75 Pakistan Economic and Social Review Volume XXXIX, No. 1 (Summer 2001), pp. 75-86 ELASTICITY AND BUOYANCY OF MAJOR TAXES IN PAKISTAN FAUZIA MUKARRAM* Abstract. This paper examines the elasticity and buoyancy of major taxes in Pakistan over the period 1981-2001 by using the Chain Indexing Technique. The study reveals that estimates of elasticity and buoyancy are higher for direct taxes followed by sales taxes. However, customs and excise duties appear to be relatively rigid, due to which the overall tax elasticity is also low. Further, the estimates of buoyancy are higher than their corresponding elasticities for all the taxes, confirming thereof that most of the growth in revenues has been achieved due to enhanced tax rates and broadened tax bases instead of automatic growth. I. INTRODUCTION The ever-widening budgetary gap in Pakistan has compelled successive governments to find new sources of revenues. With the contracting external capital inflow tremendous pressure has build up on the internal revenue generation to meet the growing expenditure needs. However, the rigidity of the taxation system has become a major constraint in the way of indigenous resource mobilization efforts. Table 1 shows that tax to GDP ratio has in fact decreased over time. In this regard, predicting the level of revenues from each tax is an essential task. Therefore, the concept of elasticity and buoyancy of taxes is a crucial factor in assessing the effectiveness of the tax system and for the design of future tax policy. Elasticity of taxes 1 measures the change in tax revenues due to the change in GDP (or relevant GDP *The author is an Economist with Social Policy and Development Centre, Karachi. Acknowledgements are due to Dr. Hafiz A. Pasha, former Managing Director of Social Policy and Development Centre, who provided technical guidance for this study and motivated the author for undertaking this work. All the shortcomings, however, belong to the author only. 1 The coefficient of elasticity depends upon the level of tax rates, the progressivity of the rate structure and the responsiveness of the tax base to changes in GDP.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

75

Pakistan Economic and Social Review Volume XXXIX, No. 1 (Summer 2001), pp. 75-86

ELASTICITY AND BUOYANCY OF MAJOR TAXES IN PAKISTAN

FAUZIA MUKARRAM*

Abstract. This paper examines the elasticity and buoyancy of major taxes in Pakistan over the period 1981-2001 by using the Chain Indexing Technique. The study reveals that estimates of elasticity and buoyancy are higher for direct taxes followed by sales taxes. However, customs and excise duties appear to be relatively rigid, due to which the overall tax elasticity is also low. Further, the estimates of buoyancy are higher than their corresponding elasticities for all the taxes, confirming thereof that most of the growth in revenues has been achieved due to enhanced tax rates and broadened tax bases instead of automatic growth.

I. INTRODUCTION The ever-widening budgetary gap in Pakistan has compelled successive governments to find new sources of revenues. With the contracting external capital inflow tremendous pressure has build up on the internal revenue generation to meet the growing expenditure needs. However, the rigidity of the taxation system has become a major constraint in the way of indigenous resource mobilization efforts. Table 1 shows that tax to GDP ratio has in fact decreased over time. In this regard, predicting the level of revenues from each tax is an essential task. Therefore, the concept of elasticity and buoyancy of taxes is a crucial factor in assessing the effectiveness of the tax system and for the design of future tax policy. Elasticity of taxes1 measures the change in tax revenues due to the change in GDP (or relevant GDP *The author is an Economist with Social Policy and Development Centre, Karachi.

Acknowledgements are due to Dr. Hafiz A. Pasha, former Managing Director of Social Policy and Development Centre, who provided technical guidance for this study and motivated the author for undertaking this work. All the shortcomings, however, belong to the author only.

1The coefficient of elasticity depends upon the level of tax rates, the progressivity of the rate structure and the responsiveness of the tax base to changes in GDP.

76 Pakistan Economic and Social Review

component/tax base), which is also termed as ‘automatic’ change. If the elasticity of taxes exceeds unity there is no need to manipulate tax rates frequently, as frequent and ad hoc changes in tax rates distort consumption and investment decisions thereby creating uncertainty. The decomposition of elasticity into tax to base and base to GDP elasticity makes it possible to get the response of the tax yield to a change in the tax base2 and, the response of tax base to a change in GDP. Buoyancy of taxes measures the change in tax revenues due to the change in tax rates, bases, regulations, or administration efficiency, which are also known as ‘discretionary’ changes. Buoyancy measures the total change in tax revenues, i.e., not only due to the change in GDP but also due to the discretionary tax changes.

TABLE 1

Tax to GDP Ratio of Major Taxes (%)

Year Total Taxes

Direct Taxes

Customs Duties

Excise Duties

Sales Tax

1980-81 12.74 2.57 5.17 3.85 1.15

1985-86 11.31 1.92 5.36 3.05 0.98

1990-91 11.82 1.96 5.30 2.60 1.96

1995-96 12.26 3.51 4.07 2.34 2.34

2000-01 11.71 3.86 1.86 1.50 4.49

The taxation system of Pakistan has undergone major restructuring over the late 1980s, and more so, during the decade of the 1990s. It is thus important to analyze the way it has affected the revenue generating potential of various taxes. However no study has been undertaken over the entire decade to calculate the elasticity and buoyancy of major taxes for the period. The most recent estimates are available only up to the year 1990 thus necessitate updating the analysis. This study, therefore, is an effort towards this end.

II. REVIEW OF LITERATURE Akbar and Ahmed (1997) examined the elasticity and buoyancy of various taxes and expenditures of Federal Government during the period 1973-1990

2Growth in tax base is caused by both the increase in GDP and discretionary changes.

MUKARRAM: Elasticity and Buoyancy of Major Taxes in Pakistan 77

by using the Prest methodology (1962). They found that the overall elasticity and buoyancy of taxes were low because of the low elasticity and buoyancy of customs duty and excise duty. The elasticity and buoyancy were found to be relatively higher for sales tax followed by income taxes. Gillani (1986) estimated the elasticity and buoyancy of Pakistan’s federal tax system for the years 1971-72 to 1982-83 by using the Divisia Index Method (DIM) and the Proportional Adjustment Method (PAM) and found different results. Her study showed that, with a few exceptions, almost all the growth in various taxes stemmed from endogenous factors and was not due to the discretionary changes. Jeetun (1978) found direct and indirect taxes of Pakistan very inelastic over the period 1960-61 to 1975-76. Among indirect taxes, customs duties appeared to be more elastic, followed by import duties, excise duties and sales taxes respectively. The main reason for the low elasticity was found to be the low tax-to-base elasticities.

III. DATA SOURCES AND METHODOLOGY The methodology adopted for estimating the elasticity of major taxes of Pakistan in this study consists of the following steps:

1. To remove the effects of discretionary changes from the actual tax yields.

2. To specify and estimate an econometric model, which correlates the series of adjusted tax revenues to relevant tax bases.

Various techniques are available for removing the effects of discretionary changes though the most commonly used method is Chain Indexing Technique (1962). This method involves the adjustment of the tax yield series to subtract the revenue effect of the discretionary changes from the actual tax yield so as to represent the tax revenues that would have been obtained in each year if the rates applicable in the reference year had prevailed throughout the period.

IV. DATA

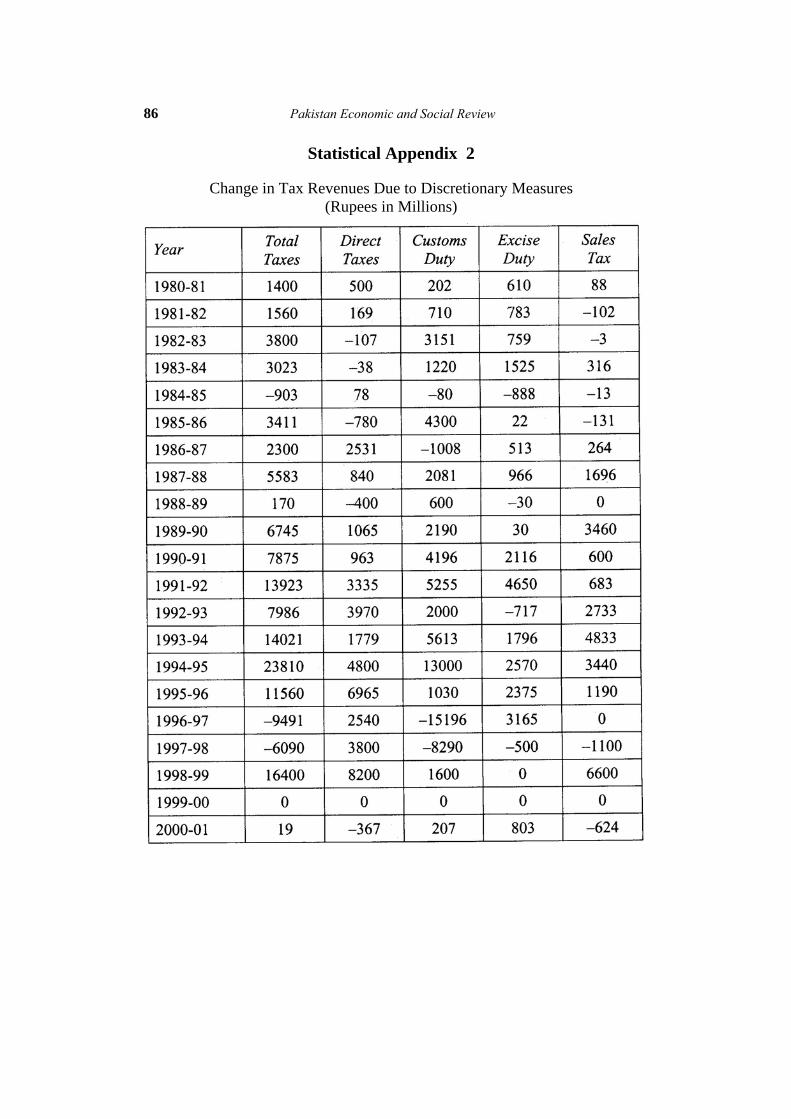

Impact of Discretionary Changes Precise data on the discretionary changes were available from budget documents only up to the fiscal years 1971-72 to 1982-83. Afterwards the reporting on such data had stopped which made it very difficult to get information about it. The estimates were made by going through the budget speeches and predicting the change in revenues due to the change in tax rates and their respective bases, and further, assuming a certain rate of growth in

78 Pakistan Economic and Social Review

tax bases. Since this method was arbitrary, there were no reliable estimates available. For this study, the discretionary changes were calculated by taking the difference between the budget estimates made at the beginning of current fiscal year (Yt1) and revised budget estimates made the next year (Yt+1), assuming that the discrepancy between the two has been due to the discretionary tax changes.

This methodology worked well, however, there were some problems of over projection3 and subsequent non-implementation of revenue targets which made the rate adjusted series underestimated. For instance, in 1992-93 the government announced the budgetary measures for excise duties of Rs. 7 billion. But the collection was actually less than base line by Rs. 0.7 billion. Similarly, in the year 1994-95, over projection in sales tax and excise duties was as much as Rs. 17 billion and Rs. 5 billion respectively. In 1996-97, the additional sales taxes were announced to the tune of Rs. 26 billion, whereas the actual collection was even less by Rs. 0.7 billion. In addition, during the year 1996-97 and 1997-98, the target for customs duties was over projected by Rs. 23 billion and Rs. 12 billion.

To handle such problems, the data were adjusted in such a way so as to reflect the actual collection because if left unadjusted the rate adjusted series would have become erratic and it would given inaccurate results. The adjustment was done by taking the difference between budget estimates and revised estimates to reflect the actual impact of budgetary measures for these years, even though it entailed both the impact of budgetary measures and implementation problems.

An unrealistic revenue targets questioned the authenticity of budget estimates and hampered the government’s credibility, hence from the year 1999-2000 onwards the revenue estimates made at the time of announcement of budget included the impact of budgetary measures without giving any explicit information. Since, there was no subsequent change in the budget estimates the revenue impact for the year 1999-2000, comes as zero and minimal for the year 2000-01.

The data cover the period 1980-81 through 2000-2001. The figures on budgeted and revised tax yields have been taken from various issues of Federal Budget in Brief. The information about other variables has been taken from Pakistan Economic Surveys.

3Over projection denote the difference between the revised budget estimate and revised

collection.

MUKARRAM: Elasticity and Buoyancy of Major Taxes in Pakistan 79

Tax Bases for Major Taxes As different taxes are levied to tap a certain stream of income, there is not same base for all the taxes. Respective bases for individual taxes are shown in Table 2.

TABLE 2

Bases for Major Taxes

Taxes Base

Direct taxes Non-agricultural GDP4

Customs duties Rupee value of dutiable imports, i.e. total imports excluding the import of food items and pharmaceuticals5

Excise duties Large scale value-added + selected services (Finance and Insurance + Transport and Communication)6

Sales tax3 Rupee value of dutiable imports + large scale manufacturing value added7

The Model The Ordinary Least Square method has been employed for regression of the equations. The variables have been taken in long form to compute the values in percentages. The equation for measuring the elasticity has been specified in the following form:

ln RTi = β0 + β1 ln TBi + εi

4Non-agricultural GDP has been taken as a base for direct tax since no tax is levied on

income earned from agriculture sector. 5As food items and pharmaceutical products are exempted from customs duty, total imports

net of these two items is taken as base for the customs duties. 6Excise duty is collected from large-scale manufacturing sector and specific services so they

are taken as the base for it. 7Sales tax is imposed on domestic production as well as imports so dutiable imports and

large-scale value added is taken as base for sales tax collection. The imposition of sales tax on electricity and gas distribution since the fiscal year 1999-2000 has changed the base for sales tax (by as much as 12%). But for the present analysis, the base has been kept the same as changing the base just for two years would have distorted the results.

80 Pakistan Economic and Social Review

MUKARRAM: Elasticity and Buoyancy of Major Taxes in Pakistan 81

TABLE 3

Elasticities and Buoyancy of Major Taxes (With Reference to GDP)

82 Pakistan Economic and Social Review

undergoing liberalization and structural adjustment drive. Export duties have been reduced gradually and were removed entirely in 1997-98. The tariff slabs have been revised over time and maximum tariff rate has been reduced to 30% in 1999-2001 whereas the number of tariff slabs has also been reduced to four. Decomposition of elasticity shows that tax to base and base to GDP elasticity is 0.34 and 0:98 respectively. The reason for low elasticity has been the low tax to base elasticity despite the almost unity base to GDP elasticity.

Excise Duties For excise duties the estimate of elasticity and buoyancy are 0.47 and 0.76 with respect to GDP, indicating thus, that the slow growth of excise tax revenues has due both to low automatic growth and reduction in the rates also. The share of excise duties in total tax collection has fallen from 30.23% in 1980-81 to 12.84% in 1999-2001. This represents a decline of 57.52% in its share. This reduction is a result of both the reduction in rates and replacement of excise duty on various items with sales tax to avoid the multiplicity of taxes. This trend is likely to be continued which is likely to bring the coefficient of elasticity further down. The break up of elasticity shows that base to GDP elasticity is greater than one, i.e. 1.04 whereas the tax to base elasticity is only 0.45.

Sales Tax The results of the present study show that the highest elastic taxes of Pakistan are the sales taxes with the elasticity of 1.0 representing 1.0% increase in GDP translates proportionately into sales tax revenues. The coefficient of buoyancy is 1.51, a slightly lower coefficient than for direct taxes. Sales taxes have been the most buoyant source of revenue. Their share in total taxes has gone up from 9.0% in 1980-81 to 38.33% in 1999-2001, signifying an absolute increase of 325.88%. Tax reforms, especially during the late nineties, have increased the collection from this source substantially. This includes the abolition of multiple taxes, introduction of general sales tax (GST) of value added tax (VAT) type system, and enhancements of tax rates. Decomposition of elasticity for sales tax shows that tax to base elasticity is 1.01 whereas base to GDP elasticity is 0.98.

Impact of Time Dummy Time dummy appeared significant in the elasticity and buoyancy equation of only the customs duties but Durbin-Watson statistics of these equations fell in the rejection region. However, the buoyancy of excise duties with respect to GDP and base the dummy for the years 1999-2000 and 2000-2001

MUKARRAM: Elasticity and Buoyancy of Major Taxes in Pakistan 83

combined appeared to be highly significant having the magnitudes of (–0.19) and (–0.20) respectively; the reason being the drastic reduction in the excise duty collection during these years.

VI. SUMMARY AND CONCLUSIONS This paper has examined the elasticity and buoyancy of major taxes of Pakistan by using the chain indexing technique for the period 1981-2001. The results given in Table 5 show that the elasticity and buoyancy is the highest for direct taxes followed by sales taxes. The coefficient of elasticity exceeds unity only for direct taxes and is almost unity for sales taxes. Customs duties and excise duties appear to be relatively rigid. Therefore, it is expected that the direct taxes and sales tax will be the pillar of the future resource mobilization strategy of Pakistan. As far as buoyancy is concerned, the results show that the buoyancy of all the taxes is higher than their corresponding elasticities and well above unity for direct taxes and sales taxes. This implies that budgetary changes have increased the responsiveness of tax revenues to income changes. Tax reforms, therefore, have improved the overall tax system. However, as the elasticity of individual taxes for most taxes has not exceeded one, constant interference with the tax rates will be necessitated to keep abreast with the ever-growing expenditure needs. The decomposition of elasticity shows that the tax to base and base to income elasticity has been approximately equal for direct taxes and sales taxes but for customs duties and excise duties the divergence between the two is significant. Due to this, the overall tax structure of Pakistan is inelastic despite the better performance of direct taxes and sales taxes.

84 Pakistan Economic and Social Review

REFERENCES

Akbar, Mohammad and Ahmed, Qazi Masood (1997), “Elasticity and buoyancy of revenues and expenditure of Federal Government”. Pakistan Economic and Social Review, Volume 35, No. 1 (Summer), pp. 43-56.

Gillani, Syeda Fizza (1986), “Elasticity and buoyancy of federal taxes in Pakistan”. The Pakistan Development Review, Volume XXV, No. 2 (Summer), pp. 163-174.

Jeetun, Azad (1978), Buoyancy and Elasticity of Taxes in Pakistan. Research Report No. 11 (May). Applied Economics Research Centre, University of Karachi, Karachi.

Jeetun, Azad (1978), Elasticity of Income Taxes in Pakistan: An Alternative Approach. Discussion Paper No. 27 (May). Applied Economics Research Centre, University of Karachi, Karachi.

Jeetun, Azad (1978), Elasticities and Buoyancies of Excise Duties and Import Duties: A Disaggregated Study. Discussion Paper No. 28 (August). Applied Economics Research Centre, University of Karachi, Karachi.

Sury, M. M. (1985), “Buoyancy and elasticity of union excise revenue in India: 1950-51 to 1980-81”. Margin, Volume 18, No. 1 (October), pp. 40-68.

Mansfield, Charles Y. (1972), “Elasticity and buoyancy of a tax system: A method applied to Paraguay”. International Monetary Fund Staff Papers, Volume 19, No. 2 (July), pp. 425-46.

Prest, Alan R. (1962), “The sensitivity of the yield of personal income tax in the United Kingdom”. The Economic Journal, Volume LXXII, No. 287 (September), pp. 576-596.

MUKARRAM: Elasticity and Buoyancy of Major Taxes in Pakistan 85

Statistical Appendix 1

The methodology for removing the effect of discretionary changes is derived as follows:

86 Pakistan Economic and Social Review

Statistical Appendix 2

Change in Tax Revenues Due to Discretionary Measures (Rupees in Millions)

Related Documents