Financial Risk Management Prof. Dr. Jörg Prokop Winter Term 2014/15 Financial Risk Management 2 Course Contents • Concept of risk management • Mechanics of financial markets, in particular derivatives markets • Applications and limitations of financial derivatives in risk management

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Risk Management

Prof. Dr. Jörg Prokop

Winter Term 2014/15

Financial Risk Management 2

Course Contents

• Concept of risk management

• Mechanics of financial markets, in particular derivatives markets

• Applications and limitations of financial derivatives in riskmanagement

Preliminary Course Outline

1. What Is Risk?

2. Introduction to Derivatives

3. Mechanics of Futures Markets

4. Hedging Strategies Using Futures

5. Interest Rates

6. Determination of Forward and Futures Prices

7. Swaps

8. Properties of Options

9. Binomial Trees

10. The Black-Scholes-Merton Model

11. Conclusion

Financial Risk Management 3

Financial Risk Management 4

Recommended Readings

• Hull, John C. Options, Futures, and Other Derivatives, 8th ed., Pearson 2012 [OFD]

� main textbook (note: the older editions 6 or 7 will do as well)

• Hull, John C. Solutions Manual for Options, Futures, and Other Derivatives, 8th ed., Pearson 2012

• Damodaran, Strategic Risk Taking: A Framework For Risk Management, Pearson 2008 [SRT] (draft version: http://pages.stern. nyu.edu/~adamodar/New_Home_Page/valrisk/book.htm)

• Hull, John C. Fundamentals of Futures and Options Markets, 7th ed., Pearson 2011

� alternative textbook

Financial Risk Management 5

Preliminary Schedule

Date Time Room Topic Chapter

17 Sep 14.00-17.00 BC-207 • What Is Risk?• Introduction to Derivatives

• SRT 1, 2, 4• OFD 1

18 Sep 14.00-17.00 BC-208 • Mechanics of futuresmarkets

• Hedging strategies usingfutures

• OFD 2• OFD 3

19 Sep 09.00-12.0014.00-17.00

BC-208BC-208

• Interest rates• Forward and futures prices• Swaps• Properties of Options

• OFD 4• OFD 5• OFD 7• OFD 9, 10

30 Sep 10.00-13.0014.00-17.00

BC-207BC-208

• Binomial trees• The Black-Scholes-Merton

model• Conclusion / recap session

• OFD 12• OFD 13,

14• OFD 35

Financial Risk Management 6

Course Organization

• Assessment: – Written examination, date tba– The exam will be closed book. However, you will be

permitted a hand-written two-sided “cheat sheet” with notes and / or formulae.

• Slides & course announcements=> Moodle

• Best way to contact me: [email protected]

Financial Risk Management: What Is Risk?

Suggested Reading:• SRT, ch. 1, 2, 4• Holton, Defining Risk, Financial Analysts

Journal, 2004, Vol. 60, No. 6, pp. 19-25

Financial Risk Management 8

Basic Principle

„There’s no such thing as a free lunch.“

(Hessen, Free Lunch, in: Eatwell/Milgate/Newman: The New Palgrave: A Dictionary of Economics, Volume II, London 1988, p. 450)

� How does that relate to Finance and Economics?

Financial Risk Management 9

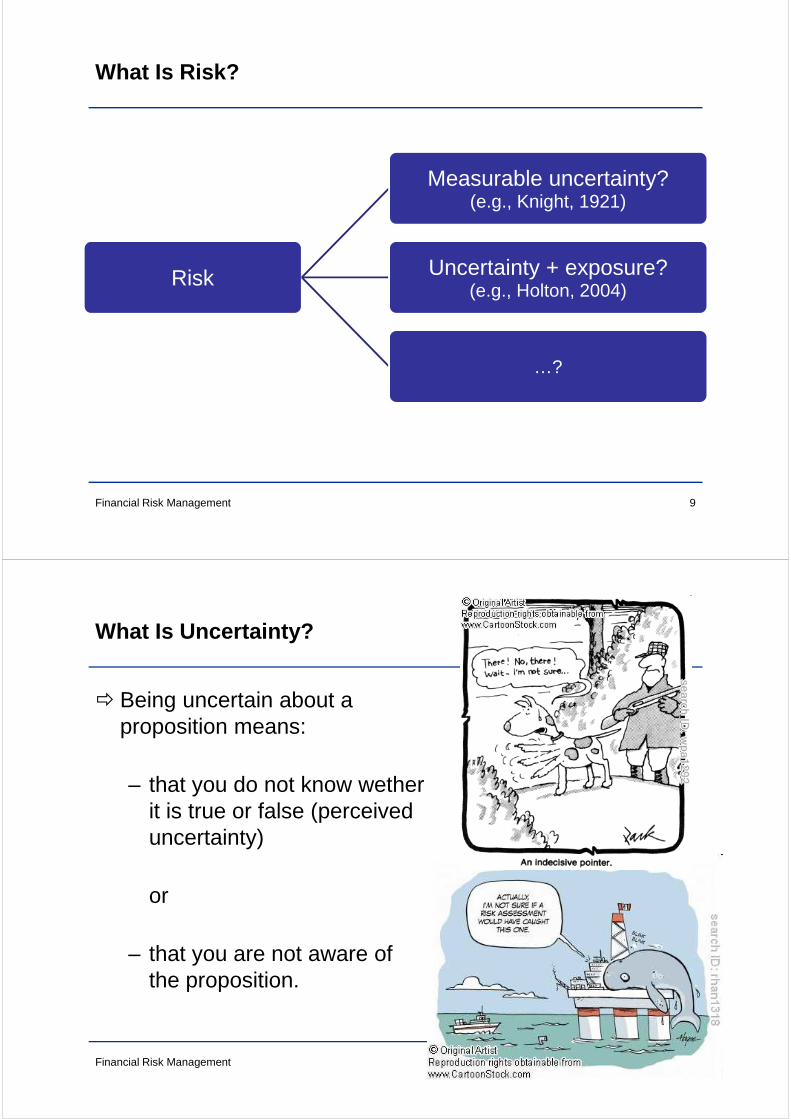

What Is Risk?

Risk

Measurable uncertainty?(e.g., Knight, 1921)

Uncertainty + exposure? (e.g., Holton, 2004)

…?

Financial Risk Management 10

What Is Uncertainty?

� Being uncertain about a proposition means:

– that you do not know wetherit is true or false (perceiveduncertainty)

or

– that you are not aware ofthe proposition.

Financial Risk Management 11

What Is Exposure?

� Having exposure to a proposition means:

• that you care whether it is true or false

or

• that you would carewhether it is true orfalse if you were awareof the proposition.

Financial Risk Management 12

Taking Risk

Some situations that involve risk:• Trading natural gas,• launching a new business,• military adventures,• asking for a pay raise,• sky diving, and• romance.

Do organizations (e.g., companies) take risk? Who does?

Financial Risk Management 13

Why Do We Care About Risk?The St. Petersburg Paradox

• Try the following:– Flip a coin. If it comes up tails, you receive one dollar.

In this case, you may flip it again. If it comes up tails again, your winnings will be doubled.

– You may continue the game to double your winnings as long as the coin does not come up heads.

– If it comes up heads, the experiment ends, and you receive your accumulated gains.

• How much would you pay to participate in this game?

Financial Risk Management 14

Why Do We Care About Risk?The St. Petersburg Paradox

• Expected value:

• Judging only on the basis of the game‘s expected value, we would be willing to pay a very (or even infinitely) high amount of cash to participate

• However, in reality most people would pay only a few $�St. Petersburg Paradox (first published by D. Bernoulli in St.

Petersburg Academy Proceedings, 1738)

∑∞

=

∞==++++=

+⋅+⋅+⋅+⋅=

1 2

1...

2

1

2

1

2

1

2

1

...816

14

8

12

4

11

2

1

i

E

Financial Risk Management 15

Expected Utility Theory

“The determination of the value of an item must not be based on its price, but rather on the utility it yields. The price of the item is dependent only on the thing itself and is equal for everyone; the utility, however, is dependent on the particular circumstances of the person making the estimate. Thus there is no doubt that a gain of one thousand ducats is more significant to a pauper than to a rich man though both gain the same amount.”

(Bernoulli, 1738, [cited in Econometrica 22(1), 1954, p. 24])

How can we turn this idea into a decision model?

Financial Risk Management 16

Expected Utility Theory

• Bernoulli‘s approach: Utility functions

�Step 1: Assign a subjective utility value toevery potential outcome of the uncertain target variable

�Step 2: Calculate the expectation value of the distribution of uncertain utility values from step 1

�Expected Utility Theory

W~

( )WU

( )[ ]W~

UE

NB: The following discussion of Expected Utility Theory is partly based on Elton / Gruber / Brown / Goetzman: Modern Portfolio Theory and Investment Analysis, 6th ed., Hoboken 2003, chapter 10

Financial Risk Management 17

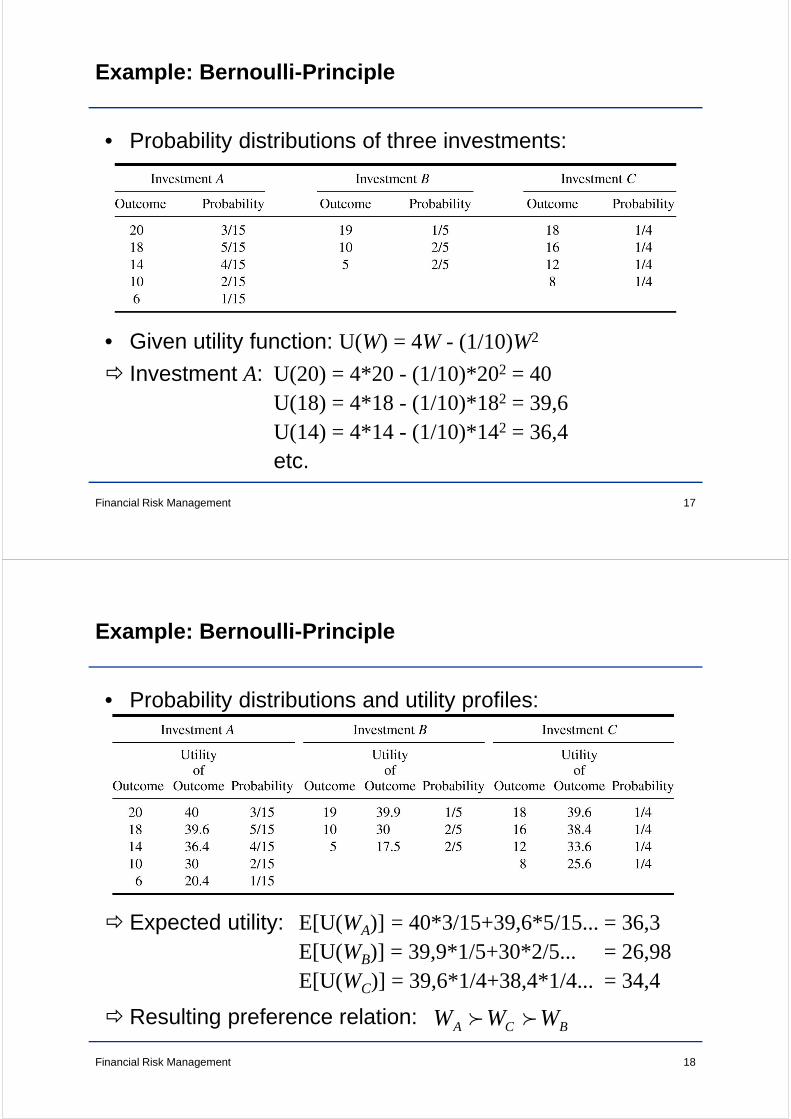

• Probability distributions of three investments:

• Given utility function: U(W) = 4W - (1/10)W2

� Investment A: U(20) = 4*20 - (1/10)*202 = 40U(18) = 4*18 - (1/10)*182 = 39,6U(14) = 4*14 - (1/10)*142 = 36,4etc.

Example: Bernoulli -Principle

Financial Risk Management 18

• Probability distributions and utility profiles:

� Expected utility: E[U(WA)] = 40*3/15+39,6*5/15... = 36,3E[U(WB)] = 39,9*1/5+30*2/5... = 26,98E[U(WC)] = 39,6*1/4+38,4*1/4... = 34,4

� Resulting preference relation:

Example: Bernoulli -Principle

BCA WWW ff

Financial Risk Management 19

Characteristics of Utility Functions

Example: „Fair gamble“

� The investor‘s options:

Financial Risk Management 20

Characteristics of Utility Functions

(strictly) concave

(strictly) convex

linear

Utility functions given:(1) Risk preference (e.g., U(W) = W2)(2) Risk neutrality (e.g., U(W) = W)(3) Risk aversion (e.g., U(W) = W0,5)

Financial Risk Management 21

Risk Management

http://www.sciencecartoonsplus.com/gallery/risk/index.php

Financial Risk Management 22

Risk Management

• Potential risk management actions:

– Reduce risk exposure

– Maintain current level of risk exposure

– Increase risk exposure

• Let’s focus on the first one:How can we reduce risk exposure?

http://www.sciencecartoonsplus.com/gallery/risk/index.php

Financial Risk Management 23

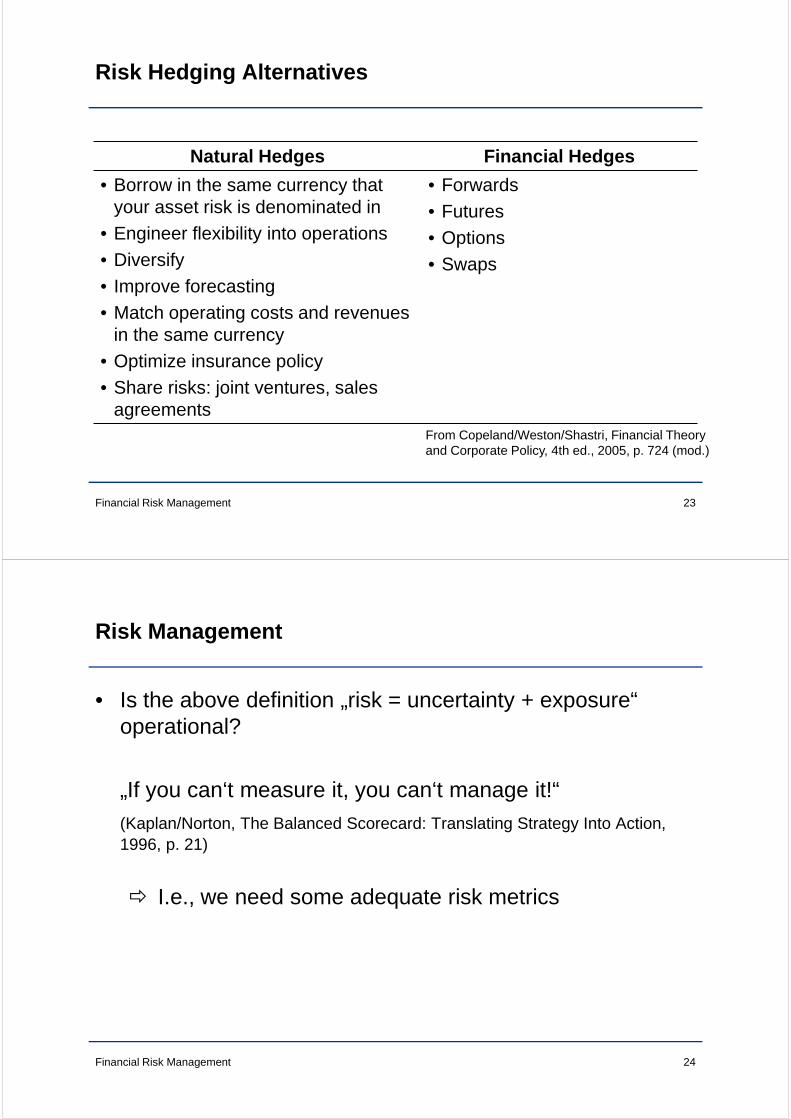

Risk Hedging Alternatives

From Copeland/Weston/Shastri, Financial Theoryand Corporate Policy, 4th ed., 2005, p. 724 (mod.)

Natural Hedges Financial Hedges

• Borrow in the same currency thatyour asset risk is denominated in

• Engineer flexibility into operations• Diversify• Improve forecasting• Match operating costs and revenues

in the same currency• Optimize insurance policy• Share risks: joint ventures, sales

agreements

• Forwards• Futures• Options• Swaps

Financial Risk Management 24

Risk Management

• Is the above definition „risk = uncertainty + exposure“ operational?

„If you can‘t measure it, you can‘t manage it!“(Kaplan/Norton, The Balanced Scorecard: Translating Strategy Into Action, 1996, p. 21)

� I.e., we need some adequate risk metrics

Financial Risk Management 25

Risk vs Return

• There is a trade off between risk and expected return

• The higher the risk, the higher the expected return

• We can characterize investments by their expected return (µi) and standard deviation of returns (σi):

• The relationship between two investments’ return data can be described by their covariance (σij), or by theircorrelation coefficient (ρij):

∑=

⋅==n

jjijii rwr

1,

~]~[Eµ ( )∑=

−⋅==n

jijijii rw

1

2,

2 ~ µσσ

( ) ( )∑=

−⋅−=n

kjjkiikkij rrw

1

~~ µµσji

ijij σσ

σρ

⋅=

Systematic vs Non-Systematic Risk

• Nonsystematic risk– Results from uncontrollable or random events that are

firm-specific– Examples: labor strikes, lawsuits

• Systematic risk– Attributable to forces that affect all similar investments– Examples: war, inflation, political events

Financial Risk Management 26

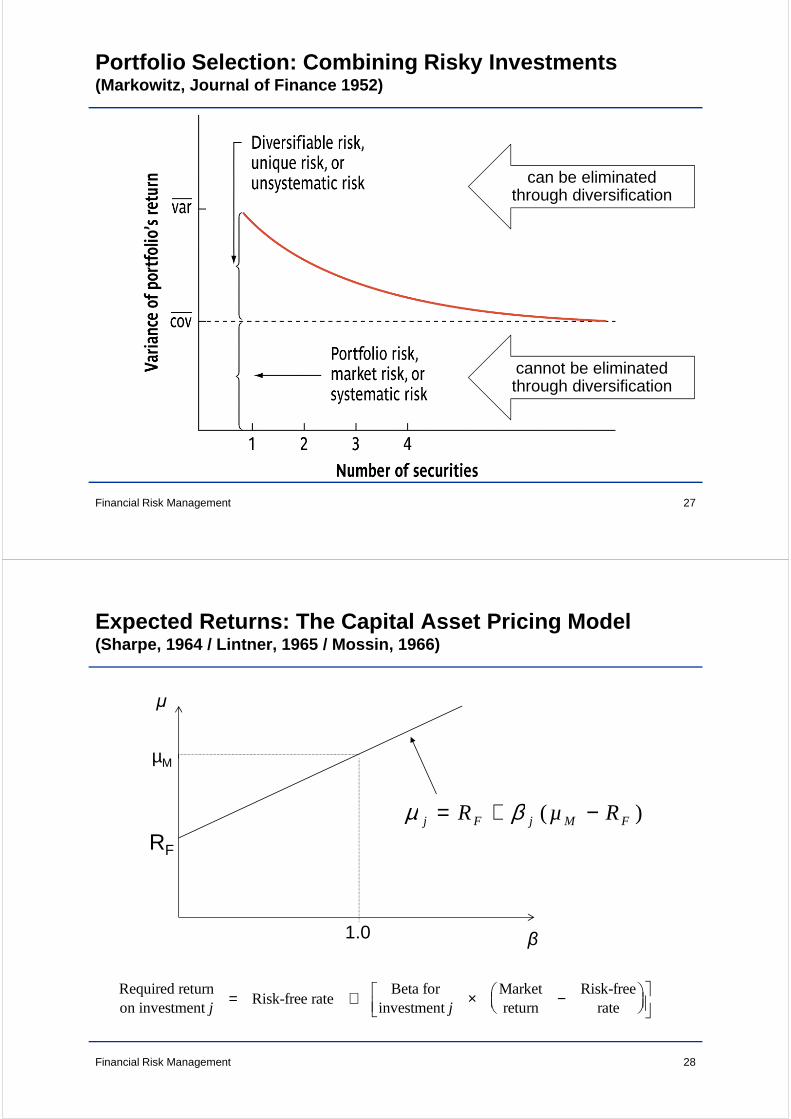

Portfolio Selection: Combining Risky Investments(Markowitz, Journal of Finance 1952)

Financial Risk Management 27

can be eliminated through diversification

cannot be eliminated through diversification

Financial Risk Management 28

Expected Returns: The Capital Asset Pricing Model(Sharpe, 1964 / Lintner, 1965 / Mossin, 1966)

1.0 β

RF

µM

)( FMjFj RµR −+= βµ

μ

Required returnon investment j

= Risk-free rate +Beta for

investment j

×

Marketreturn

−Risk-free

rate

Financial Risk Management 29

Alpha

• Alpha = extra return on a portfolio in excess of that predicted by CAPM

so that

)( FMPFP RR −+= µβµ

)( FMPFP RR −−−= µβµα

Financial Risk Management 30

Key Assumptions Underlying the CAPM

• Investors are risk averse

• Investors care only about an investment’s risk (σ) and expected return (µ) � Implies either normally distributed returns or quadratic utility function

• Unsystematic risks of different assets are independent

• Investors focus on returns over one period

• All investors can borrow or lend at the same risk-free rate

• Tax does not influence investment decisions

• All investors make the same estimates of µ’s, σ’s and ρ’s.

Critique Regarding the µ-σ Framework

• Quadratic utility function:– Implies negative marginal utility for certain (high) ranges

of wealth– Implies increasing absolute risk aversion– Implies that investors are equally averse to good and to

bad outcomes of the same absolute amount

• Normal distribution of returns:– Skewness?– Kurtosis?– Jumps?

Financial Risk Management 31

Financial Risk Management 32

Digression: Arbitrage Pricing Theory(Ross , Journal of Economic Theory, 1976, pp. 341-360)

• Assumptions:– Returns depend on several factors– Arbitrage-free markets (law of one price)

• Expected return is linearly dependent on the realization of the factors

• Each factor is a separate source of systematic risk

• Unsystematic risk is the proportion of total risk that is unrelated to all the factors

IlilIiIiii µβµβµβαµ ⋅++⋅+⋅+= ...2211

Digression: The Carhart (1997) Model

• In the Carhart (1997) model, there are four factors representing the market risk premium, high minus low B/M, small minus big, and momentum arbitrage portfolios respectively.

• The Fama-French (1993) three factor model is simply the four factor model without the momentum factor.

33

)()(

)())(()(

11

YRPRYRPR

SHMLHMLS

SMBSMBSFMkt

MktSFS

RERE

RERRERRE

ββββ

++

+−+=

Financial Risk Management

Financial Risk Management 34

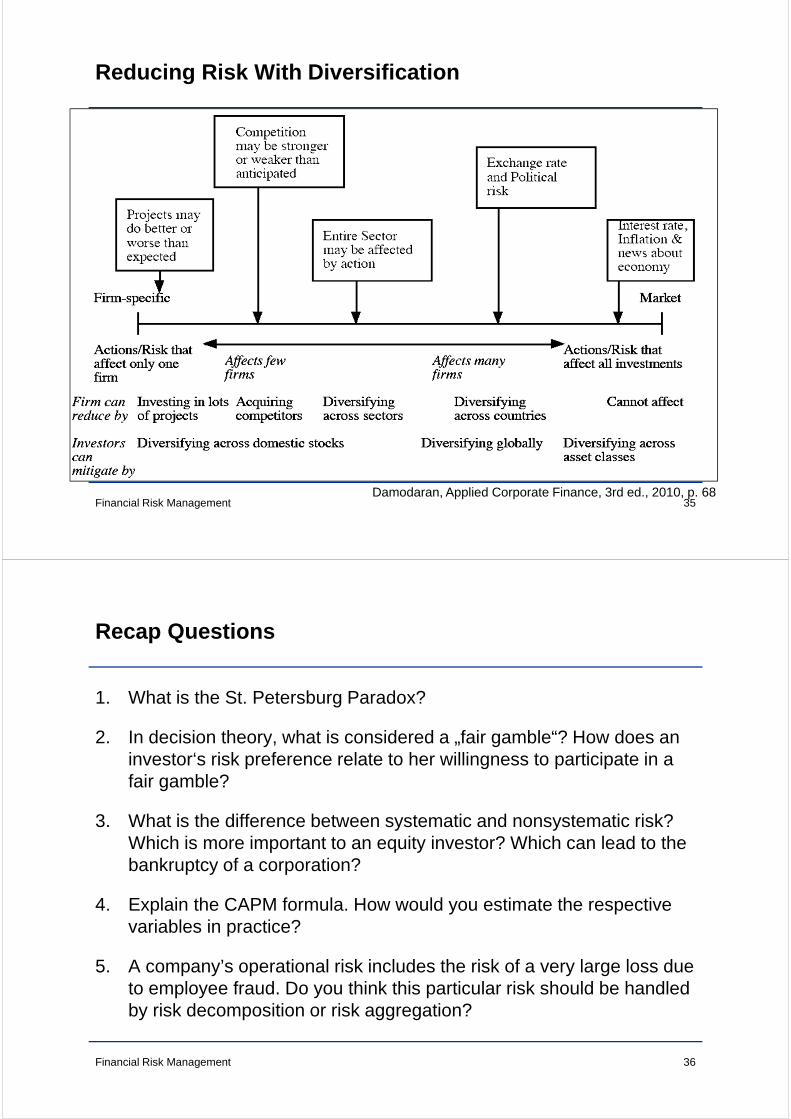

Approaches to Risk Reduction

• Risk aggregation �Aims to get rid of non-systematic risks with

diversification

• Risk decomposition�Tackles risks one by one

• In practice companies use both approaches

Reducing Risk With Diversification

Financial Risk Management 35Damodaran, Applied Corporate Finance, 3rd ed., 2010, p. 68

Recap Questions

1. What is the St. Petersburg Paradox?

2. In decision theory, what is considered a „fair gamble“? How does an investor‘s risk preference relate to her willingness to participate in a fair gamble?

3. What is the difference between systematic and nonsystematic risk? Which is more important to an equity investor? Which can lead to the bankruptcy of a corporation?

4. Explain the CAPM formula. How would you estimate the respective variables in practice?

5. A company’s operational risk includes the risk of a very large loss due to employee fraud. Do you think this particular risk should be handled by risk decomposition or risk aggregation?

Financial Risk Management 36

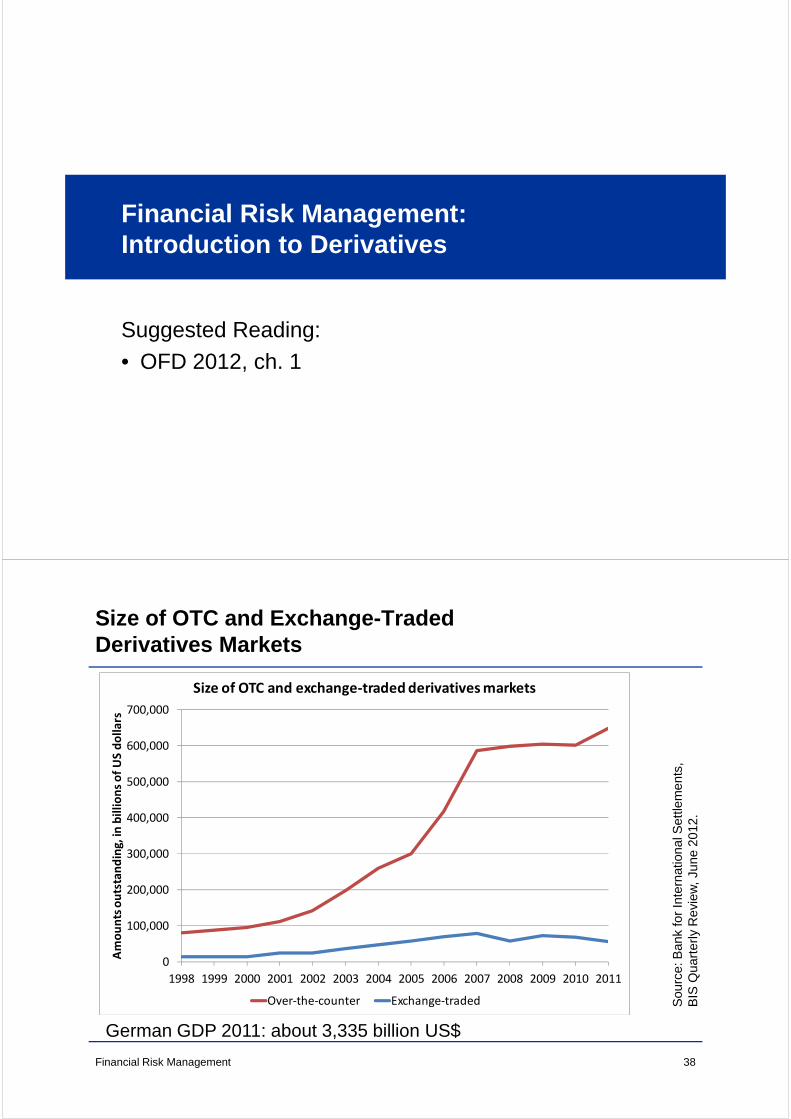

Financial Risk Management: Introduction to Derivatives

Suggested Reading:• OFD 2012, ch. 1

Financial Risk Management 38

Size of OTC and Exchange-Traded Derivatives Markets

Sou

rce:

Ban

k fo

r In

tern

atio

nal S

ettle

men

ts,

BIS

Qua

rter

ly R

evie

w, J

une

2012

.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Am

ou

nts

ou

tsta

nd

ing

, in

bil

lio

ns

of

US

do

lla

rs

Size of OTC and exchange-traded derivatives markets

Over-the-counter Exchange-traded

German GDP 2011: about 3,335 billion US$

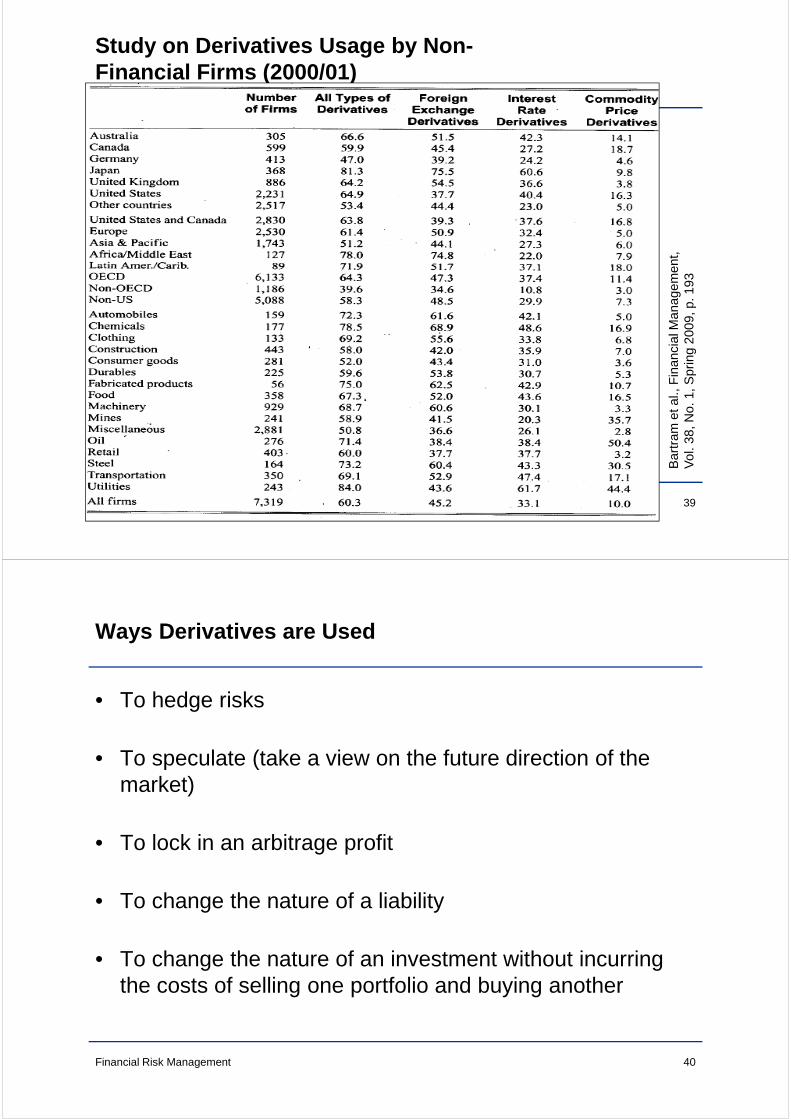

Study on Derivatives Usage by Non-Financial Firms (2000/01)

Financial Risk Management 39

Bar

tram

et a

l., F

inan

cial

Man

agem

ent,

Vol

. 38,

No.

1, S

prin

g 20

09, p

. 193

Financial Risk Management 40

Ways Derivatives are Used

• To hedge risks

• To speculate (take a view on the future direction of the market)

• To lock in an arbitrage profit

• To change the nature of a liability

• To change the nature of an investment without incurring the costs of selling one portfolio and buying another

Financial Risk Management 41

Forward Price

• The forward price for a contract is the delivery price that would be applicable to the contract if it were negotiated today (i.e., it is the delivery price that would make the contract worth exactly zero)

• The forward price may be different for contracts of different maturities

Financial Risk Management 42

Terminology

• The party that has agreed to buy has what is termed a long position

• The party that has agreed to sell has what is termed a short position

Financial Risk Management 43

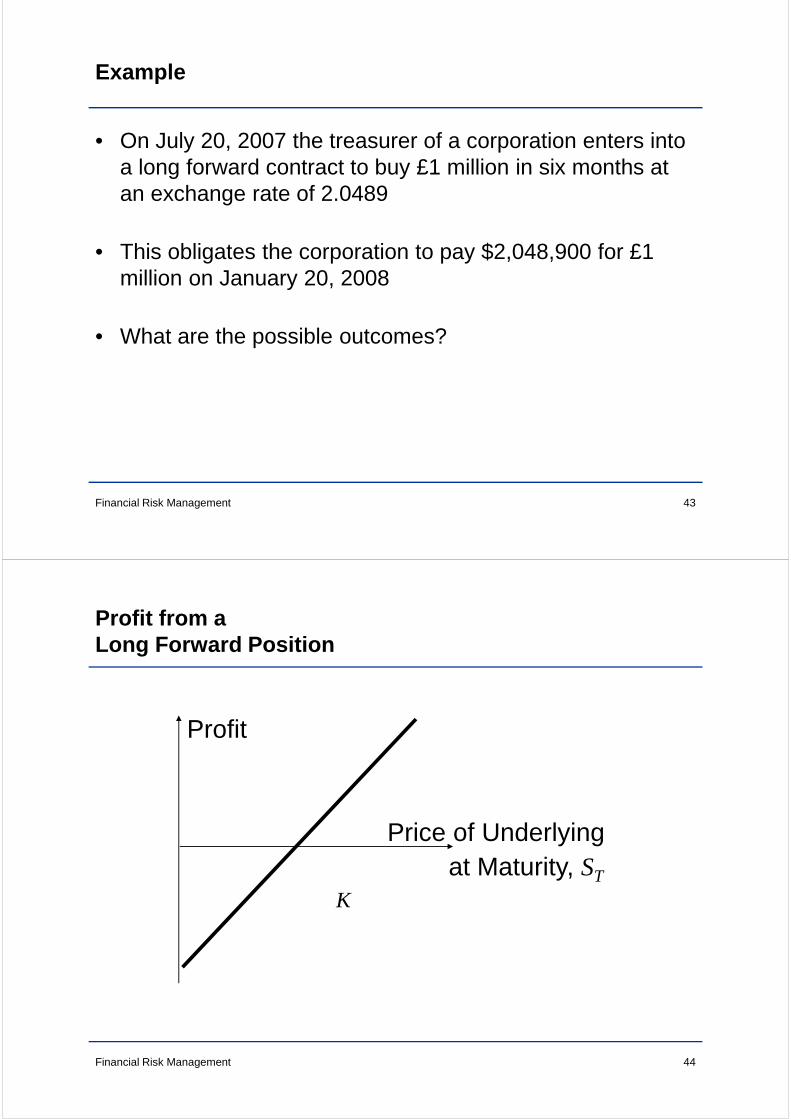

Example

• On July 20, 2007 the treasurer of a corporation enters into a long forward contract to buy £1 million in six months at an exchange rate of 2.0489

• This obligates the corporation to pay $2,048,900 for £1 million on January 20, 2008

• What are the possible outcomes?

Financial Risk Management 44

Profit from aLong Forward Position

Profit

Price of Underlyingat Maturity, ST

K

Financial Risk Management 45

Profit from a Short Forward Position

Profit

Price of Underlyingat Maturity, ST

K

Financial Risk Management 46

Futures Contracts

• Agreement to buy or sell an asset for a certain price at a certain time

• Similar to forward contract

• Whereas a forward contract is traded OTC, a futures contract is traded on an exchange

Financial Risk Management 47

Examples of Futures Contracts

• Agreement to:

– Buy 100 oz. of gold @ US$900/oz. in December (NYMEX)

– Sell £62,500 @ 2.0500 US$/£ in March (CME)

– Sell 1,000 bbl. of oil @ US$120/bbl. in April (NYMEX)

Financial Risk Management 48

1. Gold: An Arbitrage Opportunity?

• Suppose that:– The spot price of gold is US$900– The 1-year forward price of gold is US$1,020– The 1-year US$ interest rate is 5% per annum

• Is there an arbitrage opportunity?

Financial Risk Management 49

2. Gold: Another Arbitrage Opportunity?

• Suppose that:– The spot price of gold is US$900– The 1-year forward price of gold is US$900– The 1-year US$ interest rate is 5% per annum

• Is there an arbitrage opportunity?

Financial Risk Management 50

The Forward Price of Gold

If the spot price of gold is S and the forward price for a contract deliverable in T years is F, then

F = S (1+r )T

where r is the 1-year (domestic currency) risk-free rate of interest.

In our examples, S = 900, T = 1, and r =0.05 so thatF = 900(1+0.05) = 945

Financial Risk Management 51

1. Oil: An Arbitrage Opportunity?

• Suppose that:– The spot price of oil is US$95– The quoted 1-year futures price of oil is US$125– The 1-year US$ interest rate is 5% per annum– The storage costs of oil are 2% per annum

• Is there an arbitrage opportunity?

Financial Risk Management 52

2. Oil: Another Arbitrage Opportunity?

• Suppose that:– The spot price of oil is US$95– The quoted 1-year futures price of oil is US$80– The 1-year US$ interest rate is 5% per annum– The storage costs of oil are 2% per annum

• Is there an arbitrage opportunity?

Financial Risk Management 53

Options

• A call option is an option to buy a certain asset by a certain date for a certain price (the strike price)

• A put option is an option to sell a certain asset by a certain date for a certain price (the strike price)

Financial Risk Management 54

American vs European Options

• An American option can be exercised at any time during its life

• A European option can be exercised only at maturity

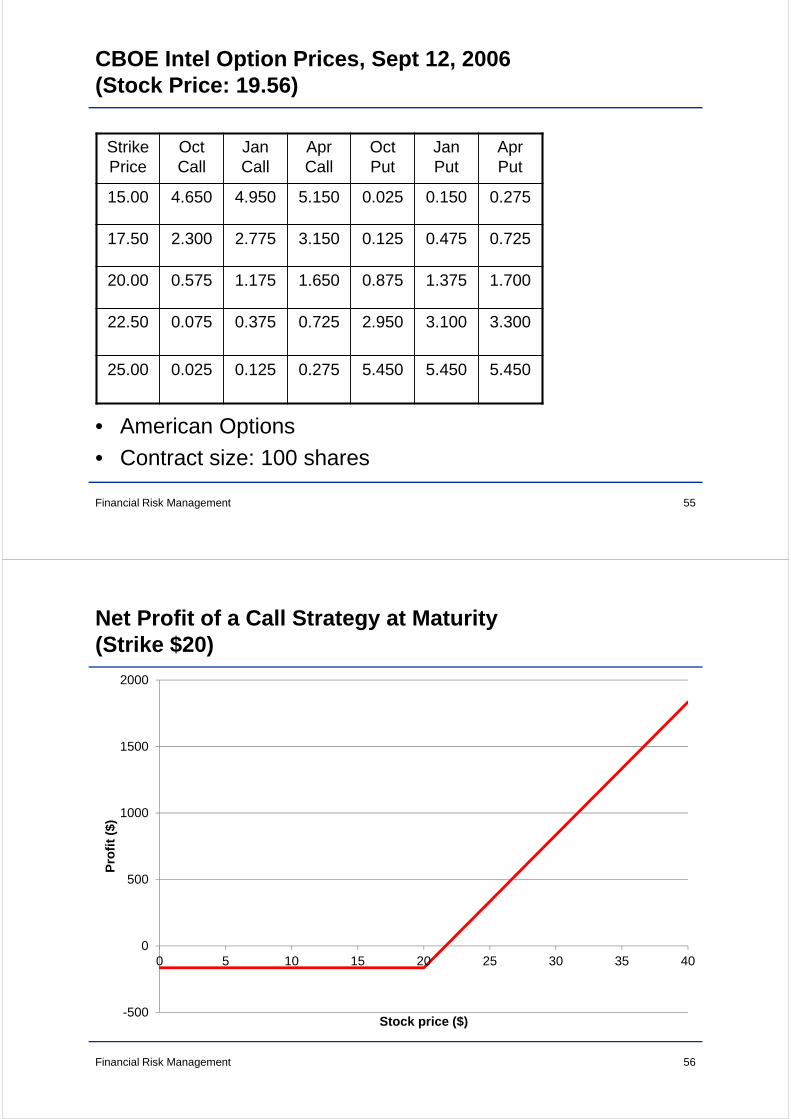

CBOE Intel Option Prices, Sept 12, 2006 (Stock Price: 19.56)

• American Options• Contract size: 100 shares

Financial Risk Management 55

Strike Price

Oct Call

Jan Call

Apr Call

Oct Put

Jan Put

Apr Put

15.00 4.650 4.950 5.150 0.025 0.150 0.275

17.50 2.300 2.775 3.150 0.125 0.475 0.725

20.00 0.575 1.175 1.650 0.875 1.375 1.700

22.50 0.075 0.375 0.725 2.950 3.100 3.300

25.00 0.025 0.125 0.275 5.450 5.450 5.450

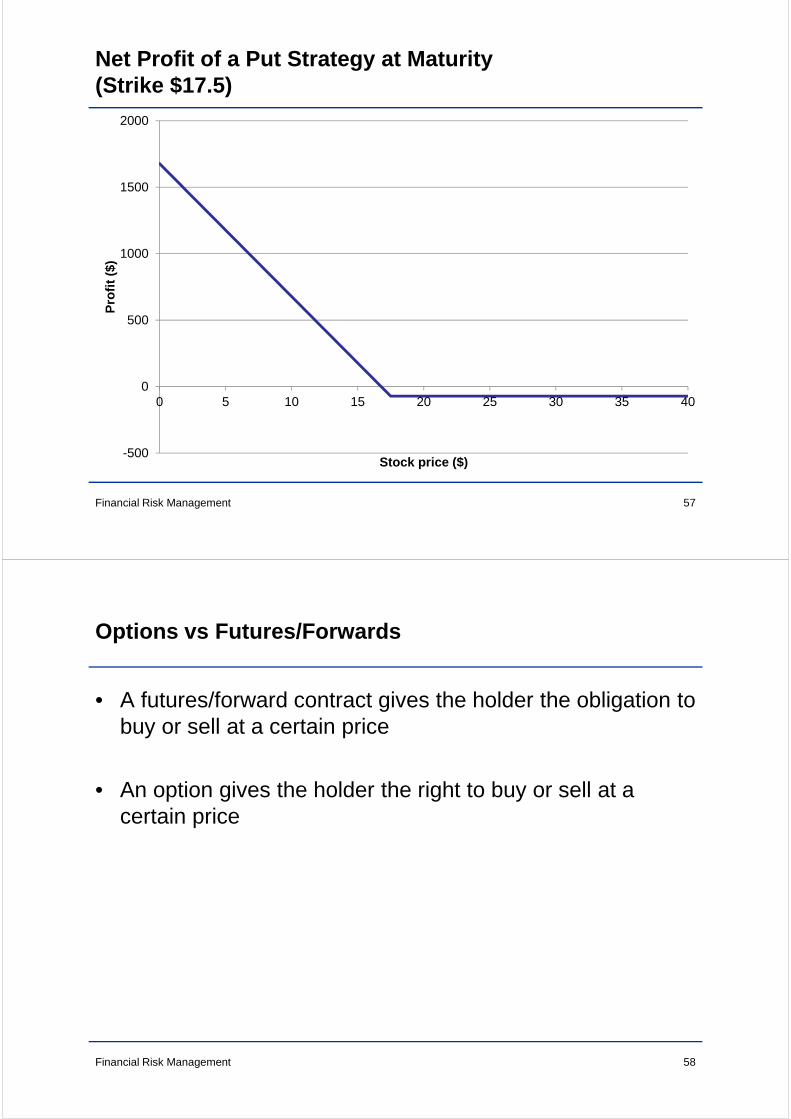

Net Profit of a Call Strategy at Maturity(Strike $20)

Financial Risk Management 56

-500

0

500

1000

1500

2000

0 5 10 15 20 25 30 35 40

Pro

fit

($)

Stock price ($)

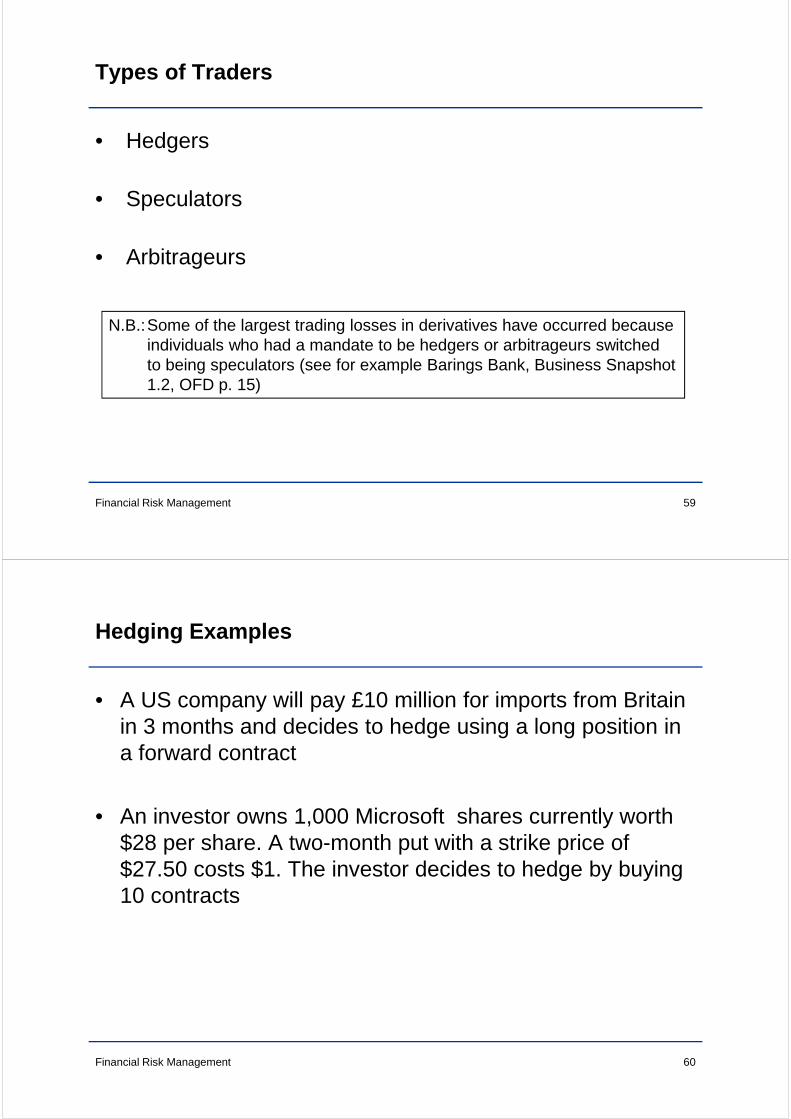

Net Profit of a Put Strategy at Maturity(Strike $17.5)

Financial Risk Management 57

-500

0

500

1000

1500

2000

0 5 10 15 20 25 30 35 40

Pro

fit

($)

Stock price ($)

Financial Risk Management 58

Options vs Futures/Forwards

• A futures/forward contract gives the holder the obligation to buy or sell at a certain price

• An option gives the holder the right to buy or sell at a certain price

Financial Risk Management 59

Types of Traders

• Hedgers

• Speculators

• Arbitrageurs

N.B.:Some of the largest trading losses in derivatives have occurred because individuals who had a mandate to be hedgers or arbitrageurs switched to being speculators (see for example Barings Bank, Business Snapshot 1.2, OFD p. 15)

Financial Risk Management 60

Hedging Examples

• A US company will pay £10 million for imports from Britain in 3 months and decides to hedge using a long position in a forward contract

• An investor owns 1,000 Microsoft shares currently worth $28 per share. A two-month put with a strike price of $27.50 costs $1. The investor decides to hedge by buying 10 contracts

Financial Risk Management 61

Value of Microsoft Shares With and Without Hedging

Financial Risk Management 62

Speculation Example

• An investor with $2,000 to invest feels that a stock price will increase over the next 2 months. The current stock price is $20 and the price of a 2-month call option with a strike of $22.50 is $1

• What are the alternative strategies?

Financial Risk Management 63

Arbitrage Example

• A stock price is quoted as £100 in London and $200 in New York

• The current exchange rate is 2.0300 $/£

• What is the arbitrage opportunity?

Accounting for Derivatives

• Ideally hedging profits (losses) should be recognized at the same time as the losses (profits) on the item being hedged

• Ideally profits and losses from speculation should be recognized on a mark-to-market basis

• Roughly speaking, this is what the accounting treatment of futures under U.S. GAAP and IFRS (and many other accounting frameworks) attempts to achieve

• EU: IAS 39 (financial instruments: recognition and measurement), to be superseded by IFRS 9 (issued Nov 2009, but not yet endorsed)

Financial Risk Management 64

Derivatives: The IFRS Perspective (here: IAS 39.9)

A derivative is a financial instrument or other contract within the scope of this standard (see paragraphs 2-7) with all three of the following characteristics:(a) its value changes in response to the change in a specified interest

rate, financial instrument price, commodity price, foreign exchange rate, index of prices or rates, credit rating or credit index, or other variable, provided in the case of a non-financial variable that the variable is not specific to a party to the contract (sometimes called the‘underlying’);

(b) it requires no initial net investment or an initial net investment that is smaller than would be required for other types of contracts that would be expected to have a similar response to changes in market factors; and

(c) it is settled at a future date.

Financial Risk Management 65

How to Account for Derivatives (IAS 39.9)

A financial asset or financial liability at fair value through profit or loss is a financial asset or financial liability that meets either of the following conditions.(a) It is classified as held for trading. A financial asset or financial liability

is classified as held for trading if it is:(i) acquired or incurred principally for the purpose of selling or

repurchasing it in the near term;(ii) part of a portfolio of identified financial instruments that are

managed together and for which there is evidence of a recent actual pattern of short-term profit-taking; or

(iii) a derivative (except for a derivative that is a financial guarantee contract or a designated and effective hedging instrument).

(b) (b) Upon initial recognition it is designated by the entity as at fair value through profit or loss.

Financial Risk Management 66

Hedge Accounting (IAS 39)

• Hedge accounting recognises the offsetting effects on profit or loss of changes in the fair values of the hedging instrument and the hedged item. (IAS 39.85)

• Definitions (IAS 39.9): – A hedging instrument is a designated derivative […] whose fair

value or cash flows are expected to offset changes in the fair value or cash flows of a designated hedged item […].

– A hedged item is an asset, liability, firm commitment, highly probable forecast transaction or net investment in a foreign operation that (a) exposes the entity to risk of changes in fair value or future cash flows and (b) is designated as being hedged […].

– Hedge effectiveness is the degree to which changes in the fair value or cash flows of the hedged item that are attributable to a hedged risk are offset by changes in the fair value or cash flows of the hedging instrument […].

Financial Risk Management 67

Embedded Derivatives (IAS 39.10 & 11)

39.10: An embedded derivative is a component of a hybrid (combined) instrument that also includes a non-derivative host contract — with the effect that some of the cash flows of the combined instrument vary in a way similar to a standalone derivative. […]

39.11: An embedded derivative shall be separated from the host contract and accounted for as a derivative under this standard if, and only if:(a) the economic characteristics and risks of the embedded derivative are

not closely related to the economic characteristics and risks of the host contract (see Appendix A paragraphs AG30 and AG33);

(b) a separate instrument with the same terms as the embedded derivative would meet the definition of a derivative; and

(c) the hybrid (combined) instrument is not measured at fair value with changes in fair value recognised in profit or loss (i.e. a derivative that is embedded in a financial asset or financial liability at fair value through profit or loss is not separated). […]

Financial Risk Management 68

Financial Risk Management 69

Recap Questions

1. Explain carefully the difference between hedging, speculation, and arbitrage.

2. Explain carefully the difference between selling a call option and buying a put option.

3. A trader enters into a short cotton futures contract when the futures price is 50 cents per pound. The contract is for the delivery of 50,000 pounds. How much does the trader gain or lose if the cotton price at the end of the contract is (a) 48.20 cents per pound and (b) 51.30 cents per pound?

4. What is the difference between the over-the-counter market an the exchange-traded market? What are the bid and offer quotes of a market maker in the over-the-counter market?

Financial Risk Management 70

Recap Questions

6. Suppose that a June put option to sell a share for $60 costs $4 and is held until June. Under what circumstances will the seller of the option (i.e., the party with the short position) make a profit? Under what circumstances will the option be exercised? Draw a diagram illustrating how the profit from a short position in the option depends on the stock price at maturity of the option.

7. Describe the profit from the following portfolio: a long forward contract on an asset and a long European put option on the asset with the same maturity as the forward contract and a strike price that is equal to the forward price of the asset at the time the portfolio is set up.

8. What are the main ideas underlying the accounting treatment of derivatives according to IAS 39? What does the term “hedge accounting” mean in this context?

Related Documents