annual report 2008 EMIRA annual report 2008 A DIVERSIFIED AND BALANCED PORTFOLIO

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

annual report 2008

EMIRA annual report 2008

A DIVERSIFIED AND BALANCED PORTFOLIO

1 Objectives

2 Portfolio of top ten properties

4 Portfolio summary

6 Manager’s report

20 Directorate

23 Corporate governance

29 Sustainability

33 Annual financial statements

62 Property listing

71 Strategic Real Estate Managers (Pty) Ltd financial statements

86 Administration information

87 Form of proxy

A property fund created under the Emira Property Scheme, registered in terms of the Collective Investment Schemes Control Act

Share code: EMIISIN: ZAE000050712(“Emira”)

www.emira.co.za

>

A Fibonacci spiral is created by drawing arcs connecting the opposite corners of squares.

Leonardo Da Vinci used it for beauty and balance in the design of architecture and for balance in the design of art.

It was used in the design of the Notre Dame Cathedral in Paris.

It also appears in the physical proportions of the human body, movements in the stock market and many other aspects of life and the universe.

The Greeks recognised it as ‘dividing a line in the extreme and mean ratio’. The Renaissance artists knew it as the Divine Proportion.

Distributions per participating interest

92,04 cents annualised growth of 11,8%

Net asset value per participating interest 1 169 cents

an increase of 1,9%

Capital projects completed R330 million

Fuel Group Acsa ParkRandridge Mall Hyde Park CornerWorldWear Fashion Mall

A DIVERSIFIED AND BALANCED PORTFOLIO

Hyde Park Corner Boundary Terrace

A robust portfolio of 164 properties spanning the office, retail and industrial sectors across a wide national footprint, in all the major cities of South Africa.

A broad base of more than 4 000, predominantly blue-chip – tenants, ranging from listed giants and government departments to individual entrepreneurs.

A strong balance sheet with access to funding from the equity and debt capital markets, as well as traditional mortgages and short-term finance.

4 000 TENANTS

R7,8TOTAL ASSETSBILLION

164 PROPERTIES

emira property fund annual report 2008

1

Objectives

Results for the Results for theyear ended year ended %

30 June 2008 30 June 2007 change

FINANCIAL HIGHLIGHTSDistributions per participatory interest (cents) 92,04 82,35 12Headline earnings per participatory interest (cents) 122,12 76,77 59Vacancy factor (%) 6,8 5,9 —

Portfolio valuation analysisMarket value (R’000) 7 491 436 7 314 742 2Net asset value per participatory interest (cents) 1 169 1 148 2Listed market price per participatory interest (cents) 819 1 090 (25)Premium/(discount) to net asset value (%) (30) (5) —

SALIENT FEATURESParticipatory interests in issue 492 818 989 488 514 461 1Market capitalisation (R’000) 4 036 188 5 324 808 (24)Long-term borrowings (R’000) 1 327 204 1 287 050 3Long-term borrowings to total assets (%) 17,0 17,4 —Number of properties 164 168 (2)

The Fund’s principal objective is to grow earnings from a quality-based

property portfolio. Growth will be sought by making strategic investments

where yields are enhancing in the medium to long term. Management will

continually maintain the quality of the portfolio by disposals of assets,

which no longer meet the strategic objectives of the Fund.

THE STRATEGIC objECTIvES oF THE FUNd ARE To:

Optimise net income and growth in distributions;

Apply gearing to the portfolio to the extent that it enhances returns, limited to 60% as provided for in

the Collective Investment Schemes Control Act;

Increase market capitalisation, liquidity and spread of investors through selective acquisitions and

capital raising;

Selectively recycle assets;

Broaden the Fund’s geographic exposure to KwaZulu-Natal, the Western and Eastern Cape;

Maintain a balanced exposure to the retail, office and industrial property sectors, given the relative size

constraints of these sectors;

Dispose of non-performing or potentially under-performing properties;

Reduce vacancies and smooth the lease expiry profile of the portfolio; and

Meet the requirements and deadlines of the Property Sector Charter.

emira property fund annual report 2008

2

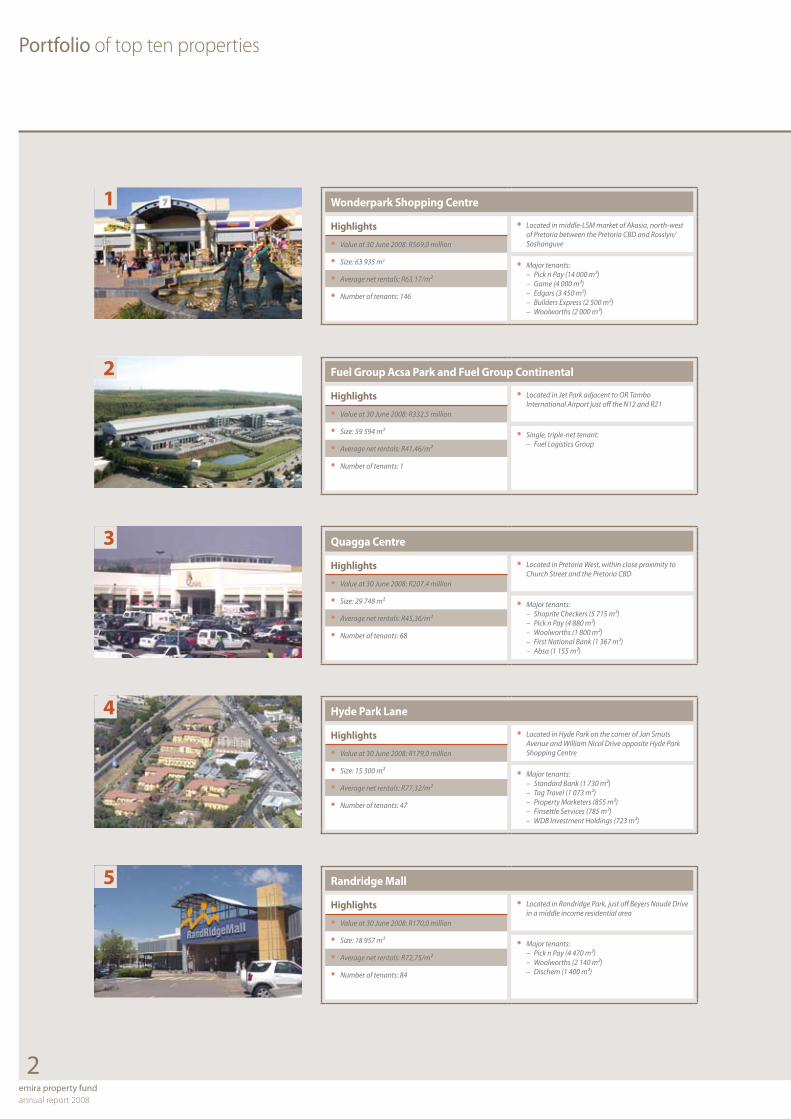

Wonderpark Shopping Centre

Highlights

Value at 30 June 2008: R569,0 million•Size: 63 935 m• 2

Average net rentals: R63,17/m²•Number of tenants: 146•

Located in middle-LSM market of Akasia, north-west •of Pretoria between the Pretoria CBD and Rosslyn/Soshanguve

Major tenants: •Pick n Pay (14 000 m²) –Game (4 000 m²) –Edgars (3 450 m²) –Builders Express (2 500 m²) –Woolworths (2 000 m²) –

Fuel Group Acsa Park and Fuel Group Continental

Highlights

Value at 30 June 2008: R332,5 million•Size: 59 594 m²•Average net rentals: R41,46/m²•Number of tenants: 1•

Located in Jet Park adjacent to OR Tambo •International Airport just off the N12 and R21

Single, triple-net tenant:•Fuel Logistics Group –

Hyde Park Lane

Highlights

Value at 30 June 2008: R179,0 million•Size: 15 300 m²•Average net rentals: R77,32/m²•Number of tenants: 47•

Located in Hyde Park on the corner of Jan Smuts •Avenue and William Nicol Drive opposite Hyde Park Shopping Centre

Major tenants:•Standard Bank (1 730 m²) –Tag Travel (1 073 m²) –Property Marketers (855 m²) –Finsettle Services (785 m²) –WDB Investment Holdings (723 m²) –

Quagga Centre

Highlights

Value at 30 June 2008: R207,4 million•Size: 29 748 m²•Average net rentals: R45,36/m²•Number of tenants: 68•

Located in Pretoria West, within close proximity to •Church Street and the Pretoria CBD

Major tenants:•Shoprite Checkers (5 715 m²) –Pick n Pay (4 880 m²) –Woolworths (1 800 m²) –First National Bank (1 367 m²) –Absa (1 155 m²) –

Randridge Mall

Highlights

Value at 30 June 2008: R170,0 million•Size: 18 957 m²•Average net rentals: R72,75/m²•Number of tenants: 84•

Located in Randridge Park, just off Beyers Naudé Drive •in a middle income residential area

Major tenants:•Pick n Pay (4 470 m²) –Woolworths (2 140 m²) –Dischem (1 400 m²) –

Portfolio of top ten properties

1

2

3

4

5

emira property fund annual report 2008

3

Portfolio of top ten propertiescontinued

WorldWear Fashion Mall

Highlights

Value at 30 June 2008: R159,0 million•Size: 13 629 m²•Average net rentals: R94,79/m²•Number of tenants: 67 •

Located on Beyers Naudé Drive adjacent the •N1 freeway and close to Cresta Shopping Centre

Major tenants: •Mr Price Home (2 500 m²) –The Pro Shop (1 025 m²) –Seemanns (616 m²) –

Lynnridge Mall

Highlights

Value at 30 June 2008: R157,5 million•Size: 14 220 m²•Average net rentals: R88,60/m²•Number of tenants: 57•

Located in Lynnwood Ridge, in the eastern suburbs •of Pretoria

Major tenants:•Pick n Pay (3 930 m²) –Mr Price Home (1 707 m²) –Absa Bank (1 190 m²) –Lion Bridge (915 m²) –

Faerie Glen office Park

Highlights

Value at 30 June 2008: R124,5 million•Size: 10 324 m²•Average net rentals: R76,08/m²•Number of tenants: 9•

Situated east of Pretoria overlooking Atterbury Drive, •a short drive from Menlyn Shopping Centre

Major tenants:•Softline VIP (5 755 m²) –FNB (1 296 m²) –Sanlam (960 m²) –

boundary Terraces

Highlights

Value at 30 June 2008: R130,0 million•Size: 8 205 m²•Average net rentals: R110,74/m²•Number of tenants: 10•

Located on the outskirts of the Claremont CBD, •opposite the Newlands Cricket Stadium

Major tenants:•Coronation Asset Management (3 391 m²) –Citadel Investment Services (1 348 m²) –Pinnacle Point Investments (1 326 m²) –

Woodmead office Park

Highlights

Value at 30 June 2008: R123,1 million•Size: 17 514 m²•Average net rentals: R54,67/m²•Number of tenants: 42•

Located within the Woodmead office node with •exposure to the M1 highway

Major tenants:•DB Thermal (2 755 m²) –Young & Rubicam (1 970 m²) –Regenesys (1 752 m²) –

6

7

8

9

10

4emira property fund annual report 2008

Portfolio summary

Portfolio value by sector

O�ces

Retail

Industrial

46%

36%

18%

Portfolio GLA by sector

O�ces

Retail

Industrial

37%

32%

31%

Portfolio value by region

Gauteng

Western Cape

Free State

KwaZulu-Natal

Eastern Cape73%

10%

4%

12%1%

Portfolio GLA by region

Gauteng

Western Cape

Free State

KwaZulu-Natal

Eastern Cape70%9%

5%

14%

2%

Tenant profile

42%

19%

39%Grade A

Grade B

Grade C

Tenants have been graded as follows:

“A” grade: Large national tenants, large listed

tenants, government and major franchisees.

These include, inter alia, the Department

of Labour, Edgars Consolidated Stores,

FirstRand Bank, Pepkor, Pick n Pay Stores, the

Standard Bank Group, Ster-Kinekor, Truworths

International and Virgin Active.

“B” grade: National tenants, listed tenants,

franchisees and medium to large professional

firms. These include, inter alia, Debonairs

Pizza, Fishaways, John Dory’s, Mikes Kitchen,

Rage Distribution, Torga Optical, UCS Group,

Vodacom and Wimpy.

“C” grade: Other tenants comprise all other

tenants that do not fall into the above two

categories.

emira property fund annual report 2008

5

Portfolio summarycontinued

Lease expiry profile by sector (% of GLA)

1,41,4

12,6 7,3

6,66,9 5,4

4,66,6 5,4

7,64,1 9,3

3,1 3,5 2,7

4,0

7,4

O�ces Retail Industrial

Year 5+

Year 4

Year 3

Year 2

Year 1

Vacant

Lease expiry profile (% of GLA)

Year 5+

Year 4

Year 3

Year 2

Year 1

Vacant

21,0

9,3

16,6

18,9

27,4

6,8

Lease expiry profile by sector (% of revenue)

O�ces Retail Industrial

10,5

8,8

8,2

4,2

8,7

16,5

8,4

8,4

5,2

4,2

5,4

2,8

3,1

1,5

3,9

Year 5 +

Year 4

Year 3

Year 2

Year 1

vacancy profile by sector (% of GLA)

O�ces Retail Industrial

3,1

3,8

4,0

5,6

4,4

9,8

9,8

9,0

10,7

9,6

4,5

2,6

3,1

2,8

4,0

June 2008

March 2008

December 2007

September 2007

June 2007

Weighted average lease escalation by sector (%)

8,0

9,2

9,5

Industrial

Retail

O�ces

vacancy profile (% of GLA)

5,5

6,3

6,8

5,9

5,9

December 2007

March 2008

June 2008

September 2007

June 2007

Average annualised yield achieved by the portfolio was 9,8%

6emira property fund annual report 2008

Manager’s report

The directors of Strategic Real Estate Managers (Pty) Limited (“STREM”) are pleased to present their report on Emira’s performance for the year ended 30 June 2008.

CHIEF ExECUTIvE oFFICER’S MESSAGEDuring the year, the Emira Property Fund capitalised on its portfolio of properties which is well diversified across South Africa in the office, retail and industrial markets. The Fund focused on applying its capital resources to maximising long-term growth in value and distributions through refurbishments and upgrades to strategic assets in the portfolio.

Distributions per participatory interest (“PI”) once again showed strong growth, amounting to 92,04 cents, an increase of 11,8% from the previous year. The continued demand for rental properties across all sectors resulted in healthy income growth in Emira’s portfolio, supported by double-digit upward reversions on new leases and lease renewals in the office and industrial sectors, while costs were also successfully contained.

Despite higher interest rates during the period, net asset value per PI grew by 1,9% from 1 148 cents to 1 169 cents as a result of an increase in the value of investment properties and a rise in the fair value of derivative financial instruments. Excluding the provision for deferred tax, net asset value per PI grew by 2,6% from 1 201 cents to 1 232 cents.

In line with the global contagion across equity markets, the price of Emira’s PIs on the JSE declined by 24,9% to 819 cents on 30 June 2008 from 1 090 cents the previous year, in line with the 27,7% decrease of the listed property sector. Emira’s closing price at year-end reflected a discount of 29,9% to its net asset value of 1 169 cents per PI. The PIs achieved a maximum level of 1 330 cents on 6 November 2007, and its lowest point of 806 cents on 20 June 2008. Distributions amounting to 86,59 cents were paid to PI holders during the year, which dampened the negative performance of the PIs to 17,0%.

Supply side fundamentals in the property market remained solid for the duration of the financial year despite a tighter economy and slowing growth. Vacancy rates continue to decrease across the industry, largely the result of rampant prices for serviced land and inflationary building costs which have constrained the number of new developments coming on stream.

In the retail sector, the large retail chains remain in a strong position, although smaller players started to feel the impact on lower discretionary income among consumers. GDP growth, albeit at a more muted rate in the financial year, continued to filter through to demand for increased space across the industrial and office sectors. In addition, the increased cost of development and the demand for rental properties has supported rental levels, with positive reversions on renewals persisting. Industrial and office rentals are enjoying double digit growth in rentals, while the retail sector, which had led the cycle has slowed and is showing slightly lower rental increases. Emira’s diversified portfolio of good quality properties remained well positioned during the year.

While there was an increased supply of retail, office and industrial properties for sale in the latter part of the year as a result of higher interest rates, sellers’ inflated expectations resulted in unrealistic income yield expectations. As a result, Emira’s investment focus was rather on internal opportunities to upgrade strategic properties to maximise value and enhance incremental yields.

Hurlingham Office Park, corner Republic Road and William Nicol Drive, Hurlingham

7emira property fund

annual report 2008

Manager’s reportcontinued

Emira invested a total of approximately R330 million in its property portfolio during the financial year, opting to focus on refurbishments and upgrades. Based on the Fund’s well established pool of assets, which are in good locations, Emira chose the route of adding value through reinvestments. Major refurbishments included, among others, Lake Buena Vista in Centurion; the Quagga Shopping Centre in Pretoria West and the Granada Centre in Umhlanga Rocks.

A further highlight of the year under review was Emira’s replacement of R650 million of bank-sourced debt with funds raised in the capital market. With the tangible benefit of a R2 million reduction in annual interest costs to the Fund, the move is strategically significant due to the introduction of an additional source of funding for growth. Emira now has the ability to raise capital through equity markets, traditional mortgages as well as the debt capital market, the first Property Unit Trust (“PUT”) to do so in South Africa. The Fund will therefore better be able to optimise capital raised, depending on prevailing market conditions. Based on the quality of its properties and tenants, as well as the conservative covenants in place, the income streams from the ring-fenced portfolio of 36 properties were independently rated AAA, resulting in the meaningful saving on interest charges for the debt.

PRoSPECTS ANd oUTLookEmira will continue to evaluate investment opportunities as prices in the physical market correct to reflect the underlying fundamentals. Softening property prices could deliver value adding opportunities for the Fund, especially as sellers’ expectations become more realistic. In line with the clearly defined, limited mandate from the board, the managers will also continue to appraise opportunities to invest in vacant land or buildings where returns compensate for inherent risks. As a result of the higher cost of capital and debt, the manager anticipates that earnings enhancing capital projects will be less plentiful than in 2008.

A recent change in legislation pertaining to Collective Investment Schemes in Property has permitted investments in other listed South African property funds. This could present yield enhancing investment opportunities, especially should there be continued pressure on local listed property prices.

The current financial contagion in the developed markets of Western Europe and North America is expected to result in growth in those economies slowing in 2008 and 2009. This is expected to have a lagged impact in the markets in which the fund operates. Nonetheless, growth in the South African economy, although at a more muted rate than in the past few years, continues to provide some support for rental demand, particularly in the office and commercial environments. Simultaneously, the supply side fundamentals of the property market complement Emira’s well established and diversified property portfolio with its extensive tenant base. The manager anticipates that rentals will remain relatively healthy with stable vacancies, although the retail sector could come under further pressure as a result of high interest rates, food and fuel prices. The STREM board remains confident that the Fund will continue to show strong growth in distributions for the forthcoming year ending 30 June 2009.

8emira property fund annual report 2008

Manager’s reportcontinued

1. THE SoUTH AFRICAN PRoPERTY MARkET

1.1 South African listed property sector

1.1.1 Total returns to June 2008 During the 12 months to June 2008, overall equity markets have been volatile,

with total returns of 9,8% for the JSE All Share Index and –8,9% for the JSE FINDI 30 Index.

Compound annual returns to 30 June 2008 (Pre-tax)

Period All Share FINDI 30 PLSs PUTs R 153% % % % %

1 year 9,8 (8,9) (19,1) (23,2) (3,0)

3 year 30,4 18,5 14,7 6,2 2,4

5 year 30,4 25,0 19,9 13,9 5,6

10 year 16,9 9,4 16,9 14,1 9,0

Source: Inet-Bridge

Over the same period the Property Loan Stock (“PLS”) index and Property Unit Trust (“PUT”) decreased by –19,1% and –23,2% respectively.

1.1.2 The listed property and bond yield differential Capital values on the listed property sector showed a negative

performance of (27,7%) during the 12 months ended 30 June 2008. The weakness in the sector since January 2008 wiped out all the gains made since July 2006, with the sector showing a (0,6%) return on a two year time horizon. Listed property funds, on average, showed strong double digit weighted distribution growth for the 12 months ended 30 June 2008. Despite the uncertain local economic outlook, market expectations for listed property sector distribution growth remain at double digits, albeit at slightly lower levels than in 2008.

As a result of uncertainty across financial markets, weakening bond yields and the loss of capital value in the listed property sector, both locally and internationally, the differential between the historic listed property yield and the R157 narrowed to (0,9%) at 30 June 2008, from (2,4%) in July 2007. This weakness suggests that the market is discounting slightly slower growth in listed property distributions as tighter economic conditions take effect.

1.2 South African physical property market The weakness in equity markets and the listed property sector did

not materially filter through to the physical property market due to strong supply side fundamentals and increasing demand for

space. While the retail sector has felt some pressure from the impact of higher interest rates and inflation on consumers, the economy

continues to show growth which is supporting the physical office and industrial markets. The scarcity of vacant serviced land and inflationary pressures on building costs continue to translate into demand for rental space.

Listed property index

150

200

250

300

350

400

450

Apr 2008Jan 2008Oct 2007Jul 2007Apr 2007Jan 2007Oct 2006Jul 2006

Source: Inet-Bridge

The R 157 and the property yield differential

-3%-2%-1%0%1%2%3%4%5%6%

6%7%8%9%10%11%12%13%14%15%

200820072006200520042003200220012000

Di�erential Long bond (R 157)

Source: Inet-Bridge

9emira property fund

annual report 2008

Manager’s reportcontinued

The Investment Property Databank’s (IPD) South Africa Annual Property Index, which measures ungeared total returns to direct property investments, showed a return of 27,7% in 2007, slightly ahead of the 2006 overall property return of 27,1%.

The performance in 2007 reflected the second highest annual return since the index was initiated in 1995. These returns consisted of strong capital growth of 17,7%, from 16,5% in 2006. Net income growth of 17,6% was reported, the highest since 1997. The sharp capital growth resulted in lower net income yields of 7,6% at year-end.

For the second consecutive year, the industrial property sector led the pack with a return of 33,6%, from 31,4% in 2006. The office sector delivered increased returns of 30,8% in 2007 from 25,0% the previous year, while higher interest rates and oil prices impacting consumer demand started to filter into the retail sector whose return slowed to 26,0% from 27,7% a year earlier.

Across all sectors of the property market, income returns continued to trend downwards during 2007, due to the continued high levels of underlying capital growth in property values.

IPD total returns for 2007

Total return

%

Income return(2006)

%

Capital growth(2006)

%

All property 27,7 (27,1) 8,6 (9,2) 17,7 (16,5)

Retail 26,0 (27,7) 8,0 (8,4) 16,8 (17,9)

Offices 30,8 (25,0) 9,6 (10,3) 19,5 (13,4)

Industrial 33,6 (31,4) 10,3 (10,9) 21,3 (18,7)

Other 25,0 (21,9) 10,3 (10,3) 13,5 (10,6)

Source: IPD

Total returns % annualised

PeriodRetail

%Offices

%Industrial

%All property

%

1 year 26,0 30,8 33,6 27,7

3 year 28,8 27,0 32,5 28,3

5 year 25,9 21,0 27,8 24,6

10 year 18,9 13,9 16,8 17,0

13 years 18,9 13,5 16,6 16,7

Source: IPD

Vacancy rates across the property market continued to trend downwards as a result of increasing demand. Overall vacancies reached a low point of 3,1% at the end of 2007 from 4,5% in 2006 and the high of 12,8% in 2002.

From a global perspective, the higher total returns in South Africa in 2007 were in line with current trends in Australia, New Zealand, South Korea and several European countries. Despite these higher returns, South African income yields exceed the global average.

Quagga Centre, cnr Church Street and West Street, Pretoria West

10emira property fund annual report 2008

Manager’s reportcontinued

2. EMIRA’S PERFoRMANCE ANd PRoPERTY PoRTFoLIo

2.1 Emira’s performance and tradeability on the jSE In line with the weakness across both the local and international listed property

markets, during the year ended 30 June 2008, the price of Emira’s PIs declined by 24,9% from 1 090 cents to 819 cents at the end of the period. Total distributions paid during the year, amounting to 86,59 cents, dampened the negative return by 7,9% to 17,0%.

142,7 million PIs traded during the year ended 30 June 2008, representing 29% of the weighted average number of PIs in issue.

2.2 Performance relative to the IPd index According to the 2007 IPD index, which aggregates the capital and income of

listed and unlisted portfolios to provide a measure of total annual performance, Emira achieved a return of 38,9%, representing the third consecutive year for which the Fund has delivered returns in excess of 38%. This reflects a significant outperformance on the 26,9% and 26,7% increase recorded by the IPD South Africa Listed Funds Benchmark and the IPD Universe respectively.

Emira traded at a higher income return of 9,1% compared to its listed benchmark. In addition, the Fund’s capital growth of 27,6% exceeded the listed benchmark’s measure of 17,0% for 2007.

2.3 Portfolio exposure In line with Emira’s strategic objectives to maintain a balanced exposure to retail,

office and industrial properties and to optimise net income and growth in distributions, the assets in the Fund’s portfolio are of a high quality and continue to meet its objectives to deliver sustainable growth in income and to diversify risk. The broad geographic footprint of the portfolio with its base of more than 4 000 tenants provides the Fund with further diversification benefits.

At 30 June 2008, Emira’s property consisted of 164 properties, with a total GLA of 1 188 367 m2, which was valued at R7,5 billion, translating into an average value of R45,7 million per property.

Management is committed to continuously increasing Emira’s investor appeal, and consequently its market capitalisation and liquidity by growing the property portfolio. Maximising returns necessitates active management of the portfolio, acquiring new properties which meet the investment criteria and reinvesting to add value to core properties, while disposing of non-performing or potentially under-performing properties. Five properties were disposed of and transferred out of the Fund during the year for a total consideration of R170,5 million, representing a forward exit yield of 6,5% and a premium of 71% to book value. The Fund has also reached agreement to dispose of a further two non-core properties, one of which has been transferred subsequent to year-end, while the other transaction is still suspensive on certain conditions. Acquisitions totalling R97,1 million in respect of three properties were completed at an average income yield of 9,5%. In addition, total refurbishments of R231,8 million were completed on ten properties at a yield of 11,4% during the year. The board has approved further investments of R75,8 million at an estimated yield of 9,3%.

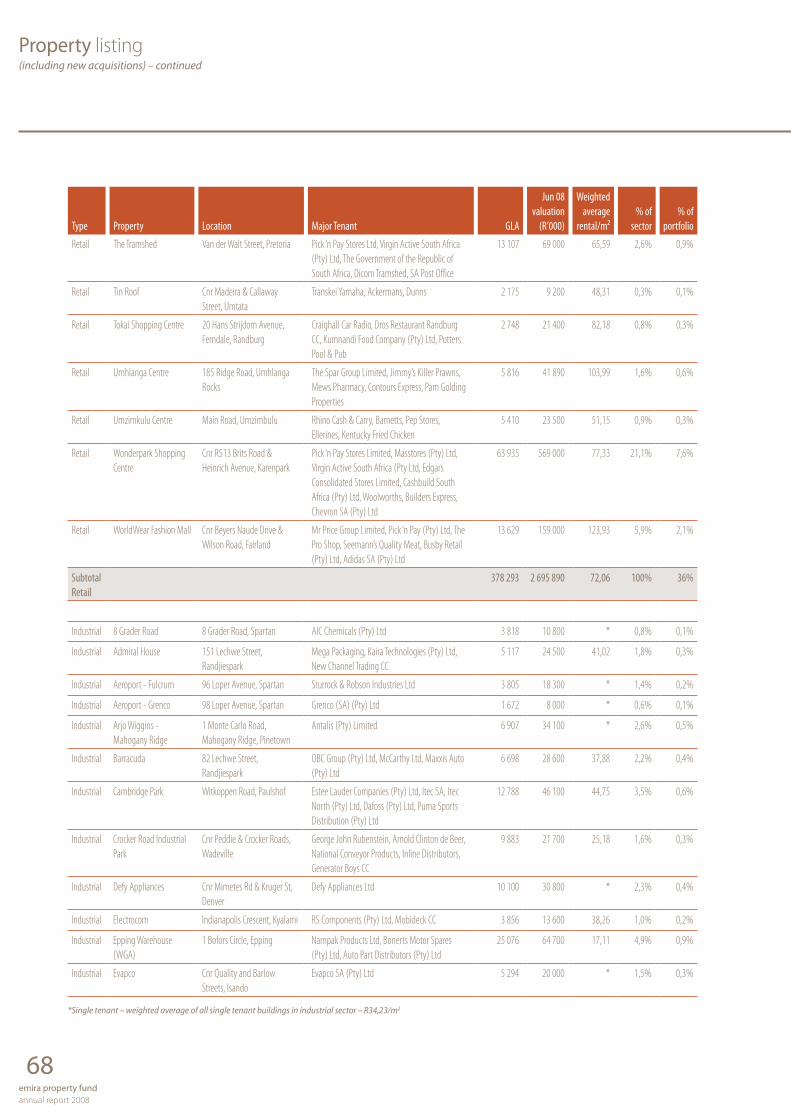

A detailed breakdown of Emira Property Fund’s portfolio is disclosed on page 62.

Knightsbridge Manor, 33 Sloane Street, Bryanston

11emira property fund

annual report 2008

Manager’s reportcontinued

3. oFFICE PoRTFoLIo

3.1 Market conditions The IPD reported that the office sector, which traditionally

lags retail and industrial performance, showed a total return of 30,8% in 2007, underpinned by record levels of capital growth, at 19,5%.

Increased cyclical output in both financial and business sectors of the economy continues to underpin the performance of the office rental market, driven by expansion of existing companies and demand from new entities for office space. Notably, office vacancy rates, at 5,4% for 2007, were at their lowest levels since the late 1990s and their peak of 23% in 2002. Higher demand was experienced for A-grade office space with vacancy levels below 4,0% in 2007.

In contrast, new office space has been slow in coming onstream despite strong economic demand. Scarcity of vacant land, delays in obtaining regulatory approvals and inflating building costs are impacting decisions to embark on new construction projects.

Developments are concentrated in nodes including Sandton, Centurion, Midrand, Woodmead, Melrose/Waverley, Umhlanga/La Lucia, Highveld Technopark and Pretoria East. Recent years have seen offices outside of Gauteng, Western Cape and KwaZulu-Natal producing very strong returns.

The approval of increased bulk rights close to prospective Gautrain stations is resulting in extensive redevelopment and upgrade opportunities for office developments in Sandton, Rosebank and Centurion.

3.1.1 SAPOA office vacancies and development SAPOA office vacancies continued to show a declining trend, dropping from

6,2% or 778 795 m2 in June 2007 to 4,9% or 642 542 m2 in June 2008.

3.2 Emira’s portfolio

3.2.1 Exposure At 30 June 2008, Emira’s office portfolio was valued at R3,5 billion and comprised

46% of the Fund’s total investment properties by value. The Fund owns 73 office buildings, with total GLA of 444 676 m2 and an average value of R47,5 million.

office vacancy rates and net income growth

-6%

0%

6%

12%

18%

24%

30%

-3%

0%

3%

6%

9%

12%

15%

20072004200119981995

2,5 3,0

10,2

14,016,9

18,8

23,622,2

17,0

7,710,6

5,4

O�ce vacancy rates Net income growth

11,3

Source: IPD

office vacancy rates and total new development

0

200 000

400 000

600 000

800 000

1 000 000m2

0%

3%

6%

9%

12%

15%

2008200720062005200420032002

Total development Total vacancies

Source: SAPOA

12emira property fund annual report 2008

Manager’s reportcontinued

Emira’s office portfolio comprises the following grades of property, with the majority being B-grade office space.

GradeNumber of

buildings GLA (m2)

A-grade 25 154 816

B-grade 44 259 267

C-grade 4 27 991

Because of sellers demanding low asking yields on office properties, Emira focused on upgrading and refurbishing several properties in its portfolio during the year in order to add value while realising higher incremental returns.

The development of Faerie Glen Phase 4 was completed in December 2007 for a total consideration of R29,9 million, implying a forward yield of 10,1%. The Faerie Glen Office Park now comprises a GLA of 10 324 m2 and was independently valued at R124,5 million.

Major refurbishments with total investments of R62,8 million completed during the financial year included:

Refurbishment and upgrade of foyers, bathrooms and park aesthetics at the •Hurlingham Office Park; Refurbishment and upgrade of foyers, bathrooms and park aesthetics at the •Knightsbridge Office Park; and Lake Buena Vista (see detailed case study below).•

3.2.2 Vacancies and letting Emira’s office vacancies increased to 10,7% at 30 June 2008 compared to 9,8% in

June 2007, mainly as a result of ongoing refurbishments to ensure sustainable future income streams and enhance income yields associated with several properties.

Major office vacancies include:

On completion of the major upgrade at Lake Buena Vista (GLA 6 894 m• 2) (see case study below), Momentum Short Term Insurance commenced its five-year lease on the entire property in July 2008. Due to the continuing refurbishments at Hurlingham Office Park (GLA •15 430 m2), vacancy levels were at 6 341 m2 in June 2008 of which 5 300 m2 is situated in the recently refurbished blocks which are now available for letting.Letting has been put on hold at the FNB Building (GLA 6 745 m• 2) while aspects relating to a potential refurbishment are approved by the various authorities, as a result, vacancies as at 30 June 2008 were 3 599 m2.

> CASE STUDY: Lake Buena Vista – Capitalising on location to attract top class tenant

Lake Buena Vista was a B-grade building with five floors of offices and two levels of basement parking with a total GLA of 5 735 m2. It is well-positioned in the heart of Centurion fronting on to the Centurion Lake in Pretoria and is in close proximity to the Centurion Mall. Within walking distance of the site for the Centurion Gautrain Station, Lake Buena Vista will enjoy further benefits once the Gautrain becomes operational in 2010.

Lake Buena Vista, Gordon Hood Avenue, Centurion

13emira property fund

annual report 2008

Manager’s reportcontinued

The previous anchor tenant of the property vacated the premises in April 2007 and Emira was faced with the decision of whether to refurbish the building or let it at a lower rental in its existing condition. No significant improvements had been made to the property since August 2003.

Investigations indicated that with an investment of approximately R30 million, the building could be upgraded to A-grade offices and that by adding parking and other improvements would attract a better quality tenant with the benefit of improved rental rates. While SAPOA statistics indicated a shortage of A-grade offices in the area, an excess supply of B-grade office space existed which strengthened Emira’s case for the investment. Based on the merits of the proposed upgrade and its potential to attract blue-chip tenants, the board of Emira approved the project on risk, that is, without a tenant in hand.

The upgrade, completed in July 2008, increased the total rentable area by 20,2% to 6 894 m2 by converting various balconies to office space and reducing the ratio of common space relative to the usable space of the building. In addition, the parking ratio was improved from 2,3 bays per 100 m2 to 4,4 bays per 100 m2 by converting the ground floor to parking. Double digit incremental returns on the investment were attributable to the combined impact of the office grade enhancement and the increased rentable area. On completion of the upgrade, Emira successfully concluded a five-year lease with Momentum Short Term Insurance for the entire building.

4. RETAIL PoRTFoLIo

4.1 Market conditions Although the retail sector, which generally leads the commercial

property cycle, experienced strong total returns of 26,0% in 2007, these are in a downward trend.

During 2007, the retail sector was particularly influenced by higher interest rates and the introduction of the National Credit Act. Rampant food and fuel prices had a further dampening effect on discretionary income since the beginning of 2008, with retail sales consistently trending down since the beginning of 2007.

Despite this, net income growth for 2007 remained above inflation, supported by decreasing vacancies which reached their lowest levels in 10 years. Vacancy rates for 2007 were 2,3%, equalling levels last seen in 1997.

4.2 Emira’s portfolio

4.2.1 Exposure At 30 June 2008, Emira’s retail portfolio was valued at R2,7 billion and

comprised 36% of the Fund’s total investment properties by value. The Fund owns 41 shopping centres, with total GLA of 378 293 m2 and an average value of R65,8 million.

Retail vacancy rates and net income growth

0%

1%

2%

3%

4%

5%

6%

7%

-5%

0%

5%

10%

15%

20%

25%

20072004200119981995

2,32,9

4,3

5,2

6,25,9

6,5

4,6

3,83,5

2,3

0,60,4

Retail vacancy rates Net income growth

Source: IPD

14emira property fund annual report 2008

Manager’s reportcontinued

Investments made by Emira in its retail portfolio during the year, were focused on improvements rather than the acquisition of new properties, due to purchase prices remaining inflated.

The Fund invested R26,3 million in one completely new development, namely the Wonderpark Builder’s Express with a total GLA of 3 948 m2. It was completed in May 2008 and is located on the same site as the Wonderpark Shopping Centre, north of Pretoria.

Major refurbishments and extensions with total value of R148,5 million were completed during the financial year:

Property LocationValue(Rm) Completion date

Tramshed Pick n Pay Pretoria CBD 10,4 November 2007

Wonderpark Caltex refurbishment Akasia, Pretoria North 6,8 February 2008

Lynnridge Mall Extension

Lynnwood Ridge, Pretoria 17,5 May 2008

Wonderpark upgrade for major tenants Akasia, Pretoria North 9,6 May 2008

Quagga Extensions Pretoria West 91,9 June 2008

Epsom Downs Shopping Centre

William Nicol, Bryanston 11,3 June 2008

4.2.2 Vacancies and letting Emira’s retail vacancies increased to 4,4% at 30 June 2008 compared to 3,1% in

June 2007, as a result of increased refurbishments in progress at year-end.

Major retail vacancies include:

Ongoing construction at the Granada Centre in Umhlanga Rocks (GLA 5 818 m• 2) with completion due in March 2009. Vacancies of 1 301 m• 2 at the WorldWear Fashion Mall (GLA 13 629 m2) resulted during the remodelling and relocation of smaller tenants to accommodate the larger tenancy of Pick n Pay. Vacancies at the Quagga Shopping Centre (GLA 29 748 m• 2) in Pretoria decreased to 969 m2 as the extensions reached completion.

> CASE STUDY: Wonderpark Shopping Centre – Incremental investment to secure blue-chip retailers

Wonderpark Shopping Centre is located in the suburb of Akasia in Pretoria North and services the nodes of Akasia, Soshanguve and Rosslyn.

The centre is the largest property, both by value and GLA, in Emira Property Fund’s portfolio. It was acquired in September 2006, on completion of a significant redevelopment completed by Momentum in 2005. The upgrade entailed increasing the GLA from 36 564 m2 to 59 702 m2 which enabled the total number of tenants at the centre to increase from 68 to 135.

Wonderpark Shopping Centre, corner Brits Road and Heinrich Avenue, Karenpark

15emira property fund

annual report 2008

Manager’s reportcontinued

In June 2007, the Fund was approached by Mr Price Sports to open a store at the centre. At the same time national retailing chains Truworths, Markham and Foschini, requested extensions to their existing stores while increasing their brand exposure in the centre. The long-term benefits included enhancing the appeal of Wonderpark Shopping Centre among consumers.

On evaluation of the opportunity, Emira concluded that with a relatively small investment of R10,0 million for the extensions totalling 3 143 m2, a double digit incremental return would be achieved. In addition, the increased rental income from these national tenants would enhance the quality of the Fund’s income stream.

In addition to the extensions for these national tenants, several smaller stores were relocated to facilitate the upgrade. The extensions were completed in May 2008, with the tangible benefits of these investments including longer term leases to higher quality tenants which will also improve foot traffic.

5. INdUSTRIAL PoRTFoLIo

5.1 Market conditions SAPOA reported that the industrial sector produced the highest

property returns in 2007, with a total return of 33,6%, underpinned by capital growth of 21,3%.

The significant increase in retail sales which brought about greater demand for warehousing and distribution space, as well as increased activity in the manufacturing sector supported the sector’s performance. Income growth remained solid during 2007, as a result of the continued shortage of industrial developments to meet economic demand for both distribution and the manufacturing sector.

Underlying property fundamentals continue to support the industrial sector with vacancies at 2,2%, a ten year low. At the same time, record gross rentals and net income rates per m2 have been reported by IPD.

In 2007 industrial warehouses once again produced the highest returns of the industrial sector at 35,9%. This was followed by high tech industrials and standard industrial units. Light manufacturing lagged the other property types.

5.2 Emira’s portfolio

5.2.1 Exposure At 30 June 2008, Emira’s industrial portfolio was valued at R1,3 billion and

comprised 18% of the Fund’s total investment properties by value. The Fund owns 50 industrial properties, with total GLA of 365 397 m2 and an average value of R26,6 million.

Industrial vacancy rates and net income growth

0%

2%

4%

6%

8%

10%

12%

14%

-6%

-3%

0%

3%

6%

9%

12%

15%

20072004200119981995

5,3

7,9

9,6

10,9

12,3

10,4

6,5

2,63,3

2,23,1

0,70,4

Industrial vacancy rates Net income growth

Source: IPD

16emira property fund annual report 2008

Manager’s reportcontinued

5.2.2 Vacancies and letting Emira’s industrial vacancies increased to 4,5% at 30 June 2008.

Major industrial vacancies include:

Goodyear Tycon (GLA 5 870 m• 2) which was vacated by the single tenant on expiry and negotiations are continuing with prospective tenants to let this space;One Highveld (GLA 6 012 m• 2) is an industrial property with a relatively high proportion of office space which accounts for 1 400 m2 of the total vacancy of 1 815 m2; andCambridge Park (GLA 12 788 m• 2) 1 528 m2 became fully let to Puma from July 2008.

> CASE STUDY: Fuel Group Acsa Park– Using additional bulk rights to maximise return potential

The Fuel Group Acsa Park, located adjacent to the OR Tambo International Airport, was a new development acquired from RMB Properties by Emira in May 2006 for a consideration of R215,3 million. With its GLA of 46 673 m2, it makes up 12,8% of the Fund’s industrial portfolio and constitutes its largest industrial property by GLA.

The building serves as the Fuel Group’s Head Office and the main Gauteng distribution facility of its subsidiary company, RTT.

Fuel Group subsequently secured an extensive distribution agreement for Continental Tyres, and set about finding a suitable location for the additional distribution centre.

At the same time, Emira viewed this as an opportunity to maximise its development on the Fuel Group Acsa Park property, using the available bulk to meet the increased requirements of its existing tenant.

The STREM board approved the development of a second phase to accommodate the Fuel Group’s increased requirements at a total cost of R41,0 million. The project was completed in November 2007 and resulted in the development on the site increasing to a total GLA of 59 594 m2.

By fully utilising the bulk rights, and erecting the additional buildings, Emira achieved an incremental return of 10,1% on the additional invested capital.

6. ACQUISITIoNS ANd CAPITAL PRojECTS Acquisitions and capital projects totalling approximately R330 million were

concluded during the year. Emira focused on upgrading and refurbishing a number of properties as this enabled the Fund to add value and enhance incremental yields in excess of what could be achieved on acquisitions of additional properties. Capital investments were funded by a combination of equity and debt.

Fuel Group Acsa Park, cnr Springbok and Jones Street, Bardene

17emira property fund

annual report 2008

Manager’s reportcontinued

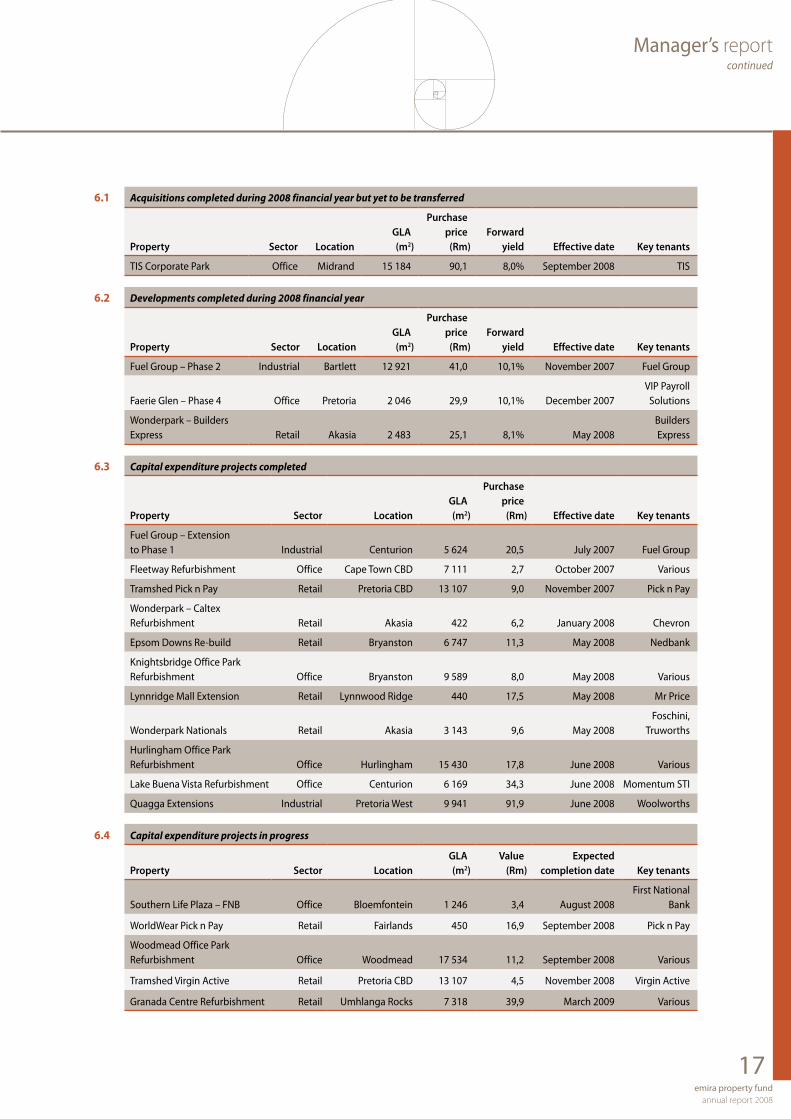

6.1 Acquisitions completed during 2008 financial year but yet to be transferred

Property Sector LocationGLA(m2)

Purchaseprice

(Rm)Forward

yield Effective date Key tenants

TIS Corporate Park Office Midrand 15 184 90,1 8,0% September 2008 TIS

6.2 Developments completed during 2008 financial year

Property Sector LocationGLA(m2)

Purchaseprice

(Rm)Forward

yield Effective date Key tenants

Fuel Group – Phase 2 Industrial Bartlett 12 921 41,0 10,1% November 2007 Fuel Group

Faerie Glen – Phase 4 Office Pretoria 2 046 29,9 10,1% December 2007VIP Payroll

Solutions

Wonderpark – Builders Express Retail Akasia 2 483 25,1 8,1% May 2008

Builders Express

6.3 Capital expenditure projects completed

Property Sector LocationGLA(m2)

Purchaseprice

(Rm) Effective date Key tenants

Fuel Group – Extension to Phase 1 Industrial Centurion 5 624 20,5 July 2007 Fuel Group

Fleetway Refurbishment Office Cape Town CBD 7 111 2,7 October 2007 Various

Tramshed Pick n Pay Retail Pretoria CBD 13 107 9,0 November 2007 Pick n Pay

Wonderpark – Caltex Refurbishment Retail Akasia 422 6,2 January 2008 Chevron

Epsom Downs Re-build Retail Bryanston 6 747 11,3 May 2008 Nedbank

Knightsbridge Office Park Refurbishment Office Bryanston 9 589 8,0 May 2008 Various

Lynnridge Mall Extension Retail Lynnwood Ridge 440 17,5 May 2008 Mr Price

Wonderpark Nationals Retail Akasia 3 143 9,6 May 2008Foschini,

Truworths

Hurlingham Office Park Refurbishment Office Hurlingham 15 430 17,8 June 2008 Various

Lake Buena Vista Refurbishment Office Centurion 6 169 34,3 June 2008 Momentum STI

Quagga Extensions Industrial Pretoria West 9 941 91,9 June 2008 Woolworths

6.4 Capital expenditure projects in progress

Property Sector LocationGLA(m2)

Value(Rm)

Expected completion date Key tenants

Southern Life Plaza – FNB Office Bloemfontein 1 246 3,4 August 2008First National

Bank

WorldWear Pick n Pay Retail Fairlands 450 16,9 September 2008 Pick n Pay

Woodmead Office Park Refurbishment Office Woodmead 17 534 11,2 September 2008 Various

Tramshed Virgin Active Retail Pretoria CBD 13 107 4,5 November 2008 Virgin Active

Granada Centre Refurbishment Retail Umhlanga Rocks 7 318 39,9 March 2009 Various

18emira property fund annual report 2008

Manager’s reportcontinued

7. dISPoSALS Two properties which were considered non-core were sold during the year under

review, but were awaiting transfer at year-end. Kuehne & Nagel was transferred on 15 July 2008 and Barvic House on 30 September 2008.

7.1 Awaiting transfer out of Emira

Property Sector Location GLA (m2)

Valuation on30 December

2007 (Rm)Sale price

(Rm)Yield

(%)

Barvic House Office Randburg, Gauteng 3 322 11,3 10,1 5,2

Kuehne & Nagel Office Berea, Durban 2 140 5,3 8,8 10,4

In addition, five properties which were sold in the previous financial year were transferred out of Emira during the year ended 30 June 2008. The proceeds received from disposals were used to fund capital expenditure and repay debt.

7.2 Transferred out of Emira in 2008 financial year

Property Sector Location GLA (m2)

Valuation on30 December

2006 (Rm)Sale price

(Rm)Yield

(%)

Contact Centre OfficesParktown,

Johannesburg 1 184 6,9 9,0 6,4

Inspectorate OfficesOrmonde,

Johannesburg 2 704 6,2 7,3 9,3

11 Park Lane OfficesParktown,

Johannesburg 3 676 16,4 20,5 7,4

Fourways Game Retail Fourways, Sandton 8 000 58,1 119,7 6,0

Wierda Gables Offices Sandown, Sandton 2 007 11,9 14,0 8,0

* The valuations as at December 2006 have been used to reflect the premium to book value

realised by the Fund on disposal. Valuations as at June 2007 reflected the disposal prices and

therefore no premium to book value would have been evident.

Management continually evaluates properties to ensure that the portfolio is optimised, and buildings are disposed of where these investments are found to fall outside Emira’s investment criteria, risk profile and return requirements.

8. vALUATIoNS ANd NET ASSET vALUE The Fund has elected to have independent valuations of its entire portfolio at

least every three years. To achieve this, independent valuers value approximately one-third of the portfolio each year. These valuations are included as part of the Fund’s overall portfolio movement below.

As a result of advantageous renewals and rising rentals in the office and industrial portfolios, property values rose in both sectors. In contrast, retail properties experienced a mixed performance. The Fund’s smaller properties in outlying areas continued to benefit from good rental growth, the capital expenditure at several of the centres was value enhancing, however, certain of the neighbourhood and convenience centres were impacted by the deteriorating retail conditions.

19emira property fund

annual report 2008

Manager’s reportcontinued

8.1 Total portfolio movement

June 2007 June 2008 Difference Difference

Sector (R’000) R/m2 (R’000) R/m2 (%) (R’000)

Offices 3 317 664 7 409 3 467 316 7 864 4,5 149 652

Retail 2 784 378 7 433 2 695 890 7 126 (3,2) (88 488)

Industrial 1 212 700 3 414 1 328 230 3 635 9,5 115 530

Total 7 314 742 7 491 436 176 694

Net asset value grew from 1 148 cents to 1 169 cents (1 232 cents excluding the deferred tax provision), representing growth of 1,9%. This is the result of growth in the value of the portfolio, as well as gains in the fair value of derivatives.

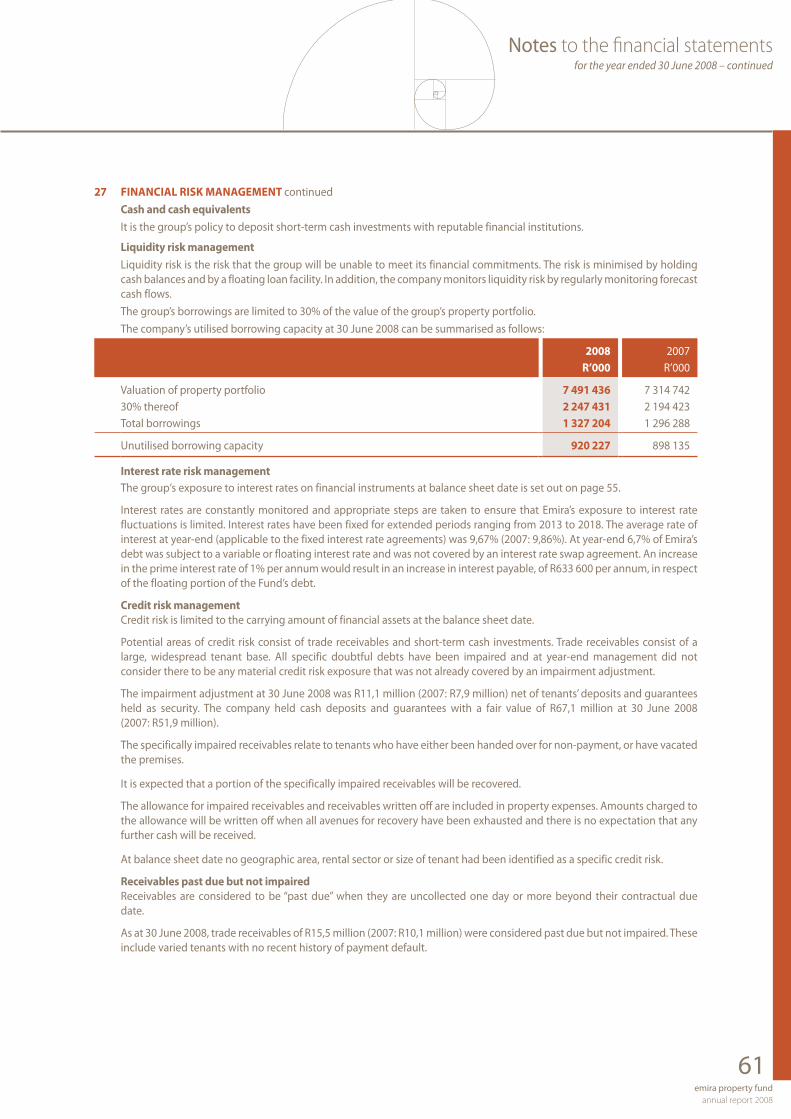

9. GEARING Emira engaged FirstRand Bank Limited to assist the Fund in accessing the debt capital

markets, thereby reducing its overall cost of funding.

On 28 March 2008, the Fund undertook a commercial mortgage backed securitisation (“CMBS”), whereby it issued five-year notes to Rand Merchant Bank (“RMB”) amounting to R650 million. The proceeds received were used to repay existing loans received from RMB. The securitisation enabled the Fund to reduce the margin payable on these loans from 125 basis points to 93 basis points (including amortised securitisation costs). The notes attract interest at the three-month JIBAR rate. Existing interest rate swaps that were already in place prior to the securitisation have been novated to RMB which has resulted in an average all in fixed rate of 9,78% on this loan. These interest rate swaps revert back to Emira in April 2013, whereafter they will continue until their expiry dates. The weighted average cost of the entire debt of the Fund at 30 June 2008, is 9,67%, as per below.

9.1 Rate % TermAmount

(Rm)%

of debt

1. Debt – Fixed 10,21 November 2008 100,0 7,5 – Swap 9,38 December 2014 — —

2. Preference shares – Floating 10,91* January 2012 90,0 6,7

3. Debt – Swap 9,78 April 2013 650,0 48,5

4. Debt – Swap 9,20 June 2013 500,0 37,3

Total 9,67 1 340,0 100,0

Less: Costs capitalised not yet amortised (12,8)

Per balance sheet 1 327,2

*Using a prime rate of 15,5% per annum.

As at 30 June 2008, 93,3% of the Fund’s debt was fixed by way of interest rate swap agreements.

The Fund had a total debt facility of R1,8 billion as at 30 June 2008. Based on total assets of R7,8 billion at 30 June 2008, Emira could increase its gearing levels to a maximum of R4,7 billion, compared to R1,3 billion or 17% at year-end.

During the first half of 2008, amendments to the Collective Investment Schemes Control Act effectively increased the gearing limits on property unit trusts from 30% to 60%.

emira property fund annual report 2008

20

Directorate

dIRECToRS oF THE MANAGEMENT CoMPANY, STRATEGIC REAL ESTATE MANAGERS (PTY) LIMITEd (STREM)

1. benedict james van der Ross (61)

(Non-executive Chairman)

Qualifications: Dip Law

Occupation: Company Director

Mr Van der Ross was admitted to the Cape Bar as attorney in 1970 and practised law for his own account until 1988. He has served as director of various companies including Executive Director for the Urban Foundation and Independent Development Trust.

He was appointed Commissioner to the First Independent Electoral Commission by the State President on the advice of the Transitional Executive Council and subsequently served as Deputy Chief Executive Officer of the Independent Development Trust and acting Chief Executive Officer of South African Rail Commuter Corporation.

He currently serves on a number of boards including those of FirstRand, Naspers, Momentum Group, and is the Chairman of RMB Asset Management.

2. Warren kirkwood Schultze (48)

(Executive Director)

Qualifications: BCom, BAcc, CA (SA)

Occupation: Chief Executive Officer of Eris Property Group (previously RMB Properties)

Prior to joining RMB Properties, Mr Schultze served his articles with Arthur Young and was later appointed Financial Director for two property financing and property trading companies. During this time he gained extensive experience in property asset management, property financing and property trading activities.

He was appointed Chief Operating Officer of RMB Properties in 2000 and Chief Executive Officer in 2004. He was appointed Chief Executive Officer of Eris Property Group on 1 April 2008.

3. james William Andrew Templeton (35)

(Chief Executive Officer)

Qualifications: BCom (Hons), CFA

Occupation: Chief Executive Officer of Strategic Real Estate Managers (Pty) Ltd

Mr Templeton joined RMB Properties in April 2004 as Business Development Executive. Previously he was employed at Barnard Jacobs Mellet Securities as an Equities Analyst for seven years.

He was the top-ranked analyst in the Real Estate sector according to the Financial Mail in 2002 and 2003 and was appointed CEO of STREM in July 2004. Mr Templeton currently also serves as the Deputy Chairman of the Association of the Property Unit Trusts.

emira property fund annual report 2008

21

Directoratecontinued

4. Peter john Thurling (53)

(Chief Financial Officer)

Qualifications: BCom, BAcc, CA (SA)

Occupation: Chief Financial Officer of Strategic Real Estate Managers (Pty) Ltd

Mr Thurling, a chartered accountant with over 20 years’ experience in the property industry, in particular with listed property vehicles. Previously he was the Financial Director of Corovest Property Group and the Chief Financial Officer of Freestone Property Holdings Limited.

5. Michael Simpson Aitken (51)

(Non-executive Director)

Qualifications: BA, LLB

Occupation: Director

Over 20 years’ experience in property-related activity, with specific expertise in asset and fund management related to directly-held and listed property vehicles. He was previously an Executive Director of Freestone Property Holdings Limited. Currently Managing Director of Corovest Property Group and the non-executive Chairman of Hyprop Investments Limited.

6. Liliane Sylvie barnard (43)

(Independent Non-executive Director)

Qualifications: BCom

Occupation: Consultant

Ms Barnard has 20 years’ experience in the asset management industry. She headed the asset management of Old Mutual Properties (Pty) Ltd and has 11 years experience in managing listed property portfolios for Old Mutual Asset Managers (Pty) Ltd. She is now an independent consultant to the listed property industry and its investors.

She is also an independent non-executive director of Redefine Income Fund.

7. bryan Hugh kent (63)

(Independent Non-executive Director)

Qualifications: BCom, FCMA, CA(SA)

Occupation: Director

Mr Kent was previously a partner at Pricewaterhouse. He is presently a financial business consultant with considerable experience in property matters and financial structuring. He was also previously a non-executive director of Freestone Property Holdings Limited and chairman of its audit and risk committee.

He is currently a non-executive director of Set Point Technology Holdings Limited and non-executive director of Cadiz Holdings Limited and CIC Holdings Limited (Namibia).

He is Chairman of Country Bird Holdings which was recently listed on the JSE.

emira property fund annual report 2008

22

Directoratecontinued

8. Nocawe Eustacia Makiwane (49)

(Non-executive Director)

Qualifications: BSocScience (UCT), BA (Hons) Economics (Wits), Executive Leadership Programme (Wharton Business School), MBA (University of Exeter)

Occupation: Managing Director of Avuka Investments

Ms Makiwane has served on the boards of Sentech, National Electricity Regulator and Blitec, a 100% black-owned IT company. Currently she serves as a non-executive director of National Housing Finance Corporation (“NHFC”), a parastatal specialising in whole financing for low-income housing and Rural Housing Loan Fund, a section 21 company focusing on facilitating housing and finance to rural communities in South Africa.

9. Matthys Stefanus benjamin Neser (51)

(Independent Non-executive Director)

Qualifications: BSc (Building Management), MBA

Occupation: Director

Mr Neser has been involved with the Abcon group of companies since 1981 and has acted as Chief Executive Officer for the various companies in the group since the early 1990s. He is active in the residential and commercial property field as well as in other business ventures.

10. Nkululeko Leonard Sowazi (44)

(Non-executive Director)

Qualifications: MA Planning (UCLA)

Occupation: Deputy Chairman of the Tiso Group

Mr Sowazi is the founding deputy Chairman of the Tiso Group, a black empowerment investment company with interests in natural resources, industrial services and investment banking. He is currently a member of the boards of JSE listed Exxaro Resources, Aveng Limited and is a non-executive director of the boards of Grinaker-LTA, Trident Steel (Pty) Ltd, African Explosives Limited, Alstom SA and Improchem. He is also Chairman of Idwala Industrial Holdings, The Home Loan Guarantee Company and the Financial Markets Trust.

Mr Sowazi was previously Executive Deputy Chairman of African Bank Investments Limited and prior to that Managing Director of the Mortgage Indemnity Fund (Pty) Ltd. He also served on the board of Kagiso Trust Investment Company, Kagiso Media and Development Bank of South Africa.

23emira property fund

annual report 2008

Corporate governance

INTRodUCTIoNThe directors of STREM acknowledge the importance of the principles of good corporate governance and support the Code of Corporate Practices and Conduct contained in the King II report and recognise their responsibility in conducting the affairs of Emira with integrity, openness and accountability in accordance with generally accepted corporate practices.

Although Emira is listed on the JSE Limited (“JSE”) and is therefore subject to the code, it is not a legal entity and is regulated in terms of the Collective Investments Schemes Control Act of 2002 (“CISC Act”). Certain requirements of the code are therefore not directly applicable to the Fund. However, the Managers have adopted the principles of the code, being fairness, accountability, responsibility and transparency.

The Fund has complied with the code, where applicable and to the following extent:

THE boARd oF dIRECToRS

StructureAs at 30 June 2008 the board consisted of ten members:

Director Date appointed

Board of directorsnumber of meetings/

attendance

Audit committeenumber of meetings/

attendance

Executive directors

JWA Templeton* (CEO) July 2004 9/9 4/4

WK Schultze* September 2003 9/9 4/4

PJ Thurling (CFO) April 2007 9/8

Non-executive directors

BJ van der Ross*† (Chairman) September 2003 9/7 4/4

MS Aitken April 2007 9/8

LS Barnard† September 2003 9/8

BH Kent** April 2007 9/8 4/3

NE Makiwane* August 2006 9/9 4/4

MSB Neser September 2003 9/8

NL Sowazi August 2006 9/7

* Audit committee** Audit committee chairman† Remuneration committee

The capacity of the directors may be categorised as follows:Executive directors: Messrs JWA Templeton and PJ Thurling are employed by STREM, and remunerated out of the service charge payable by the Fund to STREM. Mr WK Schultze is employed by Eris Property Group.

Non-executive directors: Mr BJ van der Ross is a director of FirstRand Limited and Momentum Group Limited. Mr MS Aitken is employed by Corovest Property Group Holdings (Pty) Limited. Mr NL Sowazi and Ms NE Makiwane represent Emira’s BEE partners.

Independent non-executive directors: Messrs BH Kent, MSB Neser and Ms LS Barnard are not significant holders of Emira participatory interests, as defined in the Code.

The roles of Chairman and Chief Executive Officer are completely separated. The directors have a wide range of skills. The directors of STREM are appointed at the discretion of STREM shareholders.

The board schedules to meet at least four times per year. In addition, eleven asset performance committee meetings were held during the year and were attended by the executive members of the board.

All directors have unrestricted access to the advice and services of the Fund’s secretary and to the Fund’s records, information, documents and property. Non-executive directors also have unfettered access to management at any time. The fund is in the process of developing and implementing a formal orientation procedure and training for new directors.

24emira property fund annual report 2008

Corporate governancecontinued

The board will ensure that it has the expertise, independence and diversity it needs to function independently. Independence of the board from the management team will be achieved by:

maintaining a non-executive chairperson;•maintaining a balance of executive and non-executive directors;•the remuneration of the non-executive directors being unrelated to the financial performance of Emira; and•all directors being entitled to seek independent professional advice concerning the affairs of Emira at the Fund’s expense.•

The board sets the strategic objectives of the Fund and determines the investment and performance criteria as well as being responsible for the proper management, control compliance and ethical behaviour of the business under its direction.

Committees

Audit committeeDuring the year, the audit committee comprised five members of which the Chairman was non-executive. In August 2008, the audit committee was reconstituted to comprise only independent non-executive directors. Accordingly, Messrs BJ van der Ross, WK Schultze and JWA Templeton stepped down from the audit committee and Ms LS Barnard joined the committee. The committee meets at least four times per year with the Fund’s external auditors and executive management as well as the executives responsible for finance, the compliance officer and internal auditors.

The primary objectives of the committee are to provide the board with additional independent and objective assurance regarding the efficacy and reliability of the financial information used by the directors, to assist them in the discharge of their duties. The audit committee is required to provide reasonable assurance to the board that adequate and appropriate financial and operating controls are in place; that significant business, financial and other risks have been identified and are being suitably managed; and that satisfactory standards of governance, reporting and compliance are in operation. The committee also monitors proposed changes in accounting policies, and discusses and advises the board on the accounting implications of major transactions.

The board is responsible for the group’s system of internal and operational control. The executive directors are charged with the responsibility of ensuring that assets are protected, systems operate effectively and all valid transactions are recorded properly. Comprehensive reviews and testing of the effectiveness of the internal control systems in operation are performed by internal auditors, who report to the audit committee. The internal audit function co-ordinates with other internal and external providers of assurance to ensure proper coverage of financial, operational and compliance controls.

The committee has the co-operation of all directors, management and staff and is satisfied that controls and systems within the Fund have been adhered to and, where necessary, improved during the period under review.

Investment committeeAn investment committee comprises at least two executive directors, and four senior staff employed by STREM with the appropriate skills and experience. The committee meets on an ad hoc basis to assess acquisitions and disposals, and makes recommendations to the board.

Remuneration committeeDuring the year a remuneration committee was established as a sub-committee of the board. The committee comprises the Chairman of the board of directors and an independent non-executive director. The committee considers and recommends the remuneration payable to non-executive directors by the management company.

Management and financial controlDuring the year independent internal auditors performed a management and financial control review. No significant weaknesses were identified and the overall conclusion was that the:

directors had maintained an adequate system of internal controls and accounting records;•the Fund’s assets are safeguarded and appropriately insured;•the Fund should remain a going-concern for the foreseeable future; and•management understood the Fund’s policy and employed the appropriate strategy.•

25emira property fund

annual report 2008

Corporate governancecontinued

directorate

Details of the directors are set out on pages 20 to 22 of this report. According to the articles of association of STREM, one third of the executive and non-executive directors shall retire at the following annual general meeting of STREM and will be eligible for re-election.

Directors of STREM holdings in Participatory Interests

The directors’ holdings in the participatory interests of the Fund as at 30 June 2008 were:

Beneficial Beneficial Held by Beneficial Beneficial Held by direct indirect associates Total direct indirect associates Total 2008 2008 2008 2008 2007 2007 2007 2007

Executive directors

Warren Schultze 391 000 391 000 391 000 391 000

James Templeton 149 800 149 800 89 800 89 800

Peter Thurling 32 000 88 000 120 000 32 000 88 000 120 000

Non-executive directors

Michael Aitken 20 000 288 000 308 000 20 000 288 000 308 000

Liliane Barnard 107 700 107 700 107 700 107 700

Bryan Kent 218 878 218 878 218 878 218 878

Nocawe Makiwane 1 511 133 1 511 133 890 414 890 414

Thys Neser 20 000 20 000 40 000 20 000 20 000 40 000

Nkululeko Sowazi 7 820 221 7 820 221 7 820 221 7 820 221

Ben van der Ross 3 176 915 3 176 915 2 496 377 2 496 377

Totals 201 800 13 226 147 415 700 13 843 647 141 800 11 924 890 415 700 12 482 390

Since the end of the financial year to the date of this report, the interests of directors have remained unchanged.

Directors’ remunerationThe directors of STREM are remunerated from the management fee payable by the Fund.

Directors’ dealingsThe board has adopted policies prohibiting dealings by directors and certain other managers in periods immediately preceding the announcement of its interim and year-end financial results and at any other time deemed necessary by the board or as required in terms of the JSE regulations.

SECRETARY oF THE FUNdDesiree Isserow is the company secretary who was appointed on 1 October 2007. Her business and postal addresses, which are also the Fund’s registered and business addresses, are set out on page 86.

AUdIToRSThe Fund’s auditors are PricewaterhouseCoopers Inc.

MAjoR INTEREST HoLdERMomentum is the majority interest holder in Emira with 34,4% of the participatory interests in issue.

SPECIAL RESoLUTIoNSA full list of the special resolutions passed by the fund during the year will be made available to participatory interest holders on request.

26emira property fund annual report 2008

Corporate governancecontinued

MATERIAL CHANGES ANd SUbSEQUENT EvENTS To THE bALANCE SHEET dATEThe only events which are required to be noted are the disposal of two properties, details of which are noted on page 18.

STRUCTURE oF THE FUNdEmira Property Fund (“the Fund”) is a property unit trust in terms of the Collective Investment Schemes Control Act, No 45 of 2002. The Fund is managed by Strategic Real Estate Managers (Pty) Limited (“STREM”), which is approved by the Registrar of Collective Investment Schemes to manage the Fund.

In terms of the Collective Investment Schemes Control Act, No 45 of 2002 (“CISC Act”) the Fund is obliged to distribute all income earned to its participatory interest holders. As a result of its distribution obligations, no income tax or capital gains tax is payable by the Fund.

Windrifter Share Block (Pty) Limited*

The Colony Centre Share Block (Pty) Limited

Surgate Share Block (Pty) Limited*

Paddy’s Pad (2091) (Pty) Limited

No 9 Sturdee Holdings Share Block (Pty) Limited*

Kenview Share Block (Pty) Limited*

Backbone Investments (Pty) Limited*

Azgold Investments (Pty) Limited

Arnold Properties (Pty) Limited* Freestone Property Investments (Pty) Limited*

Emira Property Fund* 492 818 989 PIs listed on the JSE Limited

Freestone Property Holdings Limited Property Loan Stock Company

Eris Property Group (Pty) Limited • Property Managers

Corovest Property Group Holdings (Pty) Limited 15%

Auditors: PricewaterhouseCoopers Inc. • Report on fair presentation of financial statements

Trustee: Absa Bank Limited • Protects PI holders’ interests • Acts as custodian of Fund’s assets and

securities • Ensures compliance with Trust Deed and

legislation

RMB Properties (Pty) Limited 15%

FirstRand Asset Management (Pty) Limited 70%**

Registrar of Collective Investment Schemes • Ensures compliance with Collective

Investment Schemes Control Act, 2002, and monitors the operation of the collective investment scheme

JSE Limited • Ensures compliance with JSE requirements and provides a market for trading PIs

MANAGEMENT REGULATORY BODIES

Participatory interest (PI) holders Effective ownership in property portfolio

Strategic Real Estate Managers (Pty) Limited • Asset management • Reports to PI holders

* Property owning entities** In the process of being transferred to another FirstRand Group company

27emira property fund

annual report 2008

Corporate governancecontinued

MANAGEMENT oF THE FUNd

STREM – Asset managementSTREM has been approved by the Registrar of Collective Investment Schemes to manage the Emira Property Scheme.

STREM receives an amount equal to 0,5% of the total market capitalisation of the Fund, calculated monthly on the average daily closing price of the Fund as recorded by the JSE Limited, plus total long-term borrowings.

Fees paid for the period amounted to R33,4 million (2007: R21,9 million).

Property managementProperty management of the Fund has been outsourced to RMB Properties (Pty) Limited (“RMB Properties”), a subsidiary company of FirstRand, and Alliance Property Group (Pty) Limited, who managed the group’s rural property portfolio until the end of May 2008. RMB Properties ceded all its property services to a new company named Eris Property Group (Pty) Limited (“Eris”) on 1 April 2008. From 1 June 2008, the entire property portfolio was outsourced to Eris Property Group.

Property management fees and commissions paid for the period were R48,1 million (2007: R55,1 million).

RISk MANAGEMENTThe STREM management philosophy on risk recognises that managing risk is an integral part of generating sustainable PI holder value and enhancing stakeholder interest. It also recognises that an appropriate balance should be struck between entrepreneurial endeavour and sound business practice.

The management of STREM operates a risk management framework, which is based on COSO’s Enterprise Risk Management Framework. The underlying premise of enterprise risk management is that every entity exists to provide value for its stakeholders. All entities face uncertainty, and the challenge for management is to determine how much uncertainty to accept as it strives to grow stakeholder value.

Value is maximised when management sets strategy and objectives to strike an optimal balance between growth and return goals and related risks, and efficiently and effectively deploys resources in pursuit of the entity’s objectives.

Enterprise risk management in STREM encompasses:Aligning risk appetite and strategy which considers the risk appetite in evaluating strategic alternatives, setting related objectives, and •developing mechanisms to manage related risks.Enhancing risk response decisions by selecting alternative risk response, which includes risk avoidance, reduction, sharing or acceptance.•Reducing operational losses by gaining enhanced capabilities to identify potential events and establish responses.•Identifying and managing multiple cross-enterprise risks.•Seizing opportunities by identifying a full range of potential events.•Improving deployment of capital by obtaining robust risk information to allow management to effectively assess overall capital needs and •enhance capital allocation.

These capabilities inherent in enterprise risk management help management achieve the Fund’s performance and profitability targets and prevent loss of resources. Enterprise risk management helps to ensure effective reporting and compliance with laws and regulations, and helps avoid damage to the Fund’s reputation and associated consequences.

28emira property fund annual report 2008

Corporate governancecontinued

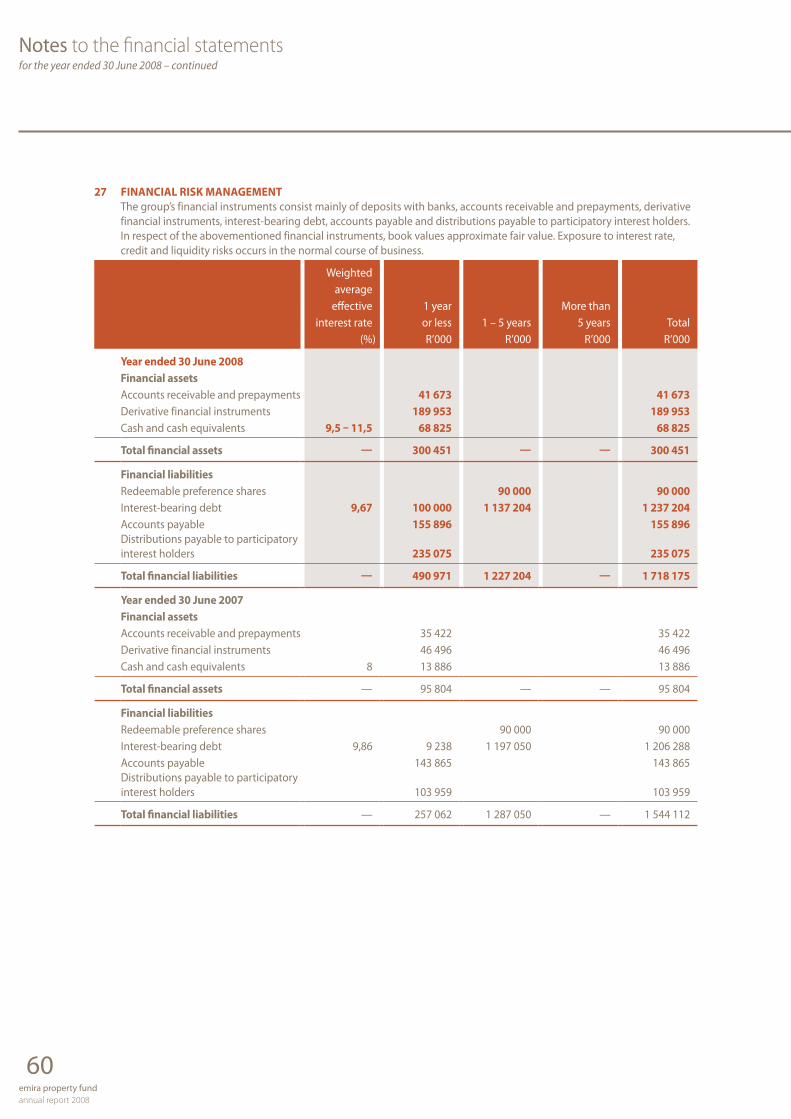

Financial risk factorsThe financial instruments of the group consist mainly of deposits with banks, long-term borrowings, derivative instruments, accounts receivable and accounts payable. The Fund issues or purchases financial instruments in order to finance operations and to manage the interest rate risks that arise from these operations.

The Fund’s credit, interest and liquidity risks are continually monitored.

The main objective of using financial instruments is to reduce the uncertainty over future cash flows arising principally as a result of interest rate fluctuations. The Fund finances its operations through the combination of bank borrowings and issue of additional units.

Interest rate risk managementAs at 30 June 2008, approximately 93% of total borrowing facilities were at fixed rates (in terms of the swap contracts).

Credit risk managementThe Fund has no significant concentration of credit risk due to a large number of widespread tenants.

The Fund has policies in place to ensure that lease agreements concluded are with tenants with an appropriate credit history. The Fund has policies that limit the amount of credit exposure to any one financial institution, and cash transactions are limited to high credit quality financial institutions. The debts are monitored on a continual basis in order to maintain a low default rate on trade receivables.

Liquidity risk managementCash flows are monitored on a monthly basis to ensure that cash resources are adequate to meet the funding requirements of the Fund.

29emira property fund

annual report 2008

Sustainability

INTRodUCTIoNThe Emira Property Fund recognises its responsibility to protect the interests of all its stakeholders and believes that good governance is essential to the Fund’s long-term sustainability and functioning. The objective of the Fund is to conform to its stringent requirement for transparency, while operating profitably and remaining accountable to the broader community which it serves and respecting the natural environment.

The Fund has embraced the King II report’s guidelines for socially responsible reporting according to the “triple bottom line” – the economic, social and environmental impacts of its properties.

Going forward, the Fund is formalising its approach in order to reflect its commitment to sustainable business practice, and introduce measurable targets for the future.

STAkEHoLdER ENGAGEMENTThe STREM board considers it a duty to keep all the Fund’s stakeholders informed and up to date with regard to its practices, policies and financial results, while remaining accountable for the sustainability of the Fund to its investors and tenants.

Direct discussions with stakeholders are always welcomed by the Fund. In addition to communication at the annual results presentation which is made to key shareholders and analysts, media releases are published when appropriate as well as ad hoc meetings with interested parties on request.

The Fund meets regularly with its shareholders and recognises its fiduciary duty to maximise the value of its assets for their benefit. In addition, shareholders are encouraged to attend the Fund’s annual general meeting to vote on resolutions and, where appropriate, to enter into discussions with the STREM directors.

The Fund has defined its major stakeholders and communicates with them as follows:Investors•Tenants•Suppliers and property management services providers•Asset managers•Communities•Government•

As part of its duty as a South African corporate citizen, the Fund is committed to its responsibility of engaging with local communities where its operations have a potential environmental impact on their surroundings. The Fund aims to develop a positive working relationship with local communities through organised committees. For example, when the Fund engages in property development, where required, the impacts are fully evaluated with environmental impacts assessments, which involve extensive consultation with the local communities.

Through its property management service provider, RMB Properties/Eris, the Fund engages with its base of more than 4 000 tenants on a daily basis. These tenants range from small owner-run enterprises, to blue chip companies and government departments spanning local, provincial and national government. The Fund also engages with government departments in matters relating to properties, for example zoning, planning permissions and rates.

30emira property fund annual report 2008

Sustainabilitycontinued

ECoNoMIC IMPACT

TransformationThe Fund is committed to empowering historically disadvantaged South Africans and considers this as an imperative to model corporate citizenship.