CASH 39th Annual Conference The Day After Tomorrow: Post-Bond Issuance Compliance Requirements C.A.S.H. 2018 Annual Conference February, 26 2018 Presented by: Daniel M. Maruccia Overview of Topics Tax Compliance Continuing Disclosure Audits, Oversight, and Annual Reporting

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CASH 39th Annual Conference

The Day After Tomorrow:Post-Bond Issuance

Compliance Requirements

C.A.S.H. 2018 Annual Conference

February, 26 2018

Presented by:

Daniel M. Maruccia

Overview of Topics

Tax Compliance

Continuing Disclosure

Audits, Oversight, and Annual Reporting

CASH 39th Annual Conference

Tax Compliance

3

Tax Compliance

• Protecting tax-exempt status

• Covenants to Bondholders in your Tax Certificate

4

CASH 39th Annual Conference

Tax Compliance

• Post-issuance federal tax requirements generally fall into three categories:

(1) Qualified use of proceeds and financed property;

(2) Arbitrage yield restriction and rebate; and

(3) Record-keeping.

5

Tax Compliance

6

CASH 39th Annual Conference

Private Activity Bonds

7

What is it?

Private Activity Bonds

8

The Rule / The Concept

CASH 39th Annual Conference

Tax Compliance – Private Activity Bond Tests

Private Activity Bond Tests apply at issuanceand after the bonds are issued.

Private Business Use Test: More than 10 percent of the proceeds, or assets financed with the proceeds, are used for any private business use.

9

Tax Compliance – Private Activity Bond Tests

•What is “Private?”

10

CASH 39th Annual Conference

Tax Compliance – Private Activity Bond Tests

Private Security or Payment Test: More than 10 percent of the Bonds are secured by interest in property used for private business purposes.

Includes lease payments pledged for the security of the bonds, from the lease of property to nongovernmental persons.

11

Tax Compliance – Private Activity Bond Tests

Private Loan Financing Test: More than 5 percent of the proceeds, or more than $5M (whichever is less), is loaned to a nongovernmental person.

12

CASH 39th Annual Conference

Governmental vs. Private Business Use

Bad Use

• Management and Service Contracts (maybe)

• Research Agreements

• Leasing to a nongovernmental person or entity (even if they are subleasing back to a governmental entity)

• Loaning proceeds to a nongovernmental person or entity)

13

Tax Compliance – Private Use

Best Practices to Avoid Private Activity• Maintain a detailed list of assets financed with

Bonds.

• Do not dispose of equipment financed with Bonds, until the end of the useful life of such equipment, or until the Bonds are fully paid.

• Consult with counsel prior to change in use of facilities financed with Bond proceeds.

14

CASH 39th Annual Conference

Tax Compliance - Arbitrage

Arbitrage• What is it?

• What’s the public policy?

15

Tax Compliance - Arbitrage

2 Questions:• Do I have it?

• Can I keep it?

16

CASH 39th Annual Conference

Tax Compliance – Yield Restrictions

Yield Restrictions

• Gross proceeds of a bond may not be invested in investments earning a yield higher than the yield of the bond issue.

• If proceeds are permitted to be invested at a yield higher than the yield on the bonds, rebate payments may be required to be made to the U.S. Treasury.

17

Tax Compliance – Record Retention

Record Retention

• Retain all records sufficient to support Bondholders’ exclusion of interest from income taxation.

• Retain records of the Bonds for the life of the bonds, plus 6 years.

18

CASH 39th Annual Conference

Tax Compliance - What Records to Retain

• SLGS Subscription or other open market securities for any advance refunding of Bonds.

• Project Draw/Expenditure Schedules.

• FA/Underwriter’s structuring information

• Bond Insurance quotes and calculations supporting cost and benefit of Bond Insurance

• All invoices, payments, and certificates related to costs of issuance of the Bonds.

• Bond Transcript

• Records of Investments for the Bonds

19

• Documentation of compliance with investment restrictions.

• Investment activity statements

• Invoices relating to equipment purchased or projects constructed or acquired using Bond proceeds

• Documentation of annual comparison of Bond proceeds expenditure schedules with actual expenditures incurred.

• Arbitrage reports

• Returns and payments to IRS

• Contracts under which Bond proceeds are spent

Tax Compliance

20

A consideration at issuance of what happens after issuance.

CASH 39th Annual Conference

Tax Compliance - Hedge Bonds

Hedge Bonds:• Issuer must reasonably expect that 85% of

the spendable proceeds of the issue will be spent within 3 years; and

• Issuer must reasonably expect that not more than 50% of the proceeds are invested in nonpurpose investments having substantially guaranteed yield for 4 years or more.

21

Tax Compliance – Best Practices

• Post Issuance Tax Compliance Policy; and

• Tax Certificate

22

CASH 39th Annual Conference

Continuing Disclosure

23

Continuing Disclosure

Securities and Exchange Act of 1934

• Initial Disclosure Document (Official Statement)

• Continuing Disclosure Agreement (at issuance)

• Continuing Disclosure obligations– Annual filings

– Event Notices

24

CASH 39th Annual Conference

Continuing Disclosure

SEC Rule 15c2-12

25

Continuing Disclosure

26

Mechanics of compliance with The Undertaking.

CASH 39th Annual Conference

Continuing Disclosure

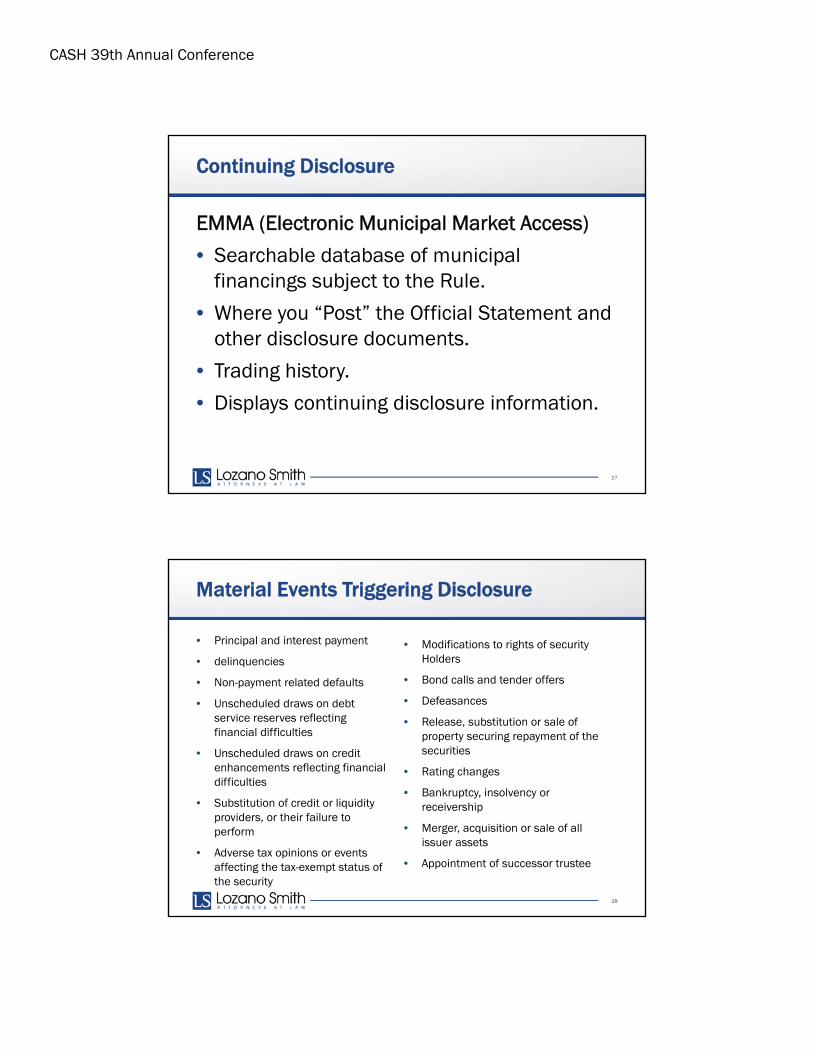

EMMA (Electronic Municipal Market Access)

• Searchable database of municipal financings subject to the Rule.

• Where you “Post” the Official Statement and other disclosure documents.

• Trading history.

• Displays continuing disclosure information.

27

Material Events Triggering Disclosure

• Principal and interest payment

• delinquencies

• Non-payment related defaults

• Unscheduled draws on debt service reserves reflecting financial difficulties

• Unscheduled draws on credit enhancements reflecting financial difficulties

• Substitution of credit or liquidity providers, or their failure to perform

• Adverse tax opinions or events affecting the tax-exempt status of the security

28

• Modifications to rights of security Holders

• Bond calls and tender offers

• Defeasances

• Release, substitution or sale of property securing repayment of the securities

• Rating changes

• Bankruptcy, insolvency or receivership

• Merger, acquisition or sale of all issuer assets

• Appointment of successor trustee

CASH 39th Annual Conference

MCDC Initiative

“Municipalities Continuing Disclosure Cooperation”

• Address violations of the federal securities laws by municipal issuers and underwriters of municipal securities.

• Recommend favorable settlements to issuers and underwriters if they self-report to the Division possible violations.

• Focus on “materially inaccurate statements” in Official Statements regarding prior compliance.

29

The Standard (Anti-Fraud Rule)

“A misrepresentation or omission is material if there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision.”(Basic Inc. v. Levinson (1988) 485 U.S. 224, 231-32)

30

CASH 39th Annual Conference

Disclosure Standard

• Accountability begins and ends with issuer and underwriter, even where a dissemination agent was engaged.

• Issuer’s should have policies, procedures, and practices in place to ensure obligations are met.

31

Disclosure Standard

GFOA Alert: Best Practices• Understand and discuss issuer’s policies and procedures on

disclosure.

• Know who is filing what, when, and where.

• Know what you have promised to do in the Continuing Disclosure Agreement.

• Be aware of what the issuer has posted on EMMA.

• Recognize that each official statement must include a statement about whether the issuer has failed to materially comply with previous commitments within the past five years.

32

CASH 39th Annual Conference

Audits, Oversight, and Annual Reporting

33

Prop 39 Accountability Measures

• For both traditional authority and Prop 39 bonds, the measure must specify its purposes for which bond proceeds may only be applied, create an account into which the bond proceeds must be deposited, and require an annual report regarding the amount of funds collected and expended and project status.

• Additionally, for Prop 39 bonds, there must be annual, independent performance and financial audits and a Citizen’s bond oversight committee must be established.

34

CASH 39th Annual Conference

Establish Citizens Oversight Committee

• “The purpose of the citizens’ oversight committee shall be to inform the public concerning the expenditure of bond revenues. The citizens’ oversight committee shall actively review and report on the proper expenditure of taxpayers’ money for school construction. The citizens’ oversight committee shall advise the public as to whether a school district . . . is in compliance with the requirements of [Prop. 39]. . . .” (Ed. Code §15278(b))

35

Bond Oversight Committee

Establishment of Bond Oversight Committee (BOC)

• Board action establishing BOC within 60 days of noting election results on Board minutes

• Application/vetting process for BOC members

• District provides administrative support

• BOC provides reports/advice; not binding on Board

• BOC may bring Taxpayer Waste Action

36

CASH 39th Annual Conference

What Do They Do:

• Provide “oversight for . . . ensuring” that bond revenues are used properly (Ed. Code §15278(b)(1)&(2))

• Review required annual audits

– Financial audit

– Performance audit

• Inspect facilities

• Review deferred maintenance

proposals or plans

• Issue yearly reports

What Don’t They Do:

• Participate in bond sale

• Determine how funds will be spent

• Participate in facilities planning

• Participate in selecting contractors

• Appoint or fill vacancies on committee

CASH 39th Annual Conference

SB 1029 – More Reporting

What We Used to Have

• California Debt Investment and Advisory Commission (CDIAC) currently requires debt issuance reports, at time the debt is proposed, and once debt is actually sold

• CDIAC currently requires periodic reporting for limited types of issuers:

What We Have Now

• Certification that debt issuer has adopted debt policy

• Adoption of debt policy prior to issuance of new debt

• Annual report of debt issuer due each January until all debt is repaid or redeemed

• CDIAC to collect, provide, track, and report on State and local debt

• CDIAC to act as State statistical “clearinghouse”

39

SB 1029 –More Transparency

What’s in a Debt Policy?

• Stated purposes for which Debt Proceeds may be used

• Types of Debt that May be Issued

• Relationship of the Debt to the Capital Improvement Program or Budget

• Planning Goals and Objectives for Debt

• Internal Control Procedures for Debt Proceeds

40

CASH 39th Annual Conference

SB 1029 –More Transparency

What’s in an Annual Report?

• For each Annual Reporting Period (July 1 through June 30):– Debt Authorized During the

Reporting Period

– Debt Outstanding During the Reporting Period

– Use of Debt Proceeds During the Reporting Period

41

SB 1029 – Timing is Everything

When Must I Adopt a Debt Policy?

• Issuers must adopt a debt policy prior to filing with CDIAC the “Report of Proposed Debt Issuance”

• The Report of Proposed Debt Issuance will contain a “checkbox”

• Failure to File Report of Proposed Debt Issuance does not affect validity of bonds

When Must I File the Annual Report?

• Annual report due to CDIACSeven months following each Reporting Period

• That means, by January 31, 2019, if the Issuer elects to issue any new debt in 2018

42

CASH 39th Annual Conference

TAKE-AWAYS

Questions

44

CASH 39th Annual Conference

45

Disclaimer:These materials and all discussions of these materials are for instructional purposes only and do not constitute legal advice. If you need legal advice, you should contact your local counsel or an attorney at Lozano Smith. If you are interested in having other in-service programs presented, please contact [email protected] or call (559) 431-5600.

Copyright © 2018 Lozano Smith All rights reserved.No portion of this work may be copied, distributed, sold or used for any commercial advantage or private gain, nor any derivative work prepared therefrom, nor shall any sub-license be granted, without the express prior written permission of Lozano Smith through its Managing Partner. The Managing Partner of Lozano Smith hereby grants permission to any client of Lozano Smith to whom Lozano Smith provides a copy to use such copy intact and solely for the internal purposes of such client. By accepting this product, recipient agrees it shall not use the work except consistent with the terms of this limited license.

Daniel [email protected]

One Capitol Mall, Suite 640Sacramento, CA 95814T 916.329.7433 | F 916.329.9050

Related Documents