The Best Emotions, Digitally Annual Report 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Annu

al R

epor

t 201

1

DRFA

N11

The Best Emotions, Digitally

Annual Report

2011

Registered Office42 avenue de Friedland / 75380 Paris Cedex 08 / FranceTel.: +33 (0) 1 71 71 10 00Fax: +33 (0) 1 71 71 10 01 New York Office800 Third Avenue/New York, NY 10022/USATel.: 1 212 572 7000

www.vivendi.com

The Annual Report in English is a translation of the French “Document de référence” provided for information purposes. This translation is qualified in its entirety by reference to the “Document de référence”.

Annual Report

2011

CO

NTE

NTS

Key figures – Simplified economic organization chart 04

Information about the Company – Corporate Governance 68

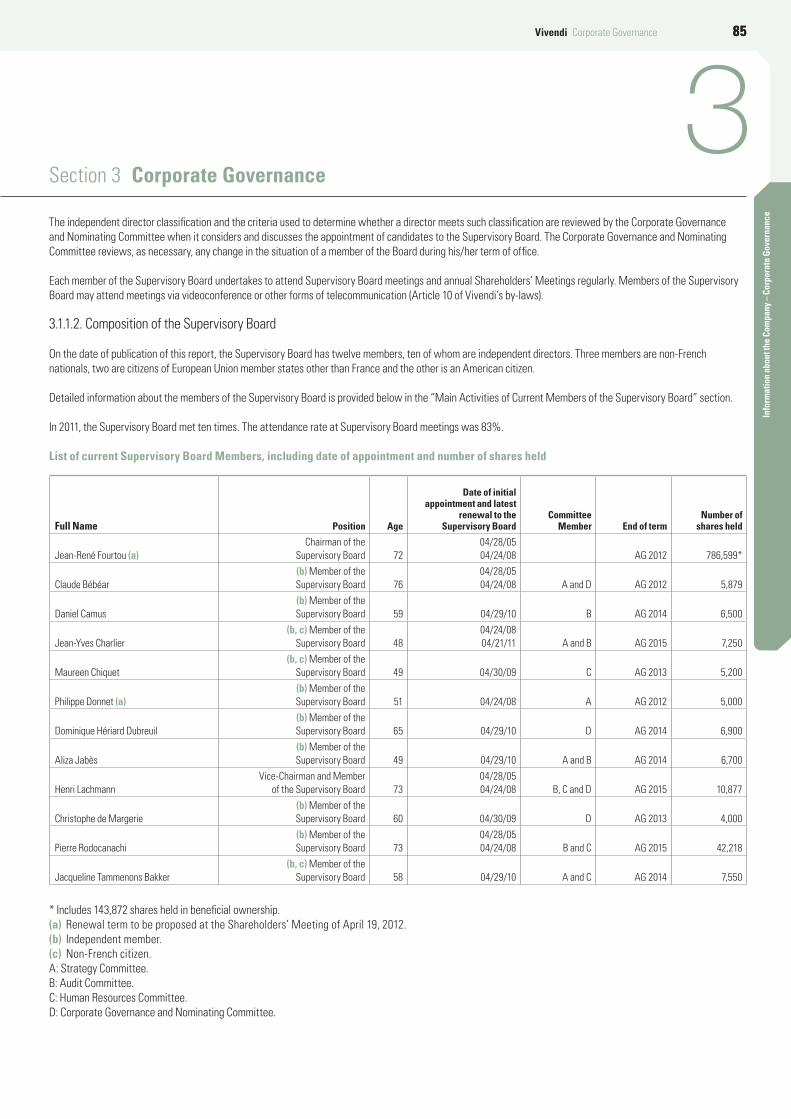

1. General Information about the Company 702. Additional Information about the Company 703. Corporate Governance 844. Report by the Chairman of the Vivendi Supervisory Board

on Corporate Governance, Internal Audits and Risk Management – Fiscal Year Ended December 31, 2011 118

5. Statutory Auditors’ Report, prepared in accordance with Article L.225-235 of the French Commercial Code, on the Report Prepared by the Chairman of the Supervisory Board of Vivendi S.A. 127

2

3

1Description of the Group and its Businesses – Litigation – Risk Factors 12

1. Description of the Group 141.1. Strategy 141.2. Highlights 161.3. FinancialCommunicationPolicyandValueCreation 191.4. SustainableDevelopmentPolicy 211.5. HumanResources 251.6. Insurance 291.7. Investments 292. Description of the Group’s Businesses 302.1. ActivisionBlizzard 302.2. UniversalMusicGroup 332.3. SFR 352.4. MarocTelecom 412.5. GVT 472.6. Canal+Group 512.7. OtherOperations 583. Litigation 604. Risk Factors 65

Financial Report – Consolidated Financial Statements – Statutory Auditors’ report on the Consolidated Financial Statements – Statutory Financial Statements 128

Selected key consolidated financial data 130I. 2011 Financial Report 131 Summaryofthe2011,2010and2009majorevents 1321. Majorevents 1332. Earningsanalysis 1363. Cashflowfromoperationsanalysis 1404. Businesssegmentperformanceanalysis 1425. Treasuryandcapitalresources 1576. Outlook 1627. Forwardlookingstatements 1638. Otherdisclaimers 163

II. Appendices to the Financial Report: Unaudited supplementary financial data 164

III. Consolidated Financial Statements for the year ended December 31, 2011 169

StatutoryAuditors’reportontheConsolidatedFinancialStatements 169

ConsolidatedStatementofEarnings 170 ConsolidatedStatementofComprehensiveIncome 171 ConsolidatedStatementofFinancialPosition 172 ConsolidatedStatementofCashFlows 173 ConsolidatedStatementsofChangesinEquity 174 NotestotheConsolidatedFinancialStatements 176

IV. Vivendi SA 2011 Statutory Financial Statements 2651. StatutoryAuditor’sReportonthe

FinancialStatements 2662. StatutoryFinancialStatements 2683. Notestothe2011StatutoryFinancialStatements 2724. SubsidiariesandAffiliates 295 MaturityofTradeAccountspayable 296 FinancialResultsoftheLastFiveYears 297 StatutoryAuditor’sReportonrelatedparty

AgreementsandCommitments 298

Recent Events – Outlook – Statutory Auditor’s Report 300

Recent events 302Outlook 302Statutory Auditors’ report on the ANI forecast before the impact of the transactions announced in the second half of 2011 303

Independent Auditors Responsible for Auditing the Financial Statements 304

Statutory Auditors 306Alternate Statutory Auditors 306

4 5

6

1Key Figures 2011

Revenues by Business Segment 6Revenues by Geographical Zone 6EBITA by Business Segment 7Earnings Attributable to Vivendi SA Shareowners and Adjusted Net Income 7Adjusted Net Income per Share and Dividend per Share 8Financial Net Debt and Equity 8Headcount by Business Segment 9Headcount by Geographical Zone 9Simplified Economic Organization Chart 10

kEy figurES – SimplifiEd ECONOmiC OrgaNizaTiON CharT

05000 10000 15000 20000 25000 30000

2009

2010

2011

5,0000 10,000 15,000 20,000 25,000 30,000

2011 2010 2009

6 Vivendi 2011 Annual Report

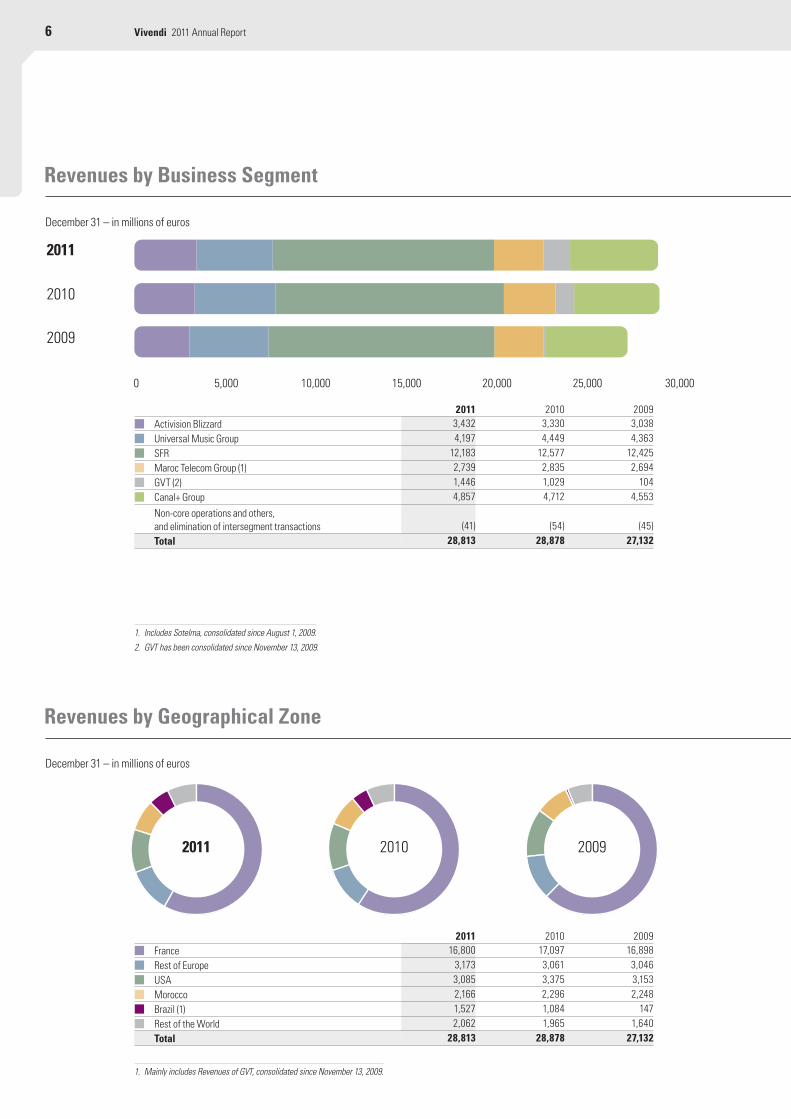

2011 2010 2009Activision Blizzard 3,432 3,330 3,038Universal Music Group 4,197 4,449 4,363SFR 12,183 12,577 12,425Maroc Telecom Group (1) 2,739 2,835 2,694GVT (2) 1,446 1,029 104Canal+ Group 4,857 4,712 4,553

Non-core operations and others, and elimination of intersegment transactions (41) (54) (45)Total 28,813 28,878 27,132

1. Includes Sotelma, consolidated since August 1, 2009.

2. GVT has been consolidated since November 13, 2009.

Revenues by Geographical Zone

Revenues by Business Segment

December 31 – in millions of euros

December 31 – in millions of euros

2011 2010 2009France 16,800 17,097 16,898Rest of Europe 3,173 3,061 3,046USA 3,085 3,375 3,153Morocco 2,166 2,296 2,248Brazil (1) 1,527 1,084 147Rest of the World 2,062 1,965 1,640Total 28,813 28,878 27,132

1. Mainly includes Revenues of GVT, consolidated since November 13, 2009.

0 1000 2000 3000 4000 5000 6000

2009

1,0000 2,000 3,000 4,000 5,000 6,000

2010

2011

0 1,000 2,000 3,000

2009

2010

2011

7

Key F

igur

es –

Sim

plifi

ed E

cono

mic

Org

aniz

atio

n Ch

art

Vivendi Key Figures

1

Earnings Attributable to Vivendi SA Shareowners and Adjusted Net Income

EBITA by Business Segment

December 31 – in millions of euros

December 31 – in millions of euros

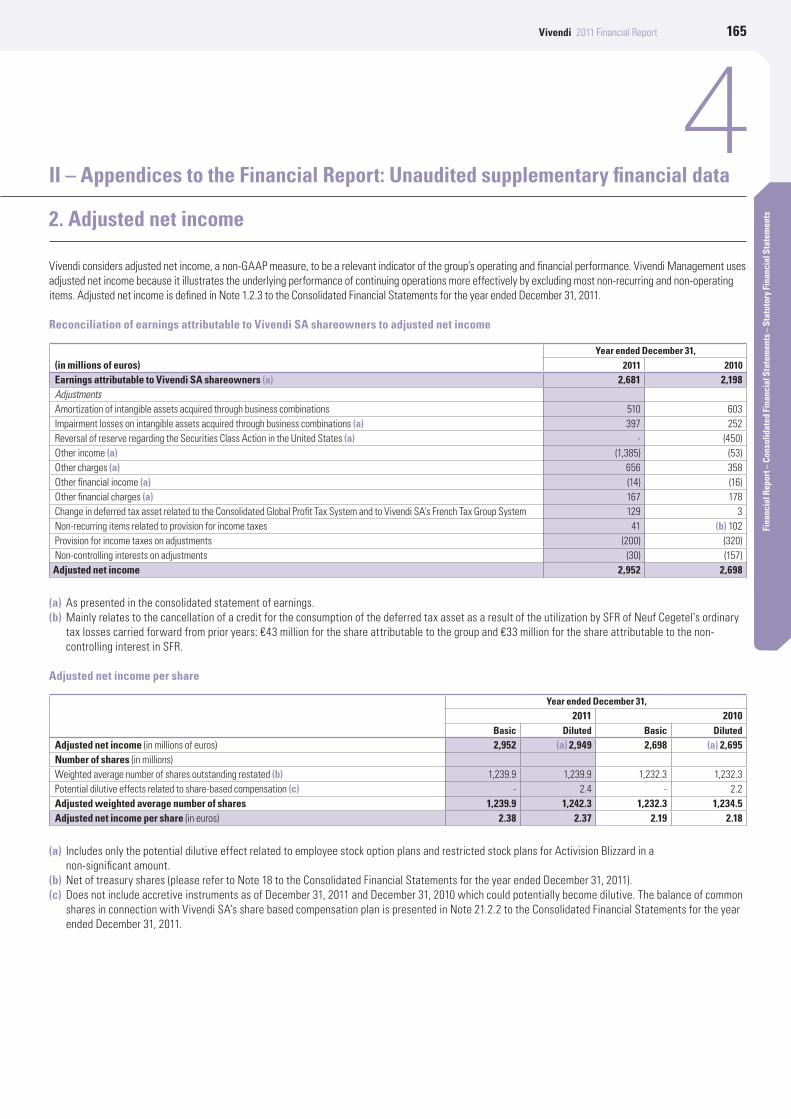

2011 2010 2009Earnings attributable to Vivendi SA Shareowners 2,681 2,198 830Adjusted Net Income 2,952 2,698 2,585

Vivendi considers Adjusted Net Income, a non-GAAP measure, to be a relevant measure to assess the Group’s operating and financial performance. Vivendi Management uses Adjusted Net Income because it better illustrates the underlying performance of continuing operations by excluding most non-recurring and non-operating items.

2011 2010 2009Activision Blizzard 1,011 692 484Universal Music Group 507 471 580SFR 2,278 2,472 2,530Maroc Telecom Group (1) 1,089 1,284 1,244GVT (2) 396 277 20Canal+ Group 701 690 652Holding & Corporate (100) (127) (91)Non-core operations and others (22) (33) (29)Total 5,860 5,726 5,390

Vivendi considers EBITA, a non-GAAP measure, to be a relevant measure to assess its operating segments performance as reported in the segment data. The method used in calculating EBITA excludes the accounting impact of the amortization of intangible assets acquired through business combinations, impairment losses on goodwill and other intangibles acquired through business combinations, and other financial income and charges related to financial investing transactions and to transactions with shareowners. This enables Vivendi to measure and compare the operating performance of operating segments regardless of whether their performance is driven by the operating segment’s organic growth or acquisitions.

1. Includes Sotelma, consolidated since August 1, 2009.

2. GVT has been consolidated since November 13, 2009.

0 5,000 10,000 15,000 20,000 25,000 30,000

2009

2010

2011

0 0.50 1.00 1.50 2.00 2.50

2009

2010

2011

8 Vivendi 2011 Annual Report

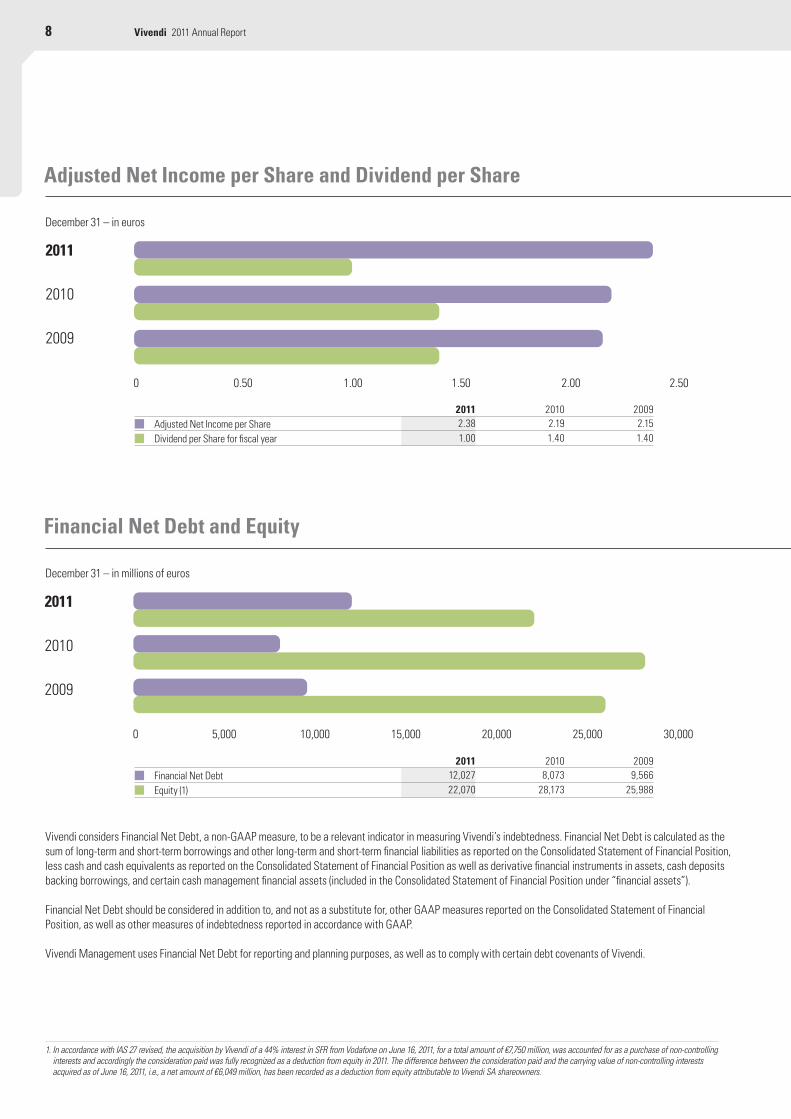

December 31 – in euros

Financial Net Debt and Equity

Adjusted Net Income per Share and Dividend per Share

December 31 – in millions of euros

Vivendi considers Financial Net Debt, a non-GAAP measure, to be a relevant indicator in measuring Vivendi’s indebtedness. Financial Net Debt is calculated as the sum of long-term and short-term borrowings and other long-term and short-term financial liabilities as reported on the Consolidated Statement of Financial Position, less cash and cash equivalents as reported on the Consolidated Statement of Financial Position as well as derivative financial instruments in assets, cash deposits backing borrowings, and certain cash management financial assets (included in the Consolidated Statement of Financial Position under “financial assets”).

Financial Net Debt should be considered in addition to, and not as a substitute for, other GAAP measures reported on the Consolidated Statement of Financial Position, as well as other measures of indebtedness reported in accordance with GAAP.

Vivendi Management uses Financial Net Debt for reporting and planning purposes, as well as to comply with certain debt covenants of Vivendi.

2011 2010 2009Adjusted Net Income per Share 2.38 2.19 2.15Dividend per Share for fiscal year 1.00 1.40 1.40

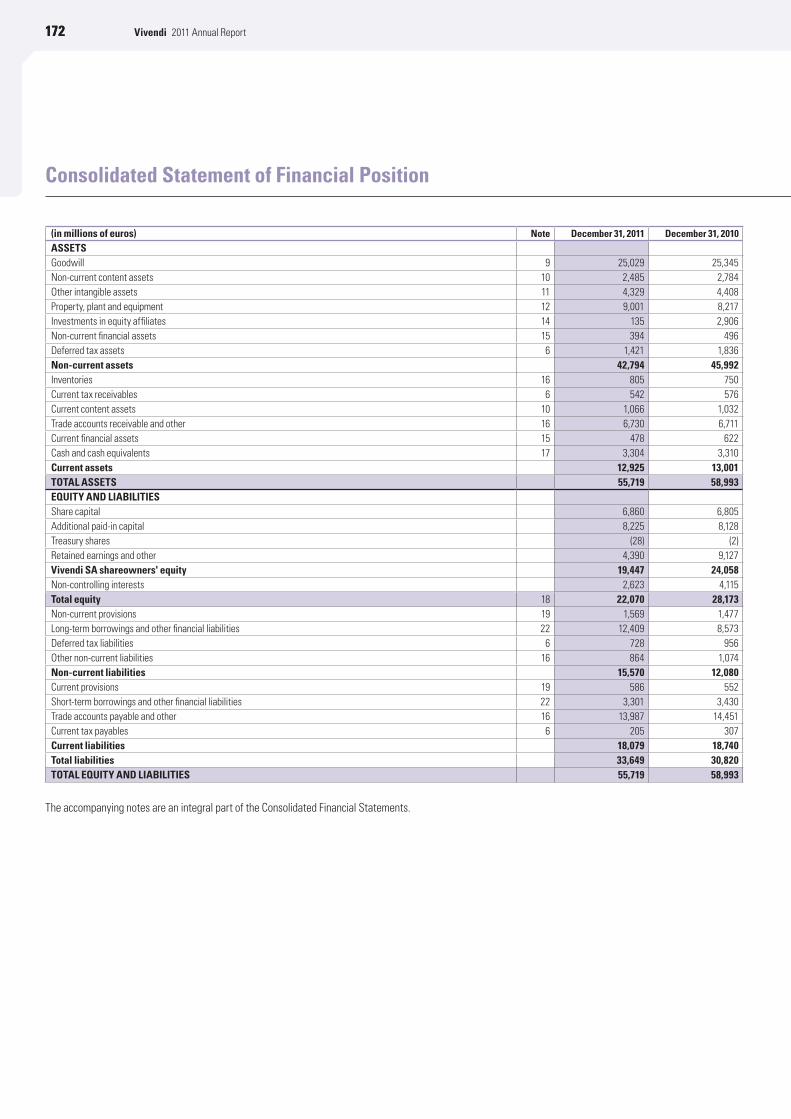

2011 2010 2009Financial Net Debt 12,027 8,073 9,566Equity (1) 22,070 28,173 25,988

1. In accordance with IAS 27 revised, the acquisition by Vivendi of a 44% interest in SFR from Vodafone on June 16, 2011, for a total amount of €7,750 million, was accounted for as a purchase of non-controlling interests and accordingly the consideration paid was fully recognized as a deduction from equity in 2011. The difference between the consideration paid and the carrying value of non-controlling interests acquired as of June 16, 2011, i.e., a net amount of €6,049 million, has been recorded as a deduction from equity attributable to Vivendi SA shareowners.

2011 2010 2009

0 5,500 11,000 16,500 22,000 27,500 33,000 38,500 44,000 49,500 55,000 60,500

2009

2010

2011

9

Key F

igur

es –

Sim

plifi

ed E

cono

mic

Org

aniz

atio

n Ch

art

Vivendi Key Figures

1

Headcount by Geographical Zone

Headcount by Business Segment

December 31

December 31

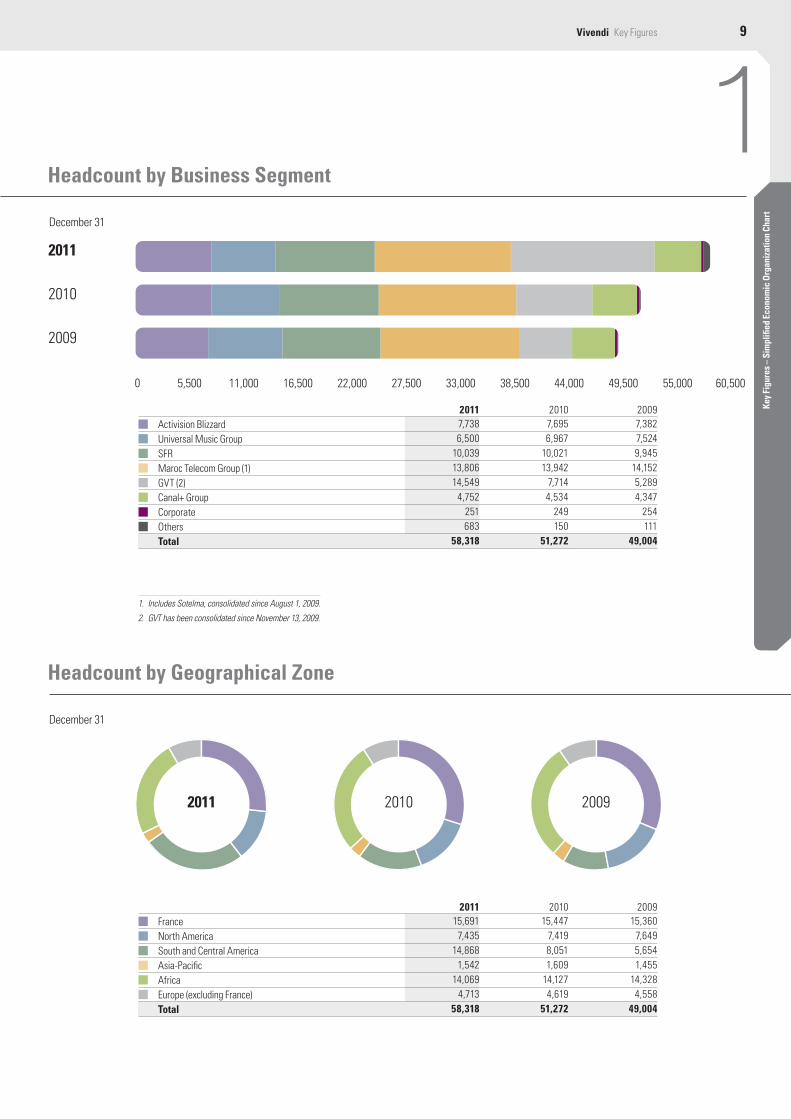

2011 2010 2009Activision Blizzard 7,738 7,695 7,382Universal Music Group 6,500 6,967 7,524SFR 10,039 10,021 9,945Maroc Telecom Group (1) 13,806 13,942 14,152GVT (2) 14,549 7,714 5,289Canal+ Group 4,752 4,534 4,347Corporate 251 249 254Others 683 150 111Total 58,318 51,272 49,004

1. Includes Sotelma, consolidated since August 1, 2009.

2. GVT has been consolidated since November 13, 2009.

2011 2010 2009France 15,691 15,447 15,360North America 7,435 7,419 7,649South and Central America 14,868 8,051 5,654Asia-Pacific 1,542 1,609 1,455Africa 14,069 14,127 14,328Europe (excluding France) 4,713 4,619 4,558Total 58,318 51,272 49,004

10 Vivendi 2011 Annual Report

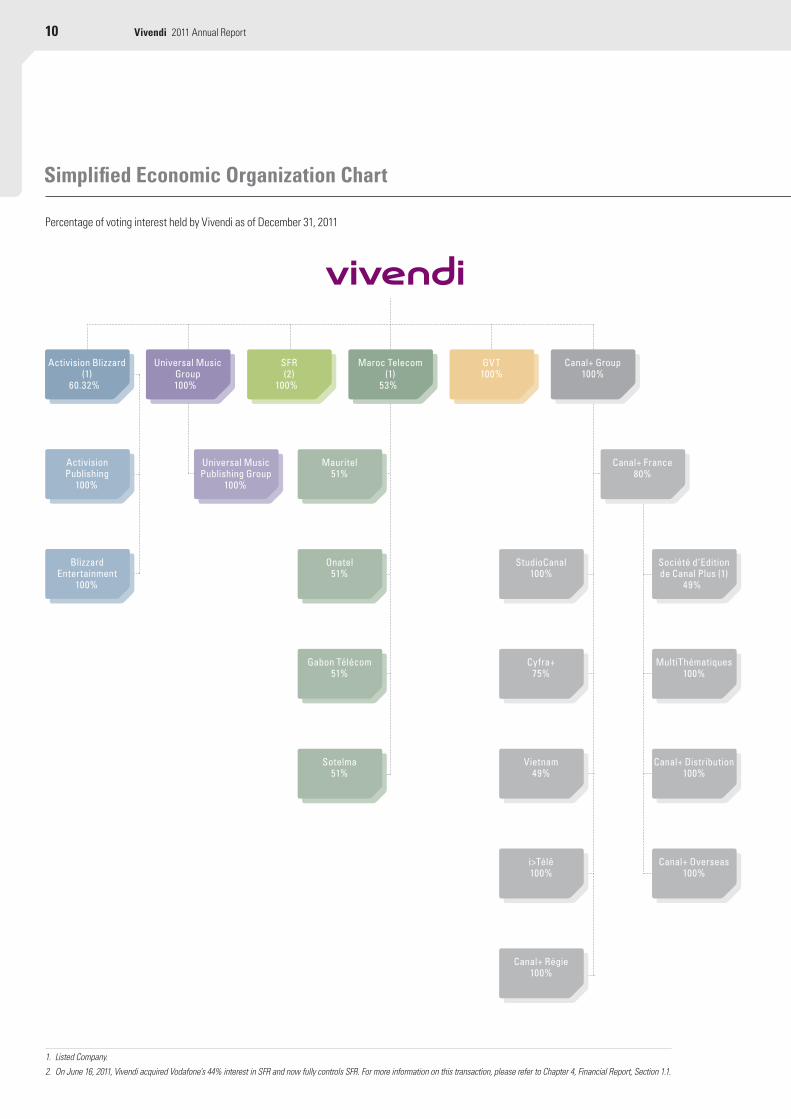

Simplified Economic Organization Chart

1. Listed Company.

2. On June 16, 2011, Vivendi acquired Vodafone’s 44% interest in SFR and now fully controls SFR. For more information on this transaction, please refer to Chapter 4, Financial Report, Section 1.1.

ActivisionBlizzard(1)

60.32%

GVT100%

UniversalMusicPublishingGroup

100%

SFR(2)

100%

Mauritel51%

GabonTélécom51%

BlizzardEntertainment

100%

Sotelma51%

Canal+France80%

MarocTelecom(1)

53%

Canal+Group100%

Sociétéd’EditiondeCanalPlus(1)

49%

StudioCanal100%

MultiThématiques100%

Cyfra+75%

Vietnam49%

Canal+Distribution100%

i>Télé100%

Canal+Overseas100%

Canal+Régie100%

UniversalMusicGroup100%

Onatel51%

ActivisionPublishing

100%

Percentage of voting interest held by Vivendi as of December 31, 2011

11

Key F

igur

es –

Sim

plifi

ed E

cono

mic

Org

aniz

atio

n Ch

art

Section 2Description of the Group’s Businesses 302.1. Activision Blizzard 302.1.1. ActivisionPublishingProductHighlights 302.1.2. BlizzardEntertainmentProductHighlights 312.1.3. Seasonality 322.1.4. RegulatoryEnvironment 322.1.5. Piracy 322.1.6. Competition 322.1.7. RawMaterials 322.1.8. ResearchandDevelopment 332.2. Universal Music Group 332.2.1. RecordedMusic 332.2.2.MusicPublishing 342.2.3.Merchandising 342.2.4.Seasonality 342.2.5.RegulatoryEnvironment 342.2.6.Piracy 352.2.7.Competition 352.2.8.RawMaterials 352.2.9.ResearchandDevelopment 35

2.3. SFR 352.3.1. PerformanceandServices 362.3.2.Network 372.3.3.Seasonality 382.3.4.Responsibility,Commitment 382.3.5.RegulatoryEnvironment 392.3.6.Piracy 412.3.7.Competition 412.3.8.RawMaterials 412.3.9.ResearchandDevelopment 412.4. Maroc Telecom Group 412.4.1. Morocco 422.4.2.International 432.4.3.Seasonality 452.4.4. RegulatoryenvironmentinMorocco 452.4.5. CompetitioninMorocco 462.4.6. RawMaterials 462.4.7. ResearchandDevelopment 472.5. GVT 472.5.1. Productsandservices 472.5.2. Retail/SmallandMediumEnterprise(SME)Segment 482.5.3. CorporateSegment 482.5.4.Network 482.5.5.Seasonality 492.5.6.RegulatoryEnvironment 492.5.7.Competition 502.5.8.RawMaterials 512.5.9.ResearchandDevelopment 512.6. Canal+ Group 512.6.1. PayTVinFrance 512.6.2.InternationalPayTV 532.6.3.OtherBusinesses 542.6.4.Seasonality 552.6.5.RegulatoryEnvironment 552.6.6.Piracy 572.6.7.Competition 572.6.8.RawMaterials 582.6.9.ResearchandDevelopment 582.7. Other Operations 582.7.1. VivendiMobileEntertainment 582.7.2.Digitick 582.7.3.Wengo 592.7.4.SeeTickets 59

Section 1Description of the Group 141.1. Strategy 141.2. Highlights 161.2.1. 2011Highlights 161.2.2. 2012Highlights 181.3. Financial Communication Policy

and Value Creation 191.3.1. InvestmentPolicy 191.3.2. FinancialCommunicationPolicy 191.3.3. ValueCreationin2011 201.4. Sustainable Development Policy 211.4.1. MainSustainableDevelopmentIssues 211.4.2.Vivendi’sStrategicIssues 221.4.3.ImplementationofSustainableDevelopmentPolicy 221.4.4.TheCreate JoySolidarityProgram 241.5. Human Resources 251.5.1. EmployeeShareOwnershipandEmployeeSavingPlans 251.5.2.SocialdialogueandHRdevelopment 261.5.3.ContributiontoEmploymentDevelopment 261.5.4.EqualityofOpportunityinEducationalPrograms 271.6. Insurance 291.7. Investments 29

2DESCRIPTION OF THE GROUP AND ITS BUSINESSES – LITIGATION – RISK FACTORS

Section 4

Risk Factors 65Legal risks 65Risks Associated with the Group’s Operations 65Industrial Risks or Risks Associated with the Environment 67Risks Associated with the Current Economic and Financial Situation 67Market risks 67

Section 3

Litigation 60

Section1 Description of the Group

14 Vivendi 2011AnnualReport

Vivendicreates,publishesanddistributesdigitalproductsandservices.TheGroupreliesonthestrengthofitsinventorsanddesigners,itsengineersanditsbrandsto offertoitscustomersdigitalcontent,platformsanddistributionnetworksofthehighestquality.Itcontrolstheentirevaluechain,fromproductiontopublishingand distributionofcontent(videogames,musicandaudiovisualworks).

Aleaderincommunicationandentertainment,Vivendibringstogethertheworld’sleaderinvideogames(ActivisionBlizzard),theworld’sleaderinmusic(Universal MusicGroup),France’sleaderinalternativetelecommunications(SFR),Morocco’sleaderintelecoms(MarocTelecomGroup),Brazil’sleaderinalternativehigh-speedInternetoperations(GVT),andFrance’sleaderinpay-TV(Canal+Group).

• ActivisionBlizzard:theworld’snumberoneindependentpublisherofonlineandconsolevideogames.• UniversalMusicGroup:theworld’sleaderinrecordedmusic,numberoneinmostmajorcountries,andthelargestcatalogofmusicalworks.• SFR:thenumberonemobileandfixed-linealternativetelecommunicationsoperatorinEuropeandFrance’salternativetelecomleader.• MarocTelecomGroup:thenumberonemobileandfixed-linetelecommunicationsoperatorinMorocco,whichalsohasafootholdinBurkinaFaso,Gabon,

MauritaniaandMali.• GVT:Brazil’salternativetelecomleader,thebestperforminghigh-speedoperatorinBrazilofferingfixed-linetelephony,Internet,andpay-TVservices

and products.• Canal+Group:France’sleadingpublisherofpremiumandthemechannels,France’sleaderintheaggregationanddistributionofpay-TVoffersand

Europe’s largestproduceranddistributoroffilms.

In2011,Vivendistrengthenedseveralofitsbusinesslines.ThecompanybecamethesoleshareholderinSFRbypurchasingVodafone’s44%interestinwhatconstitutestheGroup’slargestcashflowcontributor.

Inmusic,VivendienteredintoanagreementtoacquireEMIRecordedMusic,whosecatalogofartistsincludesPinkFloyd,theBeatles,MariaCallasandMilesDavis.Thistransactionwasmadeattheparticularlyfavorablepriceofapproximately€1.4 billion(fivetimesEBITDAaftersynergies)atatimewhendigitalsalesareprevailingandthemusicmarketisshowingsignsofrecovery.

Intelevision,Canal+GroupfinalizedboththeprojectedmergerofitsTVplatforminPolandwithTVN’s“n”platformandtheprojectedacquisitionoftheDirect 8andDirectStarchannelsinFrance.Approvalispendingfromthecompetentregulatoryauthoritiesforbothtransactions,whichwillbesourcesofimportantsynergiesand valuecreation.

Inaddition,VivendiownszaOza(acontent-sharingwebsite,throughsubscription),Digitick(France’sleaderinelectronicticketing),SeeTickets(thenumbertwoticketingbusinessintheUK)andWengo(theFrenchleaderinexpertphonecounseling).

1.1. Strategy

Vivendi’sstrategyistofocusoncreatingvaluethroughorganicgrowththatisbasedoninnovation,strengtheningitspositionsinrapid-growthcountriesaswellasintra-Groupsynergies.

Innovation, a daily commitment Whenitcomestoinnovation,theGroupisfollowingaprocessthatinvolvesallitssubsidiariesandwhichincludesthesupplyofinformationongrowthvectorsanddiversificationtotheManagementBoardandSupervisoryBoardonaregularbasis.Thegoalistoidentifyandinvestinnewgrowthvectorstofacilitatetheemergenceofambitiousdevelopmentprojectsbeyondthenaturalscopeofeachofitsbusinesslines:• allGroupmanagershavebeenmadeawareofthechallengesfacinginternalgrowthanddiversification;• manysubsidiarieshaveconvertedthesearchforinternaldevelopmentprojectsintoclearguidelines;• ad hocgovernancecommitteeshavebeencreatedtosetprioritiesandapprovetheallocationofspecificresources.Thisincreasedthevisibilityofcertain

projectsandacceleratedtheirimplementation;• aGroupcommittee,involvingallGroupsubsidiaries,hasbeenestablishedtoopenupnewdevelopmentprospects.

Theseinitiativeshaveledtotheidentificationofsourcesofgrowthincontentandservices,interactivecontentdistributionplatforms,connectedhomeservicesand offerstobusinesses.

Thisentireapproachisbasedonactivemonitoring,whichmakesitpossibletoanticipateandrespondtocustomerexpectationsandtechnologicalchanges.

Vivendi’sbusinesslinesshareuseofthesamenewtechnologiesandfacethesamechangesinuseastheircustomers.Internetaccesshasbecomeomnipresent;youngergenerationsbornaftertheadventoftheInternetuseitroutinelyandintuitively,andconnectedobjectsaremultiplyinginnumber.Contentconsumptionmethodsareevolvingwithusagethatison-demand,interactiveandcontinuousonallscreens.TheInternetoftomorrowwillbemobileandsocial.Itwillaccompanysocietaltrendssuchastheagingofthepopulationandaccesstohealthandeducationforall.

Section1 Description of the Group

15Vivendi DescriptionoftheGroup

Des

crip

tion

of th

e G

roup

– L

itiga

tion

– Ri

sk F

acto

rs

2IdentificationofnewcustomerbehaviorisencouragedatalllevelsofthebusinessandisaccompaniedbybothdiscussionsbetweenGroupexpertsandagreaterproximitytoinnovativestartupecosystems:• workinggroupshavebeencreatedtofacilitatethetransferofknowledgeandsharingofbestpracticesinrelationtonetworks,platforms,computer

systems,purchasesandcustomerrelations;• aTechnologicalCommitteeledbyCanal+Groupbringstogetherinternalexpertsandthirdpartieswhotogetheranticipatenewtechnologiesanduses

in theareasoftelevisionandvideo;and• anopeninnovationprogramhasbeenbuiltaroundAtelier SFR(abetatestplatform),SFR Jeunes Talents Startup (asupportprogramforinnovativeyoung

businesses)andSFR Développement(aninvestmentfund).Theaimistorespondtotechnologicalchangesinaflexibleandrapidmanner.

Eachsubsidiaryoffersmanyinnovativeservices.SFRconstantlyenrichestheneufboxTVoffer:ithasdevelopedapplicationsthataredesignedtoguaranteecontinuityofuseovermultiplescreens;ithasintegratednewservicesintoitstelevisionportal,suchasDokeoTV,aninteractiveedutainmentapplication;andithascreatedanon-demandvideogameportalthatenablesplayerstoplaygamesdirectlyontheirtelevision.

Inparallel,SFRisactivelyengagedinexpandingitsoperationalscopetoactivitiesthatarerelatedtoitscorebusiness.Recently,itlaunchednewservicesandpartnershipssuchasBuyster,anonlinepaymentsolutionthatworkswiththreeoperatorsandSynapseCloud,amedicalimage-hostingservicessolution,whichwas developedwithFujifilm.

UniversalMusicGrouphascreatedtheVevovideoplatformforwatchingmusicvideos.Itiscurrentlythesecondlargestvideohostingsiteintheworld,withmorethan60 millionuniquevisitors,andisthenumber-oneplatformforwatchingmusicvideosintheUnitedStates.Itattractsmajorinternationaladvertisers.In2011,UniversalMusicalsolaunchedOFF.tv,thefirstWebTVchanneltobecompletelyintegratedwithamusiclabel.ByvirtueofapartnershipwithSFR,OFF.tvisaccessible toneufboxcustomersthroughaninteractiveapplicationthatmakesitpossibletoviewHDvideos.

AmongthenewservicesofferedtoyoungerusersbytheMarocTelecomGroup,theMTTalkofferprovidesaccesstosocialnetworksfrommobiledevices.The UniversalMusicpackage,designedinpartnershipwithUMG,hasprovedacommercialsuccess.TheMarocTelecomGrouphasalsodevelopedMenara,the first onlineinformationsitethatisavailableintheMoroccanandFrenchlanguages.

Canal+Groupoffersitscustomersanever-expandingrangeofinteractivecontentandservices.Inanticipationofmarketdevelopmentsrelatedtothearrivalofconnectedtelevisions,theGroupcreatedCanalPlayInfinity,anunlimitedvideoon-demandsubscriptionofferthatisaccessibleonallscreens.SFRheldapreviewlaunchoftheserviceinNovember2011.ThisisthefirstofferofitskindavailableinFrance.Canal+andCanalSatchannelsarealsoavailableontheMicrosoftXbox360.

ActivisionBlizzardinnovatedbybringingtogetherthevideogameandtoyindustriesinauniqueproduct,Skylanders Spyro’s Adventure.Througha“magicportal”,figurinescometolifeinavideogame.Itiseverychild’sdream!LaunchedinOctober2011,thegamewasagreatsuccess.TheGroupcontinuedthedevelopmentofits successfulfranchisesbycreatingtheEliteplatform,whichwasdesignedtoconnectover30 millionplayersofCall of Duty.OnJanuary31,2012,Elitealreadyhadoverseven millionregisteredusers.

InOctober2011,GVTlaunchedapay-TVservicebasedonaninnovativeset-topboxmodel.Thishybridset-topboxcombinessatellitetechnologyforthelineardistributionofchannelsandtelevisionoverIPnetworksforinteractiveservicessuchasvideoondemand,catch-upVoDandnetworkapplications.Attheendof February2012,theservicealreadyhad80,000subscribers.

Stronger position in rapid-growth countriesVivendi’sapproachtoactivelybuildingastrongerpositioninrapid-growthcountriesisbasedontwodifferentials:thedifferenceindemographicgrowthbetween“rapid-growth”and“mature”countries,whichbringsthousandsofyoungpeopletotheageofdigitalconsumption,andthedifferenceintermsofeconomicgrowth,whichprovidesagrowingnumberofpeoplein“rapid-growth”countrieswiththefinancialmeanstoaccessdigitalproductsandservices.

TheMarocTelecomGroupcontrolstelecomoperatorsinGabon,Mauritania,BurkinaFaso,andMaliatatimewhenmobiletelephonyuseisescalatingalloverAfrica,whichiscreatingnewdemandsandservices,suchasinthebankingsector.

Canal+GrouphasapresenceinallFrench-speakingcountriesinAfrica,theIndianOcean,andVietnam(whereitholds49%ofajointventurebetweenCanal+GroupandVTV,theVietnamesepublicbroadcastinggroup).

UMGhasaworldwidepresence.However,theworld’sleaderinrecordedmusicisnonethelesstryingtoincreaseitsfootholdandprospectsinRussia,China,India,Indonesia,Vietnam,theMiddleEastandNorthAfrica.ThegrowthoftheInternetandotherdigitalplatformsmakesitpossibleforUMGtoreachpopulationsthatwerepreviouslydifficulttoaccess.

ActivisionBlizzardhasastrongpresenceinAsia:nearlyhalfthesubscribedplayersofitsflagshipgame,World of Warcraft,comefromthiscontinent.Thisgame,with morethan10.2 millionsubscribers,isdistributedin10languages,andaversioninBrazilianPortuguesewasrecentlylaunched.ThevideogamepublisherintendstoadaptCall of DutyfortheAsianregionsinthenearfuture.

Section1 Description of the Group

16 Vivendi 2011AnnualReport

Sincetheendof2009,VivendihascontrolledtheoperatorGVTinBrazil.GVTwascreatedin2000andhasexperiencedconsiderablegrowthinthefixed-linetelephonyandhigh-speedInternetsectors.Itsrevenuesareexpectedtoincreasefourfoldbetween2009and2014.

VivendiplaysacentralroleinthegrowthofGVT:• itsfinancialassistanceissignificantlyacceleratingthedeploymentoftheBrazilianoperator’snetwork(whichwasdeployedto22newcitiesin2011)

and generatingsignificantrevenuegrowth(in2011,therewasover39%revenuegrowthinBrazilianreals);and• intra-GroupsupportandsynergiesallowGVTtolaunch(oracceleratethemarketingof)innovativenewproducts.Theoperatorismakingonlinegames

availabletoitscustomersonfavorabletermsinpartnershipwithActivisionBlizzard(World of Warcraft).DuetothesupportofGroupeCanal+andSFR,GVT launchedahybridpay-TVofferwithsatellitebroadcastingoftelevisionchannelsandIPnetworkdistributionofallinteractiveservices.InpartnershipwithUMG,itisalsoofferingGVTsubscribersunlimitedaccesstothousandsofsongsandmusicvideosbyGroupartists,aswellastolivebroadcastsof concerts.

Organic growth and intra-Group synergiesVivendiintendstostrengthenthepositionofitsvariousexistingbusinesslines,implementsynergiesbetweenitsgroupentitiesanddeveloprelatedactivitieswithhigh-potential.

Inthebroadcontextofdevelopingdigitaluseanddistributionmodels,theGroupisprovidingthestabilityandsupportnecessarytoimplementthesechangessuccessfullyinallofitsoperationalentities.TheVivendiGroup’sbusinessunitsallpertaintothedigitalandnewtechnologiessector.Theyaredirectlytargetedat the endconsumervialeadingbrandssuchasActivisionBlizzard,UniversalMusic,SFR,MarocTelecom,GVT,andCanal+.TheGroupofferscreativedigitalcontent,high-speedtelecommunicationsservicesandplatformsforexchangingoraccessingdigitalcontentandservices.ThesecommonalitiesgiveVivendiacompetitiveadvantage.Throughafruitfulexchangeofskillsandananticipationoftechnologicaldevelopments,itispossibletodevelopahighlevelofexpertisewithregardto subscriptions,brands,distributionandcreationplatforms,andcopyright.MembershipintheGroupallowsvariousbusinesslinestocometogethertorespondto concretechallengessuchastheimpactofsocialnetworks,thedevelopmentofcustomerrelationships,thechallengesofvery-high-speedInternetaccessandthe consequencesoftheincreasingpresenceofcloudcomputing.

Vivendi’sperformancereliesheavilyonitseconomicmodel,whichissubscription-based,bothfortelecommunicationsandfortelevision,musicworks,audiovisualplatformsandonlinegames.TheGrouphasthenecessaryskillsandexpertisetogrowitssubscriberbase,maintaincustomerloyaltyandoptimizetheincomethatit generates.Thesubscriptionmodelisasignificantadvantagebecauseitprovidesarecurringandthereforepredictablesourceofincome.

Inaddition,intra-Groupdiscussionsregardingtechnologicalexpertiseandoperationalprocessesinareassuchascustomerrelations,procurement,logisticsandinsurancerevenue,allowtheGrouptocapitalizeonitskeystrengths.

Throughthesharingoftechnologicalknowledge,theGroupoptimizestheperformanceofitsplatformsandnetworksaswellasthequalityofitsservices.For example,know-howexchangedbetweenGVT,SFRandGroupeCanal+recentlyacceleratedthelaunchofGVT’spay-TVservice.

Thecreationin2011ofapurchasegroupthatbringstogetheralloftheGroupsubsidiariesinordertofacilitatethesharingofbestpractices,jointpurchasingandthe coordinationofinitiativeswithkeysuppliersisanotherexampleofthestrongpowerofsynergies.

Atthesametime,theGroupisexpandingitsconnectedactivitiesingrowthmarkets.Recently,Vivendiinvestedintheticketingindustry,asectoratthejunctionbetweentheentertainmentanddigitalsectors.ItacquiredDigitickinFranceandSeeTicketsintheUKinordertobenefitfromthemovetowardsdigitalandpaperlessticketingforliveentertainment.TheseacquisitionsstrengthenVivendi’sexpertiseindevelopinginnovativesolutionsatthecuttingedgeofallofitsbusinesslines.

1.2. Highlights

1.2.1. 2011 Highlights

January• VivendisellstheremainderofitsinterestinNBCUniversal(12.34%)foratotalof$3.8 billion.• Vivendireceives€1.254 billionandendsthelitigationconcerningthesharecapitalownershipofthephoneoperatorPTCinPoland.• GVTcommencesoperationsinRiodeJaneiro,aswellasinseveralcitiesintheSãoPaulometropolitanregion.

February• IntheclassactionlawsuitintheUnitedStates,theUSDistrictCourtfortheSouthernDistrictofNewYorkrulesthat,inapplyingthe“Morrison”decision

oftheUSSupremeCourt,onlyshareholderswhopurchasedsecuritiesontheNewYorkStockExchangemayfileclaimswithaUScourttoseekdamages.• MarocTelecomlaunchesnewmobileterminalsintheAmazigh(Berber)language,offeringbothpre-paidandsubscriptionservices.• StudioCanalandLionsgatemoviestudiosannouncethesigningofanagreementforthedistributionof550filmsfromMiramax’sprestigiouscatalog.

Section1 Description of the Group

17Vivendi DescriptionoftheGroup

Des

crip

tion

of th

e G

roup

– L

itiga

tion

– Ri

sk F

acto

rs

2March• SFR,incollaborationwithGoogle™andSamsung,launchesthe“NexusS,”thelatestgenerationofAndroid™webphone.• StudioCanaliselectedasthe“Europeandistributoroftheyear”byCartoonMovie2011,theco-productionforumforEuropeananimatedfilms.• TheFrenchVictoires de la MusiquehonoranumberofUMGartists,includingGaëtanRoussel,Benl’OncleSoul,Stromae,BernardLavilliers,AbdAlMalik,

PhilippeKaterine,EddyMitchellandM.• GVTannouncesitsstrongestgrowthsinceitsfounding,with2010revenuesamountingto2.43 billionBrazilianreals,a43%increasecomparedto2009.

Its customerportfolioincreased50.3%comparedto2009,with4.23 millionlinesinservice.• MarocTelecomlaunchestheMTTalkservice,anewsharedapplicationallowingaccesstosocialnetworksfromamobiledevice,includingfrom

traditional handsets.

April• VivendiandVodafoneenterintoanagreementforVivendi’spurchaseofVodafone’s44%interestinSFR.• TheCanal+Group,TF1andFranceTélévisionsenterintoanagreementtoobtainbroadcastingrightsforthe2011RugbyWorldCup.• Vevo,UMG’smusicvideowebsite,islaunchedintheUK.

May• Vivendisetsupthreesyndicatedbankinglinesinatotalamountof€5 billion,increasingitsfinancialsecurityandextendingitsaveragedebtduration.• GVTiselectedasthemostreliablefixed-lineandbroadbandinternetproviderinBrazilbyInfoMagazine,thecountry’smaintechnologymagazine.• La Poste(51%)andSFR(49%)launchLa PosteMobile,ajointventurewiththegoalofgainingmorethan2.4 millioncustomers.• Canal+andtheFrenchNationalRugbyLeagueenterintoanewbroadcastagreementfortheTop14overthenextfiveseasons(2011-2012through

2015-2016).

June• FollowingtheauthorizationgrantedbytheEuropeanCommission,VivendiacquiresVodafone’s44%interestinSFRwithadealvalueof€7.75 billion.• LadyGaga’snewalbum,BornthisWay,exceedsglobalsalesoftwo millioncopiesinjustoveraweek.• MarocTelecomdoublesitsADSLspeedsforitscustomersatnoadditionalcharge(increasingspeedsfrom1to4Mbits)andoffersanoverallprice

reductionforallspeeds(from2to20Mbits/s).• SFRlaunchesthe“Carrées”formula,anewpricepolicythatrewardscustomerloyalty.• GVTlaunchesoperationsintwonewcitiesinthemetropolitanstateofSãoPaulo:SantoAndréandSãoBernardodoCampo.• SFRandFnacjoinforcestodistributetelephonyservicesthroughouttheFnacstorenetwork.• FollowingacallfortendersfromLigue1,theCanal+Groupsecuresitslong-termpartnershipwithFrenchfootballandstrengthensitsfootballoffering

until 2016.• SFRsignsanagreementwithVirginMobile(two millioncustomers),whichbecomesa“FullMVNO”ontheSFRnetwork.

July• Vivendiissues€1.75 billioninbonds.Aftertheacquisitionofa44%stakeinSFR,thistransactionisconsistentwithVivendi’spolicyofbalancingitsdebt

betweenbanklinesofcreditandbondissues.• Vono,GVT’ssupplierofInternettelephonysolutions,increasesthenumberofBraziliancitiesinwhichitofferslong-distancecommunicationsatlocal

callingpricesfrom250to468.• StudioCanalconsolidatesthenamesofitsvarioussubsidiariesunderthesingleStudioCanalbrandandthusemphasizesitsnumberonepositioninEurope.• UMGjoinsforceswithBaidu,China’sleadingChinese-languagesearchengine,todistributeitsdigitalmusiccatalogthroughthejointventureOne-StopChina.• MarocTelecomlaunchesapre-paid3GInternetofferingforJawalcards.

August• UniversalMusicGroupDistributionlaunchesdigster.fm,amusicalplaylistservicedistributedviaSpotify.• SFRofferstwonewprepaidreloadsforunlimitedvoiceandWi-Fiaccessservice.• VivendiacquiresSeeTicketsUK,aBritishticket-salescompanywhichisamajorplayerintheticketingmarket,forapurchasepriceofapproximately

€95 million.

September• SFRacquiresa15-MHzduplexfrequencyblockinthe4G(2.6GHz)frequencybandfor€150 millionforaperiodof20years.• MarocTelecomlaunchesVocalis,anewmobilesolutionspeciallyadaptedforthevisually-impairedpopulation.• SFRsignsa“FullMVNO”agreementwithNRJMobile,whichhasone millionactivecustomers.• UMGformajointventurewithLiveNation,theworldleaderintheorganizationofconcertsandonlineticketsales,todevelopthemanagementofartists

andtheirbrands.• StudioCanalsignsanexclusiveagreementwithAntonCapitalEntertainment,aEuropeaninvestmentfund,toco-financeapproximatelyonehundred

internationalfilmsdistributedbythestudiooverathree-yearperiod,foratotalof€500 million.

Section1 Description of the Group

18 Vivendi 2011AnnualReport

October• ActivisionBlizzardlaunchesSkylanders: Spyro’s Adventure,aninnovativegamecombiningphysicalactionfigureswithvideogames.• SFRlaunchestheRedseries,no-commitmentofferingssoldexclusivelyonline.• SFRintegratesTVondemandandVoDbysubscriptionintoitsSFRTVandNeufboxTVmobileapps.• GVTlaunchesitspayTVserviceinBraziliancitieswherethecompanyisactive.• VivendiwinstheResponsibleInvestmentForum(FIR)–VigeoprizeinthecategoryforCAC40indexcompanies.• MarocTelecomislistedonthenewlylaunchedNYSEEuronextstockindex,theCACInternational25.

November• VivendiandUMGenterintoafinalagreementwithCitigroupregardingthepurchaseofEMI’srecordedmusicdivisionforatotalof£1.2 billion.• Canal+andOrangeannounceastrategicpublishing,commercialandtechnologypartnershiprelatingtotheOrangeCinémaSérieschannelpackage,

with a viewtotheCanal+Group’sacquisitionofa33.33%minorityinterestintheequitycapitalofOrangeCinémaSéries.• ActivisionBlizzardreleases Call of Duty®: Modern Warfare® 3.Salesofthegameexceed$775 millioninglobalboxreceiptswithinfivedaysofitsrelease.• TheCanal+GroupoffersCanalPlayInfinity,anew,subscription-based,unlimitedvideo-on-demandservicefor€9.99permonth,launchedinpreviewwithSFR.• ActivisionBlizzardlaunches Call of Duty® Elite,asocialplatformdesignedtofacilitatebetterandeasiergamingbetweenplayers.Itgainsone million

premiummembersinthefirstsixdaysafteritslaunch.• SFRandFranceTélécom–Orangeannounceanagreementtorolloutfiberopticbroadbandinovereleven millionFrenchhouseholdsoutsideofvery

denselypopulatedregions.• MarocTelecomreleasesJawalThaniya,anewprepaidmobileofferwhichisbilledbythesecond.• Vivendiissues35 millionsharesofActivisionBlizzard,thusreducingitsstakeinActivisionBlizzardtoapproximately60%.• Vivendiissues€1 billioninbondsinordertolengthenitsdebtmaturities.

December• TheBolloréandCanal+groupsannouncethesigningofafinalagreementfortheacquisitionbytheCanal+GroupoftheBolloréGroup’sfreechannels,

Direct8andDirectStar.ThisagreementissubjecttoapprovalbythecompetentantitrustauthoritiesandbyFrance’sSuperiorAudiovisualCouncil(Conseil supérieur de l’audiovisuel ).

• VivendiisannouncedasafoundingmemberoftheCEOcoalition,aninitiativelaunchedbytheEuropeanCommissionseekingtomaketheInterneta place ofexpressionthatensuresthesafetyofchildren.

• Canal+winstherightstobroadcastthefirstchoiceoftheChampionsLeague.• SFRandUMGlaunchOFF.tv,ahigh-definitioninteractivemusicprogramapplication.• Call of Duty®: Modern Warfare® 3exceeds$1 billioninrevenueinthefirst16daysofsales.• Canal+openstheCanal+storeinVélizy,thefirststorecompletelydedicatedtotheCanal+universeandservices.• TheCanal+,ITIandTVNgroupsfinalizeastrategicpartnershiptoconsolidatetheirpay-channelplatformsinPolandandforCanal+totakeamajorstake

in TVN’sequitycapital.Thistransactionistobesubmittedtothecompetentregulatoryauthoritiesforapproval.• Vivendisignsanewbankcreditfacilityfor€1.1 billionwhichearlyrefinancesanexistingfacility.• SFRacquiresa10-MHzduplexfrequencyblockinthe4G(800MHz)frequencybandfor€1.065 billionforaperiodof20years.• StudioCanalbecomesamajorityshareholderofTandemCommunications,theEuropeanleaderintheproductionandsaleoftelevisionseries.

1.2.2. 2012 Highlights

January• Vivendiissues€1.25 billioninbonds.• zePass(asubsidiaryofDigitick,whichisitselfasubsidiaryofVivendi),thelargestsecond-handeventticketingbrokerinFrance,launchespermanent

second-handeventticketingfortheParisNationalOpera.• SFR’sgame-on-demandserviceismadeaccessibleaspartoftheEvolutionneufboxoffering(ADSLandfiber).• VivendiisrankedseventhintheGlobal100listofcompanies,emphasizingitssignificantcommitmenttosustainabledevelopment.

February• Asaresultofitsapplicationofthe“Morrison”decisioninrelationtotheclass-actionlawsuitintheUnitedStates,theManhattanSouthernDistrict

of the USFederalCourtdismissestheclaimsofindividualshareholderswhohadpurchasedcompany’ssharesontheParisstockmarket.• MarocTelecomreceivesVigeo’s“TopPerformerCSR2011”Trophyforitsworkinthepreventionofcorruptionanditscorporateresponsibility.• AsaconsequenceofafourthmobilephoneoperatorenteringtheFrenchmarket,SFRadaptsits“Redseries”and“Carrées”formulainresponseto

the new mobilephonemarketsituation.

Section1 Description of the Group

19Vivendi DescriptionoftheGroup

Des

crip

tion

of th

e G

roup

– L

itiga

tion

– Ri

sk F

acto

rs

21.3. Financial Communication Policy and Value Creation

1.3.1. Investment Policy

Creatingshareholdervalueisbasedonincreasedprofitabilityfromoperations,achievedthroughavigorousinnovationandinvestmentpolicy.

Investmentprojectsareselectedbasedonamulti-criteriaanalysisinvolving:• growth,withanimpactonbothincreasedadjustednetincomepershareaswellastheabilitytogeneratecash;• thereturnoncapitalemployedcomparedtotheweightedaveragecostofcapital,adjustedfortheimpactoftheacquisitionrisks,asassessed

in the mediumandlongterms;and• in-depthriskassessment.

TheyarereviewedbyVivendi’sInvestmentCommittee,andthereafterbytheManagementBoard,whilethemostsignificantinvestmentsarereviewedbytheSupervisoryBoard’sStrategyCommitteeandthereafterbytheSupervisoryBoarditself.Formajortransactions,apost-acquisitionauditisperformedapproximatelyoneyearaftertheacquisition.Thisanalysisre-examinestheconditionsofvaluecreationbycomparingactualoperationalandfinancialresultswiththeassumptionsmadeduringtheinvestmentdecisionprocess.ItthendrawsconclusionsfromthiscomparisontopromotebestpracticeswithintheGroupinthefuture.

1.3.2. Financial Communication Policy

ThepurposeofthefinancialcommunicationpolicyistoprovideallshareholderswithpreciseandaccurateinformationontheGroup’sstrategy,position,resultsand financialdevelopment.ItfollowsproceduresadoptedpursuanttoapplicableFrenchstandards,includingtheFrenchFinancialSecurityActof2003,aswellas InternationalFinancialReportingStandards(“IFRS”)andbenchmarkssetforthintheCommitteeofSponsoringOrganizationsoftheTreadwayCommission(“COSO”)report.

TheInvestorRelationsdepartment,basedinbothParisandNewYork,maintainspermanentrelationshipswithanalystsatbrokeragefirmsandwithinvestmentfundmanagersandanalysts.ThedepartmentprovidesinformationonaregularbasistoconveyaclearunderstandingofthevariouseventsimpactingtheGroup’scurrentandfutureperformanceonthefinancialmarkets.Thisdepartmentalsomanagestheanalyst/investorrelationssectionoftheGroup’swebsite(www.vivendi.com),whichisupdatedregularly.Thissectionofthewebsiteisdirectedprimarilyatinstitutionalinvestors.

Vivendialsocommunicateswithinstitutionalinvestorsthroughmeetingsorganizedinthemainglobalfinancialmarketsandthroughtheparticipationofitshead-office andGroupbusinessexecutivesininvestors’conferences.

In2011,Vivendi’smanagement,theInvestorRelationsDepartmentandtheseniorexecutivesoftheGroup’sbusinesslinesmetmanyinstitutionalinvestorsoverthe courseof435“events”,themajorityofwhichtookplaceinFrance,theUKandtheUnitedStates,butalsoinothercountriesinEurope,AsiaandtheMiddleEast.ThesemeetingsallowedVivendi’smanagementtocommentontheresultsandoutlookoftheGrouptomanagersandanalystsfrom440financialinstitutionsat variousroadshows(managementvisited31destinationsduringtheyear),investorconferences(managementparticipatedin21conferencesduringtheyear)or meetingsattheheadquartersofVivendioritssubsidiaries.Specificfinancialcommunicationshavebeensetupwhichareaimedatanalystsandinvestorswhospecializeinsociallyresponsibleinvesting.

Communication to individual shareholdersCommunicatingwithallofitsindividualshareholderstokeeptheminformedofitsactivitiesandstrategyisatoppriorityforVivendi.TheShareholders’Club,createdin2010,helpsVivenditomeetthisgoal.In2011,Clubmembersreceivednumerousdocumentstohelpkeepthemup-to-datewiththeprogressofthecompany(includingLetterstotheShareholders,theActivityandSustainableDevelopmentReportandpressreleases).Memberswerealsoinvitedtoattend18informationmeetings,heldinParisandelsewhereinFrance.Jean-BernardLévy,ChairmanoftheManagementBoard,wenttoGrenobleandStrasbourg,andPhilippeCapron,ChiefFinancialOfficerandamemberoftheManagementBoard,wenttoNice.Mr.CapronalsoledameetingattheActionariafair.SinceitscreationVivendihasattendedtheParisstockmarketandfinancialproductsfaireveryyear.Moreover,meetingswiththeCommunicationsDepartmentandeducationalsessionswiththe Ecole de la Bourseonthetopics“Howtoreadafinancialarticle”and“GeneralShareholders’Meetings”wereorganizedinvariouscities.Finally,thethematicmeetings,“Jeudi, c’est Vivendi”,continuetotakeplace.In2011,thesemeetingsfocusedonsuchtopicsasmusic,StudioCanalandculturaldiversity.

TheShareholders’ClubalsostrivestoofferitsmembersadditionalbenefitsrelatedtotheGroup’sactivities,suchas:previewscreeningsoffilmsproducedordistributedbyStudioCanal;ticketstotheOlympiaTheaterandCanal+TVshows;liverebroadcastsofoperas;ticketstotheVivendiSeveTrophygolftournament;and visitstotheSFRsecuritycenter.Asafurtherexpressionofitscommitmenttokeepinvestorsinformed,inOctober2011,Vivendilauncheditswebzine,“Sh@ringVivendi”(availableatwww.vivendi.com),whosemanyarticlesandvideosaretargetedpredominantlyatshareholders.Vivendihasalsocreatedanotherinterestingactivityforits shareholders:everyFridayafternoon,shareholderscanlistento“audionews”fromVivendi(atwo-minutecommentaryinaudioformat)whichcontainsthelatest newsabouttheGroupanditssubsidiaries.

Section1 Description of the Group

20 Vivendi 2011AnnualReport

Inaddition,theShareholders’Committeemetfourtimesin2011.ItfocusedontheAnnualShareholders’Meeting,Actionariaanddigitaldevelopments.ThecommitteeactsasabridgebetweenVivendimanagementandtheshareholders,whocancontactthecommitteeatanytimeviaemail([email protected])withtheirquestions.

Finally,Vivendi’sindividualshareholderinformationserviceisavailabletoanswershareholders’questionsfromMondaytoFriday(toll-freeat0805050050inFranceand+33171713499outsideFrance).

1.3.3. Value Creation in 2011

TheGrouptookseveralmajorstepsforwardin2011:thedisputewithDeutscheTelekomregardingtheownershipofthesharecapitalofPTCinPolandwasresolved,thesaleofVivendi’sremaining20%stakeinNBCUniversalwascompletedinJanuary,andtheacquisitionofthe44%stakeinSFRheldbyVodafonewascompletedinJune.Vivendinowhasexclusivecontroloverallofitsbusinesslines,whicharefocusedontelecommunicationssubscriptionsinFrance,Morocco,Sub-SaharanAfricaandBrazil,andonmedia(television,videogamesandmusic)globally.TheGroupisalsowellpositionedtobenefitfromgrowingconsumerdemandforhigh-content,high-speedInternetaccessandinteractiveservicesaroundtheworld.

Duringthesecondhalfof2011,Vivendiannouncedthreesignificantinvestments,whichremainsubjecttoapprovalfromthecompetentauthorities.First,the acquisitionbyUMGofEMI’srecordedmusicbusinesswillenabletheconsolidationofUMG’spositionasagloballeaderinrecordedmusicbyconsiderablyenrichingitsportfolioofartistsandgeneratingconsiderablesynergies.Second,GroupeCanal+hastakenastrategicstepbygainingafootholdintheadvertising-financedtelevisionmarketinFrancewiththeacquisitionoftheDirect8andDirectStarchannels,whichwerepreviouslyownedbytheBolloréGroup.Thisacquisitiontakestheformofapartnership,withtheBolloréGrouptakinganequitystakeinVivendi.Third,GroupeCanal+implementedasimilarstrategyinPolandthroughthe creationofapartnershipwiththeGroupsITIandTVN.Underthisarrangement,GroupeCanal+tookcontrolofthepay-TVplatformformedbythecombinationof “Cyfra+”,whichitcontrolled,and“n”whichwascontrolledbyTVN.Canal+isalsomakingaminoritystakeinthecapitalofthefree-TVGroupTVN.

Groupactivitiesrecordedverystrongoperationalperformance,achievinganadjustednetincomeofmorethan€2.85 billioninNovemberaftertheannouncementof theacquisitionofthe44%stakeinSFRpreviouslyheldbyVodafone,despitethenegativeimpactoftaxmeasuresinFranceapprovedbytheFrenchgovernmentin September2011,whichdecreasedGroupearningsbyover€350 million.ThisexcellentperformancederivedfromallofVivendi’sbusinesslines,butinparticularActivisionBlizzardandGVT.

ThenetfinancialdebtoftheVivendiGrouptotaled€12 billionasofDecember31,2011.Asofthatdate,theaverageeconomicmaturityoftheGroup’sdebtwasapproximatelyfouryearsandVivendiSAhadnearly€6.3 billioninavailablecreditlines.TheGroupmaintainsasolidfinancialposition,allowingittocontinueitsvalue creatingstrategy;payregular,substantialdividendstoitsshareholders;andmaintainitsqualitycreditrating(currentlyBBB).Shareholdersthusbenefitfromthe capitalleveragecreatedbydebtthatiscarefullycontrolledintermsofbothvolumeandcost.

Share PriceVivendisharesarelistedoncompartmentAofEuronextParis(ISINcodeFR0000127771).AsofDecember31,2011,Vivendihadtheeleventh-largeststockmarketcapitalizationintheCAC40IndexandthelargestcapitalizationintheStoxxEurope600Mediaindex.Followingtheacquisitionofthe44%stakeinSFRpreviouslyheldbyVodafone,VivendistockwastransferredfromtheMSCIEuropeMediaIndextotheMSCIEuropeTelecomIndexinAugust2011.

2011wasmarkedbyaveryvolatilestockmarketenvironment,dueinparticulartothesovereigndebtcrisisinEurope.Inthiscontext,theCAC40Indexfellby17.8%drivenbylowerfinancialstocks.TheVivendisharepricepartiallybenefittedfromitsroleasdefensivestock,withadecreaseofjust16.2%.Itclosedat€16.92onDecember31,2011.Onthebasisofreinvesteddividends,theperformanceofVivendisharesin2011washigherthantheCAC40by3.3points.

Duringthefirsthalfof2011,VivendisharesperformedcomparablytotheCAC40.TheincreasinglycompetitiveenvironmentintheFrenchtelecommunicationssector wasoffsetbythepositivenewsoftheresolutionofthedisputeinPolandandtheacquisitionofthe44%stakeinSFR.Duringthesecondhalfoftheyear,the performanceoftheVivendishareimprovedduetogoodGroupoperatingincomeandthestrategicacquisitionsmadeinthemusicandtelevisionsectors,despiteunfavorabledevelopmentsinthetaxregimeinFrance.

Dividend per ShareThepaymentofadividendof€1persharein2012forfiscalyear2011,representingatotaldistributionof€1.25 billion,willbesubmittedforapprovalbytheOrdinary Shareholders’MeetingonApril19,2012.ThedividendwillbepayableincashfromMay9,2012.AtitsmeetingofFebruary29,2012,afterhavingheardareportfromtheSupervisoryBoard,Vivendi’sManagementBoardresolvedtoallocatetoeachshareholderonebonusshareforevery30sharesheld,distributableasfromMay9,2012.

Section1 Description of the Group

21Vivendi DescriptionoftheGroup

Des

crip

tion

of th

e G

roup

– L

itiga

tion

– Ri

sk F

acto

rs

21.4. Sustainable Development Policy

Vivendi,throughitsworldwidebusinessactivities,exertsahuman,intellectualandculturalinfluenceonsociety.In2011,theGroupinvested€2.4 billioninvideogames,music,filmandaudiovisualprogramminganddedicated€3.4 billiontonetcapitalexpenditure,including€3 millionintelecommunicationsbusiness.TheGroup’scontributiontosustainabledevelopmentisparticular:tosatisfythecommunicationsneedsofcurrentandfuturegenerations,nourishtheircuriosity,developtheir talentsandencourageinterculturaldialog.

Since2003,Vivendihasidentifiedthreespecificissues:protectingandempoweringyoungpeoplewhentheyusemultimediaservices,promotingculturaldiversityand sharingknowledge.ThesethreeissuesformpartoftheGroup’sbroaderindustrialchallenge:innovatingtokeepitstensof millionsofcustomersoneverycontinentsatisfied.

In2011,VivendiwontheFrenchForumforSociallyResponsibleInvestment(FIR)–VigeoinauguralawardintheCAC 40companycategory.Thisawardwascreatedas part of SociallyResponsibleInvestmentWeekandwasgiventoJean-BernardLévy,theChairmanofVivendi’sManagementBoard,inthepresenceofNathalie Kosciusko-Morizet,theFrenchMinisterofEcology,SustainableDevelopment,TransportandHousing.Thejuryevaluatedtheperformanceofthecompeting businesseswithregardtotheintegrationofsustainabledevelopmentissues(principles,goalsandrisks)incorporategovernance.

Vivendialsohasaveryhighscoringfromextra-financialratingsagencies.TheGroupreneweditsmembershipinthemainSRI(SociallyResponsibleInvesting)indices:theDowJonesSustainabilityWorldEnlargedIndex(DowJones)createdinlate2010,theASPIEurozoneIndex(Vigeo);theEthibelSustainabilityIndex(Ethibel);the ECPIEthicalIndexes(E-capitalPartners);andtheFTSE4GoodGlobal(FTSE).InApril2011,Vivendirankedn°1ex aequoworldwideintheFTSE4GoodESGRatings.ThisrankingwasestablishedbyFTSE(FinancialTimesStockExchange,anindependentcompanyjointlyownedbytheFinancialTimesandtheLondonStockExchangeGroup)andisawardedbasedontheresultsoftheannualevaluationofextra-financialperformanceofselectedcompaniesontheFTSE4GoodIndex.In2011,theGroupalsojoinedtheStoxxGlobalESGLeadersIndexandwasgrantedCorporateResponsibilityPrimestatusbyOekom.Inaddition,eachyear,Vivendicontributestothe CarbonDisclosureProject(CDP),whichisaninternationalprogramthatpublishesareportonthecarbonfootprintandclimatechangestrategiesoftheworld’s500 largestcompanies.

InJanuary2012,VivendiwasrankedseventhontheGlobal100mostsustainablecorporationsintheworld.ThisannouncementwasmadeattheopeningoftheDavosEconomicForum.VivendiisthefirstFrenchcompanytoappearontheGlobal100list.

TheEMAS(EcoManagementandAuditScheme)certificationforVivendiSA’senvironmentalapproachhasbeenconfirmed.VivendiisoneofthefewFrenchcompanies havingreceivedthiscertification.ThisEuropeancertificationisoneofthemostdemandingawardsintermsofenvironmentalmanagementandcommitmentto stakeholders.

TheGroupappliesarigoroussustainabledevelopmentpolicy,whichtakesintoconsiderationtheeconomic,social,societalandenvironmentalperformancesrelatedto itsvariousoperationsanditsbroadgeographicpresence.ThispolicyrequiresVivenditoclearlydemonstrateitscommitmentstoallofitspartners:customers,shareholders,employees,suppliers,publicauthoritiesandthesocietyatlarge.

VivendiisamemberoftheUnitedNationsGlobalcompact.ThismembershipdemonstratestheGroup’sdedicationtotwomainobjectives:reaffirmingtheGroup’scommitmentinfavorofhumanrightswhileitsbusinessesexpandintonewmarketsandcontributingtobettermeetingthecommunicationneedsaswellasthedesire forentertainmentofdisadvantagedconsumers.

Eachyear,Vivendireportsonitspolicies,actionsandextra-financialreportinginanActivityandSustainableDevelopmentReportandinapublicationentitled“SociographicsandEnvironmentalPolicy”.ThesereportsareavailableontheGroup’swebsiteunderthe“SustainableDevelopment”and“FinancialInformation”tabs.BesidesthestandardsrequiredbytheFrenchNewEconomicRegulationsActof2001(NREAct),Vivendipublisheseconomicandcorporategovernanceindicators,as wellasindicatorsrelatedtoitsstrategicchallenges.

Forthetenthconsecutiveyear,the2011ActivityandSustainableDevelopmentReportwasprovidedwithamoderatelevelofassurancebyKPMGSA,oneof Vivendi’sstatutoryauditors,onthebasisofselectedsocialindicatorsattheGrouplevelandenvironmentalindicatorsforitsbusinessunits.Thisexternalauditor’sreport,along withthereportingmethodologyappliedbyKPMG,appearsinthesustainabledevelopmentonlinedetailedreportonwww.vivendi.com.

1.4.1. Main Sustainable Development Issues

GiventhekeycharacteristicsoftheGroup’sactivities,Vivendihasidentifiedpriorityareasforaction.

Asaproduceranddistributorofcontent,theGroupmustevaluatetheopportunitiesandrisksthatsuchcontentcouldrepresentforitsvariouscustomers.Since2003,therefore,Vivendihasidentifiedthreestrategicsustainabledevelopmentissues:protectingandempoweringyoungpeoplewhentheyusemultimediaservices,promotingculturaldiversityandknowledgesharing(seesection1.4.2.,“Vivendi’sSpecificIssues”inthissection).

Section1 Description of the Group

22 Vivendi 2011AnnualReport

SinceVivendiisattheheartofbroadband-andmobility-driventechnologicaldevelopments,theGroupmustreconcileitsneedtokeepstepwiththedigitalrevolutionwithitsneedtosatisfythedemandsofitskeystakeholders(includingemployees,consumers,artists,suppliersandthesocietyatlarge)andregulatoryrequirements.Managinghumancapital,valuingcontent,payingattentiontosuppliersandcommunicatingwithitsstakeholdersarealsoamongthe Group’ssustainabledevelopmentissues.

ThesubscriptionbusinessmodelonwhichtheGroup’sbusinessunitsrelyraisestheissueofcollectionandprocessingofpersonaldataofsubscribersand customers.IneverycountryinwhichVivendioperates,thecompanyseekstomeetsubscriberexpectationsregardingcontentandserviceofferingswhilesimultaneouslymaintainingarigorousethicalpolicyforthemanagementofpersonaldata.

Lastly,asVivendioperatesinnewmarketsinhigh-growthcountries,itmustassessitscontributiontolocaldevelopmentintheemergingcountriesinwhichithasa presence.Thisincludesemployment,investmentsininfrastructures,developmentoflocaltalentsandaccesstonewinformationandcommunicationtechnologies,whichisoneofthekeystosuccessessoughtbygovernmentsintheenhancementofeducationandcompetitiveness.

1.4.2. Vivendi’s Strategic Issues

Startingin2003,bytheveryidentificationofitsthreestrategicissues,Vivendihasinnovatedbywideningthescopeofitssocietalresponsibility.TheGrouphasformulateditsambitionsinapositiveandconcretemanner.

Protecting and empowering youthVivendihastheresponsibilityofaccompanyingallaudiences,particularlyyoungpeople,inthedevelopmentoftheirculturalandmediapractices,whileatthesametimebuildingamoresecuredigitaluniverse.Indoingso,theGroupmustreconcilethedevelopmentofcontentandserviceofferingsdrivenbynewtechnologieswiththe protectionofyoungconsumersfrompracticesorbehaviorsthatmaybeharmfultothem.Mobiletelephones,Internet,gamesandfilmsmaycontainsensitivecontentorleadtoinappropriatebehavior.TheGroup’sbusinessunitsworkincollaborationwithVivendi’ssustainabledevelopmentdepartmenttoaddressthisissueat aGrouplevel.

Promoting cultural diversity in content production and distributionVivendiaimstopromoteculturaldiversityasanecessarymanifestationofhumandignityandapillarofsocialcohesion.ItthussharesUNESCO’sview,asexpressedinits ConventionontheProtectionandPromotionoftheDiversityofCulturalExpressions(whichcameintoforceinMarch2007)thatculturaldiversityis“amainspringforsustainabledevelopmentforcommunities,peoplesandnations”.Vivendi’sambitionistoencouragethediversityofmusicalrepertoires,promotediversityofcinematographicand televisualexpression,promotelocaltalentandenhanceculturalheritage.

Sharing knowledge by reducing the digital dividePromotingknowledgesharinginordertofosterbothaspiritofopennesswithothersandamutualunderstandingisthethirdspecificissueofVivendi’ssustainabledevelopmentpolicy.Throughitsinternationalreach,theGroupexercisesacertaininfluenceovertherepresentationofvariousculturesand,throughthis,itcanpromotemutualunderstanding.Itmustensurethequalityofitscontent,encouragedialogbetweenculturesandfacilitateaccesstonewtechnologies.Vivendithuscontributestoreducingthedigitaldividebyallowingschoolsanduniversitiestobenefitfromadvantageousserviceoffers.Italsoconductstrainingand educationalactivitiesfordisadvantagedpeopleusingnewcommunicationtechnologies.

1.4.3. Implementation of Sustainable Development Policy

1.4.3.1.Inclusionofsustainabledevelopmentcriteriaintheassessmentofthevariableremunerationofmanagementcompensation

DuringtheGeneralShareholders’MeetingofApril30,2009,theChairmanoftheSupervisoryBoardannouncedthatsustainabledevelopmentobjectivesshallbe includedinthecalculationofthecompensationformembersoftheVivendimanagementteambeginningin2010.

Themanagementboardhasthusrequestedthatthecriteriasetoutforeachbusinessunitreflectstheparticularknow-howandpositioningofeachunitandthatthe criteriaberelevant,measurableandabletobeconfirmedbyaspecializedfirm.

Accordingly,whencalculatingbonusesfortherelevantmembersofthemanagementteam,theirindividualcontributiontomeetingthestrategicsustainabledevelopmentobjectivesfortheGroup,suchassupportingyoungpeopleintheirmediapractices,promotingculturaldiversityorbridgingthedigitaldivide,are to be measuredandaccountedfor.

VivendiisoneofthefirstcompaniesintheCAC 40toincorporateperformanceobjectiveslinkedtoitssocietalresponsibilityintothevariablecompensationofseniorexecutives.Theextra-financialratingagencyVigeohelpstheGroupevaluateitsgoals.

ThegoalschosenbyVivendi’ssubsidiariesincludetheactionsundertakenbySFRandMarocTelecomGrouptoreducethedigitaldividebyfacilitating,forexample,accessibilitytoproductsandservicesfordisabledordisadvantagedpersons;theactionsofGVT,whichhaschosentodeployambitiousInterneteducationprogramsin Brazil;theactionsofCanal+Grouptoencouragediversityinthefilmsbroadcastonitschannels;orthecommitmentbyUniversalMusicGrouptopromotelocaltalentinemergingcountries.Measurableindicatorshavebeenidentifiedthatcorrespondtoeachofthesegoals.

Section1 Description of the Group

23Vivendi DescriptionoftheGroup

Des

crip

tion

of th

e G

roup

– L

itiga

tion

– Ri

sk F

acto

rs

2MarocTelecomreceivedtheVigeoTrophy(TopPerformerCSR2011)foritseffortstopreventcorruptionanditsvolunteerpolicytocombatthedigitaldivide.This awardisarecognitionoftheworkthathasbeendonebyMarocTelecom.Italsodemonstratestheconsistencyofthesustainabledevelopmentpoliciesenacted attheGrouplevelandwithinitssubsidiariesaswellastherelevanceofmakingeffortstolessenthedigitaldivideaGrouppriority.

1.4.3.2.SustainableDevelopmentIssues:Cross-Mobilization

TheChairmanoftheManagementBoardregularlyincludessustainabledevelopmentissuesontheagendasformeetingsoftheManagementBoardortheRisk Committee.TheChairmanalsoinvitesexpertstothesemeetingsinordertodiscussandanalyzethedevelopmentoftheGroup’sactivitieswithregardto meeting sustainabledevelopmentchallenges.

TheSustainableDevelopmentDepartmentcoordinatesthistaskinclosecollaborationwithallheadquarters’operatingdepartments,aswellaswiththoseofthe Group’sbusinessunits.

TogetherwiththeInvestorRelationsDepartment,theSustainableDevelopmentDepartmentorganizesmeetingswiththefinancialcommunitytopresentthe Group’s sustainabledevelopmentpolicy.

TheSustainableDevelopmentDepartmentworksregularlywiththeAuditDepartmentwhentheRiskCommitteecarriesoutitsexaminationofsustainabledevelopmenttopicsorother morespecificactions,suchasthepreparationofaquestionnaireforcompletionbytheprincipalsuppliersofthebusinessunits.Both departmentshaveestablishedamapofsustainabledevelopmentrisks.Thegoalfor2012istoadaptthismaptoeachbusinessunit’sspecifics.

InconnectionwiththeGeneralCounsel’sOffice,theSustainableDevelopmentDepartmentcontributestopromotingtheComplianceProgramwithintheGroupandamongitsvariouspartners.ItparticipatesintasksrelatedtothemonitoringofVivendi’spoliciesregardingtheprocessingandcollectionofpersonaldata.

InclosecollaborationwiththeHumanResourcesDepartment,theSustainableDevelopmentDepartmentisinvolvedinincorporatingandapplyingsustainabledevelopmentcriteriaintheGroup’smanagementcompensationschemes.ItalsocarriesoutinitiativestohelpraiseawarenessamongtheGroup’ssocialpartners.It wasinvolvedinpreparingtheExpertReportfortheVivendiGroupWorksCouncil.

Moreover,since2003,theSustainableDevelopmentDepartmenthasreliedontheworkofasustainabledevelopmentcommitteethatmeetsseveraltimesayear.This committeebringstogetherrepresentativesinchargewithsustainabledevelopmentissuesfromtheGroup’sparticularbusinessunitsandrepresentativesfrom theheadquarters.

1.4.3.3.Changesinreportinginaccordancewiththe“GrenelleII”LawandtheGlobalReportingInitiative

In2011,Vivendimadechangestoitsextra-financialreporting.Theobjectiveistohavethebestmanagementtoolpossiblewhilesimultaneouslysatisfyingnationaland internationalregulatoryandprofessionalrequirements.

1.4.3.3.1. The “Grenelle II” LawInJuly2011,VivendiaskedrepresentativesfromtheLegalDepartmentandAuditDepartmentandmanagersinchargeofreportingforvariousGroupbusinessunitsto attendameetingoftheSustainableDevelopmentCommittee.Thismeetingwasdedicatedtochangesinthecollectingandconsolidationofenvironmental,socialandsocietaldataasdefinedunderthetermsofthe“GrenelleII”law.Thiswaspartofthesensitizationprocessconductedbycorporateheadquartersto the subsidiariesoftheGroupsince2009.

Article116oftheFrenchNewEconomicRegulationsActof2001(NREAct)containednoprovisionsregardingsocietyatlarge.However,startingin2008,Vivendihas organizedthecollectionofsocietaldataconnectedtoitsthreestrategicissues.TheGrenelleIILawsetsforthandstrengthensthesocietaldimensionof extra-financialreportingbycompanies.Inordertocomplywithit,Vivendidefinedsocietalindicatorsdirectlyrelatedtoitsactivities.Asaresult,extra-financialreportingcan meetitsprimaryfunctiontobethemostelaboratemanagementtoolpossibletoavoidrisksandstrengthenopportunitiesrelatedtotheGroup’ssustainabledevelopmentpolicy.

ThetakingintoaccountoftheGroup’simpactonsociety,ofFrenchregulationsandofinternationalreferentialshasledVivenditoincludeitsthreestrategicissueswithinthescopeofits“actionsundertakentopromotehumanrights”.TheprotectionandempowermentofyoungpeopleispartoftheUnitedNationsConventionon theRightsoftheChildof1989(Art.17).Thepromotionofculturaldiversityisbasedonseveralfoundingtexts,amongwhicharetheUniversalDeclarationofHuman Rightsof1948(Art.27),theUNESCOUniversalDeclarationonCulturalDiversityof2001(Art.5)andtheUNESCOConventionontheProtectionandPromotion oftheDiversityofCulturalExpressionsof2005(Art.2).Thesharingofknowledgecontributessignificantlytotheexerciseofhumanrights,asisstatedin theCharterofFundamentalRightsoftheEuropeanUnion(2000)(Art.11)relatedtofreedomofexpressionandinformationortheUnitedNationsinitsMillenniumDevelopmentGoals(2000).

Thereportingprotocolthatdefinestherequirementsandprocessforgatheringextra-financialdatathereforenowincludesachapteronsocietaldata.ItdescribesthemannerinwhichVivendiconsiderstheterritorial,economicandsocialimpactofitsactivity,itsrelationshipwithstakeholders,includingsubcontractorsandsuppliers,

Section1 Description of the Group

24 Vivendi 2011AnnualReport

andthefairnessofitspractices.Thislastaspectincludesanti-corruptionmeasuresandmeasuresdesignedtopromoteconsumerhealthandsafety.ItalsoincludesactionstopromotehumanrightsthatgobeyondbasicsocialrightsandincorporatetheGroup’sthreestrategicissues.

AllGroupentities,asdefinedinVivendi’smethodologicalnoteonreporting(whichispresentedinthesustainabledevelopmentspecificationsavailableonthe corporatewebsite),uploadallofthesocietal,environmentalandsocialindicatorsdefinedintheprotocol.Thepurposeistodiscloseinthe2012RegistrationDocument (Document de référence)theextra-financialindicatorsthataremostrelevanttotheGroup.

1.4.3.3.2. The Global Reporting Initiative (GRI)TheGlobalReportingInitiative(GRI)wascreatedin1997.Itsmissionistosetguidelinesthatwillhelporganizationsreportontheireconomic,environmentalandsocial performance.Besidesuniversallyapplicableguidelines,sectorsupplementsmakeitpossibletoaddressthechallengesspecifictocertainsectors.Giventhe intellectualandculturalimpactofthemediaindustry,aninternational,multi-partnerworkinggroupwascreatedin2009todevelopasectorsupplementspecificallyformediaorganizations.

Vivendiisafoundingmemberofthisworkinggroup.Accordingly,itactivelycontributestothedevelopmentofsectorindicatorstobepublishedinthefirsthalfof2012.Thisworkinggrouprepresentsasignificantadvancewithregardtothereportingframeworkthatwillapplytotheentiremediaindustryinternationally.Severalthemesareincludedinthissupplement,includingfreedomofexpression;pluralismandthequalityofcontenteditorial;independence;protectionofpersonaldata;accessibility andmedialiteracy.

1.4.3.4.AnEnhancedDialoguewithStakeholders

Vivendiiscontinuingtostrengthendialoguewithitsvariouspartners.In2011,itpresenteditssustainabledevelopmentpolicytoinstitutionalanduniversityrepresentativebodies,andatinternationalmeetings.

TheGroupwasinvolvedintheParisEuroplaceworkshopsonthetheme“SustainableDevelopment–CSR–SRI(SociallyResponsibleInvestment),valuecreationleveraging–ContributionstoG-20andB-20goals”.

TheEssecBusinessSchoolinvitedVivenditoexplainhow,startingin2003,theGrouphaddefinedinnovativeobjectivesinitsunderstandingofitsresponsibilityto society.Thisconferencecenteredonthetheme“Innovation,Efficiency,Responsibility”.

VivendiwasalsoapartnerinthetenthEuropeanForumforSustainableDevelopmentandResponsibleEnterprise(FEDERE)inParis.Itcontributedtodiscussionsonthetheme“ManagingSRIstrategyininternationalcompetition:whatactionplantotakeinthefaceofpressurefromregulators,financialmarketsandcitizens?”

VivendiisoneofthefoundingmembersofaninitiativeannouncedonDecember1,2011byNeelieKroes,VicePresidentoftheEuropeanCommissioninchargeof theEuropeanDigitalAgenda.Theaimofthisinitiative,calledCEOCoalitiontomaketheInternetabetterplaceforkids,istomaketheInternetaplaceforexpressionthatensuresthesafetyofchildrenasmuchaspossible.ItfitsperfectlyintoVivendi’sstrategicissueswithregardtosociety.

Byjoiningthe CEO Coalition,Vivendiisclearlyexpressingitswillingnesstoshareitsbestpracticesandexpertisewithothermembermediaandtelecommunicationsbusinesses.TheGroupwantstostrengthenataEuropeanlevel,itsdialoguewithsocietyatlargeandpublicauthorities.Thisprocessis groundedintheGroup’ssustainabledevelopmentpolicy.

VivendisupportstheEuropeanCommission’s Safer Internet Program.Aspartofthisprogram,theGrouphascontinueditspartnershipswith European Schoolnetand the Insafenetworkandlaunchedtheonlineplatform Pan-EU Youth.Thepurposeofthis‘first-of-its-kind’projectistoofferyoungEuropeansa placeforexpressionanddiscussionaboutmattersofcitizenship.The Pan-EU Youthinitiativeoffersthreeonlineconsultationsonthethemesof“youngpeopleinthemedia”,“digitallives”,and“e-skills”.

ThefourthUnitedNationsAllianceofCivilizationsForumtookplacefromDecember10to13,2011inDoha(Qatar).Onthisoccasion,Vivendiwasinvitedtotakepartin adebateon“Newstrategiesfordialogue,understandingandinterculturalcooperation”alongsidepoliticalandacademicrepresentativesfromtheMiddleEastandEurope.

1.4.4. The Create Joy Solidarity Program

Create JoywaslaunchedbyVivendiin2008.ThissolidarityprogramsupportsthedevelopmentofunderprivilegedyoungpeoplebymakingentertainmentaccessibletothemwhilealsoteachingthemnewskillsandenablingthemtoplanbetterforthefuturethroughprojectsrelatedtoVivendi’sbusinessunits:videogames,music,telecommunications,theInternet,televisionandfilms.Create JoysupportsprojectsinFrance,theUK,theUnitedStates,Brazil,Morocco,MaliandBurkinaFaso.

Section1 Description of the Group

25Vivendi DescriptionoftheGroup

Des

crip

tion

of th

e G

roup

– L

itiga

tion

– Ri

sk F

acto

rs

2In2011,Create Joyfinancedapproximatelythirtyprojectsdevelopedbyassociationsthatworkwithhospitalizedchildren(including Starlight Children’s Foundation,USA; Medicinema,UK; Jeunes Talents,France),disabledyouth(Fondation Mallet, Toiles Enchantées, Signes de Sens,France),andunderprivilegedyoungpeople(Orchestre à l’Ecole, Apprentis d’Auteuil, Chance aux concours,France; Music For Youth, Vital Regeneration,UK; Reel Works Teen Filmmaking, Madison Square Boys & Girls Club,USA; CDI, Agencia do Bem,Brazil; Binkad,Mali; Cinéma Numérique Ambulant, BiblioBrousseand Lutt’Opie,BurkinaFaso).

In2011,VivendidevelopedseveraloriginalinitiativesthatenabledassociationstocometogetheranddiscusstheirCreate Joyprojects.

1.5. Human Resources

Vivendiiscommittedtoensuringthatemployees’contributionsarerewardedequitably.Consequently,theGrouphasimplementedaprofit-sharingpolicythatexceedslegalrequirementsandthatstronglyencouragesemployeeshareownership.Inadditiontotheseinternalprovisions,Vivendihasappliedasocialresponsibilitypolicytoassistregionsdeeplyaffectedbyunemploymentandindustrialrestructuringstohelpstimulateindustrialrevitalizationandjobgrowth.

1.5.1. Employee Share Ownership and Employee Saving Plans

ThestepstakentopromoteemployeeshareownershipwithintheVivendiGroupin2011wereacontinuationofthemeasureslaunchedin2008.ThatwastheyearthatsawthecreationoftheOpusprogram(leveragedsharecapitalincreasewithaninvestmentandminimumreturnguarantee)andofthecustomaryannualrightsissuefor employeesoftheGroup’sFrenchcompanies.The“Opus 11”programwaslaunchedsimultaneouslyinFranceandworldwide.

Development of Employee Saving Plans in FranceEmployeeshareownershipandsavingsincreasedin2011,asaresultofthecontributionsmadebytheGroup’sFrenchcompaniesundervariousparticipatorycompensationplans(includingstatutoryprofitsharing,optionalprofitsharingandemployer’scontribution).Asignificantportionoftheseemployeesavingscontinued tobeallocatedtoemployeeshareholdings.Atthesametime,employeescontinuedtodiversifytheirsavingswithinthevariousinvestmentoptionsoffered tothemundertheVivendiGroupSavingsPlan(“PEG”)andtheinvestmentoptionsofferedundertheirrelevantcompanyagreements.

In2011,netamountsreceivedbyemployeesoftheGroup’sFrenchcompaniesundertheoptionalprofitsharingplans(intéressement),statutoryprofitsharingplans(participation)andpursuanttocontributionsmadebyemployerstotheGroup’ssavingsplan(Plan d’épargne groupeorPEG)reachedarecordamountof€108.92 million,up12.5%comparedto2010.Theaggregateamountofadditionalemployeesavingsamountedto€84.6 million,€61.6 millionofwhichwasinvestedin thevariousPEGfunds.Theremaining€23 millionwasallocatedbyemployeestoretirementsavingplans(€12.4 millionofwhichwasallocatedtoPercoatSFR)and tovariousfundsorplansmaintainedbytheemployees’relevantcompanies.

Share Capital Increase for the Benefit of EmployeesOnMay10,2011,theManagementBoardapprovedtheannualsharecapitalincreaseforthebenefitoftheGroup’semployeesthroughthePEG,pursuanttoauthorizationsgivenbytheGeneralShareholders’MeetingofApril21,2011.ThetransactionwassuccessfullycompletedonJuly21,2011.Forthefourthconsecutiveyear,thecapitalincreaseinvolvedthesimultaneouslaunchofacustomaryemployeeoffering(inFrance)andaFrenchandinternationalleveragedplanwhichincludedaninvestmentandminimumreturnguarantee,called“Opus 11”.

In2011,aminimumguaranteedreturnwasoffered,compoundedattherateof2.5%peryearaswasthecaseforthetwopreviousyears.“Opus 11”wasofferedto employeesinallmajorcountriesinwhichtheGroupoperates,e.g.,France,theUnitedStates,Brazil,Morocco,GreatBritain,GermanyandtheNetherlands.

Despiteuncertaintiesinthemacroeconomicenvironment,the“Opus 11”projectwasatremendoussuccess.Theamountssubscribedconsiderablyexceededsubscriptionsforpreviousyears.Thetwoportionsofthecapitalincreasefor2011(customaryandleveraged)resultedinacapitalincreasetotaling€143.1 million,including€115 millionfor“Opus 11”,representinga49.7%increasecomparedto2010(arecordyear)and€28.1 millionforthecustomaryoffering,representinga29.5%increasecomparedto2010(alsoarecordyear).Asaresultofthistransaction,9,371,605newshareswereissued,including7,530,185sharesunder“Opus 11”and1,841,420sharesunderthecustomaryemployeeoffering.Thisvolumeofnewly-issuedshares,a31%increasecomparedtothe2010capitalincreasereservedfor employees,represents0.75%ofVivendi’soutstandingsharecapital.Uponcompletionofthetransaction,theportionofVivendi’ssharecapitalheldbyitsemployeeswas2.68%intheaggregate.

Thecapitalincreasewassubscribedforby10,861employees,including9,521through“Opus 11”and6,983inthecustomaryemployeeofferinginFrance.Theoverallparticipationrateofeligibleemployeesamountedto27.6%intotalunderthetwoshareplans.24.2%oftheparticipationwasfor“Opus 11”alone,49.1%ofwhichwasattributabletoemployeesinFranceand6.3%toemployeesoutsideFrance.InFrance,57.2%ofemployeesparticipatedinatleastoneofthetwoemployeeofferingplans.

Giventhesuccessofthe“Opus”program,theBoardofDirectorsresolved,onDecember13,2011,torenewtheprogramin2012aspartoftheemployeesharecapitaloffering,inparallelwiththecustomaryemployeeoffering.

Section1 Description of the Group

26 Vivendi 2011AnnualReport

1.5.2. Social dialogue and HR development

Throughout2011,thecorporatepartnersoftheGroupWorksCouncil,theEuropeanAuthorityforDialogbetweenManagementandLaborandtheheadquarters’WorksCouncilwereregularlyupdatedastotheGroup’sstrategy,financialposition,socialpolicy,andmainachievementsforthefiscalyear.Theannualtwo-daytrainingcoursecoveredGroupstrategyinthetelecomsindustryandknowledgeofthevariousVivendibusinesslinesandattendeeswerealsointroducedtotheAudit CommitteeandRiskCommittee.

2011endedwithamutualagreementtoadapttheGroup’semployeerepresentativebodiestoaninternationalenvironment(Morocco,BrazilandtheUSA).Accordingly,EuropeanemployeerepresentativesandmanagementhavebegunnegotiationswithaviewtounitingtheentireGrouparoundacommonsetof corporate andsocietalgoals.

Vivendihascreatedani3program(standingforInitiative,InnovationandInformation),whichenablesitssubsidiariestoincreaseandshareawarenessofthemajorhumanresourcesprojectstheydevelop.

TheVivendiGroup’strainingpolicyencouragesemployeestoacquireandstrengthentheskillsrequiredtofulfilltheirobjectivesandtopursuetheircareerdevelopment.EmployeetrainingrequestsandneedsareidentifiedanddiscussedbytheManagementandemployeerepresentatives.Theyarealsodiscussedduring eachemployee’sannualperformancereview.ThepercentageofpayrolldedicatedtotrainingremainssignificantlyhigherthanthatrequiredunderFrenchlaw.

Trainingisbothakeycomponentintherecruitmentofyoungprofessionalsandanassetforthecompany,whichisdiversifyingitsrecruitmentpoolsaccordingly.Vivendicontinuestomeetthecommitmentsitmadein2009,withthehiringof606employeesonalternatingwork-studycontractsinFrance(comparedto669in2010whencomparedonalike-for-likebasis).

Forseveralyears,VivendihasbeendevelopingatrainingprograminpartnershipwithINSEAD(theEuropeanBusinessAdministrationInstitute)toimproveitsemployees’futureleaders’skills.Thismade-to-measuretrainingprogramaimstodeveloptheskillsneededtobetterunderstandthenationalandinternationalbusinessenvironment,toanticipatemajortrendsinourmarkets,tolearnbestpractices,tochallengeexperiencesandtoredefineacceptedbeliefs.

Withanemploymentrateof34%,femalerepresentationintheGroupisconsiderablyhigherthantheCAC40benchmarks.Vivendiwishestoincreasethenumberof womenonexecutivecommittees.ConvincedthattheincreasedhiringofwomeninaseniormanagerialroleisanindicatorofsuccessfortheGroup,inlate2011,the ManagementBoardapprovedamentoringandnetworkingprogramtopromotegenderdiversityattheGroup’shighestlevels.Inaddition,alloftheFrenchsubsidiarieshavesignedinnovativeagreementsregardinggenderdiversityandprofessionalequality.

Withregardstoriskprevention,jobsafetyandworkingconditions,studieshavebeencarriedoutbyvariousentitiestoimplementrelevanttrainingprograms.Vivendicontinuestoimplementmeasuresinrelationtostressmanagementandpsychological-socialrisks.ThesemeasuresaretailoredtoeachGroupentity.Theyincludetrainingoflocalmanagers,afreehotlineavailabletoemployees,and/orinformationprovidedtoworkplacerepresentativeagencies(IRPs)byaspecialistphysician.

Vivendiencouragesinternalmobilityamongitsvariousbusinessunitsthroughthreemethods:anannualinterviewfocusingonemployeegoals,apeoplereviewby managementandaspecializedwebsite.Thewebsite,whichisaccessibleviatheIntranetsite,hasbeenimprovedthroughtheintegrationofnewtechnologiessuch ase-learningsothatemployeescanprepareforpossibletransfersbetweenbusinessunits.

Inaddition,asuccessionplaninrelationtotopmanagementpositionsandhigh-potentialemployeeshasbeenputintoplacewithineachGroupbusinessunit.Assoonasemergingleadersareidentified,theyareguidedbyapersonalizeddevelopmentplanthatencouragesgreatermobilityamongtheGroup’svariousbusinesses.

1.5.3. Contribution to Employment Development

Since2004,VivendihasmadecommitmentstotheFrenchpublicauthoritiestocontributetothecreationofjobsinregionsparticularlyaffectedbyunemploymentand industrialrestructuringintwodifferentways:• creating,viasubcontractors,twocallcenterslinkedtotheGroup’sactivity,oneinBelfort(atyear-end2005),theotherinDouai(atyear-end2006),with

a targetofcreating300full-timeequivalent(FTE)jobsateachlocation,or600jobsintotal.Atyear-end2011,theheadcountsatthesecenterswere462 and470FTEjobsrespectively;and

• aidtherevitalizationofvulnerableorlowemploymentareasidentifiedbytheFrenchMinistriesoftheEconomyandIndustry:€5 millionwillbeallocatedoverafive-yearperiodtoconsultancyandthefundingofprojectsdesignedtocreatejobs.

Theseprojectswereundertakenunderthetermsofaninitialfive-yearagreement(2005/2009).Theywerecontinuedunderasecondagreementinitiallyplannedforthreeyears(2010/2012).

Accomplishments under the 2005/2009 five-year agreement: 4,361 jobs createdTheresultsoftheelevenprogramsestablishedunderthe2005/2009five-yearagreementwerehighlysatisfactory:asofDecember31,2011,jobscertifiedbycommitmentcommittees,whichweresetupwithpublicauthoritiesineachrelevantarea,totaled5,263,andactualjobcreationstotaled4,361,whichrepresentedmorethan83%of certifiedjobs.

Section1 Description of the Group

27Vivendi DescriptionoftheGroup

Des

crip

tion

of th

e G

roup

– L

itiga

tion

– Ri

sk F

acto

rs

2Atyear-end2011,Vivendiexceededitsoverallgoaltocreate2,800jobsinallemploymentareasby88%forcertifiedjobsandby56%foractualjobscreated.

ThefirstemploymentprogramwassetupinMarch2005andthelatestprogramwaslaunchedinMarch2008.Eachprogramhasanoperatinglifetimeofatleastthreeyears.During2010and2011,severalprogramshavebeenextendedbeyondtheirinitialthree-yearperiod,inagreementwithandattherequestofthefollowingpublicauthorities:AbbevilleandMontdidier(Somme),ThannandCernay(Haut-Rhin),Pas-de-Calais(extensioncenteredontheCalaisareas),aswellasLeTonnerrois(Yonne).Atyear-end2011,onlytwoprogramswerestillnotcomplete(Haut-JuraandLeTonnerrois).Asaresult,the2011resultsforthefive-yearagreement(2005/2009)arenotentirelyfinal.

Moreover,attheendoftheoperationalphase,theeconomicdevelopmentcompaniesinvolvedremainwithintheseareasinordertofollowtheprogressoftheprogramstheyinstitutedandtoensurethatproposedjobstranslateintoactualones.

Mostoftheprogramshaveexceededtheirjobcreationgoalsconsiderably,albeittodifferingdegrees:157%inArles,100%intheSomme(AbbevilleandMontdidier),74%inThannandCernay(Haut-Rhin),73%intheOise,71%inDreux,58%inthePas-de-Calais,34%inSarrebourgand12%inChalon-sur-Saône.Atyear-end2011,theHaut-Jura(Saint-Claude)programalreadyexceededitsgoalby44%andtheLeTonnerroisprogramslightlyexceededitsgoalby3%.OnlytheAutun-Château-Chinonprogramislaggingbehind:thegoalhasbeenexceededby25%intermsofjobplanningbuthasnotyetbeenreachedintermsofjobcreation.