1 LESSON 1 INTRODUCTION TO ACCOUNTING STRUCTURE: 1.1 Introduction 1.2 Objectives of Accounting 1.3 Uses of Accounting Information 1.4 Principles of Accounting 1.4.1 Accounting Concepts 1.4.2 Accounting Conventions 1.5 Some Important Terms used in Book – Keeping 1.6 Summary 1.7 Key Words 1.1 INTRODUCTION: Accounting can be defined as, `an art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events which are, in part at least of a financial character, and interpreting the result thereof.” Accounting, which involves recording, classifying and summarizing the transactions of financial nature in order to compute the results and financial position of the business. Accounting facilitates external reporting to the owners or shareholders, potential investors, trade creditors, creditors for expenses, banks and financial institutions, management and employees, society, Income-tax department, academicians, and other interested parties. As this branch of accounting is based OBJECTIVES: To explain the meanings and importance of accounting To know the utility of accounting information to various stakeholders To know the principles which guide the preparation and reporting of accounting statements To familiarize with the frequently used words in accounting

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

LESSON 1

INTRODUCTION TO ACCOUNTING

STRUCTURE: 1.1 Introduction

1.2 Objectives of Accounting

1.3 Uses of Accounting Information

1.4 Principles of Accounting

1.4.1 Accounting Concepts

1.4.2 Accounting Conventions

1.5 Some Important Terms used in Book – Keeping

1.6 Summary

1.7 Key Words

1.1 INTRODUCTION:

Accounting can be defined as, `an art of recording, classifying and summarizing in a

significant manner and in terms of money, transactions and events which are, in part at least

of a financial character, and interpreting the result thereof.” Accounting, which involves

recording, classifying and summarizing the transactions of financial nature in order to

compute the results and financial position of the business. Accounting facilitates external

reporting to the owners or shareholders, potential investors, trade creditors, creditors for

expenses, banks and financial institutions, management and employees, society, Income-tax

department, academicians, and other interested parties. As this branch of accounting is based

OBJECTIVES: To explain the meanings and importance of accounting To know the utility of accounting information to various stakeholders To know the principles which guide the preparation and reporting of accounting

statements To familiarize with the frequently used words in accounting

2

on historical or past data, it is described as the post-mortem of financial transactions. In

Financial Accounting all the transactions of financial nature are recorded in a book called

Journal in chronological order or in order of their occurrence, then classified in another book

called Ledger and finally summarized into a schedule called Trial Balance, from which an

Income statement is prepared to know the results of the transactions of financial nature in a

business firm as on a particular date and the same are analyzed with the help of the tools of

financial analysis, such as, comparative and common size financial statements, trend analysis,

Ratio analysis, fund flow analysis and cash flow analysis. These days, Double Entry System

of Accounting is followed by every Corporate and also most businesses which are organized

in forms other than Corporate. Hence the subsequent discussion in this chapter and latter

chapters would be on Double Entry System of Book Keeping.

1.2 OBJECTIVES OF ACCOUNTING:

Accounts are maintained

1. To have a permanent record of all mercantile transactions.

2. To maintain records of incomes, expenses and losses in such a way that the net profit or

net loss for any selected period may be readily ascertained.

3. To keep records of assets and liabilities in such a way that the financial position of the

undertaking at any point of time may be readily ascertained.

4. To enable the review and revision of policies in the light of past experience brought to

light by analyzing and interpreting records and reports.

1.3 USERS OF ACCOUNTING INFORMATION:

The importance of accounting is to provide meaningful information about a business enterprise

to those persons who are directly or indirectly interested in the performance and financial

position of business enterprise. Such persons may include owners, creditors, investors,

employees, government, public, research scholars and the managers.

3

1. Owners:

The owners of a business furnish capital to be used for the purpose of business. They are

interested to know whether the business has earned a profit or loss during a particular period

and also its financial position on a particular date. They want accounting reports in order to

have an appraisal of past performance and also for an assessment of future prospects.

2. Creditors:

The creditors include suppliers of goods and services, bankers and other lenders of money.

They are interested in the financial stability of the concern before making loans or granting

credit. They look to the ability of the business to pay interest and principal as and when it

becomes due for payment. They also look to the trends of earnings as it ultimately affects the

solvency of a concern.

3. Investors:

Investors look not only the earning capacity of business but also its financial strength and

solvency before deciding whether to subscribe or not for the shares in a Company. They are

interested in steady and good return on their capital, the safety of their capital and appreciation

in the value of the shares.

4. Employees:

Employees are interested in earning capacity of a concern as their salaries, bonus and pension

schemes are dependent on this factor. They have a permanent stake in the business and in order

to have an assurance of steady employment they are very much interested in the stability of the

organization.

5. Government:

Government is interested in accounting statements and reports in order to see the performance

of a particular unit, its cost structure and income in order to impose tax and excise duty.

4

6. Public:

The public as consumers is interested in accounting statements in order to know whether control

is exercised on production, selling and distribution expenses in order to reduce the prices of

goods they buy. They can also judge whether the economic resources of the concern are being

utilized for the benefit of the common man or not.

7. Research Scholars:

Such persons are interested in accounting statements and reports in order to get data for proving

their thesis on which they are working and hence to complete their research projects.

8. Managers:

The managers of an enterprise need accounting information for planning, control, evaluation of

performance and decision-making. Their main responsibility is to operate the business so as to

obtain maximum return on capital employed without causing any detriment to the interest of the

stakeholders.

1.4 PRINCIPLES OF ACCOUNTING:

Accounting is a system evolved to achieve a set of objectives. The objective being able to

communicate accounting information, to its users. In order to achieve the goals, we need a set

of rules or guidelines. These guidelines are termed here as Basic Accounting Principles.

In order to ensure authenticity, and comparability in the matter of recording and interpretation

of Accounts, Accounting Principles are followed. These Principles can be divided into

Concepts and Conventions. The following few paragraphs deal with these concepts and

conventions.

1.4.1 ACCOUNTING CONCEPTS:

5

The term `concepts’ includes those basic assumptions or conditions upon which the science of

accounting is based. The following are the important accounting concepts. The term Concept

means an idea or thought. Basic Accounting Concepts are the fundamental ideas or basic

assumptions underlying the theory and practice of financial accounting.

1. Separate Entity Concept:

Business is treated separate from the proprietor. All the transactions are recorded in the books

of business and not in the books of the proprietor. The proprietor is treated as a creditor for the

business. When he contributes capital he is treated as person who has invested his amount in

the business. Therefore, capital appears in the liabilities of balance sheet of the Organisation.

The concept of separate entity is applicable to all forms of business organizations. For

example, in case of a partnership business or sole proprietorship business, though the partners

or sole proprietor are not considered as separate entities in the eyes of law, but for accounting

purposes they will be considered as separate entities. The major effects of this concept are

that:

a) Financial position of the business can be easily found out.

b) Earning capacity of business can be easily ascertained.

c) The personal affairs of the owners are not mixed up with that of the business

2. Going Concern Concept:

The assumption is that business will continue to exist for unlimited period of time. There is

neither the intention nor the necessity to liquidate the particular business venture in the

foreseeable future. On account of this concept, the accountant while valuing the assets does not

take into account sale value of assets. Moreover, he charges depreciation on fixed assets on the

basis of their expected lives rather than on their market values.

3. Money Measurement Concept:

Only those transactions are recorded in accounting which can be expressed in terms of money.

Measurement of business in terms of money helps in understanding the state of affairs of the

business in a much better way. For example if a business owns Rs.10,000 of cash, certain

6

quantity of raw materials, two factories, 1,000 square feet of building space etc. These amounts

cannot be added together to produce a meaningful total of what the business owns. However, if

these items are expressed in monetary terms such as Rs.10,000 of cash, Rs.12,000 of raw

materials, Rs.2,00,000 of factories, and Rs.50,000 of building, all such items can be added and

much more intelligible and precise estimate about the assets of the business will be available.

The transactions which cannot be expressed in monetary terms fall beyond the scope of

accounting. This is also a limitation of accounting. For example, if a business has got a team of

dedicated and trusted employees, it is definitely an asset to the business but since their monetary

measurement is not possible, they are not shown in the books of the business

4. Cost Concept:

According to this concept, an asset is recorded at its cost in the books of account, i.e., the price

which is paid at the time of acquiring it. This concept is mainly applicable for fixed assets.

Current assets are not affected by it. Cost concept has the advantage of bringing objectivity in

the preparation and presentation of financial statements. In the absence of this concept the

figures shown in the accounting records would have depended on the subjective views of a

person. However, on account of continued inflationary tendencies the preparation of financial

statements on the basis of historical costs, creates problems of credibility in judging the

financial position of the business. This is the reason for the growing importance of inflation

accounting.

5. Accounting period Concept:

According to this concept, the life of the business is divided into appropriate time periods for

studying the results shown by the business after each segment. This is because though the life

of the business is considered to be indefinite (according to going concern concept), the

measurement of income and studying the financial position of the business after a very long

period would not be helpful in taking proper corrective steps at the appropriate time. It is

therefore, absolutely necessary that after each segment or time interval the businessman must

7

`stop and `see back’, how things are going. In accounting such a time period or time is called

`accounting period’. It is usually one year.

Every business wants to know the result of his investment and efforts after a certain period.

Usually one-year period is regarded as an ideal for this purpose; it may be 6 months or 2 years

also. This concept helps financial position and earning capacity of one year may be compared

with another year and also in planning and increasing the efficiency of business.

6. Dual Aspect Concept:

This is the basic concept of accounting. According to this concept every business transaction

has a dual effect. The two fold aspects are Receiving of benefit and Giving of equivalent

benefit. For example, if A starts a business with a capital of Rs.10,000. There are two aspects

of the transaction. On the one hand the business has asset of Rs.10,000 while on the other hand

the business owes to the proprietor a sum of Rs.10,000 which is taken as proprietor’s capital.

This expression can be shown in the form of following equation:

Capital (Equities) = Cash (Assets)

10,000 = 10,000

The term `assets denotes the resources owned by a business while the term “Equities” denotes

the claims of various parties against the assets, Equities are of two types. They are owners’

equity and outsiders’ equity. Owners’ equity (or capital) is the claim of owners against the

assets of the business while outsiders’ equity (or liabilities) is the claim of outside parties such

as creditors, debenture-holders against the assets of the business. Since all assets of the

business are claimed by someone (either owners outsiders), the total of assets will be equal to

total of liabilities, thus:

Equities = Assets

OR

Liabilities + Capital = Assets

In the example given above, if the business purchases furniture worth Rs.5,000 out of the

money provided by A, the situation will be as follows:

8

Equities =Assets

Capital Rs.10,000 = Cash Rs.5,000 + Furniture Rs.5,000

Subsequently if the business borrows Rs.30,000 from a bank, the new position would be as

follows:

Equities = Assets

Capital Rs.10,000 + Bank Loan Rs.30,000 = Cash 35,000 + Furniture Rs.5,000.

The term `accounting equation’ is also used to denote the relationship of equities to assets.

The equation can be technically stated as “for every debit, there is an equivalent credit”. As a

matter of fact the entire system of double entry book-keeping is based on this concept.

7. Matching Concept:

Every businessman is eager to make maximum profit at minimum cost. Hence, he tries to find

out revenue and cost during the accounting period. In order to ascertain the profit made by the

business during a period, it is necessary that `revenues’ of the period should be matched with

the costs (expenses) of the period. The term `matching’ means appropriate association of

related revenues and expenses. In other words, surplus made by the business during a period

can be measured only when the revenue earned during a period is compared with the

expenditure incurred for earning the revenue. On account of this concept, adjustments are made

for all outstanding expenses, accrued incomes, prepaid expenses and unearned incomes, etc.,

while preparing the final accounts at the end of the accounting period.

8. Realization Concept:

According to this concept revenue is recognized when a sale is made. Sale is considered to be

made at the point when the property in goods passes to the buyer and he becomes legally liable

to pay and not when the actual payment is made. For example, A places an order with B for

supply of certain goods yet to be manufactured. On receipt of order, B purchases raw materials,

employs workers, produces the goods and delivers them to A. A makes payment on receipt of

9

goods. In this case the sale will be presumed to have been made not at the time of receipt of the

cash for the goods but at the time when goods are delivered to A.

9. Accounting Equivalence Concept:

The proprietor provides funds for acquisition of assets. Hence the assets owned by the business

must be equal to the funds provided by the proprietor. Funds provided by the proprietor are

called equity. Hence accounting equivalence concept is:

Assets = Equities

In addition to own funds, money is borrowed which is known as liability. Therefore assets are

acquired through equity and liability. Therefore, accounting equation is:

Assets = Owner’s Equity + liabilities

10. Objective Evidence Concept:

This concept relates with the verification of accounting record with Objective evidence.

Objective evidence means study of those documents and vouchers on the basis of which

accounting record has been made. This helps a lot in auditing of accounts and Account remains

free from error and fraud due to existence of vouchers, documents etc.

1.4.2 ACCOUNTING CONVENTIONS:

The term `convention’ includes those customs or traditions which guide the accountant while

preparing the accounting statements. The following are the important accounting conventions:

Convention of Consistency

Convention of Conservatism.

Convention of Full Disclosure.

10

Convention of Materiality.

1. Convention of Consistency:

Continuance of same practice for number of years indicates consistency. Whatever accounting

practice has been adopted in one year, the same should be continued in future years also. If

depreciation is charged on fixed assets according to diminishing balance method, it should be

done year after year. This is necessary for the purposes of comparison. However, consistency

does not mean inflexibility. It does not forbid introduction of improved accounting techniques.

If better method is found, it must be followed, but a note for making a change must be in the

accounts. The biggest advantage of this convention is that it facilitates comparison of one

year’s accounts with other years.

2. Convention of Conservation:

Future is uncertain. Though projections may be made about future events, no one can forecast

future with perfect certainty in business. Therefore some arrangement or provision is made to

meet future uncertainties. Every sincere businessman makes an estimate of future losses and

then some provision for it e.g., provision for bad debts is made. However, businessmen mostly

ignore the items of future profits. This tendency is termed as conservatism. Therefore, the

common accounting practices are:

o Do not consider any income or gain till the same is realized in cash.

o Create or make a provision for future expected losses and contingencies on the

basis of past experience.

The convention of conservatism has become target of serious criticism these days especially on

the ground that it goes against the convention of full disclosure. It also gives room to the

accountant to create secrete reserves (e.g. by creating excess provision for bad and doubtful

11

debts, depreciation etc.), and the financial statements do not depict a true and fair view of state

of affairs of the business.

3.Convention of Full Disclosure:

Accounting records and statements should be honest and materially informative, Exclusion of

material facts makes them incomplete and unreliable. This convention is gaining more

importance because most of big businesses are run in the form of joint stock companies where

ownership is divorced from management. The Companies Act, 1956, not only requires that

Income Statement and Balance Sheet of a company must give a true and fair view of the state of

affairs of the company but it also gives the prescribed forms in which these statements are to be

prepared. The practice of appending notes to the accounting statements (such as about

contingent liabilities or market value of investments) is pursuant to the convention of full

disclosure. This is done to benefit the proprietor and all those outsiders who are interested in

assessing the efficiency of financial position of the business unit.

4.Convention of Materiality:

Materiality means relative importance. Whether a matter should be disclosed or not in the

financial statements depends on its materiality, i.e., whether it is material or not. According to

this convention accounting record should be made of all material facts. Immaterial items may

either be clubbed with material items and then recorded or these may be ignored. For example

purchase of a waste paper basket, might amount to purchase of a capital asset, since this lasts

for more than a year, but by virtue of the amount involved, it is better treated as revenue

expenditure. Thus, the term `materiality’ is a subjective term. The accountant should regard an

item as material if there is reason to believe that knowledge of it would influence the decision

of the informed investor.

12

1.5 SOME IMPORTANT TERMS USED IN BOOK – KEEPING: Before you get into the

specifics of Accounting, you should be familiar with some of the terms which are generally

used in Accounting. A few of them are given below:

Business Transactions: Any exchange of money or money’s worth is called business

transaction. Events like purchase and sale of goods, receipts and payments of cash for

services or on personal accounts are the examples of transactions. When payment for

business activity is made immediately, it is called cash transaction, but when the

payment is postponed to a future date, it is called a credit transaction.

Debtor: A debtor is a person who owes something to the business

Creditor: A creditor is a person to whom something is owing, by the business.

Debit and Credit: To debit an account means to enter the transaction on the debit side

of that account. To credit an account means to enter the transaction on the credit side

of that account.

Capital: It is the amount invested by the proprietor in the business. For the business,

capital is a liability towards the owner. Sometimes it is called `owner’s equity’ i.e.

owners claim against the assets. Owner’s equity or capital is always equal to assets

minus liabilities.

Drawing: It is the value of cash or goods withdrawn from the business by the owner

for his personal use.

Goods: It includes all commodities or articles in which a trader deals.

13

Assets: These are the material things or possessions or properties of the business

including the amounts due to it. Examples are Cash and Bank balances, Land and

Building, Plant and Machinery etc.

Liabilities: The term liabilities denote the amounts which the business owes to others

such as loan from bank, creditors for goods supplied, for outstanding expenses etc.

Accounts: An account is a summary of the record of all the transactions relating to a

person, asset, expense or gain. It has two sides-the left hand side called the debit side

and the right hand side called the credit side.

Accounts are of three types Personal, Real and Nominal accounts:

Personal Accounts:

These are the accounts of natural persons (such as Ram”s accounts, Gopal’s account)

artificial persons (such as Uday Ltd., Syndicate Bank’,) and representative personal

account (such as Prepaid Insurance account, outstanding salary account) with whom

the trader deals)

Real Accounts:

Accounts relating to properties or assets of a trader are known as real accounts. It

includes tangible assets such as building, furniture, cash etc., and also intangible

assets such as goodwill, trade marks, patent rights

Nominal Accounts:

Accounts dealing with expenses, losses, gains and incomes are called Nominal

Accounts, e.g. salaries account, wages account, commission account etc.

Real and Nominal Accounts are also called Impersonal accounts because they

do not affect any particular person but affect business in general.

1.6 SUMMARY:

14

Accounting can be defined as, `an art of recording, classifying and summarizing in a significant

manner and in terms of money, transactions and events which are, in part at least of a financial

character, and interpreting the result thereof.” Accounting is a system evolved to achieve a set

of objectives. The objective is to communicate accounting information to its users. In order to

achieve the goals, we need a set of rules or guidelines. These guidelines are termed here as

Accounting Principles. The importance of accounting is to provide meaningful information

about a business enterprise to those persons who are directly or indirectly interested in the

performance and financial position of business enterprise. Such persons may include owners,

creditors, investors, employees, government, public, research scholars and the managers.

1.7 KEY WORDS:

Double Entry System of Book Keeping Separate Entity Concept

Going Concern Concept Money Measurement Concept

Cost Concept Accounting period Concept

Dual Aspect Concept Matching Concept

Realization Concept Accounting Equivalence Concept

Objective Evidence Concept Convention of Consistency

Convention of Conservatism. Convention of Full Disclosure.

Convention of Materiality.

Try yourself:

1. Explain the principles of Accounting.

2. Discuss important Accounting Concepts

3. Explain the significance of Accounting conventions.

4. Who are the users of Accounting information?

FURTHER READINGS:

Jain S.P. and Narang, K.L., .Advanced Accountancy, Kalyani Publishers

Mukherjee & Khan, Modern Accountancy, Tata Mcgraw Hill

15

LESSON 2 ACCOUNTING CYCLE - I

STRUCTURE

STRUCTURE:

STRUCTURE: 2.1 Introduction

2.2 Journal

2.3 Ledger

2.4 Subsidiary Books- Division Of Journal

2.5 Trial Balance

2.6 Accounting Cycle

2.7 Summary

2.8 Key Words

2.1 INTRODUCTION:

As discussed in the first chapter, businesses aim at earning profit. Entities which do not have

profit earning as an objective also aim to be financially viable. Therefore, earning a profit or

being viable is an important objective which is pursued by all organizations. However, it is

not possible to ascertain whether operations have been viable or not, unless a proper record of

all the transactions is kept in a systematic way.

OBJECTIVES:

Explain importance of Journal, be able to record transactions in the journal

Know the importance of Ledger, be able to do the ledger posting, and Balance the accounts

Describe the importance and utility of Subsidiary books. Prepare the trial balance

16

Maintaining such a systematic record of all transaction is called book-keeping and when such

record-keeping moves on to classifying and summarizing, preparation of final reports and

interpretation, we call it accounting.

In India, Accounting had been practised as far back as Mauryan Dynasty times which we can

see from Kautilya’s Artha Shastra. However, the present day accounting has its origins in

Luco Pacioli’s Double Entry System of Accounting. In this chapter, we shall learn to

journalise, and post it into the ledger. The two steps mark the beginning of the Accounting

cycle.

2.2 JOURNAL :

Journal is the book wherein a business transaction is first written or recorded and therefore it

is also known as book of Original Entry. In the French language Jour means day. Journal

therefore is a book where day to day transactions are written. Journal is written

chronologically i.e., it is written date wise, for example; transaction relating January 1 are first

written followed by January 2, January 3 and so on. Journal has columns for Date,

Particulars, Ledger Folio, Debit and Credit. The format is as follows:

Date Particulars LF Debit Amount Credit Amount

1999 Jan 1

1999 Jan 2

1999 Jan 3

In the date column, date of the transaction is recorded, in the particulars column details

relating to the accounts affecting the transaction are recorded. Both the debit and credit

aspects of the transaction are recorded. The Amounts column relating to the debit and credit

are placed side by side. Each transaction entered in the Journal is known as Journal Entry and

the act of entering or writing the transaction in the Journal is known as journalizing. A

Journal Entry is written in a specific form in which account relating to debit is written in the

17

first line and Account relating to Credit is written in the second line. While writing the

second line a little space is left and then written as given under.

Date Particulars LF Debit Amount Credit Amount

Ravi’s A/c Dr. 5000

To Cash 5000

Each Journal entry is followed by a narration given in brackets. Narration is the explanation

about the journal entry. For E.g.:

Date Particulars LF Debit Amount Credit Amount Ravi’s A/c Dr.

To Cash

(Paid Cash to Ravi)

5000 5000

While Journalizing the transaction the rules of journalizing need to be followed. The rules of

journalising accounts are as follows:

Personal Accounts (A/cs relating to persons

Debit the Receiver Credit the giver

Real Accounts (A/cs relating to assets)

Debit what comes in Credit what goes out

Nominal Accounts (A/cs relating to expenses, losses, income and gains)

Debit all expenses and losses

Credit all incomes and gains

STEPS TO BE FOLLOWED:

1) Identify the accounts being affected in the transaction.

2) Categorize them into real, nominal and personal

3) Apply the relevant rules of debit and credit

18

However, in order to journalize it is very important that you should be to identify and classify

the accounts into proper categories. You should know the category into which a particular

account falls. For example you should know whether Capital Account is a personal account,

nominal account or a real account, only then you can apply the rule related to that category.

Consider, Cash since it is a real account you should apply the rules relating to real account.

And again take Rent since we know that it is a nominal account rules of debit and credit

relating to nominal accounts need to be applied while journalising the transactions. Personal

Accounts relate to Accounts relating to persons. Persons could mean individuals, business

organization, a sole proprietary concern, partnership firm, and so on. It could be a bank, an

educational, institution, a hospital or any institution. The term person includes a natural

person as well as an artificial person.

Real accounts relate to assets. They could be land, building, motor car, machinery, furniture,

cash, goodwill, patents and so on. Assets could be Tangible or intangible. Examples of

intangible assets could be good will, patents, trade and so on.

Nominal accounts relate to expenses, losses, incomes and gains. For eg: Rent, Interest, Salary.

Having understood the meaning of a journal, the rules of journalizing, the style of writing a

journal entry, the format of a journal, the various type of accounts, we shall now try to enter or

write sample business transactions into a Journal.

January 1, 2005 – Ravi Started business with Cash Rs.50000

In this business transaction it is obvious that Cash A/c is affected. We see that Cash is being

brought into the business. So the first account that is affected is Cash and the other is the

Personal A/c of the owner which is called as Capital.

Now since Cash is a real account the rules of debit and credit relating to Real accounts need to

be applied. And the rule is debit what comes in and credit what goes out. We see here that

cash is coming into the business and so we need to debit the Cash A/c.

19

The other account affected is the Capital A/c. Capital being a personal account, the rule of

personal a/cs need to be applied. And the rule is debit the receiver and credit the giver. Here

the owner of the business is supplying or giving capital to the business. It may be noted that

business unit is separate from the owner. Therefore we credit the capital a/c of the owner. So

the journal entry will be written thus:

Date Particulars LF Debit Amount Credit Amount Jan 1, 2005 Cash A/c Dr.

To Capital A/c (Being Capital brought in)

50000 50000

If the name is not given it may be written as Cash A/c Dr. To Capital Account.

January 2, 2005 – Bought Furniture Rs.2000

In this transaction you see that one of the accounts is Furniture, the other being Cash. How do

you know that Cash is the other account. It is because you cannot buy anything without

paying. If you have bought furniture it means that you have paid for it. Suppose you feel that

it could be a credit transaction. Then it may be remembered that if it were a credit

transaction, the name of the concern, selling on credit would be given. Since it is not given

we may safely assume that the two accounts affected in this transaction are Furniture A/c and

Cash A/c.

Analysis: After identifying that the two accounts Furniture and Cash are Real accounts

apply the rules of real accounts. Furniture is coming into the organization, debit it. Credit the

cash a/c since it is going out of the organization.

Date Particulars LF Debit Amount Credit AmountJan 2,2005 Furniture A/c Dr.

To Cash A/c (Being Furniture purchased)

2000 2000

20

January 3, 2005 Rent paid Rs. 1000

The accounts affected here are Rent and Cash. While Rent is a nominal account (since it is an

expenditure) Cash is a real A/c. Treat Rent as per nominal account rule. Debit all expenses,

rent should therefore be debited. As per Real A/c Rules Credit what goes out, therefore credit

cash account.

Date Particulars LF Debit Amount Credit AmountJan 3, 2005 Rent A/c Dr.

To Cash A/c (Being the rent paid)

1000 1000

It may be noted here, that to whom the Rent is paid is not so important when Cash has

changed hands.

Now having understood the procedure of writing business transactions in a Journal, it is now

the time to get thorough with it. Therefore the following illustrations:

(1) Brought into business Cash Rs.50000, Land Rs.100000, building Rs.250000,

Furniture Rs.20000, Machinery Rs.200000

Date Particulars LF Debit Amount Credit AmountFeb 1, 2005 Cash A/c Dr. 50000 Land A/c Dr. 100000 Building A/c Dr. 250000 Furniture A/c Dr. 20000 Machinery A/c Dr. 200000 To Capital A/c 620000 (Being Capital Brought in)

It may be noted that in Double Entry System of book-keeping, Debit = Credit therefore sum

of all debits (6,20,000) should be equal to a single credit in the above transactions.

Incidentally it may be noted that an entry where there are more than one debit or one credit it

is called combined or a composite entry.

21

(2) Purchases Rs.30000

Date Particulars LF Debit Amount Credit AmountFeb 2, 2005 Purchases A/c Dr.

To Cash A/c (Being purchases made or goods purchases)

30000 30000

When goods are purchased they may also be referred to as purchases. That is the reason we

have debited it as purchases rather than as goods.

(3) Purchases from Mohan Raj Rs.45,000

Date Particulars LF Debit Amount Credit AmountFeb 3, 2005 Purchases A/c Dr.

To Mohan Raj A/c (Purchases on credit from Mohan Raj)

45000 45000

Note: It may be noted here that while in the previous entry Cash has been credited, here

Mohan Raj’s name has been credited. That’s because it is a credit transaction (so understood

because the name of the person has been given). In this case cash has not gone out Mohan

Raj’s A/c is a personal account and since Mohan Raj has given the goods and the rule is

credit the giver therefore his name has been credited.

(4) Purchases from Mohan Raj for Cash Rs.35000

Date Particulars LF Debit Amount Credit AmountFeb 4, 2005 Purchases A/c Dr.

To Cash A/c (Being the purchases made on Cash)

35000 35000

Note: How does one know that it is a Cash transaction because it so mentioned. Although

the name of the person transacting is given it is clearly mentioned that it is a Cash transaction

and so Mohan Raj’s name recedes into the background. It is not to be recorded.

22

(5) Sales Rs. 25000

Date Particulars LF Debit Amount Credit AmountFeb 5, 2005 Cash A/c Dr.

To Sales A/c (Being Cash Sales made)

25000 25000

(6) Sale made to Ravi Rs.15000

Date Particulars LF Debit Amount Credit AmountFeb 5, 2005 Ravi’s A/c Dr.

To Sales A/c (Being Sales made on Credit to Ravi)

15000 15000

(7) Sale made to Ravi Rs.20000 for Cash

Date Particulars LF Debit Amount Credit AmountFeb 6, 2005 Cash A/c Dr.

To Sales A/c (Being Cash Sales made to Ravi for Cash)

20000 20000

(8) Machinery purchased Rs.60000

Date Particulars LF Debit Amount Credit AmountFeb 7, 2005 Machinery A/c Dr.

To Cash A/c (Being Machinery Purchased)

60000 60000

It may be noted here that debit is given to machinery and although it is a purchase, purchases

a/c is not debited; because the name of the asset that is machinery is specified and it is to be

differentiated from “Purchases” or “Goods” meant for resale.

23

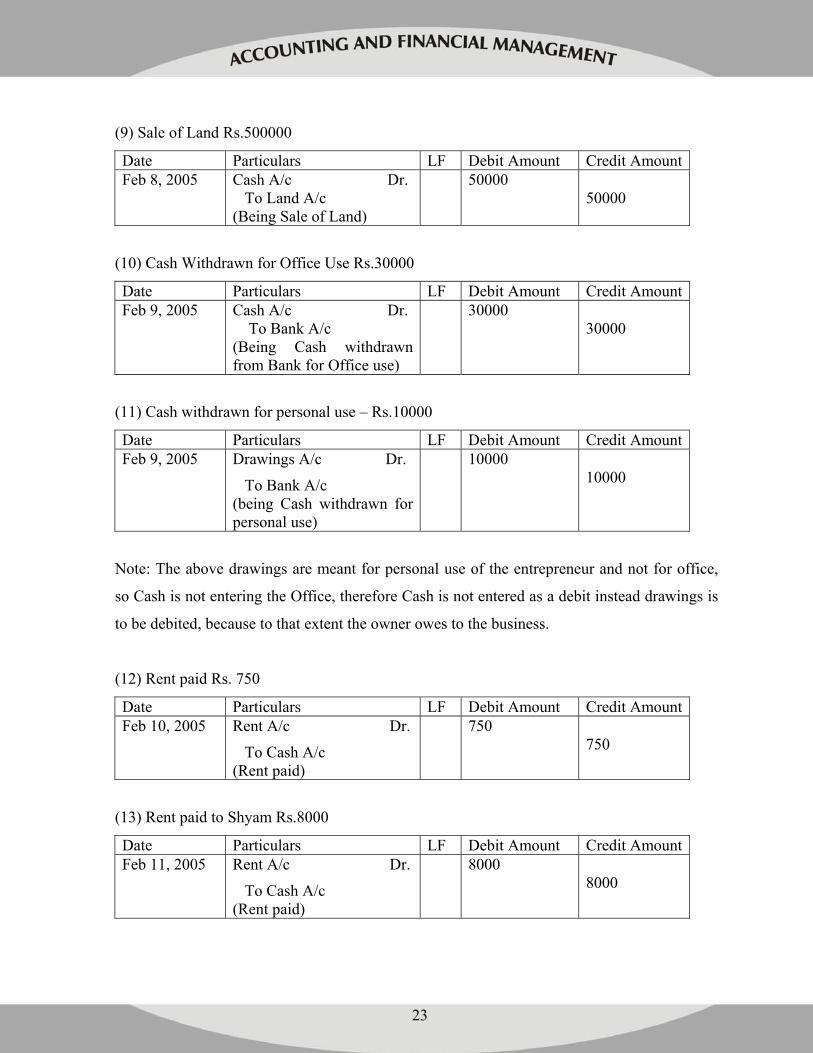

(9) Sale of Land Rs.500000

Date Particulars LF Debit Amount Credit AmountFeb 8, 2005 Cash A/c Dr.

To Land A/c (Being Sale of Land)

50000 50000

(10) Cash Withdrawn for Office Use Rs.30000

Date Particulars LF Debit Amount Credit AmountFeb 9, 2005 Cash A/c Dr.

To Bank A/c (Being Cash withdrawn from Bank for Office use)

30000 30000

(11) Cash withdrawn for personal use – Rs.10000

Date Particulars LF Debit Amount Credit AmountFeb 9, 2005 Drawings A/c Dr.

To Bank A/c (being Cash withdrawn for personal use)

10000 10000

Note: The above drawings are meant for personal use of the entrepreneur and not for office,

so Cash is not entering the Office, therefore Cash is not entered as a debit instead drawings is

to be debited, because to that extent the owner owes to the business.

(12) Rent paid Rs. 750

Date Particulars LF Debit Amount Credit AmountFeb 10, 2005 Rent A/c Dr.

To Cash A/c (Rent paid)

750 750

(13) Rent paid to Shyam Rs.8000

Date Particulars LF Debit Amount Credit AmountFeb 11, 2005 Rent A/c Dr.

To Cash A/c (Rent paid)

8000 8000

24

In the above transaction although name is given since Rent A/c is more important, which is an

expense; therefore rent is debited.

(14) Interest Received Rs.2000

Date Particulars LF Debit Amount Credit AmountFeb 11, 2005 Cash A/c Dr.

To Interest A/c (Being Interest Received)

2000 2000

(15) Commission Received Rs. 1500

Date Particulars LF Debit Amount Credit AmountFeb 13, 2005 Cash A/c Dr.

To Commission A/c (Being Commission Received)

1500 1500

(16) Interest on Capital Rs.800

Date Particulars LF Debit Amount Credit AmountFeb 15, 2005 Interest on Capital A/c Dr.

To Cash A/c (Being Interest paid on Capital)

800 800

2.3 LEDGER:

Ledger is a book where account wise information is documented. While the Journal gives data

in chronological form, the ledger gives account wise information. All the transactions related

to a particular account are put at one place. For e.g., if you would like to know the

transactions you carried out with your customer Ravi you need not search throughout the

journal to trace out transactions relating to Ravi instead you go to ledger and locate Ravi’s

A/c thereon and find all the transactions relating to Ravi. It is more useful than the day to day

information provided in the journal. Ledger is the second stage in the Accounting cycle.

From the journal transfer is made into the ledger under various heads of account. This

process of transfer is known as Ledger posting.

25

HOW IS LEDGER POSTING DONE:

Various accounts which are found affected in the journal are opened in the ledger. An

account is in T form. On either side of the account debit and credit aspects are shown. The

name of the account is given on the top. The debit aspects relating to the account are recorded

on the left side, while Credit aspects are recorded on the right side as shown below:

Name of the Account

Debit side Credit side

On debit side, ‘To’ is used as a prefix of the account while on the credit side the word ‘By’ is

prefixed. A look at the Format shall further clarify this:

NAME OF THE ACCOUNT

Dr. Cr.

Date Particulars Dr. side

JF Amount Rs.

Date Particulars Cr. Side

JF Amount Rs.

To … Name of the A/C

By …… Name of the A/c

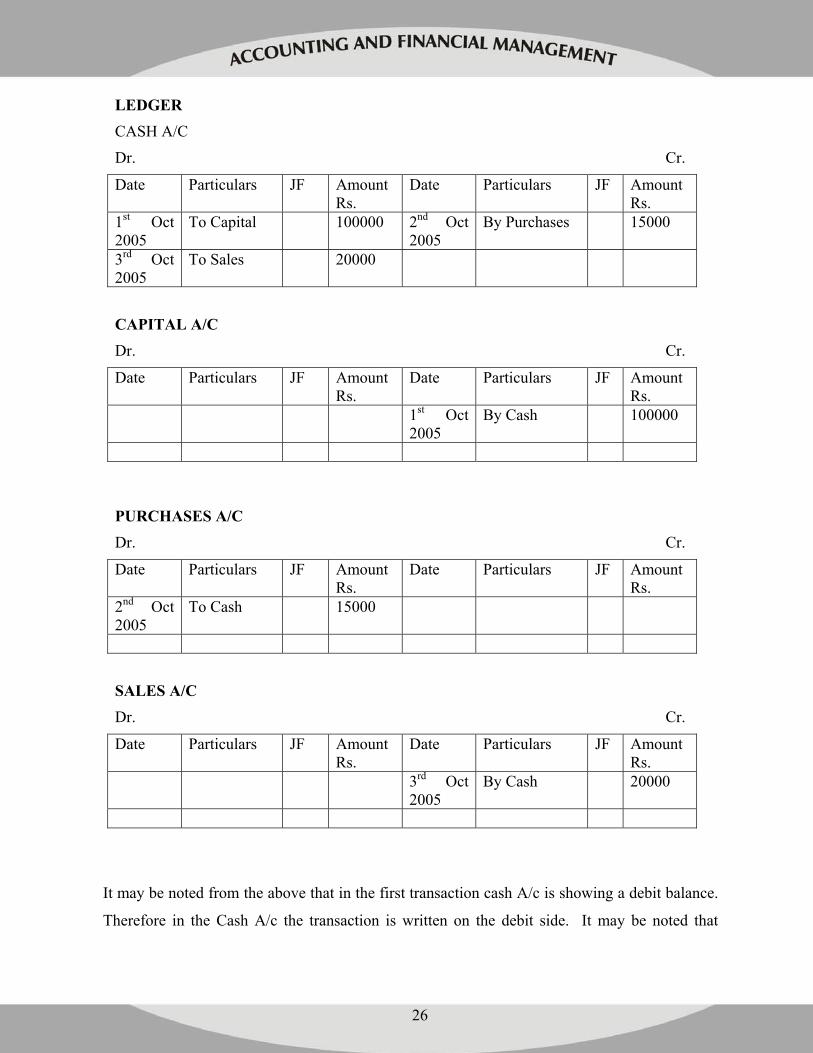

Now let us post some Journal entries into the ledger.

Example:1

JOURNAL

Date Particulars JF Amount Amount 1.10.2005 Cash A/c – Dr.

To Capital (Being capital brought in)

1,00,000=00 1,00,000=00

2.10.2005 Purchases A/c – Dr. To Cash (Being purchase made)

15,000=00 15,000=00

3.10.2005 Cash A/c – Dr. To Sales (Being Sales made)

20,000=00 20,000=00

Treatment:

26

LEDGER CASH A/C

Dr. Cr.

Date Particulars JF Amount Rs.

Date Particulars JF Amount Rs.

1st Oct 2005

To Capital 100000 2nd Oct 2005

By Purchases 15000

3rd Oct 2005

To Sales 20000

CAPITAL A/C Dr. Cr.

Date Particulars JF Amount Rs.

Date Particulars JF Amount Rs.

1st Oct 2005

By Cash 100000

PURCHASES A/C Dr. Cr.

Date Particulars JF Amount Rs.

Date Particulars JF Amount Rs.

2nd Oct 2005

To Cash 15000

SALES A/C

Dr. Cr.

Date Particulars JF Amount Rs.

Date Particulars JF Amount Rs.

3rd Oct 2005

By Cash 20000

It may be noted from the above that in the first transaction cash A/c is showing a debit balance.

Therefore in the Cash A/c the transaction is written on the debit side. It may be noted that

27

when the name of the account having the credit balance is written Viz: in the Cash A/c it is

written as To Capital Account. Whereas in the capital account which shows credit balance it is

written as By Cash A/c on the credit side.

In the second transaction purchases A/c is showing a debit balance and therefore in the

purchases A/c the transaction is written on the debit side as ‘To Cash A/c. Whereas in the

Cash A/c which is showing credit balance it is written as “By purchases”.

In the third transaction Cash A/c is showing a debit balance and therefore on the debit side of

the cash account it is written as ‘To Sales’, while in the Sales A/c it is recorded as ‘By Cash’.

From the above three transactions it is seen as to how ledger posting or transfer of transaction

is made from the journal to the ledger.

Example: 2

Journalise the following transactions and post them in the Ledger:

• Capital brought in Rs.50,000

• Purchases Rs.10,000

• Purchases from Ravi Rs.5,000

• Sales Rs. 8,000

• Sales to Mohan Rs.7,000

JOURNAL

Date Particulars LF Dr. Cr. Cash A/c – Dr.

To Capital A/c (Being Capital brought in)

50,000 50,000

Purchases A/c – Dr.

To Cash A/c

(Being purchases made for Cash)

10,000 10,000

28

Mohan A/c – Dr.

To Sales A/c

(Being Cash Sales made)

7,000 7,000

Cash A/c – Dr.

To Sales A/c

(Being Cash Sales made)

8,000 8,000

Purchases A/c – Dr.

To Ravi A/c

(Purchases made on Credit)

5,000 5,000

CASH A/C

Dr. Cr.

Date Particulars Amount Date Particulars Amount To Capital 50000 By Purchases 10000 To Sales 8000 By Balance C/d 48000 Total 58000 Total 58000

CAPITAL A/C

Dr. Cr.

Date Particulars Amount Date Particulars Amount To Balance C/d 50000 By Cash 50000 Total 50000 Total 50000

PURCHASES A/C

Dr. Cr.

Date Particulars Amount Date Particulars Amount To Cash 10000 By Balance c/d 15000 To Ravi 5000 Total 15000 Total 15000

29

SALES A/C

Dr. Cr.

Date Particulars Amount Date Particulars Amount To balance c/d 15000 By Cash 8000 By Mohan 7000 Total 15000 Total 15000

RAVI A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount To Balance c/d 5000 By Purchase 5000 Total 5000 Total 5000

MOHAN A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount To Sales 7000 By Balance c/d 7000 Total 7000 Total 7000 A brief explanation of how the above entries are posted in the ledger is given below:

In the first transaction we see that Cash A/c is showing a debit balance. Therefore in the Cash

A/c we write “To Capital A/c on the debit side. Capital A/c is showing a credit balance

therefore on the credit side of the capital a/c we write “By Cash”. Similarly in the second

transaction purchases a/c is showing a debit balance and so on the debit side of purchase a/c

we write To Cash and since cash a/c is showing credit balance we write “By purchases” in the

Cash A/c. The other transactions are also posted on the same lines.

In the above manner all the transactions in the journal are referred to and transactions relating

to a particular account are written under that particular head. After such posting is done the

debit and the credit side are totaled up separately to find out which side is heavier. If the debit

side of an account is more than that the credit side of that particular account it is said to

possess debit balance. If the credit side is heavier the account is said to have credit balance.

30

It is very important to know which side of the account is heavier, because it explains the

position of the account. For eg: Consider the following Cash A/c.

CASH A/C.

Dr Cr. Date Particulars Amount Date Particulars Amount

To Balance B/d 30000 By Purchases 10000

To Sales 15000 By Salaries 2000

To Ravi 8000 By Rent 3000

To Commission 3000 By Interest 5000

Total 56000 Total 20000

We see in the above account that the Debit side has total of Rs.56,000 whereas the credit side

has a total of Rs.20000. It is obvious that the debit side is heavier by Rs.36,000. Therefore it

is said that the Cash A/c has a debit balance, the balance being Rs.36000. Debit balance in

the Cash A/c (Rs.36000) implies that in the Cash A/c there is still a balance of Rs.36000 and

it is carried down (C/d) to the next period. That’s why it is written as By Balance C/d. In the

beginning of the next period it is written as to Balance B/d meaning to say that balance has

been brought down from the previous period. Suppose you are closing the account on 31st

January, the balance is carried down on that day and is shown as an opening balance in the

next period. Look at the account shown hereunder:

CASH A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount

To Balance B/d 30000 By Purchases 10000

Jan 2005 To Sales 15000 Jan 2005 By Salaries 2000

To Ravi 8000 By Rent 3000

To Commission 3000 By Interest 5000

31.1.05 By Balance C/d 36000

Total 56000 Total 56000

1.2.05 To Balance b/d 36000

31

What do Debit and Credit Balances mean:

1. If a personal account shows a debit balance it means that the person is a debtor which

means he has to pay money to the firm. If it shows a credit balance he has to receive

money from the firm.

2. If Real accounts show debit balance it means that the firm owns property or asset to

the extent of balance in the account

3. If a nominal account shows a debit balance it means than an expense or loss to that

extent has been incurred by the firm and vice versa.

Posting of a compound entry:

Consider the following Compound Entries and try to understand how these are posted.

Ex:1 Cash A/c – Dr. Rs.10000

Furniture A/c – Dr. Rs.40000

To Capital Account Rs.50000

(Being Capital brought in the form of Cash)

We see that there are two debits for one credit in such a case three accounts are opened. Cash

A/c, Furniture A/c and Capital A/c. Cash A/c shows a debit against the credit of capital

account. Furniture A/c also shown a debit against the credit of Capital A/c which shows a

Credit balance has two details: the Cash A/c and Furniture A/c. Therefore in the Cash A/c

since it is showing the debit balance, on the debit side of the Cash A/c it is written as “To

Capital”. In the Furniture A/c which is also showing debit balance it is written as To Capital

Rs.40000.

In the Capital A/c which has two debits it is written as By Cash Rs.10000 and By Furniture

Rs.40000. Please examine the following accounts.

32

CASH A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount To Capital 10000 By Purchases 10000

FURNITURE A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount

To Capital 40000 By Purchases 10000

CAPITAL A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount

By Cash 1000

By Furniture 40000

2.4 SUBSIDIARY BOOKS - DIVISION OF JOURNAL

Journal is the book of original entry or the main book where in business transactions are

entered in a chronological order. But when the transactions are too many, quick location of a

particular transaction may not be easily done. Therefore, Journal is divided into 8 parts or

eight subsidiary books viz:

1) Cash Book

2) Purchases Book

3) Sales Book

4) Purchase Returns

5) Sales Returns

6) Bills Receivable

7) Bills payable

8) Journal proper

33

Thus subsidiary books are parts or sub-divisions of a journal. The following paragraphs explain

more about the individual Subsidiary Books.

CASH BOOK

The Cash Book records transactions dealing with receipts and payments of cash. The Format

is given below:

CASH BOOK

Date Receipts L/F Amount Date Receipts L/F Amount

Rs. Rs.

Here it may be seen that a Cash Book looks like a Cash Account. The Cash Book is different

from other subsidiary books since it is two sided. It records two aspects, the receipts aspect as

well as the payments aspect. It serves both the purpose of a journal and also a ledger.

PURCHASES BOOK

The Purchase Book records all the Credit purchases, the Voucher No. Invoice No the Name of

the Creditor and then amount of Purchases are given. The Format of the Purchase Book is

given below:

PURCHASE BOOK

Date Name of the Creditor L/F Invoice No. Amount in Rs.

34

SALES BOOK

The Sales Book, also called the Day Book, records all the Credit Sales. The Voucher No. the

Name of the Debtor and the amount of sales are recorded. The format of the Sales Book is

given below:

SALES BOOK

Date Name of the Debtor L/F Invoice No. Amount in Rs.

PURCHASE RETURNS BOOK

The Purchase Returns Books records all the Returns made out of Credit Purchases. The

format of the purchase returns is given below.

PURCHASE RETURNS BOOK

Date Debit No. Name L.F. Amount in Rs.

Debit Note: It is a note made out in duplicate. The duplicate copy is kept for office record

and the original one is sent to the seller. The party’s account is debited with the amount

written in the purchase returns book.

SALES RETURNS BOOK

Sales Returns Book shows the goods returned by the customers to whom goods have been

sold. The format of the sales return book is given below:

35

SALES RETURNS BOOK

Date Credit Note. Name L.F. Amount in Rs.

Credit note is also like a debit note. It is also made out in duplicate. The duplicate copy is

kept for office record.

BILLS RECEIVABLE BOOK

Bills Receivable Book records the amounts receivable against Bills or exchange by the

business receivable lying with us. The format of the Bills Receivable Book is given below:

BILLS RECEIVABLE BOOK

Date Drawee Tenure Payable at Due Date

BILLS PAYABLE BOOK

The Bills payable book records all the bills payable by the business. The format is given

below.

BILLS PAYABLE BOOK

Date Drawer/Payee Tenure Payable at Due Date

36

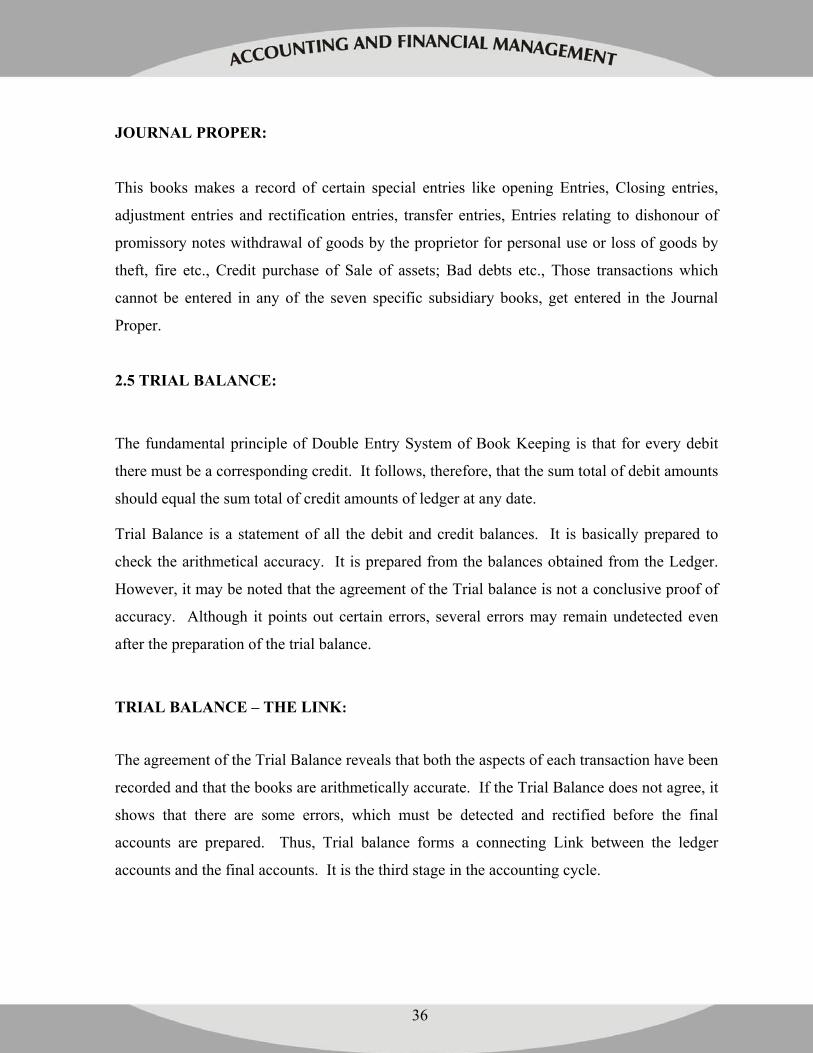

JOURNAL PROPER:

This books makes a record of certain special entries like opening Entries, Closing entries,

adjustment entries and rectification entries, transfer entries, Entries relating to dishonour of

promissory notes withdrawal of goods by the proprietor for personal use or loss of goods by

theft, fire etc., Credit purchase of Sale of assets; Bad debts etc., Those transactions which

cannot be entered in any of the seven specific subsidiary books, get entered in the Journal

Proper.

2.5 TRIAL BALANCE:

The fundamental principle of Double Entry System of Book Keeping is that for every debit

there must be a corresponding credit. It follows, therefore, that the sum total of debit amounts

should equal the sum total of credit amounts of ledger at any date.

Trial Balance is a statement of all the debit and credit balances. It is basically prepared to

check the arithmetical accuracy. It is prepared from the balances obtained from the Ledger.

However, it may be noted that the agreement of the Trial balance is not a conclusive proof of

accuracy. Although it points out certain errors, several errors may remain undetected even

after the preparation of the trial balance.

TRIAL BALANCE – THE LINK:

The agreement of the Trial Balance reveals that both the aspects of each transaction have been

recorded and that the books are arithmetically accurate. If the Trial Balance does not agree, it

shows that there are some errors, which must be detected and rectified before the final

accounts are prepared. Thus, Trial balance forms a connecting Link between the ledger

accounts and the final accounts. It is the third stage in the accounting cycle.

37

A specimen of Trial Balance is given below:

TRIAL BALANCE OF _______________ AS ON: _____________

S.No. Name of the Accounts Dr. Balance Cr. Balance

As already said the trial balance may agree and yet there may be some errors. The following

types may remain undetected, even after the tallying of Trial Balance.

i) Omission of an entry in a subsidiary book

ii) A wrong entry in a subsidiary book

iii) Posting an item to the correct side but in the wrong account

iv) Compensating errors

v) Errors of principle

PREPARATION OF TRIAL BALANCE:

Let us take a small example to understand and how a trial balance is prepared. From the

following balances taken from the ledger of Sri Ltd., prepare a trial balance as on 31-3-2004:

Opening Stock 24000 Carriage inwards 100 Traveling Expenses 775 Returns inwards 1200 Rent & Taxes 1050 Sales 42000Salaries & Wages 3145 Purchases 31500Freight out wards 130 Disallowed 450 Discount received 220 Capital Account 57000Commission paid 216 Drawings Account 9000 Bank Account 12054 Bills receivable 16000Sundry debtors 13600 Bills payable 4000 Trade creditors 10000 Closing stock 31600

38

TRIAL BALANCE OF SRI LTD.,AS ON 31-03-2004 Debit

Balances Rs.

Credit Balances Rs.

Opening Stock 24000 Travelling Expenses 774 Rent & Taxes 1050 Salaries & Wages 3144 Freight outwards 130 Bills payable 4000 Carriage Inwards 100 Returns Inwards 1200 Sales 42000 Purchases 31500 Discount allowed 450 Discount received 220 Commission paid 216 Bank account 12054 Sundry debtors 13600 Trade creditors 10000 Capital account 57000 Drawings account 9000 Bills receivable 16000 Total 1,13,220 1,13,220

Note: Closing stock is already included in Purchases and therefore should not be shown in the

Trial Balance. It should be given as an adjustment while preparing Final Accounts.

2.6 ACCOUNTING CYCLE:

Ledger

Journal Trial Balance

Final Accounts

The accounting cycle shows that a business transaction is first entered into Journal, the book

of original entry. From there it is transferred or posted to the Ledger. From the Ledger

39

Balances a Trial Balance is prepared. Trial balance is a statement of debits and credits. From

these balances the Final Accounts are prepared. Thus it may be remembered that the

Accounting Cycle starts with Journal and ends with the Final Accounts. At the Journal stage

documentation of the Business transactions is done, while at the Ledger stage account wise

information is obtained and summarized and at the Trial Balance stage List of Debit and

Credit balances is obtained to check the arithmetical accuracy and at the final accounting

stage the profit or loss position of the business is found out.

2.7 SUMMARY:

Maintaining a systematic record of all transaction is called book-keeping and when such

record-keeping moves on to classifying and summarizing, preparation of final reports and

their interpretation, we call it accounting. Journal is the book wherein a business transaction

is first written or recorded and therefore it is also known as book of Original Entry. Steps to

be followed while journalizing are: Identify the accounts being affected in the transaction;

Categorize them into real, nominal and personal and; apply the relevant rules of debit and

credit. Ledger is a book where account wise information is documented. While the Journal

gives data in chronological form, the ledger gives account wise information. All the

transactions related to a particular account are put at one place .

Journal is the book of original entry or the main book where in business transactions are

entered in a chronological order. But when there are too many transactions, Journal is divided

into 8 parts or eight subsidiary books. Thus subsidiary books are parts or sub-divisions of a

journal. Trial Balance is a statement of all the debit and credit balances. It is basically

prepared to check the arithmetical accuracy. It is prepared from the balances obtained from

the Ledger.

2.8 KEY WORDS: Journal Journalising

Narration Real Account

Nominal Account Personal Account

Ledger Ledger Posting

40

Balancing Debit Balance

Credit Balance Subsidiary Books

Trial Balance

Try Yourself:

1. Journalize the following transactions in the books of Mr. Joy.

April 1, 2004 Capital brought in Rs. 100000

April 2, 2004 Bought Machinery Rs. 50000

April 3, 2004 Purchased Good Rs. 25000

April 5, 2004 Sales Rs. 10000

April 6, 2004 Sales to Shalom Rs. 15000

April 7, 2004 Purchases from Princy Rs. 20000

April 8, 2004 Received to Divya Rs. 15000

April 9, 2004 Received Interest Rs.5000

April 10, 2004 Received Commission Rs.3000

April 11, 2004 Bought Furniture from Teja Ltd on Credit Rs. 10000

April 15, 2004 Paid Salaries Rs.5000

2. Bank A/c Dr. 56000 Discount Dr. 500 To Bills Receivable 5500 Post the above entries.

3. Given below is a Cash account, point out whether Cash book shows Debit or Credit.

CASH A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount

1.1.04 To Balance B/d 8000 17.1.04 By Purchases 3000

15.1.04 To sales 2000 19.1.04 By Rent 1000

20.1.04 To Ramya 1000 31.1.04 By Balance C/d 7000

Total 11000 Total 11000

41

4. From the following balances prepare the Trial Balance of MJS Ltd. Purchases 1,57, 500 Sales 2,10,000 Return Inwards 6,000 Carriage Inwards 500 Freight Outwards 650 Salaries & Wages 15,720 Rent & Taxes 5,260 Traveling Expenses 3,870 Opening Stock 1,20,000 Discount allowed 2,250 Discount received 1,100 Commission paid 1,080 Bank account 60,270 Sundry Debtors 68,000 Trade Creditors 50,000 Capital Account 2,85,000 Drawings Account 45,000 Bills Receivable 80,000 Bills Payable 20,000 Closing stock 1,58,000 5. What is Journal?

6. What are the various types of accounts?

7. Explain the rules of Journalising.

8. Classify the following accounts.

a. Capital

b. Cash

c. Furniture

d. Salaries

e. Goodwill

9. What do you mean by ledger posting

10. If a personal account is showing a debit balance, what does it indicate

11. Cash Book records all ----------------------- transactions.

12. Purchases Book records ---------------------.

13. Adjustment entries are written in --------------------.

42

14. Omission of an entry in a Subsidiary book affects the agreement of Trial Balance.(Yes/

No)

15. Compensating Errors go undetected by The Trial Balance.(Yes/ No)

Answers: 1. JOURNAL OF Mr. Joy Date Particulars Debit Rs. Credit Rs. April 1, 2004 Cash A/c Dr.

To Capital A/c (Being Capital Brought)

100000 100000

April 2, 2004 Machinery A/c Dr.

To Cash A/c

(Being purchase of Machinery)

50000 50000

April 3, 2004 Purchases A/c Dr.

To Cash A/c

(Being Goods purchased)

25000 25000

April 5, 2004 Cash A/c Dr.

To Sales A/c

(Being Sales made)

10000 10000

April 6, 2004 Shalom A/c Dr.

To Sales A/c

(Being Credit Sales made to Shalom)

15000 15000

April 7, 2004 Purchases A/c Dr.

To Princy A/c

(Being Credit purchases made)

20000 20000

43

April 8, 2004 Cash A/c Dr.

To Sales A/c

(Being Sales made)

15000 15000

April 9, 2004 Cash A/c Dr.

To Sales A/c

(Being Sales made)

5000 5000

April 10, 2004 Cash A/c Dr.

To Commission A/c

(Being Commission received)

3000 3000

April 11, 2004 Furniture A/c Dr.

To Teja Ltd A/c

(Furniture purchased on Credit)

10000 10000

April 15, 2004 Salaries A/c Dr.

To Cash A/c

(Being Salaries paid)

5000 5000

2. BANK A/C

Dr. Cr.

Date Particulars Amount Date Particulars Amount

To Bills

Receivable

5000

DISCOUNT A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount

To Bills receivable 500

44

BILLS RECEIVABLE A/C Dr. Cr.

Date Particulars Amount Date Particulars Amount

By Bank 5000

By Discount 500

4. Total of Trial Balance – Rs 5,66,100.

8. (a) Personal A/c, (b) Real A/c, (c) Real A/c, (D) Nominal A/c (e) Real A/c.

11. Cash

12. Credit Purchases

13. Journal Proper

14. Yes

15. Yes

FURTHER READINGS: Jain S.P. and K.L. Narang, Fundamentals of Accounting, Kalyani Publishers

Jawaharlal, Financial Accounting, Wheeler Publishing

Nitin Balwani, Accounting and Finance for Managers, Excel Books

45

LESSON 3

ACCOUNTING CYCLE-II (FINAL ACCOUNTS)

STRUCTURE:

3.1 Introduction

3.2 Capital and Revenue Items

3.3 Profit & Loss Account

3.4 Balance Sheet

3.5 Adjustments

3.6 Summary

3.7 Key Words

3.1 INTRODUCTION:

The final stage in the accounting cycle is the preparation of final accounts. It is common

knowledge that the ultimate objective of maintaining accounts is to find out profit or loss

position and also the financial position of the organization concerned.

OBJECTIVES

To be able to appreciate the need for preparation of Final Accounts.

To be able to prepare the Trading A/c

To be able to prepare the Profit and Loss A/c

To be able to prepare the Balance Sheet

46

Final accounts are prepared from the debit and credit balances of the trial balance. Final

accounts are constituted of the profit and loss account (also called Income Statement) and a

statement of assets and liabilities known as the balance sheet.

3.2 CAPITAL AND REVENUE ITEMS:

It may be noted that before preparing final accounts a distinction needs to be made between

capital and Revenue items. While the revenue items are to be shown in the Profit & Loss A/c.

The Balance Sheet records all capital items in the form of the assets and liabilities as on a

particular date.

Capital Expenditure Revenue Expenditure

1) Amount spent on acquiring permanent

asset

1) Amount spent on the conduct of

business and maintenance of capital assets

2) The expenditure adds to the revenue

earning capacity of the business

2) This Expenditure may not do so

3) May add to the value of an existing asset 3) Revenue Expenditure does not add to

any value to net asset

4) shown in the balance sheet 4) Shown in the trading or profit and loss

account

3.3 PROFIT & LOSS ACCOUNT:

As already stated profit and loss A/c shows the net income or net expenditure position of the

business organisation. It consists of two parts namely: Trading A/c and (2) Profit and Loss

A/c. The preparation of the main profit and loss account begins with the Trading Account and

ends with the Profit and Loss account. While Trading Account records the balances which are

47

directly related to the manufacturing the product, the profit and loss account records the

expenses and incomes and expenses, profits and losses which are related to the business but

not directly related to the making of the product saleable.

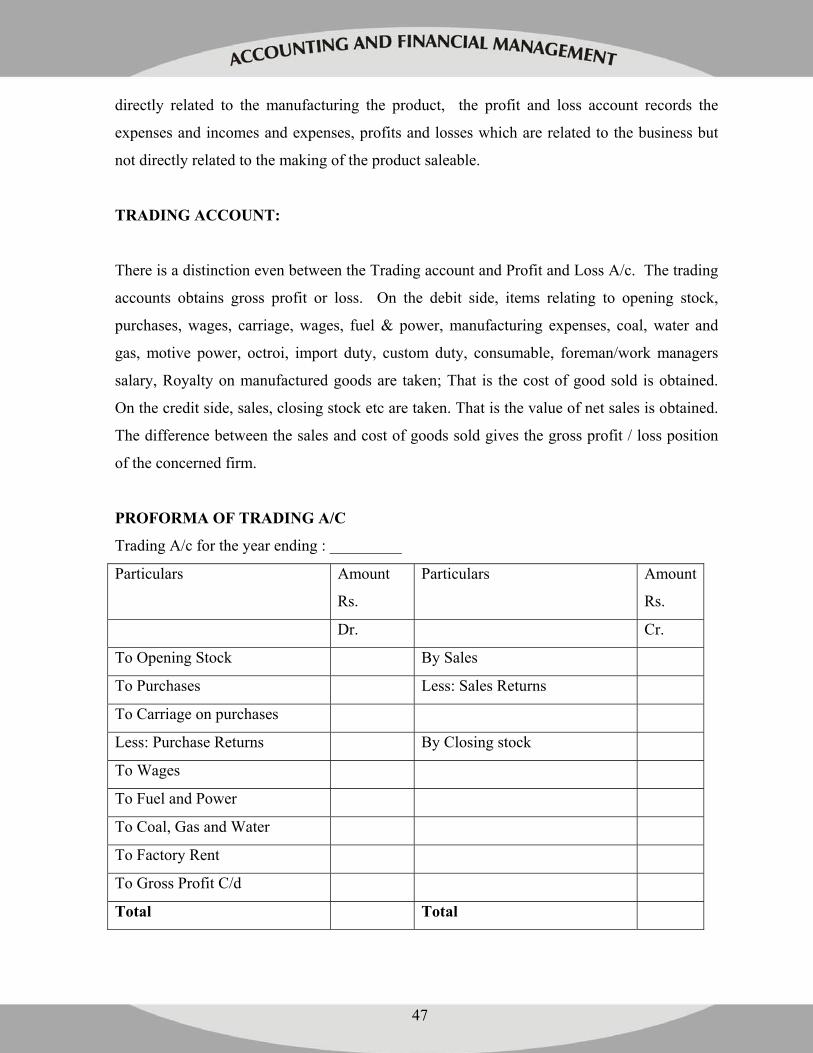

TRADING ACCOUNT:

There is a distinction even between the Trading account and Profit and Loss A/c. The trading

accounts obtains gross profit or loss. On the debit side, items relating to opening stock,

purchases, wages, carriage, wages, fuel & power, manufacturing expenses, coal, water and

gas, motive power, octroi, import duty, custom duty, consumable, foreman/work managers

salary, Royalty on manufactured goods are taken; That is the cost of good sold is obtained.

On the credit side, sales, closing stock etc are taken. That is the value of net sales is obtained.

The difference between the sales and cost of goods sold gives the gross profit / loss position

of the concerned firm.

PROFORMA OF TRADING A/C

Trading A/c for the year ending : _________

Particulars Amount

Rs.

Particulars Amount

Rs.

Dr. Cr.

To Opening Stock By Sales

To Purchases Less: Sales Returns

To Carriage on purchases

Less: Purchase Returns By Closing stock

To Wages

To Fuel and Power

To Coal, Gas and Water

To Factory Rent

To Gross Profit C/d

Total Total

48

PROFIT AND LOSS A/C:

The profit and loss account is prepared in order to find out the net profit / loss position of the

concern. The expenses and incomes taken in the profit and loss account are of indirect nature

and include the following:- Proforma of Profit And Loss A/C

To gross loss brought down To Office Salaries To Expenses To Advertisement To Traveling Salaries To Expenses incurred on commission To Bad Debts To Godown Rent To Export Expenses To Carriage outwards To Bank charges To Agents commission To Rent, Rates and Taxes To Heating and Lighting To selling and distribution expenses To Printing and Stationery To Postage and Telegram To Telephone Charges To Legal charges To Audit fees To Insurance To General Expenses To Depreciation To Repairs & Maintenance To Discount allowed To Interest on capital To Interest on loans To Discount on bills discounted To Extraordinary expenses To Loss by Fire (Not covered by Insurance) To Net profit transferred to capital A/c

Amount Rs.

By gross profit brought down By Interest Received By Discount Received By Commission Received By Rent from Tenants By Income from Investments By Apprentice premium By Interest on debentures By Income from any other sources By Miscellaneous Revenue receipts By Net loss transferred to Capital A/c

Amount Rs.

49

3.4 BALANCE SHEET:

A balance sheet shows the financial position of a business on a certain fixed date. The

financial position of any concern/organization is shown by its assets on a given date and its

liabilities on that date. The excess of assets over liabilities represents the capital which serves

as a pointer to the financial condition of the concern. It may be noted that a balance sheet is

not an account but a mere statement of assets and liabilities on a particular date. The left hand

side of the balance sheet shows all the liabilities while the right side displays the Assets

position. The specimen proforma of a balance sheet is given below:

BALANCE SHEET OF _________________ COMPANY AS ON : _____________

LIABILITIES Rs. ASSETS Rs. CURRENT LIABILITIES: • Bills payable • Sundry creditors • Bank Overdraft LONG TERM LIABILITIES: • Loan from Bank • Loan from Wife FIXED LIABILITIES: • Capital

LIQUID ASSETS: • Cash in Hand • Cash at Bank FLOATING ASSETS: • Sundry Debtors • Investments • Bills Receivable • Stock in Trade • Prepaid Expenses FIXED ASSETS: • Machinery • Building • Furniture & Fixtures • Motor Car INTANGIBLE ASSETS: • Goodwill • Patents • Copyright • Licenses FICTITIOUS ASSETS: • Advertisement • Miscellaneous Expenses • Profit & Loss A/c

TOTAL

TOTAL

50

In the reverse order of preference the Balance Sheet may be prepared as follows:

BALANCE SHEET

LIABILITIES ASSETS

1. Fixed Liabilities

2. Long Term liabilities

3. Current Liabilities

1. Fictitious Assets

2. Intangible Assets

3. Fixed Assets

4. Floating Assets

5. Liquid Asset

TOTAL: TOTAL:

Thus it goes to say, that the items in the balance sheet may be marshaled either in the order of

permanence or liquidity.

Example:

From the following balances of XYZ Ltd on 31.3.2004 you are required to prepare the

Trading and Profit and Loss Account and a Balance sheet as on that date:

Amount Rs. Amount Rs.

Stock on April 1 1000 Commission (Cr) 400

Bills Receivable 4500 Return Outward 500

Purchases 39000 Trade Expenses 200

Wages 2800 Office Fixtures 1000

Insurance 1100 Cash withdrawal 500

Sundry Debtors 30000 Cash at bank 4750

Carriage Inwards 800 Rent and Taxes 1100

Commission (Dr) 800 Carriage outward 1450

Interest on capital 700 Sales 50000

Stationery 450 Bills payable 3000

Returns inward 1300 Creditors 19650

Capital 17900 Closing stock 25000

51

TRADING & PROFIT AND LOSS A/C OF XYZ LTD

FOR THE YEAR ENDING : 31-3-2004

Particulars Amount Rs. Dr.

Particulars Amount Rs. Cr.

To Opening Stock 1000 By Sales: 50000 Less: Returns I/W 1300

48700

To purchases: 39000 Less: Returns outward 500

38500

By Closing Stock 25000

To wages 2800 To Carriage I/w 800 To Gross Profit C/d 30600 73700 73700 To Insurance 1100 By Gross Profit B/d 30600 To Commission 800 By Commission 400 To Interest on Capital 700 To Rent and Taxes 1100 To Carriage O/w 1450 To net profit transferred to Capital A/c

25200

TOTAL 31000 TOTAL 31000

BALANCE SHEET OF XYZ LTD

AS ON: 31.3.2004

LIABILITIES Rs. ASSETS Rs. Creditors 19650 Cash in hand 500 Bills payable 3000 Cash at Bank 4750 Capital: 17900 Add: Net profit 25200

43100

Bills receivable 4500

Stock 25000 Sundry debtors 30000 Office Fixtures 1000 TOTAL 65750 TOTAL 65750

52

3.5 ADJUSTMENTS:

Bits of information which are received/discovered after the preparation of Trial Balance have

to be accommodated into financial statements. They are, therefore called adjustments. It may

be remembered that sometimes adjustments thus need to be made in the final accounts. Since

the adjustments are given after the trial balance is prepared, they have to be given the two fold

effect. Once they appear in the trading/profit and loss account and the second time in the

balance sheet. These adjustments enable the firm to make its accounts fall in line with the

matching and such other concepts whichmake the final statements of account to reflect the

true and fair view of the affairs of the business. Treatment for some of the adjustments is

given below:

Closing Stock:

This may be shown on the credit side of the Trading account and the Second time on the asset

side of the balance sheet.

Outstanding Expenses:

These are expenses due to be paid but not paid. These expenses should be added to the

amounts already paid and shown in the trading account or the profit and loss account

depending upon whether it is a direct expenditure or indirect expenditure. For Eg:

outstanding wages should be added to “Wages” in Trading account and if it is outstanding

salary should be added to “Salary” account in the profit and loss account. The second effect

is that should it should be shown on the liability side of balance sheet.

Prepaid (Unexpired) Expenses:

These are expenses paid in advance and therefore should be deducted from the respective

expenditure on the debit side of Trading and profit and loss a/c and then shown on the asset

side of the balance sheet. For instance if insurance is prepaid, it should be deducted from

Insurance on the debit side of profit and loss account and should be shown on the asset side of

the Balance sheet as prepaid insurance.

53

Accrued Income:

That income which has been earned but not received during the accounting year is called

accrued income. Such income needs to be added to the respective income on the credit side

of the profit and loss and again on the asset side of the balance sheet.

Income Received In Advance:

Income received but not earned during the accounting year is known as Income received in

Advance. This should be deducted from the respective income in the profit and loss a/c and

should be shown in the balance sheet as a liability.

Depreciation:

This is reduction in the value of the fixed Asset and is usually calculated as a percentage of

the assets. The amount of depreciation is shown on the debit side of profit and loss account

and is to be deducted from the respective asset value in the balance sheet.

Bad Debts:

Debts which cannot be recovered or become irrecoverable are called bad debts. Since this is a

loss for the business it is shown on the debit side of the Profit and Loss account and deducted

from Sundry Debtors on the asset side of the Balance sheet.

Interest on Capital:

This is calculated as a percentage on capital and is shown on the debit side of Profit and Loss

account and added to capital on the liability side of the Balance sheet.

Interest on Drawings:

The two fold effect of this adjustment is that it will be shown on the credit side of profit and

loss account and is added to the amount of drawings on the liability side of the Balance sheet.

Provision for Doubtful Debts:

This is a provision maintained to meet doubtful debts. It is usually calculated as a percentage

on sundry debtors and is shown on the debit side of profit and loss account and is deducted

from sundry Debtors on the asset side of the Balance sheet.

Provision for Discount on Debtors:

In order to encourage prompt payment, discount is given to debtors. To meet the expenses of

discount a provision is maintained on debtors. This provision, known as Discount on Debtors

54

is shown on the debit side of the profit and loss account and is deducted from sundry debtors

on the asset side of the balance sheet.

Provision for Discount on Creditors:

This is calculated as a percentage on creditors and is shown on the credit side of Profit and

Loss account and is deducted from sundry creditors on the liability side of the Balance sheet.

Deferred Revenue Expenditure:

Advertisement expenditure is the best example for deferred revenue expenditure. A huge

amount may be spent on advertisement in a single year but the benefits of such advertisements

may be spread over the ensuing years too. Therefore only a part of such expenditure will be

written off each year. The written off expenditure is shown on the debit side of profit and loss

account and the unwritten part of the expenditure is shown on the asset side. Such unwritten