College Federal Reserve Challenge November 16, 2015 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

College Federal Reserve Challenge

November 16, 2015

1

Jeffrey Lacker and His Advisors

Jeffrey Lacker:

President and CEO

of Richmond Fed

Kartik Athreya:Sr. VP

John A Weinberg:

Sr. VP

Andreas Hornstein: Sr. Advisor

Robert L. Hetzel:

Sr. Economist

2

Goals For Today’s Meeting

1. Assess Progress in Reaching Dual Mandate

2. Analyze Global Economic Conditions

3. Align Monetary Policy Proposal for December

FOMC Meeting with Economic Progress

3

Unemployment Rate

U-3 declined to 5% in October, down from its 10% peak and the U-6 fell to 9.8%, now

within the range of where the Fed previously tightened4

Source: Federal Reserve Economic Data St. Louis Fed

Labor Force Participation Rate

The Labor Force Participation Rate currently stands at 62.4%5

Source: Federal Reserve Economic Data St. Louis Fed

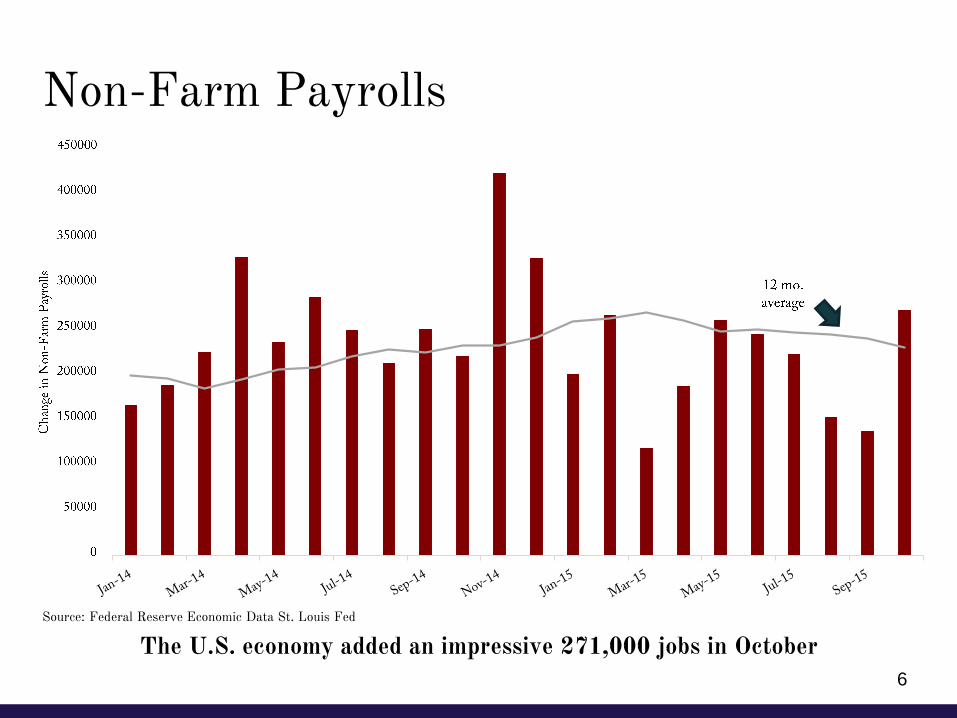

Non-Farm Payrolls

The U.S. economy added an impressive 271,000 jobs in October

6

Source: Federal Reserve Economic Data St. Louis Fed

U.S. GDP Growth

U.S. GDP in the 3rd quarter advanced at a 1.5% seasonally adjusted annual rate7

Source: Federal Reserve Economic Data St. Louis Fed

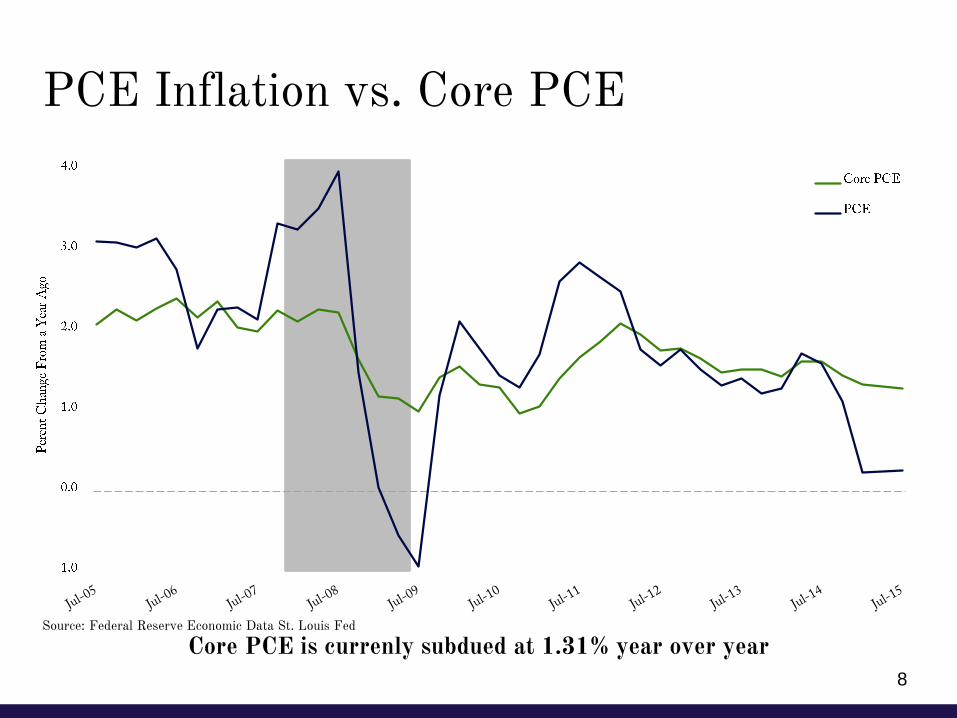

PCE Inflation vs. Core PCE

Core PCE is currenly subdued at 1.31% year over year

8

Source: Federal Reserve Economic Data St. Louis Fed

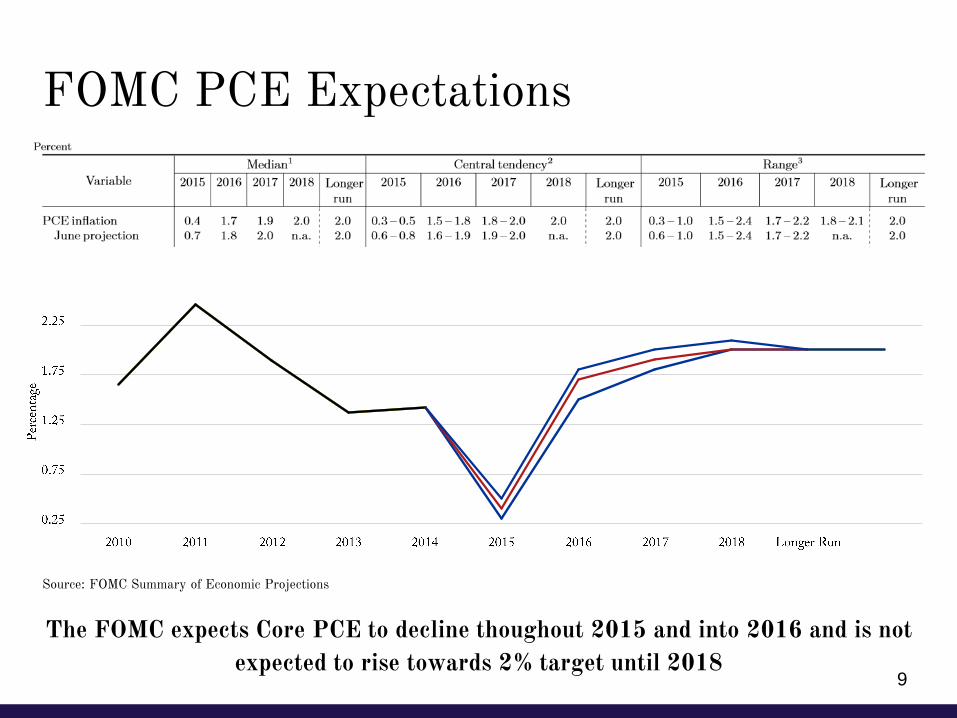

FOMC PCE Expectations

The FOMC expects Core PCE to decline thoughout 2015 and into 2016 and is not

expected to rise towards 2% target until 20189

Source: FOMC Summary of Economic Projections

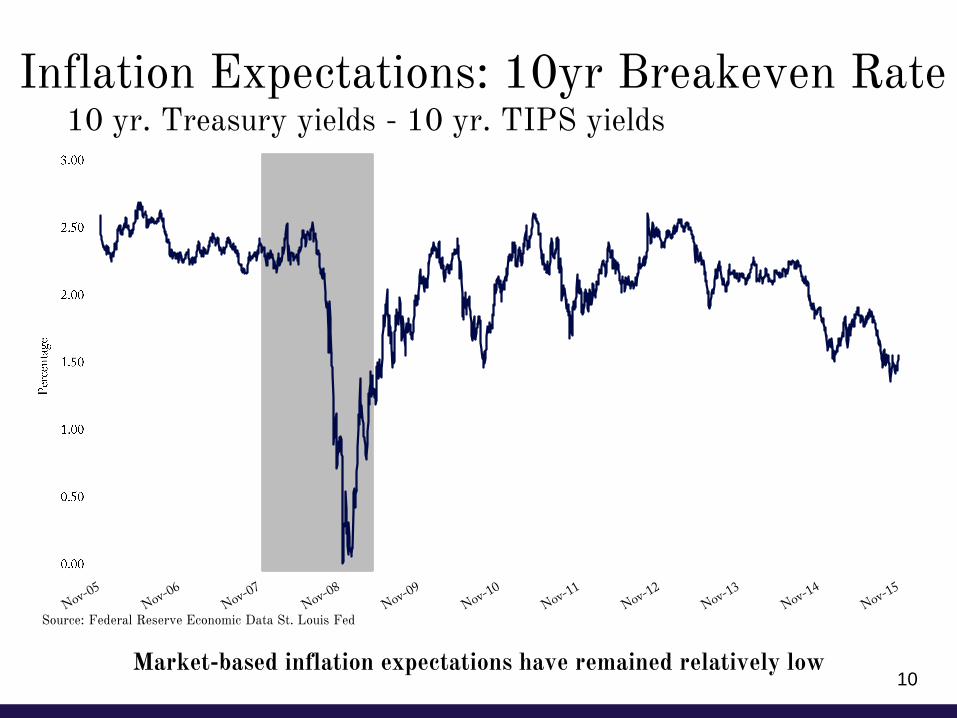

Inflation Expectations: 10yr Breakeven Rate 10 yr. Treasury yields - 10 yr. TIPS yields

Market-based inflation expectations have remained relatively low10

Source: Federal Reserve Economic Data St. Louis Fed

U.S. Trade Gap

Slowdowns in exports are significant as they widen the trade deficit

11

Source: Federal Reserve Economic Data St. Louis Fed

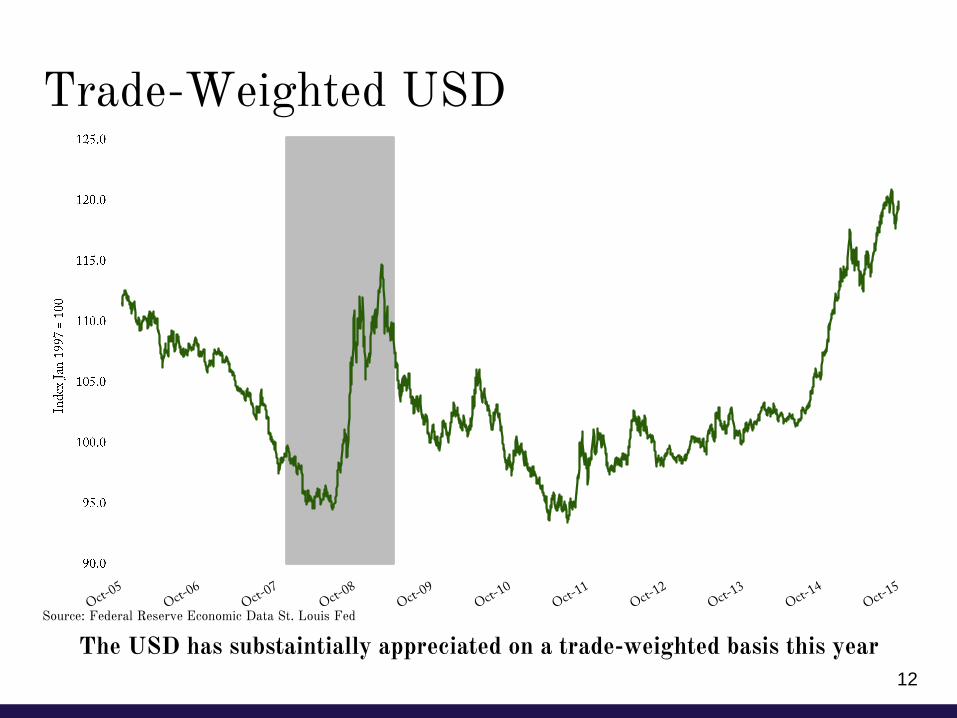

Trade-Weighted USD

The USD has substaintially appreciated on a trade-weighted basis this year

12

Source: Federal Reserve Economic Data St. Louis Fed

International Instability: Why We Care

■ Negative impacts of a stronger USD

■ Weaker net exports

■ Weakening global growth

■ Three largest trading partners:

o Canada

o Mexico

o China

Slowing growth is particularly concerning in Canada, Mexico, and China, who alone

account for 42% of total exports13

USD vs CAD & MXN

The CAD and the MXN have depreciated substaintially against the USD this year

14

Source: Federal Reserve Economic Data St. Louis Fed

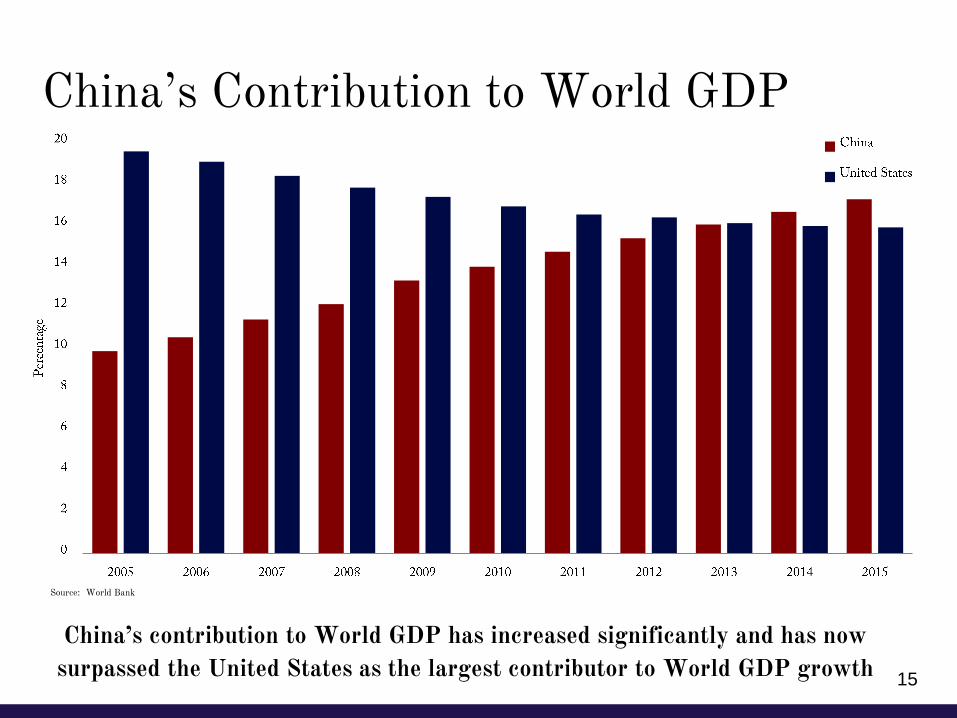

China’s Contribution to World GDP

China’s contribution to World GDP has increased significantly and has now

surpassed the United States as the largest contributor to World GDP growth

Source: World Bank

15

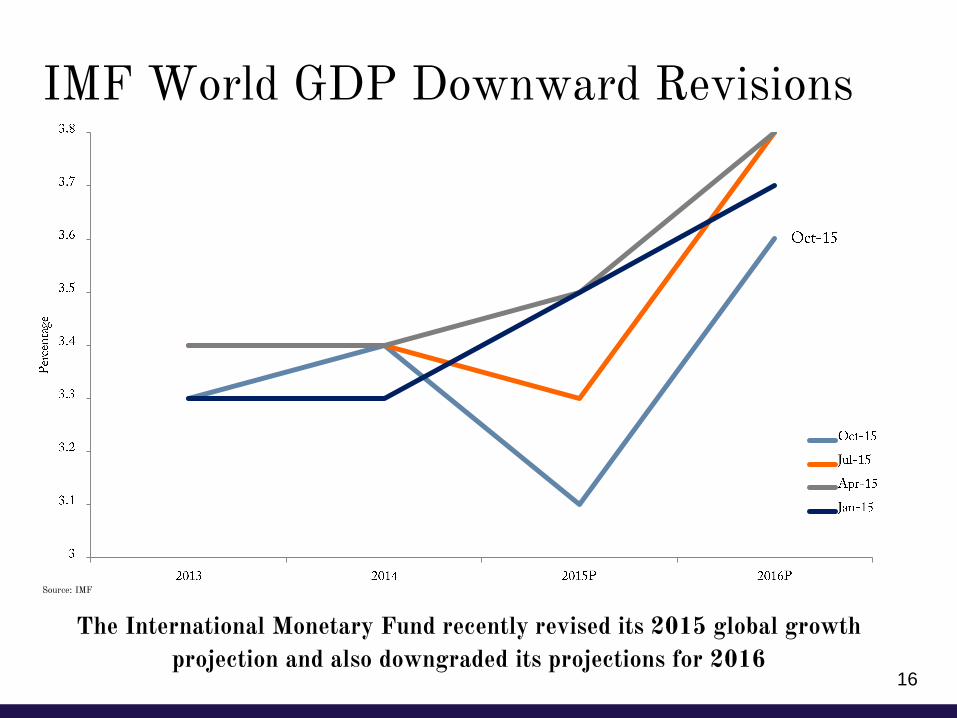

IMF World GDP Downward Revisions

The International Monetary Fund recently revised its 2015 global growth

projection and also downgraded its projections for 2016

Source: IMF

16

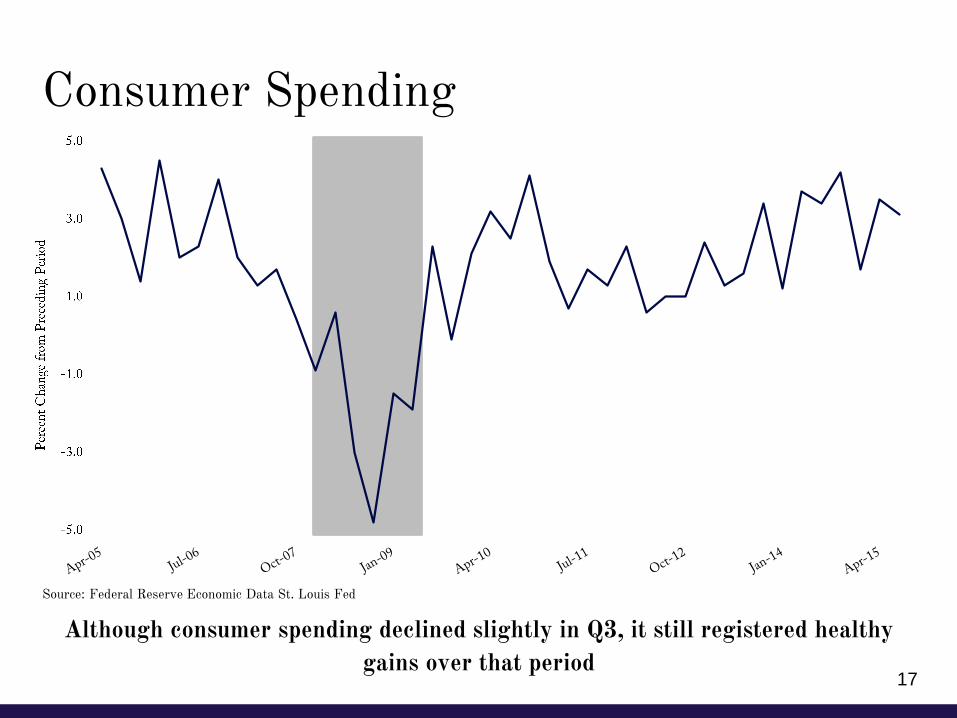

Consumer Spending

Although consumer spending declined slightly in Q3, it still registered healthy

gains over that period17

Source: Federal Reserve Economic Data St. Louis Fed

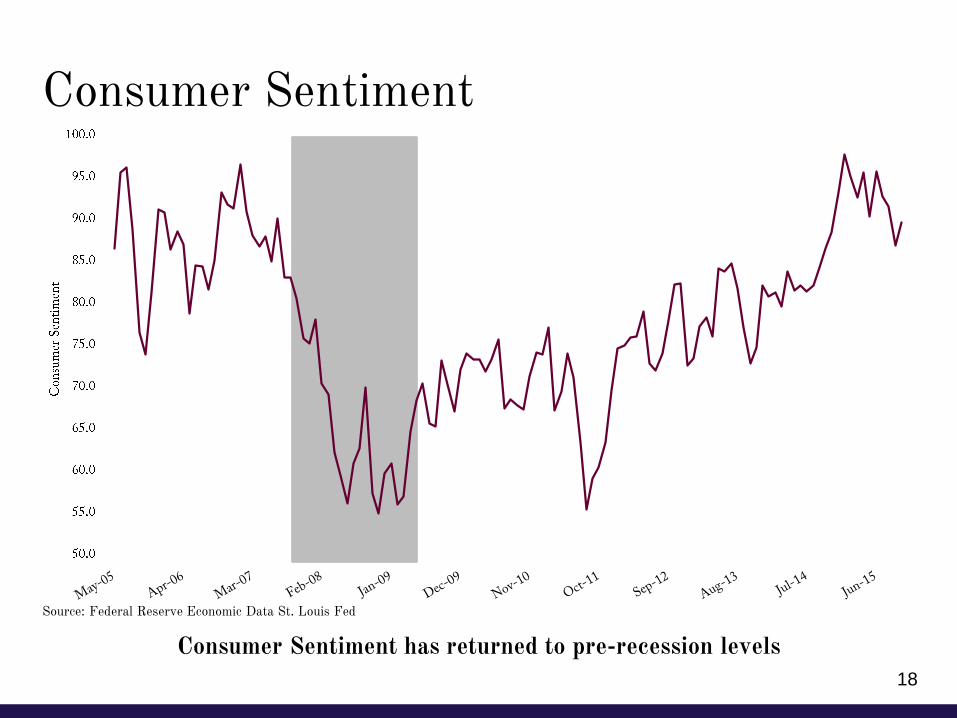

Consumer Sentiment

Consumer Sentiment has returned to pre-recession levels

18

Source: Federal Reserve Economic Data St. Louis Fed

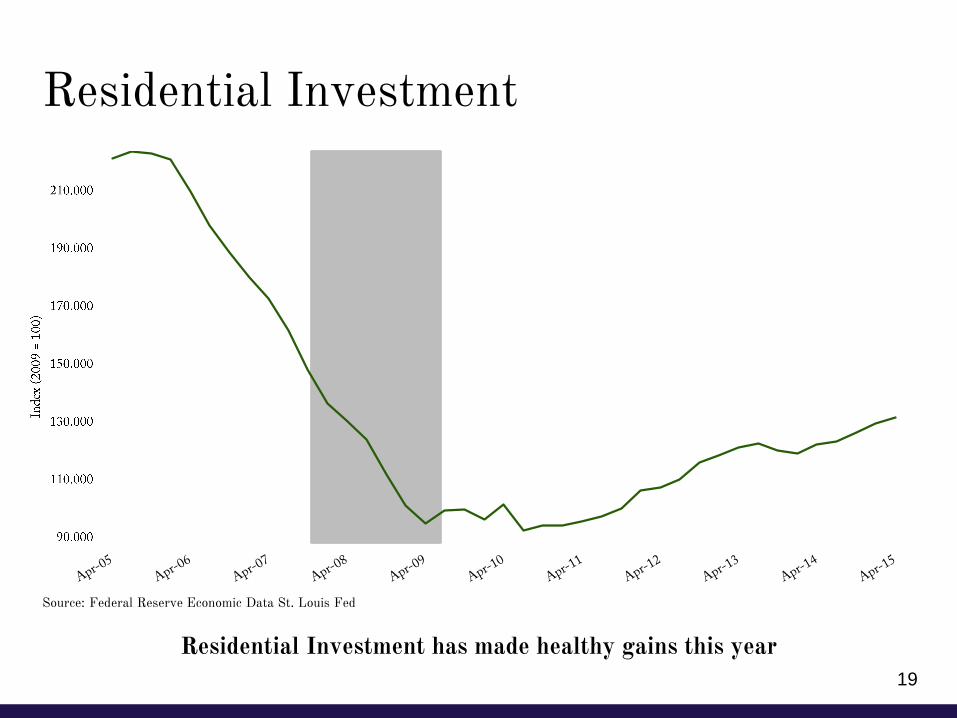

Residential Investment

Residential Investment has made healthy gains this year

19

Source: Federal Reserve Economic Data St. Louis Fed

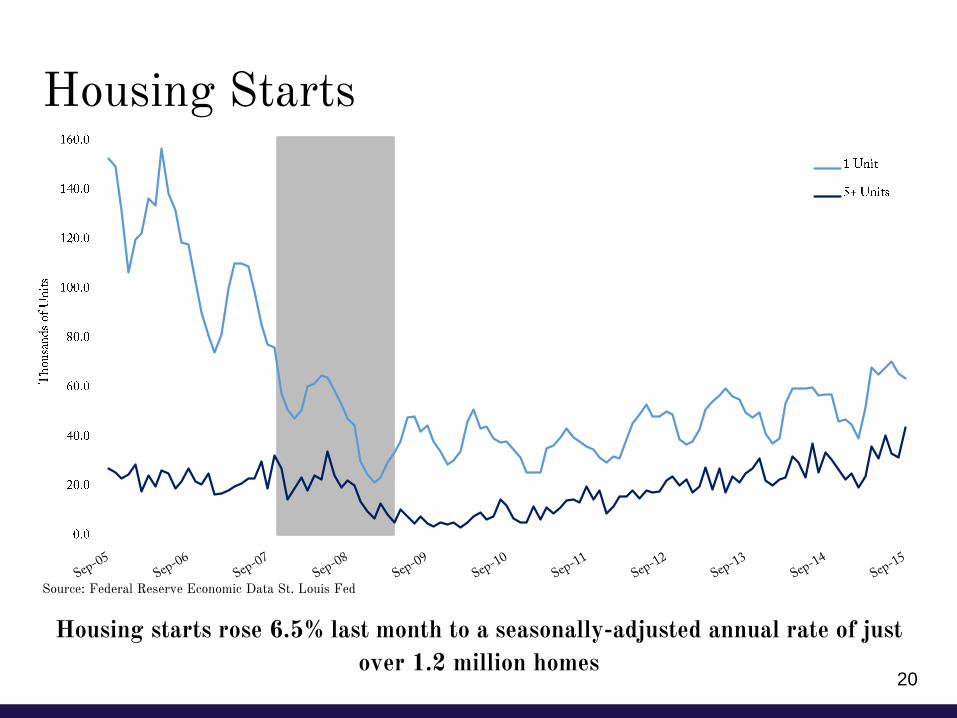

Housing Starts

Housing starts rose 6.5% last month to a seasonally-adjusted annual rate of just

over 1.2 million homes 20

Source: Federal Reserve Economic Data St. Louis Fed

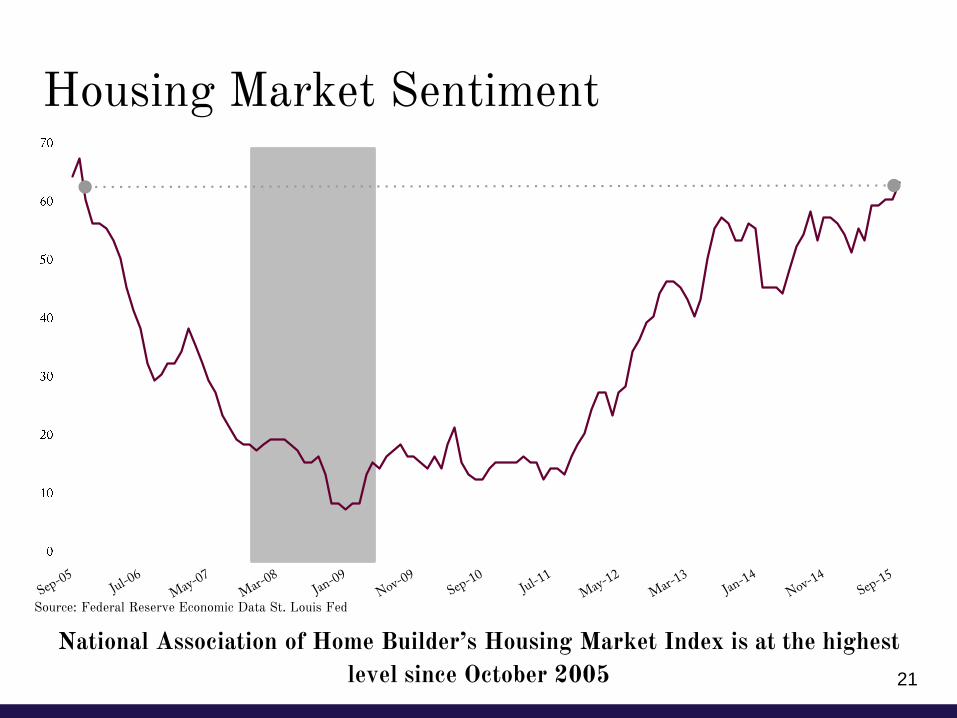

Housing Market Sentiment

National Association of Home Builder’s Housing Market Index is at the highest

level since October 2005 21

Source: Federal Reserve Economic Data St. Louis Fed

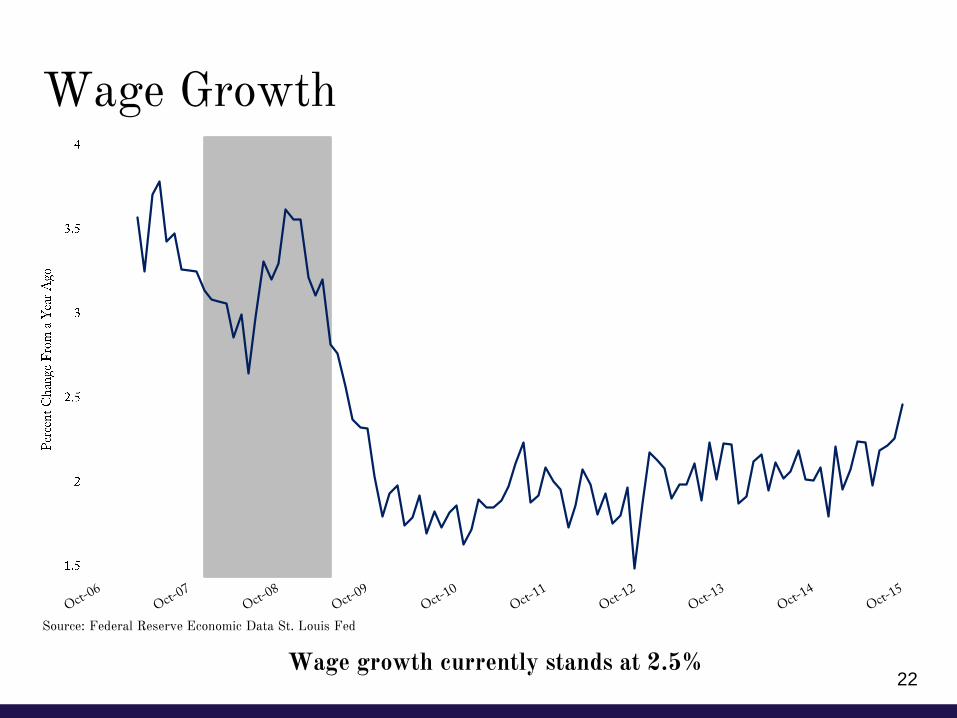

Wage Growth

Wage growth currently stands at 2.5%22

Source: Federal Reserve Economic Data St. Louis Fed

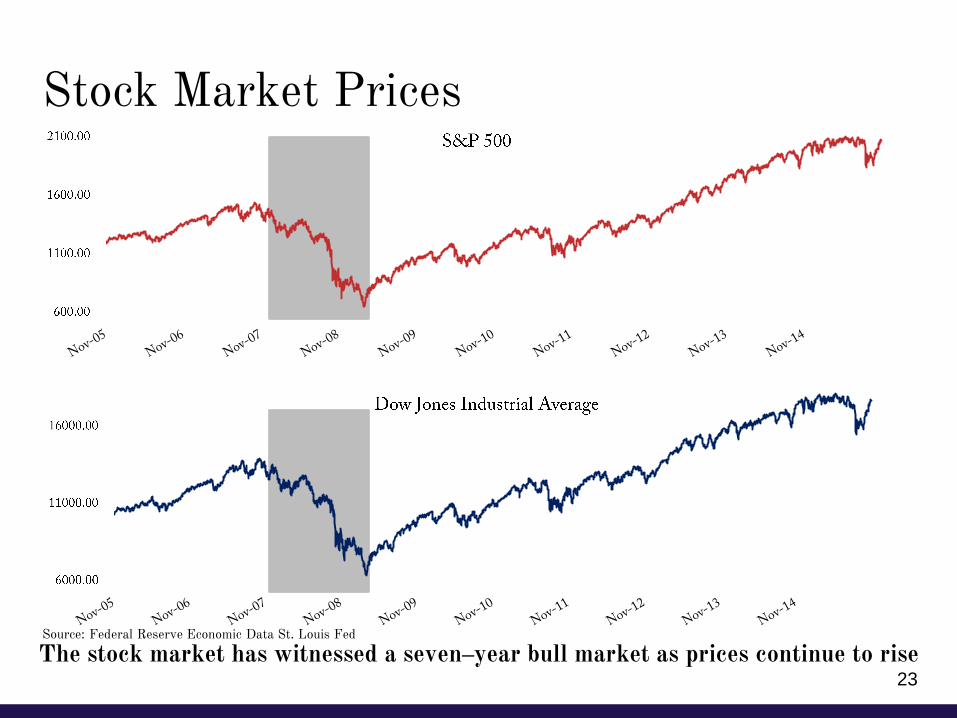

Stock Market Prices

The stock market has witnessed a seven–year bull market as prices continue to rise23

Source: Federal Reserve Economic Data St. Louis Fed

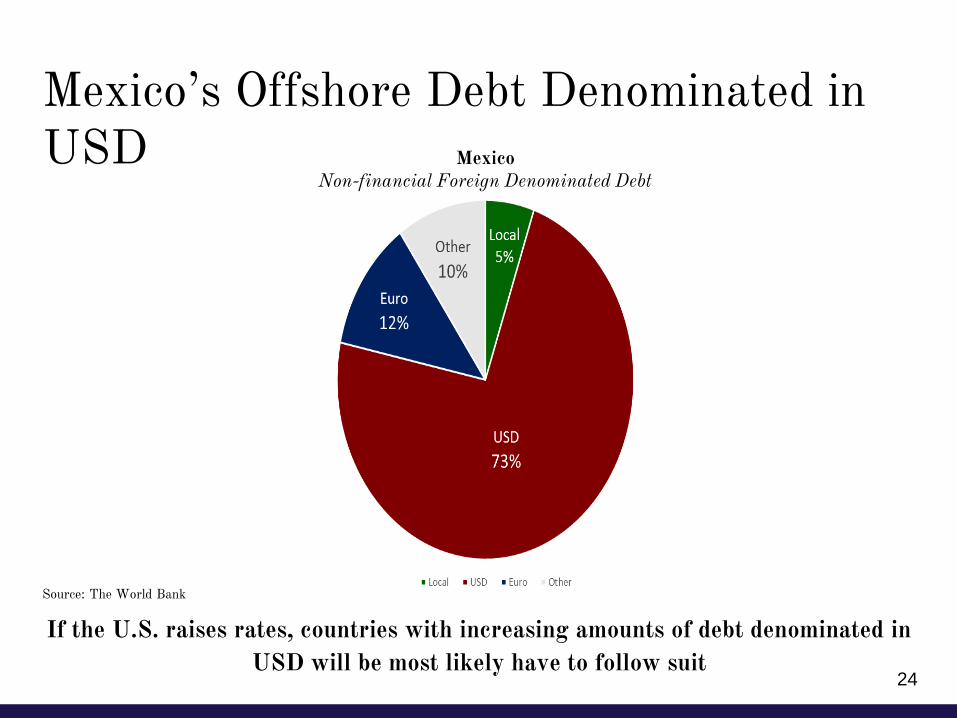

Mexico’s Offshore Debt Denominated in USD

If the U.S. raises rates, countries with increasing amounts of debt denominated in

USD will be most likely have to follow suit

Non-financial Foreign Denominated Debt Mexico

24

Source: The World Bank

CBOE Volitility Index: VIX

The VIX rose substaintially in August as investors were concerned about the

slowdown of China and its ripple effects in emerging markets 25

Source: Federal Reserve Economic Data St. Louis Fed

Inflation: History

The forces leading to inflation can build up before they are apparent in the data

26

Source: Federal Reserve Economic Data St. Louis Fed

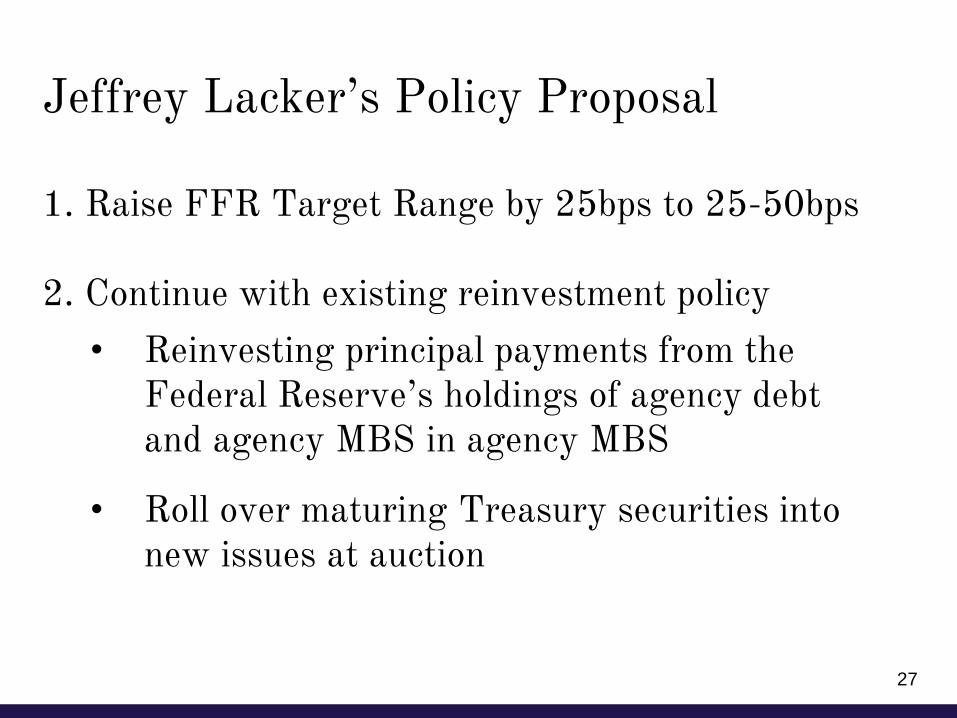

Jeffrey Lacker’s Policy Proposal

1. Raise FFR Target Range by 25bps to 25-50bps

2. Continue with existing reinvestment policy

• Reinvesting principal payments from the Federal Reserve’s holdings of agency debt and agency MBS in agency MBS

• Roll over maturing Treasury securities into new issues at auction

27

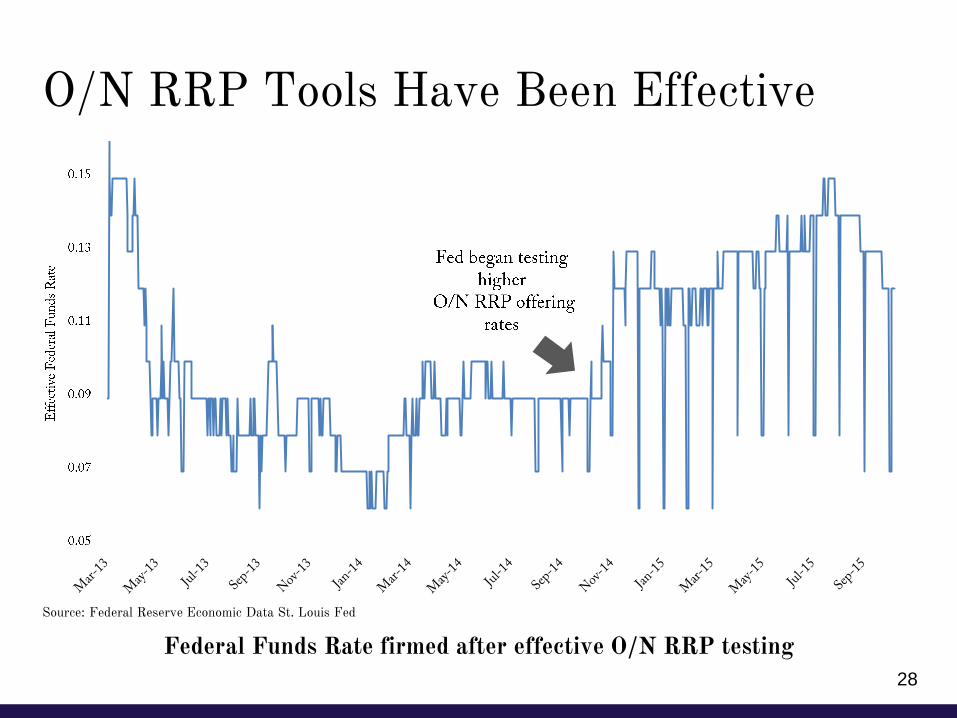

O/N RRP Tools Have Been Effective

Federal Funds Rate firmed after effective O/N RRP testing

28

Source: Federal Reserve Economic Data St. Louis Fed

Treasury Securities Maturing from SOMA

Notable increases in SOMA treasury maturities will begin in early 2016

Billion

s of

US

D

Q1

29

Source: Scotiabank Economics

Appendix

i

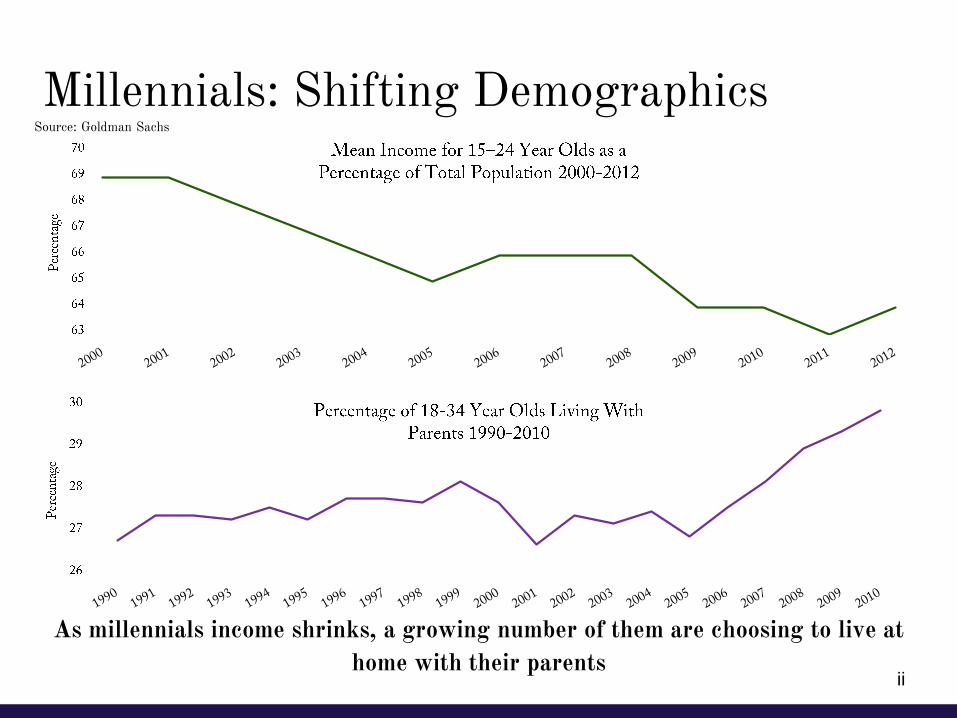

Millennials: Shifting Demographics

As millennials income shrinks, a growing number of them are choosing to live at

home with their parentsii

Source: Goldman Sachs

Student Debt Levels

The remarkable build up of student debt is historically unprecedented

iii

Housing Prices

Housing prices have risen

iv

Source: Federal Reserve Economic Data St. Louis Fed

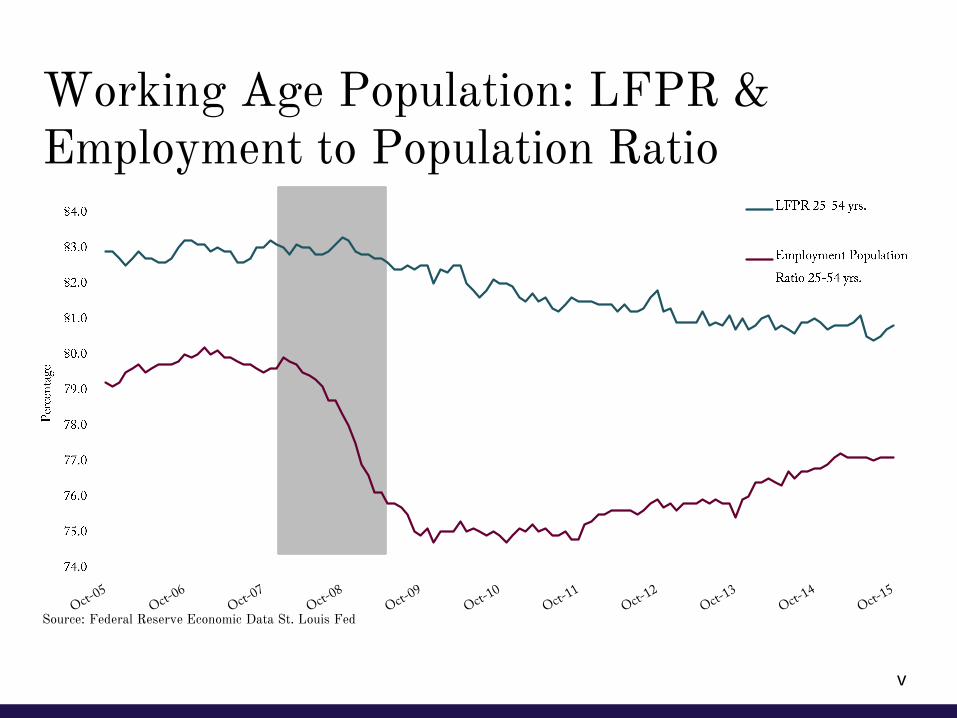

Working Age Population: LFPR & Employment to Population Ratio

v

Source: Federal Reserve Economic Data St. Louis Fed

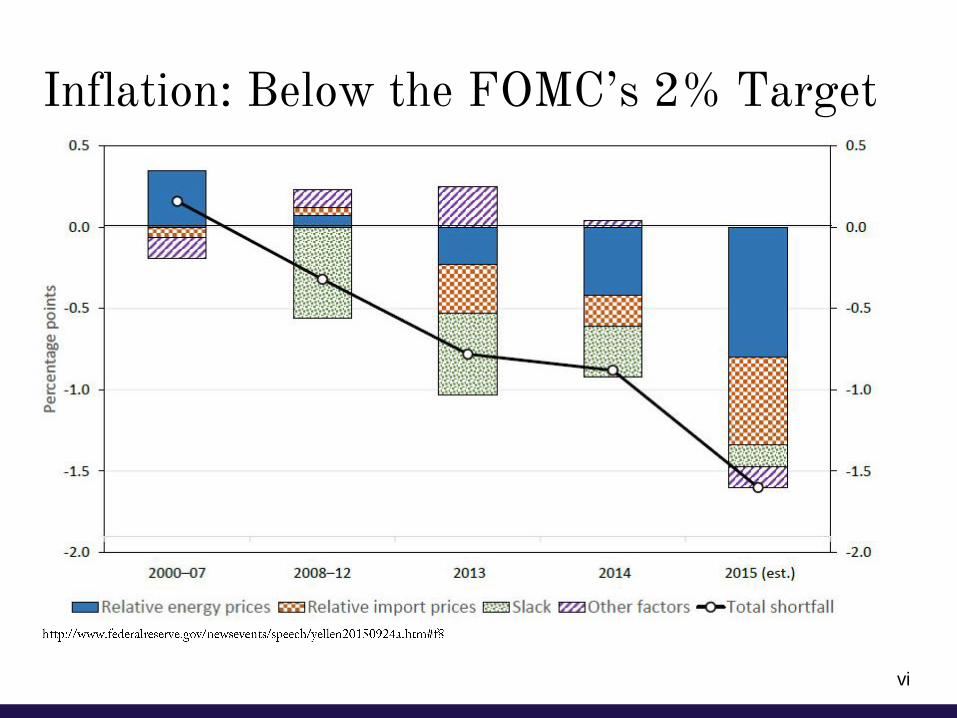

Inflation: Below the FOMC’s 2% Target

vi

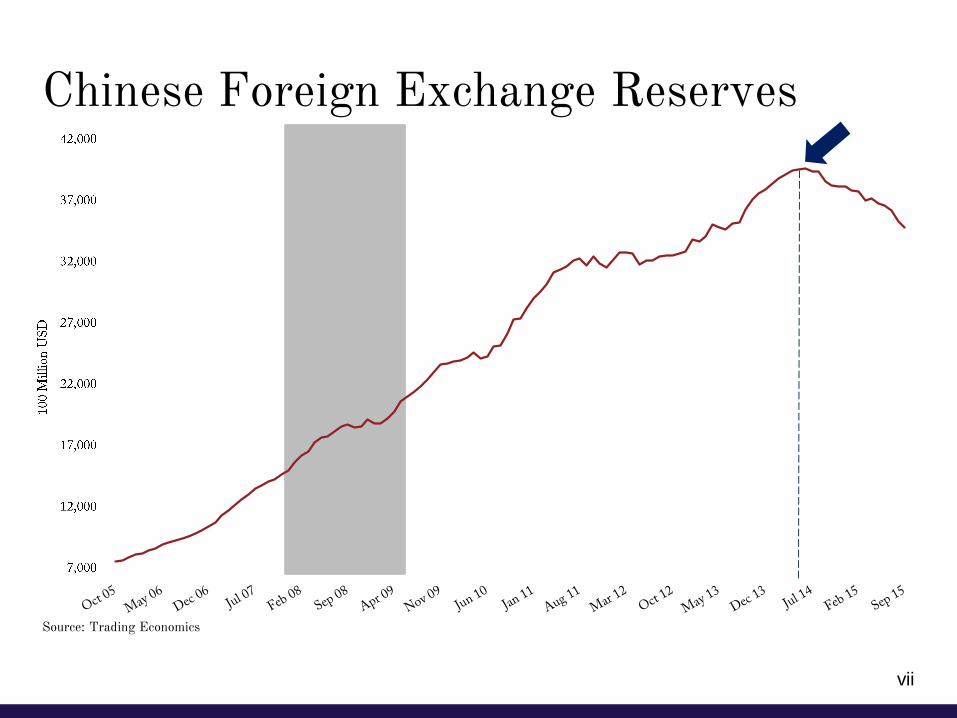

Chinese Foreign Exchange Reserves

vii

Source: Trading Economics

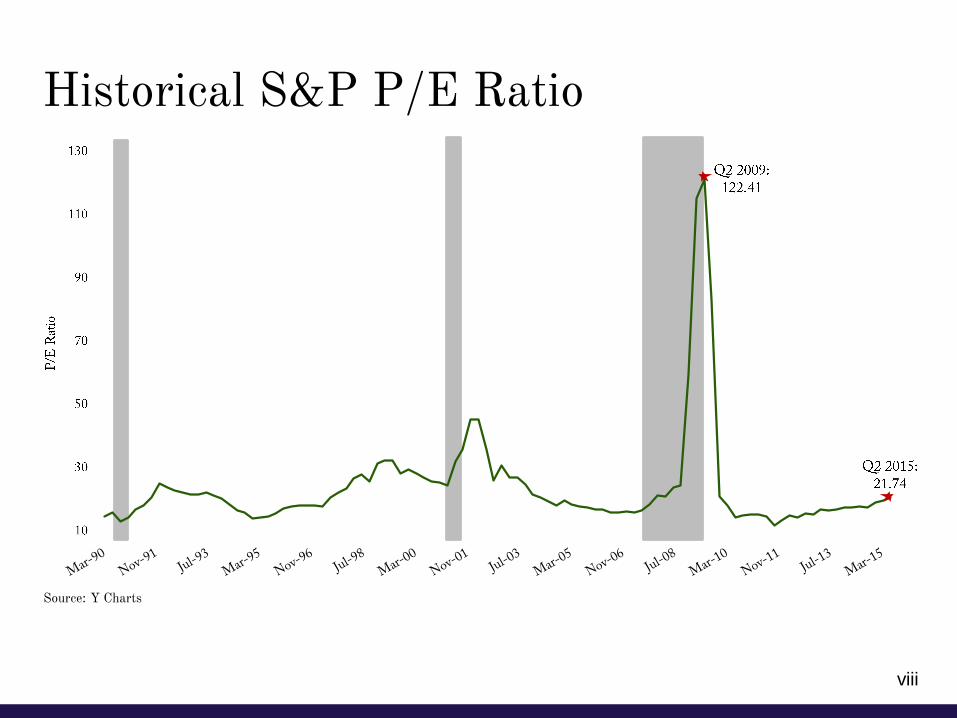

Historical S&P P/E Ratio

viii

Source: Y Charts

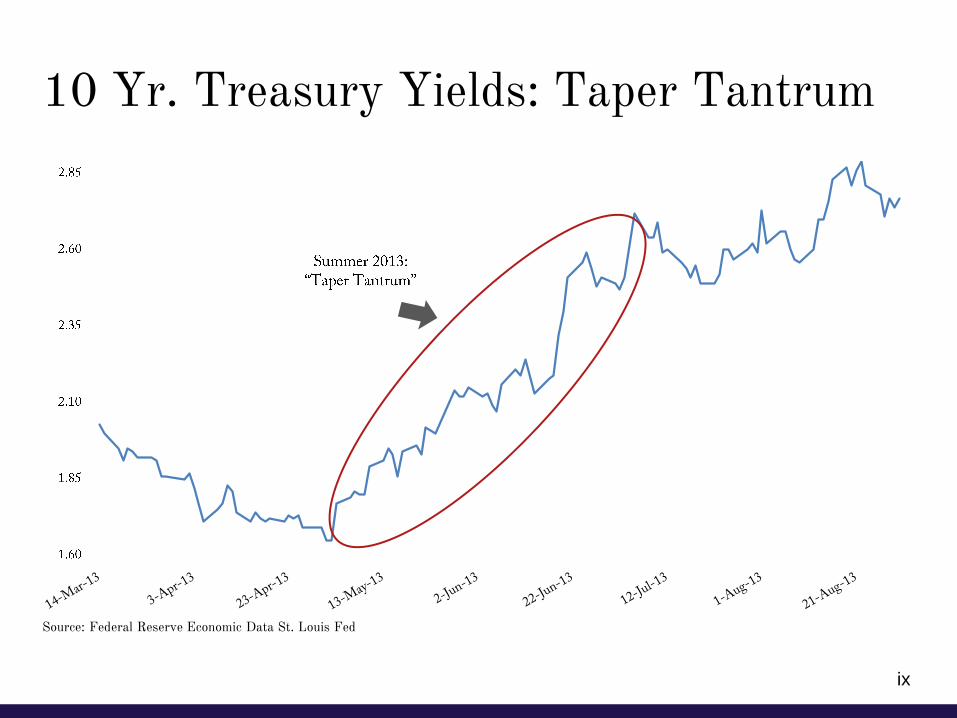

10 Yr. Treasury Yields: Taper Tantrum

ix

Source: Federal Reserve Economic Data St. Louis Fed

Related Documents