Filed Pursuant to Rule 424(b)(3) Registration No.: 333-262730 PROSHARES TRUST II Supplement dated April 25, 2022 to the Prospectuses for each ProShares Trust II ETF each dated February 23, 2022 Effective immediately, the disclosure in the “Risk Factors” section of each Prospectus is supplemented to include the following: RISKS OF GOVERNMENT REGULATION The Financial Industry Regulatory Authority (“FINRA”) issued a notice on March 8, 2022 seeking comment on measures that could prevent or restrict investors from buying a broad range of public securities designated as “complex products”—which could include the leveraged and inverse funds offered by ProShares. The ultimate impact, if any, of these measures remains unclear. However, if regulations are adopted, they could, among other things, prevent or restrict investors’ ability to buy the funds. For more information, please contact the Funds at 888-776-3898. Please retain this supplement for future reference.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Filed Pursuant to Rule 424(b)(3)Registration No.: 333-262730

PROSHARES TRUST II

Supplement dated April 25, 2022to the Prospectuses for each ProShares Trust II ETF each dated February 23, 2022

Effective immediately, the disclosure in the “Risk Factors” section of each Prospectus is supplemented to include the following:

RISKS OF GOVERNMENT REGULATION

The Financial Industry Regulatory Authority (“FINRA”) issued a notice on March 8, 2022 seeking comment on measures that could prevent or restrict

investors from buying a broad range of public securities designated as “complex products”—which could include the leveraged and inverse funds

offered by ProShares. The ultimate impact, if any, of these measures remains unclear. However, if regulations are adopted, they could, among other

things, prevent or restrict investors’ ability to buy the funds.

For more information, please contact the Funds at 888-776-3898.

Please retain this supplement for future reference.

Filed pursuant to Rule 424b3Registration No. 333-262730

IMPORTANT NOTICE

ProShares Ultra Bloomberg Crude Oil (UCO)ProShares UltraShort Bloomberg Crude Oil (SCO)

ProShares Ultra Gold (UGL)ProShares Ultra Silver (AGQ)

(each, a “Fund”, and together, the “Funds”)

Supplement dated March 11, 2022to each Fund’s Prospectus and Disclosure Document

dated February 23, 2022

The Prospectus and Disclosure Document for each Fund is hereby revised to reflect that:

New Portfolio Manager. Effective March 11, 2022, all references to Benjamin McAbee in the Prospectus are deleted. The following information is

added to the “Executive Officers of the Trust and Principals and Significant Employees of the Sponsor” section of the Prospectus:

Name PositionGeorge Banian Portfolio Manager and Associated Person of the Sponsor

George Banian, Principal of the Sponsor since March 11, 2022, has served as a registered associated person and an NFA associate member of the

Sponsor since March 11, 2022, and a Portfolio Manager of the Sponsor since March 11, 2022. In these roles, Mr. Banian’s responsibilities include

day-to-day portfolio management of certain series of the Trust. Mr. Banian also serves as a Portfolio Manager of PSA since February 2022,

Associate Portfolio Manager of PSA from August 2016 to February 2022, Senior Portfolio Analyst of PSA from December 2010 to August 2016,

and Portfolio Analyst of PSA from December 2007 to December 2010. In addition, Mr. Banian served as a Portfolio Manager of PFA since

February 2022, and an Associate Portfolio Manager of PFA from July 2021 to February 2022.

These securities have not been approved or disapproved by the United States Securities and Exchange Commission (the “SEC”) or any statesecurities commission nor has the SEC or any state securities commission passed upon the accuracy or adequacy of this Prospectus. Anyrepresentation to the contrary is a criminal offense.

NEITHER THE TRUST NOR ANY FUND IS A MUTUAL FUND OR ANY OTHER TYPE OF INVESTMENT COMPANY AS DEFINED INTHE INVESTMENT COMPANY ACT OF 1940, AS AMENDED, AND NEITHER IS SUBJECT TO REGULATION THEREUNDER.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOLNOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

Please retain this supplement for future reference.

Filed pursuant to rule 424(b)(3) Registration No. 333-262730

IMPORTANT NOTICE

ProShares Ultra Bloomberg Crude Oil (UCO) ProShares UltraShort Bloomberg Crude Oil (SCO)

ProShares Ultra Gold (UGL) ProShares Ultra Silver (AGQ)

(each, a “Fund”, and together, the “Funds”)

Supplement dated February 25, 2022 to each Fund’s Prospectus and Disclosure Document

dated February 23, 2022

The Prospectus and Disclosure Document for each Fund are hereby revised to reflect that: Addition to Risks Specific to the Oil and Precious Metals Markets and Funds. On February 24, 2022, Russia commenced a military attack on Ukraine. The outbreak of hostilities between the two countries could result in more widespread conflict and could have a severe adverse effect on the region, the markets for gold, silver, and oil and the price of Financial Instruments based on such commodities, and other markets. In addition, sanctions imposed on Russia by the United States and other countries, and any sanctions imposed in the future could have a significant adverse impact on the Russian economy and related markets. The price and liquidity of the Financial Instruments in which each Fund invests may fluctuate widely as a result of the conflict and related events. How long such conflict and related events will last and whether it will escalate further cannot be predicted. Impacts from the conflict and related events could have significant impact on a Fund’s performance, and the value of an investment in the Fund may decline significantly. These securities have not been approved or disapproved by the United States Securities and Exchange Commission (the “SEC”) or any state securities commission nor has the SEC or any state securities commission passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense. NEITHER THE TRUST NOR ANY FUND IS A MUTUAL FUND OR ANY OTHER TYPE OF INVESTMENT COMPANY AS DEFINED IN THE INVESTMENT COMPANY ACT OF 1940, AS AMENDED, AND NEITHER IS SUBJECT TO REGULATION THEREUNDER. THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

Please retain this supplement for future reference.

Filed pursuant to Rule 424(b)(3)Registration No. 333-262730

PROSHARES TRUST II

Common Units of Beneficial Interest

Fund Benchmark

ProShares Ultra Bloomberg Crude Oil (UCO) Bloomberg Commodity Balanced WTI Crude Oil IndexSM

ProShares UltraShort Bloomberg Crude Oil (SCO) Bloomberg Commodity Balanced WTI Crude Oil IndexSM

ProShares Ultra Gold (UGL) Bloomberg Gold SubindexSM

ProShares Ultra Silver (AGQ) Bloomberg Silver SubindexSM

ProShares Trust II (the “Trust”) is a Delaware statutory trust organized into separate series. The Trust may from time to time offer to sellcommon units of beneficial interest (“Shares”) of any or all of the series of the Trust listed above (each, a “Fund” and collectively, the “Funds”)or other series of the Trust. Shares represent units of fractional undivided beneficial interest in and ownership of a series of the Trust. EachFund’s Shares are offered on a continuous basis. The Shares of each Fund are listed for trading on NYSE Arca, Inc. (the “Exchange”) under theticker symbol shown above next to each Fund’s name. Please note that the Trust has series other than the Funds.

Each of the Funds is “geared” which means that each has an investment objective to seek daily investment results, before fees andexpenses, that correspond either to a multiple (2x) or an inverse multiple (-2x) of the performance of a benchmark for a single day, not for anyother period. A “single day” is measured from the time a Fund calculates its respective net asset value (“NAV”) to the time of the Fund’s nextNAV calculation. The NAV calculation times for the Funds typically range from 1:25 p.m. to 4:00 p.m. (Eastern Time). Please see the sectionentitled “Summary—Creation and Redemption Transactions” for additional details on the NAV calculation times for the Funds.

In order to achieve its investment objective, each of the Funds intends to invest in financial instruments (“Financial Instruments”) in themanner and to the extent described herein. Financial Instruments are instruments whose value is derived from the value of an underlying asset,rate or benchmark (such asset, rate or benchmark, a “Reference Asset”) and include futures contracts, swap agreements, forward contracts,option contracts, and other instruments. The Funds will not invest directly in any commodities or currencies.

The ProShares Ultra Bloomberg Crude Oil (the “Ultra Crude Oil Fund”) and the ProShares UltraShort Bloomberg Crude Oil (the“UltraShort Crude Oil Fund”) may be collectively referred to herein as the “Oil Funds.” The ProShares Ultra Gold (the “Ultra Gold Fund”) andthe ProShares Ultra Silver (the “Ultra Silver Fund) may be collectively referred to herein as the “Precious Metals Funds.” The Precious MetalsFunds and the Ultra Crude Oil Fund may be referred to herein as an “Ultra Fund” or “Ultra Funds.” UltraShort Crude Oil Fund may be referredto herein as an “UltraShort Fund.”

INVESTING IN THE SHARES INVOLVES SIGNIFICANT RISKS. PLEASE REFER TO “RISK FACTORS” BEGINNINGON PAGE 10.

THE FUNDS PRESENT SIGNIFICANT RISKS NOT APPLICABLE TO OTHER TYPES OF FUNDS. THE FUNDS ARE NOTAPPROPRIATE FOR ALL INVESTORS. THE FUNDS USE LEVERAGE AND ARE RISKIER THAN SIMILARLYBENCHMARKED EXCHANGE-TRADED FUNDS THAT DO NOT USE LEVERAGE. AN INVESTOR SHOULD ONLYCONSIDER AN INVESTMENT IN A FUND IF HE OR SHE UNDERSTANDS THE CONSEQUENCES OF SEEKING DAILYLEVERAGED OR DAILY INVERSE LEVERAGED INVESTMENT RESULTS, INCLUDING THE IMPACT OF COMPOUNDINGON FUND PERFORMANCE.

THE RETURN OF A FUND FOR A PERIOD LONGER THAN A SINGLE DAY IS THE RESULT OF ITS RETURN FOREACH DAY COMPOUNDED OVER THE PERIOD AND USUALLY WILL DIFFER IN AMOUNT AND POSSIBLY EVENDIRECTION FROM THE FUND’S STATED MULTIPLE TIMES THE RETURN OF THE FUND’S BENCHMARK FOR THESAME PERIOD. THESE DIFFERENCES CAN BE SIGNIFICANT.

THE FUNDS’ INVESTMENTS MAY BE ILLIQUID AND/OR HIGHLY VOLATILE AND THE FUNDS MAY EXPERIENCELARGE LOSSES FROM BUYING, SELLING OR HOLDING SUCH INVESTMENTS. AN INVESTOR IN ANY OF THE FUNDSCOULD POTENTIALLY LOSE THE FULL PRINCIPAL VALUE OF HIS/HER INVESTMENT WITHIN A SINGLE DAY.

SHAREHOLDERS WHO INVEST IN THE FUNDS SHOULD ACTIVELY MANAGE AND MONITOR THEIRINVESTMENTS, AS FREQUENTLY AS DAILY.

Each Ultra Fund seeks daily investment results, before fees and expenses, that correspond to two times (2x) the performance of itsbenchmark for a single day, not for any other period. The UltraShort Fund seeks daily investment results, before fees and expenses, thatcorrespond to two times the inverse (-2x) of the performance of its benchmark for a single day, not for any other period. The return of aFund for a period longer than a single day is the result of its return for each day compounded over the period and usually will differ inamount and possibly even direction from the Fund’s stated multiple times the return of the Fund’s benchmark for the same period.These differences can be significant. Daily compounding of a Fund’s investment returns can dramatically and adversely affect itslonger-term performance, especially during periods of high volatility. Volatility has a negative impact on Fund returns and the volatilityof a Fund’s benchmark may be at least as important to the Fund’s return as the return of the Fund’s benchmark.

Each of the Funds uses leverage and should produce returns for a single day that are more volatile than that of its respectivebenchmark. For example, the return for a single day of an Ultra Fund with a 2x multiple should be approximately two times as volatilefor a single day as the return of a fund with an objective of matching the same benchmark. The return for a single day of the UltraShortFund with a -2x multiple should be approximately two times as volatile for a single day as the inverse of the return of a fund with anobjective of matching the same benchmark.

Each Fund will distribute to shareholders a Schedule K-1 that will contain information regarding the income and expenses of theFund.

NEITHER THE TRUST NOR ANY FUND IS A MUTUAL FUND OR ANY OTHER TYPE OF INVESTMENT COMPANY ASDEFINED IN THE INVESTMENT COMPANY ACT OF 1940, AS AMENDED (THE “1940 ACT”), AND NEITHER IS SUBJECT TOREGULATION THEREUNDER. SHAREHOLDERS DO NOT HAVE THE PROTECTIONS ASSOCIATED WITH OWNERSHIPOF SHARES IN AN INVESTMENT COMPANY REGISTERED UNDER THE 1940 ACT. SEE RISK FACTOR ENTITLED“SHAREHOLDERS DO NOT HAVE THE PROTECTIONS ASSOCIATED WITH OWNERSHIP OF SHARES IN ANINVESTMENT COMPANY REGISTERED UNDER THE 1940 ACT IN PART ONE OF THIS PROSPECTUS FOR MOREINFORMATION.

Each Fund continuously offers and redeems Shares only in large blocks of Shares known as “Creation Units”, each of which consists of50,000 Shares. Only Authorized Participants (as defined herein) may purchase and redeem Shares from a Fund and then only in Creation Units.An Authorized Participant is an entity that has entered into an Authorized Participant Agreement with the Trust and ProShare CapitalManagement LLC (the “Sponsor”). Shares are offered to Authorized Participants in Creation Units at each Fund’s respective NAV. AuthorizedParticipants may then offer to the public, from time to time, Shares from any Creation Unit they create at a per-Share market price. The form ofAuthorized Participant Agreement and the related Authorized Participant Procedures Handbook set forth the terms and conditions under whichan Authorized Participant may purchase or redeem a Creation Unit. Authorized Participants will not receive from any Fund, the Sponsor, or anyof their affiliates, any fee or other compensation in connection with their sale of Shares to the public. An Authorized Participant may receivecommissions or fees from investors who purchase Shares through their commission or fee-based brokerage accounts.

These securities have not been approved or disapproved by the United States Securities and Exchange Commission (the “SEC”)or any state securities commission nor has the SEC or any state securities commission passed upon the accuracy or adequacy of thisProspectus. Any representation to the contrary is a criminal offense.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATINGIN THIS POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSUREDOCUMENT.

February 23, 2022

The Shares are neither interests in nor obligations of the Sponsor, Wilmington Trust Company, or any of their respectiveaffiliates. The Shares are not insured by the Federal Deposit Insurance Corporation or any other governmental agency.

This Prospectus has two parts: the offered series disclosure and the general pool disclosure. These parts are bound together andare incomplete if not distributed together to prospective participants.

COMMODITY FUTURES TRADING COMMISSIONRISK DISCLOSURE STATEMENT

YOU SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TOPARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD BE AWARE THAT COMMODITY INTERESTTRADING CAN QUICKLY LEAD TO LARGE LOSSES AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLYREDUCE THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL.IN ADDITION, RESTRICTIONS ON REDEMPTIONS MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATIONIN THE POOL.

FURTHER, COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, ANDADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR THOSE POOLS THAT ARE SUBJECT TO THESECHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS.THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED TO THISPOOL, AT PAGES 54 THROUGH 56, AND A STATEMENT OF THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN,THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT, AT PAGES 54 THROUGH 55.

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATEYOUR PARTICIPATION IN THIS COMMODITY POOL. THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THISCOMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING A DESCRIPTIONOF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT, AT PAGES 10 THROUGH 36.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY TRADE FOREIGN FUTURES OR OPTIONSCONTRACTS. TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETSFORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT TO REGULATIONS WHICH OFFER DIFFERENTOR DIMINISHED PROTECTION TO THE POOL AND ITS PARTICIPANTS. FURTHER, UNITED STATES REGULATORYAUTHORITIES MAY BE UNABLE TO COMPEL THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIESOR MARKETS IN NON-UNITED STATES JURISDICTIONS WHERE TRANSACTIONS FOR THE POOL MAY BE EFFECTED.

SWAPS TRANSACTIONS, LIKE OTHER FINANCIAL TRANSACTIONS, INVOLVE A VARIETY OF SIGNIFICANTRISKS. THE SPECIFIC RISKS PRESENTED BY A PARTICULAR SWAP TRANSACTION NECESSARILY DEPEND UPON THETERMS OF THE TRANSACTION AND YOUR CIRCUMSTANCES. IN GENERAL, HOWEVER, ALL SWAPS TRANSACTIONSINVOLVE SOME COMBINATION OF MARKET RISK, CREDIT RISK, COUNTERPARTY CREDIT RISK, FUNDING RISK,LIQUIDITY RISK, AND OPERATIONAL RISK.

HIGHLY CUSTOMIZED SWAPS TRANSACTIONS IN PARTICULAR MAY INCREASE LIQUIDITY RISK, WHICH MAYRESULT IN A SUSPENSION OF REDEMPTIONS. HIGHLY LEVERAGED TRANSACTIONS MAY EXPERIENCE

SUBSTANTIAL GAINS OR LOSSES IN VALUE AS A RESULT OF RELATIVELY SMALL CHANGES IN THE VALUE ORLEVEL OF AN UNDERLYING OR RELATED MARKET FACTOR. IN EVALUATING THE RISKS AND CONTRACTUALOBLIGATIONS ASSOCIATED WITH A PARTICULAR SWAP TRANSACTION, IT IS IMPORTANT TO CONSIDER THAT ASWAP TRANSACTION MAY, IN CERTAIN INSTANCES, BE MODIFIED OR TERMINATED ONLY BY MUTUAL CONSENT OFTHE ORIGINAL PARTIES AND SUBJECT TO AGREEMENT ON INDIVIDUALLY NEGOTIATED TERMS. THEREFORE, ITMAY NOT BE POSSIBLE FOR THE COMMODITY POOL OPERATOR TO MODIFY, TERMINATE, OR OFFSET THE POOL’SOBLIGATIONS OR THE POOL’S EXPOSURE TO THE RISKS ASSOCIATED WITH A TRANSACTION PRIOR TO ITSSCHEDULED TERMINATION DATE.

THIS PROSPECTUS DOES NOT INCLUDE ALL OF THE INFORMATION OR EXHIBITS IN THE REGISTRATIONSTATEMENT OF THE TRUST. INVESTORS CAN READ AND COPY THE ENTIRE REGISTRATION STATEMENT AT THEPUBLIC REFERENCE FACILITIES MAINTAINED BY THE SEC IN WASHINGTON, D.C.

THE TRUST WILL FILE QUARTERLY AND ANNUAL REPORTS WITH THE SEC. INVESTORS CAN READ AND COPYTHESE REPORTS AT THE SEC PUBLIC REFERENCE FACILITIES IN WASHINGTON, D.C. PLEASE CALL THE SEC AT1-800-SEC-0330 FOR FURTHER INFORMATION.

THE FILINGS OF THE TRUST ARE POSTED AT THE SEC WEBSITE AT WWW.SEC.GOV.

REGULATORY NOTICES

NO DEALER, SALESMAN OR ANY OTHER PERSON HAS BEEN AUTHORIZED TO GIVE ANY INFORMATION OR TOMAKE ANY REPRESENTATION NOT CONTAINED IN THIS PROSPECTUS, AND, IF GIVEN OR MADE, SUCH OTHERINFORMATION OR REPRESENTATION MUST NOT BE RELIED UPON AS HAVING BEEN AUTHORIZED BY THE TRUST,ANY OF THE FUNDS, THE SPONSOR, THE AUTHORIZED PARTICIPANTS OR ANY OTHER PERSON.

THIS PROSPECTUS DOES NOT CONSTITUTE AN OFFER OR SOLICITATION TO SELL OR A SOLICITATION OF ANOFFER TO BUY, NOR SHALL THERE BE ANY OFFER, SOLICITATION, OR SALE OF THE SHARES IN ANY JURISDICTIONIN WHICH SUCH OFFER, SOLICITATION, OR SALE IS NOT AUTHORIZED OR TO ANY PERSON TO WHOM IT ISUNLAWFUL TO MAKE ANY SUCH OFFER, SOLICITATION, OR SALE.

AUTHORIZED PARTICIPANTS MAY BE REQUIRED TO DELIVER A PROSPECTUS WHEN TRANSACTING INSHARES. SEE “PLAN OF DISTRIBUTION” IN PART TWO OF THIS PROSPECTUS.

PROSHARES TRUST II

Table of Contents

Page

PART ONEOFFERED SERIES DISCLOSURE

SUMMARY 4Important Information About the Funds 4Overview 4The Oil Funds 5The Precious Metals Funds 5Purchases and Sales in the Secondary Market 6Creation and Redemption Transactions 6Breakeven Amounts 6Important Tax Information 7

RISK FACTOR SUMMARY 8Risks Related to All Funds 8Risks Related to the Oil Funds and Precious Metals Funds 9

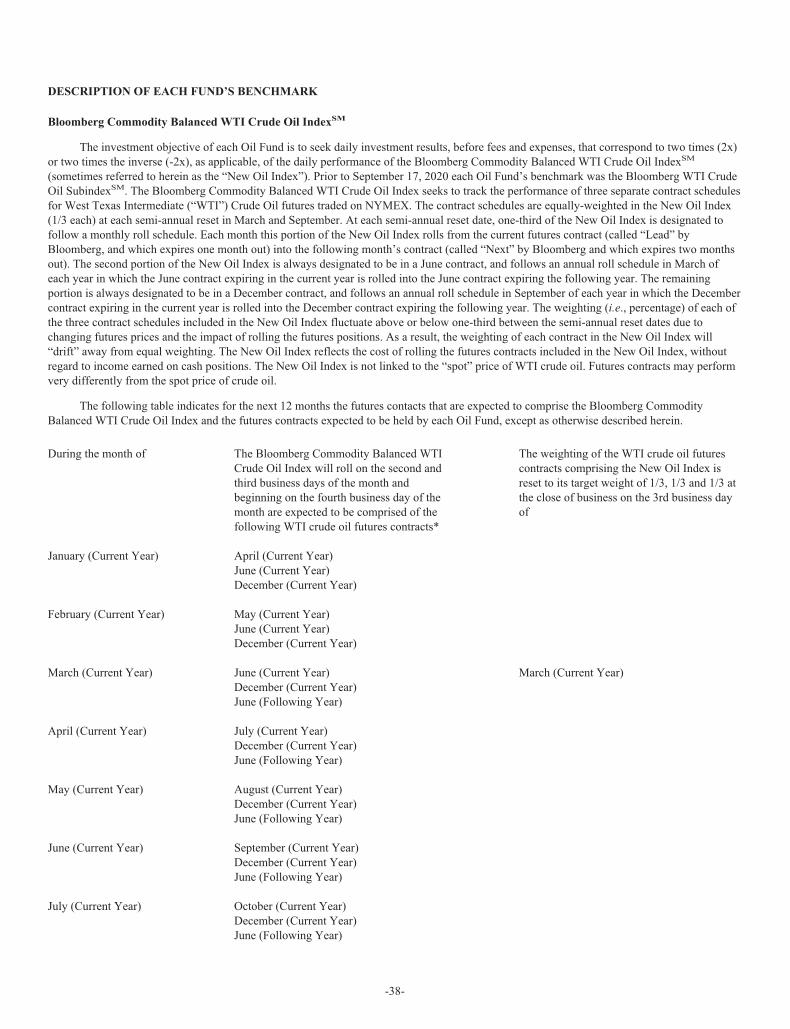

RISK FACTORS 10CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS 37DESCRIPTION OF EACH FUND’S BENCHMARK 38

Bloomberg Commodity Balanced WTI Crude Oil IndexSM 38Information About the Index Licensor 39

DESCRIPTION OF THE PRECIOUS METALS FUNDS’ BENCHMARKS 40Bloomberg Gold SubindexSM 40Information About the Index Licensor 41Bloomberg Silver SubindexSM 41Information About the Index Licensor 42

INVESTMENT OBJECTIVES AND PRINCIPAL INVESTMENT STRATEGIES 42Investment Objectives 42

PERFORMANCE OF THE OFFERED COMMODITY POOLS OPERATED BY THE COMMODITY POOL OPERATOR 50MANAGEMENT’S DISCUSSION AND ANALYSIS OFFINANCIAL CONDITION AND RESULTS OF OPERATIONS 53CHARGES 54

Breakeven Table 54MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONS 56

Status of the Funds 57U.S. Shareholders 58

-i-

Page

PART TWOGENERAL POOL DISCLOSURE

PERFORMANCE OF THE OTHER COMMODITY POOLSOPERATED BY THE COMMODITY POOL OPERATOR 67USE OF PROCEEDS 78WHO MAY SUBSCRIBE 78CREATION AND REDEMPTION OF SHARES 78

Creation Procedures 79Redemption Procedures 80Creation and Redemption Transaction Fee 81Special Settlement 81

LITIGATION 81DESCRIPTION OF THE SHARES; THE FUNDS; CERTAIN MATERIALTERMS OF THE TRUST AGREEMENT 82

Description of the Shares 82Principal Office; Location of Records; Fiscal Year 82The Funds 82The Trustee 83The Sponsor 83Duties of the Sponsor 86Ownership or Beneficial Interest in the Funds 86Management; Voting by Shareholders 86Recognition of the Trust and the Funds in Certain States 86Possible Repayment of Distributions Received by Shareholders 87Shares Freely Transferable 87Book-Entry Form 87Reports to Shareholders 87Net Asset Value (“NAV”) 87Indicative Optimized Portfolio Value (“IOPV”) 88Termination Events 88

DISTRIBUTIONS 88THE ADMINISTRATOR 88THE CUSTODIAN 89THE TRANSFER AGENT 89THE DISTRIBUTOR 89

Description of SEI 89THE SECURITIES DEPOSITORY; BOOK-ENTRY ONLY SYSTEM; GLOBAL SECURITY 89SHARE SPLITS OR REVERSE SPLITS 90CONFLICTS OF INTEREST 90MATERIAL CONTRACTS 91

Administration and Accounting Agreement 91Transfer Agency and Service Agreement 91Custody Agreement 92Distribution Agreement 92

PURCHASES BY EMPLOYEE BENEFIT PLANS 92General 92“Plan Assets” 93Ineligible Purchasers 93

-ii-

Page

PLAN OF DISTRIBUTION 94Buying and Selling Shares 94Authorized Participants 94Likelihood of Becoming a Statutory Underwriter 94General 94

LEGAL MATTERS 95EXPERTS 95WHERE INVESTORS CAN FIND MORE INFORMATION 95RECENT FINANCIAL INFORMATION AND ANNUAL REPORTS 95PRIVACY POLICY 95

The Trust’s Commitment to Investors 95The Information the Trust Collects About Investors 96How the Trust Handles Investors’ Personal Information 96How the Trust Safeguards Investors’ Personal Information 96

INCORPORATION BY REFERENCE OF CERTAIN DOCUMENTS 96FUTURES COMMISSION MERCHANTS 98

Litigation and Regulatory Disclosure Relating to FCMs 98Margin Levels Expected to be Held at the FCMs 159

SWAP COUNTERPARTIES 159Litigation and Regulatory Disclosure Relating to Swap Counterparties 159

APPENDIX A—GLOSSARY OF DEFINED TERMS A-1

-iii-

PART ONEOFFERED SERIES DISCLOSURE

SUMMARY

Investors should read the following summary together with the more detailed information in this Prospectus before investing in Shares ofany of the Funds, including the information under the caption “Risk Factors,” and all exhibits to this Prospectus and the informationincorporated by reference in this Prospectus, including the financial statements and the notes to those financial statements in the Trust’s AnnualReport on Form 10-K, and the Quarterly Reports on Form 10-Q, and Current Reports, if any, on Form 8-K. Please see the section entitled“Incorporation by Reference of Certain Documents” in Part Two of this Prospectus. Investors should also read any updated Prospectus,supplements to this Prospectus, notices and press releases, and other important information about the Funds which are posted on the Sponsor’swebsite at www.ProShares.com.

For ease of reference, any references throughout this Prospectus to various actions taken by any or all of the Funds are actually actionstaken by the Trust on behalf of such Funds.

The definitions of capitalized terms used in this Prospectus can be found in the Glossary of Defined Terms in Appendix A and throughoutthis Prospectus.

Important Information About the Funds

THE FUNDS PRESENT SIGNIFICANT RISKS NOT APPLICABLE TO OTHER TYPES OF FUNDS. THE FUNDS ARE NOTAPPROPRIATE FOR ALL INVESTORS. THE FUNDS USE LEVERAGE AND ARE RISKIER THAN SIMILARLY BENCHMARKEDEXCHANGE-TRADED FUNDS THAT DO NOT USE LEVERAGE. AN INVESTOR SHOULD ONLY CONSIDER AN INVESTMENTIN A FUND IF HE OR SHE UNDERSTANDS THE CONSEQUENCES OF SEEKING DAILY LEVERAGED OR DAILY INVERSELEVERAGED INVESTMENT RESULTS, INCLUDING THE IMPACT OF COMPOUNDING ON FUND PERFORMANCE.

THE RETURN OF A FUND FOR A PERIOD LONGER THAN A SINGLE DAY IS THE RESULT OF ITS RETURN FOR EACHDAY COMPOUNDED OVER THE PERIOD AND USUALLY WILL DIFFER IN AMOUNT AND POSSIBLY EVEN DIRECTIONFROM THE FUND’S STATED MULTIPLE TIMES THE RETURN OF THE FUND’S BENCHMARK FOR THE SAME PERIOD.THESE DIFFERENCES CAN BE SIGNIFICANT.

THE FUNDS’ INVESTMENTS MAY BE ILLIQUID AND/OR HIGHLY VOLATILE AND THE FUNDS MAY EXPERIENCELARGE LOSSES FROM BUYING, SELLING OR HOLDING SUCH INVESTMENTS. AN INVESTOR IN ANY OF THE FUNDSCOULD POTENTIALLY LOSE THE FULL PRINCIPAL VALUE OF HIS/HER INVESTMENT WITHIN A SINGLE DAY.

SHAREHOLDERS WHO INVEST IN THE FUNDS SHOULD ACTIVELY MANAGE AND MONITOR THEIR INVESTMENTS,AS FREQUENTLY AS DAILY.

Each Ultra Fund seeks daily investment results, before fees and expenses, that correspond to two times (2x) the performance of itsbenchmark for a single day, not for any other period. The UltraShort Fund seeks daily investment results, before fees and expenses, thatcorrespond to two times the inverse (-2x) of the performance of its benchmark for a single day, not for any other period. The return of a Fund fora period longer than a single day is the result of its return for each day compounded over the period and usually will differ in amount andpossibly even direction from the Fund’s stated multiple times the return of the Fund’s benchmark for the same period. These differences can besignificant. Daily compounding of a Fund’s investment returns can dramatically and adversely affect its longer-term performance especiallyduring periods of high volatility.

Volatility has a negative impact on Fund performance and the volatility of a Fund’s benchmark may be at least as important to the Fund’sreturn as the return of the Fund’s benchmark. Each of the Funds uses leverage and should produce returns for a single day that are more volatilethan that of its benchmark. For example, the return for a single day of an Ultra Fund with a 2x multiple should be approximately two times asvolatile for a single day as the return of a fund with an objective of matching the same benchmark. The return for a single day of the UltraShortFund with a -2x multiple should be approximately two times as volatile for a single day as the inverse of the return of a fund with an objective ofmatching the same benchmark.

Overview

Each Fund is listed below along with its respective benchmark:

-4-

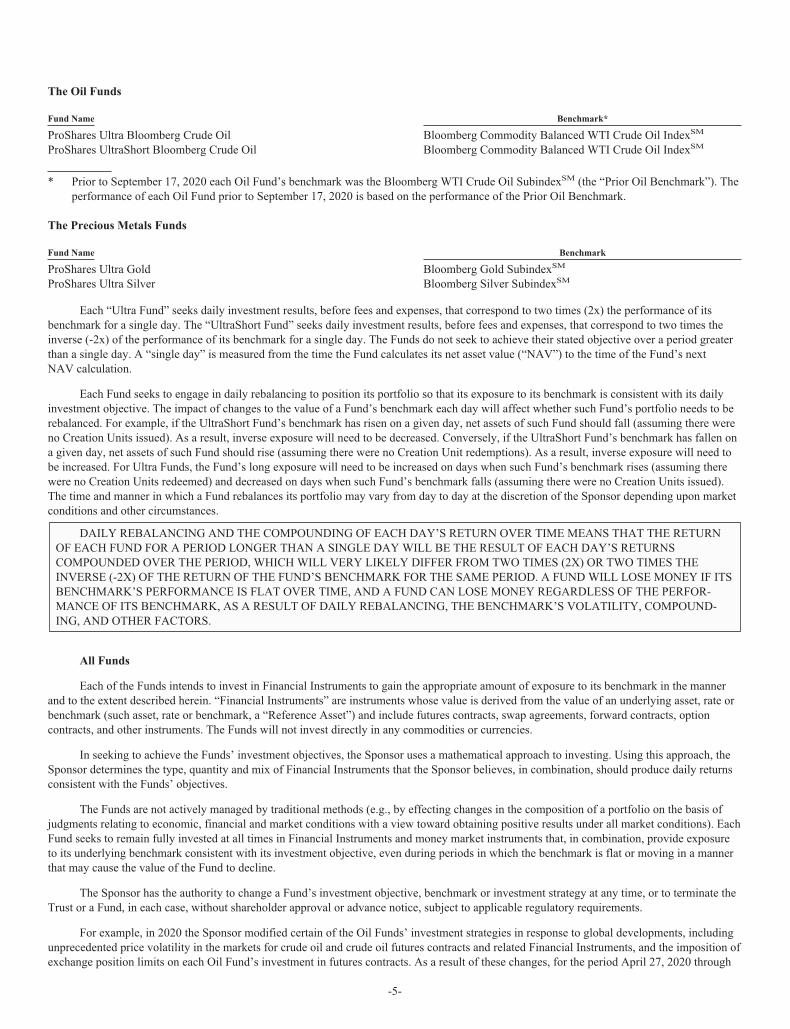

The Oil Funds

Fund Name Benchmark*

ProShares Ultra Bloomberg Crude Oil Bloomberg Commodity Balanced WTI Crude Oil IndexSM

ProShares UltraShort Bloomberg Crude Oil Bloomberg Commodity Balanced WTI Crude Oil IndexSM

* Prior to September 17, 2020 each Oil Fund’s benchmark was the Bloomberg WTI Crude Oil SubindexSM (the “Prior Oil Benchmark”). Theperformance of each Oil Fund prior to September 17, 2020 is based on the performance of the Prior Oil Benchmark.

The Precious Metals Funds

Fund Name Benchmark

ProShares Ultra Gold Bloomberg Gold SubindexSM

ProShares Ultra Silver Bloomberg Silver SubindexSM

Each “Ultra Fund” seeks daily investment results, before fees and expenses, that correspond to two times (2x) the performance of itsbenchmark for a single day. The “UltraShort Fund” seeks daily investment results, before fees and expenses, that correspond to two times theinverse (-2x) of the performance of its benchmark for a single day. The Funds do not seek to achieve their stated objective over a period greaterthan a single day. A “single day” is measured from the time the Fund calculates its net asset value (“NAV”) to the time of the Fund’s nextNAV calculation.

Each Fund seeks to engage in daily rebalancing to position its portfolio so that its exposure to its benchmark is consistent with its dailyinvestment objective. The impact of changes to the value of a Fund’s benchmark each day will affect whether such Fund’s portfolio needs to berebalanced. For example, if the UltraShort Fund’s benchmark has risen on a given day, net assets of such Fund should fall (assuming there wereno Creation Units issued). As a result, inverse exposure will need to be decreased. Conversely, if the UltraShort Fund’s benchmark has fallen ona given day, net assets of such Fund should rise (assuming there were no Creation Unit redemptions). As a result, inverse exposure will need tobe increased. For Ultra Funds, the Fund’s long exposure will need to be increased on days when such Fund’s benchmark rises (assuming therewere no Creation Units redeemed) and decreased on days when such Fund’s benchmark falls (assuming there were no Creation Units issued).The time and manner in which a Fund rebalances its portfolio may vary from day to day at the discretion of the Sponsor depending upon marketconditions and other circumstances.

DAILY REBALANCING AND THE COMPOUNDING OF EACH DAY’S RETURN OVER TIME MEANS THAT THE RETURNOF EACH FUND FOR A PERIOD LONGER THAN A SINGLE DAY WILL BE THE RESULT OF EACH DAY’S RETURNSCOMPOUNDED OVER THE PERIOD, WHICH WILL VERY LIKELY DIFFER FROM TWO TIMES (2X) OR TWO TIMES THEINVERSE (-2X) OF THE RETURN OF THE FUND’S BENCHMARK FOR THE SAME PERIOD. A FUND WILL LOSE MONEY IF ITSBENCHMARK’S PERFORMANCE IS FLAT OVER TIME, AND A FUND CAN LOSE MONEY REGARDLESS OF THE PERFOR-MANCE OF ITS BENCHMARK, AS A RESULT OF DAILY REBALANCING, THE BENCHMARK’S VOLATILITY, COMPOUND-ING, AND OTHER FACTORS.

All Funds

Each of the Funds intends to invest in Financial Instruments to gain the appropriate amount of exposure to its benchmark in the mannerand to the extent described herein. “Financial Instruments” are instruments whose value is derived from the value of an underlying asset, rate orbenchmark (such asset, rate or benchmark, a “Reference Asset”) and include futures contracts, swap agreements, forward contracts, optioncontracts, and other instruments. The Funds will not invest directly in any commodities or currencies.

In seeking to achieve the Funds’ investment objectives, the Sponsor uses a mathematical approach to investing. Using this approach, theSponsor determines the type, quantity and mix of Financial Instruments that the Sponsor believes, in combination, should produce daily returnsconsistent with the Funds’ objectives.

The Funds are not actively managed by traditional methods (e.g., by effecting changes in the composition of a portfolio on the basis ofjudgments relating to economic, financial and market conditions with a view toward obtaining positive results under all market conditions). EachFund seeks to remain fully invested at all times in Financial Instruments and money market instruments that, in combination, provide exposureto its underlying benchmark consistent with its investment objective, even during periods in which the benchmark is flat or moving in a mannerthat may cause the value of the Fund to decline.

The Sponsor has the authority to change a Fund’s investment objective, benchmark or investment strategy at any time, or to terminate theTrust or a Fund, in each case, without shareholder approval or advance notice, subject to applicable regulatory requirements.

For example, in 2020 the Sponsor modified certain of the Oil Funds’ investment strategies in response to global developments, includingunprecedented price volatility in the markets for crude oil and crude oil futures contracts and related Financial Instruments, and the imposition ofexchange position limits on each Oil Fund’s investment in futures contracts. As a result of these changes, for the period April 27, 2020 through

-5-

September 17, 2020, the Oil Funds invested in longer dated futures contracts than the futures contracts included in their benchmark at the time(i.e., the Prior Oil Benchmark).

ProShare Capital Management LLC, a Maryland limited liability company, serves as the Trust’s Sponsor and commodity pool operator.The principal office of the Sponsor and the Funds is located at 7272 Wisconsin Avenue, 21st Floor, Bethesda, Maryland 20814. The telephonenumber of the Sponsor and each of the Funds is (240) 497-6400.

Purchases and Sales in the Secondary Market

The Shares of each Fund are listed on NYSE Arca, Inc. (the “Exchange”) under the ticker symbols shown on the front cover of thisProspectus. Secondary market purchases and sales of Shares are subject to ordinary brokerage commissions and charges.

Creation and Redemption Transactions

Only an Authorized Participant may purchase (i.e., create) or redeem Shares with the Funds. Authorized Participants may create andredeem Shares only in large blocks of Shares known as “Creation Units”, each of which consists of 50,000 Shares. An “Authorized Participant”is an entity that has entered into an Authorized Participant Agreement with the Trust and the Sponsor. Creation Units are offered to AuthorizedParticipants at each Fund’s NAV. Creation Units in a Fund are expected to be created when there is sufficient demand for Shares in such Fundthat the market price per Share is at a premium to the NAV per Share. Authorized Participants will likely sell such Shares to the public at pricesthat are expected to reflect, among other factors, the trading price of the Shares of such Fund and the supply of and demand for the Shares at thetime of sale. Similarly, it is expected that Creation Units in a Fund will be redeemed when the market price per Share of such Fund is at adiscount to the NAV per Share. The Sponsor expects that the exploitation of such arbitrage opportunities by Authorized Participants and theirclients will tend to cause the public trading price of the Shares to track the NAV per Share of a Fund over time, though there can be noguarantees this will be the case. Retail investors seeking to purchase or sell Shares on any day effect such transactions in the secondary market atthe market price per Share, rather than in connection with the creation or redemption of Creation Units.

A creation transaction, which is subject to acceptance by SEI Investments Distribution Co. (“SEI” or the “Distributor”), generally takesplace when an Authorized Participant deposits a specified amount of cash (unless as provided otherwise in this Prospectus) in exchange for aspecified number of Creation Units. Similarly, Shares can be redeemed only in Creation Units, generally for cash (unless as provided otherwisein this Prospectus). Except when aggregated in Creation Units, Shares are not redeemable. The prices at which creations and redemptions occurare based on the next calculation of the NAV after an order is received in proper form, as described in the Authorized Participant Agreement andthe related Authorized Participant Procedures Handbook. From time to time the Sponsor, in its sole discretion, may impose limits on the numberof Creation Units that may be created each day by each Authorized Participant, or on the total number of Creation Units that may be created byall Authorized Participants on such day, or may suspend the purchase and/or redemption of Creation Units altogether. For example, the Sponsormay impose such limits or suspension if it believes doing so would help a Fund manage its portfolio, such as by allowing a Fund to comply withcounterparty or position limits, or to manage or otherwise comply with Share registration requirements, or in response to significant and/or rapidincreases in the size of a Fund as a result of an increase in creation activity. The manner by which Creation Units are purchased and redeemed isgoverned by the terms of this Prospectus, the Authorized Participant Agreement and Authorized Participant Procedures Handbook. Creation andredemption orders are not effective until accepted by the Distributor and may be rejected or revoked. By placing a purchase order, an AuthorizedParticipant agrees to deposit cash (unless as provided otherwise in this Prospectus) with The Bank of New York Mellon (“BNYM”, the“Custodian”, the “Transfer Agent” and the “Administrator”), acting in its capacity as custodian of the Funds.

Creation and redemption transactions must be placed each day with SEI by the create/redeem cut-off time (stated below) to receive thatday’s NAV. The Sponsor may require orders to be placed earlier if, for example, the Exchange or other exchange material to the valuation oroperation of such Fund closes before such cut-off time. Because the primary trading session for the commodities and/or futures contractsunderlying certain of the Funds have different closing (or fixing) times than U.S. Equity markets, the create/redeem cut-off time and NAVcalculation time for each Fund may differ. See the section entitled “Net Asset Value” for additional information about the NAV calculations.

Fund Create/Redeem Cut-off NAV Calculation Time

ProShares Ultra Silver (AGQ) 1:00 p.m. (Eastern Time) 1:25 p.m. (Eastern Time)ProShares Ultra Gold (UGL) 1:00 p.m. (Eastern Time) 1:30 p.m. (Eastern Time)ProShares Ultra Bloomberg Crude Oil (UCO) 2:00 p.m. (Eastern Time) 2:30 p.m. (Eastern Time)ProShares UltraShort Bloomberg Crude Oil (SCO) 2:00 p.m. (Eastern Time) 2:30 p.m. (Eastern Time)

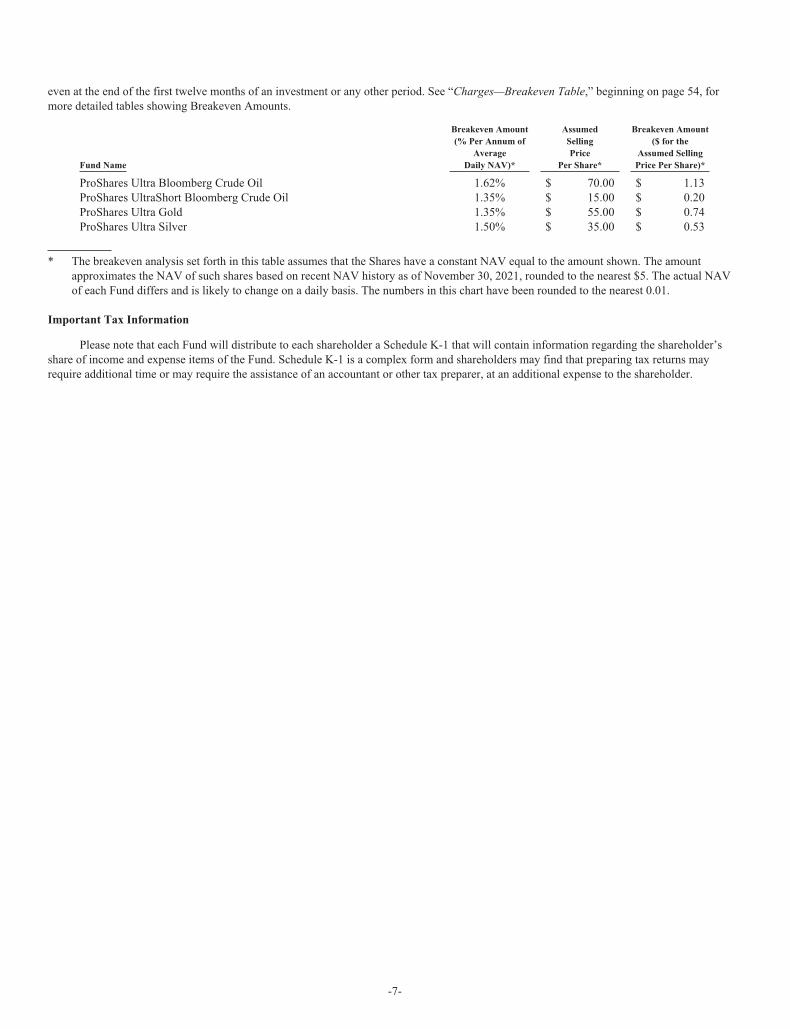

Breakeven Amounts

A Fund will be profitable only if returns from the Fund’s investments exceed its “breakeven amount.” Estimated breakeven amounts areset forth in the table below. The estimated breakeven amounts represent the estimated amount of trading income that each Fund would need toachieve during one year to offset the Fund’s estimated fees, costs and expenses, net of any interest income earned by the Fund on itsinvestments. Estimated amounts do not represent actual results, which may be different. It is not possible to predict whether a Fund will break

-6-

even at the end of the first twelve months of an investment or any other period. See “Charges—Breakeven Table,” beginning on page 54, formore detailed tables showing Breakeven Amounts.

Fund Name

Breakeven Amount(% Per Annum of

AverageDaily NAV)*

AssumedSellingPrice

Per Share*

Breakeven Amount($ for the

Assumed SellingPrice Per Share)*

ProShares Ultra Bloomberg Crude Oil 1.62% $ 70.00 $ 1.13ProShares UltraShort Bloomberg Crude Oil 1.35% $ 15.00 $ 0.20ProShares Ultra Gold 1.35% $ 55.00 $ 0.74ProShares Ultra Silver 1.50% $ 35.00 $ 0.53

* The breakeven analysis set forth in this table assumes that the Shares have a constant NAV equal to the amount shown. The amountapproximates the NAV of such shares based on recent NAV history as of November 30, 2021, rounded to the nearest $5. The actual NAVof each Fund differs and is likely to change on a daily basis. The numbers in this chart have been rounded to the nearest 0.01.

Important Tax Information

Please note that each Fund will distribute to each shareholder a Schedule K-1 that will contain information regarding the shareholder’sshare of income and expense items of the Fund. Schedule K-1 is a complex form and shareholders may find that preparing tax returns mayrequire additional time or may require the assistance of an accountant or other tax preparer, at an additional expense to the shareholder.

-7-

RISK FACTOR SUMMARY

Risks Related to All Funds

• The use of leveraged or inverse leveraged positions increases risk and could result in the total loss of an investor’s investment within asingle day.

• Due to the compounding of daily returns, each Fund’s returns over periods longer than a single day will likely differ in amount and possiblyeven direction from the Fund’s stated multiple times the return of its benchmark for such period.

• Intraday price performance of Fund shares will likely differ from the Fund’s stated multiple times the performance of its benchmark forsuch day.

• There is no guarantee that any Fund will achieve its investment objective.

• Historical average volatility does not predict future volatility, which may be significantly higher or lower than historical averages.

• In order to achieve a high degree of correlation with their applicable underlying benchmarks, the Funds seek to rebalance their portfoliosdaily to keep exposure consistent with their respective investment objectives.

• Each Fund seeks to achieve its investment objective even during periods when the performance of the Fund’s benchmark is flat or when thebenchmark is moving in a manner that may cause the value of the Fund to decline.

• Shareholders’ tax liability may exceed cash distributions on the Shares.

• Investors in the Funds may be exposed to various tax risks, as described in further detail below.

• Potential negative impact from rolling futures positions; there have been extended periods in the past where the investment strategies utilizedby the Funds have caused significant and sustained losses.

• The number of underlying components included in a Fund’s benchmark may impact the volatility of such benchmark, which could adverselyaffect an investment in the Shares.

• Possible illiquid markets may cause or exacerbate losses: the large size of the positions the Funds may acquire increases these risks.

• Changes implemented by the benchmark provider that affect the composition and valuation of the benchmark could negatively impact theperformance of the benchmark and therefore the performance of the Funds.

• The particular benchmark used by a Fund may underperform other asset classes and may underperform other indices or benchmarks basedupon the same underlying Reference Asset.

• A Fund may change its investment objective, benchmark and investment strategies, and/or may terminate, at any time without share-holder approval.

• Financial markets, including the benchmark and Financial Instruments used by a Fund and Fund Shares may be subject to unusual tradingactivity, volatility, and potential fraud and/or manipulation by third parties, which could have a negative impact on the performance of thebenchmark and the Fund or the liquidity and price of Fund Shares.

• Historical correlation trends between Fund benchmarks and other asset classes may not continue or may reverse, limiting or eliminating anypotential diversification or other benefit from owning a Fund.

• Benchmark changes and market transactions, including the daily rebalancing of futures contracts by the Funds may have a significant impacton the performance of the benchmark and the Funds and the trading, liquidity and price of Fund Shares.

• The lack of active trading markets for the Shares may result in losses upon the sale of such Shares.

• Investors may be adversely affected by redemption or creation orders that are subject to postponement, limits, suspension or rejection undercertain circumstances.

• Purchases Creation Units by Authorized Participants may be limited or suspended by the Sponsor in its sole discretion. For example, theSponsor may limit or suspend the purchase of Creation Units if it believes doing so would help a Fund manage its portfolio such as by allow-ing it to comply with counterparty or position limits, or to manage or otherwise comply with Share registration requirements, or in responseto significant and/or rapid increases in the size of a Fund as a result of an increase in creation activity. This may, among other things, causeFund Shares to trade at a premium to NAV or otherwise have a negative impact on the liquidity and trading of Fund shares.

• The NAV per Share may not correspond to the market price per Share.

-8-

• Investors may be adversely affected by an overstatement or understatement of a Fund’s NAV due to the valuation method employed or errorsin the NAV calculation.

• The liquidity of the Shares may also be affected by the withdrawal from participation of Authorized Participants, which could adverselyaffect the market price of the Shares.

• Shareholders that are not Authorized Participants may only purchase or sell their Shares in secondary trading markets, and the conditionsassociated with trading in secondary markets may adversely affect investors’ investment in the Shares.

• A Fund’s listing exchange may halt trading in the Shares of a Fund which would adversely impact investors’ ability to sell Shares and couldlead to investor losses.

• Shareholders do not have the protections associated with ownership of shares in an investment company registered under the 1940 Act.

• Regulatory and exchange daily price limits, position limits and accountability levels may cause the Sponsor restrict the creation of CreationUnits, which could have a negative impact on the operation of each Fund, prevent a Fund from achieving its investment objective, and disruptsecondary market trading of Fund Shares.

• The use of futures contracts may expose the Funds to liquidity and other risks, which could result in significant loss to the Funds.

• Margin requirements and position limits applicable to futures contracts and swaps and the availability of and market required by swapcounterparties may limit a Fund’s ability to achieve sufficient exposure and prevent a Fund from achieving its investment objective.

• The insolvency of a futures commission merchant (“FCM”) or clearinghouse or the failure of an FCM or clearinghouse to properly segregateFund assets held as margin on futures transactions may result in losses to the Funds.

• A Fund’s performance could be adversely affected if an FCM reduces its internal risk limits for the Fund.

• The use of swap agreements may expose the Funds to liquidity risk, counterparty credit risk and other risks, which could result in significantloss to the Funds.

• The use of derivatives, such as swap agreements and forward contracts, exposes the Funds to counterparty credit risks.

• The use of options strategies may expose the Funds to significant loss and liquidity, counterparty and other risks. The use of an options strat-egy is costly and may not protect a Fund.

• Natural disasters and public health disruptions, such as the COVID-19 Virus, may have a significant negative impact on the performance ofeach Fund.

Risks Related to the Oil Funds and Precious Metals Funds

• A number of factors may have a negative impact on the price of commodities, such as oil, gold and silver, and the price of Financial Instru-ments based on such commodities.

• The Oil Funds are linked to an index of crude oil futures contracts, and are not directly linked to the “spot” price of crude oil. Oil futures con-tracts may perform very differently from the spot price of crude oil.

• The Precious Metals Funds do not hold gold or silver bullion. Rather, the Precious Metals Funds use Financial Instruments to gain exposureto gold or silver bullion. Using Financial Instruments to obtain exposure to gold or silver bullion may cause tracking error and subject thePrecious Metals Funds to the effects of contango and backwardation as described herein.

• In April 2020, the market for crude oil futures contracts experienced a period of “extraordinary contango” (the spot price for a commodity issignificantly lower than the price of the futures contract in that commodity) that resulted in a negative price in the May 2020 WTI crude oilfutures contract. If all or a significant portion of the futures contracts held by the Oil Funds at a future date were to reach a negative price,investors in any such Fund could lose their entire investment.

-9-

RISK FACTORS

Investing in the Funds involves significant risks not applicable to other types of investments. The Funds may be highly volatile andyou could potentially lose the full principal value of your investment within a single day. Before you decide to purchase any Shares, youshould consider carefully the risks described below together with all of the other information included in this Prospectus, as well asinformation found in documents incorporated by reference in this Prospectus. These risk factors may be amended, supplemented orsuperseded from time to time by risk factors contained in any periodic report, prospectus supplement, post-effective amendment or in otherreports filed with the SEC in the future.

The assets that the Funds invest in can be highly volatile and the Funds may experience sudden and large losses when buying,selling or holding such instruments; you can lose all of your investment within a single day.

Investments linked to commodity or currency markets can be highly volatile compared to investments in traditional securities and theFunds may experience sudden and large losses. These markets may fluctuate widely based on a variety of factors including changes in overallmarket movements, political and economic events, wars, acts of terrorism, natural disasters (including disease, epidemics and pandemics) andchanges in interest rates or inflation rates. High volatility may have an adverse impact on the performance of the Funds. An investor in any of theFunds could potentially lose the full principal value of his or her investment within a single day.

Important Information about the Oil Funds.Global developments affecting crude oil markets and the markets for crude oil futurescontracts and related Financial Instruments, have caused unprecedented volatility. This has resulted in, among other things, a negative price forthe May 2020 WTI crude oil futures contract and significant volatility in the performance and trading price of each Oil Fund. Investors inoil-related products, including the Oil Funds, could suffer rapid and significant losses on their investments, including the possibility of total loss,especially in light of recent market conditions. For example, if all or a significant portion of the futures contracts held by the Ultra Crude OilFund at a future date were to reach a negative price, investors in the Fund could lose their entire investment with little or no warning. If suchevent were to occur, and the price of WTI crude oil futures contracts subsequently reversed, investors in the Short Crude Oil Fund could suffersignificant losses or lose their entire investment.

The use of leveraged or inverse leveraged positions increases risk and could result in the total loss of an investor’s investment within asingle day.

Each Fund utilizes leverage in seeking to achieve its investment objective and will lose more money in market environments adverse to itsdaily investment objective than funds that do not employ leverage. The use of leveraged and/or inverse leveraged positions increases risk andcould result in the total loss of an investor’s investment within a single day. The more a Fund invests in leveraged positions, the more thisleverage will magnify any losses on those investments. A Fund’s investments in leveraged positions generally requires a small investmentrelative to the amount of investment exposure assumed. As a result, such investments may give rise to losses that far exceed the amount investedin those instruments.

For example, because the Ultra Funds and the UltraShort Fund offered hereby include a two times (2x) or a two times inverse (-2x)multiplier, a single-day movement in the benchmark for one of these Funds approaching 50% at any point in the day could result in the total lossor almost total loss of an investment in such Fund if that movement is contrary to the investment objective of the Fund. This would be the casewith downward single-day or intraday movements in the underlying benchmark of an Ultra Fund or upward single day or intraday movements inthe benchmark of an UltraShort Fund even if the underlying benchmark maintains a level greater than zero at all times and even if thebenchmark subsequently moves in an opposite direction, eliminating all or a portion of the prior adverse movement. It is not possible to predictwhen sudden large changes in the daily movement of a benchmark may occur.

Due to the compounding of daily returns, each Fund’s returns over periods longer than a single day will likely differ in amount and possiblyeven direction from the Fund’s stated multiple times the return of its benchmark for such period.

Each of the Funds is “geared” which means that each has an investment objective to seek daily investment results, before fees andexpenses, that correspond either to two times (2x) or two times the inverse (-2x) of the performance of a benchmark for a single day, not for anyother period. A single day is measured from the time a Fund calculates its respective NAV to the time of the Fund’s next NAV calculation. TheNAV calculation times for the Funds typically range from 1:25 p.m. to 4:00 p.m. (Eastern Time); please see the section entitled“Summary—Creation and Redemption Transactions” for additional details on the NAV calculation times for the Funds. The return of a Fund fora period longer than a single day is the result of its return for each day compounded over the period, and usually will differ from two times (2x)or two times the inverse (-2x) of the return of the Fund’s benchmark for the same period. Compounding is the cumulative effect of applyinginvestment gains and losses and income to the principal amount invested over time. Gains or losses experienced over a given period will increaseor reduce the principal amount invested from which the subsequent period’s returns are calculated. The effects of compounding will likely causethe performance of a Fund to differ from the Fund’s stated multiple times the return of its benchmark for the same period. The effect ofcompounding becomes more pronounced as benchmark volatility and holding period increase. The impact of compounding will impact eachshareholder differently depending on the period of time an investment in a Fund is held and the volatility of the benchmark during the holdingperiod of an investment in the Fund.

-10-

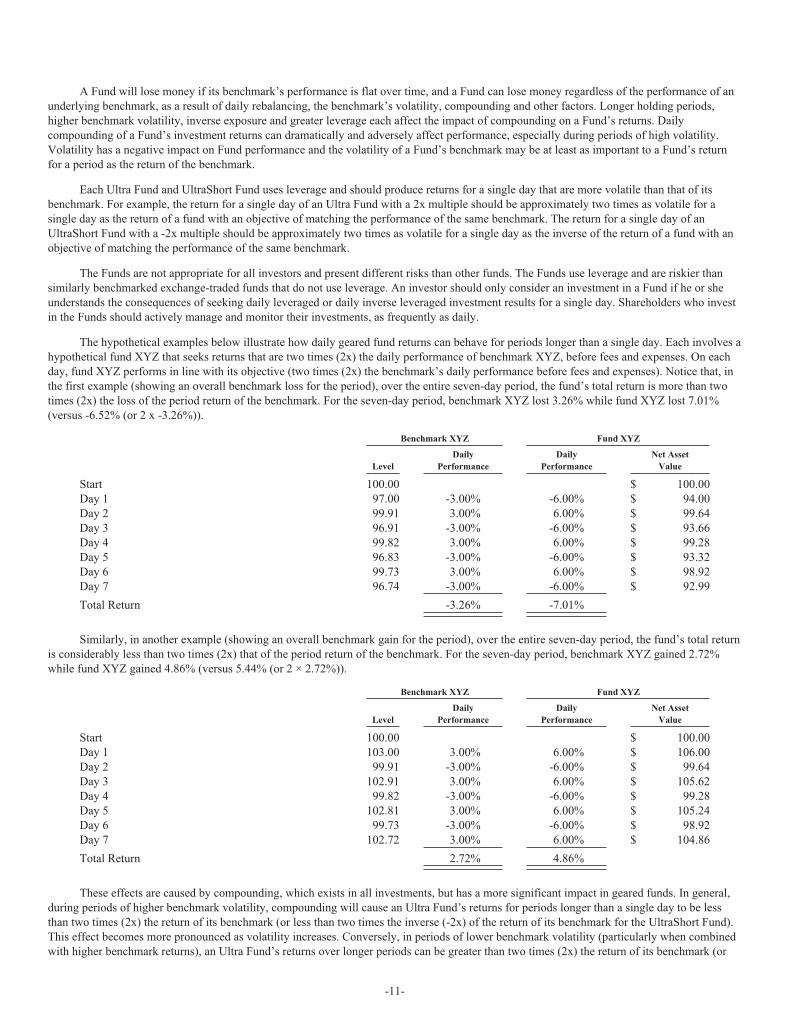

A Fund will lose money if its benchmark’s performance is flat over time, and a Fund can lose money regardless of the performance of anunderlying benchmark, as a result of daily rebalancing, the benchmark’s volatility, compounding and other factors. Longer holding periods,higher benchmark volatility, inverse exposure and greater leverage each affect the impact of compounding on a Fund’s returns. Dailycompounding of a Fund’s investment returns can dramatically and adversely affect performance, especially during periods of high volatility.Volatility has a negative impact on Fund performance and the volatility of a Fund’s benchmark may be at least as important to a Fund’s returnfor a period as the return of the benchmark.

Each Ultra Fund and UltraShort Fund uses leverage and should produce returns for a single day that are more volatile than that of itsbenchmark. For example, the return for a single day of an Ultra Fund with a 2x multiple should be approximately two times as volatile for asingle day as the return of a fund with an objective of matching the performance of the same benchmark. The return for a single day of anUltraShort Fund with a -2x multiple should be approximately two times as volatile for a single day as the inverse of the return of a fund with anobjective of matching the performance of the same benchmark.

The Funds are not appropriate for all investors and present different risks than other funds. The Funds use leverage and are riskier thansimilarly benchmarked exchange-traded funds that do not use leverage. An investor should only consider an investment in a Fund if he or sheunderstands the consequences of seeking daily leveraged or daily inverse leveraged investment results for a single day. Shareholders who investin the Funds should actively manage and monitor their investments, as frequently as daily.

The hypothetical examples below illustrate how daily geared fund returns can behave for periods longer than a single day. Each involves ahypothetical fund XYZ that seeks returns that are two times (2x) the daily performance of benchmark XYZ, before fees and expenses. On eachday, fund XYZ performs in line with its objective (two times (2x) the benchmark’s daily performance before fees and expenses). Notice that, inthe first example (showing an overall benchmark loss for the period), over the entire seven-day period, the fund’s total return is more than twotimes (2x) the loss of the period return of the benchmark. For the seven-day period, benchmark XYZ lost 3.26% while fund XYZ lost 7.01%(versus -6.52% (or 2 x -3.26%)).

Benchmark XYZ Fund XYZ

LevelDaily

PerformanceDaily

PerformanceNet Asset

Value

Start 100.00 $ 100.00Day 1 97.00 -3.00% -6.00% $ 94.00Day 2 99.91 3.00% 6.00% $ 99.64Day 3 96.91 -3.00% -6.00% $ 93.66Day 4 99.82 3.00% 6.00% $ 99.28Day 5 96.83 -3.00% -6.00% $ 93.32Day 6 99.73 3.00% 6.00% $ 98.92Day 7 96.74 -3.00% -6.00% $ 92.99

Total Return -3.26% -7.01%

Similarly, in another example (showing an overall benchmark gain for the period), over the entire seven-day period, the fund’s total returnis considerably less than two times (2x) that of the period return of the benchmark. For the seven-day period, benchmark XYZ gained 2.72%while fund XYZ gained 4.86% (versus 5.44% (or 2 × 2.72%)).

Benchmark XYZ Fund XYZ

LevelDaily

PerformanceDaily

PerformanceNet Asset

Value

Start 100.00 $ 100.00Day 1 103.00 3.00% 6.00% $ 106.00Day 2 99.91 -3.00% -6.00% $ 99.64Day 3 102.91 3.00% 6.00% $ 105.62Day 4 99.82 -3.00% -6.00% $ 99.28Day 5 102.81 3.00% 6.00% $ 105.24Day 6 99.73 -3.00% -6.00% $ 98.92Day 7 102.72 3.00% 6.00% $ 104.86

Total Return 2.72% 4.86%

These effects are caused by compounding, which exists in all investments, but has a more significant impact in geared funds. In general,during periods of higher benchmark volatility, compounding will cause an Ultra Fund’s returns for periods longer than a single day to be lessthan two times (2x) the return of its benchmark (or less than two times the inverse (-2x) of the return of its benchmark for the UltraShort Fund).This effect becomes more pronounced as volatility increases. Conversely, in periods of lower benchmark volatility (particularly when combinedwith higher benchmark returns), an Ultra Fund’s returns over longer periods can be greater than two times (2x) the return of its benchmark (or

-11-

greater than two times the inverse (-2x) of the return of its benchmark for the UltraShort Fund). Actual results for a particular period are alsodependent on the magnitude of the benchmark return in addition to the benchmark volatility. Similar effects exist for the UltraShort Fund, andthe significance of these effects may be even greater with such inverse leveraged or leveraged funds.

The graphs that follow illustrate this point. Each of the graphs shows a simulated hypothetical one-year performance of a benchmarkcompared with the performance of a geared fund that perfectly achieves its geared daily investment objective. The graphs demonstrate that, forperiods greater than a single day, a geared fund is likely to underperform or overperform (but not match) the benchmark performance (or theinverse of the benchmark performance) times the multiple stated as the daily fund objective. Investors should understand the consequences ofholding daily rebalanced funds for periods longer than a single day and should actively manage and monitor their investments, as frequently asdaily. A one-year period is used solely for illustrative purposes. Deviations from the benchmark return (or the inverse of the benchmark return)times the fund multiple can occur over periods as short as two days (each day as measured from NAV to NAV) and may also occur in periods ofa single day, or even intra-day. To isolate the impact of daily leveraged or inverse leveraged exposure, these graphs assume: a) no fund expensesor transaction costs; b) borrowing/lending rates of zero percent (to obtain required leveraged or inverse leveraged exposure) and cashreinvestment rates of zero percent; and c) the fund consistently maintaining perfect exposure (-2x or 2x) as of the fund’s NAV time each day. Ifthese assumptions were different, the fund’s performance would be different than that shown. If fund expenses, transaction costs and financingexpenses greater than zero percent were included, the fund’s performance would also be different than shown. Each of the graphs also assumes avolatility rate of 35% which is an approximate average of the five-year historical volatility rate of the most volatile benchmark referenced herein(the daily performance of Bloomberg Commodity Balanced WTI Crude Oil Index) as of November 30, 2021. A benchmark’s volatility rate is astatistical measure of the magnitude of fluctuations in its returns.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS. NO REPRESENTATION IS BEINGMADE THAT ANY BENCHMARK OR FUND WILL OR IS LIKELY TO ACHIEVE GAINS OR LOSSES SIMILAR TO THOSE SHOWNOR WILL EXPERIENCE VOLATILITY SIMILAR TO THAT SHOWN. THE INFORMATION PROVIDED IN THE CHART BELOW ISFOR ILLUSTRATIVE PURPOSES ONLY.

One-Year Simulation; Benchmark Flat (0%)

(Annualized Benchmark Volatility 35%)

0%

20%

40%

60%

-20%

-40%

-60%

On

e Y

ea

r in

de

x R

etu

rn

Index Return 0.0% +2X Fund Return -11.5% -2X Fund Return -30.7%

The graph above shows a scenario where the benchmark, which exhibits day-to-day volatility, is flat or trendless over the year (i.e.,provides a return of 0% over the course of the year), but the Ultra Fund (2x) and the UltraShort Fund (-2x) are both down.

-12-

One-Year Simulation; Benchmark Down 28%

(Annualized Benchmark Volatility 35%)

0%

20%

40%

60%

-20%

-40%

-60%

On

e Y

ea

r in

de

x R

etu

rn

Index Return -28.0% +2X Fund Return -54.2% -2X Fund Return 34.0%

The graph above shows a scenario where the benchmark, which exhibits day-to-day volatility, is down over the year, but the Ultra Fund(2x) is down less than two times the benchmark and the UltraShort Fund (-2x) is up less than two times the inverse of the benchmark.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS. NO REPRESENTATION IS BEINGMADE THAT ANY BENCHMARK OR FUND WILL OR IS LIKELY TO ACHIEVE GAINS OR LOSSES SIMILAR TO THOSE SHOWNOR WILL EXPERIENCE VOLATILITY SIMILAR TO THAT SHOWN. THE INFORMATION PROVIDED IN THE CHART BELOW ISFOR ILLUSTRATIVE PURPOSES ONLY.

One-Year Simulation; Benchmark Up 28%

(Annualized Benchmark Volatility 35%)

0%

25%

50%

75%

100%

125%

150%

-25%

-50%

-75%

On

e Y

ea

r in

de

x R

etu

rn

Index Return 28.0% +2X Fund Return 45.0% -2X Fund Return -57.9%

The graph above shows a scenario where the benchmark, which exhibits day-to-day volatility, is up over the year, but the Ultra Fund (2x)is up less than two times the benchmark and the UltraShort Fund (-2x) is down more than two times the inverse of the benchmark.

The historical five-year average volatility of the benchmarks utilized by the Funds ranges from 14.44% to 34.94% as of November 30,2021, as set forth in the table below.

-13-

Benchmark

HistoricalFive-Year

Average VolatilityRate as of

November 30, 2021

Bloomberg Commodity Balanced WTI Crude Oil SubindexSM* 34.94%Bloomberg Gold SubindexSM 14.44%Bloomberg Silver SubindexSM 28.91%

* Prior to September 17, 2020, each Oil Fund’s benchmark was the Bloomberg WTI Crude Oil Subindex (sometimes referred to herein as the“Prior Oil Index”). Effective September 17, 2020, each Oil Fund’s benchmark is the Bloomberg Commodity Balanced WTI Crude OilIndexSM

Historical average volatility does not predict future volatility, which may be significantly higher or lower than historical averages.

Fund performance for periods greater than a single day can be estimated given any set of assumptions for the following factors: a)benchmark volatility; b) benchmark performance; c) period of time; d) financing rates associated with leveraged exposure; and e) other Fundexpenses. The tables below illustrate the impact of two factors that affect a geared fund’s performance: benchmark volatility and benchmarkreturn. Benchmark volatility is a statistical measure of the magnitude of fluctuations in the returns of a benchmark and is calculated as thestandard deviation of the natural logarithms of one plus the benchmark return (calculated daily), multiplied by the square root of the number oftrading days per year (assumed to be 252). The tables show estimated fund returns for a number of combinations of benchmark volatility andbenchmark return over a one-year period. To isolate the impact of daily leveraged or inverse leveraged exposure, these graphs assume: a) nofund expenses or transaction costs; b) borrowing/lending rates of zero percent (to obtain required leveraged or inverse leveraged exposure) andcash reinvestment rates of zero percent; and c) the fund consistently maintaining perfect exposure (2x or -2x) as of the fund’s NAV time eachday. If these assumptions were different, the fund’s performance would be different than that shown. If fund expenses, transaction costs andfinancing expenses were included, the fund’s performance would be different than that shown.

The first table below shows an example in which a geared fund has an investment objective to correspond (before fees and expenses) totwo times (2x) the daily performance of a benchmark. The geared fund could incorrectly be expected to achieve a 20% return on a yearly basis ifthe benchmark return was 10%, absent the effects of compounding. However, as the table shows, with a benchmark volatility of 40%, such afund would return 3.1%. In the charts below, shaded areas represent those scenarios where a geared fund with the investment objective describedwill outperform (i.e., return more than) the benchmark performance times the stated multiple in the fund’s investment objective; conversely,areas not shaded represent those scenarios where the fund will underperform (i.e., return less than) the benchmark performance times themultiple stated as the daily fund objective.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS. NO REPRESENTATION IS BEINGMADE THAT ANY BENCHMARK OR FUND WILL OR IS LIKELY TO ACHIEVE GAINS OR LOSSES SIMILAR TO THOSE SHOWNOR WILL EXPERIENCE VOLATILITY SIMILAR TO THAT SHOWN. THE INFORMATION PROVIDED IN THE CHART BELOW ISFOR ILLUSTRATIVE PURPOSES ONLY.

-14-

Estimated Fund Return Over One Year When the Fund’s Objective is to Seek Daily Investment Results, Before Fees and Expenses, thatCorrespond to Two Times (2x) the Performance of a Benchmark for a Single Day.

One YearBenchmark

Performance

Two Times (2x)One Year

BenchmarkPerformance

Benchmark Volatility

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70%-60% -120% -84.0% -84.0% -84.2% -84.4% -84.6% -85.0% -85.4% -85.8% -86.4% -86.9% -87.5% -88.2% -88.8% -89.5% -90.2%-55% -110% -79.8% -79.8% -80.0% -80.2% -80.5% -81.0% -81.5% -82.1% -82.7% -83.5% -84.2% -85.0% -85.9% -86.7% -87.6%-50% -100% -75.0% -75.1% -75.2% -75.6% -76.0% -76.5% -77.2% -77.9% -78.7% -79.6% -80.5% -81.5% -82.6% -83.6% -84.7%-45% -90% -69.8% -69.8% -70.1% -70.4% -70.9% -71.6% -72.4% -73.2% -74.2% -75.3% -76.4% -77.6% -78.9% -80.2% -81.5%-40% -80% -64.0% -64.1% -64.4% -64.8% -65.4% -66.2% -67.1% -68.2% -69.3% -70.6% -72.0% -73.4% -74.9% -76.4% -77.9%-35% -70% -57.8% -57.9% -58.2% -58.7% -59.4% -60.3% -61.4% -62.6% -64.0% -65.5% -67.1% -68.8% -70.5% -72.3% -74.1%-30% -60% -51.0% -51.1% -51.5% -52.1% -52.9% -54.0% -55.2% -56.6% -58.2% -60.0% -61.8% -63.8% -65.8% -67.9% -70.0%-25% -50% -43.8% -43.9% -44.3% -45.0% -46.0% -47.2% -48.6% -50.2% -52.1% -54.1% -56.2% -58.4% -60.8% -63.1% -65.5%-20% -40% -36.0% -36.2% -36.6% -37.4% -38.5% -39.9% -41.5% -43.4% -45.5% -47.7% -50.2% -52.7% -55.3% -58.1% -60.8%-15% -30% -27.8% -27.9% -28.5% -29.4% -30.6% -32.1% -34.0% -36.1% -38.4% -41.0% -43.7% -46.6% -49.6% -52.6% -55.7%-10% -20% -19.0% -19.2% -19.8% -20.8% -22.2% -23.9% -26.0% -28.3% -31.0% -33.8% -36.9% -40.1% -43.5% -46.9% -50.4%

-5% -10% -9.8% -10.0% -10.6% -11.8% -13.3% -15.2% -17.5% -20.2% -23.1% -26.3% -29.7% -33.3% -37.0% -40.8% -44.7%0% 0% 0.0% -0.2% -1.0% -2.2% -3.9% -6.1% -8.6% -11.5% -14.8% -18.3% -22.1% -26.1% -30.2% -34.5% -38.7%5% 10% 10.3% 10.0% 9.2% 7.8% 5.9% 3.6% 0.8% -2.5% -6.1% -10.0% -14.1% -18.5% -23.1% -27.7% -32.5%

10% 20% 21.0% 20.7% 19.8% 18.3% 16.3% 13.7% 10.6% 7.0% 3.1% -1.2% -5.8% -10.6% -15.6% -20.7% -25.9%15% 30% 32.3% 31.9% 30.9% 29.3% 27.1% 24.2% 20.9% 17.0% 12.7% 8.0% 3.0% -2.3% -7.7% -13.3% -19.0%20% 40% 44.0% 43.6% 42.6% 40.8% 38.4% 35.3% 31.6% 27.4% 22.7% 17.6% 12.1% 6.4% 0.5% -5.6% -11.8%25% 50% 56.3% 55.9% 54.7% 52.8% 50.1% 46.8% 42.8% 38.2% 33.1% 27.6% 21.7% 15.5% 9.0% 2.4% -4.3%30% 60% 69.0% 68.6% 67.3% 65.2% 62.4% 58.8% 54.5% 49.5% 44.0% 38.0% 31.6% 24.9% 17.9% 10.8% 3.5%35% 70% 82.3% 81.8% 80.4% 78.2% 75.1% 71.2% 66.6% 61.2% 55.3% 48.8% 41.9% 34.7% 27.2% 19.4% 11.7%40% 80% 96.0% 95.5% 94.0% 91.6% 88.3% 84.1% 79.1% 73.4% 67.0% 60.1% 52.6% 44.8% 36.7% 28.5% 20.1%45% 90% 110.3% 109.7% 108.2% 105.6% 102.0% 97.5% 92.2% 86.0% 79.2% 71.7% 63.7% 55.4% 46.7% 37.8% 28.8%50% 100% 125.0% 124.4% 122.8% 120.0% 116.2% 111.4% 105.6% 99.1% 91.7% 83.8% 75.2% 66.3% 57.0% 47.5% 37.8%55% 110% 140.3% 139.7% 137.9% 134.9% 130.8% 125.7% 119.6% 112.6% 104.7% 96.2% 87.1% 77.5% 67.6% 57.5% 47.2%60% 120% 156.0% 155.4% 153.5% 150.3% 146.0% 140.5% 134.0% 126.5% 118.1% 109.1% 99.4% 89.2% 78.6% 67.8% 56.8%

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS. NO REPRESENTATION IS BEINGMADE THAT ANY BENCHMARK OR FUND WILL OR IS LIKELY TO ACHIEVE GAINS OR LOSSES SIMILAR TO THOSE SHOWNOR WILL EXPERIENCE VOLATILITY SIMILAR TO THAT SHOWN. THE INFORMATION PROVIDED IN THE CHART BELOW ISFOR ILLUSTRATIVE PURPOSES ONLY.

Estimated Fund Return Over One Year When the Fund’s Objective is to Seek Daily Investment Results, Before Fees and Expenses, thatCorrespond to Two Times the Inverse (-2x) of the Performance of a Benchmark for a Single Day.

One YearBenchmark

Performance

Two TimesInverse (-2x) of

One YearBenchmark

Performance

Benchmark Volatility

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70%-60% 120% 525.0% 520.3% 506.5% 484.2% 454.3% 418.1% 377.1% 332.8% 286.7% 240.4% 195.2% 152.2% 112.2% 76.0% 43.7%-55% 110% 393.8% 390.1% 379.2% 361.6% 338.0% 309.4% 277.0% 242.0% 205.6% 169.0% 133.3% 99.3% 67.7% 39.0% 13.5%-50% 100% 300.0% 297.0% 288.2% 273.9% 254.8% 231.6% 205.4% 177.0% 147.5% 117.9% 88.9% 61.4% 35.8% 12.6% -8.0%-45% 90% 230.6% 228.1% 220.8% 209.0% 193.2% 174.1% 152.4% 128.9% 104.6% 80.1% 56.2% 33.4% 12.3% -6.9% -24.0%-40% 80% 177.8% 175.7% 169.6% 159.6% 146.4% 130.3% 112.0% 92.4% 71.9% 51.3% 31.2% 12.1% -5.7% -21.8% -36.1%-35% 70% 136.7% 134.9% 129.7% 121.2% 109.9% 96.2% 80.7% 63.9% 46.5% 28.9% 11.8% -4.5% -19.6% -33.4% -45.6%-30% 60% 104.1% 102.6% 98.1% 90.8% 81.0% 69.2% 55.8% 41.3% 26.3% 11.2% -3.6% -17.6% -30.7% -42.5% -53.1%-25% 50% 77.8% 76.4% 72.5% 66.2% 57.7% 47.4% 35.7% 23.1% 10.0% -3.2% -16.0% -28.3% -39.6% -49.9% -59.1%-20% 40% 56.3% 55.1% 51.6% 46.1% 38.6% 29.5% 19.3% 8.2% -3.3% -14.9% -26.2% -36.9% -46.9% -56.0% -64.1%-15% 30% 38.4% 37.4% 34.3% 29.4% 22.8% 14.7% 5.7% -4.2% -14.4% -24.6% -34.6% -44.1% -53.0% -61.0% -68.2%-10% 20% 23.5% 22.5% 19.8% 15.4% 9.5% 2.3% -5.8% -14.5% -23.6% -32.8% -41.7% -50.2% -58.1% -65.2% -71.6%

-5% 10% 10.8% 10.0% 7.5% 3.6% -1.7% -8.1% -15.4% -23.3% -31.4% -39.6% -47.7% -55.3% -62.4% -68.8% -74.5%0% 0% 0.0% -0.7% -3.0% -6.5% -11.3% -17.1% -23.7% -30.8% -38.1% -45.5% -52.8% -59.6% -66.0% -71.8% -77.0%5% -10% -9.3% -10.0% -12.0% -15.2% -19.6% -24.8% -30.8% -37.2% -43.9% -50.6% -57.2% -63.4% -69.2% -74.5% -79.1%

10% -20% -17.4% -18.0% -19.8% -22.7% -26.7% -31.5% -36.9% -42.8% -48.9% -55.0% -61.0% -66.7% -71.9% -76.7% -81.0%15% -30% -24.4% -25.0% -26.6% -29.3% -32.9% -37.3% -42.3% -47.6% -53.2% -58.8% -64.3% -69.5% -74.3% -78.7% -82.6%20% -40% -30.6% -31.1% -32.6% -35.1% -38.4% -42.4% -47.0% -51.9% -57.0% -62.2% -67.2% -72.0% -76.4% -80.4% -84.0%25% -50% -36.0% -36.5% -37.9% -40.2% -43.2% -46.9% -51.1% -55.7% -60.4% -65.1% -69.8% -74.2% -78.3% -82.0% -85.3%30% -60% -40.8% -41.3% -42.6% -44.7% -47.5% -50.9% -54.8% -59.0% -63.4% -67.8% -72.0% -76.1% -79.9% -83.3% -86.4%35% -70% -45.1% -45.5% -46.8% -48.7% -51.3% -54.5% -58.1% -62.0% -66.0% -70.1% -74.1% -77.9% -81.4% -84.6% -87.4%40% -80% -49.0% -49.4% -50.5% -52.3% -54.7% -57.7% -61.1% -64.7% -68.4% -72.2% -75.9% -79.4% -82.7% -85.6% -88.3%45% -90% -52.4% -52.8% -53.8% -55.5% -57.8% -60.6% -63.7% -67.1% -70.6% -74.1% -77.5% -80.8% -83.8% -86.6% -89.1%50% -100% -55.6% -55.9% -56.9% -58.5% -60.6% -63.2% -66.1% -69.2% -72.5% -75.8% -79.0% -82.1% -84.9% -87.5% -89.8%55% -110% -58.4% -58.7% -59.6% -61.1% -63.1% -65.5% -68.2% -71.2% -74.2% -77.3% -80.3% -83.2% -85.9% -88.3% -90.4%60% -120% -60.9% -61.2% -62.1% -63.5% -65.4% -67.6% -70.2% -73.0% -75.8% -78.7% -81.5% -84.2% -86.7% -89.0% -91.0%

-15-

The foregoing tables are intended to isolate the effect of benchmark volatility and benchmark performance on the return of leveraged orinverse leveraged funds. The Funds’ actual returns may be greater or less than the returns shown above.

Correlation and Performance Risks

While the Funds seek to meet their investment objectives, there is no guarantee they will do so. Factors that may affect a Fund’s ability tomeet its investment objective include: (1) the Sponsor’s ability to purchase and sell Financial Instruments in a manner that correlates to a Fund’sobjective, including the Sponsor’s ability to enter into new positions and contracts to replace exposure that has been reduced or terminated by acounterparty or otherwise; (2) an imperfect correlation between the performance of the Financial Instruments held by a Fund and theperformance of the applicable benchmark; (3) bid-ask spreads on such Financial Instruments; (4) fees, expenses, transaction costs, financingcosts and margin requirements associated with the use of Financial Instruments and commission costs; (5) holding or trading FinancialInstruments in a market that has become illiquid or disrupted; (6) a Fund’s Share prices being rounded to the nearest cent and/or valuationmethodologies; (7) changes to a benchmark that are not disseminated in advance; (8) the need to conform a Fund’s portfolio holdings to complywith investment restrictions or policies, position limits and accountability levels, and regulatory or tax law requirements; (9) early orunanticipated closings of the markets on which the holdings of a Fund trade, limiting or preventing the Fund from executing intended portfoliotransactions; (10) accounting standards; (11) differences caused by a Fund obtaining exposure to only a representative sample of the componentsof a benchmark, overweighting or underweighting certain components of a benchmark or obtaining exposure to assets that are not included in abenchmark; (12) large movements of assets into and/or out of a Fund, particularly late in the day; (13) significant and/or rapid increases in thesize of the Fund as a result of an increase in creation activity that cause the Fund to approach or reach Share registration limits, position oraccountability limits, and (14) events such as natural disasters (including disease, epidemics and pandemics) that can be highly disruptive toeconomies, markets and companies including, but not limited to, the Sponsor and third party service providers.

In order to achieve a high degree of correlation with their applicable underlying benchmarks, the Funds seek to rebalance their portfoliosdaily to keep exposure consistent with their respective investment objectives. A Fund’s ability to achieve or maintain such exposure may belimited by a number of factors. For example, being materially under- or overexposed to the benchmarks may prevent a Fund from achieving ahigh degree of correlation with their applicable underlying benchmarks. Market disruptions or closures, large movements of assets into or out ofthe Funds, regulatory restrictions, market volatility, illiquidity, margin requirements, accountability levels, position limits, and daily pricefluctuation limits set by the exchanges and other factors will adversely affect a Fund’s ability to adjust exposure to requisite levels. The targetamount of a Fund’s portfolio exposure may be impacted by changes to the value of its benchmark each day. Other things being equal, moresignificant movement in the value of its benchmark, up or down, will require more significant adjustments to a Fund’s portfolio. Because of this,it is unlikely that the Funds will be perfectly exposed (i.e., 2x or -2x, as applicable) at the end of each day, and the likelihood of being materiallyunder- or overexposed is higher on days when the benchmark levels are volatile at or near the close of the trading day.

The time and manner in which a Fund rebalances its portfolio may vary from day to day at the discretion of the Sponsor depending uponmarket conditions and other circumstances. Unlike other funds that do not rebalance their portfolios as frequently, each Fund may be subject toincreased trading costs associated with daily portfolio rebalancings. The effects of these trading costs have been estimated and included in theBreakeven Table. See “Charges—Breakeven Table” below.