1 | Page A Comparative Study on Financial Performance of SBI Life Insurance and ICICI Prudential Life Insurance Research Project Submitted in Partial Fulfilment of the Requirements for the Degree of BCOM Honours By Harshita Kataria to the DEPARTMENT OF COMMERCE BHOPAL SCHOOL OF SOCIAL SCIENCES April, 2021 Submitted by Guided by Harshita Kataria Dr Swapna Pillai Associate Professor Department of Commerce

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 | P a g e

A Comparative Study on Financial Performance of SBI Life

Insurance and ICICI Prudential Life Insurance

Research Project Submitted in Partial Fulfilment of the Requirements

for the Degree of

BCOM Honours

By

Harshita Kataria

to the

DEPARTMENT OF COMMERCE

BHOPAL SCHOOL OF SOCIAL SCIENCES

April, 2021

Submitted by Guided by

Harshita Kataria Dr Swapna Pillai

Associate Professor

Department of Commerce

2 | P a g e

CERTIFICATE

It is certified that the work contained in the project report titled “A Comparative Study on

Financial Performance of SBI Life Insurance and ICICI Prudential Life Insurance,” by

“Harshita Kataria,” has been carried out under my/our supervision and that this work has

not been submitted elsewhere for a degree*

Signature of Supervisor: …………….

Name : Dr Swapna Pillai, Associate Professor

Department : Commerce

Bhopal School of Social Sciences

April, 2021

3 | P a g e

DECLARATION

I hereby declare that this project report entitled “A Comparative Study on Financial

Performance of SBI Life Insurance and ICICI Prudential Life Insurance “was carried out by

me for the degree of BCOM Honours under the guidance and supervision of Dr Swapna

Pillai , Associate Professor of Department of Commerce, BSSS College. The interpretations

put forth are based on my reading and understanding of the original texts and they are not

published anywhere in any form. The other books, articles and websites, which I have made

use of are acknowledged at the respective place in the text. This research report is not

submitted for any other degree or diploma in any other University.

Place: Bhopal

Name of the Student: Harshita Kataria

Class & Section: B.Com (Hons) III ‘A’

Date: 30th April 2021

4 | P a g e

ACKNOWLEDGEMENT

I would like to thank our Principal Dr. Fr. John P.J. and Vice Principal Dr Sr Sonia Kurien

for their immense support and blessings. I thank our HOD Dr Amit Kumar Nag for his

support. I would like to express my special thanks of gratitude to my research guide Dr.

Swapna Pillai, Associate Professor of Department of Commerce for her valuable suggestions

and guidance and for giving me the golden opportunity to do this wonderful research project

on the topic: A Comparative Study on Financial Performance of SBI Life Insurance and

ICICI Prudential Life Insurance, Without her help it would have been difficult for me to have

reached this state of completion of my project report. Also, I would like to thank my parents

and friends who helped me a lot in the preparation of this project.

I wish to acknowledge the help of all those who have provided me information, guidance and

other help during my research period.

5 | P a g e

SUMMARY

Insurance has been playing a vital role in advanced and emerging nations and has been

recognized as a reliable tool for the mobilization of public savings. In India, the insurance

sector has gone through various phases, such as deregulation, regulation, nationalization,

privatization and globalization. Liberalization has opened the door for many private players

to join hands with international partners. Since 2000, the Indian life insurance sector has been

characterized by intense competition between the private and public sector players and within

the private sector players. This study aims to examine the financial performance of ICICI

Prudential Life Insurance and SBI Life Insurance during the period 2017-18 to 2019-20. For

measuring it, various financial ratios have been calculated taking into consideration liquidity,

solvency, profitability and persistency ratio of ICICI Prudential Life Insurance and SBI Life

Insurance. For further analysis of the data, a t-test is applied, and the results of the t-test

reveal that there is a significant difference in the current ratio of selected insurers.

This study mainly depends on the secondary data. The relevant and required data were

collected from the text books, websites, National and International articles, as well as annual

reports of ICICI Prudential Life Insurance and SBI Life Insurance.

6 | P a g e

INDEX

S.NO. CONTENTS PAGE NO.

1. Rationale of the study 8

2. Introduction to the industry 8

3. Introduction to the company 10

4. Justification of the topic 12

5. National Review 14

6. International Review 17

7. Objectives of the study 20

8. Research Hypothesis 20

9. Scope of the study 20

10. Research Design 21

11. Limitation of the study 21

12. Data representation and interpretation 23

13. Hypothesis testing 34

14. Major findings 36

15. Discussions and suggestions 37

16. Conclusions 37

17. References 39

18. Annexure 43

7 | P a g e

CHAPTER 1 : INTRODUCTION OF

THE TOPIC

1.1 Rationale of the Study

1.2 Introduction to the Industry

1.3 Introduction to the Company

1.4 Justification of the Topic

8 | P a g e

1.1 RATIONALE OF THE STUDY:

1.1.1 Why the need for the study?

To compare the companies to identify which company is the market leader.

To understand their financial performance.

1.1.2 What information will the study add?

This research will help in analysis of companies.

This research will make us understand the companies’ market share, financial strength

and quality of their business.

1.2 INTRODUCTION OF THE INDUSTRY:

Insurance is the backbone in managing the risk of the country. The insurance providers offer diversity

of products to business, thus ensuring protection from risk thereby guaranteeing financial stability .It

helps individual and organization to minimize the consequences of risk which impart significant cause

on the growth and development of insurance industry. Insurance plays a key role in stabilizing the

economy, trade and commerce.

What is Life Insurance?

(Life Insurance) is defined as a contract between the policy holder and the insurance

company, where the life insurance company pays a specific sum to the insured individual's

family upon his death. The life insurance sum is paid in exchange for a specific amount of

premium.

The Indian Insurance Industry is divided into 2 basic sectors – Life Insurance and Non-life

Insurance (also called General Insurance ) Both these sectors are regulated by Insurance

Regulatory and Development Authority (IRDA) of India which is a government body which

frames the rules for the entire industry and all insurance companies have to abide by them. IRDA is

the policy maker for the entire insurance industry in India and also serves as the custodian of

consumers rights.

9 | P a g e

Growth of Life Insurance Industry

As an industry, insurance is regarded as a slow-growing, safe sector for investors. This perception is

not as strong as it was in the 1970s and 1980s. (A Brief Overview of the Insurance Sector) . The

Indian Insurance has been growing rapidly since 2000, as it was liberalised after more than 50

years of monopoly of LIC, where private life insurers have entered the insurance sector with

innovative practices leading to more business. Indian consumers, who have always seen life

insurance as a tax saving system, are now suddenly turning to the private sector and snapping

up the new innovative products on offer. The Private players have taken some market share

from LIC, and major growth has happened because of market expansions. The Indian

Insurance Industry is getting ready for new era, where it is building world-class risk

Management capability. The insurance industry has come a long way from being an open

competitive market to nationalized then back to a liberalized market in India.

Current market Scenario

.According to (Indian Insurance Industry Report , 2021) the insurance industry of India has 57

insurance companies 24 are in the life insurance business, while 33 are non-life insurers. Among the

life insurers, Life Insurance Corporation (LIC) is the sole public sector company. According to

(McKinsey, 2007) it was estimated that India is likely to emerge as the fifth largest market in the

world by 2025.

In India, most private companies have entered into business with collaboration with

established Insurance Companies in the world, both in the life and non-life Insurance Sectors.

These global players' skills contribute to the performance of the Indian insurance sector, as it

replicates the learning acquired from other industries over a long span of time. The

international partner of any insurance firm in India is not allowed to own more than 26% of

the shares in Indian insurance company as per IRDA regulations. We have seen big financial

groups in India like SBI, ICICI and HDFC enter this pace and become aggressive players. .

Other famous corporate groups like the Tata’s, Birla’s and the Ambani’s have also formed insurance

companies.

10 | P a g e

1.3 INTRODUCTION TO THE COMPANY:

For the purpose of the present study, two renowned private life insurance companies namely,

ICICI Prudential Life Insurance and SBI Life Insurance were selected. Brief profiles of the

selected insurers are as follows:

SBI Life Insurance Company Ltd.

It is a joint venture life insurance company between State Bank of India (SBI), the

largest state-owned banking and financial services company in India, and BNP

Paribas Cardif. It incorporated October 11, 2000, and received permission from IRDA on

March 29, 2001, to carry on the life insurance business .SBI has a 62.1% stake in the

company and BNP Paribas Cardif owns a 22% stake. Other investors are Value Line Pte. Ltd.

and MacRitchie Investments Pte. Ltd., holding a 1.95% stake each while the remaining 12%

is free float stake with public investors.

SBI Life incorporated with an authorized capital of Rs. 2000 crore, while it is paid up capital

is Rs.1000 crore. SBI Life, which started its operations with the vision “To be the most

trusted and preferred life insurance provider,” initially depended upon the Bancassurance and

now is developing its own agency team for selling insurance products. SBI Life’s insurance

products include various policies meant to address different needs of different sections of the

society. It offers unit-linked, child plans, protection plans, saving plans, retirement, group

plans, etc. With customer service excellence and product innovations, the company has been

growing year after year. SBI Life Insurance has received many awards and accolades for the

work in the field. Following are some of them:

SBI Life Insurance has won ‘Brand of the Year 2016-17’ award in the insurance

category

SBI Life Insurance has won ‘Private Sector Life Insurance Company of the Year’

award at Fintelekt Insurance Awards

SBI Life Insurance has won ‘Bancassurance Leader, Life Insurance’ in large

companies category.

11 | P a g e

ICICI Prudential Life Insurance Company Limited

It is a life insurance company in India. Established as a joint venture between ICICI

Bank and Prudential plc, ICICI Prudential is engaged in life insurance and asset management

business. The firm offers long term life insurance plans and is headquartered in Mumbai. In

2016, the firm became the first insurance company in India to be listed in the domestic stock

exchanges.

ICICI Prudential Life Insurance Company has been promoted jointly by ICICI Bank limited,

a leading private sector Indian bank, and Prudential Corporation Holdings Limited by

contributing 74% and 23% capital, respectively. It was incorporated on July 20, 2000, and

received a certificate of registration from IRDAI to carry out the life insurance business on

November 20, 2000. ICICI Life began its operations in financial year 2001 with the vision to

build an enduring institution that serves with sensitivity the protection and long-term saving

needs of customers. ICICI Prudential Life, known as ICICI Life, has become the first

insurance company in India to be listed on the NSE and the BSE in 2017. It offers health

insurance, term insurance, savings, and retirement plans for individuals and groups to meet

varied needs of the customers.

ICICI Prudential Life Insurance has received many awards and accolades for the work in the

field. Following are some of them:

ICICI Prudential Life has received ‘Life Insurance Company of the Year’ award at

India Summit and Awards 2019

ICICI Prudential Life has received ‘Life Insurance Provider of the Year’ by Outlook

Money Awards 2018

ICICI Prudential Life has received ‘Best Term Insurance Provider of the Year’ award

by Money Today Financial Awards 2017-18

ICICI Prudential Life is awarded as ‘Best Customer Orientation in Life Insurance’

award by Emerging Asia Awards 2018

ICICI Prudential Life is awarded as ‘Best Growth in Life Insurance’ category by

Emerging Asia Awards 2018.

12 | P a g e

1.4 JUSTIFICATION OF THE TOPIC:

1.4.1 What is the potential utility of the findings (local, national, global)?

This analysis will help the investors who want to invest in such companies.

To identify their good points and points of improvement.

1.4.2 What are the implications of the study?

Comparison of market share.

Comparison of profitability.

Ratio analysis to find out their financial strength.

Measuring Quality of the Businesses.

13 | P a g e

CHAPTER 2: REVIEW OF

LITERATURE

2.1 National Reviews

2.2 International Reviews

14 | P a g e

2.1 NATIONAL REVIEWS:

1. (Naidu & Paramasivan, 2015) highlighted that the measurement of performance of

insurance firms become important, because they not only include the money saving and risk

transfer process, but also help to properly redirect funds in order to finance investment

activities in the economy.

2. (Joshi & Takodia, 2017) study suggests that all life insurers need to raise understanding

on the definition of life insurance and on different life insurance undertakings among

investors in order to increase market share and growth in a sector. When looking at Life

insurers, they must have adequate weightage for different factors such as the timeliness of

pay-out and the sum of their claims, ensure that investors are at the best possible convenience

in the settlement, provide integrity and retain strong financial position to draw the interest of

investors.

3. (Kumari, 2013) analysed efficiency assessment of India's post-liberalization life insurance

market by using different ratios. The study concluded that India has registered a rise in both

insurance penetration and density since Indian insurance market was opened to private firms.

India's life insurance spectrum is enormous. The total assets to earned premium ratio,

investment income to earned premium ratio and investment income to total investment ratio

represent an insurer's economic solidity and reveal the performance with respect to

investment decisions.

4. (Dr.Parmasivan, 2015) has carried out a comparative analysis of insurance providers in

India in the public and private Life Insurance Companies. Current ratio and debt equity ratio

is estimated to measure the solvency ratio for financial efficiency. The analysis shows that

LIC already dominates the market. The new commercial channels of promotion are used by

private sector insurance providers in comparison to LIC. The sale of more plan-linked units

allows private insurers to capture LIC market share. Private insurers are also better than LIC's

solvency and lapse ratios. In comparison with private life insurance the service of death

lawsuits was higher for LIC.

5. ( Mishra, 2015) suggest that the current public insurers with ensuring cost-effectiveness

should stay competitive also. These public sector firms have taken a range of steps with

regard to competition with private sector businesses. But, despite changing their strategy and

15 | P a g e

ideology in the post-Reform era, the government sector companies do need to reassess their

current status. Insurance firms must ensure that premium goods are guaranteed at a fair price

and companies can reduce the price of the commodity by reducing costs. Success depends on

their sustainability, competitiveness, reliability and quality of service performance.

6. (Bodla, Bodla, & Tondon, 2017 ) analysed and compared the profits of life insurance firms in

India (Public and Private). The 10-year comparison frame for the analysis varied from 2007 and 2016.

Seven factors, including Net Premium, Investment income, Underwriting income, asset return,

combined ratio, solvency ratio and profits were used for analysis of income and financial results. The

analysis showed that the net average premium over the last five years was the highest for ICICI

prudential followed by the HDFC Standard and SBI Life, while the lowest premium for the private

sector life insurers was mobilised by IDBI Federal. They concluded, too, that in almost every private

sector corporation in the past five years, the CAGR's underwriting revenue has decreased.

7. (Gulati & Jain, 2011) analysed business performance of all life insurers in industry on

the basis of various indicators. LIC was the highest rider in all forms of premiums whereas in

the private sector, ICICI Prudential Life Insurance led the Insurance Industry followed by

SBI Life Insurance and Bajaj Allianz Life Insurance. The study suggested that even after the

entry of private sector, the growth of public sector undertaking had not resulted in downfall

even after facing numerous opportunities and challenges.

8. ( Bawa & Chattha , 2013) examines the financial performance of Indian life insurance

companies by analysing their profitability determinants. Financial Efficiency was calculated

using financial ratios such as the current ratio, solvency ratio, equity ratio, and insurance debt

ratio. The samples for this analysis are 18 Indian Life Insurers (including 1 public and 17

private life insurers) and the study period is from 2007-08 to 2011-12.According to the

report, the public sector LIC is the most liquid of all life insurers. Future General Life

Insurance, IDBI, Sahara, Shri Ram Life Insurance, and SBI Life Insurance have a strong cash

position in comparison to other private insurers. Life insurers like Aviva, Bajaj Allianz, IDBI,

Max Life, Sahara and SBI Life insurance are more solvency-friendly than other insurers

.Bajaj Allianz and ICICI Prudential Return on Asset Measurements sounds good.

9. (Dar & Bhat, 2015) evaluate the financial statements and soundness of selected public and

private life insurance companies. The statistical findings of the analysis reveals that there are

significant statistical variations in the capital adequacy, revenue, profitability and liquidity

roles in selected insurers of public and private life. The overall result reveals that the capital

16 | P a g e

adequacy among selected private life insurers is much greater than the average amount of

capital of public life insurer. But the public life insurers surpass the private life insurers in

their profitability in the analysis period. The study also showed that public life insurers had a

higher liquidity in relation to private life insurers during the examined period.

10. (Solanki, 2016) examined the profitability of life insurance companies. For measuring the

profitability of the companies various ratios were calculated. The study shows that the private

sector life insurances companies should strive to increase its business by issuing more and

more policies in order to retain its market share in the competitive scenario.

11. ( Gour & Gupta , 2012) determined the solvency ratio of Indian Life insurance

companies for the period of 3 years from 2009-10 to 2011-12. It analysed whether

performance of different companies was similar or there was any significant difference. On

the basis of solvency ratio, ranks were assigned to different companies which showed that

ICICI found the best among selected companies of industry followed by Birla Sun Life, SBI,

HDFC and LIC. The paper also observed that solvency of life insures depend on returns

received from total investible funds and interest rate.

12 (Vasavi & Reddy, 2020) analysed that there is a significant difference in the earnings and

profitability performance of ICICI Prudential Life Insurance and SBI Life Insurance. The

findings suggested that ICICI Prudential Life Insurance outperformed SBI Life Insurance for

two indicators of the three indicators chosen for the report. ICICI Prudential Life Insurance

has shown itself to be a more stable insurer by having a higher mean valuation for the income

on investments ratio and return on equity ratio. Although ICICI Prudential Life Insurance has

taken SBI Life Insurance’s lead over the whole study period in retaining the higher

investment earnings ratio, it is evident that its results include a persistent decrease in its

investment earnings ratio.

13. (Neelaveni, 2012) evaluated the performance of five life insurance companies in the

period of 2002-03 in terms of various plans and policies on the basis of annual growth rate.

The study concluded that LIC being the public sector insurance provider was lagging behind

due to competition faced by private insurers whereas in terms of financial aspects, private life

insurance providers were doing well.

17 | P a g e

2.2 INTERNATIONAL REVIEWS:

1.According to (McKinsey, 2011) the Indian Life Insurance sector is the lowest-profit market

for shareholders in all Asian nations, However, according to IRDA figures in 2010-11, the

Life insurance industry showed net income of Rs 26,57 billion compared to a net loss of Rs

9,89 billion in 2009-10. (www.irda.gov.in).

2. (Malik, 2011) determined the relationship of profitability and internal factors of insurance

companies in Pakistan. Multiple regression models have been used to determine specific

factors under which profitability has been taken as a dependent variable while age, size of

company, volume of capital, leverage and loss ratio as independent variables .The study

covered the time period from 2005 to 2009. The findings suggested that there was no

relationship of profitability with age, but significant positive relationship with size and

volume of capital, and significantly negative relationship with loss ratio and leverage.

3. (Bikker, 2012) investigated the competitiveness and efficiency in the Dutch Life Insurance

Industry by the evaluation of unused scale economies and measuring efficiency market share

dynamics between 1995 to 2010. The result of the study showed that economies significantly

decrease with size of insurer and unused economies of scale did not exist under strong

competition.

4. ( Akotey, Sackey, Amoah , & Manso, 2013) examines in particular the main drivers of

Ghana's life insurance industry's profitability. The annual financial statements of ten life

insurance companies covering a period of 11 years (2000‐2010) were sampled and analysed

through panel regression. The results showed that while gross written premiums relate

positively to the performance of profits by insurers, their relationship to investment income is

negative. The findings also revealed that life insurers suffered considerable damages as a

result of overtrading and price reductions.

5. (Ayele, 2012) explores the effect on Ethiopia's success of the insurance industry from

2003 to 2011 for the period of 9 years. The samples taken for this analysis are 9 Life

Insurance Companies. The findings of the regression analysis shows that the most important

determinants of the success of life insurance industry are leverage, scale, amount of stock,

growth and liquidity, while ROA has statistically negligible relation to, age and tangibility.

18 | P a g e

6. In (Greene & Segal , 2004) Research 'Profitability and Economical efficiency in the U.S.

Life insurance industry' the relationship between cost inefficiency and sustainability has been

discussed in the US Life Insurance Industry. An established, dynamic life insurance market

can be the primary engine of sustainability and cost-effectiveness. The study indicates that

cost inefficiency is significant in comparison to profits in the life insurance sector and that

inefficiencies are adversely correlated with performance ratio including equity income.

7. (Smajla, 2014) highlighted Croatian insurance firms level of financial well-being using

CARAMEL Model. This research is being conducted in Croatia on 24 insurance

undertakings. The study found that company liquidity ratios were not good and suggests that

the health of the insurance firms capital adequacy and liquidity indicators be taken into

account by the Croatian regulatory bodies.

19 | P a g e

CHAPTER 3: RESEARCH

METHODOLOGY

3.1 Objectives of the Study

3.2 Research Hypothesis

3.3 Scope of the Study

3.4 Research Design

3.5 Limitation of the study

20 | P a g e

3.1 OBJECTIVES OF THE STUDY:

The main objective of the present study is to study the financial performance of SBI and

ICICI Prudential life insurance companies. The other objectives of the present study are the

followings.

I. To evaluate the financial soundness, business efficiency and overall performance of SBI

Life Insurance and ICICI Prudential Life Insurance.

II. To analyse the solvency, profitability and liquidity position of SBI Life Insurance and

ICICI Prudential Life Insurance for last three years (i.e. FY 2018 to FY 2020).

3.2 RESEARCH HYPOTHESIS:

H0: There is no significant difference between Current Ratio of SBI Life Insurance and

ICICI Prudential Life Insurance.

3.3 SCOPE OF THE STUDY:

The present study is based on secondary data, which has been extracted from different

websites, National and International articles as well as annual reports of ICICI Prudential Life

Insurance and SBI Life Insurance. To analyse the quantitative data, the ratio analysis has

been used. For the purpose of the present study, two renowned private life insurance

companies in India namely, ICICI Prudential Life Insurance and SBI Life Insurance are

selected. This study aims to examine the profitability performance of ICICI Life and SBI

Life during the period 2017-18 to 2019-2020.

21 | P a g e

3.4 RESEARCH DESIGN:

3.4.1 SAMPLE OF THE STUDY:

The sample for this study includes 2 Indian life insurers namely, ICICI Prudential Life Insurance and

SBI Life Insurance.

3.4.2 DURATION OF THE STUDY:

The research analyses the data for 3 years from 2017-18 to 2019-20

3.4.3 SOURCE OF DATA:

This study mainly depends on the secondary data. The relevant and required data were

collected from the text books, websites, National and International articles, as well as annual

reports of ICICI Prudential Life Insurance and SBI Life Insurance.

3.4.4 TOOLS and TECHINIOUE:

The present study is an analytical study. For the analysis of data in the form of various

profitability ratios, liquidity ratio, Persistency Ratio, Solvency Ratio and the statistical tools

like T-Test have been employed.

3.5 LIMITATION OF THE STUDY:

The data collected for the study depends on published financial statements of the

companies which may incorporate some drawbacks.

The horizon of the study merely confined to very less number of variables as the

determinants of insurance company's profitability and measuring financial

performance without considering any overall performance measurement tool.

The data which has been used for the study mainly secondary data, so limitation of

secondary data remains with it and also applies to this study.

The Financial statement study is based on only three years.

22 | P a g e

CHAPTER 4: DATA

REPRESENTATION AND ANALYSIS

1.1 Data Representation & Interpretation

1.2 Hypothesis Testing

23 | P a g e

4.1 DATA REPRESENTATION AND INTERPRETATION:

4.4.1 LIQUIDITY RATIOS:

Liquidity is a very critical part of a business. Liquidity is required for a business to meet its

short term obligations. A higher liquidity ratio represents that the company is highly rich in

cash.

Liquidity ratios determine how quickly a company can convert the assets and use them for

meeting the dues that arise. The higher the ratio, the easier is the ability to clear the debts and

avoid defaulting on payments.

This is a very important criterion that creditors check before offering short term loans to the

business. An organisation which is unable to clear dues results in creating impact on the

creditworthiness and also affects credit rating of the company.

A. Current Ratios – Current Ratio also known as the working capital ratio is the

most widely used ratio. The current ratio is a measure of a company’s ability to pay off the

obligations within the next twelve months. This ratio is used by creditors to evaluate whether

a company can be offered short term debts. Thus, Current Ratio is a measurement of financial

health of enterprise.

Computation: The formula for calculating Current Ratio is:

The ideal level of Current Ratio is 2:1. The ratio is considered as safe margin of solvency due

to the fact that if the current assets are reduced to half, then also the creditors will be able to

get their payments in full.

Current Ratio = Current Assets

Current Liabilities

24 | P a g e

Significance of Current Ratio

This financial metric helps to determine a company’s immediate financial standing.

A higher ratio often indicates greater liquidity and more stability.

The financial tool helps to understand a firm’s working capital requirement more

effectively.

It comes in handy for making an informed investment-related decision.

GRAPH 1-CURRENT RATIO

1.83 1.781.93

0.790.91

1.15

0

0.5

1

1.5

2

2.5

Mar-18 Mar-19 Mar-20

YEARS

SBI LIFE INSURANCE

ICICI PRUDENTIAL LIFEINSURANCE

YEAR SBI LIFE INSURANCE ICICI PRUDENTIAL

LIFE INSURANCE

MAR 2018 1.83

0.79

MAR 2019 1.78

0.91

MAR 2020 1.93

1.15

TABLE 1 - CURRENT RATIO

25 | P a g e

Interpretation:

Graph 1 depicts that the current ratio is fluctuating during the study period in the case

of SBI Life Insurance. A considerable decline in the current ratio from 1.83 in FY

2018 to 1.78 in FY 2019 and an increase in the ratio from 1.78 in FY 2019 to 1.93 in

FY 2020 can be observed from the graph whereas there is a constant increase in the

current ratio of ICICI Prudential Life Insurance from FY 2018 to FY 2020 i.e. from

0.79 to 1.15 respectively.

The Current ratio is higher in SBI Life Insurance than ICICI Prudential Life Insurance

for all the years during the study period.

B. Quick Ratios- Quick Ratio also known as Liquid Ratio is used to determine whether a

company or a business has enough liquid assets which are able to be instantly converted into

cash to meet short term financial obligations.

Computation: The formula for calculating Quick Ratio is:

Quick ratio of 1:1 is an accepted standard, since for every rupee of current liabilities, there is a rupee

of quick assets.

Significance of Quick Ratio:

It is precisely an indicator of a company’s ability or limitation in discharging its debts and

obligations. A company’s lenders, suppliers and investors rely on quick ratio to determine if

it has enough liquid assets for discharging its short-term liabilities.

Quick Ratio = Quick Assets

Current Liabilities

26 | P a g e

GRAPH 2- QUICK RATIO

Interpretation:

Graph 2 depicts that the quick ratio is fluctuating during the study period in the case

of SBI Life Insurance. A considerable decline in the quick ratio from 1.83 in FY 2018

to 1.78 in FY 2019 and an increase in the ratio from 1.78 in FY 2019 to 1.93 in FY

2020 can be observed from the graph whereas there is a constant increase in the quick

ratio of ICICI Prudential Life Insurance from FY 2018 to FY 2020 i.e. from 0.79 to

1.15 respectively.

1.83 1.781.93

0.790.91

1.15

0

0.5

1

1.5

2

2.5

Mar-18 Mar-19 Mar-20

YEARS

SBI LIFE INSURANCE

ICICI PRUDENTIAL LIFEINSURANCE

YEAR SBI LIFE INSURANCE ICICI PRUDENTIAL

LIFE INSURANCE

MAR 2018

1.83

0.79

MAR 2019

1.78

0.91

MAR 2020

1.93

1.15

TABLE 2 - QUICK RATIO

27 | P a g e

The Quick ratio is higher in SBI Life Insurance than ICICI Prudential Life Insurance

for all the years during the study period.

4.4.2 PROFITABILITY RATIOS:

The primary objective of each business enterprise is to earn profits. In fact profit earning is

considered essential not only for the survival of the business but is also required for its

expansion and diversification. Profitability ratios are a type of accounting ratio that helps in

determining the financial performance of business at the end of an accounting period.

Profitability ratios show how well a company is able to make profits from its operations.

Net Profit Ratio (%) – This ratio establishes the relationship in terms of

percentage between Net Profit and Revenue from Operations, i.e., Net Sales. It

shows the percentage of Net Profit earned on Revenue from Operations.

Computation: The formula for calculating Net Profit Ratio is:

Higher the net profit ratio, better the business.

Significance of Net Profit Ratio:

Investors, shareholders and business owners can review the firm’s net profit margin to

analyse its growth trends effectively.

Net Profit Ratio is an indicator of overall efficiency of the business.

Net Profit Ratio = Net Profit x100

Revenue from Operations

28 | P a g e

GRAPH 3- NET PROFIT RATIO (%)

Interpretation:

Graph 3 depicts that there is a considerable decline in the Net Profit Ratio from

89.77% in FY 2018 to 73.33% in FY 2020 in the case of SBI Life Insurance and from

88.57% in FY 2018 to 40.35% in FY 2020 in the case of ICICI Prudential Life

Insurance.

The Net Profit Ratio is higher in SBI Life Insurance than ICICI Prudential Life

Insurance for all the years during the study period.

89.77 88.2

73.33

88.57

66.36

40.35

0

10

20

30

40

50

60

70

80

90

100

Mar-18 Mar-19 Mar-20

YEARS

SBI LIFE INSURANCE

ICICI PRUDENTIAL LIFEINSURANCE

YEAR SBI LIFE INSURANCE ICICI PRUDENTIAL

LIFE INSURANCE

MAR 2018

89.77

88.57

MAR 2019

88.20

66.36

MAR 2020

73.33

40.35

TABLE 3-NET PROFIT RATIO (%)

29 | P a g e

4.4.3 PERSISTENCY RATIO (%)

Persistency is a key parameter for insurance companies. It measures the proportion of

policy holders who have continued with their policies. It indicates the ability of the

Company to retain customers. In India, the persistency ratios are published for the 13th

month, 25th month, 37th month, 49th month and 61st month as majority of savings regular

premium policies have a minimum 5-year premium payment period.

Computation: The formula for calculating Persistency Ratio is:

Higher Persistency Ratio indicates a large pool of satisfied customers

Lower Persistency Ratio indicates inability to retain customers.

Significance of Persistency Ratio:

It’s important for insurers to maintain a persistent book as it contributes to profitability.

It gauges the trust customer have in long-term products and services being offered by the

insurer.

A. PERSISTENCY RATIO% [13TH MONTH] –

The 13th month persistency measures the renewal premium paid by the policyholder

at the commencement of the second year.

It reflects the quality of the sale made by the company.

Persistency Ratio = Number of Policyholders Paying the Premium x 100

Net Active Policyholders

30 | P a g e

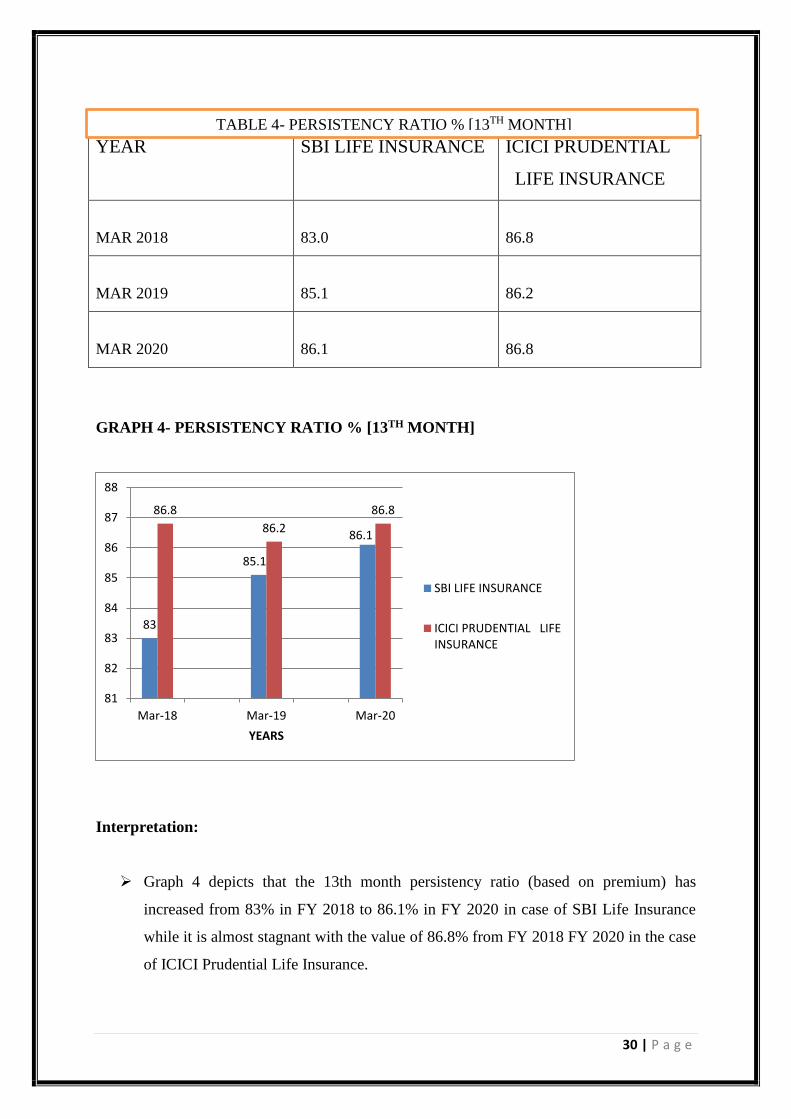

GRAPH 4- PERSISTENCY RATIO % [13TH MONTH]

Interpretation:

Graph 4 depicts that the 13th month persistency ratio (based on premium) has

increased from 83% in FY 2018 to 86.1% in FY 2020 in case of SBI Life Insurance

while it is almost stagnant with the value of 86.8% from FY 2018 FY 2020 in the case

of ICICI Prudential Life Insurance.

YEAR SBI LIFE INSURANCE ICICI PRUDENTIAL

LIFE INSURANCE

MAR 2018

83.0

86.8

MAR 2019

85.1

86.2

MAR 2020

86.1

86.8

TABLE 4- PERSISTENCY RATIO % [13TH MONTH]

83

85.1

86.1

86.8

86.2

86.8

81

82

83

84

85

86

87

88

Mar-18 Mar-19 Mar-20

YEARS

SBI LIFE INSURANCE

ICICI PRUDENTIAL LIFEINSURANCE

31 | P a g e

The 13th month persistency ratio is higher in ICICI Prudential Life Insurance than

SBI Life Insurance for all the years during the study period.

B. PERSISTENCY RATIO% [49TH MONTH] -

The 49th month persistency measures the renewal premium paid by the policyholder

at the commencement of the fourth year.

The 49th month tells about the ability of the Insurance Companies to retain their

customers.

GRAPH 5- PERSISTENCY RATIO % [49TH MONTH]

63.9

66.4

67.3

64.2

65

67.3

62

63

64

65

66

67

68

Mar-18 Mar-19 Mar-20

YEARS

SBI LIFE INSURANCE

ICICI PRUDENTIAL LIFEINSURANCE

YEAR SBI LIFE INSURANCE ICICI PRUDENTIAL

LIFE INSURANCE

MAR 2018

63.9

64.2

MAR 2019

66.4

65.0

MAR 2020

67.3

67.3

TABLE 5- PERSISTENCY RATIO % [49TH MONTH]

RATIO

32 | P a g e

Interpretation:

Graph 5 depicts that the 49th month persistency ratio (based on premium) has

increased from 63.9% in FY 2018 to 67.3% in FY 2020 in case of SBI Life Insurance

and from 64.2% in FY 2018 to 67.3% in FY 2020 in the case of ICICI Prudential Life

Insurance.

The 49th month persistency ratio is lower in SBI Life Insurance in the FY 2018, it

becomes higher than ICICI Prudential Life Insurance in the FY 2019 and then

becomes equal to ICICI Prudential Life Insurance in the FY 2020

4.4.4 SOLVENCY RATIO (%)

Solvency is a regulatory measure of capital adequacy. It is critical in determining any

organisation’s ability to meet future contingencies and fund growth plans. It defines how

good or bad an insurance company’s financial situation is on defined solvency norms. IRDAI

mandates a minimum solvency ratio of 150% to minimise bankruptcy risk. (Khatri, 2017)

Computation: The formula for calculating Persistency Ratio is:

Higher the solvency ratio, the greater the chances of policyholders claim getting paid.

Lower Solvency ratio indicates inability of the Company to pay claims and meet future

contingencies.

Significance of Solvency Ratio:

Solvency ratio is an indicator of a company’s financial capacity to meet both short-

term and long-term liabilities

Solvency ratio helps identify whether the company has enough buffer to settle all

claims in extreme situations.

Solvency Ratio = Available Capital

Required Capital

33 | P a g e

GRAPH 6- SOLVENCY RATIO %

Interpretation:

Graph 6 depicts that the solvency ratio of SBI Life Insurance witnessed an increasing

trend from 206% in the period 2017- 2018 to 213% in the period 2018- 2019, but in

the period 2019- 2020 that trend got reversed and the ratio declined to 195% whereas

there is a constant decrease in the solvency ratio of ICICI Prudential Life Insurance

from 252% in FY 2018 to 194% in FY 2020.

206 213

195

252

215

194

0

50

100

150

200

250

300

Mar-18 Mar-19 Mar-20

YEARS

SBI LIFE INSURANCE

ICICI PRUDENTIAL LIFEINSURANCE

YEAR SBI LIFE INSURANCE ICICI PRUDENTIAL

LIFE INSURANCE

MAR 2018

206

252

MAR 2019

213

215

MAR 2020

195

194

TABLE 6- SOLVENCY RATIO (%)

34 | P a g e

The Solvency ratio is higher in ICICI Prudential Life Insurance for the FY 2018 and

FY 2019 by 46% and 2% respectively whereas it is lower than SBI Life Insurance for

the FY 2020 by 1%.

4.2 HYPOTHESIS TESTING:

4.2.1 T –TEST

SBI LIFE

INSURANCE

ICICI PRUDENTIAL

LIFE INSURANCE

Mean 1.846667 0.95

Variance 0.005833 0.0336

Observations 3 3

Pearson Correlation 0.785714

Hypothesized Mean Difference 0

Df 2

t Stat 11.76255

P(T<=t) one-tail 0.003575

t Critical one-tail 2.919986

P(T<=t) two-tail 0.00715

t Critical two-tail 4.302653

Results

Since p is less than p< 0.05, H0 is rejected and hence it is proved that there is a significant

difference between Current Ratio of SBI Life Insurance and ICICI Life Insurance.

35 | P a g e

CHAPTER 5: RESULTS AND

DISCUSSIONS

5.1 Major Findings

5.2 Discussions & Suggestions

5.3 Conclusion

36 | P a g e

5.1 MAJOR FINDINGS:

The Insurance Sector is growing and grooming from subsequent past years

considering their achievements and financial reports of both the companies.

The Current Ratio of ICICI Prudential Life Insurance indicates that current liabilities

of the enterprise are greater than their current asset which means that the enterprise

would be unable to meet its short –term financial obligations if they become due.

ICICI Prudential is not in a good financial health.

The Current Ratio of SBI Life Insurance indicates that the current liabilities of the

enterprise are lower than their current asset which means that the enterprise would be

able to meet its short –term financial obligations if they become due. SBI Life

Insurance gives the evidence of sound liquidity position.

SBI Life Insurance has higher Current Ratio than ICICI Prudential Life Insurance

during the study period which shows that SBI Life Insurance has better Liquidity

Position than ICICI Prudential Life Insurance.

The Quick Ratios and Current Ratios of both the companies are same which means

that there are no inventories and prepaid expenses in both the firms.

There is a decline in the Net Profit Ratio during the study period of 3 years which

shows deterioration in the operational efficiency of both the firms.

The Net Profit Ratio is higher in SBI Life Insurance than ICICI Prudential Life

Insurance during the study period which shows that SBI Life Insurance is performing

its operations more efficiently than ICICI Prudential Life Insurance.

The 13th month persistency ratios are improved from what they were in FY18 which

reflects that there is a rise in the sale of both the companies Insurance policies.

ICICI Prudential Life Insurance has higher 13th month persistency ratio than SBI Life

Insurance during the study period which shows that there are more sales of ICICI

Prudential Life Insurance than SBI Life Insurance.

The 49th month persistency ratios are improved from what they were in FY18 which

implies that the associated policyholders are satisfied with the customer service,

customer loyalty, product utility, post sales service, returns on their product, product

portfolio, etc. and are renewing their policies even after commencement of the fourth

year.

37 | P a g e

Both the companies are at equal position in terms of 49th month persistency ratio for

the FY 2020 which shows that both the companies have same ability to retain their

customers in the particular year.

Both the Companies have a solvency ratio more than the mandatory requirement of

150% during the study period which shows that both the companies have enough

buffers to settle all claims in extreme situations.

Since p is less than p< 0.05, H0 is rejected and hence it is proved that there is a

significant difference between Current Ratio of SBI Life Insurance and ICICI Life

Insurance.

5.2 DISCUSSION AND SUGGESTIONS:

It is suggested to ICICI Prudential Life Insurance to raise extra finance to meet their

short-term financial obligations.

In my opinion, it will be beneficial to both the companies if they cut down their

expenses to increase their net profit as the study shows decline in their Net Profit

Ratio during the study period of 3 years.

Both the companies should look for the factors which are leading to deterioration of

their operational efficiency and taking necessary measures to counter them.

Since p is less than p< 0.05, H0 is rejected and hence it is proved that there is a

significant difference between Current Ratio of SBI Life Insurance and ICICI

Prudential Life Insurance.

5.3 CONCLUSION:

The study has aimed to examine the financial performance of Indian life insurance companies

i.e. SBI Life Insurance and ICICI Prudential Life Insurance through analysing the

determinants of their profitability. Performance of companies can affect economy as a whole

and therefore it requires empirical analysis to judge the performance. For measuring financial

performance, financial ratios such as Liquidity Ratio, Profitability Ratio, Persistency Ratio

and Solvency Ratio have been calculated. T-Test was also conducted to check if there was a

significant difference between the Current Ratio of SBI Life Insurance and ICICI Prudential

Life Insurance .The study evaluated that SBI Life Insurance have sound liquidity position and

ICICI Prudential Life Insurance is not in a good financial health. Profitability measure of SBI

Life Insurance is better than ICICI Prudential Life Insurance. But, there is a decline in the

38 | P a g e

Profitability Ratio during the study period which shows deterioration in the operational

efficiency of both the firms. Hence, both the firms needs to adopt immediate corrective

measures to arrest the downfall in the ratio .As far as 13th persistency ratio is concerned the

performance of ICICI Prudential Life Insurance is better than that of SBI Life Insurance but it

can be seen that SBI Life Insurance is trying to increase their ratio over the previous years

and has reached very near to the ratio of ICICI Life Insurance in FY 2020.Both the

companies are at equal position in terms of 49th month persistency ratio for the FY 2020

which shows that SBI Life Insurance is equally cable to retain their customers than that of

ICICI Prudential Life Insurance and is better in FY 2019 . From the analysis of T-Test

results, it is clear that there is a significant difference between Current Ratio of SBI Life

Insurance and ICICI Prudential Life Insurance .Thus, in the light of above findings, it can be

concluded that SBI Life Insurance is performing better than ICICI Prudential Life Insurance.

39 | P a g e

BIBLIOGRAPHY

Works Cited

Akotey, J. O., Sackey, F. G., Amoah , L., & Manso, R. F. (2013, May 17). The financial performance

of life insurance companies in Ghana. Journal of Risk Finance, 14(3), 286-302.

Bawa, D. K., & Chattha , S. (2013, November). Financial Performance of Life Insurers in Indian

Insurance Industry . Pacific Business Review International, 6(5), 44-52.

Gour, B., & Gupta , M. C. ( 2012, June). A Review on Solvency Margin in Indian Insurance

Companies. International Journal of Recent Research and Review, II, 43-47.

Mishra, K. K. (2015, September 9). Comparative Study Of Public and Private Life Insurance

Companies in India. International Journal of Research in Finance and Marketing, 5, 16-19.

Indian Insurance Industry Report . (2021, January). Retrieved from India Brand Equity Foundation:

https://www.ibef.org/industry/insurance-sector-india.aspx

A Brief Overview of the Insurance Sector. (n.d.). Retrieved from Investopedia:

https://www.investopedia.com/ask/answers/051915/how-does-insurance-sector-work.asp

Ayele, A. G. (2012, May). Factors Affecting Profitability of Insurance Companies in Ethiopia: Panel

Evidence. ” Doctoral Thesis, Addis Ababa University.

Bikker, J. A. (2012, November). Performance of the life insurance industry under pressure: efficiency,

competition and consolidation. Utrecht School of Economics, 12-19.

Bodla, D. B., Bodla, S., & Tondon, D. (2017 , September –October ). Profitability Performance of

Life Insurance Companies – A Study in Indian Context . Research gate International Journal

of Computing and Business Research, 7( 3).

Dar , S. A., & Bhat, J. A. (2015, April). A Comparative Evaluation of Financial Performance and

Soundness of Selected Public and Private Life Insurers in India. Pacific Business Review

International, 7(10), 55-64.

Dr.Parmasivan. (2015). A Comparative Study of Public and Private Life Insurance Companies in

India. 1(7), 15-18.

Greene, W. H., & Segal , D. (2004, May ). Profitability and Efficiency in the U.S. Life Insurance

Industry. Journal of Productivity Analysis, 21, 229–247.

40 | P a g e

Gulati , N. C., & Jain, C. M. (2011, OCTOBER ). Comparative Analysis of the Performance of All

the Players of the Indian Life Insurance Industry. VSRD International Journal of Business &

Management Research, 1( 8), 561-569.

Joshi, M. C., & Takodia, T. M. (2017, January 1). A Study of Recent Trend and Awareness &

Preferences in Life Insurance Sector in India. Research Gate, 144-159.

Khatri, Y. (2017, June 27). 6 ratios to know when buying insurance. Retrieved from The Economics

Times: https://economictimes.indiatimes.com/wealth/insure/6-ratios-to-know-when-buying-

insurance/articleshow/59297010.cms?utm_source=contentofinterest&utm_medium=text&ut

m_campaign=cppst

Kumari, T. H. (2013). Performance Evaluation of Indan Life Insurance Industry in Post

Liberalisation. International Journal of Social Sciences Arts and Humanities, 1, 7-14.

Life Insurance. (n.d.). Retrieved from Aegon Life: https://www.aegonlife.com/insurance-basics/life-

insurance/what-life-insurance

Malik, H. (2011, November). Determinants of Insurance Companies Profitability: An Analysis of

Insurance Sector of Pakistan . Academic Research International, 1(3), 315-321.

McKinsey. (2011). Retrieved from http://www.Thehindubusinessline.com/industry-and-

economy/banking/article2692453.ece.

Naidu, C. K., & Paramasivan, D. C. (2015, Sep). A Comparative Study of Public and Private Life

Insurance Companies in India. International Journal of Multidisciplinary Research Review,

pp. 15-18.

Neelaveni, V. (2012, March ). Financial Performance of Life Insurance Companies and Products .

Zenith International Journal of Business Economics & Management Research, 2(3 ), 233-

258.

Smajla, N. (2014). Measuring financial soundness of insurance companies by using CARAMELS

model–case of Croatia. Interdisciplinary Management Research, 10, 600-609.

Solanki, R. (2016, June). An Analytical Study Of Profitability Of Life Insurance Companies In India:

A Study Of Selected Private Sector Insurance Companies. Abhinav National Monthly

Refereed Journal of Research in Commerce & Management, 5(6), 8-12.

Vasavi, V., & Reddy, P. M. (2020). Earnings and Profitability Analysis of Life Insurance Companies-

Comparative Study of ICICI Prudential and SBI Life Insurance Companies. International

Management Review, 16(2), 76-84.

41 | P a g e

Websites:-

https://www.moneycontrol.com/financials/iciciprudentiallifeinsurancecompany/profit-

lossVI/IPL01#IPL01

https://www.moneycontrol.com/financials/sbilifeinsurancecompany/balance-sheetVI/SLI03

https://www.sbilife.co.in/sites/SBILife/Annual-Report/FY2019-

20/pdf/SBI%20Life%20IR%202020.pdf

https://www.iciciprulife.com/about-us/investor-relations/financial-information.html

https://en.wikipedia.org/wiki/ICICI_Prudential

https://en.wikipedia.org/wiki/SBI_Life_Insurance_Company

https://byjus.com/commerce/liquidity-ratio/

https://groww.in/p/current-ratio/

https://byjus.com/commerce/profitability-ratios/

Books: -

Management Accounting by Dr. S.P. Gupta and Dr. K.L. Gupta, Sahitya Bhawan

Publication.

42 | P a g e

ANNEXURE

43 | P a g e

SBI Life Insurance

Company Ltd.

Balance Sheet

------------------- in Rs. Cr. -------------------

Mar 20 Mar 19 Mar 18

12 months 12 months 12 moths

EQUITIES AND LIABILITIES

SHAREHOLDER'S FUNDS

Equity Share Capital 1,000.03 1,000.00 1,000.00

Total Share Capital 1,000.03 1,000.00 1,000.00

Reserves and Surplus 7,743.06 6,576.36 5,527.82

Total Reserves and Surplus 7,743.06 6,576.36 5,527.82

Total Shareholders Funds 8,743.08 7,576.36 6,527.82

NON-CURRENT LIABILITIES

Other Long Term Liabilities 80,374.58 74,829.34 62,069.86

Long Term Provisions 73,440.22 60,592.14 49,558.08

Total Non-Current Liabilities 153,814.81 135,421.48 111,627.95

CURRENT LIABILITIES

Other Current Liabilities 2,783.79 3,377.13 3,216.13

Short Term Provisions 238.51 358.88 348.54

Total Current Liabilities 3,022.30 3,736.01 3,564.67

Total Capital And Liabilities 165,580.19 146,733.85 121,720.44

ASSETS

NON-CURRENT ASSETS

Tangible Assets 567.99 563.37 581.29

Capital Work-In-Progress 13.19 31.85 0.00

Fixed Assets 581.18 595.22 581.29

Non-Current Investments 158,813.21 139,324.71 114,435.87

Long Term Loans And Advances 364.48 172.50 170.90

Total Non-Current Assets 159,758.88 140,092.44 115,188.06

CURRENT ASSETS

Current Investments 0.00 0.00 0.00

Cash And Cash Equivalents 1,423.23 2,420.63 2,644.63

Short Term Loans And Advances 4,398.08 4,220.78 3,887.75

Other Current Assets 0.00 0.00 0.00

Total Current Assets 5,821.31 6,641.41 6,532.37

Total Assets 165,580.19 146,733.85 121,720.44

44 | P a g e

SBI Life Insurance Company Ltd.

Profit & Loss Account (in Rs. Cr.)

Mar 20 Mar 19 Mar 18

12 months 12months

12

months INCOME

Revenue From Operations [Gross] 1,939.35 1,504.16 1,281.47

Less: Excise/Service Tax/Other Levies 0.00 0.00 0.00

Revenue From Operations [Net] 1,939.35 1,504.16 1,281.47

Total Operating Revenues 1,939.35 1,504.16 1,281.47

Other Income 6.79 13.54 11.47

Total Revenue 1,946.14 1,517.70 1,292.93

EXPENSES

Cost Of Materials Consumed 0.00 0.00 0.00

Operating And Direct Expenses 0.00 0.00 0.00

Changes In Inventories Of FG,WIP And Stock-In Trade 0.00 0.00 0.00

Employee Benefit Expenses 0.00 0.00 0.00

Finance Costs 0.00 0.00 0.00

Depreciation And Amortisation Expenses 0.39 0.62 0.30

Other Expenses 524.19 128.29 107.43

Total Expenses 532.59 144.83 108.47

Profit/Loss Before Exceptional, Extra Ordinary Items And Tax 1,413.55 1,372.86 1,184.46

Exceptional Items 0.00 0.00 0.00

Profit/Loss Before Tax 1,413.55 1,372.86 1,184.46

Tax Expenses-Continued Operations

Current Tax -8.63 46.07 34.07

Less: MAT Credit Entitlement 0.00 0.00 0.00

Deferred Tax 0.00 0.00 0.00

Tax For Earlier Years 0.00 0.00 0.00

Total Tax Expenses -8.63 46.07 34.07

Profit/Loss After Tax And Before Extra-Ordinary Items 1,422.18 1,326.80 1,150.39

Profit/Loss From Continuing Operations 1,422.18 1,326.80 1,150.39

Profit/Loss For The Period 1,422.18 1,326.80 1,150.39

OTHER ADDITIONAL INFORMATION

EARNINGS PER SHARE

Basic EPS (Rs.) 14.22 13.27 11.50

Diluted EPS (Rs.) 14.22 13.27 11.50

VALUE OF IMPORTED AND INDIGENIOUS RAW

MATERIALS STORES, SPARES AND LOOSE TOOLS Imported Raw Materials 0.00 0.00 0.00

Indigenous Raw Materials 0.00 0.00 0.00

STORES, SPARES AND LOOSE TOOLS

Imported Stores And Spares 0.00 0.00 0.00

Indigenous Stores And Spares 0.00 0.00 0.00

DIVIDEND AND DIVIDEND PERCENTAGE

Equity Share Dividend 0.00 200.00 200.00

Tax On Dividend 0.00 41.11 40.72

Equity Dividend Rate (%) 0.00 20.00 20.00

45 | P a g e

ICICI Prudential Life Insurance

Company Ltd.

Balance Sheet (in Rs. Cr.)

Mar 20

Mar 19

Mar 18

12 months 12 months 12 months

EQUITIES AND LIABILITIES

SHAREHOLDER'S FUNDS

Equity Share Capital 1,435.86 1,435.78 1,435.50

Total Share Capital 1,435.86 1,435.78 1,435.50

Reserves and Surplus 5,782.76 5,587.63 5,427.46

Total Reserves and Surplus 5,848.28 5,610.95 5,448.95

Total Shareholders Funds 7,284.14 7,046.74 6,884.45

NON-CURRENT LIABILITIES

Long Term Borrowings 0.00 0.00 0.00

Deferred Tax Liabilities [Net] 0.00 0.00 0.00

Other Long Term Liabilities 57,383.98 48,679.61 39,176.87

Long Term Provisions 88,036.75 103,699.85 92,312.36

Total Non-Current Liabilities 145,420.73 152,379.47 131,489.23

CURRENT LIABILITIES

Short Term Borrowings 0.00 0.00 0.00

Trade Payables 0.00 0.00 0.00

Other Current Liabilities 3,302.86 3,638.62 3,425.41

Short Term Provisions 27.53 25.51 22.18

Total Current Liabilities 3,330.39 3,664.13 3,447.60

Total Capital And Liabilities 156,035.26 163,090.33 141,821.28

ASSETS

NON-CURRENT ASSETS

Tangible Assets 457.27 462.76 404.48

Intangible Assets 0.00 0.00 0.00

Capital Work-In-Progress 20.35 12.86 17.58

Other Assets 0.00 0.00 0.00

Fixed Assets 477.62 475.62 422.06

Non-Current Investments 151,256.20 159,008.54 138,540.11

Deferred Tax Assets [Net] 0.00 0.04 0.05

Long Term Loans And Advances 463.09 270.19 145.06

Other Non-Current Assets 0.00 0.00 0.00

Total Non-Current Assets 152,196.90 159,754.39 139,107.28

CURRENT ASSETS

Current Investments 0.00 0.00 0.00

Inventories 0.00 0.00 0.00

Trade Receivables 0.00 0.00 0.00

Cash And Cash Equivalents 810.56 661.02 203.74

Short Term Loans And Advances 3,027.80 2,674.92 2,510.26

Other Current Assets 0.00 0.00 0.00

Total Current Assets 3,838.36 3,335.94 2,714.00

Total Assets 156,035.26 163,090.33 141,821.28

46 | P a g e

ICICI Prudential Life Insurance Company Ltd. Profit & Loss account (in Rs. Cr.)

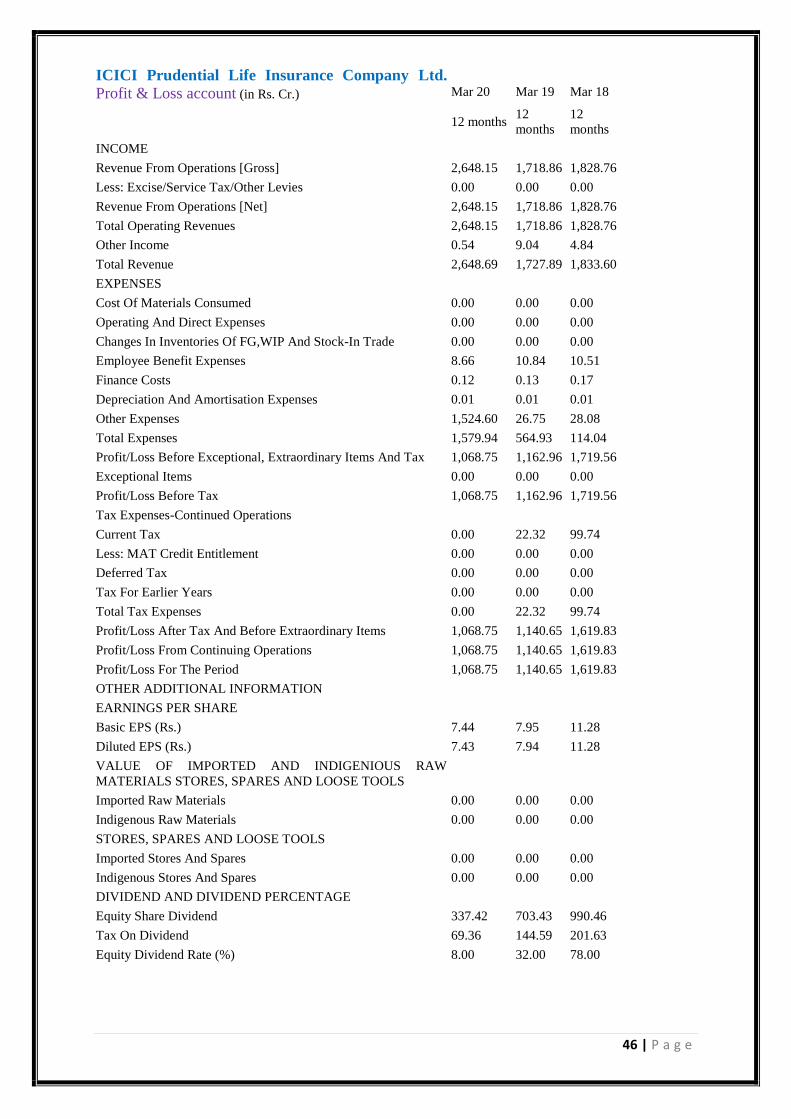

Mar 20

Mar 19

Mar 18

12 months 12

months

12

months

INCOME

Revenue From Operations [Gross] 2,648.15 1,718.86 1,828.76

Less: Excise/Service Tax/Other Levies 0.00 0.00 0.00

Revenue From Operations [Net] 2,648.15 1,718.86 1,828.76

Total Operating Revenues 2,648.15 1,718.86 1,828.76

Other Income 0.54 9.04 4.84

Total Revenue 2,648.69 1,727.89 1,833.60

EXPENSES

Cost Of Materials Consumed 0.00 0.00 0.00

Operating And Direct Expenses 0.00 0.00 0.00

Changes In Inventories Of FG,WIP And Stock-In Trade 0.00 0.00 0.00

Employee Benefit Expenses 8.66 10.84 10.51

Finance Costs 0.12 0.13 0.17

Depreciation And Amortisation Expenses 0.01 0.01 0.01

Other Expenses 1,524.60 26.75 28.08

Total Expenses 1,579.94 564.93 114.04

Profit/Loss Before Exceptional, Extraordinary Items And Tax 1,068.75 1,162.96 1,719.56

Exceptional Items 0.00 0.00 0.00

Profit/Loss Before Tax 1,068.75 1,162.96 1,719.56

Tax Expenses-Continued Operations

Current Tax 0.00 22.32 99.74

Less: MAT Credit Entitlement 0.00 0.00 0.00

Deferred Tax 0.00 0.00 0.00

Tax For Earlier Years 0.00 0.00 0.00

Total Tax Expenses 0.00 22.32 99.74

Profit/Loss After Tax And Before Extraordinary Items 1,068.75 1,140.65 1,619.83

Profit/Loss From Continuing Operations 1,068.75 1,140.65 1,619.83

Profit/Loss For The Period 1,068.75 1,140.65 1,619.83

OTHER ADDITIONAL INFORMATION

EARNINGS PER SHARE

Basic EPS (Rs.) 7.44 7.95 11.28

Diluted EPS (Rs.) 7.43 7.94 11.28

VALUE OF IMPORTED AND INDIGENIOUS RAW

MATERIALS STORES, SPARES AND LOOSE TOOLS

Imported Raw Materials 0.00 0.00 0.00

Indigenous Raw Materials 0.00 0.00 0.00

STORES, SPARES AND LOOSE TOOLS

Imported Stores And Spares 0.00 0.00 0.00

Indigenous Stores And Spares 0.00 0.00 0.00

DIVIDEND AND DIVIDEND PERCENTAGE

Equity Share Dividend 337.42 703.43 990.46

Tax On Dividend 69.36 144.59 201.63

Equity Dividend Rate (%) 8.00 32.00 78.00

Related Documents