2004 the medical technology industry at a glance

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2004

the medical technology industry at a glance

2004

the medical technology industry at a glance

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

letter from the president

Dear AdvaMed Members and Friends,

The medical technology industry continues to be one of the most vital and dynamic sectors of the U.S. economy and a leading force in the revolution that is transforming America’s health care system. This revolution is improving patient outcomes and speeding recovery time while reducing overall health care spending.

Fueled by record spending on research and development, the U.S. medical technology industry continues to be the world leader in producing innovative lifesaving and life-enhancing products. By all relevant measures of growth – employment trends, production values, exports, global market share, venture capital financing – the medical technology industry sets a standard that is the envy of most business sectors.

The medical technology industry’s impressive economic performance is exceeded only by its contributions to improving the health and well-being of patients worldwide. Breakthrough medical technologies are able to detect diseases earlier and offer new, more effective treatment options for leading causes of disability and mortality such as heart disease, cancer and other illnesses.

More effective treatment options generate economic benefits as well. Over the years, medical technology innovations have led to decreases in the number of disabled Americans, increases in outpatient and minimally invasive surgical procedures, and shorter hospital stays. As a result, patients are able to live longer, healthier, more productive lives for far less than it would have cost just a few years ago.

The future of the medical technology industry looks to be even brighter than the present. Coming breakthroughs in areas such as device miniaturization and nanotechnology, molecular and gene-based diagnostics, information technology, and artificial organs and tissue engineering promise to provide innovative solutions to some of the most persistent and debilitating health care problems. Such innovation bodes well not only for the economic health of the medical technology industry but for the overall health of U.S. patients and the health care system as well.

The information presented in this report, prepared by The Lewin Group, illustrates the robust nature of the U.S. medical technology industry and the positive impact innovations in medical technology are having on patients’ lives and the nation’s health care system.

Pamela G. Bailey

President,Advanced Medical Technology Association

letter from the president

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

SECTION I – THE STATE OF INNOVATION 1

Chapter 1: Industry Overview 3

1.1 U.S. Market Size for the Medical Device and Diagnostics Industry 4

1.2 Distribution of Medical Companies by Size 4

1.3 Distribution of U.S. Firms by North American Industrial Classifications 5

1.4 Mergers and Acquisitions Transaction Volume 6

1.5 Initial Public Offerings of Venture-Backed Medical Device Firms 6

1.6 Venture Capital Financing in the Medical Device Industry 7

Chapter 2: The Global Leader 9

2.1 International Markets for the Medical Device and Diagnostics Industry 10

2.2 Market Sizes, Compound Annual Growth Rates for Selected Regions 10

2.3 Total U.S. Exports of Medical Device and Diagnostics Industry 11

2.4 U.S. Medical Technology Industry Trade Statistics 11

2.5 Estimated Worldwide Market for Selected Cardiovascular Devices 12

Chapter 3: Research & Development 13

3.1 R&D Spending as a Percentage of Sales, U.S. Medical Device Industry 14

3.2 R&D as a Percentage of Sales for U.S. Medical Device Industry and Selected 14Industrial Sectors (U.S.)

i

table of contents

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

3.3 Medical Device Industry R&D Spending as a Percentage of Sales by 15Standard Industrial Classification

3.4 Medical Device Industry R&D Spending as a Percentage of Sales by Company Size 15

3.5 National Institutes of Health Bioengineering Awards 16

3.6 Number of Medical Device Patents 16

3.7 Top Ten Factors Affecting Companies’ Ability to Develop New Medical Technologies 17Over Past Five Years

3.8 Top Ten Factors Influencing Companies’ Product Development Priorities Over 17Past Five Years

Section II – THE VALUE OF INNOVATION 19

Chapter 4: Economic Benefits 21

4.1 Production, Medical Device and Diagnostics Industry 22

4.2 Employment Trends of U.S. Medical Device and Diagnostics Industry 22

4.3 Trend in Selected Industry Producer Indexes 23

4.4 Change in Intercontinental Marketing Services (IMS) Composite Medical-Surgical 24 Price Index

Chapter 5: Regulatory Review 25

5.1 PMAs Approved by FDA 26

5.2 Original PMA Receipt Cohort Performance: FDA Review Days, 90th Percentile 26

5.3 510(k) Receipt Cohort Performance: FDA Review Days, 90th Percentile 27

5.4 FDA Office of Device Evaluation Staffing Levels 27

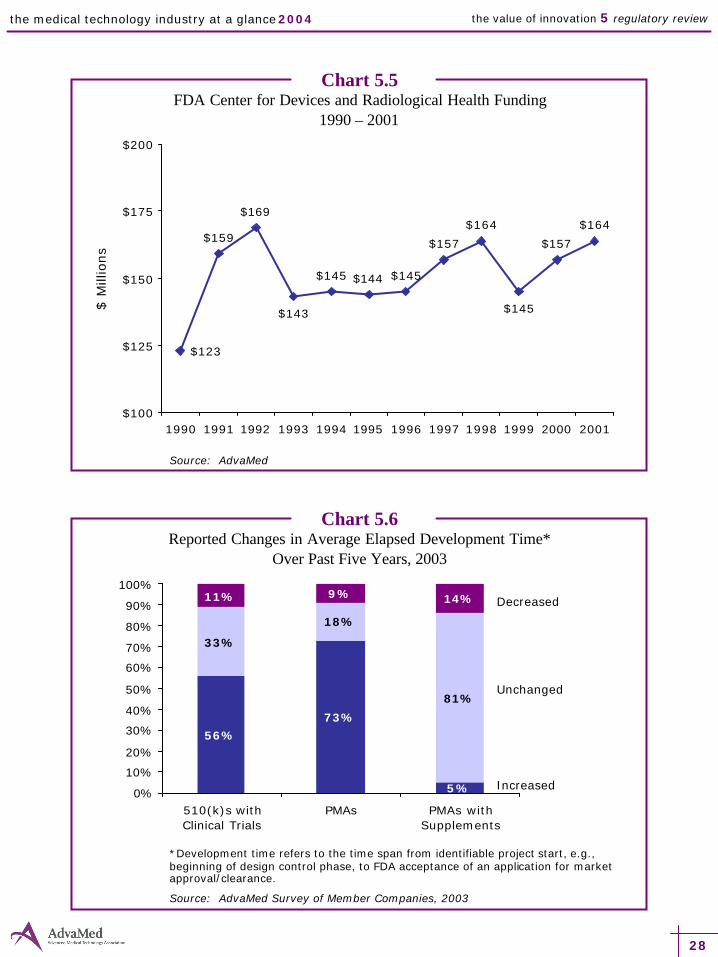

5.5 FDA Center for Devices and Radiological Health Funding 28

5.6 Reported Changes in Average Elapsed Development Time Over Past Five Years 28

5.7 Faster to Market: Europe or U.S.? 29

ii

table of contents

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

Chapter 6: Coverage & Payment 31

6.1 Reported Impact of Third Party Payer Issues on Innovation 32

6.2 Reported Speed of Coverage and Payment by Third Party Payers 32

6.3 Medicare Approval Process: Drug-Eluting vs. Bare Metal Coronary Stents 33

Chapter 7: Patient Care 35

7.1 Projected vs. Actual Number of Chronically Disabled Americans Age 65+ 36

7.2 Percentage Distribution of Inpatient vs. Outpatient Surgeries 36

7.3 Inpatient Hospital Length of Stay by Age Cohort (U.S.) 37

7.4 Number of Total Hip and Total Knee Replacement Procedures (U.S.) 37

7.5 Total Cataract Procedures (U.S.) 38

7.6 Number of Pacemaker Implant Procedures (U.S.) 38

7.7 Changes in the Treatment of Heart Attacks 39

7.8 Death Rates for Diseases of the Heart (U.S.) 39

7.9 Estimated Number of U.S. Patients with Implantable Cardiover-Defibrillator, 40Pacemaker, or Either Device

7.10 Use of Mammography by Women Age 40+ Years (U.S.); Death Rates 41 for Malignant Neoplasm of Breast for Females (U.S.)

7.11 Cost vs. Cost-Effectiveness of Drug-Eluting Stents 42

Appendix 43

iii

table of contents

SECTION I

the state of innovation

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

Medical technology plays a vital role in delivering safe, effective, and high-quality health care. The industry has developed life-saving and life-enhancing products such as pacemakers, artificial joints, drug-eluting stents, and laparoscopic devices for minimally invasive surgery. Innovations such as microminiature and remote surgery techniques, DNA-based diagnostics, tissue-engineered organs, and advanced information technologies are poised to further enhance quality of care. Medical innovation has great potential to synthesize advances in the sciences, bioengineering, biomaterials, genomics, computing, and telecommunications to develop technologies that will extend our ability to prevent, diagnose, and treat disease. Further advances will address the world’s current health care challenges, including treating and responding to outbreaks of new infectious diseases, biodefense, and meeting health needs in underdeveloped or war-torn areas.

The medical technology industry invests heavily in research and development, driven by constant innovation and short product life cycles. The bulk of R&D spending for medical devices and diagnostics comes from private sources. In 2002, the industry spent 11.4 percent of its sales on R&D, higher than any industry except that for drugs and medicine. Small companies, including many start-ups and highly innovative firms, spent an average of 343 percent of their revenue on R&D.

Adequate financing is critical to the successful development and commercialization of medical technology. Start-up companies are particularly dependent on capital financing prior to achieving a viable revenue stream. However, after peaking in 2000, venture capital financing fell sharply in the medical device industry along with many other industries, as did the number of initial public offerings of venture-backed firms.

The U.S. remains the global leader in innovation in medical technology. The U.S. medical technology industry is the largest producer of medical devices and diagnostics, with production estimated at $77 billion in 2002. Further, the U.S. is one of the world’s largest exporters of medical technology, selling to other countries an estimated $20.3 billion, or about a quarter of total U.S. production. Although the U.S. share of the growing world market declined during the 1980s due to slowed domestic growth, the U.S. share of the world market is currently about 42 percent.

“America’s health care system has advantages no other nation can match, but also challenges we cannot ignore.”

President George W. Bush

2

SECTION I

the state of innovation

chapter 1

industry overview

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

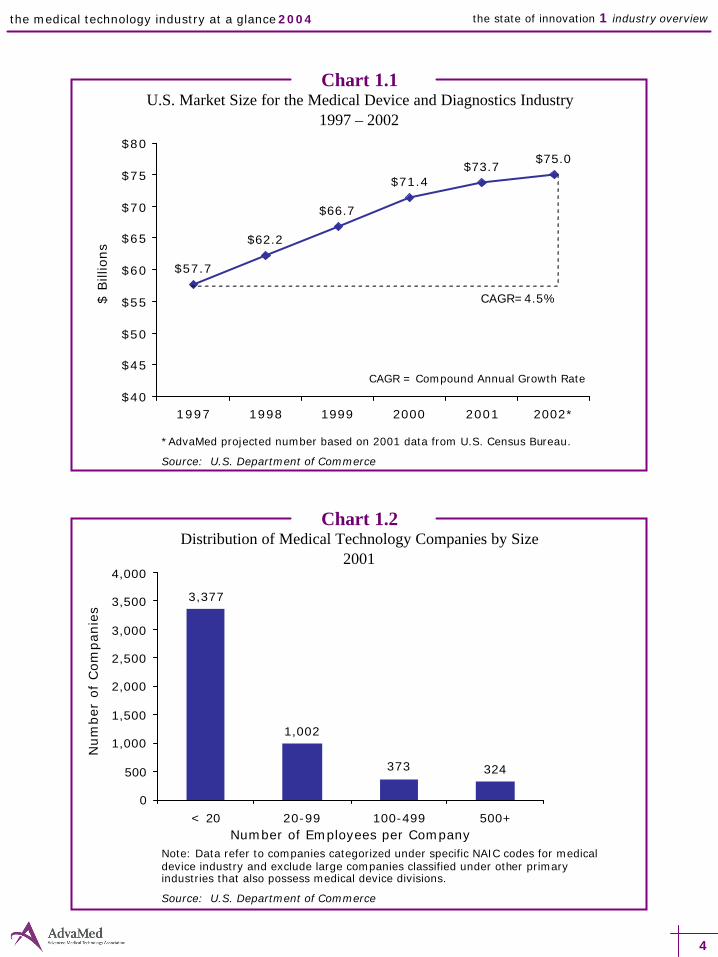

$75.0$73.7

$71.4

$66.7

$62.2

$57.7

$40

$45

$50

$55

$60

$65

$70

$75

$80

1997 1998 1999 2000 2001 2002*

4

Chart 1.2Distribution of Medical Technology Companies by Size

2001

324373

1,002

3,377

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

< 20 20-99 100-499 500+

Note: Data refer to companies categorized under specific NAIC codes for medical device industry and exclude large companies classified under other primary industries that also possess medical device divisions.

Source: U.S. Department of Commerce

Num

ber

of

Com

panie

sChart 1.1

U.S. Market Size for the Medical Device and Diagnostics Industry1997 – 2002

*AdvaMed projected number based on 2001 data from U.S. Census Bureau.

Source: U.S. Department of Commerce

$ B

illio

ns

CAGR=4.5%

CAGR = Compound Annual Growth Rate

Number of Employees per Company

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

Chart 1.3Distribution of U.S. Firms by North American Industrial Classifications

2001

Note: Data refer to companies categorized under specific NAIC codes for medical device industry and exclude large companies classified under other primary industries that also possess medical device divisions.

Source: U.S. Department of Commerce

Ophthalmic9%

Lab Apparatus7%

IVDs4%

SurgicalAppliances &

Supplies28%

Dental16%

Irradiation3%

Surgical & Medical

Instruments25%

Electromedical8%

5

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

Chart 1.4Mergers & Acquisitions Transaction Volume

1997 – 2003

*Deals refers to merger and/or acquisition activity.

Source: Windhover's Strategic Transaction Database

Tota

l Valu

e ($

Bill

ions)

Chart 1.5Initial Public Offerings of Venture-Backed Medical Device Firms

1996 – 2003

Source: Venture One

Num

ber of D

eals

6

$0

$5

$10

$15

$20

$25

$30

$35

1997 1998 1999 2000 2001 2002 20030

10

20

30

40

50

60

70

80

90

Total Value Number of Deals*

Ave

rage

Am

ount

Rais

ed (

$ M

illio

ns)

Num

ber o

f IPO

s

$0

$20

$40

$60

$80

$100

$120

1996 1997 1998 1999 2000 2001 2002 20030

5

10

15

20

25

30

35

Average Amount Raised Number of IPOs

the medical technology industry at a glance 2004 the state of innovation 1 industry overview

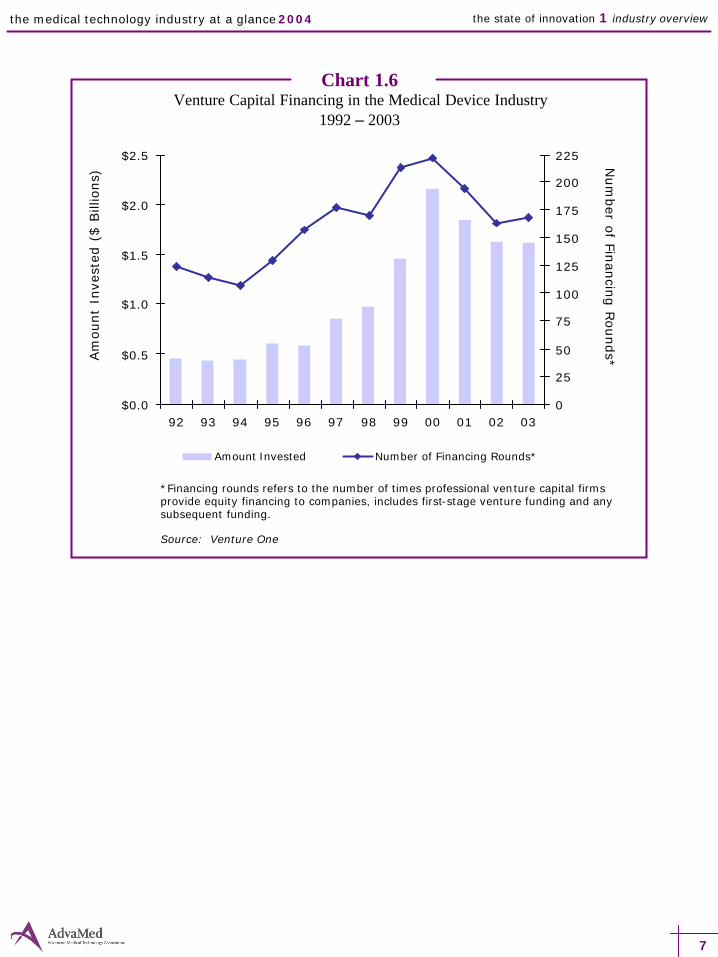

Chart 1.6Venture Capital Financing in the Medical Device Industry

1992 – 2003

*Financing rounds refers to the number of times professional venture capital firms provide equity financing to companies, includes first-stage venture funding and any subsequent funding.

Source: Venture One

Am

ount

Inve

sted

($ B

illio

ns)

Num

ber o

f Financin

g R

ounds*

7

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

92 93 94 95 96 97 98 99 00 01 02 030

25

50

75

100

125

150

175

200

225

Amount Invested Number of Financing Rounds*

chapter 2

the global leader

10

the medical technology industry at a glance 2004 the state of innovation 2 the global leader

Chart 2.1International Markets for the Medical Device and Diagnostics Industry

2000

Source: AdvaMed

$ B

illio

ns

Chart 2.2Market Sizes, Compound Annual Growth Rates for Selected Regions

1991 – 1999

Source: AdvaMed

10.6%7.3%14.1%Total

12.5%8.6%16.6%Rest of World

8.7%2.6%15.2%Japan

10.4%9.3%11.5%EU

10.8%7.4%14.3%U.S.

1991-19991995-19991991-1995

$72

$35

$25

$13

$0

$10

$20

$30

$40

$50

$60

$70

$80

US EU Japan Rest of World

Total 2000 Global Market = $169 Billion

11

the medical technology industry at a glance 2004 the state of innovation 2 the global leader

Chart 2.4U.S. Medical Technology Industry Trade Statistics

2002 – 2003

Source: U.S. International Trade Commission

Chart 2.3Total U.S. Exports of Medical Device and Diagnostics Industry

1989 – 2003

$0

$5

$10

$15

$20

$25

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

Source: U.S. International Trade Commission

$ B

illio

ns

-1.40-1.40 Asia (excl. Japan)

1.201.30 Japan

-1.40- 1.04 Mexico

1.301.60 Canada

0.560.74UK

-0.47-0.22Germany

0.530.65France

0.732.00 EU total

0.503.30U.S. Trade Surplus

22.0018.30U.S. Imports

$22.50$20.30 U.S. Exports

2003($ in Billions)

2002($ in Billions)

12

the medical technology industry at a glance 2004 the state of innovation 2 the global leader

Chart 2.5Estimated Worldwide Market for Selected Cardiovascular Devices

2001

Source: PJB Medical Publications, Inc.

114Ventricular Assist Devices

115Brachytherapy Systems

130Atherectomy Catheters

155Ablation Catheters

200Endovascular Stent-Grafts

231Diagnostic Electrophysiology Catheters

255Vascular Sealing Devices

433Other

590Peripheral Stents

832Heart Valves

1,900Implantable Cardioverter Defibrillators

2,000Angioplasty Devices

2,300Coronary Stents

$ 2,874Pacemakers and Accessories

$ 12,199Total

70Embolic Protection Systems

Revenue (in Millions)Category

chapter 3

research & development

14

the medical technology industry at a glance 2004 the state of innovation 3 research & development

Chart 3.1R&D Spending as a Percentage of Sales, U.S. Medical Device Indus try

1990 - 2002

5.4% 5.5%6.0%

6.8%7.2%

8.4%

9.6%

11.1%

12.9%

10.1%10.9%

12.3%11.4%

0%

2%

4%

6%

8%

10%

12%

14%

90 91 92 93 94 95 96 97 98 99 00 01 02

Source: S&P's Compustat. Data from publicly traded companies

Chart 3.2R&D as a Percentage of Sales for U.S. Medical Device Industry and

Selected Industrial Sectors, United States, 2002

3.5%

0.5%

0.8%

1.1%

3.1%

3.9%

4.1%

5.6%

7.5%

11.4%

12.9%

All Companies

Paper/Forest

Metals/Mining

Leisure

Aerospace/Defense

Electrical/Electronics

Auto

Telecom

Office Equipment

Medical Devices

Drugs & Medicine

Source: S&P's Compustat. Data from publicly traded companies

15

the medical technology industry at a glance 2004 the state of innovation 3 research & development

Chart 3.3Medical Device Industry R&D Spending as a Percentage of Sales by

Standard Industrial Classification, 1990, 1998, and 2002

33%

10%

5%

3%

8%

11%

23%

14%

6%

3%

9%

13%

11%

4%

3%

2%

7%

8%

0% 5% 10% 15% 20% 25% 30% 35%

199019982002

Source: S&P's Compustat. Data from publicly traded companies

Chart 3.4Medical Device Industry R&D Spending as a Percentage of Sales by Company

Size, 1990 and 2002

6% 4%

343%

39%24% 14% 5% 9%7%6%15%

47%

0%

50%

100%

150%

200%

250%

300%

350%

400%

< $5 M* $5-20 M $20-100 M $100-500 M $500 M-1 B > $1 B

1990

2002

*Excludes companies with no revenue.

Source: S&P's Compustat. Data from publicly traded companies

Perc

enta

ge o

f Sale

s

Revenue

Electromedical &Electrotherapeutic

Apparatus

X-Ray & RelatedIrradiationApparatus

Dental Equipment & Sales

Orthopedics,Surgical Appliances &

Supplies

Surgical & MedicalInstruments

Diagnostics &Reagents

16

the medical technology industry at a glance 2004 the state of innovation 3 research & development

Chart 3.5National Institutes of Health Bioengineering Awards

1997 – 2002

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

1997 1998 1999 2000 2001* 2002*0%

1%

2%

3%

4%

5%

6%

7%

Funding Percent

Source: National Institutes of Health

Fundin

g (

$ M

illio

ns)

Percen

t of T

ota

l NIH

Fundin

g

Chart 3.6Number of Medical Device Patents

1989 – 2003

4,1784,500 4,737

5,5546,010

7,943 8,196

9,091

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1989 1991 1993 1995 1997 1999 2001 2003

Note: Estimates based on PTO-recommended methodology.

Source: U.S. Patent and Trademark Office

* Estimated Data

17

the medical technology industry at a glance 2004 the state of innovation 3 research & development

Chart 3.7Top Ten Factors Affecting Companies’ Ability to

Develop New Medical Technologies Over Past Five Years, 2003

Source: AdvaMed Survey of Member Companies, 2003

Chart 3.8Top Ten Factors Influencing Companies’ Product

Development Priorities Over Past Five Years, 2003

Source: AdvaMed Survey of Member Companies, 2003

46.3%

53.1%

54.3%

54.3%

56.8%

63.9%

66.7%

71.6%

74.1%

84.0%FDA Regulatory Requirements

Cost of Clinical Research

Medicare Coverage & Reimbursement Requirements

R&D Costs Related to Expansion/ Contraction into New Markets

U.S. Private Payer Coverage & Reimbursement Requirements

International Regulatory Requirements

Litigation Risks & Costs

R&D Costs Related to Acceptance in Existing Markets

Sales, General & Administrative Related to Expansion/Contraction into

New Markets

Availability/Cost of Capital Funding

43.8%

46.9%

51.6%

52.3%

55.4%

58.5%

60.0%

62.5%

78.5%

81.5%FDA Regulatory Requirements

Issues Related to Intellectual Property Protection

Customer Demand for Cost-saving or Cost-effective Technology

Price-sensitivity of Customers

Medicare Coverage & Reimbursement Requirements

Private Payer Coverage & Reimbursement Requirements

Overseas Market Opportunities

Changes in Revenues

Payer Demand for Evidence of Clinical Effectiveness and/or Cost Effectiveness

Availability/Cost of Capital Funding

SECTION II

the value of innovation

20

the medical technology industry at a glance 2004 the value of innovation 4 economic benefits

the value of innovation

Medical technology continues to transform health care in ways that could not have been conceived even ten years ago. Through advances in technology, physicians can detect diseases earlier, provide less invasive treatment options, reduce recovery times, and enable patients to resume active, productive lives more quickly.

• Medical technology has made great contributions to the screening and early detection of malignant breast tumors. When caught early, survival rates are higher and costs of treatment are lower. • A study published in the New England Journal of Medicine found that for patients who had a previous heart attack and reduced pumping capacity, there was a 31 percent reduction in the risk of death for those who received a defibrillator versus those who received conventional therapy.1

• Laparoscopic cholecystectomy (minimally invasive gallbladder removal surgery) decreased inpatient length of stay from about 7.5 days for conventional open surgery to about 2.6 days and has reduced recovery times.2

Despite these great advances, significant challenges remain for the medical technology industry. Though average review times for 510(k) applications for “substantially equivalent” devices have fallen to less than 100 days, review times for PMA applications for truly novel devices, including many breakthrough technologies, can be high – more than 250 days, at the 90th percentile. With the passage of the Medical Device User Fee

and Modernization Act (MDUFMA), the implementation of user fees should provide the FDA with the resources it needs to make the latest breakthrough technologies avail-able more quickly to those who need them.

The Medicare coverage and payment process for new technology continues to be a concern. In a recent AdvaMed survey, 44 percent of respondents indicated that the length of time it takes to secure coverage had significantly hindered their ability to bring an innovative new technology to patients, while nearly half of respondents identified inadequate payment levels as the single greatest reimbursement-related hurdle. Medicare has made certain strides in conducting a more open and accountable process for making new technology coverage decisions, including the speed with which it moved to cover the breakthrough drug-eluting stents in 2003. Even so, many beneficial technologies remain uncovered, and the time-consuming and somewhat uncertain requirements of the Medicare process pose a formidable, additional challenge to innovation and patient access to technological advances.

“The benefits from lower infant mortality and better treatment of heart attacks have been sufficiently great that they alone are about equal to the entire cost increase for medical care over time. Thus, recognizing that there are other benefits to medical care, we conclude that medical spending as a whole is clearly worth the cost.”

David M. Cutler, Ph.D., Professor of Economics, Harvard UniversityMark McClellan, M.D., Ph.D., CMS Administrator

1Moss AJ, et al. Prophylactic implantation of a defibrillator in patients with myocardial infarction and reduced ejection fraction. New England Journal of Medicine 2002;346(12):877-83.

2Cohen MM, et al. Has laparoscopic cholecystectomy changed patterns of practice and patient outcomes in Ontario? Canadian Medical Association Journal 1996;154:491-500.

SECTION II

chapter 4

economic benefits

chapter 4

economic benefits

22

the medical technology industry at a glance 2004 the value of innovation 4 economic benefits

100,000

150,000

200,000

250,000

300,000

350,000

400,000

88 89 90 91 92 93 94 95 96 97 98 99 00 01

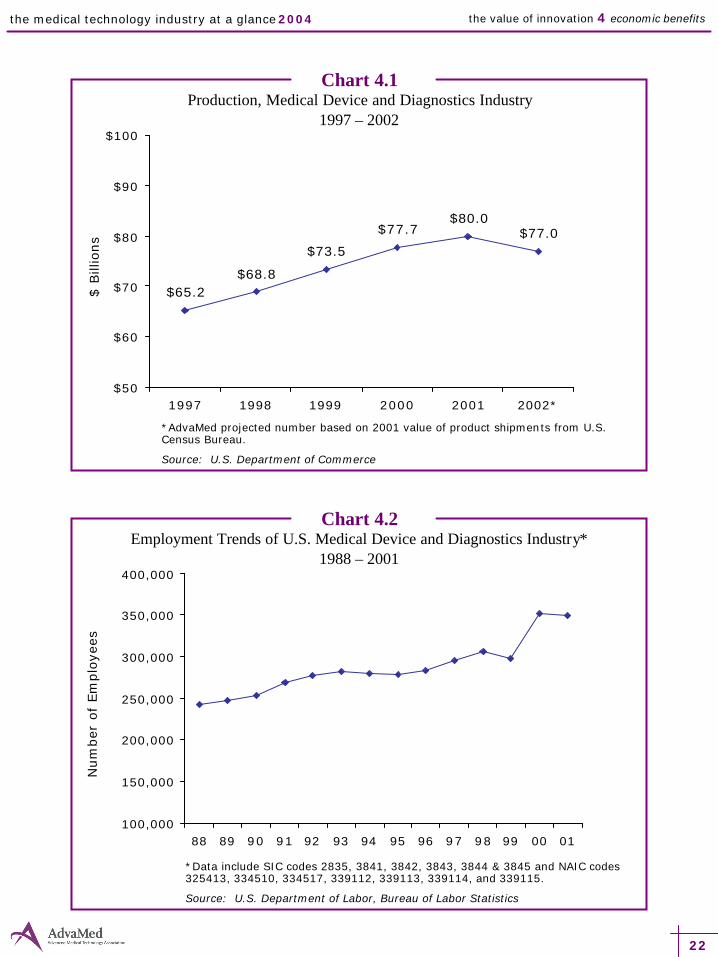

Chart 4.1Production, Medical Device and Diagnostics Industry

1997 – 2002

*AdvaMed projected number based on 2001 value of product shipments from U.S. Census Bureau.

Source: U.S. Department of Commerce

Chart 4.2Employment Trends of U.S. Medical Device and Diagnostics Industry*

1988 – 2001

*Data include SIC codes 2835, 3841, 3842, 3843, 3844 & 3845 and NAIC codes 325413, 334510, 334517, 339112, 339113, 339114, and 339115.

Source: U.S. Department of Labor, Bureau of Labor Statistics

$65.2$68.8

$73.5

$77.7$80.0

$77.0

$50

$60

$70

$80

$90

$100

1997 1998 1999 2000 2001 2002*

$ B

illio

ns

Num

ber

of

Em

plo

yees

23

the medical technology industry at a glance 2004 the value of innovation 4 economic benefits

Chart 4.3Trend in Selected Industry Producer Price Indexes

2001 – 2002

Producer Price Index (PPI) is a family of indexes that measures the average change over time in selling prices received by domestic producers of goods and services. PPIs measure price change with respect to the base period, 1982, which is set to 100.

Source: U.S. Department of Labor, Bureau of Labor Statistics, Producer Price Index website, Public Data Query

131.1

130.8

127.9

196.2

226.3

0 50 100 150 200 250

PPI-Commodities

Surgical & MedicalInstruments4

Surgical & MedicalHospitals3

In vitro & In vivoDiagnostics2

Drugs1

1SIC 283 - Medicinal chemicals and botanical products, pharmaceutical preparations, in vitro and in vivo diagnostics and biological products.

2SIC 2835 - In vitro diagnostic substances, reagents, standards and controls, blood bank, hematology, coagulation products, microbiology, serology, histology, virology, cytology products, other in vitro diagnostics, including culture media, in vivo diagnostic substances including contrast media and radioactive reagents.

3SIC 8062 - Medicare patients, Medicaid patients and all other patients (various diseases and disorders). Does not include psychiatric or specialty hospitals.

4SIC 3841 - Surgical and medical instruments and apparatus, diagnostic apparatus, syringes and needles and hospital furniture.

24

the medical technology industry at a glance 2004 the value of innovation 4 economic benefits

Chart 4.4Change in Intercontinental Marketing Services (IMS) Composite Medical-

Surgical Price Index2002 – 2003

Note: Percent change in Overall Pharmaceutical Index is 3Q02 – 3Q03; all others Nov ‘02 – Nov ‘03

Source: Hospital Materials Management

CPI (Medical Care Commodities) = 1.9%

8.1%

4.5%

2.8%1.6% 1.5%

0.4% 0.2% 0.2% 0.1%

-0.2%

-2.0%

-4.0%

0.0%

4.0%

8.0%

12.0%Su

ture

nee

dles

,

ENT instru

men

ts

Cath

eter

sPh

arm

aceu

ticals

Surg

ical a

nd

med

ical

instru

men

tsX- r

ay equ

ipm

ent

Bloo

d tran

sfus

ion

& IV

equ

ipm

ent

Diagn

ostic

ap

para

tus

Ortho

pedic

instru

men

tsCl

inica

l lab

orat

ory

instru

men

tsBl

ood

pres

sure

ap

para

tus

Elec

trom

edica

leq

uipm

ent

chapter 5

regulatory review

26

the medical technology industry at a glance 2004 the value of innovation 5 regulatory review

404

341 335

374

200

250

300

350

400

450

1999 2000 2001* 2002*

Chart 5.1PMAs Approved by FDA

1996 – 2001

28

45

26

52

45 45

0

10

20

30

40

50

60

1996 1997 1998 1999 2000 2001

Source: FDA, ODE Annual Reports

Chart 5.2Original PMA Receipt Cohort Performance: FDA Review Days

(Filing to Final Action), 90th Percentile, 1999 – 2002

Source: FDA, ODE Annual Reports

Num

ber

of

Day

sN

um

ber

Appro

ved

*2001 – 12 still under review *2002 – 16 still under review

27

the medical technology industry at a glance 2004 the value of innovation 5 regulatory review

160

153

162 162

148

150

152

154

156

158

160

162

164

1999 2000 2001 2002

Chart 5.4FDA Office of Device Evaluation Staffing Levels

1996 – 2002

Source: FDA, ODE Annual Reports

368

356

340

330

359353 354

300

350

400

1996 1997 1998 1999 2000 2001 2002

Num

ber

of

Sta

ff

Chart 5.3510(k) Receipt Cohort Performance: FDA Review Days(Receipt to Final Action), 90th Percentile, 1999 – 2002

Source: FDA, ODE Annual Reports

Num

ber

of

Day

s

28

the medical technology industry at a glance 2004 the value of innovation 5 regulatory review

Chart 5.5FDA Center for Devices and Radiological Health Funding

1990 – 2001

$159

$169

$145 $144 $145

$157

$164

$157

$164

$145$143

$123

$100

$125

$150

$175

$200

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Source: AdvaMed

$ M

illio

ns

Chart 5.6Reported Changes in Average Elapsed Development Time*

Over Past Five Years, 2003

*Development time refers to the time span from identifiable project start, e.g., beginning of design control phase, to FDA acceptance of an application for market approval/clearance.

Source: AdvaMed Survey of Member Companies, 2003

56%

73%

5%

33%

18%

81%

11% 9% 14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

510(k)s withClinical Trials

PMAs PMAs withSupplements

Decreased

Unchanged

Increased

29

the medical technology industry at a glance 2004 the value of innovation 5 regulatory review

Chart 5.7Faster to Market: Europe or U.S.?

2003

Source: AdvaMed Survey of Member Companies, 2003

U.S.5%

Europe76%

No Difference

19%

chapter 6

coverage & payment

32

the medical technology industry at a glance 2004 the value of innovation 6 coverage & payment

Chart 6.1Reported Impact of Third Party Payer Issues on Innovation

2003

Note: “Other third party payment” issues named include coding issues, demonstrating clinical efficacy, demonstrating safety, demonstrating clinical effectiveness, adding data on costs, clinical outcomes, and specific patient populations.Source: AdvaMed Survey of Member Companies, 2003

25% 28% 29%41%

28%28%

44%30%

47% 44%

27% 29%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Significantly

Some

Not

Tech assessment

requirements

Slowness in securing coverage

Adequate Medicare payment

Adding dataon clinical outcomes

Chart 6.2Reported Speed of Coverage and Payment by Third Party Payers

2003

Source: AdvaMed Survey of Member Companies, 2003

35%41%

9% 10% 11%

24%22%

9% 10%

26%28%

34%45%

26%

6%6%

28%

23%

26%

9%3%

19%13%

37%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Medicare Medicaid Private PPO Private HMO Private Feefor Service

Fastest

Slowest

33

the medical technology industry at a glance 2004 the value of innovation 6 coverage & payment

Chart 6.3Medicare Approval Process:

Drug-Eluting vs. Bare Metal Coronary Stents

In order to ensure patient access to this technology as rapidly as possible, the Centers for Medicare & Medicaid Services (CMS) took the unprecedented step of assigning two new diagnosis-related groups (DRGs) for drug-eluting stents before the CYPHER™ stent gained FDA approval. Medicare then began covering and paying for this technology upon FDA approval. In contrast, when J&J introduced the first bare metal coronary stent into the U.S. in 1994, it was not until more than three years after FDA approval that Medicare reassigned this technology to a higher-paying DRG. This 3-year time lag is typical for many new technologies.

1986

HospitalPayment3 years

Bare Metal Coronary Stents

J&J Licenses StentTechnology

1990 1993 1994 1995 1997

J&J RequestsICD-9 Code for Coronary Stents

2 Randomized Controlled Trials

(STRESS & BENESTENT)

Presented to FDA

FDA Approval of PALMAZ-SCHATZ® Coronary

Stent

ICD-9Code for Coronary

Stents

Medicare Reassigns Coronary Stents to DRG 116

Hospital Payment

Immediate

Drug-Eluting Coronary Stents

Apr 12003

Sep 2000

Oct2002

Apr 242003

Reviewed SIRIUS Study

Plans with CMS

Sep 2001

Nov2001

Medicare Assigns Drug-eluting

Coronary Stents to new DRGs 526 & 527

FDA Approval of CYPHER™

Coronary Stent

Medicare Assigns Unique

ICD-9 Code

Formal Request for ICD-9 code

Provided Preliminary

SIRIUS Clinical & Cost Data

Apr 2002

Presented 9-mo.

SIRIUS Data

Jun 2002

Presented RAVEL Clinical Data

Source: Timelines adapted from Cordis.

chapter 7

patient care

36

the medical technology industry at a glance 2004 the value of innovation 7 patient care

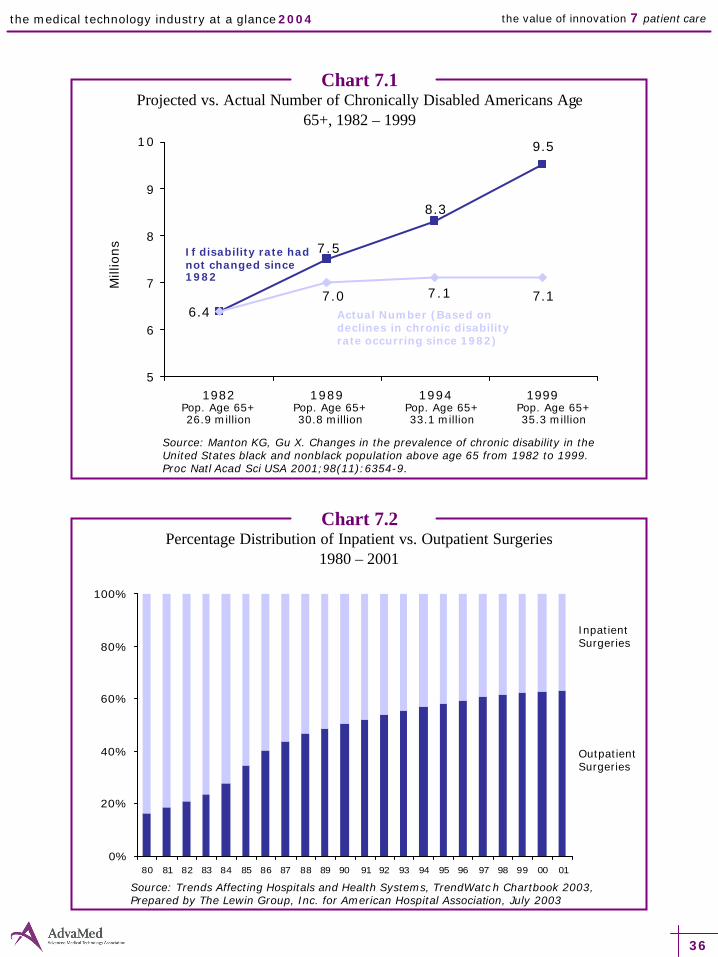

9.5

7.5

8.3

7.17.17.06.4

5

6

7

8

9

10

1982 1989 1994 1999

Chart 7.1Projected vs. Actual Number of Chronically Disabled Americans Age

65+, 1982 – 1999

Source: Manton KG, Gu X. Changes in the prevalence of chronic disability in the United States black and nonblack population above age 65 from 1982 to 1999. Proc Natl Acad Sci USA 2001;98(11):6354-9.

Chart 7.2Percentage Distribution of Inpatient vs. Outpatient Surgeries

1980 – 2001

0%

20%

40%

60%

80%

100%

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01

Source: Trends Affecting Hospitals and Health Systems, TrendWatch Chartbook 2003, Prepared by The Lewin Group, Inc. for American Hospital Association, July 2003

Mill

ions

If disability rate had not changed since 1982

Actual Number (Based on declines in chronic disability rate occurring since 1982)

Pop. Age 65+26.9 million

Pop. Age 65+30.8 million

Pop. Age 65+33.1 million

Pop. Age 65+35.3 million

Inpatient Surgeries

Outpatient Surgeries

37

the medical technology industry at a glance 2004 the value of innovation 7 patient care

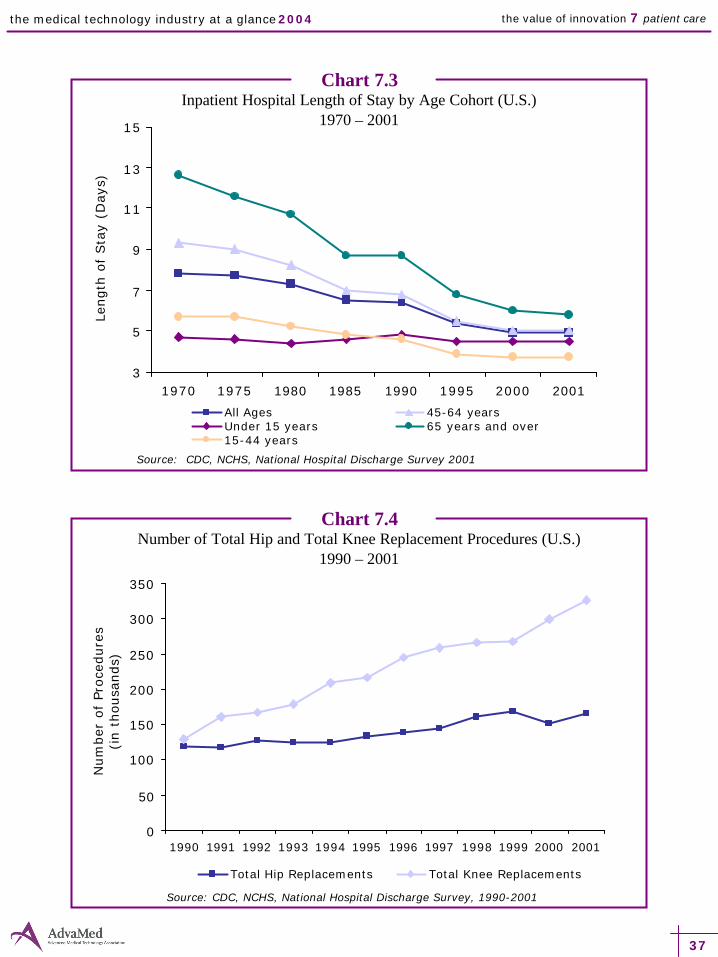

0

50

100

150

200

250

300

350

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Total Hip Replacements Total Knee Replacements

Chart 7.3Inpatient Hospital Length of Stay by Age Cohort (U.S.)

1970 – 2001

Source: CDC, NCHS, National Hospital Discharge Survey 2001

Chart 7.4Number of Total Hip and Total Knee Replacement Procedures (U.S.)

1990 – 2001

Source: CDC, NCHS, National Hospital Discharge Survey, 1990-2001

3

5

7

9

11

13

15

1970 1975 1980 1985 1990 1995 2000 2001

All Ages 45-64 yearsUnder 15 years 65 years and over15-44 years

Length

of

Sta

y (D

ays

)N

um

ber

of

Pro

cedure

s (i

n t

housa

nds)

38

the medical technology industry at a glance 2004 the value of innovation 7 patient care

Chart 7.5Total Cataract Procedures (U.S.)

1999 – 2001

*PMMA = polymethylmethacrylate

Source: Health Products Research, Inc.

0

500

1,000

1,500

2,000

2,500

3,000

1999 2000 2001Silicone IOLs Other Foldable IOLs PMMA IOLs*

Tota

l C

ata

ract

Pro

cedure

s(i

n t

housa

nds)

Chart 7.6Number of Pacemaker Implant Procedures* (U.S.)

1997 – 2001

Source: The Lewin Group analysis of the Health Care Utilization Project (HCUP), Nationwide Inpatient Sample (NIS), 1997 – 2001.

Num

ber

of

Pro

cedure

s

*Pacemaker implant ICD-9-CM codes: 37.80 - Insertion of permanent pacemaker, initial or replacement, type of device not

specified; 37.81 - Initial insertion of single-chamber device, not specified as rate responsive;37.82 - Initial insertion of single-chamber device, rate responsive; and 37.83 - Initial insertion of dual-chamber device.

0

25,000

100,000

125,000

150,000

175,000

200,000

225,000

1997 1998 1999 2000 2001

Total Implants

37.83

37.8237.8137.80

39

the medical technology industry at a glance 2004 the value of innovation 7 patient care

Chart 7.7Changes in the Treatment of Heart Attacks

1984 – 1998

Source: Cutler and McClellan, Health Affairs, Sept/Oct 2001

0%

10%

20%

30%

40%

50%

60%

1984 1986 1988 1990 1992 1994 1996 1998

Catheterization Angioplasty w/o stent

Angioplasty w/stent Bypass Surgery

Perc

ent

of

Case

s

Chart 7.8Death Rates for Diseases of the Heart (U.S.)

1950 – 2001

0

100

200

300

400

500

600

700

1950 1960 1970 1980 1990 1995 2000 2001

Source: CDC, National Center for Health Statistics

Death

s per

100,0

00 r

esi

dent

popula

tion

40

the medical technology industry at a glance 2004 the value of innovation 7 patient care

0

100

200

300

400

500

600

700

800

900

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Either Device Pacemaker ICD

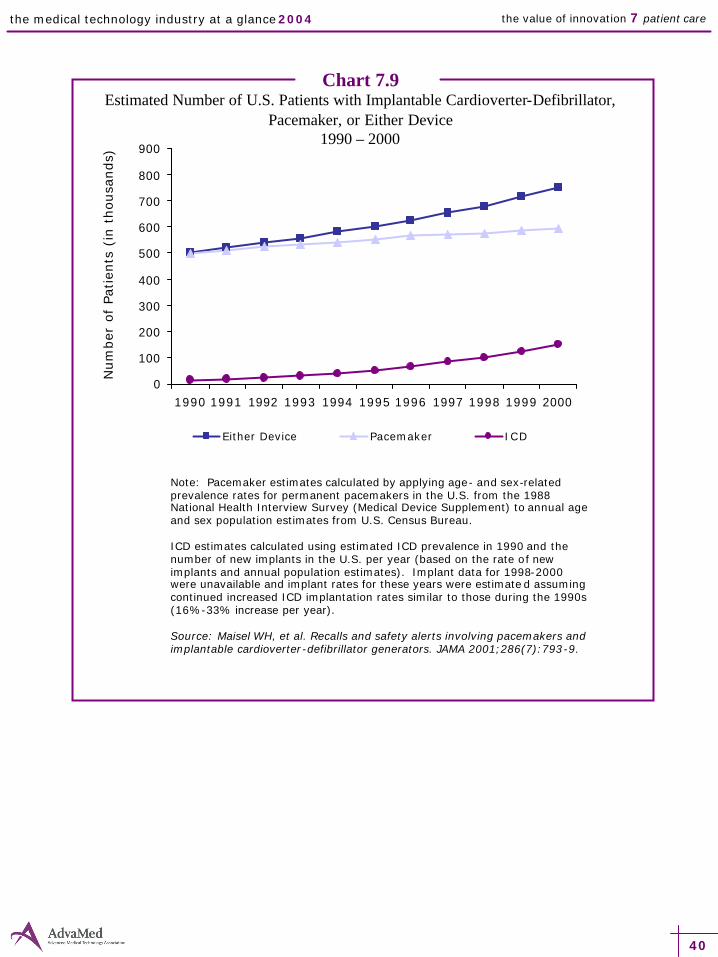

Chart 7.9Estimated Number of U.S. Patients with Implantable Cardioverter-Defibrillator,

Pacemaker, or Either Device1990 – 2000

Note: Pacemaker estimates calculated by applying age- and sex-related prevalence rates for permanent pacemakers in the U.S. from the 1988 National Health Interview Survey (Medical Device Supplement) to annual age and sex population estimates from U.S. Census Bureau.

ICD estimates calculated using estimated ICD prevalence in 1990 and the number of new implants in the U.S. per year (based on the rate of new implants and annual population estimates). Implant data for 1998-2000 were unavailable and implant rates for these years were estimated assuming continued increased ICD implantation rates similar to those during the 1990s (16%-33% increase per year).

Source: Maisel WH, et al. Recalls and safety alerts involving pacemakers and implantable cardioverter-defibrillator generators. JAMA 2001;286(7):793-9.

Num

ber

of

Patien

ts (

in t

housa

nds)

41

the medical technology industry at a glance 2004 the value of innovation 7 patient care

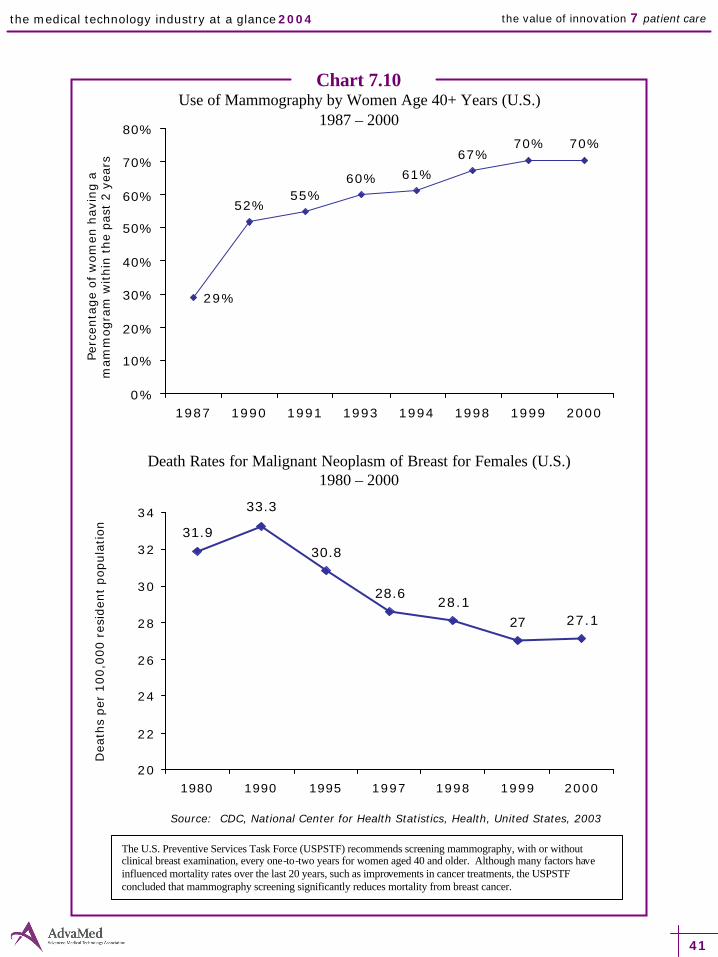

Chart 7.10Use of Mammography by Women Age 40+ Years (U.S.)

1987 – 2000

52%55%

60% 61%

67%70% 70%

29%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1987 1990 1991 1993 1994 1998 1999 2000

Source: CDC, National Center for Health Statistics, Health, United States, 2003

Perc

enta

ge o

f w

om

en h

avi

ng a

m

amm

ogra

m w

ithin

the

pas

t 2 y

ears

Death Rates for Malignant Neoplasm of Breast for Females (U.S.)1980 – 2000

31.9

33.3

30.8

28.628.1

27 27.1

20

22

24

26

28

30

32

34

1980 1990 1995 1997 1998 1999 2000

Dea

ths

per

100,0

00 r

esid

ent

popula

tion

The U.S. Preventive Services Task Force (USPSTF) recommends screening mammography, with or without clinical breast examination, every one-to-two years for women aged 40 and older. Although many factors have influenced mortality rates over the last 20 years, such as improvements in cancer treatments, the USPSTF concluded that mammography screening significantly reduces mortality from breast cancer.

42

the medical technology industry at a glance 2004 the value of innovation 7 patient care

Chart 7.11Cost vs. Cost-Effectiveness of Drug-Eluting Stents

Source: Adapted from presentation by David J. Cohen, MD, Harvard Clinical Research Institute, “Cost-Effectiveness of Sirolimus-Eluting Stents for Treatment of Complex Coronary Stenoses: The SIRIUS Trial”

Drug-Eluting vs. Conventional Stents: Initial Hospital Costs

$7,264$4,398

$2,701

$2,704

$1,379

$1,362

$0

$5,000

$10,000

$15,000

Drug-Eluting Stent Conventional Stent

Procedures Room/Ancillary MD Fees

12-Month Events: Repeat Revascularization

13.3%

6.9%4.9%

28.4%

20.0%22.9%

0%

10%

20%

30%

40%

50%

TLR TVR Any

Perc

ent

of p

atie

nts

Drug-Eluting Stent Conventional Stent

A recent economic analysis suggests that the use of drug-eluting stents is cost-effective given the reduction in long-term costs associated with their use. Previous studies have shown that drug-eluting stents reduce both angiographic and clinical restenosis compared with conventional bare metal stents. This study found that drug-eluting stents reduce the need for repeat treatments and rehospitalizations and their associated costs. While initial in-hospital costs were about $2800 higher with the drug-eluting stent than with the conventional stent, the one-year follow-up medical costs for the drug-eluting stent sample were about $2500 lower per patient than

$11,345$8,464

$5,468$8,040

$0

$5,000

$10,000

$15,000

$20,000

Drug-Eluting Stent ConventionalStent

Initial Hospitalization Follow-up

$16,813 $16,504

Drug-Eluting vs. Conventional Stents: 1-Year Medical Care

Costs

those in the conventional stent sample. Thus, the actual cost difference between drug-eluting stents and traditional stents after one year is about $300. The emergence of longer stents and improved implantation techniques could improve the cost-effectiveness of drug-eluting stents in the future.

Note: TLR= target lesion revascularization rate; TVR = target vessel revascularization rate

$11,345

$8,464

Cost Difference+$2,880 Cost Difference

+$309

Appendix

supplementary data tables

45

the medical technology industry at a glance 2004

Appendix A-1: Industry Overview

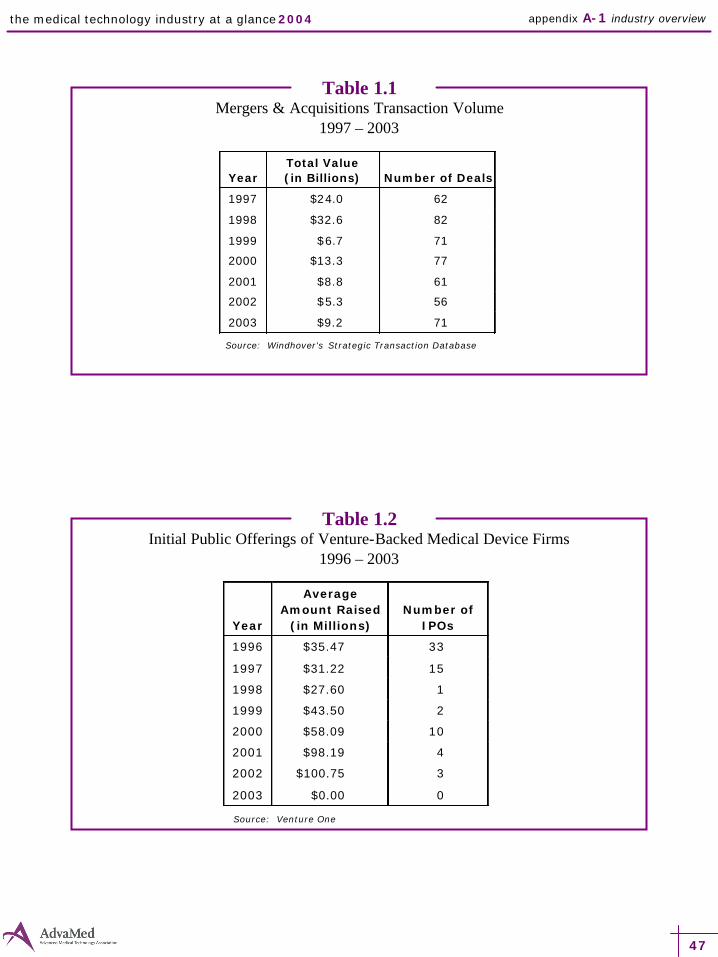

Table 1.1 Mergers and Acquisitions Transaction Volume 47(Corresponds to Chart 1.4)

Table 1.2 Initial Public Offerings of Venture-Backed Medical Device Firms 47(Corresponds to Chart 1.5)

Table 1.3 Venture Capital Financing in the Medical Device Industry 48(Corresponds to Chart 1.6)

Appendix A-2: The Global Leader

Table 2.1 Total U.S. Exports of Medical Device and Diagnostics Industry 49(Corresponds to Chart 2.3)

Appendix A-3: Research & Development

Table 3.1 National Institutes of Health Bioengineering Awards 50(Corresponds to Chart 3.5)

Appendix A-4: Economic Benefits

Table 4.1 Employment Trends of U.S. Medical Device and Diagnostics Industry 51(Corresponds to Chart 4.2)

Note: Data displayed in the appendix tables are included only for charts not showing data in corresponding chapters.

list of tables

46

the medical technology industry at a glance 2004

Appendix A-7: Patient Care

Table 7.1 Percentage Distribution of Inpatient vs. Outpatient Surgeries 52 (Corresponds to Chart 7.2)

Table 7.2 Inpatient Hospital Length of Stay by Age Cohort 53 (Corresponds to Chart 7.3)

Table 7.3 Number of Total Hip and Total Knee Replacement Procedures (U.S.) 53 (Corresponds to Chart 7.4)

Table 7.4 Total Cataract Procedures (U.S.) 54(Corresponds to Chart 7.5)

Table 7.5 Number of Pacemaker Implant Procedures (U.S.) 54(Corresponds to Chart 7.6)

Table 7.6 Changes in the Treatment of Heart Attacks 55(Corresponds to Chart 7.7)

Table 7.7 Death Rates for Diseases of the Heart (U.S.) 55(Corresponds to Chart 7.8)

list of tables

47

the medical technology industry at a glance 2004

Year

Average Amount Raised

(in Millions) Number of

IPOs

1996 $35.47 33

1997 $31.22 15

1998 $27.60 1

1999 $43.50 2

2000 $58.09 10

2001

2002

2003

$98.19

$100.75

$0.00

4

3

0

Table 1.1Mergers & Acquisitions Transaction Volume

1997 – 2003

Source: Windhover's Strategic Transaction Database

Year

Total Value (in Billions) Number of Deals

1997 $24.0 62

1998 $32.6 82

1999 $6.7 71

2000 $13.3 77

2001 $8.8 61

2002 $5.3 56

2003 $9.2 71

appendix A-1 industry overview

Table 1.2Initial Public Offerings of Venture-Backed Medical Device Firms

1996 – 2003

Source: Venture One

48

the medical technology industry at a glance 2004

Table 1.3Venture Capital Financing in the Medical Device Industry

1992 – 2003

Source: Venture One

appendix A-1 industry overview

Year

Amount Invested

(in Millions)

Number of Financing Rounds

1992 $454.70 124

1993 $432.39 114

1994 $444.09 107

1995 $610.41 129

1996 $592.80 157

1997 $854.85 177

1998 $972.07 170

1999 $1,459.68 213

2000 $2,154.23 222

2001 $1,855.12 194

2002 $1,625.04 163

2003 $1,614.75 168

49

the medical technology industry at a glance 2004

Table 2.1Total U.S. Exports of Medical Device and Diagnostics Industry

1989 – 2003

Source: U.S. International Trade Commission

Year

Total Exports (In Billions)

1989 $5.7

1990 $6.9

1991 $8.2

1992 $9.2

1993 $9.8

1994 $10.7

1995 $12.1

1996 $13.6

1997 $13.7

1998 $14.9

1999 $16.5

2000 $17.4

2001 $19.4

2002 $20.3

2003 $22.5

appendix A-2 the global leader

50

the medical technology industry at a glance 2004

Table 3.1National Institutes of Health Bioengineering Awards

1997 – 2002

appendix A-3 research & development

*Estimated Data

Source: National Institutes of Health

Year

Funding ($ Millions)

Percent of Total NIH Funding

1997 $412.6 4.6%

1998 $501.1 5.1%

1999 $697.5 6.2%

2000 $771.2 5.9%

2001* $692.4 4.6%

2002* $825.9 4.9%

51

the medical technology industry at a glance 2004

Table 4.1Employment Trends of U.S. Medical Device and Diagnostics Industry

1988 – 2001

Source: U.S. Department of Labor, Bureau of Labor Statistics

appendix A-4 economic benefits

Year

Number of Employees

1988 242,802

1989 247,333

1990 253,630

1991 268,457

1992 277,335

1993 282,430

1994 279,569

1995 277,979

1996 283,369

1997 295,360

1998 305,700

1999 297,000

2000 351,722

2001 349,571

52

the medical technology industry at a glance 2004

Table 7.1Percentage Distribution of Inpatient vs. Outpatient Surgeries

1980 – 2001

appendix A-7 patient care

Inpatient Outpatient

Year

Number of Surgeries

(in Thousands) Percentage of Surgeries

Number of Surgeries

(in Thousands) Percentage of Surgeries

1980 15,714 83.7% 3,054 16.3%

1981 15,675 81.5% 3,562 18.5%

1982 15,533 79.3% 4,061 20.7%

1983 15,130 76.2% 4,715 23.8%

1984 14,379 72.2% 5,530 27.8%

1985 13,162 65.4% 6,951 34.6%

1986 12,222 59.7% 8,247 40.3%

1987 11,691 56.2% 9,126 43.8%

1988 11,384 53.2% 10,028 46.8%

1989 10,989 51.5% 10,351 48.5%

1990 10,845 49.5% 11,070 50.5%

1991 10,693 47.7% 11,712 52.3%

1992 10,552 46.2% 12,308 53.8%

1993 10,182 44.6% 12,624 55.4%

1994 9,834 42.8% 13,155 57.2%

1995 9,701 41.9% 13,462 58.1%

1996 9,546 40.5% 14,024 59.5%

1997 9,509 39.3% 14,678 60.7%

1998 9,734 38.4% 15,594 61.6%

1999 9,540 37.6% 15,845 62.4%

2000 9,729 37.3% 16,383 62.7%

2001 9,780 37.0% 16,685 63.0%

Source: American Hospital Association, Trends Affecting Hospitals and Health Systems, 2003

53

the medical technology industry at a glance 2004

Table 7.2Inpatient Hospital Length of Stay by Age Cohort

1970 – 2001

appendix A-7 patient care

Length of Stay (in Days) by Age Cohort

Year All Ages < 15 Yrs 15-44 Yrs 45-64 Yrs > 65 Yrs

1970 7.8 4.7 5.7 9.3 12.6

1975 7.7 4.6 5.7 9.0 11.6

1980 7.3 4.4 5.2 8.2 10.7

1985 6.5 4.6 4.8 7.0 8.7

1990 6.4 4.8 4.6 6.8 8.7

1995 5.4 4.5 3.9 5.5 6.8

2000 4.9 4.5 3.7 5.0 6.0

2001 4.9 4.5 3.7 5.0 5.8

Source: CDC, NCHS, National Hospital Discharge Survey 2001

Table 7.3Number of Total Hip and Total Knee Replacement Procedures (U.S.)

1990 – 2001

Number of Procedures

Year

Total Hip Replacements (in Thousands)

Total Knee Replacements (in Thousands)

1990 119 129

1991 117 160

1992 127 167

1993 125 179

1994 124 209

1995 134 216

1996 138 245

1997 144 259

1998 160 266

1999 168 267

2000 152 299

2001 165 326

Source: CDC, NCHS, National Hospital Discharge Survey, 1990-2001

54

the medical technology industry at a glance 2004

Year

Silicone IOLs (in Thousands)

Other Foldable IOLs

(in Thousands)

PMMA IOLs (in Thousands)

1999 1085 1085 355

2000 1226 1174 208

2001 1057 1400 185

Table 7.4Total Cataract Procedures (U.S.)

1999 – 2001

Source: Health Products Research, Inc.

Table 7.5Number of Pacemaker Implant Procedures

1997 – 2001

Number of Procedures*

Year 37.80 37.81 37.82 37.83 Total

Implants

1997 4,113 19,636 23,012 113,568 160,329

1998 3,011 16,335 22,893 116,100 158,339

1999 3,318 15,460 22,295 126,936 168,009

2000 2,551 15,125 22,027 137,325 177,028 2001 2,272 15,892 22,706 159,952 200,822

Source: The Lewin Group analysis of the Health Care Utilization Project (HCUP), Nationwide Inpatient Sample (NIS), 1997 – 2001.

appendix A-7 patient care

*Pacemaker implant ICD-9-CM codes:37.80 - Insertion of permanent pacemaker, initial or replacement, type of device not

specified;37.81 - Initial insertion of single-chamber device, not specified as rate responsive; 37.82 - Initial insertion of single-chamber device, rate responsive; and37.83 - Initial insertion of dual-chamber device.

55

the medical technology industry at a glance 2004 appendix A-7 patient care

Table 7.6Changes in the Treatment of Heart Attacks

1984 – 1998

Percent of Cases

Year Catheterization

Bypass Surgery

Angioplasty w/o stent

Angioplasty w/stent

1984 11% 5% 2% 1986 20% 7% 3% 1988 28% 9% 7% 1990 35% 11% 10% 1992 43% 14% 14% 1994 48% 16% 18% 0% 1996 52% 16% 12% 5% 1998 53% 15% 6% 15%

Source: Cutler and McClellan, Health Affairs, Sept/Oct 2001

Table 7.7Death Rates for Diseases of the Heart, U.S.,

1950 – 2001

Year

Deaths per 100,000 resident

population

1950 586.8

1960 559.0

1970 492.7

1980 412.1

1990 321.8

1995 293.4

2000 257.6

2001 247.8

Source: CDC, NCHS

58

the medical technology industry at a glance 2004

3130 Fairview Park DriveSuite 800

Falls Church, VA 22042www.lewin.com

Related Documents