Current & Future Trends in International Trade International Trade Transaction Process within developed, developing and transitional economies Trade Facilitation System & Trade Security Single Window Concept From Paper to Digital documents ʹ e standards Transaction Cost

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Current & Future Trends in International Trade

International Trade Transaction Process within developed,

developing and transitional economies

Trade Facilitation System & Trade Security

Single Window Concept

From Paper to Digital documents – e standards

Transaction Cost

Trade Facilitation

• Improving Documentary Requirements, and procedures on Trade in Goods

(EXPORT + Import + Transit)• Reforming Customs Procedures• Making Trade Procedures as Efficient as possible through:

procedures, documentation and information.

• eliminating all unnecessary elements and duplications in formalities, processes and procedures

• Alignment of national procedures, operations and documents with international conventions, standards and practices

• Process of developing internationally standard formats for practices and procedures, documents and information

International Organizations DealingWith Trade Facilitation , International rules and standards

• IMO

• ISO

• UN-CEFACT

• WCO

• WTO

• IMF

• World Bank

• OECD

• UNCTAD

• ITC

Impediment to Trade Facilitation

• excessive data /documentation requirements• Red-tapism• High release and clearance times • Antiquated customs techniques and inefficiencies leading to high logistics

costs• Absence of co-ordination between customs and other agencies• Inadequate transit regimes• Corruption• Regulatory/administrative barriers in establishing and operating new

businesses • Port congestion• Scarce use of IT• Lack of quick legal redress• Unattractive tariff regimes

• ORDER/PREPARE• TRANSPORT• CUSTOMS• PAYMENT• Exporter/importer• Insurance company• Chamber of commerce• Export/import agent• Licensing authorities• Embassies• Credit checking company• Supplier• Other intermediaries

Freight forwarder• Transporter/carrier• Shipping line• Export inspection agency• Other intermediaries

• Custom clearance• Health authorities• Port management• Custom brokers• Other intermediaries

Bank• Financial institutions• intermediaries

Too Many Players in the Value Chain

Too Many Documents

• Enquiry• Order• Despatch advice• Collection order• Payment order• Documentary credit• Forwarding instructions• Forwarder's invoice• Goods receipt• Air waybill• Road consignment note• Rail consignment note• Bill of lading

• Freight invoice• Cargo manifest• Export licence• Exchange control doc.• Phytosanitary certificate• Veterinary certificate• Certificate of origin• Consular invoice• Dangerous goods declaration• Import licence• Customs delivery note• TIR carnet

Types of Risks

Commercial risks

Political risks

Risks arising out of foreign laws

Cargo risks

Credit risks

Exchange fluctuations risks.

Objective

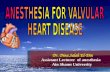

• To understand International Supply Chain model constituting of trade facilitation & e-business solutions that meet the needs of the potential 45 Parties involved in the execution of National and International TradeTransactions involving Several hundred activities undertaken in some 70 relationships whilst recognising the variety of technical and business capabilities of the parties and contribute resulting in cost savings while transacting International Trade.

• The International Trade Transaction Process consists of integrated and coordinated flows of information, goods & payments

Source: The UN/CEFACT International Supply Chain Reference Model

International Trade Transaction Process

CommercialProcedures

• Establish Contract• Order Goods• Advise On Delivery• Request Payment

TransportProcedures

• Establish Transport Contract

• Collect,Transport and Deliver Goods

• Provide Waybills, Goods Receipts Status reports etc.

RegulatoryProcudures

• Obtain Import/Export Licences etc

• Provide Customs Declarations

• Provide Cargo Declaration

• Apply Trade Security Procedures

• Clear Goods for Export/Import

Financial Procedures

• Provide Credit Rating• Provide Insurance• Provide Credit• Execute Payment• Issue Statements

INVOLVES

Prepare For

ExportExport Transport Import

SHIPBUY PAY

Prepare For

Import

WTO-Related ArticlesGATT 1994

Art V Freedom of Transit

Art VIII Fees and Formalities connected with importation and exportation

Art X Publication and Administration ofTrade Regulation.

Article V: Freedom of Transit

• No obstacles or unreasonable charges on transit• Freedom of transit… most convenient routes…• Transit;

– No delays, no restrictions– Exempt from custom duties or other charges– Administrative expenses (reasonable, cost of services)

• MFN treatment with respect to ALL:» Charges;» Regulations;» formalities

Article VIII: Fees & Formalities

• Limited in amount (cost of services rendered)• Not to represent protection to domestic products• No import fax for fiscal purposes• Import and export formalities should be reduced• Document requirements:

– Less– Simplified

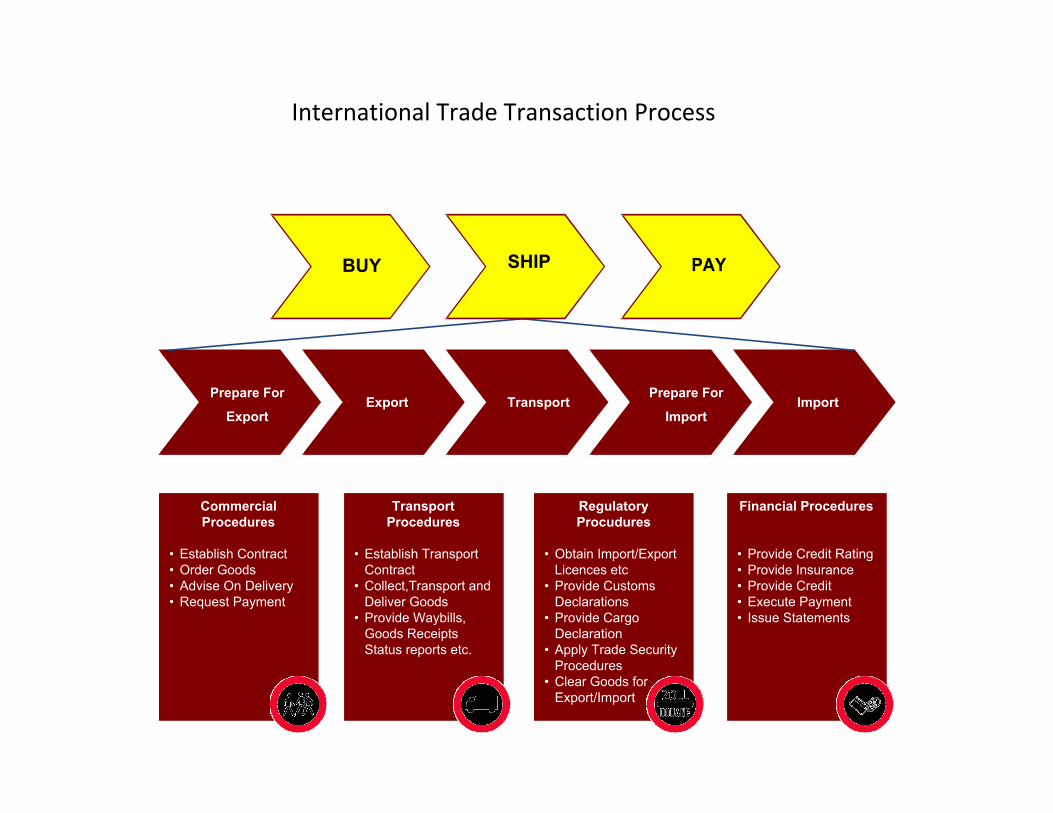

Article X: Transparency

Publication and Administration of Trade Regulation• Publication ALL Laws, regulation, administrative ruling, and judicial

decisions (import + export)• Measures imposing a new requirement, restriction, or prohibition on

imports, or payment, shall be published before enforcement• Uniform, impartial, and reasonable administration of laws, and decisions

on Import and Export.• Judicial/Arbitral System to review and correct action relating to customs

matters.

Other WTO AgreementsRules on Trade Facilitation

1. Custom Valuation Agreement

2. Agreement on Pre-Shipment Inspection

3. Agreement on Import Licensing Procedures

4. Agreement on Rules of Origin

5. Agreement on Technical Barriers to Trade

6. Agreement on Sanitary and Phyto-Sanitary Measures

Trade Security Initiatives

•World Customs Organization’s Advanced Cargo Information (ACI)

• US Customs 24 Hour Rule , CTPAT

• International Maritime Organization’s International Ship & Port Facility Security Code (ISPS)

• The European Commission communication on a Simple & Paperless environment for Customs & Trade , AEO

• RMS

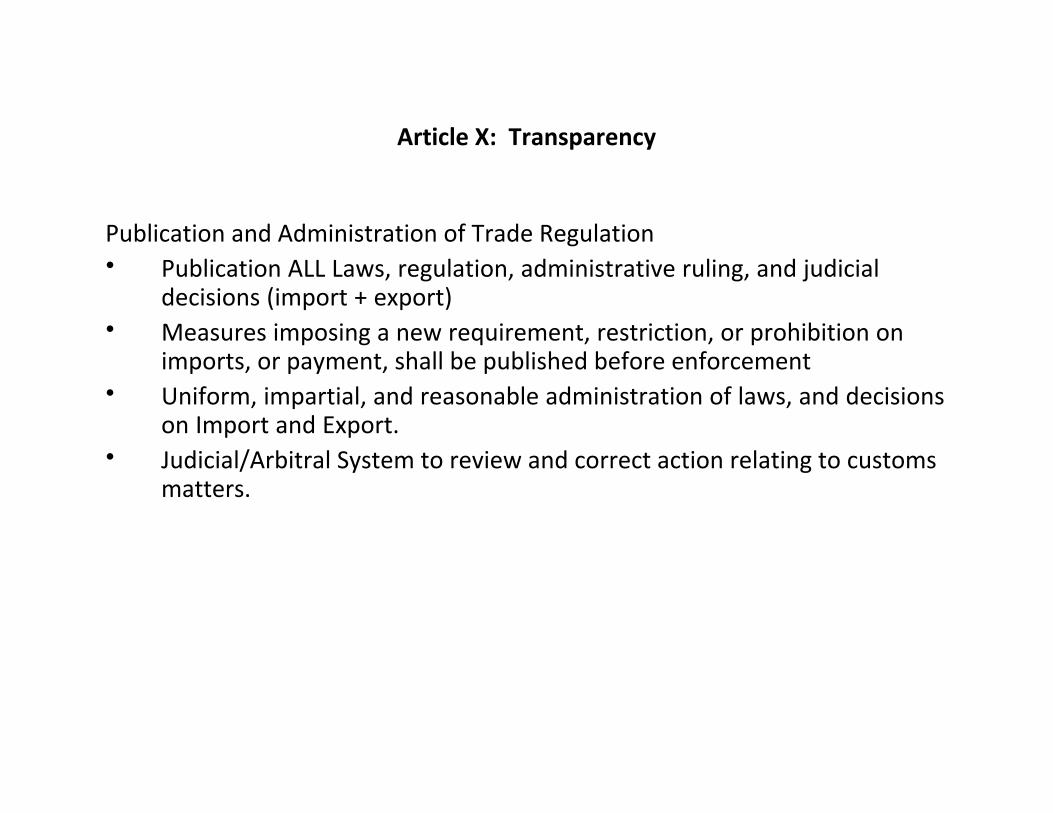

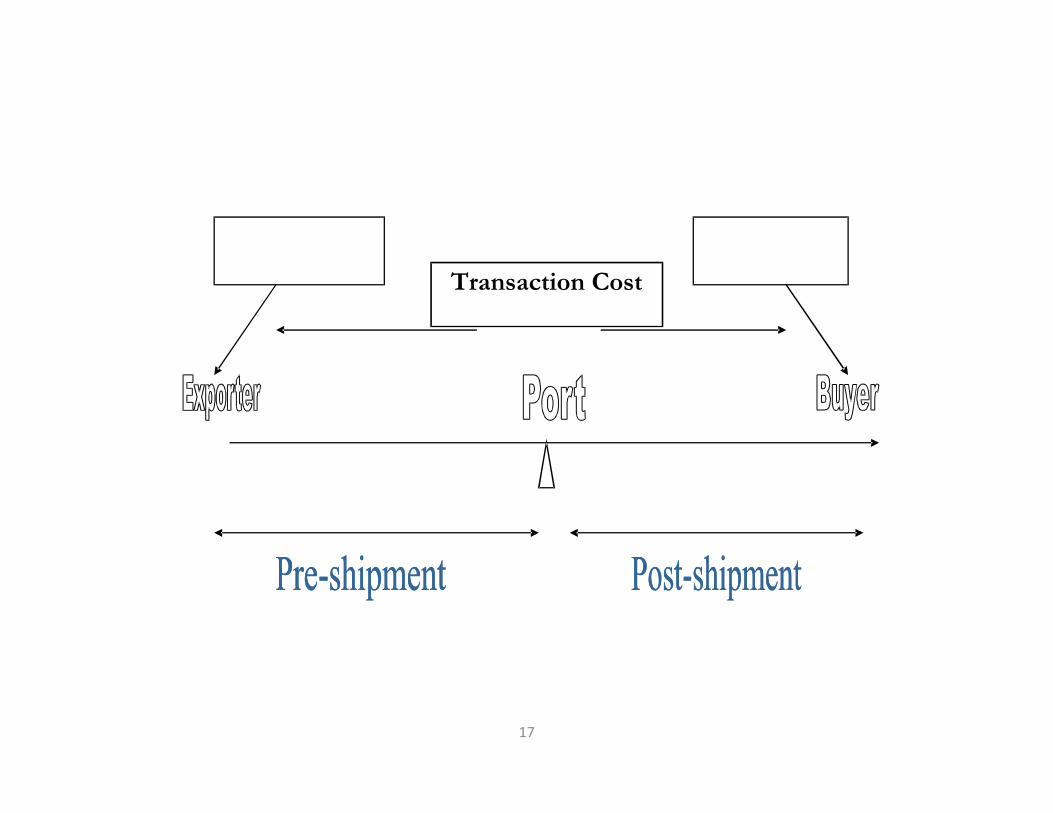

UNDERSTANDING INTERNATIONAL COSTS

• PRODUCT COST

• TRANSACTION COST

• LANDED COST

• TOTAL COST

17

Transaction Cost

Transaction Cost

There are different non-price factors that are not related with physical process ofproduction of goods such as administrative processes, government rules andregulations, infrastructural bottlenecks etc. for which an exporter employs its ownresources either in terms of ‘time’ or in terms of ‘money’ before the actualshipments of export items.

The multiplicity of rules and regulations, rule-bound administrative procedures andpractices, inadequate infrastructural facilities and appropriate institutional supportadversely affect the export promotion efforts. These non-price factors, oftenreferred to as “transaction costs”, impede the impetus given to export growth evenwhen other trade policy issues have been addressedby the Government

Transaction Costs Classifications

i. Information costs – firms and individuals face costs in the search for information about products, prices, inputs and buyers or sellers.

ii. Negotiating costs – arise from the physical act of the transaction, such as negotiating and writing contracts

(costs in terms of managerial expertise,hiring of lawyers, etc), or paying for the services of an intermediary to the transaction such as a broker etc

iii. Monitoring or enforcement costs – arise after an exchange has been

negotiated. This may involve monitoring the quality of goods from a supplieror monitoring the behaviour of a supplier or buyer to ensure that all the preagreed terms of the transaction are met

Transaction Costs - Factors Responsible(a) Complex administrative processes(b) Bureaucratic approach of public agents(c) Procedural delays in clearing imported inputs for exports at the customs(d) Multiplicity of rules and regulations(e) Stringent but inefficient implementation processes(f) Information constraints regarding credit availability and export remittances(g) Infrastructural bottlenecks related to transportation and communication(h) Institutional factors which intensify rent-seeking activities in an economy(i) Political environment as it affects any change in policy stances

While factors (a) and (b) are interdependent due to multiplicity of rules andregulations and hence, multiplicity of paperwork results from theadministrative processes which are not simple and transparent; factor(c) could be explained in terms of factor (e) which, in turn, is partlyattributable to factors (a) and (d) Factors (a), (c), (d) and (e) could beclubbed together as they cause time constraint in export transactions whichhave also been referred to as “procedural delays”. Institutional factors andpolitical environment prevailing in the exportingcountry - enlisted as factors (h) and (i), have a major bearing on all the otherfactors.

An Export transaction process

(i) Obtaining different export-import codes and registrations

(ii) Obtaining different licenses

(iii) Revalidation of export licences

(iv) Issuance of Export House/Trading House certificates

(v) Obtaining various refunds like duty drawbacks etc

(vi) Getting remittances through banks

(vii) Custom clearances

(viii) Final dispatch of export consignments

Applicable Acts , Manuals

Foreign Trade (Development & Regulation) Act 2010

Foreign Trade (Regulations) Rules 1993

Foreign Trade Policy 2009-2014

Foreign Exchange Management Act 1999

Customs Act 1962

Customs Tariff Act 1975

Central Excise Act 1944

Central Excise Tariff Act 1985

Conservation of Foreign Exchange and Prevention of Smuggling Activities Act 1974

Marine Insurance Act 1963 Carriage of goods by Sea Act 1925

Carriage by Air Act 1972and many other acts and regulations

World Customs Organisation www.wcoomd.org

Govt. of India Directory of sites www.goidirectory.nic.in

Ministry of Finance www.finmin.nic.in

Directorate General of Foreign Trade www.nic.in/eximpol

General Taxation in India (non-govt.)www.taxindiaonline.com

General Taxation (non-govt) www.indiantaxsolutions.com

Licence, Import/Export policy (non-govt.)www.LicenceIndia.com

General Business Information (non-govt.)www.e-indiabiz.com

Customs Websites of other countrieshttp://www.customs.govt.nz/library/Links+to+Other+Sites/default.htm

Websites

Airports Authority of India www.airportsindia.org.in

Central Excise and Service Tax http://sermon.nic.in

Directorate General of Safeguards http://dgsafeguards.gov.in

Indian Customs and Excise Gateway http://www.icegate.gov.in/

The Customs, Excise and Service Tax Appellate Tribunal Website

www.cestat.gov.in

Central Excise, Ahmedabad-I www.cenexahmedabad.nic.in

Central Excise Bangalore http://centralexcisebangalore.kar.nic.in

Customs Commissionerate -Ahmedabad

http://ahmedabadcustoms.gov.in

Electronic Data Interchange (EDI) For Trade (eTrade)

CATALYST FOR INTERNATIONAL TRADE AND ECONOMIC GROWTH

Understanding EDI and Internet based ecommerce

SME leveraging technology for growth in international Trade

Introduction

• Introduction of Aligned Documentation System according to UN Lay out Key – 1988

• Development of Software for Pre-shipment Export Documents – 1990

• Acceptance of UN etrade Docs

• National standards for EDI –EDIfact – 1996

• Rolling out of GS1 (Bar coading) -1995

• e-governance was initially drawn on June 2000 with a primary emphasis on networking government departments and developing in-house government applications

• During 2003-2007 government of India approved National e-Governance Plan (NeGP) for implementation with 27 Mission Mode Projects (MMPs).This project would create efficient ,transparent , secure electronic delivery of services by trade regulatory /facilitating agencies,simply procedures and reduce the transaction cost and time ,Introduce UN/CEFACT standards and practices

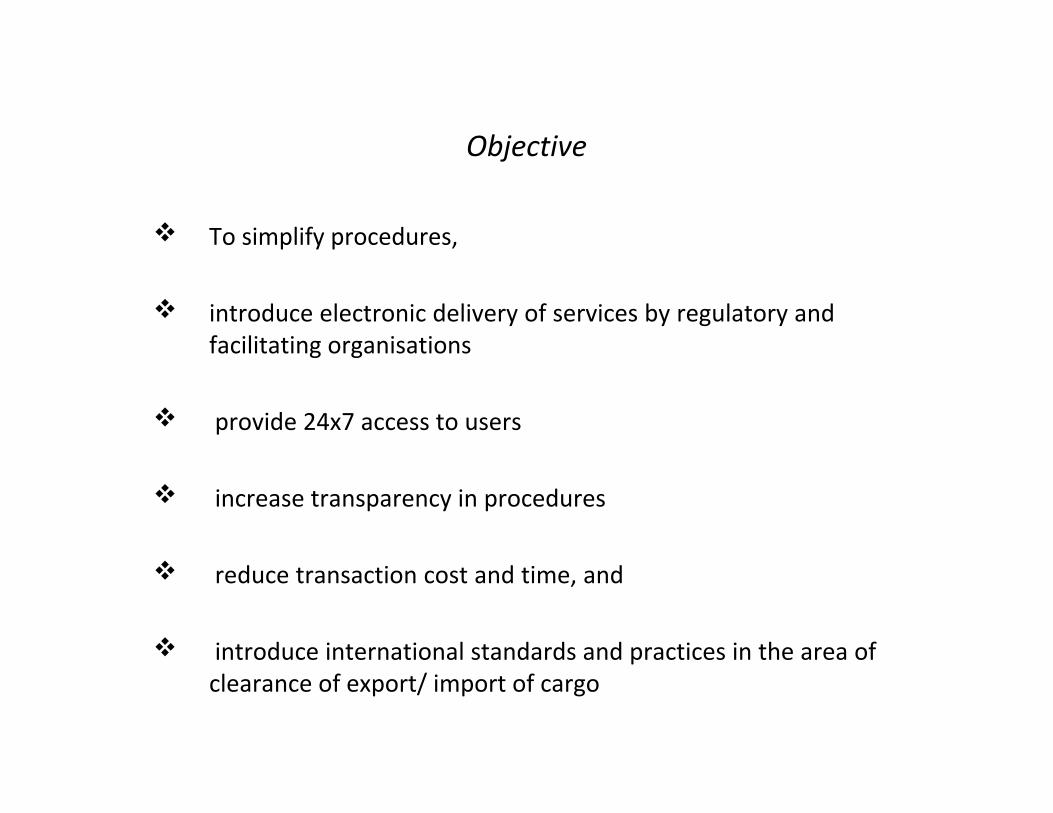

Objective

To simplify procedures,

introduce electronic delivery of services by regulatory and facilitating organisations

provide 24x7 access to users

increase transparency in procedures

reduce transaction cost and time, and

introduce international standards and practices in the area of clearance of export/ import of cargo

e-Trade Coverage to increase Export Competitiveness

• Airports • Airlines• Apparel/Textile export Promotion Councils• Banks and RBI• Customs• Container Corporation of India (CONCOR)• Directorate General of Foreign Trade (DGFT) • Export Promotion Organisations, DG Commercial

Intelligence/Statistics and Inland Container Depots/ Container Freight Stations

• Indian Railways• Port Trusts

Services available

• Electronic filing and clearance of export import documents

• e-Payment of custom duties and charges of ports, airports, CONCOR, etc.

• Filing and processing of licences for DGFT

• e-Payment of licence fee for DGFT

• Electronic exchange of documents between community partners such as Customs, ports, airports, DGFT, CONCOR, Banks, etc.

CUSTOMS EDI

• Customs rolled out ICES 1.5 at 119 locations• RMS is operational by Customs at 96 locations • Operationalisation of Customs message exchange with 13 major + 4 private

seaports is through PCS , message xchange system in place with airports , Concor , Banks

• Implementation of design and development of challan management application and testing tp operatinalize ePAO

• IBA would ensure that all concerned banks start ePayments for Customs duties .

• Customs reported that a circular has been issued to make the ePayment mandatory for all accredited clients and payments above Rs. 1 lakh at locations wherever ePayment is operational. ePayment is made mandatory from 01.10.2011.

CONCOR

• All their EXIM locations have uniform internal automation and connected through a centralised system.

• CONCOR rolled out the web based user interface system at certain EXIM locations

• CONCOR is also connected with Indian Railways for online rail receipts generation.(FOIS)

• The electronic message interface with Customs has been started for 5 messages

• On the subject of making the system mandatory CONCOR views are that the same should be done for all ICDs/CFSs

• Container tracking and tracing system is provided

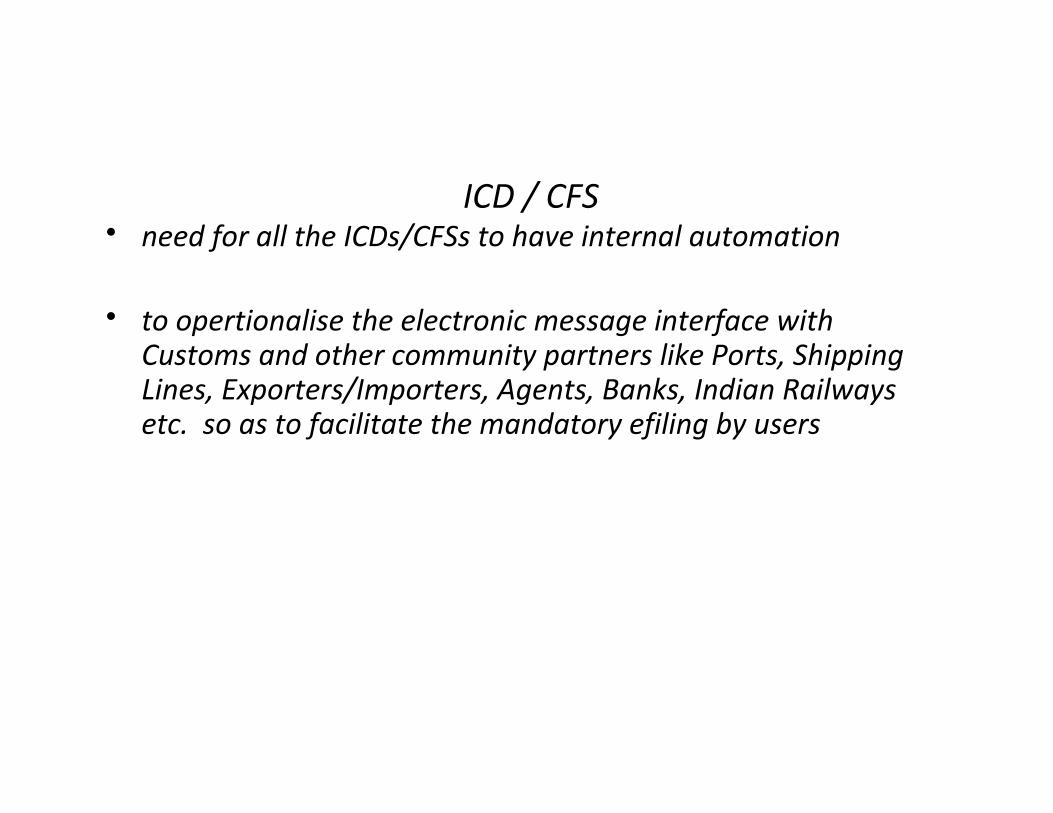

ICD / CFS • need for all the ICDs/CFSs to have internal automation

• to opertionalise the electronic message interface with Customs and other community partners like Ports, Shipping Lines, Exporters/Importers, Agents, Banks, Indian Railways etc. so as to facilitate the mandatory efiling by users

Ports , Banks

• Web based system for all major ports for document submission with trade partners, payment acceptance

• Integration of non-major seaports into PCS by IPA• RTGS,NEFT implementation by Banks

• Disbursal of export incentives thru Banks

• Banks given interface with all trading partners for acceptance of on line payments and issuance of receipts

DGFT

• DGFT to opretaionalise the eBRC system

• Issues on Customs – DGFT interface for Ch.3 schemes to be resolved

• Physical dispensation of paper and digital signature integration in Customs

• Issuance of all licenses • Digital signature integration with institutional partner like

CONCOR, IPA, Airports Custodians, Banks

Airports

• Ministry of Civil Aviation and AAI is ensuring the web based community partner interface system and bar code integration at major airports.

• AAI has floated the RFP for the Airports community system (ACS)

• MoCA/AAI to ensure that custodians at smaller locations to be ready for message exchange with Customs

• For Tracking and Tracing system ,RFID ,Bar Coding

Challenges

• Dispensation of physical submission of documents

• Coverage to include upcoming/smaller locations

• etrade to be effective for all transactions like GSP etc

Registration

(IEC)

Licensing

( EXIM )

Bank Guarantee

Sourcing of Raw Material Warehousing

Excise Clearances

Custodian ( Concor / AAI )

Custom Clearance

Loading ogGoods on Aircraft

/ Vessel

EGM/Mate receipts /Are 1

Airway Bill /Bill Of Lading

Bank Documents,Expor

t Incentive ,Insurance Documents

Export Cycle

Airports Ports

ICD

• AAI , DIAL • CONCOR , CWC

DGFT

EPC

ECGC

• Customs

• Excise

Banks

Insurance Companiy

• Airlines,• Shipping lines

Exporter ,Importer

Role of Intermediaries

EXPORTS Regulations for Samples , Spares , Gifts ,Repaired goods , Consignment Export

REGISTRATION OF EXPORTER , IMPORTERS

To export or import in India, IEC Code is mandatory

An application for grant of IEC number from Regional Authority of

Directorate General Foreign Trade.

IEC Code Online Application Form

Application Fee

Profile of Exporter , Importer

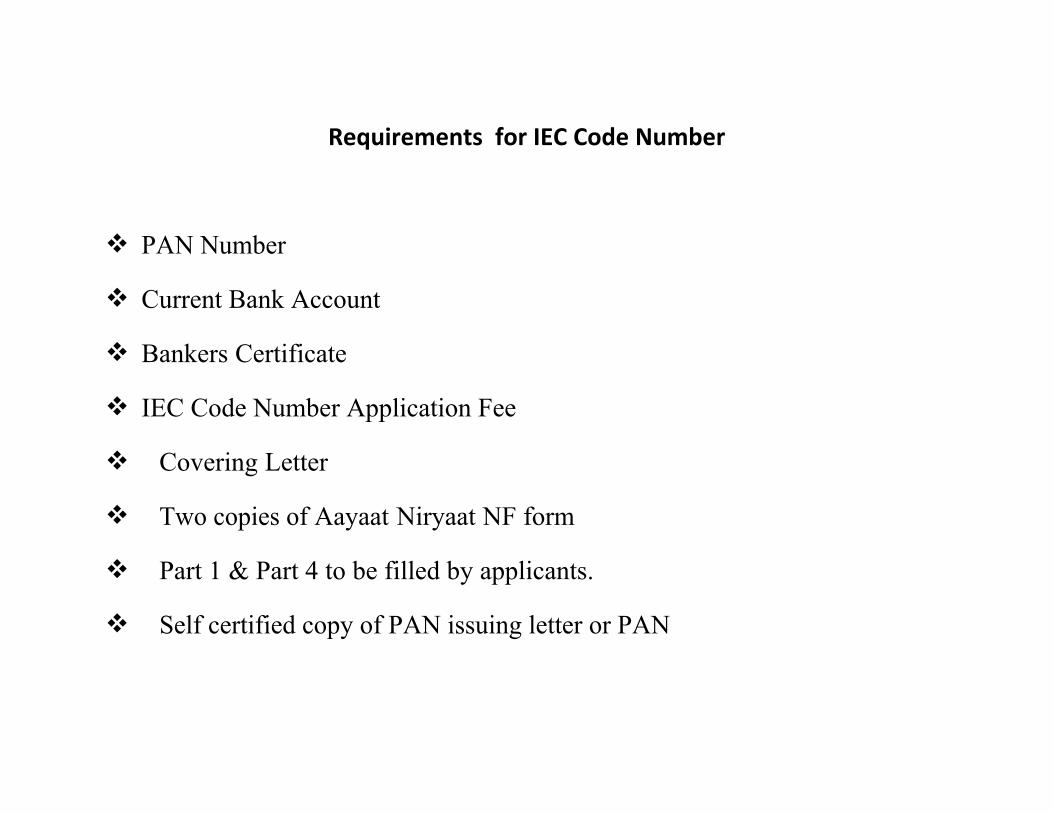

Requirements for IEC Code Number

PAN Number

Current Bank Account

Bankers Certificate

IEC Code Number Application Fee

Covering Letter

Two copies of Aayaat Niryaat NF form

Part 1 & Part 4 to be filled by applicants.

Self certified copy of PAN issuing letter or PAN

Obtain RCMC from the specific Export Promotion Council Registration with Customs Understand applicable export ,Import Schemes along with the HSN

Confirmation from EPC , Freight Forwarder etc Apply for Excise registration ( if applicable ) Apply for VAT ,CST ( If applicable ) Understand components of Sales Contract , Delivery Terms (INCOTERMS) EXIM Documentation Export Incentives or Import Duties on the products Exported or Imported Freight Rates Packaging Gudielines

• Exports regulations under FEMA, 1999

RBI Master circular for exports and services

• Memorandum on Project & Sevices Exports (PEM)

Categories of exports

• Cash Exports

• Deferred Payment Exports

• Project Exports

• Software Exports

• Services Exports

Agencies connected with Exports

Director General of Foreign Trade

- Formulation of trade policy; allotment of importer-exporter code number

Customs

- Valuation of goods, physical aspects of exports

Reserve Bank of India & Authorised Dealers

- Monitoring receipts of payments & follow up

Institutions involved

RESERVE BANK OF INDIA

EXIM BANK

ECGC

AUTHORISED DEALERS

Working Group Members

EXIM Bank

ECGC

Reserve Bank of India (ECD & IECD)

Authorised Dealer & Exporter invited as special invitees

Declaration of Exports

Mandatory to declare the export of goods & Services outside India (except Nepal & Bhutan) by exporter to the specified authority in the prescribed forms (Regulation 3)

- Full value of goods or software- Where value not ascertainable – the value expected to be realized given

the market conditionsExport of services – no form prescribed – however liable to repatriate the

exchange so earned

Exemptions from Declaration

Trade samples, publicity material supplied free, personal effects of travellers (accompanied/unaccompanied)

Ship’s stores, transshipment cargo, Military/Naval/Air Force requirements, Aircraft Engine Spares Goods/Software of value less than US.$.25000/- - declaration from exporterGifts for value upto Rs.5.00 lakh – declaration

Exemptions from Declaration-Contd

Goods imported free of cost on re-export basisGoods exported upto $ 1000 to Myanmar under Barter Trade AgreementReplacement of goods free of charge as per EXIM PolicyFrom EPZ/FTZ after permission of Development Commissioner- Imported goods found defective for replacement - Goods imported from suppliers/collaborators on loan basis- Goods imported from suppliers/collaborators free of

cost - found excess after production operations

Payment of Export Value of Goods

Notification No.FEMA 14/2000-RB-Manner of Receipt & Payment RegulationsFor all ACU Countries except Nepal – through ACU Dollar AccountIn case of export of goods to Nepal, where an importer resident in Nepal has

been permitted by the Nepal Rashtra Bank to make payment in free foreign exchange, such payments shall be routed through the ACU mechanism.

For the rest of the world – by debit to the Rupee Account of a bank situated in countries other than the ACU countries or in any permitted currency

For export to Myanmar – in any freely convertible currency or through ACU mechanism

Receipt of Payment

In the form of bank draft, pay order, foreign currency notes, travellers cheques from buyer during visit to India – surrender as per time limit

Debit to NRE/FCNR Accounts of the buyerIn Rupees from credit card servicing bank against charge slip signed by buyer

using a credit cardIn accordance with directions of RBI for arrangements between

Governments/Exim BankIn the form of precious metals equivalent to the value of jewellery exported

by Gems & Jewellery units in SEZRupee account of Exchange Houses - up to Rs. 2lakhs per transaction

Export Procedure

Declaration in Form GR/SDF to be submitted in duplicate to Customs along with shipping bills

SOFTEX Forms in the triplicate to STPI/FTZ/EPZCustoms Number the form – certify value of goods & assessable value/if

SOFTEX, official of STPI/FTZ/EPZ will certifyReturn duplicate to exporter – original sent to RBI directlyGR form resubmitted to Customs along with goods to be shippedCustoms certify quantity & return form to exporter

Export Procedure

Exporter submits duplicate GR to AD within 21 days of shipment with invoice, shipping documents etc.

AD negotiates/sends for collection – report to RBI in form ENC with R-ReturnGR form endorsed for amounts credited to EEFC accountADs no longer required to submit the duplicate export declaration form & EC

copy of shipping bill to RBI after realisation of export proceeds

SOFTEX Form Procedure

• Form to be submitted in triplicate to STPI/FTZ/EPZ• Designated officials of Ministry of Information Technology, GOI at the Software

Technology Parks of India (STPIs) or at Free Trade Zones (FTZs) or Export Processing Zones (EPZs) or Special Economic Zones (SEZs) have been authorised to certify exports declared on SOFTEX forms

• Designated officials of STPIs/EPZs/SEZs also authorised to certify the Softex Form

SOFTEX Form Procedure

• Original Sent Directly to RBI by Certifying Agency• Duplicate Retuned to Exporter• Triplicate Retained by STPI/FTZ/EPZ• Duplicate form to be submitted to AD within 21 days of certification• Billing to be done for long term contracts on reaching "milestones" or once a

month – for others within 15 days of completion and for certification by the authorities in the STP

Despatch of documents

Documents to be despatched as soon as possible to overseas branches/correspondents

Documents may be sent directly to consignee where L/C or advance remittance received

Can also be done for customers with good track record

Despatch of Documents

Exporters who are “Status Holder Exporters” can despatch documents directly to consignees, subject to:

the export proceeds are repatriated through the authorised dealer named in the GR form

The duplicate copy of the GR Form is submitted to the authorised dealer for monitoring purposes by the exporters within 21 days from the date of shipment of export

PP Form Procedure

• Original PP form to be countersigned by AD– AD to countersign when parcel addressed to their branch or correspondent in

the country of import– Can be sent directly to consignee if export against LC or advance payment has

been received or the AD is satisfied based on the track record of the exporter

Direct Despatch of Documents

Authorised Dealers may permit units in Special Economic Zones (SEZs) to despatch export documents direct to the consignees outside India subject to:

the export proceeds are repatriated through the Authorised Dealer named in the GR/SDF/PP/SOFTEX Form

the duplicate copy of the respective declaration form is submitted to the Authorised Dealer for monitoring purposes by the exporters within 21 days from the date of shipment

Remittances Connected With Exports

• Export claims ADs allowed to remit– Export proceeds should have been realised & repatriated to India– Exporter is not on caution list of RBI– Exporter to be advised to surrender proportionate export incentive, if any

received by him

Consignment Exports

Documents sent at the risk of the exporterDocuments sent to correspondent to be delivered to consignee against trust

receiptRepatriations within time limit for exportsAgent allowed to deduct expenses incurred with the saleAccount sales to be received along with remittance

Consignment Exports

Freight & insurance to be arranged in India

Realisation period 15 months for exporters having warehouses abroad with prior RBI approval

Exports to East European Countries – period upto 12 months allowed by RBI to exporters with good track record

Special Facilities for Units in SEZs

Payment of export may also be received by the gem & jewellery units in SEZs and EOUs in form of precious metals i.e. gold/silver/platinum equivalent to value of jewellery exported on the condition that the sale contract provides for the same and the approximate value of the precious metal is indicated in the relevant GR/SDF/PP forms

What are Project Exports

Export of engineering goods on deferred payment terms

Execution of turnkey projects/civil construction contracts abroad

Export of services

Transportation-relatedConcepts and Terminology

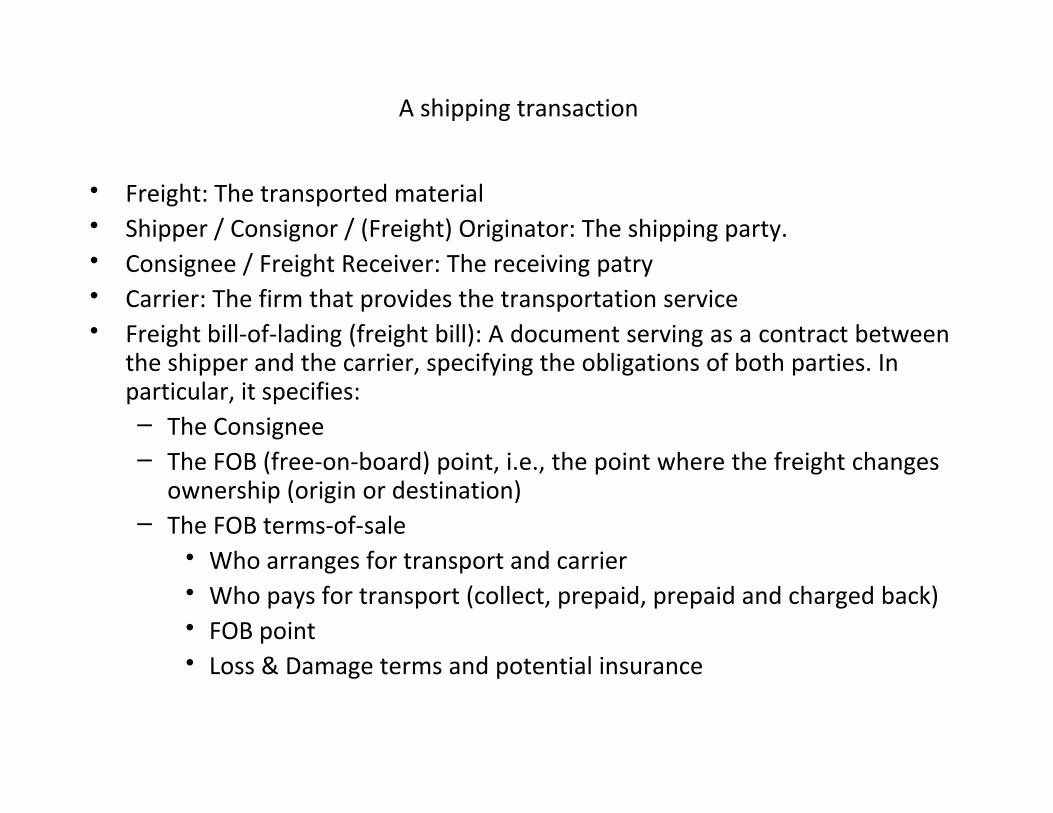

A shipping transaction

• Freight: The transported material• Shipper / Consignor / (Freight) Originator: The shipping party.• Consignee / Freight Receiver: The receiving patry• Carrier: The firm that provides the transportation service• Freight bill-of-lading (freight bill): A document serving as a contract between

the shipper and the carrier, specifying the obligations of both parties. In particular, it specifies:– The Consignee– The FOB (free-on-board) point, i.e., the point where the freight changes

ownership (origin or destination)– The FOB terms-of-sale

• Who arranges for transport and carrier• Who pays for transport (collect, prepaid, prepaid and charged back)• FOB point• Loss & Damage terms and potential insurance

Information for Obtaining Export Rate

1. What you are shipping

2. Where it is going

3. How much it weights

4. The dimensions

5. The value

6. The type of service (air, ocean, ground)

7. Any special requirements

Mediators and Integrators

• Freight forwarder: An agency that receives freight from the shipper and then arranges for transportation with one or more carriers for transport to the consignee. Typically, consolidates freight from many shippers to obtain better rates. Also, often provde pickup and delivery services, as well as other shipping services: packaging, temporary storage, customs clearing.

• Transportation Broker: An agency that obtains negotiated large-volume transportation rates from carriers and resells this capacity to shippers. No additional services are provided, though.

• NVOCC (Nonvessel-operating common carrier): Owns no vessels, but provides ocean shipping freight-forwarding services.

• Shipper’s Association: Not-for-profit association of shippers using collective bargaining and freight consolidation to obtain lower, high-volume transportation rates. Avoids premium charge paid to forwarders. Only non-competitive shippers may associate, due to monopoly restrictions.

• Integrators: Companies providing door-to-door domestic and international air-freight service. Owns and operate aircraft as well as ground delivery fleet of trucks

• 3PL: A third-party, or contract, logistics company, used to outsource logistics services. It can also handle: Purchasing, Inventory management/warehousing, transportation and order management

Charging Patterns for Common Carriers

• Related to shipment size– LTL and LCL shipments: minimum total rate for quantities below a

minimum threshold, then several weight categories with different rates.– Time-volume rates: encourages shippers to send minimum quantities

regularly, in an effort by carriers to ensure regular flow of business• Related to distance

– Uniform rates: independent of distance – Blanket rates: constant rates for certain intervals of distance rates, bulk

cargo).

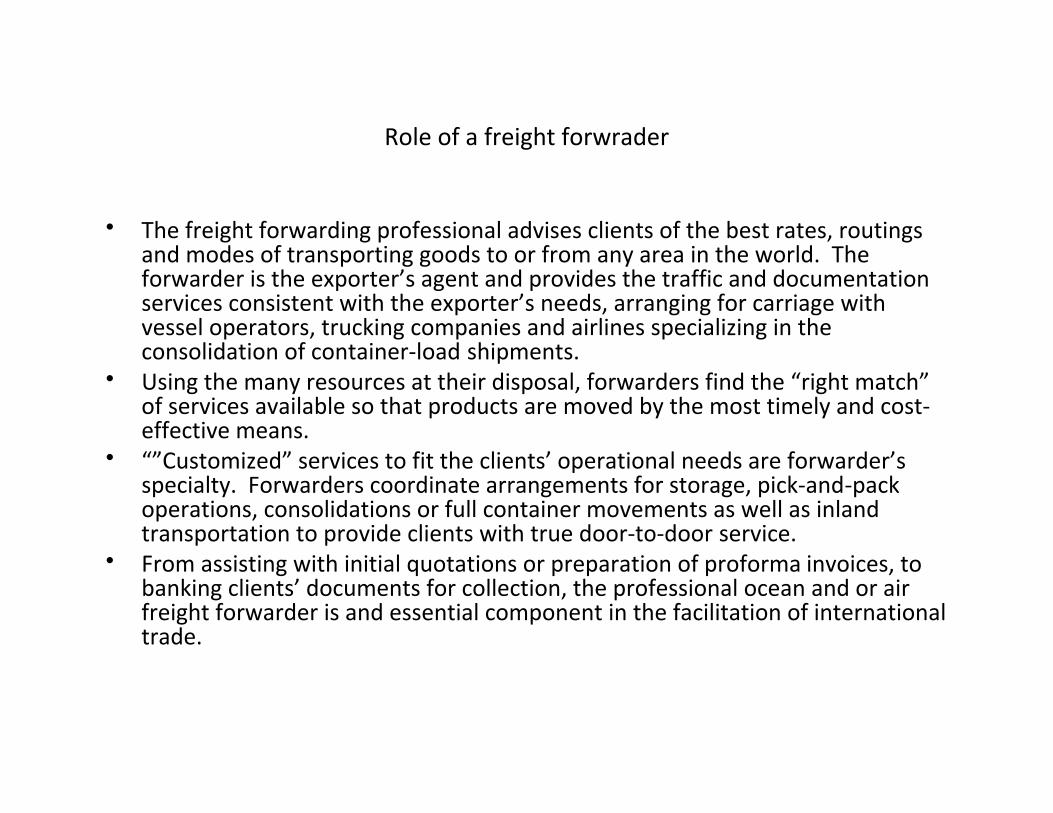

Role of a freight forwrader

• The freight forwarding professional advises clients of the best rates, routings and modes of transporting goods to or from any area in the world. The forwarder is the exporter’s agent and provides the traffic and documentation services consistent with the exporter’s needs, arranging for carriage with vessel operators, trucking companies and airlines specializing in the consolidation of container-load shipments.

• Using the many resources at their disposal, forwarders find the “right match” of services available so that products are moved by the most timely and cost-effective means.

• “”Customized” services to fit the clients’ operational needs are forwarder’s specialty. Forwarders coordinate arrangements for storage, pick-and-pack operations, consolidations or full container movements as well as inland transportation to provide clients with true door-to-door service.

• From assisting with initial quotations or preparation of proforma invoices, to banking clients’ documents for collection, the professional ocean and or air freight forwarder is and essential component in the facilitation of international trade.

73

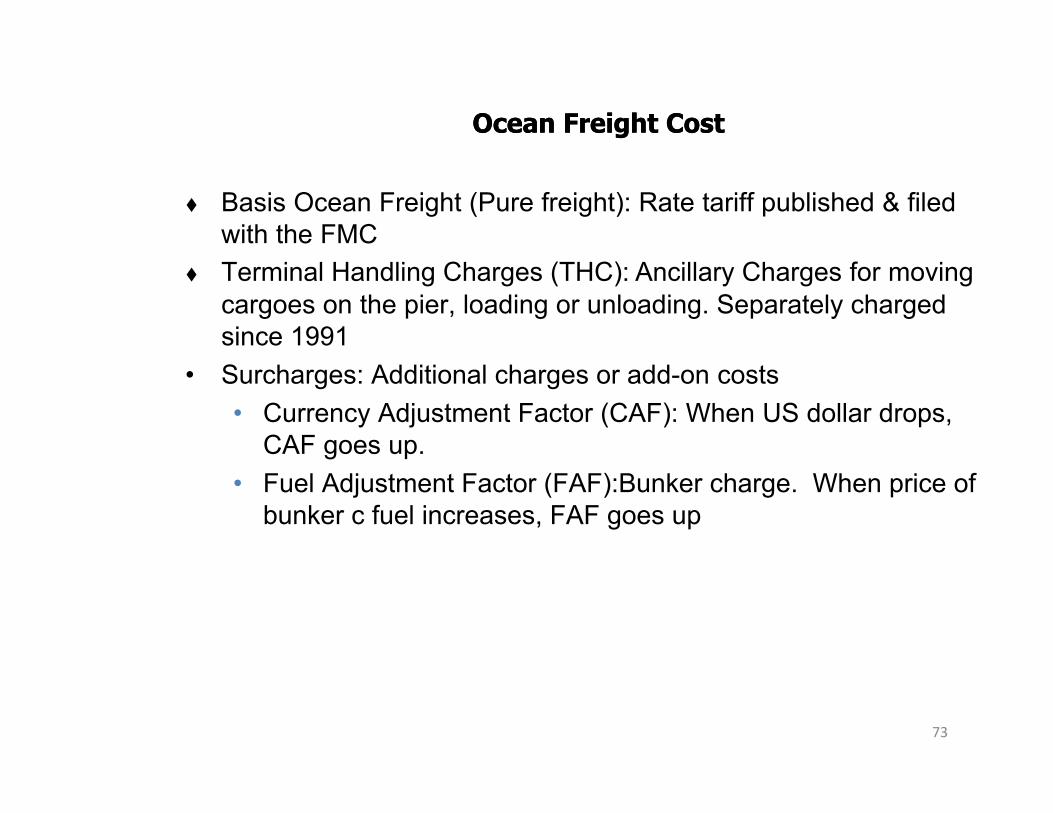

Ocean Freight CostOcean Freight Cost

Basis Ocean Freight (Pure freight): Rate tariff published & filed with the FMC

Terminal Handling Charges (THC): Ancillary Charges for moving cargoes on the pier, loading or unloading. Separately charged since 1991

• Surcharges: Additional charges or add-on costs • Currency Adjustment Factor (CAF): When US dollar drops,

CAF goes up. • Fuel Adjustment Factor (FAF):Bunker charge. When price of

bunker c fuel increases, FAF goes up

74

Ocean Bill of LadingOcean Bill of Lading

Negotiable Bill of Lading: Order Bill of Lading

• Made out "To order" or To the order of ----."

• Cargoes are released only on presentation of an original bill of lading duly endorsed by the shipper or consignee named in the bill of lading

• Non-Negotiable Bill of Lading: Straight B/L

• Consigned to the importer. Cargoes are released only to the consignee. Endorsement not needed

75

NonNon--Negotiable Sea WaybillNegotiable Sea Waybill

• Cargoes are released only to the consignee on the Sea Waybill without surrendering an original Sea Waybill.

• Often used When consignee, or importer does not need to sell the goods

during transit Specially convenient in the case of a very short transit time.

• Processing shipping documents through exporter’s bank and importer’s bank take several days

76

Multimodal Transport DocumentMultimodal Transport Document

Multimodal (Through, Combined or Intermodal) Bill of Lading

Covers two or more transportation modes: truck or rail – vessel-truck or rail

Covers all transportation from the place dispatched, taken in charge or shipped on board to the place of final destination

How to compute the size of your shipment

• In order to compute actual cubic feet, you will need to measure the length, width and height (in inches) of each piece to be shipped.

• One cubic foot is equal to a single piece with the dimensions of 12" x 12" x 12".

• To compute cubic feet, first multiply together all the dimensions for the piece being measured.

• Then divide the total by 1728.

• This calculation will give you your total amount of cubic feet for the piece.

• Total the individual pieces "cubed" to determine your total shipment cube.

•12" X 12" X 12" = 1728

•1728 / 1728 = 1 cubic foot or 12" X 12" X 12" = 1 cubic foot

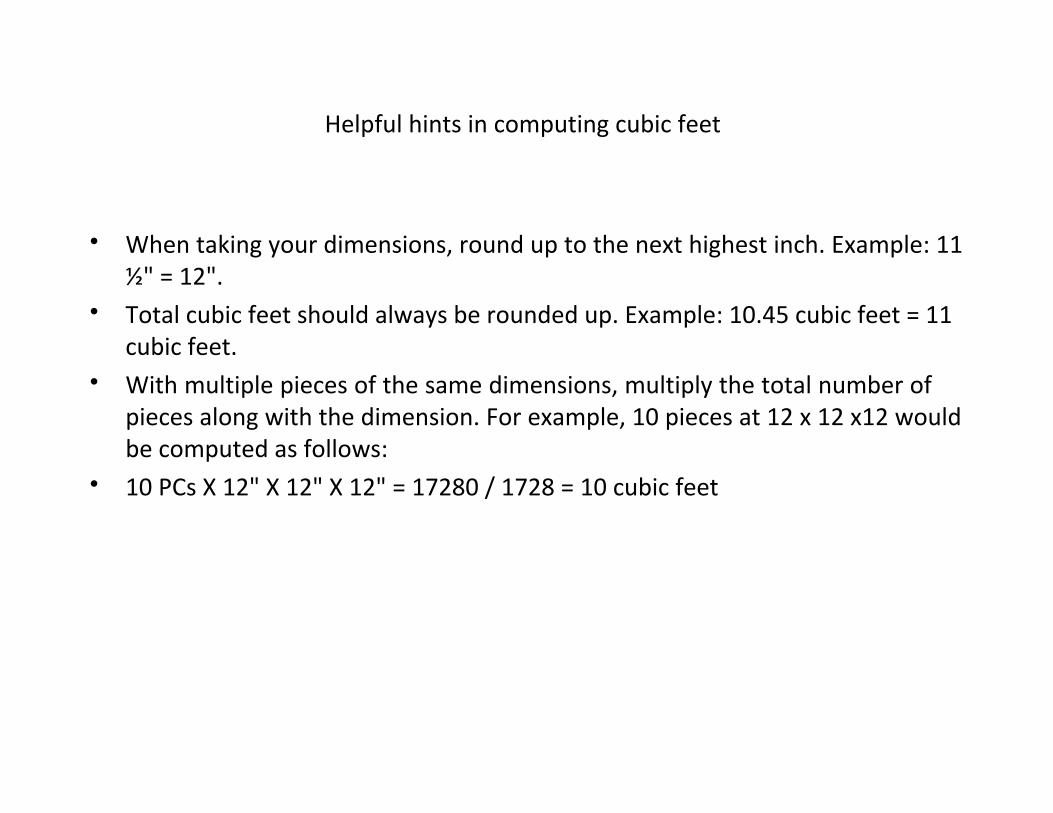

Helpful hints in computing cubic feet

• When taking your dimensions, round up to the next highest inch. Example: 11 ½" = 12".

• Total cubic feet should always be rounded up. Example: 10.45 cubic feet = 11 cubic feet.

• With multiple pieces of the same dimensions, multiply the total number of pieces along with the dimension. For example, 10 pieces at 12 x 12 x12 would be computed as follows:

• 10 PCs X 12" X 12" X 12" = 17280 / 1728 = 10 cubic feet

Moving Goods by Air

AIRFREIGHT RATES• Basic cost of Airfreight

– Charged per Kilogram (kg) Weight or Volume, whichever is greater, known as Chargeable Wt (dimensional weight)

– Rates apply for movements from the airport of origin to the airport of destination. Pre-departure and post-arrival expenses are additional to the airfreight cost

– Other additional expenses

AIRFREIGHT

DOCUMENTATION• Air Waybills

– Provides evidence of a contract of carriage between exporter and forwarder/carrier

– Proof of receipt of goods for shipment

– Unlike the ocean Bill of Lading, the AWB isn’t, when in your possession, a title to the goods

International trade contracts and Incoterms

Different countries have different business cultures and even languages. It's a good idea to make sure you have a clear written contract to minimise the risk of misunderstandings.

The contract should set out where the goods are being delivered. It should cover who is responsible for every stage of the journey, including customs clearance, and what insurance is required. It should also make it clear who pays for each different cost.To avoid confusion, internationally agreed Incoterms should be used to spell out exactly what delivery terms are being agreed, such as:

•where the goods will be delivered•who arranges transport•who is responsible for insuring the goods, and who pays for insurance•who handles customs procedures, and who pays any duties and taxesFor example, an exporter might agree to deliver goods, at the exporter's expense, to a port in the customer's country. The customer might then take over responsibility, arranging and paying for customs clearance and delivery to their premises. The exporter might also be responsible for arranging insurance for the goods until they reach the port, but pass this cost on to the customer. As well as including delivery details, the contract should cover payment. This should include what currency payment will be made in, how much will be paid, when payment is due and what payment method will be used. See the page in this guide on international trade documentation and payments.Trade in servicesWith no physical delivery of the product, contracts in services cannot use Incoterms. Instead, the key issue tends to be defining exactly what services are being provided and to what standards.

International Commercial Contracts - Incoterms

Incoterms are standard trade terms that set out buyer and seller responsibilities. They aim to avoid misunderstanding and are principally used in agreements about the delivery of goods. Each Incoterm outlines who is responsible for transport, insurance, duties and clearance. Before you use Incoterms, consider the country of the buyer. Some countries stipulate that set Incoterms are used, while others set chosen Incoterms as standard practice. Transport may also affect your choice as some Incoterms can only be used for transport by sea and inland waterways.

•Incoterms

•The International Chamber of Commerce (ICC) originally published the very first set of Incoterms in 1936. Since that first publication, they have been updated in 1953, 1967, 1980, 1990,2000 and most recently in 2010.

•Because Incoterms are standard definitions, they are used in contracts to reduce confusion and avoid traders having difficulty understanding the import requirements and shipping practice used in other countries.

•Using the correct Incoterms clarifies the contracts you have with your suppliers or customers. "Incoterms" is an ICC trademark and only the original texts of Incoterms are to be considered as authoritative for incorporation into contracts. You should use the current version and note this in the contract. These terms should also be used on any paperwork linked to the contract, such as invoices or statements. Failing to state that you are using Incoterms 2010 could result in a dispute.

Delivery terms – INCOTERMS 2010

1. E group: EXW (Ex-works)

2. F group: FCA (Free carrier), FAS (Free alongside ship), FOB (Free on board)

transfer of costs and risk

seller buyer

transfer of costs and risk

seller buyer

Delivery terms – INCOTERMS 20103. C group: CFR (Cost and freight), CIF (Cost, insurance, and freight),

CPT (Carriage paid to), CIP (Carriage and insurance paid to)

4. D group: DAT (Delivered at terminal), DAP (Delivered at place), DDP (Delivered duty paid)

transfer of costs

transfer of risk

seller buyer

transfer of costs and risk

seller buyer

Most Common Incoterms

Term Definition Risk Cost Include on Quotation

EXW Ex Works

Buyer arranges for pick up of goods at the seller’s location. Seller is responsible for packing, labeling, and preparing the goods for shipment on a specified date or time

Buyer assumes all risk

Buyer pays all transportation costs

N/A

FCA Free Carrier

Seller is responsible for costs until the buyer’s named freight carrier takes charge

Seller and Buyer

Split N/A

FAS Free Alongside Ship (over water only)

Buyer arranges for the ocean transport. Seller is responsible for packing labeling, preparing the goods for shipment, and delivering the goods to the dock.

Seller: until the goods reach the dock. Buyer: from dock to destination

Buyer: all ocean transport costs. Seller is responsible for costs associated with transporting the goods to the dock.

Costs of transporting goods to the dock.

Most Common Incoterms

Term Definition Risk Cost Include on Quotation

FOB* Free On Board FOB should also never be used unless you specify what and where such as "FOB ocean vessel at New York City

Seller arranges for ocean transport of the goods, preparing the goods for shipment, and loading the goods onto the vessel. The goods ship ocean freight collect.

Buyer: Once the items are on board

Seller: Wharfage (charges to load the goods onto the ship) and freight forwarder fees.

Costs, until on board

CFR Cost and Freight

Seller has the same responsibilities as when shipping FOB, but shipping costs are prepaid by the seller, instead of shipping collect.

Seller: assumes the risk until the shipment reaches the overseas dock.

Seller: costs of freight fees up to destination.

Add Freight to cost of product.

CIF Cost, Insurance, and Freight

Seller has the same responsibilities as when shipping CFR with addition of including a marine insurance policy

Seller:; until the shipment reaches the overseas dock.

Seller insurance and freight forwarder fees.

Insurance, freight and cost of goods

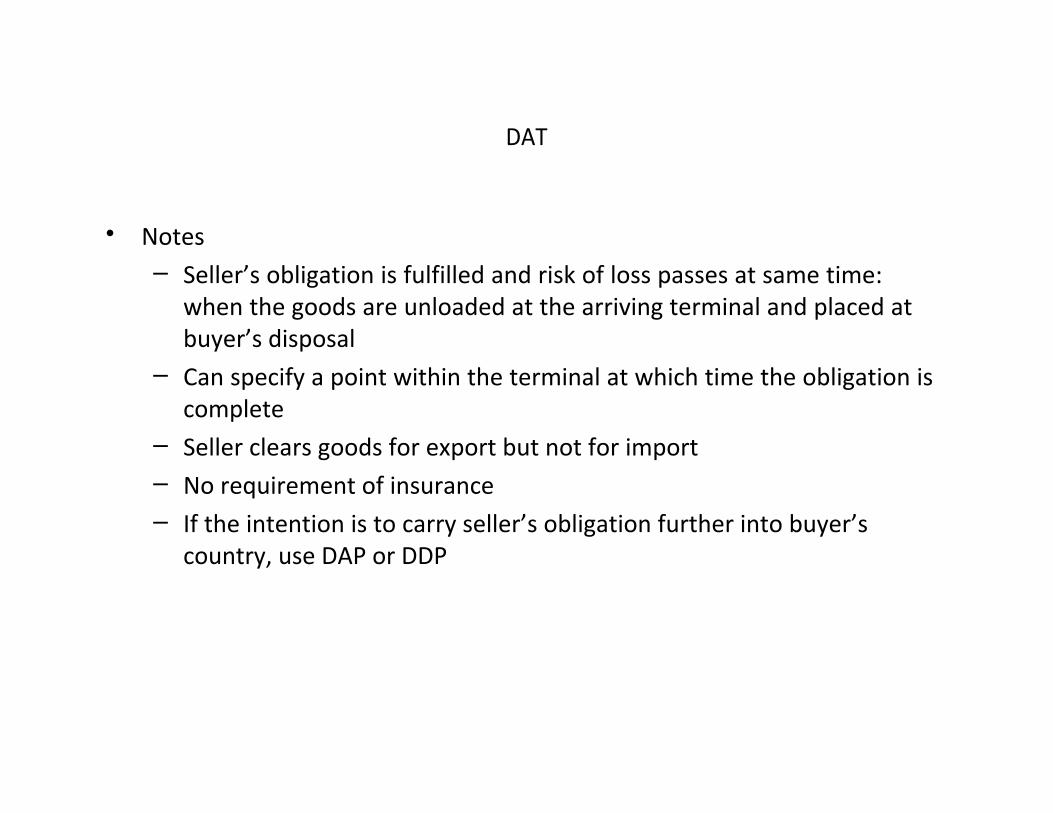

DAT

• Delivered at Terminal – Seller delivers when the goods, once unloaded from the arriving

means of transport, are placed at the disposal of the buyer at a named terminal at the named port or place of destination.

– “Terminal” includes any place, whether covered or not, such as a quay, warehouse, container yard or road, rail or air cargo terminal.

– The seller bears all risks involved in bringing the goods to and unloading them at the terminal at the named port or place of destination.

DAT

• Notes– Seller’s obligation is fulfilled and risk of loss passes at same time:

when the goods are unloaded at the arriving terminal and placed at buyer’s disposal

– Can specify a point within the terminal at which time the obligation is complete

– Seller clears goods for export but not for import– No requirement of insurance– If the intention is to carry seller’s obligation further into buyer’s

country, use DAP or DDP

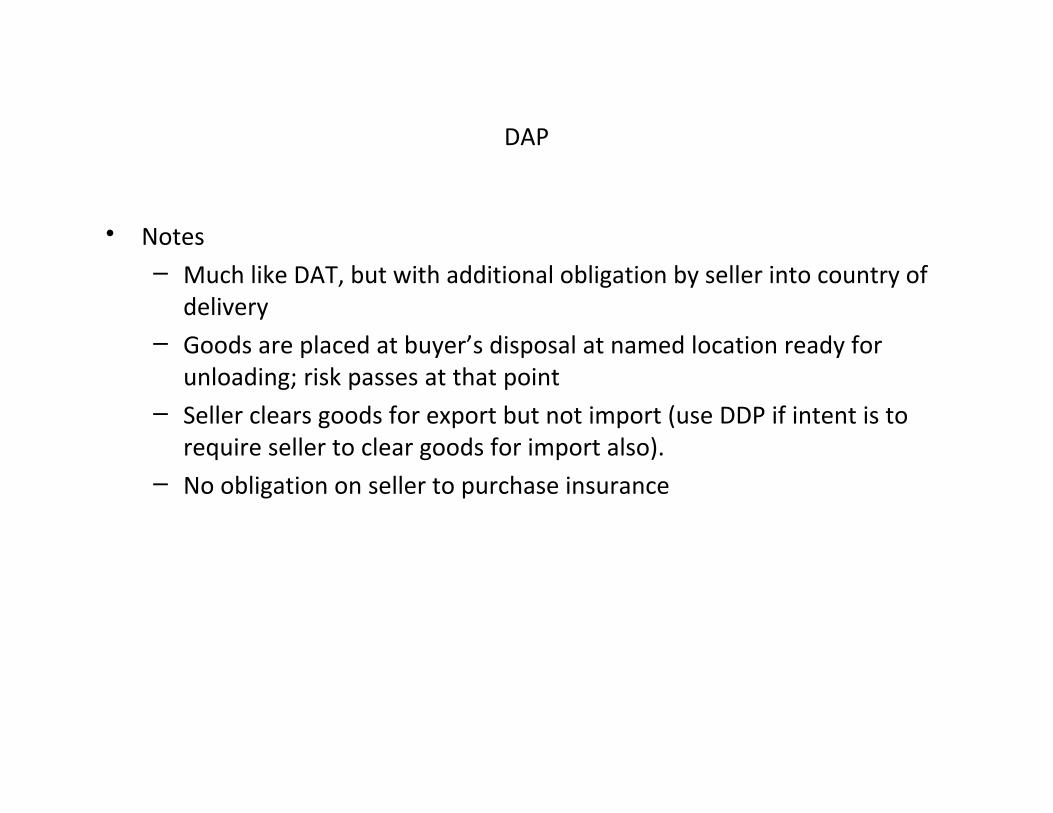

DAP

• Delivered at Place – Seller delivers when the goods are placed at the disposal of the buyer

on the arriving means of transport ready for unloading at the named place of destination.

– The seller bears all risks involved in bringing the good to the named place.

DAP

• Notes– Much like DAT, but with additional obligation by seller into country of

delivery– Goods are placed at buyer’s disposal at named location ready for

unloading; risk passes at that point– Seller clears goods for export but not import (use DDP if intent is to

require seller to clear goods for import also).– No obligation on seller to purchase insurance

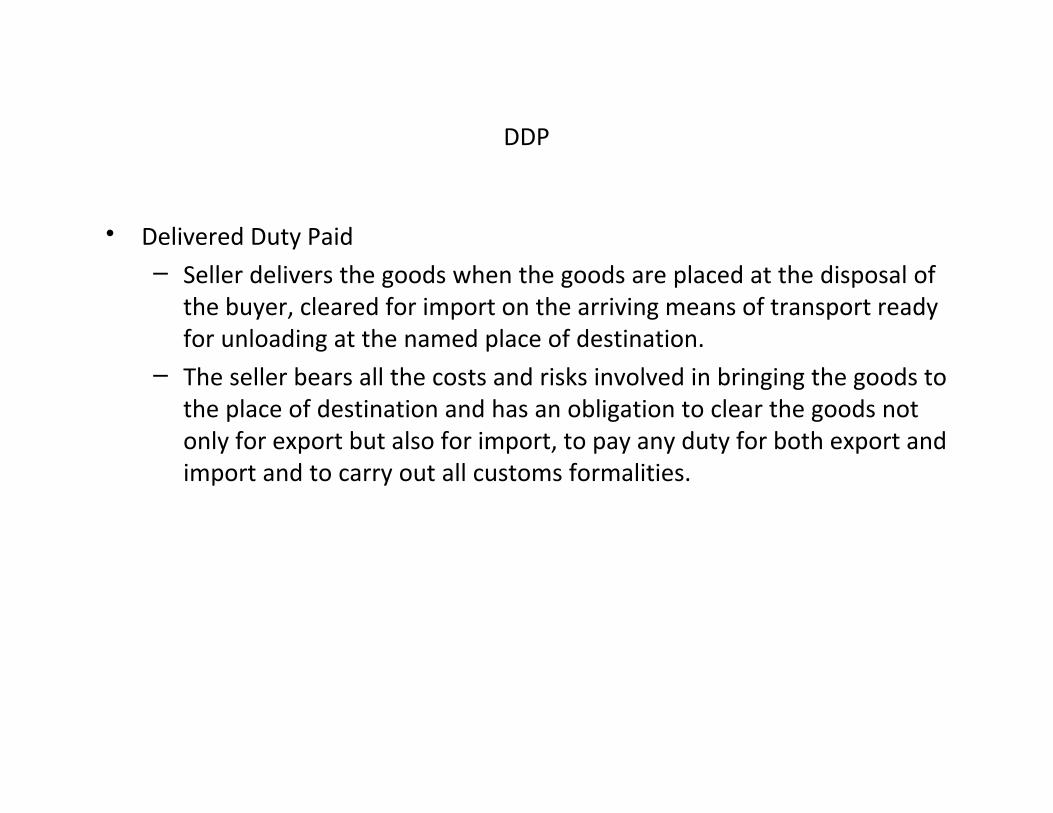

DDP

• Delivered Duty Paid – Seller delivers the goods when the goods are placed at the disposal of

the buyer, cleared for import on the arriving means of transport ready for unloading at the named place of destination.

– The seller bears all the costs and risks involved in bringing the goods to the place of destination and has an obligation to clear the goods not only for export but also for import, to pay any duty for both export and import and to carry out all customs formalities.

DDP

• Notes– Like DAP, but including seller’s obligation to clear goods for import—

pay for any necessary licenses– Maximum obligation for seller– If seller is not well-suited to clear goods for import, DAP should be

used– No obligation to pay for insurance

KEY ELEMENTS OF EXPORT - IMPORT DOCUMENTATIONthe documentation sequence for a typical international trade transaction

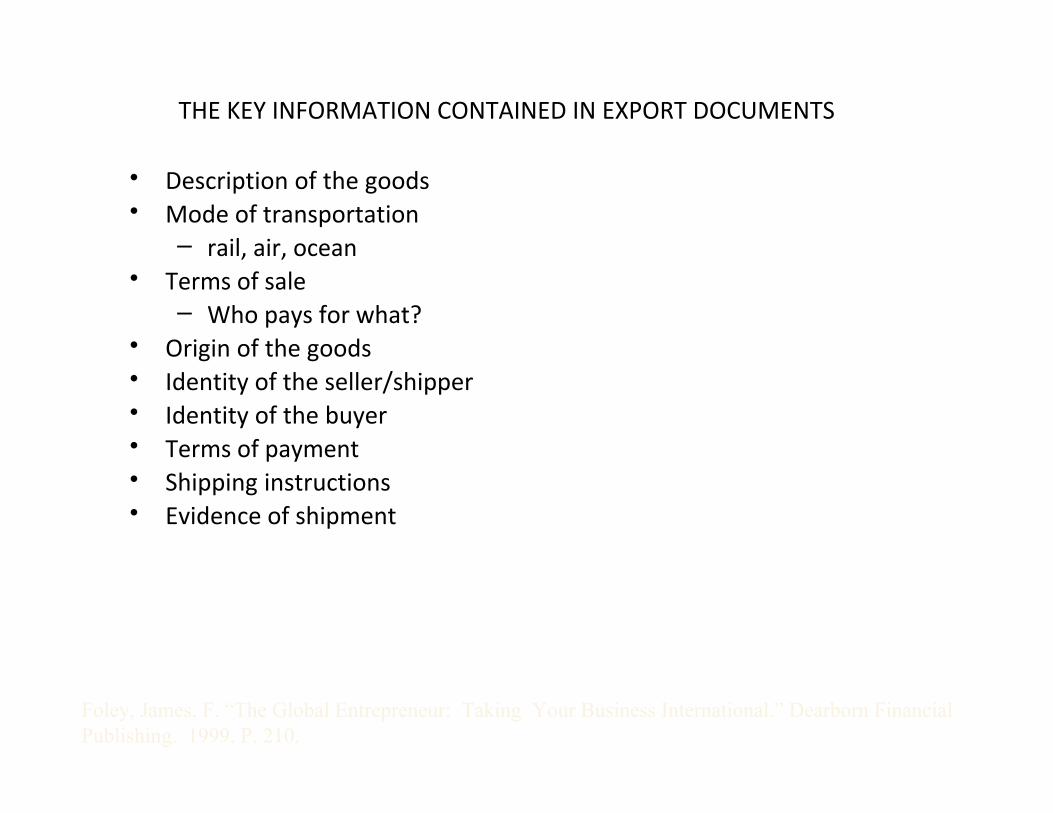

THE KEY INFORMATION CONTAINED IN EXPORT DOCUMENTS

• Description of the goods• Mode of transportation

– rail, air, ocean• Terms of sale

– Who pays for what?• Origin of the goods• Identity of the seller/shipper• Identity of the buyer• Terms of payment• Shipping instructions• Evidence of shipment

Foley, James, F. “The Global Entrepreneur: Taking Your Business International.” Dearborn Financial Publishing. 1999. P. 210.

COMMON EXPORT DOCUMENTS

• Pro forma invoice• Bill of Lading• Certificate of Origin• Packing List• Commercial Invoice• Shipper’s Export Declaration (SED)• Consular Invoice

• Inspection Certificate• Insurance Certificate• Dock/Warehouse receipt• Letter of Credit• Draft

STEPS IN THE DOCUMENTATION PROCESS

• Receive the order under accepted terms & consult with a banker or a freight forwarder.

• Begin organizing information for required export documents and export license applications.

• Evaluate modes of transportation, requirements for perishable products, and cost of various alternative modes.

• Prepare goods for shipping (marking/labeling, packing, consolidating/containerizing, insuring)

• Complete and forward required export documents.

Export Import Documents

• Understanding a Sales Contract ( CISG,UNICITRAL)

• Pre Shipment , Post Shipment Documents

• Transportation / Shipping Documents

• Customs , Excise Documentation ( ARE 1 )

• Facilitating Agency Documentation

• Relevance of Documents

( a) Confirmation of shipment and title of goods;

(b) Financial Transactions ( Receipt of Payments etc )

(c) Product Identification

(d) Correct Harmonized Classification

(e) Pre Shipment – Post Shipment Finance

(f) Export Incentives

(g) Origin and destination country Quality Inspection needs

(h) Availing Export , Import Licenses , Schemes

(g) Transportation Purpose

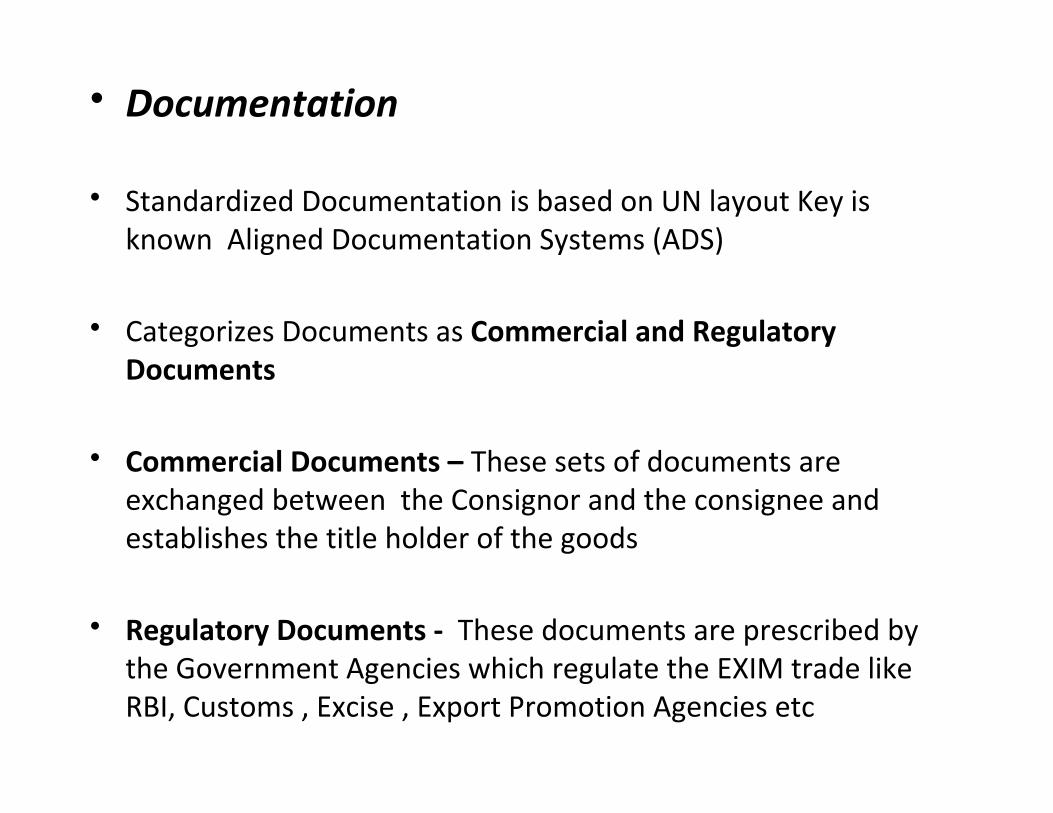

• Documentation

• Standardized Documentation is based on UN layout Key is known Aligned Documentation Systems (ADS)

• Categorizes Documents as Commercial and Regulatory Documents

• Commercial Documents – These sets of documents are exchanged between the Consignor and the consignee and establishes the title holder of the goods

• Regulatory Documents - These documents are prescribed by the Government Agencies which regulate the EXIM trade like RBI, Customs , Excise , Export Promotion Agencies etc

• Commercial Documents - Principle Documents

1. Commercial Invoice

2. Packing List

3. Certificate of Inspection

4. Insurance Certificate

5. Certificate of Insurance

6. Certificate of Origin

7. Bill of Exchange

8. Shipment Advice

• Commercial Documents - Auxiliary Documents

1. Pro-forma Invoice

2. Shipping Instruction

3. Intimation of Inspection

4. Insurance Declaration

5. Shipping Order

6. Mate’s Receipt

7. Application for Certificate of Origin

8. Letter to the Bank for Collection / Negotiation of Documents

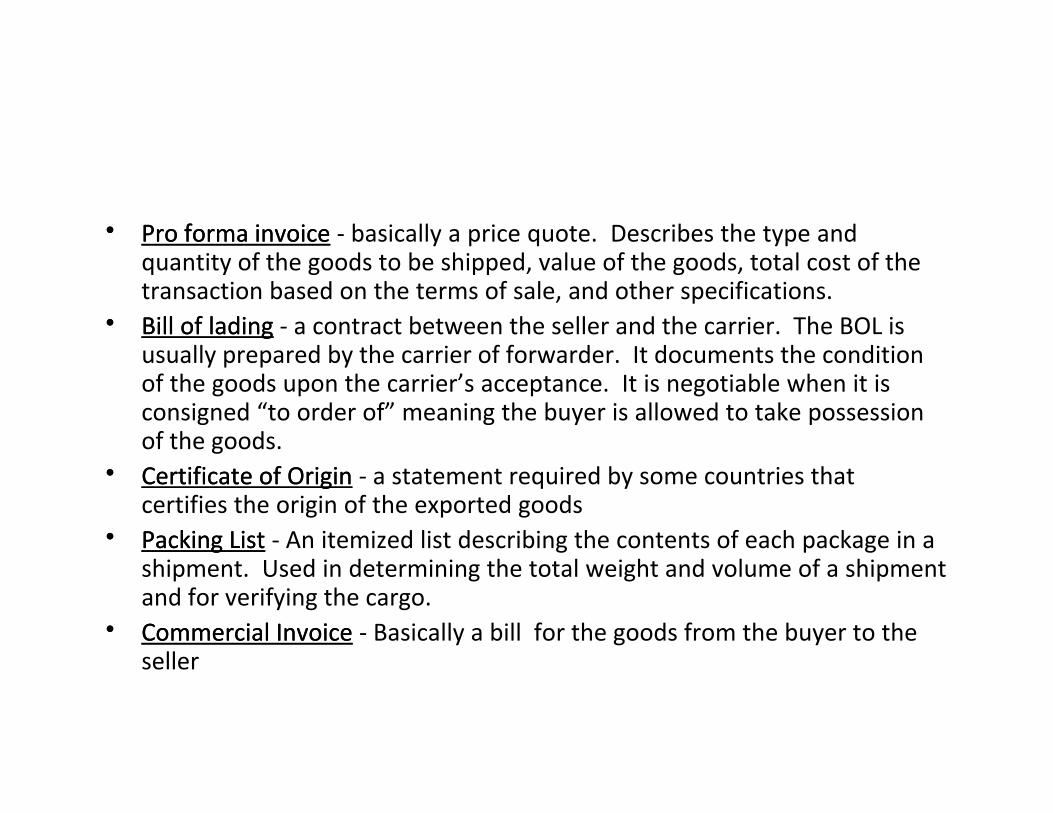

•• Pro forma invoicePro forma invoice - basically a price quote. Describes the type and quantity of the goods to be shipped, value of the goods, total cost of the transaction based on the terms of sale, and other specifications.

•• Bill of ladingBill of lading - a contract between the seller and the carrier. The BOL is usually prepared by the carrier of forwarder. It documents the condition of the goods upon the carrier’s acceptance. It is negotiable when it is consigned “to order of” meaning the buyer is allowed to take possession of the goods.

•• Certificate of OriginCertificate of Origin - a statement required by some countries that certifies the origin of the exported goods

•• Packing ListPacking List - An itemized list describing the contents of each package in a shipment. Used in determining the total weight and volume of a shipment and for verifying the cargo.

•• Commercial InvoiceCommercial Invoice - Basically a bill for the goods from the buyer to the seller

•• Consular InvoiceConsular Invoice - A document required by some foreign governments for identifying and controlling imported goods

•• Inspection CertificateInspection Certificate - a document required by some foreign governments that certifies that the goods imported conform to the order

•• Insurance CertificateInsurance Certificate - the document providing proof that the cargo (goods shipped) have been properly insured. (amount and type of insurance)

•• Dock/warehouse receiptDock/warehouse receipt - this document transfers accountability from the seller to the carrier.

•• Letter of CreditLetter of Credit - a letter from your customer’s bank to you, in which the importer’s bank guarantees payment, provided that all the terms stated in the letter are met.

•• DraftDraft - An unconditional order in writing from the drawer to the draweethat directs the drawee to pay a specified amount to a named drawer at a fixed or determinable future date.

Regulatory Documents

Primary Regulatory Documents Subsidiary Regulatory Documents

Shipping Bill / Bill Of Export / Bill of Entry

Freight Certificate

Exchange Control Documents ( SDF/ GR – I )( RBI Document )

Terminal Handling Fee / CWC Receipt

ARE 1 – Excise Document Lorry Receipt / Toll Tax Receipts

Remittance Application ( Bank Realization Certificate )

Insurance Premium Payment Certificate

Licenses ( Export / Import )

Proof of Landing /Delivery Order

• Standardized Documentation based on UN layout Key is known Aligned Documentation Systems (ADS)

• Implemented in India since September 1991

• Contained documents in Master Documents 1 and Master documents 2

• All Documents is are approximately standardized in two categories as commercial documents and regulatory documents.

Customs & Excise Tariff

• Customs Tariiff Act Two Schedules i.e. Import Tariff and Export Tariif• CE Tariff has 20 Sections and contains chapter 1-96 • Customs Tariff has one additional Section XXI• Customs Tariff has extra column giving Rate of duty for preferential area• Second Schedule of Customs Tariff is Export Tariff shows export duties

leviable. Second Schedule of Central Excise Tariff shows rates of special excise duty (SED)

• Customs Act,1962 provides the basic legal framework for Customs Administration in India.

• A large number of Rules and Regulations have been framed under this Act to carry out its purposes.

• Customs duties• governing and regulating movement of GOODS,

VESSELS/AIRCRAFTS/VEHICLES, PASSENGERS AND THEIR BAGGAGE across national borders

• India as a member of WCO has adopted international customs conventions and procedures including the Harmonized Classification System and GATT Valuation Rules.

Features Customs Administration

1. Assessment of customs duty leviable and collection of the revenue

2. Facilitating cargo clearance

3. Enforcing the prohibitions and restrictions

4. Dispute Resolution

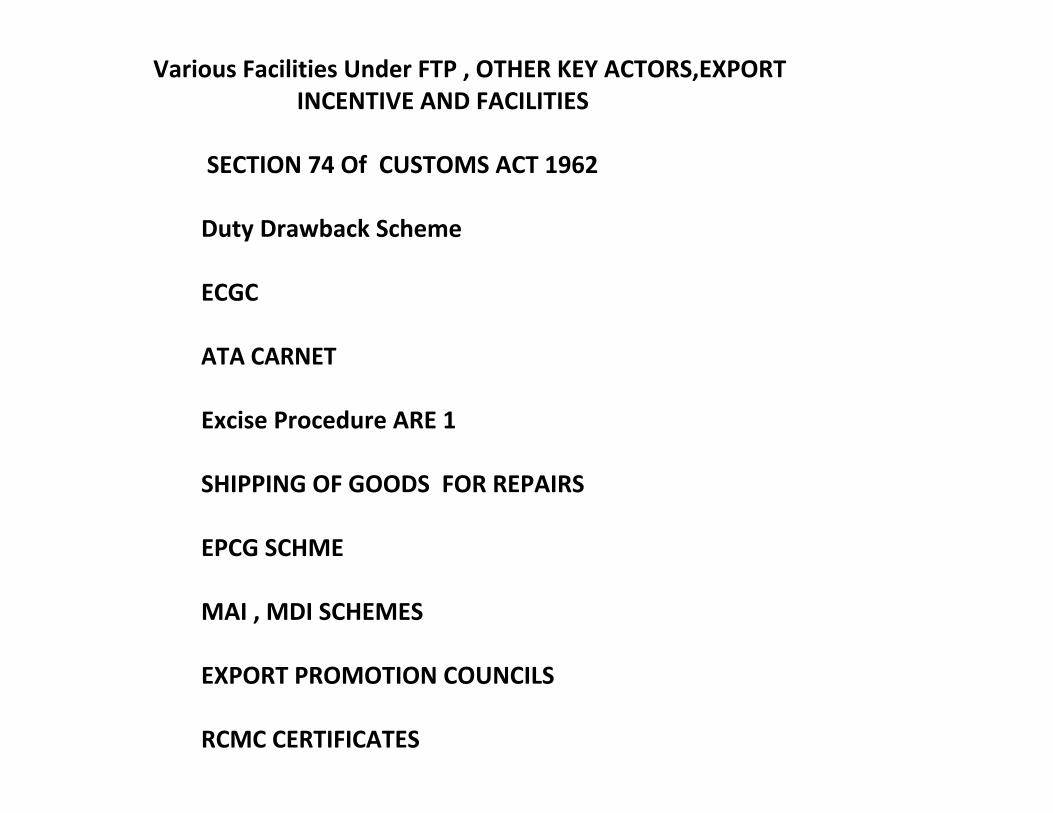

Various Facilities Under FTP , OTHER KEY ACTORS,EXPORT INCENTIVE AND FACILITIES

SECTION 74 Of CUSTOMS ACT 1962

Duty Drawback Scheme

ECGC

ATA CARNET

Excise Procedure ARE 1

SHIPPING OF GOODS FOR REPAIRS

EPCG SCHME

MAI , MDI SCHEMES

EXPORT PROMOTION COUNCILS

RCMC CERTIFICATES

113

EXPORT CLEARANCE PROCEDURES

114

Few definitions –

Section 2(5) – “bill of export” means a bill of export referred to in Section 50

Section 2(16) – “entry” in relation to goods means an entry made in a bill of entry, shipping bill or bill of export and includes in the case of goods imported or to be exported by post, the entry referred to in section 82 or the entry made under the regulations made under section 84.

Section 2(18) – “export” with its grammatical variations and cognate expressions, means taking out of India to a place out of India.

Section 2(19) – “export goods” means any goods which are to be taken out of India to a place out of India

Section 2(20) – “exporter”, in relation to any goods at any time between their entry for export and the time when they are exported, includes any owner or any person holding himself out to be the ex

115

Section 16 – Date for determination of rate of duty and tariff valuation of export goods – (1) The rate of duty and tariff valuation, if any, applicable to any export goods, shall be the rate and valuation in force –(a) in the case of goods entered for export under section 50, on the date on which the proper officer makes an order permitting clearance and loading of the goods for exportation under section 51(b) in the case of any other goods, on the date of payment of duty.

(2) The provisions of this section shall not apply to baggage and goods exported by post.

116

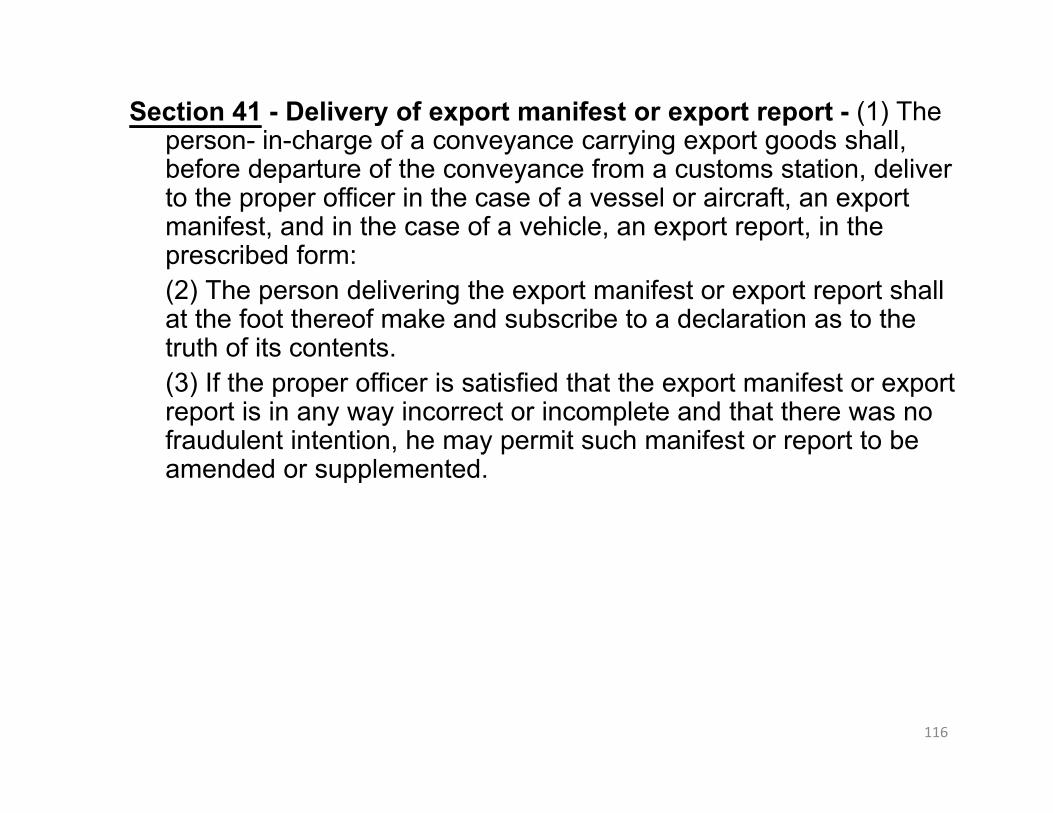

Section 41 - Delivery of export manifest or export report - (1) The person- in-charge of a conveyance carrying export goods shall, before departure of the conveyance from a customs station, deliver to the proper officer in the case of a vessel or aircraft, an export manifest, and in the case of a vehicle, an export report, in the prescribed form: (2) The person delivering the export manifest or export report shall at the foot thereof make and subscribe to a declaration as to the truth of its contents. (3) If the proper officer is satisfied that the export manifest or export report is in any way incorrect or incomplete and that there was no fraudulent intention, he may permit such manifest or report to be amended or supplemented.

117

Section 50 - Entry of goods for exportation. – (1) The exporter of any goods shall make entry thereof by presenting to the proper officer in the case of goods to be exported in a vessel or aircraft, a shipping bill, and in the case of goods to be exported by land, a bill of export in the prescribed form.(2) The exporter of any goods, while presenting a shipping bill or bill of export, shall at the foot thereof make and subscribe to a declaration as to the truth of its contents.

118

Requirements for exporter -

PAN based “Business Identification Number” (BIN) from the Directorate General of Foreign Trade

Register authorised foreign exchange dealer (bank) code and account number in the designated bank

For exports under DEEC, DEPB, DFRC etc. registration with

the concerned Customs House required

119

Customs Procedure

Customs procedure relating to export of goods fully computerised at most of the ports

Procedure can be divided in two parts -- Filing & Processing in the Group

-- Examination in the shed

120

Documents Processing

Filing of documents through EDI Filing can be done by the CHA himself or through

Customs Service Centre Documents – Invoice, Packing list, SDF (Self

Declaration form) and Annexure submitted to CSC The data in the Annexure is fed into the system Check list generated in the system is handed over to the

CHA/Exporter

• Under ICES 1.5, the computerized processing of shipping bills is handled in respect of the following categories:

•• 1. Duty Free white Shipping Bills• 2. Dutiable Shipping Bills (Cess)• 3. Drawback Shipping Bills• 4. DEEC Shipping Bills• 5. EPCG Shipping Bills• 6. DEPB Shipping Bills• 7. DFIA Shipping Bills• 8. 100 %EOU Shipping Bills• 9. Jobbing Shipping Bills• 10. Other Exim Scheme Shipping Bills• 11. NFEI Shipping Bills.

122

Processing contd.

Check list given to CHA along with documents CHA verifies the entries and returns to CSC Data submitted to system which generates shipping Bill

Number Printout of check list with S.B. No. endorsed is given to CHA Shipping Bill processed in the group Assessed by Superintendent and he checks value, Drawback

rate, DEPB rate, Licence description, validity etc. Subsequently goes to Assistant Commissioner Special instructions can be given by group to shed staff

123

Arrival of the Goods

CHA approaches Shipping Ling for forwarding note –container number

Goods brought to port and Cargo Receipt Note (CRN) given by the Port Authority

Cargo unloaded in the shed Cargo verified by the custodian and tally sheet

generated

124

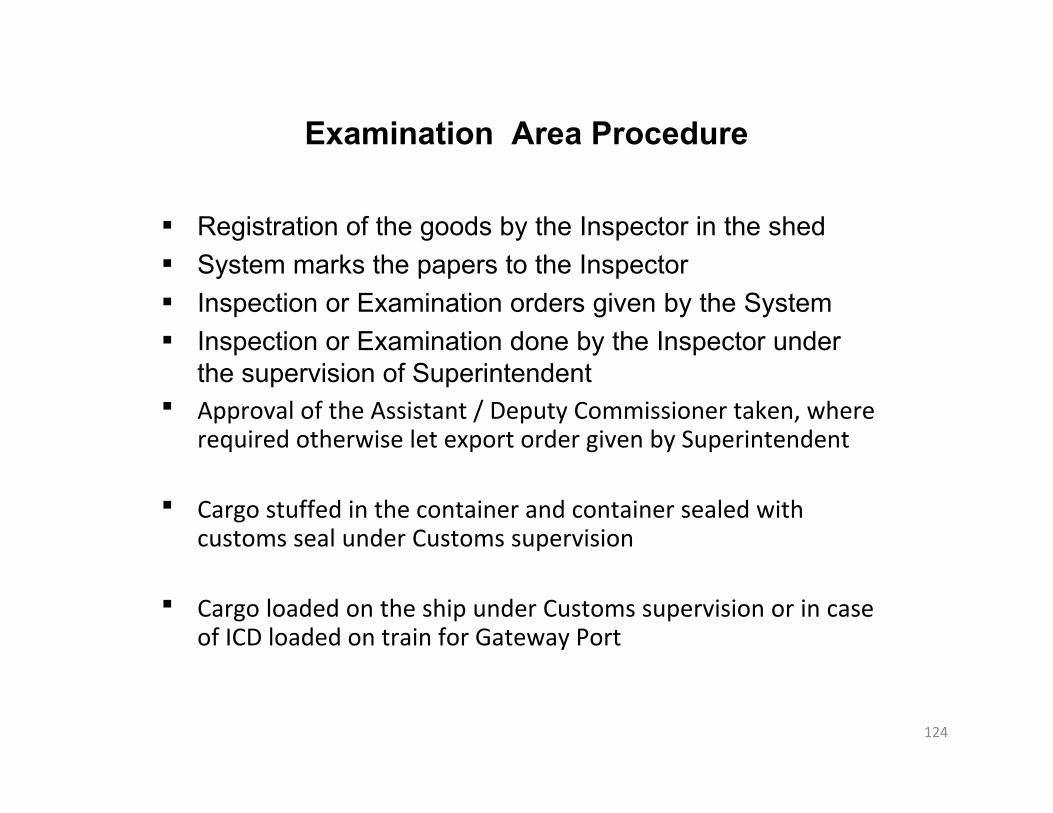

Examination Area Procedure

Registration of the goods by the Inspector in the shed System marks the papers to the Inspector Inspection or Examination orders given by the System Inspection or Examination done by the Inspector under

the supervision of Superintendent Approval of the Assistant / Deputy Commissioner taken, where

required otherwise let export order given by Superintendent

Cargo stuffed in the container and container sealed with customs seal under Customs supervision

Cargo loaded on the ship under Customs supervision or in case of ICD loaded on train for Gateway Port

• The S/B would be processed by the system on the basis of the declaration made by the exporter. The following kinds of S/B shall require clearance of the Assistant Commissioner/ Deputy Commissioner (AC/DC Exports): -

• It could vary from each custom station • i. Duty free S/B for FOB value above Rs. 10 lakh• ii. Free Trade Sample S/B for FOB value above Rs. 25,000• iii. Drawback S/B where the drawback exceeds Rs. one lakh•• The following categories of Shipping Bills re generally processed by the

Appraiser/ Supdt. (Export Assessment) first and then by the Asstt/Deputy Commissioner:

• i. DEEC• ii. DEPB• iii. DFRC• iv. EOU• v. EPCG• vi. Any other Exim Scheme, if so required

CUSTODIAN

The goods imported into India and exported out of India are allowed through designated Sea Ports / Land Custom Stations / Airports.

The goods so imported / exported are initially deposited in the custody of Custodian such as

Port authorities for goods imported through sea.

Custodians for goods imported by air

DIAL

For places other than points of landing

Inland Container Depot (ICD) ICD)-M/s CONCOR at ICD TughlakabadContainer Freight Station (CFS) CFS)-M/s CWC at ICD Patparganj

Role of Custodians

127

• Customs authorize and appoint "custodians" for all imported goodsunloaded in a Customs area to remain in their custody till these arecleared

• Custodian to arranges proper storage and safety and allows delivery to theimporters only after they fulfill all the customs formalities, pay uprequisite duties and other charges/fees

Export Promotion Schemes

•DUTY EXEMPTION/REMISSION SCHEMES:-

1) Advance AuthorisationScheme (DEEC/Adv. Licence)

2) Duty Free Replenishment Scheme (upto 4/06)

3) DEPB Scheme

4) Duty Free Import Authorisation(DFIA w.e.f 1.5.06)

•EXPORT PROMOTION CAPITAL GOODS SCHEME(EPCG)

•EOU/STP/EHTP/Biotechnology Parks

•SPECIAL ECONOMIC ZONES (separate Act & Rules framed)

•FREE TRADE AND WAREHOUSING ZONES

•DEEMED EXPORTS

•SPECIAL SCHEMES UNDER EXPORT PROMOTION

•SERVED FROM INDIA SCHEME ( formerly DFEC)

•VISHESH KRISHI AND GRAM UDYOG YOJANA

•FOCUS MARKET SCHEMES

(Export to certain specified countries)

•FOCUS PRODUCT SCHEMES

(Export of Specified commodities

Export Documents

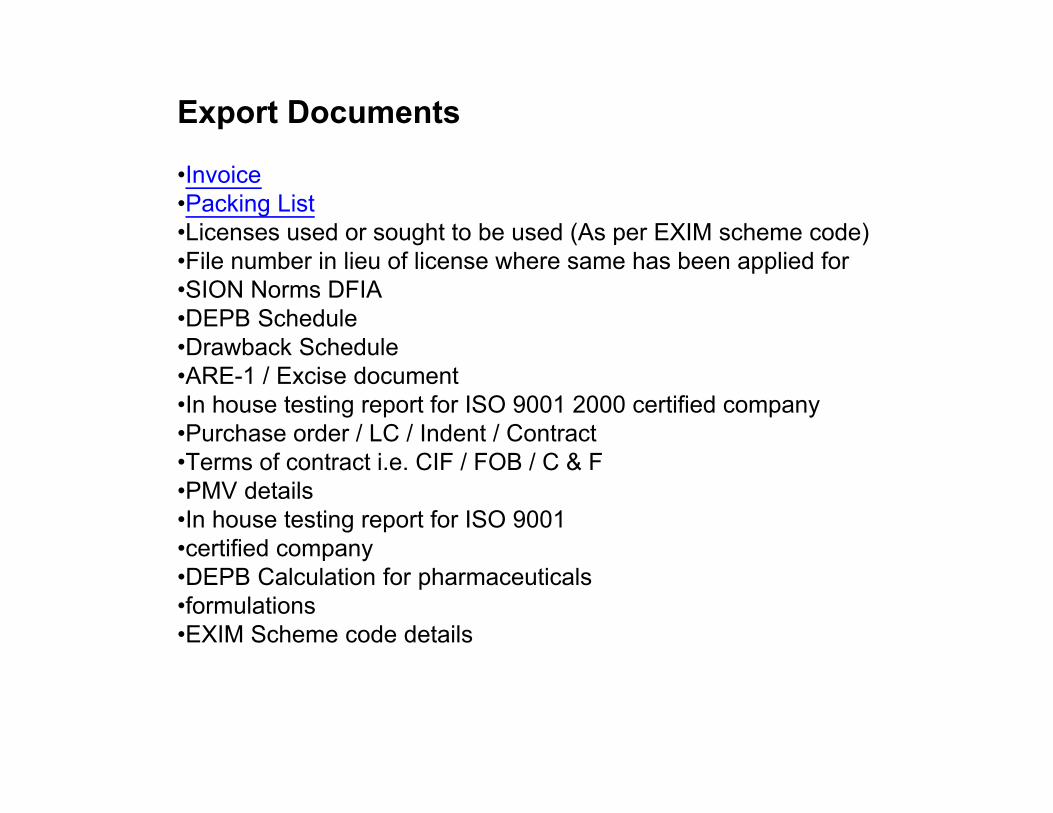

•Invoice•Packing List•Licenses used or sought to be used (As per EXIM scheme code)•File number in lieu of license where same has been applied for•SION Norms DFIA•DEPB Schedule•Drawback Schedule•ARE-1 / Excise document•In house testing report for ISO 9001 2000 certified company•Purchase order / LC / Indent / Contract•Terms of contract i.e. CIF / FOB / C & F•PMV details•In house testing report for ISO 9001•certified company•DEPB Calculation for pharmaceuticals•formulations•EXIM Scheme code details

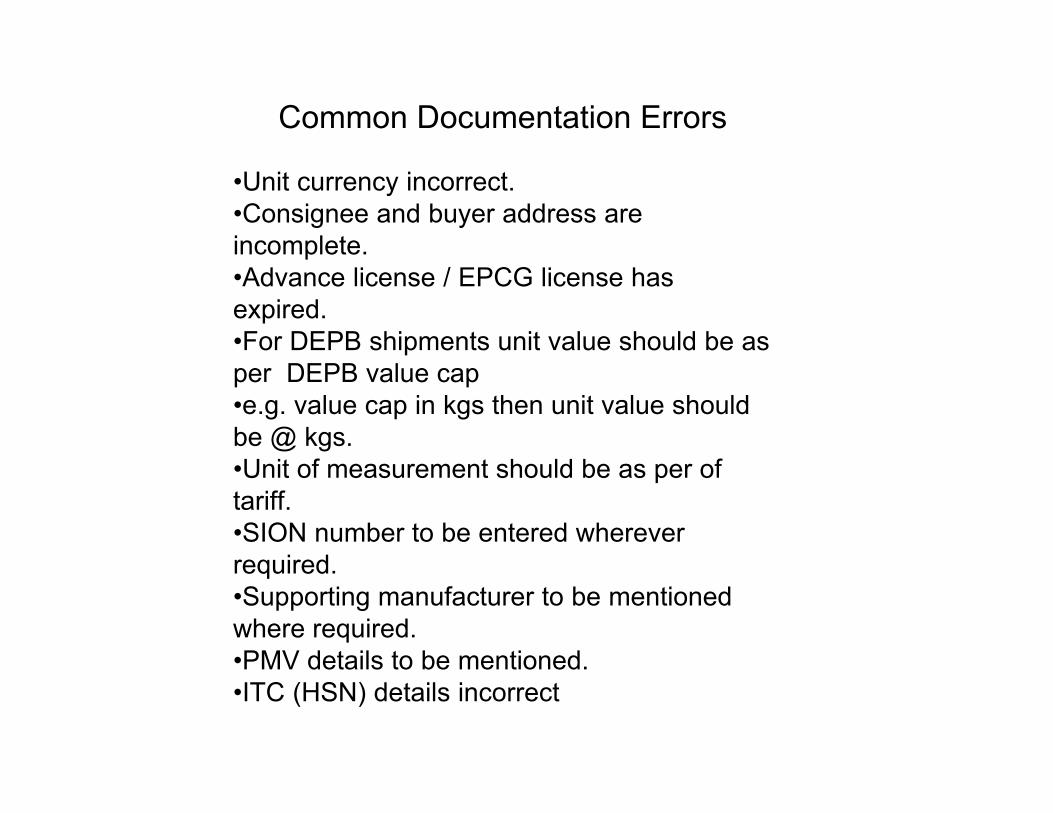

Common Documentation Errors

•Unit currency incorrect.•Consignee and buyer address are incomplete.•Advance license / EPCG license has expired.•For DEPB shipments unit value should be as per DEPB value cap•e.g. value cap in kgs then unit value should be @ kgs.•Unit of measurement should be as per of tariff.•SION number to be entered wherever required.•Supporting manufacturer to be mentioned where required.•PMV details to be mentioned.•ITC (HSN) details incorrect

Flow Chart of Cargo Clearance System Of INDIA(Export Sea Freight)

Shipper/ExporterOr

Agent

Preparation of Export Documents

SS Line •Booking •Receiving Shipping Dos for release containerfrom ICD and delivery from to CFS

Shipping Agency Department•Endorsement for Cargo Accept to nominated feeder vessel

CFS Port Authority•Port charges paid for container•Loading Empty Container in ICDand transport to Shipper warehouse

--Signed invoice/Packing list--L/C /perform invoice / insurance--SDF form / DEPB declaration -- Annexure

Entry in terms of Section 46 of Customs Act, 1962 Annexure A + C SDF in duplicate

DEPB DeclarationCMCCheck List

CMC/Shipping Bill Number Goods of Shipping Line warehouses

Concor

Goods ExamineCMC Printout Container Stuffing

Container Seal

TR 1 / TR II Handover to shipping line

Flow Chart of Cargo Clearance System Of INDIA(Sea Exports ) ICD Patparganj

Entry in terms of Section 46 of Customs Act, 1962

Annexure A + C

SDF in duplicate

DEPB Declaration

CMC

Check List

CMC/Shipping Bill Number

Goods of Shipping Line warehouses Concor

Goods Examine

CMC Printout

Container Stuffing / CONSOLIDATOR STUFFING

Container Seal

TR 1 / TR II Handover to shipping line

Registration & Processing

Obtain Carting Order & AWB from the Carrier

DIAL Counter and obtain Terminal Charges

Pay DIAL charges

Enter Export Cargo along with relevant documents

Present papers (SB/AWB/Carting Order/TC receipt) to DIAL staff in Truck Park for docking to trucks at designated Truck Dock gate

Obtain DIAL endorsement on S/B

Obtain Customs number from the respective Customs Group

Complete Customs Examination & Obtain

DIAL Staff at bonded area gate along with cargo for binning & endorsing location on the TC Receipt/AWB

Hand Over documents to Airlines

Airline submits Customs approved loading sheet for unitization or bulk loading to DIAL

Release of Export Cargo from ETV for the flight

Flow Chart of Cargo Clearance System Of INDIA( Air Exports )

Role Of PSI Agencies

• Initially used PSI Agencies for certification of quality & quantity of product

• Assurance to importers that goods conform to technical specifications & quantities correct

• Used by state owned and government departments

• Since mid sixties also used for price verification

Preshipment Inspection (PSI) Government Agencies

Pre shipment Inspection Thrird Part Inspection Agencies

Imports

Preparation of Various Types of Bill of Entries

Documents Required

Types of Bill Of Entries

Types of Duties

Procedure of Filing Bill of Entry ( EDI ) in custom as well as ICE GATE

Documentation , Custom Clearance Procedures

Case Study

PROCEDURE FOR IMPORT CARGO

Procedure by Importer - The importer importing the goods has to follow prescribed procedures for import by

ship/air/road. (There is separate procedure for goods imported as a baggage or by post.)

Bill of Entry - This is a very vital and important document which every importer has to submit under section 46.

size of Bill of Entry is 16" × 13". However, for computerizations purposes, 15" × 12" size is permitted. Bill of Entry should be

submitted in quadruplicate – original and duplicate for customs, triplicate for the importer and fourth copy is meant

for bank for making remittances.Under EDI system, Bill of Entry is actually printed on computer in triplicate only after ‘out of charge’ order is given. Duplicate

copy is given to importer.

TYPES OF BILL OF ENTRY

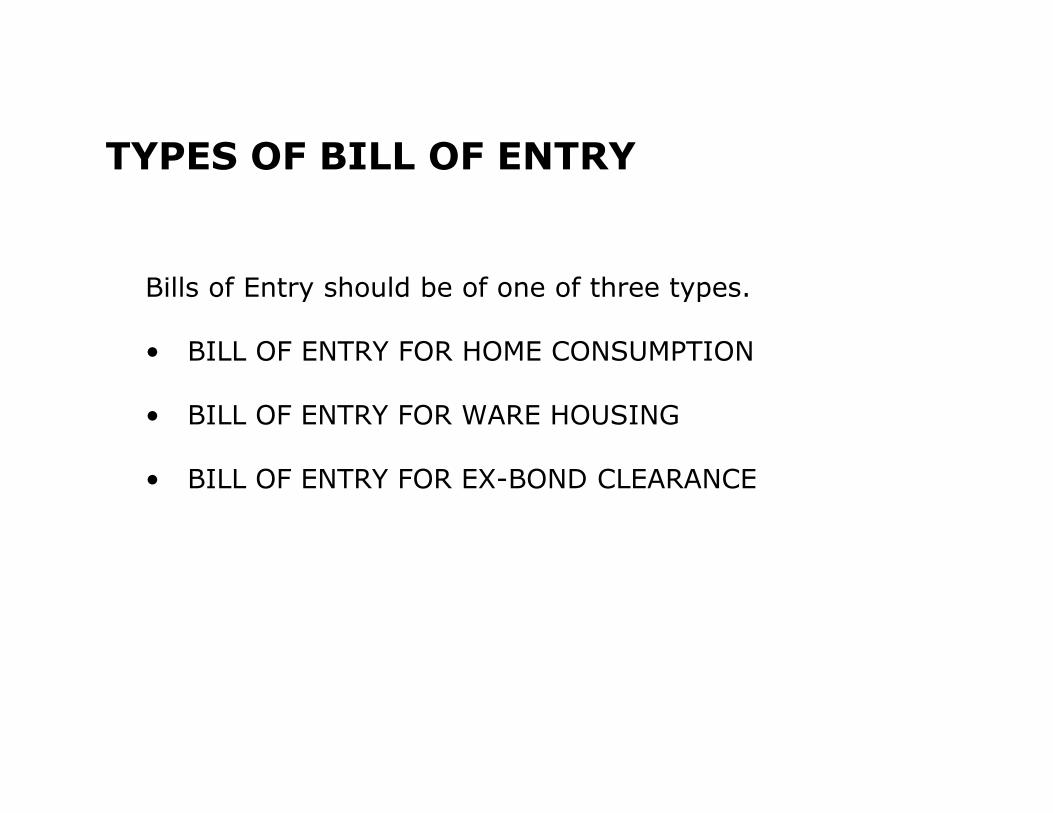

Bills of Entry should be of one of three types.

• BILL OF ENTRY FOR HOME CONSUMPTION

• BILL OF ENTRY FOR WARE HOUSING

• BILL OF ENTRY FOR EX-BOND CLEARANCE

Bill of Entry for Home Consumption:- is used when the imported goods are to be cleared on payment of full duty. Homeconsumption means use within India. It is white coloured and hence often called ‘white bill of entry’.

BILL OF ENTRY FOR WAREHOUSING :- If the imported goods are not required immediately, importer may like to store the goods in a warehouse without payment of duty under a bond and then clear from warehouse when required on payment of duty. This will enable him to defer payment of customs duty till goods are actually required by him. This Bill of Entry is printed on yellow paper and often called ‘Yellow Bill of Entry’. It is also called ‘Into Bond Bill of Entry’ as bond is executed for transfer of goods in warehouse without payment of duty. BILL OF ENTRY FOR EX-BOND CLEARANCE:- The third type is for Ex-Bond clearance. This is used for clearance from the warehouse on payment of duty and is printed on green paper. The goods are classified and value is assessed at the time of clearance from customs port. Thus, value and classification is not required to be determined in this bill of entry. The columns in this bill of entry are similar to other bills of entry. However, declaration by importer is not required as the goods are already assessed

Filing of Bill of Entry:- Normally, Bill of Entry is filed by CHA on behalf of the importer. Customs work at some ports has been computerized. In that case, the Bill of Entry has to be filed electronically, i.e. through Customs EDI system through computerizations of work. Procedure for the same has been prescribed vide Bill of Entry (Electronic Declaration) Regulations, 1995. Documents to be submitted by Importer:- Documents required by customs authorities are required to be submitted to enable them to (a) check the goods (b) decide value and classification of goods and (c) to ensure that the import is legally permitted. The documents that are essentially required are : (i) Invoice (ii) Packing List (iii) Bill of Lading / Delivery Order (iv) GATT declaration form duly filled in (v) Importers / CHAs declaration duly signed (vi) Import License or attested photocopy when clearance is under license (vii) Letter of Credit / Bank Draft wherever necessary (vii) Insurance memo or insurance policy (viii) Industrial License if required (ix) Certificate of country of origin, if preferential rate is claimed. (x) Technical literature. (xi) Test report in case of chemicals (xii) Advance License / DEPB in original, where applicable.

Assessment of Duty and ClearanceThe documents submitted by importer are checked and assessed by Customs authorities and then goods are cleared. Section 2(2) defines ‘assessment’ as follows – ‘Assessment’ includes provisional assessment, reassessment and any order of assessment in which the duty assessed is Nil. Thus, ‘assessment’ includes ‘Nil’ assessment.

Noting of Bill of Entry:- Bill of Entry submitted by importer or Customs House Agent is cross-checked with ‘Import Manifest’ submitted by person in charge of vessel / carrier. It is noted if the description tallies. ‘Noting’ really means taking on record by customs officer. This date is relevant for determining rate of customs duty. Thoka number (serial number) is given in the import section. Otherwise, it is returned for clarifications. In case of EDI system, noting is done by the system itself which also generates bill of entry number.Bill of Entry is accepted only after proper scrutiny vis-a-vis import manifest and various declarations given in bill of entry and attached documents like invoice, bill of lading etc. If such documents are not attached, the authorities can refuse to accept the Bill of Entry, and hence submission of such incomplete Bill of Entry cannot be taken as date of presentation of Bill of Entry

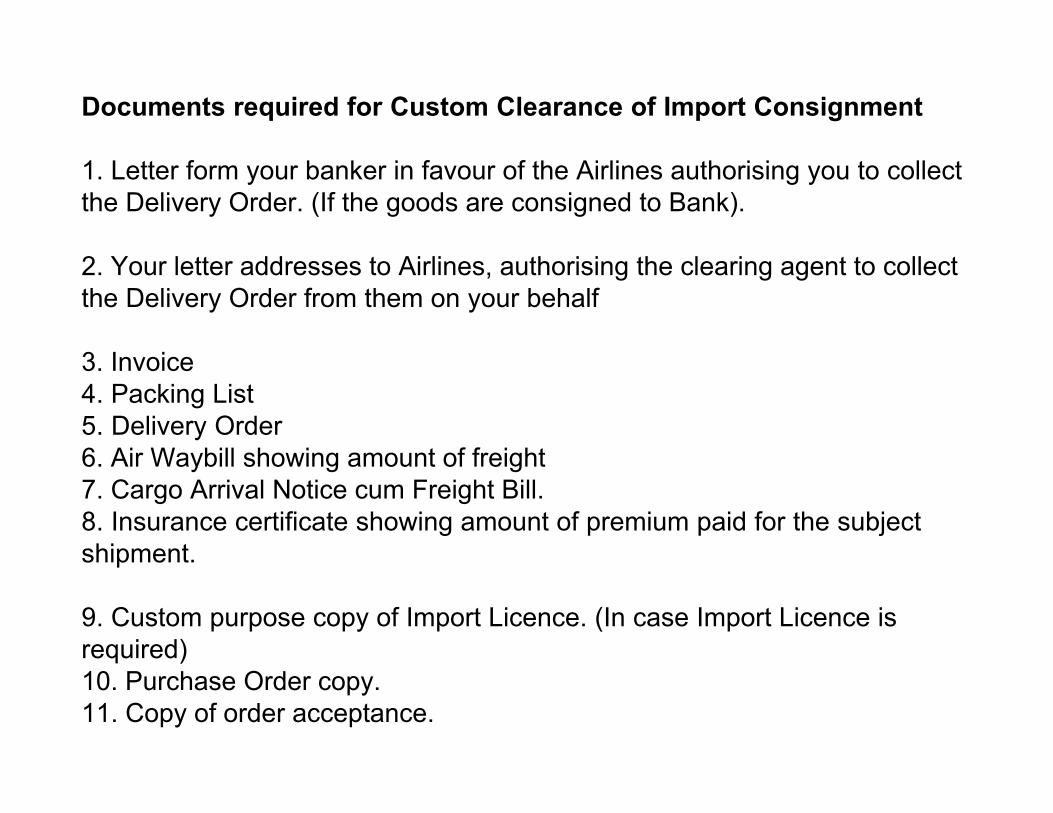

Documents required for Custom Clearance of Import Consignment

1. Letter form your banker in favour of the Airlines authorising you to collectthe Delivery Order. (If the goods are consigned to Bank).

2. Your letter addresses to Airlines, authorising the clearing agent to collectthe Delivery Order from them on your behalf

3. Invoice4. Packing List5. Delivery Order6. Air Waybill showing amount of freight7. Cargo Arrival Notice cum Freight Bill.8. Insurance certificate showing amount of premium paid for the subjectshipment.

9. Custom purpose copy of Import Licence. (In case Import Licence isrequired)10. Purchase Order copy.11. Copy of order acceptance.

12. Copy of letter of credit.13. Certificate of Origin.14. Importer’s Declaration duly signed with stamp - 2 copies.15. GATT Declaration duly sig ned with stamp- 2 copies.16. Photostat copy of Catalogue showing items imported. In addition to this orin the absence of catalogue, a technical write -up of the various itemsexplaining each item on the following lines:i. What is the item i.e., whether it is a Capital good or Components or Consumables or spare parts?ii. Material of construction of item, i.e., metallic or plastic or rubber etc.Also clarify whether it is an individual part or a subassembly or an assembly of various parts.iii. Whether it is a totally mechanical part or is a subassembly of mechanical and electrical items.iv. Function of the item in details so that proper classification can be donein custom tariff.v. In the case of spare parts, please highlight the same in the catalogue.vi. In the Technical write-up, of Spare parts, in case there are some partswhich have been manufactured solely for that particular machine andcannot be used anywhere else, it should be explained in detail.17. Your Importer Exporter Code Number (IEC Number)18. Letter addressed to the Assistant Commissioner Customs, New Delhi,authorising the clearing agent to clear your Imported consignments.19. Any other specific document which is required for clearance of yourspecific / specialised cargo for example chemical Analysis Report etc.

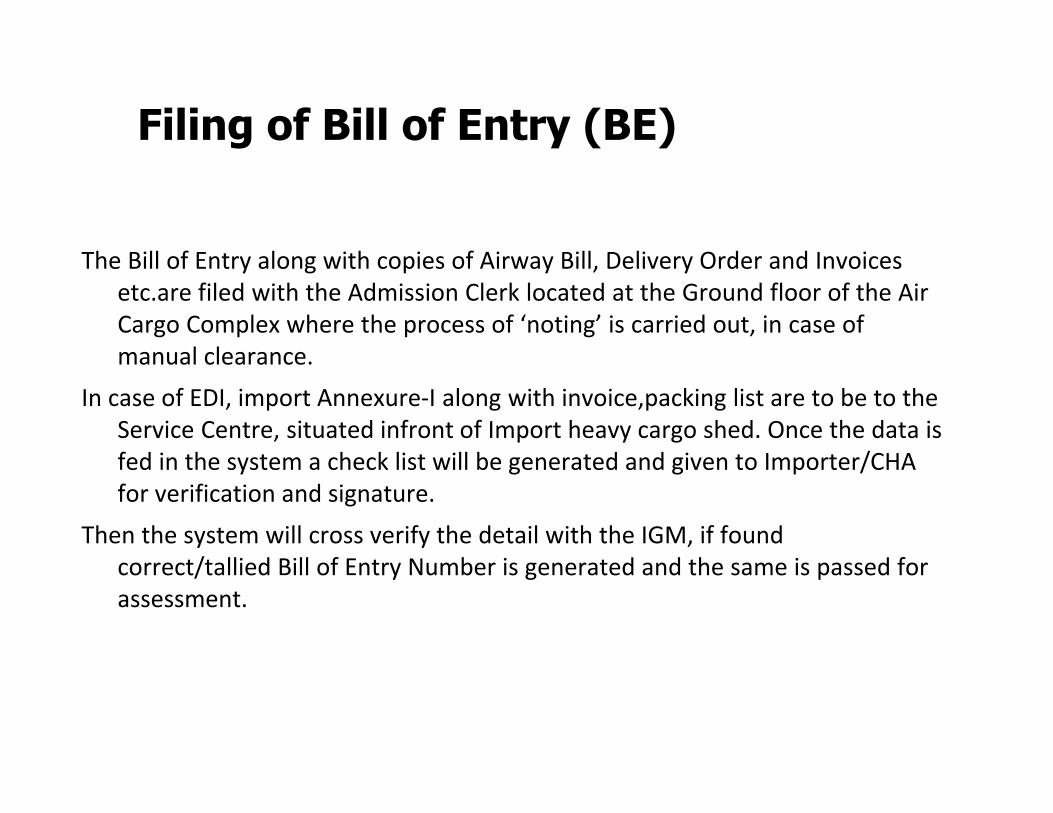

Filing of Bill of Entry (BE)

The Bill of Entry along with copies of Airway Bill, Delivery Order and Invoices etc.are filed with the Admission Clerk located at the Ground floor of the Air Cargo Complex where the process of ‘noting’ is carried out, in case of manual clearance.

In case of EDI, import Annexure-I along with invoice,packing list are to be to the Service Centre, situated infront of Import heavy cargo shed. Once the data is fed in the system a check list will be generated and given to Importer/CHA for verification and signature.

Then the system will cross verify the detail with the IGM, if found correct/tallied Bill of Entry Number is generated and the same is passed for assessment.

Appraisement

The Bill of Entry is put up to Appraisement Department for processing the same for the First or Second AppraisementIn case of Second Appraisement, ‘Duty ’is assessed and ‘paid before' the Customs Examination

Open Examination order

In case of first appraisement open examination order is obtained.To obtain the Open Examination Order, the Importer/Agent is required to contact the Shed Appraiser who will (mark and make) a remark/noting for calling the packages for Examination. He shall also indicate the name of the Examining Officer on the Bill of Entry and thereafter AAI Location Counter should be approached to get the/location Slip.

Generation of location slip

The location slip is generated at the AAI location counter on the basis of the Customs open examination order on the Bill of Entry and along with other relevant documents like Delivery Order / Sub delivery order, Copies of MAWB/HAWB.

Customs Examination Location : Examination Hall

Packages are forwarded for Customs Examination from the locations, based on the Location Slip generated by AAI.

After the Custom’s Examination, the packages are re-packed/sealed in the presence of Importer/Agent and returned to the AAI for storage into the location.

Out of customs charge

In case of First Appraisement, after completion of the Examination, the remaining Customs formalities will be completed on the first floor. After payment of duty, Office Superintendent in the Treasury Section will give ‘Out of Customs Charge' On completion of the Examination formalities, and also if the goods are in order, the Shed Appraiser will give ‘Out of Customs Charge’., in case of goods being cleared under Second Appraisement.

Issuance of Bill-Cum Gate Pass

After obtaining ‘Out of Customs Charge’ by the Importer/Agent is required to contact DIAL Billing Counter for issue of Demurrage Charges-cum-Gate Pass after payment of DIAL charges and Two copies (Green and Red) shall be issued. The green copy should be submitted to the DIAL staff located in the Examination Area and Red Copy should be retained by the Importer/Agent and proceed to the Exit Gate.

Delivery

On receipt of the Green copy of the Gate Pass, the DIAL staff shall make arrangements for delivery of the packages and shall direct the Importer/Agent to go to the Delivery Gate for taking delivery of the packages.

On verification of the Gate Pass and the packages by Customs Gate Officer and DIAL Staff, the consignments will be released to the Importer/Agent against clear signatures.

Received the documents from importer

CMC

OBTAIN CHECK OF LIST AND BILL OF ENTRY

APPRAISMENT

OPEN EXAMINATION ORDER

GENERATION OF LOCATION SLIP

CUSTOM EXAMINATION

OUT OF CUSTOM CHARGE

ISSUANCE OF BILL-CUMGATE PASS

DELIVERY OF GOODS

Flow Chart of Cargo Clearance System Of INDIA( AIR import)

General Import Clearance InformationClearance Process

No person can import or Export goods without obtaining an Importer-Exporter Code (IEC) Number along with a BIN (Business Identification Number) from the Regional Licensing Authority (Director General of Foreign Trade) The Customs authority will not clear goods unless the Importer/ Exporter has obtained Import Export Code Number or BIN Number. However no registration is necessary for the following entities;

- All Ministries/ Departments of the Central Government and agencies wholly or partially owned by them

- Diplomatic personnel, Counselor officers in India and the officials of the UNO and its specialized agencies

- Persons importing / exporting goods from / to Nepal provided the CIF value of a single consignment does not exceed Indian rupees INR 25000/-

- Persons importing / exporting goods from / to Myanmar through the Indo-Myanmar border area provided the CIF value of a single consignment does not exceed Indian rupees INR 25000/

India Import Prohibitions

The following goods are subject to prohibition, restriction or surveillance:

PROHIBITS ITEMS

- Certain animals and plants and parts or products falling under CITES (Convention on International Trade in Endangered Species of Wild Flora and Fauna).

- Wild animals as defined under Wild Life Protection Act 1972- Meat of Wild Animals- Pig Fat, Fat of bovine animals, sheep or goat- Natural Abrasives - Emery, Natural- Publications containing maps showing incorrect boundaries of India

CANALISED (restricted to certain importers)

- Rice (through FCI)- Cereals other than seed quality (through FCI)- Petroleum Oil

General Import Restrictions

The following items are not acceptable for carriage to any international destinations unless otherwise indicated. - APO/FPO addresses.- C.O.D. shipments.- Human corpses, human organs or body parts, human and animal embryos, or cremated or disinterred human remains.- Explosives (Class 1.4 explosives are acceptable for carriage to Canada, Germany, Japan, United Arab Emirates and United Kingdom. - Fire arms, weaponry, and their parts (acceptable between the U.S. and Puerto Rico).- Perishable foodstuffs and foods and beverages requiring refrigeration or other environmental control.- Live animals (including insects) except via our Live Animal Desk (1.800.405.9052).- Plants and plant material, including cut flowers (cut flowers are acceptable from the U.S. to selected points in Canadaand from Colombia and Ecuador to the U.S.).

- Lottery tickets and gambling devices where prohibited by local, state, provincial or national law.- Money (coins, cash, currency, paper money and negotiable instruments equivalent to cash such as endorsed stocks,bonds and cash letters).- Collectible coins and stamps.- Pornography.- Hazardous waste, including, but not limited to, used hypodermic needles or syringes or other medical waste.- Shipments that may cause damage to, or delay of, equipment, personnel or other shipments.- Shipments that require us to obtain any special license or permit for transportation, importation or exportation.- Shipments whose carriage, importation or exportation is prohibited by any law, statute or regulation.- Shipments with a declared value for customs in excess of that permitted for a specific destination.- Dangerous goods except as permitted under the Dangerous Goods section of these terms and conditions

RESTRICTED ITEMS

- Live Animals - other than defined under Wild Life Act 1972- Live plants- Meat of Bovine Animals- Bird's eggs, in shell, fresh, preserved or cooked- Guts, Bladder and stomach of animals other than fish- Potatoes, Garlic- Australian Lupin Seeds- Nutmeg, mace and Cardamom- Seeds- Cereals- Inorganic Chemicals- Organic or Inorganic Compounds of (I) Precious Metals, (ii) Rare Earth Metals, (iii) Radioactive Elements of Isotopes CANALISED (restricted to certain importers)- Rice (through FCI)- Cereals other than seed quality (through FCI)- Petroleum Oil

Special Import ProvisionsAs per the current Import-Export Policy & Procedure, the import of goods is also permissible under the following special schemes designed to encourage export:

- Export Promotional Capital Goods Scheme (EPCG) under which capital goods can be imported at a concessional/custom duty rate subject to export obligation.

- Duty Exemption/Remission Scheme and Duty Entitlement Pass Book Scheme under which imported raw materials and components etc. required, as imports for export production are made available to the registered exporters in advancefree of Custom duty.

- Diamond, Gem & Jewelry Export Promotion Scheme and Diamond Dollar Account Scheme for promoting export ofGold silver and jewelry articles etc.

- Special Economic Zones permitted duty free import/procurement from Duties and Tax for development of SEZ and setting up a factory in the zone, license for SSI items not required etc.

General Import Duty Exemptions

Concessional Rate of Duty applies for Imports of listed goods from Bangladesh, Republic of Korea and Sri Lanka under Bangkok Agreement.Concessional Rate of Duty applies for Import of listed goods if imported from SAARC (South Asian Association of Regional co-operation) countries, which includes -Bangladesh, Bhutan, Maldives, Nepal, Pakistan and Sri Lanka.Exemption from customs duties and taxes for listed food grains imported from Myanmar, if imported through land route.

Import Duty Exemptions for Export Promotion

Under certain schemes the importer is exempted from customs duty if the importer has procured an advance license for the import and the imported material is to be used as raw material for exports. These schemes include Advance license based Imports similar to the Value based DEEC (Duty Exemption Entitlement Certificate), Quantity based DEEC, andother Advance License schemes

Document Requirements