Electronic copy available at: http://ssrn.com/abstract=1952199 How Important Is Capital Structure Policy to Firm Survival? Y. Peter Chung A. Gary Anderson Graduate School of Management University of California, Riverside [email protected] Hyun Seung Na College of Business City University of Hong Kong [email protected] Richard Smith* A. Gary Anderson Graduate School of Management University of California, Riverside [email protected] Current draft: February 20, 2013 Abstract If there is an economically important optimal capital structure, then firms that deviate too far from the optimum will face greater risk of failure or acquisition. Using data from the oil industry we find no significant evidence that capital structure policy affects acquisition or failure probability. Firms appear to increase leverage when they face attractive growth opportunities or when poor operating performance reduces equity value or compels borrowing. Firms are acquired when rapid growth has reduced financial slack. In a clinical examination, we address the question of how firms with persistently low leverage can operate and survive for many years without being targeted for acquisition. Our evidence supports the pecking‐order hypothesis including acquisition among potential financing sources. Keywords: Capital structure, Bankruptcy, Acquisition, Oil exploration and development JEL Codes: G32, G33, G34, L25, L71 * Corresponding author. We thank Warren Bailey, Harry DeAngelo, Jun‐Koo Kang, and David Mayers, for comments on prior drafts. Chung and Smith appreciate the financial support from the A. Gary Anderson Graduate School of Management for this research.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Electronic copy available at: http://ssrn.com/abstract=1952199

How Important Is Capital Structure Policy to Firm Survival?

Y. Peter Chung

A. Gary Anderson Graduate School of Management University of California, Riverside

Hyun Seung Na College of Business

City University of Hong Kong [email protected]

Richard Smith*

A. Gary Anderson Graduate School of Management University of California, Riverside

Current draft: February 20, 2013

Abstract

If there is an economically important optimal capital structure, then firms that deviate too far from the optimum will face greater risk of failure or acquisition. Using data from the oil industry we find no significant evidence that capital structure policy affects acquisition or failure probability. Firms appear to increase leverage when they face attractive growth opportunities or when poor operating performance reduces equity value or compels borrowing. Firms are acquired when rapid growth has reduced financial slack. In a clinical examination, we address the question of how firms with persistently low leverage can operate and survive for many years without being targeted for acquisition. Our evidence supports the pecking‐order hypothesis including acquisition among potential financing sources. Keywords: Capital structure, Bankruptcy, Acquisition, Oil exploration and development JEL Codes: G32, G33, G34, L25, L71

* Corresponding author. We thank Warren Bailey, Harry DeAngelo, Jun‐Koo Kang, and David Mayers, for comments on prior drafts. Chung and Smith appreciate the financial support from the A. Gary Anderson Graduate School of Management for this research.

Electronic copy available at: http://ssrn.com/abstract=1952199

How Important Is Capital Structure Policy to Firm Survival?

Current draft: February 20, 2013

Abstract If there is an economically important optimal capital structure, then firms that deviate too far from the optimum will face greater risk of failure or acquisition. Using data from the oil industry we find no significant evidence that capital structure policy affects acquisition or failure probability. Firms appear to increase leverage when they face attractive growth opportunities or when poor operating performance reduces equity value or compels borrowing. Firms are acquired when rapid growth has reduced financial slack. In a clinical examination, we address the question of how firms with persistently low leverage can operate and survive for many years without being targeted for acquisition. Our evidence supports the pecking‐order hypothesis including acquisition among potential financing sources. Keywords: Capital structure, Bankruptcy, Acquisition, Oil exploration and development JEL Codes: G32, G33, G34, L25, L71

How Important Is Capital Structure Policy to Firm Survival? 1. Introduction

The two predominant theories of corporate capital structure are the “optimal tradeoff” hypothesis

and the “pecking order” hypothesis. Under the tradeoff hypothesis, taxes, distress costs, and agency costs

combine to yield an optimal capital structure and firms are punished for deviating from that optimum

through lower risk‐adjusted returns, and potentially failure or acquisition. Under the pecking order

hypothesis, capital structure is a result of investment opportunities and capital retention policies in the

presence of asymmetric information. Firms confronted with new investment opportunities seek to

mitigate adverse selection costs by exploiting the least risky forms of financing first. Leverage increases

when investment opportunities are abundant and demand for investment capital is high. Leverage

decreases when free cash flow is high and investment opportunities are scarce. Under this hypothesis firms

are punished through the failure to maintain enough financial slack to take on investments without

incurring substantial adverse selection costs or by retaining more slack than is optimal.

The static version of the tradeoff hypothesis (Kraus and Litzenberger (1973), Jensen and Meckling

(1976), and Morellec (2004), among others) and the pure version of the pecking order hypothesis

(Donaldson (1961) and Myers and Majluf (1984)) are the simplest articulations of the competing theories.

Bridging these two are several hybrids. Fischer, Heinkel, and Zechner (1989) and others begin with the

tradeoff hypotheses and propose that empirical capital structure is dynamic. They recognize that

restructuring is subject to economies of scale so that firms can drift away from their targets. They return to

the targets, or even over‐shoot, using lumpy episodes of debt financing. From the other direction, Myers

(1984) introduces a modified pecking order, which provides that the firms face debt capacity limitations

and frictions associated with raising capital, and cannot strictly adhere to the pecking order predictions.

Synthesizing these two, DeAngelo and DeAngelo (2007) hypothesize, consistent with the tradeoff

hypothesis, that firms do have target capital structures, but that, consistent with the pecking‐order

hypothesis, they may depart from the targets by issuing debt to pursue attractive investment opportunities.

2

Moreover, the two main hypotheses are not mutually exclusive. Empirical capital structure could be

affected by considerations of both optimal tradeoff and adverse selection.

In this paper, we address the question of whether capital structure matters by examining what

happens to firms that operate with capital structures that are much different from industry norms and that

deviate materially from endogenous estimates of capital structure policy. Our empirical approach is most

directly a test of the optimal tradeoff hypothesis. If there is an economically important optimal capital

structure, firms with capital structures much different from industry norms and from endogenous estimates

of capital structure policy are most likely to be operating away from what is optimal and will be at

competitive disadvantage. Such firms are less likely to be able to sustain profitable operations and are

more likely to be attractive as acquisition targets by those who would seek to correct the capital structure.

Those that operate close to their optimums should be able to generate more net cash flow and be better

able to take on new investment opportunities, including by acquisition of firms that operate away from

their optimums or that fail because of having chosen an inappropriate capital structure.1 Accordingly, we

measure the effects of leverage on firm survival, acquisition, and failure. We also examine the effects of

leverage on (revenue) market share of firms, and we look specifically at a subsample of low‐leverage firms,

as they are the ones most likely to be acquired if the debt tax shelter is an important driver of firm value.

Our methodological framework reflects a return to basics. Alchian (1950) argues that the

deliberate pursuit of maximum profit (in our case, through choice of an optimal capital structure) is

unrealistic as a decision construct since the information necessary to ascertain the optimum is not

observable. Nonetheless, he reasons that even if managerial choices are random, the environment in

which firms compete will identify choices that have survival value. Stigler (1958) uses this reasoning to test

for the presence of scale economies in the steel, automobile, and oil refining industries. The underlying

1 Campello (2003) studies the relation between capital structure and operating performance. She finds that during recessions debt financing has a negative impact on firm sales growth in industries in which rivals are relatively unlevered. There is no similar effect during booms or in high debt industries. Campello (2006) finds a non‐monotonic relation between debt financing and competitive conduct. Moderate debt is associated with sales gains but high debt leads to product market underperformance.

3

logic of Stigler’s “survivorship” approach is that good strategies, in the context of a competitive market,

should survive and grow while others should diminish.2

We apply this approach to the U.S. oil industry: focusing specifically on crude oil exploration and

development. We selected the oil industry for three main reasons: First, there are enough participants to

make large‐scale empirical analysis feasible, but at the same time, the single‐industry focus enables us to

examine several companies on a micro level. Second, because the end product is a commodity, firms

compete mainly on cost and, except for differences in profitability and growth opportunities, the tradeoff

and pecking order hypotheses imply similarity of capital structure across firms. Third, it is the same

industry that was studied by Modigliani and Miller (1958) in their original study of capital structure

irrelevance.3 The narrow focus on oil exploration firms yields a large sample but still enables us to fully

investigate each of the firms in the sample for appropriate inclusion, to use a narrower classification than a

2‐, 3‐, or 4‐digit industry code, and to conduct a limited clinical analysis on firms with extreme capital

structures.

We use four approaches to test the optimal tradeoff hypothesis against the alternative pecking

order hypothesis. First, we use single‐stage probit and multinomial probit models to test whether firm

survival, acquisition, and failure probabilities are affected by capital structure. The single‐stage models

enable us to examine non‐monotonic relations between capital structure and these outcome variables but

are subject to challenge because they do not formally control for the endogeneity of observed leverage

ratios. Second, to confirm the single‐stage results, and to allow for cross‐sectional variation in optimal

capital structure, we endogenize capital structure in a two‐stage model. However, because of data

limitations, we are unable to investigate non‐monotonic relationships in this model. Third, we test for the

presence of a static or dynamic optimal capital structure by aggregating firms into leverage‐based deciles

2 It is the strategies that gain share, and not necessarily the individual firms. Stigler (1958) aggregates by size, and looks at aggregated share changes in size groupings. 3 Modigliani and Miller (1958) also study electric utilities. However, as Myers (1984) notes, regulated firms are normally able to pass through inefficiencies related to capital structure, and thus are not well suited for tests of the tradeoff hypothesis.

4

and testing whether aggregated market share changes are related to factors that could affect optimal

capital structure under the tradeoff hypothesis. Fourth, we undertake a brief clinical study of firms with

persistent low leverage to gain a better understanding of how low leverage can persist over many years.

Leverage measures vary across studies. At one extreme, Lemmon, Roberts, and Zender (2008),

DeAngelo and DeAngelo (2007), and others define leverage in a way that emphasizes the potential tax

advantage of debt financing. They measure leverage as the ratio of interest‐bearing debt to total assets.

Implicitly, spontaneous financing and non‐interest‐bearing liabilities are interpreted to reduce leverage. At

the other extreme, Baker and Wurgler (2002) and others define leverage in a way that emphasizes

information asymmetry. They include preferred equity in leverage and exclude convertible debt.4 Other

studies use intermediate measures. Fama and French (2005), for example, define leverage as total

liabilities to total assets. Welch (2011) also argues for this measure, noting that it has the advantage to

treating both financial and nonfinancial liabilities as prior claims to equity. In this study, we report results

for the two extreme measures, which, for convenience, we refer to as the LRZ and BW measures. We also

assess whether total liabilities to total assets (which we refer to as the W measure) produces materially

different results. The W measure results are discussed but not reported except in descriptive statistics

tables. Generally, the results are consistent, but somewhat stronger for the BW measure than for the LRZ

measure. The W measure results are similar to those for BW.

Using the BW leverage measure in the probit analysis, firms with high book or market leverage in

one year are significantly more likely than others to be delisted from Compustat in the next. Delisting can

be due to either acquisition or failure, both of which probabilities are significantly higher for firms with high

leverage in the prior year. The relationships to delisting and failure are nonlinear, with failure probability

increasing disproportionately with leverage. The relationship to acquisition probability is nonmonotonic, as

we also find that firms with extreme low leverage are significantly more likely to be acquired in the

subsequent year. Using the LRZ measure, the signs of these relationships are the same, but only the

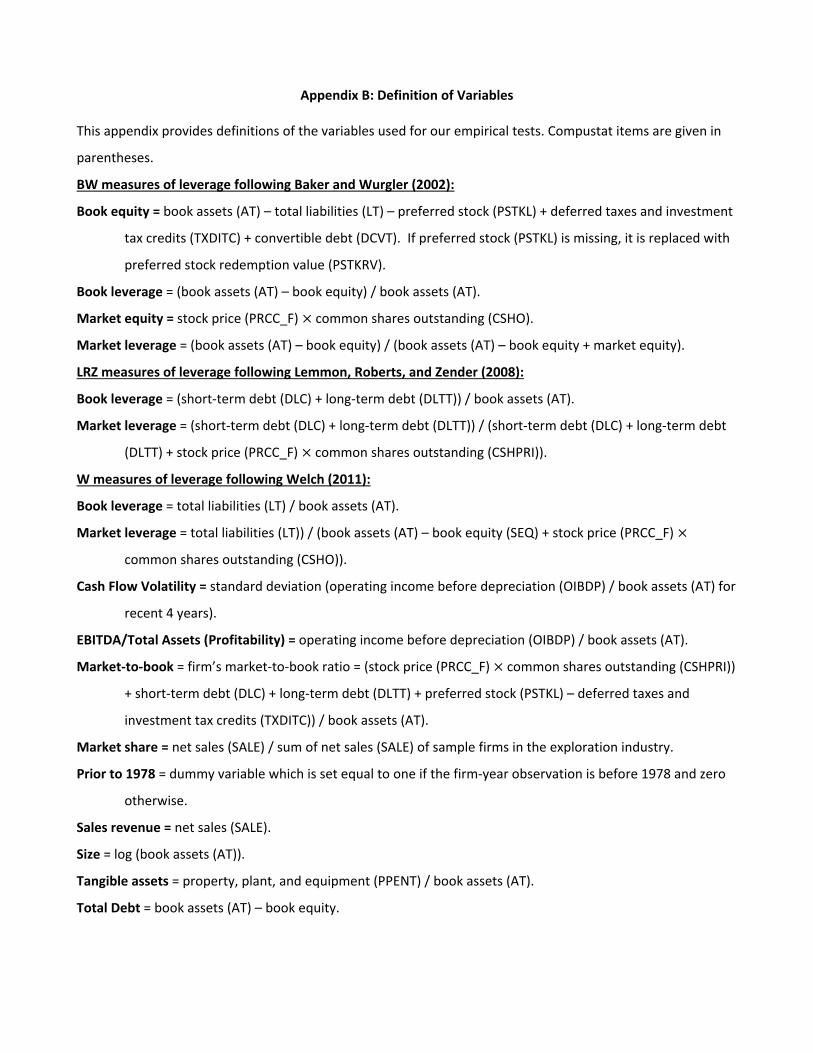

4 Appendix B provides formal definitions of the leverage measures.

5

delisting and failure probabilities are significantly related to leverage in the prior year. The difference in

findings makes sense because the LRZ measure is a less comprehensive indicator of depletion of financial

slack but a potentially better measure of exposure to default risk.

While these results seem to support optimal tradeoff, leverage in the year before delisting is not a

reliable measure of capital structure policy. We find that leverage ratios increase materially in the years

just prior to delisting. Using leverage from three years prior as an indicator of capital structure policy, and

controlling for leverage in the year before delisting, we find no significant support for the optimal tradeoff

hypothesis. Rather, the evidence shows that leverage increases when firms are in trouble for more

fundamental reasons or when the firm is growing rapidly, a result more consistent with the pecking order

hypothesis.

In the two‐stage results with endogenous capital structure that use corporate tax rates, oil prices,

and/or lags of firm characteristics as instruments, we confirm the above finding, in that we find that capital

structure policy is not significantly related to survival probability. 5 This conclusion holds regardless of

which measure is used and whether leverage is expressed as book value or market value.

We also find that neither contemporaneous nor lagged leverage measures are significant in

explaining changes in revenue shares of leverage deciles over time. In the clinical portion of our analysis,

we find that firms can operate for many years with low leverage, high profitability, and a high effective tax

rate, suggesting that any disadvantages of very high leverage are not sufficient to trigger control events.

Thus, the firm’s tax‐based capital structure policy does not appear to be of much importance to

survival. Firms with attractive growth options and those that need cash to fund their continuing

5 Similarly, Wintoki, Linck, and Netter (2012) examine causal relation between board structure and firm performance and find no significant effect of board structure, a result inconsistent with earlier findings that do not take account of endogeneity. They apply a dynamic panel generalized method of moments (GMM) estimator that relies on internal instruments such as lagged variables that allows a dynamic relationship between performance and corporate governance. Our approach, which also relies on lagged variables, is somewhat different because our dependent variable is binary.

6

unprofitable operations turn to debt financing with little apparent regard to tax considerations.6 Those

with attractive growth opportunities may turn to acquisition as internal financial slack is depleted. Overall,

our capital structure policy results are consistent with the irrelevance arguments of Miller (1977) and

DeAngelo and Masulis (1980), and with the pecking order hypothesis of Myers (1984). The results suggest

that capital structure policy does not significantly matter to the survival of the firms in the oil industry.

The balance of the paper is organized as follows. Section 2 discusses the prior empirical evidence

on capital structure, while Section 3 develops our testable hypotheses based on the Stigler (1958)

survivorship approach. Section 4 describes the data and Section 5 presents the empirical analysis and

results. Section 6 concludes.

2. Prior Evidence on Capital Structure

For the most part, empirical researchers have sought to test the competing capital structure

hypotheses by observing what managers do. Do they appear to select capital structure in a manner more

consistent with optimal tradeoff or with pecking order? Despite decades of empirical research, there is

little agreement as to what the evidence means. Fama and French (2002) observe that many of the

predictions of the two theories agree and that evidence is generally consistent with the shared predictions

so that the results are not dispositive.

Leary and Roberts (2010) point to conflicting interpretations of the evidence. They note that

Shyam‐Sunder and Myers (1999) claim to find that financing patterns are consistent with pecking order but

that Frank and Goyal (2003) claim the opposite.7 Leary and Roberts also note that while Lemmon and

Zender (2008) conclude that their evidence supports the modified pecking order interpretation, Fama and

French (2005) find that pecking order cannot explain persistent low‐leverage policies.

6Under the tradeoff hypothesis, firms with positive income tax liabilities in a given year might be expected to rely more on convertible debt financing and other firms might be expected to rely more on preferred stock. In 40% of the firm years, observations in our sample relied on convertible debt, preferred stock, or both. We found no systematic relation between the choice of financing and the firm’s tax liability. In fact, financing choices that were inconsistent with the tradeoff hypothesis were somewhat more likely than those that were consistent with it. 7 These studies all use leverage measures similar to the LRZ measure.

7

There are, moreover, important regularities that do not appear to fit either theory. Minton

and Wruck (2002), for example, using the LRZ measure, find persistent “underleverage” relative to

the tradeoff hypothesis. However, Shivdasani and Stefanescu (2010) report that once pensions

are considered, firms are less conservative in their choices of leverage than previously thought,

and that they incorporate the magnitudes of pension liabilities in their capital structure decisions.

Among the Minton and Wruck findings are that low‐leverage firms have high market‐to‐book

value ratios, that the phenomenon is not specific to particular industries, and that the firms do not have

low tax rates, high non‐debt tax shelters, or severe information asymmetries. The evidence of low‐leverage

and no‐leverage firms seems to be particularly inconsistent with the tradeoff hypothesis. However, the

evidence that firms sometimes choose equity issues even when equity is not the last resort has led Fama

and French (2005) to conclude that pecking order, as a stand‐alone hypothesis, is dead.

Baker and Wurgler (2002) and Korajczyk and Levy (2003) find that firms issue equity when market

values are high.8 Attempted market timing affects capital structure because, Baker and Wurgler find, low

leverage firms are those that raised funds when their market valuations were high, while high leverage

firms are those that raised funds when their market valuations were low. Capital structure, then, is the

cumulative outcome of past attempts to time the market. In their view, attempted market timing is an

additional consideration in the real capital structure choices of firms.9

Of course, the validity of basing inferences about the economics of capital structure choice on

observation of managerial decisions is only valid if the choices actually matter. Adopting the terminology of

evolutionary biology, Miller (1977) refers to neutral mutation as adaptive or imitative behavior that serves

no useful purpose, but also does no harm. If managers believe there is an optimal capital structure, when,

in fact, there is none, their choices will appear to support optimal tradeoff. If they believe significant

adverse selection costs are associated with raising riskier forms of capital, their choices will appear to

8 The measure used by Korajczyk and Levy is similar to the LRZ measure. 9 Related to this, Welch (2004) finds that firms do not repurchase debt and equity to counteract mechanistic effects of stock market performance on market‐value capital structure.

8

support pecking order. And, if managers think they can time the market, the evidence will support

attempted market timing. The upshot is that while managerial choices can tell us what managers believe,

they cannot necessarily tell us what is true about the relationship between capital structure and value.

Only if capital structure really does matter can we make the logical leap from managerial choice to

hypothesis validity. If, in reality, there is no material cost of operating with a capital structure that is well

away from the “optimum”, then the choices simply reflect neutral mutation/imitation. The same is true if

managers incorrectly believe that adverse selection costs are material, or that they can time the market.

Several stylized facts support the notion of neutral mutation and capital structure irrelevance. For

example, leverage ratios vary cross‐sectionally but are quite stable over time. Lemmon, Roberts, and

Zender (2008) find that leverage ratios are characterized by both a transitory and a permanent component.

They find, further, that known determinants of capital structure do a poor job of explaining heterogeneity

in leverage ratios. They also find that leverage ratios converge over time, moving toward more moderate

levels but are quite stable over long periods. Therefore, they argue, any explanation of capital structure

must be reconciled with the converging, but long‐lived stability of leverage ratios. Persistence of extreme

leverage ratios is an aspect of our empirical analysis.

Graham and Leary (2011) review the literature and evidence on capital structure and question

whether capital structure effects are either (i) important but not detected in empirical studies or (ii) the

evidence is consistent with neutral mutation except in extreme cases. They find that most of the variation

in observed capital structures is within‐industry variation, as opposed to within‐firm over time or across

industries. However, they also find that standard variables used to explain observed capital structures have

little ability to explain within‐industry variation. They also observe that the value effects of capital structure

choices appear to be modest over a broad range. Our evidence is consistent in supporting neutral mutation

and the pecking order hypothesis.

3. Testable Hypotheses

9

No previous study, to our knowledge, has focused on the relationship between capital structure

choice and survival probability. If there is an economically important optimal capital structure, we presume

there is some commonality within an industry in terms of the important factors that influence the optimum.

Indeed, Frank and Goyal (2008) find that industry is one of the most reliable factors explaining the capital

structure choices and that industry subsumes a number of factors that are of lesser importance. On the

other hand, Minton and Wruck (2002) find that financial conservatism is not an industry‐based

phenomenon, so that capital structure extremes can exist within industries and Graham and Leary (2011)

observe that within‐industry variance of capital structure is high and hard to explain empirically.

In a spirit somewhat similar to our approach, Korteweg (2010) estimates the benefits of leverage by

assuming that asset betas are common within an industry. Leary and Roberts (2010) find that industry and

year fixed effects alone do a good job of explaining leverage choices. Lemmon, Roberts, and Zender (2008),

however, find that controlling for standard factors including industry leaves most of the variation in capital

structure unexplained and driven by unobservable effects that are time‐invariant.

We control for industry effects through sample construction and for other standard factors by

inclusion of control variables. It is not necessary that we fully account for the factors that determine

optimal capital structure. Rather, in one of our approaches, we rely on the Bayesian reasoning that, if an

economically important optimum exists, then firms with very low leverage relative to the average are more

likely to be under‐levered than over‐levered, and the converse for firms with very high leverage. In a

second approach, we endogenize capital structure policy and test whether the policy is significantly related

to survival probability. In the first approach, if the tradeoff theory is correct, we should find that firms

with extreme capital structures are (i) more likely to become targets or to fail and/or (ii) more likely to be

insulated from the control market and product market competition in various ways, and (iii) have a

tendency to regress toward the mean. If capital structure is irrelevant, we should find that capital structure

policy is not significantly related to survival probability. Regression toward the mean could occur even if

capital structure does not matter, if there are important frictions to raising capital or if managers believe,

10

incorrectly, that capital structure is important. In the second approach, if the tradeoff theory is incorrect

we should find little relation between endogenized capital structure and survival probability.

One might think that if capital structure is important we should find little within‐industry variation.

Yet, we do not see such evidence in the existing literature. Possible explanations are that capital structure

is not very important, that even within an industry there are substantial differences in what would be

optimal, or that firms with suboptimal capital structures are insulated from competition. To address this,

our panel data study includes some clinical study details as overlay.

4. Data and Summary Statistics

4.1 Data

In their original 1958 paper, Modigliani and Miller support their irrelevance proposition with

evidence from two industries, including oil companies. They present evidence that the after tax rate of

return is invariant to leverage. We follow their example, by also focusing on oil companies. The industry

has the advantage of including a large number of companies with publicly available data. Because the

industry includes an array of activities, we limit the study to crude oil exploration and development

(exploration firms).

To identify firms for inclusion in the sample, we first identify all Compustat firms classified in the oil

industry on the basis of current or historical SIC codes, current or historical NAICS codes, S&P Global

Industry codes, or the former S&P industry codes. Appendix A lists the codes we use to construct the initial

sample. A firm is tentatively included if, in any year from 1950 through 2007, it is classified into any of the

codes listed in the appendix. From this sample, we exclude all non‐US firms.

The industry codes sometimes identify firms that are not appropriately classified as being in the oil

industry. These include, for example, pipeline firms, chemical firms, ethanol producers, and firms involved

primarily in minerals mining. By inspection, we exclude these firms. We also exclude oil royalty trusts that

are included in the Compustat database. From the remaining sample, we exclude enterprises for which no

11

stock price information is available, such as divisions of public companies. Because some of the

observations are for small firms for which details of financial information often are not available, we

impose the screen that for inclusion in the final sample a firm must have at least $25 million (in real year‐

2000 dollars) of total assets in the year of its first market price observation.

Next, we use the business descriptions from Compustat, Factiva, and Internet searches to verify the

scope of activity of each firm. Based on these searches, we classify firms as either exploration firms or

refiners. When we cannot verify the activity of the firm, we drop it from the sample.

Because of concerns about survivorship bias in the early Compustat data, we further limit the

sample to firm‐years from 1970 on.10 Finally, we drop refiners because of the small sample size of that

group, their fundamental difference from exploration firms, the limited variation in their capital structures,

and the near absence (one observation) of “failures”.11 Thus, the final sample includes 218 exploration

firms comprising 2015 firm‐years.

4.2. Summary Statistics

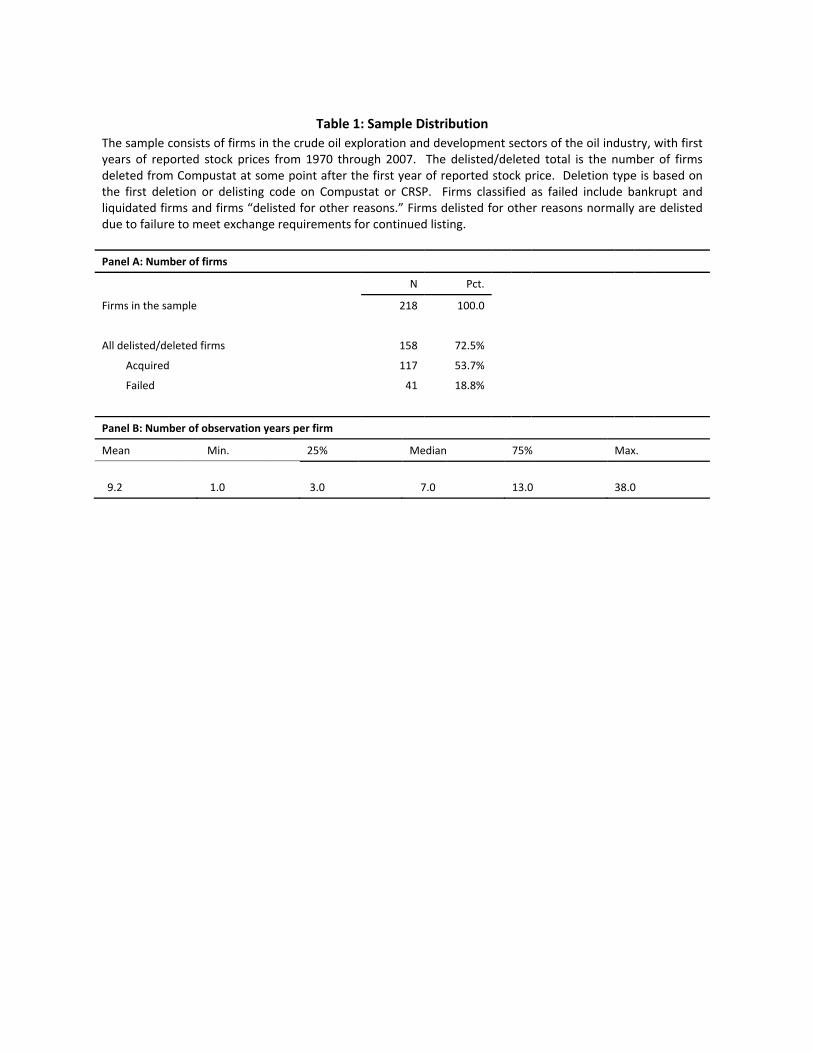

An observation in our panel is a firm‐year. Table 1 provides descriptive statistics on sample firms.

Exploration firms have an average of 9.2 yearly observations. Of these firms, well over half are acquired or

fail during our sample period; 53.7% (117 firms) are acquired and 18.8% (41 firms) fail via bankruptcy,

liquidation, or other delisting from Compustat. Normally, firms are delisted when they no longer meet the

requirements for continued exchange listing and may eventually fail. While acquisition is more likely than

failure, a number of the acquisitions occur in the face of what appears to be imminent failure. In such

cases, we rely on the Compustat and CRSP deletion codes and where they are different we review Factiva

to determine the classification.

10 Kothari et al. (1995) discuss the potential survival bias issue in early year data of Compustat. 11 For some firms there was inconsistency in identity changes between CRSP and Compustat. We searched for information on these cases using Factiva and determined whether there had been a fundamental change in identity such as acquisition by another firm.

12

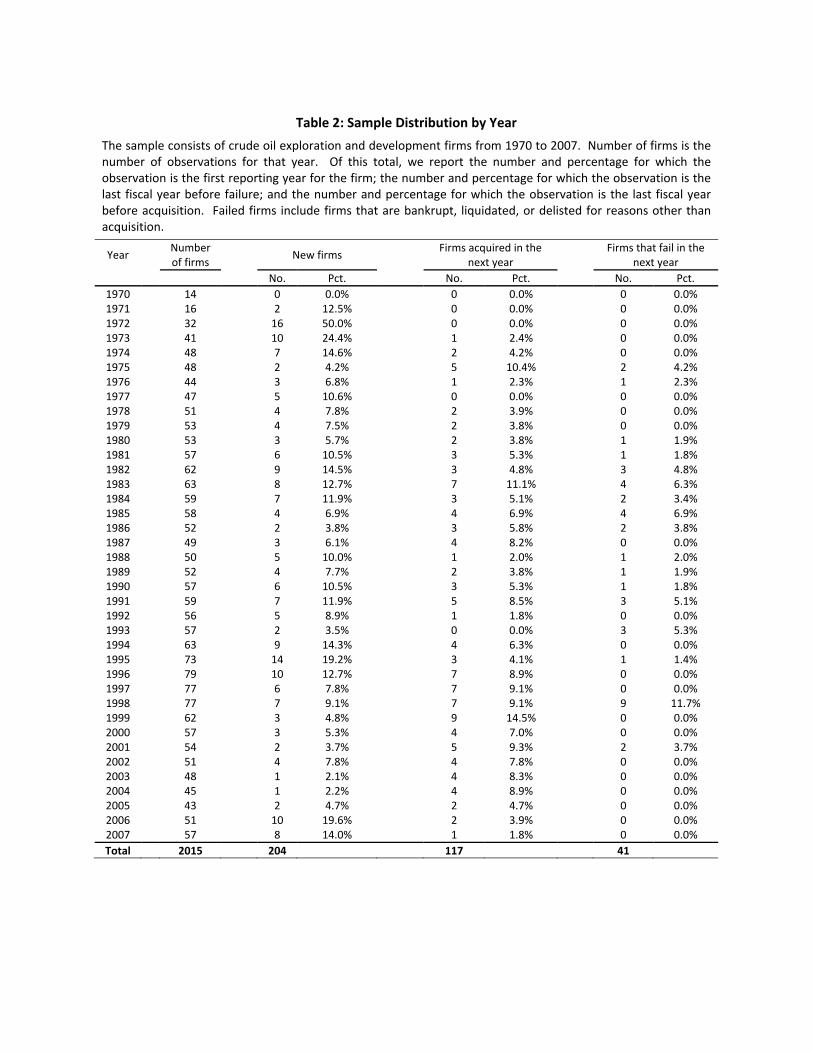

Table 2 shows the time‐series distribution of firm‐year observations. The number of exploration

firms rose sharply during the period around the first OPEC oil shock, and then the industry experienced a

wave of failures and consolidation during the 1980s. The table shows increasing numbers of firms through

the mid‐1990s, followed again by consolidation and attrition.

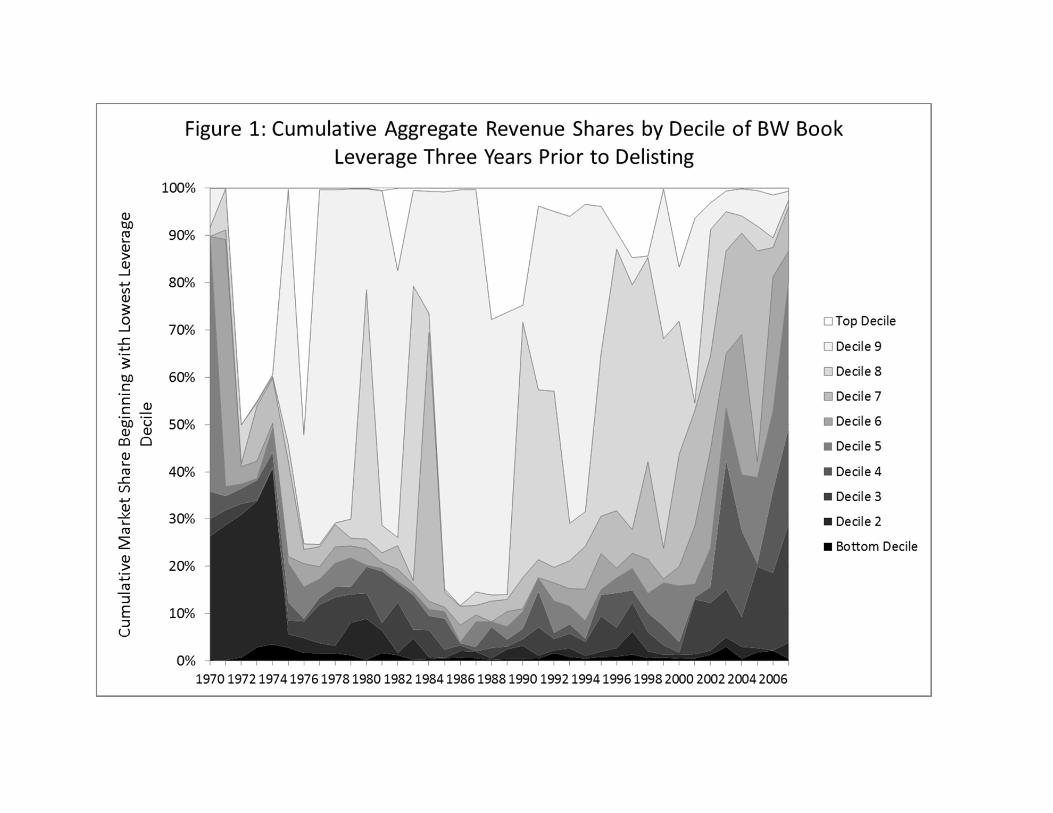

Figure 1 is a time‐series plot of market shares, aggregated into deciles based on BW book‐leverage

ratios with constant decile breakpoints determined over all observations. Because we find that book

leverage increases endogenously prior to delisting, the figure is based on book leverage measured three

years before the market share observation year.12 A decile can gain share if firms within the decile gain

share or if firms with high shares move into the decile and those with low shares move out. Patterns of

dynamically shifting market shares by decile are similar to those shown in Figure 1 if (i) decile breakpoints

are allowed to vary annually, (ii) leverage is measured in the same year as market share, or (iii) the LRZ

measure is used instead.

It is noteworthy that firms in the bottom leverage decile consistently account for a small fraction of

the total market and that in most years the highest‐levered firm in this decile has a leverage ratio of less

than 18.0%. From Figure 1, systematic shifting of market shares among deciles is apparent over time.

Firms in the bottom five deciles account for almost half of the total market during the first four years, up to

the point of the first OPEC oil price shock13. Following that, for most of the next three decades, firms in the

top few leverage deciles account for roughly 80% of the market. In later years, firms with low leverage

account for an increasingly large share of the market. Given these shifts, one might infer that managers of

larger firms act as if there is an optimal capital structure that varies over time. Alternatively, consistent

with the pecking‐order hypothesis, aggregate capital structure changes may be driven by changes in the

12 All accounting variables used in the analysis are defined in Appendix B. 13 The corresponding LRZ‐based figure shows low‐leverage firms with a small market share, except in the first few years (when the sample size is small); the highest levered firm in the low leverage decile having a LRZ book leverage ratio of 2.3%; and firms in the bottom five leverage deciles accounting for about 40% of the market during the first five years, before declining to a much lower percentage.

13

value of investment opportunities and net cash flow. It remains to be seen whether capital structure

choices are significantly related to survival probability.

5. Empirical Results and Discussions

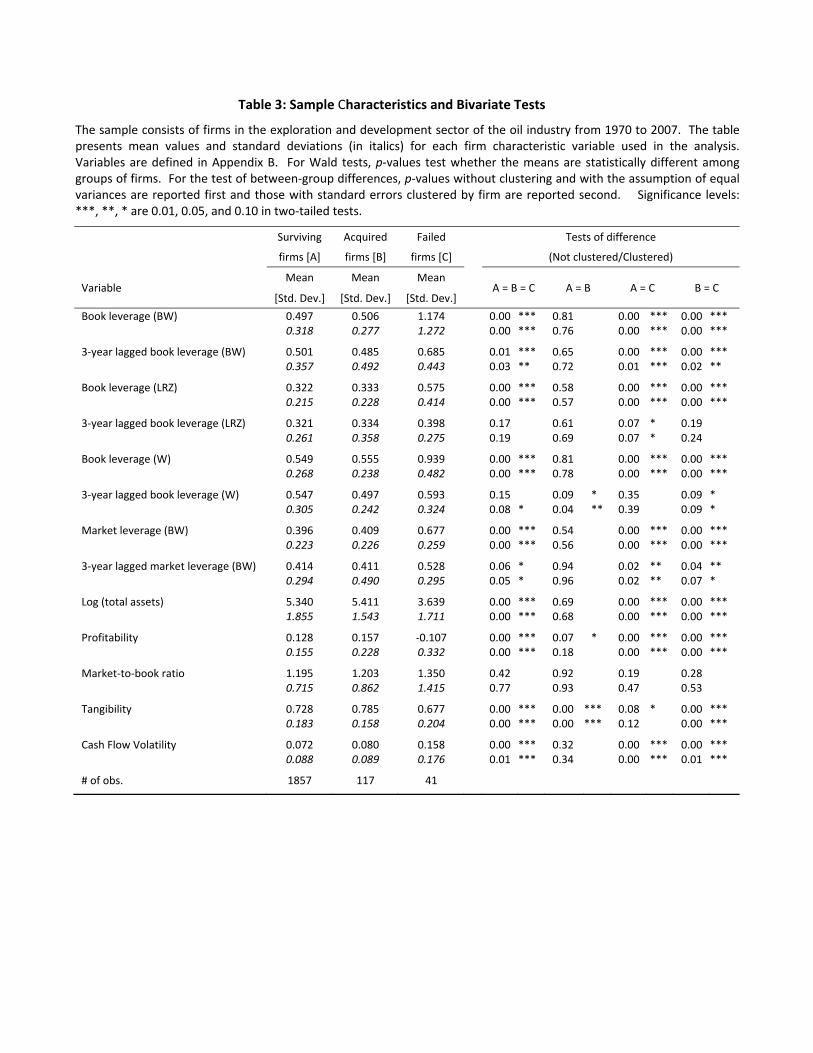

5.1. Bivariate Tests of Differences

We hypothesize that, if there is an important optimal capital structure we should find that firms

located close to the optimum flourish while others subsist, fail, or are acquired. In Table 3, we report

summary statistics and difference test results for sample exploration firms. The table compares leverage

ratios and other firm characteristics among groups that survived (group A), were acquired (group B), and

failed (group C). In the table, we test whether firm‐year observations in the year prior to acquisition or

failure have different capital structures than firm‐years associated with survival. We also test whether

acquisition or failure is related to firm size, profitability, market‐to‐book, tangibility of assets, or cash flow

volatility. The p‐values in the table are reported first based on the standard errors for all observations, and

second with clustering by firm. Clustered tests generally have similar significance levels to those without

clustering, indicating that within‐firm variance is similar to overall variance.

There are important differences among the groups, particularly between failed firms and the rest of

the sample. Acquired and surviving firms are similar in most respects. Observation‐year leverage ratios are

not statistically different between surviving and acquired firms, regardless of the leverage measure and

three‐year lagged leverage ratios are significantly different only for the W measure. However, observation

year and lagged leverage ratios of failed firms are significantly higher than those of either surviving or

acquired firms, except for the lagged difference between the failed and the acquired by the LRZ measure

and the lagged difference between the failed and the surviving by the W measure. There is also little

difference between observation‐year leverage and three‐year lagged leverage ratios of surviving firms or of

acquired firms, whereas, by any measure, the three‐year increase in leverage is considerable for failed firms.

In addition, failed firms are significantly smaller than surviving or acquired firms and are significantly less

14

profitable. We find that acquired firms have significantly more tangible assets than failed firms. Finally,

cash flows are much more volatile during the preceding four years for failed than for surviving or acquired

firms. There is no significant difference in cash flow volatility between surviving and acquired firms.

Overall, Table 3 suggests that leverage and other firm characteristics are significantly different

between failed firms and surviving or acquired firms in the oil industry and that acquired firms are similar to

survivors in many respects. Also, while the optimal trade‐off hypothesis suggests that leverage that is

either too high or too low could increase the probability of failure or acquisition, the statistics in the table

suggest that the main empirical survivorship effect is more likely to be associated with contemporaneous

leverage ratios that are too high.

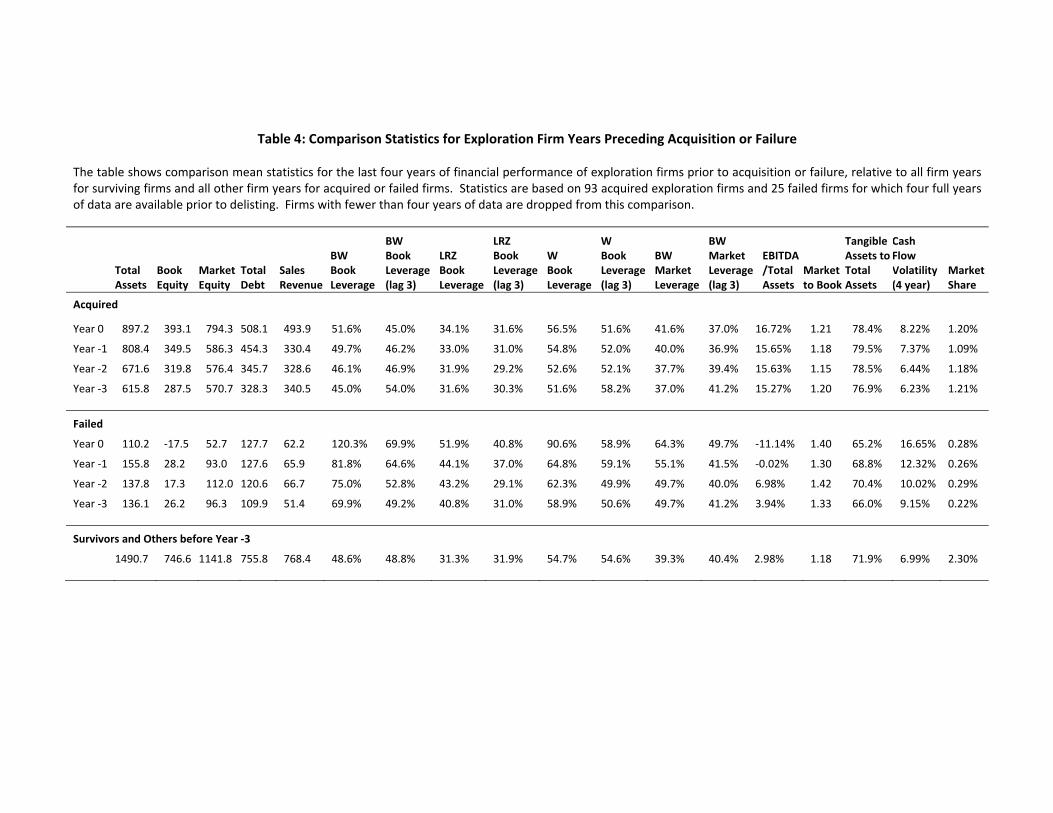

5.2. Comparison Statistics of Exploration Firms before Delisting

There are indications in Table 3 that, by any measure, leverage increases endogenously as a firm

approaches failure. Therefore, we need to distinguish between a firm’s capital structure policy and

leverage increases that are symptomatic of fundamental changes in firm performance. In the single‐stage

multivariate analysis, we include both leverage in the observation year (year 0) and the leverage measured

three years prior (year –3). From Table3, there is evidence that, even three years prior, leverage ratios of

failed firms are significantly higher than those of surviving firms, particularly for the BW and W leverage

measures. Thus, inclusion of a 3‐year lag may not be an entirely satisfactory way to assess the effect of

leverage policy for failed firms. To investigate further, in Table 4 we provide comparison statistics for

acquired and failed firms in the last year before delisting (year 0) and the three prior years, as well as

comparison statistics for all other firm years in the database (all survivor years and years before year ‐3 for

acquired and failed firms). Table 4 statistics are different from those in Table 3 because Table 4 is based on

only observations where at least four years of data are available, so that year to year differences are from a

consistent sample.

We find that acquired firms are smaller than the overall average, but are growing rapidly (at a

compound annual rate of 13.3%). Book leverage, by any measure, is increasing in this group because rapid

15

growth in the years before acquisition is financed disproportionately with debt. Market and book equity

are in approximately constant proportions to each other for acquired firms, so that the market‐to‐book

ratio is stable, and market leverage is increasing similarly to book leverage.

While sales revenue of failing firms is growing over the years before failure (at a compound annual

rate of 6.8%), operating cash flow (EBITDA/Total Assets) is declining, and is negative on average in the last

two years before they fail. Book equity also is declining and is negative on average in the year before

failure; in fact, 36% of the failing firms report negative book equity. In summary, the leverage increases of

failing firms are associated with poor operating performance. Leverage ratios are increasing because equity

is declining, and firms are covering operating needs by borrowing. These firms appear to be on a course to

failure.

For the question of whether lagged leverage ratios are reasonable indicators of capital structure

policy, Table 4 shows that both book and market leverage averages of failed exploration firms in year ‐3 are

still above the averages of other firm‐year observations. For example, BW book leverage of failed firms

averages 120.3% in the year before failure (i.e., in year 0), and 69.9% in year ‐3, whereas the average of

survivor observations is 48.6%. The similar trend in the 3‐year lag of book leverage suggests that 69.9% in

year ‐3 is above the capital structure policy choice of firms that fail within four years. In the failed firm

sample, the 3‐year lag of BW book leverage increases substantially, to 69.9% from 49.2% in year ‐3, which is

close to the average value of surviving firms.

We infer that the 3‐year lag values of leverage are also affected by the underlying phenomena that

drive these firms toward failure. Because lagging for more than three years would result in losing many

observations, we do not pursue this approach to assessing the effect of capital structure policy.

5.3. Leverage Effects on Firm Survival Probability

5.3.1. Monotonic probit analysis

Given the differences in means from Table 3, we first entertain the hypothesis that there is an

empirical monotonic relationship between capital structure and the probability of delisting, acquisition, or

16

failure. To investigate the effects of leverage on survival probability, we use probit models of firm‐year

observations in a panel, where the dependent variable is set to zero if the firm survives the next year and

one if it is delisted due to either acquisition or failure. To help distinguish between capital structure policy

and leverage increases that are symptomatic of more fundamental changes, we include both leverage in

the observation year and leverage measured three years prior.14

Because the distribution of leverage ratios is skewed and we are interested in both high and low

leverage extremes, we use the natural log of the ratio in the multivariate analysis. In the sample, 1.2%

(4.1%) of the observations have BW book leverage ratios less than 5% (10%) and 4.5% have ratios greater

than 100% (negative book equity). For the LRZ measure, which is almost always lower than the BW

measure, 10.3% have book leverage ratios below 5% and 9.8% have leverage ratios above 60%. The

percentages are similar for leverage ratios measured in year‐3.

In Table 5 probit models, we classify firm‐year observations as delisted after the observation year

or survived. We regress the binary outcome variables on the log of the firm’s book or market leverage ratio

in the observation year and the leverage ratio three years prior. The models include standard controls in

capital structure estimation in the literature: firm size (natural log of total assets), profitability (operating

income before depreciation/book total assets), market‐to‐book assets ratio, tangibility of firm’s assets, and

cash flow volatility over four years ending with the observation year.15 We also include an indicator

variable that is equal to one if the observation is from before 1978 because of the potential for survival

probabilities before then to be affected by look‐back bias in Compustat data.16 Estimates in Panel (a) are

based on BW book leverage; those in Panel (b) are based on LRZ book leverage, and those in Panel (c) are

14 We also estimated a hazard model relating failure to capital structure in earlier years. Because we find no significant relationships of failure probability to prior capital structures, and because many firms are only in our sample for a few years, results are similar to the probit results. Accordingly, we do not report results for the hazard model. 15 To the extent that these controls explain variations in capital structure in our sample, the partial effects of capital structure coefficients will reflect deviations from the optimum. However, regression models of capital structure on these controls have low explanatory power, as in earlier cited studies. 16 Shanken, Kothari, and Sloan (1995) document the potential for look‐back bias to affect Compustat data prior to 1978.

17

based on BW market leverage.17 All panels include the results of alternative specifications where we

replace the lagged leverage variable with the three‐year change in leverage and where we replace both

variables with the three‐year change and the lagged leverage variable. Coefficients on other variables are

identical to those reported and are suppressed in the table. The results in Table 5 enable us to assess the

adequacy of using the 3‐year lag to control for capital structure policy, and to contrast results for BW and

LRZ book leverage and for market leverage. Marginal effects are reported in the table to aid

interpretation.18 Standard errors are clustered by firm.19

In Panel (a), delisting (non‐survival) is positively and significantly related to BW book leverage in

year 0. The relationship to lagged leverage is marginally significant but negatively signed. In Panel (b), the

LRZ leverage measures have the same signs as those in Panel (a), but are not statistically significant. In

Panel (c), the market leverage measures using the BW definition yield results similar to those in Panel (a).

When we replace lagged leverage with the 3‐year change in any panel, the sign reverses, and the non‐

lagged coefficient is weaker. When we replace leverage in the observation year with the 3‐year lagged

value, both the level and change are positively signed and the BW measures are significant.

The BW delisting results support the endogeneity argument. Oil exploration firms are more likely

to be delisted when they are highly levered and when high leverage is a recent phenomenon. The LRZ

results indicate no significant relationship between capital structure and delisting, suggesting no

economically important relationship between leverage and firm survival. All delisting results are

inconsistent with the hypothesis that a policy of high leverage is positively related to delisting probability.

Rather, the evidence indicates that leverage ratios increase endogenously prior to delisting. The

differences between our BW and LRZ results indicate that the findings in some other studies may be

sensitive to how leverage is measured. We also find that delisting is more likely for smaller firms and those

with higher ratios of tangible to total assets.

17 The probit and multinomial probit results using the W measure are similar to the BW results in Panel (a). 18 The probit marginal effect estimates are similar to estimates obtained from linear probability models. 19 Significance levels are not materially different if robust standard errors are used without clustering.

18

The evidence in Table 5 is inconsistent with there being a relation between survival and capital

structure policy. When current leverage is included, lagged leverage, as a measure of capital structure

policy, is not positively related to delisting probability. To assess the robustness of this conclusion, we tried

including short‐ and long‐term interest rates as additional controls. Those controls were not statistically

significant at even low levels and the results for the other variables were not materially different from

those reported. We also tried adding annual fixed effects. Again, results were not materially different. In

the next subsection, we formally model and endogenize leverage policy as an alternative test of the

hypothesis.

In the last two columns of Table 5, we use multinomial probit to test separately for relationships

between capital structure and either acquisition or failure. Results based on BW book and market leverage

are, again, similar. The LRZ results are weaker but have the same signs. Based mainly on the BW models,

current high levels of debt financing are associated with higher probabilities of both acquisition and failure.

However, results for the 3‐year lagged leverage (or 3‐year change) are different. Acquisitions are more

likely when leverage has been increasing rapidly, whereas the relationships to failure probability are not

significant. For acquisitions, the evidence suggests that it is not so much the level as the rate of change in

leverage that affects acquisition probability. Results for the W measure (not reported) are similar.

Given the evidence in Table 4, that the total assets and sales revenue of acquired firms tend to be

growing rapidly, we infer that acquisition probability is consistent with the pecking‐order hypothesis ‐ firms

with good growth prospects first finance with low‐risk borrowing and then turn to other alternatives. Firms

with good growth prospects, and that have limited financial slack, appear to become prospects for

acquisition. This interpretation is reinforced by the closer alignment of the BW measure with financial slack,

coupled with the stronger results when the BW measure is used. The weaker results for the LRZ measure,

which is more closely aligned with the tradeoff hypothesis, reinforce the interpretation that acquisition

probability is not driven by suboptimal capital structure choices under the tradeoff hypothesis.

19

The evidence suggests a different interpretation for failed firms. Table 4 shows rapid increases in

leverage and decreasing profitability. Both the BW and LRZ results in Table 5 show that the current highly‐

levered capital structure is significant, but that the rate of increase is not. The evidence that lagged capital

structure is not significant and that the change is also not significant when year‐0 leverage is included

indicates that capital structure policy does not affect failure probability directly, but only does so if the firm

gets into trouble and responds by increasing leverage to unsustainable levels.

5.3.2. Monotonic probit with endogenized capital structure

To assess the robustness of our conclusion that capital structure policy does not significantly affect

survival probability, we estimate two‐stage probit models of endogenous capital structure and survival

probability.20 In the first stage, we regress capital structure on the same variables as in Table 5, but also

add the three year lags of those variables. The lagged variables are used to introduce capital structure

policy in a similar manner to the way lagged capital structure is used in Table 5. Thus, when we endogenize

capital structure and use it in a second‐stage model that includes contemporaneous variables but

instrument the lagged variables, the coefficient on capital structure serves as a test of whether capital

structure policy is significantly related to survival probability.

To capture the effects of generic shocks that might affect capital structure but are correlated with

survival probability only through capital structure, 21 we include the corporate tax rate and the three‐year

average of oil prices, ending in year 0.22 The tax rates are defined as a marginal corporate income tax rate

for the highest corporate tax bracket in the observation year. By instrumenting capital structure with these

variables, we allow for capital structure to vary with corporate tax rates and oil prices. If firms add leverage

when tax rates are high, the coefficient should be positive. The sign on oil prices is ambiguous. Firms might

reduce leverage if historically high oil prices enable them to pay down debt or they might increase leverage

20 Wooldridge (2002, 472‐477) provides a discussion on the probit model with endogenous explanatory variables. We also tried a linear probability model by 2SLS and confirmed that the results were unchanged. 21 See Roberts and Whited (2012) for discussions on the validity of instrumental variables. 22 Similar to our approach, Molina (2005) uses a firm’s marginal tax rate as an instrumental variable for leverage in order to estimate the effects of leverage on corporate credit ratings.

20

if they anticipate continuing high prices and see this as an investment opportunity. If changes in tax rates

and oil prices affect failure probability through capital structure changes, we should find that failure

probability is significantly related to endogenized capital structure.

Table 6 shows two‐stage instrumental variables (IV) results for both the BW and LRZ measures of

capital structure. In the first pair of models, both lagged firm‐specific variables and generic shock variables

are treated as instruments; in the second pair only the generic shock variables are treated as instruments.

These represent the extremes of a range of plausible assumptions. We also tried including the lagged

leverage variable in the second stage, where we obtained results similar to the first pair of models; and

excluding all of the lagged variables except lagged book value from both stages, where we obtained results

similar to the second pair of models. The estimates in Panel (a) are based on book value measures of

leverage; those in Panel (b) are based on market value measures. Because the first‐stage model results in

Panels (a) and (b) are similar, we report the first stage only for Panel (a). Models using the W measure of

leverage are not reported, but are similar to the reported results.

The results in Table 6 are consistent with our interpretation of the results in Table 5. Both of the

instruments are statistically significant in the first‐stage equations, satisfying the relevance requirement of

instrumental variables, but the endogenized leverage measures (either book or market leverage) are not

significant in the second‐stage survival models.23 That is, when we replace current‐year leverage with an

endogenous measure of capital structure policy based on firm‐specific factors and economy‐wide shocks,

contemporaneous leverage becomes non‐significant. The contrasting results for this variable in Tables 5

and 6 indicates that the significant coefficients in Table 5 arise because non‐surviving firms experience

leverage increases that are not reflective of the firm’s capital structure policy.

23 It is known that instruments only weakly correlated with the endogenous variables bias the instrumented coefficients. Stock, Wright, and Yogo (2002) suggest that the F‐statistic for the joint significance of instruments should exceed 10 for the estimates to be reliable when there is one endogenous variable. In Table 6, we estimate F‐statistics using linear probability models for each model and find that most of the F‐statistics are above 10, indicating that our results do not suffer from the weak instrument issues. We report Kleibergen‐Paap F‐statistics instead of Cragg‐Donald F‐statistics since our standard errors are clustered by firms and thus the i.i.d. assumption does not hold. In addition, according to the reported underidentification and overidentification test p‐values, our models are identified and the instruments are valid.

21

5.3.3. Nonmonotonic estimates

Because the prior analysis can only be used to test for a monotonic relationship between capital

structure and survival probability and we are agnostic as to the shape of the relationships between capital

structure and delisting, acquisition, or failure, we consider three different functional forms that allow

nonmonotonicity: (1) quadratic specifications to current and lagged capital structure; (2) a linear splined

model that allows capital structures above and below the sample mean to have different slopes; and (3)

linear splined models where the relationships of capital structure to outcomes are assumed to be linear

over a broad range, but allowed to be different in the upper and lower deciles and quintiles.

We report this analysis in Table 7. As in Table 5, we report multinomial probit estimates for

acquisition and failure outcomes. Because control variable coefficients are similar to those reported in

Table 5, we suppress them in Table 7. Because book value and market value results are similar, we report

only book value results. And because our strongest results in Table 5 are for the BW measure, we report

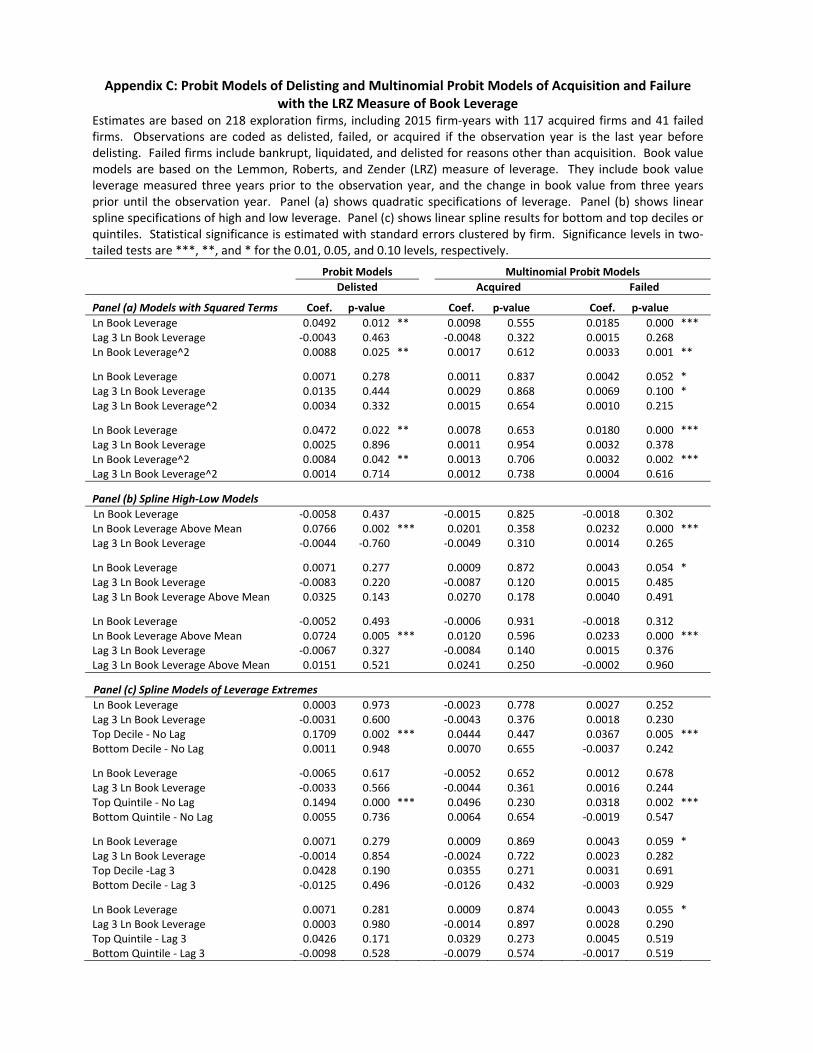

and discuss mainly those results. LRZ results are reported in Appendix C; W results are similar to the BW

results and are not reported.

(a) Quadratic specification

To test for a relationship between capital structure and outcome probability that is approximately

quadratic in the natural log of leverage, in Panel (a) we test three alternative specifications: squaring only

the current leverage ratio, only the lagged leverage ratio, and squaring both. The quadratic term for the

observation year is statistically significant for delisting probability. Solving the quadratic, however,

indicates a very low optimum of about 11.5% debt to total assets in year 0. The low optimum for current

leverage relative to the sample mean helps to explain the significant monotonic estimates in Table 5.

The relationship in Panel (a), while significant, is weak except in the extremes. Based on

investigation of the results, delisting probability increases substantially at year‐0 leverage ratios above

100%. From the minimum point to leverage ratios of either 1% or 100%, estimated delisting probability

increases by about 6.7 percentage points. We find no significant results for quadratic specifications of

22

lagged leverage. The coefficient on lagged leverage is similar to that in Table 5 and the quadratic term is

not significant. Results are not sensitive to inclusion of interest rate variables or annual fixed effects.

Delisting results for the LRZ measure of book leverage are similar, except that the lagged relationships are

never significant.

For acquired firms, results are not materially different from in Table 5, and introducing the

quadratic terms makes the observation year coefficient nonsignificant. The results again support the

inference that compelling growth opportunities that consume financial slack lead to acquisition. The

estimated observation‐year optimal capital structure in the failure model is again low, at about 10%

leverage. Failure probability increases by only about 2.2 percentage points as current leverage increases to

100% or decreases to 1%. Lagged capital structure is never statistically significant in the quadratic models,

consistent with our finding in Table 5 that capital structure policy is not significantly related to failure

probability; failure probability increases when underperformance leads to leverage ratios that are not

sustainable. LRZ results for acquisition are never significant and those for failure are consistent with results

reported in Table 5.

(b) High and low‐leverage differences

In Panel (b), we allow the slope of the leverage relationship to be different above and below the

sample mean. In each model, we include the log of book leverage and the lagged value of book leverage.

We also include, for observations above the sample mean, either a high‐leverage variable that measures

the difference between observed year‐0 leverage and the mean and is otherwise zero, or a similar lagged

high‐leverage difference variable, or both.

We again find positive relationships of delisting, acquisition, and failure probabilities to year‐0

leverage. The relationship is significantly greater for observations where leverage is above the mean. Both

the BW and LRZ results consistently indicate that the 3‐year lagged leverage interaction is not significant

and the base 3‐year lagged result is similar to that in Table 5, again supporting the view that acquisitions

occur in response to rapid growth that is financed with debt.

23

For delisting, the model in Table 7 indicates that failure probability is increasing in year‐0 leverage,

with the probability increasing by 16.3 percentage points as leverage increases from 1% to the sample

mean of 42%, and by another 9.7 percentage points as leverage increases to 100%. In the acquisition

model, the respective increases associated with year‐0 leverage are estimated to be 7.9 and 4.9 percentage

points. Similarly, in the failure model, the respective increases are 4.0 and 1.9 percentage points. For

neither acquisition nor failure probability is the 3‐year lagged interaction variable statistically significant.

Overall, these results support the inferences from Tables 5 and 6. There is no evidence that

delisting, failure, or acquisition probabilities increase for low‐leverage firms in year ‐3 and, based on Table

5, the negative coefficients on lagged book leverage are appropriately interpreted as indicating that the

rate of change in leverage is associated with higher acquisition probability due to the need to fund growth.

LRZ results appear to be weaker because the measure is less closely aligned with the pecking order

hypothesis.

(c) Models of leverage extremes

Neither the quadratic nor the high‐low models can reliably detect whether extreme leverage ratios

are associated with materially higher probabilities of delisting, acquisition, or failure. To capture the

extremes, we classify firms into book‐leverage deciles or quintiles each year. We extend the probit models

by including interactions of binary variables for the lowest and highest leverage deciles (quintiles) with the

difference between the leverage ratio and lowest observed value above the bottom quantile or between

the value and highest observed value below the top quantile. All differences are measured as observation

value minus critical value. These difference variables are constructed for both year 0 and year ‐3.

In Panel (c), the contemporaneous high leverage indicator variables are statistically significant and

positively related to delisting in both decile and quintile models. Low leverage indicators are not significant.

This is also true for the LRZ models. The results suggest that firms with very high year‐0 leverage ratios are

more likely to be acquired or fail. There is no significant evidence that firms are subject to greater risk of

non‐survival if they operate with capital structures well below the norms in year 0. However, acquisition

24

probability is significantly positive for the bottom decile; whereas failure probability is significantly negative

(both results for the bottom decile are not statistically significant in the LRZ models in Appendix C). The 3‐

year lagged variables for the highest and lowest leverage deciles and quintiles are never significant,

suggesting capital structure policy is not important for firm survival (also true in the LRZ models).

(d) Recap

Both the monotonic and non‐monotonic specifications indicate that delisting, acquisition, and

failure probabilities increase with year‐0 leverage and there is some evidence that the relationship is not

linear in the natural log of leverage. We find no evidence of an optimal capital structure based on the 3‐

year lag of leverage. The two‐stage results with endogenized capital structure confirm this conclusion in

that the endogenous leverage policy variable is not significantly related to survival. Overall, the results are

consistent with the pecking order hypothesis in that acquired firms first use debt capacity to fund growth

and then are more likely to become acquisition candidates. The positive relationship between year‐0

leverage and failure probability arises endogenously – firms with operational problems increase leverage in

the face of declining performance and are more likely to fail.

5.4. Leverage Effects on Revenue Shares

Researchers use revenue (market) share and change in revenue share as indicators of good choices.

As noted, Stigler (1958) argues that the competitive process will cause the aggregate share of firms with

good strategies to increase, and presents evidence from several industries. Appel, Worrall, and Butler

(1985) study survivorship of property and liability insurers in relation to firm size. Bring (1982) and Hibdon

and Muller (1990) study survivorship of petroleum refinery establishments by facility size. Gregory (2000)

uses the survivorship approach to assess scale economies in international liner shipping.24

We hypothesize that if there is an important optimal capital structure for exploration firms then we

should find that the aggregate revenue share of firms located close to the optimal capital structure

increases over time. To assess the relationship of capital structure to aggregate revenue share we group

24 See also Keeler (1989) regarding the US trucking industry, Danos and Eichenseher (1982) regarding the auditing industry, and Santerre and Pepper (2000) regarding US hospital services.

25

firms into deciles based on their book leverage ratios and sum the revenue shares of the firms within each

decile. The results of this aggregation for BW leverage in year ‐3 were presented earlier, in Figure 1.

It is apparent from Figure 1 that if there is an optimal capital structure, it is not stationary.

Conceivably, the optimum is affected by the main factors that would affect the tradeoff between the debt

tax shelter and bankruptcy cost. However, the data in Figure 1 provide no support for this explanation. In

various years, the top half of the observations account for anywhere from 9.2% to 95.2% of market revenue.

Based on investigation of the relations between decile market share changes and various macro‐factors, we

find that the period of high nominal interest rates from 1979 through 1985 is associated with a large

market share for highly levered firms, but the median leverage ratio measured in this way increases several

years before the interest rate spike and the leverage ratio does not decrease after 1985, when nominal

rates decline. Movement of the median leverage ratio also is not sensitive to implied short‐term real rates,

which are negative from 1974 through 1980 and unusually high from 1981 through 1986. The median

leverage ratio is high and stable over this 13‐year period. There is also no evidence that the median

leverage ratio is sensitive to corporate tax rates. When the maximum corporate rate was reduced from 46%

to 34% around the time of the Tax Reform Act of 1987, the change had no apparent effect on the median

leverage ratio.

In short, this evidence provides no support for the optimal tradeoff hypothesis, considering either a

static optimum or one that evolves over time in response to interest rates, inflation rates, and tax rates.

Moreover, we have already determined that delisting, acquisition, and failure probabilities are not

significantly related to interest rates.

Perhaps the shifting market shares in Figure 1 are attributable to the pecking order hypothesis. As

observed earlier, firms may increase leverage to pursue growth opportunities, and reduce it when their

operations generate free cash flow that is unneeded for investment. The data in the figure appear

generally to support this hypothesis. The median leverage ratio increased sharply in the year after the 1973

OPEC oil price shock, and remained high for many years. After reaching a real price of over $100 per barrel

26

in 1980, oil prices declined substantially. During this era of low prices, the median leverage ratio remained

high. As real prices began to increase around 2000, leverage ratios began to decline. While this makes a

plausible story, the data are too limited to enable us to provide rigorous empirical support. We tried

modeling the changes in the market shares of leverage deciles but were unable to find a stationary

relationship to oil prices. The only consistently significant explanatory variables were the lagged market

share of the decile and an ordinal decile rank variable. Prices or price changes interacted with binary decile

indicators were not significant. We obtained similar results using leverage quintiles and using the median

leverage ratio.25

It is not clear why increasing oil prices would trigger leverage‐increasing investment in the 1970,

but high prices in the 2000s would trigger leverage reduction. To be sure, the regulatory environment now

is different from what it was in the 1970s and may be discouraging exploration firms from investing.

5.5. Firms with Persistent Low Leverage: A Clinical Examination

The optimal tradeoff hypothesis implies that firms with persistently low leverage may be failing to

take optimal advantage of the tax deductibility of interest expense and, therefore, are likely to be

acquisition targets. Our statistical evidence does not support this, and indicates, rather, that firms are

acquired when their growth prospects have reduced financial slack, a finding more consistent with the

pecking‐order hypothesis. Still, persistent low‐leverage seems puzzling. Perhaps low‐leverage firms are

inefficient but are insulated from the take‐over market. To better assess this, we identified firms in our

sample that operated with persistent low leverage using the BW measure, and tracked their performance.

Five firms in our sample had book leverage ratios that were persistently below 20 percent.

General American Oil Company operated with low leverage from before 1970 through 1980 and

without convertible debt or preferred stock.26 During this period, company revenue was growing at a

25 We tested this at the firm level by regressing leverage on leads and lags of operating cash flow (EBITDA) and found that leverage changes are negatively related to contemporaneous and lagged cash flow, but not related to leads of cash flow. These firm‐level results are consistent with the pecking order interpretation. 26 We specifically indicate the use of convertible debt and preferred stock for these low‐leverage firms because these financing sources are important to the difference between the BW and LRZ measures.

27

compound annual rate of 17.6%, and with an unusually high average annual EBIT/sales ratio of 31.4 %. The

company carried a modest level of funded debt and increased its dividends at a compound annual rate of

11.1 %. Its average annual effective tax rate on income during the period was 33.2 %.

General American appears to have been well‐suited for takeover under the tradeoff hypothesis. It

did eventually become the target of a hostile takeover attempt, when, in one of the earliest corporate

raider actions, T. Boone Pickens made an offer in December 1982. Pickens was out‐bid by Phillips

Petroleum, which, acting as a white knight, acquired General American in 1983.27 While the outcome is

consistent with optimal tradeoff, it took more than 10 years of low‐leverage operation without apparent

challenge to precipitate the takeover attempt. Either the control market is not very effective at disciplining

inefficient capital structure choices, or the capital structure policy of the firm is not very important.

MSR Exploration operated with book leverage below 20% from 1982 through 1989 and no

convertible debt or preferred stock, but without revenue growth and with declining profitability. EBIT

turned negative in 1986 and remained negative into the mid‐1990s. After several years without interest‐

bearing debt, the company began borrowing in 1989 and continued into the 1990s, but the main reason for

increasing leverage was declining equity book value associated with operating losses. During this period,

MSR’s effective tax rate was consistently zero. The company was merged with Quicksilver Resources, Ltd.

in 1999, at which time it had a significant tax loss carry forward. In summary, MSR’s low leverage was not

indicative of an unexploited tax benefit of debt financing. In fact, the company actually increased its

borrowing for several years beginning in 1989, even though its tax liability was zero. The evidence suggests

that MSR was headed for failure, but that merger may have been preferable because it would preserve

value of assets such as its tax loss carry forward. In fact, MSR filed for bankruptcy in 1992 and was

reorganized, to extend the maturity of its outstanding debt. Restructuring just postponed failure. The

company’s use of debt financing and reorganization to support operations as performance declined is

27 Slater (1999) describes this early takeover attempt.

28

consistent with the pecking order hypothesis, as raising equity in the face of bankruptcy would not have

been feasible.

McFarland Energy operated with book leverage below 20% from 1976 through 1993.28 During this

period, except for two modest episodes of borrowing, including one convertible debt issue and small asset

sales, the company funded its operations internally, by reinvesting operating cash flows. Operating

performance during this period was modest and it lost money and had a negative tax liability most years

after the convertible debt issue. Book assets grew at a slow compounded annual rate of 1.2% and sales

grew at a rate of 2.4%. The company’s operating performance was poor, with a negative annual average

ratio of EBIT to total assets. Its average effective tax rate during the period was 5.6%. Overall, there is little

to make the company attractive as an acquisition target and performance is not bad enough to threaten its

survival. From 1993 through 1996, following a substantial acquisition that was largely debt financed, the

company’s performance improved sharply. Both revenue and profitability increased. In 1997, after

agreement with McFarland management, Monterey Resources acquired McFarland via tender offer.29

Statex Petroleum operated with book leverage below 20% in all years but one from 1974 through

1982, and without convertible debt or preferred stock. During most of this period, it operated with no

interest‐bearing debt and was majority owned by California Portland Cement Company (later renamed

CalMat). During the period, company assets grew at an annual rate of 15.6% and revenue grew at 19.7%.

Except for the last two years, the period of most rapid growth, Statex funded its growth through cash flows

from operations. In the last two, it turned to a significant increase in preferred equity (held by CalMat, on

which it paid a preferred dividend) and a modest funded debt issue to finance its growth. The company’s

average annual ratio of EBIT to total assets was 7.8% and its average effective tax rate was 7.9%. While

performance was modest, the company was insulated from the control market by virtue of the CalMat

block. In the face of declining oil prices beginning in 1983, CalMat sold its interest and PSA (formerly Pacific

28 Our sample period for the company begins in 1979 due to missing data required for complete earlier observations. 29 New York Times (1997) and U.S. Securities and Exchange Commission (1979).

29

Southwest Airlines) acquired Statex as part of its oil portfolio.30 Statex is another example of a low‐leverage

firm that, under the optimal tradeoff hypothesis, would not have attracted acquisition interest because of

its modest profitability and low effective corporate tax rate. CalMat only decided to sell when the company

became consistently unprofitable. PSA’s acquisition appears to be more of a hedging strategy than an

effort motivated by the perception that Statex was operating with an inefficient capital structure.

Wiser Oil operated with book leverage below 20% from at least 1970 through 1992 and without

convertible debt or preferred stock.31 During this 23‐year period, total assets grew at an annual rate of

6.1% and revenue grew at 7.6%. For 15 years, from 1972 through 1986, the company’s annual EBIT to

assets ratio averaged 17.4% and its effective tax rate averaged 42.9%. The company refrained from

borrowing during most of this period and distributed much of net income as dividends. Through 1986,