A PERSPECTIVE ON MUTUAL FUND SHARE CLASS DEVELOPMENTS ABSTRACT A new wave of mutual fund share classes are being considered – “T” shares and “Clean” shares – both addressing potential conflicts due to the anticipated DOL Fiduciary Rule, as well as responding to marketplace pressures and expectations by distributors. While the new White House Directive about the DOL Rule insures the Rule does not survive in its current form (and possibly will be rescinded), many industry developments influenced by this rule are irreversible. I welcome your questions and comments to this article – reach me at [email protected]. Avi Nachmany

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

APERSPECTIVEON

MUTUALFUNDSHARECLASS

DEVELOPMENTS

ABSTRACTAnewwaveofmutualfundshareclassesarebeingconsidered–“T”sharesand“Clean”shares–bothaddressingpotentialconflictsduetotheanticipatedDOLFiduciaryRule,aswellasrespondingtomarketplacepressuresandexpectationsbydistributors.WhilethenewWhiteHouseDirectiveabouttheDOLRuleinsurestheRuledoesnotsurviveinitscurrentform(andpossiblywillberescinded),manyindustrydevelopmentsinfluencedbythisruleareirreversible.Iwelcomeyourquestionsandcommentstothisarticle–[email protected]

ARisingFocusonAssetAllocationCultureHasLedtotheDominanceofNo-LoadShareClass

• Thesteadyexpansionof‘wrap’programsandassetallocation‘solutions’hasbeenpushingBDsand

wealthmanagementfirmstowardstheusemutualfunds’leastexpensiveshareclasses(aswellaslow-feeETFs).Increasingly,theshareclassesbeingselectedfornewsalesare‘noload,no12b-1fee’shareclasses.Advisorsincreasinglyearntheir‘fees-for-service’throughchargestoinvestorsdirectly(inadditionandindependentofthecostsoftheunderlyingfunds).PlanningforandanticipatingtheDOLFiduciaryRuleacceleratedthistrend(whichhasbeenunderwayformanyyears,becomingmorepronouncedpost2008-2009)

• Overall,nearlyall(80%-90%)mutualfundsalesthroughfinancialadvisorsarewithinsomeformof‘wrapped’programswhereinvestorsarechargedafee-for-service.Inversely,likelylessthan10%ofmutualfundsalestodayareinplatformsusingpointofsales(POS)commission.

Source:StrategicInsight’sAnnualSalesSurvey2016

FromNo-Load,NoRule12b-1FeestoEvenLowerFee‘Clean’Classes:AContext

Therearenumerousstructuresforthe‘fee-for-service’modelusedbyfinancialadvisors.TraditionalFAsaremanagingtheirclientassetswithinmutualfundwraps.SomeFAsarestillusinglevel-load“C”shareclassesassubstitutiontowrapaccounts(albeit“Cs”areunder10%ofFAsalestodayandtheirshareofsalesisfalling;yet“Cs”arevaluabletomanylower-balanceinvestors,aslevel-loadclasstax-adjustedtotalcostsaresignificantlylowerthanthoseincurredin‘wrap’accountsusingthesamefunds).NaturallyRIAscontinuetohelptheirHNWclientsthroughassetallocationfee-for-serviceplatformsadministeredbySchwab,Fidelity’sFundsNetwork,andothers(RIAsnowcontrolone-quarterofallAUMsofmutualfundsandETFs).

Overall,overthepastdecade,advisorsandBDshavedramaticallyshiftedtheirrevenuemodels,astheydoubledtheirshareof(morestable)revenuesgeneratedthroughon-goingfees-for-service,andgreatlyreducedtheirdependencyon(unpredictable)point-of-salescommissions.And,within

wraps/fee-basedadvisoryprograms,salesofno-load,noRule12b-1feeshavesignificantlyincreasedtoexceedtwo-thirdstoday.

Recognizingthesetrends,theSEChassignaledagrowinginterestinmonitoringshareclassandwrapaccountsuitability.

SEC’s2017Agenda:ShareClassSuitabilityandRelatedIssuesAsdisclosedbytheSECOfficeofComplianceInspectionsandExaminationsPriorities2017:excerptsfromOCIE’sExaminationsPriorities2017emphasizing”PROTECTINGRETAILINVESTORS”

• ShareClassSelection.…conflictsofinterestandotherfactorsthatmayaffectregistrants’recommendationstoinvest,orremaininvested,inparticularshareclassesofmutualfunds.Forexample,wewillidentifyandassessconflictsthatcertaininvestmentadvisorypersonnelmayhave,suchasthosewhoalsoareregisteredrepresentativesofabroker-dealer,whichmayinfluencerecommendationsinfavorofshareclassesthathavehigherloadsordistributionfees.Wewillalsoassesstheformulationofinvestmentrecommendationsandthemanagementofclientportfolios.

• WrapFeePrograms.Wewillexpandourfocusonregisteredinvestmentadvisersandbroker-dealersassociatedwithwrapfeeprograms,whichchargeinvestorsasinglebundledfeeforadvisoryandbrokerageservices.Wewilllikelyreviewwhetherinvestmentadvisersareactinginamannerconsistentwiththeirfiduciarydutyandwhethertheyaremeetingtheircontractualobligationstoclients.Areasofinterestmayincludewrapaccountsuitability,effectivenessofdisclosures,conflictsofinterest,andbrokeragepractices,includingbestexecutionandtradingaway…

• ElectronicInvestmentAdvice.Investorsareincreasinglyabletoobtaininvestmentadvicethroughautomatedordigitalplatforms.Wewillexamineregisteredinvestmentadvisersandbroker-dealersthatoffersuchservices,including“robo-advisers”thatprimarilyinteractwithclientsonlineandfirmsthatutilizeautomationasacomponentoftheirserviceswhilealsoofferingclientsaccesstofinancialprofessionals.Examinationswilllikelyfocusonregistrants’complianceprograms,marketing,formulationofinvestmentrecommendations,dataprotection,anddisclosuresrelatingtoconflictsofinterest.Wewillalsoreviewfirms’compliancepracticesforoverseeingalgorithmsthatgeneraterecommendations.

Source:StrategicInsight’sAnnualSalesSurvey2016

Towards“CleanShares:”NewLowFeeShareClass(no12b-1;NoTA/SubTAFees)?

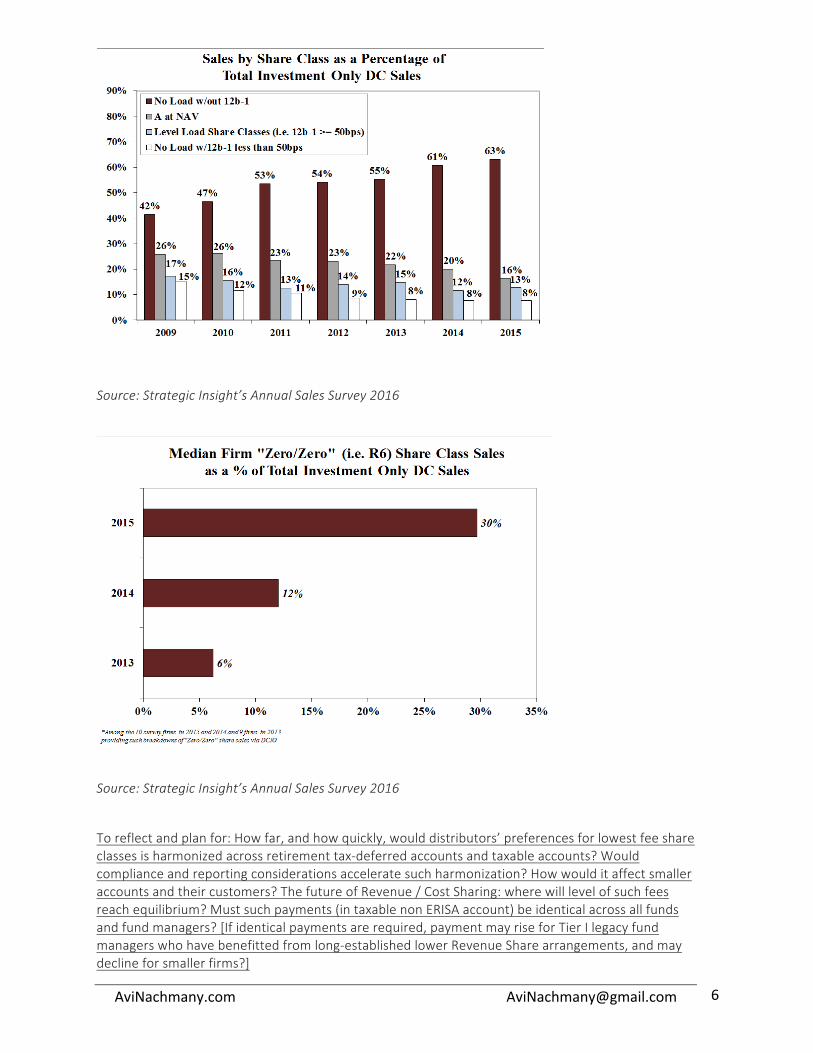

Shareclassesstrippedofmanyembeddedcosts(distributionfeesviaRule12b-1orTA/SubTAfees)havebecomedominantwithDCplans(typicallysuchshareclassesaredesignedR6).In2015,withinDCInvestmentOnlyplans,anestimated30%ofsaleswerecapturedbysuchclasses–justtwoyearsbefore,theshareofsuchfundswasatiny6%.NaturallytheshareofDCIOplansalescapturedbyR6classesisevenhighernow.

R6‘zero/zero’shareclassesareleading(generallylarge)retirementplans(shiftinfluencedbycostconsideration,litigationrisk,ERISArules,andplanningaheadoftheDOLFiduciaryRule,nowunlikelytosurviveinitscurrentformifnotcompletelyrescinded).Yet,beyondretirementplans,anewwaveof‘zero/zero’shareclassesarebeingconsiderednow.MuchofsuchdiscussionhascenteredonthenewSECNo-ActionLetterattherequestofCapitalGroup(parentofAmericanFunds).

Thesenewshareclassesaredubbed‘Clean,’(aUKterminology…)andcanbeusedinbothretirementaccountsornon-retirementaccounts.Usingsuchshareclassesallowbrokerstosettheirowncommission(naturallythefund'sprospectuswouldhavetodisclosethatthebrokermaychargeacommissiononthesaleoftheshares.Otherstatedconditions:thebrokerisactingonlyonan“agencybasis”forthesaleoftheshares;sharesdonotincludeanydistribution-relatedpaymentstothebroker).[Thereissomeambivalenceaboutpaymentofrevenuesharingin‘Clean’shares.ItisunderstoodthatinitsNo-ActionLettertheSECdidnotspecifywhethersub-TAfeeswouldbepermissible,wereafundmanagertocreateaversionofcleansharesthatincludesthem–suchshouldbepermissibleastheyarenotdistribution-relatedpayments.]

Inplanningforafuturewhere‘Clean’shareclassesarepopular(noRule12(b)1feesandnoTA/SubTAfees):who’llpayforservicingcostsoffundsonaBDplatform?WillsuchfeesbeabsorbedbyBDs,paiddirectlybyinvestors,orpaidbyfundmanagersoutoftheirfallingprofits?Whatwillbethemechanismforsuchpayment(nolongerenjoyingthemutualizationoffees)?Whattheframeworktopermitthepaymentofsuchfees)?

“T”ShareClasses:NewCommissionShareClassesforCommissionPlatform

Source:StrategicInsight’sAnnualSalesSurvey2016

Theuseoftraditional‘load’shareclasseshasdramaticallydeclinedinrecentyears.AndanticipatingtheDOLFiduciaryRulehasintroducedthepotentialfornewconflictsintheuseofsuchshareclasses,triggeringdecisionamongsomeBDstoexitcommissionplatformsforretirementaccounts.

1. Documentedinpriorchart:“A”shareswith2-4%commissionshavebeenthemostcommonlyusedinrecentyears,accountingforunder10%ofsalesin2015(inaggregate)andforalowersharelastyearandin2017(surveydatafor2016isnotyetavailable).Actuallyformostfundfirms,theshareofany“As”soldwithcommissionsaresignificantlylowerthantheaboveaggregatedatasuggest(assuchaggregateddataisdistortedduetotheexperienceofonelargefundcompany).

2. Naturally,forwealthierinvestorsthelevelofsalescommissionsforanewpurchaseareinfluencedbylargebalancesalreadyownedwithinsamehousehold(orBD),allowingcustomerstherightoflowercommissions.[Note:“Ts”donotallowsuchscalediscounts,aseachtransactionPOScommissionsaresetbythesizeofthatpurchasealone.]

3. PlanningfortheDOLFiduciaryRulehasledtoanewgenerationoffundshareclassestobeusedincommission-basedplatforms.Underwayareadaptationstotherule–whichIbelievearelikelytosurvivethelikelydemiseoftheRuleinitscurrentform–aroundcommission-basedplatforms.

4. SomeBDsareexitingsuchcommissionplatformfortheirERISAassets–andlikelyovertimeintheirtaxableaccounts;othersareintroducingmodificationstothetypeoffundspermittedintheircommission-basedplatform.

5. SomeBDsbelievethattheircustomersbenefit(throughlowerlifetimetotalcostsandotherways)iftheymaintaintheavailabilityofcommissionplatform.Thiscanbeaccomplishedwiththenewly-introducedshareclasses(designedtosidesteptheDOLFiduciaryRuleperceivedconflicts;existingshareclasses–historicallyusedincommissionplatforms--‘A’s,‘B’s,‘C’s–werebelievedtocreateconflictsfordistributorsadheringtotheDOLRule).Enter“T”shares:anewshareclass.Atypicalstructure[tosimplifytheiracceptanceanduse,itisimperativethata‘standard’of‘Ts’isestablished]:POSchargeof2.5%;breakpointsupto$1millionand1%salesloadforalltransactions$1millionandabove);NoshareholderAUMaccumulationprivileges(NoROA,NoLOI);NoCDSC;0.25%Rule12b-1fee.Generally,“Ts”donothaveaseparateShareholderServicingFees(anexceptionisJPMorgan’sAMfilingswhichinclude0.25%ShareholderServicesFeeswhichmaybeusedforpaymentforsub-transferagentorforshareholderandadministrativeservice).(Onceafirmintroduces‘Ts,’existingtransactionalshareclasses–‘As,’‘Bs,’,(possibly)‘Cs’-mayhavetobeclosedandtheirAUMsexchangedintothisnewshareclass.)

AHarmonizationofShareClassesUsedinRetirementAccountsandinTaxableAccounts?

ItisclearthatnoRule12b-1feeshareclasses,andattimes,shareclasseswithoutTA/Sub-TAfee(‘R6’)havebecomeadominantstructurewithinthemajorityofIODCnewsales,asillustratedinthenexttwocharts(2016dataisbeingcollectedandavailableinthecomingmonthsbutthetrendisirrefutable).

Source:StrategicInsight’sAnnualSalesSurvey2016

Source:StrategicInsight’sAnnualSalesSurvey2016

Toreflectandplanfor:Howfar,andhowquickly,woulddistributors’preferencesforlowestfeeshareclassesisharmonizedacrossretirementtax-deferredaccountsandtaxableaccounts?Wouldcomplianceandreportingconsiderationsacceleratesuchharmonization?Howwoulditaffectsmalleraccountsandtheircustomers?ThefutureofRevenue/CostSharing:wherewilllevelofsuchfeesreachequilibrium?Mustsuchpayments(intaxablenonERISAaccount)beidenticalacrossallfundsandfundmanagers?[Ifidenticalpaymentsarerequired,paymentmayriseforTierIlegacyfundmanagerswhohavebenefittedfromlong-establishedlowerRevenueSharearrangements,andmaydeclineforsmallerfirms?]

Inconclusion

Ithasbeenmyobservationthatitisbettertobeafastfollowerthatanearlyinnovatorofnewshareclasses,allowingsuchpatientfirmtofine-tunetheirofferingifneeded.Furthermore,theWhiteHouseFebruary3rdnewDirectiveabouttheDOLFiduciaryRule(whichiscertaintoresultintheRulebeingrescindedorgreatlymodified)suggeststhatsomefundmanagementcompaniesdelayfilingsandlaunchingnewshareclassuntilthe‘dustsettles’inthecomingmonths.Yet,somedistributorshavealreadysetinmotionprogramsaroundtheselectionanduseofshareclasseswhichmayrequiretheintroductionsofnewsuitesofsuchclassesindependentofthefutureoftheDOLRule.Overall,marketplacetrendssuggestthatthemutualfundindustryisevolvingtoafuturewhereamajorityoffundnewsalesandassetsundermanagementuseshareclasseswhichcoveronlycoremanagement,administration,andlegallyrequiredfees,side-by-sidewithlowfeeETFs,allwrappedwithanassetallocationprogramsinwhichadditionalfees-forservice,feesforplatformparticipation,andotheradministrativefeesarechargedseparatelytotheinvestor.Thepathinthatdirectionisset,andfundmanagementfirmsandtheirfundtrusteeshouldcontinuetoplanforsuchafuture.AviNachmanyNewYorkCity,[email protected]

Related Documents