Telecom Italia Group 9M 2014 Results TELECOM ITALIA GROUP 9M 2014 Results Rome, November 7th, 2014 Piergiorgio Peluso Marco Patuano

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Telecom Italia Group9M 2014 Results

TELECOM ITALIA GROUP9M 2014 ResultsRome, November 7th, 2014

Piergiorgio PelusoMarco Patuano

9M 2014 Results 2

Safe HarbourThis presentation contains statements that constitute forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Thesestatements appear in a number of places in this presentation and include statements regarding the intent, belief or current expectations of developments and changesin the customer base, estimates regarding future growth in the different business lines and the global business, market share, financial results and other aspects ofthe activities and situation relating to the Telecom Italia Group. Such forward looking statements are not guarantees of future performance and involve risks anduncertainties, and actual results may differ materially from those projected or implied in the forward looking statements as a result of various factors. Consequently,Telecom Italia makes no representation, whether expressed or implied, as to the conformity of the actual results with those projected in the forward lookingstatements. Forward-looking information is based on certain key assumptions which we believe to be reasonable as of the date hereof, but forward lookinginformation by its nature involves risks and uncertainties, which are outside our control, and could significantly affect expected results. Analysts and investors arecautioned not to place undue reliance on those forward looking statements, which speak only as of the date of this presentation. Telecom Italia undertakes noobligation to release publicly the results of any revisions to these forward looking statements which may be made to reflect events and circumstances after the date ofthis presentation, including, without limitation, changes in Telecom Italia business or acquisition strategy or planned capital expenditures or to reflect the occurrenceof unanticipated events. Analysts and investors should consult the Company's Annual Report on Form 20-F as well as periodic filings made on Form 6-K, which areon file with the United States Securities and Exchange Commission which may identify factors that affect the forward looking statements included herein.

The accounting policies and consolidation principles adopted in the preparation of the Condensed Consolidated Financial Statements as of and for the nine monthsended 30 September 2014 have been applied on a basis consistent with those adopted in the Annual Consolidated Financial Statements at 31 December 2013, towhich reference should be made, except for the new standards and interpretations adopted by the Telecom Italia Group starting from 1 January 2014 which had noeffects on the Condensed Consolidated Financial Statements as of and for the nine months ended 30 September 2014. The Telecom Italia Group CondensedConsolidated Financial Statements at 30 September 2014 have not undergone an external audit/review.

Following the classification, starting from the fourth quarter 2013, of the Sofora - Telecom Argentina group as a disposal group (Discontinued operations/Non-currentassets held for sale) the consolidated financial statements data of prior periods (including the nine months ended 30 September 2013) have been restatedaccordingly and therefore the Sofora - Telecom Argentina group is no longer separately presented as a business unit.

Furthermore:

• starting from 2014, Organic changes in Revenues, EBITDA and EBIT are determined excluding, where applicable, only the effects of the changes in the scope ofconsolidation and exchange differences and therefore don’t take into account, as in the past, non-organic income and expenses, including those non-recurring;

• starting from 2014, the Domestic business unit includes the Olivetti group, in addition to Core Domestic and International Wholesale. This different presentationreflects the commercial and business placement of the Olivetti group and the process of integrating its products and services with those offered by Telecom Italia inthe domestic market. Therefore, the Olivetti group is no longer separately presented as a business unit;

as a result, the data for prior periods under comparison have been restated, accordingly.

In this presentation reference is also made to a normalization called “Domestic Underlying Ebitda trend”, which is based on the Adjusted (for one-offs anddiscontinuities) Reported Domestic Ebitda. This representation is provided as additional information to our Reported Ebitda that represents Operating profit beforedepreciation and amortization, capital gains (losses) and impairment reversals (losses) on non-current assets.

Marco Patuano - Piergiorgio Peluso

9M 2014 Results 3

• TI 3Q’14 Results

• Financial Update

• Take-Aways

• Appendix

Agenda

Marco Patuano

9M 2014 Results 4Marco Patuano

3Q’14 Group Highlights

Service Revenues4,943 mln €

(2Q’14: 4,871 mln €)

• Improving organic performance at -5.7% YoY vs -7.1% in 2Q’14 due to a different mix:• Better domestic trend both in Fixed and Mobile underpinned by healthier competitive environment and good acquisition results in UBB KPIs

• TIM Brasil: Positive “Business Generated” results supported by an excellent MBB take-up

Ebitda2,243 mln €

(2Q’14: 2,145 mln €)

• Group Ebitda at 2.2 bln € in 3Q’14 (Reported -8.0% YoY, Organic -8.5% YoY)• Performance at domestic level (Reported Ebitda -11.6% YoY) impacted by non-recurring items; Underlying Domestic Ebitda (net of new handset subsidy approach and one-offs) -7% YoY in 3Q’14

• Sound performance in Brazil (+6.5% YoY in 3Q’14) driven by a strong results in data revenues, efficiency on network and reduction in interconnection costs

Net debt reduction to

26.57 bln €• Lower by 0.2 bln € vs FY’13 and by 0.8 bln € vs 2Q’14. Usual 2H NFP improvement kicks in

InnovativeCapex

~620 mln € YTD(Italy & Brazil)

• Focus on innovation confirmed:• Italy: current 27% NGN coverage is above the mid-point of 2014-16 of the Original Plan target; actual 74% LTE coverage shows strong upbeat vs FY’14 target at 60% and FY’15 target at 70%

• Brazil: 700Mhz spectrum acquired at fair price, ensuring a better coverage (Indoor and Rural) with a much larger penetration than the 2,500 MHz band currently used for 4G services. 81 cities have been covered so far by our MBB Project (36% Urban coverage); 100 cities will be covered by end of 2014

Argentina

• On October 24, Sale Agreement with Fintech was Amended and Restated:• Total Sale Proceeds confirmed at US$ 960mln, which now translate into a 6x Ebitdamultiple after recent Peso devaluation

• 2nd Tranche for US$ 215.7mln cashed in• Cash collateral and Break-up Fee to support completion of transaction

9M 2014 Results 5

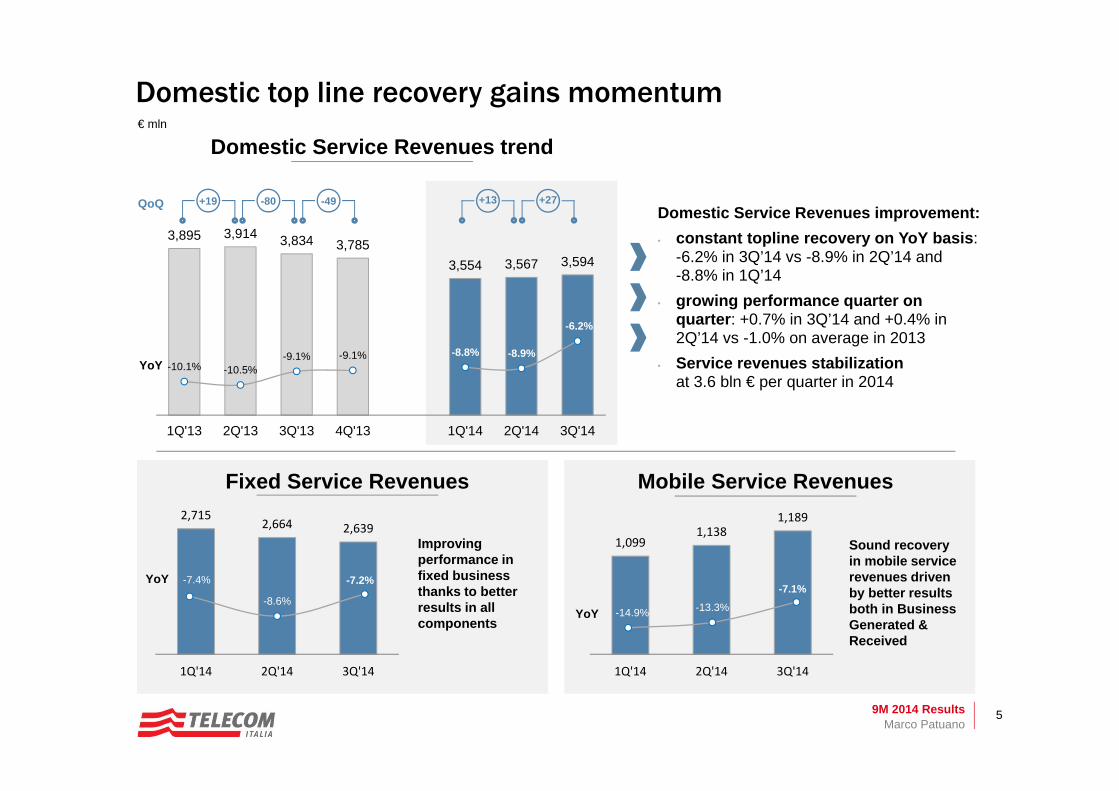

3,895 3,914 3,834 3,785 3,554 3,567 3,594

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

-10.1% -10.5%-9.1% -9.1% -8.8% -8.9%

-6.2%

Marco Patuano

Domestic Service Revenues trend

YoY

Domestic Service Revenues improvement: • constant topline recovery on YoY basis:

-6.2% in 3Q’14 vs -8.9% in 2Q’14 and -8.8% in 1Q’14

• growing performance quarter on quarter: +0.7% in 3Q’14 and +0.4% in 2Q’14 vs -1.0% on average in 2013

• Service revenues stabilizationat 3.6 bln € per quarter in 2014

QoQ

2,715 2,664 2,639

1Q'14 2Q'14 3Q'14

1,099 1,138

1,189

1Q'14 2Q'14 3Q'14

-7.4%

-8.6%

-7.2%

-14.9% -13.3%

-7.1%YoY

YoY

€ mln

Improving performance in fixed business thanks to better results in all components

Sound recovery in mobile service revenues driven by better results both in Business Generated & Received

+19 -80 -49 +13 +27

Domestic top line recovery gains momentum

Fixed Service Revenues Mobile Service Revenues

9M 2014 Results 6

2,031

1,795

3Q'13 3Q'14

Marco Patuano

40

-9.8%

-11.6%

net of newhandset subsidy

approach

Domestic Ebitda Ebitda trend%YoY,€ mln

Domestic Ebitda: progressing towards an improving FY trend

• Effects on Year-on Year performance for this quarter are:

• ~ 30 mln euro for• incentive plans for employees &

management and • salary discontinuous increases enabling

insourcing• ~ 30 mln euro for regulatory termination disputes

and other provisions • 40 mln euro for new handset subsidy approach

Ebitda Discontinuities

Normalized for discontinuous increases in labour costs, provisions & handset subsidy

net of newhandset subsidy

approach

reported

-9%

-7%

1H'14 3Q'14 4Q'14

+

Underlying Ebitda trend

-7.9%

-11.6%

-5.4%

-9.8%

1H'14 3Q'14

9M 2014 Results 7

138

1,089 1,122

443 380

249

195

106 -63 - 54

-11 -138

95

9M'13 network IT commercial&othersIT

others subsidy 9M'14

32% 32%35%

24%25%

28%

1Q 2Q 3Q

31%32%

33%

28% 28%

30%

1Q 2Q 3Q

(2) net of wholesale

2014

2013

Translating Domestic Innovative Capex into Revenues

Marco Patuano

2,0251,792

handset subsidy

network

IT

commercial&others IT

others

+102-69

innovative traditional

network

Efficiency(1): -197 mln €

(1) total domestic capex efficiency= a b c d+ + +

a b c d

33%35%

37%

1Q'14 2Q'14 3Q'14

Innovative portion on network capex9M’1435%

+8pp YoY

Innovative Mobile Service Revenues(3) Innovative Fixed Service Revenues(4)

(3) Broadband & VAS Content(4) Broadband, VAS Content & ICT

commercial&others IT

Growing penetration of Innovative Revenues on total(2)

9M 2014 Results 8

15 45

103 151

3477

123

163

0.2 0.5 >1.0 ~1.0

4Q'13 1Q'14 2Q'14 3Q'14

TI Retail NGN OLO Subloop/NGN Avg daily acquisition

Market Fiber Lines Mobile BB CB

today @27%

51%

2014 2015 2016

today @74%

2014 2015 2016

Marco Patuano

6,853 7,166 8,023 8,444 8,677 9,151 9,596

0% 1% 2%4% 5%

7%9%

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

MBB % LTE

>50%>80%

‘000

+10pp vs FY’13 FY’14 target already exceeded

NGN & LTE current Coverage

Additional Giga take-up

>50k clients per week

49

122

226

313

October~1.5k/day

Target furtherupgradable

First moveradvantage to be preserved

NGN Coverage LTE Coverage

«Open Fiber» launched

9M 2014 Results 9Marco Patuano

530 531 536

52 56 57 132 139 134

264 281 301 64 61 90

58 70 72

76 126 95

1Q'14 2Q'14 3Q'14

713 726 727

328 342 390

1,175 1,264 1,284

1,099 1,138 1,189

Outgoing voice

Incomingvoice

SMS

Traditional

BroadbandVAS content

Innovativewholesale

Service

handsets

Total

+13

+14

+39

+12

+89

+1

+48

+51

+2

+20+50 -31

€ mln, QoQ

-14.9%-13.3%

-7.1%

1Q'14 2Q'14 3Q'14 4Q'14

+

-24.1% -21.9% -16.7%

+9.9% +8.4%+16.6%

+8.7% +5.6% -0.5%

Traditional

Innovative

wholesale

Domestic Mobile

• Mobile Service Revenues improvements due to: • Constant recovery in outgoing voice and positive support from

incoming thanks to zero MTR drag

• Sound performance in Innovative revenues driven by progressive growth in browsing and additional revenue stream from new digital entertainment services

• We confirm Mobile Service Revenues is trending towards parity in 4Q’14

Quarterly Mobile Revenues Breakdown Service Revenues Trend YoY

9M 2014 Results 10

367 352 334

666 647 632

238 232 229

395 402 410

37 38 38133 134 135

878 859 861

56 73 79

1Q'14 2Q'14 3Q'14

1,271 1,231 1,195Traditional

565 574 583Innovative

2,715 2,664 2,639Service

2,771 2,737 2,718Total

Traditional

Innovative

-10.4% -13.1% -10.1%

+0.1%+1.8%

+3.0%

Wholesale & others

-7.2% -7.9%-9.3%

-7.4%

-8.6%

-7.2%

1Q'14 2Q'14 3Q'14 4Q'14

+

Outgoing voice

Access

Others

National, Int’ wholesale + Subs&others

VASICT

Broadband

handsets

-40

+9

-51

-34

-36

+9

-25

-19

Marco Patuano

Domestic Fixed

-7.4%-8.9%

-6.2%

1Q'14 2Q'14 3Q'14

Fixed Service Retail YoY• Monthly Retail Fee

upward revision effective November 1st to provide further uplift in 4Q’14

• Significant support from increasing fiber take-up

€ mln, QoQ

Quarterly Fixed Revenues Breakdown Service Revenues Trend YoY

9M 2014 Results 11

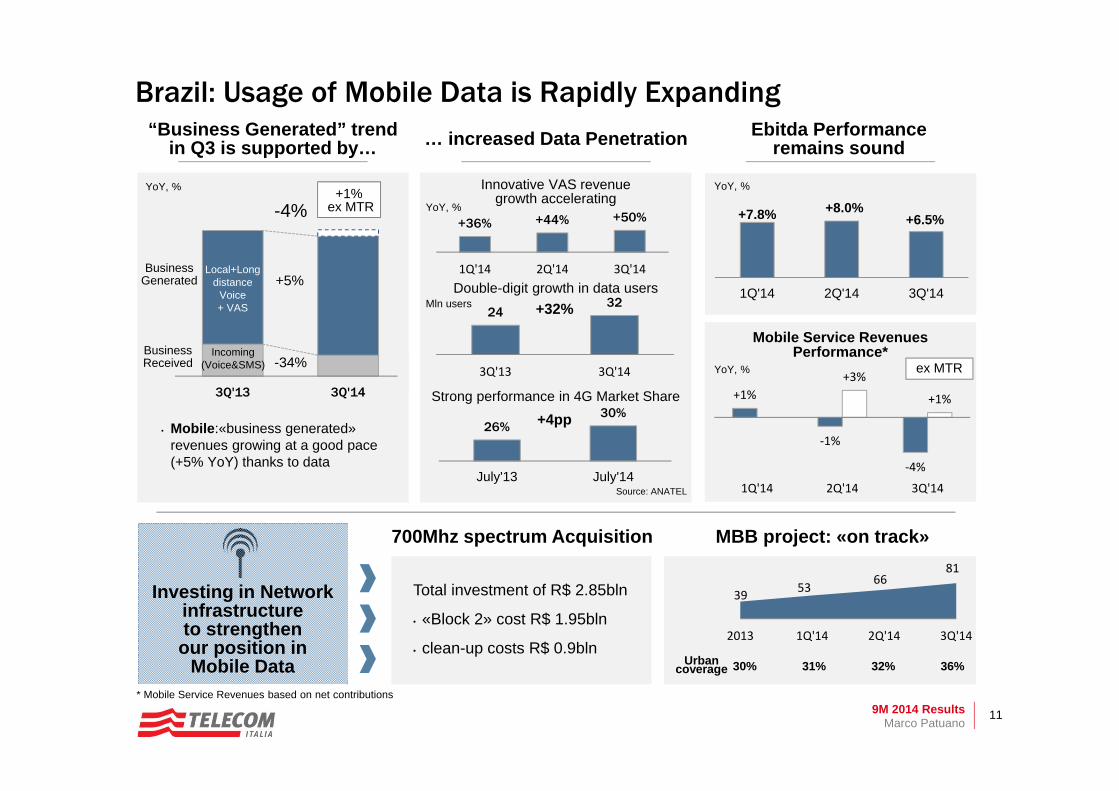

“Business Generated” trend in Q3 is supported by…

Marco Patuano

Ebitda Performance remains sound

YoY, %

+1%

‐1%

‐4%

+3%

+1%

1Q'14 2Q'14 3Q'14

ex MTR

… increased Data Penetration

• Mobile:«business generated» revenues growing at a good pace (+5% YoY) thanks to data

26%30%

July'13 July'14

Strong performance in 4G Market Share

+4pp

24 32

3Q'13 3Q'14

+32%Double-digit growth in data users

Mln users

YoY, % Innovative VAS revenuegrowth accelerating

+36% +44% +50%

1Q'14 2Q'14 3Q'14

700Mhz spectrum Acquisition

39 53 6681

2013 1Q'14 2Q'14 3Q'14

MBB project: «on track»

30% 36%31% 32%Urban coverage

Investing in Network infrastructure to strengthen our position in

Mobile Data

Total investment of R$ 2.85bln

• «Block 2» cost R$ 1.95bln

• clean-up costs R$ 0.9bln

Brazil: Usage of Mobile Data is Rapidly Expanding

3Q'13 3Q'14

Business Generated

BusinessReceived

-4%+1%

ex MTR

+5%

-34%

Local+Long distance

Voice + VAS

Incoming (Voice&SMS)

* Mobile Service Revenues based on net contributions

Source: ANATEL

+7.8% +8.0%+6.5%

1Q'14 2Q'14 3Q'14

YoY, %

Mobile Service Revenues Performance*

YoY, %

9M 2014 Results 12Piergiorgio Peluso

• TI 3Q’14 Results

• Financial Update

• Take-Aways

• Appendix

Agenda

9M 2014 Results 13

3Q’14 Reported€ mln, %YoY

Organic(1)

(1) Starting from 2014, Organic performance includes only exchange rate variations and impacts from perimeter changes(2) Including TI Media, Other & Elimination. Olivetti is included in the Domestic perimeter

Piergiorgio Peluso

Telecom Italia 3Q’14 Group Results

net of new handsetsubsidy

approach

Weight(2)€mln YoY YoY

CapexDomesticBrazil

933615317

-13.2%-9.3%

-19.7%

-12.5%-9.3%

-18.4%

-9.1%-3.6%66%

34%

RevenuesDomesticBrazil

5,4213,8051,608

-4.5%-5.0%-3.1%

-4.9%-5.0%-4.5%

70%29%

n.a.

Ebitda-CapexDomesticBrazil

1,3101,180

124

-4.0%-12.8%

-

-5.4%-12.8%

-90%9%

n.a.

EbitdaDomesticBrazil

2,2431,795

441

-8.0%-11.6%+8.4%

-8.5%-11.6%+6.5%

-7.0%-9.8%80%

20%-7%

Normalized for cost of labour, provisions &

handset subsidy

9M 2014 Results 14

2,045 2,034

1,327 1,080

864 762

2,148 2,164

9M'13 9M'14

‐53

+17 +24

1Q'14vs'13 2Q'14vs'13 3Q'14vs13

(1) Interconnection, Cost of Equipment, Other COGs(2) Acquisition costs, ADV, Customer Care, Other commercial costs

Volume/Revenue-Driven (1)

Market/Customer-Driven (2)

Process/Asset-Driven (3)

LabourCost

Solid Cost Reduction:• Commissioning: volume acquisition reduction• Advertising: cost optimization supported by single

format and brand• Operating Costs for Network & IT: savings in

procurement and positive impacts of process reengineering

• G&A: zero-budget approach and policy review

6,0406,383

-102

-246

Piergiorgio Peluso

9M’14 Domestic Opex Efficiency Plan to Overperform FY Target € mln

-11

SolidarityAgreement

ExtraordinaryCompensationPlans

Labour Cost YoY

YoY impact

neutral

negative

negative

neutral

negativeSalaryIncrease(4)

€ mln

positive

negative

-72

-31

-66

-180

-348

comm./adv./ccarebad debt/other

commercialindustrial

costs/G&A other opex total efficiency

Market-driven-102 mln euro

Process-driven-246 mln euro Including:

• 71 mln euro Sparkle provisionreversal

• 84 mln euro Antitrust fine in 2013

Operating Expenditures

External Opex net of COGs-348 mln € YoY

(3) Industrial costs, G&A, Real Estate, Other(4) Starting from February 1, 2014

9M 2014 Results 15

Reported, € mln

Piergiorgio Peluso

9M’14 Operating FCF Generation Remains Solid

1,281107

-843

-331

Ebitda Capex D operating WC&others OpFCF

Gro

up

Dom

estic

Bra

zil

vs. 2013

-184-29+397-552

OpFCF on Revenues

13%20%

25%

1Q'14 2Q'14 3Q'14

-491306

292

1Q'14 2Q'14 3Q'14

OpFCF quarterly breakdown

TI recurring stronger Second Half Operating Free Cash Flow is confirmed

9M’14 figures

-14

1,058

1,228

1Q'14 2Q'14 3Q'14 4Q'14

6,588

2,272

2,640

1,676

Ebitda Capex operatingWC&others

OpFCF

2014 Free Cash Flow Generation

5,2962,166

1,7921,338

Ebitda Capex D operatingWC&others

OpFCF

19% onRevenues

9M 2014 Results 16

-2,272 +1,213 +396 -47 +234 +241

FY'13 OpFCF Cash FinancialExpenses/Financial

Accruals

Taxes & otherimpacts

M&A Telecom Argentina(discontinued)

Dividends/ Change inequity

9M'14

9M’14 Net Financial Position Improvement

26,807 26,572

-235

+184 -88

vs. 2013

-304 +394-89 -287

Piergiorgio Peluso

FX impact

FX negative impact

-190

-1,657 mln €vs 9M’13

Including 1.3 bln euro Mandatory Convertible Bond25,507 25,272

MandatoryConvertible Bond

MandatoryConvertible Bond

€ mln

9M 2014 Results 17

Italy Brazil Argentina

• Digital terrestrial network businesses merger completion with Gruppo Editoriale L’Espresso

• Sale process on track, while new regulatory framework stilldeveloping

Towers 700Mhz Auction

TI Media

Sale Agreement renegotiated to allow for transaction completion• Same amount granted • TI Management • Discontinued operation• New US$175mln break-up fee in place

New Agreement Supports Disposal

Towers, Frequencies and Disposals Update

Towers

US$113.7mln already cashed in in Dec’13

US$215.7mln cashed in on Oct 29th, 2014

US$600.6mln TI note issued entirely purchased by the Buyer, providing Cash collateralUS$30mln service fee

Structure of the deal

a

b

c

d

US$ 960 mlnTotal Consideration

Piergiorgio Peluso

TIM Tower sale finalization soon

• Process in its Final Stage; final agreement expected to be signed by year end

• Transaction scope involving about 6.4k TIM Towers

• Proceeds expected to finance TIM network deployment, including 700 MHZ license costs

A Positive Outcome for TIM • Overall Cost in Line with

expectations• Awarded “Lot n.2” Fits our Existing

Spectrum Profile at best • Increased 4G Frequencies to

maintain momentum in TIM’s mobile data strategy

Value Extraction from Separation remains a Priority

• Tower Division created• Service Management Agreement

finalized• Advisors appointed for further steps

3G/4G Spectrum Auction

• “Lot 8” awarded to TEO consisting in30MHz for 15-year licenses on AWS(band 1700-2100Mhz) and 20Mhzon 700MHz

9M 2014 Results 18

• TI 3Q’14 Results

• Financial Update

• Take-Aways

• Appendix

Agenda

Marco Patuano

9M 2014 Results 19

Domestic

• Upbeat 3Q’14 paves the way for further improvements in 4Q and beyond:• Transition from price-based to quality-driven competition opens to further value generation

from Data, while polarization between High-Quality Network Operators and Other Operators increases

• Recovery in Mobile is well ahead and has started in Fixed, whose upside is shown by both our Retail and Wholesale take-up of Fiber offers

• Further push on convergence, offer simplification and superior quality experience for both our Consumer and Business segments ongoing

• Domestic Opex Efficiency Plan to overperform the €200mln FY’14 target, while favorably facing 2015 step-up to €400mln. In Brazil, TIM presented a strong Opex saving in 3Q with -8.1% YoY, mainly due to efficiency on network and lower interconnection costs

EfficiencyPlan

InnovativeCapex

• We are investing to strengthen our role of Digital Champion in Italy, where innovative services and content create more and more demand for bandwidth and speed – not a game for all. Network and IT transformation and delayering are a key part of the process

• Also in Brazil innovative investments are being increased in order to accelerate the implementation of new technologies for mobile data and further stimulate the commercial take-up of 4G. TIM currently covers around 36% of the urban population with 4G, serving 45 municipalities

M&A • Opportunities will be considered only if compliant with our Group’s Financial Discipline and if clearly generating value for our Companies and our shareholders / bondholders

Marco Patuano

• Supported by all the above actions, FCF generation is key to preserve our leadership in our Key Markets and to ensure our deleveraging goals

FCFgeneration

3Q’14 Group Take-Aways

Brazil • TIM Brasil is set to generate relevant value from its important, country-wide MBB expansion

9M 2014 Results 20Marco Patuano - Piergiorgio Peluso

• TI 3Q’14 Results

• Financial Update

• Take-Aways

• Appendix

Agenda

9M 2014 Results 21

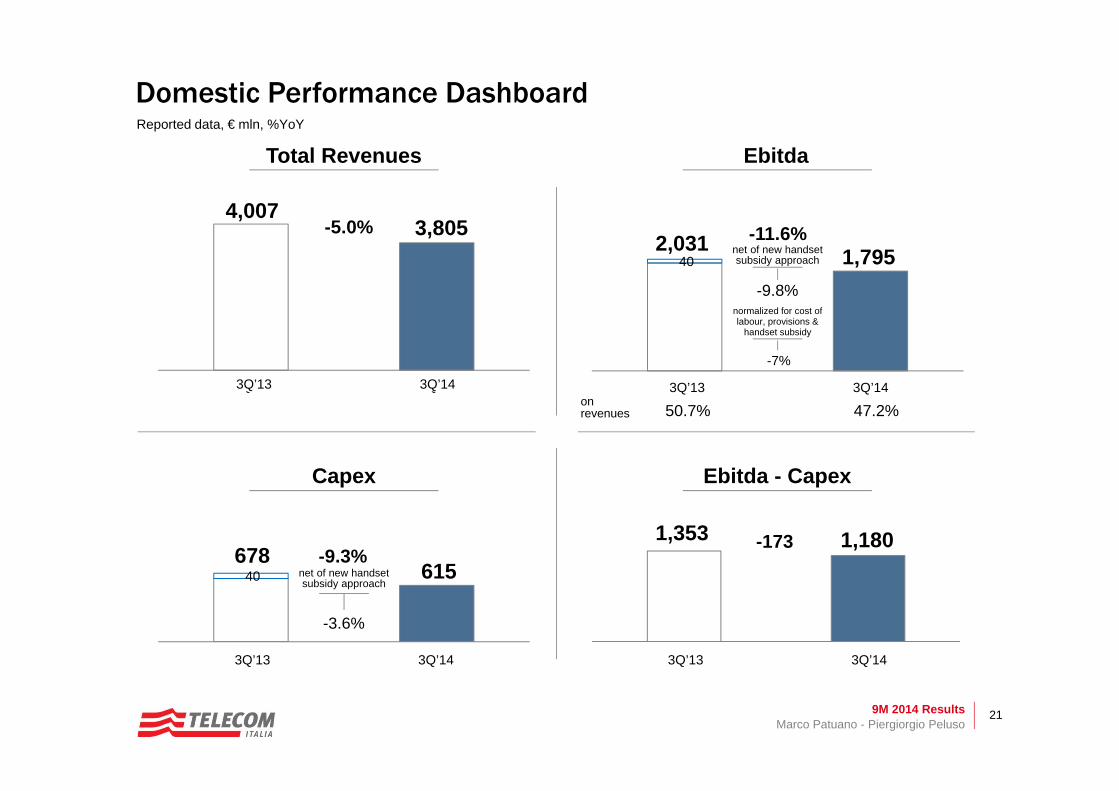

Reported data, € mln, %YoY

2Q'13 2Q'14

40

2Q'13 2Q'14

2Q'13 2Q'14

40

2Q'13 2Q'14

Total Revenues

Ebitda - Capex

Ebitda

Capex

on revenues 50.7% 47.2%

-9.8%

net of new handsetsubsidy approach

2,031 1,795-11.6%

4,0073,805

678615

-5.0%

-9.3%-1731,353 1,180

-3.6%

net of new handsetsubsidy approach

Domestic Performance Dashboard

3Q’13 3Q’14 3Q’13 3Q’14

3Q’13 3Q’143Q’13 3Q’14

normalized for cost of labour, provisions &

handset subsidy

Marco Patuano - Piergiorgio Peluso

-7%

9M 2014 Results 22

29124

3Q'13 3Q'14

386 317

3Q'13 3Q'14

415 441

3Q'13 3Q'14

1,394 1,341

290 267

3Q'13 3Q'14

Organic data*, € mln, %YoY

24.6% 27.4%

+6.5%

-4.5%

-18.4%

+95

* Excluding exchange rate

Brazil Performance Dashboard 3Q’14

Service

Handsets1,6081,684

-4%

Mobile ServiceRevenues**+1% ex-MTR

9M’14 -5.5% YoY

** Mobile Service Revenues based on net contributions

Marco Patuano - Piergiorgio Peluso

on revenues

Total Revenues

Ebitda - Capex

Ebitda

Capex

9M 2014 Results 23

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

Marco Patuano - Piergiorgio Peluso

Domestic Mobile KPIs‘000

31,858 31,706 31,554 31,221 30,996 30,660 30,374

83%85%

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

+2pp YoY

-28-20 -8 -17

-41 -34

-80

-2-1

-111 -107

-178 -197

-124-92

+75

+16

-18

Jan Feb Mar Apr May June July Aug Sep

MNP Balance

2014

2013 Cum.+504 YoY

Highlights

Clear signs of market stabilization translated into:

• better MNP balance +504k YTD• lower gross adds -36% YoY in Q3• better churn rate 25.2%; -3.6pp YoY

Mobile CB Active CB

9M 2014 Results 24

761 736 711 684 655 625 597

965 1,014 1,045 1,084 1,122 1,155 1,164

1 1 4 15 45 103 151

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

18.919.1

19.2 19.2 19.2

19.6

20.0

+3.5% +3.5% +3.6%+1.6% +1.8% +2.3%

+3.9%

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

ARPU BB YoY

€/month

Domestic Fixed KPIs

13,777 13,555 13,372 13,210 13,027 12,828 12,656

7,238 7,233 7,164 7,169 7,211 7,258 7,167

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

Fixed Access

OLO

TI retail

21,016 20,788 20,536 20,378 20,238 20,085

‘000

19,823

965 1,015 1,050 1,100 1,167 1,259 1,3156,984 6,933 6,892 6,915 6,933 6,939 6,932

Total

(201) (222)(183) (163) (182) (200) (171)

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

Line Losses

+18+22

+12YoY

BB ARPU

Marco Patuano - Piergiorgio Peluso

6,019 5,918 5,842 5,814 5,766 5,679 5,617

Flat ADSL

Total BB FastTotal

Free ADSL

Total ADSL

SI+20MbFiber

BB Access

9M 2014 Results 25

+1.9%

-10.7%

-12.6%

-22.2%

+0.7%

-8.9%

+16.9%

-18.7%-64.7%

+0.5%

-6.0%

-7.6%

-18.5%

+4.6%

+18.9%

+18.4%

-15.4%-61.8%

81

1,203

1,109

536

523

50

94

51917

wholesale(1)

Consumer+Business

services

outgoing voice

VAS

business received

handsets

(1) Including Visitors (2) Total Retail Service Revenues net of Incoming

voicefees&other

-10.0%-5.6%1,284Total 1,360

80

1,280

1,200

-12.7%-8.5%1,059business generated(2) 1,158

658

500

42

80

61344

3Q’13 3Q’14 YoY 9M YoY

Domestic Mobile Revenues BreakdownReported, € mln, %YoY

Marco Patuano - Piergiorgio Peluso

9M 2014 Results 26

Reported, € mln, %YoY

Sparkle group

Wholesale Domestic

Retail Service

Service Wireline 2,844 2,639 -7.2% -7.7%

339 304 -10.3% -3.2%

650 595 -8.5% -10.3%

1,899 1,781 -6.2% -7.5%

voice & access 1,178 1,056 -10.4% -11.2%

internet 401 415 +3.5% +1.5%

business data 279 264 -5.3% -2.9%

other 41 46 n.m. n.m.elim. & other (43) (41) n.m. n.m.

Total Wireline 2,898 2,718 -6.2% -7.1%

products 54 79 +47.8% +22.1%

Domestic Fixed Revenues Breakdown

3Q’13 3Q’14 YoY 9M YoY

Marco Patuano - Piergiorgio Peluso

9M 2014 Results 27

Liquidity Margin

€ 30,657 mln is the nominal amount of outstanding medium-long term debt. Adding the Mandatory Convertible Bond (€ 1,300 mln), the discontinued operations (€ 28 mln), IAS adjustments (€ 1,223 mln) and current financial liabilities (€ 487 mln), the gross debt figure of € 33,695 mln is reached.N.B. Debt maturities are net of € 1,262 mln (face value) of repurchased (of which € 504 in the 2013 and € 543 in the 2014) own bonds (of which € 1,047 mln related to bonds due within 2016).

Loans (of which long-term rent, financial and operating lease payable € 1,200)

Drawn bank facilityBonds

Debt Maturities

Undrawn Portion of Facility/CommittedC&CE (escluded discontinued)

Marco Patuano - Piergiorgio Peluso

Robust Liquidity Margin and Well-Distributed Debt Maturities

Fully Covered until 2018

€ mln € mln

4491,359

918

896

1,030

1,354

1,264

7,2707,0001,949

1,880

2,965

2,295

3,138

11,160

23,387

5,305

12,305

449

3,308

2,798

3,861

3,325

4,492

12,424 30,657

Liquiditymargin

Within 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 Beyond 2019 Total M/LTerm Debt

9M 2014 Results 28

N.B. The figures are net of the adjustment due to the fair value measurement of derivatives and related financial liabilities/assets, as follows: - the impact on Gross Financial Debt is equal to 2,455 €/mln (of which 687 €/mln on bonds)- the impact on Financial Assets is equal to 966 €/mln.Therefore, the Net Financial Indebtedness is adjusted by 1,489 €/mln.

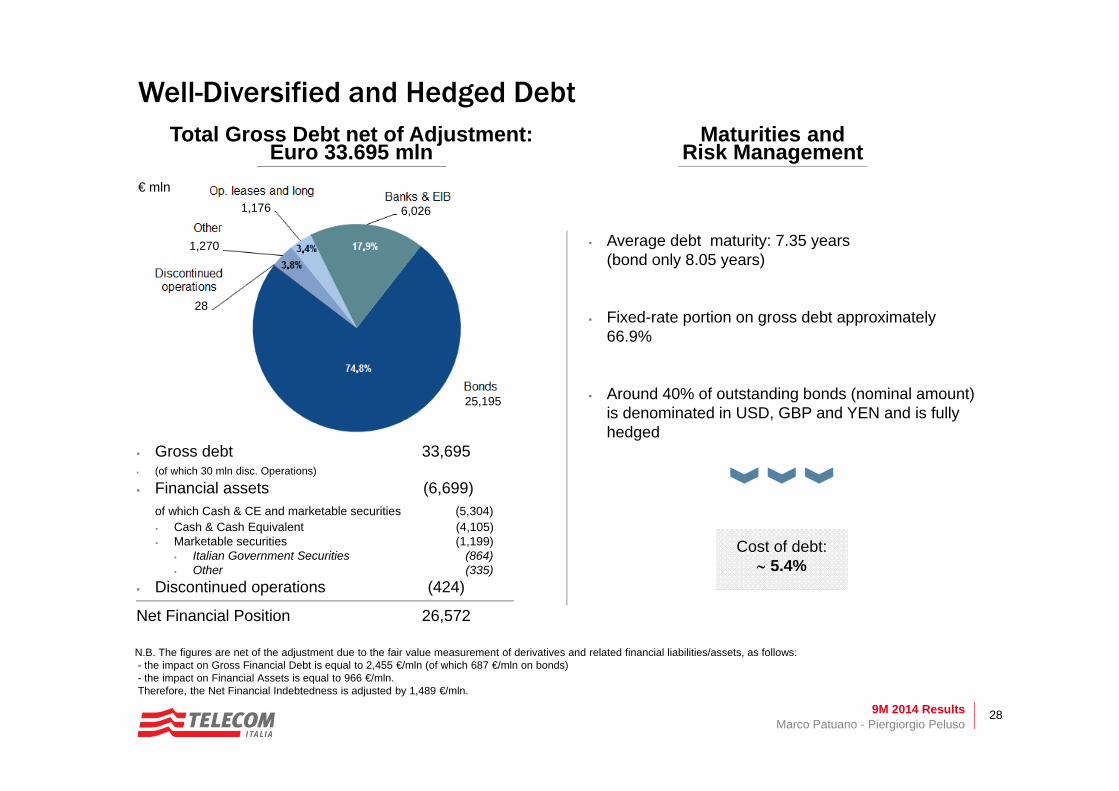

Total Gross Debt net of Adjustment: Euro 33.695 mln

Gross debt 33,695 (of which 30 mln disc. Operations)

Financial assets (6,699) of which Cash & CE and marketable securities (5,304) Cash & Cash Equivalent (4,105) Marketable securities (1,199)

Italian Government Securities (864) Other (335)

Discontinued operations (424)

Net Financial Position 26,572

Maturities and Risk Management

Cost of debt: 5.4%

Average debt maturity: 7.35 years (bond only 8.05 years)

Fixed-rate portion on gross debt approximately 66.9%

Around 40% of outstanding bonds (nominal amount) is denominated in USD, GBP and YEN and is fully hedged

Marco Patuano - Piergiorgio Peluso

Well-Diversified and Hedged Debt

1,270

1,176 6,026

25,195

.

.

..

28

€ mln

Related Documents