2021 Biomass Thermal Summit Overview of the Biomass Thermal Industry in 2021 Peter Thompson Deputy Director May 6, 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2021 Biomass Thermal SummitOverview of the

Biomass Thermal Industry in 2021

Peter ThompsonDeputy Director

May 6, 2021

2021 Biomass Thermal Summit Sponsors

Mission:

The Biomass Thermal Energy Council (BTEC) advances the sustainable use of wood and agricultural biomass for clean, efficient heat and combined heat and power to meet America’s energy needs and strengthen local economies.

Focus Areas:

• Policy and Government Affairs• Technical and Regulatory Affairs• Education and Outreach

About BTEC

Upcoming SessionsEvery Thursday at 1:00 PM ET

May 13

• The Environmental and Carbon Benefits of Biomass Energy

May 20

• Expansion of Wood Heating Tax Credits to Business Applications

May 27

• Impact and potential of the Residential Wood Heating Tax Credit

June 3

• The Successes and Lessons from the Community Wood Energy and Wood Innovations Program

June 10

• Expansion of the EPA Renewable Fuel Standard to Thermal Energy and Wood Fuel

Geographic Variances for Renewables Especially Biomass Feedstocks

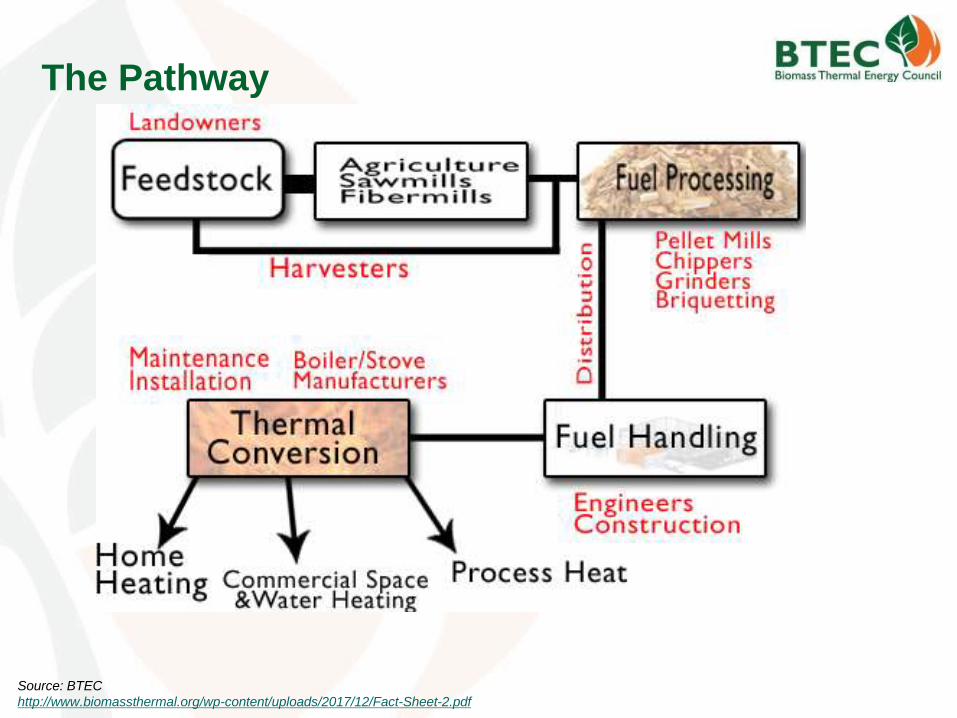

The Pathway

Source: BTEC

http://www.biomassthermal.org/wp-content/uploads/2017/12/Fact-Sheet-2.pdf

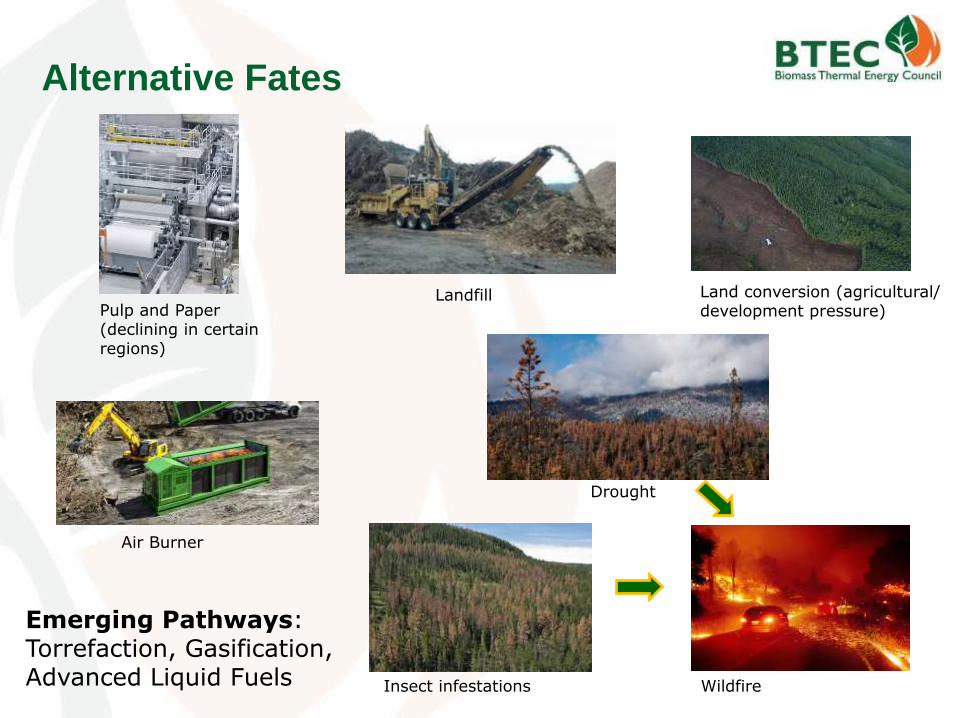

Alternative Fates

Pulp and Paper (declining in certain regions)

Insect infestations

Land conversion (agricultural/development pressure)

Drought

Landfill

Wildfire

Emerging Pathways:Torrefaction, Gasification, Advanced Liquid Fuels

Air Burner

Approximate Size of U.S. Biomass Thermal

Industry• 12.5 million residences use biomass as primary or

secondary source in space heating

• 3.5 million residences heating with biomass primarily

• In 2019,wood energy accounted for 4.4% of residential sector end-use energy consumption and 2.5% of total residential energy consumption

• Over 11,000 Commercial/Industrial Boilers

• Over 500 biomass CHP plants

Source: U.S. Census Data

Source: U.S. Energy Information Administration

Residential Scale

Primarily cord wood and pellets

Stoves, boilers, furnaces

Business-Scale

Office buildings, hospitals, universities, apartment complexes

Pellets on smaller systems; chips on larger systems

Combined Heat and Power

Industrial-Scale

Large scale heating (>5 MMBTU)

Industrial process heat, e.g. forest products, food processing

Combined heat and power (CHP) production

Benefits of Wood Energy

• Helps re-establish markets for low value wood

• Private sector: Allows for forest owners to make forest management

more profitable while reducing wildfire threat

• Public Sector: Wildfire suppression, forest health and management

• Increase rural economic development, job creation, and energy savings.

• Private forests support over 2.4 million rural jobs.

• Cost savings of nearly 50% in recent winters compared to heating oil.

The Key Barriers for Industry

1. Biomass heating equipment (residential, commercial, industrial) have initial high capital costs (at low volume) compared to fossil fuel heating systems (at high volume).

2. Forests and low-value wood requires markets to remain forests. If there is no economic value, forest face land conversion pressure.

3. Comprehensive carbon accounting and pricing for all energy options.

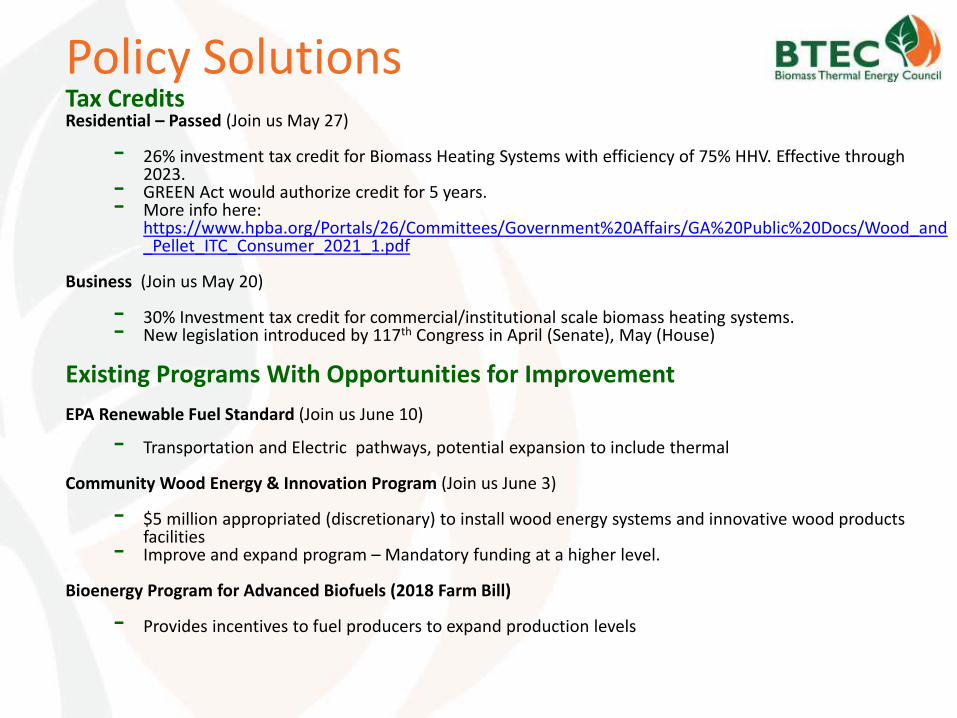

Tax CreditsResidential – Passed (Join us May 27)

- 26% investment tax credit for Biomass Heating Systems with efficiency of 75% HHV. Effective through 2023.- GREEN Act would authorize credit for 5 years. - More info here: https://www.hpba.org/Portals/26/Committees/Government%20Affairs/GA%20Public%20Docs/Wood_and_Pellet_ITC_Consumer_2021_1.pdf

Business (Join us May 20)

- 30% Investment tax credit for commercial/institutional scale biomass heating systems. - New legislation introduced by 117th Congress in April (Senate), May (House)

Existing Programs With Opportunities for Improvement

EPA Renewable Fuel Standard (Join us June 10)

- Transportation and Electric pathways, potential expansion to include thermal

Community Wood Energy & Innovation Program (Join us June 3)

- $5 million appropriated (discretionary) to install wood energy systems and innovative wood products facilities- Improve and expand program – Mandatory funding at a higher level.

Bioenergy Program for Advanced Biofuels (2018 Farm Bill)

- Provides incentives to fuel producers to expand production levels

Policy Solutions

Peter ThompsonDeputy Director

[email protected] x302

Join Us!Biomassthermal.org

Thanks for your attention!

Q&A Session

The Environmental and Carbon Benefits of Biomass Energy

Keynote Presentation: Robert Malmsheimer, PhD, JD, Professor of Forest Policy and Law, The Department of Sustainable Resources Management, SUNY ESF

Moderator: Daniel Bresette, Executive Director, Environmental and Energy Study Institute (EESI)

Ben Larson, Forest Conservation Director, Ruffed Grouse Society

David Publicover, Senior Staff Scientist/Assistant Director of Research, Appalachian Mountain Club

Sheri Smith, Regional Entomologist, Forest Service Pacific Southwest Region

Join Us Next Thursday, May 13 at 1:00 PM

Wood Heating in Northeastern US

BTEC Summit

Adam Sherman

May 6th, 2021

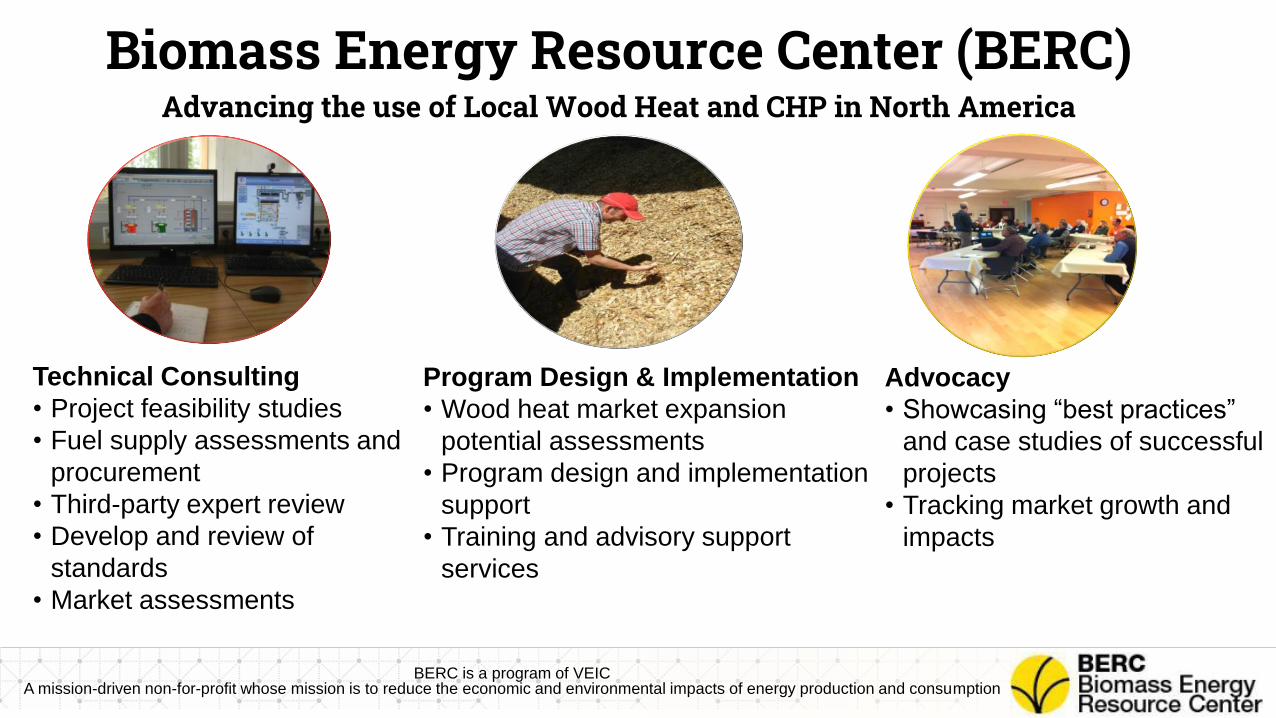

Biomass Energy Resource Center (BERC)Advancing the use of Local Wood Heat and CHP in North America

BERC is a program of VEICA mission-driven non-for-profit whose mission is to reduce the economic and environmental impacts of energy production and consumption

Technical Consulting

• Project feasibility studies

• Fuel supply assessments and

procurement

• Third-party expert review

• Develop and review of

standards

• Market assessments

Program Design & Implementation

• Wood heat market expansion

potential assessments

• Program design and implementation

support

• Training and advisory support

services

Advocacy

• Showcasing “best practices”

and case studies of successful

projects

• Tracking market growth and

impacts

Northeastern States Greenhouse Gas Goals

Maine10% GHG reduction by 2020

New Hampshire

20% GHG reduction by 2025

80% GHG reduction by 2050

Vermont

40% GHG reduction by 2030

80-95% GHG reduction by 2050

Connecticut

10% GHG reduction by 2020

80% GHG reduction by 2050

Massachusetts

25% GHG reduction by 2020

80% GHG reduction by 2050

Rhode Island

25% zero-energy new cars by 2025

State government:

10% reduction electric use by 2019

New York

40% GHG reduction by 2030

80% GHG reduction by 2050

Coal-free by 2020

Source: State websites

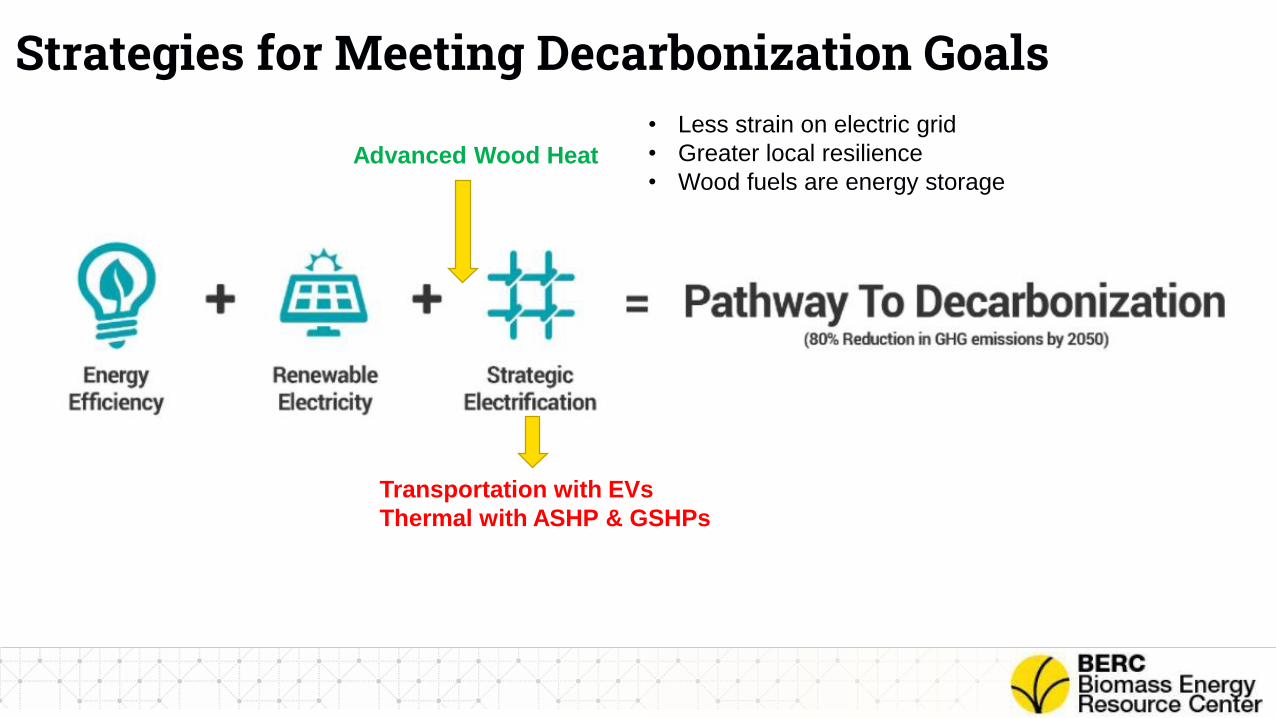

Strategies for Meeting Decarbonization Goals

Transportation with EVs

Thermal with ASHP & GSHPs

Advanced Wood Heat

• Less strain on electric grid

• Greater local resilience

• Wood fuels are energy storage

Factors for a Strong Wood Heat Market

Forestland

Area

Heating

Degree Days

Natural Gas

Pipeline Service

Advanced Wood Heating Market OverviewA

pp

lica

tio

nF

ue

lD

eliv

ery

Pro

du

ctio

n

Regional Pellet Mill Capacity

Bulk Pellet Fuel Distribution Investments

$-

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

202

0

201

9

201

8

201

7

201

6

201

5

201

4

201

3

201

2

201

1

201

0

200

9

200

8

200

7

200

6

200

5

200

4

200

3

200

2

200

1

$ p

er

MM

Btu

Northeastern US Average Heating Fuel Price Trends (2000-2020)

Propane

#2 Fuel Oil

Bulk Wood

Pellets

Traditional

Woodchips

11

Heating Fuel Cost Comparison

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

5 10 15 20 25 30 35 40 45

$/M

MB

tu

Outdoor Air Temperature

Typical ccASHP Wood pellets Propane Oil

Spectrum of Policies and Incentives Offered in NE NY VT NH ME MA

Flexible Boiler Regulations √ √

Sales Tax Exemption on Wood Heating Appliances √ √ Partial Partial

Sales Tax Exemption on Wood Fuel √ √ Residential only Residential only

State Income Tax Credit on Installed systems N/A

Residential & Commercial Boiler Incentives √ √ √ √ √

Thermal Renewable Portfolio Standards √ √ √

State Grants for Wood Heat Projects √ √ √ √ √

Government “Lead by Example” for Biomass

Thermal

√ √

System Benefits Charge on Heating Fuel Weatherization

only

Mandatory Renewable Energy Targets Applied to

Building Codes

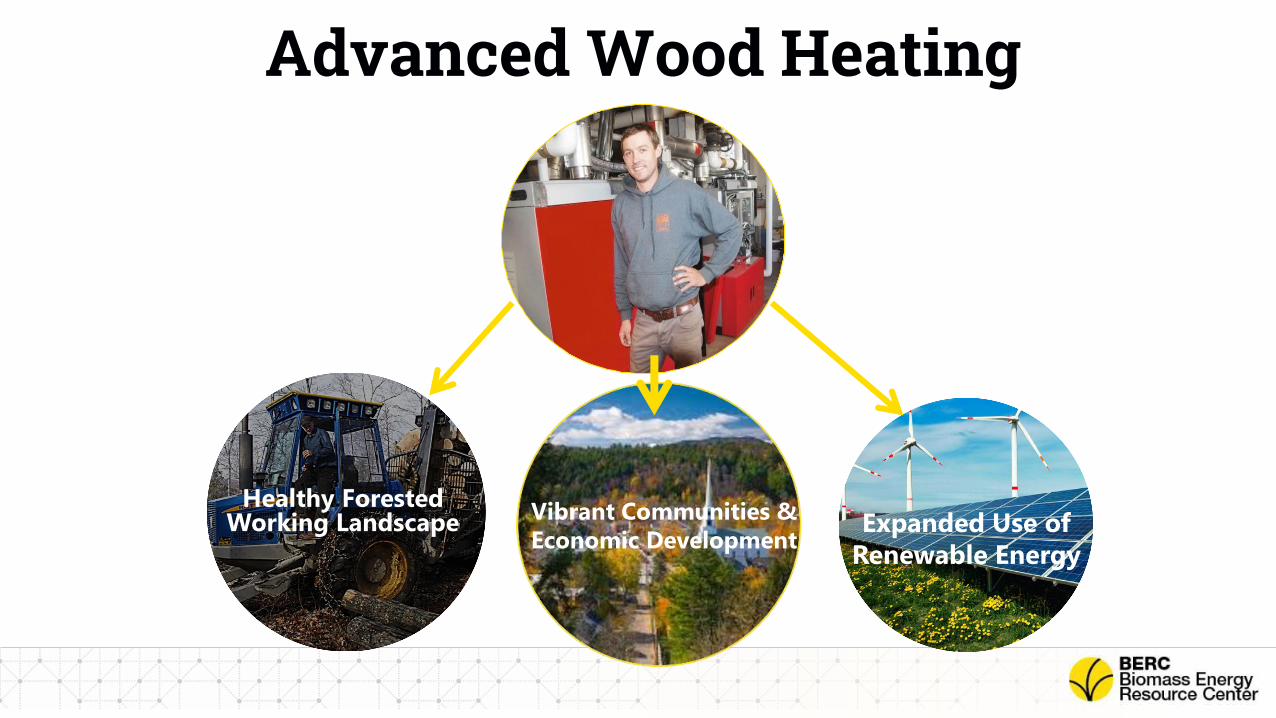

Healthy Forested Working Landscape Vibrant Communities &

Economic DevelopmentExpanded Use of

Renewable Energy

Advanced Wood Heating

Thanks!Adam Sherman

Senior Consultant

VEIC

www.veic.org

Placeholder for Extra Slides

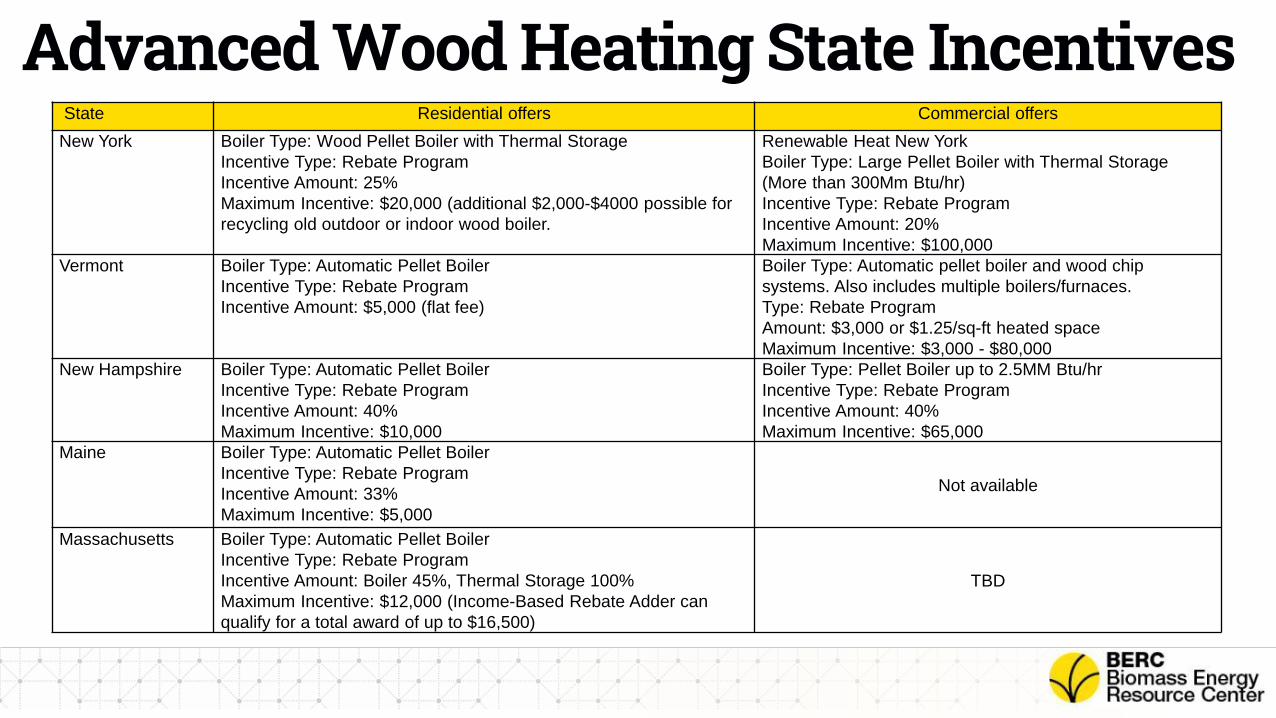

Advanced Wood Heating State IncentivesState Residential offers Commercial offers

New York Boiler Type: Wood Pellet Boiler with Thermal Storage

Incentive Type: Rebate Program

Incentive Amount: 25%

Maximum Incentive: $20,000 (additional $2,000-$4000 possible for

recycling old outdoor or indoor wood boiler.

Renewable Heat New York

Boiler Type: Large Pellet Boiler with Thermal Storage

(More than 300Mm Btu/hr)

Incentive Type: Rebate Program

Incentive Amount: 20%

Maximum Incentive: $100,000

Vermont Boiler Type: Automatic Pellet Boiler

Incentive Type: Rebate Program

Incentive Amount: $5,000 (flat fee)

Boiler Type: Automatic pellet boiler and wood chip

systems. Also includes multiple boilers/furnaces.

Type: Rebate Program

Amount: $3,000 or $1.25/sq-ft heated space

Maximum Incentive: $3,000 - $80,000

New Hampshire Boiler Type: Automatic Pellet Boiler

Incentive Type: Rebate Program

Incentive Amount: 40%

Maximum Incentive: $10,000

Boiler Type: Pellet Boiler up to 2.5MM Btu/hr

Incentive Type: Rebate Program

Incentive Amount: 40%

Maximum Incentive: $65,000

Maine Boiler Type: Automatic Pellet Boiler

Incentive Type: Rebate Program

Incentive Amount: 33%

Maximum Incentive: $5,000

Not available

Massachusetts Boiler Type: Automatic Pellet Boiler

Incentive Type: Rebate Program

Incentive Amount: Boiler 45%, Thermal Storage 100%

Maximum Incentive: $12,000 (Income-Based Rebate Adder can

qualify for a total award of up to $16,500)

TBD

LPG

Natural gas

Electricity

Heating Oil

(Fossil and

Bio)

Cordwood

Bagged Pellets

Bulk

Pellets Woodchips

2016 THERMAL FUEL MIX

LPG

Natural gas

Electricity

Heating Oil

(Fossil and

Bio)

Cordwood

Bagged Pellets

Bulk Pellets

Woodchips

Thermal

Efficiency

2030 THERMAL FUEL MIX

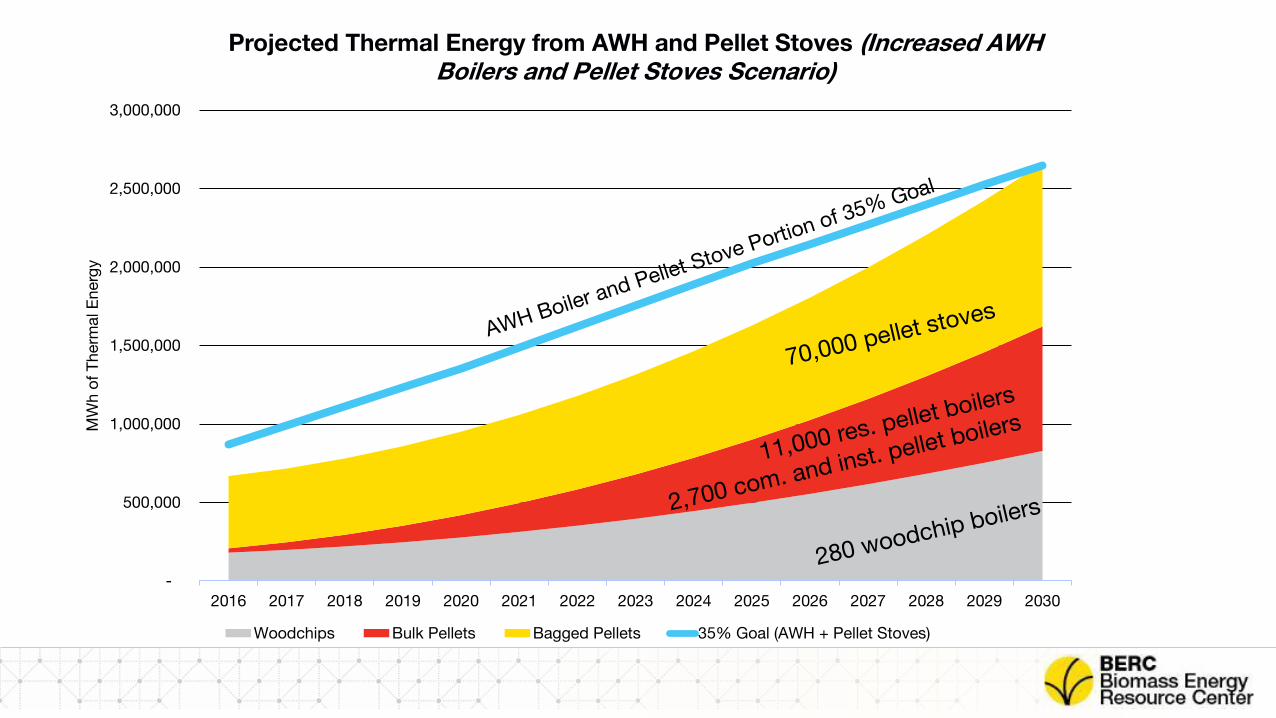

Vermont Energy Goal –35% of Thermal Energy from Wood Heat by 2030

~100 million gallons annually

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

MW

h o

f T

herm

al E

nerg

y

Projected Thermal Energy from AWH and Pellet Stoves (Increased AWH

Boilers and Pellet Stoves Scenario)

Woodchips Bulk Pellets Bagged Pellets 35% Goal (AWH + Pellet Stoves)

Annual Gallons

of Heating OilPopulation Gallons Oil/ Capita

Connecticut 473,000,000 3,500,000 135

Maine 263,000,000 1,300,000 202

Massachusetts 596,000,000 6,646,000 90

New Hampshire 137,000,000 1,320,000 104

New York 1,308,000,000 19,570,000 67

Pennsylvania 757,000,000 12,763,000 59

Rhode Island 131,000,000 1,050,000 125

Vermont 89,000,000 626,000 142

Total/Average 3,753,000,000 46,775,000 80

Regional Dependence on Oil for Heating

Source: Energy Information Administration (EIA) and 2015 US Census Data

Outlook for the 2021 Biomass Thermal Industry in the Midwest Region

BTEC Summit 2021

Presented by:Jeremy Mortl Messersmith ManufacturingBiomass Boiler [email protected] www.burnchips.com

The Vision

We propose that 15% of all thermal energy in the Midwest come from renewable energy sources with 10% derived from sustainably produced biomass by 2025. The remainder of this energy would come from solar thermal and geothermal sources. This shift in our sources for thermal energy will produce extraordinary economic, social and environmental benefits for the Midwest, which currently relies on fossil fuel for 97% of its thermal energy.

www.HeatingTheMidwest.Org

Midwest Opportunities – Public Sector

• Fuels for Schools Program• Many rural school districts

throughout the Midwest rely on propane or fuel oil to heat their facilities. Those heating dollars could be spent in the local community through biomass energy in schools.

• District Heating Systems• Municipalities• Hospitals• College Campuses• Community Centers

Midwest Opportunities – Private Sector

• Sawmills• Utilize residues from milling

operations (sawdust, shavings, chips) to heat buildings and dry kiln lumber.

• Greenhouses• Many greenhouses are

located in rural areas where natural gas is not available

Midwest Opportunities-Public K-12 Schools

Rib Lake Middle School• Rib Lake, Wisconsin

• Heated with a 4MMBTU/hrbiomass boiler system

• Hot water is distributed throughout buildings for heat

• Wood Chip fuel is locally sourced keeping fuel dollars in the local community

Midwest Opportunities-District Heating College Campus Example• Itasca Community College

• Grand Rapids, MN• 12-acre campus with 240,000

square feet of heated buildings• Heated with a 3MMBTU/hr

biomass boiler system

• Wood chip fuel is locally sourced

Midwest Opportunities-District HeatingCollege Campus • Modern Biomass Plant Building

at a college in New England• 26 MMBTU/hr Steam Boiler

heats the college campus and generates electricity.

• Boiler system ash is pneumatically transferred from the boiler room out to a sealed container

• Ash is used by local farmers as afertilizer in the soil

Midwest Opportunities-Sawmills

Roy Anderson Lumber Co.• 15 MMBTU/hr (450 HP)

• High Pressure Steam Boiler• Advanced boiler controls • Advanced Emissions Controls

• Electrical Generation + Heat for facility

• LP Steam used for drying lumber inon-site dry kilns

• Wood fuel is a bi-product of sawmill operations (green sawdust)

Midwest Opportunities-GreenhousesCreekside Aquaponics• Neenah, WI

• Aquaponics VegetableGreenhouse

• 3MMBTU/hr biomass boiler• Greenhouse, Processing

Building, Fish Tanks heated with locally sourced green wood chips

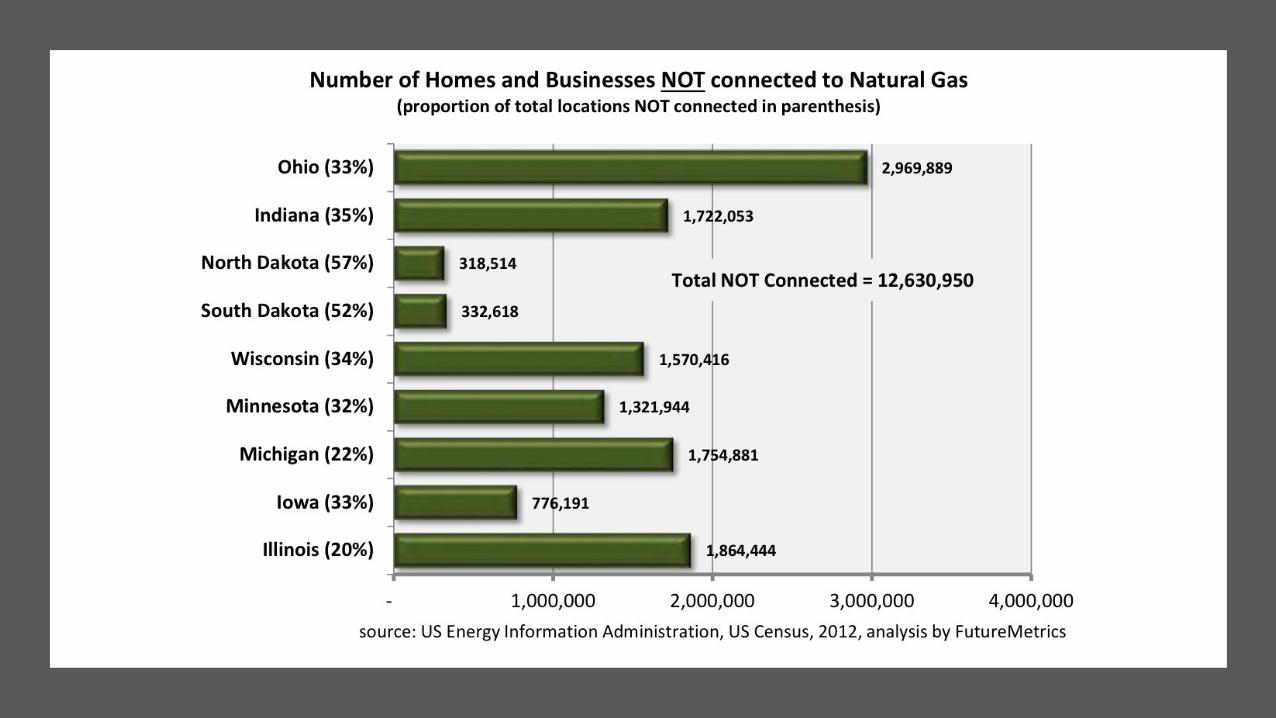

Sources of Woody Biomass in the Midwest

Forest Management

•Green wood chips from forest management•Chipped up low

grade timber and slash / tops from forest cuttings

•Chipped timber from municipal cuttings along roadways and power lines

Sawmill Residues

• Sawmill Residues •Green or dry

sawdust, planer shavings, chips

Wood ProductsManufacturing

•Wood Manufacturing Residues• Furniture

manufacturers•Hardwood flooring

manufacturers•Milling/Molding

manufacturers•Construction

material manufacturers (trusses, doors, windows, etc.)

Midwest Biomass Exchange www.mbioex.com

Biomass Trends in the Pacific Northwest

BTEC Biomass Thermal Summit

Dylan Kruse, Director of Government Affairs May 6, 2021

OUR FOCUS

Sustainable Northwest brings entrepreneurial solutions to natural resources challenges to keep lands healthy and provide economic and community benefits. We believe a healthy economy, environment, and community are indivisible, and that all are strengthened by wise partnerships, policies, and investments.

MISSION

Natural resource solutions that work for people and nature.

SUSTAINABLE

NORTHWEST

Oregon

∙21 thermal facilities

∙7+ CHP facilities

∙7 pellet production facilities

∙Use of bioenergy in production of lumber products

∙Mass timber manufacturing

∙Liquid biofuels (Red Rock)

∙Torrefaction (Restoration Fuels)

Washington

∙2 thermal facilities

∙Cogen facilities still generally operating

∙Use of bioenergy in production of lumber products

∙2 mass timber manufacturers

∙Still early stages of adopting institutional energy. Retrofitting is a challenge, as distribution systems are extremely degraded.

∙Looking at pellet production and export

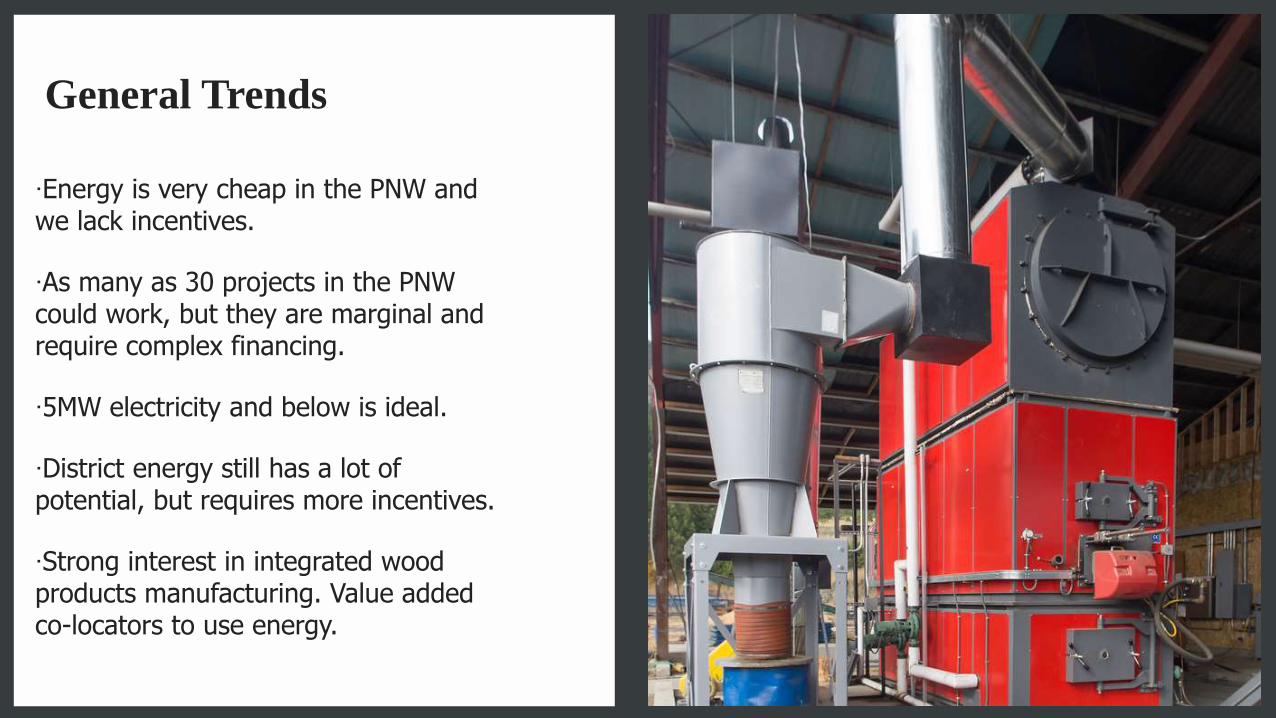

General Trends

∙Energy is very cheap in the PNW and we lack incentives.

∙As many as 30 projects in the PNW could work, but they are marginal and require complex financing.

∙5MW electricity and below is ideal.

∙District energy still has a lot of potential, but requires more incentives.

∙Strong interest in integrated wood products manufacturing. Value added co-locators to use energy.

Policy Focus

∙Energy independence used to be the driver. Carbon and broader forest and wildfire trends are a new emphasis.

∙Biomass in the context of climate change.

∙In California, CHP and microgrids are increasing drivers because of wildfire and public safety shutoffs.

∙BTU Act will be critical for the PNW, particularly the commercial component.

∙Every incentive will help in this market. A 30% credit would be HUGE and potential tipping point like we’ve seen with solar.

Biomass Trends in the Pacific Northwest

BTEC Biomass Thermal Summit – Questions and Discussion

Dylan Kruse, Director of Government Affairs May 6, 2021

Related Documents