatilityskewintobarrieroptionsfoundthat their customershad loadedupon trades that the less correctmodelswereunderpricing.Acommonconventionistolabelthissituationasadverseselectionasaparalleltoasimilarconcernamonginsurancefirms,whichworrythatthosecustomers with failing health will be more eager to purchase insurance thanthosewithbetterhealth,takingadvantageofthefactthatapersonknowsmoreabout his ownhealth than an insurance company can learn (Wilson1989). Soadverse selection is like moral hazard since it is based on informationasymmetry; thedifferenceis thatmoralhazardisconcernedwiththedegreeofrisk thatmightbe takenbasedon thisasymmetry,whereasadverseselection isconcernedwithadifference inpurchasingbehavior. In2001,GeorgeAckerlof,MichaelSpence,andJosephStiglitzwontheNobelPrizeineconomicsfortheirwork on adverse selection and its application to a broad class of economicissues.Concern about the risk from adverse selection motivates risk managers'

concern about the composition of a trading desk's customer base. The keyquestion is:Whatproportionof trades iswith counterpartieswhoare likely topossess an informational advantage relative to the firm's traders?As ageneralrule, you prefer to see a higher proportion of trades with individuals andnonfinancialcorporations thatare likely trading tomeethedgingor investmentneeds rather than seeking to exploit informational advantage. Alarm is raised

when an overwhelming proportion of trades iswith other professional traders,particularly ones who are likely to see greater deal flow or have a greaterproportion of trades with individuals and nonfinancial corporations than yourfirm's traders. Seeing greater deal flow can give a firm an informationaladvantagebyhavingamoreaccuratesenseofsupply-and-demandpressuresonthemarket.Agreaterproportionofcustomerswhoarenotprofessional tradersyieldstwofurtherpotentialinformationaladvantages:

1. At times youworkwith such customers over a long period of time tostructure a large transaction. This gives the traders advance knowledge ofsupplyanddemandthathasnotbeenseeninthemarketyet.2. Working on complex structures with customers gives traders a moreintimateknowledgeofthestructure'srisks.Theycanchoosetoretainthoserisks that this knowledge shows them are more easily manageable andattempttopasslessmanageablerisksontoothertraders.Tradersmaytendtounderestimatethedegreetowhichtheirprofitabilityisdue

to customer deal flow and overestimate the degree to which it is due toanticipatingmarketmovements.Thiscanbedangerousifitencouragesthemtoaggressively take risks inmarkets inwhich they do not possess this customerflow advantage. A striking example I once observed was a foreign exchange(FX)traderwhohadaphenomenallysuccessfultrackrecordofproducingprofitsat a largemarket-making firm.Convincedofhisprowess inpredictingmarketmovements,heacceptedalucrativeoffertomovetoafarsmallerfirm.Hewasbackathisoldjobinlessthanyear,confessinghesimplyhadnotrealizedhowmuchofhissuccesswasduetotheadvantagesofcustomerdealflow.Apithy, if inelegant,statementof thisprinciplewasattributed to theheadof

mortgage-backed trading at Kidder Peabody: “We don't want tomakemoneytrading against smart traders; we want to make money selling to stupidcustomers.”Ofcourse,stupidneedstobeunderstoodhereasmachoWallStreetlingoforinformationallydisadvantaged. It's thesortof talk that ismeant tobeheardonlyinlockerroomsandontradingfloors.AnunfriendlyleakresultedinhisquoteappearingonthefrontpageoftheWallStreetJournal.It isdelightfultoimaginethedialogueofsomeofhissubsequentconversationswiththefirm'scustomers.

2.4THEWINNER'SCURSE

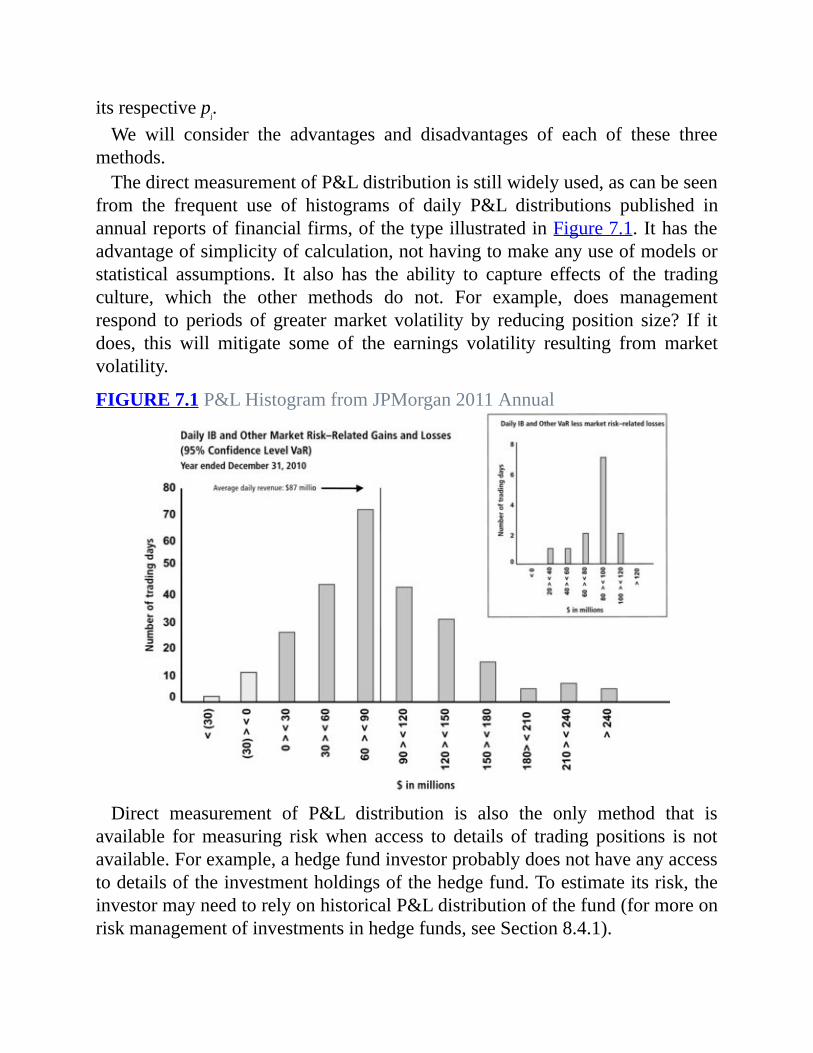

Inresponsetotherisksofadverseselection,tradersmayexhibitconfidencethatthis is not something they need to worry about. After all, adverse selectionimpactsonlythosewithlessknowledgethanthemarket.Itisararetraderwhoisnotconvincedthatshepossessesfarmoreknowledgethantherestofthemarket—belief in one's judgment is virtually a necessity for succeeding in thisdemanding profession. Whether the firm's management shares the trader'sconfidencemaybeanotherstory.However,evenifitdoes,thetradermuststillovercomeanotherhurdle—thewinner'scurse, theeconomicanomaly that saysthatinanauction,eventhosepossessing(insider)knowledgetendtooverpay.The winner's curse was first identified in conjunction with bidding for oil