CLIMATE FINANCE IN 2013-14 & THE USD 100 BILLON GOAL A report by the OECD in collaboration with Climate Policy Initiative (CPI), At the request of the incoming and current UNFCCC COP Presidencies, France and Peru Presentation to ENVIRONET-WP-STAT Task Team, Monday 2 nd November Ms. Stephanie Ockenden, Lead Analyst and Project Manager (OECD)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CLIMATE FINANCE IN 2013-14 & THE USD 100 BILLON GOAL

A report by the OECD in collaboration with Climate Policy Initiative (CPI),

At the request of the incoming and current UNFCCC

COP Presidencies, France and Peru

Presentation to ENVIRONET-WP-STAT Task Team, Monday 2nd November

Ms. Stephanie Ockenden, Lead Analyst and Project Manager (OECD)

Headline results

Data highlights

Accounting framework Data coverage and consistency Expected reporting to UNFCCC MDB attribution

Key lessons

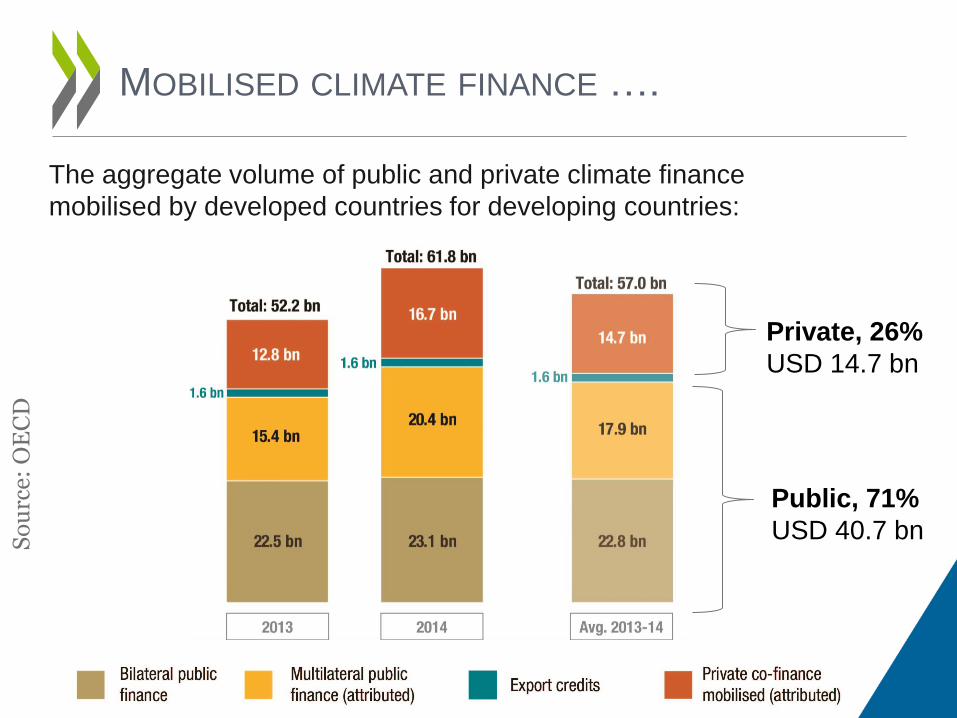

MOBILISED CLIMATE FINANCE ….

So

urc

e: O

EC

D

The aggregate volume of public and private climate finance

mobilised by developed countries for developing countries:

Public, 71%

USD 40.7 bn

Private, 26%

USD 14.7 bn

Comprehensive (though preliminary) figures for public climate finance in 2013 and 2014.

Preliminary partial estimates of mobilised private climate finance.

Transparency by breaking down climate finance by source

Transparency in outlining the accounting framework, working classifications and methodological approaches

Reflects on, as far as possible, common methodology of a group of 19 bilateral climate finance providers on their common understanding of the scope of mobilised climate finance.

Multilateral public and private flows are not counted in their entirety, rather, a share is attributed to developed economies.

DATA AND METHODOLOGICAL HIGHLIGHTS:

Headline results

Data highlights

Accounting framework Data coverage and consistency Expected reporting to UNFCCC MDB attribution

Key lessons

ACCOUNTING FRAMEWORK & WORKING

CLASSIFICATIONS

Example of working classifications and definitions:

• Classification of “developed country” providers

• Classification of “developing country” recipients

• Climate Definitions

DATA COVERAGE AND CONSISTENCY

Source Average 2013-14 Coverage of data Consistency of

data

Public

Bilateral 22.8

Multilateral 17.9

Export Credits 1.6

Mobilised Private 14.7

Aggregate 57.0

Climate finance mobilised from developed countries for developing countries (USD billion)

Source: OECD analysis

Complete Comprehensive Partial Very partial Unavailable

Consistent Broad

Convergence

Partial

convergence

Variety of

approaches Unclear

Improvements in transparency of bilateral

public finance reported to the UNFCCC:

Bilateral Public Climate Finance, 2011-14 by finance source (USD billion)

Multilateral Finance Attribution:

• MDB financing draws on retained earnings and leveraging of

money from global capital markets on the basis of their

capital, which is typically composed of “paid-in”, and “callable”

capital as well as “reserves” built up over the years, from both

developed and developing countries.

– Overall estimated that 83% of total MDB outflows are attributed

to developed economies, however this average masks

significant variation across the MBDs, (range 59-99%).

– For concessional windows, the attribution share to developed

economies is based on a weighting of current and historic financial

contributions, where the average share is 95%.

– For non-concessional windows, the attribution share to

developed economies is based on a weighting of paid-in capital and

a discounted level of highly-rated callable capital, where the

average share is 78%.

Headline results

Data highlights

Accounting framework Data coverage and consistency Expected reporting to UNFCCC MDB attribution

Key lessons

KEY LESSONS:

Methodologies for measuring and reporting climate finance

are improving.

Significant foundations from DAC statistics.

But further progress is needed on methodologies and to

improve transparency.

Our report is intended as a contribution towards enhancing

transparency, and a starting point for discussion.

THANK YOU

Read the report at:

http://www.oecd.org/env/cc/oecd-cpi-climate-

finance-report.htm

Should you have any questions please contact:

• OECD Project Owner:

• OECD Project Manager:

THE PROJECT TIMELINE...

June July August September October

Data Collection & Processing

Analysis & Drafting

Final Report

Data Consultation & Scoping

Sensitivity analysis on MDB attribution

Headline estimate Sensitivity

Concessional

Windows of MDBs

Attribution based on

weighting of current and

historical contributions

Attribution based on

current contributions only

(last replenishment

period)

Attribution based on

historical contributions

only (excluding the last

replenishment period)

USD 4.8 bn (95%) USD 4.7 bn (94%) USD 4.8 bn (96%)

Non-Concessional

Windows of MDBs

Attribution based on

paid-in and callable

capital (discounted by

90%)

Attribution based on

paid-in capital only

Attribution based on

paid-in and callable

capital (discounted by

50%)

USD 10.7 bn (78%) USD 9.6 bn (70%) USD 11.5 bn (84%)

Total MDB

attributed Climate

Finance

USD 15.5 bn (83%)

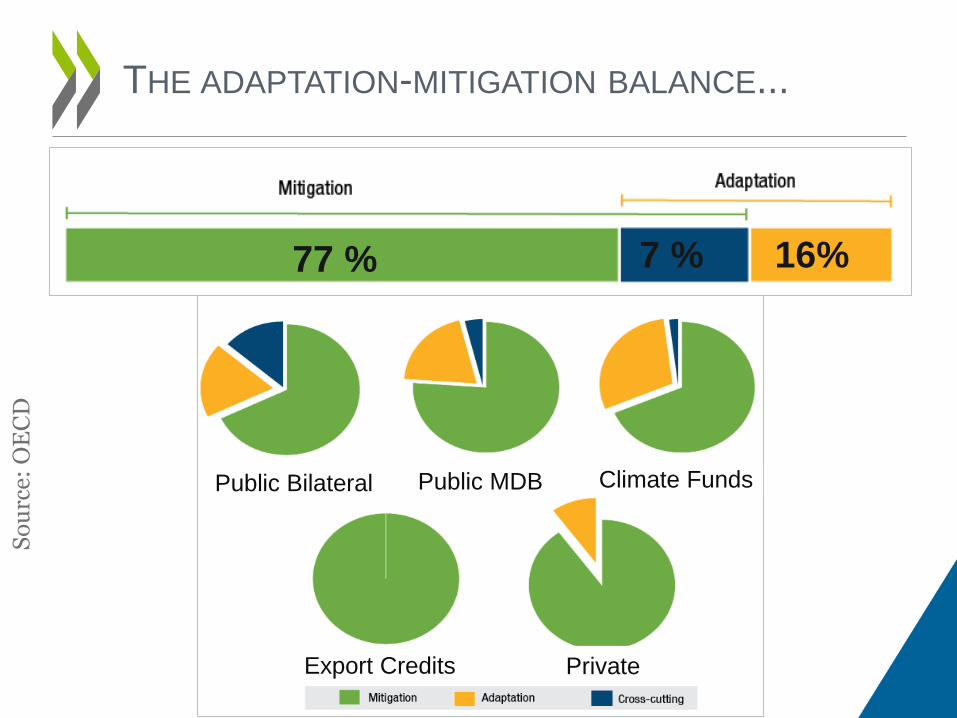

THE ADAPTATION-MITIGATION BALANCE...

77 % 7 % 16%

So

urc

e: O

EC

D

Public Bilateral Public MDB Climate Funds

Export Credits Private

Climate finance vs development finance...

Bilateral climate finance, from ODA vs total bilateral ODA commitments:

So

urc

e: O

EC

D

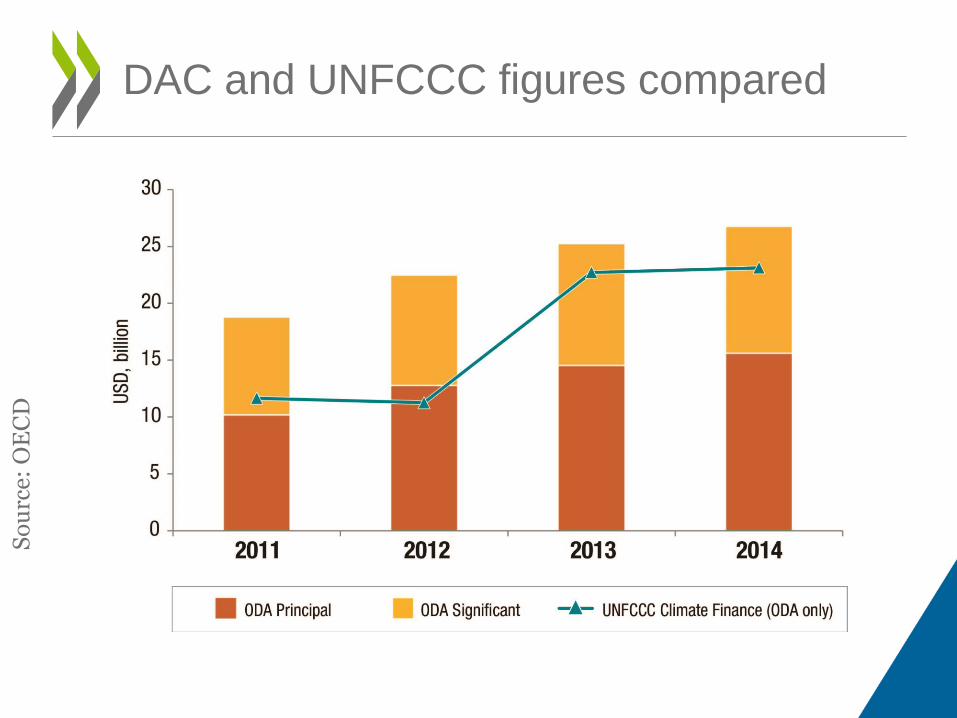

DAC and UNFCCC figures compared

So

urc

e: O

EC

D

Related Documents

![Dynamic-AI-Creator [DAC] Version 3 V3... · Dynamic-AI-Creator [DAC] Version 3.1 _____ Arma 3 vesion 1.16 required / Required addons : no Warning, DAC has lots of functions, the documentation](https://static.cupdf.com/doc/110x72/5e2083d21bd5c54c6a638e83/dynamic-ai-creator-dac-version-3-v3-dynamic-ai-creator-dac-version-31.jpg)