PHARMSTANDARD – LEADING RUSSIAN PHARMACEUTICAL COMPANY 4Q/FY 2013 Sales Results Presentation OTCPharm Introduction Igor Krylov Olga Mednikova 1 Conference call: 4Q/FY 2013 Sales Results (18.02.14)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PHARMSTANDARD – LEADING RUSSIAN PHARMACEUTICAL COMPANY

4Q/FY 2013 Sales Results Presentation

OTCPharm Introduction

Igor Krylov

Olga Mednikova

1Conference call: 4Q/FY 2013 Sales Results (18.02.14)

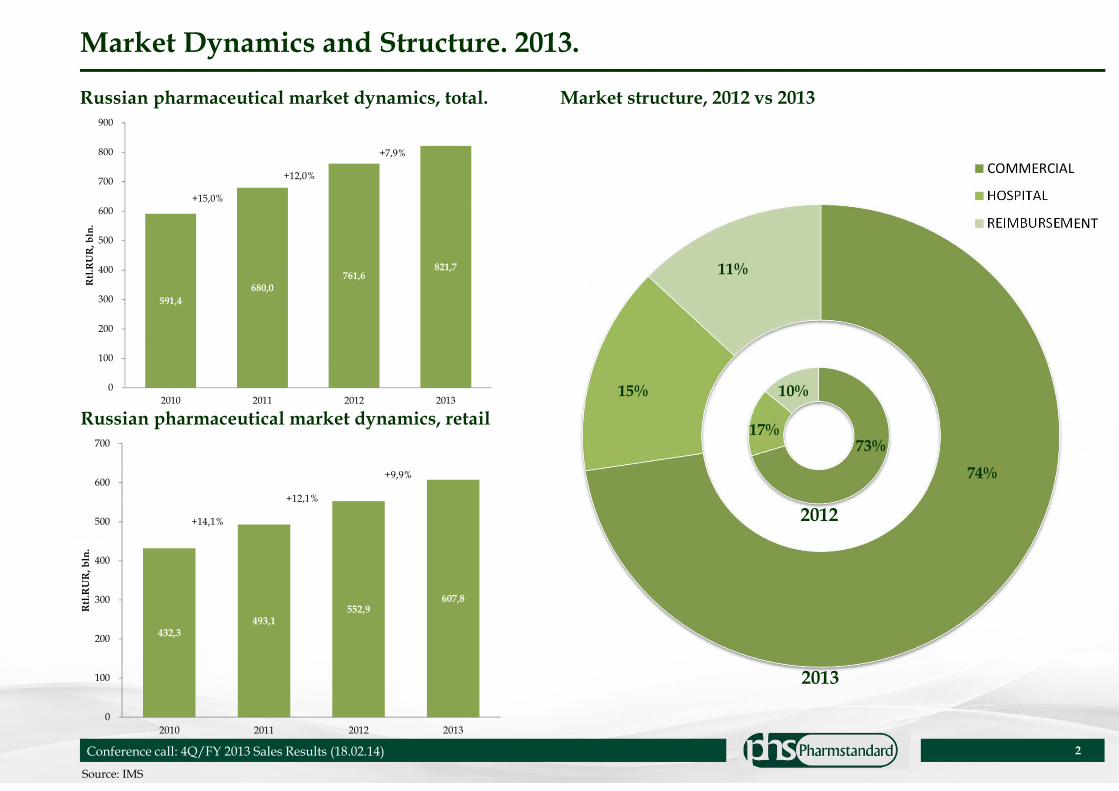

Market Dynamics and Structure. 2013.

2

Market structure, 2012 vs 2013

COMMERCIAL

HOSPITAL

REIMBURSEMENT

2012

2013

73%17%

10%

74%

15%

11%

Russian pharmaceutical market dynamics, total.

Russian pharmaceutical market dynamics, retail

Source: IMS

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

591,4

680,0 761,6

821,7

+15,0%

+12,0%

+7,9%

0

100

200

300

400

500

600

700

800

900

2010 2011 2012 2013

Rtl

.RU

R, b

ln.

432,3 493,1

552,9 607,8

+14,1%

+12,1%

+9,9%

0

100

200

300

400

500

600

700

2010 2011 2012 2013

Rtl

.RU

R, b

ln.

Leading Pharmaceutical company in Russia

The only Russian pharmaceutical company among the top-10 largest players, one of the market leaders

3

Russian Pharmaceutical Market – Total (2013)

Source:IMS

2,7%

2,7%

2,8%

2,8%

2,9%

2,9%

3,2%

3,4%

3,7%

5,3%

JOHNSON & JOHNSON

SANDOZ GROUP

SERVIER

NOVARTIS

NYCOMED/TAKEDA

ROCHE

TEVA

BAYER HEALTHCARE

PHARMSTANDARD

SANOFI-AVENTIS

# 1 Local Company and a leader in retail segment with significant market shares on the Russian market

4

Russian Pharmaceutical Market – Local (2013)

Leading Pharmaceutical company in Russia (continued)

Source:IMS

Russian Pharmaceutical Market – Retail (2013)

SANOFI-AVENTIS5,1%

PHARMSTANDARD4,3%

BAYER HEALTHCARE4,0%

SANDOZ GROUP3,5%

SERVIER3,4%

NYCOMED/TAKEDA3,3%

MENARINI3,0%

TEVA3,0%

NOVARTIS2,9%

ABBOTT2,5%

Other (1790 comp)65,1%

PHARMSTANDARD4,3%PHARMSTANDARD

15,8%

STADA5,4%

VALENTA3,8%

EVALAR3,5%

MATERIA MEDICA2,9%

MICROGEN2,8%

VEROPHARM2,7%

OZON OOO2,6%

AKRIKHIN-PHARMA2,5%

NIARMEDIK PLUS RF2,1%

Other (1790 comp)55,9%

PHARMSTANDARD15,8%

5

Source: Company data

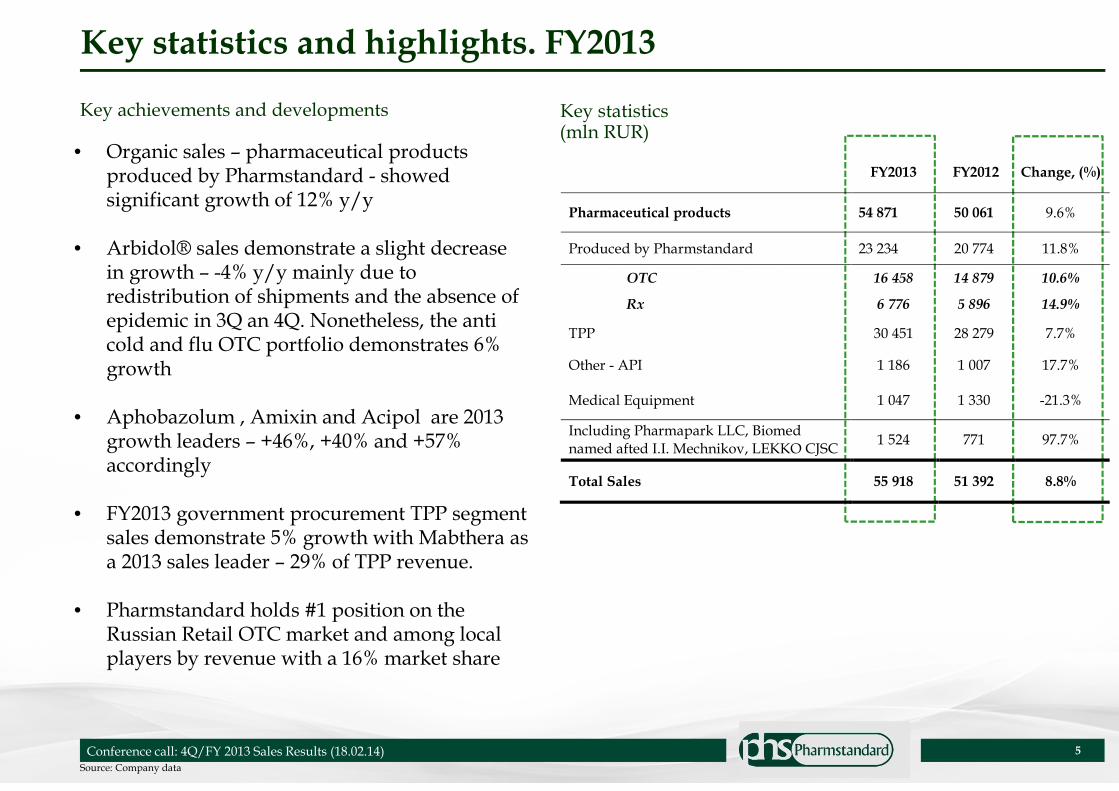

Key statistics and highlights. FY2013

Key statistics(mln RUR)

Key achievements and developments

• Organic sales – pharmaceutical products produced by Pharmstandard - showed significant growth of 12% y/y

• Arbidol® sales demonstrate a slight decrease in growth – -4% y/y mainly due to redistribution of shipments and the absence of epidemic in 3Q an 4Q. Nonetheless, the anti cold and flu OTC portfolio demonstrates 6% growth

• Aphobazolum , Amixin and Acipol are 2013 growth leaders – +46%, +40% and +57% accordingly

• FY2013 government procurement TPP segment sales demonstrate 5% growth with Mabthera as a 2013 sales leader – 29% of TPP revenue.

• Pharmstandard holds #1 position on the Russian Retail OTC market and among local players by revenue with a 16% market share

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

FY2013 FY2012 Change, (%)

Pharmaceutical products 54 871 50 061 9.6%

Produced by Pharmstandard 23 234 20 774 11.8%

OTC 16 458 14 879 10.6%

Rx 6 776 5 896 14.9%

TPP 30 451 28 279 7.7%

Other - API 1 186 1 007 17.7%

Medical Equipment 1 047 1 330 -21.3%

Including Pharmapark LLC, Biomed named afted I.I. Mechnikov, LEKKO CJSC

1 524 771 97.7%

Total Sales 55 918 51 392 8.8%

Brand Therapeutic segment

FY2013 sales

FY2012 sales

Sales growth

% growth

OTC

Afobazol ® Tranquillizer 1 273 872 401 46,0%

Amixin ® Anti-viral 1 106 792 315 39,8%

Acipol® Anti-fungal 612 390 222 56,8%

Ingalypt ® Anti-viral 488 329 160 48,5%

Magnelis® Vitamins 322 196 126 64,3%

Next® Analgesics 169 46 123 270,2%

Noopept® Tranquillizer 130 15 115 794,9%

Rx

Phosphogliv Insulin 1 373 1 162 211 18,2%

Combilipen Vitamin B1 688 534 153 28,7%

Pentalgin Anti-viral 324 213 111 52,3%

Formetine Diabetes 227 125 102 81,8%

Altevir Interferon alfa-2b 165 68 96 140,8%

Artrosan Analgesics 215 137 78 57,4%

6

Source: Company data

Top Pharmaceutical Product Drivers, FY2013

ОТС FY2013 sales in went up to RUR16 458m (+11%).

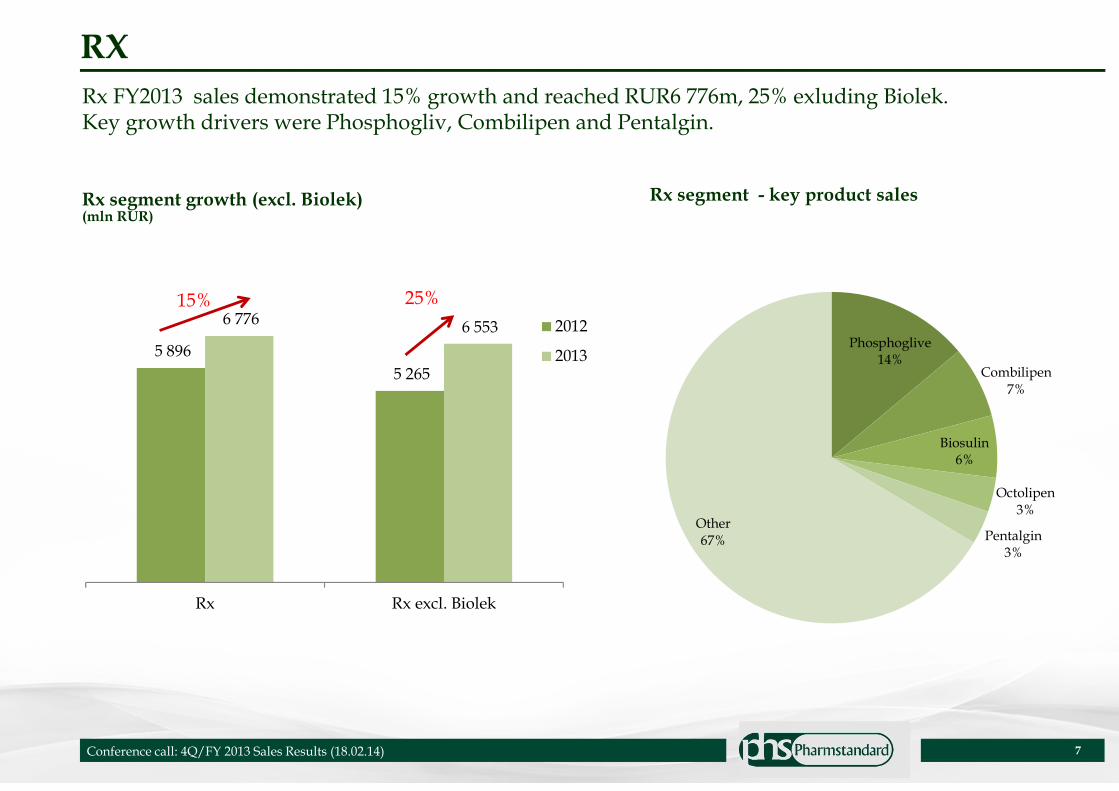

Rx FY2013 sales demonstrated 15% growth and reached RUR6 776m. Key growth drivers were Phosphogliv, Combilipenand Pentalgin.

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

7

RX

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

Rx FY2013 sales demonstrated 15% growth and reached RUR6 776m, 25% exluding Biolek.Key growth drivers were Phosphogliv, Combilipen and Pentalgin.

Rx segment growth (excl. Biolek)(mln RUR)

5 896

5 265

6 776 6 553

Rx Rx excl. Biolek

2012

2013

15% 25%

Phosphoglive14%

Combilipen7%

Biosulin6%

Octolipen3%

Pentalgin3%

Other67%

Rx segment - key product sales

Third Party Products. Close-up.

2012 2013

9

Source: Company data

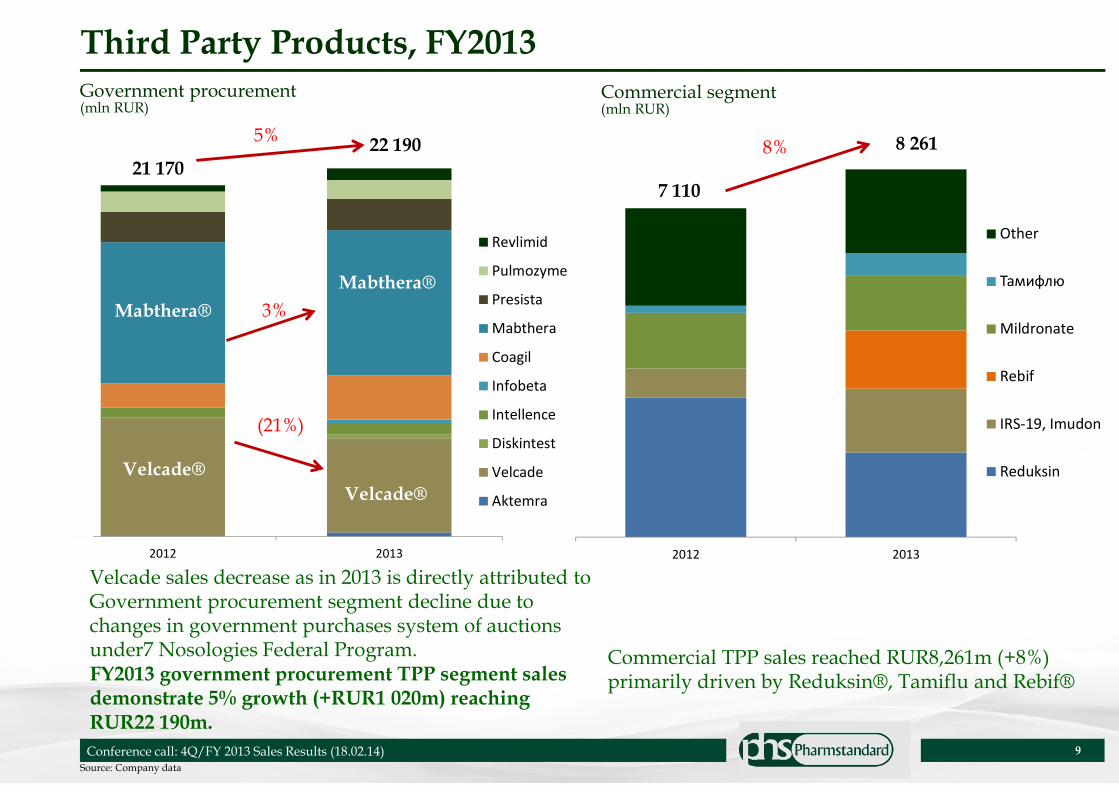

Third Party Products, FY2013

Government procurement(mln RUR)

Commercial segment (mln RUR)

Commercial TPP sales reached RUR8,261m (+8%)primarily driven by Reduksin®, Tamiflu and Rebif®

Velcade sales decrease as in 2013 is directly attributed toGovernment procurement segment decline due tochanges in government purchases system of auctionsunder7 Nosologies Federal Program.FY2013 government procurement TPP segment salesdemonstrate 5% growth (+RUR1 020m) reachingRUR22 190m.

8%

7 110

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

Revlimid

Pulmozyme

Presista

Mabthera

Coagil

Infobeta

Intellence

Diskintest

Velcade

Aktemra

2012 2013

(21%)

22 190

21 170

Velcade®

Mabthera®

Mabthera®

Velcade®

5%

3%

Other

Тамифлю

Mildronate

Rebif

IRS-19, Imudon

Reduksin

8 261

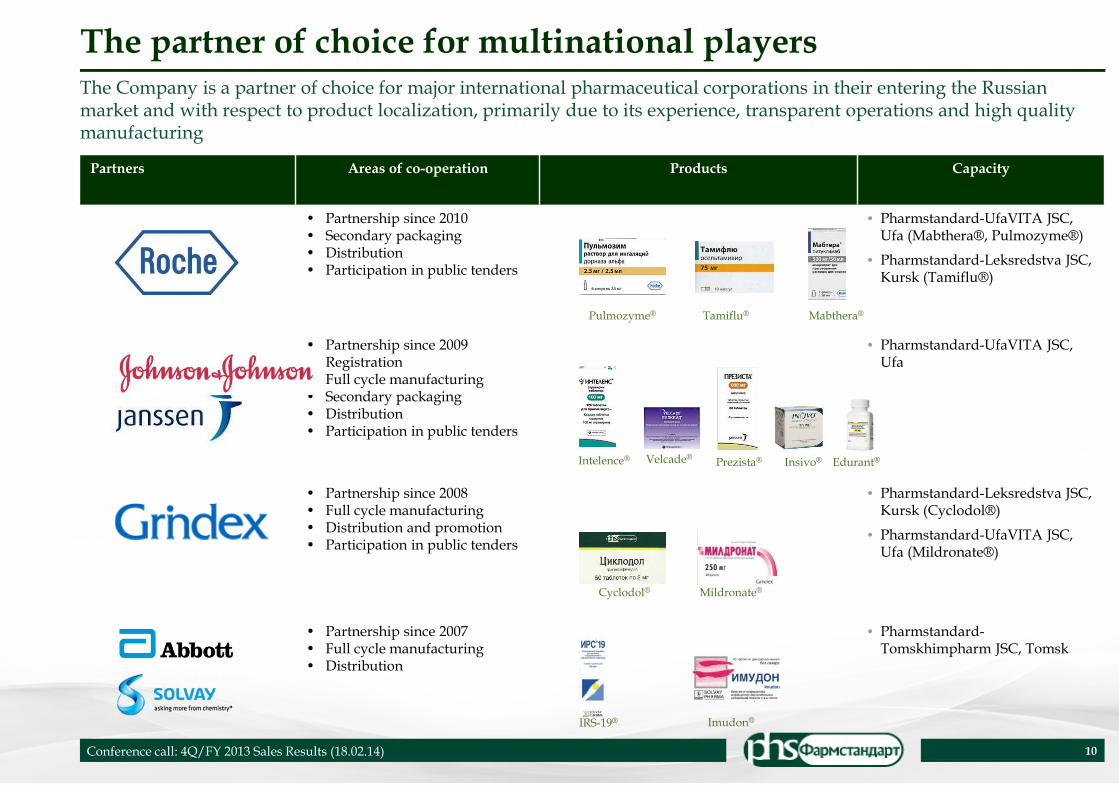

The partner of choice for multinational players

10

The Company is a partner of choice for major international pharmaceutical corporations in their entering the Russian market and with respect to product localization, primarily due to its experience, transparent operations and high quality manufacturing

Partners Areas of co-operation Products Capacity

• Partnership since 2010• Secondary packaging• Distribution• Participation in public tenders

• Pharmstandard-UfaVITA JSC, Ufa (Mabthera®, Pulmozyme®)

• Pharmstandard-Leksredstva JSC,Kursk (Tamiflu®)

• Partnership since 2009• Registration• Full cycle manufacturing• Secondary packaging• Distribution• Participation in public tenders

• Pharmstandard-UfaVITA JSC, Ufa

• Partnership since 2008• Full cycle manufacturing• Distribution and promotion• Participation in public tenders

• Pharmstandard-Leksredstva JSC, Kursk (Cyclodol®)

• Pharmstandard-UfaVITA JSC, Ufa (Mildronate®)

• Partnership since 2007• Full cycle manufacturing• Distribution

• Pharmstandard-Tomskhimpharm JSC, Tomsk

Pulmozyme® Tamiflu® Mabthera®

Intelence® Velcade® Prezista®

Cyclodol® Mildronate®

IRS-19® Imudon®

Insivo® Edurant®

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

11

FY2013 Sales Structure

Pharmaceutical products

98.1%

OTC 70.8%

TPP

54.4%

Rx29.2%

Medical equipment

1.9%

Organic sales

41.5%

API

2.1%

Therapeutic focus:• Analgesics• Cough & cold • Vitamins • Anti-viral • Anti-fungal

Product portfolio includes:• Coronary Therapy• Acid pump inhibitors• Nitrites & nitrates• ACE inhibitors• Alimentary tract

metabolism

Product portfolio includes:• Mabtera®• Velcade®• Pulmozyme®• IRS-19® & Imudon®• Coagil VII• Presista®• Mildronate®• Other

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

OTCPharm. Introduction.

Olga Mednikova

Overview of Branded OTC Spin-Off Structure

13

Current Structure

Pharmaceutical Products

Medical Equipment

Other

Rx OTCActive

PharmaceuticalIngredients

Third Party Products

Branded OTCNon-branded

OTC

Own Products

OTCPharm

Branded OTC Post Spin-Off

• 27 brands / 114 SKUs

• Key therapeutic categories

– Anti-cold and flu

– Non-narcotics and antipyretics

– Multivitamins with minerals

• 2012 sales volume: 153m packs

• 2012 net revenue: RUR12.7bn

• 2012 operating income: RUR4.5bn

• Supported by fully fledged marketing

Infrastructure

• Contract manufacturing with Pharmstandard

• Other contracts as necessary for operations

• FY2013 sales demonstrated 11% growth and

reached RUR14 bn y/y

2012 net revenue: RUR51.4bn2012 EBITDA: RUR13.5bn

25% of Pharmstandard 2012 net revenue

33% of Pharmstandard 2012 profitability

2012 net revenue: RUR50.1bn

2012 EBITDA: RUR13.2bn

2012 net revenue: RUR12.7bn

2012 EBITDA:RUR4.5bn

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

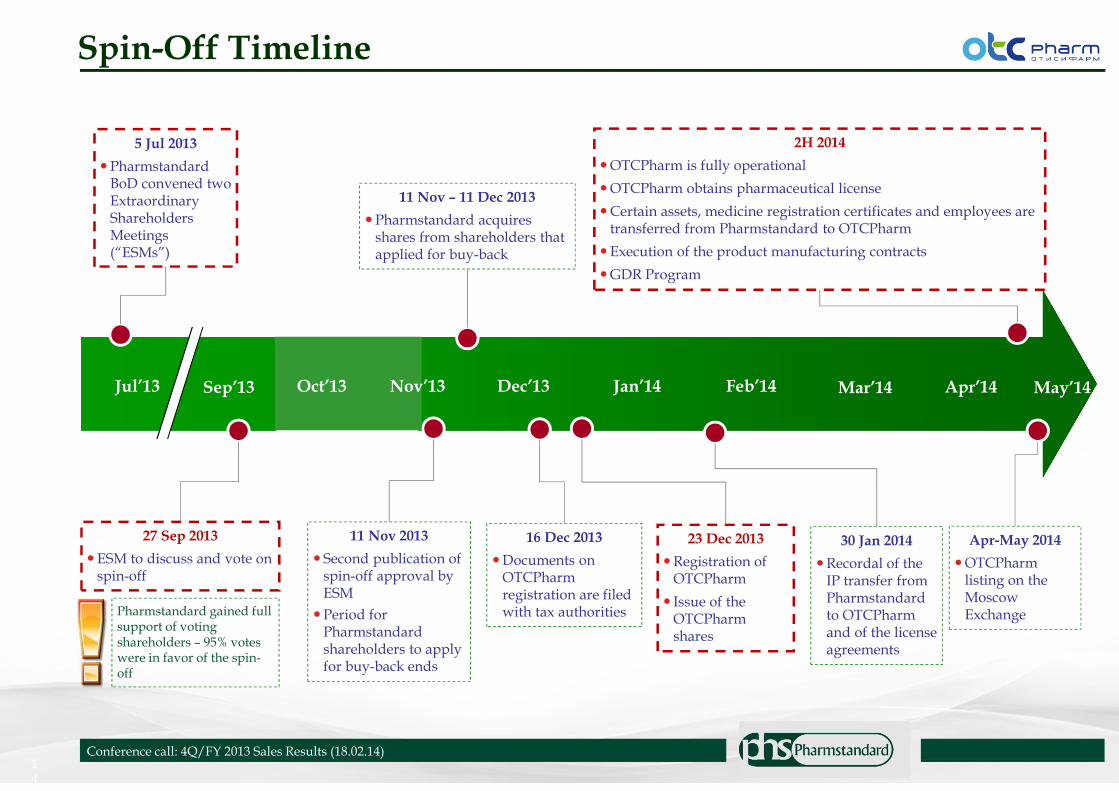

Spin-Off Timeline

14

27 Sep 2013

�ESM to discuss and vote on spin-off

Jul’13 Dec’13 Jan’14 Feb’14

11 Nov 2013

� Second publication of spin-off approval by ESM

�Period for Pharmstandard shareholders to apply for buy-back ends

11 Nov – 11 Dec 2013

�Pharmstandard acquires shares from shareholders that applied for buy-back

16 Dec 2013

�Documents on OTCPharmregistration are filed with tax authorities

23 Dec 2013

�Registration of OTCPharm

� Issue of the OTCPharmshares

30 Jan 2014

�Recordal of the IP transfer from Pharmstandard to OTCPharmand of the license agreements

2H 2014

�OTCPharm is fully operational

�OTCPharm obtains pharmaceutical license

�Certain assets, medicine registration certificates and employees are transferred from Pharmstandard to OTCPharm

�Execution of the product manufacturing contracts

�GDR Program

Sep’13

5 Jul 2013

�Pharmstandard BoD convened two Extraordinary Shareholders Meetings (“ESMs”)

Pharmstandard gained full support of voting shareholders – 95% votes were in favor of the spin-off

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

Oct’13 Nov’13 Mar’14 Apr’14

Apr-May 2014

�OTCPharmlisting on the Moscow Exchange

May’14

OTC54%

RX46%

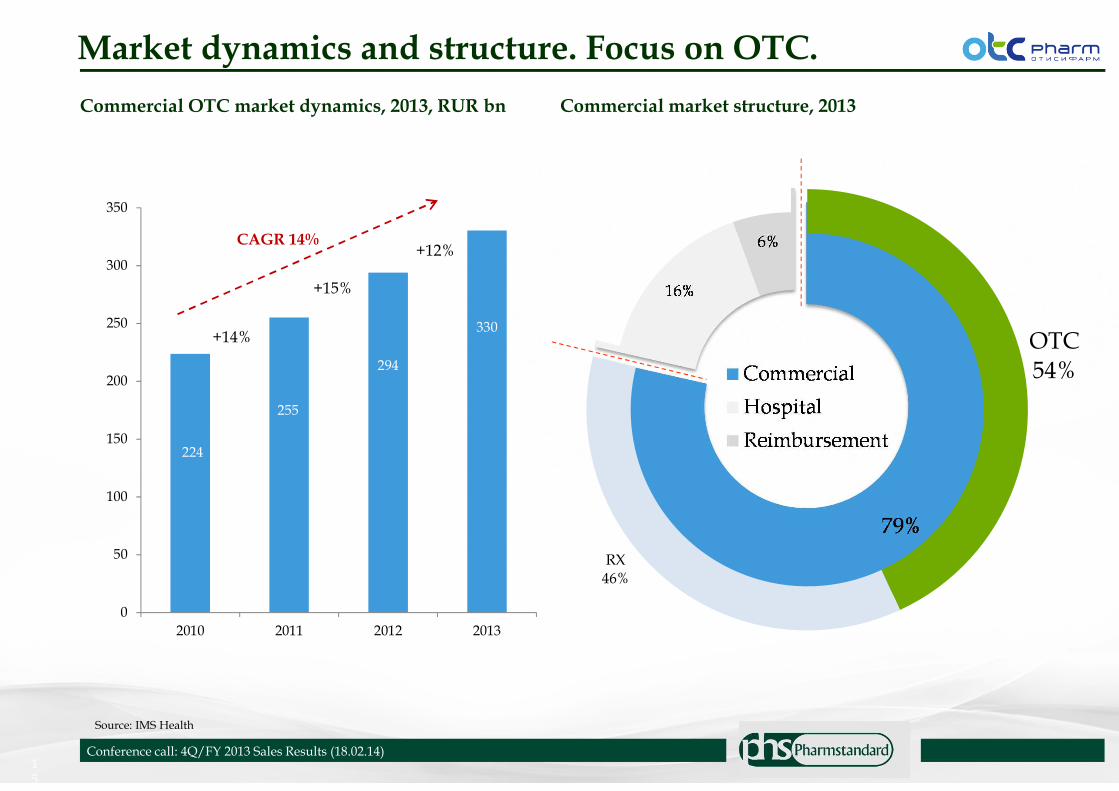

Market dynamics and structure. Focus on OTC.

15

Commercial market structure, 2013

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

224

255

294

330

0

50

100

150

200

250

300

350

2010 2011 2012 2013

Commercial OTC market dynamics, 2013, RUR bn

+14%

+15%

+12%CAGR 14%

Source: IMS Health

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

EVALAR

NYCOMED/TAKEDA

JOHNSON & JOHNSON*

TEVA*

MENARINI

STADA*

BAYER HEALTHCARE

SANOFI-AVENTIS

OTCPHARM

NOVARTIS/SANDOZ GROUP

Market Share 2013

Market Share 2012

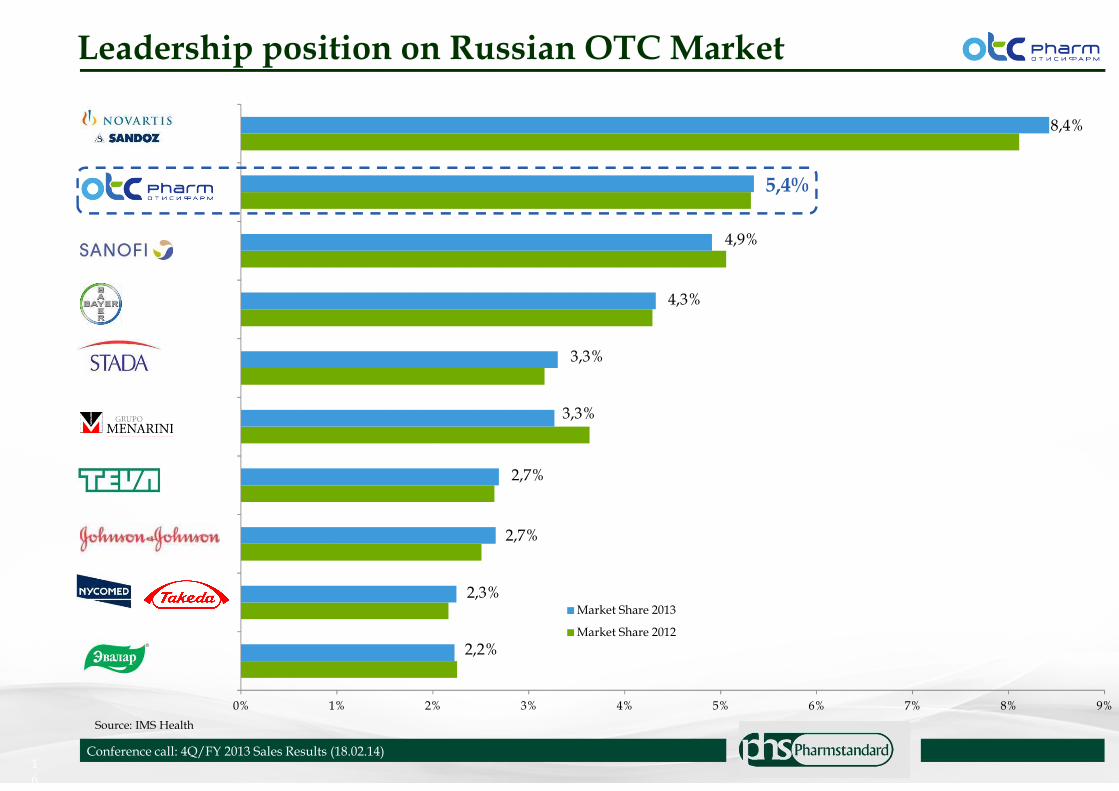

Leadership position on Russian OTC Market

16

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

8,4%

5,4%

4,9%

4,3%

3,3%

3,3%

2,7%

2,7%

2,3%

2,2%

Source: IMS Health

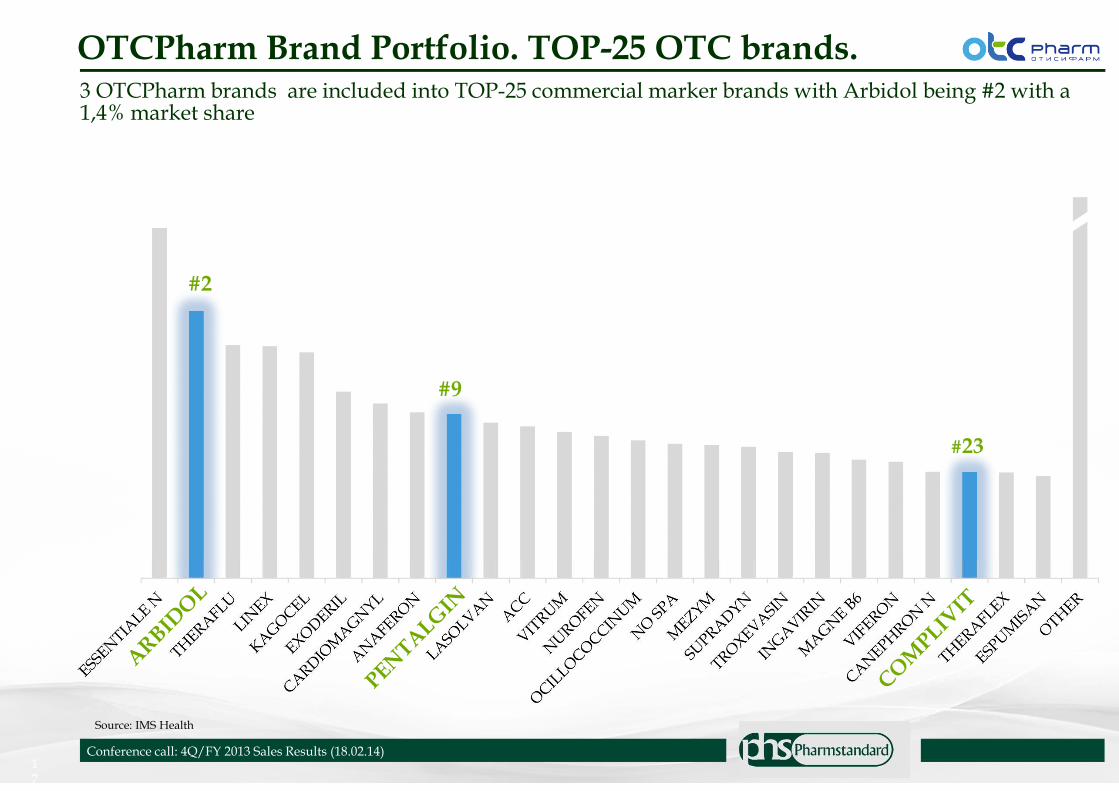

OTCPharm Brand Portfolio. TOP-25 OTC brands.

17

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

#2

#9

#23

3 OTCPharm brands are included into TOP-25 commercial marker brands with Arbidol being #2 with a 1,4% market share

Source: IMS Health

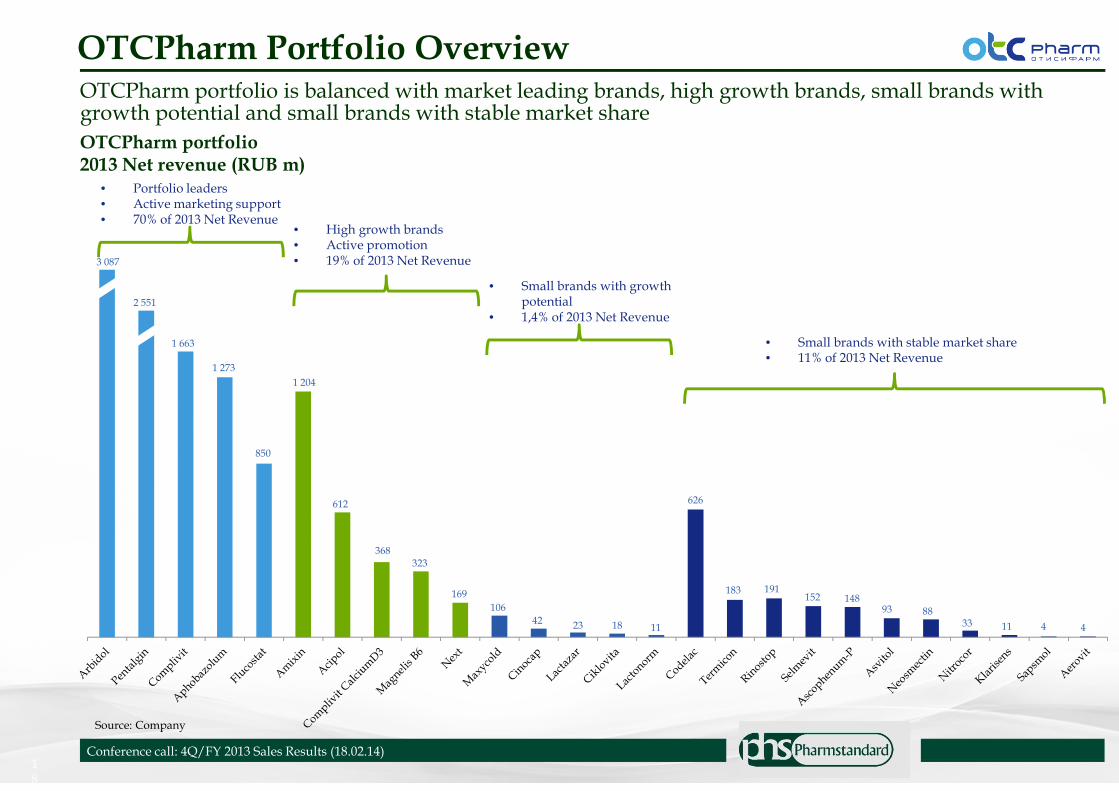

OTCPharm Portfolio Overview

18

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

Source: Company

OTCPharm portfolio is balanced with market leading brands, high growth brands, small brands with growth potential and small brands with stable market share

OTCPharm portfolio2013 Net revenue (RUB m)

• Portfolio leaders• Active marketing support• 70% of 2013 Net Revenue

• High growth brands• Active promotion• 19% of 2013 Net Revenue

• Small brands with growth potential

• 1,4% of 2013 Net Revenue

• Small brands with stable market share• 11% of 2013 Net Revenue

3 087

2 551

1 663

1 273

850

1 204

612

368323

169

106

42 23 18 11

626

183 191152 148

93 8833 11 4 4

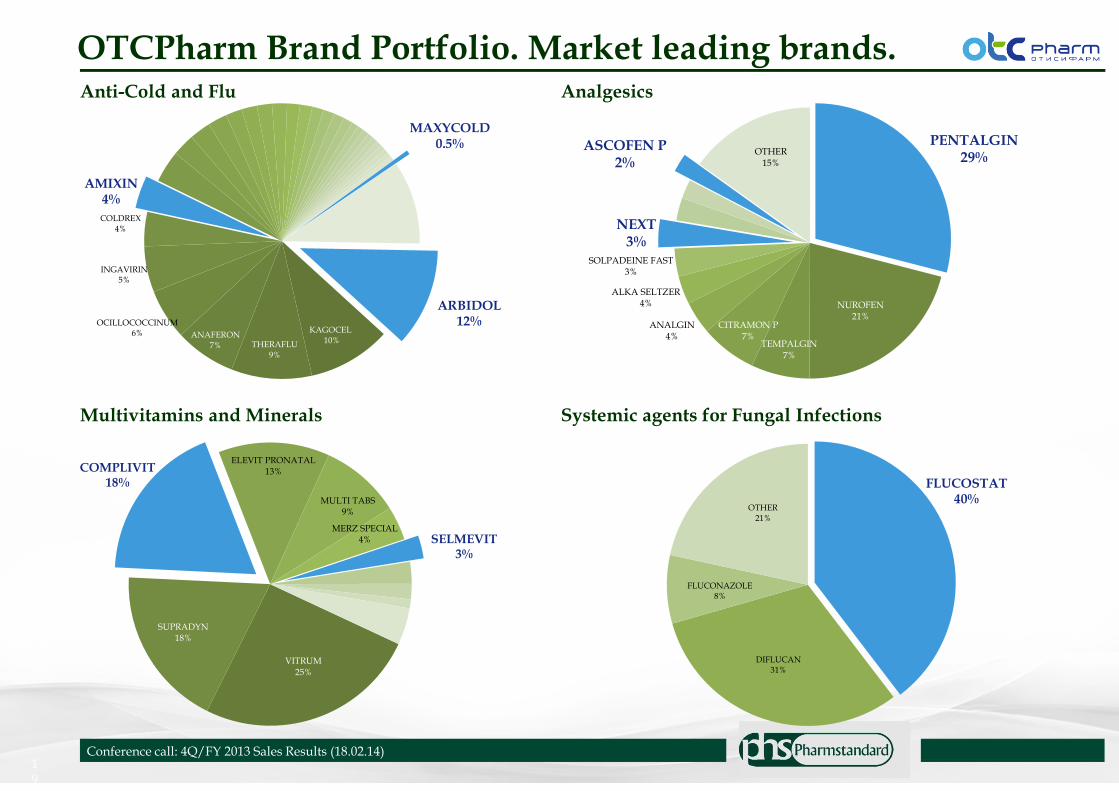

OTCPharm Brand Portfolio. Market leading brands.

19

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

Anti-Cold and Flu Analgesics

Multivitamins and Minerals Systemic agents for Fungal Infections

ARBIDOL 12%

KAGOCEL10%THERAFLU

9%

ANAFERON7%

OCILLOCOCCINUM6%

INGAVIRIN5%

COLDREX4%

AMIXIN4%

MAXYCOLD0.5%

VITRUM

25%

SUPRADYN18%

COMPLIVIT18%

ELEVIT PRONATAL13%

MULTI TABS9%

MERZ SPECIAL4% SELMEVIT

3%

PENTALGIN29%

NUROFEN21%

TEMPALGIN7%

CITRAMON P7%

ANALGIN4%

ALKA SELTZER4%

SOLPADEINE FAST3%

NEXT3%

ASCOFEN P2%

OTHER15%

FLUCOSTAT40%

DIFLUCAN31%

FLUCONAZOLE8%

OTHER21%

CALCIUM D3NYCOMED

CALCEMIN COMPLIVITCALC.D3

2012

2013

+8%

COMPLIVITCALCIUM D3

MAGNE B6 MAGNEROT MAGNELIS B6

2012

2013

+31%

MAGNELIS B6

OTCPharm Brand Portfolio. High growth brands.

20

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

Antidiarrheal microorganisms

Multivitamins and MineralsTranquillisers, Hypnotic/Sedatives

Mineral Supplements

Source: IMS Health

APHOBAZOL CORVALOL NOVO PASSIT PERSEN VALOCORDIN

2012

2013+31%

APHOBAZOLUM

2012

2013

LINEX BIFIFORM HYLAK FORTE ACIPOL BIFIDUMBACTERIN

2012

2013

+32%

ACIPOL

2012

2013

Category growth – 8%

Category growth – 9% Category growth – 16%

Category growth – 5%

OTCPharm FY 2013 revenue breakdown

21

Arbidol3 807

Pentalgin2 251

Complivit1 663

Aphobazolum1 273

Amixin1 204

Flucostat850

Codelac 626

Acipol 612

Magnelis B6 323 Rinostop 191

TOP-10 largest OTCPharm products comprise 91% of 2013 Net Revenue

TOP-10RUR12.8bn

OTHERRUR1.2bn

TOTALRUR14bn

Appendix I. Top Brands.

INNOVATIONS. AFFORDABILITY. QUALITY

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

23

Source: Company data

FY2013 / 4Q2013 Best Selling BrandsFY2013 FY2013 FY2012

BrandVolume

(mln packs)Sales

(RURm)% of total

salesVolume

(mln packs)Sales

(RURm)% of total

salesChange

(mln RUR) %

Arbidol 19,108 3 807,0 16,4% 24,974 3 975,1 19,1% - 168,0 -4,2%

Pentalgin 29,419 2 251,0 9,7% 36,995 2 418,0 11,6% - 167,0 -6,9%

Complivit 16,830 1 663,6 7,2% 17,091 1 605,4 7,7% 58,2 3,6%

Phosphoglive 3,352 1 372,8 5,9% 3,077 1 161,6 5,6% 211,2 18,2%

Aphobazolum 7,021 1 273,1 5,5% 5,727 872,2 4,2% 400,9 46,0%

Amixin 2,594 1 203,6 5,2% 1,888 851,3 4,1% 352,4 41,4%

Flukostat 6,490 849,6 3,7% 6,316 772,6 3,7% 76,9 10,0%

Combilipen 6,263 687,6 3,0% 5,054 534,1 2,6% 153,5 28,7%

Codelac 7,628 625,8 2,7% 6,780 549,0 2,6% 76,8 14,0%

Acipol 3,573 612,1 2,6% 2,590 390,3 1,9% 221,8 56,8%

TOP 10 total 102,279 14 346,2 62% 110,492 13 129,5 63% 1 217 9%

Other brands 483,278 8 887,4 38% 442,035 7 645,4 37% 1 242 16%

TOTAL SALES 585,558 23 233,6 100% 553,668 20 774,9 100% 2 459 12%

4Q2013 4Q2013 4Q2012

BrandVolume

(mln packs)Sales

(mln RUR)% of total

salesVolume

(mln packs)Sales

(mln RUR)% of total

salesChange

(mln RUR) %

Arbidol 3,980 769,4 11,4% 9,215 1 435,0 20,6% - 665,6 -46,4%

Pentalgin 8,580 632,7 9,3% 8,297 573,7 8,2% 59,0 10,3%

Complivit 5,997 577,7 8,5% 7,159 666,8 9,6% - 89,2 -13,4%

Phosphoglive 1,443 561,9 8,3% 1,185 443,7 6,4% 118,1 26,6%

Aphobazolum 2,507 454,3 6,7% 1,927 281,2 4,0% 173,1 61,6%

Acipol 2,386 409,6 6,0% 1,775 266,0 3,8% 143,5 54,0%

Amixin 0,612 281,9 4,2% 0,588 265,5 3,8% 16,4 6,2%

Combilipen 2,321 256,8 3,8% 1,668 182,1 2,6% 74,7 41,0%

Flukostat 1,483 211,1 3,1% 1,720 211,1 3,0% 0,0 0,0%

Codelac 2,358 196,6 2,9% 2,256 178,0 2,6% 18,6 10,4%

TOP 10 total 31,667 4 351,9 64% 35,791 4 503,1 65% - 151 -3%

Other brands 142,163 2 419,0 36% 124,642 2 469,9 35% - 51 -2%

TOTAL SALES 173,830 6 770,9 100% 160,433 6 973,1 100% - 202 -3%

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

24

Source: Company data

FY/4Q2013 TOP-10 OTC BrandsFY2013 FY2013 FY2012

BrandVolume

(mln packs)Sales

(mln RUR)% of total

salesVolume

(mln packs)Sales

(mln RUR)% of total

salesChange

(mln RUR) %

Arbidol 19,108 3 807,0 23,1% 24,974 3 975,1 26,7% - 168,0 -4,2%

Pentalgin 24,094 1 927,3 11,7% 32,789 2 205,4 14,8% - 278,1 -12,6%

Complivit 16,830 1 663,6 10,1% 17,091 1 605,4 10,8% 58,2 3,6%

Aphobazolum 7,021 1 273,1 7,7% 5,727 872,2 5,9% 400,9 46,0%

Amixin 2,318 1 106,4 6,7% 1,712 791,7 5,3% 314,8 39,8%

Flukostat 6,486 849,0 5,2% 6,272 765,2 5,1% 83,9 11,0%

Acipol 3,573 612,1 3,7% 2,590 390,3 2,6% 221,8 56,8%

Codelac 6,741 532,7 3,2% 5,997 476,8 3,2% 55,9 11,7%

Ingalypt 7,847 488,4 3,0% 7,526 328,8 2,2% 159,6 48,5%

Corvalol 48,895 350,4 2,1% 42,456 298,2 2,0% 52,2 17,5%

TOP 10 total 142,915 12 610,1 77% 147,135 11 709,1 79% 901 8%

Other brands 375,713 3 847,7 23% 319,836 3 170,2 21% 678 21%

TOTAL SALES 518,628 16 457,8 100% 466,970 14 879,3 100% 1 579 11%

4Q2013 4Q2013 4Q2012

BrandVolume

(mln packs)Sales

(mln RUR)% of total

salesVolume

(mln packs)Sales

(mln RUR)% of total

salesChange

(mln RUR) %

Arbidol 3,980 769,4 17,0% 9,215 1 435,0 30,4% - 665,6 -46,4%

Pentalgin 5,997 577,7 12,7% 7,159 666,8 14,1% - 89,2 -13,4%

Complivit 6,569 526,7 11,6% 6,606 493,9 10,5% 32,8 6,6%

Aphobazolum 2,507 454,3 10,0% 1,927 281,2 6,0% 173,1 61,6%

Amixin 0,547 226,2 5,0% 0,537 247,8 5,2% - 21,6 -8,7%

Flukostat 1,483 211,1 4,7% 1,708 209,0 4,4% 2,1 1,0%

Acipol 1,188 202,6 4,5% 0,815 124,3 2,6% 78,3 63,0%

Codelac 2,068 165,9 3,7% 1,927 146,5 3,1% 19,5 13,3%

Ingalypt 2,576 155,0 3,4% 7,526 328,8 7,0% - 173,8 -52,9%

Corvalol 15,466 110,0 2,4% 10,904 74,9 1,6% 35,1 46,9%

TOP 10 total 42,382 3 399,0 75% 48,323 4 008,2 85% - 609 -15%

Other brands 114,183 1 138,8 25% 81,741 712,8 15% 426 60%

TOTAL SALES 156,565 4 537,7 100% 130,064 4 721,0 100% - 183 -4%

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

25

Source: Company data

FY2013 / 4Q2013 TOP-10 Rx BrandsFY2013 FY2013 FY2012

BrandVolume

(mln packs)Sales

(mln RUR)% of total

salesVolume

(mln packs)Sales

(mln RUR)% of total

salesChange

(mln RUR) %

Phosphoglive 3,352 1 372,8 20,3% 3,077 1 161,6 19,7% 211,2 18,2%

Combilipen 6,263 687,6 10,1% 5,054 534,1 9,1% 153,5 28,7%

Biosulin 0,900 597,6 8,8% 0,894 519,3 8,8% 78,3 15,1%

Octolipen 1,432 330,2 4,9% 1,324 278,4 4,7% 51,8 18,6%

Pentalgin 5,325 323,8 4,8% 4,205 212,6 3,6% 111,1 52,3%

Rastan 0,153 270,2 4,0% 0,089 279,3 4,7%- 9,0 -3,2%

Terpincodum 1,314 225,6 3,3% 0,934 150,5 2,6% 75,1 49,9%

Formetine 2,060 226,7 3,3% 1,192 124,7 2,1% 102,0 81,8%

Artrosan 1,351 215,2 3,2% 0,898 136,8 2,3% 78,4 57,4%

Picamilon 4,689 208,8 3,1% 4,121 175,7 3,0% 33,0 18,8%

TOP 10 total 26,839 4 458,4 66% 21,788 3 572,9 61% 885 25%

Other brands 40,091 2 317,4 34% 43,383 2 322,8 39% - 5 0%

TOTAL SALES 66,930 6 775,8 100% 86,698 5 895,7 100% 880 15%

4Q2013 4Q2013 4Q2012

BrandVolume

(mln packs)Sales

(mln RUR)% of total

salesVolume

(mln packs)Sales

(mln RUR)% of total

salesChange

(mln RUR) %

Phosphoglive 1,461 655,0 29,3% 1,185 443,7 19,7% 211,2 47,6%

Combilipen 2,321 256,8 11,5% 1,668 182,1 8,1% 74,7 41,0%

Rastan 0,115 191,7 8,6% 0,062 216,0 9,6%- 24,3 -11,3%

Biosulin 0,230 158,1 7,1% 0,258 151,1 6,7% 7,0 4,6%

Octolipen 0,497 120,0 5,4% 0,396 83,6 3,7% 36,4 43,6%

Pentalgin 2,010 106,0 4,7% 1,691 79,8 3,5% 26,2 32,8%

Artrosan 0,511 82,5 3,7% 0,296 47,4 2,1% 35,2 74,3%

Picamilon 1,620 73,0 3,3% 1,175 51,1 2,3% 21,9 42,9%

Terpincodum 0,376 64,9 2,9% 0,934 150,5 6,7%- 85,5 -56,9%

Formetine 0,490 58,5 2,6% 1,192 124,7 5,5%- 66,2 -53,1%

TOP 10 total 9,631 1 766,5 79% 8,859 1 530,0 68% 236 15%

Other brands 7,635 466,6 21% 21,510 722,0 32% - 255 -35%

TOTAL SALES 17,266 2 233,2 100% 30,369 2 252,0 100% - 19 -1%

Conference call: 4Q/FY 2013 Sales Results (18.02.14)

26

Disclaimer and Confidentiality RequirementsThis presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of anoffer to buy or acquire securities of Pharmstandard JSC (the “Company”) or any of its affiliates in any jurisdiction or an inducementto enter into investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied onin connection with, any contract or commitment or investment decision whatsoever.

This presentation may contain 'forward-looking statements'. These statements may include the words "anticipate", "believe","intend", "estimate", "expect" and words of similar meaning. All statements other than statements of historical facts, possiblycontained in this presentation, including, without limitation, those regarding the Company’s financial position, business strategy,plans and objectives of management for future operations (including development plans and objectives relating to the Company'sprojects and services) are forward-looking statements. Such forward-looking statements involve known and unknown risks,uncertainties and other important factors that could cause the actual results, performance or achievements of the Company to bematerially different from results, performance or achievements expressed or implied by such forward-looking statements. Risks anduncertainties include, without limitation, general industry conditions and competition; economic conditions, such as interest rateand currency exchange rate fluctuations; technological advances and patents attained by competitors; challenges inherent in newproduct development, including obtaining regulatory approvals; domestic and foreign health care reforms and governmental lawsand regulations; and trends toward health care cost containment. Such forward-looking statements are based on numerousassumptions regarding the Company's present and future business strategies and the environment in which the Company willoperate in the future. These forward-looking statements speak only as at the date of this presentation.

The Company does not undertake to update any forward-looking statements as a result of new information or future events ordevelopments.

The Company will use reasonable efforts to include up-to-date and accurate information in this Internet site, but make norepresentations, warranties, or assurances as to the accuracy, currency, or completeness of the information provided. The Companyshall not be liable for any damages or injury resulting from your access to, or inability to access, this Internet site, or from yourreliance on any information provided at this Internet site.

The information and opinions contained in this document are provided as at the date of this presentation and are subject to changewithout notice.

All information, unless expressly specified herein, is from Company data.

1H2013 Sales Results (25.07.13)

Related Documents