THE STATE OF SENIOR LIVING & SENIOR LIVING CAPITAL MARKETS 2017 2017 SENIOR LIVING SYMPOSIUM DAN HERMANN Head of Investment Banking Ziegler LISA MCCRACKEN Senior Vice President Ziegler KEITH ROBERTSON Managing Director Ziegler B.C. Ziegler and Company | Member of SIPC & FINRA PRESENTED BY: March 16, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE STATE OF SENIOR LIVING & SENIOR LIVING CAPITAL MARKETS 2017

2017 SENIOR LIVING SYMPOSIUM

DAN HERMANNHead of Investment BankingZiegler

LISA MCCRACKENSenior Vice PresidentZiegler

KEITH ROBERTSONManaging DirectorZiegler

B.C. Ziegler and Company | Member of SIPC & FINRA

PRESENTED BY:

March 16, 2017

2

Ziegler is one of the nation’s oldest and largest investment banking firms serving healthcare providers• Full service financial services firm• Founded in 1902 with a focus on

healthcare since 1928– Celebrated 115 years of service in 2017

– Over 270 professionals and support staff dedicated to serving our clients

• National presence, demonstrated execution expertise and broad-based experience

• Strong underwriting and sales & trading capabilities.

– Primary and secondary market efforts focused exclusively on muni sector

• Ziegler’s mission is to provide tailored financial solutions

• Ziegler’s goal is to be our client’s trusted advisor and partner

THE ZIEGLER COMPANIES, INC.

3

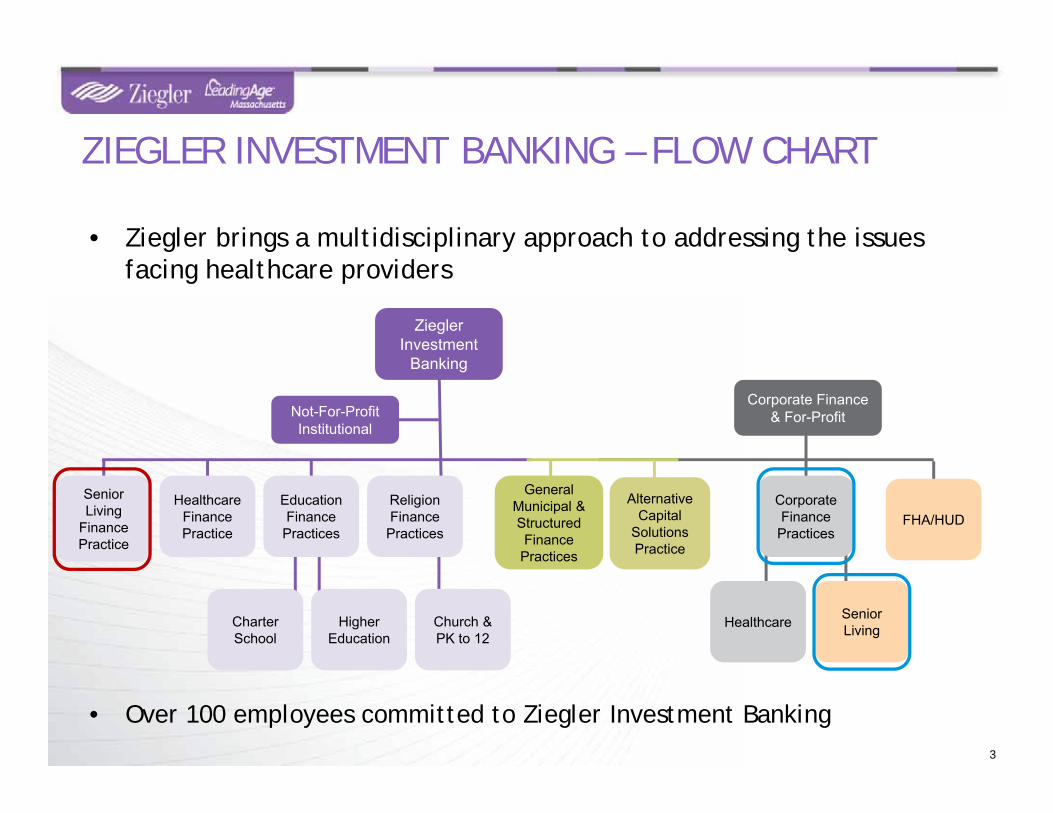

• Over 100 employees committed to Ziegler Investment Banking

• Ziegler brings a multidisciplinary approach to addressing the issues facing healthcare providers

ZIEGLER INVESTMENT BANKING – FLOW CHART

Ziegler Investment

Banking

Senior Living

Finance Practice

Not-For-Profit Institutional

Healthcare Finance Practice

Charter School

Higher Education

EducationFinance

Practices

ReligionFinance

Practices

Church & PK to 12

General Municipal &Structured Finance

Practices

Healthcare

Corporate Finance & For-Profit

CorporateFinance

Practices

AlternativeCapital

Solutions Practice

Senior Living

FHA/HUD

FHA/HOUSING:Bill Mulligan, Managing DirectorJeremy Frankel, Senior Vice PresidentBernie Gawley, SVP, Sr HUD Underwriter

CORPORATE FINANCE-SL:Bill Mulligan, Managing DirectorDan Revie, Senior Vice PresidentNick Glaisner, Vice President

CORPORATE FINANCE-HC:Neil Borg, Managing DirectorGrant Chamberlin, Managing DirectorAndy Colbert, Managing DirectorChris Hendrickson, Managing DirectorChris Rogers, Managing Director

SENIOR LIVING RESEARCH & DEVELOPMENTLisa McCracken, Director

Senior Living Research and DevelopmentSusan McDonough, Specialist, Catholic HealthcareCathy Owen, Assistant Vice PresidentKat Dymond, Research Analyst Ι Event Coordinator

INTEREST RATE PRODUCTS:Craig Naish, Managing DirectorScott Determan, DirectorMaureen Egan, Trading Specialist

West

Southeast Gulf States

Midwest

North-East

Mid-Atlantic

SENIOR LIVING FINANCE PRACTICE-NATIONAL COVERAGEREGIONAL AND PRODUCT FOCUS

Midwest: (312) 263-0110Dan Hermann, Senior Managing Director,

Head of Investment BankingTom Meyers, Managing DirectorWill Carney, Managing DirectorSteve Johnson, Managing DirectorJennifer Lavelle, DirectorMatt Mulé, Assistant Vice PresidentMichael Montgomery, Senior AssociateReanae Seth, Senior AssociateJett Saponaro, AnalystMatt Schappell, AnalystAdam Vanucci, Analyst

Mid-Atlantic: (312) 705:Michael Kelly, Managing Director (7260)Steve Jeffrey, Managing Director (7265)Amy Castleberry, Director (7258)(804) 793:Tommy Brewer, Managing Director (8490)Tad Melton, Managing Director (8487)Adam Garcia, Senior Vice President (8495)Paul Ballas, Analyst (9494)

West: (800) 327-3666Mary Muñoz, Managing DirectorSarkis Garabedian, DirectorDaren Bell, Senior Vice PresidentMichael Montgomery, Senior Associate

Southeast Gulf States:Rich Scanlon, Managing Director: 312-596-1572Brandon Powell, Managing Director: 804-793-8499Terry Herndon, Director: 312-705-7340Zane Hendricks, Analyst: 804-479-8496

Northeast: (212) 512-0400Keith Robertson, Managing DirectorChad Himel, DirectorTyler Simons, Vice PresidentJason Choi, Senior Associate

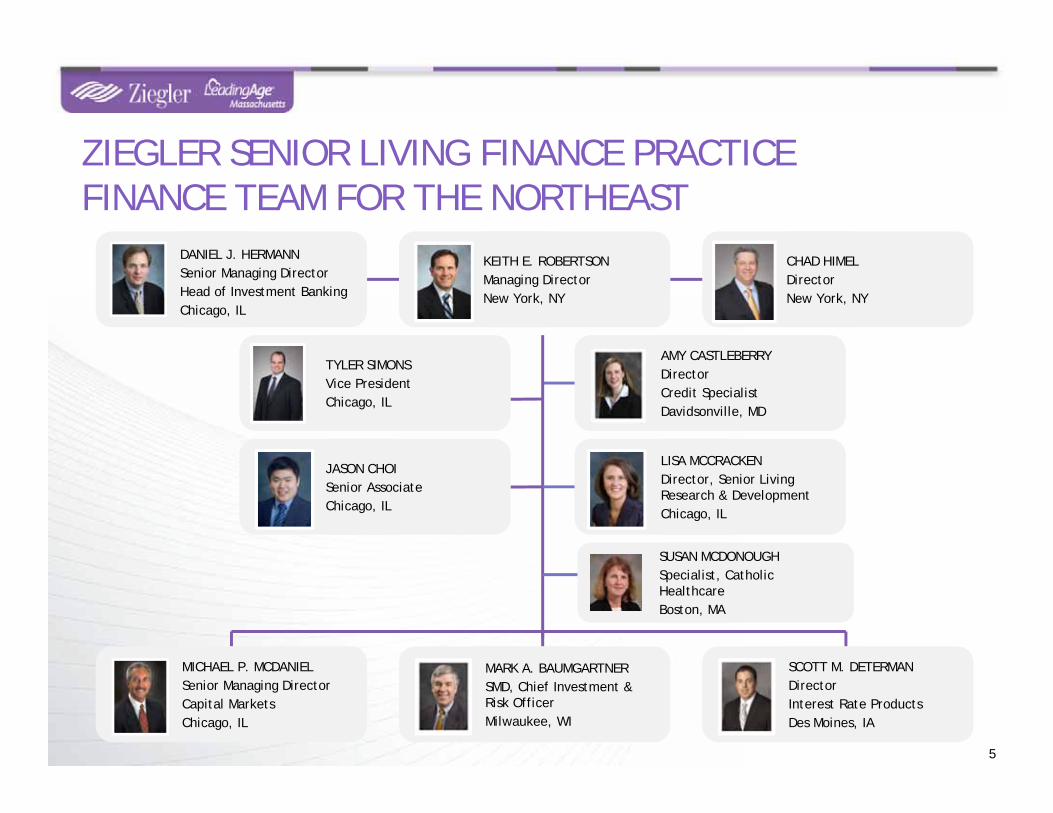

ZIEGLER SENIOR LIVING FINANCE PRACTICEFINANCE TEAM FOR THE NORTHEAST

5

KEITH E. ROBERTSONManaging DirectorNew York, NY

CHAD HIMELDirectorNew York, NY

TYLER SIMONSVice PresidentChicago, IL

MICHAEL P. MCDANIELSenior Managing DirectorCapital MarketsChicago, IL

MARK A. BAUMGARTNERSMD, Chief Investment & Risk OfficerMilwaukee, WI

AMY CASTLEBERRYDirectorCredit SpecialistDavidsonville, MD

LISA MCCRACKENDirector, Senior Living Research & DevelopmentChicago, IL

DANIEL J. HERMANNSenior Managing DirectorHead of Investment BankingChicago, IL

SCOTT M. DETERMANDirectorInterest Rate ProductsDes Moines, IA

SUSAN MCDONOUGHSpecialist, Catholic HealthcareBoston, MA

JASON CHOISenior AssociateChicago, IL

6

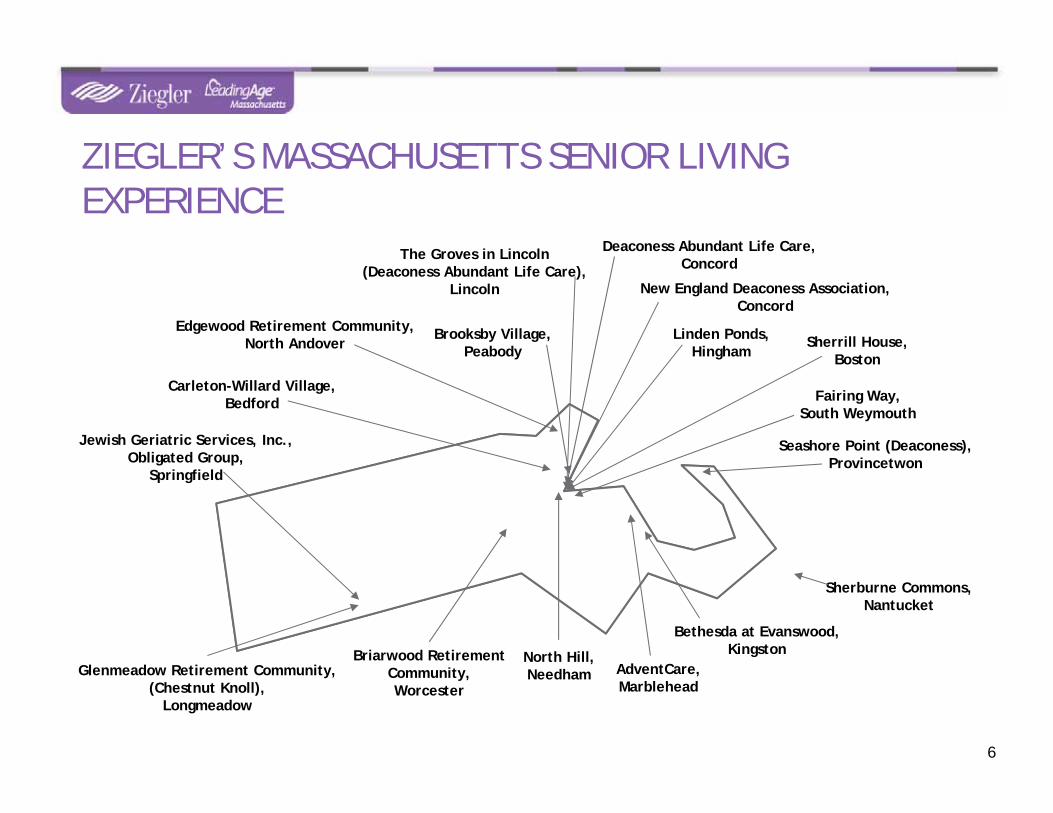

Jewish Geriatric Services, Inc.,Obligated Group,

Springfield

Bethesda at Evanswood,Kingston

Edgewood Retirement Community,North Andover

Carleton-Willard Village,Bedford

Glenmeadow Retirement Community,(Chestnut Knoll),

Longmeadow

Briarwood RetirementCommunity,Worcester

Brooksby Village,Peabody

Sherrill House,Boston

New England Deaconess Association,Concord

Sherburne Commons,Nantucket

Seashore Point (Deaconess),Provincetwon

AdventCare,Marblehead

Linden Ponds,Hingham

The Groves in Lincoln(Deaconess Abundant Life Care),

Lincoln

Deaconess Abundant Life Care,Concord

ZIEGLER’S MASSACHUSETTS SENIOR LIVING EXPERIENCE

North Hill,Needham

Fairing Way,South Weymouth

• Education– 2017: will host a total of 11 Conferences/

Symposiums– Annual Ziegler Senior Living Finance +

Strategy Conference– LeadingAge Ziegler National CFO Workshop– Ziegler National Senior Living Investor

Workshop SeriesSM

• External research– LeadingAge Ziegler 150– CARF Financial Ratios and Trends Publication

(Baker Tilly, CARF)– Resident Contract Study– Statewide CCRC Reports (MD; VA; TX) (My

LifeSite)

• Industry communication– Z-News– White papers– Ziegler CFO HotlineSM

7

• Internal information and research– Ziegler CCRC National Listing & Profile– Client-requested research– Client education sessions

• Secondary Market Investor Research– Surveillance updates on current credits– Supports active secondary trading

• Investor Market Research– ZieglerResearch.com

• Databases– Industry Trends (e.g. CCaH, Rental

CCRCs)– All Senior Living Financings– All New Communities (start-up CCRCs)

since 1990– Senior Living Rated Organizations

ZIEGLER’S SENIOR LIVING RESEARCH, EDUCATION& THOUGHT LEADERSHIP

ZIEGLER - THE UNDISPUTED LEADER INSENIOR LIVING FINANCINGS

8

Top Lead Managing UnderwritersSenior Living Finance Issues

2016

Based on full credit given to senior manager of lead-managed underwriting principal volume for senior living transactions completed nationally. Rankings and amounts through Thomson Financial Securities Data, as of 12/31/16

94.0

123.4

171.6

176.3

178.7

249.8

279.2

466.8

656.0

$2,866.4

$0

$200

$400

$600

$800

$1,0

00

$1,2

00

$1,4

00

$1,6

00

$1,8

00

$2,0

00

$2,2

00

$2,4

00

$2,6

00

$2,8

00

$3,0

00

Oppenheimer & Co.

Northland Securities

Stifel Nicolaus & Co.

Dougherty & Company

BB&T Capital Markets

Cain Brothers

RBC Capital Markets

Herbert J. Sims & Co.

Piper Jaffray & Co.

Ziegler

Millions

AGENDA

9

• YOUR KEY STAKEHOLDERS: CONSUMERS & STAFF

TOPIC 1

• NFP SENIOR LIVING GROWTH & EVOLUTIONTOPIC 2

• DISRUPTORS IMPACTING SENIOR LIVINGTOPIC 3

• SENIOR LIVING CAPITAL MARKETSTOPIC 4

QUESTIONS & ANSWERSQUESTIONS & ANSWERS

Source: Ziegler Investment Banking

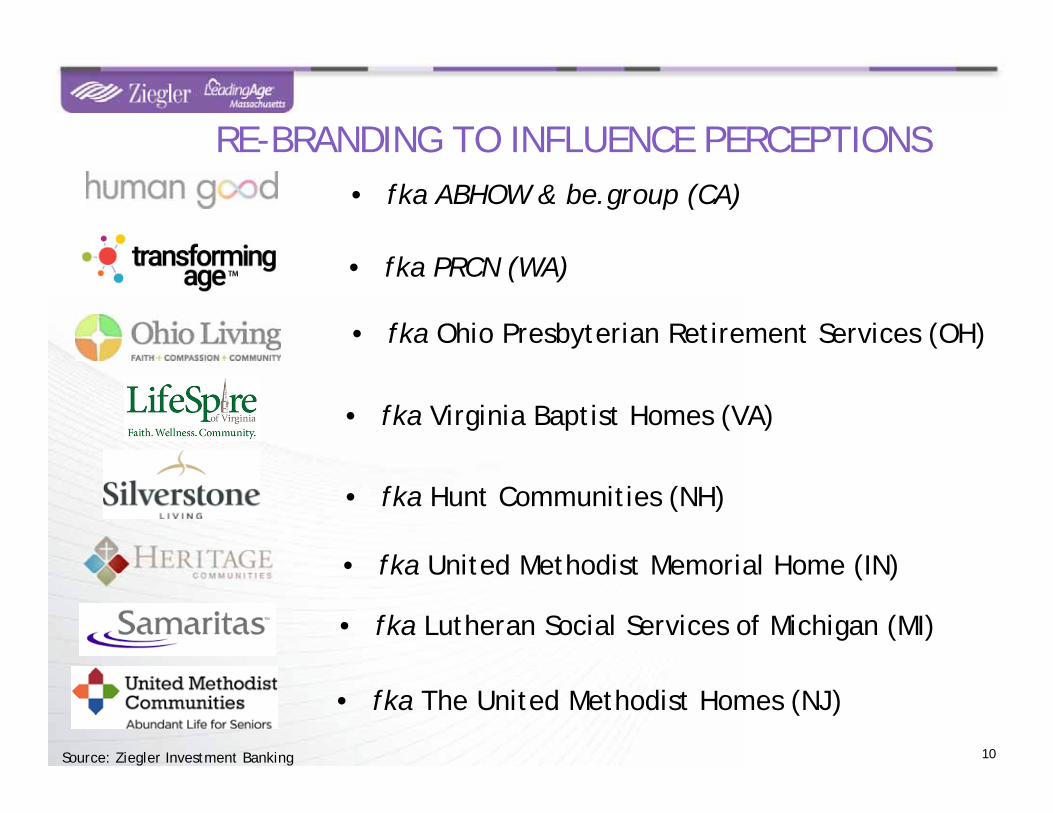

RE-BRANDING TO INFLUENCE PERCEPTIONS

• fka Lutheran Social Services of Michigan (MI)

• fka Hunt Communities (NH)

• fka United Methodist Memorial Home (IN)

• fka Virginia Baptist Homes (VA)

• fka The United Methodist Homes (NJ)

• fka Ohio Presbyterian Retirement Services (OH)

• fka PRCN (WA)

10

• fka ABHOW & be.group (CA)

• Many factors contributing to challenges:– An aging population; retirements– Increase in minimum wages– Department of labor overtime ruling– Pressure on immigration rules– Growth of the for-profit sector

• Many providers are working together, partnering with schools and universities

• Efforts to better understand work preferences, traits of the Millennials

• Not just your workforce…workforce of your partners (e.g. impact on construction costs)

11Source: Ziegler Investment Banking; and Argentum

Will need to recruit 1.2

million direct care

staff by 2025

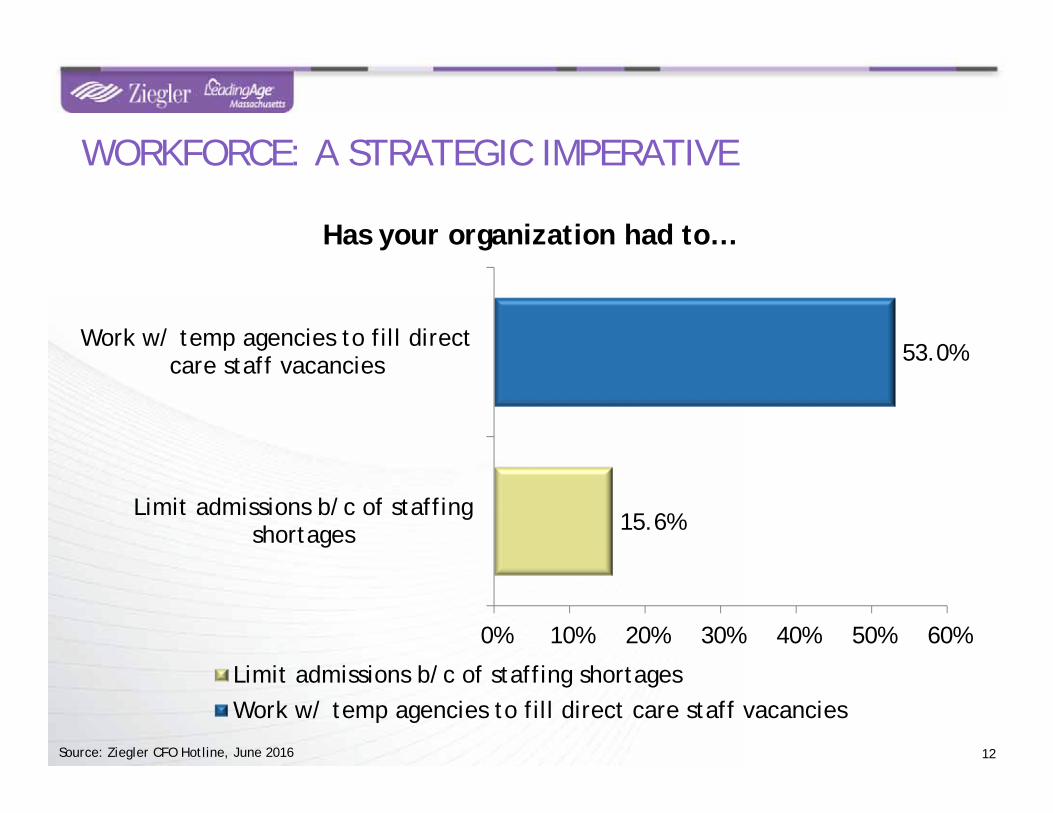

STAFFING: A COMPLEX ISSUE

12

15.6%

53.0%

0% 10% 20% 30% 40% 50% 60%

Limit admissions b/c of staffingshortages

Work w/ temp agencies to fill directcare staff vacancies

Has your organization had to…

Limit admissions b/c of staffing shortagesWork w/ temp agencies to fill direct care staff vacancies

Source: Ziegler CFO Hotline, June 2016

WORKFORCE: A STRATEGIC IMPERATIVE

TOPIC 2: NOT-FOR-PROFIT SENIOR LIVING GROWTH & EVOLUTION

14Sources: Ziegler National CCRC Listing & Profile, LeadingAge, NIC MAP® Data and Analysis Service, The National Center for Health Statistics, Centers for Medicare and Medicaid Services

TODAY’S RETIREMENT OPTIONSA LOOK AT SENIORS HOUSING SUPPLY

• 1,961 communities 600,000 unitsLife Plan Communities

• 4,800 programs 289,400 participants/dayAdult Day Programs

• 4,000 agencies 1.34 mill discharged/yr.Hospice

• 15,600 homes 1,663,000 units Nursing Homes

• 1,100 communities 53,000 unitsFreestanding Memory Care

• 30,200 communities 1million residentsAssisted Living/ Residential Care

• 12,400 agencies 4.9 mill discharged/yr.Home Health

• 1,100 properties 184,000 unitsIL Housing 3%

15%

17%

22%

24%

26%

51%

80%

% NFP

15

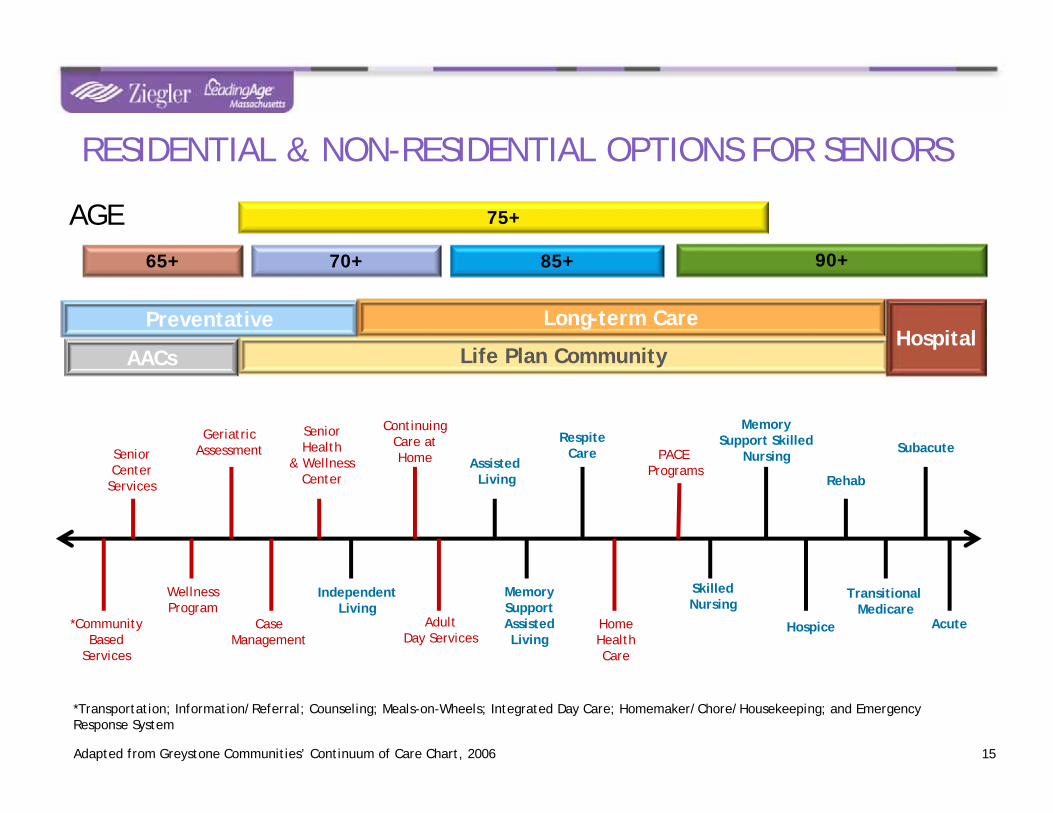

Subacute

Rehab

Memory Support Skilled

NursingPACE Programs

RespiteCare

Assisted Living

Continuing Care at Home

SeniorHealth

& WellnessCenter

GeriatricAssessmentSenior

CenterServices

*CommunityBased

Services

WellnessProgram

CaseManagement

IndependentLiving

AdultDay Services

MemorySupportAssistedLiving

HomeHealthCare

Skilled Nursing

Hospice Acute

Transitional Medicare

*Transportation; Information/Referral; Counseling; Meals-on-Wheels; Integrated Day Care; Homemaker/Chore/Housekeeping; and Emergency Response System

Adapted from Greystone Communities’ Continuum of Care Chart, 2006

AACs

15

85+65+ 90+

75+

70+

AGE

Preventative Long-term Care

Life Plan CommunityHospital

RESIDENTIAL & NON-RESIDENTIAL OPTIONS FOR SENIORS

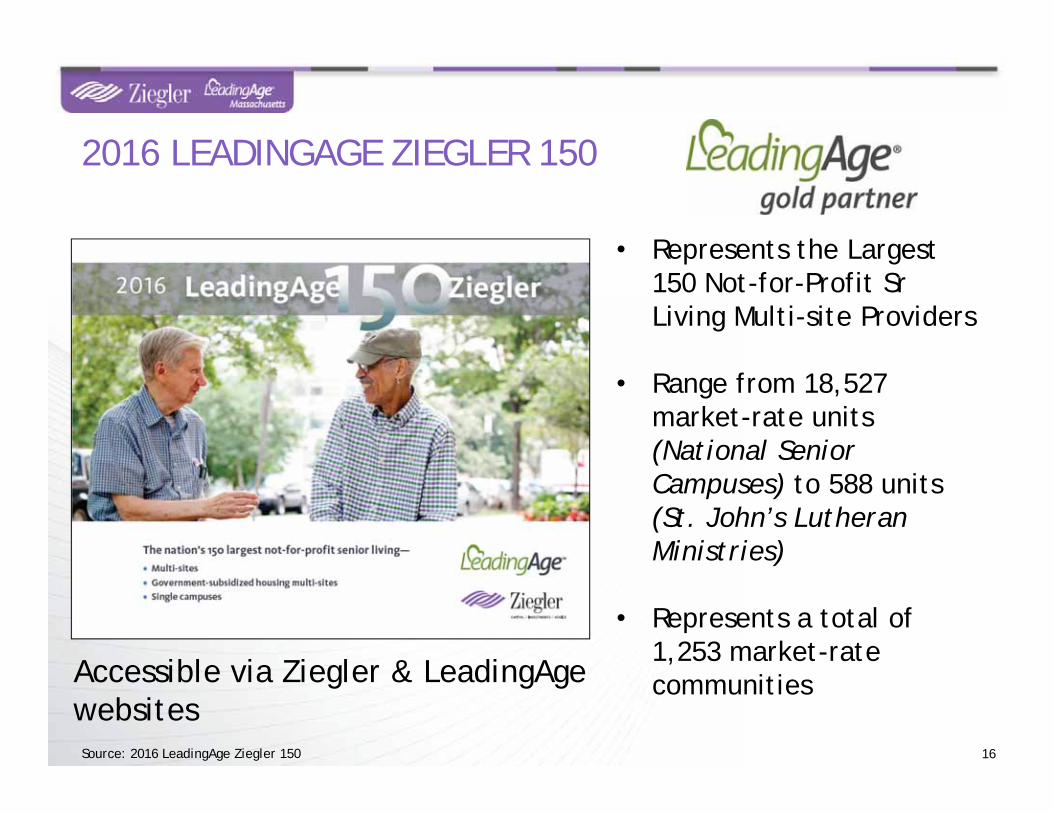

16Source: 2016 LeadingAge Ziegler 150

• Represents the Largest 150 Not-for-Profit Sr Living Multi-site Providers

• Range from 18,527 market-rate units (National Senior Campuses) to 588 units (St. John’s Lutheran Ministries)

• Represents a total of 1,253 market-rate communities

2016 LEADINGAGE ZIEGLER 150

Accessible via Ziegler & LeadingAge websites

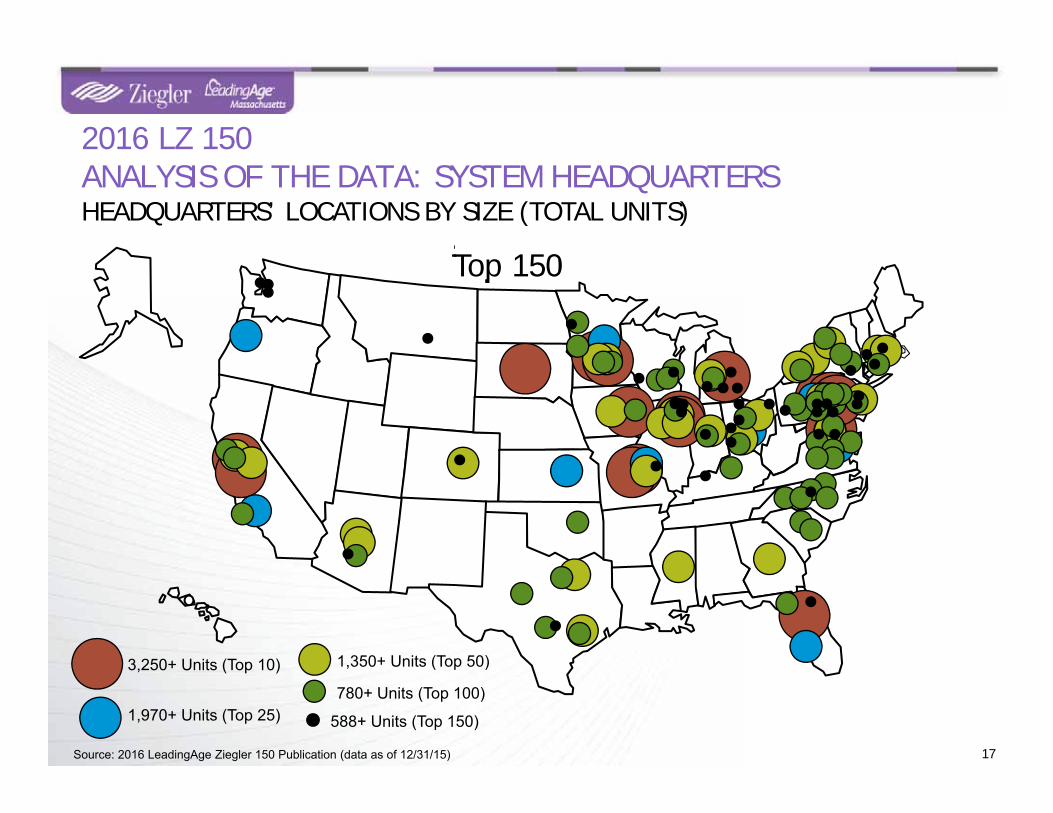

2016 LZ 150ANALYSIS OF THE DATA: SYSTEM HEADQUARTERSHEADQUARTERS’ LOCATIONS BY SIZE (TOTAL UNITS)

17Source: 2016 LeadingAge Ziegler 150 Publication (data as of 12/31/15)

588+ Units (Top 150)

3,250+ Units (Top 10)

1,970+ Units (Top 25)

1,350+ Units (Top 50)

780+ Units (Top 100)

Top 10Top 25Top 50Top 100Top 150

2016

Ran

k

2015

Ran

k

Units(as of 12/31/15)

Communities(as of 12/31/15)

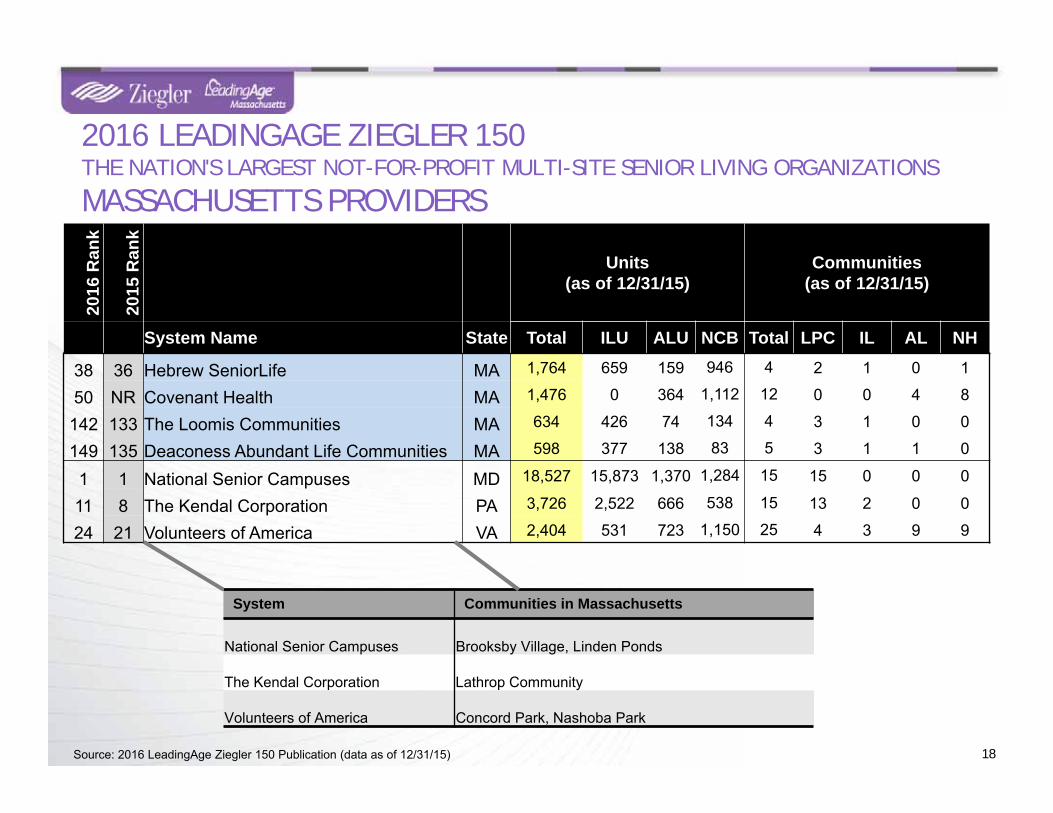

System Name State Total ILU ALU NCB Total LPC IL AL NH

38 36 Hebrew SeniorLife MA 1,764 659 159 946 4 2 1 0 1

50 NR Covenant Health MA 1,476 0 364 1,112 12 0 0 4 8

142 133 The Loomis Communities MA 634 426 74 134 4 3 1 0 0

149 135 Deaconess Abundant Life Communities MA 598 377 138 83 5 3 1 1 0

1 1 National Senior Campuses MD 18,527 15,873 1,370 1,284 15 15 0 0 0

11 8 The Kendal Corporation PA 3,726 2,522 666 538 15 13 2 0 0

24 21 Volunteers of America VA 2,404 531 723 1,150 25 4 3 9 9

2016 LEADINGAGE ZIEGLER 150THE NATION'S LARGEST NOT-FOR-PROFIT MULTI-SITE SENIOR LIVING ORGANIZATIONS

MASSACHUSETTS PROVIDERS

18Source: 2016 LeadingAge Ziegler 150 Publication (data as of 12/31/15)

System Communities in Massachusetts

National Senior Campuses Brooksby Village, Linden Ponds

The Kendal Corporation Lathrop Community

Volunteers of America Concord Park, Nashoba Park

• While not at pre-recession levels, NFP growth is increasing from recent years– Expansions to existing campuses– Growth through affiliations and acquisitions– New location development (LPCs, IL/AL, AL/MC)

• Growth through development of satellite campuses

• Providers continue to grow and diversify HCBS platforms

• Significant organizational resources are being devoted to changes in healthcare, post-acute and payment reform

19Source: Ziegler Investment Banking

INTENSE FOCUS ON GROWTH

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

1980 1985 1990 1995 2000 2005 2010 2015

Uni

ts

Year

ILU ALU NCB All Units

All other organizations pre-1980

National Senior Campuses

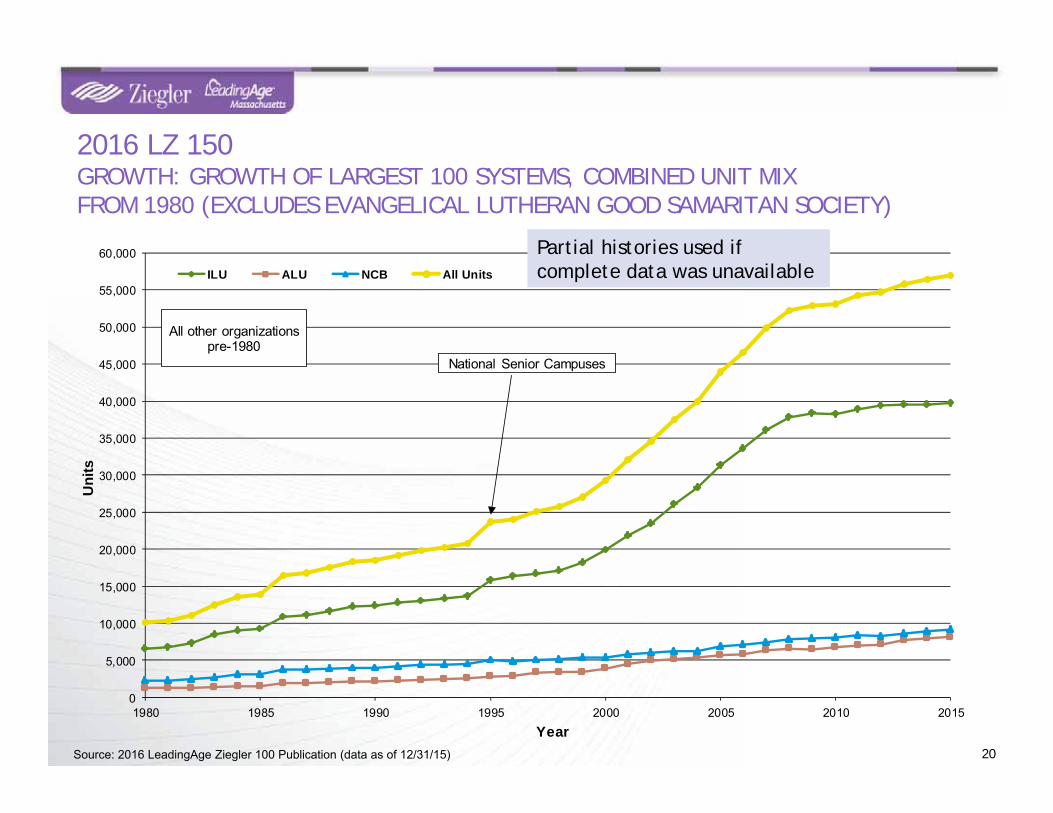

2016 LZ 150GROWTH: GROWTH OF LARGEST 100 SYSTEMS, COMBINED UNIT MIXFROM 1980 (EXCLUDES EVANGELICAL LUTHERAN GOOD SAMARITAN SOCIETY)

Partial histories used if complete data was unavailable

20Source: 2016 LeadingAge Ziegler 100 Publication (data as of 12/31/15)

Pulled Toward Growth

Growth Driven Internally

A PARADIGM SHIFT IN THE NFP SECTOR

21

THE PASTTHE FUTURE

Expansions/Repositioning

Sponsorship Transitions

HCBS Offerings

Satellite Campuses

New Community locations

NFP SENIOR LIVING GROWTH & EVOLUTION IN 2017

22

Least activity

Most activit

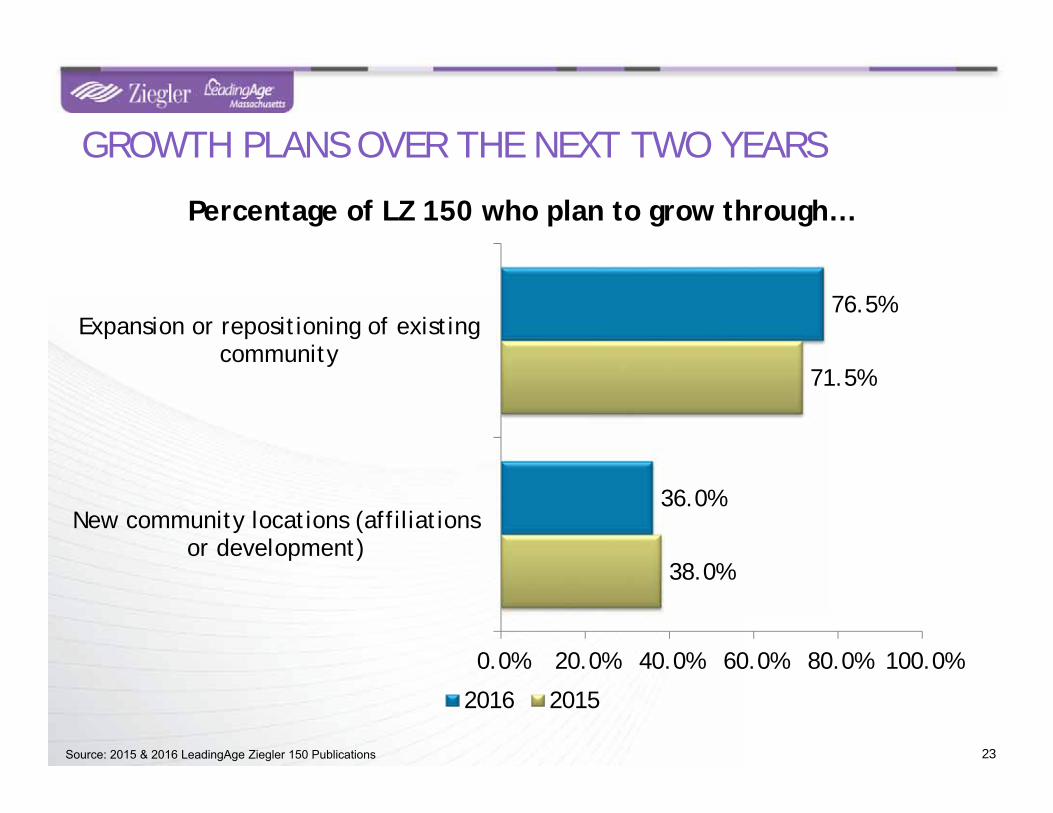

38.0%

71.5%

36.0%

76.5%

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

New community locations (affiliationsor development)

Expansion or repositioning of existingcommunity

Percentage of LZ 150 who plan to grow through…

2016 2015

GROWTH PLANS OVER THE NEXT TWO YEARS

23Source: 2015 & 2016 LeadingAge Ziegler 150 Publications

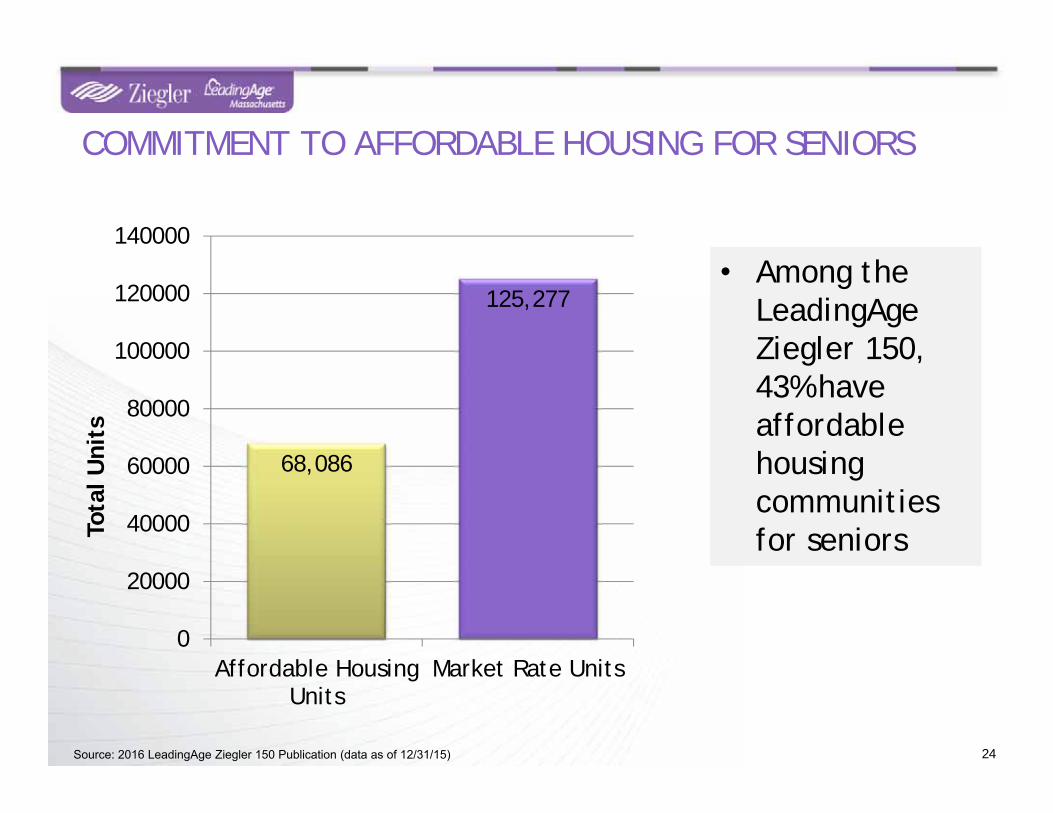

COMMITMENT TO AFFORDABLE HOUSING FOR SENIORS

24

68,086

125,277

0

20000

40000

60000

80000

100000

120000

140000

Affordable HousingUnits

Market Rate Units

Tota

l Uni

ts

Source: 2016 LeadingAge Ziegler 150 Publication (data as of 12/31/15)

• Among the LeadingAge Ziegler 150, 43% have affordable housing communities for seniors

Ran

k

2016

LZ

150

Ran

k Units(as of 12/31/15)

System Name State Total ILU ALU NCB AFF

1 2 The Evangelical Lutheran Good Samaritan Society SD 19,144 5,013 2,286 10,523 1,3222 1 National Senior Campuses MD 18,527 15,873 1,370 1,284 03 34 National Church Residences OH 18,140 779 539 542 16,2804 8 Retirement Housing Foundation CA 15,814 2,636 868 595 11,7155 24 Volunteers of America VA 12,436 531 723 1,150 10,0326 3 ACTS Retirement Services, Inc. PA 7,933 5,591 901 1,441 07 4 Presbyterian Homes and Services MN 7,349 3,503 2,127 1,426 2938 5 Benedictine Health MN 5,270 625 1,484 3,161 09 NR Mercy Housing Inc. CO 5,268 0 0 0 5,268

10 NR Christian Church Homes of Northern California CA 5,052 0 0 0 5,05211 6 Covenant Retirement Communities IL 5,015 3,146 885 984 012 16 Westminster Communities of Florida FL 4,843 2,027 476 751 1,58913 NR Senior Housing Assistance Group WA 4,797 0 0 0 4,79714 7 Ascension Senior Living MO 4,748 925 833 2,990 015 15 Cornerstone Affiliates CA 4,572 1,984 646 688 1,25416 13 Presbyterian Senior Living PA 4,503 1,808 499 1,127 1,06917 9 Lifespace Communities, Inc. IA 4,052 3,069 154 829 018 19 Pacific Retirement Services OR 3,901 2,116 333 407 1,04519 14 Lutheran Senior Services MO 3,785 1,614 709 1,003 45920 10 Trinity Senior Living Communities MI 3,745 1,184 633 1,928 034 38 Hebrew SeniorLife MA 2,529 659 159 946 76570 50 Covenant Health MA 1,476 0 364 1,112 099 NR Jewish Community Housing for the Elderly MA 1,117 0 0 0 1,117

25

2016 LEADINGAGE ZIEGLER 150LARGEST PROVIDERS OF MARKET-RATE AND AFFORDABLE UNITS

Source: 2016 LeadingAge Ziegler 150 Publication (data as of 12/31/15)

• Currently the primary mode of growth for residential settings among not-for-profit senior living providers

– Systems coming together

– Two smaller organizations joining to form larger

– Single-sites joining a system

26

UNIT GROWTH NOT JUST FROM BUILDING NEW UNITS, BUT ALSO FROM SYSTEM GROWTH

Spon

sors

hip

Tran

siti

ons

Affiliations

Acquisitions

Dispositions

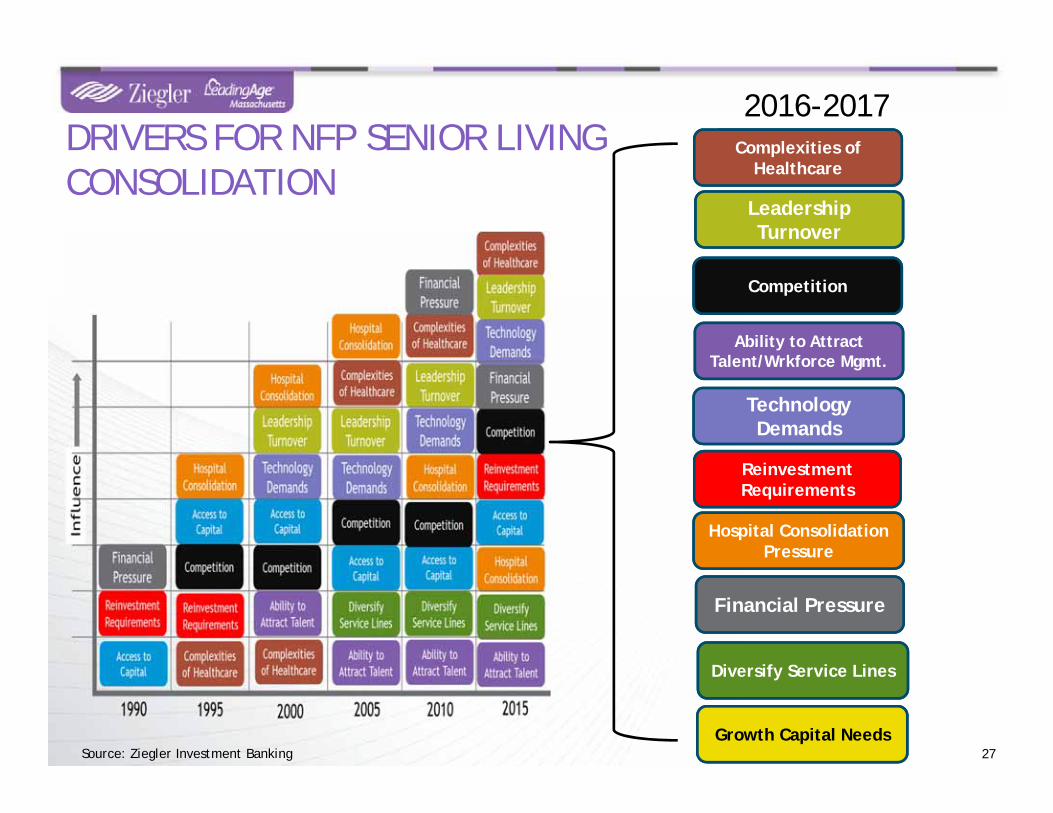

DRIVERS FOR NFP SENIOR LIVING CONSOLIDATION

27

Complexities of Healthcare

Leadership Turnover

Ability to Attract Talent/Wrkforce Mgmt.

Competition

Reinvestment Requirements

Technology Demands

Financial Pressure

Hospital Consolidation Pressure

Diversify Service Lines

2016-2017

Source: Ziegler Investment BankingGrowth Capital Needs

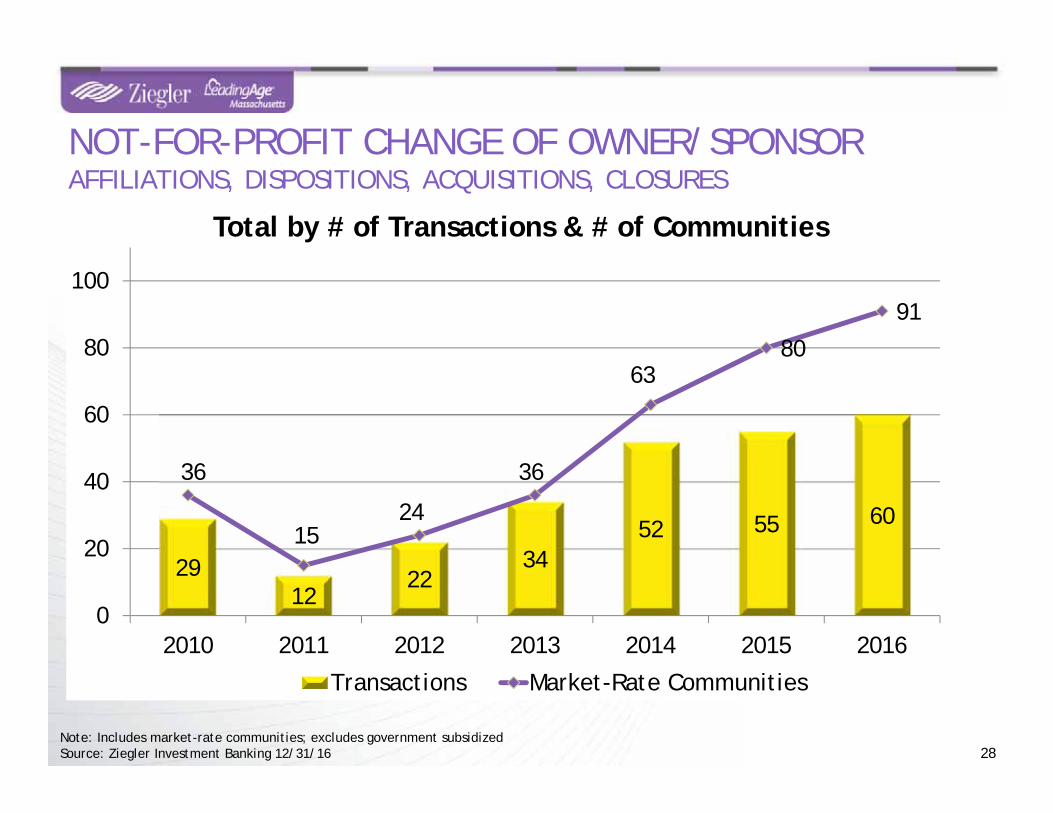

2912

2234

52 55 60

36

1524

36

6380

91

0

20

40

60

80

100

2010 2011 2012 2013 2014 2015 2016

Total by # of Transactions & # of Communities

Transactions Market-Rate Communities

Note: Includes market-rate communities; excludes government subsidizedSource: Ziegler Investment Banking 12/31/16

NOT-FOR-PROFIT CHANGE OF OWNER/SPONSORAFFILIATIONS, DISPOSITIONS, ACQUISITIONS, CLOSURES

28

29.4%46.7%

22.7%11.1% 17.5% 16.3%

41.7%

55.9%

46.7%

68.2%

61.1%63.2% 67.5%

39.6%

2.9%

6.6% 4.5%27.8% 10.5% 2.5% 3.3%

11.8%4.5% 8.8% 13.8% 15.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

NFP to NFP NFP to FP Closure of NFP FP to NFP

SPONSORSHIP TRANSITIONS BY CATEGORY2010-2016 BY NO. OF COMMUNITIES

Source: Ziegler Investment Banking, 12/31/16

7 7 5 411 14

19

12

75 4

1118

36

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014 2015 2016

NFP to NFP Sponsorship Transitions Only

Transactions Market-Rate Communities

Note: Includes market-rate communities; excludes government subsidizedSource: Ziegler Investment Banking 12/31/16

NOT-FOR-PROFIT CHANGE OF OWNER/SPONSORAFFILIATIONS, DISPOSITIONS, ACQUISITIONS, CLOSURES

30

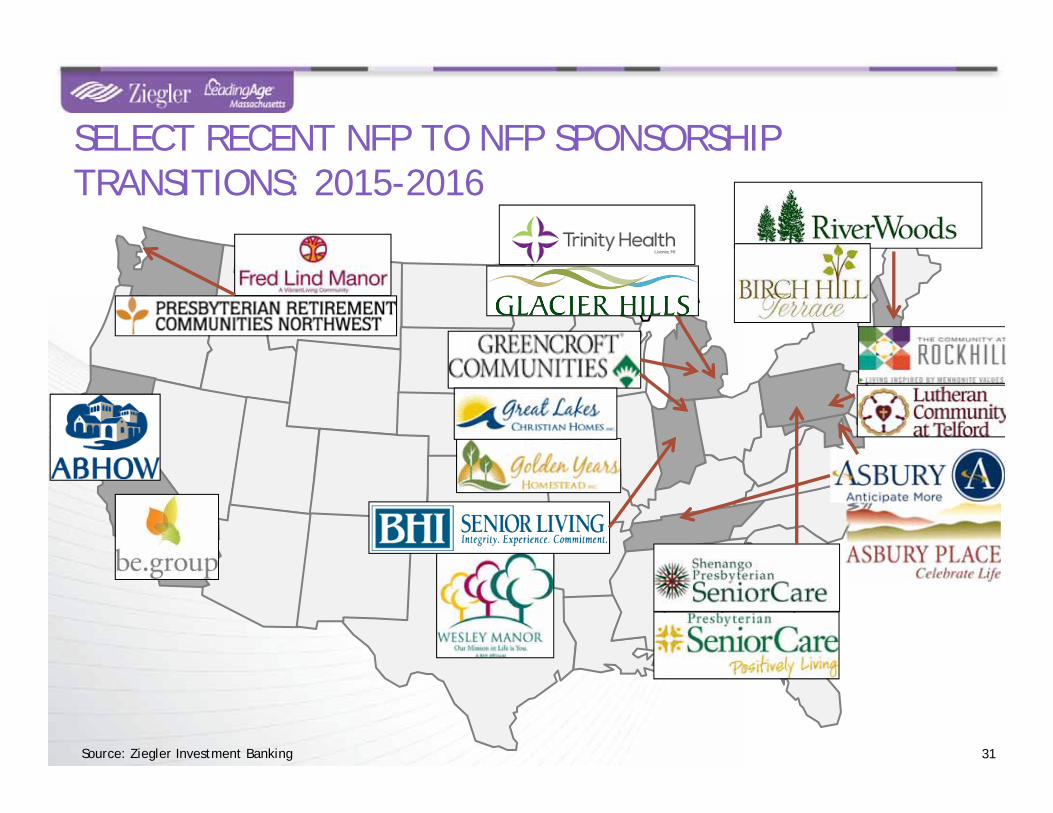

SELECT RECENT NFP TO NFP SPONSORSHIP TRANSITIONS: 2015-2016

31Source: Ziegler Investment Banking

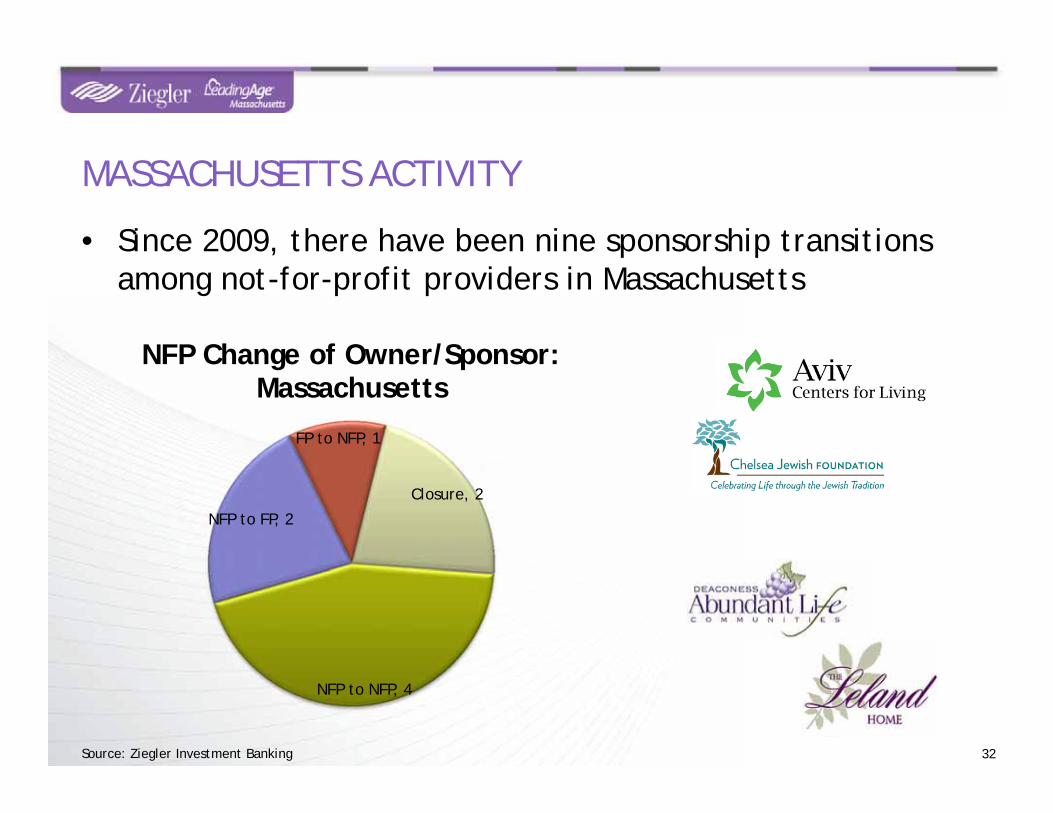

• Since 2009, there have been nine sponsorship transitions among not-for-profit providers in Massachusetts

MASSACHUSETTS ACTIVITY

32Source: Ziegler Investment Banking

NFP to NFP, 4

NFP to FP, 2

FP to NFP, 1

Closure, 2

NFP Change of Owner/Sponsor: Massachusetts

• Roughly 36% of the LZ 150 manage another community– The path to affiliation for some

• Some providers have developed consulting, development or management subsidiaries

MANAGEMENT & FOR-PROFIT SUBSIDIARIES

33

NFP SUCCESS BEYOND RESIDENTIAL SETTINGS

34Source: 2016 LeadingAge Ziegler 150

70% of the LZ150 with HCBS are below $10 million annually in HCBS revenue

TOPIC 3: DISRUPTORS IMPACTING NOT-FOR-PROFIT SENIOR LIVING

Sophistication• Do you have the scale needed to compete in the local

healthcare marketplace?• What expertise do you have regarding the ACA and payment

reform (bundles, etc.)?• Are you technologically advanced with data analytics,

outcome-based reporting, etc.?

Partnerships• Are you able to compete and be a player in the new models

of care emerging as a result of the ACA?• Are you engaged in any joint ventures, post-acute networks

or bundled-payment agreements?

INCREASING COMPLEXITY IN POST-ACUTE

36

SKILLED NURSING & POST-ACUTE:THREAT OR OPPORTUNITY?

37

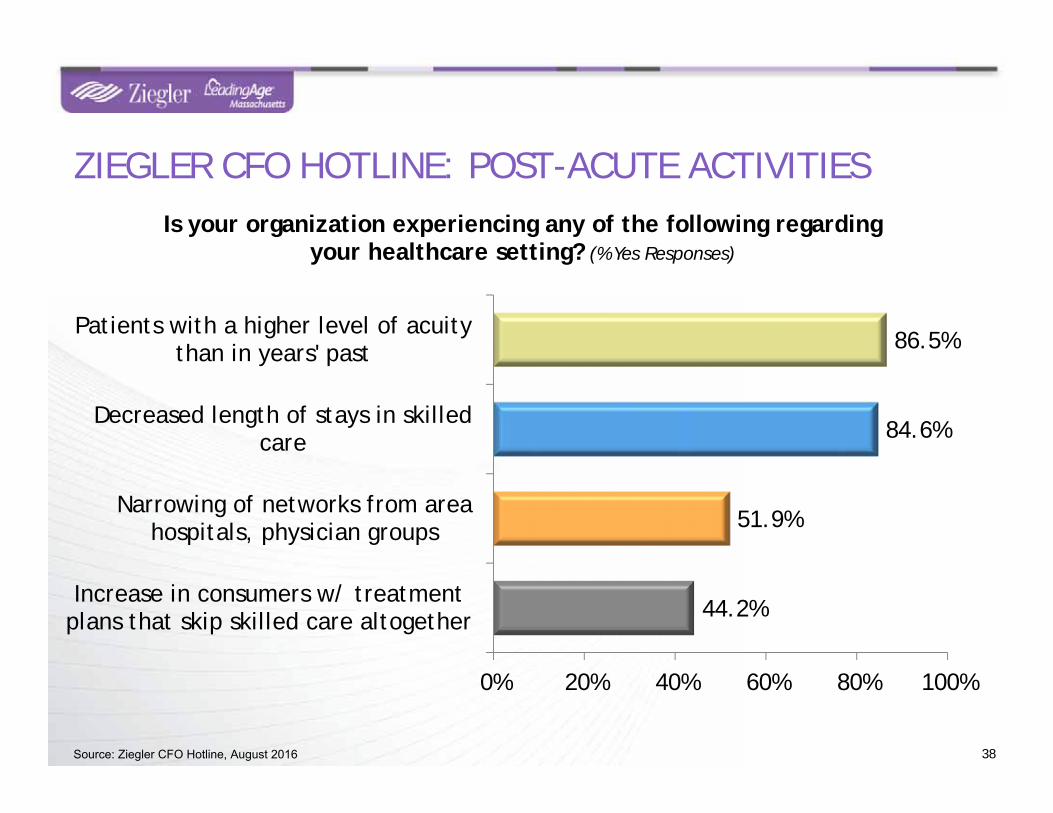

• Some providers have concerns:• Reimbursement pressures• Growth of bundles & managed care• Rising labor costs• Declining occupancy• Patients being sent directly home

• Some providers see opportunity:• New investment groups are forming• Rise of the hospitality-focused post-acute market• Overwhelming demographic tide that will

eventually need services at some point in the future

• Growth in regional operators

44.2%

51.9%

84.6%

86.5%

0% 20% 40% 60% 80% 100%

Increase in consumers w/ treatmentplans that skip skilled care altogether

Narrowing of networks from areahospitals, physician groups

Decreased length of stays in skilledcare

Patients with a higher level of acuitythan in years' past

Is your organization experiencing any of the following regarding your healthcare setting? (% Yes Responses)

38Source: Ziegler CFO Hotline, August 2016

ZIEGLER CFO HOTLINE: POST-ACUTE ACTIVITIES

Operators w/ 10 or more

properties, 33%

Operators w/ 2-9 properties,

26%

Single-site operators, 41%

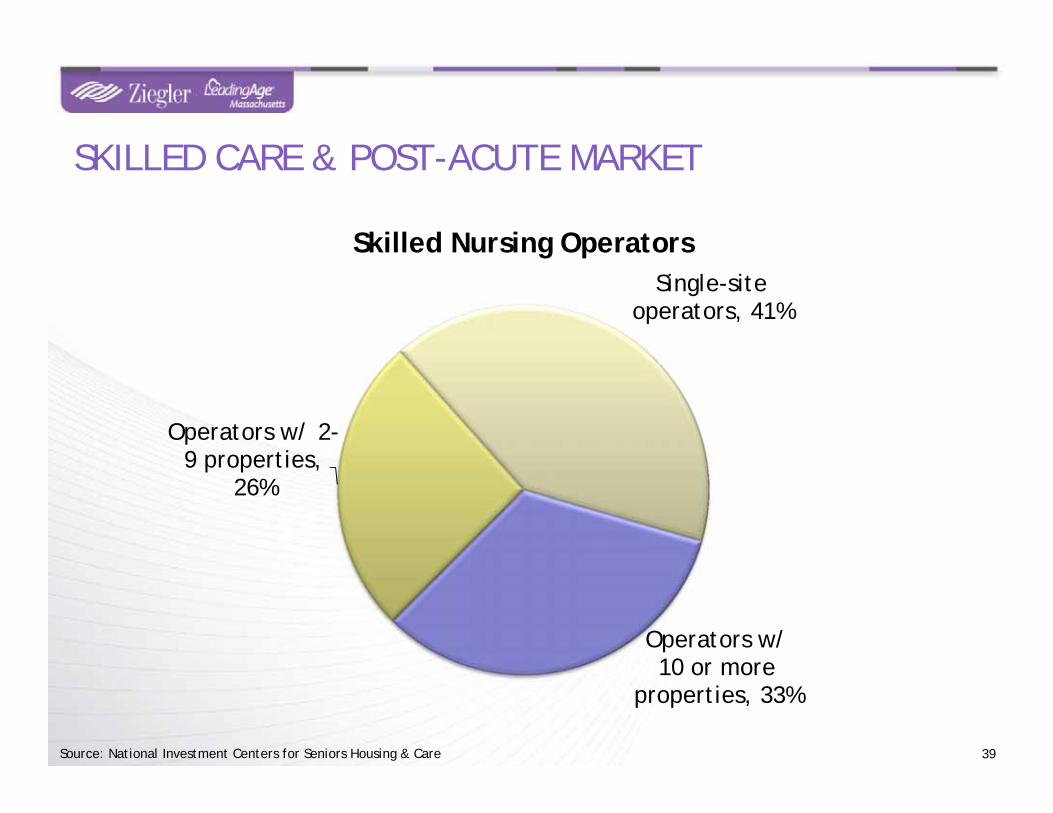

Skilled Nursing Operators

SKILLED CARE & POST-ACUTE MARKET

39Source: National Investment Centers for Seniors Housing & Care

• For-profits continue to grow nationally with new location development– Largely Independent Living, Assisted Living, Memory Care– Some hospitality-based post acute (e.g Mainstreet)

• For-profits are growing in residential services as well as home & community-based services

• Not-for-profits, however, consistently outperform for-profits with regard to occupancy

CONTINUED FOR-PROFIT GROWTH

40

For-Profit

NFP

Govt.

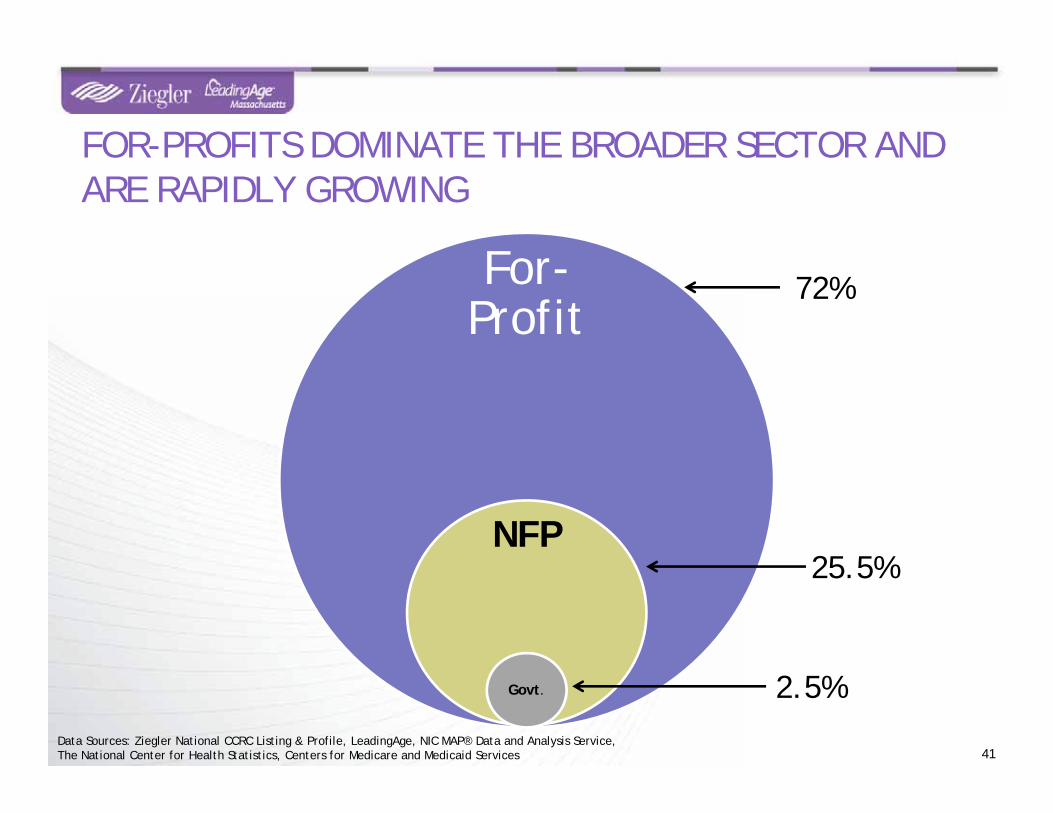

FOR-PROFITS DOMINATE THE BROADER SECTOR AND ARE RAPIDLY GROWING

41Data Sources: Ziegler National CCRC Listing & Profile, LeadingAge, NIC MAP® Data and Analysis Service, The National Center for Health Statistics, Centers for Medicare and Medicaid Services

72%

25.5%

2.5%

42

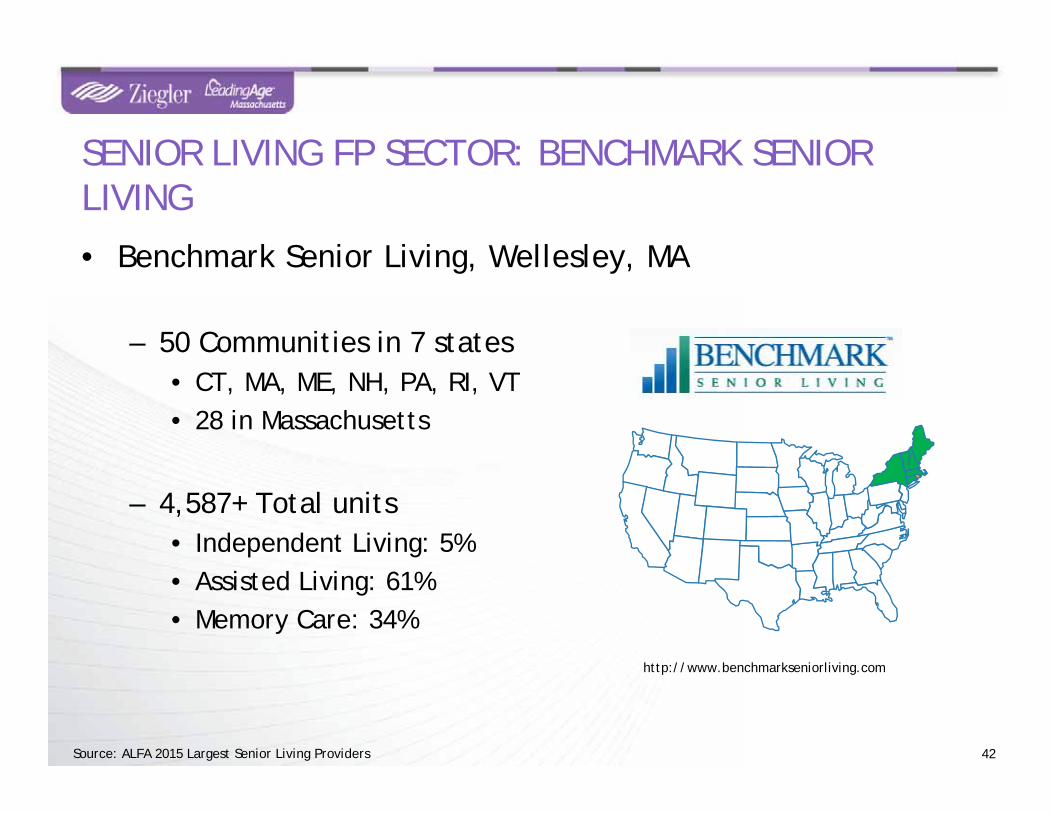

http://www.benchmarkseniorliving.com

SENIOR LIVING FP SECTOR: BENCHMARK SENIOR LIVING

• Benchmark Senior Living, Wellesley, MA

– 50 Communities in 7 states• CT, MA, ME, NH, PA, RI, VT• 28 in Massachusetts

– 4,587+ Total units• Independent Living: 5%• Assisted Living: 61%• Memory Care: 34%

Source: ALFA 2015 Largest Senior Living Providers

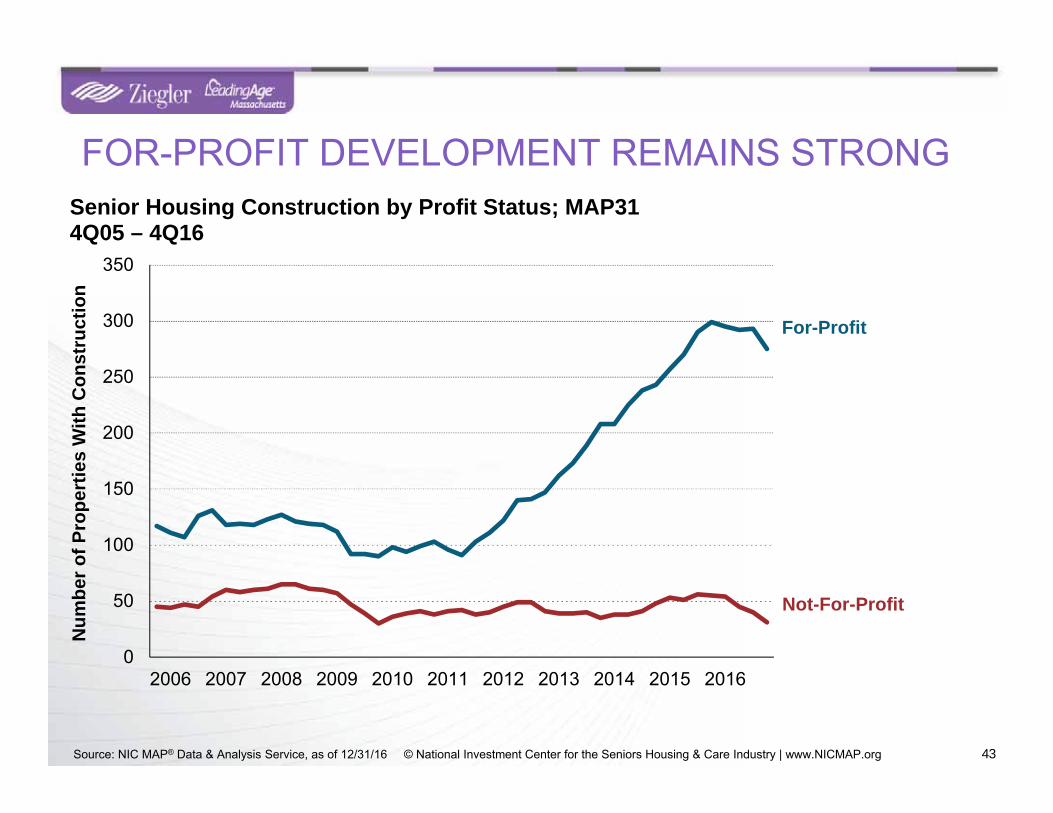

43Source: NIC MAP® Data & Analysis Service, as of 12/31/16 © National Investment Center for the Seniors Housing & Care Industry | www.NICMAP.org

FOR-PROFIT DEVELOPMENT REMAINS STRONG

43

0

50

100

150

200

250

300

350

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Num

ber o

f Pro

pert

ies

With

Con

stru

ctio

n

Senior Housing Construction by Profit Status; MAP314Q05 – 4Q16

Not-For-Profit

For-Profit

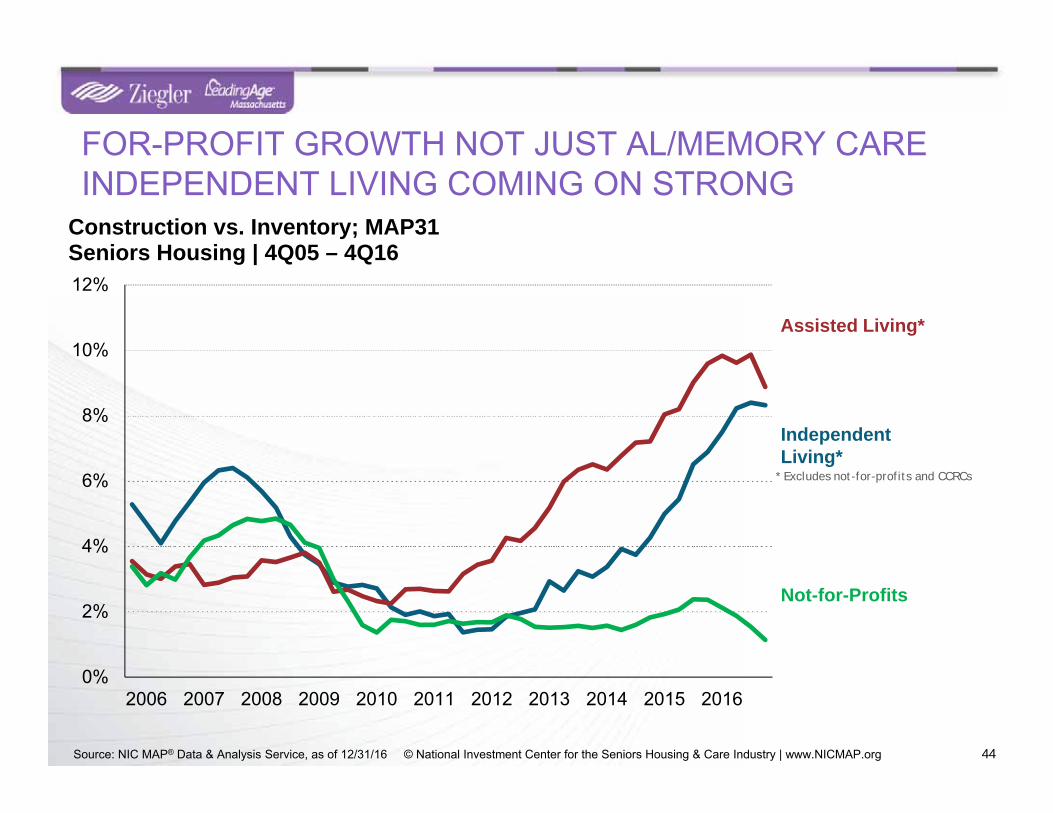

FOR-PROFIT GROWTH NOT JUST AL/MEMORY CARE INDEPENDENT LIVING COMING ON STRONG

44

* Excludes not-for-profits and CCRCs

Source: NIC MAP® Data & Analysis Service, as of 12/31/16 © National Investment Center for the Seniors Housing & Care Industry | www.NICMAP.org 44

0%

2%

4%

6%

8%

10%

12%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Construction vs. Inventory; MAP31Seniors Housing | 4Q05 – 4Q16

Independent Living*

Assisted Living*

Not-for-Profits

MASSACHUSETTS HEADLINES: FOR PROFIT GROWTH

45

February 22, 2017

46

NATIONAL OCCUPANCY IS GENERALLY HIGH

83%

85%

87%

89%

91%

93%

95%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Seniors Housing Occupancy by Profit Status; MAP314Q05 – 4Q16

Not-For-Profit

For-Profit

Source: NIC MAP® Data & Analysis Service, as of 12/31/16 © National Investment Center for the Seniors Housing & Care Industry | www.NICMAP.org

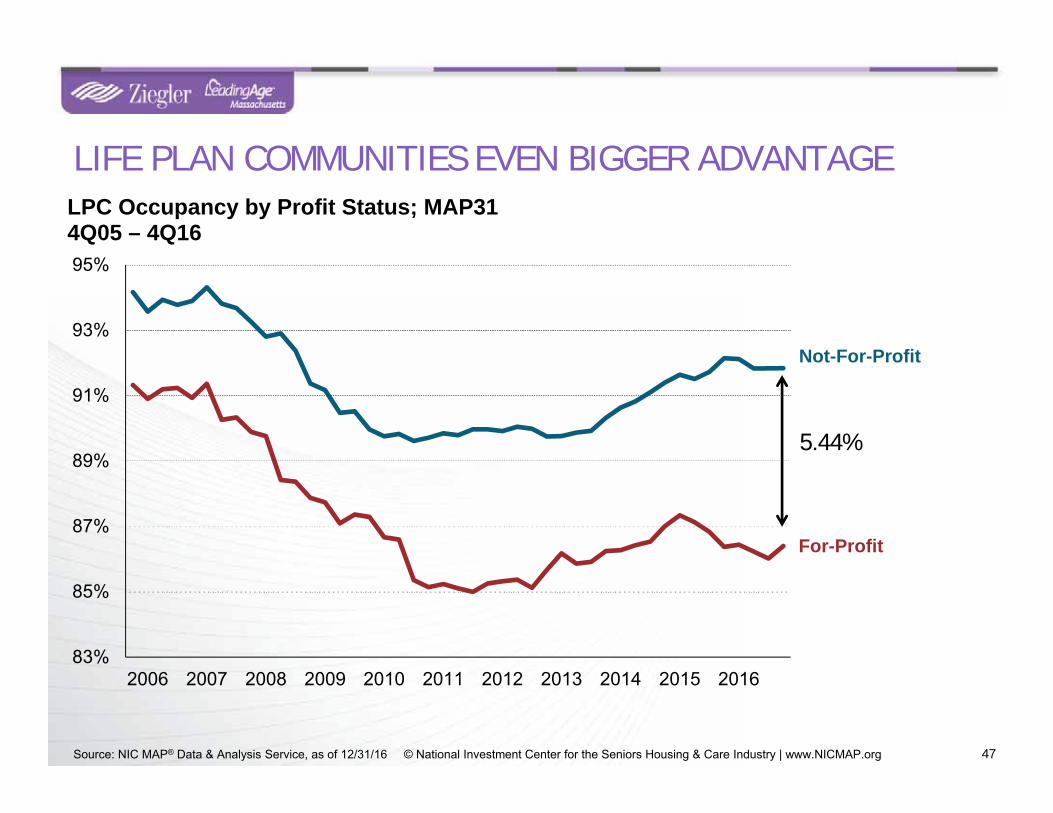

47

LIFE PLAN COMMUNITIES EVEN BIGGER ADVANTAGE

83%

85%

87%

89%

91%

93%

95%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

LPC Occupancy by Profit Status; MAP314Q05 – 4Q16

Not-For-Profit

For-Profit

5.44%

Source: NIC MAP® Data & Analysis Service, as of 12/31/16 © National Investment Center for the Seniors Housing & Care Industry | www.NICMAP.org

PRESSURES IMPACTING SKILLED NURSING OCCUPANCY

48Source: National Investment Center for the Seniors Housing & Care Industry | Skilled Nursing Data Report; data through June 2016

Operational Efficiencies

Consumer-driven

Care coordination

Data Analytics

TECHNOLOGY: PRESSURE TO KEEP UP

Source: Ziegler Investment Banking

ZIEGLER LINK•AGE FUND

Healthcare Services Healthcare IT Other

• Behavioral Change Management• Capitated Physician Models• Concierge Medicine• Homecare 2.0• Hospice and Palliative Care

• Clinical Decision Support• Medication Management• Population Analytics• Remote Monitoring• Telehealth

• Institutional Pharmacy• Medicare Advantage / Dual Eligible

Plans• Post-acute Care Diagnostics and

Therapeutics

Representative Business Models

Reduction of Hospitalizations and

Readmissions

Prevention and Wellness Strategies

Government Funded Programs / Public

Health Related Matters

Aging in Place Coordination of CareChronic Disease

Management

ZLF Fund

(RECENTLY

ACQUIRED BY

AFAM)Source: Ziegler Link.age Longevity Fund

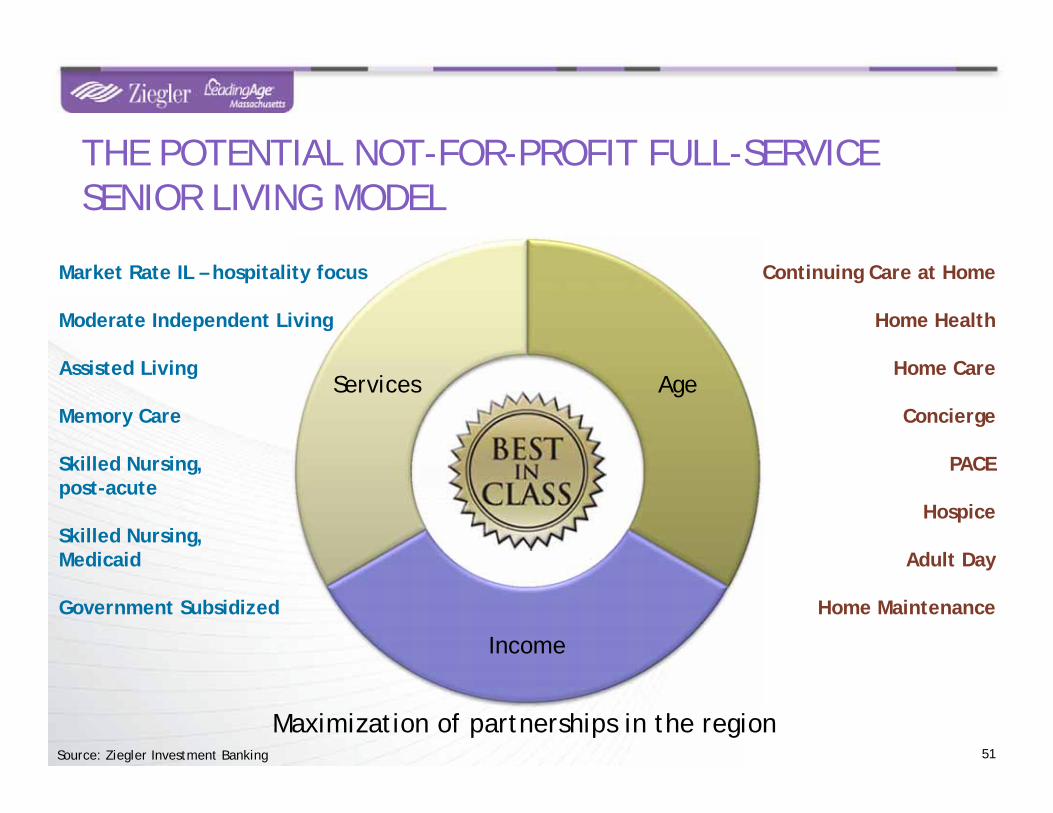

Age

Income

Services

THE POTENTIAL NOT-FOR-PROFIT FULL-SERVICE SENIOR LIVING MODEL

51

Market Rate IL – hospitality focus

Moderate Independent Living

Assisted Living

Memory Care

Skilled Nursing, post-acute

Skilled Nursing, Medicaid

Government Subsidized

Continuing Care at Home

Home Health

Home Care

Concierge

PACE

Hospice

Adult Day

Home Maintenance

Source: Ziegler Investment Banking

Maximization of partnerships in the region

TOPIC 4: THE SENIOR LIVING CAPITAL MARKETS

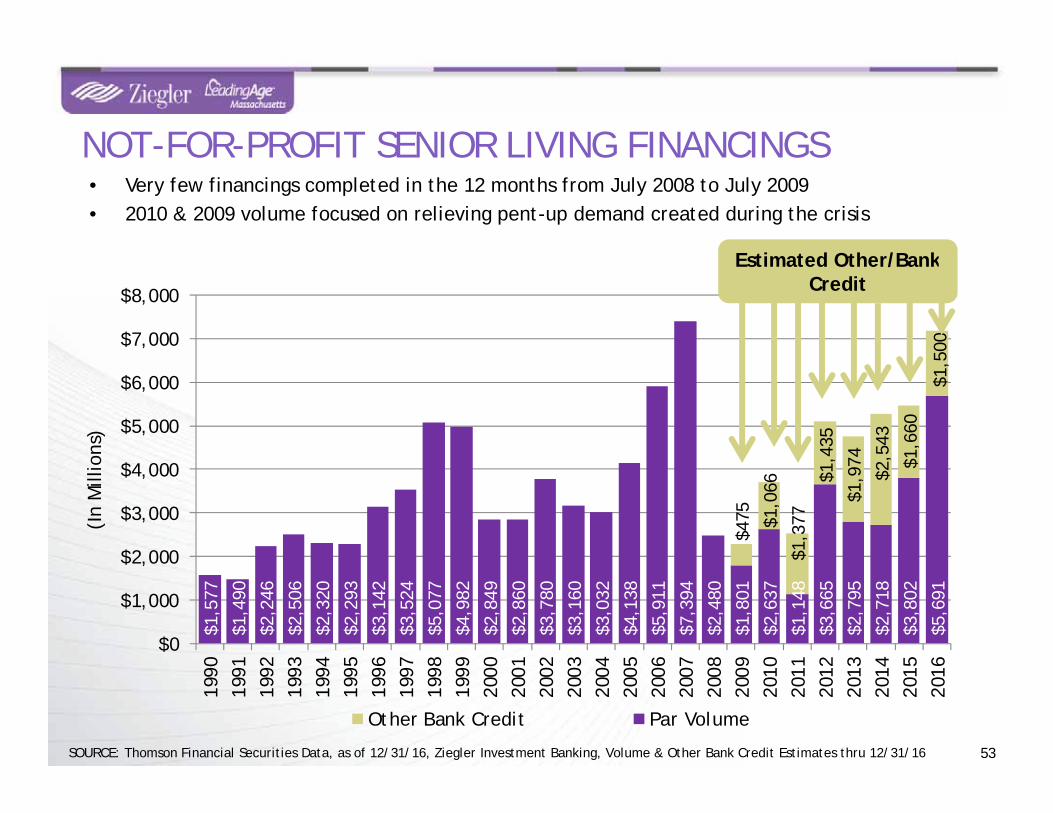

$1,5

77

$1,4

90

$2,2

46

$2,5

06

$2,3

20

$2,2

93

$3,1

42

$3,5

24

$5,0

77

$4,9

82

$2,8

49

$2,8

60

$3,7

80

$3,1

60

$3,0

32

$4,1

38

$5,9

11

$7,3

94

$2,4

80

$1,8

01

$2,6

37

$1,1

48

$3,6

65

$2,7

95

$2,7

18

$3,8

02

$5,6

91

$475 $1

,066

$1,3

77

$1,4

35

$1,9

74

$2,5

43

$1,6

60

$1,5

00

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(In

Mill

ions

)

Other Bank Credit Par Volume

53

• Very few financings completed in the 12 months from July 2008 to July 2009• 2010 & 2009 volume focused on relieving pent-up demand created during the crisis

NOT-FOR-PROFIT SENIOR LIVING FINANCINGS

SOURCE: Thomson Financial Securities Data, as of 12/31/16, Ziegler Investment Banking, Volume & Other Bank Credit Estimates thru 12/31/16

Estimated Other/Bank Credit

54

BANK CREDIT A RAPIDLY GROWING PART OF MARKET

SOURCE: Thomson Financial Securities Data, as of 12/31/16, Ziegler Investment Banking, Other Bank Credit Estimates thru 12/31/16

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Vol

ume

Mill

ions

Letter of Credit Backed VRDB's & Other Bank Credit Volume1990 - 2016

Other Bank Credit (Est.)

Letter of Credit Backed

• Letters of credit backing tax-exempt VRDB’s predominated through 2008

• Financial crisis in 2009 significantly reduced LOC volume (BASEL III/regulatory issues, bank credit allocation considerations, rating downgrades, etc.)

• Since 2009, direct bank purchases of tax-exempt debt, taxable construction loans have replaced VRDB’s

• Compared with one year ago, the sector experienced a net loss of one rating; there is also one less organization rated by multiple rating agencies.

55

NON-PROFIT SENIOR LIVING CREDIT RATING TRENDSCUMULATIVE SENIOR LIVING RATINGS

• All of these agencies publish guidelines for their ratings

• CCAC, Fitch & S&P publish rating category medians for key ratios

Rated Bond Issues Through 3/3/17

Fitch 129

S&P 40

Moody’s 2

*171

*12 organizations have debt rated by more than one rating agency. Therefore, there are a total of 159organizations with rated debt.

SOURCE: Ziegler Investment Banking, as of 3/3/17

NON-PROFIT SENIOR LIVINGCREDIT RATING TRENDS

NOTE: Excluded from the above totals: 4 ratings based on bond insured program.

0

20

40

60

80

100

120

140

160

180

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Moody's S&P Fitch

• Senior living credits predominantly in “BBB” category

THE RATINGS ENVIRONMENT

56

• Senior living credits predominantly in “BBB” category

16 19

5

37

67

25

0 2 00

10

20

30

40

50

60

70

80

A CategoryRatings

BBB CategoryRatings

BB CategoryRatings

S&P Fitch Moody's

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

A BBB BB

Systems Single Sites

Ratings Distribution by Category Ratings Category Breakdown

SOURCE: Ziegler Investment Banking, as of 3/3/17

0

5

10

15

20

25

30

35

40

1.95

2.05

2.15

2.25

2.35

2.45

2.55

2.65

2.75

2.85

2.95

3.05

3.15

3.25

3.35

3.45

3.55

3.65

3.75

3.85

3.95

4.05

4.15

4.25

4.35

4.45

4.55

4.65

4.75

4.85

4.95

5.05

5.15

5.25

5.35

5.45

5.55

5.65

5.75

5.85

5.95

6.05

6.15

6.25

6.35

6.45

6.55

6.65

6.75

6.85

6.95

7.05

Freq

uenc

y

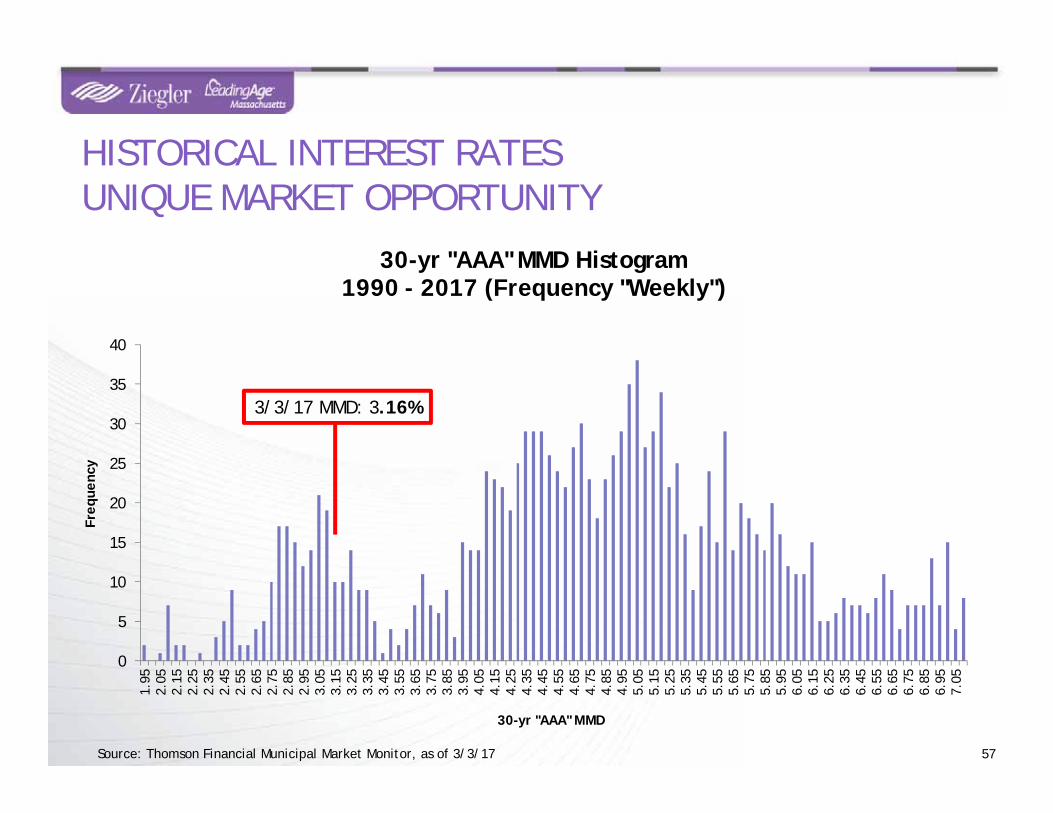

30-yr "AAA" MMD

30-yr "AAA" MMD Histogram1990 - 2017 (Frequency "Weekly")

57

HISTORICAL INTEREST RATESUNIQUE MARKET OPPORTUNITY

3/3/17 MMD: 3.16%

Source: Thomson Financial Municipal Market Monitor, as of 3/3/17

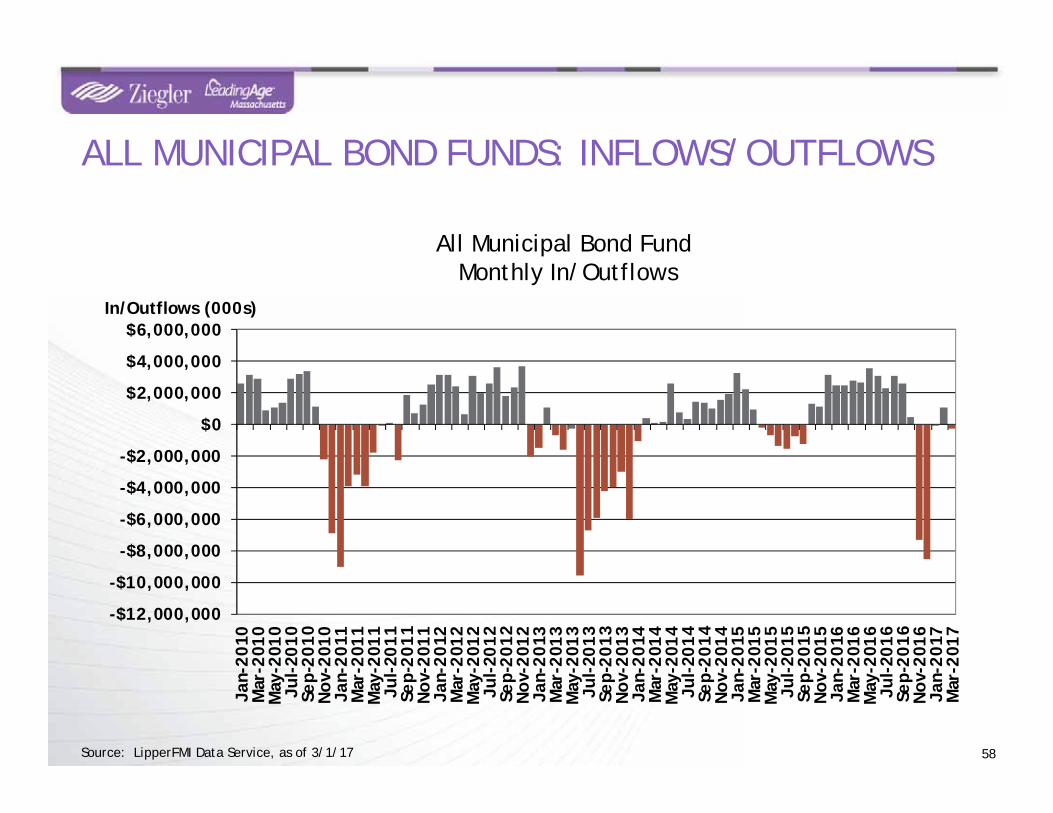

ALL MUNICIPAL BOND FUNDS: INFLOWS/OUTFLOWS

58

All Municipal Bond Fund Monthly In/Outflows

-$12,000,000

-$10,000,000

-$8,000,000

-$6,000,000

-$4,000,000

-$2,000,000

$0

$2,000,000

$4,000,000

$6,000,000

Jan-

2010

Mar

-201

0M

ay-2

010

Jul-

2010

Sep-

2010

Nov

-201

0Ja

n-20

11M

ar-2

011

May

-201

1Ju

l-20

11Se

p-20

11N

ov-2

011

Jan-

2012

Mar

-201

2M

ay-2

012

Jul-

2012

Sep-

2012

Nov

-201

2Ja

n-20

13M

ar-2

013

May

-201

3Ju

l-20

13Se

p-20

13N

ov-2

013

Jan-

2014

Mar

-201

4M

ay-2

014

Jul-

2014

Sep-

2014

Nov

-201

4Ja

n-20

15M

ar-2

015

May

-201

5Ju

l-20

15Se

p-20

15N

ov-2

015

Jan-

2016

Mar

-201

6M

ay-2

016

Jul-

2016

Sep-

2016

Nov

-201

6Ja

n-20

17M

ar-2

017

In/Outflows (000s)

Source: LipperFMI Data Service, as of 3/1/17

59

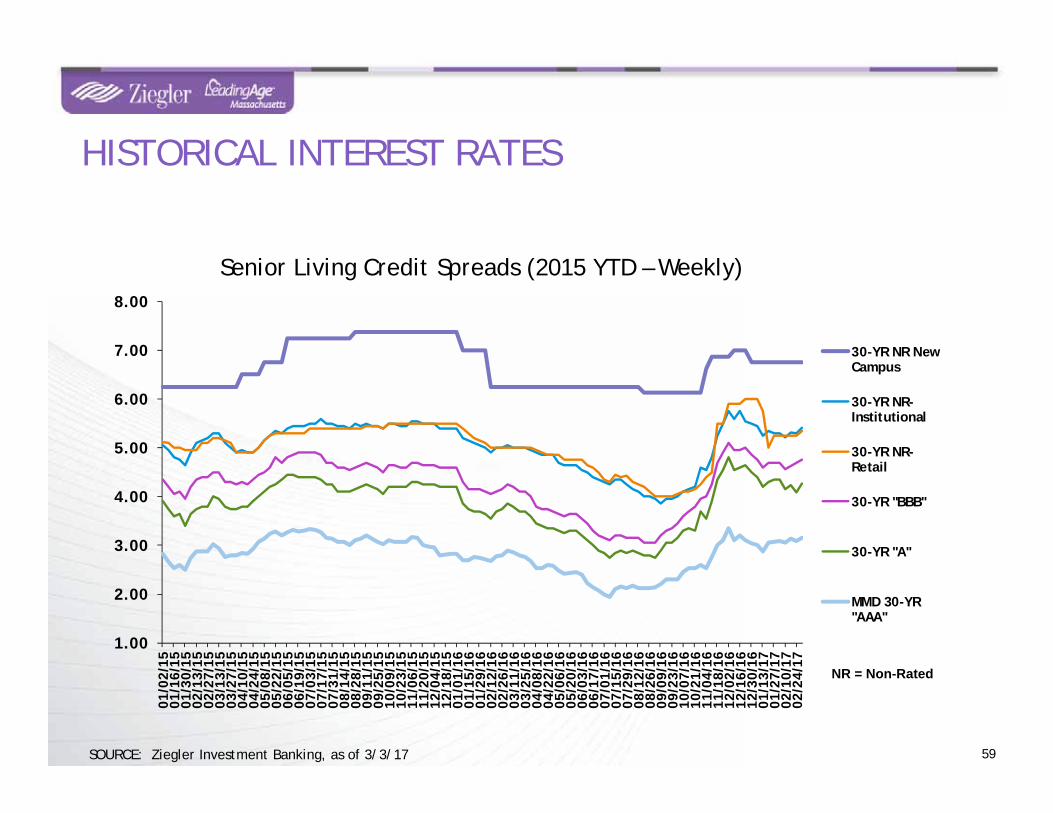

HISTORICAL INTEREST RATES

Senior Living Credit Spreads (2015 YTD – Weekly)

NR = Non-Rated

SOURCE: Ziegler Investment Banking, as of 3/3/17

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

01/0

2/15

01/1

6/15

01/3

0/15

02/1

3/15

02/2

7/15

03/1

3/15

03/2

7/15

04/1

0/15

04/2

4/15

05/0

8/15

05/2

2/15

06/0

5/15

06/1

9/15

07/0

3/15

07/1

7/15

07/3

1/15

08/1

4/15

08/2

8/15

09/1

1/15

09/2

5/15

10/0

9/15

10/2

3/15

11/0

6/15

11/2

0/15

12/0

4/15

12/1

8/15

01/0

1/16

01/1

5/16

01/2

9/16

02/1

2/16

02/2

6/16

03/1

1/16

03/2

5/16

04/0

8/16

04/2

2/16

05/0

6/16

05/2

0/16

06/0

3/16

06/1

7/16

07/0

1/16

07/1

5/16

07/2

9/16

08/1

2/16

08/2

6/16

09/0

9/16

09/2

3/16

10/0

7/16

10/2

1/16

11/0

4/16

11/1

8/16

12/0

2/16

12/1

6/16

12/3

0/16

01/1

3/17

01/2

7/17

02/1

0/17

02/2

4/17

30-YR NR NewCampus

30-YR NR-Institutional

30-YR NR-Retail

30-YR "BBB"

30-YR "A"

MMD 30-YR"AAA"

60

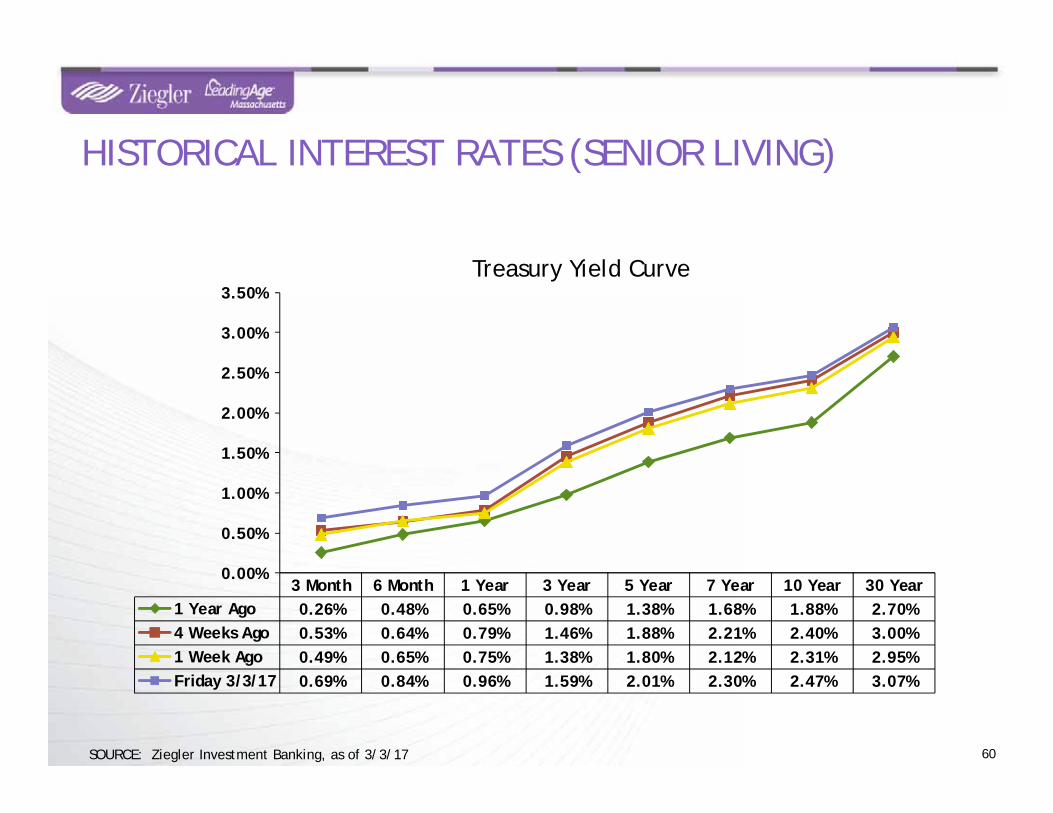

3 Month 6 Month 1 Year 3 Year 5 Year 7 Year 10 Year 30 Year1 Year Ago 0.26% 0.48% 0.65% 0.98% 1.38% 1.68% 1.88% 2.70%4 Weeks Ago 0.53% 0.64% 0.79% 1.46% 1.88% 2.21% 2.40% 3.00%1 Week Ago 0.49% 0.65% 0.75% 1.38% 1.80% 2.12% 2.31% 2.95%Friday 3/3/17 0.69% 0.84% 0.96% 1.59% 2.01% 2.30% 2.47% 3.07%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%Treasury Yield Curve

HISTORICAL INTEREST RATES (SENIOR LIVING)

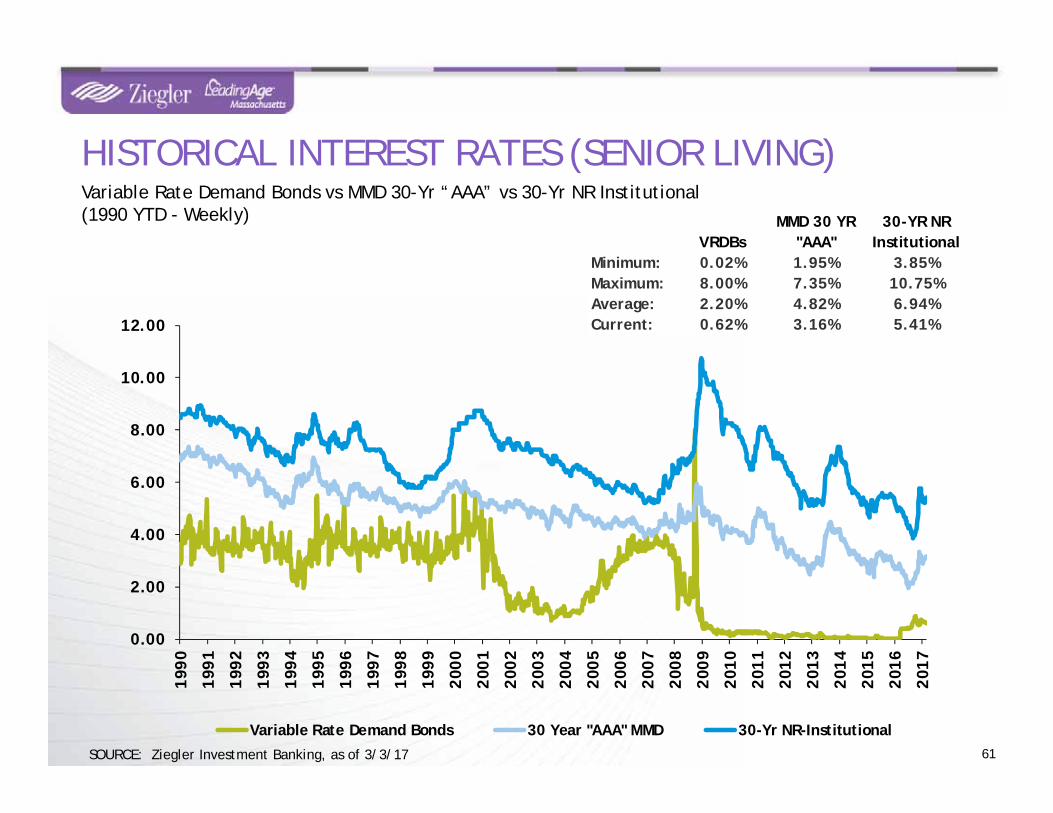

SOURCE: Ziegler Investment Banking, as of 3/3/17

VRDBsMMD 30 YR

"AAA"30-YR NR

InstitutionalMinimum: 0.02% 1.95% 3.85%Maximum: 8.00% 7.35% 10.75%Average: 2.20% 4.82% 6.94%Current: 0.62% 3.16% 5.41%

HISTORICAL INTEREST RATES (SENIOR LIVING)

61

Variable Rate Demand Bonds vs MMD 30-Yr “AAA” vs 30-Yr NR Institutional(1990 YTD - Weekly)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Variable Rate Demand Bonds 30 Year "AAA" MMD 30-Yr NR-InstitutionalSOURCE: Ziegler Investment Banking, as of 3/3/17

QUESTIONS & ANSWERS

B.C. Ziegler and Company is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be addressed to the National Registry of CPE Sponsors, 150 Fourth Avenue North, Suite 700, Nashville, TN, 37219-2417. Web site: www.nasba.org. Attendees are eligible to receive credits for attendance at the 2017 LeadingAge Massachusetts & Ziegler Senior Living Symposium. No prerequisites are required for this group-live educational conference. Program level is basic.

For more information regarding administrative policies such as complaint and refund, please contact our offices at 312-705-7262. Fees for this workshop are detailed on the registration form.

©2017 B.C. Ziegler and Company | Member SIPC and FINRA

• Ziegler is a privately-held investment bank, capital markets, wealth management and alternative investments firm

• A registered broker dealer with SIPC & FINRA

• Ziegler provides its clients with capital raising, strategic advisory services, equity & fixed-income trading, wealth management and research

• Founded in 1902, Ziegler specializes in the healthcare, senior living, educational and religious sectors as well as general municipal finance

ABOUT ZIEGLER

63

DISCLAIMERInvestment banking services offered through B.C. Ziegler and Company. FHA mortgage banking services are provided through ZieglerFinancing Corporation which is not a registered broker/dealer. Ziegler Financing Corporation and B.C. Ziegler and Company areaffiliated and referral fees may be paid by either entity for services provided.

This presentation was prepared based upon information provided to Ziegler Investment Banking (ZIB) and contains certain financialinformation, including audited and unaudited information, certain statistical information and explanations of such information innarrative form (the “Information”). ZIB believes this information to be correct as of the date or dates contained herein. However,the financial affairs change constantly, and such changes may be material. Today’s discussion may contain forward-lookingstatements, which may or may not come to fruition depending on certain circumstances, including those outside the control ofmanagement. Please be advised that ZIB has not undertaken, assumed no duty and are not obligated to update the Information. Inaddition, please be advised that past financial results do not predict future financial performance. The material in this presentationis designed to present potential financing structures and options for discussion, however it does not represent a commitment tounderwrite bonds, place debt or provide financing and thus should not be relied upon as a promise of financing or underwritingcommitment.

Related Documents