A Libertarian Perspective on Economic and Social Policy Lecture 11 Social Security ©2007 Jeffrey A. Miron

A Libertarian Perspective on Economic and Social Policy Lecture 11 Social Security ©2007 Jeffrey A. Miron.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A Libertarian Perspective on Economic and Social Policy

Lecture 11

Social Security

©2007 Jeffrey A. Miron

Introduction

• Social Security is probably the largest government transfer program in the world.– Collected $520.7 billion in taxes in 2005– Paid out $435.4 billion in benefits in 2004

• SS is widely regarded as a “success.”– Viewed as eliminating poverty among the elderly;– Providing retirement security for middle class as well.

• At the same time, SS faces financial difficulties:– The SS Trust Fund is projected to be bankrupt in

roughly 30 years.

Introduction, continued

• The standard “left” response to the pending financial insolvency is higher social security taxes:– This is not popular politically, however.

• The current “right” response is partial privatization of social security via the introduction of private accounts:– This is popular in some quarters, but also

meets with great skepticism.

Introduction, continued

• This lecture addresses the current Social Security debate. I argue that:

• What SS does is not what most people think it does.• “Fixing” SS is economically trivial but politically more

difficult• Introducing private accounts does not “fix” SS, and

Forced Savings plans are problematic anyway.• There are reasons to scale back Social Security that are

distinct from the current “crisis,” and this is politically feasible although not easy.

Outline

• Brief Description of Social Security

• The Pending Solvency Issue

• Private Accounts as a Solution

• The Pros and Cons of Forced Savings

• The Costs and Benefits of Social Security

• Proposals to Improve Social Security

The Structure of Social Security

• Taxes

• Benefits

• Trust Fund

• Unfunded Social Security Systems and the Return on Social Security Contributions

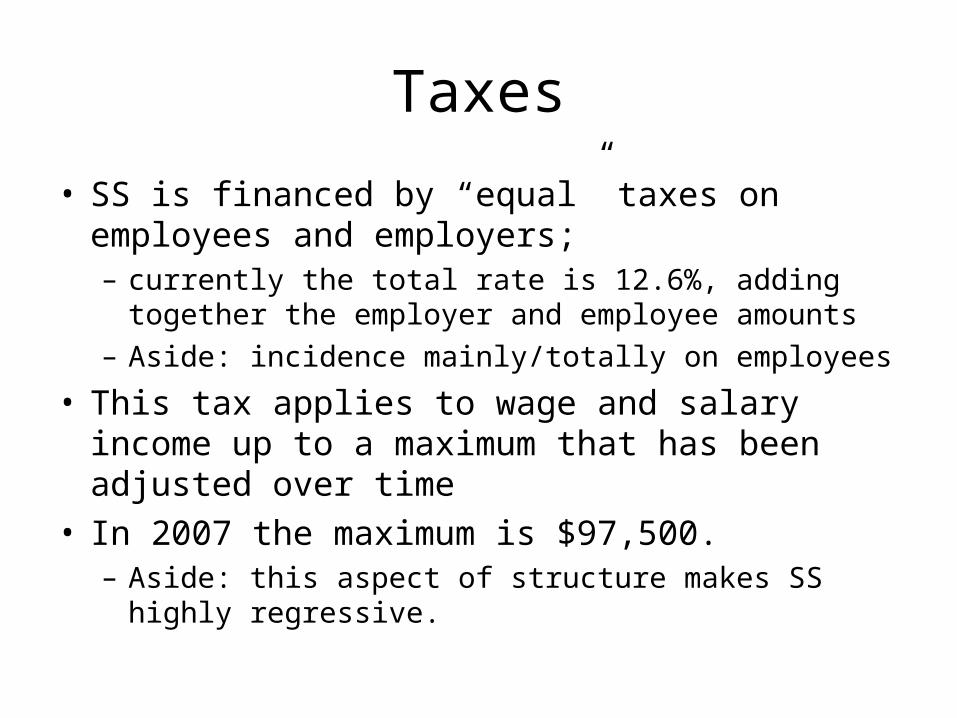

Taxes

• SS is financed by “equal” taxes on employees and employers;– currently the total rate is 12.6%, adding together the

employer and employee amounts– Aside: incidence mainly/totally on employees

• This tax applies to wage and salary income up to a maximum that has been adjusted over time

• In 2007 the maximum is $97,500.– Aside: this aspect of structure makes SS highly

regressive.

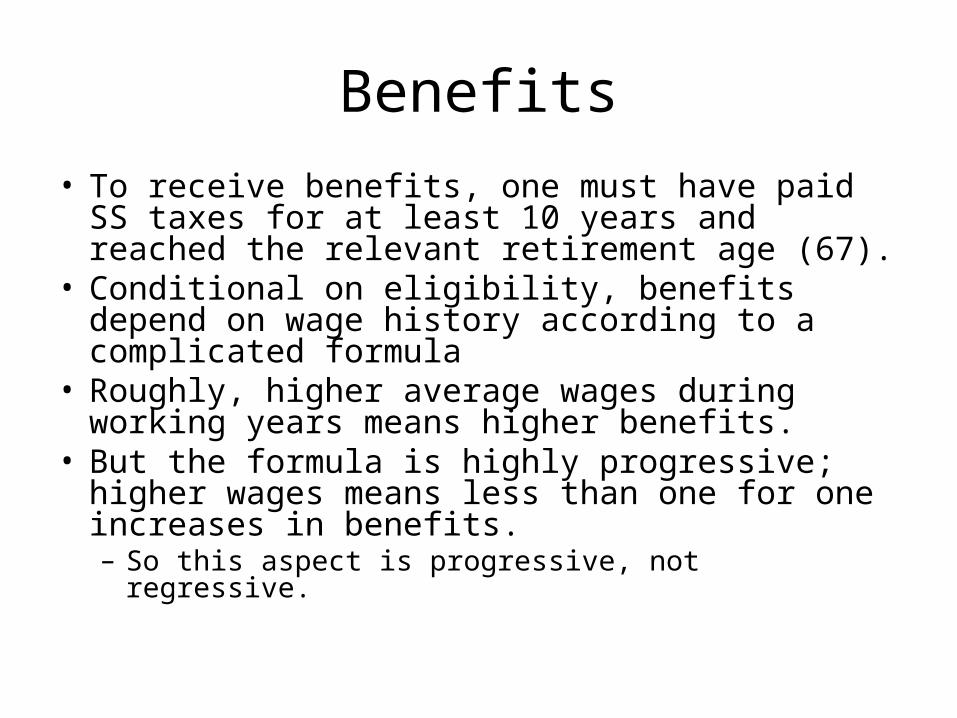

Benefits

• To receive benefits, one must have paid SS taxes for at least 10 years and reached the relevant retirement age (67).

• Conditional on eligibility, benefits depend on wage history according to a complicated formula

• Roughly, higher average wages during working years means higher benefits.

• But the formula is highly progressive; higher wages means less than one for one increases in benefits.– So this aspect is progressive, not regressive.

The Relation Between Benefits Received and Taxes Paid

• Additional participation and higher wages mean greater benefits, given the current formula and subject to the cap on eligible wages.

• But this is only because Congress chooses to make benefits depend on past earnings; this is a political trick to make people think they “own” their contributions and/or have earned benefits.

• In fact, Congress can change the formula at any time, subject only to the political ramifications.

The Social Security Trust Fund

• The Trust Fund links taxes and benefits• All taxes collected are deposited in the fund• All benefits paid flow out of this fund• The fund balance can be positive, zero, or

negative• If positive, the fund typically holds special issue

government bonds• If negative, the fund has borrowed (normally,

from the Treasury).

Funded versus Unfunded

• There are two ways to operate a trust fund:– Option 1: collect all the money at the outset, and then

pay it out over time (Funded)– Option 2: collect and pay the money as you go along

(Unfunded)

• In an unfunded system, current benefits payments come out of current taxes.

• The U.S., roughly, has an unfunded System.• Also called “Pay as You Go,” or PAYGO.

The Implications of Unfunded SS: An Example

• Assume an economy with no population growth.

• Everyone works for exactly 30 years, retires for exactly 30 years

• Everyone has the same wage; pays a certain percentage (e.g., 10%) in SS taxes

• These taxes are transferred immediately to retirees.

Example, continued

• Thus, in “steady state” the Trust Fund balance is always exactly zero.

• Same number of dollars flows in and out each year.

• Each person gets back an amount exactly equal to what he/she put in; but from someone else’s paycheck.

Example, continued

• What if population is growing?• Say there are always twice as many

working persons as retired persons.• Then under a PAYGO system, the amount

you get in retirement is twice what you paid in while working.

• More generally, if population grows at a rate of n percent, you get back n percent more than you put in.

The “Return” on Contributions

• The benefits a given person receives do not equal the taxes that person paid.

• Instead, benefits are paid from current taxes; that is the nature of PAYGO SS.

• Likewise, contributors do not own their contributions in any way, in contrast to private savings.

• Contributions are not saved or invested; simply paid out to someone already retired.

The “Return” on Contributions,continued

• Thus, talking about a return on SS contributions is meaningless: taxes are not saved or invested, so they pay no return in the normal, economic sense.

Many Analyses NeverthelessCalculate a “Return” on SS

• This “return” is the ratio of what a retiree gets out relative to what that retiree paid in.

• As the example shows, this return has no relation to interest rates or stock returns.

• In steady state, it equals the rate of growth of the wage base.

• Therefore, it depends on population and productivity growth.

• In the U.S., about 2-3 % on average.

The “Problem” with SS and Possible “Solutions”

• What is the nature of the problem?

• What are possible solutions?

• Are Private Accounts a solution?

The Current “Problem”

• According to existing projections, the Trust Fund will be bankrupt in roughly 30 years. Why?– Population growth has not been constant;– Baby boom means “too many retirees” in future– Starting in about 10-15 years, there will be more

being paid out as benefits than coming in in taxes.– And in 25-30 years, current surplus will be used up.

• This is the sense in which many observers think there is a “crisis” that needs to be fixed.

Is This Really a Problem?

• Whether the impending insolvency of the Trust Fund constitutes a problem depends on some auxiliary assumptions about the fungibility of SS and non-SS taxes and expenditures.

• These assumptions are dubious, at best:– Correct view of the “problem” is very different.

• But we’re going to accept the standard characterization for a few more minutes.

How to “Solve” the Problem

• Given the standard view, the discussion above suggests there are only three ways to make SS solvent:– Raise SS taxes– Cut SS benefits– Use non-SS taxes to pay SS benefits

• Last option implies there is not really a SS system; just a transfer to the elderly. This is correct, but ignore that for the moment.

Recent Discussion Suggests a Fourth “Solution”: Private Accounts• The claim of supporters goes as follows:

– “Return” on SS is only about 2-3%– Return on the stock market is about 7%

• Therefore, letting people “save” via private accounts will increase the return earned on savings and reduce or eliminate the financial difficulties facing SS.

What Are Private Accounts?

• Under a system of private accounts, individuals would be allowed to put some of their wages into designated stock or bond mutual funds, rather than paying them to the government as social security taxes.

• The contributors would own the accounts.• The accounts would earn a market return.• Owners would have access to the accumulated

interest and principal after some age limit (e.g., 67)

Private Accounts Sound Appealing;

In Fact, They Accomplish Nothing• They do not improve solvency, or increase

the rate of return, or improve the economy.

• The do not worsen solvency, or decrease the rate of return, or harm the economy.

• To a first approximation, introduction of private accounts has no effect on anything that matters.

Understanding Private Accounts

• To see the implications of private accounts, it is critical to ask what happens to the stream of promised benefits when private accounts are introduced.

• There are three possibilities:– No change in promised benefits.– A reduction in benefits equal in present value to the

reduction in taxes.– A reduction in benefits greater in present value than

the reduction in taxes.

Case 1: Introduce PA’s But Make No Change in Promised Benefits

• The direct effect of introducing PAs is to reduce the inflow of tax revenue into the Trust Fund.– So, the direct effect of introducing PAs is to reduce

solvency of the Trust Fund.

• Therefore, to continue to pay promised benefits, there must be an increase in some other tax.

• This means the net disposable income of taxpayers does not change:– They are paying less in SS taxes, but more in other

kinds of taxes.

Case 1: No Change in Benefits,continued

• At the same time, these taxpayers are, initially, saving more because of the taxes being put into private accounts.

• But since disposable income has not changed, and assuming the savings rate chosen by taxpayers before the introduction of private accounts was optimal, they will want to offset this forced increase in saving by reducing other saving.

• So nothing changes.– In particular, there is no additional savings to earn the

higher rate of return in the stock market.

Case 1: No Change in Benefits, continued

• That is, if we reduce someone’s SS taxes and do nothing else, this person has more disposable income and would normally save more.

• But if we reduce one kind of tax and increase another by the same amount, that person’s choice of consumption versus savings should not change.

• So, if this person can offset any forced saving, the person will do so.– And that is the normal case.

Case 1: No Change in Benefits, continued

• Thus, the introduction of private accounts, assuming no change in benefits, implies other taxes must go up.

• Everything else in the economy – savings, consumption, income – does not change.– The higher return on stocks is irrelevant if there is no

increase in savings.

• If one defines solvency of the TF as a function only of SS taxes, then solvency gets worse.

• But that’s irrelevant.

Case 2: PV of Benefit Reduction Equals PV of the Tax Reduction

• Cutting SS taxes and SS benefits by the same amount (in present value) has no effect on the solvency of the trust fund.– No need to raise other taxes to offset the cut in SS

taxes.• But to a taxpayer, a cut in SS benefits is (in PV)

equivalent to an increase in taxes.• So, again, there is no change in the disposable

income of taxpayers who receives the tax cut.• So, again, taxpayers will offset the extra savings

in the PAs with reduced savings elsewhere.

Case 2: Benefit Reduction Equals Tax Reduction, continued

• Assuming the forced savings in PAs is offset by decreased savings elsewhere, there is again no change in anything else:– Consumption, savings, income all stay the

same.– The introduction of private accounts has no

effect.

• In particular, there is no increase in savings, so the higher rate of return on stocks is irrelevant.

Case 3: PV of Benefit Reduction Exceeds PV of the Tax Reduction

• Think of this as two pieces:– Introduction of PAs combined with an exactly

equal cut in benefits– An additional benefit cut

• We know from analysis above the first part has no effect.

• The second part makes the TF more solvent.– But totally independent of the first part.

Different Explanation

• Consider an individual who gets to contribute to a private account instead of paying SS taxes.

• Say this person already owned stocks.• Then private accounts give him no new options.• And this person’s wealth does not change:

– taxes will be higher by amount necessary to pay for unchanged benefits, or benefits will be cut.

– So, desired savings does not change.• Thus, this person’s savings behavior does not

change, which means nothing in the economy changes.

What Explains the Claims of Privatization Advocates?

• The claims made for private accounts are really claims made for privatization plans that include additional changes in policy.

• Some plans include new taxes or benefit cuts in excess of the tax cuts:– These improve solvency, but not because of private

accounts

• Some plans cut taxes and benefits equally, but claim efficiency gains from these cuts:– This is probably right, but it is independent of private

accounts.

Summary So Far

• The alleged problem is that SS is not solvent; equivalently, the return is low.

• (This particular aspect of SS is a problem only to the extent one buys the accounting fictions embodied in the trust fund, but ignore that for a few more minutes).

• Introducing private accounts does nothing to improve solvency or increase the return.

• “Fixing” SS (accepting the standard definition of the problem) is “trivial:” cut benefits, raise SS taxes, or use other taxes.

Right View of Private Accounts

• Private accounts exist already; they’re called private savings.

• Question for policy is whether government should require contributions to such accounts.

• More broadly, should the government mandate a minimum rate of private savings?

Possible Justifications for Mandatory Savings

• Paternalism: some people will save too little– Can rationalize almost anything

• Externality: Society cannot restrain itself form bailing out the profligate– Exaggerated: private responses will emerge– Implies, at most, a low-income insurance

program

Possible Justifications, continued

• Income Redistribution: Some persons cannot save enough on their own– Again, justifies a low-income insurance

program, nothing more

• So, there are no convincing reasons for government to mandate private savings generally.

Effects of Forced Savings

• As implied by discussion above, the first-order effect of mandating savings is nothing:– Anyone who is already saving at least as much as the

mandated amount, and who has chosen this rate as being about right, will offset the forced saving by reducing other voluntary saving.

• For low-income households, the requirement to save might bind:– But it’s probably not good for such households, since

they need their income for current consumption.

And Forced Savings Program Have Their Own Negatives

• Administrative Costs

• Accumulations are tempting targets for taxation

• The implied promises give government an excuse to regulate financial markets

• Accepts the view that everyone is too stupid to save for retirement on their own.

Conclusions on Private Accounts

• Introducing Private Accounts and “fixing” Social Security are separate questions.– The right question on Private Accounts is whether

government should force higher savings.

• Libertarian answer is no.• In particular, government-mandated private

savings is not “privatization,” properly understood; it creates more government rather than less government.

Is There Really a Problem?If So, What is It?

• Once one ignores the accounting fiction incorporated into standard views, it becomes clear that what SS is really doing is paying current benefits out of current taxes:– So it’s just a transfer program; not a savings program

in any sense.

• The right question is therefore whether this transfer is desirable:– Specifically, does it makes sense to levy taxes and

distribute the proceeds to people who are elderly, simply because they are elderly?

The Costs of Transfers to the Elderly

• Distortionary Taxation– To pay benefits, the government must raise taxes.

Most taxes alter private behavior in inefficient ways.

• Other distortions:– Changing the age of retirement– Changing expectations about self-reliance.– Reducing national savings.

• Whether these distortions are large or small is an empirical question. But they’re certainly not zero, and in any case they are the real issue.

What are the Possible Justifications for Transfers to the Elderly?

• Same three as for mandatory savings:– Paternalism toward the myopic– Correcting an externality:

• Society cannot keep itself from bailing out the profligate– Redistributing income to those whose earnings is low.

• As with mandatory savings, however, these apply far more reasonably to low-income persons than to middle or upper income households.– Most sensible view is that the transfers should really

be thought of as disability insurance; transfers should be only to those who cannot support themselves.

Justifications for Transfers to the Elderly, continued

• Of course, once one thinks in this way, it is no longer apparent that a disabled 70 year old is more deserving than a disabled 30 year old:– Right criterion should presumably be ability to earn

income, not age per se• And the U.S. already has a disability insurance

program, which does almost exactly what I have proposed here.

• Thus, the case for anything beyond that is weak.• Thus, eliminate SS and retain, if anything, only

disability insurance / low-income insurance.

How Could the U.S. Eliminate SS?

• Even people who accept that SS is bad policy sometimes hesitate to endorse dismantling it because they think this would be unfair to current and future beneficiaries.

• In fact, there are several ways to gradually convert SS into a DI/LI program without doing serious harm to any particular group.

Eliminating SS, continued

• The most obvious approach is to gradually increase the age of eligibility:– Life expectancy has changed substantially– Age of eligibility has already been raised– Consistent with original program

• A second approach is to gradually introduce means-testing of benefit receipt and/or greater taxation of benefits:– Again consistent with original program– Effectively makes SS a guarantee against low-

income, rather than a retirement package for the middle class.

Conclusions

• The “Trust Fund” crisis (which is often exaggerated to begin with) is readily “fixed” by raising taxes or cutting benefits.

• Introducing government-mandated private accounts does nothing to address this issue.

• Setting aside SS, the case for a forced savings program is weak.

• SS is a problem, but the reason is the distortions it causes in the economy.

• Converting SS into a DI/LI program is doable, both economically and politically, but over the long term not in the short to medium term.

Related Documents