Prod John De Ta John De Ta John Dee John Deere netwrap with TamaTec+™ technology Giving you MORE than ever, for LESS. logy Product Name Width Roll Length John Deere CoverEdge TamaTec+ 51 in. (130 cm) 12,100 ft. (3,700 m) John Deere CoverEdge TamaTec+ 67 in. (170 cm) 9,000 ft. (2,750 m) John Deere Edge to Edge TamaTec+ 48 in. (123 cm) 13,200 ft. (4,025 m) John Deere Edge to Edge TamaTec+ 64 in. (163 cm) 9,700 ft. (2,950 m) available at your local John Deere Dealer ASK YOUR JOHN DEERE DEALER ABOUT NEW WRAP! Tama USA Inc. Toll Free: 1-800-225-8946 Website: www.tama-usa.com 2017 U.S. forage statistics more than 15,000 thousand tons 10,000 to 15,000 thousand tons 5,000 to 10,000 thousand tons 2,000 to 5,000 thousand tons 0 to 2,000 thousand tons Total forage production Total forage production is represented by the total of alfalfa, other hay, silage and greenchop production. 2017 national forage review States that provided data to NASS were divided into the following regions: • Southwest: Arizona, California, Nevada, New Mexico, Oklahoma, Texas • East: Kentucky, New York, Ohio, Pennsylvania • Northwest: Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming • Midwest: Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin For market reports updated monthly, visit www.progressiveforage.com/news/hay-market-reports Alfalfa hay market trends (dollars per ton) Total corn silage production Total other hay production Total alfalfa hay production Total greenchop production more than 5,000 thousand tons 3,000 to 5,000 thousand tons 1,000 to 3,000 thousand tons 100 to 1,000 thousand tons 0 to 100 thousand tons more than 5,000 thousand tons 2,000 to 5,000 thousand tons 1,000 to 2,000 thousand tons 500 to 1,000 thousand tons 0 to 500 thousand tons more than 10,000 thousand tons 5,000 to 10,000 thousand tons 1,000 to 5,000 thousand tons 500 to 1,000 thousand tons 0 to 500 thousand tons more than 5,000 thousand tons 2,000 to 5,000 thousand tons 1,000 to 2,000 thousand tons 500 to 1,000 thousand tons 0 to 500 thousand tons Midwest (average) Northwest (average) $149 $166 $203 $127 Southwest (average) East (average) May Apr July June Sept Aug Nov Dec Oct Dec 2016 Mar Feb Jan 2017 $100 $120 $140 $160 $180 $200 $220 2017 Top 10 states Sorghum silage State ranking State Acreage (in thousand acres) State Yield (tons/acre) State Production (in thousand tons) 1 Kansas 85 Missouri 19.0 Kansas 1,105 2 Texas 65 Oklahoma 18.0 Texas 975 3 South Dakota 37 Arkansas 16.0 South Dakota 407 4 Colorado 25 Colorado 15.0 Colorado 375 5 Nebraska 22 Texas 15.0 Nebraska 220 6 New Mexico 17 Georgia 13.0 Oklahoma 216 7 Oklahoma 12 Kansas 13.0 New Mexico 187 8 Georgia 8 Illinois 12.0 Georgia 104 9 Missouri 5 Louisiana 12.0 Missouri 95 10 North Carolina 4 New Mexico 11.0 North Carolina 40 Source: USDA National Ag Statistics Service 2017 annual Crop Production report, Jan. 2018 Prices With U.S. average hay prices ending 2016 at 70-month lows, presumably there was nowhere to go but up. However, it took until spring for prices to thaw out. Significant revisions in final USDA 2016 alfalfa and hay acreage estimates, along with an 11 percent acreage reduction in new alfalfa seedings, did nothing to boost prices as the new year began. A pickup in buyer interest in early February also failed to spring life into hay markets, and alfalfa hay prices continued lower in January and February 2018. Alfalfa hay prices started to improve in March, with U.S. averages rising about $31 per ton between January and May to reach $157 per ton, before plateauing in June and settling in a narrow range through November. In contrast, 2017 average prices for other hay peaked in April at $131 per ton and then settled back to prices similar to the end of 2016. As the harvest season ended and the 2017 hay crop was tucked away in sheds and stacks, growing-season factors took a back seat to domestic and foreign demand in driving hay prices. The October 2017 U.S. average price paid to alfalfa hay producers at the farm level was $152 per ton, up $3 from September and $17 more than a year earlier. The October 2017 U.S. average price for other hay moved off a 12-month low and was estimated at $118 per ton, up $5 per ton from September. Weather and drought Widespread winter precipitation improved moisture conditions in many hay- producing areas throughout the U.S., providing optimism for the 2017 growing season. The USDA’s World Agricultural Outlook Board reported about 24 percent of U.S. hay acreage was located in areas experiencing drought at the end of 2016 and that dropped to about 19 to 20 percent in January and February 2018. California’s drought area had shrunk substantially, but Oklahoma, Missouri and Colorado showed a growing presence of drought. Spring also revealed signs of significant alfalfa winterkill losses in southern South Dakota, central Minnesota and southwestern Wisconsin. Fields most affected were older fields and/or those where a late fall cutting was taken. Excessive moisture levels were also causing grower challenges elsewhere. In California, common leaf spot was evident in alfalfa fields in early spring. Late August and early September threw more curveballs at hay growers, with hurricanes hitting the Gulf Coast and Southeast, fire and smoke impacting haying activity and hay quality in the Northwest, and the drought lingering in the Northern Plains. Officials in the Northern Plains prepared a hay lottery, with livestock producers from Montana, North Dakota and South Dakota eligible to receive emergency hay. The nationwide percentage of hay area facing drought was up slightly by October, and the situation worsened during the final quarter of 2017, to 30 percent of U.S. hay-producing acreage as 2018 began. Exports 2017 continued a three-year run in which alfalfa hay exports rose from the year before. By November, 2017 alfalfa hay export sales topped 2.4 million metric tons (MT) and were just short of a new record annual high, with one month still to go on the export calendar. China was the wild card, and was frequently the top destination for U.S. alfalfa hay each month. Through the first 11 months of the year, China had purchased about 44 percent of all U.S. alfalfa exports. Japan was the second-leading market, and Saudi Arabia, nearing its goal of eliminating domestic hay production due to limits on water usage, continued expanded alfalfa production and exports from Arizona. Despite an unfavorable exchange rate and strong domestic harvest, Japan remained the leading foreign market for other hay. In very short supply of straws and timothy, South Korea was also a leading purchaser of other hay during the year. Production and inventories Notable changes in acres and tonnage produced unfolded across all forage products in 2017. • All dry hay: 2017 production was estimated at 131 million tons, down 3 percent from the revised 2016 total. Area harvested was estimated at 53.8 million acres, up 1 percent from 2016. The average yield, at 2.44 tons per acre, was down 0.08 ton from the previous year. • Alfalfa and alfalfa mixtures: Production in 2017 was estimated at 55.1 million tons, down 5 percent from the 2016 total. Harvested area, at 16.6 million acres, was 2 percent below the previous year. Average yield was estimated at 3.32 tons per acre, down 0.13 ton from 2016. • Other hay: Production in 2017 totaled 76.4 million tons, down less than 1 percent from the revised 2016 total. Harvested area, at 37.2 million acres, was up 2 percent from the previous year. Average yield was estimated at 2.05 tons per acre, down 0.05 ton from the previous year’s revised record high. • Total forage: In 2017, 17 states were included in the USDA forage estimation program, which measures annual production of forage crops. Haylage and greenchop production was converted to 13 percent moisture and combined with dry hay production to derive the total forage production. The 17-state total for all forage production was 86.7 million tons. Of this total, 44 million tons were produced from alfalfa and alfalfa mixtures. The total 2017 all haylage and greenchop production for the 17 states was 30.5 million tons, of which 20 million tons were from alfalfa and alfalfa mixtures. • Corn silage: Production was estimated at 128.4 million tons for 2017, up 2 percent from 2016 and up slightly from the previous high set in 2014. Area harvested for silage was estimated at 6.43 million acres, up 4 percent from a year ago and the most acreage devoted to corn silage since 2012. Average yield was estimated at 19.9 tons per acre, down 0.4 ton from 2016 and the lowest average since 2013. • Sorghum silage: Production was estimated at 3.77 million tons, down 10 percent from 2016 and the smallest harvest since 2011. Area harvested for silage was estimated at 284,000 acres, down 5 percent from the previous year and also the smallest harvested area since 2011. Silage yield averaged 13.3 tons per acre, down 0.7 tons per acre from 2016. One footnote: Data for Arizona, the fourth-largest sorghum silage-producing state in 2015, was discontinued for 2016-17. • New seedings of alfalfa and alfalfa mixtures: At 2.21 million acres, acreage newly seeded to alfalfa in 2017 were down about 3 percent (58,000 acres) from 2016 and the lowest acreage devoted to new seeding since USDA started releasing estimates two decades ago. New alfalfa seeding routinely surpassed 3 million acres per year between 1997 and 2006.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

John Deere netwrap with TamaTec+™ technologyGiving you MORE than ever, for LESS.

• MORE footage – LESS cost per bale• MORE bales per roll – LESS downtime• MORE baling productivity

P.O. Box 506, Highway 61-151 South, Dubuque, IOWA 52004-0506Phone: (563) 583-3035 Fax: (563) 583-3531 TOLL FREE: 1-800-225-8946Email: [email protected] www.ambraco.com

Product Name Width Roll Length

John Deere CoverEdge TamaTec+ 51 in. (130 cm) 12,100 ft. (3,700 m)

John Deere CoverEdge TamaTec+ 67 in. (170 cm) 9,000 ft. (2,750 m)

John Deere Edge to Edge TamaTec+ 48 in. (123 cm) 13,200 ft. (4,025 m)

John Deere Edge to Edge TamaTec+ 64 in. (163 cm) 9,700 ft. (2,950 m)

available at your local John Deere Dealer

John Deere netwrap with TamaTec+™ technologyGiving you MORE than ever, for LESS.

• MORE footage – LESS cost per bale• MORE bales per roll – LESS downtime• MORE baling productivity

P.O. Box 506, Highway 61-151 South, Dubuque, IOWA 52004-0506Phone: (563) 583-3035 Fax: (563) 583-3531 TOLL FREE: 1-800-225-8946Email: [email protected] www.ambraco.com

Product Name Width Roll Length

John Deere CoverEdge TamaTec+ 51 in. (130 cm) 12,100 ft. (3,700 m)

John Deere CoverEdge TamaTec+ 67 in. (170 cm) 9,000 ft. (2,750 m)

John Deere Edge to Edge TamaTec+ 48 in. (123 cm) 13,200 ft. (4,025 m)

John Deere Edge to Edge TamaTec+ 64 in. (163 cm) 9,700 ft. (2,950 m)

available at your local John Deere Dealer

John Deere netwrap with TamaTec+™ technologyGiving you MORE than ever, for LESS.

• MORE footage – LESS cost per bale• MORE bales per roll – LESS downtime• MORE baling productivity

P.O. Box 506, Highway 61-151 South, Dubuque, IOWA 52004-0506Phone: (563) 583-3035 Fax: (563) 583-3531 TOLL FREE: 1-800-225-8946Email: [email protected] www.ambraco.com

Product Name Width Roll Length

John Deere CoverEdge TamaTec+ 51 in. (130 cm) 12,100 ft. (3,700 m)

John Deere CoverEdge TamaTec+ 67 in. (170 cm) 9,000 ft. (2,750 m)

John Deere Edge to Edge TamaTec+ 48 in. (123 cm) 13,200 ft. (4,025 m)

John Deere Edge to Edge TamaTec+ 64 in. (163 cm) 9,700 ft. (2,950 m)

available at your local John Deere Dealer

ASK YOUR JOHN DEERE DEALER ABOUT NEW WRAP!

Tama USA Inc.Toll Free: 1-800-225-8946Website: www.tama-usa.com

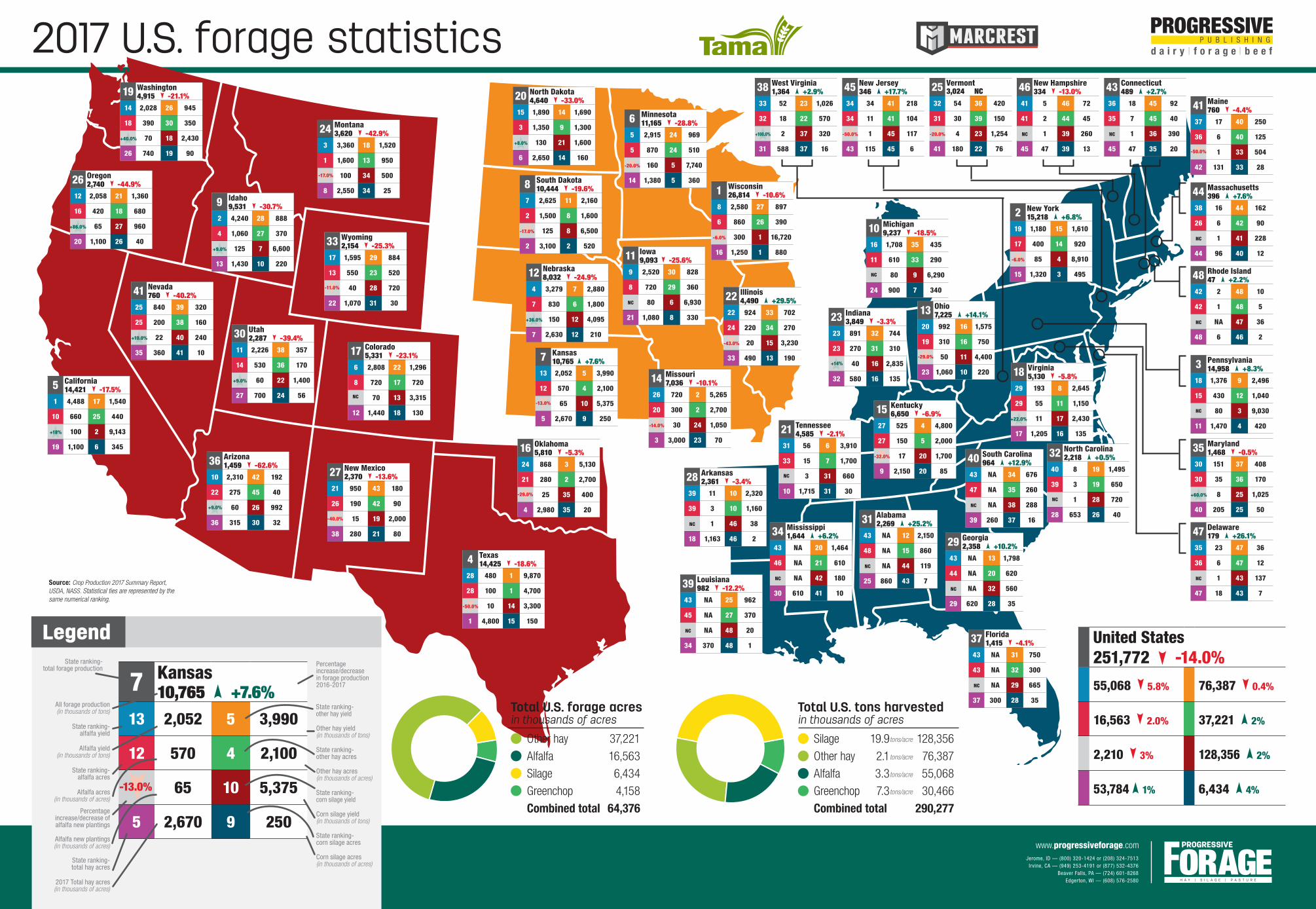

2017 U.S. forage statistics

more than 15,000 thousand tons

10,000 to 15,000 thousand tons

5,000 to 10,000 thousand tons

2,000 to 5,000 thousand tons

0 to 2,000 thousand tons

Total forage production

Total forage production is represented by the total of alfalfa, other hay, silage and greenchop production.

2017 national forage review

States that provided data to NASS were divided into the following regions:• Southwest: Arizona, California, Nevada, New Mexico, Oklahoma, Texas• East: Kentucky, New York, Ohio, Pennsylvania• Northwest: Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming• Midwest: Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin

For market reports updated monthly, visit www.progressiveforage.com/news/hay-market-reports

Alfalfa hay market trends (dollars per ton)Total corn silage production

Total other hay production

Total alfalfa hay production

Total greenchop production

more than 5,000 thousand tons3,000 to 5,000 thousand tons1,000 to 3,000 thousand tons100 to 1,000 thousand tons0 to 100 thousand tons

more than 5,000 thousand tons2,000 to 5,000 thousand tons1,000 to 2,000 thousand tons500 to 1,000 thousand tons0 to 500 thousand tons

more than 10,000 thousand tons5,000 to 10,000 thousand tons1,000 to 5,000 thousand tons500 to 1,000 thousand tons0 to 500 thousand tons

more than 5,000 thousand tons2,000 to 5,000 thousand tons1,000 to 2,000 thousand tons500 to 1,000 thousand tons0 to 500 thousand tons

Midwest(average)

Northwest(average)

$149

$166

$203

$127

Southwest (average)

East (average)

MayApr JulyJune SeptAug Nov DecOctDec2016

MarFebJan2017

$100

$120

$140

$160

$180

$200

$220

2017 Top 10 statesSorghum silage

State ranking

StateAcreage

(in thousand acres)

StateYield

(tons/acre)State

Production (in thousand

tons)

1 Kansas 85 Missouri 19.0 Kansas 1,105

2 Texas 65 Oklahoma 18.0 Texas 975

3 South Dakota 37 Arkansas 16.0 South Dakota 407

4 Colorado 25 Colorado 15.0 Colorado 375

5 Nebraska 22 Texas 15.0 Nebraska 220

6 New Mexico 17 Georgia 13.0 Oklahoma 216

7 Oklahoma 12 Kansas 13.0 New Mexico 187

8 Georgia 8 Illinois 12.0 Georgia 104

9 Missouri 5 Louisiana 12.0 Missouri 95

10 North Carolina 4 New Mexico 11.0 North Carolina 40

Source: USDA National Ag Statistics Service 2017 annual Crop Production report, Jan. 2018

PricesWith U.S. average hay prices ending 2016 at 70-month lows, presumably there

was nowhere to go but up. However, it took until spring for prices to thaw out.Significant revisions in final USDA 2016 alfalfa and hay acreage estimates, along

with an 11 percent acreage reduction in new alfalfa seedings, did nothing to boost prices as the new year began. A pickup in buyer interest in early February also failed to spring life into hay markets, and alfalfa hay prices continued lower in January and February 2018.

Alfalfa hay prices started to improve in March, with U.S. averages rising about $31 per ton between January and May to reach $157 per ton, before plateauing in June and settling in a narrow range through November.

In contrast, 2017 average prices for other hay peaked in April at $131 per ton and then settled back to prices similar to the end of 2016.

As the harvest season ended and the 2017 hay crop was tucked away in sheds and stacks, growing-season factors took a back seat to domestic and foreign demand in driving hay prices. The October 2017 U.S. average price paid to alfalfa hay producers at the farm level was $152 per ton, up $3 from September and $17 more than a year earlier. The October 2017 U.S. average price for other hay moved off a 12-month low and was estimated at $118 per ton, up $5 per ton from September.

Weather and droughtWidespread winter precipitation improved moisture conditions in many hay-

producing areas throughout the U.S., providing optimism for the 2017 growing season.

The USDA’s World Agricultural Outlook Board reported about 24 percent of U.S. hay acreage was located in areas experiencing drought at the end of 2016 and that dropped to about 19 to 20 percent in January and February 2018. California’s drought area had shrunk substantially, but Oklahoma, Missouri and Colorado showed a growing presence of drought.

Spring also revealed signs of significant alfalfa winterkill losses in southern South Dakota, central Minnesota and southwestern Wisconsin. Fields most affected were older fields and/or those where a late fall cutting was taken.

Excessive moisture levels were also causing grower challenges elsewhere. In California, common leaf spot was evident in alfalfa fields in early spring. Late August and early September threw more curveballs at hay growers, with hurricanes hitting the Gulf Coast and Southeast, fire and smoke impacting haying activity and hay quality in the Northwest, and the drought lingering in the Northern Plains. Officials in the Northern Plains prepared a hay lottery, with livestock producers from Montana, North Dakota and South Dakota eligible to receive emergency hay.

The nationwide percentage of hay area facing drought was up slightly by October, and the situation worsened during the final quarter of 2017, to 30 percent of U.S. hay-producing acreage as 2018 began.

Exports2017 continued a three-year run in which alfalfa hay exports rose from the year

before. By November, 2017 alfalfa hay export sales topped 2.4 million metric tons (MT) and were just short of a new record annual high, with one month still to go on the export calendar.

China was the wild card, and was frequently the top destination for U.S. alfalfa hay each month. Through the first 11 months of the year, China had purchased about 44 percent of all U.S. alfalfa exports. Japan was the second-leading market, and Saudi Arabia, nearing its goal of eliminating domestic hay production due to limits on water usage, continued expanded alfalfa production and exports from Arizona.

Despite an unfavorable exchange rate and strong domestic harvest, Japan remained the leading foreign market for other hay. In very short supply of straws and timothy, South Korea was also a leading purchaser of other hay during the year.

Production and inventoriesNotable changes in acres and tonnage produced unfolded across all forage

products in 2017.

• All dry hay: 2017 production was estimated at 131 million tons, down 3 percent from the revised 2016 total. Area harvested was estimated at 53.8 million acres, up 1 percent from 2016. The average yield, at 2.44 tons per acre, was down 0.08 ton from the previous year.

• Alfalfa and alfalfa mixtures: Production in 2017 was estimated at 55.1 million tons, down 5 percent from the 2016 total. Harvested area, at 16.6 million acres, was 2 percent below the previous year. Average yield was estimated at 3.32 tons per acre, down 0.13 ton from 2016.

• Other hay: Production in 2017 totaled 76.4 million tons, down less than 1 percent from the revised 2016 total. Harvested area, at 37.2 million acres, was up 2 percent from the previous year. Average yield was estimated at 2.05 tons per acre, down 0.05 ton from the previous year’s revised record high.

• Total forage: In 2017, 17 states were included in the USDA forage estimation program, which measures annual production of forage crops. Haylage and greenchop production was converted to 13 percent moisture and combined with dry hay production to derive the total forage production.

The 17-state total for all forage production was 86.7 million tons. Of this total, 44 million tons were produced from alfalfa and alfalfa mixtures. The total 2017 all haylage and greenchop production for the 17 states was 30.5 million tons, of which 20 million tons were from alfalfa and alfalfa mixtures.

• Corn silage: Production was estimated at 128.4 million tons for 2017, up 2 percent from 2016 and up slightly from the previous high set in 2014. Area harvested for silage was estimated at 6.43 million acres, up 4 percent from a year ago and the most acreage devoted to corn silage since 2012. Average yield was estimated at 19.9 tons per acre, down 0.4 ton from 2016 and the lowest average since 2013.

• Sorghum silage: Production was estimated at 3.77 million tons, down 10 percent from 2016 and the smallest harvest since 2011. Area harvested for silage was estimated at 284,000 acres, down 5 percent from the previous year and also the smallest harvested area since 2011. Silage yield averaged 13.3 tons per acre, down 0.7 tons per acre from 2016. One footnote: Data for Arizona, the fourth-largest sorghum silage-producing state in 2015, was discontinued for 2016-17.

• New seedings of alfalfa and alfalfa mixtures: At 2.21 million acres, acreage newly seeded to alfalfa in 2017 were down about 3 percent (58,000 acres) from 2016 and the lowest acreage devoted to new seeding since USDA started releasing estimates two decades ago. New alfalfa seeding routinely surpassed 3 million acres per year between 1997 and 2006.

2017 U.S. forage statistics

State ranking- total forage production

Legend

Jerome, ID — (800) 320-1424 or (208) 324-7513 Irvine, CA — (949) 253-4191 or (877) 532-4376

Beaver Falls, PA — (724) 601-8268Edgerton, WI — (608) 576-2580

United States251,772 -14.0%

55,068 5.8% 76,387 0.4%

16,563 2.0% 37,221 2%

2,210 3% 128,356 2%

53,784 1% 6,434 4%

7 Kansas10,765 +7.6%

13 2,052 5 3,990

12 570 4 2,100

65 10 5,375

5 2,670 9 250

-13.0%

Source: Crop Production 2017 Summary Report, USDA, NASS. Statistical ties are represented by the same numerical ranking.

Total U.S. forage acresin thousands of acres in thousands of acres

Total U.S. tons harvestedAll forage production(in thousands of tons)

State ranking- alfalfa yield

State ranking-alfalfa acres

Percentage increase/decrease of alfalfa new plantings

State ranking-total hay acres

Alfalfa yield (in thousands of tons)

Alfalfa acres(in thousands of acres)

Alfalfa new plantings(in thousands of acres)

2017 Total hay acres(in thousands of acres)

Percentage increase/decrease in forage production 2016-2017

State ranking-other hay yield

State ranking-corn silage yield

Other hay yield(in thousands of tons)

Other hay acres(in thousands of acres)

Corn silage acres(in thousands of acres)

Corn silage yield(in thousands of tons)

State ranking-other hay acres

State ranking-corn silage acres

41 Nevada760 -40.2%

25 840 39 320

25 200 38 160

22 40 240

35 360 41 10

+10.0%

4 Texas14,425 -18.6%

28 480 1 9,870

28 100 1 4,700

10 14 3,300

1 4,800 15 150

-50.0%

25 Vermont3,024 NC

32 54 36 420

31 30 39 150

4 23 1,254

41 180 22 76

-20.0%

38 West Virginia1,364 +2.9%

33 52 23 1,026

32 18 22 570

2 37 320

31 588 37 16

+100.0%

45 New Jersey346 +17.7%

34 34 41 218

34 11 41 104

1 45 117

43 115 45 6

-50.0%

46 New Hampshire334 -13.0%

41 5 46 72

41 2 44 45

1 39 260

45 47 39 13

NC

41 Maine760 -4.4%

37 17 40 250

36 6 40 125

1 33 504

42 131 33 28

3 Pennsylvania14,958 +8.3%

18 1,376 9 2,496

15 430 12 1,040

80 3 9,030

11 1,470 4 420

47 Delaware179 +26.1%

35 23 47 36

36 6 47 12

1 43 137

47 18 43 7

NC

18 Virginia5,130 -5.8%

29 193 8 2,645

29 55 11 1,150

11 17 2,430

17 1,205 16 135

+22.0%15 Kentucky

6,650 -6.9%27 525 4 4,800

27 150 5 2,000

17 20 1,700

9 2,150 20 85

-32.0%

39 Louisiana982 -12.2%

43 NA 25 962

45 NA 27 370

NA 48 20

34 370 48 1

NC

28 Arkansas2,361 -3.4%

39 11 10 2,320

39 3 10 1,160

1 46 38

18 1,163 46 2

NC

8 South Dakota10,444 -19.6%

7 2,625 11 2,160

2 1,500 8 1,600

125 8 6,500

2 3,100 2 520

-17.0%

30 Utah2,287 -39.4%

11 2,226 38 357

14 530 36 170

60 22 1,400

27 700 24 56

+9.0%

33 Wyoming2,154 -25.3%

17 1,595 29 884

13 550 23 520

40 28 720

22 1,070 31 30

24 Montana3,620 -42.9%

3 3,360 18 1,520

1 1,600 13 950

100 34 500

8 2,550 34 25

9 Idaho9,531 -30.7%

2 4,240 28 888

4 1,060 27 370

125 7 6,600

13 1,430 10 220

+9.0%

26 Oregon2,740 -44.9%

12 2,058 21 1,360

16 420 18 680

65 27 960

20 1,100 26 40

+86.0%

5 California14,421 -17.5%

1 4,488 17 1,540

10 660 25 440

100 2 9,143

19 1,100 6 345

+18%

17 Colorado5,331 -23.1%

6 2,808 22 1,296

8 720 17 720

70 13 3,315

12 1,440 18 130

2 New York15,218 +6.8%

19 1,180 15 1,610

17 400 14 920

85 4 8,910

15 1,320 3 495

-6.0%

43 Connecticut489 +2.7%

36 18 45 92

35 7 45 40

1 36 390

45 47 35 20

NC

44 Massachusetts396 +7.6%

38 16 44 162

26 6 42 90

1 41 228

44 96 40 12

NC

48 Rhode Island47 +2.2%

42 2 48 10

42 1 48 5

NA 47 36

48 6 46 2

NC

35 Maryland1,468 -0.5%

30 151 37 408

30 35 36 170

8 25 1,025

40 205 25 50

+60.0%

32 North Carolina2,218 +0.5%

40 8 19 1,495

39 3 19 650

1 28 720

28 653 26 40

34 Mississippi1,644 +6.2%

43 NA 20 1,464

46 NA 21 610

NA 42 180

30 610 41 10

NC

22 Illinois4,490 +29.5%

22 924 33 702

24 220 34 270

20 15 3,230

33 490 13 190

-43.0%

31 Alabama2,269 +25.2%

43 NA 12 2,150

48 NA 15 860

NA 44 119

25 860 43 7

NC

29 Georgia2,358 +10.2%

43 NA 13 1,798

44 NA 20 620

NA 32 560

29 620 28 35

NC

40 South Carolina964 +12.9%

43 NA 34 676

47 NA 35 260

NA 38 288

39 260 37 16

NC

37 Florida1,415 -4.1%

43 NA 31 750

43 NA 32 300

NA 29 665

37 300 28 35

NC

13 Ohio7,225 +14.1%

20 992 16 1,575

19 310 16 750

50 11 4,400

23 1,060 10 220

-29.0%

10 Michigan9,237 -18.5%

16 1,708 35 435

11 610 33 290

80 9 6,290

24 900 7 340

1 Wisconsin26,814 -10.6%

8 2,580 27 897

6 860 26 390

300 1 16,720

16 1,250 1 880

-6.0%

14 Missouri7,036 -10.1%

26 720 2 5,265

20 300 2 2,700

30 24 1,050

3 3,000 23 70

-14.0%

6 Minnesota11,165 -28.8%

5 2,915 24 969

5 870 24 510

160 5 7,740

14 1,380 5 360

-20.0%

12 Nebraska8,032 -24.9%

4 3,279 7 2,880

7 830 6 1,800

150 12 4,095

7 2,630 12 210

+36.0%

20 North Dakota4,640 -33.0%

15 1,890 14 1,690

3 1,350 9 1,300

130 21 1,600

6 2,650 14 160

+8.0%

19 Washington4,915 -21.1%

14 2,028 26 945

18 390 30 350

70 18 2,430

26 740 19 90

+40.0%

Other hay 37,221

Alfalfa 16,563

Silage 6,434

Greenchop 4,158

Combined total 64,376

Silage 19.9 128,356

Other hay 2.1 76,387

Alfalfa 3.3 55,068

Greenchop 7.3 30,466

Combined total 290,277

tons/acre

tons/acre

tons/acre

tons/acre

-17.0%

-11.0%

NC

36 Arizona1,459 -62.6%

10 2,310 42 192

22 275 45 40

60 26 992

36 315 30 32

+9.0%

27 New Mexico2,370 -13.6%

21 950 43 180

26 190 42 90

15 19 2,000

38 280 21 80

-40.0%

7 Kansas10,765 +7.6%

13 2,052 5 3,990

12 570 4 2,100

65 10 5,375

5 2,670 9 250

-13.0%

16 Oklahoma5,810 -5.3%

24 868 3 5,130

21 280 2 2,700

25 35 400

4 2,980 35 20

-29.0%

11 Iowa9,093 -25.6%

9 2,520 30 828

8 720 29 360

80 6 6,930

21 1,080 8 330

NC

-50.0%

NC

23 Indiana3,849 -3.3%

23 891 32 744

23 270 31 310

40 16 2,835

32 580 16 135

+14%

21 Tennessee4,585 -2.1%

31 56 6 3,910

33 15 7 1,700

3 31 660

10 1,715 31 30

NC

NC

NC

Related Documents