February 2015 2015 STRATEGIC DIRECTIONS: SMART UTILITY

2015 Strategic Directions: Smart Utility Report

Jul 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Feb

ruar

y 2

01

5 2015 STRATEGIC DIRECTIONS:

SMART UTILITY

SMART CITIES

2

25.0%

57.6%

17.4%

Smart City Initiative Announced

Yes No Don't know

SMART CITY INITIATIVES MAKE HEADLINES

41.3%

33.7%

33.1%

32.0%

30.2%

18.6%

12.2%

Assessing readiness

Currently in the planning stageswith relevant stakeholders

Creating a roadmap

Currently in the piloting stage

Preliminary discussions

Implementing a large-scaleSmart City deployment

Other

Foundational Activities Being Examined

3

EFFICIENCY, RESILIENCY DRIVE SMART INITIATIVES

What do you see as the primary driver of Smart City initiatives in your region?

42.5%

15.6%

8.7%

7.9%

6.6%

5.7%

2.6%

2.3%

8.2%

Improving efficiency of operations/ reducingoperating costs

Environmental/resource sustainability

Better overall management of communitysystems

Increasing critical infrastructure resilience

Attracting business investment

Increasing customer satisfaction

Improving safety and security

Increasing resident/student satisfaction/attracting new residents/students

Don’t know

4

SMARTER UTILITIES ENABLE SMART CITIES

What do you see as the top three most important systems into a smart city program to invest in first?

48.0%

41.0%

39.9%

31.1%

29.3%

22.4%

19.9%

11.9%

7.9%

7.3%

4.6%

2.7%

10.0%

Smart electric grid

Energy management systems (buildings, campuses, regions)

High-speed data network

Smart water systems

Smart buildings (energy/water efficient, smart appliances)

Renewable/distributed generation

Smart transportation

Smart waste systems

Smart street lighting

Microgrids or nanogrids

Interactive kiosks/ community information systems

Other

Don’t know

5

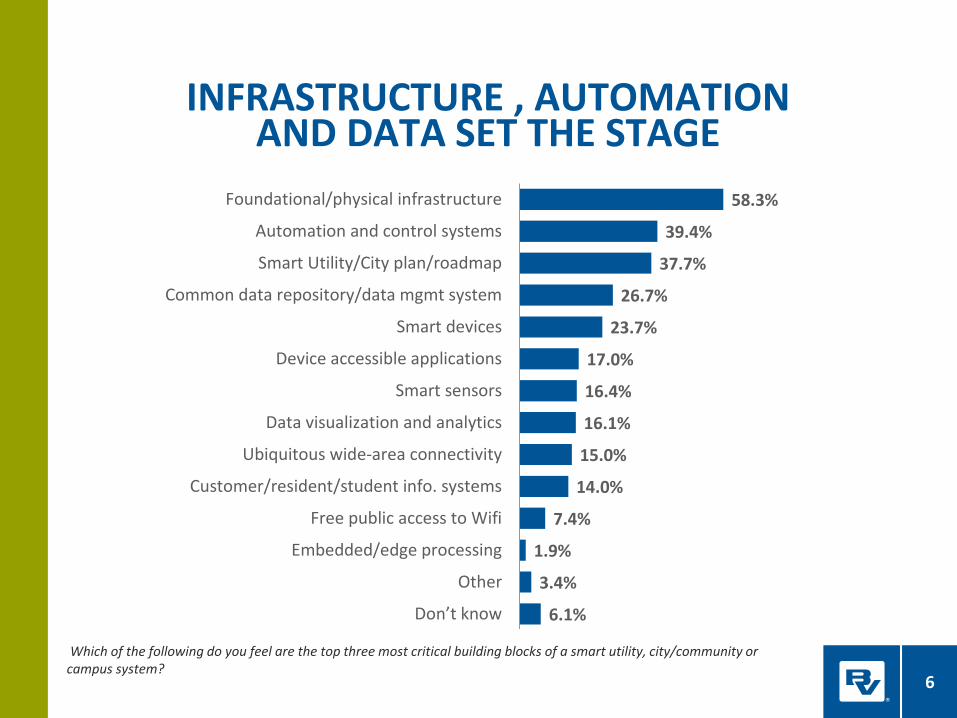

INFRASTRUCTURE , AUTOMATION AND DATA SET THE STAGE

Which of the following do you feel are the top three most critical building blocks of a smart utility, city/community or campus system?

58.3%

39.4%

37.7%

26.7%

23.7%

17.0%

16.4%

16.1%

15.0%

14.0%

7.4%

1.9%

3.4%

6.1%

Foundational/physical infrastructure

Automation and control systems

Smart Utility/City plan/roadmap

Common data repository/data mgmt system

Smart devices

Device accessible applications

Smart sensors

Data visualization and analytics

Ubiquitous wide-area connectivity

Customer/resident/student info. systems

Free public access to Wifi

Embedded/edge processing

Other

Don’t know

6

ROI CHALLENGES, CUSTOMER BUY-IN LIMIT PROGRESS

What are the top three hurdles that must be overcome to enable utility, city/community or campus systems to be managed in a smarter, more integrated way?

64.0%

36.9%

31.0%

25.6%

18.3%

18.1%

17.9%

17.7%

14.9%

13.4%

13.1%

7.3%

3.3%

5.3%

Budget constraints

Lack of resources or expertise

Policy hurdles

Gaining stakeholder support

Ownership across departments

Short-term mindset

Security concerns

Time constraints/other priorities

Lack of incentives

Process hurdles

Technology availability

Cultural barriers

Other

Don’t know

7

OPTIMISM PREVAILS DESPITE HESITATION

When do you believe there will be widespread adoption and implementation of the Smart City model across the United States?

0.7%

10.0%

31.6%

25.0%

4.1%

10.9%

17.6%

Never

In the next 1-5 years

In the next 6-10 years

In the next 11-15 years

In the next 16-19 years

In the next 20+years

Don’t know

8

TELECOMMUNICATIONS

9

TELECOM NETWORKS REQUIRE UPGRADES

56.6%

48.4%

41.4%

40.7%

34.5%

27.3%

6.0%

Needed to support capacity demandsfor Smart Grid/Smart Utility initiatives

Infrastructure is needed to supportmobile workforce

Infrastructure is obsolete or nearobsolete

Infrastructure is needed because ofcyber security initiatives

Needed to support future renewableintegration projects

To support IP network convergence

Other reason

Top Reasons For Improving Communications Infrastructure

What are the top three reasons you are planning on upgrading or building communications infrastructure in the next 5 years?

10

LEGACY CONNECTIONS SUNSET, IP RISING

26.5%

9.3%

17.9%

46.3%

Yes, considering IP networkConvergence

Yes, planning on implementingover the next 2 years

Yes, actively in the process ofconverging networkinfrastructure through an IP

No, we are not activelypursuing IP networkconvergence

Are you considering, planning or currently deploying IP network convergence?

11

IMPACT OF NEXT GENERATION TECHNOLOGIES AND STATUS OF MIGRATION

6.2%

15.7%18.0%

7.2%

11.1%12.7%

29.1%

0%

20%

40%

Major impact,already

complete withour migration

Major impact,implementingour migration

now

Major impact,still finalizingour migration

plans

Minor impact,already

complete withour migration

Minor impact,implementingour migration

now

Minor impact,still finalizingour migration

plans

Little or noimpact to our

network

Telecommunications carriers are migrating service offerings away from Frame Relay Services to next generation technologies such as IP/MPLS. What impact do you anticipate this will have on your network, and what is the status of your migration? 12

BIGGEST SECURITY CONCERNS REGARDING MANAGEMENT AND THE USE OF DATA

38.2%

18.6%

13.2%

9.6%

8.4%

0.3%

2.0%

Unauthorized system access

Data integrity

Regulatory compliance

Maintaining customer privacy

Data loss

Other

Data security is not a big concern

13

NEW REGULATIONS EMPHASIZE SECURITY

Why have you not implemented a public carrier cellular network solution?

42.9%

10.5%

31.1%

15.5%

Reasons for Not Implementing a Public Carrier Cellular

Network Solution

It does not meet our security requirements

It does not meet our requirements for QoS thatguarantee prioritization of critical utility trafficIt is not as cost effective as our private networksolutionDon’t know

14

TOP REASONS FOR DEPLOYING IP NETWORK CONVERGENCE

73.4%

62.2%

33.9%

14.0%

3.4% 2.2%

0%

20%

40%

60%

80%

Increased amountof data &

bandwidthcapabilities to

support operations

Demand foroperational

efficiency andlower operational

expense

Security concerns Op Ex savings Environmentalinitiatives

Other

15

AUTOMATION PROGRAMS

16

AUTOMATION PROGRAMS BEINGDEPLOYED

. Which of automation initiatives are you currently implementing?

51.2%

48.7%

36.2%

29.9%

25.0%

17.7%

17.7%

16.4%

14.4%

1.6%

11.8%

Enterprise-wide

Asset management

Cyber or physical security

Electric substation

Water or natural gas production,transmission, treatment facilities

Water or natural gas unmanned facilities

Water or natural gas distribution mainmonitoring and/or control

Water or natural gas customers

Electric distribution

Other

No, we are not currently implementingautomation initiatives

17

AREAS WHERE AUTOMATION PROGRAMS ARE CURRENTLY BEING IMPLEMENTED

2.1%

49.9%33.4%

14.5% Only where mandated

Only where there is positive businesscase support for new capabilities orservices

Where needed to replace outdatedequipment

Enterprise-wide regardless ofwhether it is mandated or wherethere is positive business casesupport

Which of the following best describes the areas where you are implementing automation programs?

18

DATA MANAGEMENT & ANALYTICS

19

DATA ANALYTICS CURRENTLY IMPROVES OPERATIONAL PERFORMANCE

35.4%

28.0% 27.3%

18.6%

8.1%

34.3%

0%

20%

40%

Descriptiveanalytics

Closed-loopoptimization

Predictiveanalytics

Prescriptiveanalytics

None of theabove

Don’t know

What types of data analytics does your organization currently use to improve its operational performance?

20

BUSINESS AREAS THAT WILL BENEFIT MOST FROM INCREASED DATA MANAGEMENT AND ANALYTICS CAPABILITIES

38

67.1%

44.5%

27.1%

27.0%

26.8%

24.6%

19.7%

14.6%

1.3%

Asset management

Capital investment prioritization

Customer service/engagement

Customer billing, collections and/or revenue protection

Evaluating strategic options/scenarios

Risk management

Business case development

Rate making or dynamic pricing

Other

21

OPERATIONAL AREAS THAT WILL BENEFIT MOST FROM INCREASED DATA MANAGEMENT AND ANALYTICS CAPABILITIES

48.8%

47.8%

42.9%

28.4%

24.1%

18.0%

17.7%

17.1%

7.5%

0.4%

Evaluating operational or maintenance options/scenarios

Improving/maintaining service reliability

Monitoring performance

Identifying issues and losses

Infrastructure resiliency and recovery

Resource conservation /operating efficiency

Outage management

Regulatory compliance/reporting

Streamlining projects

Other

22

www.bv.com

Related Documents