AICPA PFP Sandra Truitt 220 Leigh Farms Road Durham, NC 27707 919-490-4394 [email protected] 2016 Federal Income Tax Planning June 20, 2016 Page 1 of 17, see disclaimer on final page

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AICPAPFPSandra Truitt220 Leigh Farms RoadDurham, NC [email protected]

2016 Federal Income Tax Planning

June 20, 2016Page 1 of 17, see disclaimer on final page

The Tax Planning Environment in 2016While more than 15 major pieces of taxlegislation have been enacted into law since2000, the current tax planning environmenthas been heavily shaped by the AmericanTaxpayer Relief Act of 2012, passed inJanuary 2013, and the Protecting Americansfrom Tax Hikes (PATH) Act of 2015, passedlate last year.

Together, these legislative acts madepermanent a number of significant taxprovisions that had previously existed only intemporary form, and introduced new rates andlimitations that target high-income individuals.But while a host of popular tax benefitscommonly referred to as "tax extenders" arenow permanent fixtures in the tax code, otherswere simply extended, some only through the2016 tax year. As a result, 2016 tax planningtakes place in a relatively stable taxenvironment, with some small degree ofuncertainty regarding the potential availabilityof specific provisions heading into the 2017tax year.

Permanent provisions

These provisions are now part of thepermanent tax landscape:

• The six individual federal income tax rates(10%, 15%, 25%, 28%, 33%, and 35%)that had existed in temporary status formore than a decade, and a top 39.6% taxrate that applies to those with the highestincomes

• Special maximum tax rates generally applyto long-term capital gains and qualifieddividends; the rate is 0%, 15%, or 20%depending on your federal income taxbracket

• Higher alternative minimum tax (AMT)exemption amounts are in effect andadjusted for inflation; the AMT is essentiallya parallel federal income tax system with itsown rates and rules, and the higherexemption amounts and other relatedprovisions significantly limit the reach ofthis tax

• Personal and dependency exemptionsphase out at higher incomes, and itemizeddeductions may be limited

• "Marriage penalty" relief is now permanentin the form of an increased standarddeduction for married couples and anexpanded 15% federal income tax bracket

• Expanded tax credit provisions relating tothe dependent care tax credit, the adoptiontax credit, and the child tax credit

• Increased limits and more generous rulesof application relating to certain educationprovisions, including Coverdell educationsavings accounts, employer-providededucation assistance, and the student loaninterest deduction

• Individuals age 70½ or older can makequalified charitable distributions (QCDs)from their IRAs, and exclude thedistribution from gross income (up to$100,000 in a year); QCDs count towardsatisfying any required minimumdistributions (RMDs) that would otherwisehave had to be made from the IRA

• Individuals who itemize deductions onSchedule A of IRS Form 1040 can elect todeduct state and local general sales taxesin lieu of the deduction for state and localincome taxes

• The maximum amount that can beexpensed by a small business owner underIRC Section 179 rather than recoveredthrough depreciation deductions is$500,000, reduced by the amount by whichthe cost of qualifying property placed inservice during the year exceeds$2,010,000 (2016 figures; will be adjustedfor inflation in future years)

2015 federal income taxreturn filing deadlines formost individuals:

• Monday, April 18, 2016

• Tuesday, April 19, 2016, ifyou live in Massachusettsor Maine

• Monday, October 17,2016, if you file for anautomatic six-monthextension by the originaldue date

Page 2 of 17, see disclaimer on final page

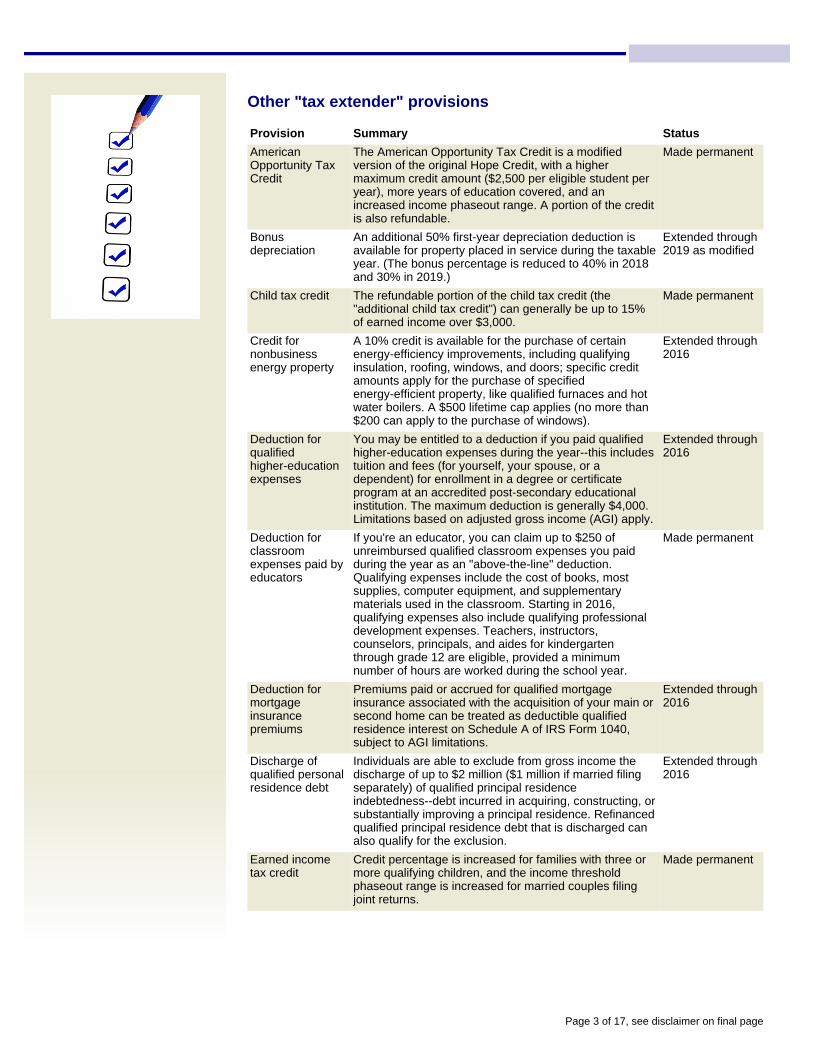

Other "tax extender" provisions

Provision Summary Status

AmericanOpportunity TaxCredit

The American Opportunity Tax Credit is a modifiedversion of the original Hope Credit, with a highermaximum credit amount ($2,500 per eligible student peryear), more years of education covered, and anincreased income phaseout range. A portion of the creditis also refundable.

Made permanent

Bonusdepreciation

An additional 50% first-year depreciation deduction isavailable for property placed in service during the taxableyear. (The bonus percentage is reduced to 40% in 2018and 30% in 2019.)

Extended through2019 as modified

Child tax credit The refundable portion of the child tax credit (the"additional child tax credit") can generally be up to 15%of earned income over $3,000.

Made permanent

Credit fornonbusinessenergy property

A 10% credit is available for the purchase of certainenergy-efficiency improvements, including qualifyinginsulation, roofing, windows, and doors; specific creditamounts apply for the purchase of specifiedenergy-efficient property, like qualified furnaces and hotwater boilers. A $500 lifetime cap applies (no more than$200 can apply to the purchase of windows).

Extended through2016

Deduction forqualifiedhigher-educationexpenses

You may be entitled to a deduction if you paid qualifiedhigher-education expenses during the year--this includestuition and fees (for yourself, your spouse, or adependent) for enrollment in a degree or certificateprogram at an accredited post-secondary educationalinstitution. The maximum deduction is generally $4,000.Limitations based on adjusted gross income (AGI) apply.

Extended through2016

Deduction forclassroomexpenses paid byeducators

If you're an educator, you can claim up to $250 ofunreimbursed qualified classroom expenses you paidduring the year as an "above-the-line" deduction.Qualifying expenses include the cost of books, mostsupplies, computer equipment, and supplementarymaterials used in the classroom. Starting in 2016,qualifying expenses also include qualifying professionaldevelopment expenses. Teachers, instructors,counselors, principals, and aides for kindergartenthrough grade 12 are eligible, provided a minimumnumber of hours are worked during the school year.

Made permanent

Deduction formortgageinsurancepremiums

Premiums paid or accrued for qualified mortgageinsurance associated with the acquisition of your main orsecond home can be treated as deductible qualifiedresidence interest on Schedule A of IRS Form 1040,subject to AGI limitations.

Extended through2016

Discharge ofqualified personalresidence debt

Individuals are able to exclude from gross income thedischarge of up to $2 million ($1 million if married filingseparately) of qualified principal residenceindebtedness--debt incurred in acquiring, constructing, orsubstantially improving a principal residence. Refinancedqualified principal residence debt that is discharged canalso qualify for the exclusion.

Extended through2016

Earned incometax credit

Credit percentage is increased for families with three ormore qualifying children, and the income thresholdphaseout range is increased for married couples filingjoint returns.

Made permanent

Page 3 of 17, see disclaimer on final page

Mass transitbenefits

The monthly exclusion for employer-provided transit passand vanpool benefits is set to the same level as theexclusion for employer-provided parking ($255 monthlyfor 2016).

Made permanent

Qualifiedsmall-businessstock

100% of capital gain from the sale or exchange ofqualified small-business stock acquired at original issueduring the tax year can be excluded from incomeprovided that certain requirements, including a five-yearholding period, are met.

Made permanent

Income Tax Fundamentals

What is "gross income"?

Your gross income is the total incomereported on your tax return, and includesitems such as wages, taxable interest,dividends, and capital gains. Basically, unlessa type of income is specifically excluded bythe Internal Revenue Code, it is included indetermining gross income.

Internal Revenue Code (IRC) Section 61(a)defines gross income as: [...] all income fromwhatever source derived, including (but notlimited to) the following items:

1. Compensation for services, includingfees, commissions, fringe benefits, andsimilar items

2. Gross income derived from business3. Gains derived from dealings in property4. Interest5. Rents6. Royalties7. Dividends8. Alimony and separate maintenance

payments9. Annuities10. Income from life insurance endowment

contracts11. Pensions12. Income from discharge of indebtedness13. Distributive share of partnership gross

income14. Income in respect of a decedent15. Income from an interest in an estate or

trust

What's not included in gross income? Itemsthat are specifically excluded from grossincome include gifts and inheritances, lifeinsurance death benefits, scholarships,

specifically excluded if certain conditions aremet. For example, Social Security benefitsmay be excluded from income, but a portion ofbenefits is included once your income reachesa certain level. Earnings within certaintax-advantaged savings vehicles like IRAs,401(k) plans, and 529 plans are excluded fromcurrent income, provided certain criteria aremet.

What is "taxable income"?

You start with your gross income, thensubtract your adjustments toincome--sometimes called "above-the-line"deductions--to determine your adjusted grossincome (AGI). Adjustments to income mayinclude deductions for student loan interest,moving expenses, and contributions to healthsavings accounts and traditional IRAs.

You're generally also able to take a standarddeduction amount that's based on your filingstatus. If you choose, you can itemizedeductions on IRS Form 1040, Schedule A,rather than claiming the standard deduction.Itemized deductions include deductions formedical expenses, mortgage interest, stateand local taxes, and charitable contributions.

You're also able to claim specific dollarexemptions for yourself, your spouse (if youare married and file a joint return), and yourdependents. Subtracting adjustments toincome, deductions, and exemptions fromyour gross income results in your taxableincome, which is used to calculate yourfederal income tax.

payments for injury or sickness, certainemployment fringe benefits, certain militarypay and benefits, interest on some state andlocal bonds, and limited gain on the sale of aprincipal residence. In some cases, income is

More than 147 millionindividual federal income taxreturns were filed for the2013 tax year.

Source: Table 1, IndividualIncome Tax Returns:Selected Income and TaxItems (based on tax year2013 preliminary data),www.irs.gov, 4/6/15

Page 4 of 17, see disclaimer on final page

Basic Standard Deduction Amounts

Filing status 2015 2016

Married filing jointlyor qualifyingwidow(er)

$12,600 $12,600

Head of household $9,250 $9,300

Single $6,300 $6,300

Married filingseparately

$6,300 $6,300

Personal Exemption Amounts

2015 2016

$4,000 $4,050

Note: Itemized deductions are limited, andpersonal exemptions are phased out, forhigh-income individuals (for 2016, individualsfiling single with AGI exceeding $259,400;married individuals filing jointly with AGIexceeding $311,300; head of household filerswith AGI exceeding $285,350; and marriedindividuals filing separately with AGIexceeding $155,650). Additional standarddeduction amounts are available for those 65and older or blind. Special rules apply if youcan be claimed as a dependent by someoneelse.

Choosing an income tax filingstatus

Your filing status is especially importantbecause it determines, in part, the tax rateapplied to your taxable income, the amount ofyour standard deduction, and the types ofdeductions and credits available. Because youmay have more than one option, make sureyou understand the qualifications. Your filingstatus is determined as of the last day of thetax year (December 31). There are fivepossible filing statuses:

Single

To use the single status, you must beunmarried or separated from your spouse byeither divorce or a written separatemaintenance decree on the last day of theyear.

Married filing jointly

Generally, you must be married and living withyour spouse; you can be married and livingapart provided that you are not legallyseparated under a divorce decree or separatemaintenance agreement. When filing jointly,you and your spouse combine your income,exemptions, deductions, and credits.

Married filing separately

You must be married on the last day of theyear. Here, you'd report only your own incomeand claim only your own deductions andcredits.

Head of household

You must be a U.S. citizen or resident alien forthe entire year and: (1) be unmarried at theend of the year (an exception applies if youlive apart from a spouse and meet certaincriteria); (2) maintain a household for yourchild, dependent parent, or other qualifyingdependent relative (the household must beyour home and generally the main home ofthe qualifying individual for more than half ofthe year); and (3) provide more than half thecost of maintaining the household.

Qualifying widow(er) with dependent child

To claim this filing status, all of the followingmust be true: (1) your spouse died in eitherthe last tax year or the tax year before that; (2)you qualified to file a joint return with yourspouse for the year he or she died; (3) youhave not remarried before the end of the taxyear; (4) you have a qualifying dependentchild; and (5) you provide over half the cost ofkeeping up a home for yourself and yourqualifying child.

The federal income taxsystem is progressive, withhigher tax rates applying asthe level of taxable incomeincreases. There are seventax rate brackets rangingfrom 10% to 39.6%.

Page 5 of 17, see disclaimer on final page

Determining your tax

The federal income tax system is progressive, with higher tax rates applying as the level oftaxable income increases. There are seven tax rate brackets ranging from 10% to 39.6%. A taxrate bracket is the tax rate that applies to a specified range of taxable income. For example, ifyou file as single for 2016, the first $9,275 of your taxable income is taxed at a rate of 10%, butthe next dollar in taxable income is taxed at a rate of 15%. You'll generally calculate your tax bylooking up your taxable income in a tax table, or by using a tax rate schedule specific to yourfiling status.

There are, however, a number of complicating factors in determining the correct amount of tax.For example, special rules and rates apply to long-term capital gains and qualified dividends. Youmight also be affected by the alternative minimum tax (AMT), rules that apply to a child'sunearned income (i.e., the "kiddie tax" rules), or the 3.8% net investment income tax that applieson the unearned investment income of some high-income individuals.

Fundamentals at a glance

Page 6 of 17, see disclaimer on final page

2016 Federal Income Tax Rates for IndividualsSingle taxpayers

If taxable income is: Your tax is:

Not over $9,275 10% of taxable income

Over $9,275 to $37,650 $927.50 + 15% of the excess over $9,275

Over $37,650 to $91,150 $5,183.75 + 25% of the excess over $37,650

Over $91,150 to $190,150 $18,558.75 + 28% of the excess over $91,150

Over $190,150 to $413,350 $46,278.75 + 33% of the excess over $190,150

Over $413,350 to $415,050 $119,934.75 + 35% of the excess over $413,350

Over $415,050 $120,529.75 + 39.6% of the excess over $415,050

Married filing jointly and qualifying widow(er)

If taxable income is: Your tax is:

Not over $18,550 10% of taxable income

Over $18,550 to $75,300 $1,855 + 15% of the excess over $18,550

Over $75,300 to $151,900 $10,367.50 + 25% of the excess over $75,300

Over $151,900 to $231,450 $29,517.50 + 28% of the excess over $151,900

Over $231,450 to $413,350 $51,791.50 + 33% of the excess over $231,450

Over $413,350 to $466,950 $111,818.50 + 35% of the excess over $413,350

Over $466,950 $130,578.50 + 39.6% of the excess over $466,950

Married individuals filing separately

If taxable income is: Your tax is:

Not over $9,275 10% of taxable income

Over $9,275 to $37,650 $927.50 + 15% of the excess over $9,275

Over $37,650 to $75,950 $5,183.75 + 25% of the excess over $37,650

Over $75,950 to $115,725 $14,758.75 + 28% of the excess over $75,950

Over $115,725 to $206,675 $25,895.75 + 33% of the excess over $115,725

Over $206,675 to $233,475 $55,909.25 + 35% of the excess over $206,675

Over $233,475 $65,289.25 + 39.6% of the excess over $233,475

Heads of household

If taxable income is: Your tax is:

Not over $13,250 10% of taxable income

Over $13,250 to $50,400 $1,325 + 15% of the excess over $13,250

Over $50,400 to $130,150 $6,897.50 + 25% of the excess over $50,400

Over $130,150 to $210,800 $26,835 + 28% of the excess over $130,150

Over $210,800 to $413,350 $49,417 + 33% of the excess over $210,800

Over $413,350 to $441,000 $116,258.50 + 35% of the excess over $413,350

Over $441,000 $125,936 + 39.6% of the excess over $441,000

Page 7 of 17, see disclaimer on final page

Deductions

"Above" vs. "below" the line

Adjustments to income are deductions that aresubtracted from your total, or gross, income toarrive at your adjusted gross income (AGI).These deductions are often described as"above-the-line" deductions because they arefactored in above the line on which AGI iscalculated. Note that you can claim anyabove-the-line deductions to which you areentitled regardless of whether you itemizedeductions on IRS Form 1040, Schedule A.

Common "above-the-line" deductions• Educator expenses• Health savings account deduction• Moving expenses• Deductible part of self-employment tax• Contributions by self-employed

individuals to SEP, SIMPLE, andqualified plans

• Health insurance deduction(self-employed individuals)

• Alimony paid• Deductible contributions to a traditional

IRA• Student loan interest deduction• Deduction for qualified higher-education

expenses (tuition and fees)*

*Available for 2016, but not for 2017(absent new legislation)

Other deductions are factored in after AGI iscalculated. It's important to note that these"below-the-line" deductions provide a taxbenefit only if you itemize deductions onSchedule A, and generally only if yourSchedule A itemized deductions are greaterthan your standard deduction amount. Note aswell that the allowable amount of some ofthese deductions depends in part on theamount of your AGI. For example, medicaldeductions are allowed only to the extent thatthey exceed 10% of AGI (7.5% for those 65and older).

Standard deduction

The standard deduction is a fixed dollaramount, indexed annually for inflation, that isdetermined according to your filing status(e.g., married filing jointly, single). Anadditional standard deduction amount appliesif you (or your spouse, if you're married andfile a joint return) are age 65 or older. Anadditional standard deduction amount alsoapplies for individuals who are blind.

2016 Standard Deduction Amounts

Filing Status / Factors 2016

Married filing jointly or qualifyingwidow(er)

$12,600

Head of household $9,300

Single $6,300

Married filing separately $6,300

Additional deduction for age 65+or blind (single or head ofhousehold)

$1,550

Additional deduction for age 65+or blind (all other filing statuses)

$1,250

Example: For tax year 2016, Jack, 62, andJill, 47, are married filing jointly. Neither isblind. They decide not to itemize theirdeductions. Their standard deduction is$12,600. If Jack was blind, their standarddeduction would be $12,600 plus $1,250, or$13,850. If both were blind, their standarddeduction would be $12,600 plus $2,500, or$15,100. If both were blind and Jack was also65, their standard deduction would be $12,600plus $3,750, or $16,350. If both were over 65and blind, their standard deduction would be$12,600 plus $5,000, or $17,600.

Note: If you can be claimed as a dependenton another taxpayer's tax return, yourstandard deduction in 2016 is generally limitedto the greater of (a) $1,050 or (b) the sum of$350 and your earned income for the year butnot more than the standard deduction youcould otherwise have claimed (if you could notbe claimed as an exemption by someoneelse).

Itemized deductions

Itemized deductions are various deductionsreported and claimed on Schedule A of yourfederal income tax return (Form 1040). Theyinclude certain personal expenses, such asmedical expenses, mortgage interest, statetaxes, charitable contributions, theft losses,and miscellaneous itemized deductions. If youhave enough of these types of expenses, youritemized deductions may exceed the standarddeduction to which you're entitled. In thatcase, itemizing deductions may beadvantageous. If your itemized deductions areless than your standard deduction, you'llgenerally want to use the standard deduction.

Page 8 of 17, see disclaimer on final page

There are a few things worth noting, however.First, if you file your tax return using themarried filing separately status and yourspouse itemizes deductions, you cannot takea standard deduction. Any deductions youtake must be itemized. Second, if you aresubject to the alternative minimum tax (AMT)(discussed later), you might be better offitemizing your deductions even though yourtotal itemized deductions do not exceed yourstandard deduction--that's because thestandard deduction is reduced to zero for AMTpurposes. Finally, itemized deductions arelimited once your AGI reaches a certain level.

Itemized Deduction Breakdown for 2013Tax Year

Based on percentage of total itemizeddeduction dollars for 2013 tax year.

Source: Table 1, Individual Income TaxReturns: Selected Income and Tax Items(based on tax year 2013 preliminary data),www.irs.gov, 4/6/15

2016 AGI Thresholds for ItemizedDeduction Limitation

Filing Status AGIThreshold

Married filing jointly orqualified widow(er)

$311,300

Head of household $285,350

Single $259,400

Married filing separately $155,650

Note: Total itemized deductions must bereduced by the smaller of (a) 3% of theamount by which your AGI exceeds the AGIthreshold for your filing status or (b) 80% ofyour itemized deductions that are affected bythe limitation. Deduction amounts relating tomedical and dental expenses, investmentinterest expenses, nonbusiness casualty andtheft losses, and gambling losses are notsubject to this limitation.

Timing or "bunching"deductions

For most people, income is reported in theyear that it's received, while deductions aregenerally taken for the year in which theexpenses are paid. In many cases, you cancontrol whether you incur an expense thisyear or next. That means you can control thetiming of your itemized deductions to someextent. For example, paying medical expensesin December rather than in January potentiallyaccelerates the deduction for those expensesinto the earlier year. Postponing major dentalwork--scheduled for December--to Januarywould delay the expense, and the resultingdeduction, until the following year.

Why would you want to do that? One reasonmight be if those deductions are worth more toyou in one year than in the other. Forexample, if you're in a higher income taxbracket this year than you expect to be in nextyear, you may want to accelerate yourdeductions into the current year to helpminimize your tax liability. Or, if you find thatyour itemized deductions typically fall justshort of the standard deduction amount thatapplies to you, you might try "bunching"deductions in alternate years to exceed thestandard deduction amount in those years.

For example, let's say that you file as singleand have total itemized deductions of $6,250for 2016--less than the $6,300 standarddeduction amount for 2016. Let's assume as

Of an estimated 147.7million federal income taxreturns filed for the 2013 taxyear, just over 44 millionclaimed itemizeddeductions.

Source: Table 1, IndividualIncome Tax Returns:Selected Income and TaxItems (based on tax year2013 preliminary data),www.irs.gov , 4/6/15

Page 9 of 17, see disclaimer on final page

well that you will be in a similar situation nextyear, with itemized deductions that equal yourstandard deduction amount. In this situation,your itemized deductions provide no taxbenefit. Consider what would happen,however, if you were able to defer $1,000 inallowable deductions to next year. Therewould be no effect on your 2016 taxes, sinceyou were already claiming the standarddeduction amount. But next year, youritemized deductions would exceed yourstandard deduction amount by $1,000, givingyou an additional $1,000 in deductions thatwould otherwise have been lost.

Bunching deductions can also help at a moregranular level. Some deductions are subject toan AGI threshold. For example, medical anddental expenses are generally deductible onlyto the extent that unreimbursed expensesexceed 10% of your AGI (7.5% of AGI through2016 if you or your spouse are age 65 orolder). If you're close but under the AGIthreshold, consider whether taking steps to"bunch" medical expenses into a single yearmight allow you to exceed the threshold in agiven year, resulting in additional deductionsthat would otherwise have been lost.

Tax Credits

What is a tax credit?

A tax credit results in a dollar-for-dollar reduction of your tax liability. After you calculate theamount of tax for which you are liable, based on your taxable income, you subtract the totalamount of any tax credits for which you are eligible. In some cases, if your tax credits exceedyour tax liability, you will be able to claim the difference as a refund.

What's the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income. Because your federal income tax is based on yourtaxable income, a tax deduction will decrease the amount of tax owed. The extent to which adeduction reduces tax, though, depends on your marginal federal income tax bracket. The higherthe rate at which you're paying tax, the more a tax deduction reduces your tax liability. Here's anexample: If you're in the 28% marginal tax bracket and have $1,000 in tax deductions, your taxliability will be reduced by $280. That same $1,000 tax deduction would result in a $350 reductionin tax liability if you are in the 35% marginal tax bracket.

A tax credit, on the other hand, is a dollar-for-dollar reduction. A tax credit of $1,000 will reduceyour tax liability by $1,000, regardless of your tax bracket.

Refundable vs. nonrefundable tax credits

Most tax credits are nonrefundable. That means a tax credit can reduce your tax liability to zero.If there's any credit remaining after offsetting all tax liability, it is generally lost, or in some casescarried over to other years.

Credits that are refundable are paid to you even if there is credit left over after reducing your taxliability to zero.

Common tax credits for individuals

Tax Credits That Are Refundable or Partially Refundable

Earned incometax credit

This is a credit for certain lower- and moderate-income people who work.The amount of the credit is based on your adjusted gross income (AGI),your filing status, and the number of qualifying children you have (if any).The maximum earned income tax credit for 2016 is $6,269, which applies totaxpayers with 3 or more qualifying children, and AGI below $23,740(married filing jointly) or $18,190 (other qualifying filing statuses).

Child tax credit A credit of $1,000 for each qualifying child you claim on your return. Thecredit is limited if your modified AGI is above a certain amount ($75,000 iffiling status single, $110,000 if married filing jointly, $55,000 if married filingseparately). Up to 15% of earned income in excess of $3,000 is refundable.

Page 10 of 17, see disclaimer on final page

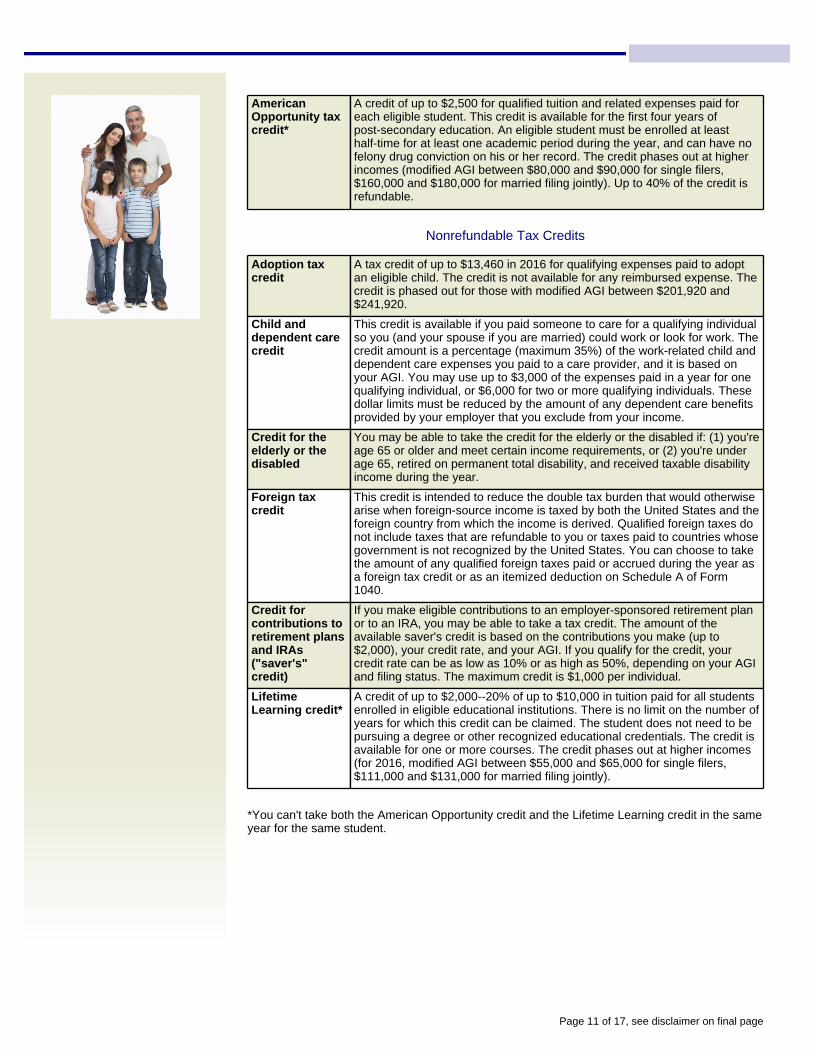

AmericanOpportunity taxcredit*

A credit of up to $2,500 for qualified tuition and related expenses paid foreach eligible student. This credit is available for the first four years ofpost-secondary education. An eligible student must be enrolled at leasthalf-time for at least one academic period during the year, and can have nofelony drug conviction on his or her record. The credit phases out at higherincomes (modified AGI between $80,000 and $90,000 for single filers,$160,000 and $180,000 for married filing jointly). Up to 40% of the credit isrefundable.

Nonrefundable Tax Credits

Adoption taxcredit

A tax credit of up to $13,460 in 2016 for qualifying expenses paid to adoptan eligible child. The credit is not available for any reimbursed expense. Thecredit is phased out for those with modified AGI between $201,920 and$241,920.

Child anddependent carecredit

This credit is available if you paid someone to care for a qualifying individualso you (and your spouse if you are married) could work or look for work. Thecredit amount is a percentage (maximum 35%) of the work-related child anddependent care expenses you paid to a care provider, and it is based onyour AGI. You may use up to $3,000 of the expenses paid in a year for onequalifying individual, or $6,000 for two or more qualifying individuals. Thesedollar limits must be reduced by the amount of any dependent care benefitsprovided by your employer that you exclude from your income.

Credit for theelderly or thedisabled

You may be able to take the credit for the elderly or the disabled if: (1) you'reage 65 or older and meet certain income requirements, or (2) you're underage 65, retired on permanent total disability, and received taxable disabilityincome during the year.

Foreign taxcredit

This credit is intended to reduce the double tax burden that would otherwisearise when foreign-source income is taxed by both the United States and theforeign country from which the income is derived. Qualified foreign taxes donot include taxes that are refundable to you or taxes paid to countries whosegovernment is not recognized by the United States. You can choose to takethe amount of any qualified foreign taxes paid or accrued during the year asa foreign tax credit or as an itemized deduction on Schedule A of Form1040.

Credit forcontributions toretirement plansand IRAs("saver's"credit)

If you make eligible contributions to an employer-sponsored retirement planor to an IRA, you may be able to take a tax credit. The amount of theavailable saver's credit is based on the contributions you make (up to$2,000), your credit rate, and your AGI. If you qualify for the credit, yourcredit rate can be as low as 10% or as high as 50%, depending on your AGIand filing status. The maximum credit is $1,000 per individual.

LifetimeLearning credit*

A credit of up to $2,000--20% of up to $10,000 in tuition paid for all studentsenrolled in eligible educational institutions. There is no limit on the number ofyears for which this credit can be claimed. The student does not need to bepursuing a degree or other recognized educational credentials. The credit isavailable for one or more courses. The credit phases out at higher incomes(for 2016, modified AGI between $55,000 and $65,000 for single filers,$111,000 and $131,000 for married filing jointly).

*You can't take both the American Opportunity credit and the Lifetime Learning credit in the sameyear for the same student.

Page 11 of 17, see disclaimer on final page

Investment Tax Basics

Ordinary income

Examples of ordinary income include wages,tips, commissions, alimony, and rentalincome. Investments often produce ordinaryincome in the form of interest. Manyinvestments--including savings accounts,certificates of deposit, money marketaccounts, annuities, bonds, and somepreferred stock--can generate ordinaryincome. Ordinary income is taxed at ordinary,or regular, income tax rates.

Note: It's possible for an investment togenerate an ordinary loss, rather than ordinaryincome. In general, ordinary losses reduceordinary income.

Capital gain and loss

If you sell stocks, bonds, or other capitalassets for more or less than you paid for them,you'll end up with a capital gain or loss.Special capital gain tax rates may apply.These rates may be lower than ordinaryincome tax rates.

Understanding basis

Generally speaking, basis refers to theamount of your investment in an asset. Yourinitial basis usually equals your cost--what youpaid for the asset. For example, if youpurchased one share of stock for $100, yourinitial basis in the stock is $100. However,your initial basis can differ from the cost if youdid not purchase an asset but rather receivedit as a gift or inheritance, or in a tax-freeexchange.

Your initial basis in an asset can increase ordecrease over time. For example, if you buy ahouse for $100,000, your initial basis in thehouse will be $100,000. If you later improveyour home by installing a $5,000 deck, youradjusted basis in the house may be $105,000.You should be aware of items that increase ordecrease the basis of your asset. For adetailed discussion of basis and adjustmentsto basis, see IRS Publication 551, Basis ofAssets.

Calculating gain or loss

Capital gain (or loss) equals the amount thatyou realize on the sale of your asset (i.e., theamount of cash and/or the value of anyproperty you receive) less your adjusted basisin the asset. If you sell an asset for more thanyour adjusted basis, you'll have a capital gain.

For example, assume you had an adjustedbasis in stock of $10,000. If you sell the stockfor $15,000, your capital gain will be $5,000. Ifyou sell an asset for less than your adjustedbasis in the asset, you'll have a capital loss.

Short term vs. long term

Generally, the amount of time that you'veowned an asset is referred to as your holdingperiod. A capital gain is classified as shortterm if the asset was held for one year or less,and long term if the asset was held for morethan one year.

Whether your capital gain is classified as shortterm or long term can make a difference inhow you calculate tax. Short-term capitalgains are taxed at the same rate as yourordinary income. The tax rates that apply tolong-term capital gains, however, aregenerally lower than ordinary income taxrates.

You can use capital losses from oneinvestment to offset the capital gainsfrom other investments (specialordering rules apply in netting gainsand losses). If your total capital lossesexceed your total capital gains, youcan generally use your excess capitalloss to offset up to $3,000 of ordinaryincome in a tax year ($1,500 formarried persons filing separately).Losses not used in one year can becarried forward to future years.

Long-term capital gain

For long-term capital gains, special tax ratesapply. The maximum tax rate at which yourlong-term capital gains are taxed depends onwhich ordinary federal income tax rate bracketyou fall into.

If your taxable income places you in thelowest two tax brackets for ordinary incometax purposes, a 0% tax rate generally appliesto long-term capital gains. So, for 2016, if yourfiling status is single and your taxable incomeis less than $37,650, you'll generally pay notax on long-term capital gains.

If you're in the 25%, 28%, 33%, or 35% taxbrackets, the maximum rate that applies tolong-term capital gains is generally 15%. Ifyou're in the top federal tax bracket (39.6%),the maximum tax rate that applies is generally20%.

What is a "wash sale"?

A wash sale occurs when yousell a security at a loss andacquire the same or asubstantially identical security(or an option on such asecurity) within 30 days of thesale (before or after). Anylosses that result from a washsale are disallowed and addedto the cost basis of the stock orsecurities.

Page 12 of 17, see disclaimer on final page

Maximum Long-Term Capital Gain Tax Rate Based on 2016 Taxable Income

Single Married filingjointly

Married filingseparately

Head ofhousehold

Tax rate

Up to $37,650 Up to $75,300 Up to $37,650 Up to $50,400 0%

$37,650 up to$415,050

$75,300 up to$466,950

$37,650 up to$233,475

$50,400 up to$441,000

15%

More than$415,050

More than$466,950

More than$233,475

More than$441,000

20%

Note: Special rates and rules apply to certain types of assets. For example, long-term capitalgain from the sale of collectibles is subject to a 28% tax rate.

Qualified dividends

If you receive dividend income, it may betaxed either at ordinary income tax rates or atthe rates that apply to long-term capital gainincome. If the dividends are qualifieddividends, they're taxed at the same tax ratesthat apply to long-term capital gains. Qualifieddividends are dividends paid to an individualshareholder from a domestic corporation or aqualified foreign corporation, provided that youhold the shares for more than 60 days duringthe 121-day period that begins 60 days beforethe ex-dividend date (a longer holding periodrequirement applies to dividends paid bycertain preferred stock).

Some dividends (such as those from moneymarket funds) continue to be treated asordinary income. Generally, ordinary dividendsare shown in box 1a of Form 1099-DIV, whilequalified dividends are shown in box 1b.

Tax-exempt income

Some income is specifically exempted fromfederal income tax. For example, while theinterest on corporate bonds is subject to tax atthe local, state, and federal level, interest onbonds issued by state and local governments(generically called municipal bonds, or munis)is generally exempt from federal income tax. Ifyou live in the state in which a specificmunicipal bond is issued, it may be tax free atthe state or local level as well. Note that theincome from Treasury securities, which areissued by the U.S. government, is exemptfrom state and local taxes but not from federaltaxes.

Caution: Interest earned on tax-free municipalbonds is generally exempt from state tax if thebond was issued in the state in which youreside, as well as from federal income tax(though earnings on certain private activitybonds may be subject to regular federalincome tax or to the alternative minimum tax).

But if purchased as part of a tax-exemptmunicipal money market or bond mutual fund,any capital gains earned by the fund aresubject to tax, just as any capital gains fromselling an individual bond are. Note also thattax-exempt interest is included in determiningif a portion of any Social Security benefit youreceive is taxable.

The interest received on Series EEsavings bonds is exempt from stateand local income taxes. In addition, theinterest on Series EE bonds purchasedon or after January 1, 1990, may beexempt from federal income taxation ifthe bonds are used for certaineducational purposes and if certainrequirements (including AGI limitations)are met.

Net investment income tax

High-income individuals generally face anadditional 3.8% net investment income tax(also referred to as the unearned incomeMedicare contribution tax) on unearnedincome. This surtax is equal to 3.8% of thelesser of:

• Your net investment income• The amount of your modified AGI

(basically, your AGI increased by anamount associated with any foreign earnedincome exclusion) that exceeds $200,000($250,000 if married filing jointly, $125,000if married filing separately)

So if you're single and have modified AGI of$250,000, consisting of $150,000 in earnedincome and $100,000 in net investmentincome, the 3.8% net investment income taxwill apply only to $50,000 of your investmentincome.

Net investment income generally includes allnet income (income less any allowableassociated deductions) from interest,

What is the "kiddie tax"?

Special rules commonlyreferred to as the "kiddie tax"rules apply when a child hasunearned income (for example,investment income). Childrensubject to the kiddie tax aregenerally taxed at their parents'tax rate on any unearnedincome over a certain amount.For 2016, this amount is$2,100 (the first $1,050 isgenerally tax free and the next$1,050 is taxed at the child'srate). The kiddie tax rules applyto (1) those under age 18, (2)those age 18 whose earnedincome doesn't exceedone-half of their support, and(3) those ages 19 to 23 whoare full-time students andwhose earned income doesn'texceed one-half of theirsupport.

Page 13 of 17, see disclaimer on final page

dividends, capital gains, annuities, royalties,and rents. It also includes income from anybusiness that's considered a passive activity,or any business that trades financialinstruments or commodities.

Note: Net investment income does not includeinterest on tax-exempt bonds, or any gainfrom the sale of a principal residence that isexcluded from income. Distributions you takefrom a qualified retirement plan, IRA, IRCSection 457(b) deferred compensation plan, orIRC Section 403(b) retirement plan are alsonot included in the definition of net investmentincome.

Tax-advantaged savingsvehicles

Taxes can take a bite out of your totalinvestment returns, so it's helpful to considertax-advantaged savings vehicles whenbuilding a portfolio. Some tax-advantagedsavings vehicles allow you to defer payingtaxes on earnings until some point in thefuture, while other tax-advantaged savingsvehicles allow earnings to escape taxationaltogether under certain circumstances.

Tax-advantaged savings vehicles forretirement

Traditional IRAs: Anyone under age 70½who earns income or is married to someonewith earned income can contribute to atraditional IRA. Depending upon your incomelevel and whether you're covered by anemployer-sponsored retirement plan, you mayor may not be able to deduct yourcontributions to a traditional IRA. Yourcontributions always grow tax deferred, butyou'll owe income taxes when you make awithdrawal.* For 2016, you can contribute upto $5,500 to an IRA, and individuals age 50and older can contribute an additional $1,000.

Roth IRAs: Roth IRA contributions can bemade only by individuals with incomes belowcertain limits. Your contributions are madewith after-tax dollars but will grow tax deferred,and qualified distributions (those satisfying afive-year holding period and made after age59½ or after becoming disabled) will be taxfree when you withdraw them. The amountyou can contribute is the same as fortraditional IRAs. Total combined contributionsto Roth and traditional IRAs cannot exceed$5,500 for 2016 for individuals under age 50.

SIMPLE IRAs and SIMPLE 401(k)s: Theseplans are generally associated with smallbusinesses. As with traditional IRAs, yourcontributions grow tax deferred, and you'll owe

income taxes when you make a withdrawal.*For 2016, you can contribute up to $12,500 toone of these plans; individuals age 50 andolder can contribute an additional $3,000.(SIMPLE 401(k) plans may also allow Rothcontributions.)

Employer-sponsored plans (401(k)s,403(b)s, 457 plans): Contributions (typicallymade on a pre-tax basis) to these plans growtax deferred, but you'll owe income taxeswhen you make a withdrawal.* For 2016, youcan contribute up to $18,000 to one of theseplans; individuals age 50 and older cancontribute an additional $6,000. Employersgenerally allow employees to make after-taxRoth contributions in lieu of pre-taxcontributions, in which case qualifyingdistributions will be tax free.

Annuities: You pay money to an annuityissuer (an insurance company), and the issuerpromises to pay principal and earnings back toyou or your named beneficiary in the future(you'll be subject to fees and expenses thatyou'll need to understand and consider).Annuities generally allow you to elect anincome stream for life (subject to the financialstrength and claims-paying ability of theissuer). There's no limit to how much you caninvest, and your contributions grow taxdeferred. However, you'll owe income taxeson the earnings when you start receivingdistributions.*

*Withdrawals prior to age 59½ may be subjectto a 10% federal income tax penalty unless anexception applies (the penalty may be 25% inthe case of a SIMPLE IRA if withdrawals aretaken within two years of beginningparticipation in the plan).

Tax-advantaged savings vehicles forcollege

529 plans: College savings plans and prepaidtuition plans let you set aside money forcollege. Your contributions grow tax deferredand can be withdrawn tax free at the federallevel if the funds are used for qualifiededucation expenses.** These plans are opento anyone regardless of income level.Contribution limits are high--typically over$300,000--but vary by plan.

Coverdell ESA: Coverdell education savingsaccounts are open only to individuals withincomes below certain limits. But if you qualify,you can contribute up to $2,000 per year, perbeneficiary. Your contributions grow taxdeferred and can be withdrawn tax free at thefederal level if the funds are used for qualifiededucation expenses.**

Page 14 of 17, see disclaimer on final page

Note: Investors should consider theinvestment objectives, risks, charges, andexpenses associated with 529 plans. Moreinformation about specific 529 plans isavailable in each issuer's official statement,which should be read carefully beforeinvesting. Before investing, consider whetheryour state offers a 529 plan that providesresidents with favorable state tax benefits. The

**Earnings are subject to federal income taxand potentially a 10% penalty tax if the fundsare not used for qualified education expenses.

availability of tax and other benefits may beconditioned on meeting certain requirements.There is also the risk that the investments maylose money or not perform well enough tocover college costs as anticipated.

Understanding the Alternative Minimum Tax (AMT)

What is the AMT?

The AMT is essentially a separate federalincome tax system with its own tax rates andits own set of rules governing the recognitionand timing of income and expenses. If you'resubject to the AMT, you have to calculate yourtaxes twice--once under the regular taxsystem and again under the AMT system. Ifyour income tax liability under the AMT isgreater than your liability under the regular taxsystem, the difference is reported as anadditional tax on your federal income taxreturn. If you're subject to the AMT in oneyear, you may be entitled to a credit that canbe applied against regular tax liability in futureyears.

Who is liable for the AMT?

Key AMT "triggers" include the number ofpersonal exemptions you claim, yourmiscellaneous itemized deductions, and yourstate and local tax deductions. So, forexample, if you have a large family and live ina high-tax state, there's a good possibility thatyou might have to contend with the AMT. IRSForm 1040 instructions include a worksheetthat may help you determine whether you'resubject to the AMT (an electronic version ofthis worksheet is also available on the IRSwebsite), but you might need to complete IRSForm 6251 to know for sure.

Common AMT adjustments

Here are some of the more common AMTadjustments.

Standard deduction and personalexemptions

The federal standard deduction, generallyavailable under the regular tax system if you

Itemized deductions

Under the AMT calculation, no deduction isallowed for state and local taxes paid, or forcertain miscellaneous itemized deductions.Your deduction for medical expenses mayalso be reduced if you or your spouse are age65 or older (the AMT adjustment for medicalexpenses effectively applies only to those whohave reached age 65 and therefore have alower AGI threshold for deducting medicalexpenses on Schedule A), and you can onlydeduct qualifying residence interest (e.g.,mortgage or home equity loan interest) to theextent the loan proceeds are used topurchase, construct, or improve a principalresidence.

Exercise of incentive stock options (ISOs)

Under the regular tax system, tax is generallydeferred until you sell the acquired stock. Butfor AMT purposes, when you exercise an ISO,income is generally recognized to the extentthat the fair market value of the acquiredshares exceeds the option price. This meansthat a significant ISO exercise in a year cantrigger AMT liability. If ISOs are exercised andsold in the same year, however, no AMTadjustment is needed, since any incomewould be recognized for regular tax purposesas well.

Depreciation

If you're depreciating assets (for example, ifyou're a sole proprietor and own an asset forbusiness use), you'll have to calculatedepreciation twice--once under regular incometax rules and once under AMT rules.

don't itemize deductions, is not allowed forpurposes of calculating the AMT. Nor can youtake a deduction for personal exemptions.

Key AMT "triggers" includethe number of personalexemptions you claim, yourmiscellaneous itemizeddeductions, and your stateand local tax deductions.

Page 15 of 17, see disclaimer on final page

AMT exemption amounts

While the AMT takes away personalexemptions and a number of deductions, itprovides specific AMT exemptions. Theamount of AMT exemption to which you'reentitled depends on your filing status.

Your exemption amount, however, begins tophase out once your taxable income exceedsa certain threshold. (Specifically, yourexemption amount is reduced by $0.25 forevery $1.00 you have in taxable income overthe threshold amount.)

AMT Exemption Amounts by Filing Status

2016

Married filing jointly $83,800

Single or head of household $53,900

Married filing separately $41,900

AMT Exemption Phaseout Threshold

2016

Married filing jointly $159,700

Single or head of household $119,700

Married filing separately $79,850

Note: In the context of AMT exemptionamounts and tax rates, taxable income reallyrefers to your alternative minimum taxableincome (AMTI). Your AMTI is your regular

The lower maximum tax rates thatgenerally apply to long-term capitalgains and qualified dividends apply tothe AMT calculation as well. So evenunder AMT rules, a maximum rate of20%, 15% (for individuals in the 25%,28%, 33%, or 35% tax bracket), or 0%(for individuals in the 10% or 15% taxbracket) applies. However, long-termcapital gains and qualified dividendsare included when you determine yourtaxable income under the AMT system.That means large capital gains andqualifying dividends can push you intothe phaseout range for AMTexemptions and can indirectly increaseAMT exposure.

Note: When it comes to the phaseout of AMTexemption amounts, a special calculationapplies to individuals who are married filingseparately. These individuals have to add anadditional amount to their AMTI beforecalculating the exemption phaseout.

AMT rates

Under the AMT, the first $186,300 (for 2016)of your taxable income is taxed at a rate of26%. If your filing status is married filingseparately, the 26% rate applies to your first$93,150 (for 2016) of taxable income. Taxableincome above these thresholds is taxed at aflat rate of 28%.

taxable income increased or decreased byAMT preferences and adjustments.

TIP: If you owe AMT, youmay be able to lower yourtotal tax (regular tax plusAMT) by claiming itemizeddeductions on Form 1040,even if your total itemizeddeductions are less than thestandard deduction. This isbecause the standarddeduction is not allowed forthe AMT and, if you claimthe standard deduction onForm 1040, you cannotclaim itemized deductionsfor the AMT.

Source: 2015 Instructionsfor Form 6251, AlternativeMinimum Tax, Individuals

Page 16 of 17, see disclaimer on final page

AICPAPFP

Sandra Truitt220 Leigh Farms Road

Durham, NC 27707919-490-4394

June 20, 2016Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016

IMPORTANT DISCLOSURES

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. Theinformation presented here is not specific to any individual's personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot beused, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer shouldseek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publiclyavailable information from sources believed to be reliable—we cannot assure the accuracy or completenessof these materials. The information in these materials may change at any time and without notice.

Page 17 of 17

Related Documents