1 ABSTRACT In this project, titled “COMPARATIVE ANALYSIS AND STUDY OF GMR GROUPS CREDIT RATING”. This aims to analyse the credit worthiness of the GMR Infrastructure ltd among the key competitors of the company using the credit rating methodology This study based on financial statements such as Ratio Analysis, Comparative balance sheet with the competitors in the same industry and business process analysis like swot analysis. By using these combined tools it enables to determine in an effective manner. The study is made to evaluate the financial position, the operational results as well as financial progress of a business concern. This study explains ways in which ratio analysis can be of assistance in long-range planning, budgeting and asset management to strengthen financial performance and help avoid financial difficulties. This study makes us to study the credit rating methodology and also about the credit rating agencies in India and finally gives the credit worthiness of the company The study not only throws on the financial position of a firm but also serves as a Stepping stone to remedial measures for GMR Infrastructure ltd. This project helps to identify and give suggestion to improve some of the concerned area of businesses in “GMR Infrastructure ltd”

64137897 Comparative Analysis Credit Rating

Dec 01, 2015

a report on comparative analysis of credit rating

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

ABSTRACT

In this project, titled “COMPARATIVE ANALYSIS AND STUDY OF GMR

GROUPS CREDIT RATING”. This aims to analyse the credit worthiness of the GMR

Infrastructure ltd among the key competitors of the company using the credit rating methodology

This study based on financial statements such as Ratio Analysis, Comparative balance

sheet with the competitors in the same industry and business process analysis like swot analysis.

By using these combined tools it enables to determine in an effective manner.

The study is made to evaluate the financial position, the operational results as well as

financial progress of a business concern.

This study explains ways in which ratio analysis can be of assistance in long-range

planning, budgeting and asset management to strengthen financial performance and help avoid

financial difficulties.

This study makes us to study the credit rating methodology and also about the credit

rating agencies in India and finally gives the credit worthiness of the company

The study not only throws on the financial position of a firm but also serves as a

Stepping stone to remedial measures for GMR Infrastructure ltd.

This project helps to identify and give suggestion to improve some of the concerned area

of businesses in “GMR Infrastructure ltd”

2

LIST OF TABLES

TABLE NO NAME OF TABLE PAGE NO 5.1 CRISIL fixed deposit rating symbols 5.2 CRISIL rating symbols for short term instruments 5.3 ICRA rating symbols for long-term debentures,

bonds and preference shares 5.4 ICRA fixed deposit rating symbols 5.5 CARE rating symbols for long-term instruments 5.6 CARE short-term investment symbols 5.7 CARE analysis rating 5.8 Rating methodology for infrastructure industries 5.9 ICRA credit rating methodology 6.1 Comparative balance sheet 6.2 Comparative profit and loss account 6.3 Comparative cash flow statements 6.4 Ratio analysis 6.5 Key parameters of rating 6.6 Rank based on the parameters 6.7 Final ranking 6.8 Sectors involved in infrastructure companies 6.9 Power sector projects involved 6.10 Roads sector projects involved 6.11 Ratings assigned by the agencies 6.12 Care ratings 6.13 Ratings explanation 6.14 Swot analysis for GMR 6.15 Swot analysis for LANCO 6.16 Swot analysis for GVK 6.17 Swot analysis for JPASSOCIAT 6.18 Comparison b/w GMR and JPASSOCIAT 6.19 Comparison b/w GMR and LANCO 6.20 Comparison b/w GMR and GVK

3

LIST OF CHARTS

CHART NO NAME OF CHART PAGE NO

2.1 Organizational chart of GMR

3.1 Process of ratio analysis 3.2 CARE’s rating process 3.3 ICRA’s rating process 3.4 CRISIL’s rating process 6.1 EBITDA margin ratio 6.2 Return on equity 6.3 Price to earnings ratio 6.4 Debt to equity ratio 6.5 Return on capital employed 6.6 Price to book value 6.7 EV/EBITDA 6.8 Cash profit margin 6.9 Operating cash flow ratio 6.10 Current ratio 6.11 Cash ratio 6.12 Asset efficiency ratio 6.13 Operating cash margin 6.14 Operating profit margin 6.15 Basic earning power ratio

4

CHAPTER-1

INTRODUCTION TO THE STUDY

1.1 INTRODUCTION:

The removal of strict regulatory framework in recent years has led to a spurt in the

number of companies borrowing directly from the capital markets. There have been several

instances in the recent past where the “fly-by-night” operators have cheated unwary investors. In

such a situation, it has become increasingly difficult for an ordinary investor to distinguish

between 'safe and good investment opportunities' and 'unsafe and bad investments'. Investors find

that a borrower's size or names are no longer a sufficient guarantee of timely payment of interest

and principal.

Investors perceive the need of an independent and credible agency, which judges

impartially and in a professional manner, the credit quality of different companies and assist

investors in making their investment decisions. Credit Rating Agencies, by providing a simple

system of gradation of corporate debt instruments, assist lenders to form an opinion on -the

relative capacities of the borrowers to meet their obligations. These Credit Rating Agencies, thus,

assist and form an integral part of a broader programme of financial disintermediation and

broadening the debt market.

Credit rating is used' extensively for evaluating debt instruments. These include long-

term instruments, like bonds and debentures as well as short-term obligations, like Commercial

Paper. In addition, pured deposits, certificates of deposits, inter-corporate deposits, structured

obligations including non-convertible portion of partly Convertible Debentures(PCDs) and

preferences shares are also rated.

1.2 DEFINITION OF CREDIT RATING:

5

A published ranking, based cut_down_on detailed financial analysis by a credit

beareu, of one's financial history, specifically as it relates to one's ability to meet debt obligation.

The highest rating is usually AAA, and the lowest is D. Lender use this information to decide

whether to approve a loan.

1.3 DETERMINANTS:

The default-risk assessment and quality rating assigned to an issue are primarily

determined by three factors :

i) The issuer's ability to pay,

ii) The strength of the security owner's claim on the issue, and

iii) The economic significance of the industry and market place of the issuer.

1.4 RATING METHODOLOGIES: Rating is a search for long-term fundamentals and the probabilities for changes in

the fundamentals. Each agency's rating process usually includes fundamental analysis of public

and private issuer-specific data, 'industry analysis, and presentations by the issuer's senior

executives, statistical classification models, and judgement. Typically, the rating agency is privy

to the issuer's short and long-range plans and budgets. The analytical framework followed for

rating methodology is divided into two interdependent segments.

The first segment deals with operational characteristics and the second one with

the financial characteristics. Besides, quantitative and objective factors; qualitative aspects, like

assessment of management capabilities play a very important role in arriving at the rating for an

instrument. The relative importance of qualitative and quantitative components of the analysis

varies with the type of issuer.

Rating is not based on a predetermined formula, which specifies the relevant

variables as well as weights attached to each one of them. Further, the emphasis on different

aspects varies from agency to agency. Broadly, the rating agency assures itself that there is a

6

good congruence between assets and liabilities of a company and downgrades the rating if the

quality of assets depreciates. The rating agency employs qualified professionals to ensure

consistency and reliability. Reputation of the Credit Rating Agency creates confidence in the

investor. Rating Agency earns its reputation by assessing the client's operational performance,

managerial competence, management and organizational set-up and financial structure. It should

be an independent company with its own identity. It should have no government interference.

Rating of an instrument does not give any fiduciary status to the credit rating agency. It is

desirable that the rating be done by more than one agency for the same kind of instrument. This

will attract investor's confidence in the rating symbol given.

A rating is a quality label that conveniently summarizes the default risk of an

issuer. The credibility of the issuer's, proposed payment schedule is complemented by the

credibility of the rating agency. Rating agencies perform this certification role by exploiting the

economies of scale in processing information and monitoring the issuer. There is an ongoing

debate about whether the rating agencies perform an information role in addition to a

certification role. Whether agencies have access to superior (private) information, or if agencies

are superior processors of information; security ratings provide information to investors, rather

than merely summarizing existing information. Empirical research confirms the information role

of rating agencies by demonstrating that news of actual and proposed rating changes affects the

price of issuer's securities.

Most studies document numerically larger price effects for downgrades than for

upgrades, consistent with the perceived predilection of

management for delaying bad news.

Despite variations across individual rating agencies, the following features appear to

be common in the rating methodology employed by different agencies:

• Two broad types of analyses are done:

7

(a) industry and business analysis and

(b) financial analysis

The key factors considered in industry and business analysis:

(a) Growth rate and relationship with the economy

(b) Industry risk characteristics

(c) Structure of industry and nature of competition

(d) Competitive position of the issuer

(e) Managerial capability of the issuer

The key factors considered in financial analysis:

(a)Earning power

(b)Business and financial risk

(c)Asset protection

(d)Cash flow adequacy

(e)Financial flexibility

(f)Quality of accounting

Subjective judgments seem to play an important role in the assessment of the issue/issuer on

various factors. While each factor is normally scored separately, no mechanical formula is used

for combining the scores on different factors to arrive at the ratings conclusion. In the ultimate

analysis of variables which are viewed as interdependent industry risk characteristics are likely to

set the upper limit on rating

1.4.1 Business analyses:

8

It is the academic desciplines of identifying business needs and determining

solutions to business problems. Solutions often include a systems development component, but

may also consist of process improvement, organizational change or strategic planning and policy

development. The person who carries out this task is called a business analysts or BA.

Those BAs who work solely on developing software systems may be called IT

Business Analysts, Technical Business Analysts, Online Business Analysts or Systems Analysts.

Business analysis as a discipline has a heavy overlap with requirement analysis

sometimes also called requirements engineering, but focuses on identifying the changes to an

organization that are required for it to achieve strategic goals. These changes include changes to

strategies, structures, policies, processes, and information systems.

1.4.1.1 Goal of business analysis

Ultimately, business analysis wants to achieve the following outcomes:

• Reduce waste

• Create solutions

• Complete projects on time

• Improve efficiency

• Document the right requirements

1.4.1.2 Business analysis includes:

Enterprise analysis or company analysis:

It focuses on understanding the needs of the business as a whole, its strategic

direction, and identifying initiatives that will allow a business to meet those strategic goals.

Requirements planning and management :

It involves planning the requirements development process, determining which

requirements are the highest priority for implementation, and managing change.

9

Requirements elicitation:

It describes techniques for collecting requirements from stakeholders in a project.

Requirements analysis

It describes how to develop and specify requirements in enough detail to allow them to be

successfully implemented by a project team.

Requirements communication

It describes techniques for ensuring that stakeholders have a shared understanding of the

requirements and how they will be implemented.

Solution assessment and validation

It describes how the business analyst can verify the correctness of a proposed solution,

how to support the implementation of a solution, and how to assess possible shortcomings

in the implementation.

There are a number of techniques that a Business Analyst will use when facilitating

business change. These range from workshop facilitation techniques used to elicit requirements,

to techniques for analyzing and organizing requirements.

The best technique to analyse the business is SWOT analysis.This is used to help

focus activities into areas of strength and where the greatest opportunities lie. This is used to

identify the dangers that take the form of weaknesses and both internal and external threats.

*The four attributes of SWOT are strength, weakness, opportunities and threats:.

Strength is defined as any internal asset, technology, motivation, finance, business links,

etc that can help to exploit opportunities and to fight off threats.

Weakness is an internal condition which hampers the competitive position or exploitation

of opportunities.

Opportunity is any external circumstance or characteristic which favour

the demand of the system or where the system is enjoying a competitive advantage.

10

Threat is a challenge of an unfavorable trend or of any external Circumstance which will

unfavorably influence the position of the system.

1.4.2 Financial statements Analysis:

The financial statements provide some extremely useful information to the

extent that the balance sheet mirrors the financial position on a particular date in terms of the

structure of assets, liabilities and owners’ equity, and so on and the profit and loss account shows

the results of operations during a certain period of time in terms of the revenues obtained and the

cost incurred during the year.

Thus, the financial statements provide a summarized view of the financial

position and operations of a firm. Therefore, much to be learnt about a firm from a careful

examination of its financial statements as invaluable documents performance reports. The

analysis of financial statements is thus, an important aid to financial analysis.The focus of

financial analysis is on key figures in the financial statements and the significant relationship that

exists between them. The analysis of financial statements is a process of evaluating the

relationship between component parts of financial statements to obtain a better understanding of

the firm’s position and performance.

The first task of the financial analyst is to select the information relevant to the

decision under consideration from the total information contained in the financial statements.

The second step is to arrange the information in a way to highlight significant relationships. The

final step is interpretation and drawing of inferences and conclusion. In brief, the financial

analysis is the process of selection, relation and evaluation.

The term financial analysis is also known as analysis and interpretation of financial

statements. It refers to the establishing meaningful relationship between various items of the two

financial statements i.e. Income statement and position statement. It determines financial strength

and weaknesses of the firm. Analysis of financial statements is an attempt to assess the efficiency

and performance of an enterprise. Thus, the analysis and interpretation of financial statements is

very essential to measure the efficiency, profitability, financial soundness and future prospects of

the business units.

11

1.4.2.1 Financial analysis serves the following purposes:

Measuring the profitability

The main objective of a business is to earn a satisfactory return on the funds invested in it.

Financial analysis helps in ascertaining whether adequate profits are being earned on the capital

invested in the business or not. It also helps in knowing the capacity to pay the interest and

dividend.

Indicating the trend of Achievements

Financial statements of the previous years can be compared and the trend regarding various

expenses, purchases, sales, gross profits and net profit etc. can be ascertained. Value of assets

and liabilities can be compared and the future prospects of the business can be envisaged.

Assessing the growth potential of the business

The trend and other analysis of the business provides sufficient information indicating the growth

potential of the business.

1.4.2.3 PARTIES INTERESTED

Analysis of financial statements has become very significant due to widespread

interest of various parties in the financial results of a business unit. The various parties interested

in the analysis of financial statements are :

(i)Investors:

Shareholders or proprietors of the business are interested in the well being of the

business. They like to know the earning capacity of the business and its prospects of future

growth.

(ii) Management:

12

The management is interested in the financial position and performance of the

enterprise as a whole and of its various divisions. It helps them in preparing budgets and

assessing the performance of various departmental heads.

(iii) Trade unions:

They are interested in financial statements for negotiating the wages or salaries or

bonus agreement with the management.

(iv) Lenders:

Lenders to the business like debenture holders, suppliers of loans and lease are

interested to know short term as well as long term solvency position of the entity.

(v) Suppliers and trade creditors:

The suppliers and other creditors are interested to know about the solvency of the

business i.e. the ability of the company to meet the debts as and when they fall due.

(vi) Tax authorities:

Tax authorities are interested in financial statements for determining the tax liability.

(vii) Researchers:

They are interested in financial statements in undertaking research work in business

affairs and practices.

(viii) Employees :

They are interested to know the growth of profit. As a result of which they can

demand better remuneration and congenial working environment.

(ix) Government and their agencies:

Government and their agencies need financial information to regulate the activities of

the enterprises/industries and determine taxation policy. They suggest measures to formulate

policies and and regulations.

(x) Stock exchange:

The stock exchange members take interest in financial statements for the purpose

of analysis because they provide useful financial information about companies.Thus; we find that

different parties have interest in financial statements for different reasons.

13

1.5 Credit rating process:

Receipt of rating request from an issuer

Assigning a rating team

Collecting information

Meeting key officials and the management team

Preview meeting

• Rating committee meeting

• Rating communication

• Rating review

• Surveillance

CHAPTER-2

PROFILE OF THE COMPANY

2.1 HISTORY:

GMR Group is one of the fastest growing Infrastructure organisation in the

country. The GMR Group was found in the year 1976.It is head quartered in Bangalore, India.

GMR also takes part in Indian Premier League's (A Twenty20 Cricket league in India) Delhi

franchise, Delhi Daredevils. Grandhi Mallikarjun Rao is the Chairman and Managing director of

GMR group. With an estimated personal worth of $6.2 billion dollars, G M Rao stands at 198th

rank in Forbes' 2008 World Billionaire list.

2.2 BACKBONE:

GMR Varalakshmi foundation is the corporate social responsibility arm of the

GMR Group.The foundation is not for profit company.The vision is to emerge as a premier

national body in the area of corporate social responsibility.The mission is to improves the lives of

the poor and needy in a self-generating way.The core activities of the foundation include

education,health& hygiene and empowerment.

2.3 GMR GROUP MEMBERS:

14

• G.M.Rao-Group chairman&founder

• Srinivas Bommidala-chairman-Highways&Urban infrastructure

• G.B.S.Raju-chairman-Corporate&International business

• Kiran kumar grandhi-chairman-Airports

• K Balasubramanian-chairman-Corporate social responsibility

• P M Kumar-executive director-Group corporate development.

• B.V.N Rao-chairman-Energy business

2.4 VISION & MISSION:

VISION :

GMR will pay a pioneering role in developing innovative projects and provide world

class services in infrastructure.

MISSION :

To build entrepreneurial organisations that make a difference to society through

creation of value.

2.5 VALUES & BELIEFS:

Humility: They value intellectual modesty and detest false pride and arrogance.

Entrepreneurship: They will seek opportunities and they are everywhere.

Teamwork and relationship: Going beyond the individual, encouraging boundary less

behavior.

Deliver the promise: They will value a deep sense of responsibility and self discipline,to

meet and surpass commitments made.

Learning: Nurturing active curiosity-to question, share and improve.

Social responsibility: Anticipating and meeting relevant and emerging needs of society.

15

Respect for individual: They will treat others with dignity, sensitivity and honour.

2.6 BUSINESS SECTORS :

GMR Groups business interests is in Airports, Highways, Energy and Urban Infrastructure. .

GMR Infrastructure Limited has in the following sectors:

1. Airports

2. Energy

3. Highways

4. Urban infrastructure

5. EPC

1.Airports:

Under operation:

• GMR hyderabad international airport(63%)

• Delhi international airport(54%)

• Instanbul sabiha gokcen international airport(40%)

• Male international airport(100%)

2.Energy:

Under operation:

• GMR Energy ltd(100%)

• GMR Power corporation(51%)

• Vemagiri power generation(100%)

Under development:

• Badrinath Hydro Power(100%)

16

• GMR kamalanga energy(80%)

• GMR Bajoli Power Project(100%)

• GMR Chattisgarh Power Project(100%)

• Upper Karnali Power Project(73%)

• EMCO Energy limited(100%)

• GMR Rajahmundry energy(100%)

• Talong hydro power(100%)

• Himtal hydro power co.(80%)

• Island power singapore(100%)

• GMR Solar Energy (100%)

• Deedwana Transmission Line (100%)

• Alwar Transmission Line (100%)

3.Highways:

Under operation:

• GMR Tambaram-Tindivanam(61%)

• GMR Tuni-Ankapalli(61%)

• GMR Ambala-Chandigarh(100%)

• GMR Adloor-Gundla Ponchanpalli(100%)

• GMR Ulunderpet(100%)

• GMR Jadcherla(100%)

Under construction:

• GMR Hyderabad Vijayawada(74%)

• Chennai outer ringroad(90%)

• Hungund-Hospet(51%)

17

4.Urban Infrastructure:

At Hyderabad Airport

• 1000 acres for commercial development

• 250 acres Aviation SEZ

• 250 acres Logistic SEZ

At Delhi Airport

• 250 acres for commercial development

In Tamilnadu

• 3300 acres SEZ

5.EPC:

GMR Group is estimating to save 8-12 percent cost by having an in-house engineering,

procurement and construction unit through extensive procurement for various verticals.GMR

Infrastructure ltd is setting up an in-house division EPC division in order to reduce future project

costs and ensures that deadlines are met.

2.7 MERGERS AND ACQUISITION OF GMR :

• The largest deal in November 2010 was China Huaneng Corp's acquisition of US-based

InterGenInc from GMR Infrastructure for $1.232 million

• GIL acquires Barasentosa lestare PT,a coal mining company in feb 26 2009

• GMR Group acquired 50 percent stake in Intergen for $1.354 million in October 2008

• GMR infrastructure ltd acquires a minority stake in DIAL from GMR holdings pvt ltd in

2008.

18

• GMR Infrastructure ltd, a unit of GMR holdings pvt ltd of india acquired Coralrose ltd ,a

construction company andsunwood properties korea BV,an Amsterdam-based real estate

agency in 2008.

• GIL acquires island power co pte ltd , a jurong island-based electric utility company from

InterGen N.V. of 800 MW.

• GMR Energy ltd has acquired 63% stake in south africa’s homeland, mining and energy

SA ltd , a unit of canada’s homeland energy group ltd in 2008.

2.8 EVENTS HAPPENED RECENTLY IN GMR:

• The important event recently happened is that , Mr.BVN.Rao(business chairman,energy

sector) launched the GMR business excellence reference manual called “blue book”

coinciding with BE assessor workshop on 7th feb 2011.

• GMR group has been awarded with “The best infrastructure project” from all over India

by property world magazine.property world belongs to the united business media group.

• GVPGL has won the prestigious national energy conversation award at delhi on 14th dec

2010.

• GHIAL and luthansa cargo AG(LCAG) on 3rd dec 2010 signed a MOU to jointly develop

RGIA,hyderabad in to a key cargo hub in south asia for the transport of temperature

sensitive pharmaceuticals.

2.9 COMPETITORS OF GMR:

Reliance Infra

Adani Power

Jaypee jaiprakash asso

Unitech

19

Lanco infrastructure

GVK Infra

IVRCL Infra

IRB Infra

II&FS Trans

2.10 KEY COMPETITORS OF GMR:

2.10.1 GVK POWER AND INFRASTRUCTURE LTD:

HISTORY:

GVK power and infrastructure ltd is a diversified business entity with a focus on

infrastructure and urban infrastructure.G.V.Krishna reddy,the chairman and managing director of

GVKPIL,is a first generation entreprenuer who establishes the business.

The area of business interests including power,roads,urban infrastructure,bio-science,hotels

and manufacturing.

The company was incorporated in the year 1994 as jagurupadu operating and maintenance

company,a private company ,under the companies act 1956.later the company name has changed

to jagurupadu operating and maintenance private ltd company in the year 2005 and then the

company has changed to private ltd to public ltd and then the company name is changed as

GVK power and infrastructure ltd. GVK foundation is involved in the corporate social

responsibility to help out the needy .

GROUP MEMBERS:

• G.V.Krishna Reddy

• G.V.Sanjay reddy

• A.Issac George

• K.Narsim Shenoy

• Abid Hussain

G.V.K SECTORS:

20

POWER:

• OPERATIONAL:

o Jagurupadu combained cycle power plant phase-1(217mw)

o Jagurupadu combained cycle power plant phase-2(220mw)

o Gautami combained cycle power plant(464mw)

• UNDER DEVELOPMENT:

o Alaknanda(330mw)-uttarkand

o Goindwal sahib(540mw)-punjab

• UNDER IMPLEMENTATION:

o Jagurupadu phase-3(800mw)-A.P

o Gautami-2(800mw)-A.P

o Goriganga(370mw)-Uttarkhand

o Rattle(690mw)-J&K

o Tokisud-Jharkhand

AIRPORTS:

• Mumbai international airport(74%)

• Bangalore international airport(29%)

ROADS:

• Jaipur-kishangarh BOT project(6lane from the 500km)

• Deoli-kota road BOT project(4 lane from the 83km)

URBAN INFRASTRUCTURE:

21

• 3000 acres SEZ in perambalur(tamilnadu)

2.10.2 LANCO INFRATECH:

HISTORY:

Lanco is the one of the fastest growing integrated infrastructure enterprises of India.The area

of business interests are in power,roads, EPC,infrastructure,property development.

The founder chairman of lanco infratech is L.Rajagopal, a techno-crat turned industrialist. He

started the lanco foundation, a charitable trust in the year 2000 to reach out to the needy.And

also he is the member of parliament,India.

GROUP MEMBERS:

• L.Madhusudhan rao-executive chairman

• G.Bhaskara rao-executive vice-chairman

• L.Sridhar-vice-chairman

• G.Venkatesh babu-managing director

LANCO SECTORS:

CONSTRUCTION:

• Power plants based on Gas, Coal, Bio-mass and Hydro.

• Irrigation and water supply projects, including dams, tunnels, lift irrigation, sewerage

schemes and marine works.

• Civil construction including commercial and residential buildings, mass housing projects

and townships, industrial structures, information technology parks, Corporate offices,

Hospitals and more.

• Transportation engineering projects including roads, highways, bridges and flyovers.

POWER:

• OPERATIONAL PROJECTS:

22

o Lanco kondapalli 1&2(734mw)

o Aban power(120mw)

o Lanco power 1&2(600mw)

o Udipi power 1(600mw)

o Lanco,chitradurga(3mw)

o Lanco,thirunelveli(10mw)

o Vamshi hydro energies(10mw)

o Vamshi industrial power(5mw)

• UNDER IMPLEMENTATION:

o Lanco kondapalli 3(732mw)

o Lanco power(3&4)(1320mw)

o Lanco anpara(1200mw)

o Udipi power 2(600mw)

o Lanco babandh(1320mw)

o Lanco budhil hydro power(70mw)

o lanco teesta hydro power(500mw)

o lanco mandakini hydro power(76mw)

ROADS:

• Bangalore-madbugal on NH-4(81km)

• Neelamangala-devihalli on NH-48(82km)

EPC:

The EPC group at lanco ensures project delivery cycles, greater capital expenditure

control, sourcing the best service and technology providers and most importantly allows its

23

clients to focus on their core business.the core competence of lanco is its experienced team for

managing contracts during all phases of project,while meeting the highest international

standards.

Lanco provides engineering,procurement,construction,project management and

commissioning services on turnkey basis to the power sector leveraging on the experience and

expertise of its group companies,its construction capability and competent manpower.

INFRASTRUCTURE:

LANCO infrastructure ltd has executed many challenging projects across india

including highways.lanco is currently executing the Varanasi non metro airport project

2.10.3 JAIPRAKASH ASSOCIATION:

HISTORY:

Jaiprakash associates was previously known as jaiprakash industries ltd but after merging

with jaypee cements in the year of 2004, the company gots its present name. Jaiprakash

associates ltd is under the jaypee group,which is an industrial infrastructural group in india .The

group was established in 1974 and has a turnover more than Rs.30,000million.

Jaiprakash associates has subsidary companies which are jaiprakash hotels,jaiprakash hydro

power and jaiprakash ventures

GROUP MEMBERS:

• Manoj gaur-executive chairman

• Sunil kumar sharma-executive vice chairman

• Sarat kumar jain-vice chairman

• Sunny gaur-managing director

• Pankaj gaur-joint managing director

24

JP SECTORS:

Civil Engineering:

Jaiprakash Associates Ltd., the flagship company of the Group, is a pioneer in

construction of river valley and hydropower projects on turnkey basis in India. Jaypee Group has

executed 13 Hydropower projects spread over 6 states of India and neighbouring Bhutan to

generate 10,290 MW of power.

Hydropower :

• OPERATIONAL:

o Baspa 2(300mw)

o Vishnuprayag(400mw)

• UNDER IMPLEMENTATION:

o Karcham wangtoo(1000mw)

• UNDER DEVELOPMENT:

o Lower siang(2700mw)

o Hirong(500mw)

o Kynshi stage-2(450mw)

o Umngot stage-1(270mw)

Thermal Power:

25

These all projects are in under implementation

• Bina power(1250mw)

• Jaypee nigrie(1320mw)

• Kannur(240mw)

• Karchana(1980mw)

• Bara(3300mw)

Transmission System:

Jaiprakash Hydro-Power Limited has plans to venture into the development of

transmission systems with the Power Grid Corporation of India Ltd (PGCIL).

Cement:

Jaypee Group is the 4th largest cement producer in the country. It produces ordinary

Portland cement and Pozzolana Portland cement under the brand names “Buland” and

“Buniyad”. The group has plants at Rewa and Bela. Jaypee group is poised to achieve cement

production capacity of 20 MTPA by the year 2009.

Hospitality:

Jaypee group owns and operates four five star deluxe hotels through a subsidiary company,

Jaypee hotels limited. These hotels are: Hotel Siddharth and hotel vasant continental in New

Delhi, Hotel Jaypee palace Agra, and Jaypee residency Manor, Mussoorie.

Real estate development:

26

Jaypee group is developing real estate in Greater Noida. Its property, Jaypee Greens,is spread

over an area of 450 acres. It comprises golf resorts , villas, townhouses.

Expressways & Highways:

Jaypee Group is constructing the prestigious 160 km long Expressway with Six lane

access that would connect the historical city of Agra with Greater Noida.

Information Technology:

Jaypee Group Company JIL Information Technology Limited (JILIT) specializes in:

Hardware & Networking, Multimedia Services & Software, and Enterprise Resource Planning.

2.11 GMR Group Organizational Chart

CHAIRMAN

Executive director

President

27

Chart:2.1

2.12 AWARDS & RECOGNISATIONS:

Mr.G.M.Rao received “first generation entreprenuer of the year” at CNBC TV18-2009 and

he also got a “doctorate” from Andhra University.

“silver plate award” for supporting cause of elders-on october 1,2009, new delhi.

AssociateVice president

General manager(H.R)

General manager(finance)

General manager(marketing)

General manager(production)

Associate manager

Associate manager

Regional officer Associate manager

Senior co-crdinator Senior Co-ordinator

Junior co-ordinator

junior Co-ordinator

Assistant Assistant

Executive vice president

Executive manager

Executive manager

Executive manager

28

RGIA also won the “essar steel infrastructure excellence award 2009” organised by CNBC

TV18-2009.

Mr.kiran kumar grandhi , chairman got “young entrepreneur award 2009” in the area of

travel and tourism.

G.M.R Vemagiri power generation ltd has won the “Innovative environmental project”

award at the CII environmental best practices award 2011 organized by CII-Godrej green

business centre on 28 & 29 January 2011

RGIA and IGIA have been rankes 1st and 4th best airports in their respective categories in the

latest ASQ rankings of Airports Council International.

CHAPTER-3

REVIEW OF THE LITERATURE:

3.1 Techniques and tools of financial analysis

29

Financial statements give complete information about assets, liabilities,equity, reserves,

expenses and profit and loss of an enterprise. They are not readily understandable to interested

parties like creditors, shareholders, investors etc. Thus, various techniques are employed for

analysing and interpreting the financial statements. Techniques of analysis of financial

statements are mainly classified into three categories :

(i) Cross-sectional analysis

It is also known as inter firm comparison. This analysis helps in analysing financial

characteristics of an enterprise with financial characteristics of another similar enterprise in that

accounting period.For example, if company A has earned 15% profit on capital invested. This

does not say whether it is adequate or not. If we analyse further and find that a similar company

has earned 16% during the same period, then only we can make a conclusion that company B is

better.Thus, it turns into a meaningful analysis.

(ii) Time series analysis

It is also called as intra-firm comparison. According to this method,the relationship

between different items of financial statement is established, comparisons are made and results

obtained. The basis of comparison may be :

– Comparison of the financial statements of different years of the same business unit.

– Comparison of financial statement of a particular year of different business units.

(iii) Cross-sectional cum time series analysis

This analysis is intended to compare the financial characteristics of two or more

enterprises for a defined accounting period. It is possible to extend such a comparison over the

year. This approach is most effective in analysing of financial statements.

3.2 Comparative position in relation to other firms

The purpose of financial statements analysis is to help the management to make a comparative

study of the profitability of various firms engaged in similar businesses. Such comparison also

helps the management to study the position of their firm in respect of sales,expenses, profitability

and utilising capital, etc.

• Assess overall financial strength

The purpose of financial analysis is to assess the financial strength of the business. Analysis also

helps in taking decisions, whether funds required for investing for business growth are provided

30

from internal sources of the business or not if yes, how much? And also to assess how much

funds have been received from external sources.

• Assess solvency of the firm

The different tools of an analysis tell us whether the firm has sufficient funds to meet its short

term and long term liabilities or not.

Ratio analysis is used to analyse the present and future earning power of the issuing

corporation and to get insight into the strengths and weaknesses of the firm. Bond rating agencies

have suggested guidelines about what value each ratio should have within a particular quality

rating. Different ratios are favoured by rating agencies. For any given set of ratios, different

values are appropriate for each industry. Moreover, the values of every firm's ratios vary in a

cyclical fashion through the ups and downs of the business cycle.

To assess the strength of security owner's claim, the protective provisions in the

indenture (legal instrument specifying bond owners' rights), designed to ensure the safety of

bondholder's investment, are considered in detail.

The factors considered in regard to the economic significance and size of issuer

includes: nature of industry 'in which issuer is, operating (specifically issues like position in the

economy, life cycle of the industry, labour situation, supply factors, volatility, major

vulnerabilities, etc.), and the competition faced by the issuer (market share, technological

leadership, production efficiency, financial structure, etc.)

3.3Ratio Analysis:

Ratio analysis is a widely-used tool of financial analysis. It can be used to

compare the risk and return relationships of firms of different sizes. It is defined as the

systematic use of ratio to interpret the financial statements so that the financial strengths and

weakness of a firm as well as its historical performance and current financial condition can be

determined. The term ratio refers to the numerical or quantitative relationship between two items

and variables. These ratios are expressed as

1. percentages,

2. fraction and

3. proportion of numbers.

31

These alternative methods of expressing items which are related to each other are, for

purposes of financial analysis, referred to as ratio analysis. It should be noted that computing the

ratios does not add any information not already inherent in the above figures of profits and

sales.What the ratio do is that they reveal the relationship in a more meaningful way so as to

enable equity investors, management and lenders make better investment and credit decisions.

3.3.1 PROCESS OF RATIO ANALYSIS

Chart:3.1

3.4 THE KEY RATIOS USED IN THE STUDY:

The main ratios which are very useful for the study that measures the business and

financial analysis.

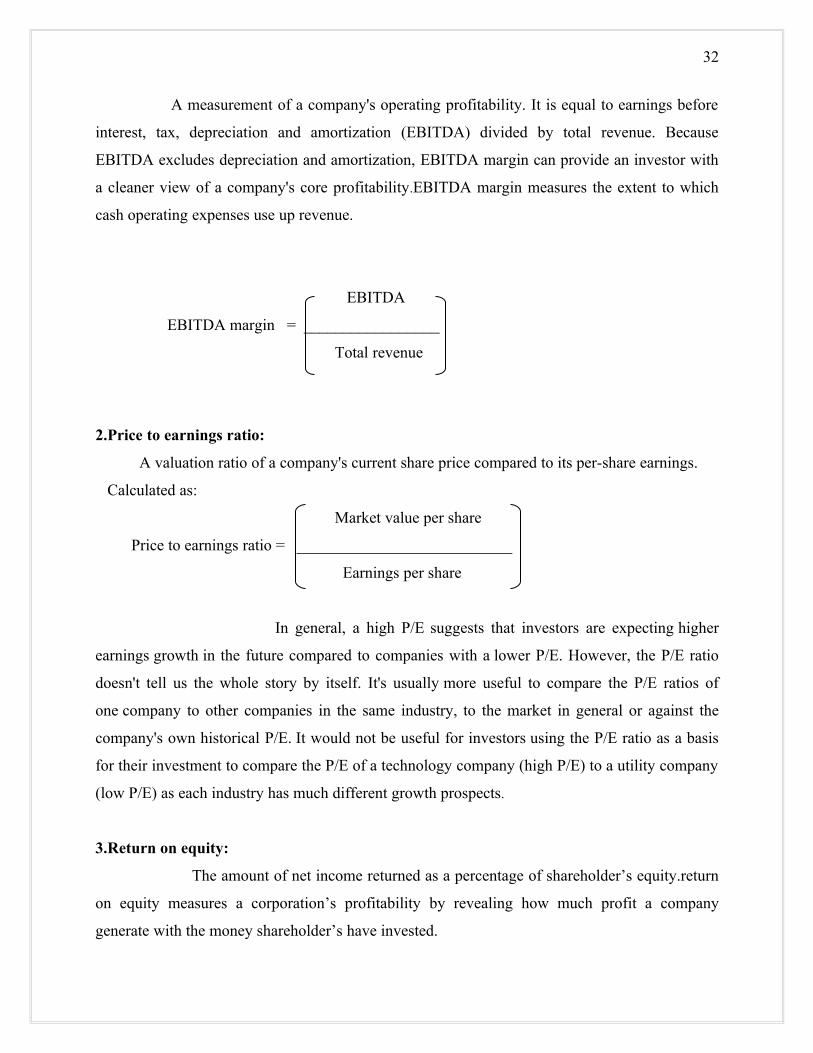

1. EBITDA Margin:

Selection of relevant data from the financial statements depending upon the objective of the analysis.

Calculation of appropriate ratios from the above data

Comparison of the calculated ratio with the ratios of the same firm in the past, or ratios developed from projected financial statements or the ratios of other firms in the same year of the same company type or the ratios of the industry to which the firm belongs

Interpretation of ratios

32

A measurement of a company's operating profitability. It is equal to earnings before

interest, tax, depreciation and amortization (EBITDA) divided by total revenue. Because

EBITDA excludes depreciation and amortization, EBITDA margin can provide an investor with

a cleaner view of a company's core profitability.EBITDA margin measures the extent to which

cash operating expenses use up revenue.

EBITDA

EBITDA margin = _________________

Total revenue

2.Price to earnings ratio:

A valuation ratio of a company's current share price compared to its per-share earnings.

Calculated as:

Market value per share

Price to earnings ratio = ___________________________

Earnings per share

In general, a high P/E suggests that investors are expecting higher

earnings growth in the future compared to companies with a lower P/E. However, the P/E ratio

doesn't tell us the whole story by itself. It's usually more useful to compare the P/E ratios of

one company to other companies in the same industry, to the market in general or against the

company's own historical P/E. It would not be useful for investors using the P/E ratio as a basis

for their investment to compare the P/E of a technology company (high P/E) to a utility company

(low P/E) as each industry has much different growth prospects.

3.Return on equity:

The amount of net income returned as a percentage of shareholder’s equity.return

on equity measures a corporation’s profitability by revealing how much profit a company

generate with the money shareholder’s have invested.

33

Calculated as:

Net income

Return on equity=______________________

Share holder’s equity

Net income is for the full fiscal year(before dividends paid to common stock holders but

after dividends to preferred stock)share holder’s equity does not include preferred shares. Also

known as “return on net worth”(RONW).

4.Debt to equity ratio:

A measure of a company's financial leverage calculated by dividing its total

liabilities by stockholders' equity. It indicates what proportion of equity and debt the company is

using to finance its assets.

Debt to equity ratio= total liabilities .

Shareholder’s equity

Sometimes only interest-bearing, long-term debt is used instead of total liabilities in the

calculation. Also known as the Personal Debt/Equity Ratio, this ratio can be applied to personal

financial statements as well as corporate ones.

If a lot of debt is used to finance increased operations (high debt to equity), the company

could potentially generate more earnings than it would have without this outside financing. If this

were to increase earnings by a greater amount than the debt cost (interest), then the shareholders

benefit as more earnings are being spread among the same amount of shareholders. However, the

cost of this debt financing may outweigh the return that the company generates on the debt

through investment and business activities and become too much for the company to handle. This

can lead to bankruptcy, which would leave shareholders with nothing.

A high debt to equity ratio generally means that a company has been aggressive in

financing its growth with debt. This can result in volatile earnings

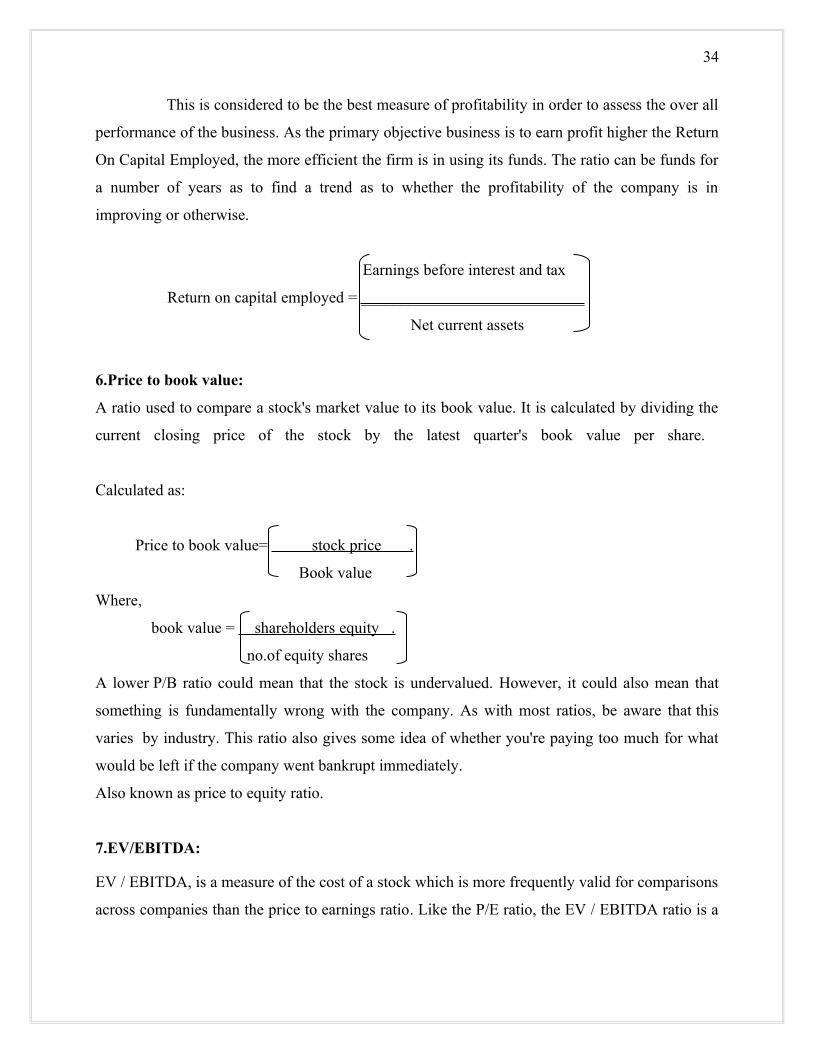

5. Return on capital employed:

34

This is considered to be the best measure of profitability in order to assess the over all

performance of the business. As the primary objective business is to earn profit higher the Return

On Capital Employed, the more efficient the firm is in using its funds. The ratio can be funds for

a number of years as to find a trend as to whether the profitability of the company is in

improving or otherwise.

Earnings before interest and tax

Return on capital employed = ____________________________

Net current assets

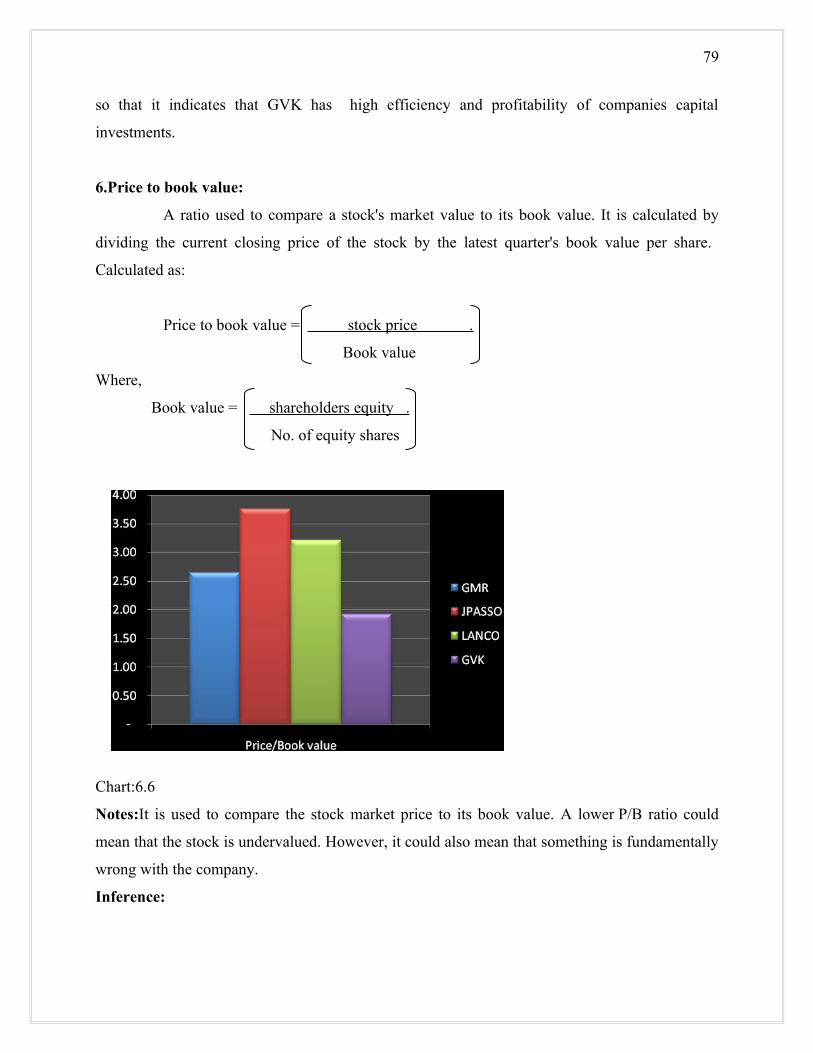

6.Price to book value:

A ratio used to compare a stock's market value to its book value. It is calculated by dividing the

current closing price of the stock by the latest quarter's book value per share.

Calculated as:

Price to book value= stock price .

Book value

Where,

book value = shareholders equity .

no.of equity shares

A lower P/B ratio could mean that the stock is undervalued. However, it could also mean that

something is fundamentally wrong with the company. As with most ratios, be aware that this

varies by industry. This ratio also gives some idea of whether you're paying too much for what

would be left if the company went bankrupt immediately.

Also known as price to equity ratio.

7.EV/EBITDA:

EV / EBITDA, is a measure of the cost of a stock which is more frequently valid for comparisons

across companies than the price to earnings ratio. Like the P/E ratio, the EV / EBITDA ratio is a

35

measure of how expensive a stock is. It measures the price in the form of Enterprise value an

investor pays for the benefit of the company's cash flow in the form of EBITDA.

Enterprise value

EV/EBITDA = _______________________________________________

Earnings before interest and tax depreciation amortization

Where, EV=Market capital+debt+preference shares+minority interest-cash

Market capital=price value*equity shares

EV/EBITDA values can vary depending on EBITDA is calculated. EBITDA can vary

due to differences in counting of depreciation and amortization which can be counted at different

rates over time. Unlike P/E ratios, however, EV / EBITDA ratios can be used to compare a wide

variety of companies.P/E ratios can be an invalid way of comparing different companies for

several reasons which are accounted for in EV / EBITDA. It is a better measurement of

companies takeover value.

8.Operating cashflow:

A measure of how well current liabilities are covered by the cash flow generated from a

Company’s operations.

Formula: OCF Ratio= cash flow from operations .

Current liabilities

The operating cash flow ratio can gauge a company's liquidity in the short term. Using cash flow

as opposed to income is sometimes a better indication of liquidity simply because, as we

know, cash is how bills are normally paid off.

Companies operations

9.Current ratio:

36

The current ratio is the ratio of total current assets to total current liabilities. It is

calculated by dividing current assets by current liabilities:

Current assets

Current Ratio = ________________

Current liabilities

The current assets of a firm, as already stated, represent those assets which can be, in the

ordinary course of business, converted into cash within a short period of time, normally not

exceeding one year and include cash and bank balances, marketable securities, inventory of raw

materials, semi-finished (work-in-progress) and finished goods, debtors net of provision for bad

and doubtful debts, bills receivable and prepaid expenses. The current liabilities defined as

liabilities which are short-term maturing obligations to be met, as originally contemplated, within

a year, consist of trade creditors, bills payable, bank credit, provision for taxation, dividends

payable and outstanding expenses.

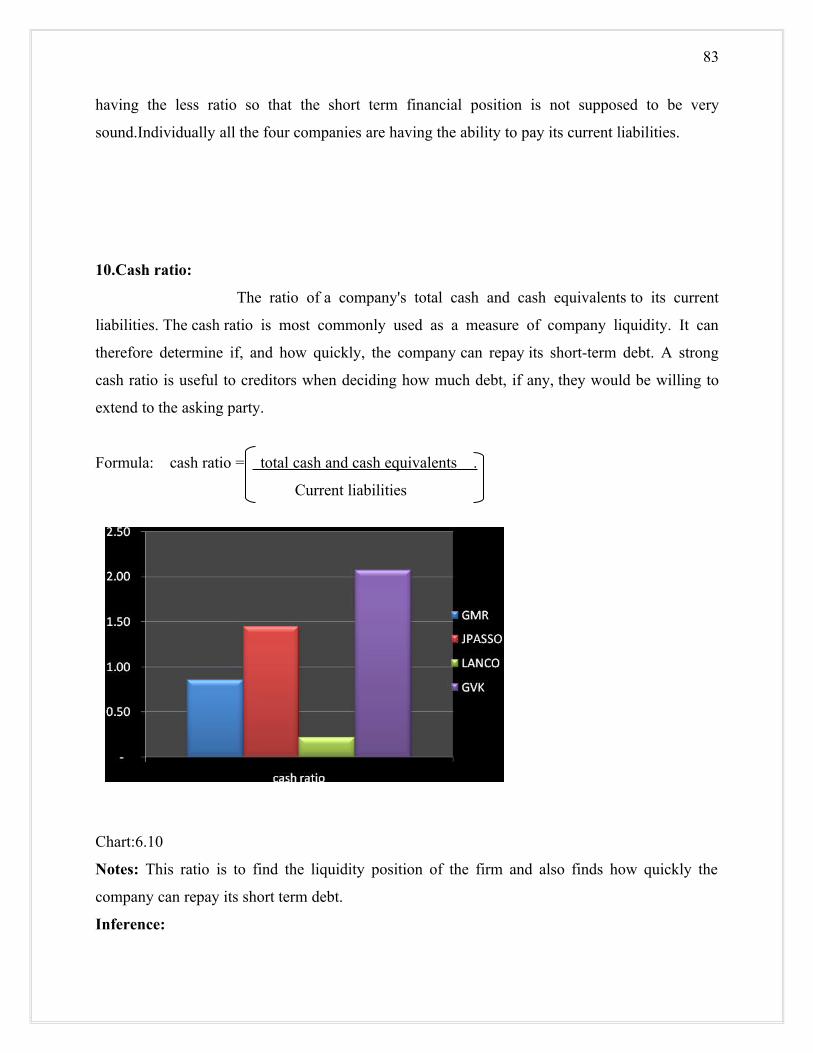

10. Cash ratio:

The ratio of a company's total cash and cash equivalents to its current

liabilities. The cash ratio is most commonly used as a measure of company liquidity. It can

therefore determine if, and how quickly, the company can repay its short-term debt. A strong

cash ratio is useful to creditors when deciding how much debt, if any, they would be willing to

extend to the asking party.

Formula: cash ratio = total cash and cash equivalents .

Current liabilities

The cash ratio is generally a more conservative look at a company's ability to cover its

liabilities than many other liquidity ratios. This is due to the fact that inventory and accounts

receivable are left out of the equation. Since these two accounts are a large part of many

companies, this ratio should not be used in determining company value, but simply as one factor

in determining liquidity.

11.Asset efficiency ratio:

The asset efficiency ratio provides an indication of how well the assets of a company

37

are utilized to generate a cash flow return. As an alternative measure, total property,

plant and equipment could be used in place of total assets for the denominator to reflect a

company’s ability to minimize waste in generating cash flows from operations based on its

investment in operational assets. These measures, tracked over a period of time, can provide

useful insights especially when the results are compared to other companies in the same industry.

Formula:

asset efficiency ratio = cash flow from operations .

Total assets

12.operating cash margin:

The operating cash margin ratio is somewhat similar to a traditional profit margin ratio

except for the use of CFO in place of either net income or operating income as the

numerator. Thus, the operating cash margin ratio provides a more robust indicator of

performance based on cash generating ability as opposed to a profit margin ratio with its focus on

accrual based accounting income. Essentially, the operating cash margin ratio highlights the

timing of cash flows with respect to the timing of sales.

Formula:

Operating cash margin = cash flow from operations .

sales

Therefore, this ratio can prove useful as part of a process to evaluate cash management

performance, as well as, credit granting policies and receivable collections. However, since cash

flow margins are likely to exhibit substantial variations among companies in different industries,

it is more effective to focus a comparative analysis on companies within the same industry.

13.Operating profit margin:

A ratio used to measure a company's pricing strategy and operating efficiency.

Calculated as:

38

Operating profit margin = earning before interest and tax .

Net sales

Operating profit margin is a measurement of what proportion of a company's revenue is

left over after paying for variable costs of production such as wages, raw materials, etc. A

healthy operating margin is required for a company to be able to pay for its fixed costs, such as

interest on debt. Also known as "net profit margin".

Operating profit margin gives analysts an idea of how much a company makes (before

interest and taxes) on each dollar of sales. When looking at operating margin to determine the

quality of a company, it is best to look at the change in operating margin over time and to

compare the company's yearly or quarterly figures to those of its competitors. If a company's

margin is increasing, it is earning more per dollar of sales. The higher the margin, is the better.

14.Basic earning power:

The basic earning power ratio compares earnings apart from the influence of taxes or

financial leverage,to the assets of the company.this allows more direct comparision of similar

firms that use different financing strategies or have different tax situations.

Formula:

Basic earning power = earnings before tax and interests .

39

Total assets

The ratio indicates basic probability of assets and is useful in comparing firms with different

degree of leverage.

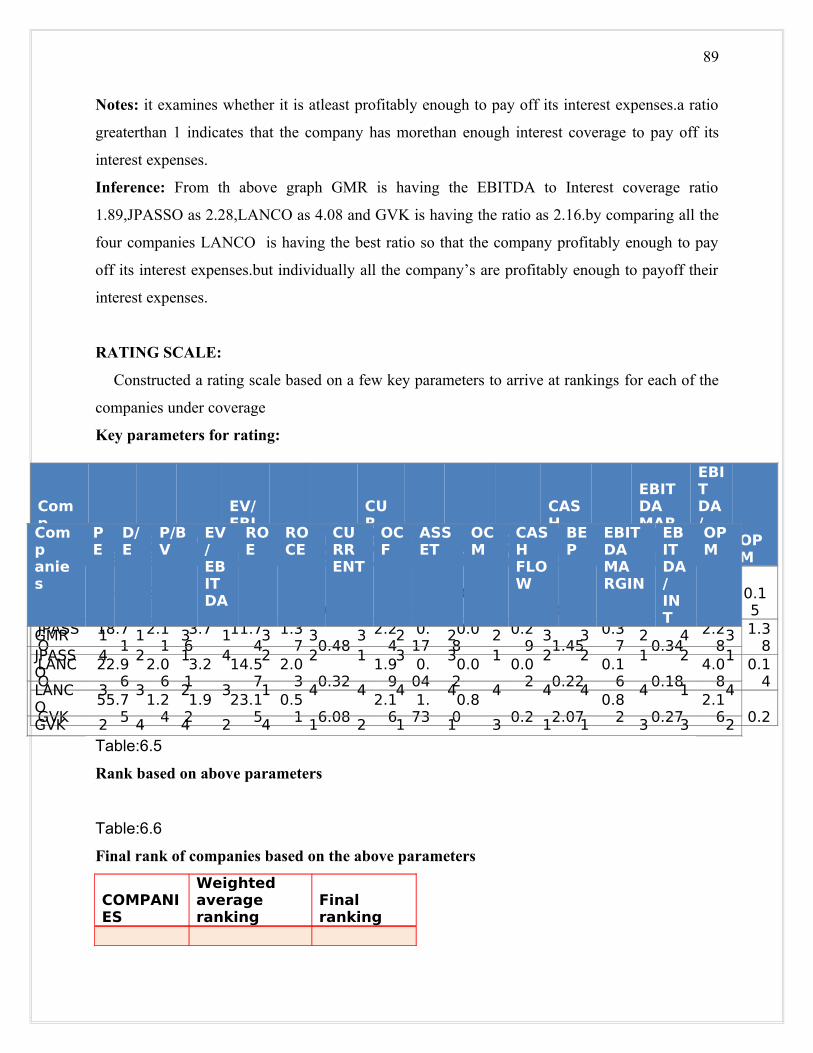

15.EBITDA to Interest coverage ratio:

The ratio that is used to assess a company’s financial durability by examining whether it is

at least profitably enough to pay off its interest expenses.

Formula:

EBITDA to interest coverage ratio= EBITDA .

Interest payments

A ratio greater than 1 indicates that the company has morethan enough interest coverage to

pay off its interest expenses.

3.5 Tips to improve financial health.

Author: Bill Hudley

Spend less money, or save more money or do both. If the annual income does nothing more

than remain constant, your financial condition will improve.

The above statement may sound come across as flippant, but it’s a fact of life,

regardless.Needless to say we all have different personalities and different responses to needs

and desires in life.

A very important yardstick, in my view, is the growth rate of personal assets. If you sit

down to all of the savings accounts, investment accounts and properly values and the total value

is greater than the same time of the previous year, it stands to improve that the financial health

intact and possibly improved.

3.5.1 Steps to Improve Financial Performance

Author: Terry Peltes

Given the challenges facing physicians, successful practices must take proactive steps to combat

negative trends and improve their overall financial performance.

40

To improve practice operations, processes can be streamlined to reduce costs; productivity

improvements can be implemented by the employees to increase revenue; a reporting structure

can be created that allows for better decision making by employees; and a rewards system can be

implemented to recognize hard-working employees.

To determine how you can improve your practice's performance, consider the

following management procedures.

1) Internal Cost Reduction Strategies

Cost reduction strategies focus on reducing the internal costs generated by

services provided to the marketplace.

2) External Cost Reduction Strategies

These strategies include the cost of services purchased from outside consultants or

vendors.

3) Asset and Credit Management Strategies

These strategies ensure that you are getting the most value from the resources invested in your

practice.

4) Personnel Resources

When managed properly, personnel costs and productivity can have a substantial

impact on profitability.

5) Management Reporting

The use of timely, relevant, properly formatted reports to manage your practice cannot

be overstated. This is a crucial link between setting financial and operational goals and

managing the practice to achieve them.

6) Revenue Enhancement

Industries can improve their financial performance by improving their ability to negotiate

favorable managed care contracts and reducing practice expenses as a percentage of revenue.

3.5.2 Excellence in Financial Management

Author: Matt H. Evans

Ratio analysis can be used to determine the time required to pay accounts payable

41

invoices.If the average number of days is close to the average credit terms, this may indicate

aggressive working capital management; i.e. using spontaneous sources of financing. However,

if the number of days is well beyond the average credit terms, this could indicate difficulty in

making payments to creditors.

3.5.3 Analyze Investments Quickly With Ratios

Author: Jonas Elmerraji

The information you need to calculate ratios is easy to come by: Every single number or

figure you need can be found in a company's financial statements. Once you have the raw data,

you can plug in right into your financial analysis and put those numbers to work for you.

Everyone wants an edge in investing but one of the best tools out there frequently is

misunderstood and avoided by new investors. When you understand what ratios tell you, as well

as where to find all the information you need to compute them, there's no reason why you

shouldn't be able to make the numbers work in your favour.

3.6 BUSINESS ANALYSIS:

Business analysis is the list of academic disciplines of identifying business needs and

determining solutions to business problems. Solutions often include a systems development

component, but may also consist of process improvement, organizational change or strategic

planning and policy development.

SWOT ANALYSIS:

A technique that enables a group or individual to move from everyday problems and

traditional strategies for a fresh perspective.swot is said to be strength and weakness as internal

environment ,opportunities and threats as external environment.

Strength:

Any existing or potential resources or capability within the organization that provides a competitive advantage in the market.

Weakness:

42

Any existing or potential force which could serve as a barrier to maintaining or achieving a competitive advantage in the market

Opportunities:

Any existing or potential force in external environment that ,if properly leveraged ,could provide a competitive advantage

Threats:

Any existing or potential force in the external environment that could erode a competitive advantage.

Aim of swot analysis:

• Take advantage of strengths and opportunities

• Minimize weaknesses and eliminate threats

3.6.1 Measures to improve the business process:

A Business process improvement (BPI) typically involves six steps:

1. Selection of process teams and leader:

Process teams, comprising 2-4 employees from various departments that are involved in the

particular process, are set up. Each team selects a process team leader, typically the person who

is responsible for running the respective process.

2. Process analysis training:

The selected process team members are trained in process analysis and documentation

techniques.

3. Process analysis interview:

The members of the process teams conduct several interviews with people working along the

processes. During the interview, they gather information about process structure, as well as

process performance data

43

4. Process documentation:

The interview results are used to draw a first process map. Previously existing process

descriptions are reviewed and integrated, wherever possible. Possible process improvements,

discussed during the interview, are integrated in to the process maps.

5. Review cycle:

The draft documentation is then reviewed by the employees working in the process.

additional review cycle may be necessary in order to achieve a common view(mental image) of

the process with all concerned employees. This stage is an interaction process.

6.Problem analysis:

A thorough analysis of process problems can then be conducted, based on the

process map, and information gathered about the process. At this time of the project, process goal

information from the strategy audit is available as well, and is used to derive measures for

process improvement.

3.7 CREDIT RATING AGENCIES IN INDIA:

The popular credit rating agencies in India are:

1.Credit Rating and Information Services of India Limited(CRISIL).

2. Investment Information and Credit Rating Agency of India Limited (ICRA) .

3. Credit Analysis and Research Limited (CARE).

4.Duff&phelps credit rating india private ltd(DCR)

5.FITCH rating agency

44

1.CRISIL :

CRISIL was set-up by ICICI and UTI in 1988, and rates debt instruments. Nearly half of

its ratings on the instruments are being used. CRISIL's market share is around 75%. It has

launched innovative products for credit risks assessment viz., counter party ratings and bank loan

ratings. CRISIL rates debentures, fixed deposits, commercial papers, preference shares and

structured obligations. Of the total value of instruments rated, debentures' accounted for 3 1.196,

formed deposits for 42.3% and commercial paper 6.6%. CRISIL publishes CRISIL rating in

SCAN that is a quarterly publication in Hindi and Gujarati, besides English.

CRISIL evaluation is carried out by professionally qualified persons and includes data

collection, analysis and meeting with key personnel in the company to discuss strategies, plans

and other issues that may effect ,evaluation of the company. The rating process ensures

confidentiality. Once the company decides to use rating, CRISIL is obligated to monitor the

rating over the life of the debt instrument.

2. ICRA :

ICRA was promoted by IFCI in 1991. During the year 1996-97, ICRA rated 261 debt

instruments of manufacturing companies, finance companies and financial institutions equivalent

to Rs. 12,850 crore as compared to 293 instruments covering debt volume of Rs. 75,742 crore in

1995-96. This showed a decline of 83.0% over the year in the volume of rated debt instruments.

Of the total amount rated cumulatively until March-end 1997, the share in terms of number of

instruments was 28.5% for debentures(including long term instruments), 49.4% for Fixed

Deposit programme (including medium- term instruments), and 22.1% for Commercial Paper

Programme (including shortterm instruments). The corresponding figures of amount involved for

these three broad rated categories was 23.8% for debentures, 52.2% for fixed deposits, and

24.0% for Commercial Paper.

The factors that ICRA takes into consideration for rating depend on the nature of

borrowing entity. The inherent protective factors, marketing strategies, competitive edge,

competence and effectiveness of management, human resource development policies and

practices, hedging of risks, trends in cash flows and potential liquidity, financial flexibility, asset

45

quality and past record of servicing of debt as well as government policies affecting the industry

are examined. Besides determining the credit risk associated with a debt instrument, ICRA has

also formed a group under Earnings Prospects and Risk Analysis (EPRA). Its goal is to provide

authentic information on the relative quality of the equity. This requires examination of almost

all parameters pertaining to the fundamentals of the company including relevant sectoral

perspectives. This qualitative analysis is reinforced and completed by way of the unbiased

opinion and informed perspective of one analyst and wealth of judgement of committee

members. ICRA opinions help the issuing company to broaden the market for their equity. As

the name recognition is replaced by objective opinion, the lesser know compapies are also able to

access the equity market.

3.CARE :

CARE is a credit rating and information services company promoted by IDBI jointly with

investment institutions, banks and finance companies. The company commenced its operations in

October 1993. 'In January 1994, CARE commenced publication of CAREVIEW, a quarterly

journal of CARE ratings. In additioh to the rationale of all accepted ratings, CAREVIEW often

carries special features of interest to issuers of debt instruments,investors and other market

players.

4.DCR:

DCR India or Duff & Phelps Credit Rating India Private Ltd is one of the top credit

rating agencies in India. Over the years, DCR India has been providing excellent services to its

clients. Duff & Phelps Credit Rating India Private Ltd (DCR India) has played an important role

in rating India's forex debt obligations.

46

Duff & Phelps Credit Rating India Private Ltd (DCR India) rated the forex debt

obligations of India as ' BBB-' or a Triple B Minus. This rating is of great importance for the

economy of India and the credibility of the national government.

This rating reflects the fact that the Indian national government is trying its best to improve the

state of Indian economy. As per the rating of DCR India, the national government of India is

trying to bring about a better economic environment through the introduction of several

economic policies and plans for the last 17 years.

Over the years India has had powerful accounts of payments. Since the decade of 1990s

the records of debt service have also been impressive. The external debt indicators of India are

also showing better patterns. All these support the rating provided by Duff & Phelps Credit

Rating India Private Ltd (DCR India)

5.FITCH:

Fitch ratings was founded as fitch publishing company on December 24,1913 by John

Knowles fitch.Located in the heart of the financial district in new York city,the fitch puvlishing

company began as a publisher of financial statistics whose consumers included the new York

stock exchange.it became a recognized leader in providing critical financial statistics to the

investment community through such publications as the “fitch bond book” and the “fitch stock

and bond manual.”In 1924,the fitch publishing company introduced the now familiar

“AAA”to”D” ratings scale to meet the growing demand for independent analysis of financial

securities.

Fitch ratings was one of the three ratings first agencies first recognized as a nationally recognized

statistical rating organization(NRSRO) by the securities and exchanges commission in 1975.

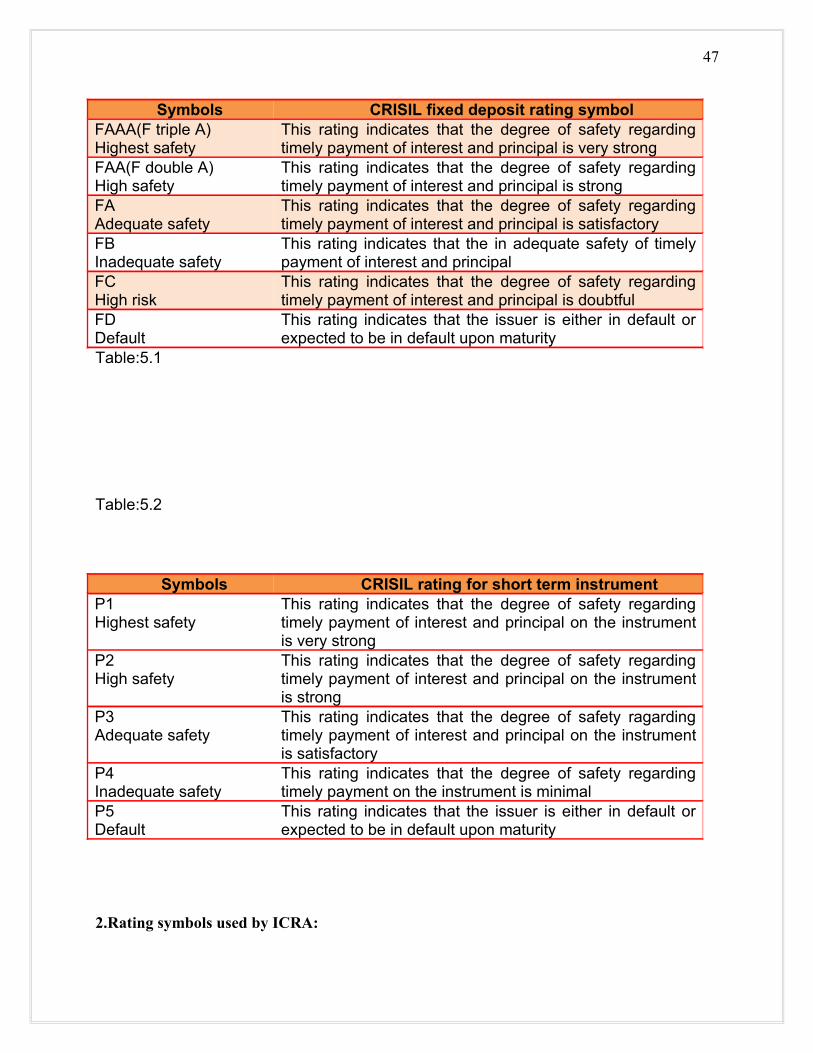

3.7.1 Rating symbols and their explaination:1.Rating symbols used by CRISIL:

47

Table:5.1

Table:5.2

2.Rating symbols used by ICRA:

Symbols CRISIL fixed deposit rating symbolFAAA(F triple A)Highest safety

This rating indicates that the degree of safety regarding timely payment of interest and principal is very strong

FAA(F double A)High safety

This rating indicates that the degree of safety regarding timely payment of interest and principal is strong

FA Adequate safety

This rating indicates that the degree of safety regarding timely payment of interest and principal is satisfactory

FBInadequate safety

This rating indicates that the in adequate safety of timely payment of interest and principal

FCHigh risk

This rating indicates that the degree of safety regarding timely payment of interest and principal is doubtful

FDDefault

This rating indicates that the issuer is either in default or expected to be in default upon maturity

Symbols CRISIL rating for short term instrumentP1Highest safety

This rating indicates that the degree of safety regarding timely payment of interest and principal on the instrument is very strong

P2High safety

This rating indicates that the degree of safety regarding timely payment of interest and principal on the instrument is strong

P3Adequate safety

This rating indicates that the degree of safety ragarding timely payment of interest and principal on the instrument is satisfactory

P4Inadequate safety

This rating indicates that the degree of safety regarding timely payment on the instrument is minimal

P5Default

This rating indicates that the issuer is either in default or expected to be in default upon maturity

48

Table:5.3

Symbols Long term debt-debentures,bonds and preference shares

LAAAHighest safety

Indicates fundamentally strong position.Risk factors are negligible. There may be circumstances adversely affecting the degree of safety but such circumstances, as may be visualised, are not likely to affect the timely payment of principal and interest as per terms

LAAHigh safety

Risk factors are modest and may vary slightly. The protective factors are strong and prospects of timely payment of interest and principal as per terms, under adverse a circumstances, as may be visual-ised, differ from LAAA only marginally.

LAAdequate safety

Risk factors are more variable and greater in periods of economic stress. The protective factors are average and any adverse change in circumstances, as may be visualised, may alter the fundamental strength and affect the timely payment of principal and interest as per terms

LBBBModerate safety

Considerable variability in risk factors.The protective factors are below average. Adverse changes in business/economic circumstances are likely to affect the timely payment of principal and interest as per terms.

LBRisk prone

Risk factors indicate that obligations may not be honoured when due. The protective factors are narrow. Adverse changes in business/ ecanomic conditions could result in inability unwillingness to service debt on time as per terms.

LCSubstantial risk

There are inherent elements of risk and timely servicing of debt/obligations could be possible only in case of continued existence of favourable circumstances.

LDDefault

Extremely speculative. Either already in default of payment of interest and/or principal as per terms or expected to default. Recovery is only likely on liquidation or reorganisation.

49

Table:5.4

3.Rating symbols used by CARE:

Symbols Medium term debt including fixed deposit programmes

MAAAHighest safety

The prospect of timely servicing of the interest and principal as per terms is the best

MAAHigh safety

The prospect of timely servicing of the interest and principal as per terms is high but not high as in MAAA rating

MAAdequate safety

The prospect of timely servicing of the interest and principal is moderate.however,debt servicing may be affected by adverse changes in the business/economic conditions

MBInadequate safety

The timely payment of interest and peincipal are more likely to be affected by future uncertainties

MCRisk prone

Susceptibility to default high.adverse changes in business/economic conditions could result in inability/unwillingness to service debts on time and as per terms

MDDefault

either in default or expected to default

A1Highest safety

The prospect of timely payment of debt/obligation is the best

A2High safety

The relative safety is marginally lower than in A1 rating

A3Adequate safety

The prospect of timely payment of interest and instalment is adequate but any adverse change in business/economic conditions may affect the fundamental strength

A4Risk prone

The degree of safety is low.likely to default in case of adverse changes in business/economic conditions

A5Default

Either in default or expected to default

50

Symbols Long term and medium term instrumentsAAAHighest safety

Debt instrument carrying the rating are considered to be of the best quality,carrying negligible investment risk.debt service payments are protected by stable cash flows with good margin.while the underlying assumptions may change,such changes as can be visualised are most unlikely to impair the strong position of such instruments

AAHigh safety

Instruments carrying this rating are judged to be of high quality by all standards.They also classified as high investment grade.They are rated lower than AAA.

AAdequate safety

Instruments with this rating are considered upper medium instrument and have many favourable investment attributes.safety for principal and interest are considered adequate.assumptions that do not materialise may have a greater impact as compared to the instruments rated higher.

BBB Such instruments are considered to be of investment grade.they indicate sufficient safety for payment of interest&principal,at the time of rating.however,adverse changes in assumptions are more likely to weaken the debt servicing capability compared to the higher rated instruments.

BB Such instruments are considered to be speculative,with inadequate protection for interest and principal payments

B Instruments with some ratings are generally classified susceptible to default.while interest and principal payments are being met,adverse changes in business conditions are likely to lead to default.

C Such instruments carry high investment risk with likelihood of default in the payment of interest and principal

D Such instruments are of the lowest category.They are either in default or are likely to be in default soon

Table: 5.5

Symbols Short term investmentsPR-1 Instruments would have superior capacity for repayments

of short term promissiory obligations.issuers of such instruments will normally be characterised by leading market positions in established industries, high rates of

51

return on funds employed etc.,PR-2 Instruments would have strong capacity for repayment of

short term promissory obligations.issuer would have most of the characteristics as for those with PR-1 instruments but to a lesser degree.

PR-3 Instruments have an adequate capacity for repayment of short term promissiory obligations.the effect of industry characteristics and market composition may be more pronounced.variability in earnings and profitability may result in changes in the level of debt protection

PR-4 Instruments have minimal degree of safety regarding timely payment of short term promisiory obligations and safety is likely to be adversally affected by short term adversity or less favourable conditions

PR-5 The instrument is in default or is likely to be in default on maturity

Table: 5.6

Symbols Credit analysis ratingCARE-1 Excellent debt management capability.such companies

will normally be characterised as leaders in the respective industries

CARE-2 Very good debt management capability.such companies would normally be regarded as close to those rated CARE-1,but with a lower capability to withstand changes in assumptions

CARE-3 Good capability for debt management.such companies are considered medium grade.assumptions that do not materialise may impair debt management capability in future

CARE-4 Barely satisfactory capability for debt management.the capacity to meet obligations is likely to be adversely affected by short term adversity or less favourable conditions

CARE-5 Poor capability of debt management.such companies are in default or are likely to default in meeting their debt obligations

Table: 5.7

3.7.2 RATING PROCESS

Client Agencies

Required for

Submits information and detailed schedules

Interacts with team, responds to queries&provides additional data necessary for the analysis

Assigns rating Team interacts with client, undertakes site visits & analyses data submitted by clients.

Press release, published in website, care view.

Rating kept under periodic surveillance

Appeal for review of rating (once)

52

Yes

NO

Chart: 3.2

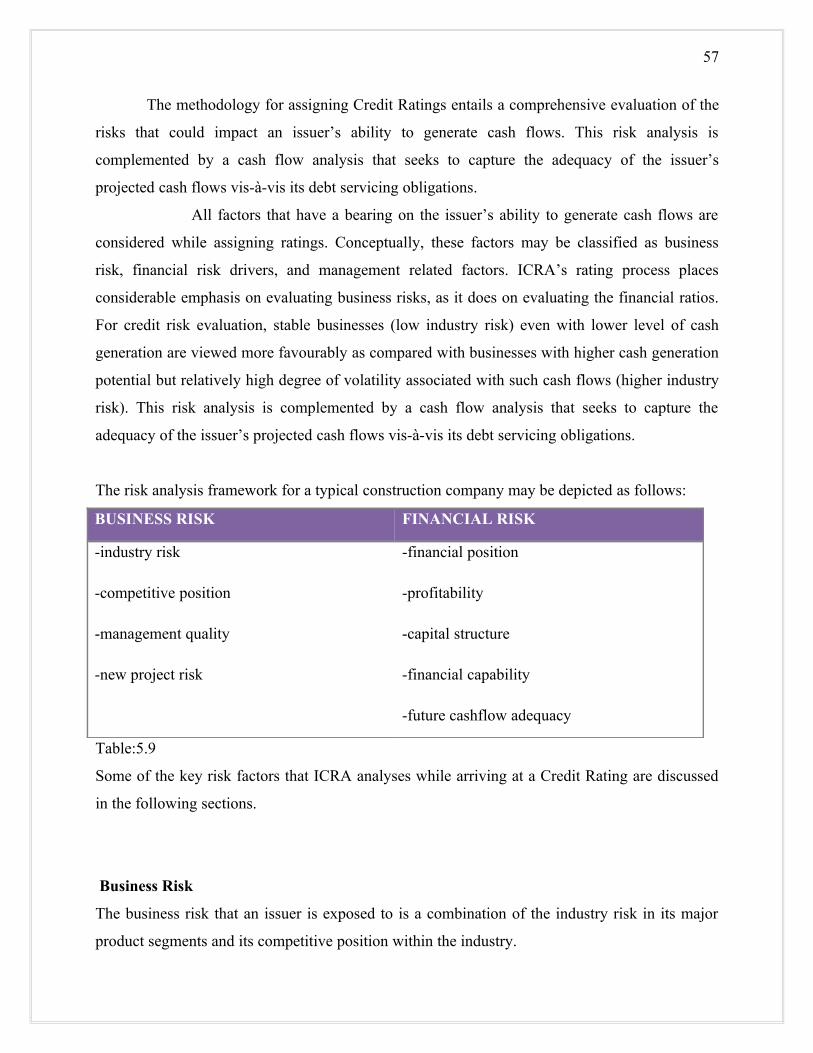

3.7.3 RATING AGENCIES METHODOLOGIES: The construction is one of the important sectors in India today. The industry can

be gauged from the fact that supports a large number of upstream and downstream industries.

The team does analysis of the information

Rating commitee awards rating.rating letter and rationale issued to client

Accept rating

53

Moreover, the industry has strong linkages with the overall economy and enjoys a large

economic multiplier effect.

The Indian construction industry can classified into three broad subgroups as follows:

Category List of construction activitiesResidential and

Commercial/industrial

Residential and commercial buildings and complexes

such as houses,offices,hospitals,restaurants,shops and