3 D.R.E. Approved Credit Hours

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 1/53

3 D.R.E. Approved Credit Hours

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 2/53

Copyright ©

2013

45HoursOnline holds the copyright to this book, Risk Management, 2 nd Edition. As its copyrightholder, 45HoursOnline authorizes this book’s use for our customers only. By “customer,” we referto any one who has paid for a course or package that includes this book. Customers may

download, copy, and print this book but only for their individual use. Customers may not distributethis book in any form without our written permission.

Publisher

45HoursOnline4228 Lobos Road

Woodland Hills, CA 91364(818) 716-1028 Voice(213) 477-2095 Fax

Disclaimers

Events and laws may change after publication. Although this publication has been carefullyresearched, 45HoursOnline can not guarantee the accuracy of the information contained herein.Before any suggestion presented in this book is acted upon, legal or other professional assistancemay be advisable.

These courses are approved for continuing education credit by the California Department of RealEstate; however, this approval does not constitute an endorsement of the views or opinionsexpressed by 45HoursOnline.

DRE Course Evaluation An online evaluation form for this course is available here on DRE’s website.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 3/53

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 4/53

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 5/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page iPage ii © 2013 45HoursOnline, All Rights Reserved

TABLE OF CONTENTS

1 Introduction 1

1.1 Terms 1

1.2 Client Satisfaction 2

1.3 What is Risk? 2

1.4 Preview 2

2 Fiduciary Duties 3

2.1 Who’s Who 3

2.2 Law of Agency 4

2.3 Agency Disclosure 4

2.4 Vicarious Liability 7

2.5 Scope of Agency 8

2.6 Standard of Care 9

2.7 The Duties 10

2.7.1 Duties to Third Parties 11

2.7.1.1 Listing Broker’s Duty to Perform a Visual Inspection 112.7.2 Duties to Client 12

2.7.3 Duties Imposed by Statute 13

2.7.3.1 Mandatory Disclosures 132.7.3.2 Transfer Disclosure Statement (TDS) 142.7.3.3 MLS 16

2.7.3.4 NHD 162.7.3.5 Visual Inspections 16

2.8 Seller Misrepresentation 17

2.8.1 Listing Contract 18

2.9 Civil Actions 19

2.9.1 Breach of Fiduciary Duty 19

2.9.2 Misrepresentation 19

2.9.3 Negligence 19

2.9.4 Negligent Advice/Referrals 20

2.10 Dispute Resolution 20

2.10.1 Provisions in CAR ® Contracts 21

2.10.2 Mediation 21

2.10.3 Small Claims Court 21

2.10.4 Arbitration 22

2.10.5 Litigation 22

2.10.6 DRE’s Enforcement Tools 23

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 6/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page iPage ii © 2013 45HoursOnline, All Rights Reserved

3 Areas of Risk 25

3.1 Negligent Misrepresentation 25

3.2 Dual Agency 27

3.2.1 Legal Issues 28 3.3 Minor Areas 30 3.3.1 Contract Preparation 30 3.3.1.1 Unauthorized Practice of Law 303.3.1.2 Listing Agreement 313.3.1.3 Contract Familiarity 323.3.1.4 Document Review 323.3.2 Trust Fund Handling 33 3.3.3 Broker Supervision 33 3.3.3.1 Risk Management Policies 343.3.4 Kickbacks 34 3.3.5 Fair Housing 35

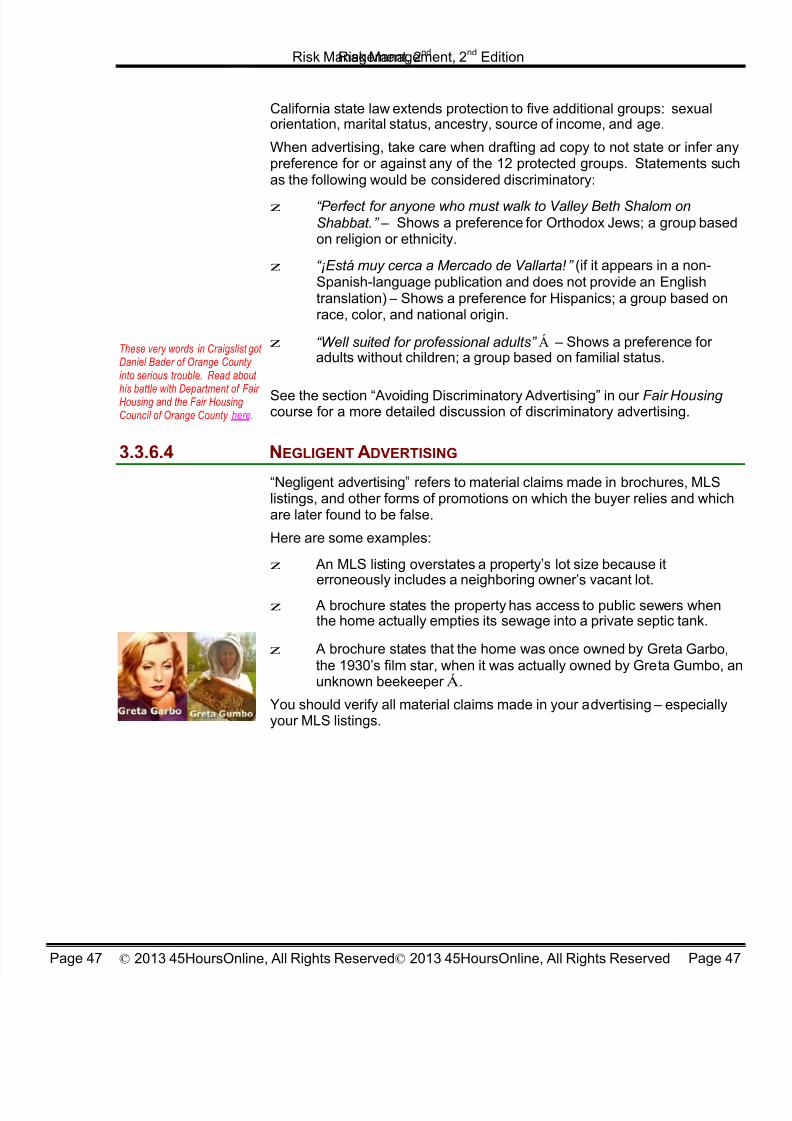

3.3.6 Advertising 36 3.3.6.1 Blind Ads 363.3.6.2 Broken Promise to Advertise 363.3.6.3 Discriminatory Advertising 363.3.6.4 Negligent Advertising 37

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 7/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 1Page 1 © 2013 45HoursOnline, All Rights Reserved

1 INTRODUCTION

We recommend you take thiscourse after you have completedour other three-hour courses( Ethics, Agency , Trust Funds, andFair Housing ). This course buildson topics described in these fourother courses.

This three-hour course will help you, a California residential real estate

agent, reduce the likelihood and intensity of disputes with your clients.Specifically, this course is concerned with disputes in which your clientsclaim damages resulting from your professional errors and omissions. Thiscourse is not concerned with disputes that arise from intentional wrongdoingsuch as fraud, theft, and illegal discrimination.

This course explains but does not focus on your legal responsibilitiestowards your clients. In the event of a dispute, your ability to prove youractions were legal is a defense – a good defense – but our focus is on howto avoid the dispute in the first place.

The topics covered in this course are mandated by the DRE (see theseguidelines for details). Most of DRE’s 50 mandated topics are also covered

in our other four three-hour courses: (1) Ethics, (2) Agency, (3)Trust Funds, and (4) Fair Housing ).

A challenge in writing this course was to arrange the 50 topics into a logicalsequence while keeping the course content to the minimum length allowedby the DRE – thirty pages.

The first of the two sections in our 30-hour Consumer Protection Reader course, “Defensive Real Estate,” is an extension of this course.

This course was last updated June, 2013.

1.1 TERMS

Before beginning, we need to define a few terms.

By “dispute” we refer to any disagreement in which your client claims youowe him restitution for damages suffered as a result of your professionalerrors and omissions.

Disputes may be resolved directly by the parties involved via negotiation orthrough neutral third-parties via mediation, arbitration, or civil litigation.

In junct ion: A court order prohibiting a party from a specif ic

course of action. Declaratory Relief: A judge’sdetermination of the parties’ r ightsunder a contract or statute.

By “clients,” we refer to buyers and sellers to whom brokers owe fiduciaryduties based in statute, contract, or common law.

By “damages” we refer to any compensation awarded to the injured party

including money judgments (dollars), injunctions Á, orders for specificperformance, and declaratory relief Á.

By “brokers,” we refer to residential real estate broker and corporatelicensees Ä and their employees and agents.

Corporate Licenses: The DRE licenses corporations to act as brokers.Corporations appoint a licensee as its “designated officer” who must be alicensed broker when initially appointed.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 8/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 2Page 2 © 2013 45HoursOnline, All Rights Reserved

1.2 CLIENT SATISFACTION

Our basic premise:

An unhappy client in a litigiousmood.

If your client becomes unhappy with his purchase, you are atrisk of being sued.

Your client may be unhappy with the condition of his home, his interest rate,his new neighbors, or his new neighborhood. The reasons for hisunhappiness may be logical or not; or reasonable or not. It doesn’t reallymatter: when your client is unhappy you are at risk of being sued.

1.3 WHAT IS RISK?

By “risk” we refer to the probability your client will become unhappy with his

transaction. Examples of risky circumstances are your ...

z buyer discovers his new home has far less square footage than hewas led to believe.

z seller discovers his house sold for considerably less than its marketvalue.

z buyer hears roosters crowing from his neighbor’s yard.

z seller who carries a second learns his mortgagee is unemployed.

When your client becomes unhappy, he will do what is our human nature,

he will blame you for his misfortune and demand restitution.

1.4 PREVIEW

In Section 2 we describe your responsibilities to your client and third partiesand your client’s right to be compensated for injuries caused by your errorsand omissions. We also describe dispute resolution methods and DRE’senforcement tools.

In Section 3 we describe two major areas of risk: (1) the risk of negligentmisrepresentation and (2) the risk of dual agency. We also describe

several other areas of relatively smaller risk.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 9/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 3Page 3 © 2013 45HoursOnline, All Rights Reserved

2 FIDUCIARY DUTIES

This Law is the subject of ourthree-hour course: Agency, 2nd

Edition.

Most of our State’ s agency lawsare in CC §§2295-2369.

The Law of Agency Á describes your responsibilities to your client andthird parties (your client’s counterparty and other stakeholders in thetransaction).

There is no single book which describes the “Law of Agency.” Much of theLaw is written into the California Codes Á but most of it is “common law.”Common law, sometimes called “judge-made law,” refers to all prevailingdecisions by State appellate courts which clarifies existing law (both statuteand common law).

Common law is sometimes clarified and enacted into statute by the Statelegislature. A well-known example is the Easton v. Strassburger (1984)decision. In that case the California Appellate Court ruled that listingbrokers have a duty to visually inspect their properties for defects anddisclose those defects to prospective purchasers.

You can find this code and allother California codes here.

The Easton decision created a new but ambiguous duty for lisiting brokers:the duty to investigate and disclose. Following the decision, brokerswondered if they could be held liable for latent defects, title defects,neighborhood nuisances, or defects concealed by the seller. To resolvethese ambiguities, the California legislature clarified Easton by passing AB1034 in 1986. That law was then encoded into the Civil Code at §2079Á.

The direction in which the common law of real estate agency is evolving isto hold brokers to increasingly higher standards of professionalism. Whilethe broker of twenty years ago may have been merely a facilitator betweenbuyer and seller, today he is almost a guarantor of the transaction.

To understand your common law duties, you must understand (1) when anagency is created, (2) the scope of your agency, (3) the standard of careyou must render, and (4) your duties as a fiduciary.

2.1 WHO’S WHO

Terms of Cooperat ion : Thecommission split between thelisting agent and the selling agentand other conditions required bythe seller or agent concerning the

sal e.

The listing agent (aka, “seller’s agent”) is the agent who signs a listingagreement with the seller. Ordinarily the listing agent offers to cooperatewith any agent who procures a buyer. His terms of “cooper ation” Á arepublished in his realty board’s MLS.

The selling agent (not to be confused with the “seller’s agent”) is the agentwho procures the buyer. If he represents only the buyer, we call him thebuyer’s agent. If the selling agent does not represent the buyer but insteadis a subagent of the selling agent, we call him the cooperating agent.

It is often the case that the buyer is unsure who his selling agentrepresents; that is, to whom his selling agent owes the fiduciary duties ofutmost care, integrity, and loyalty. The most common possibilities are thatthe selling agent: (1) represents the buyer only, (2) the seller only, or (3)both buyer and seller. Less common possibilities are that the selling agent

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 10/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 4Page 4 © 2013 45HoursOnline, All Rights Reserved

represents (4) himself, or (5) a third party (e.g., a bank, a lender, aninvestor, an estate, an HOA).

To make the agency relationships clear to all involved parties, CC §2079requires the use of the agency disclosure form (discussed later).

In this course we use the terms “agent” and “broker” interchangeably.

We use the term “principal” to refer to the buyer, the seller, or to bothbuyer and seller. We use the term “counterparty” to refer to the buyer inrelation to the seller, or to the seller in relation to the buyer.

2.2 LAW OF AGENCY

Most of the Code is quoted anddiscussed in our Ethics course.

Originally, the California law of real estate agency was based on thetraditional agency model. That model recognized agency only for theseller and left the buyer unrepresented.

In the traditional agency model, the agency relationship is established

between the listing broker and the seller via a listing agreement. In thatagreement, the seller authorizes the broker to market his property to otherbrokers via the MLS and to extend agency to cooperating brokers for ashare of the sales commission. In this model, the cooperating broker iscalled the “selling broker ” and is the agent of the seller . The cooperatingbroker therefore has “fiduciary” duties to the seller and not to the buyer.

The traditional agency model was the norm in the early 1900’s when NAR®

first published its Code of Ethics Á. Although the model worked well forREALTORS

® it created problems for buyers and sellers because …

1. buyers were left unrepresented,

2. sellers were vicariously liable for the negligent actions of both theirlisting broker and all cooperating brokers, and

3. courts imposed unintended dual agency status on both the listingand cooperating brokers after the fact.

To mitigate these problems, NAR® modified its Code and the Californialegislature enacted laws to give agency protection to buyers.

2.3 AGENCY DISCLOSURE

We refer only to CAR ® forms eventhough other firms publish simil ar forms. Other form suppl iers

Before rendering any service, the law (CC §2079.14) requires you to make aformal declaration of your intended agency relationship with your client

®

include Peninsula Regional Data using the Agency Disclosure Form (CAR Form AD ). The f orm’s wording

Service (used in San Franc iscoand the Silicon Valley) and FirstTuesday.

is exactly specified in CC §2079.16. CAR® publishes the form under the title “Disclosure Regarding Agency Relationships” and provides two slightlydifferent versions; one subtitled “Listing Firm to Seller”; the other “SellingFirm to Buyer.”

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 11/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 5Page 5 © 2013 45HoursOnline, All Rights Reserved

The Disclosure has three purposes: (1) to formally declare your agencyrelationship with respect to your principal, (2) to inform your principal ofyour agency duties, and (3) for the selling agent to clarify his agencyrelationship with the seller.

The AD must be completed in these three situations.

Click here for a Youtube videoexplaining how to fill out the ADform.

Case #1: Before signing a listing agreement ...

Execute the AD with your seller prior to signing your listing agreement.

Case #2: Before representing the buyer ...

Present the AD to your buyer when he seeks your services in more than a“casual, transitory, or preliminary manner ” (CC §2079.14 (d)).

Case #3: Before presenting an offer ...

Present an AD to the seller.

Case #4: When you change from a single agent to a dual agent ...

When your relationship with a client changes, execute a revised AD withyour client. If the change in your representation status is from single todual agency, you will have to first obtain your client’s consent to thischange and then have him sign a revised AD acknowledging your changefrom a single to a dual agent (this may be accomplished using CAR®’spurchase agreement form).

There are many ways in which your representation status with a buyer orseller may change. Here are some examples:

1. As a buyer’s agent, your buyer wishes to make an offer to a selleryou happen to already represent.

2. As a listing agent, a licensee from your brokerage presents you anoffer from his buyer.

3. As a buyer’s agent, your buyer wishes to make an offer to an ownerwhom you subsequently induce to sell with you acting as his agent.

4. Your buyer decides not to buy a home but to list his home with you.

5. As a listing agent, you decide to make an offer to purchase yourseller’s home.

6. You start your relationship with the seller as his single agent, switchto dual agency when you find him a buyer, and switch back to singleagency when your buyer decides not to purchase your seller’s

property.

The first page of the Disclosure explains the duties you owe to your client’scounterparty (i.e., “diligence, care, honesty, good faith, and disclosure”) andthe the higher fiduciary duties you him (“utmost care, integrity, and loyalty .”). The wording for the second page of the Disclosure (taken directlyfrom CC §2079.14) describes in very small print how to handle exceptionalsituations as when the buyer’s agent doesn’t deal face-to-face with the

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 12/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 6Page 6 © 2013 45HoursOnline, All Rights Reserved

seller, when a partyrefuses to sign theform, or when thebuyer’s agentdoesn’t write theoffer.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 13/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 7Page 7 © 2013 45HoursOnline, All Rights Reserved

One contingency not covered by the form is the situation in which theselling broker represents neither the seller or buyer as would occur if twounrepresented parties (perhaps a FiSBO and his next door neighbor) hireda licensee for the narrow purpose of completing the paperwork needed forthe transaction. CC §2079.20 permits exceptions:

Nothing in this article prevents an agent from selecting, as acondition of the agent ’ s employment, a specific form of agencyrelationship not specifically prohibited by this article if therequirements of §2079.14 and §2079.17 are complied with.

DRE’s license discipline includessuspension, restriction, orrevocation of your license. TheDRE also may impose fines.

The cleanest way to establish buyer’s agency is to use a buyer agreementsuch as CAR®’s Buyer Broker Representation Agreement (Form BR) .This form: (1) makes clear to your buyer the duties you owe him, (2)defines your agency as exclusive or non-exclusive, and (3) limits theduration of your agreement.

Dual agency requires the consent of both the buyer and seller; however, insigning CAR®’s residential listing agreement (Form RLA ), the seller pre-

authorizes his listing abent r to act as a dual agent should his agent procurethe buyer.

The listing agent must keep the Disclosures for three years. This isrequired for all documents signed by the agent or obtained by the agentin connection with any real estate transaction (BPC §10148).

As a fiduciary, you are required to perform your duties as you would expectyour client to perform those same duties had he your knowledge,experience, and resources. As an agent, you must be selfless in yourdevotion to your client’s interests. Should you fail to meet this standard,you risk being sued for “breach of fiduciary duty.”

If sued for breaching your fiduciary duties, your client would certainly use

your signed agency disclosure form to support his claim that you owed himthe fiduciary duties of utmost care, integrity, and loyalty. If you were unableto produce the form, the court would most likely assume that you were infact the plaintiff’s agent.

If the DRE investigates a complaint from your principal, the DRE woulddemand to see your agency disclosure. If you were unable to produce it,the DRE would likely subject you to license disciplineÁ.

Take care not to declare yourself your principal’s agent if you do not intendor if he does not expect to receive fiduciary duties from you. To dootherwise is to needlessly risk being sued for “breach of fiduciary duty”should your principal subsequently become unhappy with his transaction.

Suppose, for example, you hold an open house. At your open houseinvestor appears who wishes you to immediately submit an all-cash offer toyour seller. As the law requires, you first complete an Agency DisclosureForm in which you inadvertently elect dual agency.

When you execute the AD, you have no idea why the investor wants topurchase your seller’s home nor do you ask because you do not considerhim your client – only a third-party who wants to make an all cash offer atlist for your seller’s home.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 14/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 8Page 8 © 2013 45HoursOnline, All Rights Reserved

Two months after the sale, you are served with a lawsuit from the investor inwhich he claims that he lost a considerable amount of money owing to yourfailure to inform him that your seller’s home was subject to a zoningrestriction which precluded second story homes. His cause of action is thatyou breached your fiduciary duties by failing to inform him of the zoning

restriction. His complaint cites the AD you signed in which you elected dualagency. He argues that it was your responsibility as his agent to know hisreasons for purchasing the home and that as real estate professionalfamiliar with the local market, you would have known (or should haveknown) that he would not be permitted to add a second story.

2.4 VICARIOUS LIABILITY

Negligent acts are acts whichresult from a failure to usereasonable care. Lies , frauds,and thefts are no t negligent acts.

With the traditional agency model the seller is legally responsible for notonly the negligent acts Á of his listing agent but also those made bycooperating brokers. This legal responsibility for the acts of another is

known as vicarious l iabi l i ty . It arises out of the common law doctrine ofrespondeat superior – the responsibility of the superior for the acts ofsubordinates.

If Alice from Brokerage A cooperates with Bob from Brokerage B to sellChuck’s house and if Alice innocently misrepresents Chuck’s house as4000 sq. ft. when it is truly 3000 sq. ft., then Chuck (the seller) would bevicariously liable to the buyer for Alice’s misrepresentation. So eventhough Chuck may have never met Alice (the cooperating broker), he isliable for her misrepresentation.

Vicarious liability applies only to the negligent acts performed bysubordinates made in good faith and within the scope of the superior’s

agency.Suppose Alice had lied when she claimed Chuck’s home had 4000 sq. ft.;then she alone, not Chuck, would be liable for he fraud (assuming, ofcourse, that Chuck had no knowledge of Alice’s deception).

In California, money judgmentsmay be collected from any li abledefendant regardless of thatdefendant ’s degree of liability.The legal principal which allowsthis practice is named “ joint andseveral li ability .”

Similarly, a brokerage is vicariously liable for the professional errors madeby its agents.

Suppose George works under Sam’s broker’s license and both are sued byGeorge’s seller for negligence. If the court awarded the seller $100K andfound George (agent) 99% liable and Sam (broker) only 1% liable, the sellercould demand that Sam (broker) pay the entire $100K judgment Á eventhough George was judged to be 99 times more liable than Sam Ä.

It is a common practice for attorneys to sue any party with money orinsurance no matter how small a role that party may have had in causinghis client's injuries. Under “joint and several liability,” (aka, "Deep PocketDoctrine") plaintiffs are legally entitled to collect their entire money

judgment from any single defendant regardless of that defendants degreeof liability (source).

If a brokerage is found vicariously liable for an error made by one of itsemployees, and if the brokerage is a sole proprietorship, vicarious liability

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 15/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 9Page 9 © 2013 45HoursOnline, All Rights Reserved

attaches to the broker/owner; if the brokerage is a corporation, vicariousliability attaches to the corporation.

Put another way, if a plaintiff is awarded a money judgment against a soleproprietorship, the proprietor must pay the judgment from his personalassets (assuming the proprietor does not carry insurance). If instead, a

plaintiff is awarded a money judgment against a corporation, thecorporation must pay the judgment from its assets. Thus, the personalassets of a broker operating under his own corporation are shielded fromdamage claims arising out of negligence lawsuits against his corporation.

For example, if Sally is the designated officer for her own corporation,Sally’s Real Estate Inc., and if SRE is found 1% liable for a professionalerror made by one of SRE’s employees, call him “Dave Deadbeat,” then theplaintiff could collect his entire one million dollar judgment from either SREor Dave Deadbeat.

Note : There are many ways the plainti ff’s attorney might “ pierc e”

Sally ’s “ corporate v eil” to fi nd hisway into Sally’s deep pocket.

If Sally’s personal net worth is 25 million dollars, SRE’s is 25 cents, andDave Deadbeat’s is minus 25 thousand dollars, both SREI and Dave

Deadbeat are essentially judgment proof. The plaintiff could place a onemillion dollar lien against SRE’s future income (and/or Dave Deadbeat’sfuture income) but Sally could easily thwart this by bankrupting SRE orstarting a new corporate brokerageÁ.

2.5 SCOPE OF AGENCY

When you exceed the scope of the authority granted by your principal, youassume sole liability for the consequences. Moreover, damages caused byactions you take outside the scope of your authority are not covered by

professional liability insurance.The listing broker’s authority is normally described in his listing agreementwith his seller. For example, CAR®’s listing agreement (Form RLA) gives thebroker the authority to:

z sell a home at a particular price within a specified time period;

z exercise reasonable effort and due diligence to achieve the sale;

z order reports and disclosures, advertise, and market the home;

z list the home on the MLS and Internet; and

z use a key safe/lockbox.

Before taking any action which might be outside the scope of yourauthority, you should obtain your client’s written authorization to take thataction; otherwise, you risk assuming sole liability for any damages whichmight result from that action.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 16/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 10Page 10 © 2013 45HoursOnline, All Rights Reserved

Promotional Elephant

Suppose that without your seller’s consent you decided topromote your seller’s home by renting an elephant to be tetheredto a tree in your seller’s front yard Á. Now suppose the elephantgot loose and trampled a neighbor’s yard to smithereens. If theneighbor sued both you and your seller, it is likely the judgewould grant your seller’s motion to dismiss him from the suit on

the grounds that the rental of the elephant was taken without hisconsent and was outside the scope of the authority he grantedyou.

If, then, you were subsequently found 100% liable for the damage causedby the elephant, your E&O carrier would not pay any money judgmentawarded to the neighbor. Your insurer would argue that the elephant’srental was outside the normal scope of a broker’s authority and hence notcovered by your policy.

2.6 STANDARD OF CARE

For your client to prevail in any negligence lawsuit brought against you, hemust show you owed him a duty which you failed to provide. Examples ofduties a listing broker owes his seller are: (1) obtain fair market value, (2)exercise care during showings, and (3) provide competent advice inevaluating offers.

The sum total of all duties a broker owes his client is called the “Standard ofCare.”

The legal definition (CC §2079.2) of Standard of Care …

… is the degree of care that a reasonably prudent real estate

licensee would exercise and is measured by the degree ofknowledge through education, experience, and examination,required to obtain a license…

For an annotated copy of the Code, see our Ethics course.

Although you may not be an appraiser, real estate attorney, structuralengineer, geologist, or home inspector; as a broker you are expected toknow much more about their disciplines than your clients. For example, toobtain a broker’s license the DRE requires you to have at least two yearsexperience and to pass eight college-level real estate courses includingreal estate practice, real estate law, appraisal, real estate finance, and realestate economics. Consequently, a real estate broker is expected to knowthe fundamentals of these disciplines and to use that knowledge to protecthis clients.

NAR®’s Code of Ethics is often cited as a Standard of Care in civil actionsagainst brokers (see Barbara Nichols’ article, “Commit to the Code” inREALTOR

® Magazine Online). Some of the most relevant sections of theCode are discussed below.

Article 1: “When representing a buyer, seller, landlord, tenant, or other

client as an agent, R EALTORS® pledge themselves to protect and promote

the interests of their client.”

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 17/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 11Page 11 © 2013 45HoursOnline, All Rights Reserved

Possible violations:

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 18/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 12Page 12 © 2013 45HoursOnline, All Rights Reserved

z A buyer’s broker refers his client to a home inspector withoutmaking any effort to check the inspector’s credentials.

z The listing broker fails to disclose that many homes in the seller’ssubdivision have foundation problems.

z A selling broker encourages his buyer to make a full-price offer butfails to provide comps to support the price.

z A buyer’s broker fails to read the preliminary title report whichdescribes easements which interfere with the buyer’s intended useof the property.

Article 2: “R EALTORS® shall avoid exaggeration, misrepresentation, or

concealment of pertinent facts relating to the property or transaction.”

Possible violations:

z The listing broker makes the unfounded claim that the seller ’sneighborhood hasn’t suffered any burglaries in ten years.

z The broker fails to inform his buyer that the seller is an investornotorious among local agents for shoddy remodeling and repairs.

Article 9: “R EALTORS® , for the protection of all parties, shall ensure

whenever possible that agreements shall be in writing and shall be in clearand understandable language expressing the specific terms, conditions,obligations, and commitments of the parties.”

Possible violations:

z A broker fails to document changes to the purchase agreement(e.g., time extensions).

z A buyer’s broker fails to include a loan contingency in the purchaseagreement.

Article 11: “The services which R EALTORS® provide to their clients and

customers shall conform to the standards of practice and competencewhich are reasonably expected in the specific real estate disciplines inwhich they engage…”

Possible violations:

z The listing broker fails to advise his seller to run a credit check onthe buyer before carrying back a second.

z In a seller’s market, a listing broker advises his client to accept hisfirst offer even though it is 10% below market value.

2.7 THE DUTIES

The section describes your common law duties to your clients and to thirdparties.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 19/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 13Page 13 © 2013 45HoursOnline, All Rights Reserved

2.7.1 DUTIES TO THIRD PARTIES

A “third party” is the party opposite your client (aka, “a non-fiduciary” or“counterpar ty”). Under CC §2079.16 you owe third parties the followingduties even if your performance of these duties might have negative

consequences for your client. (Quotes are from CC §2079.16.)

z Diligence: “The diligent exercise of reasonable skill and care in the performance of the agent ’ s duties.”

z Honesty: “ A duty of honesty, fair dealing, and good faith.”

z Disclosure: “ A duty to disclose all facts materially affecting thevalue or desirability of the property that are not known to, or withinthe diligent attention and observation of the parties.”

Do not perform these duties to any degree greater than necessary if by sodoing you would disadvantage your client. For example, if your seller’s

prospective buyer asks you if the local elementary school is good and youdon’t know; answer “I don’ t know .” and not “I ’ ll find out.”

“I ’ ll find out .” would be the wrong answer because if in researching theschool you learned that it had a terrible reputation, you would have a legaland ethical responsibility to disclose its terrible reputation to the buyer withobvious negative consequences for you and your buyer. Let theprospective buyer’s agent answer the question.

Because your loyalty rests with your client, you have an obligation to learnwhatever information you can about the situation of your client’s

counterparty that could inform him in his price negotiations. For example, ifyou learned that a seller needed to sell his home quickly to flee the country

to avoid aggressive bill collectors seeking payment for a large gamblingdebt, then you should so inform your buyer and use this fact in negotiatingterms.

Remember, you must do everything that is legal and ethical to help yourclient get the best possible deal.

2.7.1.1 LISTING BROKER’S DUTY TO PERFORM A VISUAL INSPECTION

CC §2079.1 mandates that you as a listing broker conduct a visualinspection of your seller’s property and disclose to all prospective buyers“all facts materially affecting the value or desirability of the property that aninvestigation would reveal …”

Water stai ns.

The listing broker is liable for disclosing the material facts not so much forthe investigation he actually conducts but rather for what a competent andconscientious investigation wo uld reveal . Thus, if a listing broker doesn’tnotice the water marks on the wood paneling Á in his seller’s basementbecause he was wearing sun glasses at the time of his inspection, then hemight be liable for not having disclosed this defect to the home’s buyer(especially if his seller was blind).

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 20/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 14Page 14 © 2013 45HoursOnline, All Rights Reserved

As previouslymentioned, CC §2079was enacted to placelimitations on theinspection dutyrequired by the Eastonv. Strassburger(1984):

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 21/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 15Page 15 © 2013 45HoursOnline, All Rights Reserved

The inspection to be performed… pursuant to this article does notinclude or involve an inspection of areas that are reasonably andnormally inaccessible to such an inspection, nor an affirmativeinspection of areas off the site of the subject property or publicrecords or permits concerning the title or use of the property…

In Field v. Century 21 Klowden-Forness (1998), the court held that theinspection duty applies only to the listing broker – not the selling broker.Moreover, the court ruled that CC §2079 made no changes regarding anagent’s liability to his principal for injuries resulting from the agent’s breachof fiduciary duty.

In Field , the buyer’s agent (Century 21) had claimed that she was not liablefor having failed to have read her buyer’s preliminary title report because§2079 states that “the inspection [duty]… does not include or involve… anaffirmative inspection of… public records or permits concerning the title oruse of the property.” The Field court ruled that this limitation on herinspection duties did not apply to the Century 21 agent because she was

the buyer’s broker and the §2079 inspection duty applies only to the listingbroker.

Under Code of Civil Procedure §338, a defrauded person hasthree years –after the occurrenceof the fraud to file a civil action against the defrauding party ( source )

Century 21 also argued that the buyer’s suit should have been dismissedbecause it had been brought after §2079’s two-year statute of limitations.The court rejected this argument on the same grounds; that is, §2079applied only to the listing broker with respect to a third-party buyer (i.e., notrepresented by the listing broker). The court remarked that the applicablestatute of limitation is derived from the “Delayed Discovery” rule Á whichstates that the statute of limitations for a negligence suit is three years fromwhen the breach is discovered (not two years after the sale).

2.7.2 DUTIES TO CLIENT

As a fiduciary, the duties you owe your client are ambiguously defined inCC §2079.16 as the duties of “utmost care, integrity, honesty, and loyalty.”

An excellent and more detailed expression of these duties was given by theCalifornia Supreme Court in Field v. Century 21 Klowden-Forness Realty(1998):

The broker as a fiduciary has a duty to learn the material facts thatmay affect the principal ’ s decision. He is hired for his professionalknowledge and skill; he is expected to perform the necessaryresearch and investigation in order to know those important matters

that will affect the principal ’ s decision, and he has a duty to counseland advise the principal regarding the propriety and ramifications ofthe decision. The agent’s duty to disclose material information to

the principal includes the duty to disclose reasonably obtainablematerial information.

The facts that a broker must learn, and the advice and counselrequired of the broker, depend on the facts of each transaction, theknowledge and the experience of the principal, the questions asked

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 22/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 16Page 16 © 2013 45HoursOnline, All Rights Reserved

by the principal, and the nature of the property and the terms of

sale. The broker must place himself in the position of the principal

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 23/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 17Page 17 © 2013 45HoursOnline, All Rights Reserved

and ask himself the type of information required for the principal tomake a well-informed decision. This obligation requiresinvestigation of facts not known to the agent and disclosure of allmaterial facts that might reasonably be discovered.

If you represented a buyer for whom it was very important to send hisschool-aged children to an outstanding public elementary school, then itwould be your fiduciary duty to use the sources available to you to find yourbuyer a home in a neighborhood services by a good public school. Thesesources might include school rating services (such aswww.GreatSchools.org), former clients living in the neighborhood, localnewspapers, and recommendations from other agents familiar with thequality of the schools in local neighborhoods.

2.7.3 DUTIES IMPOSED BY STATUTE

Federal laws, state statutes, and municipal ordinances impose additional

duties upon licensees. Some statutes set minimum standards for anagent’s performance; others impose duties to third parties and the public,and still others mandate disclosures. These statutes are briefly describedin this section.

2.7.3.1 MANDATORYDISCLOSURES

All disclosure requirementsenacted during the last four years(2009-2013) are described in ourcourse, Consumer ProtectionReader.

There are dozens of mandatory disclosures for residential propertiesrequired by federal and state law. Among these are the Special TaxesLevies Notice (Mello-Roos and the 1915 Bond Act); geologic, earthquake,and seismic hazards; special flood hazards; and state fire responsibilityareas. There is also a plethora of mandatory disclosures for potentialenvironmental hazards including disclosures for mold, release of controlled

substances, lead-based paint; military ordnance, and industrial use zones.

According to a CAR® paper, Summary Disclosure Chart , as of January2013 there are about 40 mandatory disclosures Á. Many disclosures areonly necessary in narrow situations such as when a home is near an airportor close to a military ordnance location.

CAR®’s disclosure chart provides a summary of each disclosure, describesa disclosure “trigger,” and cross references each disclosure with a CAR®

form and supporting legal citation. CAR®’s Residential Real EstateTransaction Guide describes when and how each of these disclosuresshould be made.

You should be prepared to describe the significance of any disclosure ifasked to do so by your principal. Where any particular disclosure isespecially material, you should explain it both orally and in writing. Bytaking this precaution, you will be better able to defend yourself should yourclient later claim that you failed to make the disclosure or, if your clientadmits he signed the disclosure, that he only did so at your insistence andcomplied to your request out of trust.

Examples of disclosures that should be explained verbally and in writingare: (1) your buyer pays cash but declines to purchase title insurance, (2)

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 24/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 18Page 18 © 2013 45HoursOnline, All Rights Reserved

your seller’s TDS discloses mold or structural damage, and (3) your buyerdeclines to get a home inspection.

2.7.3.2 TRANSFER DISCLOSURE STATEMENT (TDS) The TDS is required by Article 1.5of the Civil Code commencing at

§1102. Its format is exactlyspecified at §1102.6.

The 1994 case of Jue v. Smiserestablished that buyers presentedwith disclosures late in esc r ow can acknowledge the d isclosure, complete the sale, and then suefor damages (see our Ethics

course for details about thiscase).

The buy er’s agent has the duty toevaluate the preliminary title

report and advise his client if it describes title restrictions adverseto his client ’s i nterests.

Without a doubt, the most important disclosure is the Transfer Disclosure

Statement or TDS (CAR®

form TDS).Important points to keep in mind about the TDS are the following:

z As a listing broker, you must disclose all material defects notalready disclosed by your seller. If from your visual inspection youdiscover a material defect your seller regards as insignificant, youmust nonetheless disclose even over your seller’s objections.

z You must provide the TDS to the buyer before he makes hispurchase offer. If you amend the TDS with a material addition afterthe offer has been accepted, the buyer has three days after personaldelivery of the amendment to terminate the purchase agreement. If

the amendment is mailed, the buyer has five days from the mailingdate to terminate the purchase agreement.

The law defines “material addition” as any change to the TDS afterthe purchase agreement which, had it been known to the buyerbeforehand, would have informed him to offer less or not make anoffer at all. Since materiality is often in the eye of the buyer, itbehooves listing brokers to get the TDS right the first time.

z The law (CC §2079) requires the listing broker to inspect all accessibleareas of the home and to disclose all material defects he finds.

z The law (CC §2079) does not impose upon the listing broker the duty to

inspect public records such as building permits or property records.

z The TDS provides space for both the listing and selling brokers tostate their respective disclosures.

z CC §2079 states that any lawsuit from the buyer alleging a breachof the listing broker’s duty to perform a competent visual inspectionmust be filed by the buyer within two years from the earliest of thefollowing dates: (1) date of occupancy, (2) date of the deed’srecordation, or (3) the date escrow closes.

For negligent misrepresentations by brokers (and other licensedprofessionals), the time period during which the client may file a

claim begins when the misrepresentation is discovered or shouldhave been discovered and not at the time of sale. This is called the“delayed discovery rule” and it is generally applied to the workperformed by skilled craftsmen and licensed professionals (Gryczman v.

4550 Pico Partners, Ltd. (2003)). This rule also applies to home inspectorsand overrides any contractual specifications to the contrary (Moreno v.

Sanchez (2003) ).

z A special form of the disclosure is required for manufactured homes (see CAR® Form MHTDS ).

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 25/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 19Page 19 © 2013 45HoursOnline, All Rights Reserved

Warranty: Click here for detail edinformation about the NaturalHazards Discl osur e.

z The TDS is not required for new homes which are part of asubdivision. (Disclosures for new homes in a subdivision are madeusing a special document known as a “public report.”)

z Legally enforced transfers such as foreclosures, probates, and courtorders do not require a TDS. However, in such transfers listing

brokers are not exempted from their duty to conduct a reasonablycompetent and diligent visual inspection of accessible areas (CC

§2079).

z The TDS and the Natural Hazards Disclosure Á are not warrantiesÄ, nor are they a part of any contract. Do not attach them assupplements to the contract or the counter-offer.

The buyer needs to realize that the seller’s disclosures arecompleted to the best of his knowledge and are not to be construedas guarantees that the TDS is complete or even entirely accurate.

z If two or more real estate licensees are acting as brokers in atransaction, the selling broker must deliver the statement to thebuyer unless the seller has given other written instructions fordelivery. If only one licensee is involved, that licensee must deliverthe statement to the buyer.

z If the contract requires the seller to provide a TDS and the sellerrefuses or for any reason omits it, the buyer may void his purchaseagreement.

As your client’s fiduciary, your inspection duties “depend on the facts ofeach transaction, the knowledge and the experience of the principal, the

questions asked by the principal, the nature of the property, and the termsof sale (Field v. Century 21 Klowden-Forness Realty (1998)).”

Suppose, for example, your buyer – in no uncertain terms – states that hisnext home must have a backyard large enough to build an Olympic-sizedswimming pool.

California Live Oak

You then find your buyer a suitable home with an enormous backyard in aneighborhood densely populated with California live oaks Á. Given yourknowledge of the local market and the certainty that many of the ancientoaks would have to be felled to make room for your buyer’s enormousswimming pool; it would be your duty as your buyer’s fiduciary to check thelocal ordinances to see if the oaks are protected – or, at the very least, toinsist that your buyer take the initiative to check the local tree ordinances.Should you fail in this duty and your buyer subsequently purchase the homeand later be denied a permit to build his pool, he might have an actionableclaim against you for your failure to inform him of the restriction.

With respect to the NHD or any other document prepared by a third partyexpert or public agency and delivered to the buyer, CC §1102.4 providesthat neither the seller nor his agent is liable for any errors that might becontained within the document. For example, you can not be held liable forthe errors and omission a home inspector makes in his inspection report.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 26/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 20Page 20 © 2013 45HoursOnline, All Rights Reserved

2.7.3.3 MLS

CC §1088 requires that you obtain your seller’s permission before placing

his listing into the Multiple Listing Service (paragraph six in CAR®’s Residential Listing Agreement (RLA) ). That same statute also makes the

agent “responsible for the truth of all representations and statements madeby the agent… of which that agent… had knowledge or reasonably shouldhave had knowledge to anyone injured by their falseness or inaccuracy.”Therefore, it is crucial the information you post to the MLS be accurate.

To prevent inaccuracies, you should obtain a printed copy of the MLSlisting as soon as it is posted and have it reviewed and acknowledged byyour seller.

Representations about lot size or square footage often lead to problemsbecause measuring methods are not standardized. For this reason werecommend you qualify your square foot citations using phrases such as“approximate,” “seller states that,” or “according to the Assessor ’ s records.”The size of a property is often a material consideration andmisrepresentations of size have been the source of many lawsuits.

2.7.3.4 NHD Natural Hazard Disclosure

prepares the NHD disclosures for $49.00 (as of 05-2013).

The Natural Hazard Disclosure (CAR® Form NHD) may be used to make the sixmandatory natural hazard disclosures (Earthquake Fault Zone, SeismicHazard Zones, State Fire Responsibility Areas, Very High Fire SeverityZones, Flood Zone A, and Inundation Zones) for any residential property.

2.7.3.5 VISUAL INSPECTIONS

The Lingsch Duty.

California Supreme Court’s decision in Easton v. Strassburger (1984) joltedthe residential brokerage profession. Before Easton, the disclosure duty

was the responsibility of the seller. The listing broker’s disclosure duty wasthe Lingsch Duty (after Lingsch v. Savage (1963)) which stated that thelisting broker’s disclosure duty was limited to his actual knowledge.

Before Easton, if the broker hadn’t seen the mold festooning the secondfloor ceiling of his seller’s home because he hadn’t bothered to climb thestairs; then, by the Lingsh Duty Á, the buyer could not hold the broker liablefor having failed to disclose it.

After Easton, the Court imposed a “should-have-known” standard. TheCourt reasoned that a broker had a duty to conduct at least a visualinspection of his seller’s home and disclose whatever a reasonablycompetent real estate investigation should have revealed.

Although Easton made it clear that the listing broker had a duty to inspecthis seller’s home, the Court gave no details as to how thorough such aninvestigation should be. To clarify the broker’s inspection duty, theCalifornia legislature passed a bill subsequently written into the Civil Codeas §2079 et seq. That statute requires a licensee to…

… conduct a reasonably competent and diligent visual inspection ofthe property offered for sale and to disclose to that prospective

purchaser all facts materially affecting the value or desirability of the

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 27/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 21Page 21 © 2013 45HoursOnline, All Rights Reserved

property that an investigation would reveal.… the inspection…does not include or involve an inspection of areas that arereasonably and normally inaccessible… nor an affirmativeinspection of areas off the site of the subject property or publicrecords or permits concerning the title or use of the property.

With regard to your client, your §2079 duty to investigate, inspect, anddisclose is a minimum standard. Your actual duty depends on yourknowledge of your client’s special needs, wishes, and requirements.

On CAR®’s Real Estate Transfer Disclosure Statement (TDS) , sections I

and II are completed by the seller. The listing and selling brokers fill outsections III and IV respectively “based on the results of the careful visualinspections they have conducted .” All parties and brokers sign Section V.

2.8 SELLER MISREPRESENTATION

Red flag : Security bars and pit

pull.

Suppose a seller tells his listing broker a bald-faced lie: that his home hadnever been burgled – that it was only because his overly anxious wife hadinsisted that they adopted a pit bull and installed window security barsÁ.

Relying on his seller’s lie, the listing broker assures all buyers that hisseller’s neighborhood is safe.

The Smiths purchase his seller ’s home and immediately remove the uglysecurity bars. One night, two months later, the Smiths are robbed atgunpoint in their very own master bedroom. When the police arrive, theyinform the Smiths their home had been burgled on five other recentoccasions.

Is the listing broker liable to the Smiths for having repeated his seller’s lie?No, the broker is not liable for any fraud perpetrated by his seller and“republished” to prospective buyers providing the broker was not complicitin the fraud and that it was not reasonable for the broker to have hadknowledge or suspicions to the contrary.

However, should the Smiths sue their seller for fraudulentmisrepresentation, the broker should not be surprised if he is named co-defendant.

To reduce the risk of being sued for false claims made by others, listingbrokers should take care to qualify the source of their claims (preferably inwriting):

z “My seller told me this neighborhood is very safe and that his homehas never been burgled.”

z “My seller told me his home was designed by Julia Morgan, thearchitect of Hearst ’ s Castle.”

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 28/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 22Page 22 © 2013 45HoursOnline, All Rights Reserved

One final caveat… It is always a good idea to have the law on your side

Gorbachev: “Trust but verify.”

“Coc k -a-Doodle-Dooo”!

z “My seller told me his neighbor only raises hens since he has neverheard a rooster crow.”

It is the fiduciary responsibility of the buyer’s broker (be he a single or dual

agent) to verify any claim considered material to his buyer (or delegate thisresponsibility to his buyer or to a professional). For example, if a dual agenthad repeated his seller’s claim that his neighbor did not raise roosters, itwould be his duty to verify the claim (assuming of course that uninterruptedsleep was important to his buyer).

2.8.1 LISTING CONTRACT

“My neighbor’s are wonderful !”

Lis pendens : A public not ic esecuring a claim on a property

pending resolution of a legaldispute.

CAR®’s Residential Listing Agreement (Form RLA) contains twoparagraphs which limit your liability should your seller misrepresent hisproperty without your knowledge.

The first is the Seller Representationsprovision by which the seller

warrants that he has disclosed to you all known encumbrances includingnotices of default, bankruptcy proceedings, lis pendens Á notifications, andliens; and promises to notify you should he learn of any new encumbrancesduring the listing period.

The second is the Broker’s and Seller’s Duties provision which reads:

… Seller further agrees to indemnify, defend, and hold Brokerharmless from all claims, disputes, litigation, judgments and attorneyfees arising from any incorrect information supplied by Seller, or from any material facts that Seller knows but fails to disclose.

In other words, by signing your listing agreement your seller agrees to payfor the cost of your defense should his buyer sue you for hismisrepresentations.

This provision does not exempt you from liability for your seller’smisrepresentations if (a) you should have known his representations werefalse, or (b) as a dual agent knew his representations were important toyour buyer but failed to verify them or to advise your buyer to do so.Remember also, that you have a statutory duty (CC §2079) to third parties toexercise reasonable skill and care in the performance of your duties and todisclose all material facts within your diligent attention.

but it can be an unreliable ally in a civil suit. Even with the seller’s warrantyprovisions in the listing agreement and even though the common lawexempts you from liability for “republishing” your seller’s untruths, theseprotections can be of little value when your adversary is an attorney skilledin exploiting the ambiguities in the law. Therefore, with respect to what yourseller tells you, remember President Reagan’s immortal words to Mikhail

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 29/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 23Page 23 © 2013 45HoursOnline, All Rights Reserved

2.9 CIVIL ACTIONS

Cause of Act ion: A specific l egalclaim with legal elements whichmust be proved to substantiate

the claim.

Should your client sue you, he is likely to claim one or more of these threecauses of action Á: “Breach of Fiduciary Duty,” “Negligent

Misrepresentation,” and “Negligent Advice.”

2.9.1 BREACH OF FIDUCIARY DUTY

To justify a claim for damages for a breach of fiduciary duty, the plaintiffmust prove (1) you owed him a fiduciary duty; (2) you failed to provide thatduty; and (3) his injuries were the result of your breach.

Here are some examples of breach of fiduciary duty claims:

z A seller sues his agent for having revealed to the buyer’s broker thelowest offer he was willing to accept (violation of the fiduciary duty of

“loyalty”). z A buyer sues his agent for having failed to read his property’s

preliminary title report which had described an easement permittinghis neighbor to drive cattle through the home’s backyard (violation ofthe fiduciary duty of “utmost care”).

z A buyer sues his dual agent for having falsely denied that the sellerhad an ongoing boundary dispute with his neighbor (violation of thefiduciary duty of “honesty”).

2.9.2 MISREPRESENTATION

Resciss ion: Cancellation of thesale or return of commissi on.

Misrepresentation is a false statement made by a seller or his broker toinduce a prospect to buy. When the false statement is made by a brokerabout a real estate matter, most courts hold a statement of opinion by thebroker as a statement of fact. A finding of misrepresentation allows for theremedies of rescission Á and damages.

The law distinguishes three forms of misrepresentation: (1) an intentionalmisrepresentation is a lie or any statement made with a reckless disregardfor the truth, (2) a negligent misrepresentation is a statement the agentshould have known was false; and (3) an innocent misrepresentation is afalse statement made in good faith, based on reasonable grounds.

Claims alleging “negligent misrepresentation” and “innocentmisrepresentation” represent the majority of claims made by sellers andbuyers against their brokers. These have been called, “didn’t know – didn’ tverify ” misrepresentations.

2.9.3 NEGLIGENCE

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 30/53

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 31/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 25Page 25 © 2013 45HoursOnline, All Rights Reserved

The duty may arise out of statute, such as the duty to disclose windowsecurity bars (CC §1102.16); or the duty may arise out of common law, such asduty for the buyer’s broker “to learn the material facts that may affect the

principal's decision” (Field v. Century 21 Klowden-Forness Realty (1998)).

2.9.4 NEGLIGENT ADVICE /REFERRALS

Negligent advice imposes liability for giving faulty professional advice orreferrals when the broker should have known the advice was wrong orshould have known the person whom he referred to perform a service wasnot qualified or competent to do so.

Referring a home inspector or some other service provider to your clientwithout performing due diligence to ensure the person you recommended isqualified may result in you being named as a defendant in a civil actionshould that service provider’s incompetence cost your client money.Remember that under joint-and-several liability, a plaintiff may demand youpay his entire money judgment even if you are found as little as onepercent liable for his injuries.

To avoid being found liable for a negligent referral, we recommend you …

z do not recommend any friend, relative, or any one who providesyou a referral benefit other than a satisfied client.

z give your client good reasons for your recommendation.

z refer licensed contractors whenever possible, particularly those whobelong to trade associations.

z get a release if any client chooses someone you have reason todistrust (e.g., the buyer’s dead-beat brother-in-law).

z only recommend that your clients hire contractors and serviceproviders who are insured. “Licensed, bonded and insured ” meansthat if your plaintiff wins a money judgment from both you and yourreferral, his attorney will most likely seek to collect his money

judgment from your referral’s insurance company and not from you.

z only add a service provider to your list if he has good references.

By taking proactive steps such as these and documenting them in yourtransaction file, you will be less likely to be sued for the incompetency ornegligence of someone you recommend.

2.10 DISPUTE RESOLUTION

These methods are described ingreater detail in our course, TheConsumer Protection Reader.

In this section we briefly describe four methods of third-party-assisted dispute resolution. These methods are (in ascending order of expense): (1)mediation, (2) small claims, (3) arbitration, and (4) litigation.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 32/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 26Page 26 © 2013 45HoursOnline, All Rights Reserved

2.10.1 PROVISIONS IN CAR ®

CONTRACTS

CAR®’s Residential Listing Agreement (Form RLA) states that shouldeither of you fail to first try mediation before resorting to arbitration orlitigation, then the moving party forfeits his right to recover attorney fees in

any subsequent action. An exception is made for using Small Claims Courtin lieu of mediation.

By initialing the Agreement’s Arbitration of Disputes provision Ä, both youand your seller agree that should mediation fail, binding arbitration shouldbe the recourse rather than litigation.

CAR ® contracts permit the use ofthe Small Claims Court to resolv eany dispute in lieu of mediation,arbitration, or l itigation.

Arbitration of Disputes provision as it appears in the Agreement.

CAR®’s Purchase Agreement (Form RPA-CA) is an agreement betweenthe buyer and seller; brokers are not party to the Agreement. It (like CAR®’slisting agreement) requires the parties to first try mediation to resolve theirdispute; otherwise, the party initiating arbitration or court action withouthaving first attempted to mediate the dispute forfeits his right to recoverattorney fees in any subsequent legal action. The Agreement states thatshould the buyer and seller agree to its Arbitration of Disputes provision(similar to that which is shown above), both must submit their dispute tobinding arbitrationÁ.

2.10.2 MEDIATION

Mediation is an informal and alternate form of dispute resolution directed bya third party. The first step after the parties agree to mediate their disputeis for the parties to agree upon a mediator.

Click here to see a real estateattorney ’s web page advertising

his firm’s mediation servic es.

The mediator can be anyone – a bartender, a rabbi, a mail man – nospecial credentials or training is required. However, it is usually a good ideato select a trained mediator who knows the Real Estate Law Á. CAR®

agreements require the parties to split the cost of the mediator and othermediation expenses. Again, either party may choose to take his

counterparty to Small Claims Court to force a quick settlement (seefollowing section).

2.10.3 SMALL CLAIMS COURT Equitab le Relief : Court remediesthat require parties to performcertain acts or specifically performa contract.

Small Claims Court can only be used by plaintiffs seeking monetarydamages of less than $10,000. Small Claims Court cannot be used toobtain equitable relief Á; that is, any form of restitution other than a money

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 33/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 27Page 27 © 2013 45HoursOnline, All Rights Reserved

award (not, for example, to enforce a contractor to perform).

The key advantages of resolving your dispute using Small Claims Court arespeed, economy, and finality. Neither party may be represented by anattorney, even if the defendant is a corporation. Only defendants mayappeal their case to Superior Court but, should the appellant court find thatthe defendant’s appeal is without merit, it can award the original plaintiff upto $2,000 for attorney’s fees, transportation, and lodging.

2.10.4 ARBITRATION Civi l Court : A court that handlesnon-criminal legal matters inwhich private individuals or entities sue one another for eithermoney or some other type ofrelief.

Arbitration is free market justice – justice you pay for. But becausearbitration is usually faster and less formal than civil litigation and becausedecisions by arbitration panels are almost always final; arbitration is usuallyless expensive than public justice via a civil court Á (exception: SmallClaims Court).

Unlike public justice where all documents and proceedings are open to thepublic, arbitration is 100% private. No one other than the involved partiesneed ever know the outcome of a dispute settled by arbitration; not yourclientele, not homeowners in your farm, not other licensees in yourcommunity, not the press, and certainly not the DRE. (If you fail to pay amoney judgment awarded by a civil court or by an arbitration panel, the

judgment creditor may apply for restitution to DRE’s Recovery Fund – forDRE’s explanation of this fund, click here.)

Arbitration decisions are supposed to be based on the applicable law; thatis, based on the law as applied in civil courts; but since arbitration decisionscannot be appealed, legal mistakes (for example, the admission of hearsayevidence) can not be remedied.

CAR® agreements include an Arbitration Provision which is enforceableonly when the parties have initialed the provision.

2.10.5 LITIGATION

Other than trial by combat, civil litigation is the worst way to resolve adispute. It is expensive, time consuming, lengthy, and painful. Becauselitigation is complex, most litigants must hire an attorney to serve as theirchampion at a cost of hundreds of dollars per hour .

Litigation starts with a lawsuit (aka, a “complaint”). The person initiating thelawsuit is the “plaintiff”; the person sued, the “defendant.” The plaintifftypically sues anyone he believes responsible for his losses and who hasthe wherewithal to pay his damage claims.

Defendants with “deep pockets” – especially those with E&O – areespecially prized. Under California law, the plaintiff may collect his entiremoney judgment from the defendant with the deepest pocket even if thatdefendant was found only one percent liable for the plaintiff ’s injuries (seeWiki’s article on “Joint and Several Liability”).

The plaintiff initiates a lawsuit by filing a “complaint” at the countycourthouse. The complaint states the causes for the action, the factual

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 34/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 28Page 28 © 2013 45HoursOnline, All Rights Reserved

justification, and “prays” the court to grant him “relief” (i.e., money or someother court-ordered form of restitution).

A typical complaint is written to intimidate the defendants into quicklypaying a settlement to avoid incurring ruinous litigation costs. If thedefendant fails to file an “answer” (a rebuttal), the plaintiff is entitled to a

default judgment in the full amount of his claim. Often, the defendantreturns his answer accompanied by his own complaint (“cross complaint”)in pursuit of the strategy that the best defense is a good offense.

After the defendant files his answer, the parties engage in “discovery” tocompel one another to reveal the facts each needs to prevail at trial.Discovery may consist of written questions requiring written answers(“interrogatories”), witnesses questioned before a court stenographer(“depositions”), and compulsory exchanges of documents (“subpoenas”).During the discovery process, the parties are free to amend theircomplaints with new causes of action and claims for additional damages.

Every step in civil litigation can be delayed by legal challenges argued

before a judge (“motions”). Often these challenges are initiated by thestronger party in a deliberate effort to exhaust the resources of the weakerfor the purpose of forcing the weaker party to quit his suit or settle for apittance.

Only a tiny percentage of suits are ever resolved by judge or jury. Toprevail in a civil trial, the plaintiff need only convince 3/4th’s of the jury(typically composed of postal employees and retired people) that hisdefendant was probably responsible for his injuries (source). Thestandard of proof in civil cases is “preponderance of evidence” –meaningthe plaintiff need only convince the judge or jury that his case against thedefendant is more likely true than not true.

Even after a judgment is rendered, litigation may continue. Any party mayappeal the decision if he believes he was found liable because the judgemade a significant legal error. If the appeal is rejected, the “appellant” mayappeal to a higher court and if that appeal is unsuccessful appeal to aneven higher court until ultimately reaching the end of the road: theCalifornia Supreme Court for decisions appealed from State courts, or theUnited States Supreme Court for decisions appealed from Federal courts.

If the plaintiff prevails and is awarded a money judgment, then he has thefrequently difficult and sometimes impossible task of collecting it – neitherthe court nor the sheriff will assist him. If the plaintiff (now called the“judgment creditor”) is lucky, the defendant (called the “judgment debtor”)will pay without complaint. But often the judgment creditor is unlucky. His

efforts to collect can by thwarted in innumerable ways; first and foremost:the big “BK” – bankruptcy – the end of the road for the plaintiff where theplaintiff more often than not collects a great Big Zero for all his expense,troubles, and efforts.

2.10.6 DRE’S ENFORCEMENT TOOLS

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 35/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 29Page 29 © 2013 45HoursOnline, All Rights Reserved

The DRE’s primary responsibility is to protect the public from unethical,deceptive, unprofessional, and unlawful conduct by its licensees. Notice ofwrongful conduct comes to the attention of DRE’s Enforcement Departmentin several ways. Principal among these is receipt of a written complaint

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 36/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 30Page 30 © 2013 45HoursOnline, All Rights Reserved

The DRE had access to DM V’srecords up until 2001 when theDMV changed its policy to permitonly “sworn peace officers” toaccess their database. SB 53returned DRE’s access to theDMV database.

(using DRE form 519A). The DRE receives from eight to ten thousandsuch complaints a year.

Besides warnings and public rebukes, prior to 2012 the only disciplinaryactions which could be taken by the DRE were to revoke, suspend, orrestrict a wr ongdoer’s license. But beginning in 2012, SB 53 granted the

DRE new enforcement tools:

z It may levy fines not to exceed $2,500 on both licensees andunlicensed persons found to have violated the Real Estate Law.

z It may go directly to Superior Court to enforce an administrativesubpoena (prior to 2012, the DRE had to work through the State

Attorney General as its proxy).

z It may publicize its investigations into alleged licensee wrongdoing.

z It may access Department of Motor Vehicles’ database to find alicenseeÁ.

If the DRE finds evidence of criminal wrongdoing it can refer a case to theState Attorney General for possible prosecution. The DRE can not settlecommission disputes, collect money judgments, or resolve disputesbetween licensees and their clients.

8/11/2019 (247588053) Risk Management, 2nd Edition, Book(1)(1)

http://slidepdf.com/reader/full/247588053-risk-management-2nd-edition-book11 37/53

Risk Management, 2nd EditionRisk Management, 2nd

© 2013 45HoursOnline, All Rights Reserved Page 31Page 31 © 2013 45HoursOnline, All Rights Reserved

3 AREAS OF RISK

This section describes several areas of risk. Two of the most important aregiven prominence: (1) negligent misrepresentation and (2) dual agency.Several relatively minor areas of risk are also described: (a) contractpreparation, (b) trust fund violations, (c) RESPA violations, (d) fair housingviolations, and (e) the failure of a broker to adequately supervise hisaffiliated licensees.

3.1 NEGLIGENT MISREPRESENTATION

Consider what Matt Farmer, associate real estate council for the Oregon Association of REALTOR