3-1 Bond Valuation Application of present Application of present value techniques to bonds value techniques to bonds and stocks and stocks Pricing and Valuation are Pricing and Valuation are the core issues in finance the core issues in finance

3-1 Bond Valuation Application of present value techniques to bonds and stocks Application of present value techniques to bonds and stocks Pricing and.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

3-1

Bond Valuation

Application of present value Application of present value techniques to bonds and stockstechniques to bonds and stocks

Pricing and Valuation are the Pricing and Valuation are the core issues in financecore issues in finance

3-2

Some standard forms of Bonds

C=coupon, F=face value, T=maturity dateC=coupon, F=face value, T=maturity datePure Discount or Zero-coupon bondsPure Discount or Zero-coupon bonds

PV=FV/(1+r)PV=FV/(1+r)TT

Level-coupon bondsLevel-coupon bondsPV=C/1+r + C/(1+r)PV=C/1+r + C/(1+r)22 + • • • + C/(1+r) + • • • + C/(1+r)TT + F/(1+r) + F/(1+r)TT

ConsolsConsolsPV=C/rPV=C/r

FloatersFloatersConvertiblesConvertibles

3-3

Bond Features

Coupon PaymentsCoupon Payments:: Regular interest Regular interest paymentspaymentsSemi annual for most US corporate bondsSemi annual for most US corporate bonds

Types of Coupon paymentsTypes of Coupon payments

• Fixed RateFixed Rate:: 8% per year 8% per year

• Floating RateFloating Rate:: 6-month Treasury bill rate + 6-month Treasury bill rate + 100 basis points.100 basis points.

3-4

Bond Features

Face or Par ValueFace or Par Value: : amount of money to be amount of money to be

repaid at end of loanrepaid at end of loan

$1,000/bond$1,000/bond

MaturityMaturity: : number of years from issue date until number of years from issue date until

principal is paidprincipal is paid

Coupon RateCoupon Rate: : annual coupon / face valueannual coupon / face value

3-5Features of a May Department Stores Bond

TermsTerms ExplanationsExplanations

Amount of issueAmount of issue $200 million$200 million The company will issue $200 million The company will issue $200 million worth of bonds.worth of bonds.

Date of issueDate of issue 8/4/94 8/4/94 The bonds were sold on 8/4/94.The bonds were sold on 8/4/94.

MaturityMaturity 8/1/24 8/1/24 The principal will be paid in 30 years.The principal will be paid in 30 years.

Face ValueFace Value $1,000$1,000 Denomination of the bond is in $1,000Denomination of the bond is in $1,000

Annual couponAnnual coupon 8.375 8.375 Each bondholder will receive Each bondholder will receive $83.75 per bond per year (8.375% of $83.75 per bond per year (8.375% of the face value).the face value).

Offer priceOffer price 100 100 The offer price will be 100% of the The offer price will be 100% of the $1,000 face value per bond.$1,000 face value per bond.

Coupon datesCoupon dates 2/1, 8/12/1, 8/1 $41.875 will be paid on these dates$41.875 will be paid on these dates

SecuritySecurity NoneNone

Sinking FundSinking Fund Annual from 8/1/05Annual from 8/1/05 Annual payments to this fund Annual payments to this fund starting from the indicated datestarting from the indicated date

Call ProvisionCall Provision not callable before 8/1/04not callable before 8/1/04 Deferred call featureDeferred call feature

Call PriceCall Price 104.188 initially104.188 initially Buy back price is $1041.88, declining Buy back price is $1041.88, declining declining to 100declining to 100 to $1,000 on 8/1/1to $1,000 on 8/1/1

RatingRating Moody’s A2Moody’s A2 This is one of Moody’s higher ratings. This is one of Moody’s higher ratings. The bonds have a low probability The bonds have a low probability of default.of default.

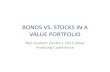

3-6

Bond Valuation(Assuming Level Coupon Payments)

Discounted Cash Flow ValuationDiscounted Cash Flow Valuation

Bond Value = PV (Promised Cash Flows) Bond Value = PV (Promised Cash Flows)

Bond Value = PV (Coupon Payments) Bond Value = PV (Coupon Payments)

+ PV (Face Value)+ PV (Face Value)

Bond Value = PV (Annuity) + PV (Lump sum)Bond Value = PV (Annuity) + PV (Lump sum)

3-7

Yield-to-Maturity (YTM)

Required market interest rate that Required market interest rate that makes the discounted cash flows of makes the discounted cash flows of the bond equal to its pricethe bond equal to its price

Interest rate that we will use in the Interest rate that we will use in the bond valuation equationbond valuation equation

Does Does notnot always equal the bond’s always equal the bond’s coupon ratecoupon rate

3-8

IPC issues 5-year $1,000 face value bonds with an annual coupon of 100. What is the coupon rate and what is the price

of the bonds if the YTM on similar bonds is 10%?

Time 0 1 2 3 4 5

Coupons PV=price 100 100 100 100 100

FaceValue

1000

3-9

General Expression for the Value of a Bond

Bond Value = C

YTM1 -

1

(1+ YTM) +

Face Value

(1+ YTM)t t

Annuity Formula

3-10

Example 2: Pricing of a regular bond

IPS issues a 10-year bondIPS issues a 10-year bond YTM = 24%YTM = 24% Coupon Rate = 8%Coupon Rate = 8% Face value = $1,000Face value = $1,000

What is the price of the bond at the issue What is the price of the bond at the issue date?date?

What is your What is your minimum sellingminimum selling price if you price if you sell this bond one year before its maturity?sell this bond one year before its maturity?

3-11

Notes on the Bond Pricing Formula

Semi annual couponsSemi annual coupons:: 10-year bond with 10-year bond with 12% coupon rate paid semi annually12% coupon rate paid semi annuallyHalve the coupon rate and quoted YTMHalve the coupon rate and quoted YTMDouble the number of periodsDouble the number of periodsYTM=APR!YTM=APR!

Risk-free market interest rate versus YTMRisk-free market interest rate versus YTMYTM takes into consideration the risk of the YTM takes into consideration the risk of the

cash flowscash flows

Finding YTMFinding YTM:: trial and error, EXCEL, trial and error, EXCEL, financial calculator.financial calculator.

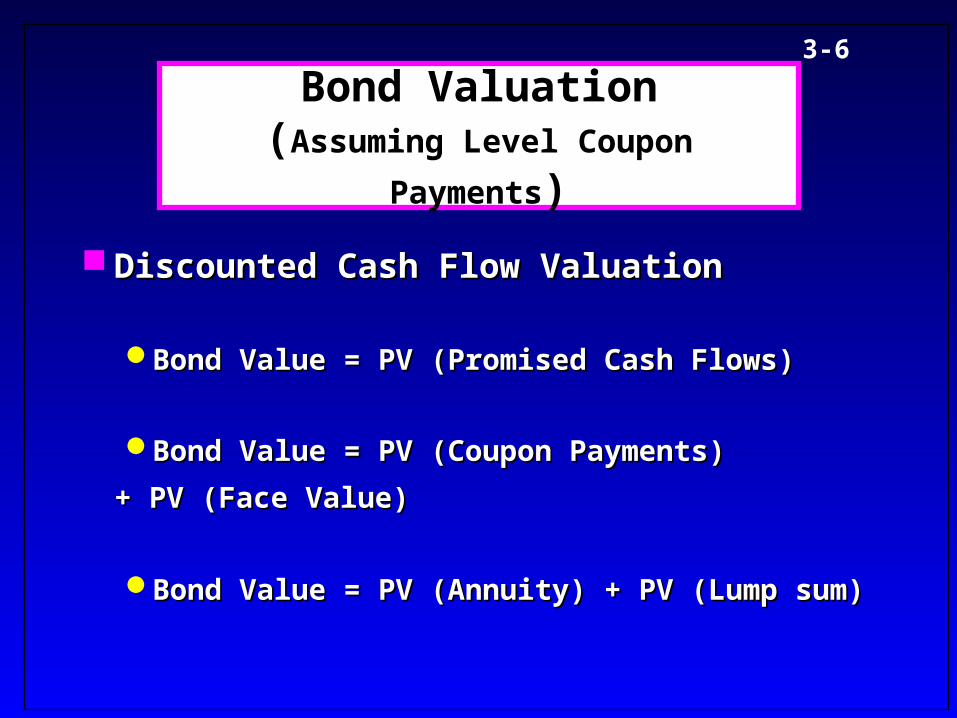

3-12

Semi-annual coupons:Semi-annual coupons:

What is the price of a $1000 bond maturing in ten years with a 12% coupon that is paid semiannually

if the YTM is 10%

3-13

Discount bond example:Discount bond example:

Suppose a year has gone by and the IPC 10% annual coupon bond has 4 years to maturity. What is the

price (present value) of the bonds if the YTM on similar bonds is 11%?

3-14

Premium Bond Example:Premium Bond Example:

Suppose in the second year the yield-to-maturity for similar bonds decreases to 9% instead of increasing to 11%. What is the price of the 4-year IPC $1000 par

value 10% annual coupon bond?

3-15Par, Discount and Premium BondsPar, Discount and Premium Bonds

The relation of YTM and the coupon rate

Par Bonds:Par Bonds:Price = Face ValuePrice = Face ValueYTM = Coupon RateYTM = Coupon Rate

Discount Bonds:Discount Bonds:Price < Face ValuePrice < Face ValueYTM > Coupon RateYTM > Coupon Rate

Premium Bonds:Premium Bonds:Price > Face ValuePrice > Face ValueYTM < Coupon RateYTM < Coupon Rate

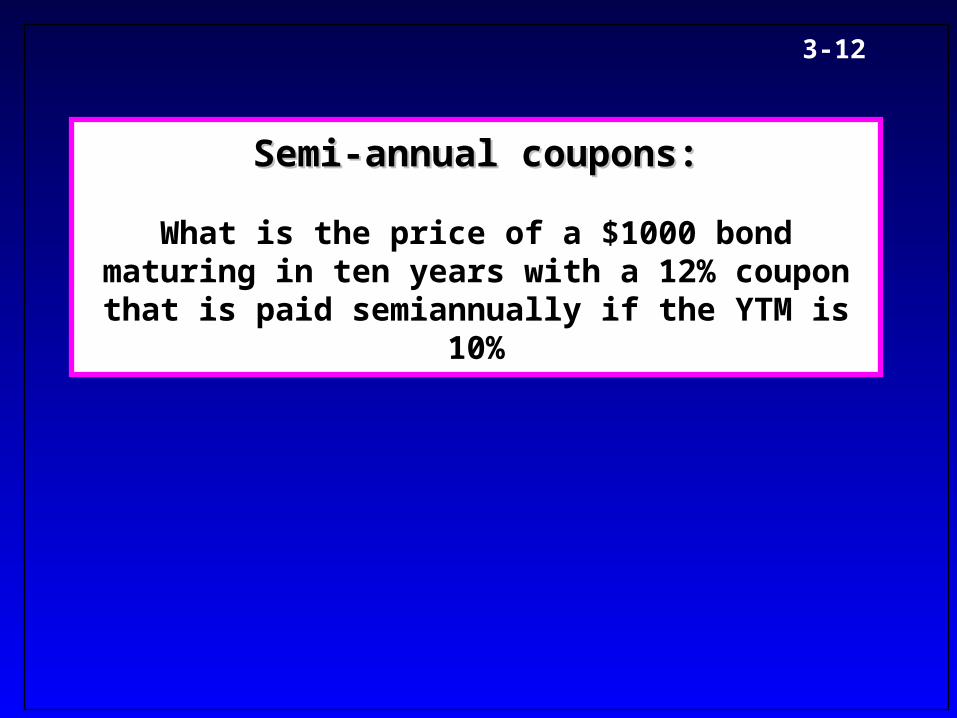

3-16

Interest Rate Risk of BondsInterest Rate Risk of Bonds

Risk that the bond you own will Risk that the bond you own will change in value because interest change in value because interest rates (e.g. YTM) have changedrates (e.g. YTM) have changed

Review:Review:As interest rates As interest rates riserise, PV , PV decreasesdecreases all all

else equalelse equalAs interest rates As interest rates fallfall, PV , PV increasesincreases all all

else equalelse equal Interest rate sensitivity depends on Interest rate sensitivity depends on

time to maturity and coupon ratetime to maturity and coupon rate

3-17

Determinants of the Interest Rate Risk of Determinants of the Interest Rate Risk of Bonds: Part IBonds: Part I

Time to Maturity:Time to Maturity:The longer the time to maturity, the greater The longer the time to maturity, the greater

the interest rate risk, all else equalthe interest rate risk, all else equal• Higher t in formula => greater compounding Higher t in formula => greater compounding

effect => small changes in r, big changes in effect => small changes in r, big changes in priceprice

10% 2-year and 15-year bonds10% 2-year and 15-year bonds• 15 year bond’s price will change more with a 15 year bond’s price will change more with a

change in the YTM.change in the YTM.

3-18Interest Rate Changes and Bond Values:

Both bonds are par bonds originally

1,035.67 (1.08)

1,000 +

(1.08)

1 - 1

0.08

100 = Price

222

1,171.19 (1.08)

1,000 +

(1.08)

1 - 1

0.08

100 = Price

151515

Suppose YTM decreases to 8%:

Suppose YTM increases to 12%:

966.20 (1.12)

1,000 +

(1.12)

1 - 1

0.12

100 = Price

222

Price = 1000.12

- 1

(1.12) +

1,000(1.12)

863.7815 15 15

1

3-19

Time to maturity

Interest rate 1 year 30 years

5% $1,047.62 $1,768.62

10 1,000.00 1,000.00

15 956.52 671.70

20 916.67 502.11

Interest Rate Risk and Time to Maturity (Figure 7.2)

Value of a Bond with a 10% Coupon Rate for Different Interest Rates and Maturities

Bond values ($)

Interest rates (%)

$1,768.62

$1,047.62

$916.67

$502.11

30-year bond

1-year bond

2000

1500

1000

500

5 10 15 20

3-20

Determinants of the Interest Rate Risk of Bonds: Part II

Coupon Rate:Coupon Rate:The lower the coupon rate, the greater the The lower the coupon rate, the greater the

interest rate risk, all else equalinterest rate risk, all else equal• Low coupon => more of the bond’s value Low coupon => more of the bond’s value

comes from the face amountcomes from the face amount

0% 0% (pure discount)(pure discount) and 10% 8-year bonds and 10% 8-year bonds• 100% of the 0% coupon bond’s price comes 100% of the 0% coupon bond’s price comes

from face amountfrom face amount• 10% bond’s price depends on eight $100 10% bond’s price depends on eight $100

annual coupons plus face valueannual coupons plus face value

3-21

Which Bond has a higher interest rate risk?

A: 30-year, 10% coupon or B: 15-year, 10% coupon?A: 30-year, 10% coupon or B: 15-year, 10% coupon?

A: 30-year, 10% coupon with face value of $1,000 or B: 25-year, A: 30-year, 10% coupon with face value of $1,000 or B: 25-year, 10% coupon, with face value of $10,000?10% coupon, with face value of $10,000?

A: 30-year, 11% coupon or B: 30-year, 9% coupon?A: 30-year, 11% coupon or B: 30-year, 9% coupon?

A: 30-year, zero-coupon with face value of $1,000 or B: 30-year, A: 30-year, zero-coupon with face value of $1,000 or B: 30-year, 10% coupon, with face value of $10,000?10% coupon, with face value of $10,000?

A: 30-year, 10% coupon or B: 25-year, 15% coupon?A: 30-year, 10% coupon or B: 25-year, 15% coupon?

A: 30-year, 10% coupon or B: 20-year, 8% coupon?A: 30-year, 10% coupon or B: 20-year, 8% coupon?

3-22

The Interest Rate Risk of Bonds

DurationDurationA measure of the interest rate risk of a bondA measure of the interest rate risk of a bondaverage maturity of a bond’s cash flowsaverage maturity of a bond’s cash flows

The higher the duration measure, the greater The higher the duration measure, the greater the interest rate riskthe interest rate risk

N

1=t

t

Bond of Price

PV(CF) =Duration

t

3-23Bond pricing Theorems

The following statements about bond pricing are The following statements about bond pricing are alwaysalways true.true.

Bond prices and market interest rates move in opposite Bond prices and market interest rates move in opposite directions.directions.

When a bond’s coupon rate is (greater than / equal to / When a bond’s coupon rate is (greater than / equal to / less than) the market’s required return (YTM), the bond’s less than) the market’s required return (YTM), the bond’s market value will be (greater than / equal to / less than) its market value will be (greater than / equal to / less than) its par value.par value.

Given two bonds identical except for maturity, the price Given two bonds identical except for maturity, the price of the longer-term bond will change more than that of the of the longer-term bond will change more than that of the shorter-term bond, for a given change in market interest shorter-term bond, for a given change in market interest rates.rates.

Given two bonds identical but for coupon, the price of the Given two bonds identical but for coupon, the price of the lower-coupon bond will change more than that of lower-coupon bond will change more than that of the the higher-coupon bond, for a given change in market higher-coupon bond, for a given change in market interest rates.interest rates.

3-24

Implicit Interest on a Zero-coupon

Suppose EIN company issues a Suppose EIN company issues a $1,000, 5-year zero-coupon bond.$1,000, 5-year zero-coupon bond.

Calculate the price if the YTM-15%Calculate the price if the YTM-15%What is the total amount of implicit What is the total amount of implicit

interest on this bond?interest on this bond?What is the yearly implicit interest What is the yearly implicit interest

using amortization (required by law)?using amortization (required by law)?

3-25

Solution

PV = 1,000 / 1.15PV = 1,000 / 1.1555 = $497 = $497 Total Implicit Interest = $1,000 - $497 = $502Total Implicit Interest = $1,000 - $497 = $502 Using straight-line interest expense, we have Using straight-line interest expense, we have

$502/5 = $102.60 per year.$502/5 = $102.60 per year. Using amortization, we have for the first year:Using amortization, we have for the first year:

Beginning value = $497Beginning value = $497 Ending value = $1,000 / 1.15Ending value = $1,000 / 1.1544 = $572 = $572 Implicit interest in year 1 = $572 - $497 = $75Implicit interest in year 1 = $572 - $497 = $75 Implicit interest in year 2 = ($1,000 / 1.15Implicit interest in year 2 = ($1,000 / 1.1533) - $572 = $86) - $572 = $86 et ceteraet cetera

What would be preferred by the corporation?What would be preferred by the corporation?

3-26

Inflation and Returns

Key issues:Key issues:

What is the difference between a What is the difference between a realreal and a and a nominalnominal return?return?

How can we convert from one to the other?How can we convert from one to the other?

ExampleExample: : Suppose we have $1,000, and Diet Coke costs Suppose we have $1,000, and Diet Coke costs $2.00 per six pack. We could buy 500 six packs. Now $2.00 per six pack. We could buy 500 six packs. Now suppose the rate of inflation is 5%, so that the price rises suppose the rate of inflation is 5%, so that the price rises to $2.10 in one year. When we invest the $1,000 it grows to to $2.10 in one year. When we invest the $1,000 it grows to $1,100 in one year. $1,100 in one year.

What’s the return in What’s the return in dollarsdollars? ?

What’s the return in What’s the return in six packssix packs??

3-27

Reading the Wall Street Journal

Majority of bonds is traded OTCMajority of bonds is traded OTC Bonds are quoted as a % of the face valueBonds are quoted as a % of the face value Bonds are quoted as ATT 7s05Bonds are quoted as ATT 7s05

AT&T issue, maturing in 2005, 7% couponAT&T issue, maturing in 2005, 7% coupon

Close = last available price on close previous Close = last available price on close previous business day (% of F)business day (% of F)

Net ChangeNet Change Current Yield = coupon / closing quote Current Yield = coupon / closing quote Volume Volume

3-28

Treasury Bonds

Always semi-annuallyAlways semi-annuallyQuoted in 32nds (smallest ‘tick’ size)Quoted in 32nds (smallest ‘tick’ size)

Bid price = 132:20 means 132 + 20/32 Bid price = 132:20 means 132 + 20/32 percent of the face value = $1,329.375percent of the face value = $1,329.375

Change: -46 means the price (bid or Change: -46 means the price (bid or ask) fell by 46/32%, or 1.4375%.ask) fell by 46/32%, or 1.4375%.

YTM is based on ask priceYTM is based on ask priceBid-ask spreadBid-ask spread““n” indicates notes, rather than bondsn” indicates notes, rather than bonds

3-29

Inflation and Returns

A.A. DollarsDollars.. Our Our returnreturn is is

($1100 - $1000)/$1000 = $100/$1000 = ________.($1100 - $1000)/$1000 = $100/$1000 = ________.

The percentage increase in the amount of The percentage increase in the amount of green stuff is 10%; our dollar return is 10%.green stuff is 10%; our dollar return is 10%.

B.B. Six packsSix packs. We can buy $1100/$2.10 = ________ . We can buy $1100/$2.10 = ________ six packs, so our return issix packs, so our return is

(523.81 - 500)/500 = 23.81/500 = 4.76%(523.81 - 500)/500 = 23.81/500 = 4.76%

The percentage increase in the amount of The percentage increase in the amount of brown brown stuff is 4.76%; our six-pack return is stuff is 4.76%; our six-pack return is 4.76%.4.76%.

3-30

Inflation and Returns, concluded

The relationship between real and nominal returns is The relationship between real and nominal returns is described by the described by the Fisher EffectFisher Effect. . Let:Let:

RR == the nominal returnthe nominal return

rr == the real returnthe real return

hh == the inflation ratethe inflation rate

According to the Fisher Effect:According to the Fisher Effect:

1 + R = (1 + r) x (1 + h)1 + R = (1 + r) x (1 + h)

From the example, the real return is 4.76%; the nominal From the example, the real return is 4.76%; the nominal return is 10%, and the inflation rate is 5%:return is 10%, and the inflation rate is 5%:

(1 + R) = 1.10(1 + R) = 1.10

(1 + r) x (1 + h) = 1.0476 x 1.05 = 1.10(1 + r) x (1 + h) = 1.0476 x 1.05 = 1.10

Related Documents