Transportation & Logistics Research David Ross, CFA [email protected] (443) 224-1316 J. Bruce Chan [email protected] (443) 224-1386 • Modal share shift (air to ground) should continue over time, as the carriers’ ground networks are operating as fast and efficient as ever, and there remains a wider gap in price than service (see Exhibits 1-3 on pp. 5-6). For this reason, we also expect ground rates to rise significantly faster than air rates, especially in regional lanes, over the next several years. • For carriers, the continued air-to-ground share shift will require more effective management—and likely a reduction in the size—of the (domestic) air fleet to avoid significant margin pressure. • Interestingly, Exhibits 4-7 (on pp. 6-7) show highest variance in actual-versus-estimated delivery dates were with the U.S. Postal Service (USPS), although it tended to be beneficial for customers, as most packages ar- rived well ahead of published transit times (which were slower times than published by the competi- tion). While this result indicates that USPS (on-time) service is not as bad as perception, it may mean that USPS is losing out on money that it could be charging for transit times that are faster/better than advertised. • FedEx Ground is significantly cheaper than UPS Ground (for retail customers), while FedEx Express and UPS Air product rates are comparable (on a same-service basis). • We reiterate our Buy ratings on FDX ($111 target price, or 13.5x our CY13 EPS estimate of $8.24) and UPS ($83 target price, or 15x our CY13 EPS estimate of $5.50) based on the companies’ strong positioning in the U.S. and International small package markets, positive pricing momentum, and growing B2C and C2C ship- ment trends, especially as the UPS Store and FedEx Office often offer the retail customer a better experience than the local post office. Our estimates and ratings assume neither company acquires TNT Express. A Parcel Shipping Experiment Our Empirical Comparison of Rates, Service, Network Patterns, and Transit Times Among Parcel Carriers March 2, 2012 In an effort to gain some first-hand insight into the small package business, we conducted an experiment that in- volved sending approximately 100 pieces of equal size and weight to various destinations in the U.S. and abroad. This allowed us to compare, on an empirical basis, the varying price and service levels among the main parcel players—namely, UPS (UPS; $76.89; Buy), FedEx (FDX; $91.12; Buy), the USPS, and a regional parcel carrier. Throughout the exercise, we kept records of costs, service exceptions, network patterns, and transit times, all of which are detailed in this report. It is important to note that our experiment was conducted using retail-rated ship- ments only, and that large shippers typically benefit from substantial rate discounts, which alter the relative attrac- tiveness of carriers. Still, we believe our results provide some beneficial insight on price levels across comparable products. Service, of course, is unaffected by discounts. While our experiment involved only about 100 of the mil- lions of packages that flow through the various parcel networks each day, it gave us a valuable perspective from which to consider some of the larger trends that we have been observing in the industry. Stifel Nicolaus does and seeks to do business with companies covered in its research re- ports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. All relevant disclosures and certifications appear on pages 14-16 of this report.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Transportation & Logistics Research

David Ross, CFA [email protected] (443) 224-1316 J. Bruce Chan [email protected] (443) 224-1386

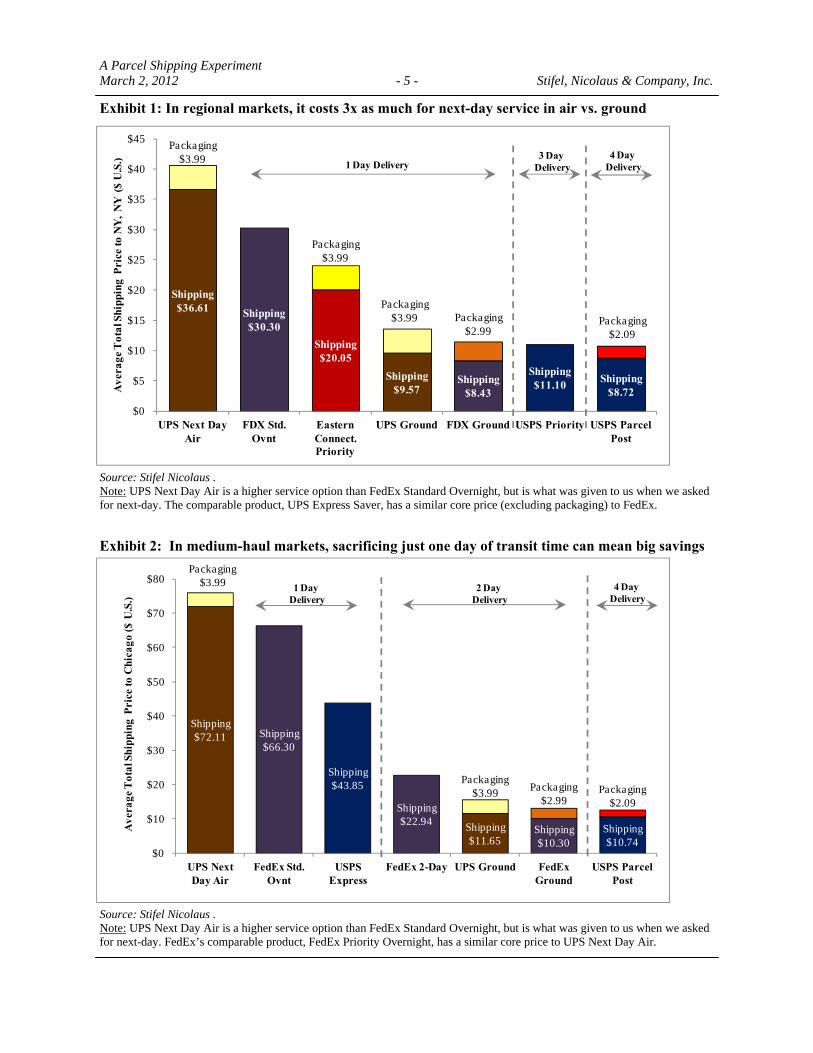

• Modal share shift (air to ground) should continue over time, as the carriers’ ground networks are operating as fast and efficient as ever, and there remains a wider gap in price than service (see Exhibits 1-3 on pp. 5-6). For this reason, we also expect ground rates to rise significantly faster than air rates, especially in regional lanes, over the next several years.

• For carriers, the continued air-to-ground share shift will require more effective management—and likely a reduction in the size—of the (domestic) air fleet to avoid significant margin pressure.

• Interestingly, Exhibits 4-7 (on pp. 6-7) show highest variance in actual-versus-estimated delivery dates were with the U.S. Postal Service (USPS), although it tended to be beneficial for customers, as most packages ar-rived well ahead of published transit times (which were slower times than published by the competi-tion). While this result indicates that USPS (on-time) service is not as bad as perception, it may mean that USPS is losing out on money that it could be charging for transit times that are faster/better than advertised.

• FedEx Ground is significantly cheaper than UPS Ground (for retail customers), while FedEx Express and UPS Air product rates are comparable (on a same-service basis).

• We reiterate our Buy ratings on FDX ($111 target price, or 13.5x our CY13 EPS estimate of $8.24) and UPS ($83 target price, or 15x our CY13 EPS estimate of $5.50) based on the companies’ strong positioning in the U.S. and International small package markets, positive pricing momentum, and growing B2C and C2C ship-ment trends, especially as the UPS Store and FedEx Office often offer the retail customer a better experience than the local post office. Our estimates and ratings assume neither company acquires TNT Express.

A Parcel Shipping Experiment

Our Empirical Comparison of Rates, Service, Network Patterns, and Transit Times Among Parcel Carriers

March 2, 2012

In an effort to gain some first-hand insight into the small package business, we conducted an experiment that in-volved sending approximately 100 pieces of equal size and weight to various destinations in the U.S. and abroad. This allowed us to compare, on an empirical basis, the varying price and service levels among the main parcel players—namely, UPS (UPS; $76.89; Buy), FedEx (FDX; $91.12; Buy), the USPS, and a regional parcel carrier. Throughout the exercise, we kept records of costs, service exceptions, network patterns, and transit times, all of which are detailed in this report. It is important to note that our experiment was conducted using retail-rated ship-ments only, and that large shippers typically benefit from substantial rate discounts, which alter the relative attrac-tiveness of carriers. Still, we believe our results provide some beneficial insight on price levels across comparable products. Service, of course, is unaffected by discounts. While our experiment involved only about 100 of the mil-lions of packages that flow through the various parcel networks each day, it gave us a valuable perspective from which to consider some of the larger trends that we have been observing in the industry.

Stifel Nicolaus does and seeks to do business with companies covered in its research re-ports. As a result, investors should be aware that the firm may have a conflict of interest

that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

All relevant disclosures and certifications appear on pages 14-16 of this report.

A Parcel Shipping Experiment March 2, 2012 - 2 - Stifel, Nicolaus & Company, Inc.

Other key takeaways: • UPS Store and FedEx Office both offer a much better customer experience than the USPS. While results will

obviously vary by location, we found the UPS Store and FedEx Office locations to be more customer-service oriented than their USPS counterparts.

• FedEx and UPS have different coverage maps, so what may be a 2-day shipment with one carrier could be a 3-day shipment with the other. Shippers should look at these maps (Exhibits 8-10 on pp. 7-8) before choosing a carrier, as it may save them time and money.

• FedEx Office locations are generally larger and have more traffic than UPS Stores, as they offer more than just shipping and packaging; however, there are many more UPS Store locations, making it more convenient for many.

• Tracking and tracing for USPS is available but for a modest surcharge. While other carriers include this ser-vice “free of charge,” it is likely already built-in to pricing. As a result, USPS may be the only carrier to allow customers to opt-out of the tracking and tracing charge.

• Regional carriers like Eastern Connection (serving the Mid-Atlantic) are a good option for larger shippers moving packages within a regional footprint. They offer good regional transit times, often at lower prices than FedEx or UPS. However, like UPS SurePost and FedEx SmartPost, service is not available to the one-off re-tail shipper.

Notes: Summary of each shipment shown in Exhibits 11-12 on pp. 9-10. Experiment conducted based on 2011 published rates. In the next section, we will highlight our general experiences with each carrier and its retail sales channel, includ-ing what we learned while in the store—directly and indirectly. But first, a brief comparison as it relates to LTL pricing: when we took our packages in (they each weighed the same and fit in the same size box for shipping by each service), on the scale, each weighed in at 5.4 lbs. For pricing, though, FedEx and UPS round up to the nearest pound, resulting in a theoretical 11% increase over what we should have paid were it priced more strictly by the weight. In fact, even a 5.01 lb. shipment would be priced as a 6.0 lb shipment in their networks. In the less-than-truckload (LTL) world, where carriers run similar but less automated networks for heavier, non-conveyorizable freight, carriers are lucky to charge even on a 500 lb. basis for an actual 540 lb. shipment, let alone 600 lbs. The UPS Store • All services always guaranteed (at no additional cost). Next Day Air is guaranteed by 10:30am for higher

density areas (cities) and by Noon for rural areas. Ground service is guaranteed on a day-definite basis by coverage map (see Exhibit 9 on p. 8).

• There are no UPS boxes at the store in which to ship anything. We had to pay for each box used to package our goods, even for overnight shipments.

• We found it interesting that Ground service to Alaska (from Baltimore, MD) is a 4-day guarantee (it must be sent by air); whereas Hawaii is a 5-day guarantee.

A Parcel Shipping Experiment March 2, 2012 - 3 - Stifel, Nicolaus & Company, Inc.

• UPS offers a 3-Day Select product that is a hybrid between air and ground. 3-Day Select basically allows faster delivery to the normal 4-6 day ground destinations.

• UPS Store also handles U.S. mail, so customers can drop off standard mail or ship USPS Priority Mail. The workers offer all services, but for those who want tracking, UPS is the only option. Interestingly, depending on origin/destination pair, UPS may also be cheaper than the USPS (typically for heavier-weight shipments).

• Customers can also buy stamps or rent a mailbox (after all, the UPS Store used to be Mail Boxes Etc). • UPS Store employees handled all of the data input for us – there were no labels for us to fill out and no hand-

writing to worry about. The UPS Store employees make sure the customer information is correct and com-plete, which should translate into fewer lost or returned packages. The process is even easier for returning customers, as the “from” information is already on file and that field is automatically populated on the ship-ping label.

• The store sells the UPS #88 car toy along with paper, boxes, pens, gift wrapping, packing materials and other related items. The store does not buy it supplies from or through UPS, and UPS charges the store for any UPS boxes/envelopes that the store chooses to stock.

• As for setting-up an account to get a discount, that service is not available at the UPS Store. Customers need to talk to a UPS salesperson in order to establish an account, which in turn requires a minimum amount of volume, and likely, a monthly minimum charge for the account.

• No UPS SurePost option available at the UPS Store - that is reserved for larger shippers who use other UPS portfolio products.

• Hours of operation: Monday-Friday, 8:30am - 6:30pm and 10:00am – 4:00pm on Saturday. Parcel pick up happens once per day between 6:00pm - 6:30pm. If the store has an unusually large number of pieces for pickup, they will alert the distribution center, who will then send an additional driver if necessary. If a cus-tomer misses the scheduled pickup and needs a package sent out that night, he can drop it off at a local sort facility until 7:00pm.

FedEx Office (formerly Kinkos) • FedEx Office has a surcharge for using Ground boxes but not for Express boxes, and we were told we needed

to use Ground boxes for our Ground shipments. Express boxes and envelopes are “free.” • Technically, a customer can ship using any variety of box, including using a “Ground” box for an Express

shipment, or vice-versa. However, store employees are trained to discourage this practice, presumably to pre-vent confusion in the sort, but likely also to keep customers from converting from higher-yielding Express to lower-yielding Ground.

• No SmartPost option for shippers at FedEx Office – this remains a product (almost exclusively) for high-volume B2C shippers.

• Service defaults to its “Standard” product which, on average is a service level below the default service pro-vided by UPS (i.e. the UPS Store defaulted us to the more expensive next-day shipping option when we just asked for next-day—we are not sure if this was by store manager design or company design, but it explains the difference in pricing).

• Ground pickup was earlier than Express, and the Express driver could not take our Ground packages, so we

A Parcel Shipping Experiment March 2, 2012 - 4 - Stifel, Nicolaus & Company, Inc.

had to drive to the nearest Ground facility to ensure that all packages went out the same day. It required much debating and calling the manager’s manager before we were able to get the address of the local facility, con-tact the local supervisor, and have him grant us access/permission to drop the packages off ourselves. We noted that there was very tight security at the Ground facility.

• Double labeling—after we filled everything out, the FedEx worker entered it into the system, printed a label and put it on the box. The process seemed redundant to us. The UPS Store was much more efficient.

• Everything would have been much easier with an account number (we have a FedEx account here at Stifel but chose not to use it for the purposes of this experiment). As in the UPS store, we were unable to sign-up for an account as an individual—had to contact a FedEx salesperson.

• Hours of operation (open more days and longer each day than UPS Stores): Monday-Friday, 7am – 11pm and 9am – 9pm on Saturday and Sunday.

Regional carrier (Eastern Connection) • To add a regional parcel carrier to the mix, we used Eastern Connection, since we are based in Baltimore. • Regional carriers typically do not have retail outlets and serve larger regional customers only. However, since

we knew the company, they made an exception for us so we could compare service and rates (even though they have no real retail rates).

USPS (the local post office) • USPS rates are often more attractive for lighter-weight packages but usually not as attractive for heavier pack-

ages. • Customer service was not as helpful with processing the shipments, but they at least stayed open late so that

we could get everything filled out and shipped. • The Priority Mail box is free, but there is a charge for bubble envelopes. • Hours of operation: Monday— Friday, 9am-2pm, 3pm-5pm • The biggest surprise was the amount of time the shipping and labeling process took. There are multiple forms

to fill out for each shipment, especially if one wants delivery confirmation or if shipping is international. • One USPS shipment was sent back to us. When it was returned, the box was in poor condition (and after only

having gone a few blocks!). We paid $113 to send it to London via Global Express Guaranteed® (GXG) on a Tuesday. By Thursday morning, a beat up box was delivered to our office, with a notice that there had been an issue at customs in NYC (basically, the wrong postal code was transcribed, and there was no procedure to check the GXG bill for what, upon inspection, was clearly an error). We reshipped the package and included the data in our overall results.

• The only guaranteed services are next-day express mail and GXG for international (which uses FedEx).

A Parcel Shipping Experiment March 2, 2012 - 5 - Stifel, Nicolaus & Company, Inc.

Exhibit 1: In regional markets, it costs 3x as much for next-day service in air vs. ground

Exhibit 2: In medium-haul markets, sacrificing just one day of transit time can mean big savings

Source: Stifel Nicolaus . Note: UPS Next Day Air is a higher service option than FedEx Standard Overnight, but is what was given to us when we asked for next-day. The comparable product, UPS Express Saver, has a similar core price (excluding packaging) to FedEx.

Source: Stifel Nicolaus . Note: UPS Next Day Air is a higher service option than FedEx Standard Overnight, but is what was given to us when we asked for next-day. FedEx’s comparable product, FedEx Priority Overnight, has a similar core price to UPS Next Day Air.

Shipping$72.11 Shipping

$66.30

Shipping$43.85

Shipping$22.94 Shipping

$11.65 Shipping$10.30

Shipping$10.74

Packaging$3.99

Packaging$3.99 Packaging

$2.99 Packaging

$2.09

$0

$10

$20

$30

$40

$50

$60

$70

$80

UPS Next Day Air

FedEx Std. Ovnt

USPS Express

FedEx 2-Day UPS Ground FedEx Ground

USPS Parcel Post

Ave

rage

Tot

al S

hipp

ing

Pric

e to

Chi

cago

($ U

.S.)

4 Day Delivery

1 Day Delivery

2 Day Delivery

Shipping$36.61 Shipping

$30.30 Shipping$20.05

Shipping$9.57

Shipping$8.43

Shipping$11.10 Shipping

$8.72

Packaging$3.99

Packaging$3.99

Packaging$3.99 Packaging

$2.99 Packaging

$2.09

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

UPS Next Day Air

FDX Std. Ovnt

Eastern Connect. Priority

UPS Ground FDX Ground USPS Priority USPS Parcel Post

Ave

rage

Tot

al S

hipp

ing

Pric

e to

NY

, NY

($

U.S

.) 3 Day Delivery

4 Day Delivery1 Day Delivery

A Parcel Shipping Experiment March 2, 2012 - 6 - Stifel, Nicolaus & Company, Inc.

Shipping$54.85 Shipping

$48.63 Shipping$48.65

Shipping$14.65

Shipping$13.01

Shipping$13.83

Shipping$11.65

Packaging$3.99

Packaging$3.99 Packaging

$2.99 Packaging

$2.09

$0

$10

$20

$30

$40

$50

$60

USPS Express UPS 2nd Day FedEx 2-Day UPS Ground FedEx Ground USPS Parcel Post

USPS Priority

Ave

rage

Tot

al S

hipp

ing

Pric

e to

Cal

ifor

nia

($ U

.S.)

3-6 Day Delivery

2-3 Day Delivery2 Day Delivery

3%

84%

10%3%

UPS On-Time Delivery Rate

1 Day Early On Time 1 Day Late 5 Days Late

97%

3%

FDX On-Time Delivery Rate

On Time 1 Day Late

Exhibit 4: UPS showed better ground on-time performance than air; packages arrived late on a few air shipments to the West

Exhibit 5: FedEx air service was excellent but saw a ground shipment to CA arrive late

Exhibit 3: Not even showing the very expensive overnight prices, ground is still a big discount to deferred air in cross-country shipments

Source: Stifel Nicolaus

Source: Stifel Nicolaus

A Parcel Shipping Experiment March 2, 2012 - 7 - Stifel, Nicolaus & Company, Inc.

Exhibit 8: FedEx Ground coverage/service map from Baltimore, MD to other points in the U.S.

100%

Eastern Connection On-Time Delivery Rate

On Time

4%9%

4%

55%

23%

5%

USPS On-Time Delivery Rate

5 Days Early 4 Days Early 3 Days Early

1 Day Early On Time 1 Day Late

Exhibit 6: USPS packages often “early” Exhibit 7: Service helps regionals compete

Source: Stifel Nicolaus

Source: FedEx website, reflects outbound shipments from Baltimore, Maryland

A Parcel Shipping Experiment March 2, 2012 - 8 - Stifel, Nicolaus & Company, Inc.

Exhibit 9: UPS Ground service map shows different transit times than FedEx for MD shippers

Source: UPS website, reflects outbound shipments from Baltimore, Maryland

Source: Eastern Connection website

Exhibit 10: Eastern Connection service map shows coverage across the East Coast, with facilities in 19 cities

A Parcel Shipping Experiment March 2, 2012 - 9 - Stifel, Nicolaus & Company, Inc.

Exhibit 11: Eastern Connection and FedEx shipment detail

Source: Stifel Nicolaus

Delivery PriceCarrier Mode City State Country Guarantee Actual Billed Total

1) ►EC Priority Boston MA USA On Time 5.40 lbs 6.00 lbs $43.652) ►EC Priority Smithfield RI USA On Time 5.40 lbs 6.00 lbs $43.653) ►EC Priority Mount Kisco NY USA On Time 5.40 lbs 6.00 lbs $29.854) ►EC Priority Baltimore MD USA On Time 5.40 lbs 6.00 lbs $24.045) ►EC Priority New York NY USA On Time 5.40 lbs 6.00 lbs $24.046) ►EC Priority New York NY USA On Time 5.40 lbs 6.00 lbs $24.047) ►EC Priority New York NY USA On Time 5.40 lbs 6.00 lbs $24.04

8) FedEx International Priority Sydney NSW Australia On Time 5.20 lbs 6.00 lbs $168.949) FedEx International Priority Central Hong Kong China On Time 5.20 lbs 6.00 lbs $151.4610) FedEx International Priority Toronto ON Canada On Time 5.15 lbs 6.00 lbs $102.2411) FedEx International Economy Sydney NSW Australia On Time 5.20 lbs 6.00 lbs $162.3212) FedEx Standard Overnight Salt Lake City UT USA On Time 5.20 lbs 6.00 lbs $83.3813) FedEx Standard Overnight Seattle WA USA On Time 5.20 lbs 6.00 lbs $83.3814) FedEx Standard Overnight Milwaukee WI USA On Time 5.20 lbs 6.00 lbs $71.4715) FedEx Standard Overnight Minneapolis MN USA On Time 5.20 lbs 6.00 lbs $71.4716) FedEx Standard Overnight St. Petersburg FL USA On Time 5.25 lbs 6.00 lbs $71.4717) FedEx Standard Overnight Atlanta GA USA On Time 5.20 lbs 6.00 lbs $66.3018) FedEx Standard Overnight Chicago IL USA On Time 5.15 lbs 6.00 lbs $66.3019) FedEx Standard Overnight New York NY USA On Time 5.15 lbs 6.00 lbs $30.3020) FedEx Standard Overnight New York NY USA On Time 5.25 lbs 6.00 lbs $30.3021) FedEx Standard Overnight New York NY USA On Time 5.20 lbs 6.00 lbs $30.3022) FedEx Standard Overnight New York NY USA On Time 5.15 lbs 6.00 lbs $30.3023) FedEx 2-Day Pasadena CA USA On Time 5.20 lbs 6.00 lbs $48.6524) FedEx 2-Day San Francisco CA USA On Time 5.20 lbs 6.00 lbs $48.6525) FedEx 2-Day Denver CO USA On Time 5.15 lbs 6.00 lbs $46.8126) FedEx 2-Day Boston MA USA On Time 5.15 lbs 6.00 lbs $22.9427) FedEx 2-Day Chicago IL USA On Time 5.20 lbs 6.00 lbs $22.9428) FedEx Ground Los Angeles CA USA 2 days late 5.50 lbs 6.00 lbs $16.0029) FedEx Ground La Jolla CA USA On Time 5.50 lbs 6.00 lbs $16.0030) FedEx Ground San Francisco CA USA On Time 5.50 lbs 6.00 lbs $16.0031) FedEx Ground Denver CO USA On Time 5.50 lbs 6.00 lbs $15.0532) FedEx Ground Boston MA USA On Time 5.50 lbs 6.00 lbs $13.2933) FedEx Ground Chicago IL USA On Time 5.50 lbs 6.00 lbs $13.2934) FedEx Ground Baltimore MD USA On Time 5.50 lbs 6.00 lbs $11.4235) FedEx Ground New York NY USA On Time 5.40 lbs 6.00 lbs $11.4236) FedEx Ground New York NY USA On Time 5.50 lbs 6.00 lbs $11.4237) FedEx Ground New York NY USA On Time 5.50 lbs 6.00 lbs $11.4238) FedEx Ground New York NY USA On Time 5.50 lbs 6.00 lbs $11.4239) FedEx Ground New York NY USA On Time 5.50 lbs 6.00 lbs $11.4240) FedEx Ground Chicago IL USA On Time 5.60 lbs 6.00 lbs $10.30

Shipment Method WeightDestination

A Parcel Shipping Experiment March 2, 2012 - 10 - Stifel, Nicolaus & Company, Inc.

Exhibit 12: UPS and USPS shipment detail

Source: Stifel Nicolaus

Delivery PriceCarrier Mode City State Country Guarantee Actual Billed Total

Shipment Method WeightDestination

41) UPS Worldwide Expedited Sydney NSW Australia 1 day early 5.40 lbs 7.00 lbs $179.3242) UPS Worldwide Express Toronto ON On Time 5.40 lbs 7.00 lbs $113.2543) UPS Next Day Air Seattle WA USA 1 day late 5.40 lbs 6.00 lbs $96.4844) UPS Next Day Air Santa Fe NM USA 1 day late 5.40 lbs 6.00 lbs $92.7045) UPS Next Day Air Milwaukee WI USA On Time 5.40 lbs 6.00 lbs $83.0846) UPS Next Day Air Minneapolis MN USA On Time 5.40 lbs 6.00 lbs $83.0847) UPS Next Day Air Tampa FL USA On Time 5.40 lbs 6.00 lbs $83.0848) UPS Next Day Air Atlanta GA USA On Time 5.40 lbs 6.00 lbs $76.1049) UPS Next Day Air Chicago IL USA On Time 5.40 lbs 6.00 lbs $76.1050) UPS Next Day Air New York NY USA On Time 5.40 lbs 6.00 lbs $40.6051) UPS Next Day Air New York NY USA On Time 5.40 lbs 6.00 lbs $40.6052) UPS Next Day Air New York NY USA On Time 5.40 lbs 6.00 lbs $40.6053) UPS Next Day Air New York NY USA On Time 5.40 lbs 6.00 lbs $40.6054) UPS 2nd Day Air Los Angeles CA USA On Time 5.45 lbs 6.00 lbs $52.6255) UPS 2nd Day Air San Francisco CA USA 5 days late 5.40 lbs 6.00 lbs $52.6256) UPS 2nd Day Air Denver CO USA On Time 5.45 lbs 6.00 lbs $50.7957) UPS Ground Commercial Los Angeles CA USA On Time 5.40 lbs 6.00 lbs $18.6458) UPS Ground Commercial San Diego CA USA On Time 5.75 lbs 6.00 lbs $18.6459) UPS Ground Commercial San Francisco CA USA On Time 5.40 lbs 6.00 lbs $18.6460) UPS Ground Commercial Denver CO USA On Time 5.40 lbs 6.00 lbs $17.5961) UPS Ground Commercial Boston MA USA On Time 5.40 lbs 6.00 lbs $15.6462) UPS Ground Commercial Chicago IL USA On Time 5.40 lbs 6.00 lbs $15.6463) UPS Ground Commercial Boston MA USA On Time 5.40 lbs 6.00 lbs $15.6464) UPS Ground Commercial Chicago IL USA On Time 5.40 lbs 6.00 lbs $15.6465) UPS Ground Commercial Chicago IL USA 1 day late 5.40 lbs 6.00 lbs $15.6466) UPS Ground Commercial Baltimore MD USA On Time 5.90 lbs 6.00 lbs $13.5667) UPS Ground Commercial New York NY USA On Time 5.40 lbs 6.00 lbs $13.5668) UPS Ground Commercial New York NY USA On Time 5.40 lbs 6.00 lbs $13.5669) UPS Ground Commercial New York NY USA On Time 5.40 lbs 6.00 lbs $13.5670) UPS Ground Commercial New York NY USA On Time 5.40 lbs 6.00 lbs $13.5671) UPS Ground Commercial New York NY USA On Time 5.40 lbs 6.00 lbs $13.56

72) USPS GXG International Melbourne VIC Australia On Time 5.23 lbs 6.00 lbs $121.0073) USPS GXG International London UK On Time 5.28 lbs 6.00 lbs $113.7574) USPS Express Mail San Mateo CA USA 1 day early 5.25 lbs $54.8575) USPS Express Mail Chicago IL USA On Time 5.26 lbs $43.8576) USPS Priority Baltimore MD USA 1 day early 5.27 lbs $11.6577) USPS Priority Atlanta GA USA 1 day early 5.26 lbs $11.6578) USPS Priority Boston MA USA 1 day early 4.89 lbs $11.6579) USPS Priority Denver CO USA 1 day early 5.29 lbs $11.6580) USPS Priority Los Angeles CA USA On Time 5.28 lbs $11.6581) USPS Priority Milwaukee WI USA On Time 5.23 lbs $11.6582) USPS Priority Minneapolis MN USA 1 day early 5.26 lbs $11.6583) USPS Priority New York NY USA 1 day early 5.28 lbs $11.6584) USPS Priority New York NY USA 1 day early 5.27 lbs $11.6585) USPS Priority New York NY USA 1 day early 5.27 lbs $11.6586) USPS Priority Portland OR USA 1 day early 5.26 lbs $11.6587) USPS Priority San Francisco CA USA 1 day early 5.26 lbs $11.6588) USPS Priority New York NY USA On Time 5.20 lbs $9.4589) USPS Parcel Post Los Angeles CA USA 5 days early 5.17 lbs $15.9290) USPS Parcel Post Chicago IL USA 4 days early 5.19 lbs $12.8391) USPS Parcel Post New York NY USA 3 days early 5.22 lbs $10.8192) USPS Parcel Post New York NY USA 4 days early 5.23 lbs $10.81

A Parcel Shipping Experiment March 2, 2012 - 11 - Stifel, Nicolaus & Company, Inc.

Exhibit 13: Stifel Nicolaus Asset-Based Logistics Comps (fi

gure

s in

$US

mill

ions

, exc

ept p

er sh

are

amou

nts)

Clos

ing

Pric

eD

ilute

dM

arke

tTo

tal

Cash

&Bo

okTT

M

2012

ETT

MTT

MTT

MTT

M

TTM

TTM

PEG

Div

.20

12E

Com

pany

nam

e (T

icke

r)Ra

ting

3/1/

2012

S/O

cap.

Deb

teq

uiv.

TEV

(a)

2011

E(b)

2012

E(b)

2013

E(b)

valu

eRe

venu

eEB

ITD

AEB

ITD

AEB

ITD

AR (c

)EB

ITRO

ARO

ERO

ICra

tio(d

)Yi

eld

FCF

Yld

A

sset

-Bas

ed L

ogis

tics

Con-

way

(C

NW

)Bu

y30

.62

56.1

1,71

8.3

794.

343

8.0

2,07

4.6

18.3

x14

.6x

10.2

x2.

3x0.

4x4.

5x5.

1x4.

7x10

.0x

3.1%

11.8

%8.

1%1.

21.

3%1.

9%Fe

dEx

Cor

p.

(FD

X)

Buy

91.1

232

0.5

29,1

99.6

1,67

9.0

1,89

6.0

28,9

82.6

15.8

x13

.0x

11.1

x1.

8x0.

7x4.

6x6.

0x5.

6x10

.4x

6.1%

10.9

%10

.0%

1.1

0.6%

2.6%

Ryde

r Sys

tem

(R

)Bu

y54

.20

51.5

2,79

0.4

3,38

2.2

104.

66,

068.

015

.5x

13.4

x10

.8x

2.1x

1.0x

4.0x

4.7x

4.4x

14.5

x2.

5%13

.1%

5.9%

1.3

2.1%

-24.

4%Un

ited

Parc

el S

ervi

ce

(UPS

)B

uy76

.89

979.

175

,282

.712

,358

.04,

275.

083

,365

.718

.2x

15.8

x14

.0x

10.6

x1.

6x8.

8x9.

6x9.

2x12

.1x

12.6

%70

.9%

25.7

%1.

63.

0%4.

0%

Min

1,71

8.3

794.

310

4.6

2,07

4.6

15.5

x13

.0x

10.2

x1.

8x0.

4x4.

0x4.

7x4.

4x10

.0x

2.5%

10.9

%5.

9%1.

10.

6%-2

4.4%

Mea

n27

,247

.84,

553.

41,

678.

430

,122

.717

.0x

14.2

x11

.5x

4.2x

0.9x

5.5x

6.4x

6.0x

11.7

x6.

1%26

.7%

12.4

%1.

31.

7%-4

.0%

Med

ian

15,9

95.0

2,53

0.6

1,16

7.0

17,5

25.3

17.0

x14

.0x

10.9

x2.

2x0.

9x4.

5x5.

5x5.

1x11

.2x

4.6%

12.5

%9.

0%1.

31.

7%2.

3%M

ax75

,282

.712

,358

.04,

275.

083

,365

.718

.3x

15.8

x14

.0x

10.6

x1.

6x8.

8x9.

6x9.

2x14

.5x

12.6

%70

.9%

25.7

%1.

63.

0%4.

0%

Stife

l Nic

olau

s Tr

ansp

orta

tion

Ave

rage

7,41

7.8

1,52

5.8

298.

68,

642.

520

.2x

16.3

x13

.4x

3.4x

1.7x

7.5x

10.0

x8.

1x12

.7x

5.2%

9.8%

9.9%

1.3

0.6%

2.7%

(a) T

otal

Ent

erpr

ise V

alue

= M

arke

t Cap

italiz

atio

n of

Equ

ity +

Tot

al D

ebt -

Cas

h +

Mar

ket V

alue

of M

inor

ity In

tere

st(b

) Stif

el N

icol

aus e

stim

ates

for t

hose

rate

d an

d Fi

rst C

all m

ean

estim

ates

for u

nrat

ed se

curit

ies

(c) E

nter

prise

val

ue a

djus

ted

to in

clud

e th

e ca

pita

lizat

ion

of o

ff ba

lanc

e sh

eet o

pera

ting

leas

es w

ith le

ase

expe

nse

(or r

ent e

xpen

se) b

eing

add

ed b

ack

to E

BITD

A fo

r the

val

uatio

n m

ultip

le c

alcu

latio

n(d

) 201

0E P

/E d

ivid

ed b

y Fi

rst C

all m

ean

or S

tifel

Nic

olau

s esti

mat

ed lo

ng-te

rm g

rowt

h ra

teEx

clud

es n

on-r

ecur

ring

item

sCa

lcul

atio

ns m

ay v

ary

due

to ro

undi

ng

Sour

ce: C

ompa

ny d

ata

, Firs

t Cal

l, an

d St

ifel N

icol

aus e

stim

ates

Com

para

tive

Val

uatio

n M

atrix

Equi

ty v

alue

as

a m

ultip

le o

fEn

terp

rise

valu

e as

a m

ultip

le o

f

A Parcel Shipping Experiment March 2, 2012 - 12 - Stifel, Nicolaus & Company, Inc.

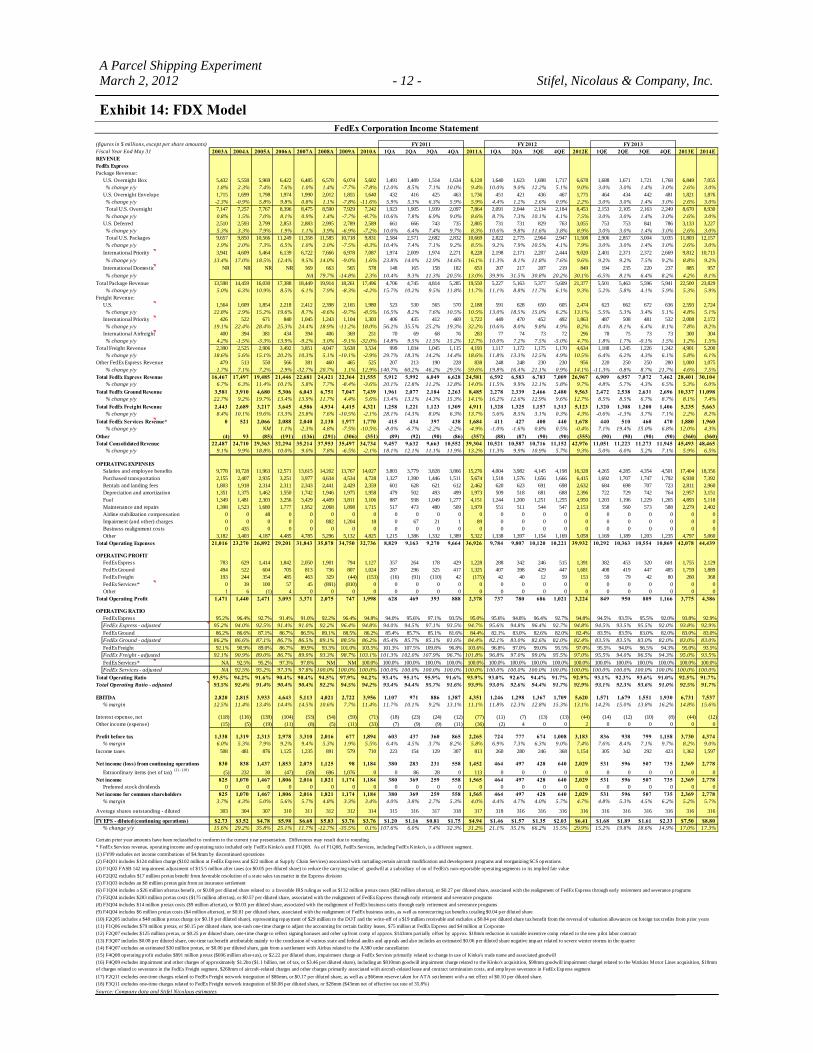

Exhibit 14: FDX Model

(figures in $ millions, except per share amounts)Fiscal Year End May 31 2003A 2004A 2005A 2006A 2007A 2008A 2009A 2010A 1QA 2QA 3QA 4QA 2011A 1QA 2QA 3QE 4QE 2012E 1QE 2QE 3QE 4QE 2013E 2014EREVENUEFedEx ExpressPackage Revenue:

U.S. Overnight Box 5,432 5,558 5,969 6,422 6,485 6,578 6,074 5,602 1,491 1,489 1,514 1,634 6,128 1,640 1,623 1,698 1,717 6,678 1,688 1,671 1,721 1,768 6,849 7,055 % change y/y 1.8% 2.3% 7.4% 7.6% 1.0% 1.4% -7.7% -7.8% 12.0% 8.5% 7.1% 10.0% 9.4% 10.0% 9.0% 12.2% 5.1% 9.0% 3.0% 3.0% 1.4% 3.0% 2.6% 3.0%U.S. Overnight Envelope 1,715 1,699 1,798 1,974 1,990 2,012 1,855 1,640 432 416 425 463 1,736 451 421 436 467 1,775 464 434 442 481 1,821 1,876 % change y/y -2.3% -0.9% 5.8% 9.8% 0.8% 1.1% -7.8% -11.6% 5.9% 5.3% 6.3% 5.9% 5.9% 4.4% 1.2% 2.6% 0.9% 2.2% 3.0% 3.0% 1.4% 3.0% 2.6% 3.0% Total U.S. Overnight 7,147 7,257 7,767 8,396 8,475 8,590 7,929 7,242 1,923 1,905 1,939 2,097 7,864 2,091 2,044 2,134 2,184 8,453 2,153 2,105 2,163 2,249 8,670 8,930 % change y/y 0.8% 1.5% 7.0% 8.1% 0.9% 1.4% -7.7% -8.7% 10.6% 7.8% 6.9% 9.0% 8.6% 8.7% 7.3% 10.1% 4.1% 7.5% 3.0% 3.0% 1.4% 3.0% 2.6% 3.0%U.S. Deferred 2,510 2,593 2,799 2,853 2,883 2,995 2,789 2,589 661 666 743 735 2,805 731 731 829 763 3,055 753 753 841 786 3,133 3,227 % change y/y 5.3% 3.3% 7.9% 1.9% 1.1% 3.9% -6.9% -7.2% 10.0% 6.4% 7.4% 9.7% 8.3% 10.6% 9.8% 11.6% 3.8% 8.9% 3.0% 3.0% 1.4% 3.0% 2.6% 3.0% Total U.S. Packages 9,657 9,850 10,566 11,249 11,358 11,585 10,718 9,831 2,584 2,571 2,682 2,832 10,669 2,822 2,775 2,964 2,947 11,508 2,906 2,857 3,004 3,035 11,803 12,157 % change y/y 1.9% 2.0% 7.3% 6.5% 1.0% 2.0% -7.5% -8.3% 10.4% 7.4% 7.1% 9.2% 8.5% 9.2% 7.9% 10.5% 4.1% 7.9% 3.0% 3.0% 1.4% 3.0% 2.6% 3.0%International Priority 3,941 4,609 5,464 6,139 6,722 7,666 6,978 7,087 1,974 2,009 1,974 2,271 8,228 2,198 2,171 2,207 2,444 9,020 2,401 2,371 2,372 2,669 9,812 10,715 % change y/y 13.4% 17.0% 18.5% 12.4% 9.5% 14.0% -9.0% 1.6% 23.8% 14.0% 12.9% 14.6% 16.1% 11.3% 8.1% 11.8% 7.6% 9.6% 9.2% 9.2% 7.5% 9.2% 8.8% 9.2%International Domestic NR NR NR NR 369 663 565 578 148 165 158 182 653 207 217 207 219 849 194 235 220 237 885 957 % change y/y NA 79.7% -14.8% 2.3% 10.4% 9.3% 11.3% 20.5% 13.0% 39.9% 31.5% 30.8% 20.2% 30.1% -6.5% 8.1% 6.4% 8.2% 4.2% 8.1%

Total Package Revenue 13,598 14,459 16,030 17,388 18,449 19,914 18,261 17,496 4,706 4,745 4,814 5,285 19,550 5,227 5,163 5,377 5,609 21,377 5,501 5,463 5,596 5,941 22,500 23,829 % change y/y 5.0% 6.3% 10.9% 8.5% 6.1% 7.9% -8.3% -4.2% 15.7% 10.2% 9.5% 11.8% 11.7% 11.1% 8.8% 11.7% 6.1% 9.3% 5.2% 5.8% 4.1% 5.9% 5.3% 5.9%

Freight Revenue:U.S. 1,564 1,609 1,854 2,218 2,412 2,398 2,165 1,980 523 530 565 570 2,188 591 628 650 605 2,474 623 662 672 636 2,593 2,724 % change y/y 22.8% 2.9% 15.2% 19.6% 8.7% -0.6% -9.7% -8.5% 16.5% 8.2% 7.6% 10.5% 10.5% 13.0% 18.5% 15.0% 6.2% 13.1% 5.5% 5.3% 3.4% 5.1% 4.8% 5.1%International Priority 426 522 671 840 1,045 1,243 1,104 1,303 406 435 412 469 1,722 449 470 452 492 1,863 487 508 481 532 2,008 2,172 % change y/y 19.1% 22.4% 28.4% 25.3% 24.4% 18.9% -11.2% 18.0% 56.2% 35.5% 25.2% 19.3% 32.2% 10.6% 8.0% 9.8% 4.9% 8.2% 8.4% 8.1% 6.4% 8.1% 7.8% 8.2%International Airfreight 400 394 381 434 394 406 369 251 70 69 68 76 283 77 74 73 72 296 78 75 73 73 300 304 % change y/y 4.2% -1.5% -3.3% 13.9% -9.2% 3.0% -9.1% -32.0% 14.8% 9.5% 11.5% 15.2% 12.7% 10.0% 7.2% 7.5% -5.0% 4.7% 1.8% 1.7% -0.1% 1.5% 1.2% 1.5%

Total Freight Revenue 2,390 2,525 2,906 3,492 3,851 4,047 3,638 3,534 999 1,034 1,045 1,115 4,193 1,117 1,172 1,175 1,170 4,634 1,188 1,245 1,226 1,242 4,901 5,200 % change y/y 18.6% 5.6% 15.1% 20.2% 10.3% 5.1% -10.1% -2.9% 29.7% 18.3% 14.2% 14.4% 18.6% 11.8% 13.3% 12.5% 4.9% 10.5% 6.4% 6.2% 4.3% 6.1% 5.8% 6.1%

Other FedEx Express Revenue 479 513 550 566 381 460 465 525 207 213 190 228 838 248 248 230 230 956 220 250 250 280 1,000 1,075 % change y/y 1.7% 7.1% 7.2% 2.9% -32.7% 20.7% 1.1% 12.9% 140.7% 60.2% 46.2% 29.5% 59.6% 19.8% 16.4% 21.1% 0.9% 14.1% -11.3% 0.8% 8.7% 21.7% 4.6% 7.5%

Total FedEx Express Revenue 16,467 17,497 19,485 21,446 22,681 24,421 22,364 21,555 5,912 5,992 6,049 6,628 24,581 6,592 6,583 6,783 7,009 26,967 6,909 6,957 7,072 7,462 28,401 30,104 % change y/y 6.7% 6.3% 11.4% 10.1% 5.8% 7.7% -8.4% -3.6% 20.1% 12.8% 11.2% 12.8% 14.0% 11.5% 9.9% 12.1% 5.8% 9.7% 4.8% 5.7% 4.3% 6.5% 5.3% 6.0%

Total FedEx Ground Revenue 3,581 3,910 4,680 5,306 6,043 6,751 7,047 7,439 1,961 2,077 2,184 2,263 8,485 2,278 2,339 2,466 2,480 9,563 2,472 2,538 2,631 2,696 10,337 11,098 % change y/y 22.7% 9.2% 19.7% 13.4% 13.9% 11.7% 4.4% 5.6% 13.4% 13.1% 14.3% 15.3% 14.1% 16.2% 12.6% 12.9% 9.6% 12.7% 8.5% 8.5% 6.7% 8.7% 8.1% 7.4%

Total FedEx Freight Revenue 2,443 2,689 3,217 3,645 4,586 4,934 4,415 4,321 1,258 1,221 1,123 1,309 4,911 1,328 1,325 1,157 1,313 5,123 1,320 1,308 1,200 1,406 5,235 5,663 % change y/y 8.4% 10.1% 19.6% 13.3% 25.8% 7.6% -10.5% -2.1% 28.1% 14.3% 8.0% 6.3% 13.7% 5.6% 8.5% 3.1% 0.3% 4.3% -0.6% -1.3% 3.7% 7.1% 2.2% 8.2%

Total FedEx Services Revenue* 0 521 2,066 2,088 2,040 2,138 1,977 1,770 415 434 397 438 1,684 411 427 400 440 1,678 440 510 460 470 1,880 1,960 % change y/y NM 1.1% -2.3% 4.8% -7.5% -10.5% -8.0% -6.7% -2.2% -2.2% -4.9% -1.0% -1.6% 0.8% 0.5% -0.4% 7.1% 19.4% 15.0% 6.8% 12.0% 4.3%

Other (4) 93 (85) (191) (136) (291) (306) (351) (89) (92) (90) (86) (357) (88) (87) (90) (90) (355) (90) (90) (90) (90) (360) (360)Total Consolidated Revenue 22,487 24,710 29,363 32,294 35,214 37,953 35,497 34,734 9,457 9,632 9,663 10,552 39,304 10,521 10,587 10,716 11,152 42,976 11,051 11,223 11,273 11,945 45,493 48,465

% change y/y 9.1% 9.9% 18.8% 10.0% 9.0% 7.8% -6.5% -2.1% 18.1% 12.1% 11.1% 11.9% 13.2% 11.3% 9.9% 10.9% 5.7% 9.3% 5.0% 6.0% 5.2% 7.1% 5.9% 6.5%

OPERATING EXPENSESSalaries and employee benefits 9,778 10,728 11,963 12,571 13,615 14,202 13,767 14,027 3,803 3,779 3,828 3,866 15,276 4,004 3,982 4,145 4,198 16,328 4,265 4,285 4,354 4,501 17,404 18,356Purchased transportation 2,155 2,407 2,935 3,251 3,977 4,634 4,534 4,728 1,327 1,390 1,446 1,511 5,674 1,518 1,576 1,656 1,666 6,415 1,692 1,707 1,747 1,792 6,938 7,392Rentals and landing fees 1,803 1,918 2,314 2,311 2,343 2,441 2,429 2,359 601 628 621 612 2,462 620 623 691 698 2,632 684 698 707 723 2,811 2,960Depreciation and amortization 1,351 1,375 1,462 1,550 1,742 1,946 1,975 1,958 479 502 493 499 1,973 509 518 681 688 2,396 722 729 742 764 2,957 3,151Fuel 1,349 1,481 2,303 3,256 3,429 4,409 3,811 3,106 887 938 1,049 1,277 4,151 1,244 1,200 1,251 1,255 4,950 1,203 1,196 1,229 1,265 4,893 5,118Maintenance and repairs 1,398 1,523 1,680 1,777 1,952 2,068 1,898 1,715 517 473 480 509 1,979 551 511 544 547 2,153 558 560 573 588 2,279 2,402Airline stabilization compensation 0 0 48 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0Impairment (and other) charges 0 0 0 0 0 882 1,204 18 0 67 21 1 89 0 0 0 0 0 0 0 0 0 0 0Business realignment costs 0 435 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0Other 3,182 3,403 4,187 4,485 4,785 5,296 5,132 4,825 1,215 1,386 1,332 1,389 5,322 1,338 1,397 1,154 1,169 5,058 1,169 1,189 1,203 1,235 4,797 5,060

Total Operating Expenses 21,016 23,270 26,892 29,201 31,843 35,878 34,750 32,736 8,829 9,163 9,270 9,664 36,926 9,784 9,807 10,120 10,221 39,932 10,292 10,363 10,554 10,869 42,078 44,439

OPERATING PROFITFedEx Express 783 629 1,414 1,842 2,050 1,901 794 1,127 357 264 178 429 1,228 288 342 246 515 1,391 382 453 320 601 1,755 2,129FedEx Ground 494 522 604 705 813 736 807 1,024 287 296 325 417 1,325 407 398 429 447 1,681 408 419 447 485 1,759 1,889FedEx Freight 193 244 354 485 463 329 (44) (153) (16) (91) (110) 42 (175) 42 40 12 59 153 59 79 42 80 260 368FedEx Services* 0 39 100 57 45 (891) (810) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0Other 1 6 (1) 4 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Total Operating Profit 1,471 1,440 2,471 3,093 3,371 2,075 747 1,998 628 469 393 888 2,378 737 780 686 1,021 3,224 849 950 809 1,166 3,775 4,386

OPERATING RATIOFedEx Express 95.2% 96.4% 92.7% 91.4% 91.0% 92.2% 96.4% 94.8% 94.0% 95.6% 97.1% 93.5% 95.0% 95.6% 94.8% 96.4% 92.7% 94.8% 94.5% 93.5% 95.5% 92.0% 93.8% 92.9%FedEx Express - adjusted 95.2% 94.0% 92.5% 91.4% 91.0% 92.2% 96.4% 94.8% 94.0% 94.5% 97.1% 93.5% 94.7% 95.6% 94.8% 96.4% 92.7% 94.8% 94.5% 93.5% 95.5% 92.0% 93.8% 92.9%FedEx Ground 86.2% 86.6% 87.1% 86.7% 86.5% 89.1% 88.5% 86.2% 85.4% 85.7% 85.1% 81.6% 84.4% 82.1% 83.0% 82.6% 82.0% 82.4% 83.5% 83.5% 83.0% 82.0% 83.0% 83.0%FedEx Ground - adjusted 86.2% 86.6% 87.1% 86.7% 86.5% 89.1% 88.5% 86.2% 85.4% 85.7% 85.1% 81.6% 84.4% 82.1% 83.0% 82.6% 82.0% 82.4% 83.5% 83.5% 83.0% 82.0% 83.0% 83.0%FedEx Freight 92.1% 90.9% 89.0% 86.7% 89.9% 93.3% 101.0% 103.5% 101.3% 107.5% 109.8% 96.8% 103.6% 96.8% 97.0% 99.0% 95.5% 97.0% 95.5% 94.0% 96.5% 94.3% 95.0% 93.5%FedEx Freight - adjusted 92.1% 90.9% 89.0% 86.7% 89.9% 93.3% 98.7% 103.1% 101.3% 102.0% 107.9% 96.7% 101.8% 96.8% 97.0% 99.0% 95.5% 97.0% 95.5% 94.0% 96.5% 94.3% 95.0% 93.5%FedEx Services* NA 92.5% 95.2% 97.3% 97.8% NM NM 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%FedEx Services - adjusted NA 92.5% 95.2% 97.3% 97.8% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Total Operating Ratio 93.5% 94.2% 91.6% 90.4% 90.4% 94.5% 97.9% 94.2% 93.4% 95.1% 95.9% 91.6% 93.9% 93.0% 92.6% 94.4% 91.7% 92.9% 93.1% 92.3% 93.6% 91.0% 92.5% 91.7%Total Operating Ratio - adjusted 93.5% 92.4% 91.4% 90.4% 90.4% 92.2% 94.5% 94.2% 93.4% 94.4% 95.7% 91.6% 93.9% 93.0% 92.6% 94.4% 91.7% 92.9% 93.1% 92.3% 93.6% 91.0% 92.5% 91.7%

EBITDA 2,820 2,815 3,933 4,643 5,113 4,021 2,722 3,956 1,107 971 886 1,387 4,351 1,246 1,298 1,367 1,709 5,620 1,571 1,679 1,551 1,930 6,731 7,537% margin 12.5% 11.4% 13.4% 14.4% 14.5% 10.6% 7.7% 11.4% 11.7% 10.1% 9.2% 13.1% 11.1% 11.8% 12.3% 12.8% 15.3% 13.1% 14.2% 15.0% 13.8% 16.2% 14.8% 15.6%

Interest expense, net (118) (116) (139) (104) (53) (54) (59) (71) (18) (23) (24) (12) (77) (11) (7) (13) (13) (44) (14) (12) (10) (8) (44) (12)Other income (expense) (15) (5) (19) (11) (8) (5) (11) (33) (7) (9) (9) (11) (36) (2) 4 0 0 2 0 0 0 0 0 0

Profit before tax 1,338 1,319 2,313 2,978 3,310 2,016 677 1,894 603 437 360 865 2,265 724 777 674 1,008 3,183 836 938 799 1,158 3,730 4,374% margin 6.0% 5.3% 7.9% 9.2% 9.4% 5.3% 1.9% 5.5% 6.4% 4.5% 3.7% 8.2% 5.8% 6.9% 7.3% 6.3% 9.0% 7.4% 7.6% 8.4% 7.1% 9.7% 8.2% 9.0%

Income taxes 508 481 876 1,125 1,235 891 579 710 223 154 129 307 813 260 280 246 368 1,154 305 342 292 423 1,362 1,597

Net income (loss) from continuing operations 830 838 1,437 1,853 2,075 1,125 98 1,184 380 283 231 558 1,452 464 497 428 640 2,029 531 596 507 735 2,369 2,778Extraordinary items (net of tax) (1) - (18) (5) 232 30 (47) (59) 696 1,076 0 0 86 28 0 113 0 0 0 0 0 0 0 0 0 0 0

Net income 825 1,070 1,467 1,806 2,016 1,821 1,174 1,184 380 369 259 558 1,565 464 497 428 640 2,029 531 596 507 735 2,369 2,778Preferred stock dividends 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Net income for common shareholders 825 1,070 1,467 1,806 2,016 1,821 1,174 1,184 380 369 259 558 1,565 464 497 428 640 2,029 531 596 507 735 2,369 2,778% margin 3.7% 4.3% 5.0% 5.6% 5.7% 4.8% 3.3% 3.4% 4.0% 3.8% 2.7% 5.3% 4.0% 4.4% 4.7% 4.0% 5.7% 4.7% 4.8% 5.3% 4.5% 6.2% 5.2% 5.7%

Average shares outstanding - diluted 303 304 307 310 311 312 312 314 315 316 317 318 317 318 316 316 316 316 316 316 316 316 316 316

FY EPS - diluted (continuing operations) $2.73 $3.52 $4.78 $5.98 $6.68 $5.83 $3.76 $3.76 $1.20 $1.16 $0.81 $1.75 $4.94 $1.46 $1.57 $1.35 $2.03 $6.41 $1.68 $1.89 $1.61 $2.33 $7.50 $8.80% change y/y 15.6% 29.2% 35.8% 25.1% 11.7% -12.7% -35.5% 0.1% 107.6% 6.0% 7.4% 32.3% 31.2% 21.1% 35.1% 66.2% 15.5% 29.9% 15.2% 19.8% 18.6% 14.9% 17.0% 17.3%

Source: Company data and Stifel Nicolaus estimates

(10) F2Q05 includes a $48 million pretax charge (or $0.10 per diluted share), representing repayment of $29 million to the DOT and the write-off of a $19 million receivable and excludes a $0.04 per diluted share tax benefit from the reversal of valuation allowances on foreign tax credits from prior years (11) F1Q06 excludes $79 million pretax, or $0.15 per diluted share, non-cash one-time charge to adjust the accounting for certain facility leases, $75 million at FedEx Express and $4 million at Corporate(12) F2Q07 excludes $125 million pretax, or $0.25 per diluted share, one-time charge to reflect signing bonuses and other upfront comp of approx. $143mm partially offset by approx. $18mm reduction in variable incentive comp related to the new pilot labor contract(13) F3Q07 includes $0.08 per diluted share, one-time tax benefit attributable mainly to the conclusion of various state and federal audits and appeals and also includes an estimated $0.06 per diluted share negative impact related to severe winter storms in the quarter(14) F4Q07 excludes an estimated $30 million pretax, or $0.06 per diluted share, gain from a settlement with Airbus related to the A380 order cancellation(15) F4Q08 operating profit excludes $891 million pretax ($696 million after-tax), or $2.22 per diluted share, impairment charge at FedEx Services primarily related to change in use of Kinko's trade name and associated goodwill(16) F4Q09 excludes impairment and other charges of approximately $1.2bn ($1.1 billion, net of tax, or $3.46 per diluted share), including an $810mm goodwill impairment charge related to the Kinko's acquisition, $90mm goodwill impairment chargel related to the Watkins Motor Lines acquisition, $10mm of charges related to severance in the FedEx Freight segment, $260mm of aircraft-related charges and other charges primarily associated with aircraft-related lease and contract termination costs, and employee severance in FedEx Express segment

FedEx Corporation Income Statement

Certain prior year amounts have been reclassified to conform to the current year presentation. Differences may result due to rounding.* FedEx Services revenue, operating income and operating ratio included only FedEx Kinko's until F1Q08. As of F1Q08, FedEx Services, including FedEx Kinko's, is a different segment.(1) FY99 excludes net income contributions of $4.9mm by discontinued operations(2) F4Q01 includes $124 million charge ($102 million at FedEx Express and $22 million at Supply Chain Services) associated with curtailing certain aircraft modification and development programs and reorganizing SCS operations

(18) F3Q11 excludes one-time charges related to FedEx Freight network integration of $0.08 per diluted share, or $28mm ($43mm net of effective tax rate of 35.8%)

FY 2012

(3) F1Q02 FASB 142 impairment adjustment of $15.5 million after taxes (or $0.05 per diluted share) to reduce the carrying value of goodwill at a subsidiary of on of FedEx's non-reportable operating segments to its implied fair value

(5) F1Q03 includes an $8 million pretax gain from an insurance settlement(4) F2Q02 excludes $17 million pretax benefit from favorable resolution of a state sales tax matter in the Express division

(6) F1Q04 includes a $26 million aftertax benefit, or $0.08 per diluted share related to a favorable IRS ruling as well as $132 million pretax costs ($82 million aftertax), or $0.27 per diluted share, associated with the realignment of FedEx Express through early retirement and severance programs

(17) F2Q11 excludes one-time charges related to FedEx Freight network integration of $86mm, or $0.17 per diluted share, as well as a $66mm reserve taken for ATA settlement with a net effect of $0.10 per diluted share.

(7) F2Q04 includes $283 million pretax costs ($175 million aftertax), or $0.57 per diluted share, associated with the realignment of FedEx Express through early retirement and severance programs

(9) F4Q04 includes $6 million pretax costs ($4 million aftertax), or $0.01 per diluted share, associated with the realignment of FedEx business units, as well as nonrecurring tax benefits totaling $0.04 per diluted share(8) F3Q04 includes $14 million pretax costs ($9 million aftertax), or $0.03 per diluted share, associated with the realignment of FedEx business units through early retirement and severance programs

FY 2011 FY 2013

A Parcel Shipping Experiment March 2, 2012 - 13 - Stifel, Nicolaus & Company, Inc.

Exhibit 15: UPS Model

(figures in $ millions, except per share amounts)1999A 2000A 2001A 2002A 2003A 2004A 2005A 2006A 2007A 2008A 2009A 1QA 2QA 3QA 4QA 2010A 1QA 2QA 3QA 4QA 2011A 1QE 2QE 3QE 4QE 2012E 2013E

REVENUEU.S. Domestic Package:

Next Day Air 5,240 5,664 5,479 5,393 5,621 6,084 6,381 6,778 6,738 6,559 5,456 1,382 1,463 1,466 1,524 5,835 1,495 1,562 1,588 1,584 6,229 1,547 1,617 1,618 1,613 6,396 6,622 % change y/y 11.7% 8.1% -3.3% -1.6% 4.2% 8.2% 4.9% 6.2% -0.6% -2.7% -16.8% 0.1% 11.3% 8.8% 7.9% 6.9% 8.2% 6.8% 8.3% 3.9% 6.8% 3.5% 3.5% 1.9% 1.9% 2.7% 3.5%Deferred 2,694 2,910 2,928 2,902 3,015 3,193 3,258 3,424 3,359 3,325 2,859 694 698 696 887 2,975 753 764 760 1,022 3,299 779 791 775 1,040 3,385 3,522 % change y/y 9.3% 8.0% 0.6% -0.9% 3.9% 5.9% 2.0% 5.1% -1.9% -1.0% -14.0% 0.1% 7.1% 4.8% 4.4% 4.1% 8.5% 9.5% 9.2% 15.2% 10.9% 3.5% 3.5% 1.9% 1.8% 2.6% 4.0%Ground 14,379 15,428 15,984 15,985 16,726 17,683 18,971 20,254 20,888 21,394 19,843 5,026 5,108 5,129 5,669 20,932 5,295 5,411 5,419 6,064 22,189 5,589 5,710 5,630 6,326 23,255 24,482 % change y/y 6.5% 7.3% 3.6% 0.0% 4.6% 5.7% 7.3% 6.8% 3.1% 2.4% -7.2% 3.1% 5.9% 5.6% 7.2% 5.5% 5.4% 5.9% 5.7% 7.0% 6.0% 5.5% 5.5% 3.9% 4.3% 4.8% 5.3%

Total U.S. Domestic Package 22,313 24,002 24,391 24,280 25,362 26,960 28,610 30,456 30,985 31,278 28,158 7,102 7,269 7,291 8,080 29,742 7,543 7,737 7,767 8,670 31,717 7,915 8,118 8,023 8,980 33,036 34,626 % change y/y 8.1% 7.6% 1.6% -0.5% 4.5% 6.3% 6.1% 6.5% 1.7% 0.9% -10.0% 2.2% 7.1% 6.2% 7.0% 5.6% 6.2% 6.4% 6.5% 7.3% 6.6% 4.9% 4.9% 3.3% 3.6% 4.2% 4.8%

International Package:Domestic 924 904 907 943 1,134 1,346 1,588 1,950 2,177 2,344 2,111 584 561 569 651 2,365 629 672 660 667 2,628 636 685 676 683 2,679 2,843 % change y/y -3.0% -2.2% 0.3% 4.0% 20.3% 18.7% 18.0% 22.8% 11.6% 7.7% -9.9% 25.9% 17.4% 6.2% 2.8% 12.0% 7.7% 19.8% 16.0% 2.5% 11.1% 1.1% 2.0% 2.4% 2.3% 1.9% 6.1%Export 2,479 2,818 2,966 3,316 4,049 4,991 5,856 6,554 7,488 8,294 7,176 1,932 2,085 1,975 2,242 8,234 2,131 2,316 2,251 2,358 9,056 2,237 2,456 2,396 2,509 9,599 10,384 % change y/y 13.9% 13.7% 5.3% 11.8% 22.1% 23.3% 17.3% 11.9% 14.3% 10.8% -13.5% 14.6% 24.3% 11.6% 9.7% 14.7% 10.3% 11.1% 14.0% 5.2% 10.0% 5.0% 6.1% 6.5% 6.4% 6.0% 8.2%Cargo 315 356 407 461 426 472 533 585 616 655 412 123 125 132 154 534 140 151 146 128 565 126 136 131 134 528 554 % change y/y 22.6% 13.0% 14.3% 13.3% -7.6% 10.8% 12.9% 9.8% 5.3% 6.3% -37.1% 36.7% 37.4% 13.8% 33.9% 29.6% 13.8% 20.8% 10.6% -16.9% 5.8% -10.0% -10.0% -10.0% 5.0% -6.6% 5.0%

Total International Package 3,718 4,078 4,280 4,720 5,609 6,809 7,977 9,089 10,281 11,293 9,699 2,639 2,771 2,676 3,047 11,133 2,900 3,139 3,057 3,153 12,249 2,999 3,277 3,203 3,326 12,806 13,782 % change y/y 9.8% 9.7% 5.0% 10.3% 18.8% 21.4% 17.2% 13.9% 13.1% 9.8% -14.1% 17.8% 23.4% 10.5% 9.2% 14.8% 9.9% 13.3% 14.2% 3.5% 10.0% 3.4% 4.4% 4.8% 5.5% 4.5% 7.6%

Supply Chain and FreightForwarding and Logistics 603 836 1,479 1,969 2,126 2,379 4,737 5,681 5,911 6,293 5,080 1,391 1,498 1,536 1,597 6,022 1,429 1,539 1,552 1,583 6,103 1,458 1,616 1,630 1,662 6,365 6,875 % change y/y 33.4% 38.6% 76.9% 33.1% 8.0% 11.9% 99.1% 19.9% 4.0% 6.5% -19.3% 16.2% 26.6% 22.9% 10.1% 18.5% 2.7% 2.7% 1.0% -0.9% 1.3% 2.0% 5.0% 5.0% 5.0% 4.3% 8.0%Freight - - - - - - 797 1,952 2,108 2,191 1,943 492 555 581 580 2,208 604 660 667 632 2,563 658 719 727 689 2,794 3,017 % change y/y NM NM 8.0% 3.9% -11.3% 8.4% 9.5% 14.1% 22.6% 13.6% 22.8% 18.9% 14.8% 9.0% 16.1% 9.0% 9.0% 9.0% 9.0% 9.0% 8.0%Other 238 582 171 303 388 434 460 369 407 431 417 104 111 108 117 440 106 116 123 128 473 111 122 129 134 497 512 % change y/y 120.4% 144.5% -70.6% 77.2% 28.1% 11.9% 6.0% -19.8% 10.3% 5.9% -3.2% 6.1% 6.7% 3.8% 5.4% 5.5% 1.9% 4.5% 13.9% 9.4% 7.5% 5.0% 5.0% 5.0% 5.0% 5.0% 3.0%

Total Supply Chain and Freight 841 1,418 1,650 2,272 2,514 2,813 5,994 8,002 8,426 8,915 7,440 1,987 2,164 2,225 2,294 8,670 2,139 2,315 2,342 2,343 9,139 2,227 2,457 2,486 2,485 9,656 10,403 % change y/y 50.2% 68.6% 16.4% 37.7% 10.7% 11.9% 113.1% 33.5% 5.3% 5.8% -16.5% 13.6% 20.6% 19.4% 12.8% 16.5% 7.6% 7.0% 5.3% 2.1% 5.4% 4.1% 6.1% 6.1% 6.1% 5.7% 7.7%

Total consolidated revenue 26,872 29,498 30,321 31,272 33,485 36,582 42,581 47,547 49,692 51,486 45,297 11,728 12,204 12,192 13,421 49,545 12,582 13,191 13,166 14,166 53,105 13,142 13,853 13,712 14,791 55,498 58,811 % change y/y 9.3% 9.8% 2.8% 3.1% 7.1% 9.2% 16.4% 11.7% 4.5% 3.6% -12.0% 7.2% 12.7% 9.3% 8.4% 9.4% 7.3% 8.1% 8.0% 5.6% 7.2% 4.4% 5.0% 4.1% 4.4% 4.5% 6.0%

OPERATING EXPENSESCompensation and benefits 15,285 16,546 17,311 18,046 19,251 20,760 22,517 24,421 25,577 26,063 25,640 6,539 6,515 6,411 6,859 26,324 6,608 6,683 6,694 7,730 27,715 6,885 7,045 6,960 7,454 28,344 29,827Repairs and maintenance 945 843 927 873 955 1,005 1,097 1,150 1,157 1,194 1,075 274 281 282 294 1,131 315 317 324 330 1,286 301 322 306 305 1,233 1,298Depreciation and amortization 1,139 1,173 1,396 1,464 1,549 1,543 1,644 1,748 1,745 1,814 1,747 451 449 448 444 1,792 441 443 447 451 1,782 463 477 470 508 1,918 2,018Purchased transportation 1,499 1,679 1,652 1,665 1,828 2,059 4,050 5,467 5,902 6,550 5,379 1,501 1,613 1,656 1,870 6,640 1,648 1,762 1,796 2,026 7,232 1,736 1,848 1,822 2,032 7,437 7,828Fuel 681 954 1,000 952 1,050 1,416 2,085 2,655 2,974 4,134 2,365 678 717 724 853 2,972 908 1,057 1,015 1,066 4,046 926 954 940 1,041 3,861 4,063Other occupancy 373 527 647 653 730 752 872 938 958 1,027 985 262 216 222 239 939 261 225 229 228 943 278 262 259 279 1,078 1,134Other expenses 3,045 3,264 3,426 3,614 3,653 3,885 4,173 4,446 4,412 4,747 4,305 981 1,011 833 1,048 3,873 975 1,006 1,042 1,138 4,161 984 1,013 999 1,079 4,075 4,289

Total operating expenses 22,967 24,986 26,359 27,267 29,016 31,420 36,438 40,825 42,725 45,529 41,496 10,686 10,802 10,576 11,607 43,671 11,156 11,493 11,547 12,969 47,165 11,571 11,921 11,756 12,699 47,947 50,457Total operating ratio 85.5% 84.7% 86.9% 87.2% 86.7% 85.9% 85.6% 85.9% 86.0% 88.4% 91.6% 91.1% 88.5% 86.7% 86.5% 88.1% 88.7% 87.1% 87.7% 91.6% 88.8% 88.0% 86.1% 85.7% 85.9% 86.4% 85.8%

By segment:OPERATING EXPENSES

U.S. Domestic Package 18,807 20,073 20,422 20,530 21,705 23,104 24,117 25,446 26,204 27,371 25,839 6,442 6,521 6,380 7,037 26,380 6,694 6,756 6,752 7,381 27,583 6,930 6,929 6,816 7,664 28,339 29,527International Package 3,488 3,801 4,141 4,393 4,877 5,641 6,483 7,379 8,381 9,686 8,332 2,212 2,250 2,257 2,510 9,229 2,454 2,642 2,648 2,656 10,400 2,548 2,732 2,673 2,760 10,713 11,387Supply Chain and Freight 672 1,112 1,796 2,344 2,458 2,675 5,838 8,000 8,094 8,472 7,144 1,896 2,031 2,048 2,118 8,093 2,008 2,128 2,147 2,152 8,435 2,094 2,261 2,267 2,274 8,895 9,543

Total operating expenses 22,967 24,986 26,359 27,267 29,040 31,420 36,438 40,825 42,679 45,529 41,315 10,550 10,802 10,685 11,665 43,702 11,156 11,526 11,547 12,189 46,418 11,571 11,921 11,756 12,699 47,947 50,457

OPERATING PROFITU.S. Domestic Package 3,506 3,929 3,969 3,750 3,657 3,856 4,493 5,010 4,781 3,907 2,319 660 748 911 1,043 3,362 849 981 1,015 1,289 4,134 985 1,189 1,207 1,316 4,698 5,099International Package 230 277 139 327 732 1,168 1,494 1,710 1,900 1,607 1,367 427 521 419 537 1,904 446 497 409 497 1,849 451 546 530 565 2,093 2,394Supply Chain and Freight 169 306 (146) (72) 56 138 156 2 332 443 296 91 133 177 176 577 131 187 195 191 704 134 197 219 211 760 860

Total operating profit 3,905 4,512 3,962 4,005 4,445 5,162 6,143 6,722 7,013 5,957 3,982 1,178 1,402 1,507 1,756 5,843 1,426 1,665 1,619 1,977 6,687 1,570 1,932 1,956 2,092 7,551 8,354

OPERATING RATIOU.S. Domestic Package 84.3% 83.6% 83.7% 84.6% 85.6% 85.7% 84.3% 83.6% 84.6% 87.5% 91.8% 90.7% 89.7% 87.5% 87.1% 88.7% 88.7% 87.3% 86.9% 85.1% 87.0% 87.6% 85.4% 85.0% 85.4% 85.8% 85.3%International Package 93.8% 93.2% 96.8% 93.1% 86.9% 82.8% 81.3% 81.2% 81.5% 85.8% 85.9% 83.8% 81.2% 84.3% 82.4% 82.9% 84.6% 84.2% 86.6% 84.2% 84.9% 85.0% 83.4% 83.5% 83.0% 83.7% 82.6%Supply Chain and Freight 79.9% 78.4% 108.8% 103.2% 97.8% 95.1% 97.4% 100.0% 96.1% 95.0% 96.0% 95.4% 93.9% 92.0% 92.3% 93.3% 93.9% 91.9% 91.7% 91.8% 92.3% 94.0% 92.0% 91.2% 91.5% 92.1% 91.7%

Total operating ratio 85.5% 84.7% 86.9% 87.2% 86.7% 85.9% 85.6% 85.9% 86.0% 88.4% 91.6% 91.1% 88.5% 86.7% 86.5% 88.1% 88.7% 87.1% 87.7% 91.6% 88.8% 88.0% 86.1% 85.7% 85.9% 86.4% 85.8%

EBITDA 5,044 5,685 5,358 5,469 5,994 6,705 7,787 8,470 8,758 7,771 5,729 1,629 1,851 1,955 2,200 7,635 1,867 2,108 2,066 2,428 8,469 2,033 2,408 2,427 2,600 9,468 10,372% margin 18.8% 19.3% 17.7% 17.5% 17.9% 18.3% 18.3% 17.8% 17.6% 15.1% 12.6% 13.9% 15.2% 16.0% 16.4% 15.4% 14.8% 16.0% 15.7% 17.1% 15.9% 15.5% 17.4% 17.7% 17.6% 17.1% 17.6%

Investment income (16) 197 527 159 63 76 82 104 86 99 75 10 (4) (18) 15 10 3 11 9 16 8 44 14 14 14 14 56 57Interest expense (17) (228) (205) (184) (173) (121) (149) (172) (211) (246) (442) (368) (85) (84) (91) (94) (354) (85) (83) (84) (96) (348) (101) (101) (99) (96) (398) (367)Other income (expense) (1,786) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Profit before tax 2,088 4,834 3,937 3,895 4,400 5,095 6,075 6,597 6,866 5,590 3,624 1,089 1,300 1,431 1,672 5,492 1,352 1,591 1,551 1,889 6,383 1,483 1,844 1,871 2,010 7,209 8,044% margin 7.8% 16.4% 13.0% 12.5% 13.1% 13.9% 14.3% 13.9% 13.8% 10.9% 8.0% 9.3% 10.7% 11.7% 12.5% 11.1% 10.7% 12.1% 11.8% 13.3% 12.0% 11.3% 13.3% 13.6% 13.6% 13.0% 13.7%

Income taxes 1,205 1,900 1,512 1,473 1,629 1,794 2,205 2,392 2,497 2,012 1,308 381 455 501 585 1,922 467 548 509 666 2,190 519 646 655 704 2,523 2,815Tax rate 57.7% 39.3% 38.4% 37.8% 37.0% 35.2% 36.3% 36.3% 36.4% 36.0% 36.1% 35.0% 35.0% 35.0% 35.0% 35.0% 34.5% 34.4% 32.8% 35.3% 34.3% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%

Net income (loss) from continuing operations 883 2,934 2,425 2,422 2,771 3,301 3,870 4,205 4,369 3,578 2,316 708 845 930 1,087 3,570 885 1,043 1,042 1,223 4,193 964 1,199 1,216 1,307 4,686 5,229Extraordinary items (net of tax) (1) - (18) 1,442 (139) (26) 832 127 32 0 (3) (3,987) (575) (164) (175) 0 61 32 (82) 0 20 0 0 20 0 0 0 0 0 0

Net income 2,325 2,795 2,399 3,254 2,898 3,333 3,870 4,202 382 3,003 2,152 533 845 991 1,119 3,488 885 1,063 1,042 1,223 4,213 964 1,199 1,216 1,307 4,686 5,229Preferred stock dividends 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Net income for common shareholders 2,325 2,795 2,399 3,254 2,898 3,333 3,870 4,202 382 3,003 2,152 533 845 991 1,119 3,488 885 1,063 1,042 1,223 4,213 964 1,199 1,216 1,307 4,686 5,229% margin 8.7% 9.5% 7.9% 10.4% 8.7% 9.1% 9.1% 8.8% 0.8% 5.8% 4.8% 4.5% 6.9% 8.1% 8.3% 7.0% 7.0% 8.1% 7.9% 8.6% 7.9% 7.3% 8.7% 8.9% 8.8% 8.4% 8.9%

Average shares outstanding - diluted 1,141 1,175 1,144 1,134 1,138 1,137 1,116 1,089 1,063 1,022 1,004 1,004 1,003 1,004 1,004 1,004 1,002 998 987 977 991 971 965 960 956 963 951

EPS - diluted (continuing operations) $2.04 $2.38 $2.10 $2.14 $2.44 $2.90 $3.47 $3.86 $4.11 $3.50 $2.31 $0.71 $0.84 $0.93 $1.08 $3.56 $0.88 $1.05 $1.06 $1.25 $4.23 $0.99 $1.24 $1.27 $1.37 $4.87 $5.50% change y/y 29.7% 16.7% -11.8% 1.8% 14.0% 19.2% 19.4% 11.3% 6.5% -14.9% -34.1% 36.8% 71.6% 69.4% 43.6% 54.2% 25.2% 24.1% 14.0% 15.6% 19.0% 12.4% 18.9% 20.0% 9.2% 15.0% 12.9%

EPS - diluted $0.77 $2.50 $2.12 $2.87 $2.55 $2.93 $3.47 $3.86 $0.36 $2.93 $2.14 $0.53 $0.84 $0.99 $1.11 $3.47 $0.88 $1.07 $1.06 $1.25 $4.25 $0.99 $1.24 $1.27 $1.37 $4.87 $5.50% change y/y -50.7% NM -15.1% 35.4% -11.3% 15.1% 18.3% 11.4% -90.7% NM -26.8% 32.8% 90.1% 80.5% 47.8% 62.1% 66.4% 26.4% 7.0% 12.3% 22.3% 12.4% 16.7% 20.0% 9.2% 14.5% 12.9%

Certain prior year amounts have been reclassified to conform to the current year presentation

Source: Company data and Stifel Nicolaus estimates

(22) 4Q11 operating profit and consolidated income before income taxes excluded the impact of the pension mark-to-market loss related to pension expense recognized outside of a 10% corridor of $827 million, allocated between U.S. Domestic Package segment ($479 million), International Package segment ($171 million), and Supply Chain & Freight segment ($177 million); net of taxes, exlusion totals $527mm

United Parcel Service Income Statement

Effective January 1, 2005, UPS changed its reporting segments and restated income statement and operating statistic financials with no impact on cash flow or earnings back to 2001. Financials prior to 2001 are not on the same basis by segment and product.(1) 1999 Net Income excludes the tax assessment charge incurred in the second quarter of $1.786 billion pretax. The tax assessment reduced 1999 net income by $1.442 billion.(2) 2000 Net Income excludes $139 million related primarily to investment gains. Specifically, a $49 million gain from sale of UPS Truck Leasing subsidiary, $241 million gain on investment held by UPS' Strategic Enterprise Fund in two companies that were acquired by other companies, and a $59 million charge for retroactive costs associated with creating new full-time jobs from existing part-time Teamster jobs.

(21) 2Q11 operating profit and consolidated income before taxes excludes the impact of certain real estate transactions, including a $15 million loss for the U.S. Domestic Package segment and a $48 million gain in the Supply Chain & Freight segment, for a combined impact of $33mm ($20mm after-taxes)

(4) 2002 Net Income excludes $1.114 billion pre-tax in extraordinary items, net ($832 million after-tax). Specifically, a $1.023 billion credit to expense related to the difference between an original tax assessment expense charge recorded in 1999 and the estimated settlement amount now approved, a $106 million restructuring charge in connection with reorganization of non-package operations, and a credit to operating expenses for the elimination of $197 million in vacation liability due to change in accounting methodology.

2010

(5) 1Q03 Net Income excludes $55 million reduction in income taxes ($0.05 per diluted share benefit) due to the resolution of a number of outstanding tax issues. Those gains were partially offset by a writedown for $58 million ($0.03 per share) of UPS's marketable securities, reflecting market conditions.

2011

(15) 4Q08 excludes a $548 million goodwill impairment charge for UPS Freight and a $27 million intangible impairment charge for a customer list in UK domestic package business

(6) 2Q03 Net Income excludes $24 million charge resulting from the sale of the company's Mail Technologies unit, as well as a $38 million one-time tax benefit(7) 3Q03 Net Income excludes $24 million pretax gain on sale of UPS Aviation Technologies in the Non-Package segment as well as $22 million income tax reduction benefit based on a federal court ruling regarding the expensing of aircraft maintenance costs.(8) 4Q03 Net Income excludes $28 million pre-tax ($18 million after-tax) gain for the redemption of long-term debt. In addition, the company lowered its effective tax rate to reflect improvements in state taxes, thus reducing the provision for income taxes. This $39 million benefit has been excluded from net (9) 3Q04 Net Income excludes $99 million credit to tax expense due to the resolution of various tax matters

2012

(3) 2001 Net Income excludes $26 million related to FAS 133 cumulative adjustment.

(16) 1Q09 excludes a $181 million ($116 million after-tax) charge for on the company's DC-8 airframes, engines and parts due to an acceleration of the planned retirement of those aircraft

(10) 4Q04 Net Income excludes $110 million impairment charge ($70 million after-tax) on Boeing 727, 747, and McDonnell Douglas DC-8 aircraft, and related engines and parts, of which $91 million was related to the U.S. domestic package segment and $19 million to the International package segment. 4Q04 also excludes a $63 million charge ($40 million after-tax) to pension expense resulting from the consolidation of data collection systems in the U.S. domestic package segment. In addition, 4Q04 net income excludes net credits to income tax expense of $43 million related to various items, including the resolution of certain tax matters, the removal of a portion of the valuation allowances on certain deferred tax assets on NOL carryforwards and an adjustment for identified tax contingency items.

(17) 2Q09 excludes a $77 million charge for the remeasurement of certain obligations denominated in foreign currencies, in which hedge accounting was not able to be applied. 2Q09 investment income includes $17mm write-down related to certain preferred shares and auction rate securities (marked down to (18) 1Q10 excludes a $98 million restructuring charge related to the reorganization of Domestic Package's management structure - voluntary retirement benefits, severance, and unvested stock compensation, as well as a $38 million loss on the sale of a specialized transportation business in Germany ($99mm after-tax, in total), plus a $76mm charge to income tax expense, resulting from a change in the tax filing status of a German subsidiary(19) 3Q10 U.S. Domestic Package operating profit and consolidated income before income taxes exclude a $109 million gain on the sale of real estate; net income and earnings per share amounts exclude the after-tax effect of that real estate sale, which totaled $61 million.(20) 4Q10 Supply Chain & Freight operating profit excludes a $71mm gain on the sale of UPS Logistics Technologies, partially offset by the exclusion of a $13mm fair value adjustment loss related to the guarantee associated with the sale of a specialized transportation business in Germany that occurred in 1Q10, for a net exclusion of $58mm; net income and earnings per share amounts exclude the after tax-effect of the sale and fair value adjustment, which totaled $32mm, or $0.03 per diluted share

(11) 3Q06 Net Income excludes $87 million pretax charge for a tentative legal settlement involving a wage-and-hour case in California as well as a $52 million income tax benefit related to favorable developments with certain international tax issues.(12) 1Q07 excludes $221 million in pretax impairment charges on Boeing 727 and 747 aircraft, and related engines and parts ($159 million - U.S. Domestic Package and $62 million - International Package), due to the acceleration of the planned retirement of these aircraft. In addition, 1Q07 excludes a $68 million pretax charge ($53 million - U.S. Domestic Package, $7 million - International Package, and $8 million - Supply Chain & Freight) related to the special voluntary separation opportunity offered to about 640 employees to reflect the cash payout and acceleration of stock compensation and certain retiree healthcare benefits under the program. After-tax charges excluded in 1Q07 net income totaled $184 million.(13) 3Q07 excludes $46 million pretax charge ($31 million aftertax) related to the restructuring and disposal of certain operations in France within the Supply Chain segment.(14) 4Q07 excludes the $6.1 billion pre-tax ($3.8 billion after-tax) withdrawal payment to the Central States pension fun in the Domestic Package segment and on the compensation and benefits line

A Parcel Shipping Experiment March 2, 2012 - 14 - Stifel, Nicolaus & Company, Inc.

Important Disclosures and Certifications

I, David Ross, certify that the views expressed in this research report accurately reflect my personal views about the subject securities or issuers; and I, David Ross, certify that no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views contained in this research re-port. For our European Conflicts Management Policy go to the research page at www.stifel.com.

Source: Blue Matrix, Stifel Nicolaus For a price chart with our ratings and target price changes for FDX go to http://sf.bluematrix.com/bluematrix/Disclosure?ticker=FDX

Source: Blue Matrix, Stifel Nicolaus For a price chart with our ratings and target price changes for UPS go to http://sf.bluematrix.com/bluematrix/Disclosure?ticker=UPS

A Parcel Shipping Experiment March 2, 2012 - 15 - Stifel, Nicolaus & Company, Inc.

Stifel, Nicolaus & Company, Inc. expects to receive or intends to seek compensation for investment banking ser-vices from FedEx Corporation and United Parcel Service, Inc. in the next 3 months. Stifel, Nicolaus & Company, Inc. makes a market in the securities of FedEx Corporation and United Parcel Ser-vice, Inc.. Stifel, Nicolaus & Company, Inc.'s research analysts receive compensation that is based upon (among other fac-tors) Stifel Nicolaus' overall investment banking revenues. Our investment rating system is three tiered, defined as follows:

BUY -For U.S. securities we expect the stock to outperform the S&P 500 by more than 10% over the next 12 months. For Canadian securities we expect the stock to outperform the S&P/TSX Composite Index by more than 10% over the next 12 months. For other non-U.S. securities we expect the stock to outperform the MSCI World Index by more than 10% over the next 12 months. For yield-sensitive securities, we expect a total return in excess of 12% over the next 12 months for U.S. securities as compared to the S&P 500, for Canadian securities as compared to the S&P/TSX Composite Index, and for other non-U.S. securities as compared to the MSCI World Index. HOLD -For U.S. securities we expect the stock to perform within 10% (plus or minus) of the S&P 500 over the next 12 months. For Canadian securities we expect the stock to perform within 10% (plus or minus) of the S&P/TSX Composite Index. For other non-U.S. securities we expect the stock to perform within 10% (plus or minus) of the MSCI World Index. A Hold rating is also used for yield-sensitive securities where we are comfortable with the safety of the dividend, but believe that upside in the share price is limited. SELL -For U.S. securities we expect the stock to underperform the S&P 500 by more than 10% over the next 12 months and believe the stock could decline in value. For Canadian securities we expect the stock to underperform the S&P/TSX Composite Index by more than 10% over the next 12 months and believe the stock could decline in value. For other non-U.S. securities we expect the stock to underperform the MSCI World Index by more than 10% over the next 12 months and believe the stock could decline in value.

Of the securities we rate, 51% are rated Buy, 47% are rated Hold, and 2% are rated Sell. Within the last 12 months, Stifel, Nicolaus & Company, Inc. or an affiliate has provided investment banking ser-vices for 17%, 10% and 0% of the companies whose shares are rated Buy, Hold and Sell, respectively.

A Parcel Shipping Experiment March 2, 2012 - 16 - Stifel, Nicolaus & Company, Inc.

Additional Disclosures FedEx Corporation is on the Stifel Analyst Select List. This Select List includes companies that Stifel Nicolaus analysts believe have the potential for the greatest total return in each of their respective areas of coverage over approximately the next 12 months. In some cases, analysts who cover more than one sub-sector may have more than one name on the list. United Parcel Service, Inc. is on the Stifel Nicolaus Income Opportunity Ideas List. This Income Opportunity Ideas List represents our Stifel Nicolaus analysts’ best yield ideas, however is not intended to represent a model portfo-lio. Each stock is on the Buy List, and offers what Stifel Nicolaus analysts believe are companies with solid funda-mentals, a favorable valuation, and a current dividend higher than that of the S&P 500 Index. Please visit the Research Page at www.stifel.com for the current research disclosures applicable to the companies mentioned in this publication that are within Stifel Nicolaus' coverage universe. For a discussion of risks to target price please see our stand-alone company reports and notes for all Buy-rated stocks. The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation or needs of individual investors. Employees of Stifel, Nico-laus & Company, Inc. or its affiliates may, at times, release written or oral commentary, technical analysis or trad-ing strategies that differ from the opinions expressed within. Past performance should not and cannot be viewed as an indicator of future performance. Stifel, Nicolaus & Company, Inc. is a multi-disciplined financial services firm that regularly seeks investment banking assignments and compensation from issuers for services including, but not limited to, acting as an under-writer in an offering or financial advisor in a merger or acquisition, or serving as a placement agent in private transactions. Moreover, Stifel Nicolaus and its affiliates and their respective shareholders, directors, officers and/or employees, may from time to time have long or short positions in such securities or in options or other derivative instruments based thereon. These materials have been approved by Stifel Nicolaus Europe Limited, authorized and regulated by the Financial Services Authority (UK), in connection with its distribution to professional clients and eligible counterparties in the European Economic Area. (Stifel Nicolaus Europe Limited home office: London +44 20 7557 6030.) No in-vestments or services mentioned are available in the European Economic Area to retail clients or to anyone in Can-ada other than a Designated Institution. This investment research report is classified as objective for the purposes of the FSA rules. Please contact a Stifel Nicolaus entity in your jurisdiction if you require additional information. The use of information or data in this research report provided by or derived from Standard & Poor’s Financial Services, LLC is © 2012, Standard & Poor’s Financial Services, LLC (“S&P”). Reproduction of Compustat data and/or information in any form is prohibited except with the prior written permission of S&P. Because of the pos-sibility of human or mechanical error by S&P’s sources, S&P or others, S&P does not guarantee the accuracy, ade-quacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. S&P GIVES NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. In no event shall S&P be liable for any indirect, special or consequential damages in connection with subscriber’s or others’ use of Compustat data and/or information. For recipient’s in-ternal use only.

Additional Information Is Available Upon Request

© 2012 Stifel, Nicolaus & Company, Inc. One South Street Baltimore, MD 21202. All rights reserved.

Related Documents