Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHINA ECONOMIC OVERVIEW

CHINA GDP AND GDP PER CAPITA

3

Source: National Bureau of Statistics – Jun 2015

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

0%

5%

10%

15%

20%

25%GDP PER CAPITA (USD)

Source: National Bureau of Statistics, IMF

RMB 45,385 (USD $7,262)2014 GDP Per Capita - China

USD$10,9232014 GDP Per Capita – Global Average

+4%YOY

VS.

CHINA'S GDP GROWTH YEAR-ON-YEAR

8.1%

7.6%7.4%

7.9%7.7%

7.5%

7.8%7.7%

7.4%7.5% 7.4%7.3%

5.8%

6.5%

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2

7.2%

Chinese economy slows down in 2015 with growth dropping to 6.5%. GDP per Capita-China inches closer to the global average.

CONSUMER CONFIDENCE

4

Source: National Bureau of Statistics – Jul 2015

CONTRIBUTION FACTORS

• GDP distribution structure adjustment (shift from heavy industrial production based economy towards services focused enrironment)

• Central bank further lower rates and loosened loan restrictions

• Consistent low unemployment rate

• Steady development of disposable household income

• Government’s policy to encourage consumption, especially for lower tiers

CHINA CONSUMER CONFIDENCE

85

90

95

100

105

110

115

Even with a slowdown in the Economy China’s consumer confidence remains well above 100 and well above the 2008 crisis levels.

CHINA ADVERTISING OVERVIEW

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015; iResearch 2014-2015

TOTAL MONITORED AD INVESTMENT

6

17.0%

-1.3%0.2%

-3.0%

-18.8%

-12.6% -13.2% -14.6%

4.1%

-4.8%-1.9%

-4.3%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Jul2014

Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun

Ad Investment YOY Growth

TOTAL MONITORED AD INVESTMENT (Jul 2014 - Jun 2015): RMB 1,243,336 MILLION

RMB: Million

H1 2015-7% YOY Growth

Advertising investment declines by 7% in 2015.

MONITORED SPENDING BY INDUSTRY

7

2%18%

-21%-1% 3%

-10%4%

-25%

25%

-18%-1%

-24%1% 11%

-12%

157%

-50%

0%

50%

100%

150%

200%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Jan-Jun 2014 Jan-Jun 2015 YOYRMB: Million

TOTAL MONITORED AD INVESTMENT BY SECTORS (Jan-Jun 2014 & 2015)

Food and drink still dominates among all categories; Pharmaceuticals keeps stable growing pace and move its place to No.2 while toiletries drops in the opposite.

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015; iResearch 2014-2015

OVERALL MEDIA LANDSCAPE

39%digital

61%traditional

34%digital

66%traditional

31%digital

69%traditional

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015

SHARE OF TIME SPENT 2012-2015

Internet via mobile phone

Internet via others

TV

Magazine

Newspaper

Radio

29%digital

33%digital 39%

digital 42%digital67%

traditional

71%traditional

61%traditional

58%traditional

MEDIA COVERAGE BY CHANNELS

10

18% 19%

74%

59%

33%

28%

96% 95%

62%

71%

23%

58%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 Q1

MEDIA PENETRATION 2012-2015

TV

Internet via others

Newspaper

Internet via mobile phone

Magazine

Radio

+9%

+35%

Source: CMMS Summer 2013-2015Note: Internet in Share of time spent including PC and mobile internet.

Digital media continues to grow penetration at a steady pace of 9% while Mobile internet consumption sees a massive jump in penetration of 58%.

CROSS TIERS MEDIA CONSUMPTION

11

Source: CMMS Summer 2013-2015

0.2 0.2 0.2 0.2 0.1 0.2 0.2 0.2 0.2

0.5 0.5 0.4 0.4 0.4 0.3 0.4 0.4 0.3

0.1 0.1 0.1 0.0 0.0 0.0 0.1 0.1 0.1

3.0 3.0 2.82.6

2.4 2.4 2.3 2.2 2.1

1.8 2.02.0

1.11.3 1.2 1.1

1.11.0

0.30.6 0.8

0.3 0.5 0.80.4 0.6 0.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2013 2014Tier 1

2015 2013 2014Tier 2

2015 2013 2014Tier 3

2015

TIME SPENT ON MEDIA PER DAY, BY CITY TIER 2013-2015

Internet via mobile phones

Internet via others

TV

Magazine

Newspaper

Radio

36%digital

41%digital

45%digital

30%digital

37%digital

41%digital 34%

digital37%

digital

41%digital

Tier 1 continues to consume more media while increase in Digital consumption across tiers.

2.4

1.8 1.92.0

2.1 2.3

3.0

1.4

1.4

1.82.0

1.9 1.70.7

0.8

1.0

1.3

1.3 1.1 0.9

0.3

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Total population 15-19 20-24 25-29 30-34 35-39 40+

TIME SPENT ON MEDIA PER DAY, BY AGE GROUP 2015

Mobile Internet via mobile phone

Internet via others

TV

Magazine

Newspaper

Radio

MEDIA CONSUMPTION BY AGE

12

Young people continue to drive heavy digital consumption, in contrast to the 40+ age group.

Source: CMMS Summer 2015

52%digital

57%digital

56%digital

52%digital

48%digital

22%digital

42%digital

CHINA DIGITAL LANDSCAPE

TOTAL POPULATION

27.8%72.2% OF NETIZENS

URBAN RURAL

INTERNET PENETRATION6% YOY

49% OF TOTAL POPULATION668,000,000NETIZENS

594,000,000 89% OF NETIZENS

MOBILE WEBMOBILE NETIZENS 13% YOY

Nearly half the population has internet access with higher growth in mobile netizensof 13%.

Sources: National Bureau of Statistics of China Dec 2014; CNNIC July 2015

DIGITAL LANDSCAPE

1,367,820,000

14

NETIZENS GROWTH RATE

Growth rate of netizens and mobile netizens is slowing down.

Sources: CNNIC July 2011-2015

485

538

591632

668

318

388

464

527

594

15%

11%10%

7%6%

15%

22%

20%

14%13%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015

TOTAL NETIZEN & MOBILE NETIZEN GROWTH(2011-2015)

Netizens Mobile Netizens Netizen Growth Mobile Netizen Growth

Units: Million

15

31% 32%

20% 19%

13% 12%

2% 7%8% 6%5% 5%5% 4%

11% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

14-Jun 15-Jun

SHARE OF TIME SPENT

Video IM Game

Finance Social Search

E-comment Entertainment News

Others

MEDIA CONSUMPTION ON PC

-20%

-15%

-10%

-5%

0%

5%

10%

15%

0

100,000

200,000

300,000

400,000

500,000

600,000

Sear

ch IM

Vid

eo

New

s

Soci

al

E-co

mm

erce

Ente

rtai

nm

ent IT

Fin

ance

Emai

l

Life

Edu

cati

on

Gam

e

Au

to

Mar

keti

ng

Rea

lEst

ate

On

line

Rec

ruit

men

t

Trav

elin

g

BB

S

MONTHLY COVERAGE BY CATEGORY

Jun-14 Jun-15 YoY Growth

-1%

1%

Source: iUserTracker Jun 2014 & 2015, including key categories (IM) of PC software.

(‘000)

5%

16

On PC, user behavior across categories remained relatively unchanged for most categories however categories like IT and finance witness big spikes in growth.

MEDIA CONSUMPTION ON MOBILE

-20%

0%

20%

40%

60%

80%

100%

0

100,000

200,000

300,000

400,000

500,000

600,000

MONTHLY COVERAGE BY CATEGORY

Jan-15* Jun-15 Growth(Jun/Jan)

22% 24%

17% 18%

12% 8%

7% 7%5% 6%4% 5%4% 4%3% 2%

21% 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-15* Jun-15

SHARE OF TIME SPEND

IM Online VideoTheme Plug-in GameSearch BrowserSocial E-readingNews&Information Online ShoppingOthers

2%

Source: mUserTracker Jan & Jun 2015 (*not compare with Jun 2014 due to huge gap after panel change), search combine both APP and site.

(‘000)

1%

-4%

17

IM is the most used on Mobile and still growing. Travel witnesses massive growth in 2015

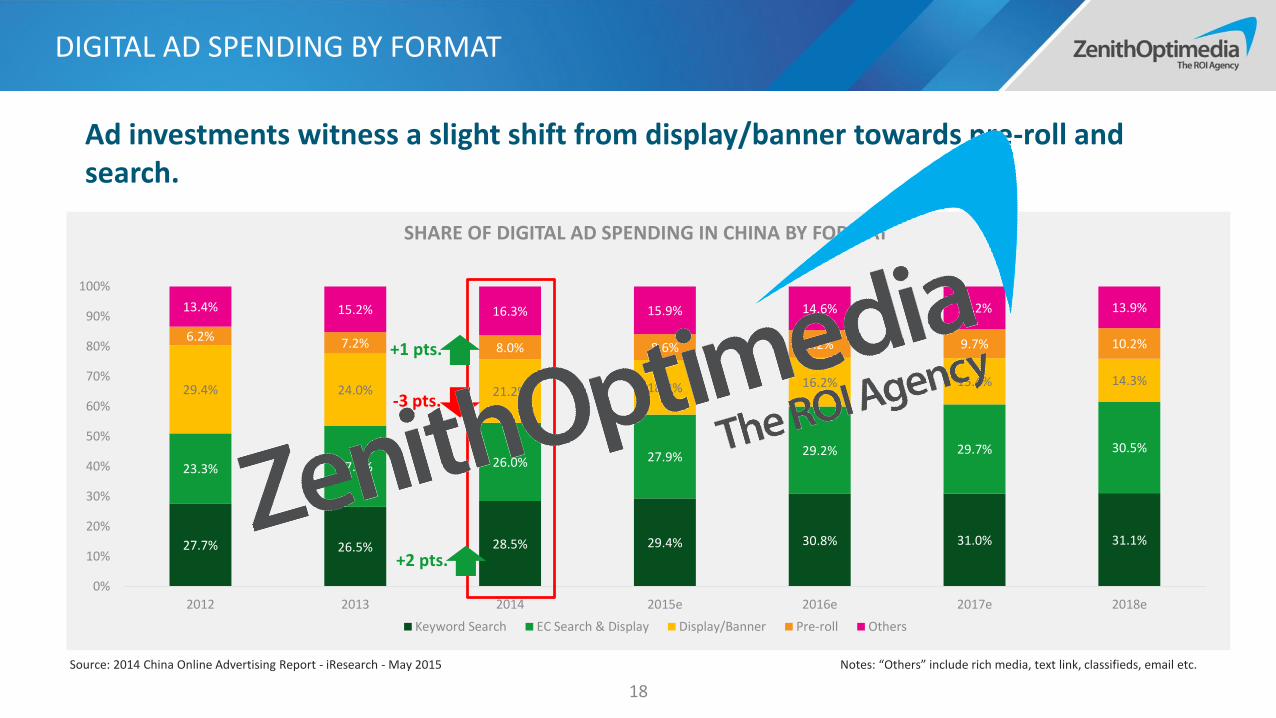

DIGITAL AD SPENDING BY FORMAT

18

27.7% 26.5% 28.5% 29.4% 30.8% 31.0% 31.1%

23.3% 27.1% 26.0% 27.9% 29.2% 29.7% 30.5%

29.4% 24.0% 21.2% 18.2% 16.2% 15.4% 14.3%

6.2% 7.2% 8.0% 8.6% 9.2% 9.7% 10.2%

13.4% 15.2% 16.3% 15.9% 14.6% 14.2% 13.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015e 2016e 2017e 2018e

SHARE OF DIGITAL AD SPENDING IN CHINA BY FORMAT

Keyword Search EC Search & Display Display/Banner Pre-roll Others

Source: 2014 China Online Advertising Report - iResearch - May 2015 Notes: “Others” include rich media, text link, classifieds, email etc.

-3 pts.

+2 pts.

+1 pts.

Ad investments witness a slight shift from display/banner towards pre-roll and search.

INTERNET+ BOOST FASTER TRANSFORMATION

19

KEY FEATURES OF INTERNET+

Traditional companies are expected to achieve rapid transformation under the Internet+ policy, as well as internet giants struggle for further growth.

• Internet+ is a new generation of ICT (Information Communication Technology), which connect any traditional industry with internet.• It was proposed by Pony Ma (Chairman of Tencent) in NPC&CPPCC early 2015, further supported by government with action plan, and become a hot topic in China Internet Conference.

CROSS BOUNDARY跨界融合

INNOVATIVE DRIVEN创新驱动

STRUCTURAL REMODELLING重塑结构

RESPECT HUMANITY尊重人性

OPEN ENVIRONMENT开放生态

CONNECT EVERYTHING连接一切

-

1,000

2,000

3,000

4,000

5,000

6,000

INDUSTRY INVESTMENT OF KEY DIGITAL COMPANIES IN 2014

Baidu

Alibaba

Tencent

Qihoo360

Xiaomi

Source: ITJUZI.COM

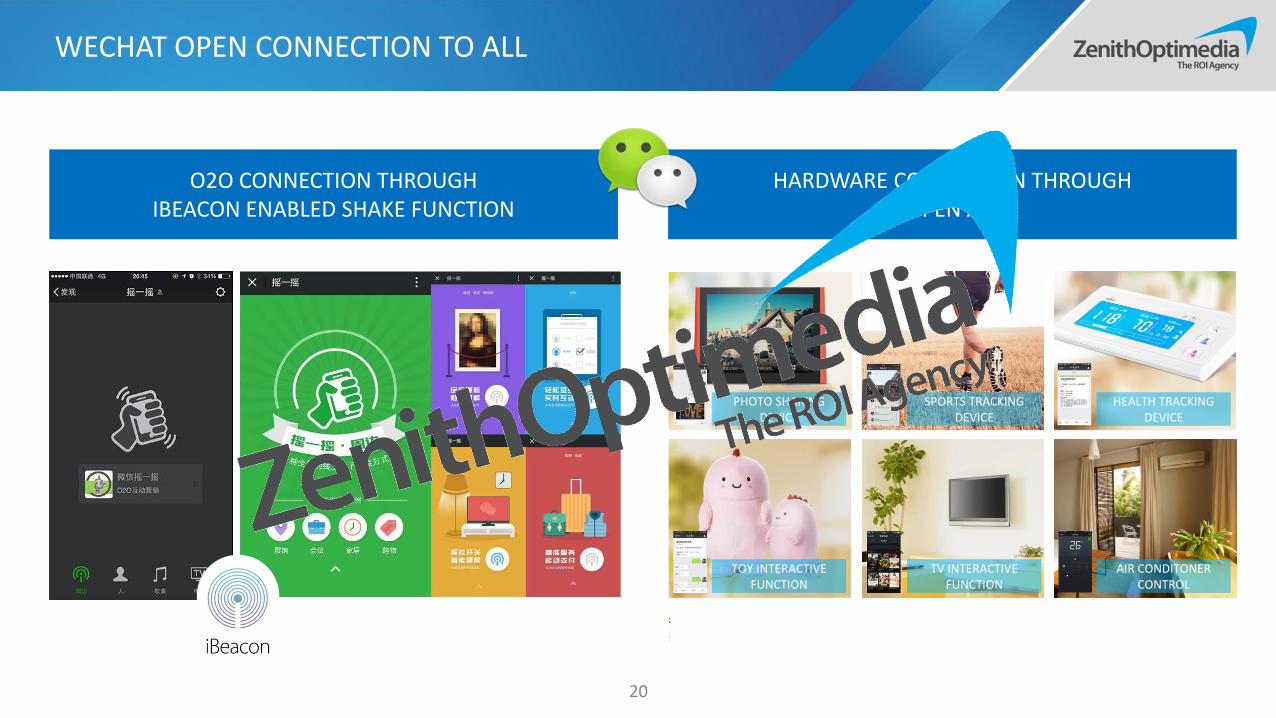

WECHAT OPEN CONNECTION TO ALL

20

O2O CONNECTION THROUGH IBEACON ENABLED SHAKE FUNCTION

HARDWARE CONNECTION THROUGHOPEN API

PHOTO SHARING DEVICE

SPORTS TRACKING DEVICE

HEALTH TRACKING DEVICE

TOY INTERACTIVE FUNCTION

TV INTERACTIVE FUNCTION

AIR CONDITONER CONTROL

THE INTERPRETATION OF NEW ADVERTISING LAW

21

New Advertising Law

Approved on:2015.04.24Force on:2015.09.01Detailed Rules:41Added Rules:33All Rules:75

Introducing a More Detailed Regulatory FrameworkThe existing law is very short and has been widely criticized for being too vague. The amended law is almost double in length and is muchmore prescriptive. The key elements of the rules cover alcohol, health food, medicine, medical device advertising etc. For example,Drinking gestures are banned in alcohol advertising; no one is allowed to promote products of medicine and health food advertising.

Focus on Children and CelebritiesUnder the new law, children under age 10 cannot endorse products at all and celebrity endorsers can be held responsible for false claims inads. If someone makes misleading claims about the product,they will be prohibited endorsement for 3 years.

Tightening Oversight of Mass Media Advertising Release BehaviorAny advertisement published via mass media shall be marked conspicuously as "advertisement" so as to distinguish it from otherinformation and avoid misleading consumers. Radio stations and TV stations shall, when publishing advertisements, comply with theprovisions of the relevant authorities under the State Council on the length of time and means of publishing, and provide clear indicationson the length of time of advertisements.

Added a Slew of Rules Targeting Internet UsersInternet users must be able to close a pop-up ad with a single click, an EDM must contain the users real identity, including their contactdetails, and any other form of electronic direct marketing is prohibited unless the recipient has consented.

"False Advertising" DefinedThe new law clarifies the scope of "false advertising". This would include, for example, fabrication of product efficacy, or claims about aproduct/service which do not match the actual conditions and which have a substantive effect on the decision to purchase.

1

2

3

4

5

MOBILE

REACH BY DEVICE

24

Source: CNNIC Jan 2010 – Jul 2015

Units: Million

Source: MIIT Communication Operation Report, May 2015

83%80% 82%

79% 78%

71%71% 70% 70% 70% 71%

68%

35%40%

50% 49% 49%45% 46% 47%

44% 44% 43% 43%

69%72% 72% 70% 73%

72%74%

79% 81% 83%86%

89%

35% 34%

16% 16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

INTERNET PENETRATION BY DEVICE

Desktop Laptop Mobile Phone Tablet TV

401.6

485.3466

97.3

178

0

100

200

300

400

500

600

2013 2014 2015

TOTAL 3G & 4G USERS IN CHINA

3G Users 4G Users

Mobile reach now overtakes desktop and laptop which have remained flat for sometime. Meanwhile more mobile users upgrade to high-speed 3G and 4G connections.

TIME SPENT ON MOBILE PHONE VS. OTHER DIGITAL

25

Sources: CMMS Summer 2015

1.4 1.41.8 2 1.9 1.7

0.7

0.8 1

1.31.3

1.1

0.9

0.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Total population 15-19 20-24 25-29 30-34 35-39 40+

TIME SPENT ON MOBILE INTERNET VS. DESKTOP INTERNET

Internet via others Internet via mobile phone

36% on mobile phone

42% on

mobile phone

42% on

mobile phone

39% on

mobile phone 37% on

mobile phone35% on

mobile phone

30% on

mobile phone

Teens and college-age users are the heaviest mobile consumers, with mobile phones taking up 42% of digital consumption.

SMARTPHONE OS

26

20.1%

79.0%

0.5% 0.1% 0.3%

2015 JUNE SMARTPHONE SALES

iPhone Android Windows Blackberry Others

Source: Kantar Worldpanel Jun 2015

MEDIAN HOUSEHOLD INCOME BY OPERATING SYSTEM

Source: CMMS Summer 2015

Unit:RMB

9,060

11,081 9,807

8,331 7,992

0

2000

4000

6000

8000

10000

12000

Android iOS WindowsPhone

Blackberry Other OS

IOS continues to expand share with increasing ads investment, driven by need oftarget higher income mobile users.

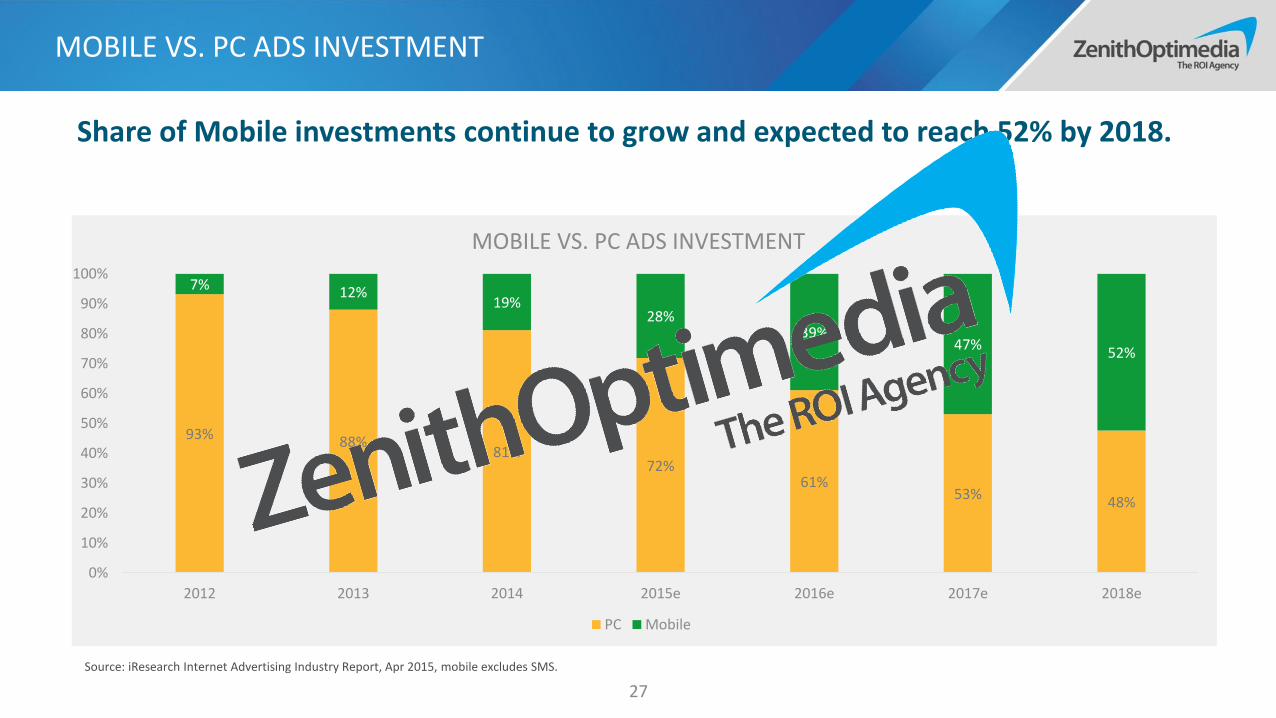

MOBILE VS. PC ADS INVESTMENT

27

93% 88%81%

72%61%

53%48%

7% 12%19%

28%39%

47%52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015e 2016e 2017e 2018e

MOBILE VS. PC ADS INVESTMENT

PC Mobile

Share of Mobile investments continue to grow and expected to reach 52% by 2018.

Source: iResearch Internet Advertising Industry Report, Apr 2015, mobile excludes SMS.

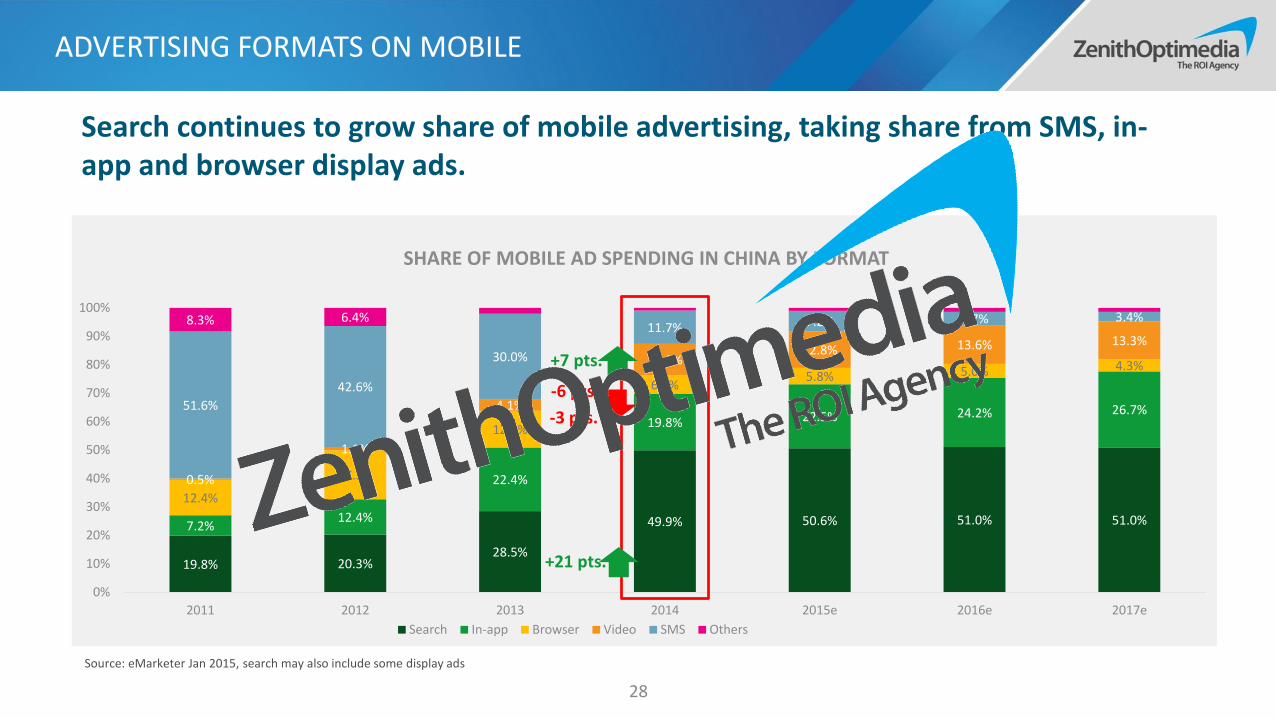

ADVERTISING FORMATS ON MOBILE

28

19.8% 20.3%28.5%

49.9% 50.6% 51.0% 51.0%7.2%12.4%

22.4%

19.8% 22.5% 24.2% 26.7%

12.4%

17.3%

12.9%

6.6%5.8% 5.0% 4.3%

0.5%

1.1%

4.1%

11.0%12.8% 13.6% 13.3%

51.6%

42.6%

30.0%

11.7% 7.2% 4.7% 3.4%8.3% 6.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015e 2016e 2017e

SHARE OF MOBILE AD SPENDING IN CHINA BY FORMAT

Search In-app Browser Video SMS Others

-3 pts.

+21 pts.

+7 pts.

-6 pts.

Source: eMarketer Jan 2015, search may also include some display ads

Search continues to grow share of mobile advertising, taking share from SMS, in-app and browser display ads.

FORMATS & CASES

DISPLAY GAMIFICATION FUNCTIONFOCUS ON STORYTELLING. USE SLIDESHOW OR

ANIMATION TO TELL THE BRAND/PRODUCT STORY OR THE MECHANISM OF A CAMPAIGN

INTEGRATE BRAND/PRODUCT INTO A MINI GAME TO BOOST ENGAGEMENT AND

SHARING

SERVE AS A LONG TERM FUNCTIONAL MOBILE PAGE, WHERE CONSUMER CAN FIND SERVICES SUCH AS E-COMMERCE.

KEY WAYS OF H5 USAGE

30

NATIVE EXPERIENCE

31

《这个陌生来电你敢接吗?》Incoming Call from Avengers

Dianping played a virtual call game from character of The Avenger 2 to promote its discounted movie tickets, which is the first widely distributed campaign using the “incoming call” interactive.

《吴亦凡即将入伍》The Unexpected Entrance of Kris Wu

Tencent game WeFire attracted consumers’ eyeball with a news-like H5 page, to broadcast rumor of celebrity Chris Wu joining army, ended with Chris jump into screen to clarify it himself.

《滴滴打车再见》The Goodbye of Didi Taxi

Didi leveraged the mobile phone interface by testing consumers to keep only one APP, and make it a teaser for its new branding campaign, claiming even the last one will be beaten by Didi.

Imitative H5 interactives tailor-made for the native environment and occasions are able to generate surprises and further drive to viral.

CONNECTED EXPERIENCE

32

Fall in Love with SummerSix God

Love MoreMercedes-Benz

Connecting two mobile phone through QR code becomes a new trend on Valentine’s Day. Utilizing the appeal of love couple, Mercedes-Benz and Six God both launched a mobile campaign by this mechanism on Chinese Valentine’s Day (Qixi). One user scan the QR code on another’s phone, then the animations in both phones will go synchronous.

Multi-screen interactives now able to transform and cater to varied viewer type with experiences that connect them to real people offline.

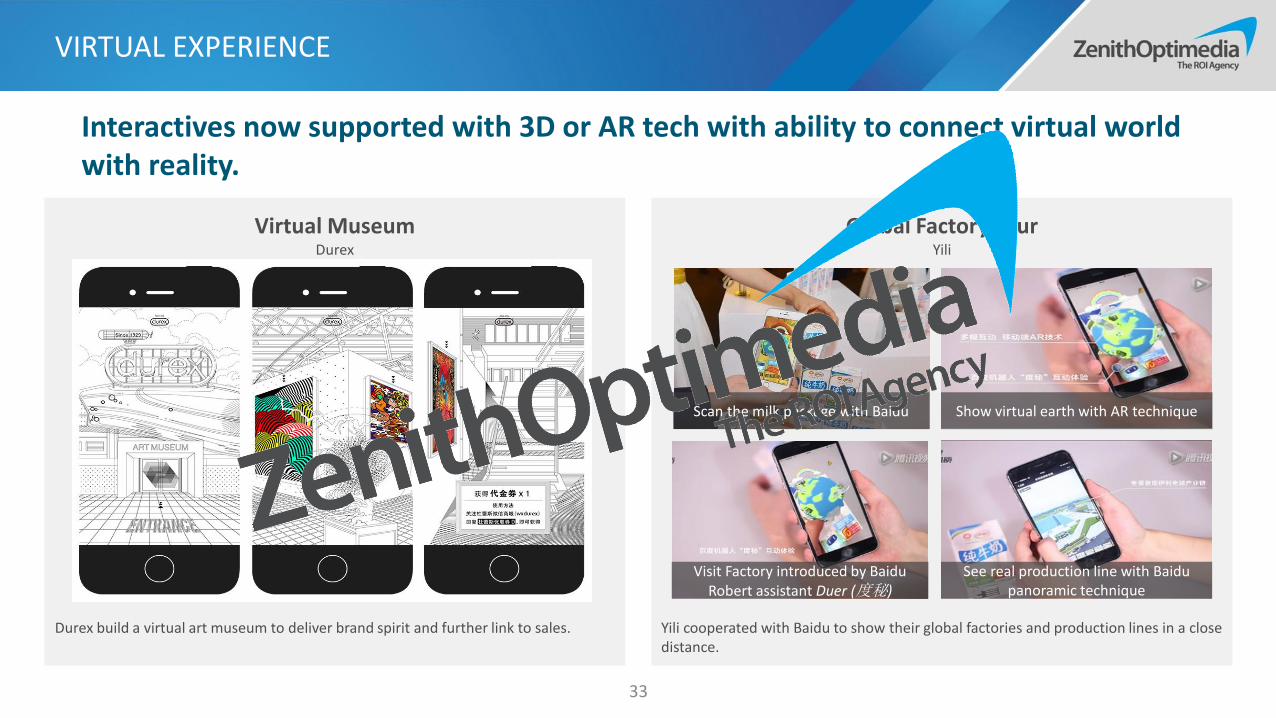

VIRTUAL EXPERIENCE

33

Yili cooperated with Baidu to show their global factories and production lines in a close distance.

Scan the milk package with Baidu Show virtual earth with AR technique

Visit Factory introduced by Baidu Robert assistant Duer (度秘)

See real production line with Baidu panoramic technique

Durex build a virtual art museum to deliver brand spirit and further link to sales.

Interactives now supported with 3D or AR tech with ability to connect virtual world with reality.

Global Factory TourYili

Virtual MuseumDurex

34

Mobile is quickly becoming the devise for convergence between online and offline. The growth of mobile will be further boosted by the government's new Internet + Policy.1.

When creating H5 interactives, keep in consideration the environment and the purchase journey stage the consumers might be in. Native format help build up relevance and enhance creative effectiveness.

2.

Make good use of technology to deliver greater brand experience however make sure it is aimed at achieving business objective.3.

VIEWPOINT ON MOBILE

Use mobile to deliver greater brand experience however do not compromise on reach.4.

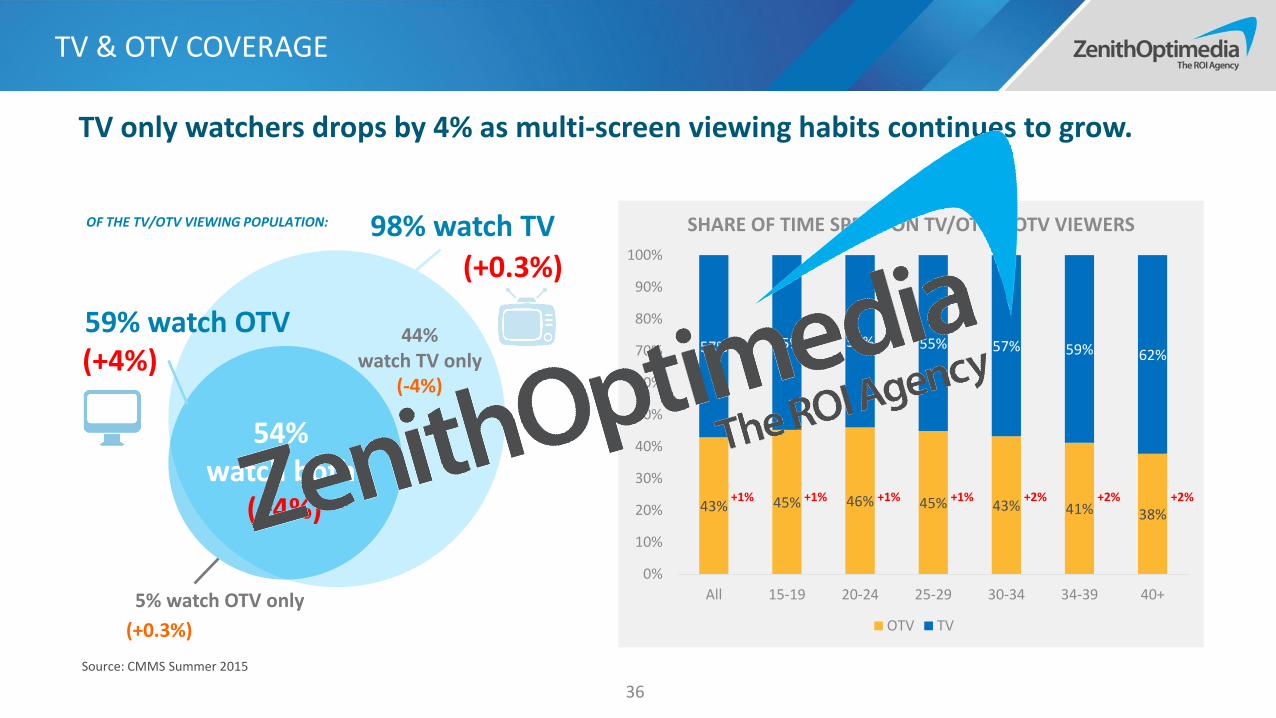

TV & OTV

Source: CMMS Summer 2015

59% watch OTV

98% watch TV

54% watch both

5% watch OTV only

OF THE TV/OTV VIEWING POPULATION:

44% watch TV only

(+4%)

(-4%)

(+0.3%)

(+0.3%)

(+4%)

43% 45% 46% 45% 43% 41% 38%

57% 55% 54% 55% 57% 59% 62%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

All 15-19 20-24 25-29 30-34 34-39 40+

SHARE OF TIME SPENT ON TV/OTV – OTV VIEWERS

OTV TV

+1% +1% +1% +1% +2% +2% +2%

TV & OTV COVERAGE

36

TV only watchers drops by 4% as multi-screen viewing habits continues to grow.

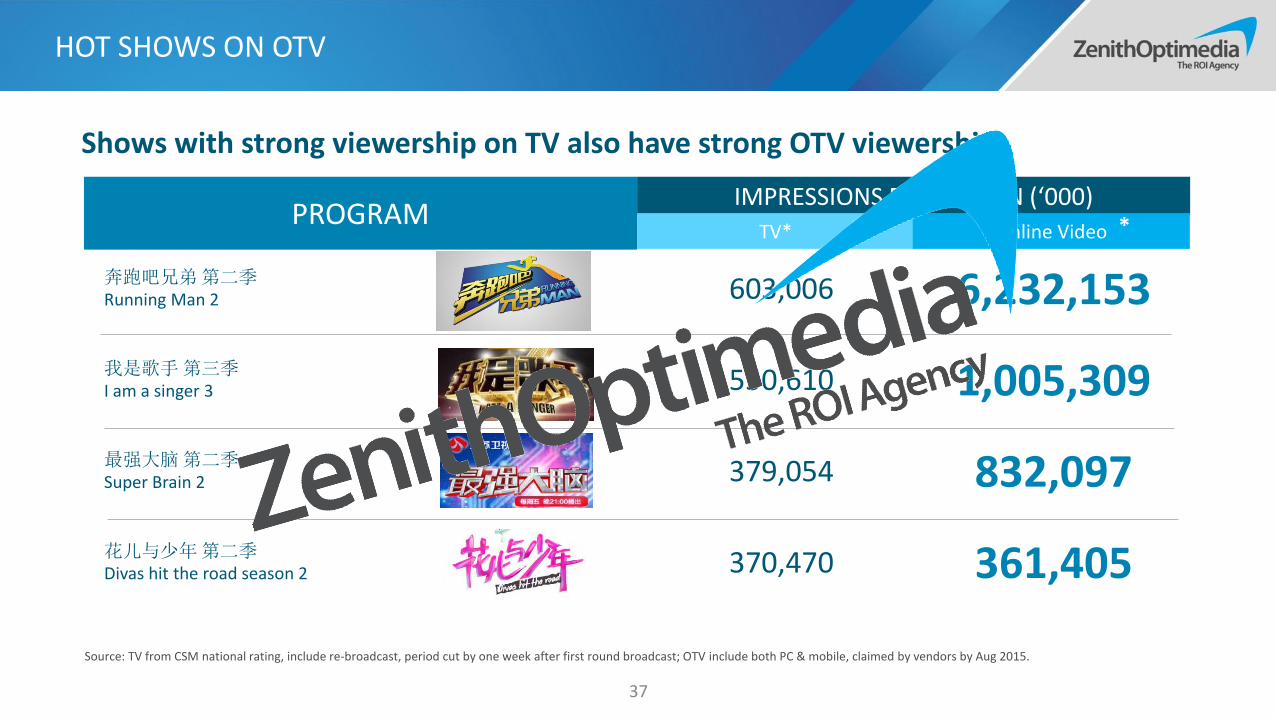

HOT SHOWS ON OTV

37

Source: TV from CSM national rating, include re-broadcast, period cut by one week after first round broadcast; OTV include both PC & mobile, claimed by vendors by Aug 2015.

Impression per episode('000)

TV* OTV

奔跑吧兄弟第二季Running Man 2 603,006 6,232,153

我是歌手第三季I am a singer 3 550,610 1,005,309

最强大脑第二季Super Brain 2 379,054 832,097

花儿与少年第二季Divas hit the road season 2 370,470 361,405

PROGRAMIMPRESSIONS PER SEASON (‘000)

TV* Online Video *

Shows with strong viewership on TV also have strong OTV viewership.

MORE TV STATION JOIN OTV BATTLE

38

Following Hunan PSTV, Zhejiang PSTV also officially launched their own online broadcast platform “China Blue TV” (CZTV.com).

Highly associated with The Voice of China

“China Blue TV” search index:Peak always happen on VOC S4 broadcast day

Same trend for website traffic even from S3 before the official launchPV UV

TV & OTV INTEGRATION

39

HALF HOUR DAILY CLIPS ON TV

24H/7D LIVE BROADCAST

BULLETS SCREEN

REAL TIME CHATTING

360 DEGREE PANORAMA VIEW

Tencent launched a long term survival challenge reality show, which was promoted across multi-platform.

ALWAYS ON ONLINE

FOLLOW & DISCUSS

CUSTORMIZED APP

VOTE & CHEER

TV

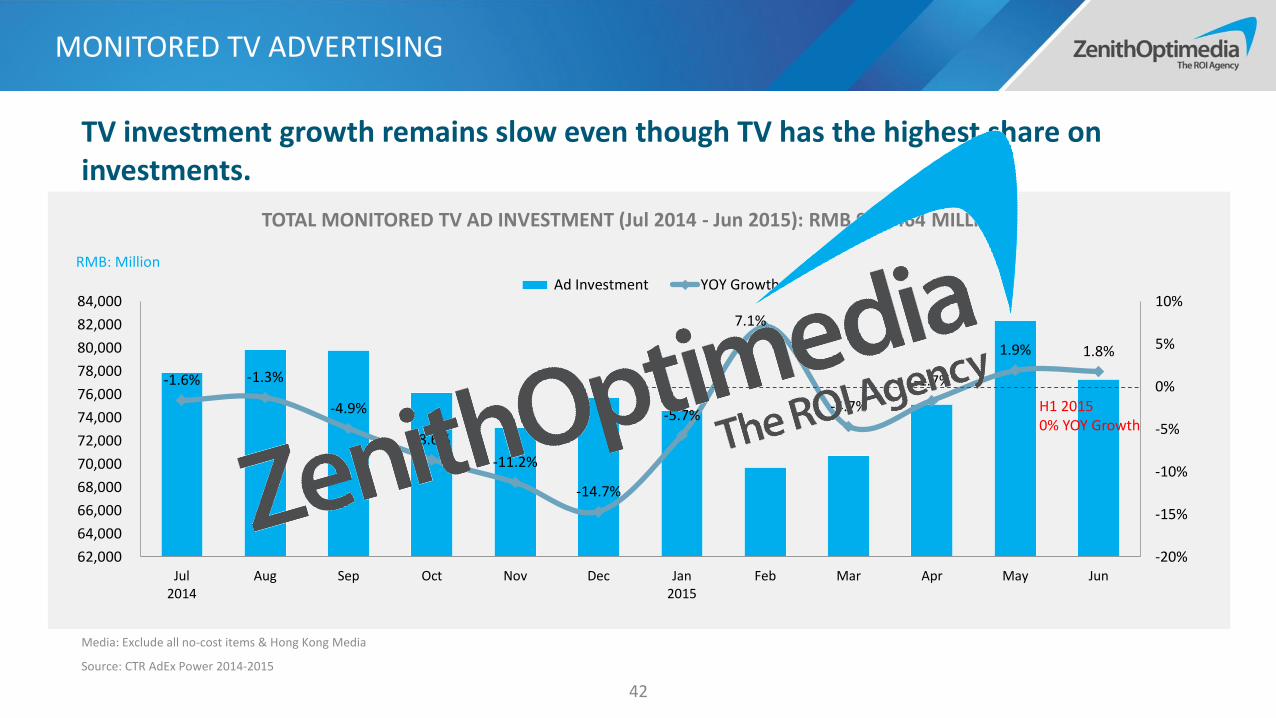

MONITORED TV ADVERTISING

42

RMB: Million

TOTAL MONITORED TV AD INVESTMENT (Jul 2014 - Jun 2015): RMB 912,464 MILLION

-1.6% -1.3%

-4.9%

-8.6%

-11.2%

-14.7%

-5.7%

7.1%

-4.7%

-1.7%

1.9% 1.8%

-20%

-15%

-10%

-5%

0%

5%

10%

62,000

64,000

66,000

68,000

70,000

72,000

74,000

76,000

78,000

80,000

82,000

84,000

Jul2014

Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun

Ad Investment YOY Growth

H1 20150% YOY Growth

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

TV investment growth remains slow even though TV has the highest share on investments.

PRIME TIME TV AD INVESTMENT

43

RMB: Million

TOTAL MONITORED TV IN PRIME TIME (17:00-24:00)AD INVESTMENT (Jul.2014-Jun.2015): RMB 597,775 MILLION

3.1%3.9%

0.7%

-2.9%

-6.8%

-9.0%

-5.0%

7.8%

-8.4%

-5.4%

-1.7%-2.9%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

0

10,000

20,000

30,000

40,000

50,000

60,000

Jul2014

Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun

Ad Investment YOY Growth

H1 2015-3% YOY Growth

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

Prime time investments are similar across months. H1 2015 sees a slight decrease in the average investment.

TV AD INVESTMENT BY CATEGORY

44

RMB: Million

TV MONITORED AD INVESTMENT BY SECTORS (Jan-Jun 2014 & 2015)

19%0%

13%

-23%

1% 4%-10% -13%

29%10%

-15%

29%

-22% -26% -25%

-4%13% 14%

-12% -11%

179%

-50%

0%

50%

100%

150%

200%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Jan-Jun 2014 Jan-Jun 2015 YOY Growth

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

Pharmaceuticals continue to strengthen investments on TV, while massive -23% drop for toiletries.

AHTV CONDUCTED THE LARGEST REVISION IN 18 YEARS ON JULY 2015

45

Data Source:Infosys 2013/1/1-2015/6/6;1800-2330; Target:P20-45 ;cities group

1.41.5

1.81.7 1.6

1.5

1.41.2

1.31.2

1

1.2

1.4

1.6

1.8

2

2.2

2013Q1

2013Q2

2014Q1

2014Q2

2014Q1

2014Q2

2015Q1

2015Q2

2015Q1

2015Q2

2013-2015 part of STV’s market share

AHTV Shandong STV Dragon STV Beijing STV

Market share%

Mon Tue Wed Thu Fri Sat Sun

19:30 The first dolphin theatre (1)

20:30 The first dolphin theatre (2)

21:20Ten years younger

Super Clinic supernannyThe end of the world into boys and girls

Super idol /Law of the

jungle

Good luck belongs to

you

How the Super

scholar Was Tempered

22:00Good luck Best choice BABY GO I love the peach garden

22:30Chinese farmers song

Super idol replay23:00

Beautiful reinforcem

ent

The masters of cooking

Distance-close

Distance-close

Mon Tue Wed Thu Fri Sat Sun

19:33 The first dolphin theatre (1)

20:30 The first dolphin theatre (2)

21:20Ten years younger

BABY GOMythBuster

s

The SurvivalDistance-

close

Super Speaker

To find you

22:00 Starlight dolphin theatre (1) Starlight dolphin theatre (1)

22:55

Starlight dolphin theatre (2)Starlight dolphin theatre

(2)23:05Starlight dolphin theatre

(1)

AHTV shifted focus from dramas and introduced 15 big ticket programs.

Original arrangement New arrangement

剧集时长 综艺时长 其他 剧集时长 综艺时长 其他 剧集时长 综艺时长 其他

Different type of programs of AHTV broadcast time percentage during 1930-2345

Before: the drama broadcast time percentage is about 70%

After: the variety broadcast time percentage is about 50%

Before “One Drama, Two Satellites” issued

After “One Drama, Two Satellites” issued

After revision

All TV stations and program owners can connect to Wechat system and activate audiences with shake function.

WECHAT OPEN SHAKE FUNCTION FOR TV

46

Improve TV Rating

Expand Content

Connect Commercial Value

180mil+ participants, 60+TV stations, 110+ programs, 100mil+ coverage excluding gala.

Source: Tencent, May 2015

3RD PARTY PROVIDERS HELP TO BUILD BETTER CONNECTION

47

TV LINK: TV CONTENT MOBILIZATION TV WATCH: LIVE TV INTERACTIVE

3rd party platform (e.g. TVM) also provide interactive service to connect mobile consumers with TV stations/programs through or throughout Wechat.

TV Studio

TVM system

Connect through mobile

Mobile Users

OTV

461MILLION USERS

69%* REACHAMONG ALL NETIZENS

8 DAYS PER MONTH

52 MINUTESPER USAGE DAY

PC MOBILE

63% REACH AMONG ALL NETIZENS

13 DAYS PER MONTH

43 MINUTESPER USAGE DAY

ONLINE VIDEO OVERVIEW

50

Source: Total netizen number from CNNIC, PC & Mobile reach number (based on CNNIC netizen), days and time spent from iUserTracker & mUserTracker Jun 2015;* PC reach has been adjusted to align with CNNIC penetration limit.

MEDIA SHARE OF TIME SPENT ON PC AND MOBILE

TIME SPENT BY VIDEO PLATFORM

51

PC

2%

+2%

-5%-2%

Source: iUserTracker & mUserTracker Jun 2014 & 2015, PC exclude software

+1%

4%

20%

19%

11%11%

8%

6%

4%

4%

3%2%

12%

iQiyi

Youku

LeTV

Sohu

PPTV

Tudou

iMangoTV

Tencent

Xunlei

CNTV

Others

PC viewership remained comparatively more stable than mobile, Youku’s leads however share slight decline with the growth of IQIYI.

Mobile Jun-2015Desk Jun-2015

30%

27%

16%

8%

6%

5%

5% 2%Youku

iQiyi

Tencent

PPS

Sohu

PPTV

Tudou

LeTV

Funshion

Others

-2%

+7%

MOBILE

Source: Claimed Publisher Data

VIDEO VIEWS BY DEVICE

52

Viewer prefer tablets and phone for online video especially when logged on to Tencent, Youku&Tudou video platforms.

20%30%

45% 46% 51% 54% 54% 55%67%

73% 55%

46% 48% 38%39% 36%

27%

26%

7%16%

9% 7% 12% 7% 10%18%

7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Tencent Youku&Tudou PPTV MangoTV iQiyi&PPS LeTV Sohu Video Baofeng Funshion

VIDEO VIEW % BY DEVICE

PC PHONE TABLET

ONLINE VIDEO ADVERTISING REVENUE

53

Source: iResearch Yearly Data Release 2014 – Online Video

0.2 0.5 3.27.3

13.5

21.9

31.8

6.59.3

12.0

15.6

18.8

20.8

22.3

3%

5%

21%

32%

42%

51%

59%

0%

10%

20%

30%

40%

50%

60%

70%

0

10

20

30

40

50

60

2012 2013 2014 2015e 2016e 2017e 2018e

2012-2017 ADVERTISING REVENUE FOR ONLINE VIDEO (MOBILE & PC)

Mobile Advertising Non-Mobile Advertising % of All OTV Advertising

RMB: Billion

Mobile video share of revenue grows massively from 21% to 32% in 2015.

YOUKU & TUDOU’S CHANGE OF STRATEGY FOCUS

PGC + UGC MORE THAN 10 MIL CHANNELS

MORE THAN 10 BIL INVESTMENT

“The end of pure video media,

evolution from a video platform,

to an entertainment eco-system”

Fan & Fun Integrated Content Marketing

IP focused

Innovative

Interactive

Integrated

I4 1. SHOW 2. FAN 3. CULTURE 4. JOURNEY

1. Eyeballs眼球经济

2. Fan Economy粉丝经济

3. Vertical Marketing 垂直人群

4. SocialHot Topics 社会话题

54

LETV: MULTIPLE SPORTS PPTV: LFP TENCENT: NBA IQIYI: CHINA OPEN

THE CONTENT COMPETITION EXPAND TO SPORTS PROGRAM

55

With the content competition turning red-hot, and release of sports strategy from government, video platforms are expanding their battlefield to sports area.

500 mil: exclusive online broadcast

right for NBA in next 5 years

250 mil EURO: exclusive online

broadcast right for LFP in next 5 years

Exclusive online broadcast right for China Open from Oct 2015-2018

Get broadcast right for 120+ sports

competitions in past 2 years.

FORMATS & CASES

PRODUCT PLACEMENT THROUGH

HOLOGRAPHIC PROJECTION

POST-PRODUCTION CONTENT PLACEMENT

57

PRODUCT PLACEMENT THROUGH

MAGIC POST

New technology allows brands to do product placement in online programs after production.

WATCH & BUY ON TV

58

VARIETY SHOW TO BUY DRAMA TO BUY ADS TO BUY

TV station and programs now are able to link all content to purchase.

3 spots of interactive ads open during “Dad, where are we going” S3: Wukonglicai, Ly.com and Inoherb.

59

Purchase function are placed on relevant video content, for higher noticeability and conversion.

ORIGINAL COOPERATION CELEBRITY COOPERATION CATEGORY PRODUCT CO-OP

Note: coming soon in iQiyi

WATCH & BUY IN OTV

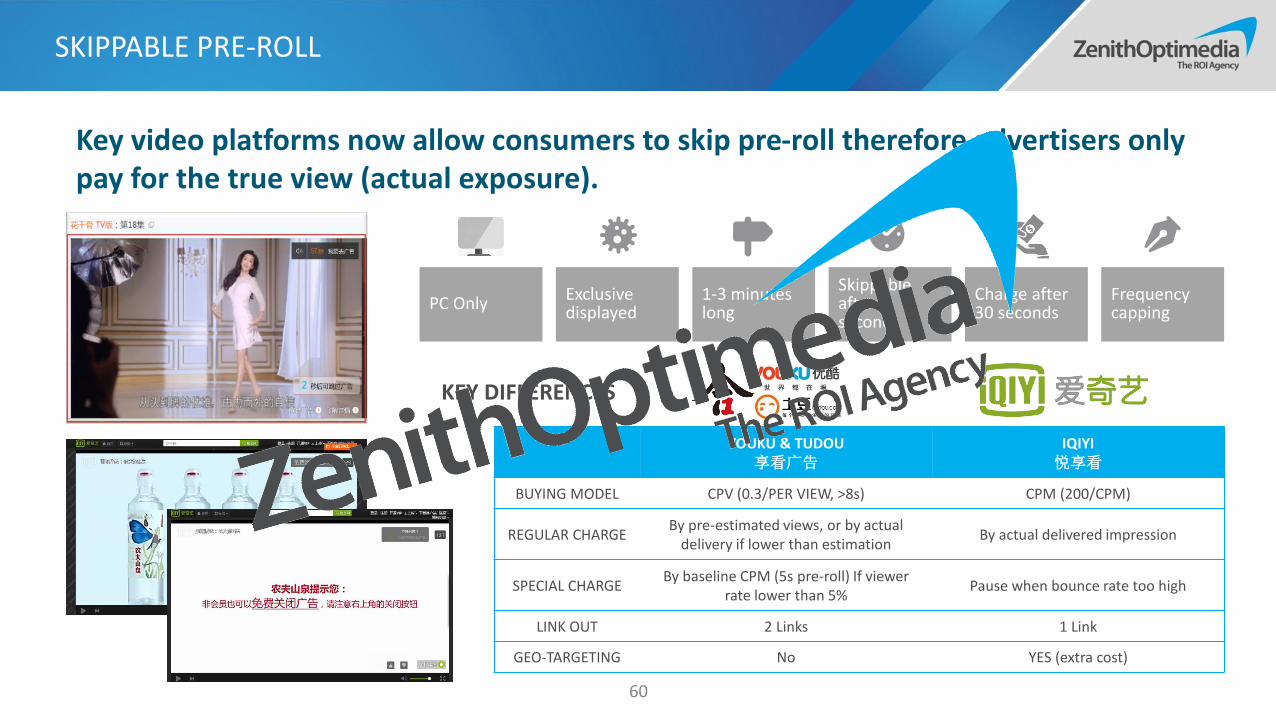

SKIPPABLE PRE-ROLL

60

Key video platforms now allow consumers to skip pre-roll therefore advertisers only pay for the true view (actual exposure).

YOUKU & TUDOU享看广告

IQIYI悦享看

BUYING MODEL CPV (0.3/PER VIEW, >8s) CPM (200/CPM)

REGULAR CHARGEBy pre-estimated views, or by actual

delivery if lower than estimationBy actual delivered impression

SPECIAL CHARGEBy baseline CPM (5s pre-roll) If viewer

rate lower than 5%Pause when bounce rate too high

LINK OUT 2 Links 1 Link

GEO-TARGETING No YES (extra cost)

Exclusive displayed

1-3 minutes long

Skippable after 5 seconds

Charge after 30 seconds

Frequency cappingPC Only

KEY DIFFERENCES

CASE: SMART CREATIVE PLAY

61

L'Oréal group make advertising on OTV more noticeable by combining “display” with video and adding strong call for action message.

DRAMA VARIETY SHOW

CASE: RIO’S OCCASION CONTENT PLACEMENT

62

From popular drama My Sunshine to hot variety show Running Man, RIO invests on a series of content placement as the look to build strong association with friends gathering.

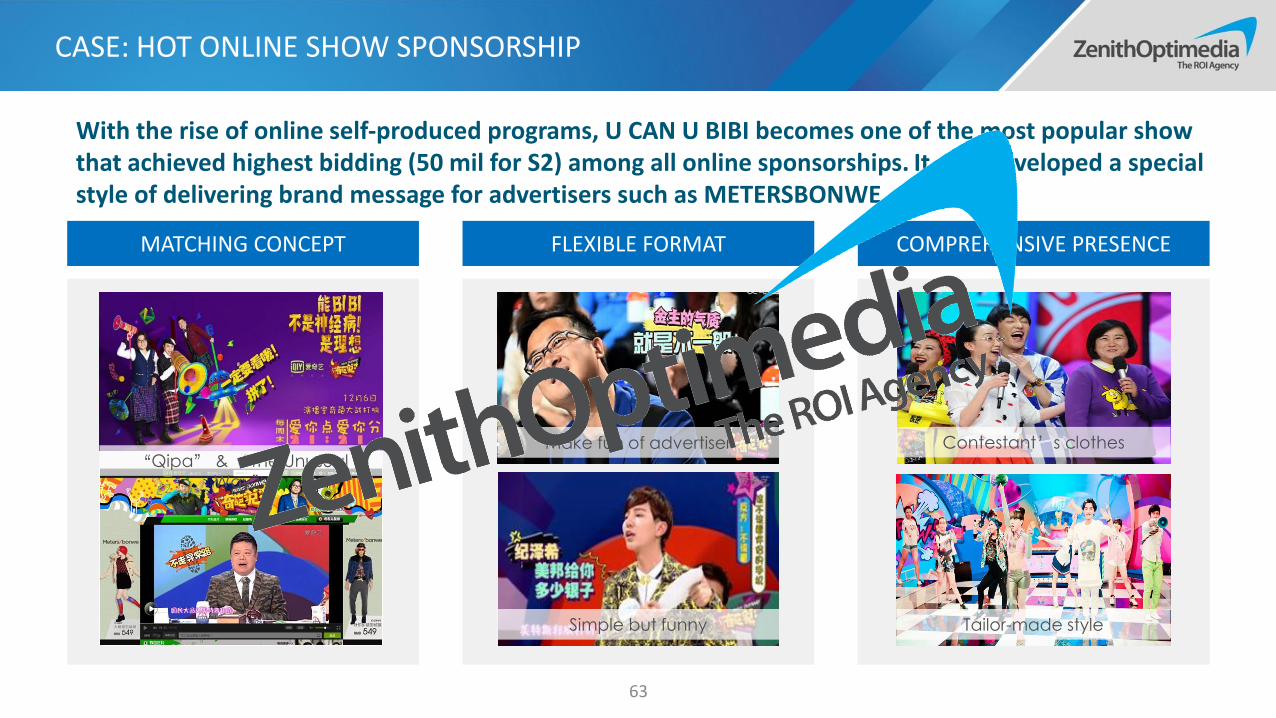

CASE: HOT ONLINE SHOW SPONSORSHIP

63

i

MATCHING CONCEPT FLEXIBLE FORMAT COMPREHENSIVE PRESENCE

Make fun of advertiser

Simple but funny Tailor-made style

Contestant’s clothes“Qipa” & “The Unusual

Way”

With the rise of online self-produced programs, U CAN U BIBI becomes one of the most popular show that achieved highest bidding (50 mil for S2) among all online sponsorships. It also developed a special style of delivering brand message for advertisers such as METERSBONWE.

CASE: MENGNIU FIRST AD FOR FIRST DAY

64

Teaser - Raise Curiosity5 Weibo posted by Deluxe during 5 days before new year to warm up for the new release, get 64k forwards, 12.7k comments

Warm up - Create Hot Topic Media and KOL joined the discussion, achieved 90 mil coverage, 61.6k forwards and 15.4k comments

Tipping Point - Interactive Live Topic + First Ad ReleaseHost invited audience to guess and count down for the new year, together with first 90s TVC release, which delivered the brand value of “better 2015” at the most relevant moment.

Mengniu associated with Hunan PSTV for their New Year celebration live broadcast. The brand welcomed the first day of 2015 with their new ad which gained massive attention. At the same time it created interactive on social supported by impact display cross big digital platforms

65

To build brand association with content look to go beyond single devise consider TV and OTV ( PC +Mobile). Try to leverage all elements of the content such as celebrity, fans, events etc.

1.

Consider post-production opportunities if budget doesn’t allow for in program integration, however all initiatives should always connect and drive to brand platforms.2.

Test True View pre-roll, compare visits and actual conversion per reach point for regular vs True View pre-roll.3.

Look to collaborate with online PGC & UGC program opportunities to increase interaction and deliver brand experience in a native environment.4.

VIEWPOINT ON VIDEO & OTV

SOCIAL

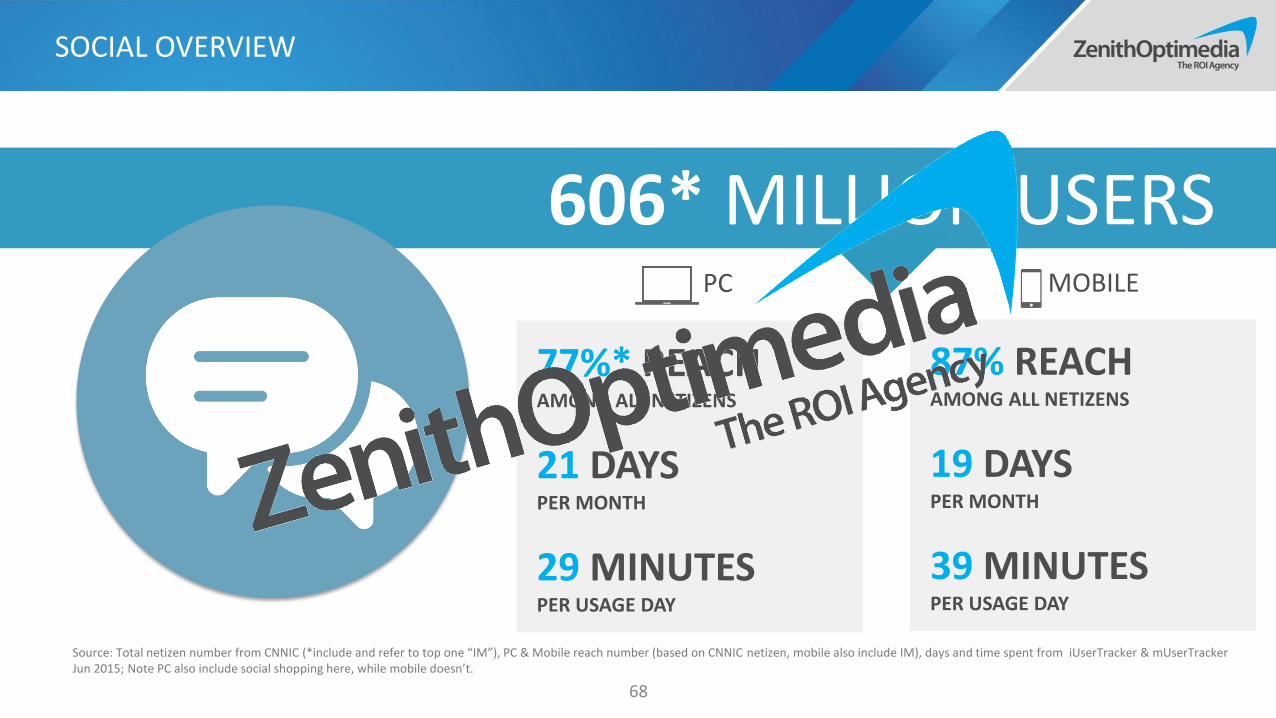

606* MILLION USERS

77%* REACHAMONG ALL NETIZENS

21 DAYS PER MONTH

29 MINUTESPER USAGE DAY

PC MOBILE

87% REACHAMONG ALL NETIZENS

19 DAYS PER MONTH

39 MINUTESPER USAGE DAY

SOCIAL OVERVIEW

68

Source: Total netizen number from CNNIC (*include and refer to top one “IM”), PC & Mobile reach number (based on CNNIC netizen, mobile also include IM), days and time spent from iUserTracker & mUserTrackerJun 2015; Note PC also include social shopping here, while mobile doesn’t.

71%

7%

5%

4%

6%QQ

Q-Zone

Sina Weibo

Aliwangwang

Baidu Tieba

Qtalk

Waiwai

Sina Blog

Others

44%

41%

6%2% 3%

Sina Weibo

Q-Zone

Momo

Baidu Tieba

Qiushibaike

QQ Light

Others

11%

-5%

-1%

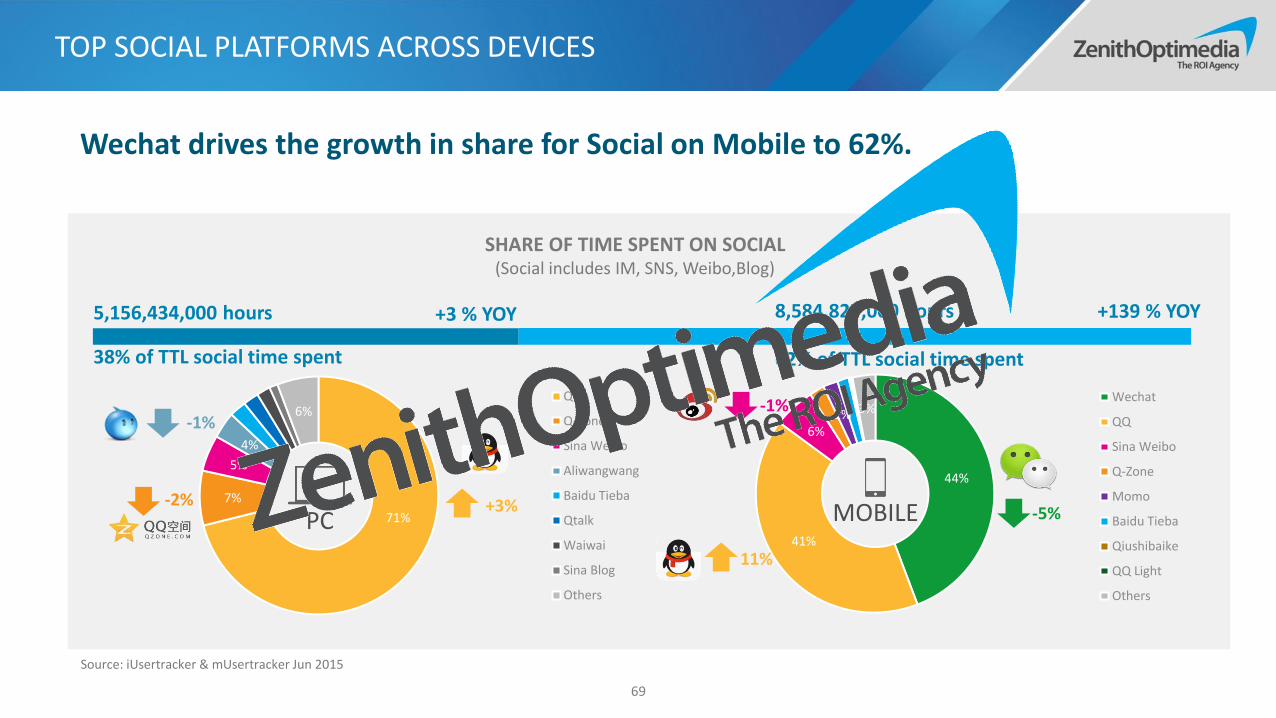

5,156,434,000 hours

38% of TTL social time spent

+3 % YOY 8,584,827,000 hours

62% of TTL social time spent

+139 % YOY

+3%-2%

-1%

TOP SOCIAL PLATFORMS ACROSS DEVICES

69

Source: iUsertracker & mUsertracker Jun 2015

SHARE OF TIME SPENT ON SOCIAL(Social includes IM, SNS, Weibo,Blog)

PC MOBILE

Wechat drives the growth in share for Social on Mobile to 62%.

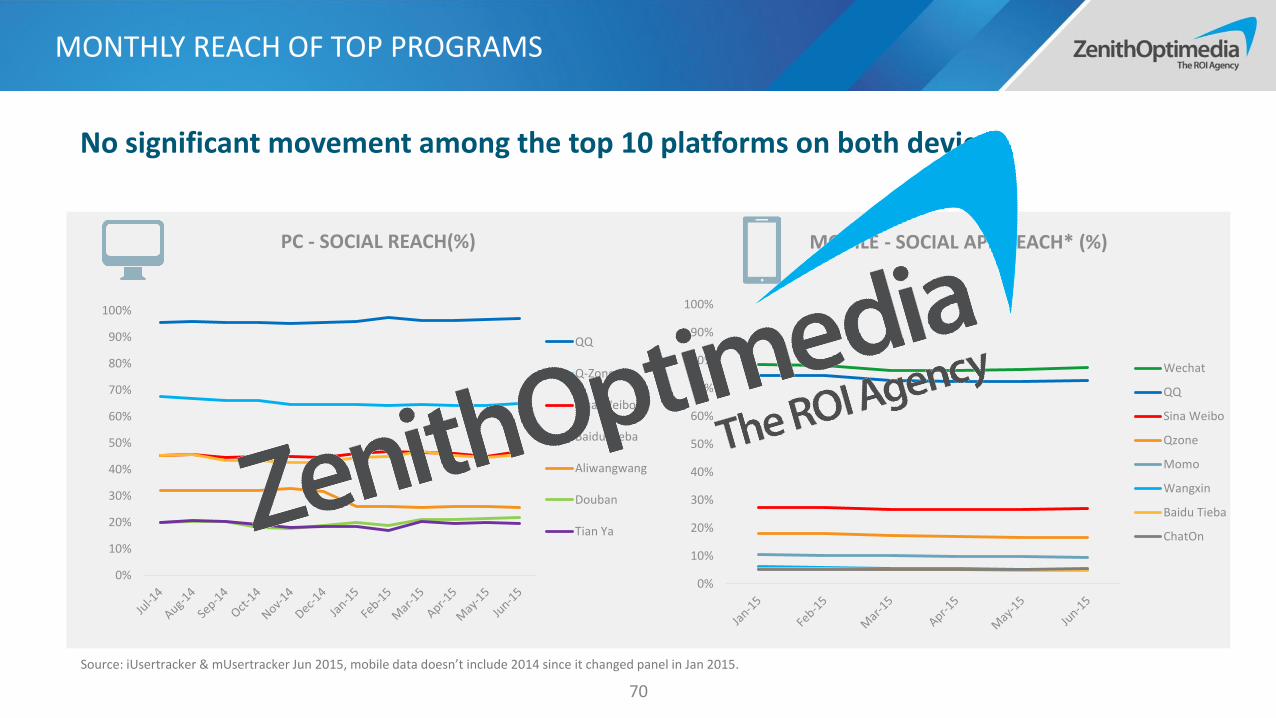

MONTHLY REACH OF TOP PROGRAMS

70

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

PC - SOCIAL REACH(%)

Q-Zone

Sina Weibo

Baidu Tieba

Aliwangwang

Douban

Tian Ya

Source: iUsertracker & mUsertracker Jun 2015, mobile data doesn’t include 2014 since it changed panel in Jan 2015.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MOBILE - SOCIAL APP REACH* (%)

Sina Weibo

Qzone

Momo

Wangxin

Baidu Tieba

ChatOn

No significant movement among the top 10 platforms on both devices.

VERTICAL SOCIAL APPS

71

Q&A SOCIAL PICTURE SOCIAL SPORTS SOCIAL MOM SOCIAL CAREER SOCIAL

Vertical platforms driven by diverse consumer needs and interests.

-

1,000

2,000

3,000

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Monthly Coverage (K'000)

3,000

3,500

4,000

4,500

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Monthly Coverage (K'000)

2,600 2,800 3,000 3,200 3,400

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Monthly Coverage (K'000)

- 500

1,000 1,500 2,000

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Monthly Coverage (K'000)

-

200

400

600

Monthly Coverage (K'000)

FORMATS & CASES

WECHAT OPEN MOMENT ADS SYSTEM TO ALL

73

1 2

3

4

5

AVATAR + NAME PROMOTION TAG

LINK TO DETAILS

PICTURES (9 MAX)

LIKE / COMMENT

EXPOSE TO HIGH ACTIVE USERS

EXPOSE TO MORE OF THEIR FRIENDS IF THEY INTERACTIVE WITH THE ADS

DATA ANALYSIS FROM WECHAT

ADS ENGINE FEEDS

4+

FOR ADS TO BE DELIVERED

POSITION

5th

AFTER THE 4+ FEEDS

TIME SPAN

6H

WITHOUT INTERACTIVE

RESERVED

7D

& ONE AD TO ONE PERSON IN 48H

VIEWABLE

100%

ADS SHOWN IN THE SCREEN

EXPOSURE

3WAYS

FEEDS, DETAILED PAGE, SHARE OUT

PROTECT

10MINS

CHARGE ONCE FOR FEED ADS*

PROTECT

4MAX

CHARGE TIMES WITHIN 7 DAYS

FORMAT MECHANICS EXPOSURE

COST

40 CPM WITHOUT GEO-TARGETING140 CPM FOR BJ&SH TARGETING90 CPM FOR OTHER KEY CITY TARGETING1.1X FOR GENDER TARGETING1.2X FOR LINK TO DETAILS

NATIVE WECHAT EXPERIENCE

74

The movie “Tiny Time” are promoted through series of fake Wechat dialogues posted by actors and actress. Users are also invited to check more details after sending out a default message.

L’Oreal Paris promote Cannes campaign by creating a fake moment page, in which celebrities are posting latest content in Cannes Film Festival, and consumers can also like or type in comment, exactly like how they do in the real moment.

《时代姐妹花,邀你来撕逼》The Invitation of Tiny Time

《戛纳明星朋友圈》The Moment of Celebrities in Cannes

Brand look to deliver stronger brand experience with native advertising on Wechat.

CASE: CHANDO DELIVERS DIFFERENT MESSAGES TO DIFFERENT GROUPS

75

Moments Ads Three different versions of landing pageVivian Xu’s “private”

moment page

To leverage the current hot topic ‘sleepless new moms’, Chando utilized its spokesperson Vivian Xu and launched a Wechat campaign to promote anti-aging product “Sleep” cream. Different from other H5 interactive, Chando gave out 3 different versions of communication and was able to become a part of the conversation.

Share to separate groups in real moment in Vivian’s tone

China World Trade Corporation - Milan Expo campaign

Wanda Half-year Celebration HONDA MODE Launch

QUICK FLASHING IN WECHAT MOMENTS

76

To achieve this effect, participants need to spontaneously change their avatar and post similar information required by organizer/brand in their personal moments.

Flash mob activity could be a way to activate fans and drive public attention in short time without paid ads, but it requires loyalty or attractive incentive.

77

Use Wechat Moment Ads to reach out to a large audience base. Include call to action mechanism which drives consumers to sign up for the brands’ Wechat accounts for always on interaction.

1.

Use Wechat to deliver richer brand experience while Weibo to create hot topics to keep brand fresh in the category. Brand needs to find the right balance depending on the objective.

2.

Use other social platforms to strengthen brand specific association and incremental reach. Also can be used to reach the core target.3.

VIEWPOINT ON SOCIAL

MAGAZINE AND NEWSPAPER

31%

68%63%

31%

16%

95%

30%

64%67%

46%

16%

96%

28%

59%

71%

58%

19%

95%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Magazine Reach NewspaperReach

Internet Reach Mobile InternetReach

Radio Reach TV Reach

2013-2015 REACH OF PRINT MEDIA

2013 2014 2015

PRINT MEDIA OVERVIEW

80

Source: CMMS Summer 2013-2015

14.6 minutes on magazine

35.4 minutes on newspaper

DAILY TIME SPENT ON PRINT

Print readership continues to decline as viewer shift online.

-10.9%

-17.9% -18.4%

-15.2%

-22.7%

-19.9%

-14.3%

-25.8%

-29.1%

-25.9%

-30.1%

-26.6%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

July2014

Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun

Ad Investment YOY Growth

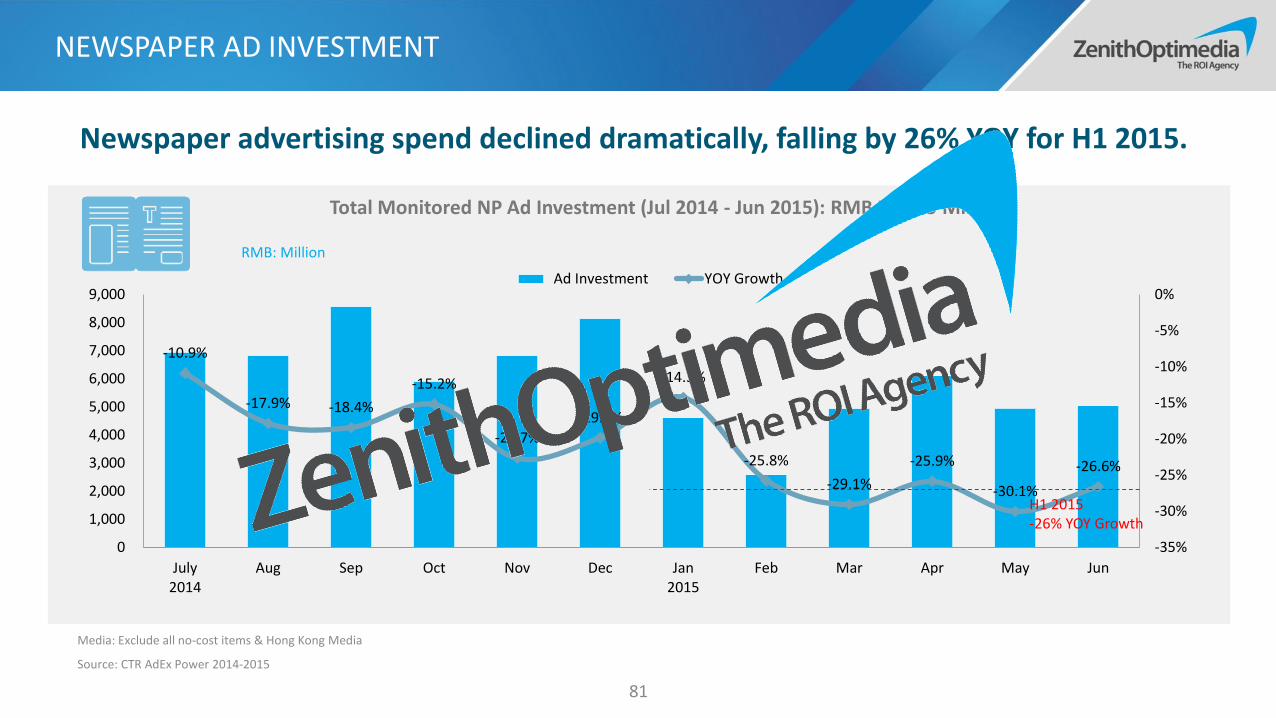

Total Monitored NP Ad Investment (Jul 2014 - Jun 2015): RMB 71,455 Million

RMB: Million

NEWSPAPER AD INVESTMENT

81

H1 2015-26% YOY Growth

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

Newspaper advertising spend declined dramatically, falling by 26% YOY for H1 2015.

NP Monitored Ad Investment By Sectors (Jan-Jun 2014 & 2015)

The Ad spend in Newspaper decreases among all categories.

NEWSPAPER AD INVESTMENT BY INDUSTRY

82

RMB: Million

-27%-44%

-17% -7%-28%

-45%

-2%-23% -28%

-40%-21% -29% -30%

-2%

-56% -47%

2%-15%

71%

148%

-56%

-100%

-50%

0%

50%

100%

150%

200%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000Jan-Jun 2014 Jan-Jun 2015 YOY Growth

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

MAGAZINE AD INVESTMENT

83

Total Monitored MG Ad Investment (Jul2014 - Jun2015): RMB 16,902 Million

-13.5%

-11.2%-9.6%

-11.1%

-13.4%-12.3%

-10.8%

-3.8%

-14.1%

-18.7%

-20.8%

-16.4%

-25%

-20%

-15%

-10%

-5%

0%

0

500

1,000

1,500

2,000

2,500

Jul2014

Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun

Ad Investment YOY GrowthRMB: Million

H1 2015-15% YOY Growth

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

Declining investment on magazine slipped for 15% YOY for the first half of 2015.

MAGAZINE AD INVESTMENT BY INDUSTRY

84

MG Monitored Ad Investment By Sectors (Jan-Jun 2014 & 2015)

-14% -8%-19%

-26%-15%

-25% -30%-17% -22%

2%

-32%-19% -18% -19%

-35% -36%

-5%

41%

94%80%

-62%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

0

500

1,000

1,500

2,000

2,500Jan-Jun 2014 Jan-Jun 2015 YOY Growth

RMB: Million

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

Ad spend on magazine drop in all the key categories.

FORMATS & CASES

CASE: VIVO CREATE HOT TOPIC WITH SPECIAL EXECUTION IN NEWSPAPER

86

D1: Scan QR code to Wechat page, with teaser message “See you at Wechat on May 14 th D2: Wechat ads on May 14th

As a teaser of new product launch, Vivo bought 4 full pages in People’s Daily with most of the space in blank except for eye-catching copy and QR code, which were also handed to attendees during the launch event hosted on the same day generating curiosity and talk ability.

87

When investing in magazine & newspaper, think in a long term view, be more focused in title selections to leverage key assets of major publication.1.

Use print to further widen reach however need to link or drive traffic to other media especially brand owned platforms. This will help maximize the impact of print.2.

VIEWPOINT ON PRINT

RADIO

90

Source: CMMS Summer 2013-2015

1 hour 5 minutes on radio

-3.5% YOY

Car Owners Non Car-Owners58 minutes on radio 1 hour 11 minutes on radio

DAILY TIME SPENT ON RADIO (YESTERDAY)

-1.7% YOY

16%

48%

13%16%

49%

10%

19%

53%

13%

0%

10%

20%

30%

40%

50%

60%

Total Population Car Owners Car Non-Owners

MONTHLY REACH OF RADIO 2013-2015 BY CAR OWNERSHIP

2013 2014 2015

-6.8% YOY

Total Population

RADIO OVERVIEW

Radio continues to increase reach among car owners, however time spent per person declines with increase in light listeners.

45%

8%

3% 3% 2% 2% 2% 1.3% 0.7% 0.6% 0.3%2%

7%

2% 2%1% 1% 1% 0.4% 0.3% 0.3% 0.4%

57.6

63.6

57.6 58.8

70.8

52.8

45.6

62.4

73.8

79.8 88.8

57.6

79.2

57.6 58.8

77.4

66

76.2

57

67.2

73.2

54.6

0

10

20

30

40

50

60

70

80

90

100

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Private Car Home Taxi Bus Company Public Area Park/Green Belt School Metro Cycling/Walking Company Car

LOCATION & TIME SPENT - CAR OWNERS VS. NON CAR OWNERS

Petration - Car Owners Petration - Non Car-owners Time Spent - Car Owners Time Spent - Non Car-owners

RADIO CONSUMPTION

91

MinutesPenetration

Car owners spend averagely more time in radio when travelling in other transportations, however non car-drivers spend more when staying at fixed places.

RADIO AD INVESTMENT

92

TOTAL MONITORED RD AD INVESTMENT (Jul 2014 - Jun 2015): RMB 36,356 MILLION

23.0% 23.1%

17.2%19.6%

28.3%

19.6%

-2.4%

17.2%

-3.6%

7.6% 6.7%

10.5%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jul2014

Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun

Ad Investment YOY GrowthRMB: Million

H1 20156% YOY Growth

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

Radio investments grow at a steady pace of 6%.

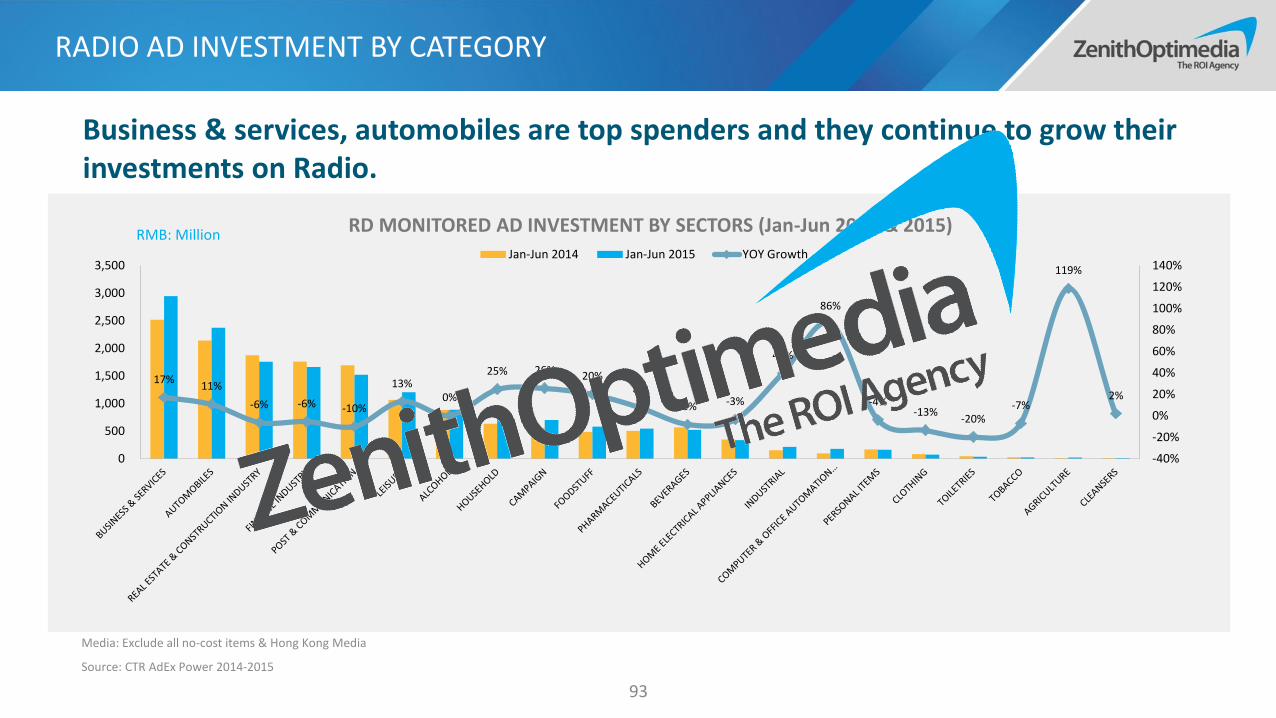

RD MONITORED AD INVESTMENT BY SECTORS (Jan-Jun 2014 & 2015)

17%11%

-6% -6% -10%

13%0%

25% 26% 20%8%

-8% -3%

40%

86%

-4%-13%

-20%-7%

119%

2%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

0

500

1,000

1,500

2,000

2,500

3,000

3,500Jan-Jun 2014 Jan-Jun 2015 YOY Growth

RMB: Million

RADIO AD INVESTMENT BY CATEGORY

93

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

Business & services, automobiles are top spenders and they continue to grow their investments on Radio.

FORMATS & CASES

CASE: LIVE BROADCASTING IN CADILLAC

95

• Monday - Tuesday: free oral broadcast + ads clip, as preview for Friday• Friday: freestyle oral broadcast, with car features introduced also through HIT

FM Weibo during 16:00 - 19:00

CADILLAC cooperated with HIT FM, and delivered special features of ATS-L through interactive broadcasting experience, with one DJ seat in the room and another in the moving car, a first for the radio station.

96

Radio works well to reach middle and upper classes, especially car owners however due to the high clutter need to create stand out communication.1.

Leverage RJs and in program integration to stand out and also drive local area activations at relatively lower costs.2.

VIEWPOINT ON RADIO

OOH

OOH AD INVESTMENT

98

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

TOTAL MONITORED OOH AD INVESTMENT (Jul 2014 - Jun 2015): RMB 40,640 MILLION

14.6%

11.2%

14.8% 14.5%

8.7% 7.7%

0.9%

5.7%4.0%

-3.7% -3.3%

-9.2%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2,800

2,900

3,000

3,100

3,200

3,300

3,400

3,500

3,600

Jul2014

Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun

Ad Investment YOY Growth

RMB: Million

OOH investments remain stable, with only 1% decline in H1 2015.

H1 2015-1% YOY Growth

OOH AD INVESTMENT BY INDUSTRY

99

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2014-2015

OOH Monitored Ad Investment By Sectors (Jan-Jun 2014 & 2015)

2.3% 4.5% 10.8% 15.3% 2.7% -0.2%21.5%

-5.2%13.9%

-39.3% -26.3%7.6%

-15.3%15.6%

-27.8% -19.3%-3.7% -5.7% -10.5%

200.1%

-32.1%-1.3%

-100%

-50%

0%

50%

100%

150%

200%

250%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jan-Jun 2014 Jan-Jun 2015 YOY GrowthRMB: Million

Beverages & Food reduce investment by 26% while Business & Services, Real Estate and Post & Communication continue to increase investments.

TOP 10 OOH ADVERTISER IN 2015 H1

100

Online brands join in the competition, with 4 out of 5 new entries coming from digital roots - 58.com, Tu’niu, Liepin and Tmall; Mengniu also show strong presence in H1 2015; KFC and Nongfu Spring still secure their top 2 position.

Source:CODC Jan-Jun 2015

482

505

598

604

614

619

621

634

794

1,176

- 200 400 600 800 1,000 1,200 1,400

Tmall

Liepin.com

Suning Appliance

Mengniu

Gold Jiangnan

Tuniu.com

Suning Commerce

58.com

Nongfu Spring

KFC

Growth(vs Jan-Jun,2014)

27%

-29%

109%

124%

70%

61%

146%

-4%

96%

21486%

RMB: Million

DIFFERENT MEDIA WITH DIFFERENT DEVELOPMENT

101

Screen, Metro and Airport show stable growth with development of tier 2&3 cities.

Source: CODC Jan-Jun 2014 & 2015Description: Metro, bus and taxi screens are included in screen media; Railway expand tracking coverage into more stations in 2015.

31,157

12,336

4,627 4,237 3,086 2,436

749 443

35,107

13,466

4,717 4,921 3,029 2,440

730 2,440

13% 9% 2% 16% -2% 0% -2%

451%*

-300%

-200%

-100%

0%

100%

200%

300%

400%

500%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Screen Metro Single Airport Bus Body Bus Shelter Network Railway*

OOH SPENDING BY FORMAT

2014 Jan-Jun 2015 Jan-Jun YTD Growth

RMB: Million

SCREEN AND METROS STILL THE KEY

102Sources:CODC Jan-Jun 2014 & 2015

Unit:RMB Million

Metro, 20%

Single, 7%

Airport, 7%

Bus Body, 5%

Bus Shelter, 4%

Network, 1% Railway Station, 4%

Building LCD, 34%

LED Screen, 10%

Metro TV, 3%Bus LCD, 3%Metro LCD, 1%Taxi Screen, 1%

Screen53%

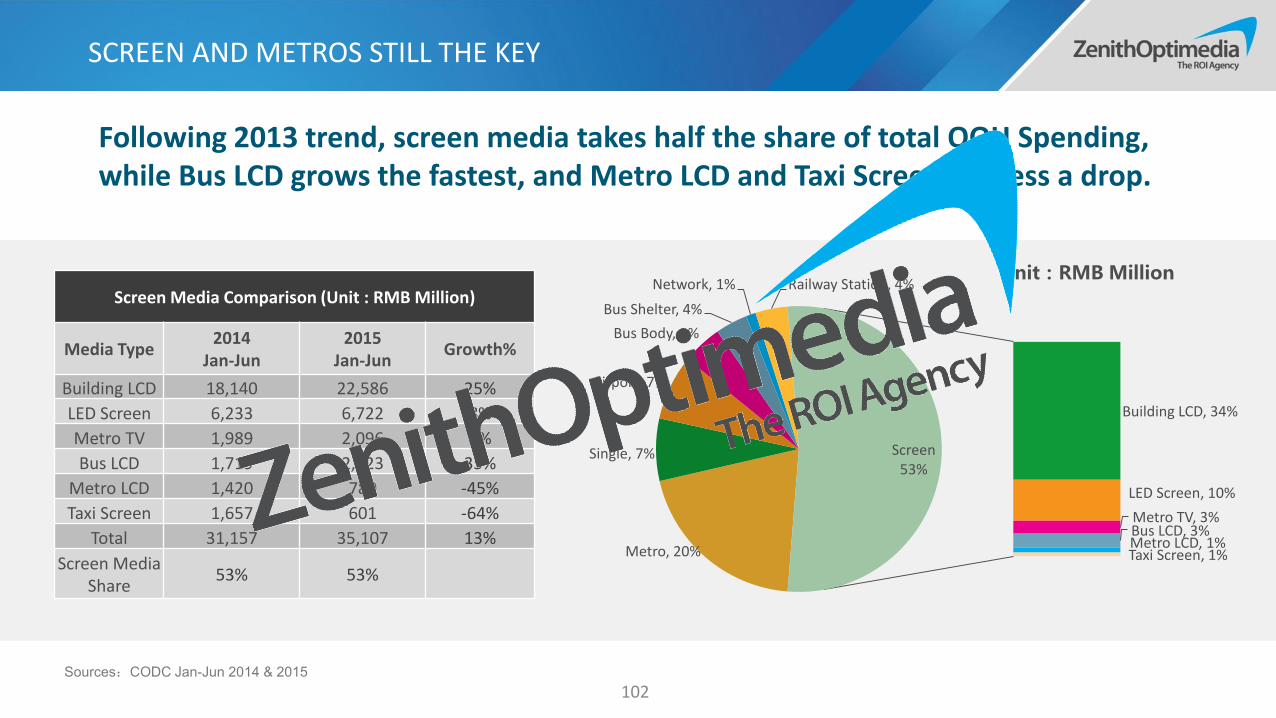

Screen Media Comparison (Unit : RMB Million)

Media Type2014

Jan-Jun2015

Jan-JunGrowth%

Building LCD 18,140 22,586 25%

LED Screen 6,233 6,722 8%

Metro TV 1,989 2,096 5%

Bus LCD 1,719 2,323 35%

Metro LCD 1,420 780 -45%

Taxi Screen 1,657 601 -64%

Total 31,157 35,107 13%

Screen Media Share

53% 53%

Following 2013 trend, screen media takes half the share of total OOH Spending, while Bus LCD grows the fastest, and Metro LCD and Taxi Screen witness a drop.

OOH TREND ACROSS TIERS

103

Source: CODC Jan-Jun 2015

Units:Million RMB

50%, Screen 24%, Metro

6%, Single

8%, Airport4%, Bus Body

3%, Bus Shelter

1%, Network

4%, Railway

Screen

Metro

Single

Airport

Bus Body

Bus Shelter

Network

Railway

54%, Screen

19%, Metro

7%, Single

7%, Airport5%, Bus Body

4%, Bus Shelter

3%, Railway

Screen

Metro

Single

Airport

Bus Body

Bus Shelter

Network

Railway

58%, Screen4%, Metro

13%, Single

5%, Airport

6%, Bus Body

8%, Bus Shelter

3%, Network

4%, Railway

Screen

Metro

Single

Airport

Bus Body

Bus Shelter

Network

Railway

SHARE OF OOH FORMAT INVESTMENT CROSS TIERS

Metro in T1&2 are slowing down while screen media, airport develop faster in Tier 3 due to improvement in infrastructure. Bus body and shelter still maintain their importance however decline in T1&2.

FORMATS & CASES

OOH GOING MORE “REAL”

105

REAL PRODUCT DISPLAY REAL 3D EFFECT AUGMENTED REALITY

More real products are displayed extra to the regular format or original placement

More vivid animation are created in LED screen

through upgraded tech

More engaged experience are activated through new

technology

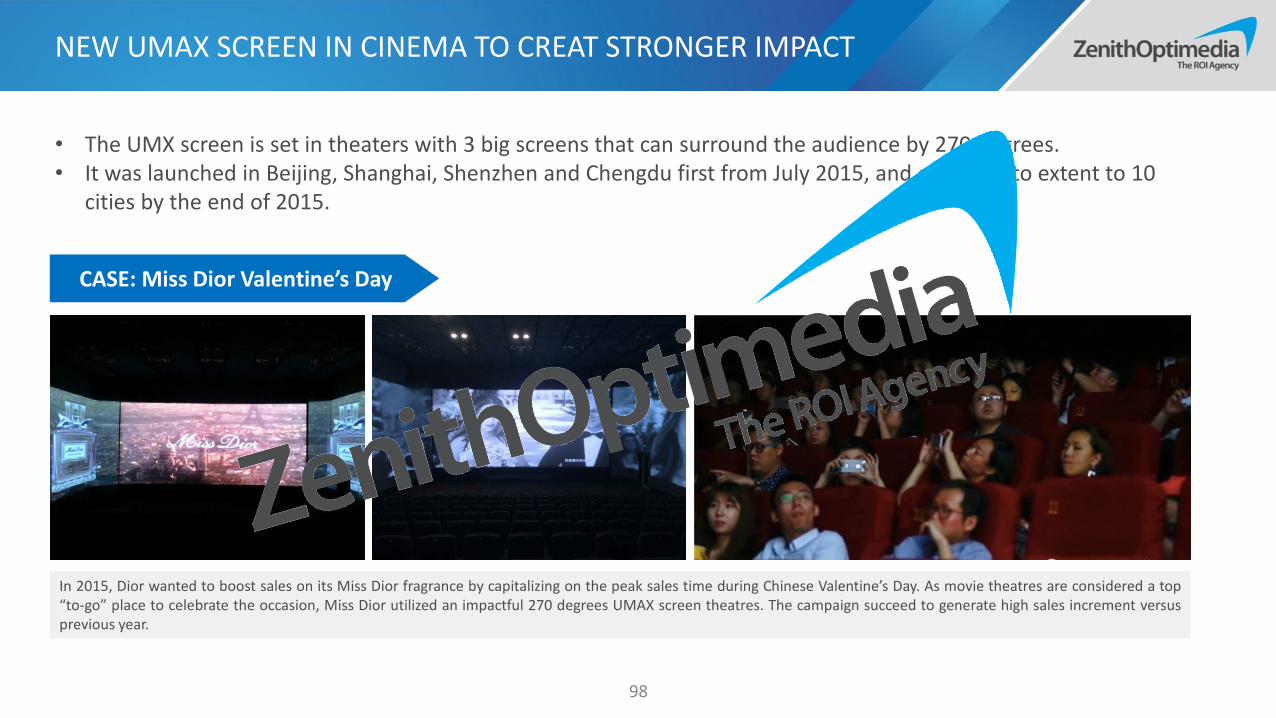

NEW UMAX SCREEN IN CINEMA TO CREAT STRONGER IMPACT

• The UMX screen is set in theaters with 3 big screens that can surround the audience by 270 degrees. • It was launched in Beijing, Shanghai, Shenzhen and Chengdu first from July 2015, and expected to extent to 10

cities by the end of 2015.

In 2015, Dior wanted to boost sales on its Miss Dior fragrance by capitalizing on the peak sales time during Chinese Valentine’s Day. As movie theatres are considered a top“to-go” place to celebrate the occasion, Miss Dior utilized an impactful 270 degrees UMAX screen theatres. The campaign succeed to generate high sales increment versusprevious year.

CASE: Miss Dior Valentine’s Day

98

PRECISE TARGETING THROUGH CHINA POST SCREENS

107

AUDIENCE RECOGNITON‘biometric feature signature’

Individuals Directional movement Number of glances Dwell time of each glance

IMON TargetEngage™ launched new OOH targeting format with real-time programmatic buy by upgrading traditional street kiosk space into mobile connected screens.

WIFI HOTSPOT

VARIOUS INTERACTIVE THROUGH IWON

108

Banners served after Wi-Fi connecting

Customized individual e-coupons

Brand/product placement in

interactive game

Brand Involvement

with educational cartoon

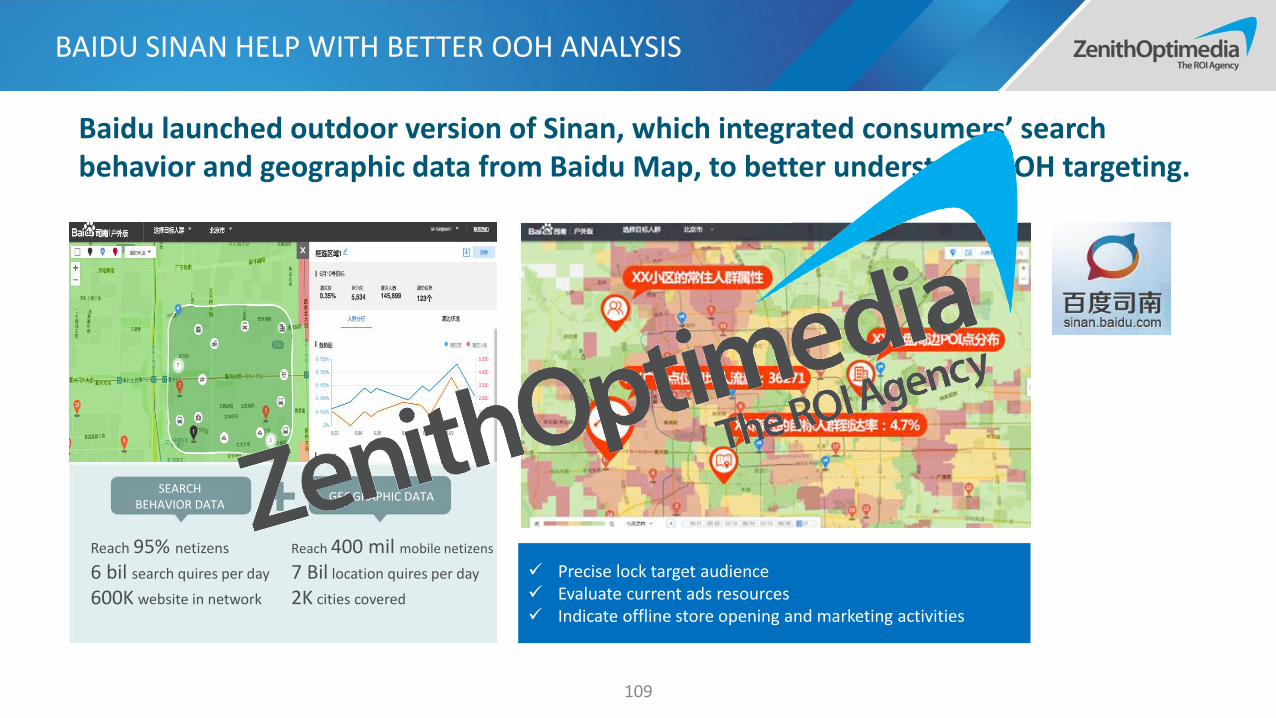

BAIDU SINAN HELP WITH BETTER OOH ANALYSIS

109

Baidu launched outdoor version of Sinan, which integrated consumers’ search behavior and geographic data from Baidu Map, to better understand OOH targeting.

Precise lock target audience Evaluate current ads resources Indicate offline store opening and marketing activities

SEARCH BEHAVIOR DATA

GEOGRAPHIC DATA

Reach 95% netizens

6 bil search quires per day

600K website in network

Reach 400 mil mobile netizens

7 Bil location quires per day

2K cities covered

110

With the improvement in OOH and Mobile technology, OOH can enable integration of offline and online activities to deliver stronger brand experience. Mechanics need to be simple and user friendly.

1.

Combination of AOD technology with OOH can help turn OOH into a more targeted medium.2.

Using new data system to improve pre-campaign evaluation and post-campaign measurement to evaluate the true value of the investment.3.

VIEWPOINT ON OOH

E-COMMERCE

374 MILLION USERS

56%* REACH AMONG ALL NETIZENS

7 DAYS PER MONTH

15 MINUTESPER USAGE DAY

PC MOBILE

46% REACH AMONG ALL NETIZENS

9 DAYS PER MONTH

11 MINUTESPER USAGE DAY

E-COMMERCE OVERVIEW

112

Source: Total netizen number from CNNIC, PC & Mobile reach number (based on CNNIC netizen), days and time spent from iUserTracker & mUserTracker Jun 2015;* PC reach has been adjusted to align with CNNIC penetration limit,, both PC and mobile here don’t include social shopping.

56%

19%

11%

2%Taobao

Tmall

JD.com

VIP.com

Suning

Meituan (GB)

Dangdang

Yhd.com

Amazon

Others

-1%

+3%

Source: iUserTracker & mUserTracker Jun 2014-2015

64%7%

6%

4%

3%

2%2%

Taobao

Meituan (GB)

Jindong

Tmall

VIP

Mogujie

Meilishuo

Jumei

Juhuasuan (GB)

Nuomi (GB)

Others

PC MOBILE

-3%

TOP EC PLATFORMS ACROSS DEVICES

113

SHARE OF TIME SPENT ON EC

+3%

-2%

+9%

Alibaba drives growth with increased share on mobile.

* Dianping ranks after JD if added.

B2C vs. C2C

114

Source: iResearch Yearly Data Release 2014 – E-commerce

B2C is expected to take more than half share of all transactions, dominated by TMALL and JD.

25.3%34.6%

40.4% 45.3%51.0% 56.0% 60.6% 63.5%

74.7%65.4%

59.6% 54.7%49.0% 44.0% 39.4% 36.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015e 2016e 2017e 2018e

ONLINE SHOPPING MARKET - B2C VS. C2C BY TOTAL TRANSACTIONS

B2C C2C

60.4%19.5%

3.0%

2.9%1.7%

1.5%1.4%

1.3% 1.1%

MARKET SHARE OF TOP B2C PALYERS BY TOTAL TRANSACTIONS (2014)

TMALL

JD.com

VIP.com

Suning.com

Gome.com.cn

yhd.com

Dangdang

Amazon.cn

Yixun.com

Jumei.com

Other

SHOWROOMING AMONG SEARCH SAVVY MOBILE USERS

While in brick and mortar stores many actually search on their mobile devices and make online purchase.

Source: McKinsey iConsumer China 2015

74% of shoppers who use mobile search are showrooming – checking out products in store but

buying online or from other competitor’s retail channels

115

E-COMMERCE CATEGORIES

Most frequent online purchases are packaged and fresh food – though the most popular category overall is still apparel at 66% penetration and 2,700RMB spent per year.

Source: McKinsey iConsumer China 2015

Consumer usage of online food shopping is very high in China at 40+% versus under 10% in the US.

Buying food online is becoming more feasible due to quicker delivery time, with roughly 40% using same or next day delivery.

116

M-COMMERCE

117

98.5% 94.2%85.5%

66.3%

49.4%38.9%

32.4% 28.8%

1.5% 5.8%14.5%

33.7%

50.6%61.1%

67.6% 71.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015e 2016e 2017e 2018e

SHOPPING TRANSACTIONS - MOBILE VS. PC

PC Mobile

Source: iResearch Yearly Data Release Jun 2015 – E-commerce

Mobile will account for more than half of all transactions, growing speed slows down but still higher than 100%.

69%45% 45%

14% 7% 5% 4%4%

426%

490%

298%

243%

115%

61%38% 23%

0%

100%

200%

300%

400%

500%

600%

0

10,000

20,000

30,000

40,000

50,000

60,000

2011 2012 2013 2014 2015e 2016e 2017e 2018e

SHOPPING TRANSACTION – MOBILE vs PC

PC Mobile PC growth Mobile growth

THE RISING OF OVERSEA PURCHASE

Both external & internal platforms put efforts to make oversea purchase easier, while verticals see a boom quickly, especially in beauty and infant milk category.

淘世界

118

MORE FUSION FOR ONLINE AND OFFLINE

Both traditional and digital giants are building their O2O ecosystem with a focus on data integration and varied services .

ALIBABA EXPAND TO OFFLINE WANDA EXPAND TO ONLINE DASHANG EXPAND TO ONLINE

Wanda announced the cooperation with Tencentand Baidu for e-commerce business in 2014, and officially launched its first physical platform Feifanby end of July, 2015.

Dashang Group, one of the biggest retailers in China, launched its own e-commerce platform Tiangou in Nov 2014.

Alibaba invested in Intime in March 2014, and further became its No.1 shareholder in July 2015, meanwhile launched APP “Miaojie” to serve for offline shopping.

119

GROUP-BUY UPGRADE USER FLOW WITH MOBILE PAYMENT

120

Group-buy service are upgraded, from “pay and consume” to “consume and pay”, with simplified flow facilitated by mobile and flexible discount operation.

“SHANHUI”/”FLASH DISCOUNT” FROM DIANPING“DISCOUNT PAYMENT”

FROM MEITUANDIANPING IS THE PLATFORM TO INITIATE THIS SERVICE,

FOLLOWED BY MEITUAN

FORMATS & CASES

USER GENERATED CONTENT BRIDGE FOR SALES

122

Taobao opened its mobile platform to public to encourage high quality user generated content while also sharing revenue with generators.

One of the most valuable writers earned 136K within 7 days by producing hundreds of qualified content.

123

E-commerce is no longer just about purchase it is a medium which can drive also awareness and consideration. Communication needs to be developed accordingly.1.

New brands entering China can test the market with E-commerce while for existing brands can use E-commerce to locate threats from new and up coming brands. 2.

Brands need to converge all resources such as KOL’s, branded and associated content, reviews etc. to drive greater conversion on purchase.3.

VIEWPOINT ON E-COMMERCE

SEARCH

536 MILLION USERS

76% REACH AMONG ALL NETIZENS

12 DAYS PER MONTH

9 MINUTESPER USAGE DAY

PC MOBILE

68%* REACH AMONG ALL NETIZENS

10 DAYSPER MONTH

13* MINUTESPER USAGE DAY

Source: Total netizen number from CNNIC, PC & Mobile reach number (based on CNNIC netizen), days and time spent from & mUserTracker Jun 2015;* Mobile reach refer to CNNIC mobile phone usage number as minimum, time spent refer to APP usage (while days refer to website usage).

SEARCH OVERVIEW

126

SEARCH RANKING BY PAGE VIEWS

127

Change in Reach

-1%

+4%

+2%

Change in Reach

+9%

-19%

Source: iUsertracker & mUsertracker Jun 2014-2015, use site data for mobile, but Shenma is not well tracked according to the market share published by CNZZ, Mar 2015Note: PVs are within iResearch panel geography, scale may not be representative of the total online population

-

50,000

100,000

150,000

200,000

250,000

Jul-

14

Au

g-14

Sep

-14

Oct

-14

No

v-14

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

PV OF SEARCH ENGINE ON PC (Mil)

Baidu Haosou Sogou Etao

Google Soku Bing

-

10,000

20,000

30,000

40,000

50,000

60,000

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15

PV OF SEARCH ENGINE ON MOBILE (Mil)

Baidu Easou Sogou Etao Bing

+9%

Baidu, 80%

Shenma*, 13%

Sogou, 6%

MARKET SHARE OF MOBILE SEARCH

Usage of 360 search continues to grow, though still dwarfed by Baidu’s dominant share of search. Sogou surpassed Easou in mobile, also Shenma gains share rapidly with the support of UC browser.

PC & MOBILE DIFFERENCES CROSS TIME

128

0 1 2 3 4 5 6 7 8 9 1 0 1 1 1 2 1 3 1 4 1 5 1 6 1 7 1 8 1 9 2 0 2 1 2 2 2 3

Monday

Tuesday

Wednesday

ThursdayFriday

Saturday

Sunday

PC MOBILE

Source: Baidu Tanxing Jul 2015

PC dominates working time (day and week days) while mobile spikes up during me time (night and weekends).

PC VS. MOBILE SEARCH CROSS THE DAY

PC MOBILE

PC VS. MOBILE SEARCH CROSS THE WEEK

THE RISING OF VOICE & PICTURE SEARCH

129

Voice and picture search is predicted to grow by 50%.

Source: Baidu Mobile Website Trend Report, Jan 2015

VOICE & PICTURE SEARCH INDEX

GENERAL SEARCH INDEX

J a n F e b M a r A p r M a y J u n J u l A u g S e p O c t N o v D e c

VOICE SEARCH VOICE INPUT VOICE TRANSFORMING VOICE HELPER

FORMATS & CASES

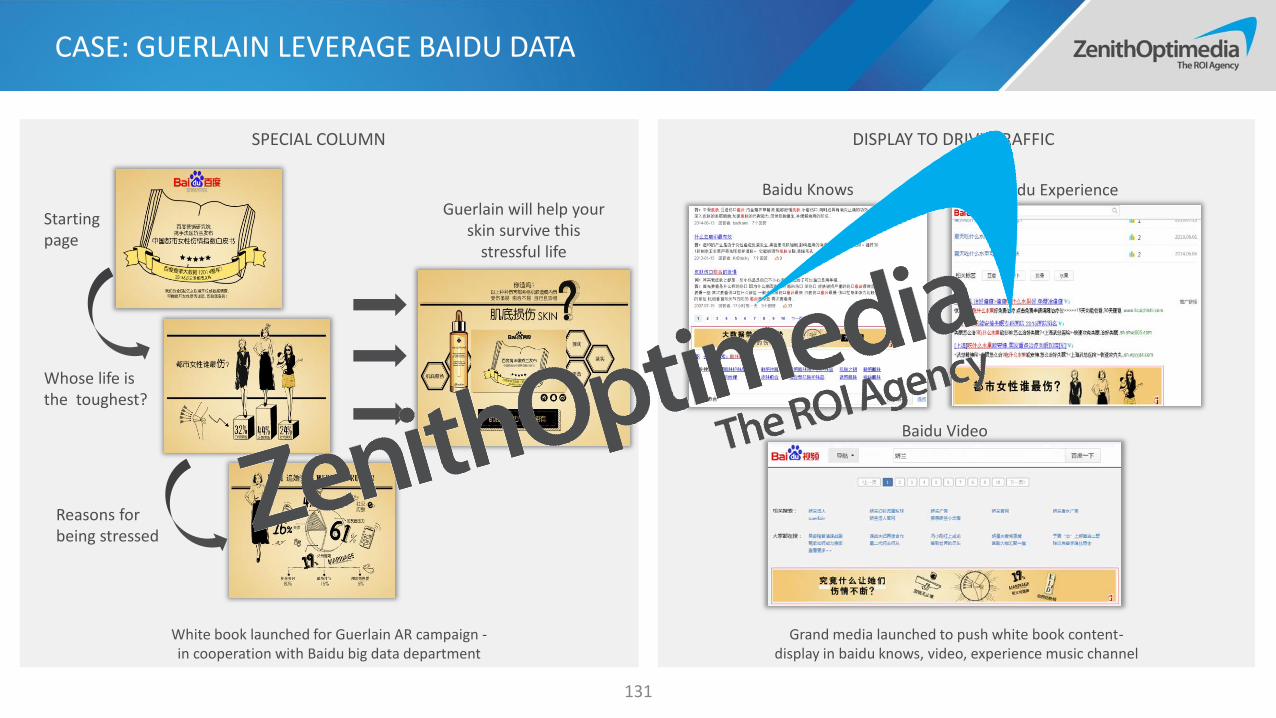

White book launched for Guerlain AR campaign -in cooperation with Baidu big data department

Grand media launched to push white book content-display in baidu knows, video, experience music channel

CASE: GUERLAIN LEVERAGE BAIDU DATA

131

Starting page

Whose life is the toughest?

Reasons for being stressed

Guerlain will help your skin survive this

stressful life

Baidu Knows Baidu Experience

Baidu Video

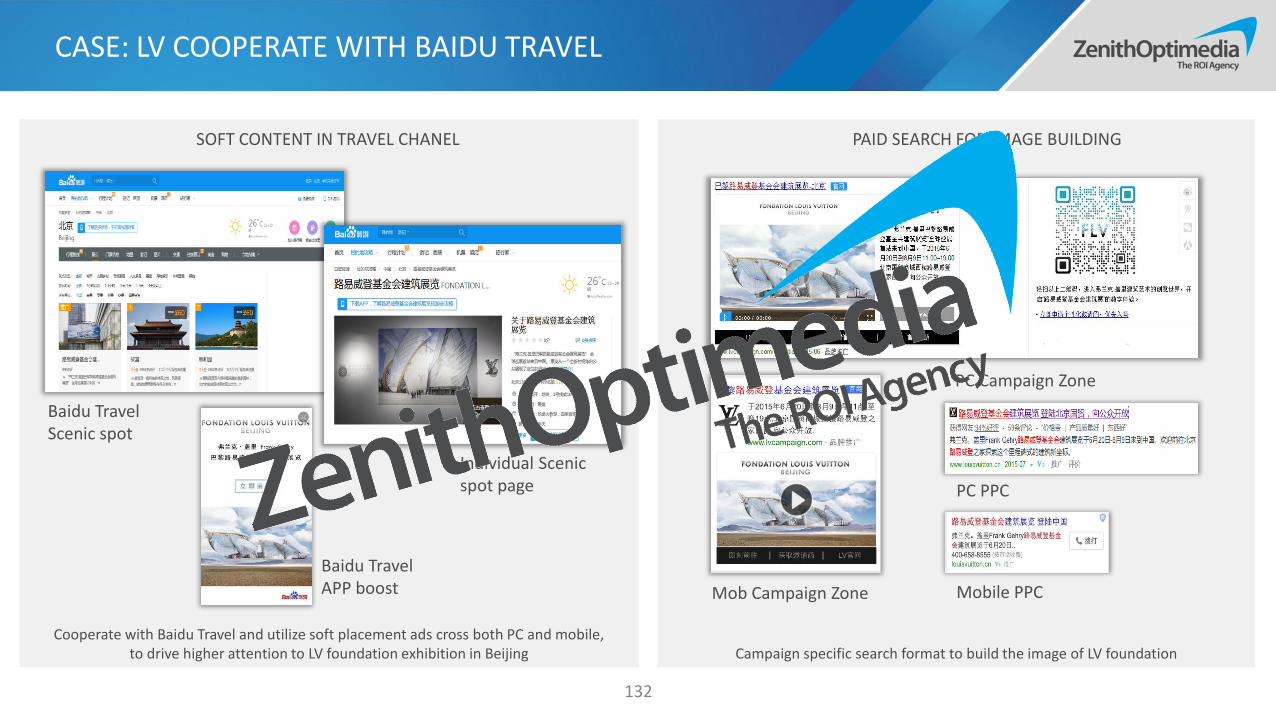

SPECIAL COLUMN DISPLAY TO DRIVE TRAFFIC

Cooperate with Baidu Travel and utilize soft placement ads cross both PC and mobile, to drive higher attention to LV foundation exhibition in Beijing Campaign specific search format to build the image of LV foundation

SOFT CONTENT IN TRAVEL CHANEL PAID SEARCH FOR IMAGE BUILDING

CASE: LV COOPERATE WITH BAIDU TRAVEL

132

PC Campaign Zone

Mob Campaign Zone

PC PPC

Baidu Travel APP boost

Baidu Travel Scenic spot

Individual Scenic spot page

Mobile PPC

Keep a close watch of 2nd, 3rd players in both PC and mobile beyond Baidu (e.g. 360, Shenma), as they also have strong background, and are trying hard to grab share.1.

Optimize delivery across time bands and devices when doing search campaigns.2.

Pay attention to the rise of picture and voice search, start to integrate this new tech in campaign where necessary. 3.

When investing in search platforms, especially Baidu, look to leverage key assets of the ecosystem beyond paid search.4.

133

VIEWPOINT ON SEARCH

PROGRAMMATIC BUYING

PROGRAMMATIC INVESTMENT USA VS. CHINA

136

4%9%

15%

21%

0%

10%

20%

30%

40%

50%

60%

70%

0

5

10

15

20

25

2013 2014e 2015e 2016e

INVESTMENT OF PROGRAMMATIC DISPLAY IN CHINA

Programmatic digital display ad spending

Programmatic mobile ad spending

% of total digital display ad spending

24%

45%

55%

63%

0%

10%

20%

30%

40%

50%

60%

70%

0

5

10

15

20

25

2013 2014e 2015e 2016e

INVESTMENT OF PROGRAMMATIC DISPLAY IN USA

Programmatic digital display ad spending

% of total digital display ad spending

BILLION (USD) BILLION (RMB)

China witnesses a rapid growth in programmatic investments however way behind USA.

Source: USA data from eMarketer Oct 2014, China data from iResearch programmatic report 2014

DATA TECHNOLOGY EMPOWERING PROGRAMMATIC EFFICIENCY

137

1st party data

1st Party DataVisitors’ cookiesMobile Phone No.QQ numberPayment CardContacts…

3rd Party Data Provider• Online Behavior

• Purchasing Behavior

programmed buy Inventory Bidding Performance Optimization…

3rd party data

2nd party data

2nd Party DataAd PlacementIPISPURL

…

• Cookies Cleaning• Audience Verification• Data Segments• Data Safety• …

Audience Insight

Inventory Estimation

• Comprehensive data processing for client’s first party data to command programmatic targeting

• Integrate offline database, CRM for data cleansing, mining, analytics and look-alike modeling

• Consumer insight research to facilitate decision making of planning and strategy

EXTENDED TARGETING BEYOND AUDIENCE SEGMENT

138

• Targeting based on public interests, completed integration with Baidu Search Index & Taobao Purchasing Index

• Targeting based on environmental factors, weather, temperature, air quality, and other event based signals

• Extension of TV ad to cover incremental reach on PC and mobile, full media channel coverage for audience interaction with brand

Search Index

Purchase Index

Sync with Localized Online IndexTrigger Ads Based on Real-time Data Across Platforms

WeatherIndex

SportsIndex

PurchasingIndex

SearchIndex More..

TV

Trigger Ads on 2nd And 3rd Screens Based on TV Ads

SOCIALLY INTELLIGENT MEDIA VIA PROGRAMMATIC

139

• Integrated with leading social platforms, taking advantage of effective and timely reach audience

• Harness valuable social data, listen and respond to social trend promptly depending on different attitude

• Tailor campaign objectives flexibly according to negative, neutral or positive attitude

Listen What Your Customers Are SayingInfluence TA with 1:1 Creative Based on Individuals’ Attitude

Listen Analysis Response

Listen social feedbacks on brands by contextual targeting in UGC on mainstream social media via API

Analysis whether audiences’ attitude based on AOD are negative/neutral/positive about the brand according to UGC, Key Word and Tags.

Response promptly by displaying the 1:1 dynamic creative ads on vertical media platform accordingly in real time

Negative

Branding Ads

From 0 to 1

AOD social serves as instant online

crisis PR specialist, bridges consumers

with brand in a positive way

Build consumers’ confidence to brand

and brand recognition

Positive/Neutral

Promotion Ads

1+1>2

AOD social is complementary to

traditional advertising and offline PR

Enhance brand preference and brand

loyalty

BE WHERE YOUR USERS ARE

140

• Focus on mobile data analytics of location and purchasing transactions, target audience from different view

• Consolidated footprint and location technologies, reverse predict audience offline behavior

• Integrated offline transaction platform, closing the loop of offline sales attribution to online promotion

Offline

Capture

Online

Profiling

Offline

Transaction

Online

Tracking

Consumers’

Purchasing Behavior

Data in Circle

Capture consumers’ purchasing behavior from their offline purchase history data

Launch Ad campaigns for selected TA on multiple online platforms

Profiling data is done by matching raw data with AOD demo database to lock in TAs

Drive TAs to purchase at offline stores and feedback the purchasing data to AOD at the same time

Feedback the tracking data to database and refine the profiling process

21

3

4

HOLISTIC INVENTORY SOLUTION FOR PROGRAMMATIC BUYING

141

• Precise cross media frequency control by audience maximizing media ROI

• Established returnable video inventory management platform with major video publishers, control inventory distribution by audience

• VivaKi verified media to ensure brand quality and premium inventory supply

Available PMP Models: Preferred Deals & Programmatic Direct Buy

Frequency Capping on Premium Inventory

Returnable Premium Audience Buying

Preferred Deals Program

matic Direct Buy(PDB)

Bid

din

gFixed

price

Reserved Banner Reserved OTV

Quality Low High

Private Auction

Open Bidding(RTB)

Low Frequency

Reach 1+ 2+

High Frequency

Reach 5+ 6+

Brands

PMP

SelectionReturn

FORMATS & CASES

TRAVEL

BEAUTY

BEAUTY CAMERA

LIFE

LAUNCH CAMPAIGN AT RIGHT TIME AND RIGHT MESSAGE IN RIGHT PLACE

143

Ads triggered only when

temperature > 25°C

Deliver relevant message in relevant environment with different mindset

Campaign Goal

Educate consumers for hair removalEnhance brand preference with limited budget

Where & Who

Target young female in selected key cities through mobile programmatic buy

Result

200% higher CTR and time spent than expected70% search query increase in mobile

Unaided awareness raise 25%

25°C

UPLIFT BRAND THROUGH SOCIAL PROGRAMMATIC BUYING

144

Campaign goal

Brand Awareness

Solution

AOD Social Solution

Est. Result

Buzz increase 20%+

Brand reputation uplift 4%+

When audiences’ attitude is….

Positive/Neutral Negative

Promotional Ads

Affiliate Ads

Emotional Leading

Branding Ads

Reduce Concerns

IMPROVE TA% INTELLIGENTLY WITH PMP

145

Campaign goal

Frequency Capping

Improve the ratio of TA

(4 times reach)

Launch Model

PDB (Private Direct Buy)

Result

4 times UV is 23.4%

Only 2% reach over frequented

146

Continue increasing investment in programmatic buys for greater efficiency and precision targeting.1.

Leverage the power of data from both partnership, and real time connection or tracking, to generate stronger consumer understanding and insights.2.

Upgrade from standard version to customized version which is built to target the potential consumers of the specific brand with the right communication.3.

Optimize current investment through PMP, to control frequency cross platforms, as well as secure premium inventories among qualified target audience. 4.

VIEWPOINT ON PROGRAMMATIC BUYING

MYKIM CHIKLI CEO ZENITHOPTIMEDIA GROUP CHINASHANN BIGLIONE HEAD OF STRATEGY ZENITHOPTIMEDIA GROUP CHINASAMEER SINGH HEAD OF CHANNEL PLANNING ZENITHOPTIMEDIA GROUP CHINAOLIVIA ZHANG ASSOCIATE DIRECTOR STRATEGY ZENITHOPTIMEDIA GROUP CHINAMOLLIE CHEN SUPERVISOR STRATEGY ZENITHOPTIMEDIA GROUP CHINAVIVI WAN DESIGNER BUSINESS DEVELOPMENT ZENITHOPTIMEDIA GROUP CHINA

Related Documents