2016 Capital Market Assumptions February 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2016CapitalMarketAssumptionsFebruary2016

TABLEOFCONTENTS

TABLEOFCONTENTS............................................................................................................................................................2

INTRODUCTION.......................................................................................................................................................................3

INFLATION.................................................................................................................................................................................7

FIXEDINCOME..........................................................................................................................................................................8

CashEquivalents...............................................................................................................................................................11

Low‐DurationFixedIncome........................................................................................................................................12

CoreFixedIncome............................................................................................................................................................13

Non‐CoreFixedIncome..................................................................................................................................................14

Core‐PlusFixedIncome.................................................................................................................................................16

Long‐DurationFixedIncome.......................................................................................................................................16

USTreasuryInflationProtectedSecurities(TIPS).............................................................................................17

EQUITY.......................................................................................................................................................................................19

USLarge‐CapEquity........................................................................................................................................................20

USSmall/Mid‐CapEquity..............................................................................................................................................22

USEquity..............................................................................................................................................................................22

Non‐USLarge‐CapEquity..............................................................................................................................................23

Non‐USSmall‐CapEquity..............................................................................................................................................24

EmergingMarketsEquity..............................................................................................................................................24

Non‐USEquity....................................................................................................................................................................25

ALTERNATIVES......................................................................................................................................................................26

RealEstate...........................................................................................................................................................................26

DiversifiedInflation‐Related........................................................................................................................................27

MarketableAlternatives................................................................................................................................................28

Non‐MarketableAlternatives......................................................................................................................................28

RISK.............................................................................................................................................................................................29

CORRELATIONCOEFFICIENTS........................................................................................................................................33

SOURCES...................................................................................................................................................................................35

1

INTRODUCTIONSellwoodConsultingupdatesitscapitalmarketsassumptionsonanannualbasis.Our2016assumptionsreflectinformationasofDecember31,2015,unlessotherwisenoted.Thisreportdocumentsourprocessforcreatingthesecapitalmarketsassumptions,andweprovidedetailedmethodologyforeach.Severalover‐archingprinciples,however,informallofouranalysis:

1. Webelievethatforward‐lookingcapitalmarketassumptionsareanimportant,butfarfromtheonlyimportant,inputforproperlyconstructingportfolios.Greatcareshouldbetakennottorelyonlyonmean‐varianceanalysiswhenconstructingportfolios.Generallyspeaking,ananalysisthatreliesonlyonmean‐varianceanalysiswillover‐allocatetoassetswithinsignificantlysuperiorrisk/returnestimates,andassetsthatarelessliquidorlessfrequentlypriced.

2. Ourassumptionsareforward‐lookinginnatureandreflectaten‐yearhorizon.Theyareappropriateforanalysisofportfolioswithlong‐term(10yearorgreater)horizons.Forportfolioswithshorterhorizons,alternatemethodsofanalysisshouldbeemployed.

3. Wepurposefullyusedifferentmethodstoestimatereturnandrisk.Thefirstpartofthispaperexplainsthedifferentmethodsweemploytoestimatethefuturereturnofeachindividualassetclass.Laterinthepaper,weexplainamorestandardizedapproachtoestimatingfutureriskofthesameassetclasses.

4. Ourreturnassumptionsutilizeabuild‐upapproachbasedonthecurrentvaluesoftheindividualdriversofexpectedreturnthatareuniquetoeachassetclass.

5. Forassetclasseswherethemarketprovidesacurrentviewofforward‐lookingreturns,ourassumptionsheavilyweightthemarketview.

6. Wherepossible,allofourreturnassumptionsincorporatecurrentvaluations.Wherewehaveidentifiedacurrentvaluationanditslong‐termmean,ourestimatesconsidera50%reversionfromthecurrentvaluationleveltoitslong‐termmeanovertheprospectiveten‐yearperiod.

7. Ourassumptionsarepresentedinnominalterms.Wherewehaveusedhistoricalreturnsinourinputanalysis,wehavealwaystransformedthemtoreal,after‐inflation,returns,soastostripouthistoricalinflation.Attheendofthebuild‐upprocess,whereappropriate,weaddthemarket’scurrentmeasureofforward‐lookinginflationbacktotheassumptionstocreatenominalforward‐lookingreturnassumptions.

8. Ourbasereturncalculationsareofandforcompoundreturns.Aftercalculatingacompoundreturnandariskassumption,wecombinethetwomathematicallytocalculate

2

anarithmeticaverageexpectedreturn,whichisanecessaryinputformean‐varianceanalysis.

9. Ourassumptionsarepassiveinnatureandassumenoactivemanagement.

10. Ourapproachtomodelingtheexpectedriskofeachassetcategoryismulti‐faceted.First,weexaminethehistoricalstandarddeviationofthereturnsforaproxyindexfortheassetcategory(boththefullhistoryandmostrecent10years).Next,weexaminethehistoricalworst‐caseannualreturnexperience(orinthecaseofassetcategoriesthatarenotpricedtomarket,themaximumtwo‐yearpeak‐to‐troughexperience)fortheassetclass.Ifnecessary,weadjustourriskestimatesupwardtoensurethattheactualworst‐caseexperiencehadatleasta2%probabilityofoccurring(onceevery50years)underourassumedreturnandriskdistributionparameters.Finally,forassetclasseswhereourconfidenceinthedataavailableforexaminationislimited,wequalitativelyadjustourriskassumptiontoreflectthisuncertainty.

11. Ourcorrelationcoefficientassumptionsaremostlyderivedfromhistory,withanemphasis

ontherecentpast.Weseekaproxyforeachassetcategorywehavemodeledwithaslongahistoryaspossible,andthencalculateourcorrelationassumptionsusingasimpleaverageofthefollowing,foreachpairofassetcategories:

Longest‐termcorrelation 10‐yearcorrelation 5‐yearcorrelation 3‐yearcorrelation

Thisapproachpurposefullyoverweightstherecentpast,whileacknowledgingthelong‐termpast.Itisalsoamoreconservativemeasureforcorrelationbenefittoaportfolio,becauserecentcorrelationshavebeenhigherthantheyhavebeenhistorically.

12. Weroundourassumptionstothenearest10basispoints,inthecaseofarithmeticaveragereturn,andnearest25basispoints,inthecaseofrisk.

13. OurassumptionsareapplicabletoUS‐based,non‐taxableinvestors.FortaxableclientslocatedintheUnitedStates,wemaintainaseparatemethodologythatconsiderstheeffectsoftaxesonexpectedreturnsandrisk.

14. Wehavestrivedtoconstructasetofassumptionsthatisstraightforward,explainable,fullydocumented,andreplicablebyotherresearchers.Ourassumptionsareascomplexasnecessarybutnomorecomplexthannecessary,andtheyhavenohiddenconstraints.Wecouldmakethemmorecomplicated,butwedonotbelievethatdoingsowouldmakethembetter.

Insummaryform,our2016forward‐lookingassumptionsfollowonthenextpage.

3

NominalCompoundReturn Risk

NominalArithmeticReturn

SharpeRatio

Inflation 1.54% 3.00% 1.60% ‐‐‐

FixedIncome

CashEquivalents 0.30% 1.50% 0.30% ‐‐‐

Low‐DurationFixedIncome 1.39% 3.25% 1.40% 0.34

CoreFixedIncome 2.45% 5.00% 2.60% 0.43

Core‐PlusFixedIncome 2.95% 6.00% 3.10% 0.44

Non‐CoreFixedIncome 4.96% 14.25% 5.90% 0.33

Long‐DurationFixedIncome 3.09% 10.25% 3.60% 0.27

TIPS 1.94% 6.75% 2.20% 0.24

GlobalEquities

USEquity 5.24% 19.00% 6.90% 0.26

USLarge‐CapEquity 5.21% 19.25% 6.90% 0.26

USSmall/Mid‐CapEquity 5.34% 20.25% 7.20% 0.25

Non‐USEquity 6.30% 24.00% 8.80% 0.25

Non‐USLarge‐CapEquity 6.25% 23.50% 8.70% 0.25

Non‐USSmall‐CapEquity 6.50% 27.75% 9.80% 0.22

EmergingMarketsEquity 7.40% 29.75% 11.20% 0.24

Alternatives RealEstate 4.71% 18.75% 6.30% 0.24

DiversifiedInflation‐Related 3.46% 14.25% 4.40% 0.22

MarketableAlternatives 4.94% 12.25% 5.60% 0.38

Non‐MarketableAlternatives 8.10% 31.50% 12.30% 0.25

Inflation

CashLow‐DurFI

CoreFICore+FI

Non‐CoreFI

Long‐DurFI

TIPS

USEquityUSLCEquity USSCEquity

Non‐USEquityNon‐USLCEquity

Non‐USSCEquity

EMEquity

RealEstate

Inflation‐Related

MarketableAlts

Non‐MarketableAlts

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

0% 5% 10% 15% 20% 25% 30% 35%

ExpectedArithmeticReturn

ExpectedRisk(StandardDeviationofReturnDistribution)

2016SellwoodConsultingCapitalMarketAssumptions

4

Historicalreturndistributions(historicalrealreturns,plusourassumedfutureinflation)aredepictedbelowinblue,andourforward‐lookingassumedreturndistributionsareshownintan:

CashEquivalents Low‐Duration FixedIncome

Core FixedIncome Core‐Plus FixedIncome

Non‐Core FixedIncome Long‐Duration FixedIncome

TIPS USEquity

USLarge‐Cap Equity USSMID‐Cap Equity

Non‐US Equity Non‐US Large‐Cap Equity

Non‐US Small‐Cap Equity Emerging Markets Equity

RealEstate DiversifiedInflation Hedges

‐60%

‐53%

‐46%

‐39%

‐32%

‐25%

‐18%

‐11% ‐4%3%

10%17%24%31%38%45%52%59%

Marketable Alternatives

‐60%

‐53%

‐46%

‐39%

‐32%

‐25%

‐18%

‐11% ‐4%3%

10%17%24%31%38%45%52%59%

Non‐Marketable Alternatives

5

INFLATION

Modeled:USCPI‐UInflationCompoundReturn:1.54%

ArithmeticAverageReturn:1.60%Risk:3.00%

Themarkettellsusitsexpectationforforward‐lookingten‐yearinflation,andourassumptionreflectsthatmarketassumption.OnDecember31,2015,themarket’syieldfora10‐YearUSTreasuryBondwas2.27%,andtherealyieldfora10‐YearTIPSsecuritywas0.73%.Thedifferencebetweenthetwoapproximatesthemarket’sinflationexpectationoverthenexttenyears,1.54%.TheFederalReservehaspublishedthisinflationapproximation–theso‐called“TIPSbreakevenspread”–since2003.Thefollowingchartdepictsthefullhistoryofthismeasure,laidagainsttheactualsubsequentinflation(asmeasuredbyCPI)thatoccurred.Wehavechosentodepictthefive‐yearTIPSbreakevenspreadandsubsequentfive‐yearinflation,becausethe10‐yearvaluesdonotyetoffersufficientinformationforevaluation.Withtheexceptionofespeciallyilliquidmarketperiods,whichdistortthemeasurebecauseofliquiditydifferencesbetweenTIPSandnominalTreasuryBonds,themeasurehasdoneafairjobofpredictingsubsequentinflationanddoesnotappeartobebiasedpositivelyornegatively.

‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

TIPSBreakevenSpreadandSubsequentCPI‐ 5Years

Subsequent5‐YearCPI 5‐YearBreakevenSpread

6

FIXEDINCOMEFixedincomereturnsareverydependentonentryyields.FortheBarclaysAggregateIndex,since1976,yieldshaveexplained84%ofsubsequent10‐yearreturns:

Itwouldbetemptingtosimplysetourbond‐marketassumptionsasthecurrentyield,buttodosowouldbetoignoreprospectsforchanginginterestrates,changingcompositionofthebondbenchmarks,andthenegativeeffectsofbonddefaults.Instead,webuildavaluationmodelforeachbondcategoryforwhichweassumeareturn.Still,currentyieldsanchorouranalysis:ineachcase,thecompoundreturnassumptionthatwecalculatewiththismodelisclosetothecurrentnominalyieldfortheassetclass.Allofourfixedincomeassumptionsuseanidenticalbuilding‐blockmodelasourbaseanalysis,butwehavemadesomequalitativeadjustmentstotheanalysis,wherenoted.Ourbuildingblockmodelbeginswiththefixedincomeassetclass’scurrentrealyieldandduration.Wethenexaminethelong‐termaverageoftherealyield,andassumethatovertheprospectiveten‐yearperiod,theasset’srealyieldrevertshalfwaytothataverage.Forassetcategoriesthatpayayieldspreadascompensationforhigherrisk,weusesimilarcalculationstoassumethereversionofyieldspreadhalfwaytoitshistoricalaverage.Forthemostpart,weassumethatlong‐termaveragedefaultandrecoveryrateswillpersistintotheprospectiveten‐yearperiod.1Giventheseinputs,wecancalculatetheasset’sexpectedforward‐looking10‐yearreturn.Ratherthanrelyingonhistoricalreturnandyieldinformation,thisapproachhastheadvantageofbeingresponsivetothechangingcompositionofseveralindexeswemodel.

1OursourceforhistoricaldefaultandrecoveryratesforallbondsisMoodys.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

1976

1977

1978

1980

1981

1983

1984

1985

1987

1988

1990

1991

1993

1994

1995

1997

1998

2000

2001

2002

2004

2005

2007

2008

2010

2011

2012

2014

2015

BarclaysAggregateYield&Subsequent10‐YearReturn

BarclaysAggregateYield Subsequent10‐YearReturn

R2=0.84

7

Inmostcases,wehaveusedthe5‐YearTreasuryBondasourfirstfixedincomebuildingblock–theblockuponwhichwestackyieldspreadsandinflation.Tocalculateitsforward‐lookingten‐yearreturn,webeginwithtoday’srealyield,0.45%.Weassumeten‐yearreversionhalfwaytothelong‐termaveragemeanrealyieldof2.08%.Inordertocapturethelongesttimehorizonpossible,wecalculateallrealyieldsbyadjustingthenominalyieldbyaninflationseries2.Weassumethatthereversiontoameanrealyieldwilloccurinevenincrementsineachofthefuturetenyears.Weassumefurtherthatthesecurity’sdurationwillstayconstantovertheten‐yearperiod.Thelastbuildingblock,thoughitisassumedtobezeroforaTreasurysecurity,isanassumeddefaultrate,adjustedforanassumedrecoveryrate.Finally,becauseallofthisanalysisiscalculatedinrealterms,weaddbackthemarket’sinflationassumptiontoarriveatanominalreturnassumption.Ourcalculationforthe5‐YearUSTreasuryBondfollows.Ourassumptionsare:

Maturity: 5yearsCurrentRealYield: 0.45%Duration: 4.76yearsLong‐TermAverageRealYield: 2.08%CumulativeYieldChange(10Years): +0.81%(halfwayfromcurrenttolong‐termaverage)ExpectedDefaultRate: 0%ExpectedDefaultRecoveryRate: N/A

2 Since2003,ourrealyieldsarebasedontheconstantmaturityTIPSyieldscalculatedbytheFederalReserveformaturitieslongerthan2years.Priorto2003,inordertocalculaterealyieldsweadjustedtheapplicableyieldwiththeprior12‐monthcoreCPIindex.Forexample,fora5‐yearTreasurybond,wecalculateahistoricalrealyieldseriesbysubtractingprior12‐monthcoreCPIfromhistorical5‐yearTreasurybondyieldspriorto2003,andbyusingthethen‐current5‐yearTIPSbreakevenyieldafter2003.Duetoamorestableseries,thecoreCPIindexhasprovenabetterpredictorofsubsequentCPIinflationthanhastheCPIindexitself.

TreasuryBondReturn

YieldSpreadReturn

Inflation

Default/Recovery NegativeReturn

FixedIncomeSecurityReturn

5-Year Treasurys -- Total ReturnYear 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Real Yield 0.45% 0.53% 0.61% 0.69% 0.78% 0.86% 0.94% 1.02% 1.10% 1.18% 1.26%Duration 4.76 4.76 4.76 4.76 4.76 4.76 4.76 4.76 4.76 4.76 4.76 Parallel Yield Change 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.81%12-month return 0.06% 0.14% 0.23% 0.31% 0.39% 0.47% 0.55% 0.63% 0.71% 0.80%Compound Factor 100.06% 100.14% 100.23% 100.31% 100.39% 100.47% 100.55% 100.63% 100.71% 100.80% 4.37% 0.43%

market 10-year inflation 1.54%nominal 10-yr annualized return 1.97%

8

Undertheassumptionswehaveoutlined,thesecurityexpectstoearnarealannualizedcompoundreturnof0.43%overthenext10years.Addingourinflationassumption,wearriveatacompoundreturnassumptionforthesecurity:1.97%annualized.Wehavemadesimilarcalculationsfor10‐and20‐yearTreasurybonds,whicharerelevanttocalculationsofforecastsforcertainbondsoflongermaturities.Thosecalculationsareasfollows:10‐YearTreasuryBondsAssumptions(10‐YearTreasury):

Maturity: 10yearsCurrentRealYield: 0.73%Duration: 8.77yearsLong‐TermAverageRealYield: 2.35%CumulativeYieldChange(10Years): +0.81%(halfwayfromcurrenttolong‐termaverage)ExpectedDefaultRate: 0%ExpectedDefaultRecoveryRate: N/A

Ourprojectednominal10‐yearannualizedreturnis1.92%.20‐YearTreasuryBondsAssumptions(20‐YearTreasury):

Maturity: 20yearsCurrentRealYield: 1.07%Duration: 14.15yearsLong‐TermAverageRealYield: 2.57%CumulativeYieldChange(10Years): +0.75%(halfwayfromcurrenttolong‐termaverage)ExpectedDefaultRate: 0%ExpectedDefaultRecoveryRate: N/A

Ourprojectednominal10‐yearannualizedreturnis1.88%.

10-Year Treasurys -- Total ReturnYear 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Real Yield 0.73% 0.81% 0.89% 0.97% 1.05% 1.13% 1.21% 1.30% 1.38% 1.46% 1.54%Duration 8.77 8.77 8.77 8.77 8.77 8.77 8.77 8.77 8.77 8.77 8.77 Parallel Yield Change 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.81%12-month return 0.02% 0.10% 0.18% 0.26% 0.34% 0.43% 0.51% 0.59% 0.67% 0.75%Compound Factor 100.02% 100.10% 100.18% 100.26% 100.34% 100.43% 100.51% 100.59% 100.67% 100.75% 3.91% 0.38%

market 10-year inflation 1.54%nominal 10-yr annualized return 1.92%

20-Year Treasurys -- Total ReturnYear 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Real Yield 1.07% 1.15% 1.22% 1.30% 1.37% 1.45% 1.52% 1.60% 1.67% 1.75% 1.82%Duration 14.15 14.15 14.15 14.15 14.15 14.15 14.15 14.15 14.15 14.15 14.15 Parallel Yield Change 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.75%12-month return 0.01% 0.08% 0.16% 0.23% 0.31% 0.38% 0.46% 0.53% 0.61% 0.68%Compound Factor 100.01% 100.08% 100.16% 100.23% 100.31% 100.38% 100.46% 100.53% 100.61% 100.68% 3.49% 0.34%

market 10-year inflation 1.54%nominal 10-yr annualized return 1.88%

9

CashEquivalentsModeled:91‐DayT‐Bills

CompoundReturn:0.30%ArithmeticAverageReturn:0.30%

Risk:1.50%WeusethemodeloutlinedaboveforCashEquivalents.Assumptions(91‐DayT‐Bills):

Maturity: 91daysCurrentRealYield: ‐1.82%Duration: 0.25yearsLong‐TermAverageRealYield: 0.90%CumulativeYieldChange(10Years): +1.36%(halfwayfromcurrenttolong‐termaverage)ExpectedDefaultRate: 0%ExpectedDefaultRecoveryRate: N/A

Theseassumptionsyieldanominalcompoundreturnexpectationof0.30%:

Wecautionthatthereisaninherentproblemwithforecastinga10‐yearreturnforanassetthatmaturesevery91days.Nominalcashreturnsarehighlysensitivetonominalshort‐terminterestrates,whichweexpecttobeasvariableoverthenextdecadeastheyhavebeenhistorically.Asillustratedinthechartbelow,whileinvestorstypicallydemandapositiverealyieldfromcash,periodsofnegativerealreturntocashhaveexistedforconsiderableperiodsoftime–includingthemostrecentperiodsince2008.Ourriskassumptionreflectsanappropriaterangeofuncertaintyaroundourreturnprojectionforcashequivalents.

91-Day T-Bills -- Total ReturnYear 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Real Yield -1.82% -1.68% -1.55% -1.41% -1.28% -1.14% -1.00% -0.87% -0.73% -0.60% -0.46%Duration 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 Parallel Yield Change 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 1.36%12-month return -1.85% -1.72% -1.58% -1.45% -1.31% -1.17% -1.04% -0.90% -0.77% -0.63%Compound Factor 98.15% 98.28% 98.42% 98.55% 98.69% 98.83% 98.96% 99.10% 99.23% 99.37% -11.76% -1.24%

market 10-year inflation 1.54%nominal 10-yr annualized return 0.30%

‐6%

‐1%

4%

9%

14%

19%

24%

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Historical RealCashYieldRealCashYield

FederalFundsRate

10

Low‐DurationFixedIncomeModeled:1‐3YearAggregateFixedIncome

CompoundReturn:1.39%ArithmeticAverageReturn:1.40%

Risk:3.25%WeuseourbasemodelforLow‐DurationFixedIncome.Assumptionsfor2‐YearUSTreasuryBond:

Maturity: 2yearsCurrentRealYield: ‐1.01%Duration: 1.96yearsLong‐TermAverageRealYield: 1.73%CumulativeYieldChange(10Years): +1.37%(halfwayfromcurrenttolong‐termaverage)

Theseassumptionsyieldanominalcompoundreturnexpectationof0.88%:

Ourassumptionreflectsa50%proportionofcorporatebonds.Forhalftheassumedportfolio,then,weaddaspreadfor1‐3yearcorporatebonds:Assumptions:

ProportioninCorporates: 50%CurrentSpread: 1.08%Long‐TermAverageSpread: 1.32%SpreadDuration: 1.61yearsCumulativeSpreadChange(10Yrs): +0.12%(halfwayfromcurrenttolong‐termaverage)

Finally,wemakeassumptionsfortheexpecteddefaultrateandrecoveryratefordefaultedsecurities.Thesecalculationsonlyapplytotheproportionoftheassumptionpertainingtocorporatesecurities.Thefollowingfiguresrepresentthehistoricalaveragefortheassetclass:

2-Year Treasurys -- Total ReturnYear 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Real Yield -1.01% -0.87% -0.73% -0.60% -0.46% -0.32% -0.19% -0.05% 0.09% 0.22% 0.36%Duration 1.96 1.96 1.96 1.96 1.96 1.96 1.96 1.96 1.96 1.96 1.96 Parallel Yield Change 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 0.14% 1.37%12-month return -1.28% -1.14% -1.00% -0.87% -0.73% -0.59% -0.46% -0.32% -0.18% -0.05%Compound Factor 98.72% 98.86% 99.00% 99.13% 99.27% 99.41% 99.54% 99.68% 99.82% 99.95% -6.42% -0.66%

market 10-year inflation 1.54%nominal 10-yr annualized return 0.88%

1-3 Year Corporates -- Spread Effect (over Treasurys) Year 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Spread 1.08% 1.09% 1.10% 1.12% 1.13% 1.14% 1.15% 1.16% 1.18% 1.19% 1.20%Duration 1.61 1.61 1.61 1.61 1.61 1.61 1.61 1.61 1.61 1.61 1.61 Parallel Yield Change 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.12%12-month return 1.06% 1.07% 1.08% 1.10% 1.11% 1.12% 1.13% 1.14% 1.16% 1.17%Compound Factor 101.06% 101.07% 101.08% 101.10% 101.11% 101.12% 101.13% 101.14% 101.16% 101.17% 11.72% 1.11%

Proportion 50.00%Spread Effect (Total) 0.56%

11

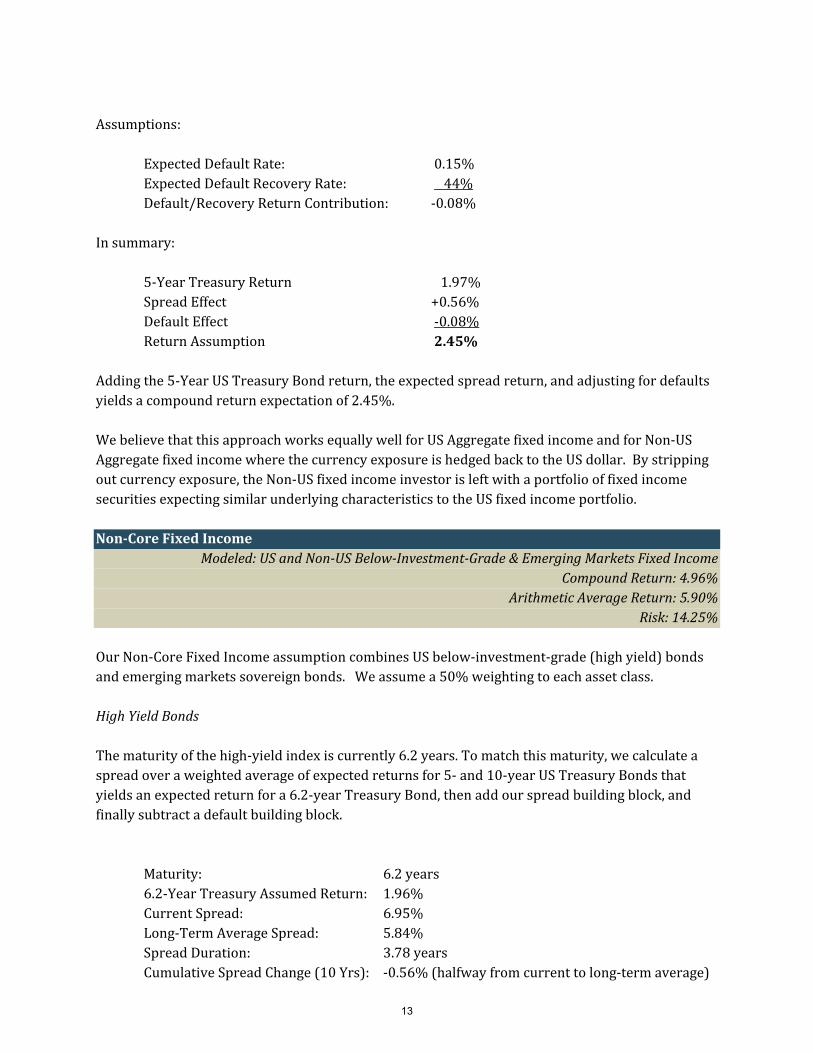

Assumptions:

ExpectedDefaultRate: 0.15%ExpectedDefaultRecoveryRate: 44%Default/RecoveryReturnContribution: ‐0.08%Multipliedby0.5(halfofportfolio); ‐0.04%

Insummary,ourreturnassumptionforlow‐durationfixedincomebuildsupseveralsourcesofreturn:

2‐YearTreasuryReturn 0.88%SpreadEffect +0.56%DefaultEffect ‐0.04%ReturnAssumption 1.39%(differenceexplainedbyrounding)

Combiningthe2‐YearTreasuryBondreturnandtheexpectedreturnfromspread,andthensubtractingtheexpecteddefaultrateafteradjustingforrecovery,yieldsourreturnassumptionof1.39%incompoundterms.CoreFixedIncome

Modeled:USInvestment‐GradeAggregateandHedgedNon‐USAggregateFixedIncomeCompoundReturn:2.45%

ArithmeticAverageReturn:2.60%Risk:5.00%

Thebaselevelofourbuilding‐blockapproachforCoreFixedIncomeisthe5‐YearTreasuryBond,outlinedabove.Tothisexpectedreturn,weaddanexpectationforspreadreturn:

CurrentSpread(BCAggregate): 0.56%Long‐TermAverageSpread: 0.56%SpreadDuration: 3.28yearsCumulativeSpreadChange(10Yrs): +0.00%(halfwayfromcurrenttolong‐termaverage)

Ourassumptionsfordefaultandrecoveryratesareinlinewithhistory.Wesubtractadefaultcontributionbasedontheseinputvariables:

BC Aggregate -- Spread Effect (over Treasurys) Year 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Spread 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56%Duration 3.23 3.23 3.23 3.23 3.23 3.23 3.23 3.23 3.23 3.23 3.23 Parallel Yield Change 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%12-month return 0.57% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56% 0.56%Compound Factor 100.57% 100.56% 100.56% 100.56% 100.56% 100.56% 100.56% 100.56% 100.56% 100.56% 5.78% 0.56%

12

Assumptions:

ExpectedDefaultRate: 0.15%ExpectedDefaultRecoveryRate: 44%Default/RecoveryReturnContribution: ‐0.08%

Insummary:

5‐YearTreasuryReturn 1.97% SpreadEffect +0.56%DefaultEffect ‐0.08% ReturnAssumption 2.45%

Addingthe5‐YearUSTreasuryBondreturn,theexpectedspreadreturn,andadjustingfordefaultsyieldsacompoundreturnexpectationof2.45%.WebelievethatthisapproachworksequallywellforUSAggregatefixedincomeandforNon‐USAggregatefixedincomewherethecurrencyexposureishedgedbacktotheUSdollar.Bystrippingoutcurrencyexposure,theNon‐USfixedincomeinvestorisleftwithaportfoliooffixedincomesecuritiesexpectingsimilarunderlyingcharacteristicstotheUSfixedincomeportfolio.Non‐CoreFixedIncome

Modeled:USandNon‐USBelow‐Investment‐Grade&EmergingMarketsFixedIncomeCompoundReturn:4.96%

ArithmeticAverageReturn:5.90%Risk:14.25%

OurNon‐CoreFixedIncomeassumptioncombinesUSbelow‐investment‐grade(highyield)bondsandemergingmarketssovereignbonds.Weassumea50%weightingtoeachassetclass.HighYieldBondsThematurityofthehigh‐yieldindexiscurrently6.2years.Tomatchthismaturity,wecalculateaspreadoveraweightedaverageofexpectedreturnsfor5‐and10‐yearUSTreasuryBondsthatyieldsanexpectedreturnfora6.2‐yearTreasuryBond,thenaddourspreadbuildingblock,andfinallysubtractadefaultbuildingblock.

Maturity: 6.2years6.2‐YearTreasuryAssumedReturn: 1.96%CurrentSpread: 6.95%Long‐TermAverageSpread: 5.84%SpreadDuration: 3.78yearsCumulativeSpreadChange(10Yrs): ‐0.56%(halfwayfromcurrenttolong‐termaverage)

13

ExpectedDefaultRate: 2.80% ExpectedDefaultRecoveryRate: 39%

Ourassumedreturncontributionfromhighyieldspreadbuildingblock,beforeaccountingfordefaults,is3.45%(assuming50%oftheportfolio):

EmergingMarketsDebtThecurrentmaturityofanindexofemergingmarketssovereignbondsis11.3years.Tomatchthisduration,wecalculateaspreadoveraweightedaverageofexpectedreturnsfor10‐and20‐yearUSTreasuryBondsthatyieldsanexpectedreturnfora11.3‐yearTreasuryBond.

Maturity: 11.3years11.3‐YearTreasuryAssumedReturn: 1.92%CurrentSpread: 3.94%Long‐TermAverageSpread: 3.56%SpreadDuration: 6.34yearsCumulativeSpreadChange(10Yrs): ‐0.19%(halfwayfromcurrenttolong‐termaverage)

Theseassumptionsyieldanassumptionforreturncontributionfromemergingmarketsdebtspread,beforeaccountingfordefaults,of1.99%(assuming50%oftheportfolio):

Ourfinalbuildingblockisanadjustmentforexpecteddefaultandrecoveryrates.Thequalitycompositionoftheemergingmarketsdebtuniversehaschangedovertime,sowedonotapplyhistoricaluniverse‐widedefaultandrecoveryrates.Instead,weexaminethehistoricaldefaultandrecoveryratesbyqualityrating,andapplythoseratestothecurrentuniversequalitycomposition.Historically,investment‐gradeemergingmarketsissueshaveexperienced1.9%defaultrates.Speculative‐gradeemergingmarketsissueshaveexperienced17.2%defaultrates.Theuniverseiscurrently58%investmentgradeand42%speculativegrade.Weightinghistoricaldefaultratesbythecurrentuniversecompositionresultsinourassumptionforfuturedefaultrates.Historicalrecoveryratesindefault,regardlessofrating,hasbeen63%.

High Yield -- Spread Effect (over Treasurys) Year 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Spread 6.95% 6.89% 6.84% 6.78% 6.73% 6.67% 6.62% 6.56% 6.51% 6.45% 6.39%Duration 3.78 3.78 3.78 3.78 3.78 3.78 3.78 3.78 3.78 3.78 3.78 Parallel Yield Change -0.06% -0.06% -0.06% -0.06% -0.06% -0.06% -0.06% -0.06% -0.06% -0.06% -0.56%12-month return 7.16% 7.10% 7.05% 6.99% 6.94% 6.88% 6.83% 6.77% 6.72% 6.66%Compound Factor 107.16% 107.10% 107.05% 106.99% 106.94% 106.88% 106.83% 106.77% 106.72% 106.66% 95.06% 6.91%

Proportion 50.00%Spread Effect (Total) 3.45%

EMD -- Spread Effect (over Treasurys)Year 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Spread 3.94% 3.92% 3.90% 3.88% 3.86% 3.85% 3.83% 3.81% 3.79% 3.77% 3.75%Duration 6.34 6.34 6.34 6.34 6.34 6.34 6.34 6.34 6.34 6.34 6.34 Parallel Yield Change -0.02% -0.02% -0.02% -0.02% -0.02% -0.02% -0.02% -0.02% -0.02% -0.02% -0.19%12-month return 4.06% 4.04% 4.02% 4.00% 3.99% 3.97% 3.95% 3.93% 3.91% 3.89%Compound Factor 104.06% 104.04% 104.02% 104.00% 103.99% 103.97% 103.95% 103.93% 103.91% 103.89% 47.68% 3.98%

Proportion 50.00%Spread Effect (Total) 1.99%

14

ExpectedDefaultRate: 8.4% ExpectedDefaultRecoveryRate: 63%

Wesubtracttheexpectedunrecovereddefaultfromthetotalyield:

DefaultRate RecoveryRate UnrecoveredRate

DefaultEffectonReturn

HighYield 2.8% 39% 61% ‐1.74%EMDebt 8.4% 63% 37% ‐3.10%Insummary: HighYield EMDebt Combined

TreasuryReturn 1.96% 1.92% ‐‐‐SpreadEffect +6.91% +3.98% ‐‐‐DefaultEffect ‐1.74% ‐3.10% ‐‐‐ReturnAssumption 7.13% 2.79% 4.96%WeaveragetheHighYieldandEmergingMarketsDebtassumptionstoarriveatourforward‐lookingcompoundreturnexpectationfornon‐corefixedincome:4.96%.Core‐PlusFixedIncome

Modeled:80%USInvestment‐GradeAggregate;20%Non‐CorePlusSectorsCompoundReturn:2.95%

ArithmeticAverageReturn:3.10%Risk:6.00%

Thisreturnassumptionexpectsareturncalculatedasfollows:

80%oftheexpectedreturnofCoreFixedIncome +20%oftheexpectedreturnofNon‐CoreFixedIncomeThisprocessyieldsanexpectedcompoundreturnof2.95%.Long‐DurationFixedIncome

Modeled:USLong‐TermGovernment/CreditFixedIncomeCompoundReturn:3.09%

ArithmeticAverageReturn:3.60%Risk:10.25%

Ourmodelassumes50%eachin(i)10‐and20‐YearUSTreasuryBondsand(ii)long‐durationUSinvestment‐gradecorporatebonds.Whilethecompositionofmostlong‐durationfixedincomeindexesdiffersslightlyfromthisapproach,webelievethatmostdifferenceswillcanceleachotherout.

15

TreasuryComponentFortheTreasurycomponent,weuseourbasicmodeltoaveragetheexpectedreturnsfor10‐and20‐yearTreasuryBonds(outlinedabove)toapproximatethereturnofa15‐yearTreasuryBond.ThisaverageexpectedreturnfortheTreasurycomponentis1.90%.SpreadComponentWeaddaspreadcomponentconsistingoflong‐termUSinvestment‐gradecorporatebonds:Assumptions:

ProportioninCorporates: 50%CurrentSpread: 2.25%Long‐TermAverageSpread: 1.72%SpreadDuration: 11.96yearsCumulativeSpreadChange(10Yrs): ‐0.26%(halfwayfromcurrenttolong‐termaverage)ExpectedDefaultRate: 0.15% ExpectedDefaultRecoveryRate: 44%

Insummary:

TreasuryReturn 1.90%(averageof10‐and20‐yearTreasurys)SpreadEffect +1.23%(50%proportion)DefaultEffect ‐0.04%(50%proportion)ReturnAssumption 3.09%

OurreturnassumptionforthecombinedTreasuryandcorporateLong‐DurationFixedIncomebasketassumes50%ineachcategory.Thiscompoundreturnassumptionis3.09%.USTreasuryInflationProtectedSecurities(TIPS)

Modeled:USTIPSCompoundReturn:1.94%

ArithmeticAverageReturn:2.20%Risk:6.75%

Long Corporates -- Spread Effect (over Treasurys) Year 0 1 2 3 4 5 6 7 8 9 10 Cumulative AnnualizedStarting Spread 2.25% 2.22% 2.20% 2.17% 2.14% 2.12% 2.09% 2.07% 2.04% 2.01% 1.99%Duration 11.96 11.96 11.96 11.96 11.96 11.96 11.96 11.96 11.96 11.96 11.96 Parallel Yield Change -0.03% -0.03% -0.03% -0.03% -0.03% -0.03% -0.03% -0.03% -0.03% -0.03% -0.26%12-month return 2.56% 2.54% 2.51% 2.49% 2.46% 2.43% 2.41% 2.38% 2.35% 2.33%Compound Factor 102.56% 102.54% 102.51% 102.49% 102.46% 102.43% 102.41% 102.38% 102.35% 102.33% 27.34% 2.45%

Proportion 50.00%Spread Effect (Total) 1.22%

16

GiventhatthefirstUSTIPSissuancewasin1997,wearehesitanttorelyonany“long‐term”yieldorspreadaveragestofurthermodeltheassetclass.Instead,wemodelaproxyfortheBarclaysUSTIPSIndex,whichcurrentlyhasamaturityof8.5years.Aportfolioof30%5‐yearTreasuryBonds,and70%10‐yearTreasurybondsresultsinahypotheticalTreasurybondwith8.5‐yearmaturity.Assumingourinflationexpectationof1.54%peryearfortheprospective10‐yearperiod,theexpectedTIPSreturnissimplyaweightedaverageofourreturnexpectationsforthenominal10‐yearand5‐yearTreasurybonds.Applyingtheseweightstoourreturnprojectionsforthosebondsresultsina10‐yearTIPSreturnassumptionof1.94%:

(30%x1.97%)+(70%x1.92%)=1.94%.

17

EQUITYToderiveourequityreturnassumptions,weevaluatetwomethodologies:(i)abuilding‐blockapproachusingtheso‐calledShillerprice‐to‐earnings(P/E)measureand(ii)anequityriskpremiumestimatethataveragesthecurrentimpliedequityriskpremiumbasedonafreecashflowtoequitymodelandthehistoricalaverageequityriskpremium. EquityRiskPremium/BuildingBlockApproachFreeCashFlowtoEquityModel

WhereourbuildingblockscallforaP/Emeasure,weassumethatthiscurrentvaluationmetricwillreverthalfwaytoitslong‐termmeanovertheprospectiveten‐yearperiod.Ourapproachemploys“Shillerearnings,”whichrepresentaten‐yearaverage,adjustedforinflation.Webelievethatthisapproachappropriatelysmoothestheimpactofyear‐to‐yearearningsvolatility,andresearchshowsthatofallthevariedwaystocalculateaP/Eratio,theShillerP/Emeasurehashistoricallyshownthehighestpredictivepoweroverfuture10‐yearreturns.3Ourbuildingblockapproachisconsistentacrossequitycategories:

Assumed(Expected)USInflation+CurrentDividendYield+ExpectedRealEarningsGrowth+ReversioneffectofP/E(halfwaytolong‐termmean,over10years)+CapitalizationPremium(ifapplicable)

TheseinputsareavailablewithreliableandrobustdatafortheUSlarge‐capstockmarket,butnotforUSsmall/mid‐capequitiesorforglobalequities.Forthisreason,wehavechosentoanchorourUSsmall/mid‐capandglobalequityassumptionstoourUSlarge‐capequityassumptioninseveralways.

3 Vanguard.Forecastingstockreturns:Whatsignalsmatter,andwhatdotheysaynow?https://personal.vanguard.com/pdf/s338.pdf

CurrentDividendYield

ExpectedReal EarningsGrowth

Inflation

(+/‐)P/EReversionEffect

EquitySecurityReturn

CapitalizationPremiumImpliedEquityRiskPremium

Expected10‐Year TreasuryReturn

18

USLarge‐CapEquityModeled:USMid‐andLarge‐CapitalizationEquities

CompoundReturn:5.21%ArithmeticAverageReturn:6.90%

Risk:19.25%OurreturnassumptionsforUSlarge‐capequityaretheaverageoftwoseparateapproaches:avaluation‐basedbuilding‐blockapproach,andamodifiedDamadoranfreecashflowtoequitymodel.BuildingBlockApproachWefindtheShillerP/Emetrictobethemostusefulofvariousvaluationmetricsfromtheperspectiveofutilityinforecastingreturns.ThefollowingchartdepictstheShillerP/EmetricfortheUSmarket,since1951(thepost‐WWIIperiod).TheShillerP/Eatagivenpointintimeisdepictedonthehorizontalaxis,andthesubsequent10‐yearinflation‐adjustedreturnisdepictedontheverticalaxis.Wehavedecomposedthedataarrayintothreeeconomicregimes–thepost‐warboom(inblue;1951‐1965);thegreatinflationaryperiod(intan;1966‐1984);andthegreatmoderation(ingrey;1985‐2015).Examiningthedatathiswayyieldsusefulinsightsand,importantly,highpredictivepowerfortheShillerP/Emetricoversubsequentrealreturn.TheS&P500’scurrentpositiononthechartisindicatedbytheboldverticalline.

Forthevaluation‐basedbuildingblockapproach,wecreateourbuildingblocksfromtheS&P500Index:

R²=0.878

R²=0.880

y=‐0.006x+0.214R²=0.875

‐10%

‐5%

0%

5%

10%

15%

20%

0 5 10 15 20 25 30 35 40 45 50

Subsequent10‐YearRealReturn

Starting‐PointShillerP/EValuation

Long‐TermShillerP/Eversus10‐yrInflation‐AdjustedReturnsByEconomicRegime,Since1951(Postwarperiod)

CurrentValue PostwarBoom GreatInflation GreatModeration

19

1.54% Inflation 2.11% CurrentDividendYield 1.74% Long‐TermCompoundAverageRealEarningsGrowth(Since1871) WemeasureexpectedP/Ereversionhalfwaytolong‐termmean: ShillerP/E Current 26.06

Long‐TermAverage 16.65 AnnualReversionEffect ‐2.19% (halfwaytolong‐termaverage)

ThebuildingblocksapproachresultsinanexpectedcompoundreturnforUSLarge‐CapEquityof3.20%.ThisapproachrepresentshalfofourcalculationforLarge‐CapUSEquity.EquityRiskPremium/DiscountedFreeCashFlowModelFortheimpliedequityriskpremium,wereferenceandmodifyadiscountedfreecashflowmodelcreatedbyProfessorAswathDamodaranoftheSternSchoolofBusiness4thatusesafreecashflowtoequityapproachtoaccountfordividendsaswellasstockbuybacks.Ourmodifiedfree‐cash‐flow‐to‐equitymodelemploysseveralinputvariables:Beginning(current)S&P500level= 2043.94Baseyearfreecashflowtoequity,S&P500= $106.095ExpectedS&P500earningsgrowthovernext5years= 4.80%6ExpectedS&P500earningsgrowthforyears5‐10= 1.92%7WeapplyastandarddiscountedcashflowmethodologytothesevariablesandsolvefortherateofgrowththatmakesthediscountedforecastedvalueoftheS&P500identicaltotoday’svalue.

2043.94106.09 1.0480

1106.09 1.0480

1106.09 1.0480

1106.09 1.0480

1106.09 1.0480

1106.09 1.0480 1.0192

0.0192 1

SolvingforryieldstheexpectednominalreturnfortheS&P500overthenext10years,undertheseassumptions.Thatrateofreturnis7.92%.Subtractingourassumed10‐YearTreasuryreturnof1.92%resultsinanexpectedequityriskpremiumof6.00%.Thisimpliedequityriskpremiumishigherthanwhathistoryhasdelivered.Tocorrectforthis,weaveragethecurrentimpliedforward‐lookingequityriskpremium(6.00%)andthelong‐termhistoricalgeometricaveragerealizedequityriskpremium(4.60%)toderiveanequityrisk

4 http://pages.stern.nyu.edu/~adamodar/ 52015S&P500Dividends=$42.66+buybacks=$63.43.6I/B/E/Sanalystconsensusearningsgrowthoverthenextyearis5.55%.Historically,theI/B/E/Sconsensusanalystforecasthasoverstatedsubsequentactualearningsgrowthby15.6%.Wereduceourassumptionforearningsgrowthby13.5%(1‐(1/1.155))accordingly.

7 Ourforecastedreturnforthe10‐yearTreasuryBond,asaproxyfortheten‐yearrisk‐freerate.

20

premiumestimateof5.30%forUSLarge‐CapEquity.Substitutingthisassumedequityriskpremiumintothemodelresultsinareturnestimateof7.22%.Averagingtheexpectedreturnsgeneratedbythebuilding‐blocksapproachandthediscountedfreecashflowmodelyieldsanexpectedcompoundreturnof5.21%.USSmall/Mid‐CapEquity

Modeled:USSmall‐andMid‐CapitalizationEquitiesCompoundReturn:5.34%

ArithmeticAverageReturn:7.20%Risk:20.25%

ToourUSLarge‐CapEquityassumption,weaddasmall/mid‐capcompoundreturnpremium.Historically,small‐capsecuritieshaveexperiencedareturnpremiumof0.25%annualized.USsmall‐capstockshavealsohistoricallytradedatahigheraveragevaluationthanUSlarge‐capstocks–inaratioofapproximately1.2:1,asindicatedbythehorizontallineinthefollowingchart.Thecurrentvaluationpremium,asindicatedbytheblueline,ishigheratapproximately1.5.

Whilewearedisinclinedtoreadtoomuchintothisvaluationmetric,givenitslimitedhistory(since1979),wedousethisvaluationinsighttoreduceourexpectationforsmall‐capreturnpremiumbyhalf.Assuch,weadd0.125%toourlarge‐capequityassumptiontoyieldacompoundreturnassumptionforUSsmall/mid‐capequitysecuritiesof5.34%.USEquity

Modeled:USEquities,AllCapitalizationsCompoundReturn:5.24%

ArithmeticAverageReturn:6.90%Risk:19.00%

OurreturnassumptionforUSEquityisintendedtomodeltheentireUSequitymarket.Itassumesthecurrentweightingoflarge‐andsmall/mid‐capitalizationequitiesintheUSequitymarket–81%

0.7

0.9

1.1

1.3

1.5

1.7

1.9

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2010

2011

2012

2013

2014

2015

RatioofUSSmall‐CaptoUSLarge‐CapShillerP/E

RelativeValue AverageRelativeValue

21

large,and19%small/mid8.TheseweightsareappliedtotheunderlyingUSLarge‐CapandUSSmall/Mid‐CapEquityassumptionstoyield5.24%incompoundterms:

(81%x5.21%)+(19%x5.34%)=5.24%.

Non‐USLarge‐CapEquityModeled:Non‐USLarge‐CapitalizationEquities,DevelopedandEmerging

CompoundReturn:6.25%ArithmeticAverageReturn:8.70%

Risk:23.50%Webuildseparateassumptionsfordevelopedandemergingnon‐USmarkets,andthenweighthemaccordingtocurrentmarketweightstoconstructourNon‐USLarge‐CapEquityassumption,whichisintendedtomodelequitiesofbothdevelopedandemergingmarkets.Becauseofdatalimitations,wehavereliedlessonactualhistoricalexperienceforinternationalmarketsthanwehaveonqualitativeadjustmentstomorerobustUSmarketdata.Fordevelopedmarkets,ourassumedbuildingblocksareasfollows: 1.54% Inflation 3.17% CurrentDividendYield 1.35% CompoundAverageRealEarningsGrowth(Since1988) WemeasureexpectedP/Ereversionhalfwaytolong‐termmean: ShillerP/E Current 14.10

Long‐TermAverage 13.709 AnnualReversionEffect ‐0.12%(halfwaytolong‐termaverage)

Thisapproachyieldsanexpectedcompoundreturnfordeveloped‐marketsnon‐USlarge‐capitalizationequitiesof5.94%.Ouremergingmarketsequityapproachisdetailedbelow.Itscompoundreturnassumptionis7.40%.Developedmarketscurrentlycomprise79%,andemergingmarkets21%,ofthenon‐UStotalequitymarketcapitalization.Applyingthoseweightstoourdevelopedandemergingmarketsassumptionsyieldsanon‐USlarge‐capitalizationcompoundreturnassumptionof6.25%.

8Russell,http://www.russell.com/indexes/documents/US_Indexes_comparison.pdf.9OverthelongestcommonperiodforwhichwehavebothUS(S&P500)andDevelopedNon‐US(MSCIEAFE)earningsseries(since1995),EAFEhastradedatanaveragevaluationlevelapproximately82.6%oftheleveloftheS&P500.Weapplythisfractiontoourassumptionforthelong‐termP/EofUSlarge‐capitalizationstockstoarriveatourassumedlong‐termaveragevaluationleveltowhichweexpectnon‐USlarge‐capitalizationstockstorevert.

22

Non‐USSmall‐CapEquityModeled:Non‐USSmall‐CapitalizationEquities,DevelopedandEmerging

CompoundReturn:6.50%ArithmeticAverageReturn:9.80%

Risk:27.75%

ToourNon‐USLarge‐CapEquityassumption,weaddacompoundreturnpremiumbuildingblockof0.25%,thesameundiscountedhistoricalpremiumweusedforUSsmall‐capequities.Thisyieldsacompoundreturnassumptionof6.50%.Givenverylimiteddatafornon‐USsmall‐capitalizationequities,wearenotinclinedtomakeavaluationadjustmentbasedonreversiontoanaverage.EmergingMarketsEquity

Modeled:EmergingMarketsEquityCompoundReturn:7.40%

ArithmeticAverageReturn:11.20%Risk:29.75%

Ourassumedbuildingblocksareasfollows: 1.54% Inflation 2.81% CurrentDividendYield 1.32% RealEarningsGrowth10WemeasureexpectedP/Ereversionhalfwaytolong‐termmean: ShillerP/E Current 10.50

Long‐TermAverage 14.7011 Annualreversioneffect1.74% (halfwaytolong‐termaverage)

AddingthisP/Ereversionmeasuretotheotherbuildingblocksyieldsanexpectedcompoundreturnof7.40%.

10Overthelongestcommonperiodforwhichwehavedataondeveloped(MSCIEAFE)andemerging(MSCIEM)marketsearnings(1995),theemergingmarketshaveaveraged98%oftheearningsgrowthrateofdevelopedmarkets.Weapplythisproportiontoourassumedlong‐termearningsgrowthratefordevelopedmarketstoyieldanassumedemergingmarketsearningsgrowthrateof1.32%.

11Since1995,thelongestdataseriesavailablefornon‐USmarketearnings,theaverageShillerP/Eratioforemergingmarketshasbeen19.8.Wenotethattheperiodsince1995hasgloballybeenaperiodofhighervaluationsthanhavehistoricallybeenexperienced.Forthisreason,wedonotassumethatemergingmarketsearningswillreverttotherelativelyhighlevel–instead,weassumethatemergingmarketswillcommandanaverageP/Eratio1.00higherthandevelopednon‐USmarketswill.

23

Non‐USEquityModeled:Non‐USEquities,AllRegions&Capitalizations

CompoundReturn:6.30%ArithmeticAverageReturn:8.80%

Risk:24.00%OurreturnassumptionforNon‐USEquityisintendedtomodeltheentireNon‐USequitymarket.Itassumesthecurrentweightingoflarge‐capandsmall‐capmarketsequitiesintheinternationalequitymarket–80%large‐capand20%small‐cap.TheseweightsareappliedtotheunderlyingNon‐USLarge‐CapEquityandNon‐USSmall‐CapEquityassumptions.Thisweightingyieldsacompoundreturnassumptionof6.30%:

(80%x6.25%)+(20%x6.50%)=6.30%.

24

ALTERNATIVESAlternativeassetsshareacommonelementofnoteasilybeingmodeledwithpublic‐marketindexproxies.Aswell,wearemorereluctanttorelyontheirlong‐termhistory,givengrowthinassetsallocatedtosuchstrategiesoverthelastseveraldecadesandthedynamicnatureofstrategiesemployed.RealEstate

Modeled:Public(USEquityREITs)andOpen‐EndedPrivateCoreRealEstateCompoundReturn:4.71%

ArithmeticAverageReturn:6.30%Risk:18.75%

Ourexpectedreturnreflectsgoing‐incapratesforpublicequityandcoreprivaterealestate.ForpublicequityREITs,wecalculatethecurrentcaprate,definedasincomedividedbyprice,oftheFTSENAREITAllEquityREITSIndex:3.72%.ThefollowingchartdepictstheinverseofthecapratefortheequityREITbenchmark:itshistoricalprice‐to‐incomeratio.Thepresentlowcaprateisexplainedbyhighvaluationsrelativetotheindex’sownhistory.

OurcaprateassumptionforcoreprivaterealestateisbasedontheUrbanLandInstituteconsensusestimateoftheNCREIFcapitalizationrateasofDecember31,2015:5.7%incompoundterms.12Thiscapratereflectscurrentincomereturnonanunleveredbasisandexcludescapitalappreciation.Averagingthesetwocapratesyieldsareturnassumptionof4.71%.

12 UrbanLandInstitute.http://uli.org/research/centers‐initiatives/center‐for‐capital‐markets/barometers‐forecast‐and‐data/uli‐real‐estate‐consensus‐forecast/

0.05.010.015.020.025.030.035.0 NAREITAllEquityREITS

Price/12‐MonthTrailingIncome

Price/Income AveragePrice/Income

25

Wenotethattheprimarydriverofreturnforcorerealestateoverthelongtermhasbeenincome,notappreciation.ForequityREITS,inrealtermssince1973,historicalpriceappreciationhasaveraged0.23%peryear,andincomehasaveraged3.30%peryear.DiversifiedInflation‐Related

Modeled:Diversifiedportfoliocontaining1/3each:RealEstate,Commodities,andUSTIPSCompoundReturn:3.46%

ArithmeticAverageReturn:4.40%Risk:14.25%

Weassumeadiversifiedportfoliocontaining1/3eachinUSTIPS,RealEstate,andCommodities.TheUSTIPScomponentissimplyourexpectedreturnforUSTIPS,asoutlinedabove:1.94%,incompoundterms.TheRealEstatecomponentisourRealEstateAssumption:4.71%incompoundterms.FortheCommoditiescomponent,webuildamodelassumingthatcommodityreturncanbedecomposedintothreesources:collateralreinvestmentyield,commodityspotreturn,androllyield.Weassume0%forrollyield,knowingthatithasbeenpositiveandnegativeovervarioushistoricalperiods,asthebuyingandsellingbalancebetweencommodityinvestorsandcommodityconsumershasshifted.Overthelastdecade,rollyieldhasbeennegative.Forspotreturn,wecalculateaseriesofthelast10yearsofrealpricesfortheBloombergCommodityIndexandassumethatthecurrentrealpriceoftheindexwillreverthalfwaytoits10‐yearaverage,inevenincrementsoverthenext10years.ThecurrentrealspotpricefortheBloombergCommodityIndexis81.2,andits10‐yearaveragerealpriceis157.9.Revertinghalfwaytothisaveragerealpriceimpliesacompoundrealspotreturnof3.44%peryear.Insummary,fortheCommoditiescomponent: Collateral: 0.30%(ourassumednominalreturnforCashEquivalents) Spotreturn: 3.44% Rollyield: 0.00% Commodityreturn: 3.74%FortheDiversifiedInflation‐Relatedassumption,weassumeacompoundreturnof:

1/3(1.94%)+1/3(4.71%)+1/3(3.74%)=3.46%

26

MarketableAlternativesModeled:HedgeFundsofFunds,GlobalGTAA,Daily‐ValuedAlternativeStrategies

CompoundReturn:4.94%ArithmeticAverageReturn:5.60%

Risk:12.25%Weassumeadiversifiedportfoliothatwilltendtoapproximatethefollowingmarketexposuresovertime: 30%USEquity 30%Non‐USEquity 20%CoreFixedIncome 20%Non‐CoreFixedIncomeWeightingthoseassumptionsaccordinglyresultsinacompoundreturnassumptionof4.94%.Thisapproachdoesnotexplicitlyreflecttheuseofleverageinmarketablealternativesstrategies.Alternativesvehiclesthatemployleveragecanearnhigherreturns,butduetothemechanicsofperformance‐basedfeeschedules,alsosubtracthigherfeesfromthosereturns.Giventhatourassumptionsetisintendedtobepassiveinnatureandnotreflectactivemanagement,forhedgefunds,weareassuminganindustryaveragehedgefundoffunds.Non‐MarketableAlternatives

Modeled:VentureCapital,PrivateEquity,DistressedCredit,inLockupVehiclesCompoundReturn:8.10%

ArithmeticAverageReturn:12.30%Risk:31.50%

Weassumeadiversifiedportfoliothatwilltendtoapproximatethefollowingmarketexposuresovertime,plusapremiumforilliquidity: 50%USEquity 50%Non‐CoreFixedIncome +3.00%illiquidity/leveragepremiumWeightingthoseassumptionsaccordinglyresultsinacompoundreturnassumptionof8.10%.Giventhatourassumptionsetisintendedtobepassiveinnatureandnotreflectactivemanagement,weareassuminganindustry‐averageactivemanagerorcollectionofactivemanagers.

27

RISKOurriskassumptionsaremostlyderivedfromhistory,butwehaveenhancedhistoricalmetricswithqualitativeoverlaysinseveralassetcategories.Foreachassetcategory,webeganbyexaminingthefollowinghistoricalannualreturns:Inflation USCPICashEquivalents 91‐DayT‐BillsLow‐DurationFixedIncome Barclays1‐3YearGovernment/CreditCoreFixedIncome BarclaysUSAggregateNon‐CoreFixedIncome 50%MLHighYieldMasterII,50%JPMorganEMBIbackto1994;

100%MLHighYieldMasterIIbefore1994Long‐DurationFixedIncome BarclaysLongGovernment/CreditTIPS BarclaysUSTIPSUSEquity Russell3000backto1979;S&P500before1979USLarge‐CapEquity Russell1000backto1979;S&P500before1979USSmall‐CapEquity Russell2000Non‐USEquity MSCIACWIexUSIMIbackto1994;MSCIEAFEbefore1994Non‐USLarge‐CapEquity MSCIACWIexUSbackto2001;MSCIEAFEbefore2001Non‐USSmall‐CapEquity MSCIACWIexUSSmallCapEmergingMarketsEquity MSCIEmergingMarketsRealEstate FTSENAREIT,NCREIFProperty,andNCREIFODCE(separately)DiversifiedInflation‐Related 1/3each:FTSENAREIT,BarclaysUSTIPS,BloombergCommodityMarketableAlternatives HFRIFundofFunds;and30%ourUSEquityseries,30%ourNon‐US

Equityseries,20%ourCoreFixedIncomeseries,and20%ourNon‐CoreFixedIncomeseries(separately)

Non‐MarketableAlternatives Averageof2xourUSEquityseriesand2xourNon‐CoreFixedIncomeseries

Ineachcase,wecalculatedthelongest‐termstandarddeviationofreturnspossibleforthecategory.Then,wecalculatedthestandarddeviationofannualreturnsoverthelasttenyears.Theaverageofthesetwofiguresrepresentsourbase‐caseriskassumption.Next,weexaminedtheworstannualreturnforeachproxyindex,goingbackasfaraspossibleintohistory.Weassumedthisreturnastheworst‐casescenario.Insomecases,thenormalreturndistributionimpliedbyourreturnandriskassumptionssuggestedthattheworst‐casescenariohadlessthana2%probability(1in50years)ofoccurring.Inthosecases,weadjustedourriskassumptionupwarduntiltheworst‐casescenariohadatleasta2%probabilityofoccurringunderourassumednormalreturndistribution.Toperformthisprobabilityanalysisforprivaterealestate,weexaminedrollingtwo‐yearperiodstoaccountforthefactthatdeclines,asmeasuredbyappraisalsandilliquidity,occurmoreslowlythaninpublicmarkets.

28

Finally,basedonthisanalysisandourqualitativeassessmentofthequalityandlongevityofourreturndata,wemadeseveralqualitativeadjustments,wherenoted.Theresultsofthisriskanalysisfollow.Thefollowingtabledepictsactualstandarddeviationsofannualreturn,measuredinthelongterm(asfarbackashistorywillallow),forthelasttenyears,andtheaverageofthosetwofigures.AddingorsubtractingourqualitativeadjustmentresultsintheRiskAssumptionatthefarright.

LongTerm 10Years AverageQualitativeAdjustment

RiskAssumption(Rounded)

Inflation 4.94% 1.21% 3.08% 0.00% 3.00%

CashEquivalents 3.26% 1.93% 2.59% ‐1.00% 1.50%

Low‐DurationFixedIncome 4.57% 2.14% 3.36% 0.00% 3.25%

CoreFixedIncome 6.89% 3.06% 4.98% 0.00% 5.00%

Core‐PlusFixedIncome 5.41% 4.43% 4.92% 1.00% 6.00%

Non‐CoreFixedIncome 12.98% 15.65% 14.31% 0.00% 14.25%

Long‐DurationFixedIncome 11.16% 9.47% 10.32% 0.00% 10.25%

TIPS 6.30% 7.15% 6.72% 0.00% 6.75%

USEquity 17.42% 19.57% 18.50% 0.50% 19.00%

USLarge‐CapEquity 17.47% 19.51% 18.49% 0.75% 19.25%

USSmall/Mid‐CapEquity 18.44% 21.82% 20.13% 0.00% 20.25%

Non‐USEquity 22.98% 24.77% 23.88% 0.00% 24.00%

Non‐USLarge‐CapEquity 22.50% 24.40% 23.45% 0.00% 23.50%

Non‐USSmall‐CapEquity 26.11% 30.23% 28.17% ‐0.50% 27.75%

EmergingMarketsEquity 34.73% 36.42% 35.58% ‐5.75% 29.75%

RealEstate 19.08% 22.92% 21.00% ‐2.25% 18.75%

DiversifiedInflation‐Related 12.74% 15.12% 13.93% 0.25% 14.25%

MarketableAlternatives 10.05% 10.02% 10.04% 2.11% 12.25%

Non‐MarketableAlternatives 30.40% 32.55% 31.48% 0.00% 31.50%

StandardDeviationofReturns

29

Thefollowingtableexaminestheprobabilityoftheactualexperiencedworstcaseoccurringunderourassumednormaldistributionofreturns,asimpliedbyourexpectedreturnandstandarddeviationofreturns,afteraccountingforqualitativeadjustmentstorisk.Wemeasuretheactualworst‐casescenarioin“sigmas,”orstandarddeviationsfromourassumedmeanreturn.Measuringthisway,weask,“Howlikelywastheactualexperiencedworstcase,accordingtothedistributionparameterswehaveassumed?”Wehavequalitativelyadjustedseveralassetclassestoensurethattheprobabilityoftheactuallyexperiencedworstcaseisalwaysgreaterthan2%,meaningweassumethattheexperiencedworstcasehasatleastaone‐in‐fifty‐yearchanceofhappeningunderourassumptions.

ActualWorstCase,in

SigmasfromAssumption

ImpliedProbabilityofActualWorstCaseOccurring

CashEquivalents 0.02% (2011) 0.18 85.7%

Low‐DurationFixedIncome 0.55% (1994) 0.27 78.9%

CoreFixedIncome ‐2.92% (1994) 1.10 27.0%

Core‐PlusFI ‐4.26% (1994) 1.25 21.2%

Non‐CoreFixedIncome ‐18.86% (2008) 1.73 8.3%

Long‐DurationFixedIncome ‐8.83% (2013) 1.20 22.9%

TIPS ‐8.61% (2013) 1.60 10.9%

USEquity ‐37.31% (2008) 2.33 2.0%

USLarge‐CapEquity ‐37.60% (2008) 2.31 2.1%

USSmall/Mid‐CapEquity ‐36.79% (2008) 2.18 2.9%

Non‐USEquity ‐45.99% (2008) 2.30 2.2%

Non‐USLarge‐CapEquity ‐45.24% (2008) 2.30 2.1%

Non‐USSmall‐CapEquity ‐50.01% (2008) 2.16 3.1%

EmergingMarketsEquity ‐53.33% (2008) 2.16 3.1%

RealEstate ‐37.34% (1974) 2.33 2.0%

DiversifiedInflation‐Related ‐28.61% (2008) 2.33 2.0%

MarketableAlternatives ‐21.37% (2008) 2.22 2.6%

Non‐MarketableAlternatives ‐56.17% (2008) 2.17 3.0%

AlternatebenchmarksforRealEstateandNon‐MarketableAlternatives:

NCREIFProperty(2Years) ‐22.23% (2008‐9) 1.52 12.8%

NCREIFODCE(2Years) ‐36.79% (2008‐9) 2.30 2.1%

MarketableAlternatives(build‐up) ‐27.71% (2008) 2.75 0.6%

WorstYear

30

OurqualitativeadjustmentstoRiskwereasfollows:CashEquivalents(‐1.00%)

Whilethelong‐termstandarddeviationofreturnstocashhasbeengreaterthan3%,thatvolatilitywasexperiencedathigherlevelsofcashreturn.Webelieveitisunlikelyforthedistributionofreturnstocashequivalentstobeaswideashistoricallyevident,givenitscurrentlowlevelofreturn.Wequalitativelyadjusttherisktocashequivalentsdownwardby100basispoints.

Core‐PlusFixedIncome(+1.00%)

Whilebecauseofdiversificationeffectslong‐termvolatilityforourmodeledCore‐PlusserieshasbeenlowerthanthatforCoreFixedIncome,recent(last10years)volatilityhasbeenapproximately50%higher.Ourmodestadjustmentacknowledgesthattheriskierelementsinherentinplussectorsprovideawiderdistributionofreturns,regardlessoftheirmeasuredyear‐over‐yearvolatility.

USEquity,USLarge‐CapEquity(+0.50%,+0.75%)

Thesecategorieswereadjustedupwardtomaketheiractualworst‐caseexperiencegreaterthana2%probabilityofoccurringundertheassumeddistribution.

Non‐USSmall‐CapEquity,EmergingMarketsEquity(‐0.50%,‐5.75%)

Giventhelimitedhistoryforapublic‐marketproxyforeachassetclass,wearereluctanttorelytooheavilyonhistoricallymeasuredvolatility.Assuch,weadjustedtheriskdownwardsuchthateachassetclass’sactualworstcase(2008)representsanapproximately3%probabilityofoccurrenceundertheassumeddistribution.

RealEstate(‐2.25%)

ThisdownwardadjustmentacknowledgesthatthepublicmarketproxywehavechosentorepresentCoreRealEstateincludessomeriskiernon‐coreelements.Wehaveadjustedtheassumptionsuchthatthe1974experienceforpublicREITs,andthecombined2008/2009experienceforcoreopen‐endedprivaterealestatefunds,eachrepresentanapproximate2%probabilityofoccurrenceunderourassumeddistribution.

DiversifiedInflation‐Related(+0.25%)Weadjustedtheassumedriskupwardtomakethecategory’sactualworst‐caseexperiencegreaterthana2%probabilityofoccurringundertheassumeddistribution.

MarketableAlternatives(+2.11%)

Thisadjustmentaveragesourtwoapproachesformodelingthehistoryforthisassetcategory.Theupwardadjustmentmakestheriskassumptionhalfwaybetweenthehistoricallymeasuredvolatilityofeachapproach.

31

CORRELATIONCOEFFICIENTSOurforward‐lookingcorrelationassumptionsaremostlyderivedfromlong‐termhistorybutemphasizetherecentpast.Ourprocessfirstidentifiesareasonableproxyforeachassetcategory,typicallyanindexthatrepresentstheassetclass.Forseveralassetclasses,wehaveusedourjudgmenttoconstructaproxyreturnstreamfortheassetclassthateitherhasalongerhistoryforevaluation,ortoconstructamarketableproxyforanon‐marketableasset.Ourcorrelationassumptionsarebasedonthesereturnstreams:Inflation USCPICashEquivalents 91‐DayT‐BillsLow‐DurationFixedIncome Barclays1‐3YearGovernment/CreditCoreFixedIncome BarclaysUSAggregateNon‐CoreFixedIncome 50%MLHighYieldMasterII,50%JPMorganEMBIbackto1994;

100%MLHighYieldMasterIIbefore1994Long‐DurationFixedIncome BarclaysLongGovernment/CreditTIPS BarclaysUSTIPSUSEquity Russell3000backto1979;S&P500before1979USLarge‐CapEquity Russell1000backto1979;S&P500before1979USSmall‐CapEquity Russell2000Non‐USEquity MSCIACWIexUSIMIbackto1994;MSCIEAFEbefore1994Non‐USLarge‐CapEquity MSCIACWIexUSbackto2001;MSCIEAFEbefore2001Non‐USSmall‐CapEquity MSCIACWIexUSSmallCapEmergingMarketsEquity MSCIEmergingMarketsRealEstate FTSENAREIT,NCREIF,andNCREIFODCEMarketableAlternatives HFRIFundofFundsDiversifiedInflation‐Related 1/3each:FTSENAREIT,BarclaysUSTIPS,BloombergCommodityNon‐MarketableAlternatives Averageof2xtheNon‐CoreFixedIncomeseriesand2xtheUS

EquityseriesUsingthosestreams,weconstructedacorrelationmatrixthattakesthesimpleaverageoffourothercorrelationmatrices–constructedwith3years,5years,and10yearsofdata,andonewithasmuchdataaspossiblegoingbacktoeachseries’inception.Averagingthesefourmeasuresgivesacknowledgementtothelong‐termhistorywhileemphasizingtherecentpast,whencorrelationshavebeenhigherthanlong‐termhistoryhasdelivered.Thisapproachisthereforeconservativeinthediversificationbenefitthatwillappearfromcorrelationinourmodeling.Wequalitativelyadjustedonlytherealestatecorrelationcoefficients.OurassumedcoefficientsforrealestateaveragethecalculatedcoefficientsforpublicREITsandprivaterealestate.Finally,weranourcalculatedcorrelationcoefficientsthroughtheIbbotsonstatisticalcorrelationmatrixtester,whichmadeslightadjustmentstoensurethatthematrixispositivesemi‐definite.

32

Ourassumedreturncorrelationmatrixfollows:

Inflation

CashEquivalents

Low‐DurationFixedIncome

CoreFixedIncome

Core‐PlusFixedIncome

Non‐CoreFixedIncome

Long‐DurationFixedIncome

TIPS

USEquity

USLarge‐CapEquity

USSMID‐CapEquity

Non‐USEquity

Non‐USLarge‐CapEquity

Non‐USSmall‐CapEquity

EmergingMarketsEquity

RealEstate

DiversifiedInflation‐Related

MarketableAlternatives

Non‐MarketableAlternatives

Inflation

1.00

0.03‐0.06‐0.19‐0.090.11‐0.260.01

0.08

0.08

0.11

0.10

0.09

0.13

0.09‐0.030.13

0.14

0.09

CashEquivalents

0.031.00

0.21

0.00‐0.06‐0.14‐0.06‐0.02‐0.17‐0.17‐0.16‐0.10‐0.10‐0.07‐0.03‐0.060.02‐0.11‐0.17

Low‐DurationFixedIncome

‐0.060.211.00

0.76

0.70

0.33

0.54

0.64

0.00

0.00

0.00

0.13

0.14

0.12

0.16

0.28

0.38

0.06

0.12

CoreFixedIncome

‐0.190.00

0.761.00

0.91

0.41

0.93

0.80‐0.04‐0.04‐0.050.07

0.07

0.07

0.10

0.39

0.39

0.01

0.13

Core‐PlusFixedIncome

‐0.09‐0.060.70

0.911.00

0.74

0.83

0.83

0.27

0.28

0.25

0.40

0.40

0.39

0.42

0.55

0.63

0.27

0.47

Non‐CoreFixedIncome

0.11‐0.140.33

0.41

0.741.00

0.33

0.54

0.68

0.69

0.65

0.79

0.79

0.76

0.78

0.50

0.76

0.60

0.83

Long‐DurationFixedIncome

‐0.26‐0.060.54

0.93

0.83

0.331.00

0.72‐0.10‐0.09‐0.110.00

0.00‐0.010.03

0.34

0.30‐0.050.06

TIPS

0.01‐0.020.64

0.80

0.83

0.54

0.721.00

0.08

0.09

0.08

0.26

0.25

0.27

0.30

0.41

0.57

0.15

0.26

USEquity

0.08‐0.170.00‐0.040.27

0.68‐0.100.081.00

1.00

0.93

0.85

0.86

0.80

0.73

0.44

0.60

0.74

0.93

USLarge‐CapEquity

0.08‐0.170.00‐0.040.28

0.69‐0.090.09

1.001.00

0.92

0.86

0.86

0.79

0.73

0.43

0.60

0.74

0.93

USSM

ID‐CapEquity

0.11‐0.160.00‐0.050.25

0.65‐0.110.08

0.93

0.921.00

0.79

0.79

0.77

0.69

0.44

0.61

0.74

0.88

Non‐USEquity

0.10‐0.100.13

0.07

0.40

0.79

0.00

0.26

0.85

0.86

0.791.00

1.00

0.96

0.90

0.40

0.70

0.77

0.88

Non‐USLarge‐CapEquity

0.09‐0.100.14

0.07

0.40

0.79

0.00

0.25

0.86

0.86

0.79

1.001.00

0.95

0.90

0.41

0.70

0.76

0.88

Non‐USSm

all‐CapEquity

0.13‐0.070.12

0.07

0.39

0.76‐0.010.27

0.80

0.79

0.77

0.96

0.951.00

0.88

0.37

0.69

0.78

0.83

EmergingMarketsEquity

0.09‐0.030.16

0.10

0.42

0.78

0.03

0.30

0.73

0.73

0.69

0.90

0.90

0.881.00

0.36

0.68

0.67

0.79

RealEstate

‐0.03‐0.060.28

0.39

0.55

0.50

0.34

0.41

0.44

0.43

0.44

0.40

0.41

0.37

0.361.00

0.78

0.38

0.63

DiversifiedInflation‐Related

0.13

0.02

0.38

0.39

0.63

0.76

0.30

0.57

0.60

0.60

0.61

0.70

0.70

0.69

0.68

0.781.00

0.49

0.72

MarketableAlternatives

0.14‐0.110.06

0.01

0.27

0.60‐0.050.15

0.74

0.74

0.74

0.77

0.76

0.78

0.67

0.38

0.491.00

0.74

Non‐MarketableAlternatives

0.09‐0.170.12

0.13

0.47

0.83

0.06

0.26

0.93

0.93

0.88

0.88

0.88

0.83

0.79

0.63

0.72

0.741.00

SellwoodConsulting2016CorrelationCoefficientAssumptions

33

SOURCESWearegratefultoseveralsourcesforouranalysis.Theywere:FRED,TheSt.LouisFedFederalReserveEconomicData

http://research.stlouisfed.org/fred2/

FTSENAREIThttps://www.reit.com/data‐research/reit‐indexes/ftse‐nareit‐us‐real‐estate‐index‐historical‐values‐returns

ProfessorAswathDamodaran,SternSchoolofBusiness http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/implpr.html

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2581517

ResearchAffiliateshttp://www.researchaffiliates.com

Blackrock http://www.blackrock.com

PIMCO http://www.pimco.com

Standard&Poors http://www.standardandpoors.com

UrbanLandInstitutehttp://uli.org/research/centers‐initiatives/center‐for‐capital‐markets/barometers‐forecast‐and‐data/uli‐real‐estate‐consensus‐forecast/

MorganStanleyCapitalInternationalhttp://www.msci.com/

Moodyshttps://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_151031https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_154805

Russellhttp://www.russell.com/indexes/documents/US_Indexes_comparison.pdf

ProfessorRobertShillerhttp://www.econ.yale.edu/~shiller/data.htm

Vanguardhttps://personal.vanguard.com/pdf/s338.pdf

ThisworkislicensedunderaCreativeCommonsAttribution‐NoDerivatives4.0InternationalLicense.Toviewacopyofthislicense,visithttp://creativecommons.org/licenses/by‐nd/4.0/.

34

Related Documents