5-1 Double-Entry System CHAPTER 5

5-1 Double-Entry System CHAPTER 5. 5-2 Double-Entry System The double-entry system is considered as the heart of modern accounting. All accounting systems.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

5-1

Double-Entry System

CHAPTER 5CHAPTER 5

5-2

Double-Entry System

The double-entry system is considered as the heart of modern accounting.

All accounting systems operate on the basis of the double-entry system.

Manual accounting system

Computerized accounting system

5-3

Double-Entry System

The double-entry system provides checks and balances to ensure that your books are always in balance.

In double-entry accounting, each transaction has two journal entries: a debit and a credit.

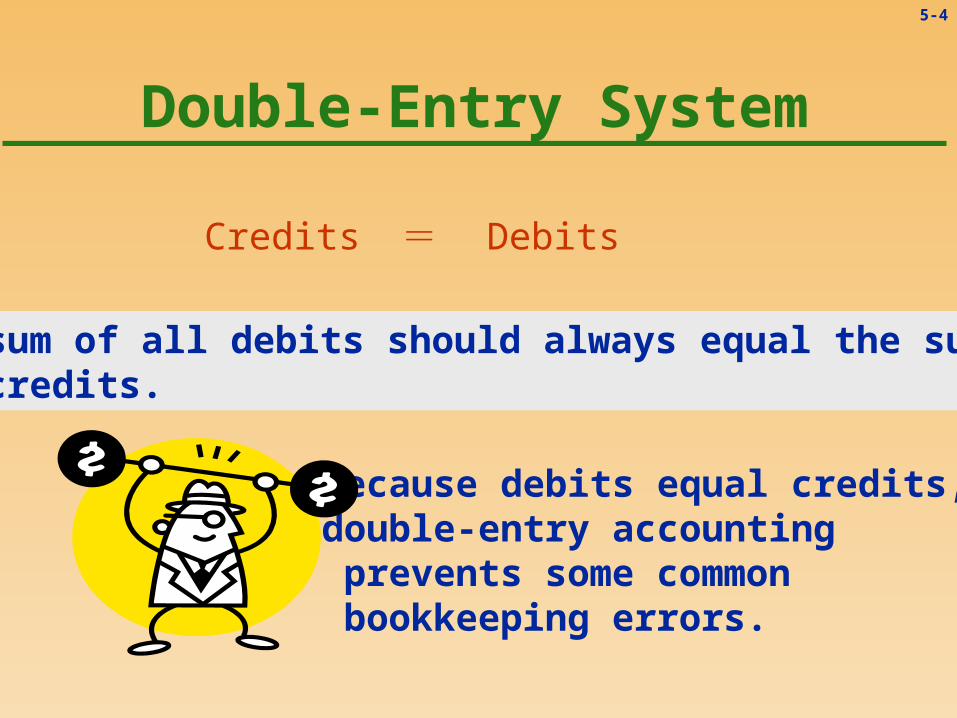

5-4

Double-Entry System

Credits Debits=

Because debits equal credits, double-entry accounting prevents some common bookkeeping errors.

The sum of all debits should always equal the sum of all credits.

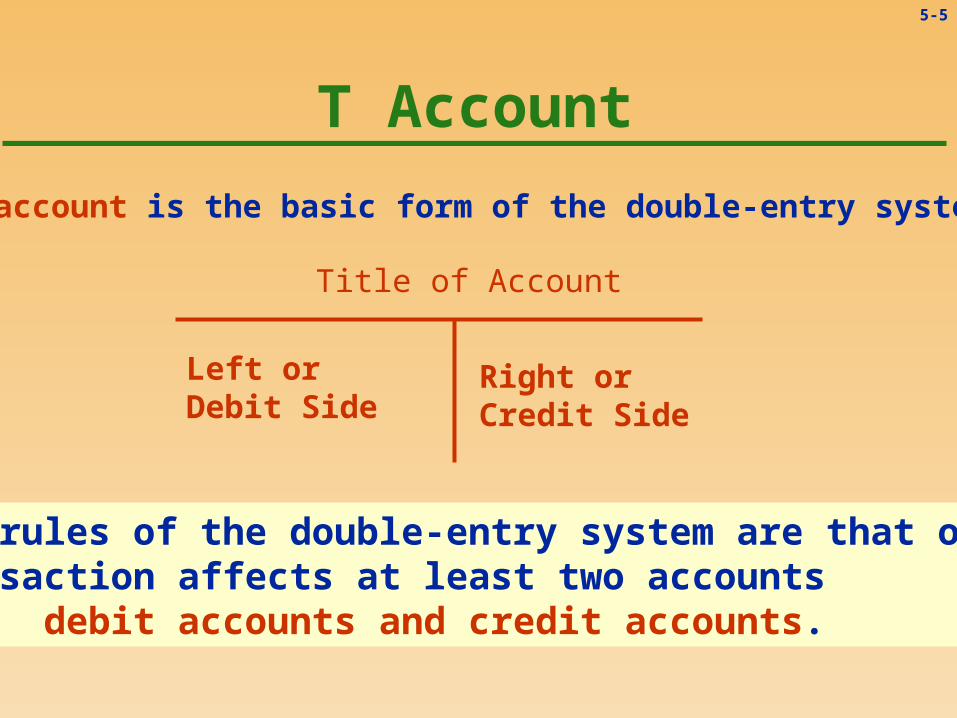

5-5

T Account

The T account is the basic form of the double-entry system.

Title of Account

Left orDebit Side

Right orCredit Side

The rules of the double-entry system are that one transaction affects at least two accounts --- debit accounts and credit accounts.

5-6

Double-Entry System

Assets = Liabilities + Owner’s Equity

Accounting equation

Account Type Debit Credit

Assets Increase Decrease

Liabilities Decrease Increase

Owner’s equity Decrease Increase

Income Decrease Increase

Expenses Increase Decrease

5-7

Transaction Analysis

Now, let’s analyze the transaction of

George Ross Photocopy Company

…

5-8

Transaction Analysis

Transaction 1

March 3: Mr. George starts his photocopy company on March 1 with 20,000 us dollars that was immediately deposited into the bank.

Assets

Owner’s equity ? Increase or decrease

Debited or Credited

5-9

Transaction Analysis

Transaction 1

Account Type Debit Credit

Cash at Bank Increase

George Ross, Capital Increase

Cash at Bank $10,000

George Ross, Capital $10,000

5-10

Transaction Analysis

Transaction 2

March 6: Rented another office, paying a year’s rent in advance, $4,800 by check.

Assets 1 ? Increase or decrease

Debited or CreditedAssets 2

5-11

Transaction Analysis

Transaction 2

Account Type Debit Credit

Prepaid Rent Increase

Cash at Bank Decrease

Prepaid Rent $4,800

Cash at Bank $4,800

5-12

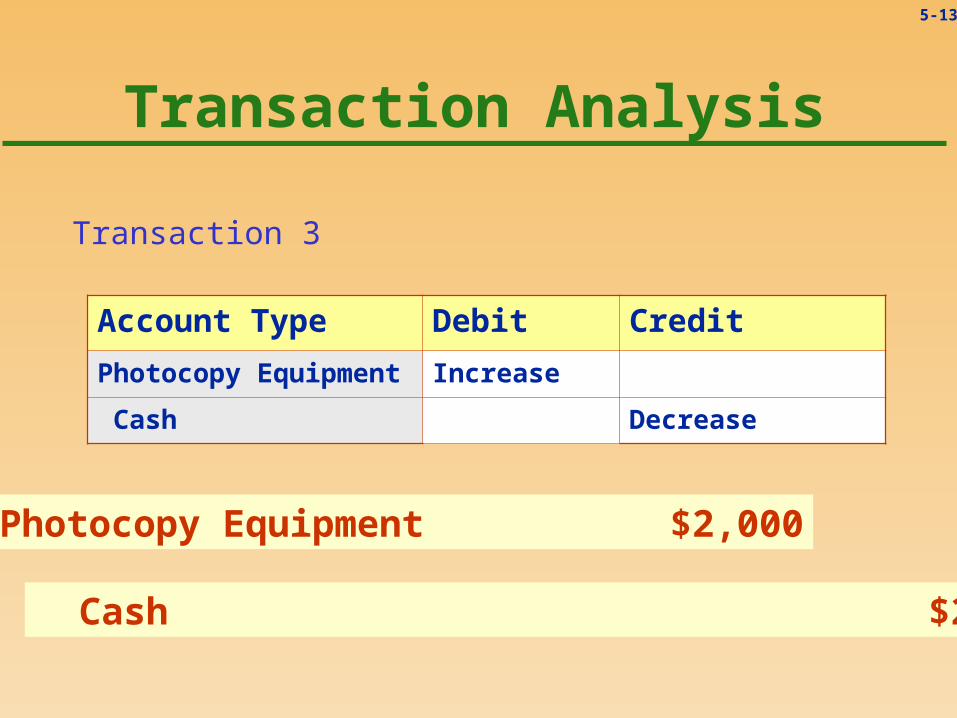

Transaction Analysis

Transaction 3

March 7: Purchased photocopy equipment for $2,000 with cash.

Assets 1

Assets 2?

Increase or decrease

Debited or Credited

5-13

Transaction Analysis

Transaction 3

Account Type Debit Credit

Photocopy Equipment Increase

Cash Decrease

Photocopy Equipment $2,000

Cash $2,000

5-14

Transaction Analysis

Transaction 4

March 7: Purchased office equipment from Hougas Equipment Co. for $5,300, paying $2,300 in cash and agreeing to pay the rest next month.

Assets 1

Assets 2 ? Increase or decrease

Debited or CreditedLiability

5-15

Transaction 4

Transaction Analysis

Account Type Debit Credit

Office Equipment Increase

Cash Decrease

Accounts Payable Increase

Office Equipment $5,300

Cash $2,300

Accounts Payable 3,000

5-16

Transaction Analysis

Transaction 5

March 8: Purchased on credit photocopy supplies for $2,300 an office supplies for $800 from Tim Supply Co.

Assets

Liability?

Increase or decrease

Debited or Credited

5-17

Transaction Analysis

Transaction 5

Account Type Debit Credit

Photocopy Supplies Increase

Office Supplies Increase

Accounts Payable Increase

Photocopy Supplies $2,300

Office Supplies 800

Accounts Payable $3,100

5-18

Transaction Analysis

Transaction 6

March 8: Paid $600 in cash for a one-year insurance policy with coverage effective March 1.

Assets 1

Assets 2?

Increase or decrease

Debited or Credited

5-19

Transaction 6

Transaction Analysis

Account Type Debit Credit

Prepaid Insurance Increase

Cash Decrease

Prepaid Insurance $600

Cash $600

5-20

Transaction Analysis

Transaction 7

March 9: Paid Tim Supply Co. $3,100 of the amount owed by check.

Assets ? Increase or decrease

Debited or CreditedLiability

5-21

Transaction 7

Transaction Analysis

Account Type Debit Credit

Accounts Payable Decrease

Cash at Bank Decrease

Accounts Payable $3,100

Cash at Bank $3,100

5-22

Transaction Analysis

Transaction 8

March 10: Performed a service by printing throwaways for a garment dealer and agreed to collect the fee at the beginning of the next month, $6,000.

Assets ? Increase or decrease

Debited or CreditedOwner’s equity

5-23

Transaction 8

Transaction Analysis

Account Type Debit Credit

Accounts Receivable Increase

Photocopy Fees Earned Increase

Accounts Receivable $6,000

Photocopy Fees Earned $6,000

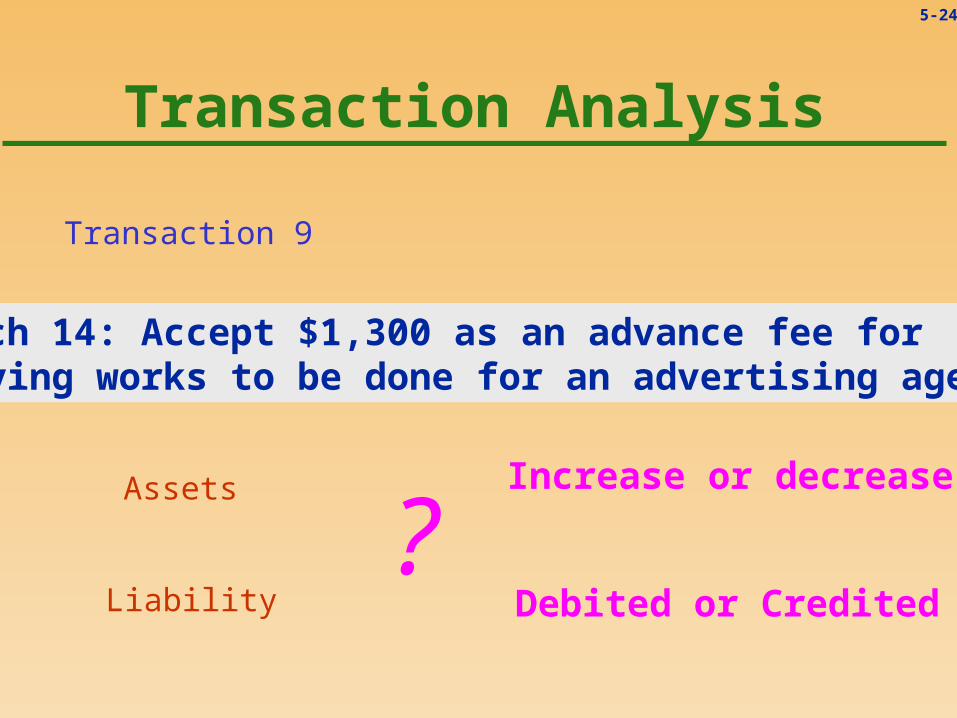

5-24

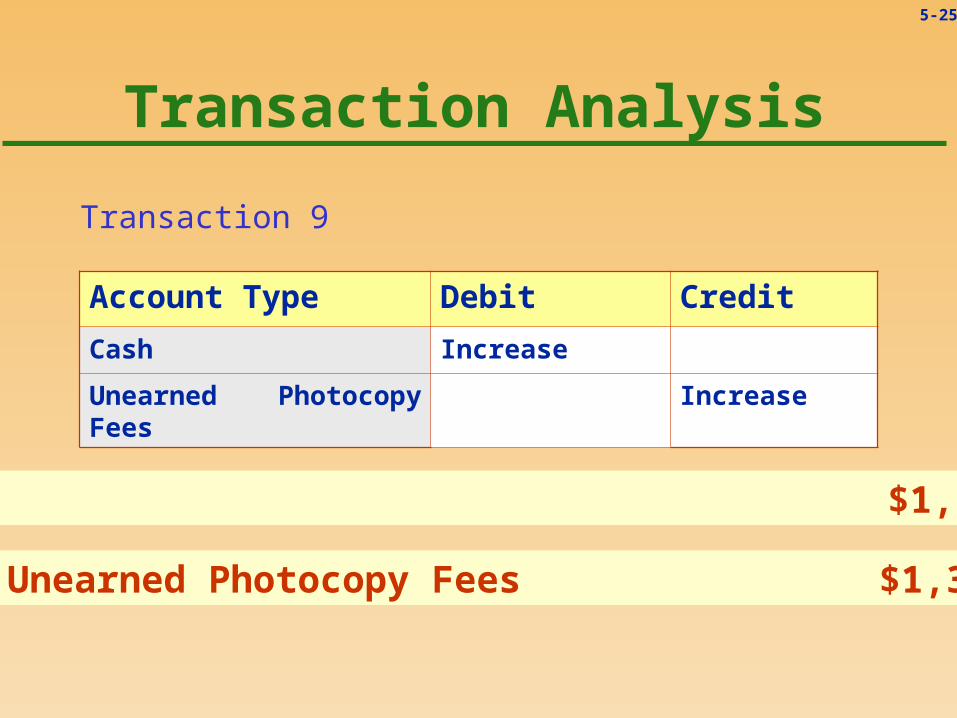

Transaction Analysis

Transaction 9

March 14: Accept $1,300 as an advance fee for copying works to be done for an advertising agency.

Assets

Liability?

Increase or decrease

Debited or Credited

5-25

Transaction 9

Transaction Analysis

Account Type Debit Credit

Cash Increase

Unearned Photocopy Fees Increase

Cash $1,300

Unearned Photocopy Fees $1,300

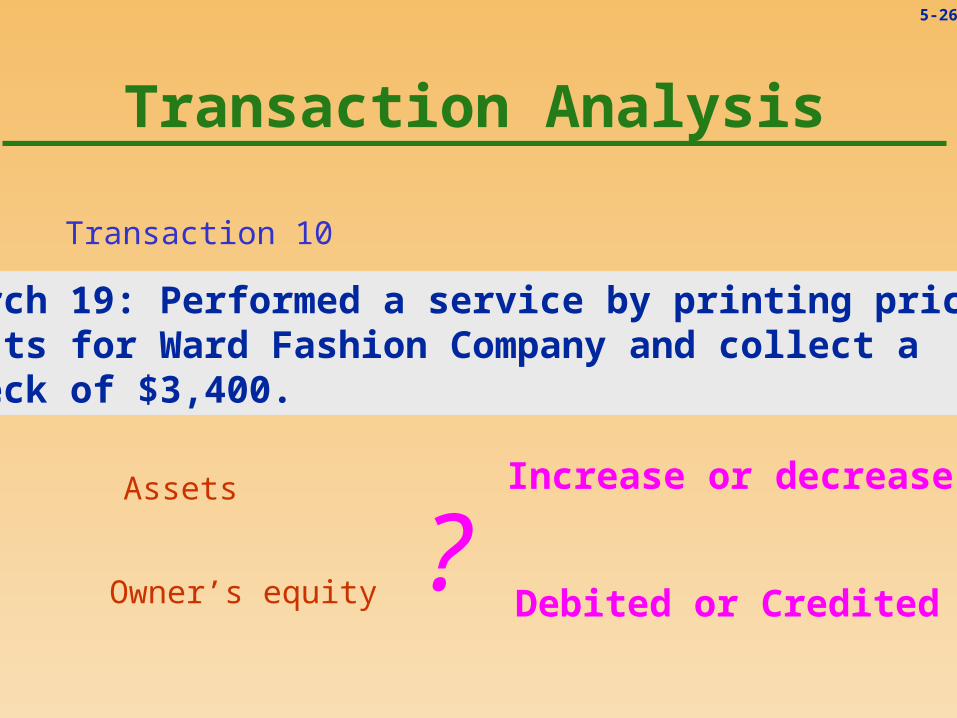

5-26

Transaction Analysis

Transaction 10

March 19: Performed a service by printing price lists for Ward Fashion Company and collect a check of $3,400.

Assets

?Increase or decrease

Debited or CreditedOwner’s equity

5-27

Transaction 10

Transaction Analysis

Account Type Debit Credit

Cash Increase

Photocopy Fees Earned Increase

Cash at Bank $3,400

Photocopy fees Earned $3,400

5-28

Transaction 11

Transaction Analysis

Account Type Debit Credit

George Ross, Withdrawals Decrease

Cash Decrease

George Ross, Withdrawals $980

Cash $980

March 24: George Ross withdrew $980 from the business for personal living expenses.

5-29

Transaction Analysis

Transaction 12

March 25: Paid the secretary salary, $1,100.

Account Type Debit Credit

Office Salary Expense Decrease

Cash Decrease

Office Salary Expense $1,100

Cash $1,100

5-30

Transaction 13

Transaction Analysis

Account Type Debit Credit

Utility Expense Decrease

Cash Decrease

Utility Expense $230

Cash $230

March 29: Received and not paid the utility bill of $700.

5-31

Transaction 14

Transaction Analysis

Account Type Debit Credit

Telephone Expense Decrease

Accounts Payable Increase

Telephone Expense $120

Accounts Payable $120

March 31: Received a telephone bill, $120.

5-32

T account

Cash(at Bank)

Bal. $410

3. $10,00014. 1,30019. 3,400

6. $4,8007. 2,0007. 2,3008. 6009. 3,10024. 98025. 1,10029. 230

5-33

T account

Accounts Receivable

10. $6,000

Bal. $6,000

Photocopy Supplies

8. $2,300

Bal. $2,300

Office Supplies

8. $800

Bal. $800

Prepaid Insurance

8. $600

Bal. $600

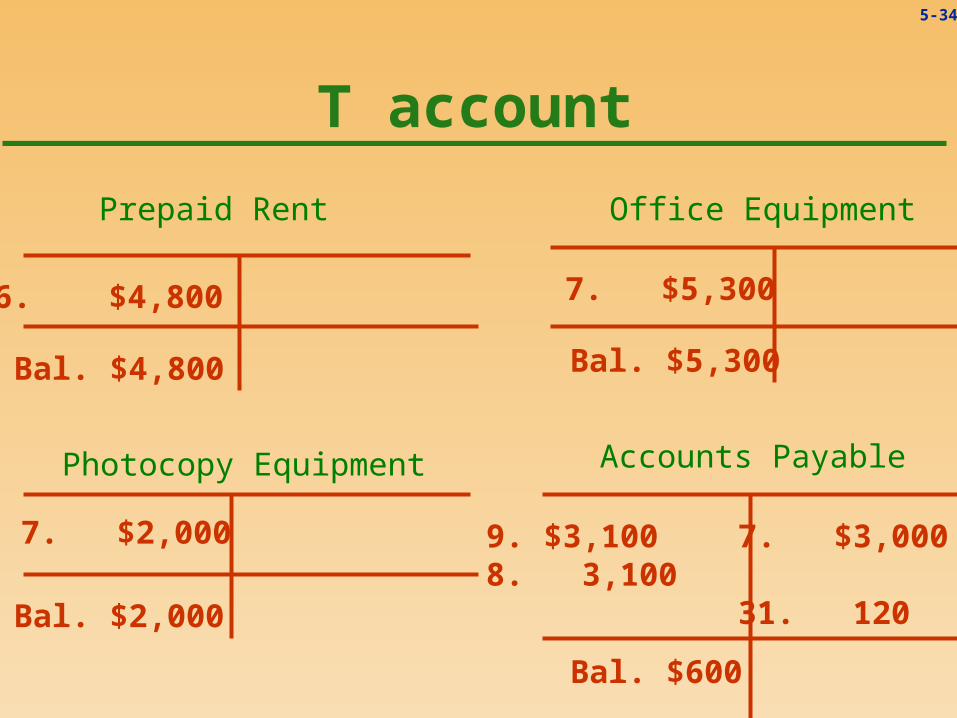

5-34

T account

Prepaid Rent

6. $4,800

Bal. $4,800

Photocopy Equipment

7. $2,000

Bal. $2,000

Office Equipment

7. $5,300

Bal. $5,300

Accounts Payable

9. $3,1008. 3,100

Bal. $600

7. $3,000

31. 120

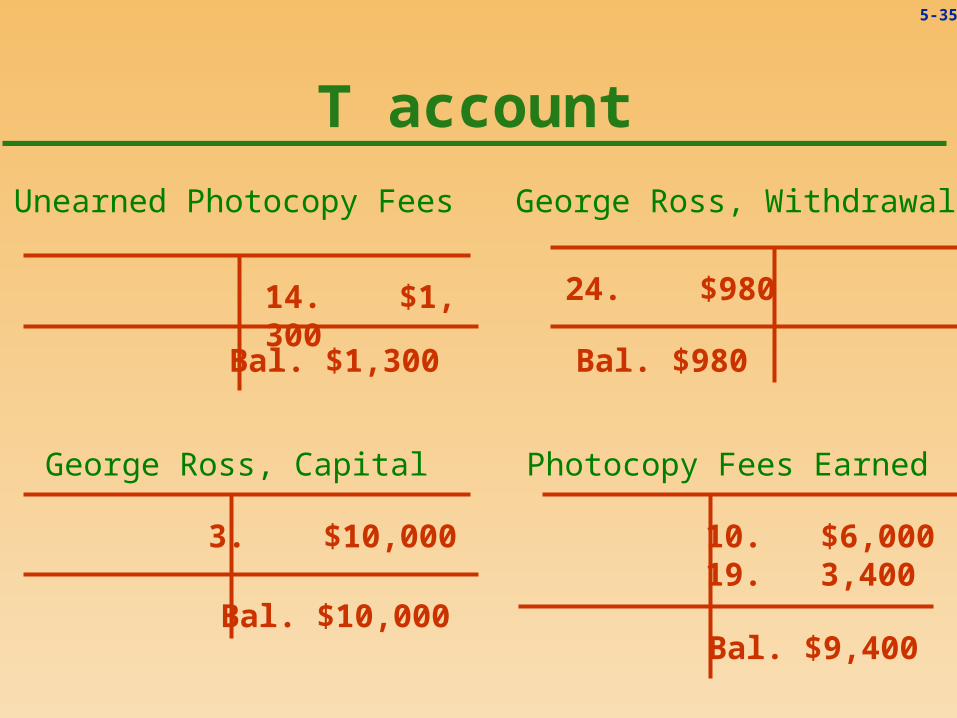

5-35

T account

Unearned Photocopy Fees

14. $1,300

Bal. $1,300

George Ross, Capital

3. $10,000

Bal. $10,000

George Ross, Withdrawal

24. $980

Bal. $980

Photocopy Fees Earned

Bal. $9,400

10. $6,00019. 3,400

5-36

T account

Office Salary Expense

25. $1,100

Bal. $1,100

Utility Expense

29. $230

Bal. $230

Telephone Expense

31. $120

Bal. $120

5-37

T account

On the basis of the T account calculation, we get the result as follows:

Assets = Liabilities + Owner’s Equity

$21,390 = $4420 + $16,970

5-38

WE ARE SAILING RIGHT ALONG!!

Related Documents