As part of our commitment to continuous process improvement and cost reduction of our valued client, we’re now driving of global processes. A business case for transactional services of F&A Outsourcing – P2P, O2C, R2R Marvin R. Panlican

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

As part of our commitment to continuous

process improvement and cost reduction of

our valued client, we’re now driving of

global processes.

A business case for

transactional services

of F&A Outsourcing –

P2P, O2C, R2R

Marvin R. Panlican

Business Case Page 1

I. Introduction

Any Finance and Accounting Professional has a set of primary concerns – optimizing

expenditure, lowering costs and getting the maximum benefit for the expense made.

Transformational Finance and Accounting solutions are the order of the day. With F&A

solutions offered today, you can reduce overall cost, optimize the use of resources and

technology for the company benefit, manage cash inflow and outflow in the best manner possible

and also adhere to the necessary compliance while you do this.

Whether you need to streamline, optimize or transform your organizations Finance and

Accounting function, you need access to world class processes and technology in the perfect

blend to achieve this goal. Best F&A Outsourcing offers services methodology, not only help in

identifying gaps in your current process, but also ensure a smooth and risk-free transformation.

F&A Outsourcing must also consider best solution by using the well-defined operational metrics

like productivity, turn-around-time and accuracy that keep you in control. You also have access

to a 24/7 Helpdesk that makes certain that you have complete and comprehensive support.

This study gives you better insights into your processes that leverage Analytics and

giving you a holistic yet deep view of the processes and fosters decision making. Moreover, it

covers the best solutions of complete Procure to Pay (P2P), Order to Cash (O2C), and Record to

Report (R2R) processes including solutions for Accounts Payable, Accounts Receivable and

General Accounting.

II. Facts of the Case

Procure to Pay

Procure-to-pay processes involve all stages of a business’ transactions and are integral to

overall enterprise efficiency. Organizations face a number of challenges with these processes that

can affect profitability, compliance, and efficiency, including profit recovery, process

automation, and process optimization.

Business Case Page 2

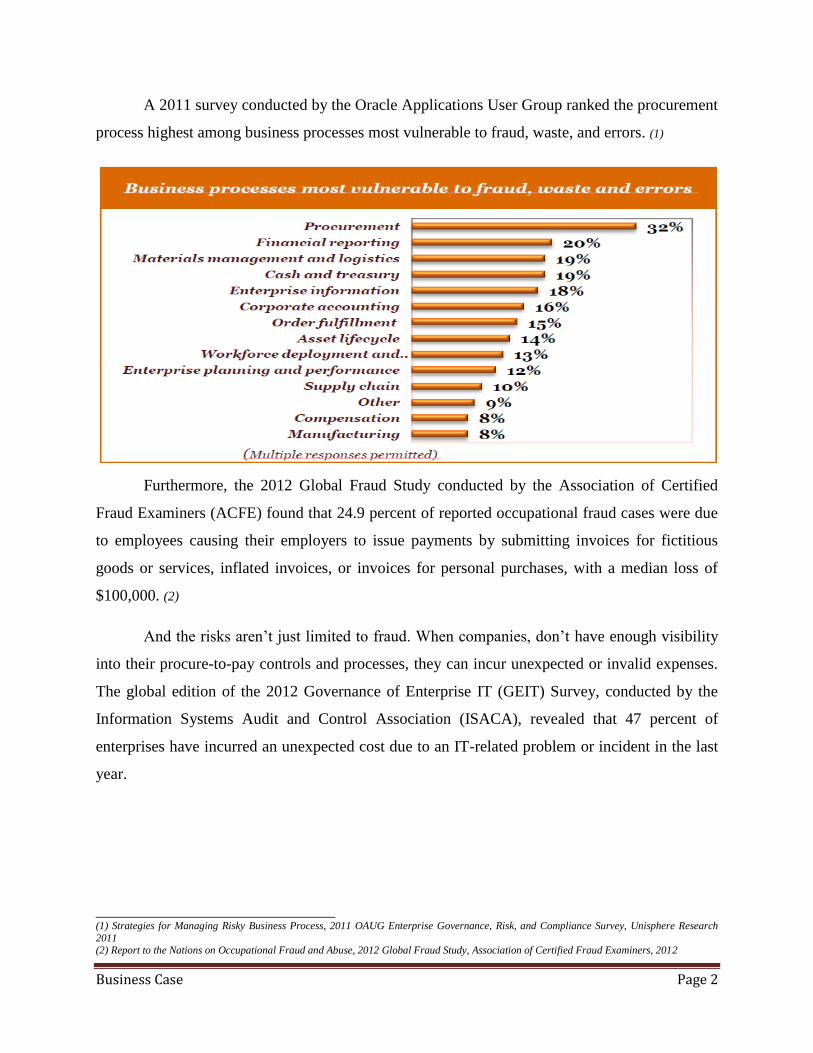

A 2011 survey conducted by the Oracle Applications User Group ranked the procurement

process highest among business processes most vulnerable to fraud, waste, and errors. (1)

Furthermore, the 2012 Global Fraud Study conducted by the Association of Certified

Fraud Examiners (ACFE) found that 24.9 percent of reported occupational fraud cases were due

to employees causing their employers to issue payments by submitting invoices for fictitious

goods or services, inflated invoices, or invoices for personal purchases, with a median loss of

$100,000. (2)

And the risks aren’t just limited to fraud. When companies, don’t have enough visibility

into their procure-to-pay controls and processes, they can incur unexpected or invalid expenses.

The global edition of the 2012 Governance of Enterprise IT (GEIT) Survey, conducted by the

Information Systems Audit and Control Association (ISACA), revealed that 47 percent of

enterprises have incurred an unexpected cost due to an IT-related problem or incident in the last

year.

______________________________ (1) Strategies for Managing Risky Business Process, 2011 OAUG Enterprise Governance, Risk, and Compliance Survey, Unisphere Research

2011 (2) Report to the Nations on Occupational Fraud and Abuse, 2012 Global Fraud Study, Association of Certified Fraud Examiners, 2012

Business Case Page 3

Order to Cash

The order to cash cycle is the financial lifeblood of any organization. Not only does it

determine how quickly an order from a customer is translated into cash in the bank, it also

determines the customer experience and perception of the service provider. This is further

compounded by challenges such a price pressures, cost pressures, increasing stakeholder value

that are often seem contradictory in nature. All these aspects make it imperative for an

organization to focus on having a best-in-class Order-to-Cash Cycle.

Moreover, financial loss due to fraud and error is a growing problem for organizations. A

recent survey by the Association of Certified Fraud Examiners (ACFE) estimates that the

average organization loses 5% of its revenues to fraud each year. Applied to the 2011 Gross

World Product, this figure translates to a potential projected annual fraud loss of more than $3.5

trillion. However the costs to an organization due to fraud and error are not just financial; there

are intangible costs as well, with potentially far greater consequences, such as negative goodwill,

loss in public confidence and brand value. One of the business processes where there is

considerable potential for fraud and error is in the order to cash cycle. Order-to-cash is a set of

business processes that involve receiving and fulfilling customer sales for goods or services. An

Order-to-cash cycle consists of multiple sub-processes including: customer order is documented,

order is fulfilled or service is scheduled, order is shipped to customer or service is performed,

invoice is created and sent to customer, customer sends payment/collection, and payment is

recorded in general ledger.

A challenging economy is partly to blame. Steady reductions in headcount have stretched

workforces already under pressure to work harder and faster with limited resources - increasing

the possibility of error. Reduced headcount can also lead to fraud through excessive access to

data. With limited resources to complete processes, appropriate segregation of duties (SOD) is

not always possible. With fewer employees to segregate access, the remaining employees are

likely to have excess access to data, resulting in higher exposure for fraud to be committed.

Financial pressures on individuals have added to the risk of fraud as previously exemplary

employees succumb to temptation. An ACFE report says that approximately 87% of

occupational fraudsters had never been charged or convicted of a fraud related offense. Rampant

growth in transaction volumes compounded by increased business complexity has also made

Business Case Page 4

organizations more susceptible to error and fraud as they struggle to cope with the workload and

fraudsters exploit loopholes in systems, safe in the knowledge that massive transaction volumes

will potentially mask their activity. Finally, increases in cross-border trading, together with the

lengthening of supply chains has introduced greater risk of fraud and error as companies struggle

to maintain visibility to core financial processes and to implement sufficient business controls in

remote locations. It is clear that if left unchecked, fraud and error in the OTC cycle may pose a

significant cost and risk to the business. This can manifest itself in several detrimental ways,

such as the inability to respond confidently to compliance challenges, the impairment of profit

margins, a reduction in cash flow and operational inefficiency.

Record to Report

Finance and accounting professionals who manage corporate financial reporting and

disclosures are well aware of the amount of time and effort it takes to do the job well. Pressure to

meet deadlines to prepare quality financial statements and reports and to satisfy regulatory

reporting requirements—the Sarbanes-Oxley Act of 2002 (SOX), 2009 XBRL (eXtensible

Business Reporting Language) Reporting Mandate of the Securities & Exchange Commission

(SEC), and the Dodd-Frank Act of2010—means that finance and accounting departments are

constantly overloaded. Anyone who works in the field, or knows people who do, has heard the

war stories about how much work it takes to complete the reporting.

There is no firm definition of the Record-to-Report process, but it is widely

acknowledged to encompass the sequence of activities surrounding the ‘period close’ in

subsidiaries; the collection of year-to-date balances (or monthly movements) at a summary level;

their consolidation according to merger or equity accounting rules and subsequent reporting to a

variety of internal and external stakeholders, in a mixture of manual and electronic (e-filing)

formats.

Business Case Page 5

The diagram above illustrates the typical timescales for the Record-to-Report Process

Although the R2R process is similar across industry sectors and follows a well-trodden

path each reporting period, many finance organisations still face serious challenges in the area of

financial governance.

For example, 15% of global businesses say that they have missed statutory deadlines for

filings due to late changes to charts of accounts, exposing their companies to the risk of financial

penalties and damaging falls in their share price. 88% have experienced delays in the last 12

months when executing financial close, reporting and filing.

III. Problem Statement

Business Case Page 6

As more companies are seeking to move beyond procurement into fully deployed supply

chain systems, a key challenge for many companies is in the area of improving efficiency in their

procure to pay cycle for many of their contracted services, especially in the area of facilities

maintenance and on-site contract management. There exist multiple challenges in environments

where field associates are working from manual or electronic systems, requisitioning on-site

services for maintenance or other activities, and ensuring that this information is captured

effectively. In addition, there exist significant challenges to ensure that the proper service level

agreement is fulfilled, the correct price is charged, the purchase order is transmitted correctly, the

invoice matches, and finally, that the supplier is paid the correct amount for the actual services

delivered. While many enterprise systems claim that these elements are simply defined within

their structural logic, the truth is that there are many opportunities for error, and that without a

planned process for managing the procure to pay cycle, that the organization may be bearing

significant costs due to non-compliance to system or process requirements.

On the other hand, consumer products companies face increasing challenges around

management of the order-to-cash process. These include the ability to effectively manage high

order volumes and to deal with a high level of deductions. The challenges also include

optimizing and understanding trade promotions spend that is required for category success and

consumer adoption. Risk management is also challenging, particularly in the current economic

climate. In the case of credit risk, for example, it is hard to be confident that credit levels are

right, even for long-established and trusted customers. Any customer, including the largest brick-

and-mortar entities, can pose risks that can only be understood with deep trending and analytics.

Moreover, there is no firm definition of the Record-to-Report process, but it is widely

acknowledged to encompass the sequence of activities surrounding the ‘period close’ in

subsidiaries; the collection of year-to-date balances (or monthly movements) at a summary level;

their consolidation according to merger or equity accounting rules and subsequent reporting to a

variety of internal and external stakeholders, in a mixture of manual and electronic (e-filing)

formats.

IV. Issues

Business Case Page 7

These are the following challenges that may arise in Procure to pay, Order to Cash, and

Record to report;

Procure to pay

Procure-to-pay processes involve all stages of a business’ transactions and are integral to

overall enterprise efficiency. Organizations face a number of challenges with these processes that

can affect profitability, compliance, and efficiency, including profit recovery, process

automation, and process optimization.

Profit Recovery - One of the most consistent problems organizations face in the

procure-to-pay process is undetected financial leakage. Companies often fail to realize

the efficiencies that can be gained through the automation of key business processes. For

example, invoice payments are typically reviewed through a system of manual approvals.

This process is not only time consuming, but it can also fail to take advantage of early

payment discounts or avoid late payment penalties. Furthermore, a manual approval

process leaves the door open to potential fraud through post-approval modifications.

Another example of financial leakage is the reimbursement of employee expenses. Many

companies use a manual process to reimburse funds outside of their current systems,

which leaves them at risk of unpaid or duplicate payments, or payments being made for

expenses that have not been properly approved or vetted. At the other end of the

spectrum, inconsistent and stale master data across business units often impedes the

procurement process and creates unnecessary risk to financial integrity. The absence of

common or centralized master data—or lack of automation in approving, recording, and

reviewing master data on a regular basis—often makes master data fragmented and

unreliable, and impairs visibility and optimization of the procure-to-pay process. A good

example of this issue is found with the maintenance of vendor records. Companies

typically have multiple employees with access to the vendor master and they often

duplicate supplier entries in a system. Unfortunately, the data cleansing process is

commonly overlooked and typically occurs on an ad-hoc basis. Without better control of

vendor master data, the chance of fraud, mismanagement of funds, and/or financial

leakage remains significant. Finally, companies often fail to account for the elevated

risks that result from poor segregation of roles and responsibilities, as well as,

Business Case Page 8

unrestricted access to sensitive data. Most access to sensitive data and segregation of

duties analysis occurs on an annual basis and with little resolution. While this may be

sufficient for most year-end audits, it fails to provide the continuous control over

segregation of duties and access to sensitive data. In today’s business environment,

companies face high attrition rates and manage employees with frequently shifting roles

and responsibilities, so access control violations can go unnoticed for weeks, possibly

months, before being picked up. Furthermore, employees are often found to have access

to highly sensitive data that should be strictly monitored and restricted, yet companies

repeatedly fail to notice this until it is too late.

Process Automation - Since the procure-to-pay process is critical to every

organization, it is paramount that the process be as efficient and effective as possible, and

not a source of vulnerability. When you consider automation, the most basic aspects

would be automating transactions, managing the flow of information, and routing

approvals, while the more advanced aspects would include matching, vendor validation,

and alternate approvals. Today, many companies are not taking full advantage of

automating the procure-to-pay process, which could help tighten controls, lower resource

needs for manual validations and processing data inputs, which in turn lowers the risk of

errors that are inevitable with high volumes of manual inputs. One of the main reasons

companies are not fully leveraging opportunities to automate the procure-to-pay process

is simply limited visibility. Management lacks visibility into what data is available from

other departments, what controls could be implemented, and what processes can be

combined to increase efficiency and reduce risk. An example of this is automated

workflows that are either not used or not configured to support a growing company.

Workflows that aren’t configured to leverage the HR structure as the single source of

truth, for example, don’t automatically reflect any personnel changes in the HR structure,

and therefore fail to ensure that documents and approval needs are routed to appropriate

reviewers. By configuring the workflows appropriately, you can eliminate the need for

manual rerouting of approval requests, automatically sending them to a new purchasing

manager, for instance, if the initially assigned purchasing manager has moved on to a

different role, or has left the company. Another example is the failure to define and set

up automated matching rules to prevent financial loss between purchasing, receiving, and

Business Case Page 9

accounts payable. Companies typically have various types of matching within each

department (e.g., procurement analyst matches the requisition against the purchase order

before submitting it to vendors, receiving matches the purchase order to the packing slip

before completing receipt and sending to accounts payable, accounts payable matches the

purchase order to the invoice before making the payment). Manual matching for every

transaction not only consumes a lot of time and resources, but it is also error-prone.

Automated matching can help consolidate the various matching rules within each

individual department, as well as streamline and accelerate the matching process.

Matching rules can be defined to fit the needs of all three departments and provide

processing constraints to prevent further processing if a transaction fails the matching

requirements. This will free up time to focus on reviewing and resolving the true

exceptions identified from the automated matching process. The review and resolution

are critical in this process. While automation can help prevent unwanted transactions and

data from flowing through the procure-to-pay process, it is management's responsibility

to promptly review and resolve issues in order to avoid financial leakage that could be

caused by not processing transactions in a timely manner. For example, processing of a

purchase order may be time-sensitive to the requestor, and delays could lead to delays in

other projects or payments resulting in the accrual of late fee penalties.

Process Optimization - Another big challenge companies face is business-process

optimization. When it comes to optimizing the procure-to-pay process, the focus shifts to

higher value-add activities like cultivating optimal payables strategies with real-time

supplier and banking information exchange, centralized master data management,

workflow-driven approvals management, and global, electronic payment capabilities.

However, because most companies departmentalize different stages of the procure-to-pay

process, they miss the opportunities and value associated with process optimization. A

typical scenario might be when an individual employee initiates a requisition specifying

what product and vendor they want to purchase from, the requisition is approved by the

reporting manager, and the approved requisition is sent to the purchasing department for

processing. If the purchasing department is centralized, chances are someone will

forecast purchasing needs or consolidate requisitions from different departments,

subsidiaries, or geographical locations to strategically select vendors, take advantage of

Business Case Page 10

volume pricing, and initiate competitive bids with various vendors. Use of master data to

store pricing plans with different vendors and incentives offered by various vendors

allows the company to take advantage of the best deals available to meet purchasing

needs and assist with contract and price negotiations. In summary, decentralized

purchasing and inconsistencies in the purchasing process across different departments,

subsidiaries, or geographical locations become a challenge when you’re trying to control

financial leakage. This is more challenging for companies that do not enforce a

centralized single source of truth for master data. Multiple master data sources cause

challenges for enforcing consistent purchasing policies, process optimization, and

automation for the enterprise across different business units. Finally, the lack of

automation will lead to workarounds and increase the need for manual compensating

controls which then decrease effectiveness of automated controls applied in upstream

processes.

Order to Cash

Increasing pressure to;

Reduce time to market the product and services

Improve the margin

Retain existing customers and attract new ones

Price Pressures with reducing tariffs/costs

High cost of business processes

Varied statutory and compliance requirements across different countries/regions

Varied supplier/vendor performance and agreements across different regions

Record to Report

Data Posting Errors – can be result of a number of factors including;:

o Errors from accounting systems - Transactions posting from accounting

systems might not post to the appropriate accounts, or significant

transaction data points might be missing after the interface has processed.

These errors can be the result of an inaccurate or incomplete setup of the

Business Case Page 11

accounting system process. Management would be required to research

and resolve these errors before the closing process would be complete.

Part of the challenge in resolving posting issues from accounting systems

is helping ensure compliance with corporate policy. The resolution of

posting issues might require updating the original transaction in the source

system instead of making the adjustments directly in the target system.

Additional time would be required to help ensure those transactions are

updated according to policy prior to resubmission.

o Posting transactions to prior closed periods - Prior period posting of

transactions can be problematic. Over the course of the period, previously

unrecorded transactions might be identified and need to be entered in the

period they were incurred. Period management tends to be a very manual

process with limited visibility.

Allocation set-up errors - The process of setting up general ledger allocation

journal entries and running them should be a controlled process much like code

development. Accounting activity requiring allocating journal entries should be

well researched and planned. The use of ERP native or additional advanced

controls cannot take the place of the research needed to create allocations. Good

processes augmented with native ERP and advanced controls, support accurate

and well-controlled accounting.

Allocation formulas should be documented, well tested, and approved

through user acceptance. The schedule by which those allocations are generated

should also be documented and tested. This testing will help ensure that

dependent data from preceding transactions is captured and subsequent and

dependent transactions are created and posted accurately. Once approved, the

allocation formulas and the associated schedules should be restricted from further

update.

Business Case Page 12

General ledger reconciliation process - General ledger reconciliation can be a

difficult and time consuming process. Quite often, clear ownership and

responsibility for accounts has not been established. This lack of ownership can

lead to unauthorized journal entries being posted to sensitive accounts making the

GL reconciliation process long and difficult.

When the organization makes use of suspense accounting, reconciliation

issues can even be further exacerbated. Financial services organizations, in

particular, make frequent use of suspense accounting. Depending on the

accounting system, some suspense accounts are controlled by the system directly,

whereas other accounts can accept manual journal entries. These suspense

accounts can be misused if good ownership and oversight are not in place.

Knowing critical suspense accounts in use and the volume of transactions

affecting these accounts helps management prioritize and plan its reconciliation

for an efficient close process.

General ledger consolidation - The consolidation process can produce unexpected

results during financial reporting. The consolidation activities might highlight

some unusual activity once the preliminary financial statements are generated.

Possible causes of these issues could include data errors during the consolidation

process, inadequate drill- down capability for detail analysis, or even adjusting

entries were either unauthorized, not justified, or inaccurate.

General ledger master data maintenance - Organizations face challenges with

general ledger master data errors and complexity due to limited data standards and

incomplete understanding of master data change impacts. These challenges are

further complicated by the lack of segregation between master data maintenance

and daily transaction processing, allowing users to add/modify GL segment

values when entering the transactions without considering the impacts to other

areas of record-to-report process (e.g., FSG account range, consolidation

mapping, and reconciliation effort).

Business Case Page 13

V. Recommendations and Action Plans

High-risk activities and high impact to profits - Advanced financial controls provide out-of-the

box as well as configurable content to oversee the entire procure-to-pay (P2P) business process

and satisfy needs of P2P practitioners, auditors, and IT staff. In the P2P process, potential

vendors are identified, contracts and terms are negotiated, and supplier profiles are setup as

master data. The establishment of a vendor master and other master data provides a consistent set

of information, and rules that adhere to and support the enterprises policies, procedures, terms,

and agreements. It is strongly recommend that organizations take the time to standardize on a

single vendor master and the appropriate policies and procedures for their organization up front.

It is then critical for organizations to carefully and periodically monitor for changes made to

supplier data and assess the accuracy of the data.

A myriad of scenarios could cause errors—as well as potential fraud and abuse—that

result in significant realized financial losses, especially if they go undetected over an extended

length of time. Advanced financial controls can oversee the maintenance to vendor data such as

potential duplicate vendors in the system. Duplicates entered by different users can go

undetected because of differences in spelling of supplier names or other key data fields.

Transaction Controls Governor (TCG), in Oracle, can compare and find suppliers that have

similar—but different—spelling, perhaps as a result of abbreviations or simple transposition

errors. This same ETCG control can also find vendor data matches on other fields including tax

identification, address, bank routing information, and so forth, increasing the probability that the

vendor is a duplicate. Without these controls in place, overtime errors are likely to be introduced

into the procurement and payment processes, resulting in real financial losses that will incur

additional time and expenses to recover.

Another red flag that owners of vendor master data should be watching for are frequent

updates to a particular vendor or vendors for a particular buyer. Configuration Controls Governor

(CCG) monitors changes to vendor, accounts payable, and purchasing setup configuration data

including address, bank routing information, receipt and purchase order dates, payment terms

including discounts, and tax information. CCG will produce ‘snapshots’ of before and after

Business Case Page 14

values that are updated. An ‘audit trail’ will provide answers to who, what, and when the updates

were made. With visibility into frequent changes to P2P setup data, procurement rules and

payment terms manipulation may alert managers to fraudulent activity and should be further

investigated to determine the root cause.

Of course, having proper user roles and segregation of responsibilities will significantly

help mitigate loss by blocking users from setting up combinations of financially harmful

scenarios. Application Access Controls Governor (AACG) provides visibility of users’ access

all the way down to individual P2P menus and submenus, and maps the entire security in a

graphical interface, which provides an efficient means for analysis and remediation. For

example, a user such as a buyer should not be setting up or changing vendor master data and then

executing purchase orders or even payments to those same vendors.

There are many ways financial results can be negatively affected through schemes such

as creating a purchase order on-the-fly as goods or services are received that would ordinarily

require a lead-time. These high-risk P2P activities could circumvent hard-won negotiated

agreements, including pricing. Using advanced financial controls in concerned with delivered

ERP system configurations provides a highly effective controls environment while allowing

efficient processing of compliant P2P transactions. For instance, CCG may monitor vendor and

temporary changes to order-to-delivery lead-times, TCG can detect transactions where purchase

orders are created or modified on or about the same day as the goods are received, and AACG

can ensure policies are in place where a user cannot both create or modify purchase order and

receive goods.

Increasing automation to improve audit efficiency and timely detection - Advanced financial

controls empower the P2P organization and the audit staff in a number of ways. There are

limited resources to audit and assure the enterprise that P2P activities are performed in

accordance with established policies. Advanced financial controls are fully automated and

companies are rapidly moving from resource-intensive manual controls to automated controls.

The automation includes the scheduling of controls for periodic testing and monitoring of P2P

setup and configurations, users responsibilities, P2P transactions, as well as capturing inline P2P

Business Case Page 15

transactions in real-time to prevent committing transactions before they have been properly

reviewed and approved.

Manual controls are typically prioritized tightly and heavily dependent on available audit

staff and P2P resources. Because of this, monitoring and manual sampling of transactions may

have to be restricted to higher cost, low volume activities at the expense of high-volume

transactions, but the latter can quickly accumulate in significant financial risk and exposure.

Automation affords more scope and breadth of testing controls, monitoring more P2P activities

and providing a greater level of assurance to company stakeholders.

As incidents are inevitably identified, advanced financial controls employ a multi-user

workflow and remediation process that will alert and notify the necessary P2P stakeholders. The

tracking and reporting of incident status and aging delivers the visibility necessary to manage

high-risk P2P activities.

Audit time and effort can be greatly reduced when internal audit and line-of-business

users can setup and monitor their P2P activities, including producing their own evidence of

control effectiveness. Supporting evidence can be produced in advance of the audit engagement

and used by external auditors, thereby reducing fees paid to perform these tasks.

Clearly, effective oversight will require executives to anticipate changes to evolve and

keep pace with innovation. System software with complete process will continue to be a vital

solution and active player in managing P2P risks and providing the flexible, advanced controls

that prevent errors and financial leakage by monitoring configurations, users, and transactions.

Related Documents