1 ĐẠI HỌC HOA SEN Khoa Kinh tế Thương mại

5 Net Present Value and Other Investment Criteria

Oct 30, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

ĐẠI HỌC HOA SENKhoa Kinh tế Thương mại

3

CORPORATE FINANCE

CHAPTER 5

NET PRESENT VALUE and OTHER INVESTMENT CRITERIA

4

References

• Fundamentals of Corporate Finance, Brealey et al., McGraw Hill, 5th edition, USA, 2007.

• Foundation of Financial Management, Block & Hirt, McGraw Hill, 12th edition,USA, 2008.

• Other relevant materials.

5

Chapter 5: NET PRESENT VALUE and OTHER INVESTMENT

CRITERIA

• Main Contents:

1. Net Present Value

2. Other Investment Criteria

3. Examples of mutually exclusive projects

4. Capital rationing

5. A last look

6

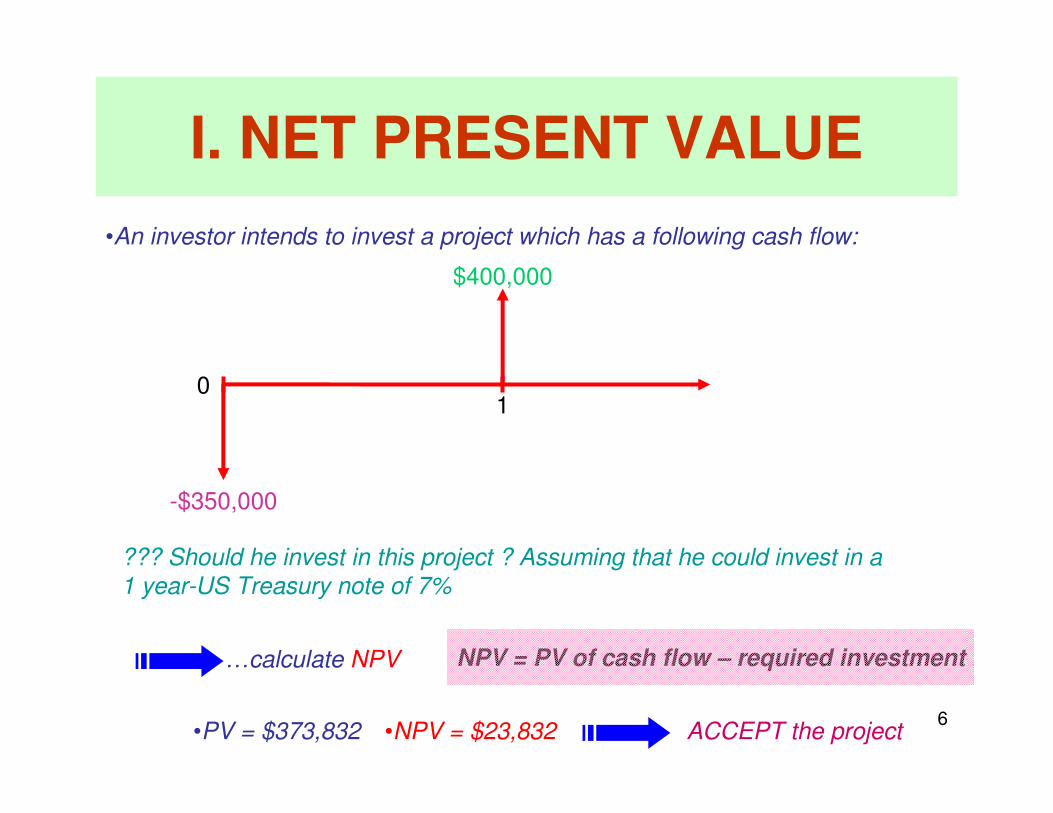

I. NET PRESENT VALUE

•An investor intends to invest a project which has a following cash flow:

01

-$350,000

$400,000

??? Should he invest in this project ? Assuming that he could invest in a 1 year-US Treasury note of 7%

…calculate NPV NPV = PV of cash flow – required investment

•PV = $373,832 •NPV = $23,832 ACCEPT the project

7

I. NET PRESENT VALUE (cont’d)

1 year-US Treasury note of 7%

Opportunity cost of capital

�NPV – present value of cash flows minus required investment

8

I. NET PRESENT VALUE (cont’d)

�Risk and Present Value

… the investment is more risky than investing a 1 year-treasury note of 7%

…the investment is as risky as investing a stock with rate of return of 12%

01

-$350,000

$400,000

•NPV with rate of return of 12% = $7,143 < $23,832

A risky dollar is worth less than a safe one

9

I. NET PRESENT VALUE (cont’d)

10

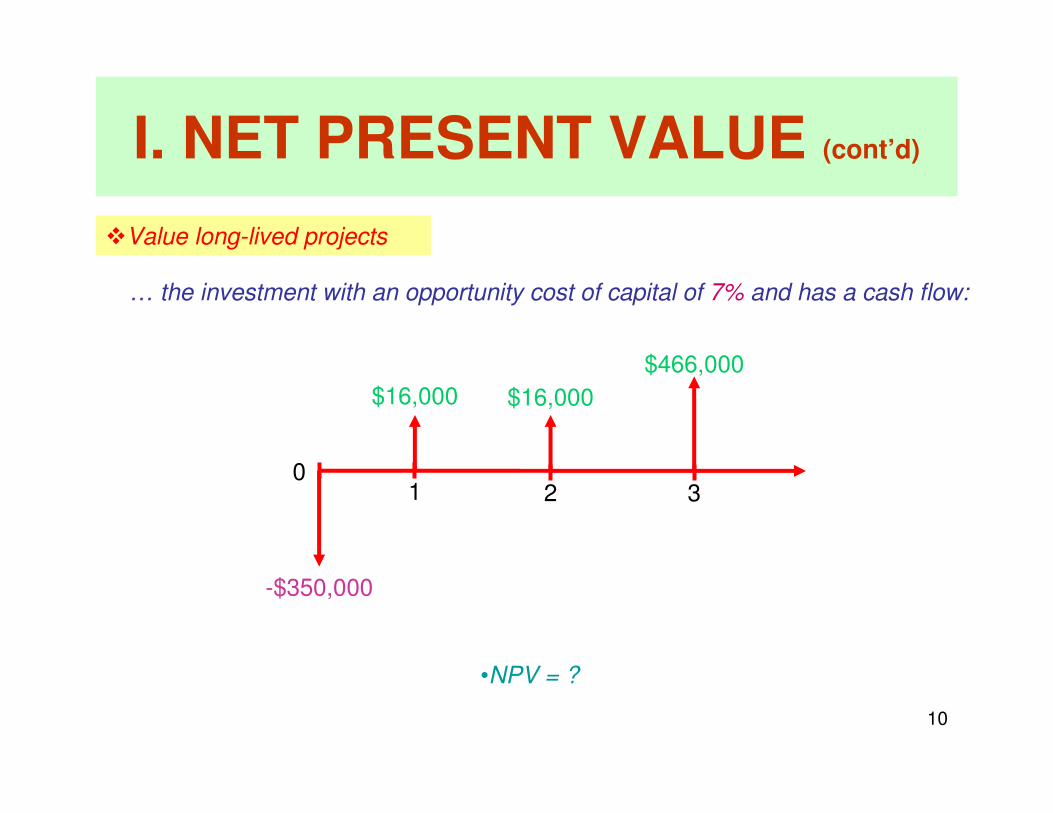

I. NET PRESENT VALUE (cont’d)

�Value long-lived projects

… the investment with an opportunity cost of capital of 7% and has a cash flow:

01

-$350,000

$16,000

•NPV = ?

2

$16,000

3

$466,000

11

I. NET PRESENT VALUE (cont’d)

�Value long-lived projects (cont’d)

12

I. NET PRESENT VALUE (cont’d)

�Value long-lived projects (cont’d)

In case that the investor decides to sell this project by selling 1,000 stocks

What is the price of one stock ?

•Price per share: $409.3

01

-$350,000

$16

2

$16

3

$466

•Net gain: ~ $59,300

13

I. NET PRESENT VALUE (cont’d)

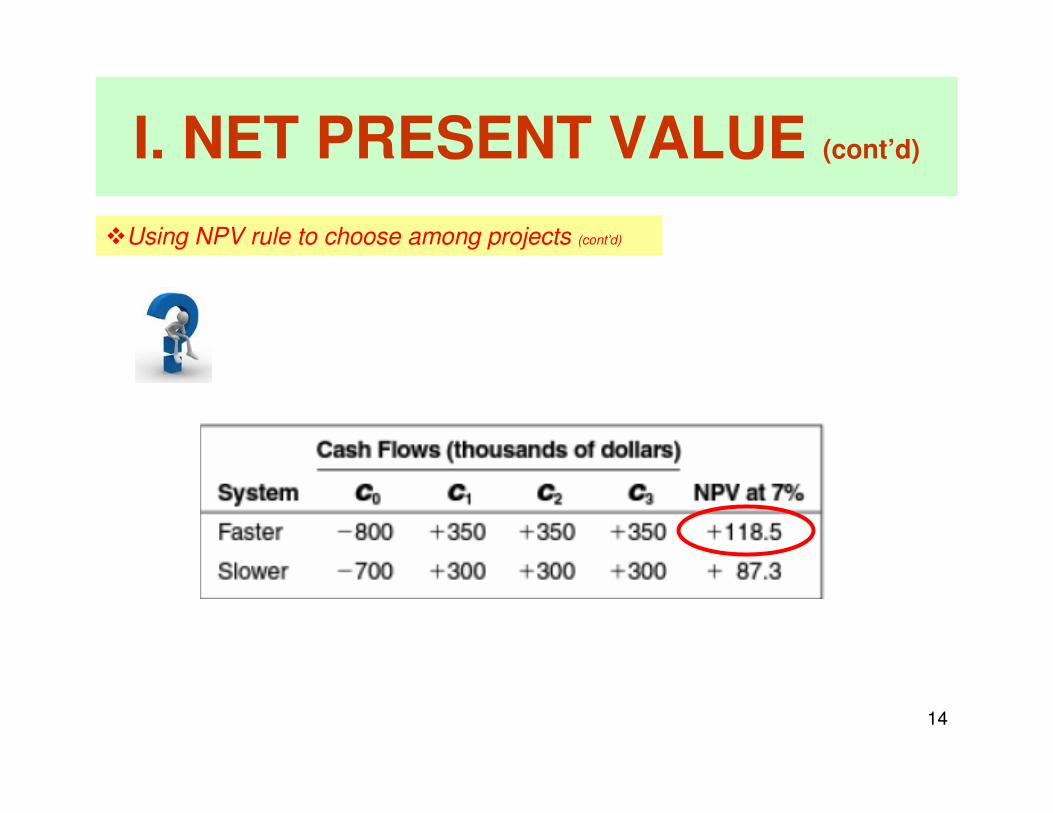

�Using NPV rule to choose among projects

Project A and B are Mutual exclusive projects

Project A

What would I

choose ?

Project B

Select the project whose NPV is higher!!

14

I. NET PRESENT VALUE (cont’d)

�Using NPV rule to choose among projects (cont’d)

15

II. OTHER INVESTMENT CRITERIA

…time until cash flows recover the initial investment in the project

�Payback period

Payback rule

…a project should be accepted if its payback period is less than a specified cutoff period

WHAT IF ?

A or B ??NPV < 0, the payback period = 1NPV > 0, the payback period = 2

NPV > 0, the payback period = 2

Project B

A or B ??NPV > 0, the payback period = 1

Select…Project A

16

II. OTHER INVESTMENT CRITERIA

Which project should you choose if you don’t care NPV ?

�Payback period (cont’d)

…calculate Discounted Payback

17

II. OTHER INVESTMENT CRITERIA

�Payback period (cont’d)

•Discounted Payback

How long must the project last in order to offer a positive NPV ?

Steps to calculate Discounted Payback

1 Calculate the PV of the cash flow

2 Add each PV up to be equal with initial investment

18

II. OTHER INVESTMENT CRITERIA

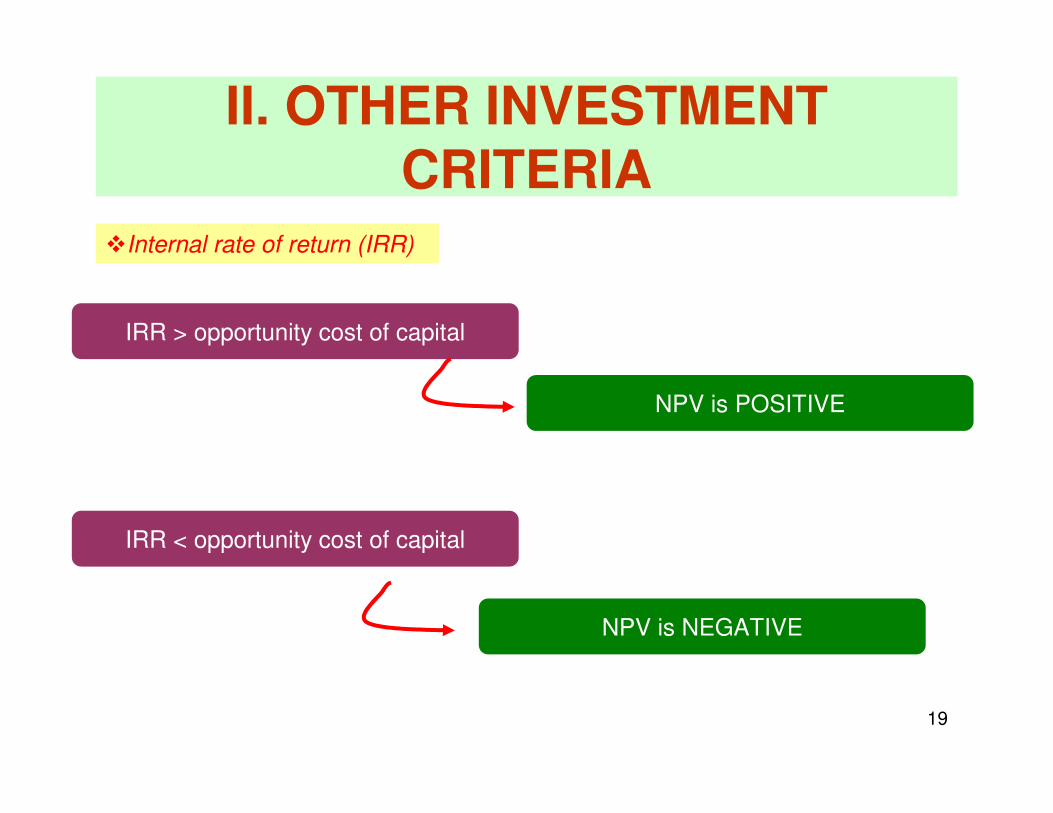

�Internal rate of return (IRR)

…selecting project whose IRR is higher than the opportunity cost of capital

??? How to calculate the IRR ?

Setting NPV = 0 and calculate the IRR

IRR is the discount rate at which NPV = 0

19

IRR > opportunity cost of capital

II. OTHER INVESTMENT CRITERIA

�Internal rate of return (IRR)

NPV is POSITIVE

IRR < opportunity cost of capital

NPV is NEGATIVE

20

II. OTHER INVESTMENT CRITERIA

�Internal rate of return (IRR)

21

II. OTHER INVESTMENT CRITERIA

�Internal rate of return (IRR)

Supposing that you have a project with the following relevant cash flow:

…calculate IRR

22

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR

is not the opportunity cost

is the profitability of a project

23

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR

•Pitfall 1: Lending or Borrowing

???D and E have the same attraction ?

Not exactly !!!!!

D

E What received today is repaid more and more tomorrow

You are in borrowing with high interest rate

What paid today is received more and more tomorrow

You are in lending with high interest rate

24

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR (cont’d)

•Pitfall 2: Multiple Rate of Return

-$40+$15+$15+$15+$15-$22

C5C4C3C2C1C0

Cash flow

…the project has two IRRs

25

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR (cont’d)

•Pitfall 2: Multiple Rate of Return (cont’d)

Solution Modified IRR

1 Combining last two cash flows into one PV of year 4

2 If the PV is negative, combining last three cash flows into one PV of year 3

�Steps to calculate modified IRR (applied for a 4-year project):

3 If the PV is still negative, combining last four cash flows into one PV of year 2and so on

4If the PV is positive, making a new modified cash flow and calculate the modified IRR

26

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR (cont’d)

•Pitfall 2: Multiple Rate of Return (cont’d)

IRR = 12.53%0)1(98.10

11522 2 =

+

+

+

+−

IRRIRR

r = 10%

27

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR (cont’d)

•Pitfall 3: Mutually exclusive projects

…the higher IRR does not mean the higher NPV

28

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR (cont’d)

29

II. OTHER INVESTMENT CRITERIA

�Some pitfalls with the IRR (cont’d)

•Pitfall 4: Mutually exclusive projects involving different outlays

Misranking as comparing projects with the same lives but different outlays

IRR mistakenly favor small projects with high rates of return but low NPVs

30

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS

Timing decision

Long and short lived equipment

Replacement decision

31

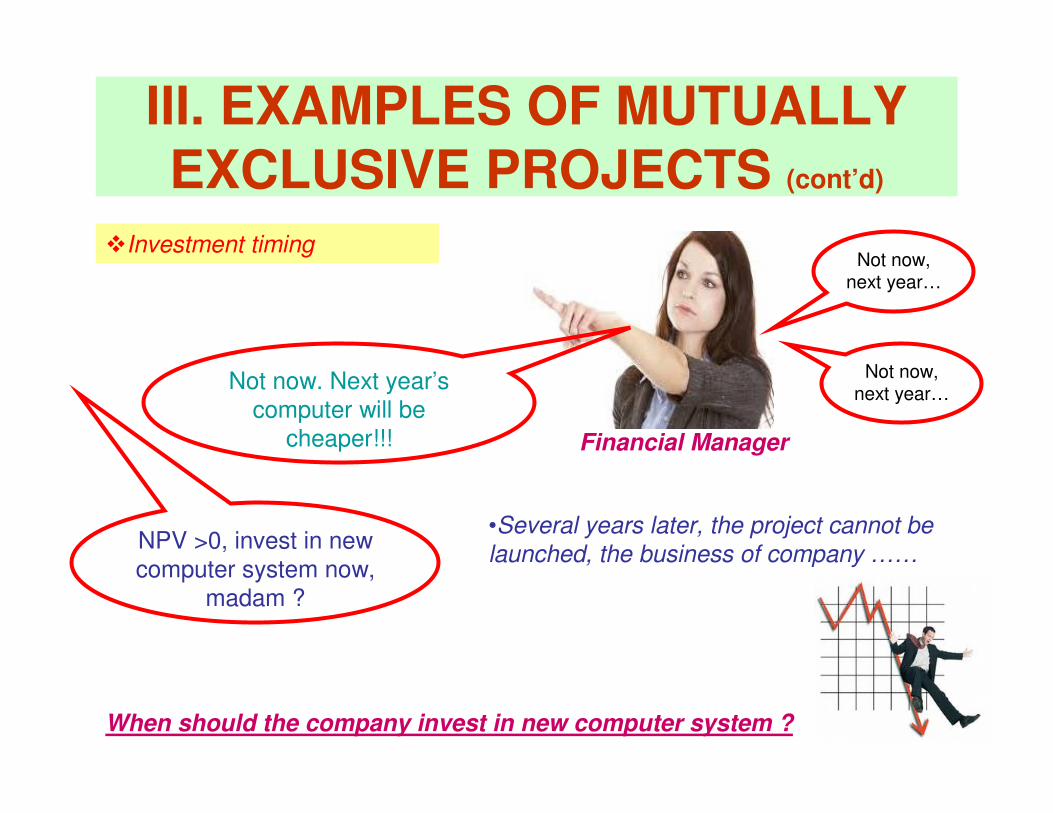

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS (cont’d)

When should the company invest in new computer system ?

�Investment timing

NPV >0, invest in new computer system now,

madam ?

Not now. Next year’s computer will be

cheaper!!!

•Several years later, the project cannot be launched, the business of company ……

Not now, next year…

Not now, next year…

Financial Manager

32

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS (cont’d)

�Investment timing (cont’d)

•A new computer system can last for 4 years

…choosing an investment time that results in the highest NPV today

33

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS (cont’d)

�Investment timing (cont’d)

34

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS (cont’d)

�Long versus short lived equipment

…selecting two machines with the same function:

Which machine should Samsung choose ?

…calculating the Equivalent Annual Annuity

…and select the machine that has the lowest Equivalent Annual Annuity

…the cash flow per period with the same PV as the cost of buying and operating a machine

35

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS (cont’d)

�Long versus short lived equipment (cont’d)

…selecting two machines with the same function:

Machine Fshould be selected

36

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS (cont’d)

�Replacing an Old Machine

•…will be last in 2 more years

•…cost $12,000 per year to operate

CURRENT MOTO

•…will be last in 5 years

•…cost $8,000 per year to operate

NEW MOTO

Which moto should you choose ?Higher than 12

Continue using the current moto

37

III. EXAMPLES OF MUTUALLY EXCLUSIVE PROJECTS (cont’d)

�Replacing an Old Machine (cont’d)

38

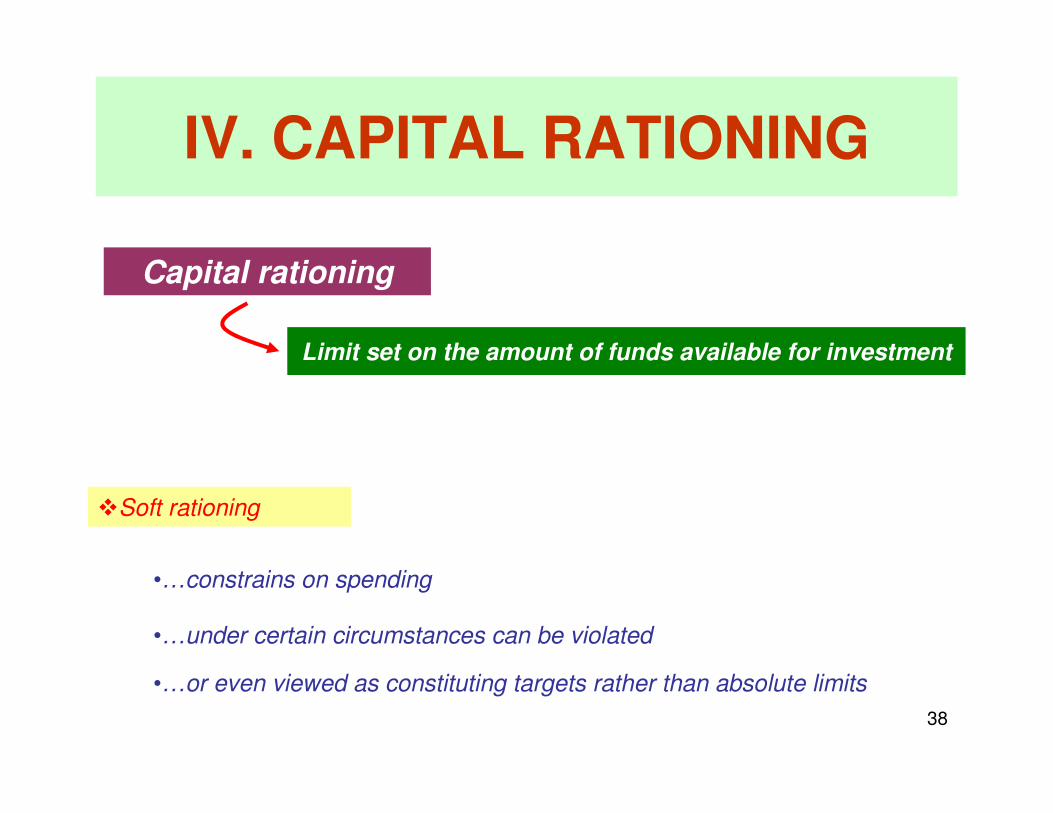

IV. CAPITAL RATIONING

�Soft rationing

Capital rationing

Limit set on the amount of funds available for investment

•…constrains on spending

•…under certain circumstances can be violated

•…or even viewed as constituting targets rather than absolute limits

39

IV. CAPITAL RATIONING (cont’d)

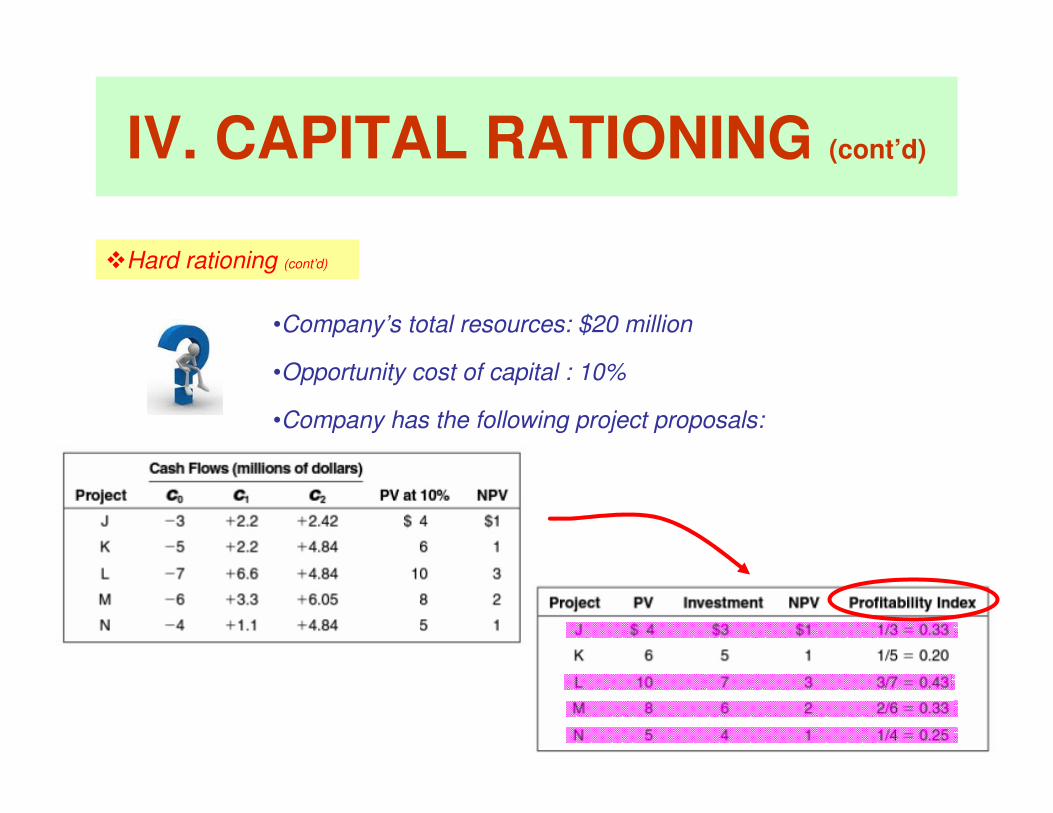

�Hard rationing

•…a capital budget must be adhered

•…applied as company has limited resources

40

IV. CAPITAL RATIONING (cont’d)

�Hard rationing (cont’d)

•Company’s total resources: $20 million

•Opportunity cost of capital : 10%

•Company has the following project proposals:

41

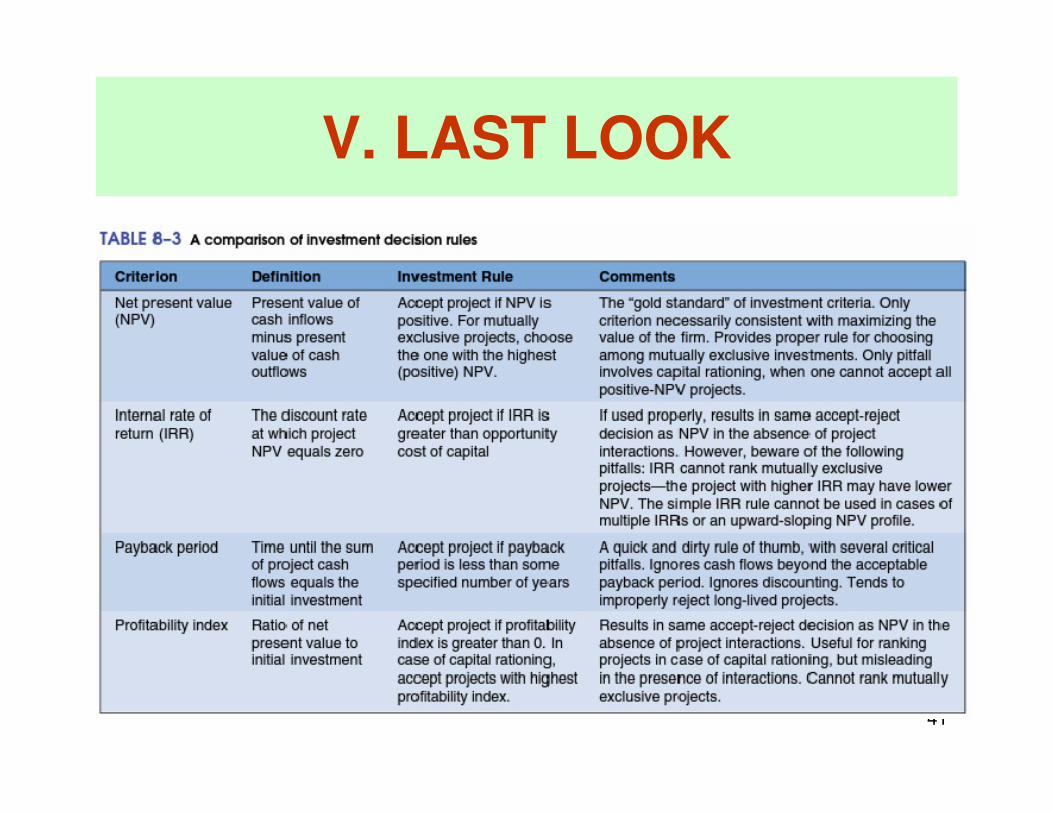

V. LAST LOOK

42

Thank you for your attention !

Related Documents