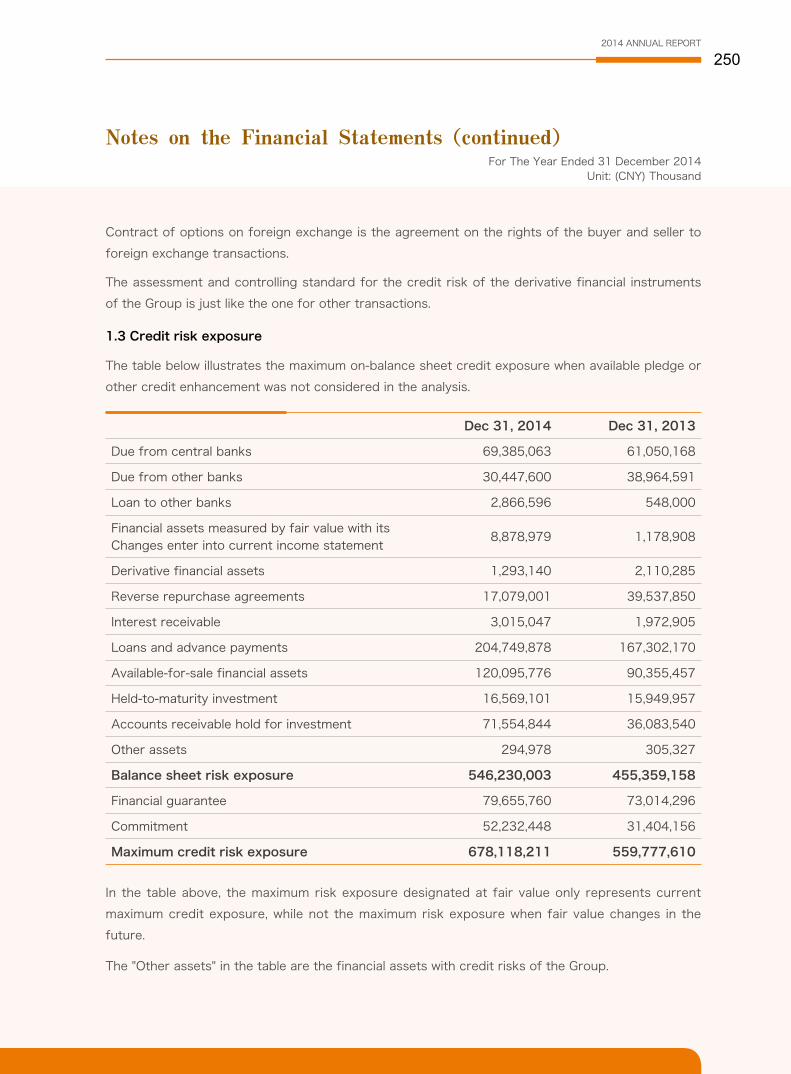

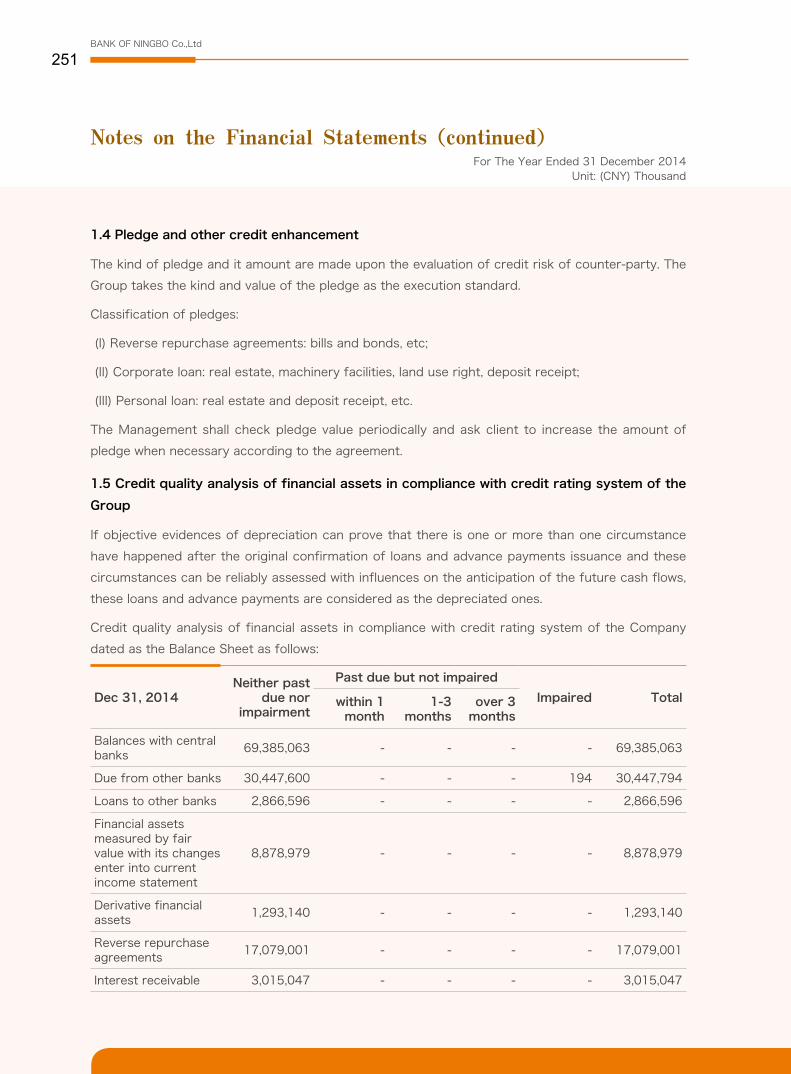

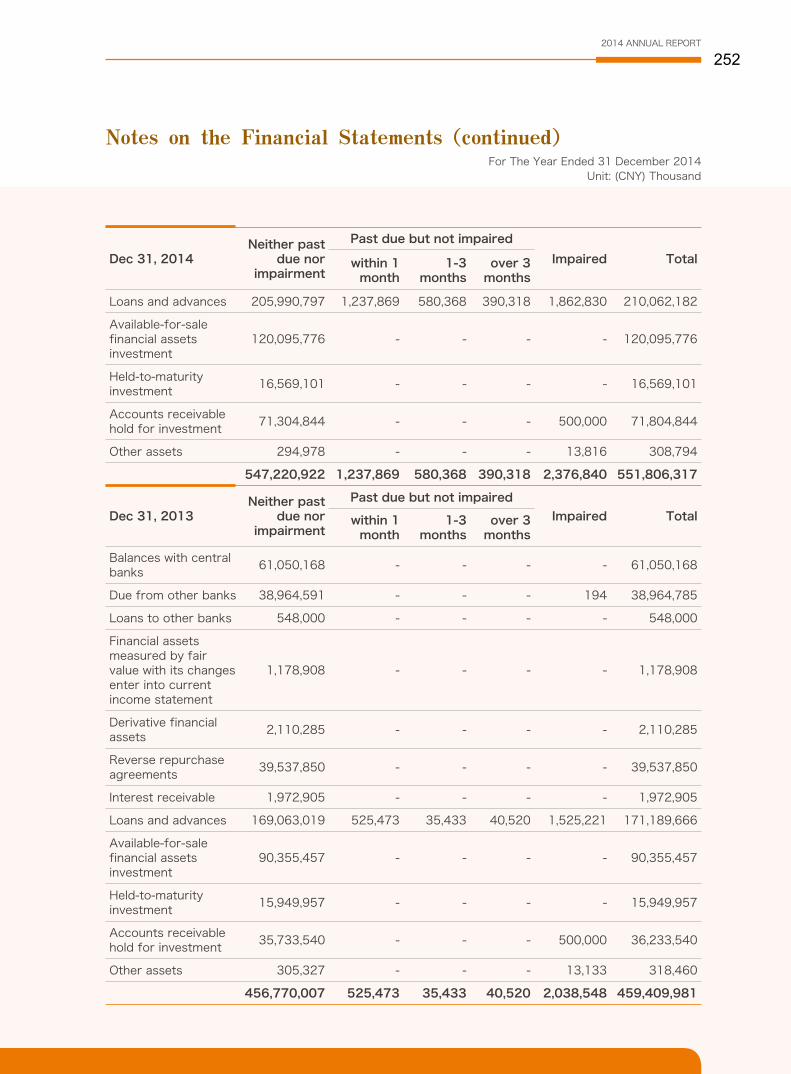

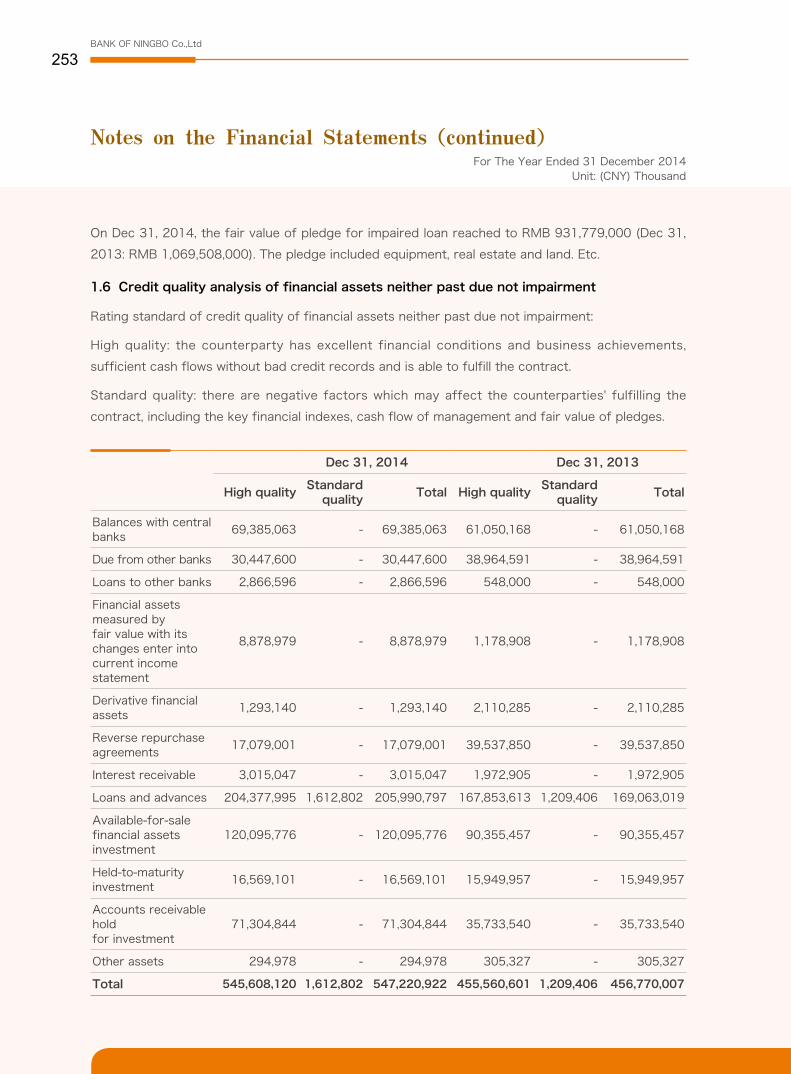

2014 ANNUAL REPORT 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2014 ANNUAL REPORT

1

BANK OF NINGBO Co.,Ltd

2

2014 ANNUAL REPORT

3

BANK OF NINGBO Co.,Ltd

1

The Board of Directors, Board of Supervisors, directors, supervisors and senior

managers of the Company ensure the authenticity, accuracy and completeness of

contents, and guarantee no fraulds, misleading statements or major omissions in this

report. They are willing to burden any individual and joint legal responsibilities.

All the directors, supervisors and senior managers are able to guarantee the

authenticity, accuracy and completeness of this report without any objection.

The 6th meeting of the 5th Board of Directors of the company approval the text and

abstract of 2014 Annual Report on 24 April 2015. 15 out of 17 directors were present.

Director Li Hanqiong authorize director Chen Guanghua to vote. Director Ben Shenglin

authorize director Zhu Jiandi to vote. Part of supervisors attended this meeting as well.

The Company's profit distribution plan was passed by the Board of Directors as

follows: taking the total share capital on 31 Dec. 2014 as the base number, cash bonus

of RMB 4.5 yuan (including tax) per 10 shares was distributed to all shareholders,

and 2 shares for every 10 shares were given by converting capital reserve into share

capital. This plan will be submitted to 2014 general meeting of stockholders for further

approval.

The Chairman of the board Mr. Lu Huayu, the president Mr. Luo Mengbo, the vice

president Mr. Luo Weikai, who is in charge of accounting, and the general manager

of accounting department Ms. Sun Hongbo hereby declare to pledge the authenticity,

accuracy and completeness of financial statements in the annual report.

Financial data and indicators included in this annual report are following the criterias of

the Chinese Accounting Standard for Business Enterprises. All data in the consolidated

financial statements of Bank of Ningbo Co., Ltd. and its subsidiary Yongying Fund

Management Co., Ltd. is subject to the unit of RMB except for further explanation.

Ernst & Young Hua Ming LLP audited the 2014 Financial Statements of the Company

in accordance with domestic accounting principles and signed off longtop's financial

statements.

The forward-looking statements in this annual report including future plans are not

commitments to investors. Thus please pay attention to investment risks.

Major risks

The company has described major risks and will adopt the measures to control risks.

For details, please refer to relevant contents about risk management in Sectoion Six

Report of the Board of Directors.

Chapter One Important Notes

2014 ANNUAL REPORT

2

Contents

Chapter One Important Notes ----------------------------------------------------- 001

Chapter Two Company Profile ---------------------------------------------------- 003

Chapter Three Highlights of Accounting Data and Financial Indicators ----- 008

Chapter Four Chairman's Statement --------------------------------------------- 013

Chapter Five President's Statement --------------------------------------------- 015

Chapter Six Report of the Board of Directors ------------------------------ 017

Chapter Seven Important Matters -------------------------------------------------- 085

Chapter Eight Changes in Share Capital and Shareholding --------------- 099

Chapter Nine Directors, Supervisors, Senior Manager and Basic

Information on Employees --------------------------------------- 111

Chapter Ten Corporate Governance -------------------------------------------- 131

Chapter Eleven Internal Control ------------------------------------------------------ 142

Chapter Twelve Financial Statements ---------------------------------------------- 154

Chapter Thirteen Catalogue ------------------------------------------------------------- 155

Chapter Fourteen Audited Financial Statement ------------------------------------ 156

BANK OF NINGBO Co.,Ltd

3

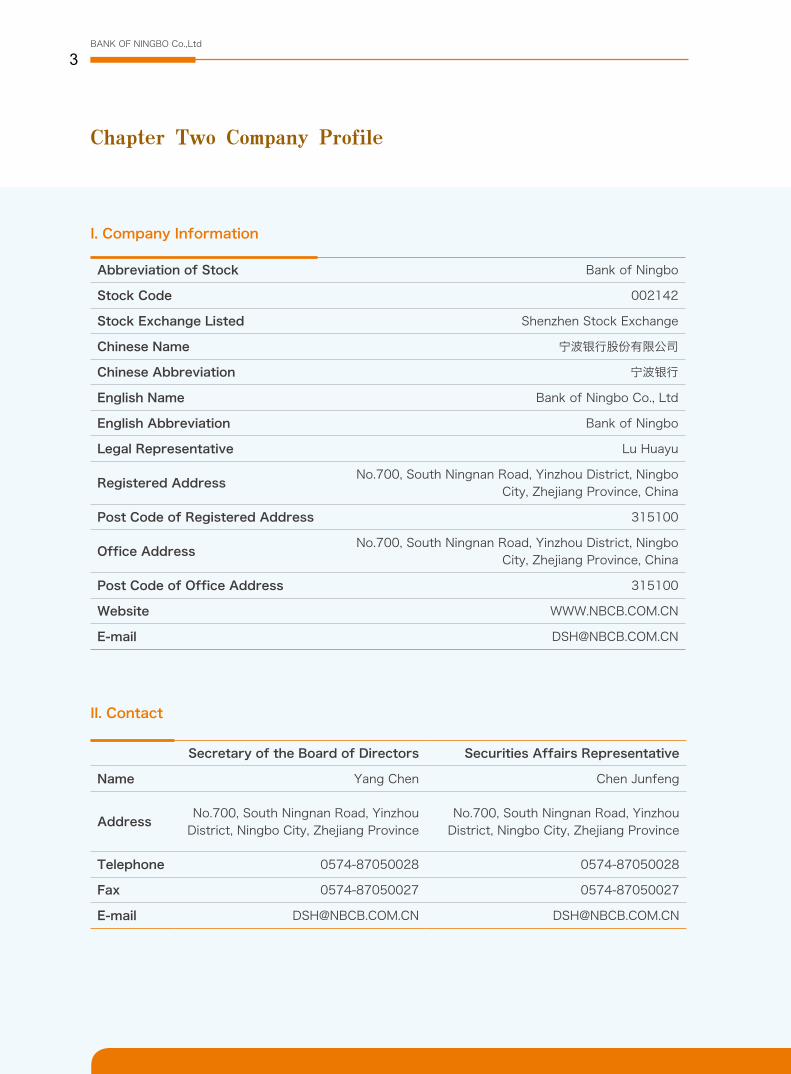

Chapter Two Company Profile

I. Company Information

II. Contact

Abbreviation of Stock Bank of Ningbo

Stock Code 002142

Stock Exchange Listed Shenzhen Stock Exchange

Chinese Name 宁波银行股份有限公司

Chinese Abbreviation 宁波银行

English Name Bank of Ningbo Co., Ltd

English Abbreviation Bank of Ningbo

Legal Representative Lu Huayu

Registered AddressNo.700, South Ningnan Road, Yinzhou District, Ningbo

City, Zhejiang Province, China

Post Code of Registered Address 315100

Office AddressNo.700, South Ningnan Road, Yinzhou District, Ningbo

City, Zhejiang Province, China

Post Code of Office Address 315100

Website WWW.NBCB.COM.CN

E-mail [email protected]

Secretary of the Board of Directors Securities Affairs Representative

Name Yang Chen Chen Junfeng

AddressNo.700, South Ningnan Road, Yinzhou

District, Ningbo City, Zhejiang ProvinceNo.700, South Ningnan Road, Yinzhou

District, Ningbo City, Zhejiang Province

Telephone 0574-87050028 0574-87050028

Fax 0574-87050027 0574-87050027

2014 ANNUAL REPORT

4

Chapter Two Company Profile(continued)

III. Information Disclosure and Place of Maintenance

IV. Registration Changes

V. Other Information

(I) Accounting firm appointed by the company

Newspaper Nominated by the Company for

information disclosureChina Securities Journal, Shanghai Securities

News, Securities Times and Securities Daily

Website Nominated by China Securities

Regulatory Commission (CSRC) for Anuual

Report Publishment

http://www.cninfo.com.cn

Place for Maintenance of the Annual ReportOffice of the Board of Directors of Bank of

Ningbo Co., Ltd.

Registration Date

Registration Place

Registration No. of Business License of Enterprise as

Legal Person

Tax Registration No.Organization

Code

Initial Registration

April 10th,

1997

Ningbo

Administrative

Bureau for

Industry and

Commerce

No.

330200400003994

G.S.Y.Z.NO.

330201711192037,

S.Y.D.Z. NO.

330204711192037

71119203-7

Changes of Main Business After Listing

None

Changes of Controlling Shareholdersin the Past

None

Name of Accounting Airm Ernst & Young Hua Ming LLP (Limited Liability Parternership )

Office Address of the Accounting Firm

Floor 50 of Shanghai World Financial Center, No.100, Century Avenue, Shanghai City

Signed Accountants Guo Hangxiang, Chen Sheng

BANK OF NINGBO Co.,Ltd

5

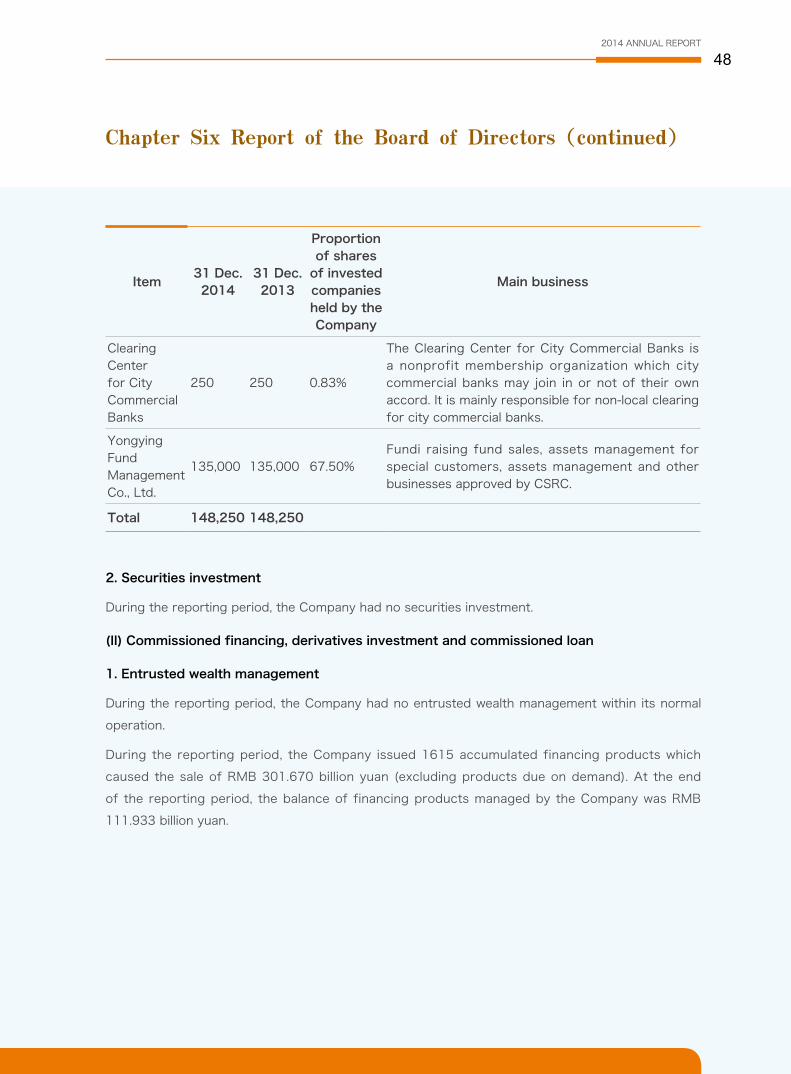

VI. Development Vision, Enterprise Culture and Investment Value

(I) Development Vision: to develop as a respected modern commercial bank with a good

reputation and core competitiveness

(II) Enterprise Culture: honesty and professionalism, compliance and efficiency, integration

and innovation

(III) Investment Value:

1. Adhere to the entry principle of "knowing the market and understanding the customers", insist on

creating eight profit centers, namely Cooperate Banking, Retail Banking, Personal Banking, Financial

Market, Credit Card Center, Bill Business, Investment Banking, Asset Custody, etc., so as to form a

diversified profit growth mode.

2. Adhere to the development strategy of "joint development of regional markets", continue to

promote unified actions between the head office、branches and sub-branches, comprehensively

design business procedures, and continuously enhance execution construction. The scale and profit

of branches have exceeded fifty percent, of the whole company, the scale and profit of Personal

Banking and Retail Company in Ningbo are increased to 50% as well.

Chapter Two Company Profile(continued)

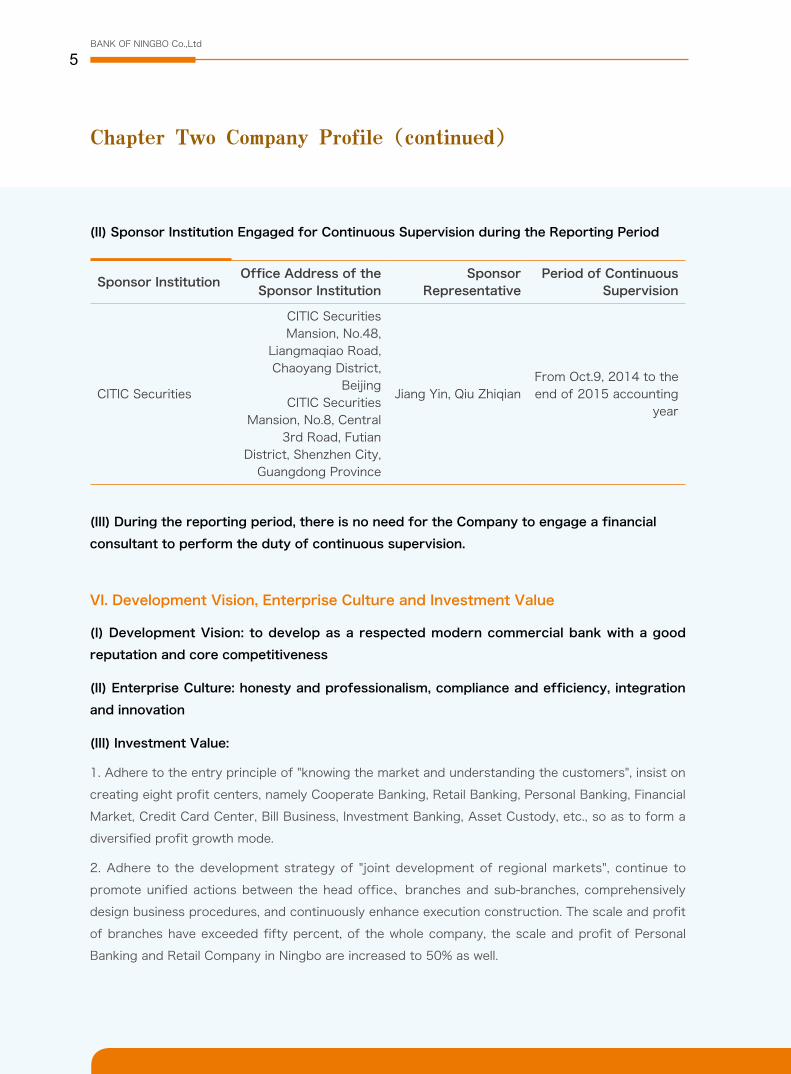

(II) Sponsor Institution Engaged for Continuous Supervision during the Reporting Period

(III) During the reporting period, there is no need for the Company to engage a financial

consultant to perform the duty of continuous supervision.

Sponsor InstitutionOffice Address of the

Sponsor InstitutionSponsor

RepresentativePeriod of Continuous

Supervision

CITIC Securities

CITIC Securities Mansion, No.48,

Liangmaqiao Road, Chaoyang District,

BeijingCITIC Securities

Mansion, No.8, Central 3rd Road, Futian

District, Shenzhen City, Guangdong Province

Jiang Yin, Qiu ZhiqianFrom Oct.9, 2014 to the end of 2015 accounting

year

2014 ANNUAL REPORT

6

Chapter Two Company Profile(continued)

3. Follow business aim of "being well-matched, serving small and medium-sized enterprises",

offer specialized financing service to customers; since the smooth running of Maxwealth Fund

Management Co., Ltd. which is dominated by the Company, Maxwealth Financial Leasing Co., Ltd.,

as company's wholly-owned subsidiary, is authorized. The means of services become more flexible,

while the range is widen.

4. Abide by the concept "reducing cost by controlling risk", build a full-process risk management

mode and a vertical independent credit approval system, strictly implement the five mechanisms for

prevention and continue to optimize compliance management, so as to keep asset quality at a good

level and to prevent various risks effectively.

VII. Major Awards and Rankings in 2014

(I) In January, 2014, "Best Small and Medium-Sized Commercial Bank" on the 2nd "Leading China"

Summit Forum of innovation and development in financial industry, which was jointly hold by JRJ.

com and PBC School of Finance in the Tsinghua University;

(II) In May, 2014, "2013 Best Small and Medium-Sized Corporate" in the 1st competition of listed

companies, organized by Sina Finance;

(III) In May, 2014, special award of the 3rd Ningbo "Top Ten Donation Enterprises" issued by the

Ningbo Charity Federation;

(IV) In June, the third place of "2013 Scientific and Technological Development Award" offered by

the Head Office of the People's Bank of China in the platform of company's medium and small-sized

enterprise online financing business project;

(V) In July, 2014, "2013 Best Jin Niu Investor Award" by China Securities Journal;

(VI) In July, 2014, on "the 2nd Jin Niu Financial Management Forum", the company and its products

were rewarded as "2013 Jin Niu Money Management Banking Award" and "2013 Jin Niu Products of

Money Management";

(VII) In September, 2014, the 2nd Outstanding Contribution Award of China Charity (company

award)" issued by the China Charity Federation;

(VIII) In September, 2014, in the list of "2014 Top 1000 International Banks" issued by the Banker,

the Company was ranked the 220th with about 4.165 billion U.S. dollars tier-I capital;

BANK OF NINGBO Co.,Ltd

7

Chapter Two Company Profile(continued)

(IX) In September, 2014, in the list of "2014 Top 500 International Banks" issued by the Banker, the

Company was ranked the 264th and rated as A+;

(X) In December, 2014, the Company was rated as Baa2 by Moody, the same as famous national

commercial banks;

(XI) In January, 2015, "The Most Influential Award in 2014"and "The Best Derivatives Transaction

Award in 2014" in domestic currency market between banks, which were issued by the China

Foreign Exchange Trade System(CFETS); transaction supervisors and traders were respectively

rewarded by the titles of "Excellent Transaction Supervisor" and "Excellent Trader".

2014 ANNUAL REPORT

8

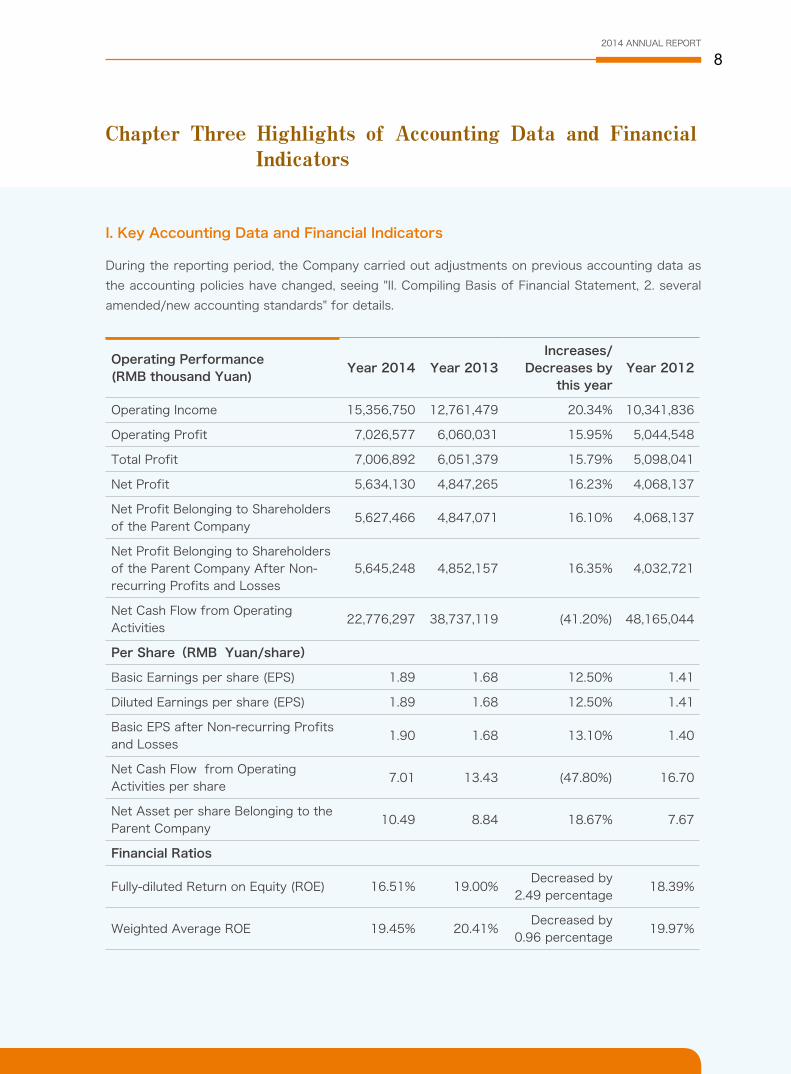

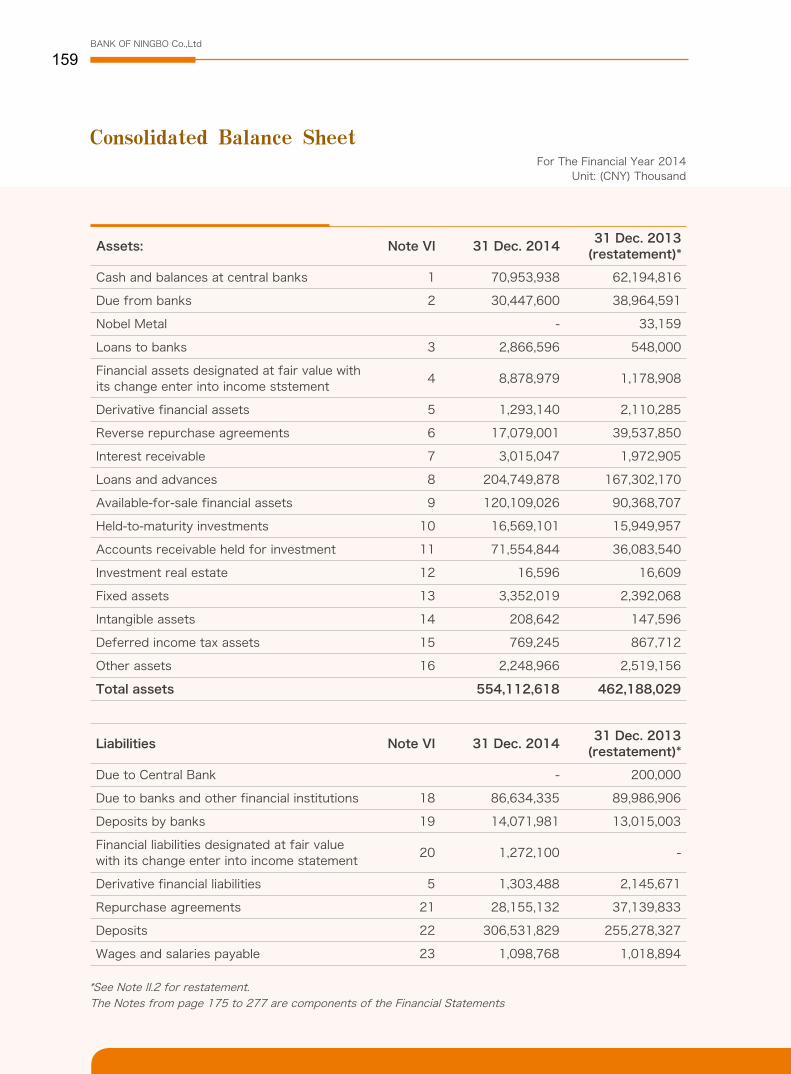

Chapter Three Highlights of Accounting Data and Financial Indicators

I. Key Accounting Data and Financial Indicators

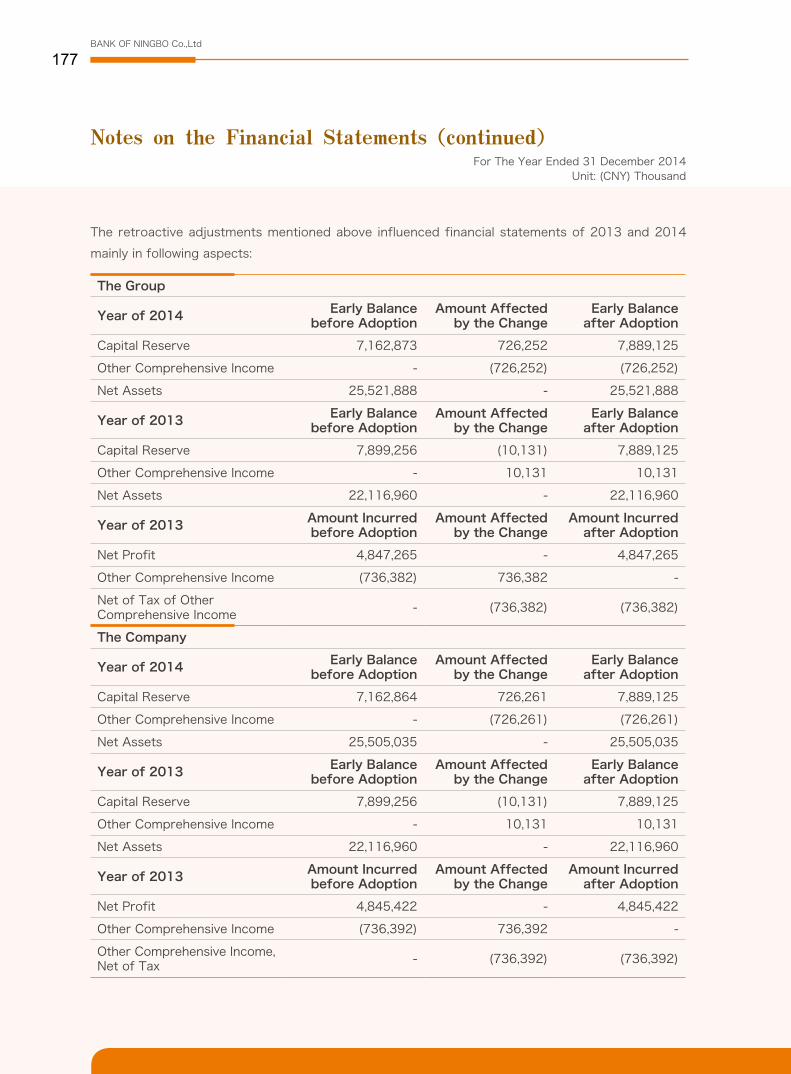

During the reporting period, the Company carried out adjustments on previous accounting data as

the accounting policies have changed, seeing "II. Compiling Basis of Financial Statement, 2. several

amended/new accounting standards" for details.

Operating Performance(RMB thousand Yuan)

Year 2014 Year 2013Increases/

Decreases by this year

Year 2012

Operating Income 15,356,750 12,761,479 20.34% 10,341,836

Operating Profit 7,026,577 6,060,031 15.95% 5,044,548

Total Profit 7,006,892 6,051,379 15.79% 5,098,041

Net Profit 5,634,130 4,847,265 16.23% 4,068,137

Net Profit Belonging to Shareholders of the Parent Company

5,627,466 4,847,071 16.10% 4,068,137

Net Profit Belonging to Shareholders of the Parent Company After Non-recurring Profits and Losses

5,645,248 4,852,157 16.35% 4,032,721

Net Cash Flow from Operating Activities

22,776,297 38,737,119 (41.20%) 48,165,044

Per Share(RMB Yuan/share)

Basic Earnings per share (EPS) 1.89 1.68 12.50% 1.41

Diluted Earnings per share (EPS) 1.89 1.68 12.50% 1.41

Basic EPS after Non-recurring Profits and Losses

1.90 1.68 13.10% 1.40

Net Cash Flow from Operating Activities per share

7.01 13.43 (47.80%) 16.70

Net Asset per share Belonging to the Parent Company

10.49 8.84 18.67% 7.67

Financial Ratios

Fully-diluted Return on Equity (ROE) 16.51% 19.00%Decreased by

2.49 percentage 18.39%

Weighted Average ROE 19.45% 20.41%Decreased by

0.96 percentage 19.97%

BANK OF NINGBO Co.,Ltd

9

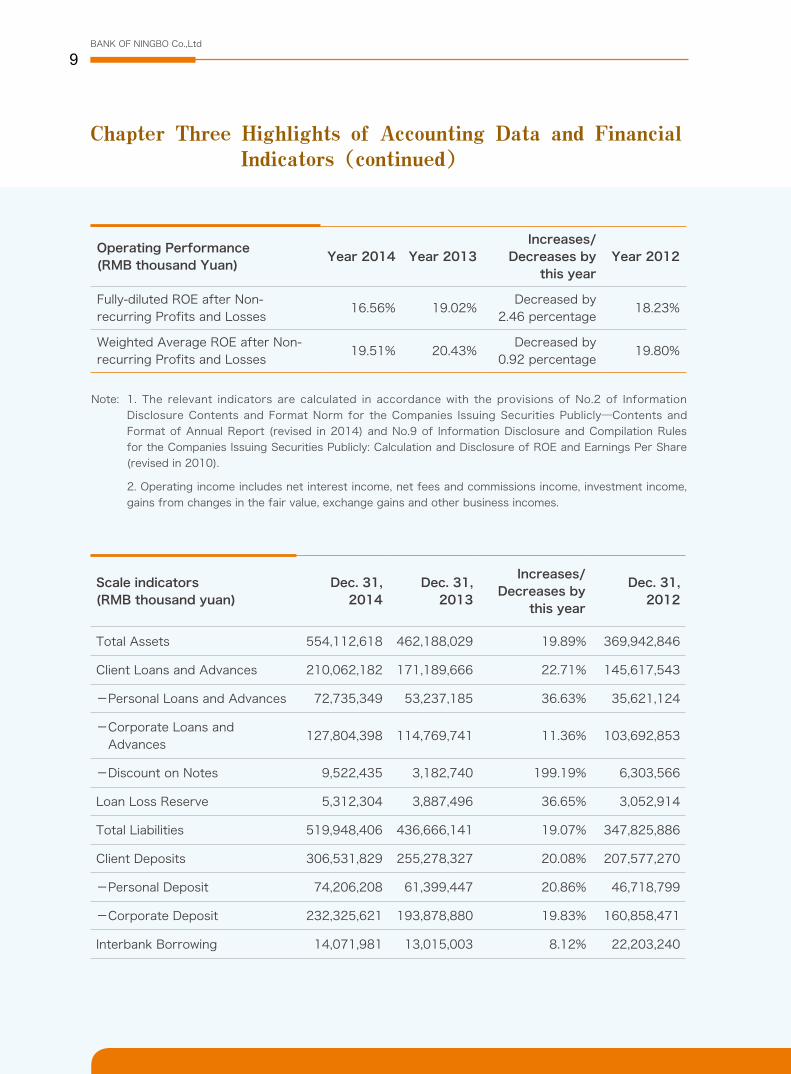

Operating Performance(RMB thousand Yuan)

Year 2014 Year 2013Increases/

Decreases by this year

Year 2012

Fully-diluted ROE after Non-recurring Profits and Losses

16.56% 19.02%Decreased by

2.46 percentage18.23%

Weighted Average ROE after Non-recurring Profits and Losses

19.51% 20.43%Decreased by

0.92 percentage19.80%

1. The relevant indicators are calculated in accordance with the provisions of No.2 of Information Disclosure Contents and Format Norm for the Companies Issuing Securities Publicly—Contents and Format of Annual Report (revised in 2014) and No.9 of Information Disclosure and Compilation Rules for the Companies Issuing Securities Publicly: Calculation and Disclosure of ROE and Earnings Per Share (revised in 2010).

2. Operating income includes net interest income, net fees and commissions income, investment income, gains from changes in the fair value, exchange gains and other business incomes.

Note:

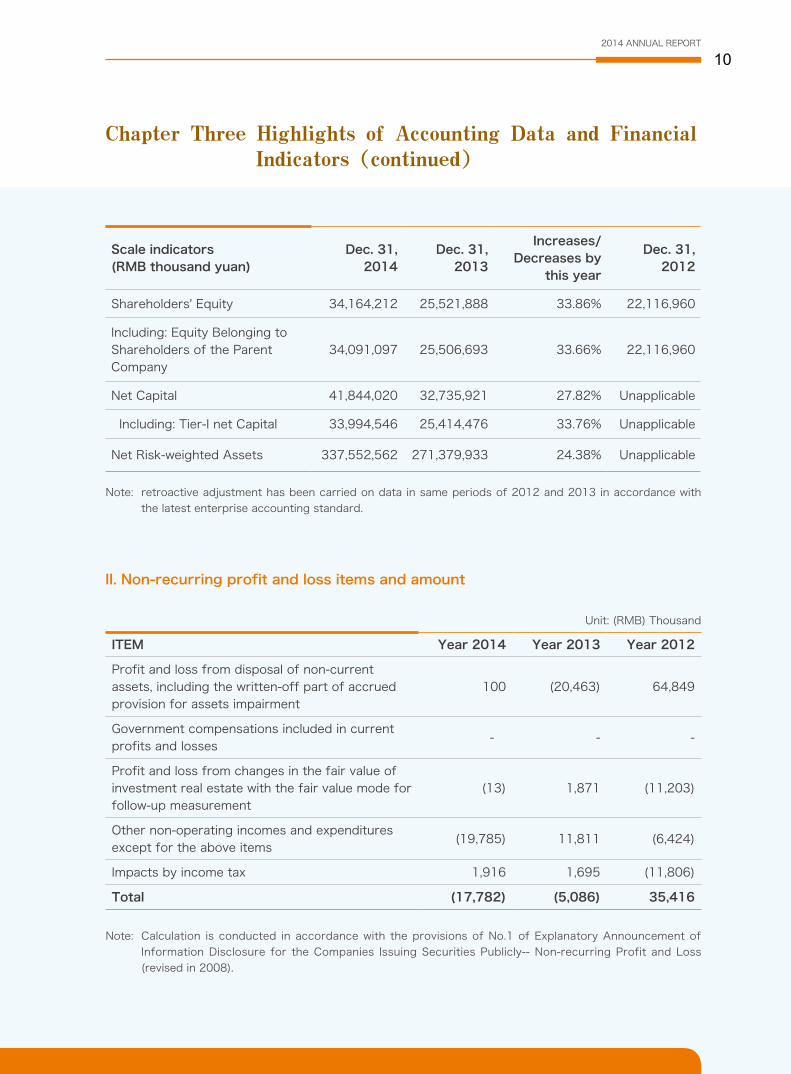

Scale indicators(RMB thousand yuan)

Dec. 31, 2014

Dec. 31, 2013

Increases/Decreases by

this year

Dec. 31, 2012

Total Assets 554,112,618 462,188,029 19.89% 369,942,846

Client Loans and Advances 210,062,182 171,189,666 22.71% 145,617,543

-Personal Loans and Advances 72,735,349 53,237,185 36.63% 35,621,124

-Corporate Loans and Advances

127,804,398 114,769,741 11.36% 103,692,853

-Discount on Notes 9,522,435 3,182,740 199.19% 6,303,566

Loan Loss Reserve 5,312,304 3,887,496 36.65% 3,052,914

Total Liabilities 519,948,406 436,666,141 19.07% 347,825,886

Client Deposits 306,531,829 255,278,327 20.08% 207,577,270

-Personal Deposit 74,206,208 61,399,447 20.86% 46,718,799

-Corporate Deposit 232,325,621 193,878,880 19.83% 160,858,471

Interbank Borrowing 14,071,981 13,015,003 8.12% 22,203,240

Chapter Three Highlights of Accounting Data and Financial Indicators(continued)

2014 ANNUAL REPORT

10

Scale indicators(RMB thousand yuan)

Dec. 31, 2014

Dec. 31, 2013

Increases/Decreases by

this year

Dec. 31, 2012

Shareholders' Equity 34,164,212 25,521,888 33.86% 22,116,960

Including: Equity Belonging to Shareholders of the Parent Company

34,091,097 25,506,693 33.66% 22,116,960

Net Capital 41,844,020 32,735,921 27.82% Unapplicable

Including: Tier-I net Capital 33,994,546 25,414,476 33.76% Unapplicable

Net Risk-weighted Assets 337,552,562 271,379,933 24.38% Unapplicable

retroactive adjustment has been carried on data in same periods of 2012 and 2013 in accordance with the latest enterprise accounting standard.

Calculation is conducted in accordance with the provisions of No.1 of Explanatory Announcement of Information Disclosure for the Companies Issuing Securities Publicly-- Non-recurring Profit and Loss (revised in 2008).

Note:

Note:

II. Non-recurring profit and loss items and amount

ITEM Year 2014 Year 2013 Year 2012

Profit and loss from disposal of non-current assets, including the written-off part of accrued provision for assets impairment

100 (20,463) 64,849

Government compensations included in current profits and losses

- - -

Profit and loss from changes in the fair value of investment real estate with the fair value mode for follow-up measurement

(13) 1,871 (11,203)

Other non-operating incomes and expenditures except for the above items

(19,785) 11,811 (6,424)

Impacts by income tax 1,916 1,695 (11,806)

Total (17,782) (5,086) 35,416

Unit: (RMB) Thousand

Chapter Three Highlights of Accounting Data and Financial Indicators(continued)

BANK OF NINGBO Co.,Ltd

11

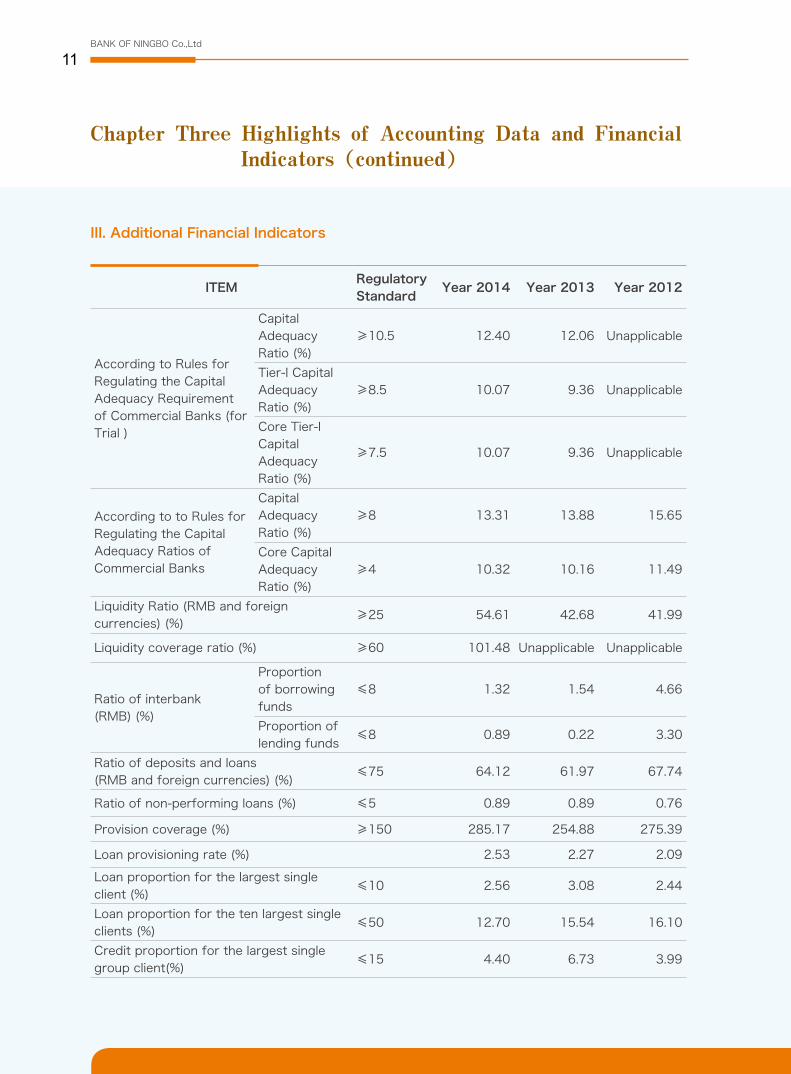

III. Additional Financial Indicators

ITEMRegulatory Standard

Year 2014 Year 2013 Year 2012

According to Rules for Regulating the Capital Adequacy Requirement of Commercial Banks (for Trial )

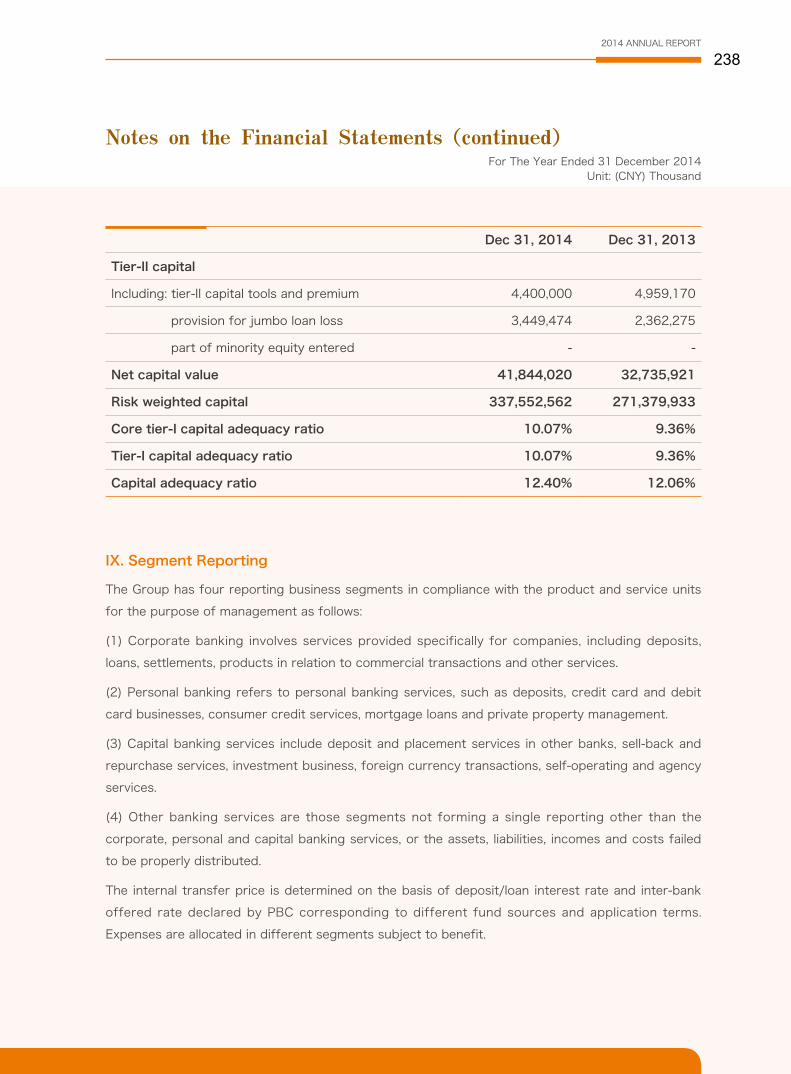

CapitalAdequacyRatio (%)

≥10.5 12.40 12.06 Unapplicable

Tier-I CapitalAdequacyRatio (%)

≥8.5 10.07 9.36 Unapplicable

Core Tier-I Capital AdequacyRatio (%)

≥7.5 10.07 9.36 Unapplicable

According to to Rules for Regulating the Capital Adequacy Ratios of Commercial Banks

Capital Adequacy Ratio (%)

≥8 13.31 13.88 15.65

Core Capital Adequacy Ratio (%)

≥4 10.32 10.16 11.49

Liquidity Ratio (RMB and foreign currencies) (%)

≥25 54.61 42.68 41.99

Liquidity coverage ratio (%) ≥60 101.48 Unapplicable Unapplicable

Ratio of interbank(RMB) (%)

Proportion of borrowing funds

≤8 1.32 1.54 4.66

Proportion of lending funds

≤8 0.89 0.22 3.30

Ratio of deposits and loans(RMB and foreign currencies) (%)

≤75 64.12 61.97 67.74

Ratio of non-performing loans (%) ≤5 0.89 0.89 0.76

Provision coverage (%) ≥150 285.17 254.88 275.39

Loan provisioning rate (%) 2.53 2.27 2.09

Loan proportion for the largest single client (%)

≤10 2.56 3.08 2.44

Loan proportion for the ten largest single clients (%)

≤50 12.70 15.54 16.10

Credit proportion for the largest single group client(%)

≤15 4.40 6.73 3.99

Chapter Three Highlights of Accounting Data and Financial Indicators(continued)

2014 ANNUAL REPORT

12

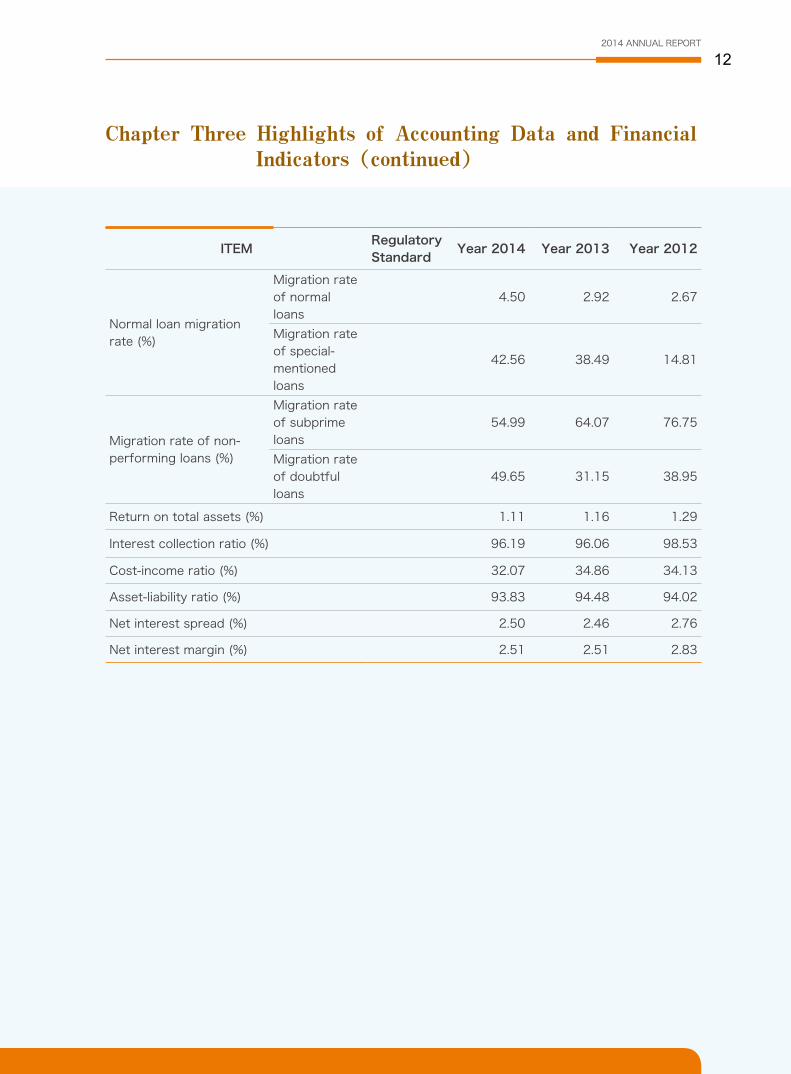

ITEMRegulatory Standard

Year 2014 Year 2013 Year 2012

Normal loan migration rate (%)

Migration rate of normal loans

4.50 2.92 2.67

Migration rate of special-mentioned loans

42.56 38.49 14.81

Migration rate of non-performing loans (%)

Migration rate of subprime loans

54.99 64.07 76.75

Migration rate of doubtful loans

49.65 31.15 38.95

Return on total assets (%) 1.11 1.16 1.29

Interest collection ratio (%) 96.19 96.06 98.53

Cost-income ratio (%) 32.07 34.86 34.13

Asset-liability ratio (%) 93.83 94.48 94.02

Net interest spread (%) 2.50 2.46 2.76

Net interest margin (%) 2.51 2.51 2.83

Chapter Three Highlights of Accounting Data and Financial Indicators(continued)

BANK OF NINGBO Co.,Ltd

13

In 2014, as the world economic recovery remained shakily, Chinese economy, though relatively in

a high growth rate, was confronted with emerging structural contradictions and decreasing. The

banking industry faced a new era in financial evolution. However, as the marketization of interest

rates accelerating, the internet financing emerging, regulatory policies becoming rigorous, and

competition in the industry intensifying, banking industry is facing a more complex business

environment.

Facing the new situation and new challenge, the Company persisted in the concept of"prudent

operation and stable development". It actively seized market opportunities, accelerated the

promotion of operational transformation, continued to advance the construction of profit centers,

comprehensively enhanced risk control capacity and gradually improved management quality and

competitiveness. Up to Dec.31st, 2014, the Company had a total asset of 554.113 billion Yuan and

realized the annual net profit of 5.627 billion yuan attributed to the equity shareholders of the

parent company, up by 16.10% compared to the previous year. It owned 246 operating institutions,

increasing by 37 since the beginning of the year, It, thus effectively meets the requirements of

sustainable development of the Company.

We continued to optimize business structure. The Company had established a business mode

with eight profit centers cooperated, namely Corporate Banking, Retail Banking, Personal Banking,

Financial Market, Credit Card, Bill Business, Investment Banking and Asset Custody, and had gradually

changed the traditional profit growth pattern by a high spread between lending and deposit rates.

Under the cooperation between the head office, branches and sub-branches, the development

dynamics was more balanced, diversified businesses in branches were steadily promoted. Scale and

profit of branches have occupied more than half of them in the whole Company. The operation in

Ningbo had transformed successfully, as Retail Banking increased its proportion to 50% in terms of

scale and profit, which formed an endogenous development mechanism.

We continued to advance our quality of services. The Company always adheres to the fundamental

point of providing more diversified products and more efficient services. As Yongying Fund

Management Co., Ltd. was successfully established, in 2014, Yongying Financial Leasing Co., Ltd., as

wholly-owned subsidiary of the Company, was prepared to construct, signifying that the Company

initiated its integrated operation and the channel for customer service stretched out continuously.

Meanwhile, banking project of operation process was started on time and "financial factory" type

of medium and background service supporting system was established formally, so that working

procedures had been effectively shortened, efficiency had been continuously improved and good

customer reputation of Bank of Ningbo in the market had been built.

We withstood the test of risk management. The Company held the principle of "Risk control is cost

reduction". We improved the overall risk management system, and structured the comprehensive

Chapter Four Chairman's Statement

2014 ANNUAL REPORT

14

Chapter Four Chairman's Statement(continued)

Chairman:

risk management system which covered credit risk, market risk, operational risk, moral risk, legal

risk and reputation risk. The Company implemented vertical and independent credit approval

system to effectively avoid industrial and regional risks. It had made substantial progress in new

capital accord project, with risk monitoring and control means enriched gradually. In September

2014, the Company successfully completed Secondly Public Offering and new capital about 3.1

billion yuan was increased, so that the capital of the Company was more sufficient and the capacity

of withstanding risk was significantly enhanced.

We paid more attention to technological innovation. The Company always take the improvement

of technological competitiveness as a priority. By enhancing systematic construction and software

development, stronger support for the development of business had been offered. In 2014, the

Company improved corporate e-banking and personal e-banking functions, developed different

versions of mobile banking for all mainstream operating systems, and updated the construction

of e-channel. It successfully implemented direct sales banking and Wechat banking, and kept up

the space of the industry in the business model transformation. The Company carried out the

construction of IT system groups, successfully implemented many core business systems. The

Company was ranked to the first place among other banks, in terms of surveillance of informational

technology, which was hold by CBRC.

We continued to create brand image. The Company always held the social responsibility of "equality

& honesty, sincerity for customers, caring employees, creating public benefit, participation in

environmental protection, rewards to the society". It binded operation/management and social

responsibility closely, which improved its brand popularity and social reputation. In 2014, the famous

rating agency Moody rated the Company at the Baa2 level; among top 1000 banks global , the

Company was ranked 220 by Banker referring to the tier-1 capital It received dozens of rewards,

including "Best Medium- and Small-sized Company" by Sina Finance, and "the Most Trustworthy

Bank" by Investor's Journal.

2015 is a year when Chinese economic structure is till in deep adjustment. Pressures from profit

growth and non-performing prevention and control in banking industry are still high. For these

opportunities and challenges, the Company will always persist in the principle of "prudent operation

and stable development", working hard and skillfully created more products, better service and

better performance, so as to reward shareholders, customers and the society for your trust and

support.

BANK OF NINGBO Co.,Ltd

15

Chapter Five President's Statement

In 2014, despite unsatisfactory economic situation, the Company carefully carried out various

decisions made by the board of directors, and focused on working objectives of "expanding profit

channel, updating marketing mode, strictly controlling non-performing assets and accelerating

talent training", which were specified at the beginning of the year. It operated carefully and

developed steadily so as to better achieve dynamic balance among benefit, quality and scale, and

various business indicators made at the beginning of the year were well completed. Up to Dec.31st ,

2014, the Company reached its total asset to 554. 113 billion yuan, up by 19.89% compared to that

at the beginning of the year; net profit attributed to the equity shareholders of the parent company

was 5.627 billion yuan, up by 16.10% compared to that in the same period of last year; basic EPS is

1.89 yuan, up by 0.21 yuan during the same period; non-performing loan rate is 0.89%, flush with

that at the beginning of the year; loan provision rate is 2.53%, up by 0.26% compared to that at the

beginning of the year.

In 2014, confronted with economic slowdown and intensified competition in the industry, the

Company further strengthened the construction of eight profit centers, expanded the product

system and extended business lines, which remarkably improved the customer service level and the

integrated income level. Moreover, for these opportunities and challenges, the Company developed

intermediate business in terms of bills, investment banking and custody, and effectively explored

new profit growth points. It also actively followed economic development trend, and regulated

credit structure so that the credit resource was contributed to those state encouraged and

supported real economy, high-end manufacturing industry, modern service industry and medium-

and small-sized enterprises. Thus steady growth in profit was realized.

In 2014, facing severe challenges of asset quality in banking industry, the Company firmly

promoted full-process risk management system and enhanced risk pre-management by virtue of

front, medium and background efficient linkage, so as to help customer achieve "early discovering,

early warning and early processing" towards risk. It paid close attention to the change of macro-

economic situation, inspected and eliminated risks timely and actively adjusted credit structure, so

that a batch of risk loans were effectively avoided. The Company promoted new capital accord, and

successfully launched such sub-projects as non-retail credit risk exposure modeling, retail credit risk

exposure modeling and data governance. In 2014, the risk management capacity of the Company

had passed the market test. Despite that major business regions were still engaged in absorbing

excess capacity and significant adjustment of economic structure, the asset quality was kept at a

good level.

In 2014, the Company successfully developed and listed several system, including the second

-generation payment, phase II comprehensive financial platform, asset custody, and Yinguantong

etc, so that a more efficient business supporting system was constructed for sustainable

2014 ANNUAL REPORT

16

Chapter Five President's Statement(continued)

President:

development of the bank. Adhering to the trend of internet finance, the Company launched direct

sales banking, Wechat banking, corporate e-banking 5.0, personal e-banking 5.0 and mobile banking

3.0, so that the quality of business e-channel was greatly improved. After years of persistent efforts,

the technological system construction and software development capacities of the Company were

significantly improved, and the superiority in similar banks appeared gradually.

In 2014, carried by process innovation projects, the Company found problems and crucial reasons

in the frontline of handling business, comprehensively advanced various business processes and

had completed 20 process innovation projects, so that redundant procedures were effectively

reduced and handling efficiency was improved. The Company insisted on outstanding service

concept, strengthened the idea of focusing service details, and developed special theme activities in

accordance with the characteristics of mainstream customers of sales networks, so as to enhance

interaction with customers and comprehensively improve customer experience in those customer

activities.

In 2015, the Company will carry on the spirit of "industriousness for three years" and centered on

four prior work: "expanding profitability channels, upgrading marketing modes, controlling non-

performing assets and speeding up talents fostering" under the leadership of the board of director.

It will define goals, insist on direct, continuously improve work methods, reasonably master dynamic

balance between risk management and business development, accumulate comparative advantages,

and reward shareholders and the society with excellent performance and professional financial

services.

BANK OF NINGBO Co.,Ltd

17

Chapter Six Report of the Board of Directors

I. Analysis on operations in 2014

(I) General overview

In 2014, the Company closely adhered to work line of "expanding profitability channels, upgrading

marketing modes, controlling non-performing assets and speeding up training of talents" made at

the beginning of the year, continued to optimise construction of eight profit centers, effectively

improved risk management capacity and continuously enhanced linkage between the head office

and the branches, so that various businesses were smoothly implemented, asset quality was further

improved and profitability was continuously improved. Main performances were as follows:

1. Steady growth of asset scale and coordinated development of various businesses

As of Dec.31, 2014, the total assets of the Company were RMB 554.113 billion yuan, increasing by

RMB 91.925 billion yuan compared with that on Dec. 31, 2013 and up by 19.89%; the deposits were

RMB 306.532 billion yuan, increasing by RMB 51.254 billion yuan compared with that on Dec. 31,

2013 and up by 20.08%; the loans were RMB 210.062 billion yuan, increasing by RMB 38.873 billion

yuan compared with that on Dec. 31, 2013 and up by 22.71%.

2. Profitability was gradually improved and business structure was continuously optimized

In 2014, the operating income of the Company was RMB 15.357 billion yuan, increasing by RMB

2.595 billion yuan year-on-year with a growth rate of 20.34%; the operating profit was RMB 7.027

billion yuan, increasing by RMB 0.967 billion yuan year-on-year with a growth rate of 15.95%; the

net profit attributable to the parent company was RMB 5.627 billion yuan, increasing by RMB 780

million yuan year-on-year with a growth rate of 16.10%; net fee and commission income was RMB

2.485 billion yuan, accounting for 16.18% of operating income, up by 3.49 pecent points, realizing

continuous optimization of business structure; in 2014, with non-public offering, the weighted

average net assets return ratio was 19.45%, down by 0.96 percent points; basic EPS (earnings per

share) is RMB 1.89 yuan, up by RMB 0.21 yuan.

3. Asset quality was remained stable and ability of resisting risk was enhanced

At the end of Dec. 31, 2014, NPL ratio of the Company was 0.89%, flush with that on Dec. 31,

2013; the provision coverage was 2.53%, up by 0.26 percentage points compared with that on Dec.

31, 2013. The Company kept the good quality of assets.

4. Continuously promotion of capital supplement and improvement of capital adequacy level

During the reporting period, the Company had completed non-public offering; up to Dec. 31, 2014,

the capital adequacy ratio (calculated according to "Administrative Measures for the Capital of

Commercial Banks (for Trial Implementation)") is 12.40%, up by 0.34 percentage points compared

2014 ANNUAL REPORT

18

with that on Dec. 31, 2013. The core tier-I capital adequacy ratio was 10.07% and the tier-I capital

adequacy ratio was 10.07% as well, up by 0.71 percentage points compared with that on Dec. 31,

2013.

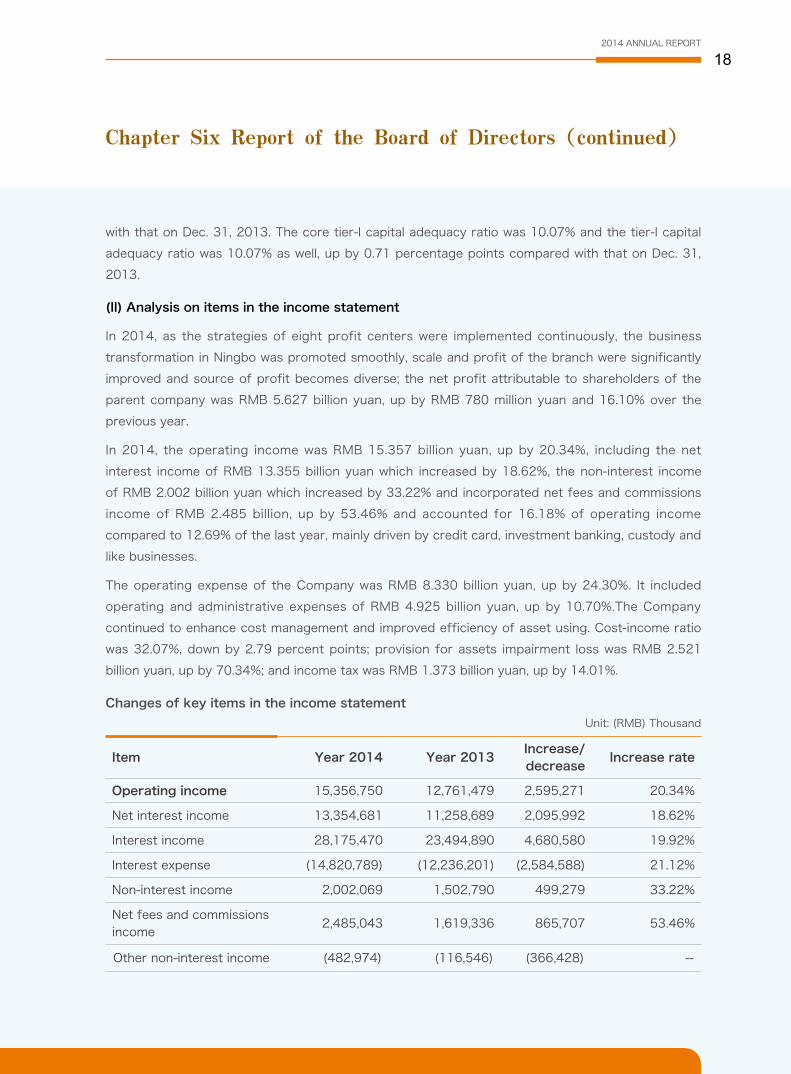

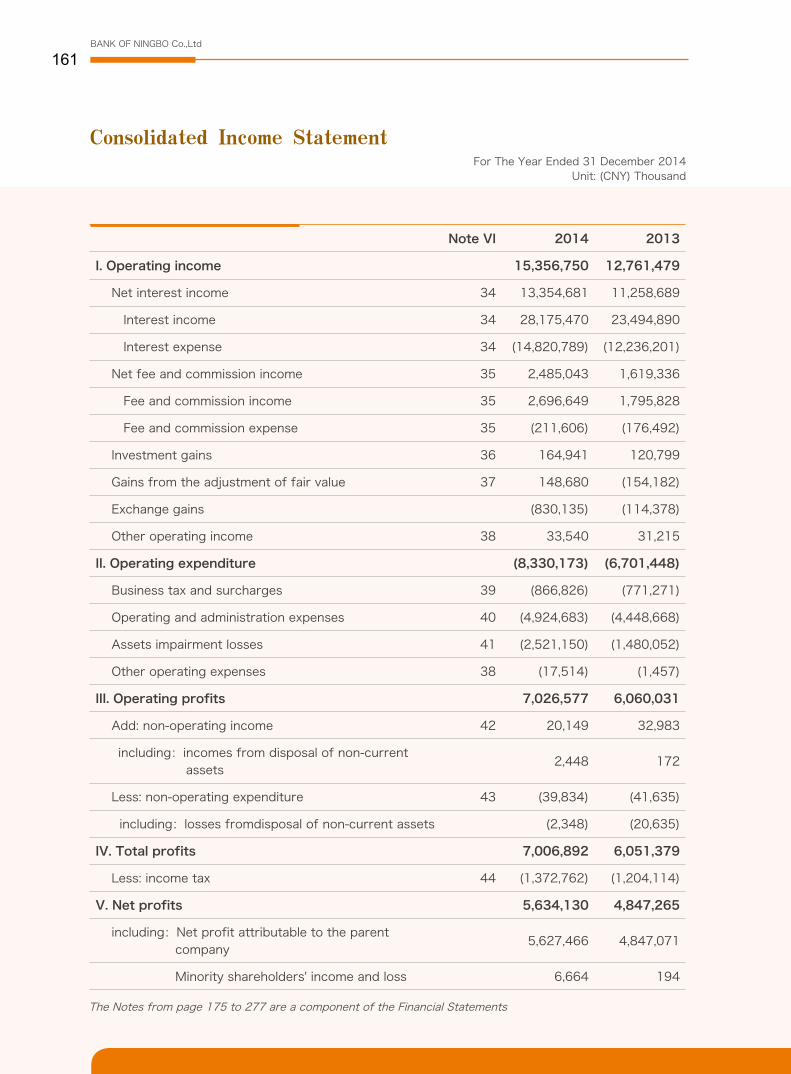

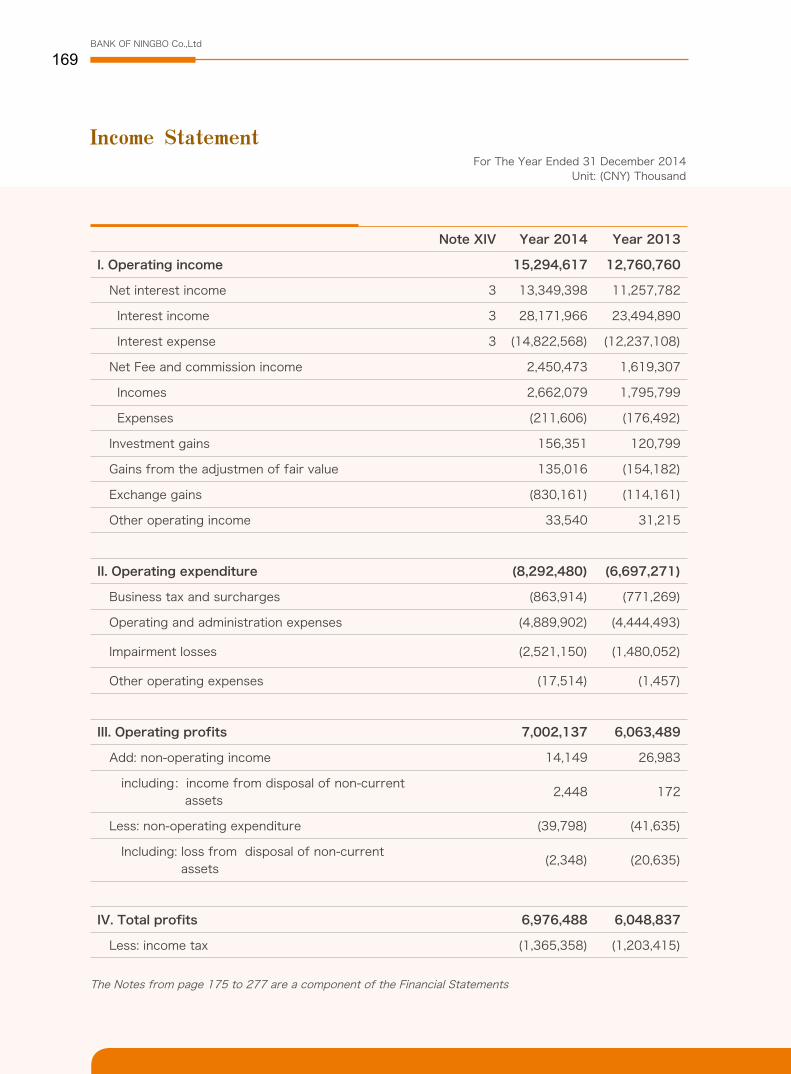

(II) Analysis on items in the income statement

In 2014, as the strategies of eight profit centers were implemented continuously, the business

transformation in Ningbo was promoted smoothly, scale and profit of the branch were significantly

improved and source of profit becomes diverse; the net profit attributable to shareholders of the

parent company was RMB 5.627 billion yuan, up by RMB 780 million yuan and 16.10% over the

previous year.

In 2014, the operating income was RMB 15.357 billion yuan, up by 20.34%, including the net

interest income of RMB 13.355 billion yuan which increased by 18.62%, the non-interest income

of RMB 2.002 billion yuan which increased by 33.22% and incorporated net fees and commissions

income of RMB 2.485 billion, up by 53.46% and accounted for 16.18% of operating income

compared to 12.69% of the last year, mainly driven by credit card, investment banking, custody and

like businesses.

The operating expense of the Company was RMB 8.330 billion yuan, up by 24.30%. It included

operating and administrative expenses of RMB 4.925 billion yuan, up by 10.70%.The Company

continued to enhance cost management and improved efficiency of asset using. Cost-income ratio

was 32.07%, down by 2.79 percent points; provision for assets impairment loss was RMB 2.521

billion yuan, up by 70.34%; and income tax was RMB 1.373 billion yuan, up by 14.01%.

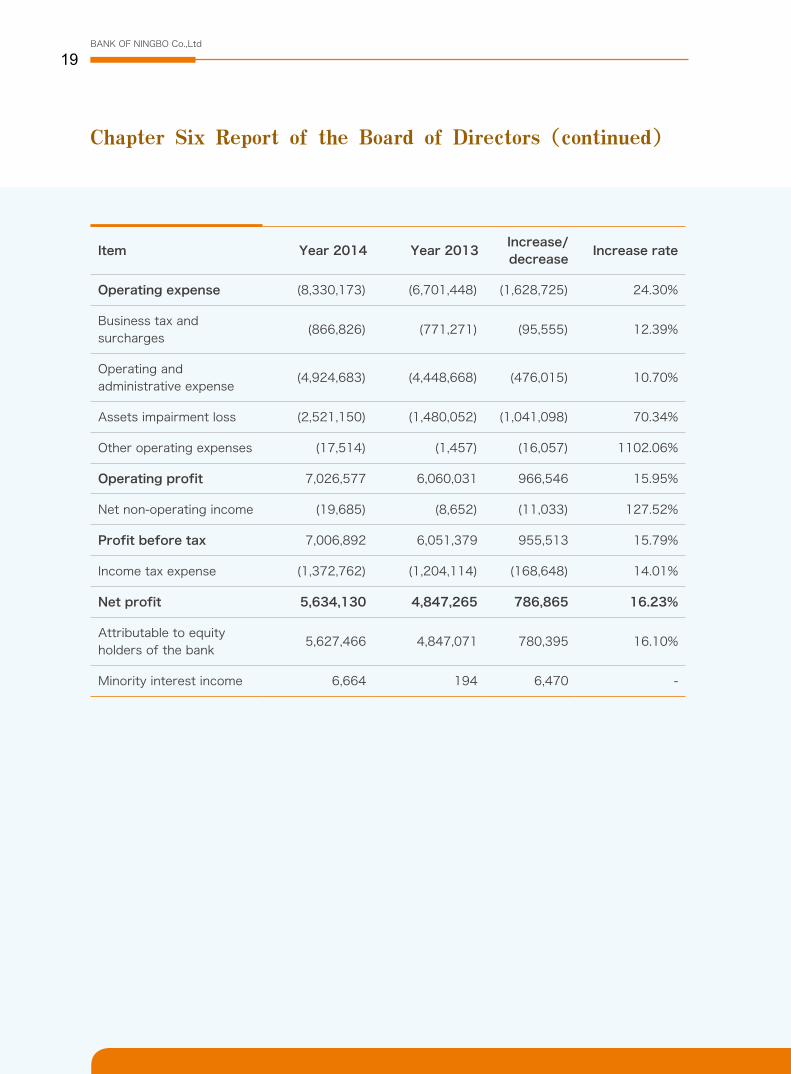

Changes of key items in the income statement

Unit: (RMB) Thousand

Item Year 2014 Year 2013Increase/decrease

Increase rate

Operating income 15,356,750 12,761,479 2,595,271 20.34%

Net interest income 13,354,681 11,258,689 2,095,992 18.62%

Interest income 28,175,470 23,494,890 4,680,580 19.92%

Interest expense (14,820,789) (12,236,201) (2,584,588) 21.12%

Non-interest income 2,002,069 1,502,790 499,279 33.22%

Net fees and commissions income

2,485,043 1,619,336 865,707 53.46%

Other non-interest income (482,974) (116,546) (366,428) --

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

19

Item Year 2014 Year 2013Increase/decrease

Increase rate

Operating expense (8,330,173) (6,701,448) (1,628,725) 24.30%

Business tax and surcharges

(866,826) (771,271) (95,555) 12.39%

Operating and administrative expense

(4,924,683) (4,448,668) (476,015) 10.70%

Assets impairment loss (2,521,150) (1,480,052) (1,041,098) 70.34%

Other operating expenses (17,514) (1,457) (16,057) 1102.06%

Operating profit 7,026,577 6,060,031 966,546 15.95%

Net non-operating income (19,685) (8,652) (11,033) 127.52%

Profit before tax 7,006,892 6,051,379 955,513 15.79%

Income tax expense (1,372,762) (1,204,114) (168,648) 14.01%

Net profit 5,634,130 4,847,265 786,865 16.23%

Attributable to equity holders of the bank

5,627,466 4,847,071 780,395 16.10%

Minority interest income 6,664 194 6,470 -

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

20

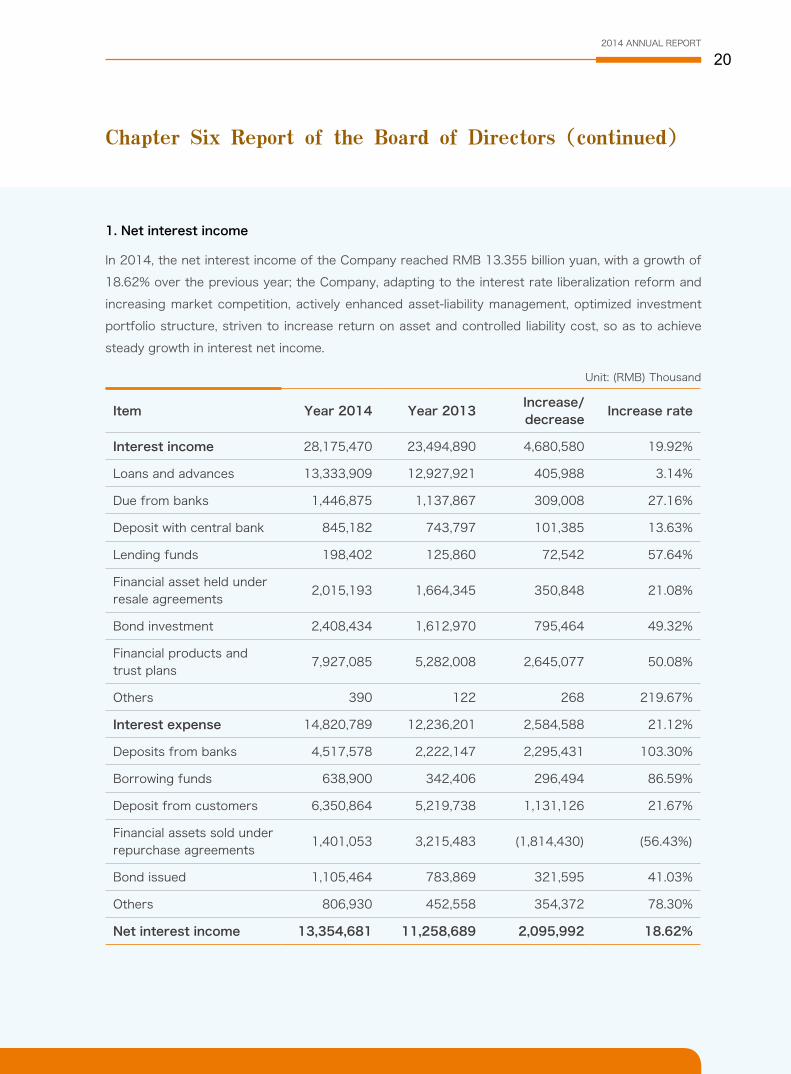

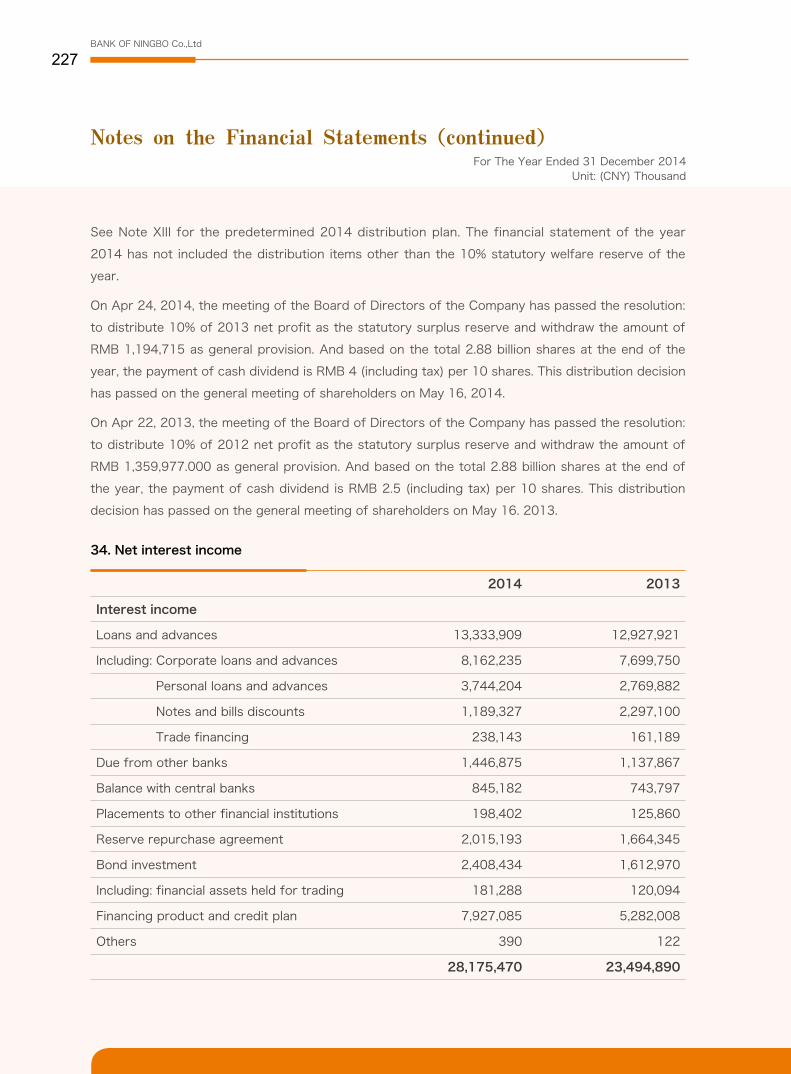

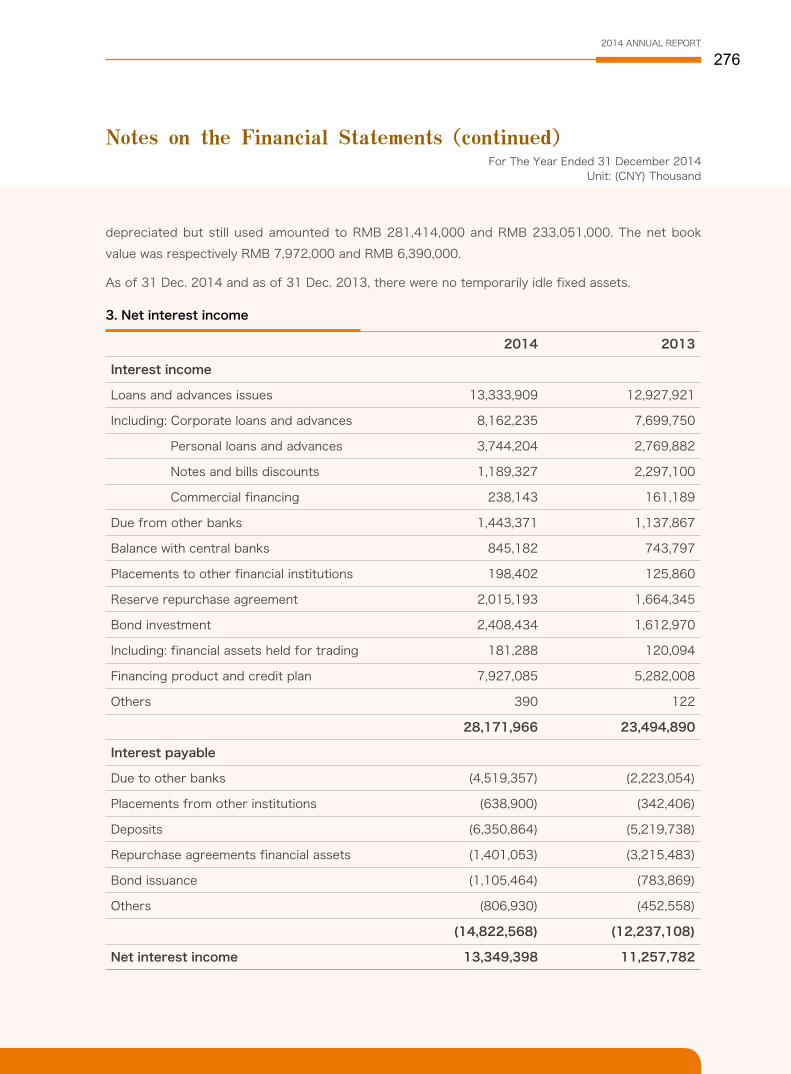

1. Net interest income

In 2014, the net interest income of the Company reached RMB 13.355 billion yuan, with a growth of

18.62% over the previous year; the Company, adapting to the interest rate liberalization reform and

increasing market competition, actively enhanced asset-liability management, optimized investment

portfolio structure, striven to increase return on asset and controlled liability cost, so as to achieve

steady growth in interest net income.

Unit: (RMB) Thousand

Item Year 2014 Year 2013Increase/decrease

Increase rate

Interest income 28,175,470 23,494,890 4,680,580 19.92%

Loans and advances 13,333,909 12,927,921 405,988 3.14%

Due from banks 1,446,875 1,137,867 309,008 27.16%

Deposit with central bank 845,182 743,797 101,385 13.63%

Lending funds 198,402 125,860 72,542 57.64%

Financial asset held under resale agreements

2,015,193 1,664,345 350,848 21.08%

Bond investment 2,408,434 1,612,970 795,464 49.32%

Financial products and trust plans

7,927,085 5,282,008 2,645,077 50.08%

Others 390 122 268 219.67%

Interest expense 14,820,789 12,236,201 2,584,588 21.12%

Deposits from banks 4,517,578 2,222,147 2,295,431 103.30%

Borrowing funds 638,900 342,406 296,494 86.59%

Deposit from customers 6,350,864 5,219,738 1,131,126 21.67%

Financial assets sold under repurchase agreements

1,401,053 3,215,483 (1,814,430) (56.43%)

Bond issued 1,105,464 783,869 321,595 41.03%

Others 806,930 452,558 354,372 78.30%

Net interest income 13,354,681 11,258,689 2,095,992 18.62%

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

21

The table below shows interest income and expense, average balance and average interest rate of

interest-bearing assets and interest-bearing liabilities.

Unit: (RMB) Thousand

Item

Year 2014 Year 2013

Average balance

Interest income/ expense

Average yield/

cost

Average balance

Interest income/ expense

Average yield/

cost

Assets

General loans 164,909,416 11,868,950 7.20% 144,437,672 10,415,319 7.21%

Securities investment

182,008,982 10,335,520 5.68% 131,290,936 6,894,978 5.25%

Deposit with central bank

56,327,379 845,182 1.50% 49,377,918 743,797 1.51%

Due from banks and other financial institutions

70,983,178 3,660,860 5.16% 61,827,432 2,928,194 4.74%

Total interest-bearing assets

474,228,955 26,710,512 5.63% 386,933,958 20,982,288 5.42%

Liabilities

Deposits 289,139,466 6,350,864 2.20% 246,569,244 5,219,738 2.12%

Due to banks and other financial institutions

161,893,472 7,364,461 4.55% 118,999,904 5,281,930 4.44%

Bonds payable 22,627,539 1,105,464 4.89% 16,121,686 783,869 4.86%

Total interest-bearing liabilities

473,660,477 14,820,789 3.13% 381,690,834 11,285,537 2.96%

Net interest income

11,889,723 9,696,751

Net interest spread(NIS)

2.50% 2.46%

Net interest margin(NIM)

2.51% 2.51%

(1) the average balance of the interest-bearing assets and the interest-bearing liabilities refers to daily

balance on average.

(2) General loans exclude discounts and advances; due from banks and other financial institutions

Note:

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

22

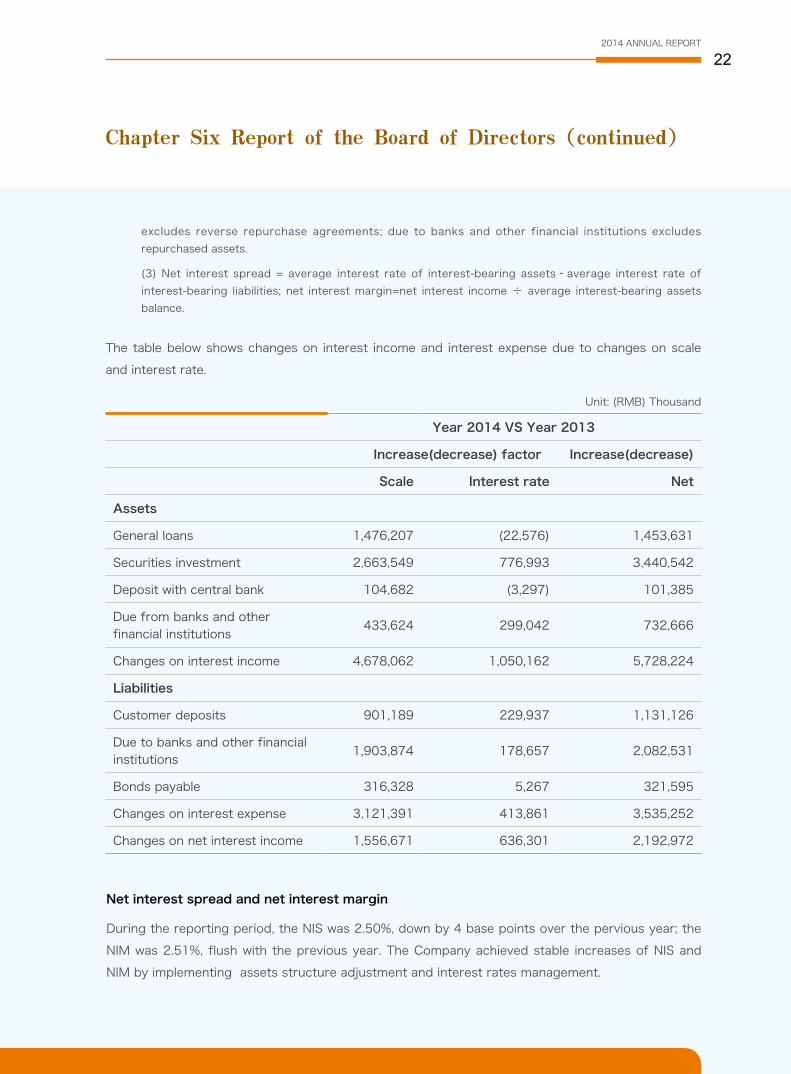

The table below shows changes on interest income and interest expense due to changes on scale

and interest rate.

Unit: (RMB) Thousand

excludes reverse repurchase agreements; due to banks and other financial institutions excludes

repurchased assets.

(3) Net interest spread = average interest rate of interest-bearing assets–average interest rate of

interest-bearing liabilities; net interest margin=net interest income ÷ average interest-bearing assets

balance.

Year 2014 VS Year 2013

Increase(decrease) factor Increase(decrease)

Scale Interest rate Net

Assets

General loans 1,476,207 (22,576) 1,453,631

Securities investment 2,663,549 776,993 3,440,542

Deposit with central bank 104,682 (3,297) 101,385

Due from banks and other financial institutions

433,624 299,042 732,666

Changes on interest income 4,678,062 1,050,162 5,728,224

Liabilities

Customer deposits 901,189 229,937 1,131,126

Due to banks and other financial institutions

1,903,874 178,657 2,082,531

Bonds payable 316,328 5,267 321,595

Changes on interest expense 3,121,391 413,861 3,535,252

Changes on net interest income 1,556,671 636,301 2,192,972

Net interest spread and net interest margin

During the reporting period, the NIS was 2.50%, down by 4 base points over the pervious year; the

NIM was 2.51%, flush with the previous year. The Company achieved stable increases of NIS and

NIM by implementing assets structure adjustment and interest rates management.

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

23

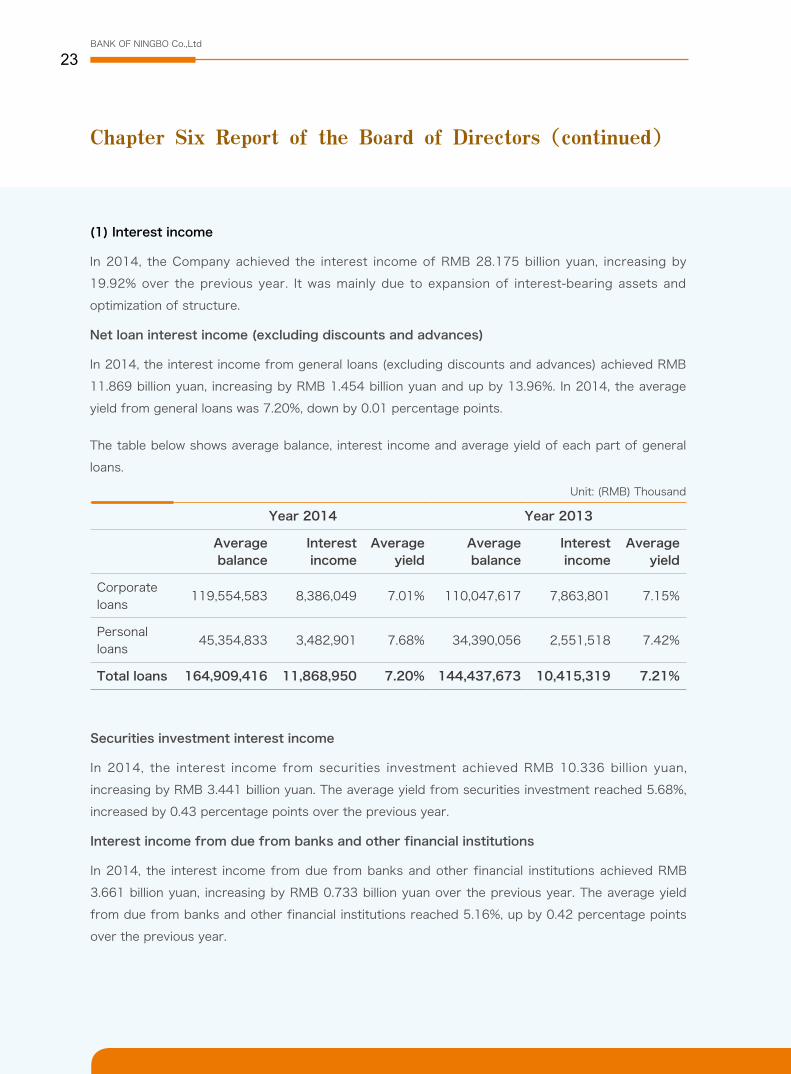

(1) Interest income

In 2014, the Company achieved the interest income of RMB 28.175 billion yuan, increasing by

19.92% over the previous year. It was mainly due to expansion of interest-bearing assets and

optimization of structure.

Net loan interest income (excluding discounts and advances)

In 2014, the interest income from general loans (excluding discounts and advances) achieved RMB

11.869 billion yuan, increasing by RMB 1.454 billion yuan and up by 13.96%. In 2014, the average

yield from general loans was 7.20%, down by 0.01 percentage points.

The table below shows average balance, interest income and average yield of each part of general

loans.

Securities investment interest income

In 2014, the interest income from securities investment achieved RMB 10.336 billion yuan,

increasing by RMB 3.441 billion yuan. The average yield from securities investment reached 5.68%,

increased by 0.43 percentage points over the previous year.

Interest income from due from banks and other financial institutions

In 2014, the interest income from due from banks and other financial institutions achieved RMB

3.661 billion yuan, increasing by RMB 0.733 billion yuan over the previous year. The average yield

from due from banks and other financial institutions reached 5.16%, up by 0.42 percentage points

over the previous year.

Unit: (RMB) Thousand

Year 2014 Year 2013

Average balance

Interest income

Average yield

Average balance

Interest income

Average yield

Corporate loans

119,554,583 8,386,049 7.01% 110,047,617 7,863,801 7.15%

Personal loans

45,354,833 3,482,901 7.68% 34,390,056 2,551,518 7.42%

Total loans 164,909,416 11,868,950 7.20% 144,437,673 10,415,319 7.21%

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

24

Unit: (RMB) Thousand

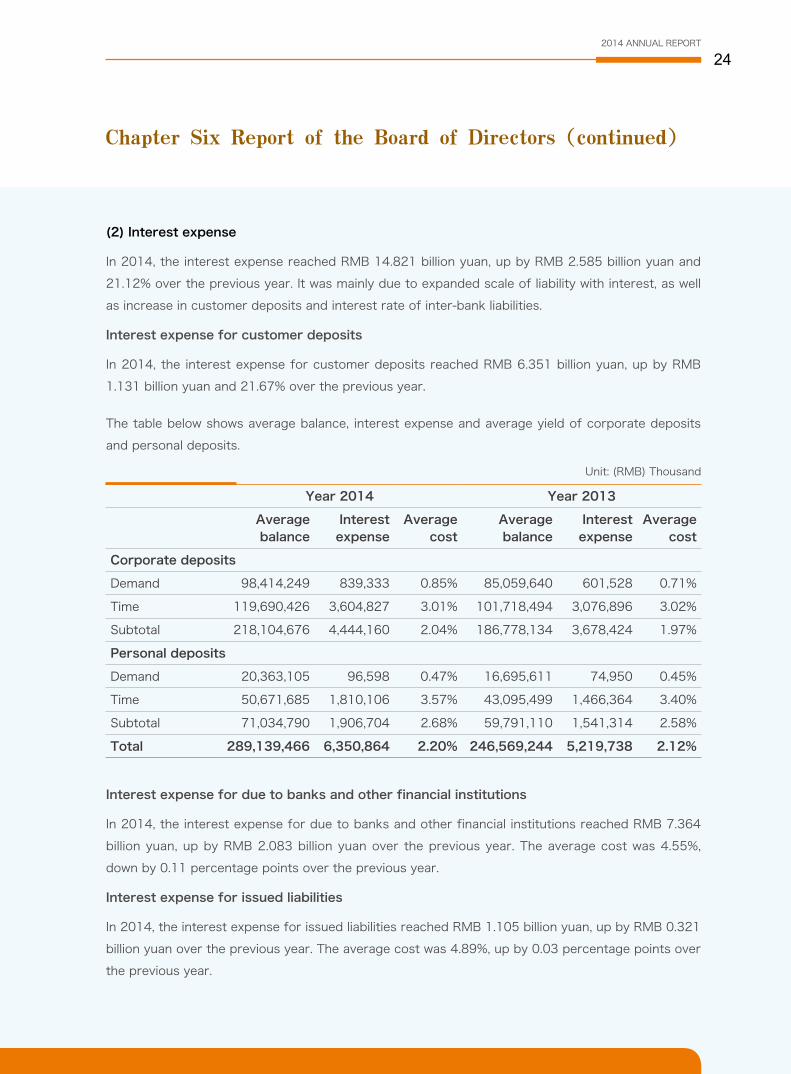

(2) Interest expense

In 2014, the interest expense reached RMB 14.821 billion yuan, up by RMB 2.585 billion yuan and

21.12% over the previous year. It was mainly due to expanded scale of liability with interest, as well

as increase in customer deposits and interest rate of inter-bank liabilities.

Interest expense for customer deposits

In 2014, the interest expense for customer deposits reached RMB 6.351 billion yuan, up by RMB

1.131 billion yuan and 21.67% over the previous year.

The table below shows average balance, interest expense and average yield of corporate deposits

and personal deposits.

Interest expense for due to banks and other financial institutions

In 2014, the interest expense for due to banks and other financial institutions reached RMB 7.364

billion yuan, up by RMB 2.083 billion yuan over the previous year. The average cost was 4.55%,

down by 0.11 percentage points over the previous year.

Interest expense for issued liabilities

In 2014, the interest expense for issued liabilities reached RMB 1.105 billion yuan, up by RMB 0.321

billion yuan over the previous year. The average cost was 4.89%, up by 0.03 percentage points over

the previous year.

Year 2014 Year 2013

Average balance

Interest expense

Average cost

Average balance

Interest expense

Average cost

Corporate deposits

Demand 98,414,249 839,333 0.85% 85,059,640 601,528 0.71%

Time 119,690,426 3,604,827 3.01% 101,718,494 3,076,896 3.02%

Subtotal 218,104,676 4,444,160 2.04% 186,778,134 3,678,424 1.97%

Personal deposits

Demand 20,363,105 96,598 0.47% 16,695,611 74,950 0.45%

Time 50,671,685 1,810,106 3.57% 43,095,499 1,466,364 3.40%

Subtotal 71,034,790 1,906,704 2.68% 59,791,110 1,541,314 2.58%

Total 289,139,466 6,350,864 2.20% 246,569,244 5,219,738 2.12%

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

25

Net fee and commission income

Unit: (RMB) Thousand

Unit: (RMB) Thousand

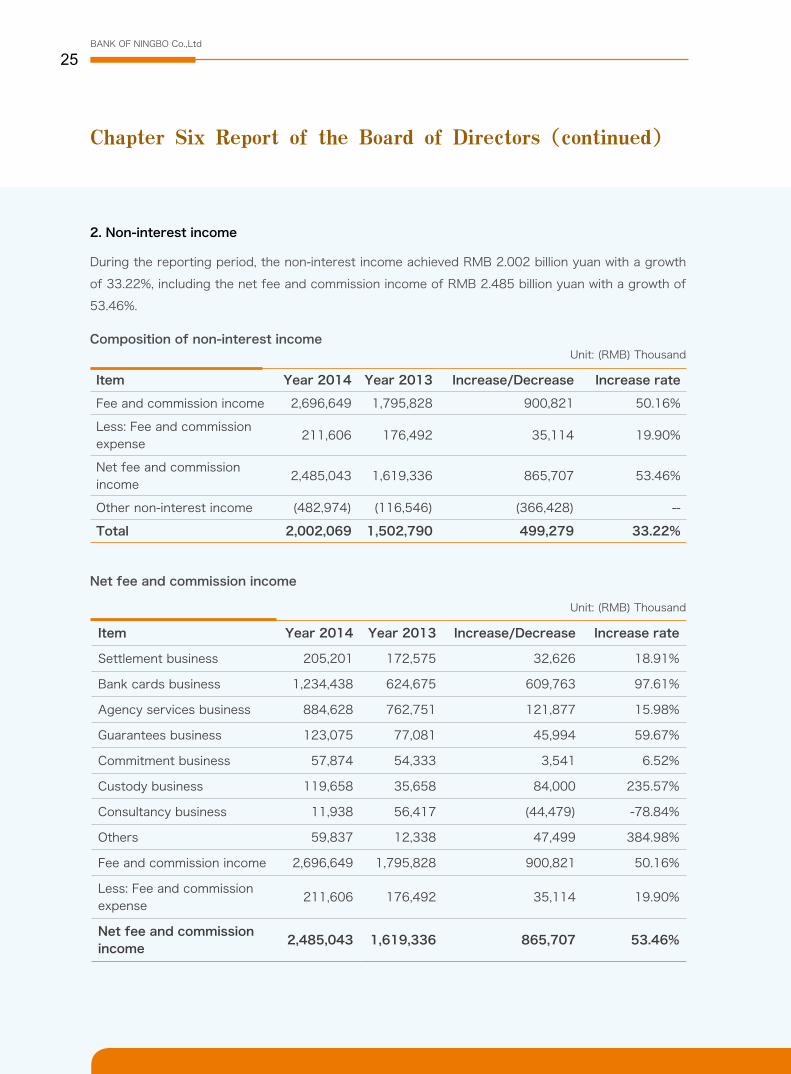

2. Non-interest income

During the reporting period, the non-interest income achieved RMB 2.002 billion yuan with a growth

of 33.22%, including the net fee and commission income of RMB 2.485 billion yuan with a growth of

53.46%.

Composition of non-interest income

Item Year 2014 Year 2013 Increase/Decrease Increase rate

Fee and commission income 2,696,649 1,795,828 900,821 50.16%

Less: Fee and commission expense

211,606 176,492 35,114 19.90%

Net fee and commission income

2,485,043 1,619,336 865,707 53.46%

Other non-interest income (482,974) (116,546) (366,428) --

Total 2,002,069 1,502,790 499,279 33.22%

Item Year 2014 Year 2013 Increase/Decrease Increase rate

Settlement business 205,201 172,575 32,626 18.91%

Bank cards business 1,234,438 624,675 609,763 97.61%

Agency services business 884,628 762,751 121,877 15.98%

Guarantees business 123,075 77,081 45,994 59.67%

Commitment business 57,874 54,333 3,541 6.52%

Custody business 119,658 35,658 84,000 235.57%

Consultancy business 11,938 56,417 (44,479) -78.84%

Others 59,837 12,338 47,499 384.98%

Fee and commission income 2,696,649 1,795,828 900,821 50.16%

Less: Fee and commission expense

211,606 176,492 35,114 19.90%

Net fee and commission income

2,485,043 1,619,336 865,707 53.46%

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

26

Unit: (RMB) Thousand

In 2014, the Company took advantages of its integrated finance service to adjust the direction of

business development, and continued to promote transformation and innovation of intermediate

business. The income from bank cards reached RMB 1.234 billion yuan, up by 0.610 billion yuan and

97.61% over the previous year, mainly due to increased income from settlement; the income from

guarantees business was RMB 0.123 billion yuan, up by 59.67%, mainly due to significant growth

of income in guarantee business; the income from custody business was 0.120 billion yuan, up by

235.57%, mainly due to significant growth in securities and fund custody businesses; and income

from other businesses was 0.060 billion yuan, up by 384.98%, mainly due to rapid growth of income

from management business of fund subsidiary.

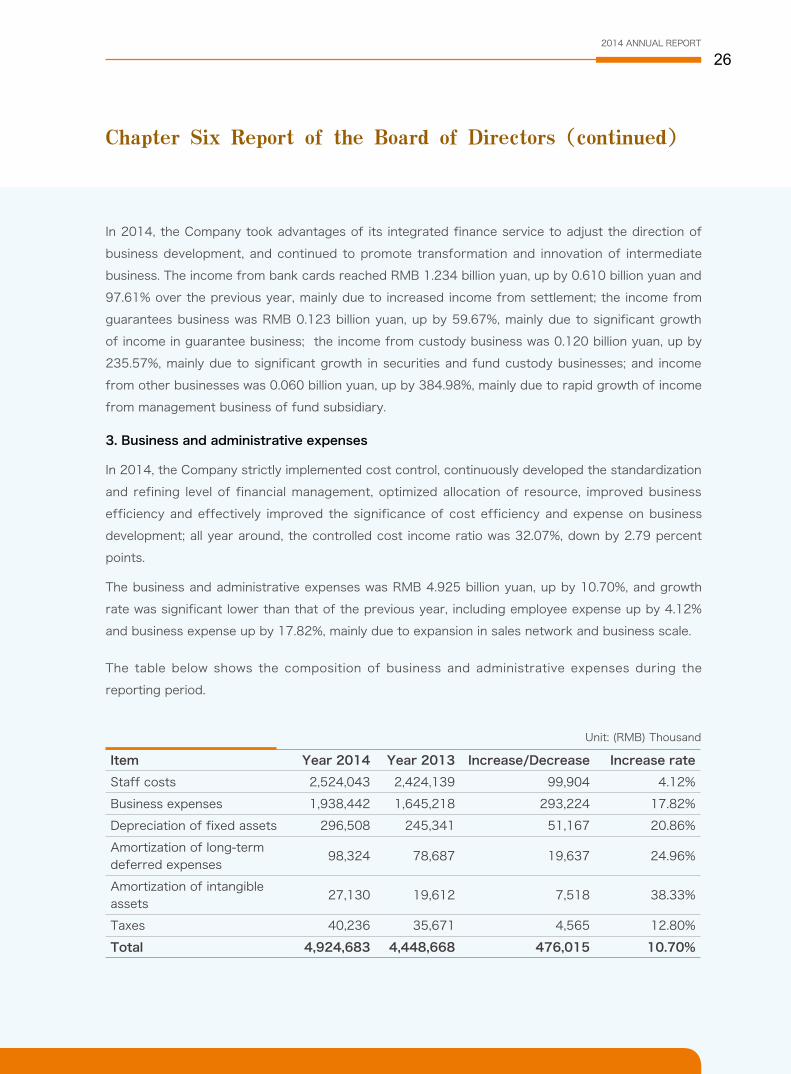

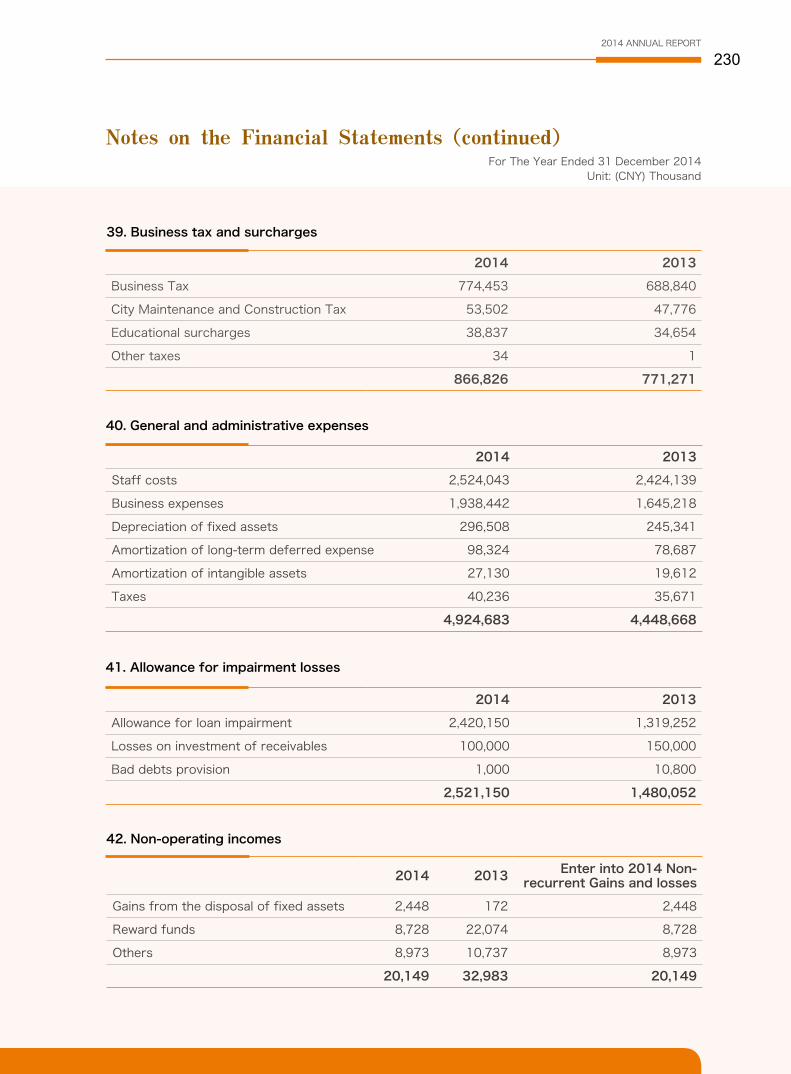

3. Business and administrative expenses

In 2014, the Company strictly implemented cost control, continuously developed the standardization

and refining level of financial management, optimized allocation of resource, improved business

efficiency and effectively improved the significance of cost efficiency and expense on business

development; all year around, the controlled cost income ratio was 32.07%, down by 2.79 percent

points.

The business and administrative expenses was RMB 4.925 billion yuan, up by 10.70%, and growth

rate was significant lower than that of the previous year, including employee expense up by 4.12%

and business expense up by 17.82%, mainly due to expansion in sales network and business scale.

The table below shows the composition of business and administrative expenses during the

reporting period.

Item Year 2014 Year 2013 Increase/Decrease Increase rate

Staff costs 2,524,043 2,424,139 99,904 4.12%

Business expenses 1,938,442 1,645,218 293,224 17.82%

Depreciation of fixed assets 296,508 245,341 51,167 20.86%

Amortization of long-term deferred expenses

98,324 78,687 19,637 24.96%

Amortization of intangible assets

27,130 19,612 7,518 38.33%

Taxes 40,236 35,671 4,565 12.80%

Total 4,924,683 4,448,668 476,015 10.70%

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

27

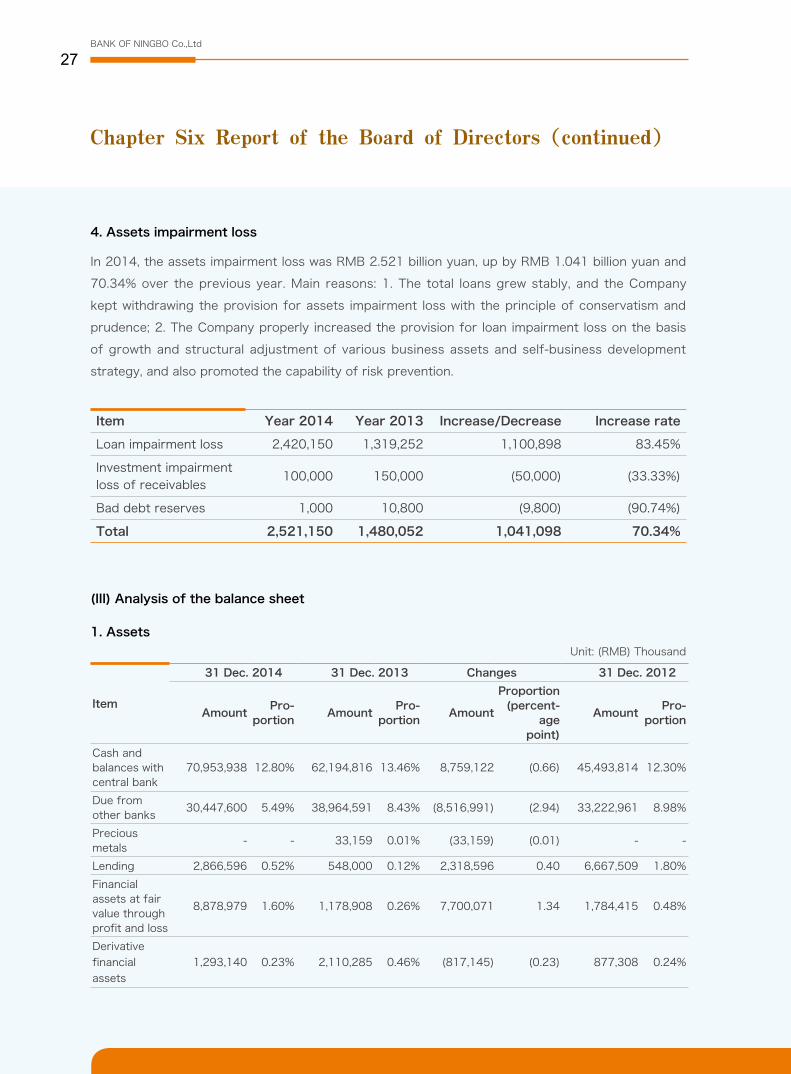

4. Assets impairment loss

In 2014, the assets impairment loss was RMB 2.521 billion yuan, up by RMB 1.041 billion yuan and

70.34% over the previous year. Main reasons: 1. The total loans grew stably, and the Company

kept withdrawing the provision for assets impairment loss with the principle of conservatism and

prudence; 2. The Company properly increased the provision for loan impairment loss on the basis

of growth and structural adjustment of various business assets and self-business development

strategy, and also promoted the capability of risk prevention.

(III) Analysis of the balance sheet

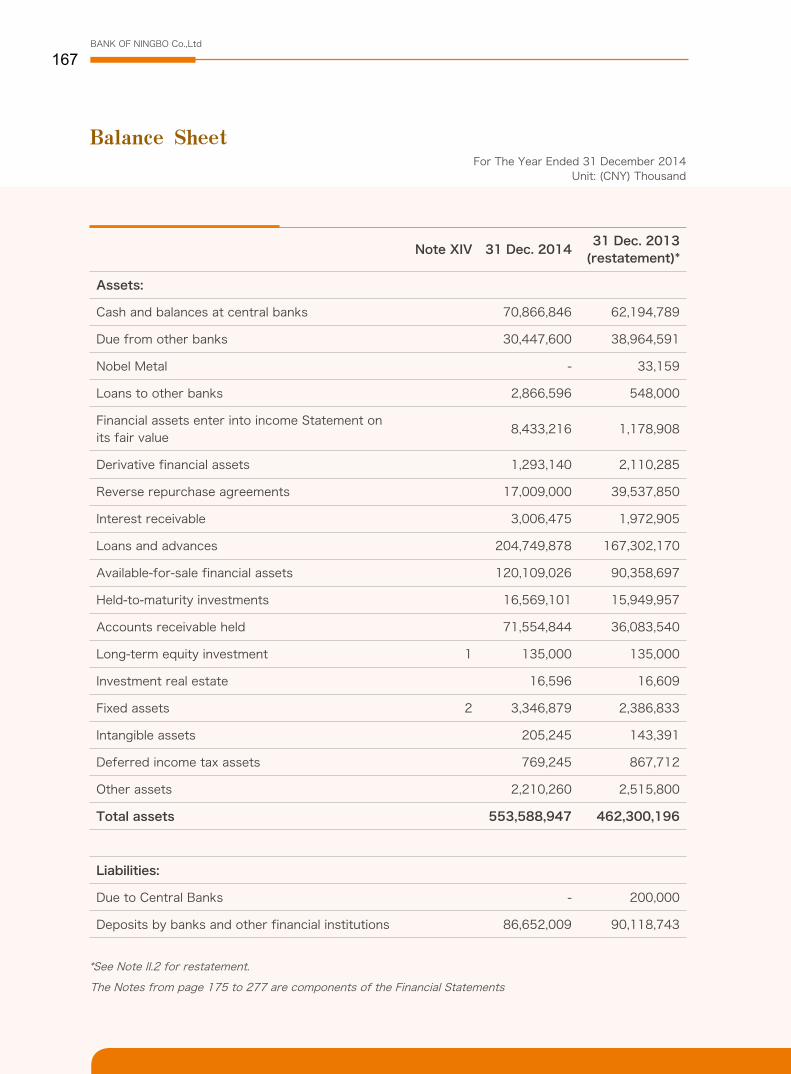

1. Assets

Unit: (RMB) Thousand

Item Year 2014 Year 2013 Increase/Decrease Increase rate

Loan impairment loss 2,420,150 1,319,252 1,100,898 83.45%

Investment impairment loss of receivables

100,000 150,000 (50,000) (33.33%)

Bad debt reserves 1,000 10,800 (9,800) (90.74%)

Total 2,521,150 1,480,052 1,041,098 70.34%

Item

31 Dec. 2014 31 Dec. 2013 Changes 31 Dec. 2012

AmountPro-

portionAmount

Pro-portion

Amount

Proportion (percent-

age point)

AmountPro-

portion

Cash and balances with central bank

70,953,938 12.80% 62,194,816 13.46% 8,759,122 (0.66) 45,493,814 12.30%

Due from other banks

30,447,600 5.49% 38,964,591 8.43% (8,516,991) (2.94) 33,222,961 8.98%

Precious metals

- - 33,159 0.01% (33,159) (0.01) - -

Lending 2,866,596 0.52% 548,000 0.12% 2,318,596 0.40 6,667,509 1.80%

Financial assets at fair value through profit and loss

8,878,979 1.60% 1,178,908 0.26% 7,700,071 1.34 1,784,415 0.48%

Derivative financial assets

1,293,140 0.23% 2,110,285 0.46% (817,145) (0.23) 877,308 0.24%

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

28

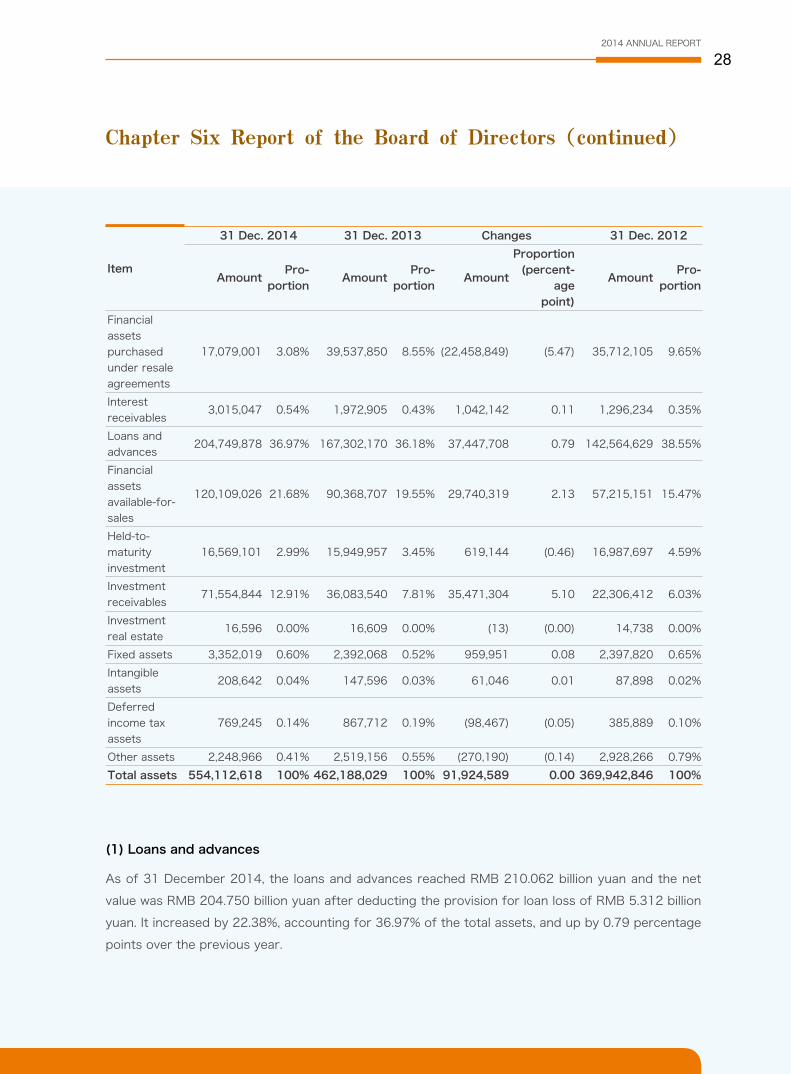

Item

31 Dec. 2014 31 Dec. 2013 Changes 31 Dec. 2012

AmountPro-

portionAmount

Pro-portion

Amount

Proportion (percent-

age point)

AmountPro-

portion

Financial assets purchased under resale agreements

17,079,001 3.08% 39,537,850 8.55% (22,458,849) (5.47) 35,712,105 9.65%

Interest receivables

3,015,047 0.54% 1,972,905 0.43% 1,042,142 0.11 1,296,234 0.35%

Loans and advances

204,749,878 36.97% 167,302,170 36.18% 37,447,708 0.79 142,564,629 38.55%

Financial assets available-for- sales

120,109,026 21.68% 90,368,707 19.55% 29,740,319 2.13 57,215,151 15.47%

Held-to-maturity investment

16,569,101 2.99% 15,949,957 3.45% 619,144 (0.46) 16,987,697 4.59%

Investment receivables

71,554,844 12.91% 36,083,540 7.81% 35,471,304 5.10 22,306,412 6.03%

Investment real estate

16,596 0.00% 16,609 0.00% (13) (0.00) 14,738 0.00%

Fixed assets 3,352,019 0.60% 2,392,068 0.52% 959,951 0.08 2,397,820 0.65%

Intangible assets

208,642 0.04% 147,596 0.03% 61,046 0.01 87,898 0.02%

Deferred income tax assets

769,245 0.14% 867,712 0.19% (98,467) (0.05) 385,889 0.10%

Other assets 2,248,966 0.41% 2,519,156 0.55% (270,190) (0.14) 2,928,266 0.79%

Total assets 554,112,618 100% 462,188,029 100% 91,924,589 0.00 369,942,846 100%

(1) Loans and advances

As of 31 December 2014, the loans and advances reached RMB 210.062 billion yuan and the net

value was RMB 204.750 billion yuan after deducting the provision for loan loss of RMB 5.312 billion

yuan. It increased by 22.38%, accounting for 36.97% of the total assets, and up by 0.79 percentage

points over the previous year.

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

29

Corporate loan

As of Dec.31, 2014, the corporate loan was RMB 127.804 billion yuan, accounting for 60.84%

of the total loans and advances, and down by 6.20 percentage points over the previous year. In

2014, the Company enhanced adjustment of customer and product structure so as to meet multi-

levelfinancing demand of customers and increase loan support to small, micro and rural realted

enterprises.

Discount

As of Dec.31, 2014, the discounts achieved RMB 9.522 billion yuan, accounting for 4.53% of the

total loans and advances, and up by 2.67 percentage points compared with that of 31 December

2013. The Company, depending on credit loan schedule, properly increased the amount of notes

discounted and improved the return of notes discounted.

Personal loan

As of Dec.31, 2014, the personal loans totalized RMB 72.735 billion yuan, accounting for 34.63%

of the total loans and advances, and up by 3.53 percentage points. In 2014, with the changes in

economic situation, the Company, on the basis of strengthening regular customer base of personal

loan, futher increased personal consumption loans and credit card loans.

Unit: (RMB) Thousand

ItemYear 2014 Year 2013

Amount Proportion Amount Proportion

Corporate loans and advances

127,804,398 60.84% 114,769,741 67.04%

Loans 123,301,697 58.70% 110,332,334 64.45%

Trade financing 4,502,701 2.14% 4,437,407 2.59%

Discounts 9,522,435 4.53% 3,182,740 1.86%

Personal loans and advances

72,735,349 34.63% 53,237,185 31.10%

Personal consumption loans 66,652,085 31.73% 46,849,314 27.37%

Personal operation loans 4,492,093 2.14% 4,664,492 2.72%

Personal housing loans 1,591,171 0.76% 1,723,379 1.01%

Total loans 210,062,182 100.00% 171,189,666 100.00%

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

30

Unit: (RMB) Thousand

Unit: (RMB) Thousand

Situation of ten financial bonds held with the highest face value

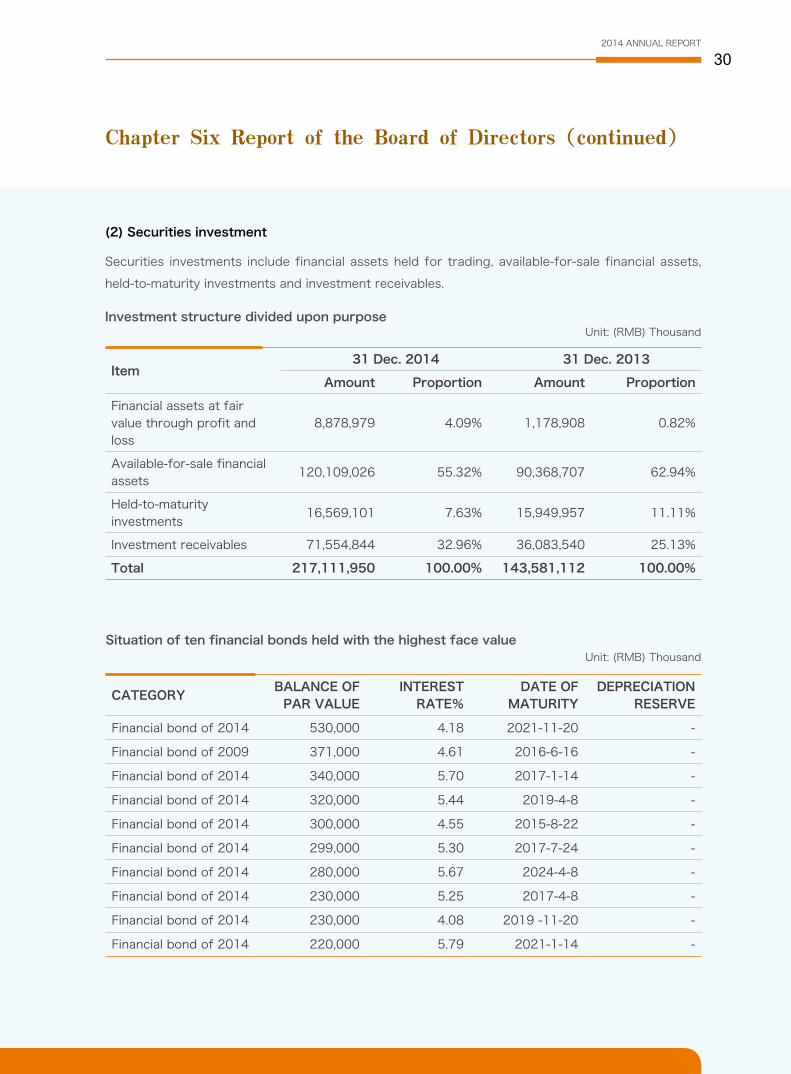

(2) Securities investment

Securities investments include financial assets held for trading, available-for-sale financial assets,

held-to-maturity investments and investment receivables.

Investment structure divided upon purpose

Item 31 Dec. 2014 31 Dec. 2013

Amount Proportion Amount Proportion

Financial assets at fair value through profit and loss

8,878,979 4.09% 1,178,908 0.82%

Available-for-sale financial assets

120,109,026 55.32% 90,368,707 62.94%

Held-to-maturity investments

16,569,101 7.63% 15,949,957 11.11%

Investment receivables 71,554,844 32.96% 36,083,540 25.13%

Total 217,111,950 100.00% 143,581,112 100.00%

CATEGORYBALANCE OF

PAR VALUEINTEREST

RATE%DATE OF

MATURITYDEPRECIATION

RESERVE

Financial bond of 2014 530,000 4.18 2021-11-20 -

Financial bond of 2009 371,000 4.61 2016-6-16 -

Financial bond of 2014 340,000 5.70 2017-1-14 -

Financial bond of 2014 320,000 5.44 2019-4-8 -

Financial bond of 2014 300,000 4.55 2015-8-22 -

Financial bond of 2014 299,000 5.30 2017-7-24 -

Financial bond of 2014 280,000 5.67 2024-4-8 -

Financial bond of 2014 230,000 5.25 2017-4-8 -

Financial bond of 2014 230,000 4.08 2019 -11-20 -

Financial bond of 2014 220,000 5.79 2021-1-14 -

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

31

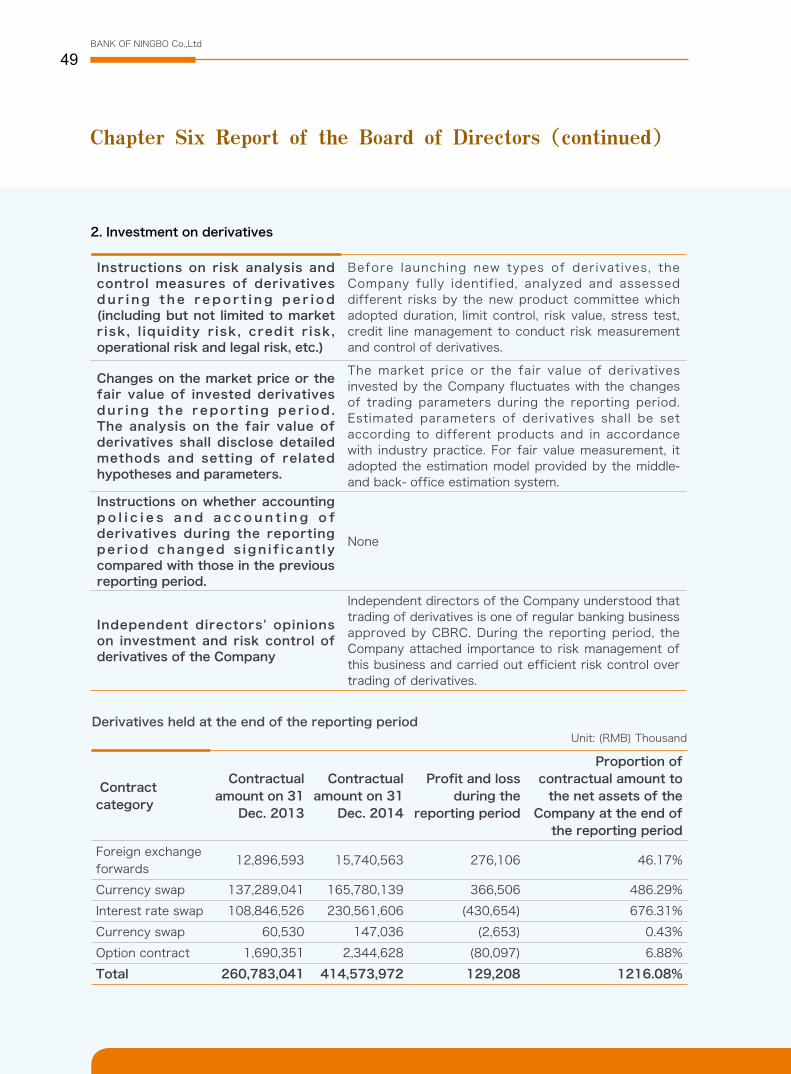

(3) Derivative financial instruments held at the end of the reporting periodUnit: (RMB) Thousand

Derivative financial instruments

31 Dec. 2014

Contract/nominal amount

Fair value of assets Fair value of liabilities

Foreign exchange forwards

15,740,563 139,832 (30,776)

Currency swap 165,780,139 744,101 (810,252)

Interest rate swap 230,561,606 244,848 (349,760)

Currency swap 147,036 - (1,914)

Option contract 2,344,628 164,359 (110,786)

Total 414,573,972 1,293,140 (1,303,488)

During the reporting period, the following derivative financial instruments were used in transactions:

Swap Contract: Swap contract refers to a commitment between two parties to exchange cash flow

within an agreed period. The Company mainly adopted Interest Rate Swaps and Currency Interest

Rate Swaps.

In an Interest Rate Swap, both parties agrees to pay interest to each other at an agreed interest

rate within an agreed period. Both parties, as based on the same currency and the same amount,

will exchange a fixed interest rate for a floating interest rate, or exchange one floating interest

rate for another. By the end of the agreed period, the interest will be paid according to the agreed

interest rate.

Currency Interest Rate Swap refers to the exchange based on different currencies and different

interest rates. The principal will be retrieved at the expiry date of the contract.

Forward Contract: In a forward contract, a financial product will be purchased or sold at an agreed

price on an agreed date in the future.

Option contract: an option refers to the right to sell or purchase a certain quantity of subject

matters at a specific price (strike price) within a specific period.

Nominal amount of derivative financial instruments in the balance sheet was regarded as a basis

to comparing with fair value assets or liabilities in the balance sheet, which did not represent the

cash flow in the future or the fair value at present. Therefore, it should not be used to reflect the

credit risk or market risk of the Company. With the fluctuation of foreign exchange rate and market

interest rate, as related to the contract terms of derivative financial instruments, the evaluated

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

32

value of derivative financial instruments may have positive (assets) or negative (liabilities) effect on

the bank. Such effect may vary from time to time.

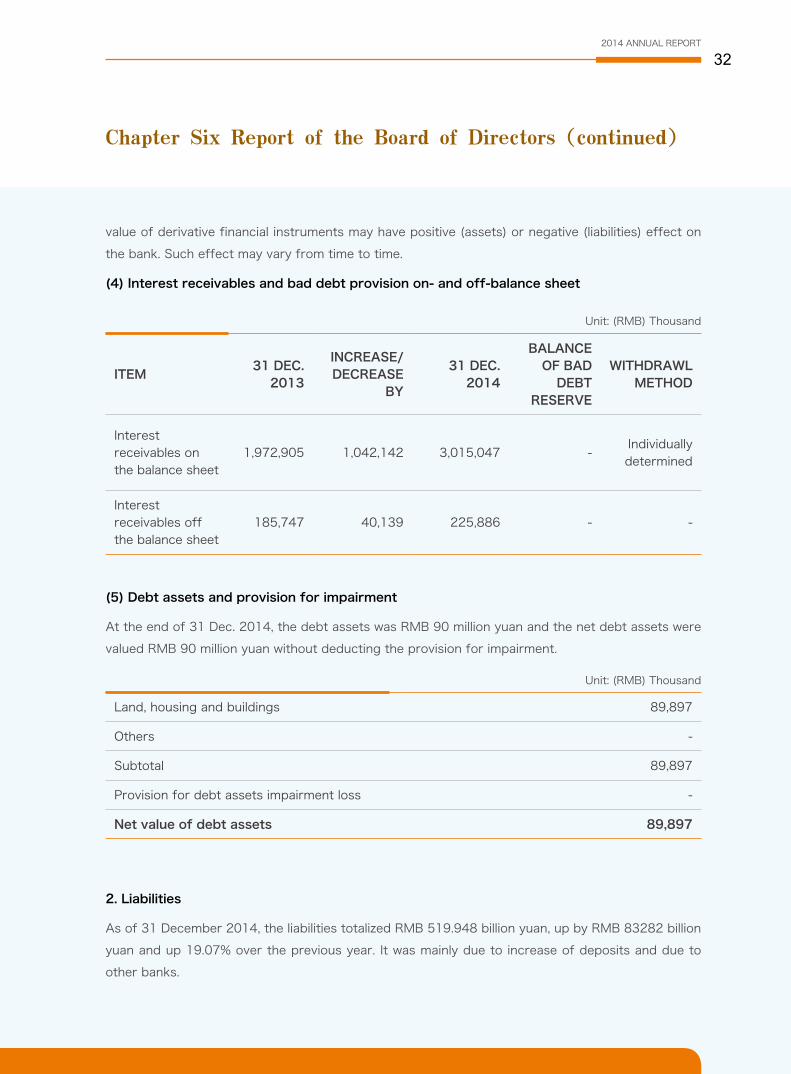

(4) Interest receivables and bad debt provision on- and off-balance sheet

(5) Debt assets and provision for impairment

At the end of 31 Dec. 2014, the debt assets was RMB 90 million yuan and the net debt assets were

valued RMB 90 million yuan without deducting the provision for impairment.

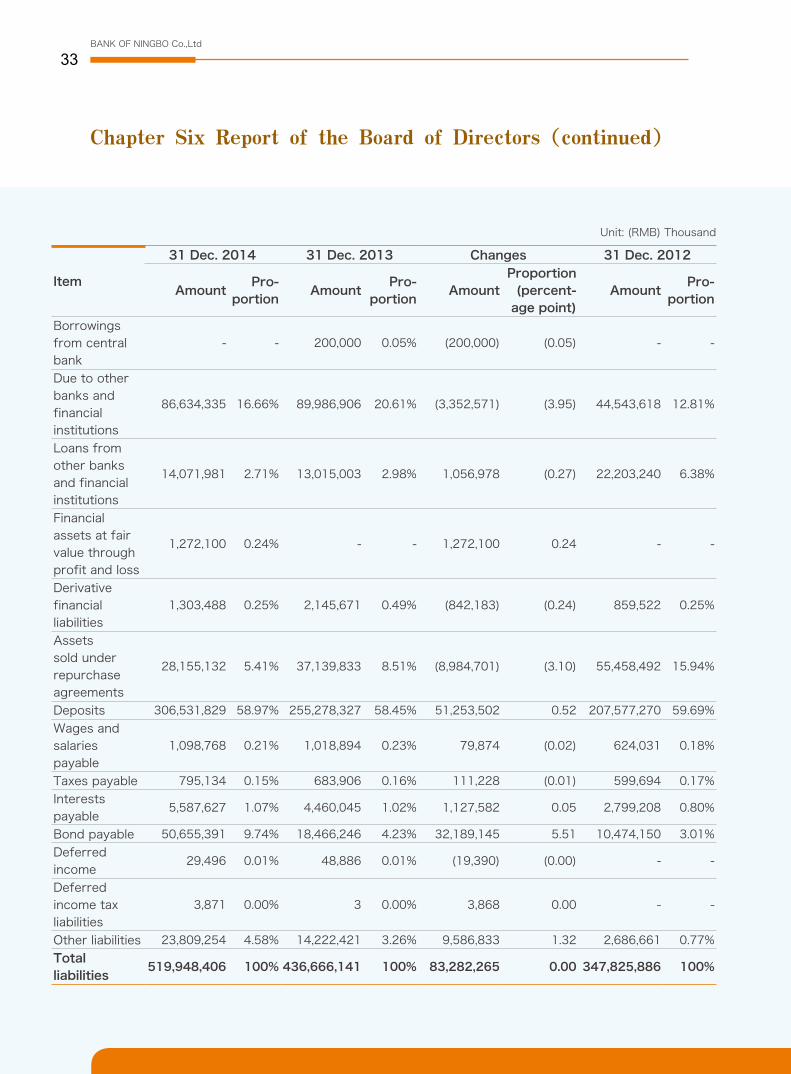

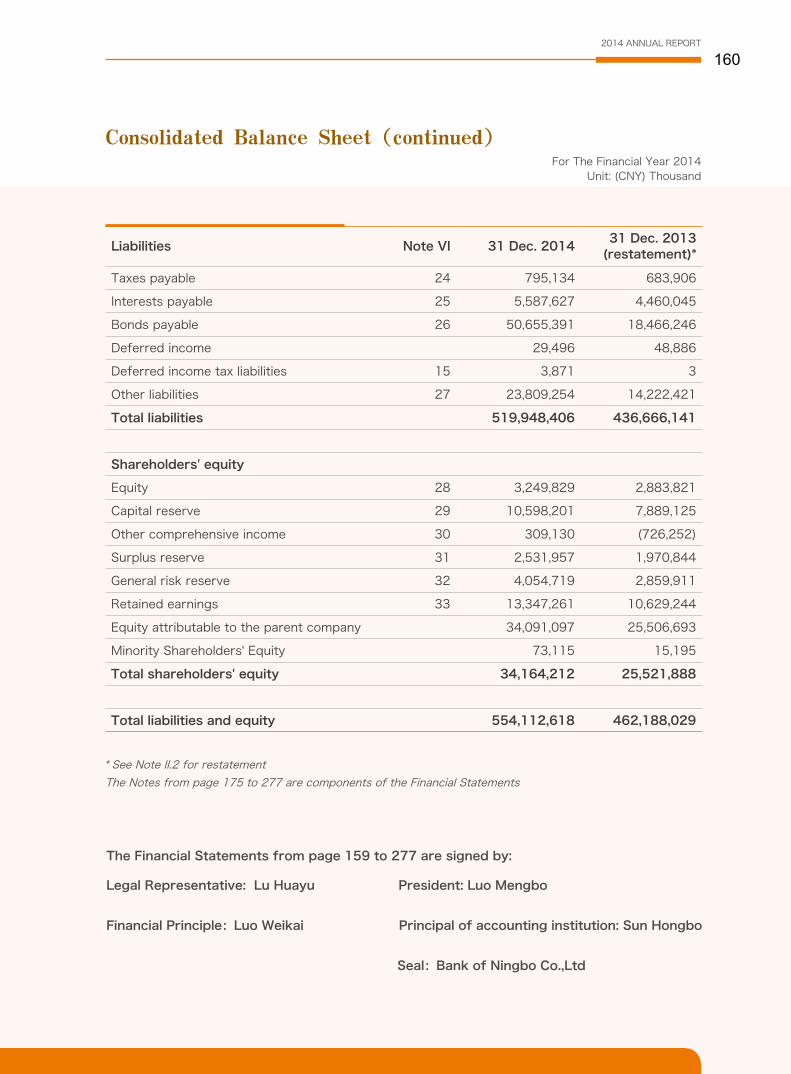

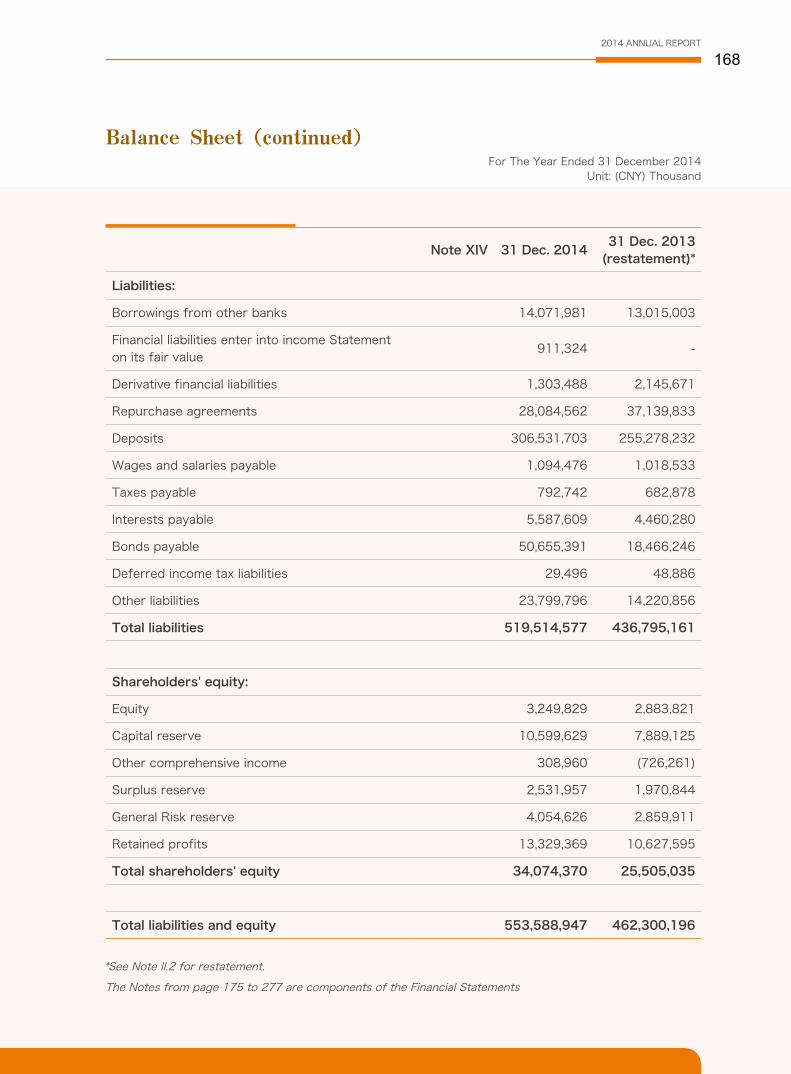

2. Liabilities

As of 31 December 2014, the liabilities totalized RMB 519.948 billion yuan, up by RMB 83282 billion

yuan and up 19.07% over the previous year. It was mainly due to increase of deposits and due to

other banks.

Unit: (RMB) Thousand

Unit: (RMB) Thousand

ITEM31 DEC.

2013

INCREASE/DECREASE

BY

31 DEC. 2014

BALANCE OF BAD

DEBT RESERVE

WITHDRAWL METHOD

Interest receivables on the balance sheet

1,972,905 1,042,142 3,015,047 -Individually determined

Interest receivables off the balance sheet

185,747 40,139 225,886 - -

Land, housing and buildings 89,897

Others -

Subtotal 89,897

Provision for debt assets impairment loss -

Net value of debt assets 89,897

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

33

Unit: (RMB) Thousand

Item

31 Dec. 2014 31 Dec. 2013 Changes 31 Dec. 2012

AmountPro-

portionAmount

Pro-portion

AmountProportion

(percent-age point)

AmountPro-

portion

Borrowings from central bank

- - 200,000 0.05% (200,000) (0.05) - -

Due to other banks and financial institutions

86,634,335 16.66% 89,986,906 20.61% (3,352,571) (3.95) 44,543,618 12.81%

Loans from other banks and financial institutions

14,071,981 2.71% 13,015,003 2.98% 1,056,978 (0.27) 22,203,240 6.38%

Financial assets at fair value through profit and loss

1,272,100 0.24% - - 1,272,100 0.24 - -

Derivative financial liabilities

1,303,488 0.25% 2,145,671 0.49% (842,183) (0.24) 859,522 0.25%

Assets sold under repurchase agreements

28,155,132 5.41% 37,139,833 8.51% (8,984,701) (3.10) 55,458,492 15.94%

Deposits 306,531,829 58.97% 255,278,327 58.45% 51,253,502 0.52 207,577,270 59.69%

Wages and salaries payable

1,098,768 0.21% 1,018,894 0.23% 79,874 (0.02) 624,031 0.18%

Taxes payable 795,134 0.15% 683,906 0.16% 111,228 (0.01) 599,694 0.17%

Interests payable

5,587,627 1.07% 4,460,045 1.02% 1,127,582 0.05 2,799,208 0.80%

Bond payable 50,655,391 9.74% 18,466,246 4.23% 32,189,145 5.51 10,474,150 3.01%

Deferred income

29,496 0.01% 48,886 0.01% (19,390) (0.00) - -

Deferred income tax liabilities

3,871 0.00% 3 0.00% 3,868 0.00 - -

Other liabilities 23,809,254 4.58% 14,222,421 3.26% 9,586,833 1.32 2,686,661 0.77%

Total liabilities

519,948,406 100% 436,666,141 100% 83,282,265 0.00 347,825,886 100%

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

34

Unit: (RMB) Thousand

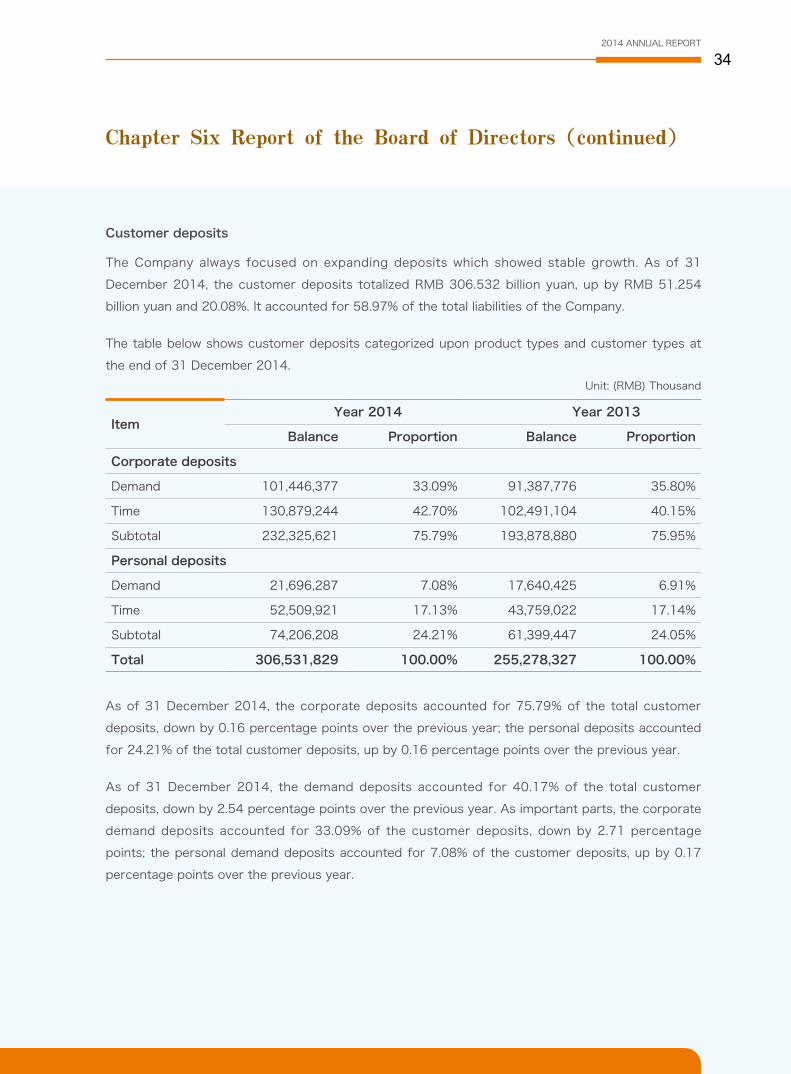

Customer deposits

The Company always focused on expanding deposits which showed stable growth. As of 31

December 2014, the customer deposits totalized RMB 306.532 billion yuan, up by RMB 51.254

billion yuan and 20.08%. It accounted for 58.97% of the total liabilities of the Company.

The table below shows customer deposits categorized upon product types and customer types at

the end of 31 December 2014.

As of 31 December 2014, the corporate deposits accounted for 75.79% of the total customer

deposits, down by 0.16 percentage points over the previous year; the personal deposits accounted

for 24.21% of the total customer deposits, up by 0.16 percentage points over the previous year.

As of 31 December 2014, the demand deposits accounted for 40.17% of the total customer

deposits, down by 2.54 percentage points over the previous year. As important parts, the corporate

demand deposits accounted for 33.09% of the customer deposits, down by 2.71 percentage

points; the personal demand deposits accounted for 7.08% of the customer deposits, up by 0.17

percentage points over the previous year.

Item Year 2014 Year 2013

Balance Proportion Balance Proportion

Corporate deposits

Demand 101,446,377 33.09% 91,387,776 35.80%

Time 130,879,244 42.70% 102,491,104 40.15%

Subtotal 232,325,621 75.79% 193,878,880 75.95%

Personal deposits

Demand 21,696,287 7.08% 17,640,425 6.91%

Time 52,509,921 17.13% 43,759,022 17.14%

Subtotal 74,206,208 24.21% 61,399,447 24.05%

Total 306,531,829 100.00% 255,278,327 100.00%

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

35

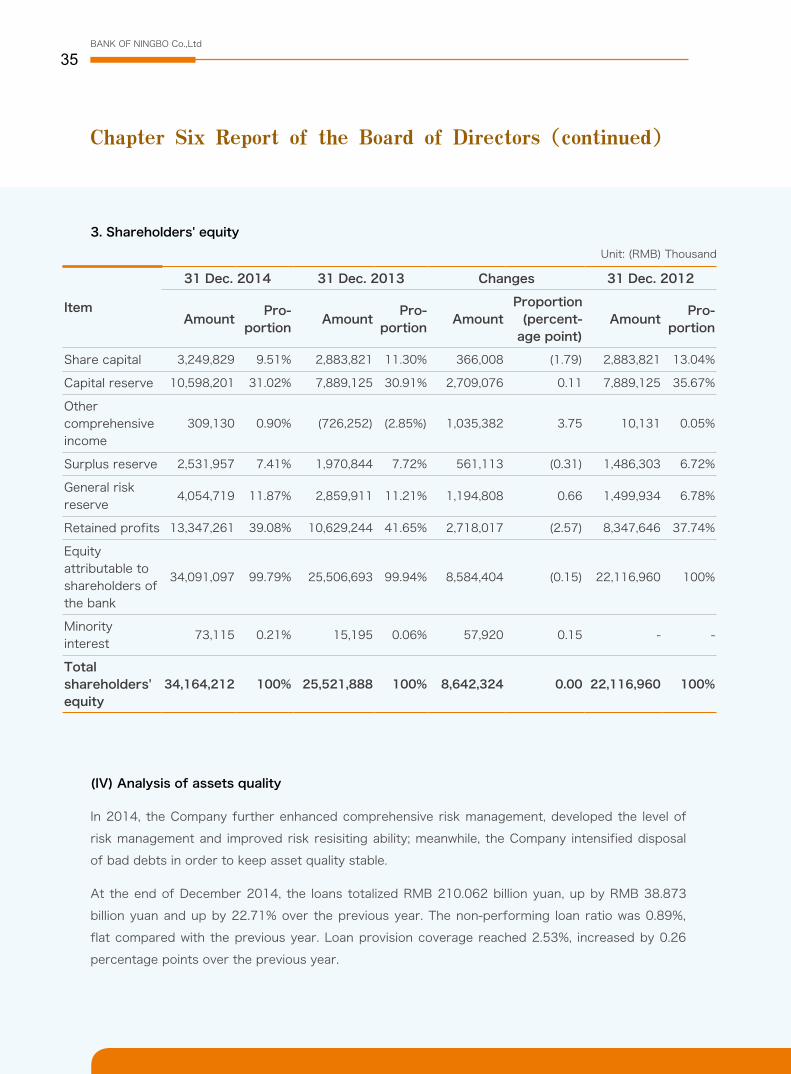

3. Shareholders' equity

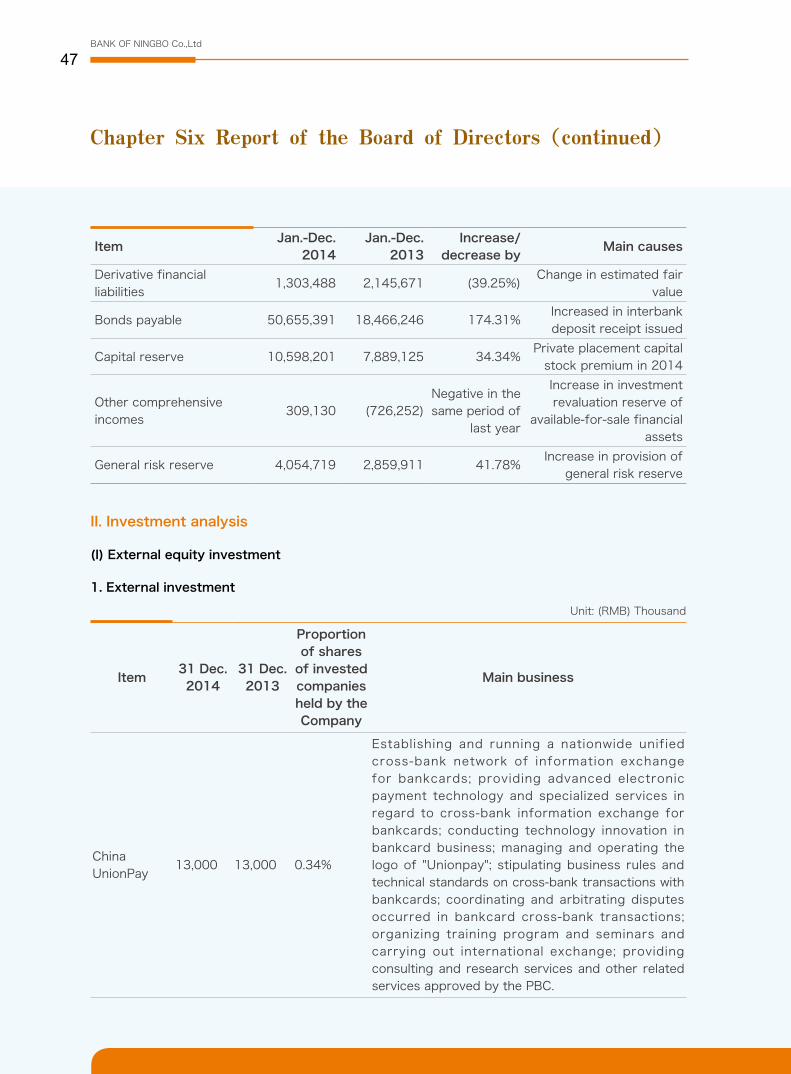

(IV) Analysis of assets quality

In 2014, the Company further enhanced comprehensive risk management, developed the level of

risk management and improved risk resisiting ability; meanwhile, the Company intensified disposal

of bad debts in order to keep asset quality stable.

At the end of December 2014, the loans totalized RMB 210.062 billion yuan, up by RMB 38.873

billion yuan and up by 22.71% over the previous year. The non-performing loan ratio was 0.89%,

flat compared with the previous year. Loan provision coverage reached 2.53%, increased by 0.26

percentage points over the previous year.

Unit: (RMB) Thousand

Item

31 Dec. 2014 31 Dec. 2013 Changes 31 Dec. 2012

AmountPro-

portionAmount

Pro-portion

AmountProportion

(percent-age point)

AmountPro-

portion

Share capital 3,249,829 9.51% 2,883,821 11.30% 366,008 (1.79) 2,883,821 13.04%

Capital reserve 10,598,201 31.02% 7,889,125 30.91% 2,709,076 0.11 7,889,125 35.67%

Other comprehensive income

309,130 0.90% (726,252) (2.85%) 1,035,382 3.75 10,131 0.05%

Surplus reserve 2,531,957 7.41% 1,970,844 7.72% 561,113 (0.31) 1,486,303 6.72%

General risk reserve

4,054,719 11.87% 2,859,911 11.21% 1,194,808 0.66 1,499,934 6.78%

Retained profits 13,347,261 39.08% 10,629,244 41.65% 2,718,017 (2.57) 8,347,646 37.74%

Equity attributable to shareholders of the bank

34,091,097 99.79% 25,506,693 99.94% 8,584,404 (0.15) 22,116,960 100%

Minority interest

73,115 0.21% 15,195 0.06% 57,920 0.15 - -

Total shareholders' equity

34,164,212 100% 25,521,888 100% 8,642,324 0.00 22,116,960 100%

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

36

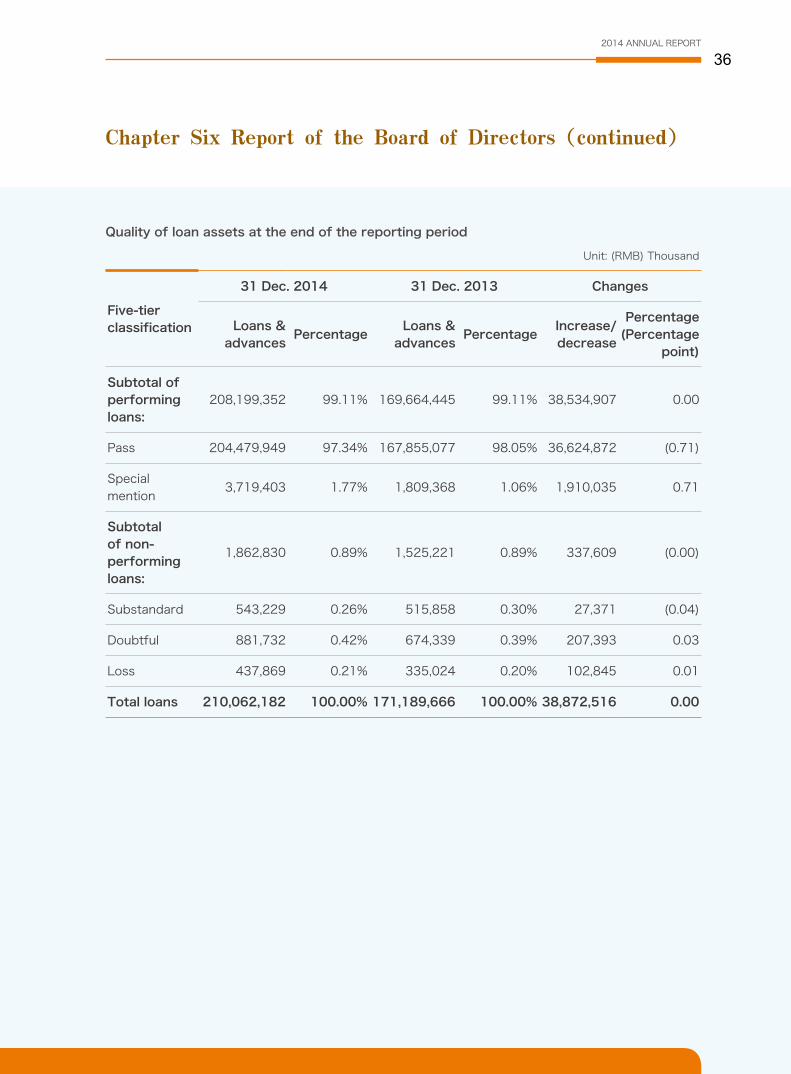

Quality of loan assets at the end of the reporting period

Unit: (RMB) Thousand

Five-tier classification

31 Dec. 2014 31 Dec. 2013 Changes

Loans & advances

PercentageLoans &

advancesPercentage

Increase/decrease

Percentage (Percentage

point)

Subtotal of performing loans:

208,199,352 99.11% 169,664,445 99.11% 38,534,907 0.00

Pass 204,479,949 97.34% 167,855,077 98.05% 36,624,872 (0.71)

Special mention

3,719,403 1.77% 1,809,368 1.06% 1,910,035 0.71

Subtotal of non-performing loans:

1,862,830 0.89% 1,525,221 0.89% 337,609 (0.00)

Substandard 543,229 0.26% 515,858 0.30% 27,371 (0.04)

Doubtful 881,732 0.42% 674,339 0.39% 207,393 0.03

Loss 437,869 0.21% 335,024 0.20% 102,845 0.01

Total loans 210,062,182 100.00% 171,189,666 100.00% 38,872,516 0.00

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

37

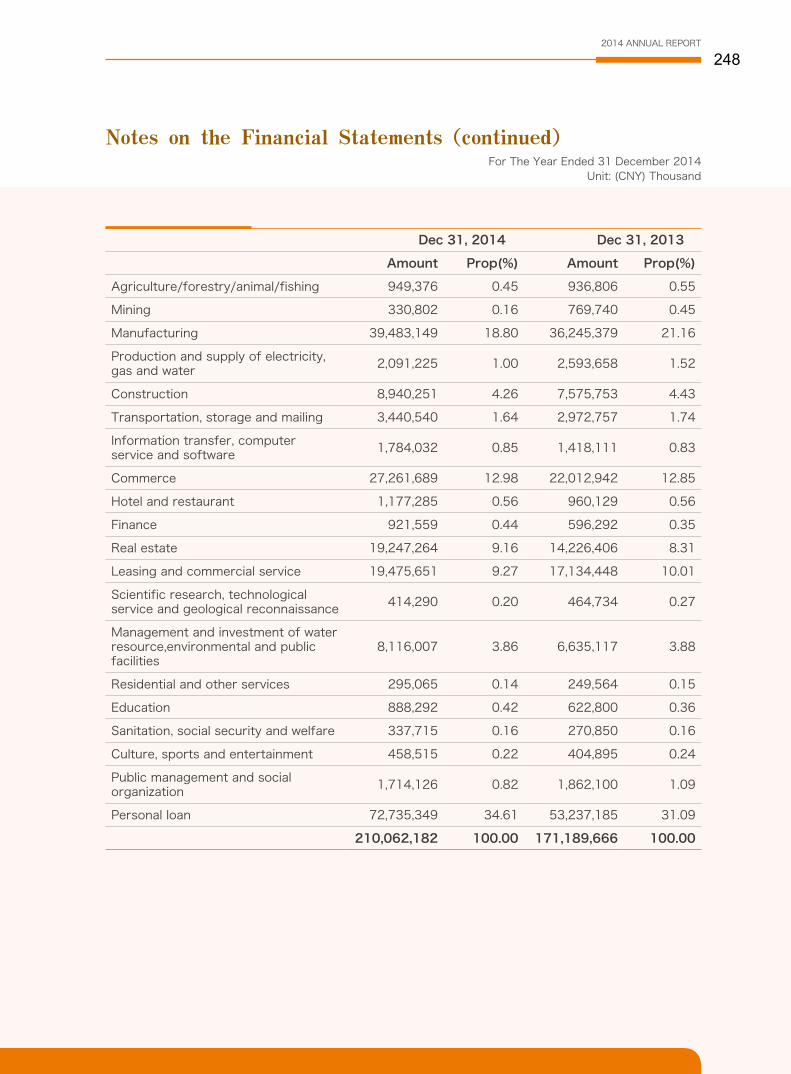

Industry Year 2014

Amount Proportion

Agriculture, forestry, animal husbandry, fishing 949,376 0.45%

Mining 330,802 0.16%

Manufacturing 39,483,149 18.80%

Production & supply of power, gas, water 2,091,225 1.00%

Construction 8,940,251 4.26%

Transportation, storage, mailing 3,440,540 1.64%

Information transfer, computer service and software 1,784,032 0.85%

Commerce 27,261,689 12.98%

Hotel, restaurant 1,177,285 0.56%

Finance 921,559 0.44%

First-hand property mortgage loan for legal persons 8,056 0.00%

Loans for corporate operational property 6,217,764 2.96%

Leasing and commercial service 19,475,651 9.27%

Scientific research, technology service and geological exploitation

414,290 0.20%

Water resource, environment and public facilities management and investment

8,116,007 3.86%

Real estate development 10,751,252 5.12%

Loans for urban construction 2,270,192 1.08%

Resident service and other services 295,065 0.14%

Education 888,292 0.42%

Health, social security and welfare 337,715 0.16%

Culture, sports and entertainment 458,515 0.22%

Public management and social organization 1,714,126 0.82%

Personal loans 72,735,349 34.61%

Total 210,062,182 100.00%

Loan proportion in different industries at the end of the reporting period

Unit: (RMB) Thousand

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

38

Unit: (RMB) Thousand

Unit: (RMB) Thousand

Unit: (RMB) Thousand

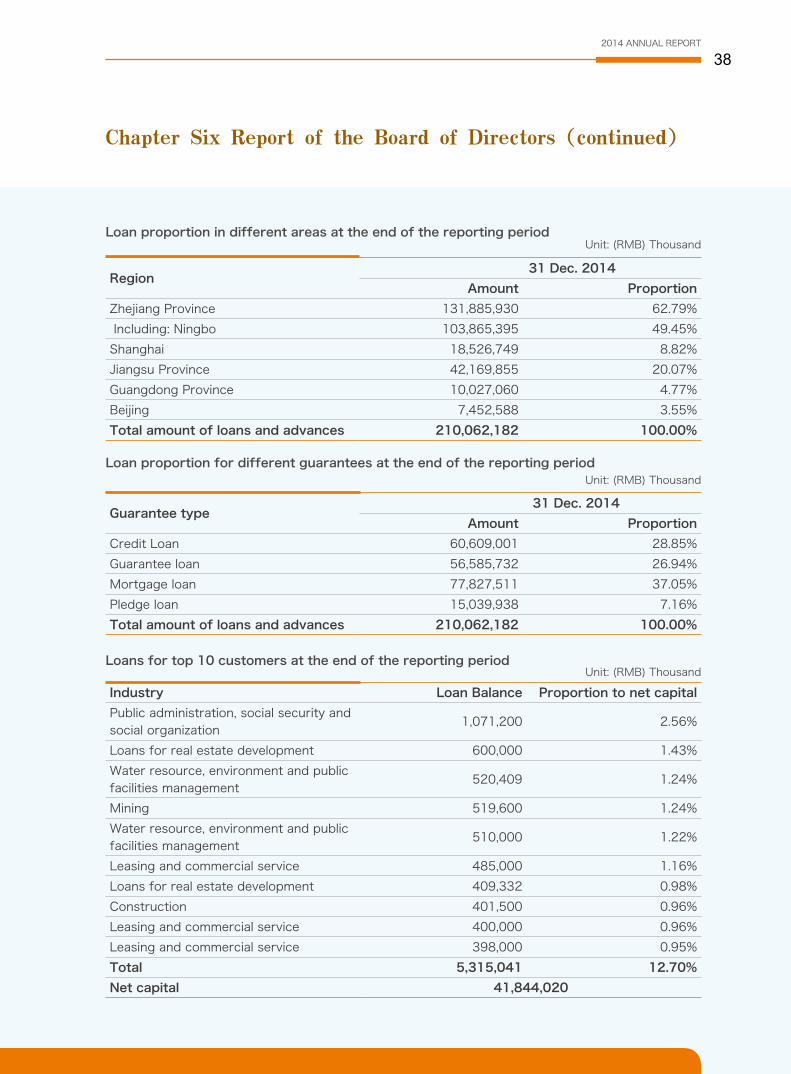

Loan proportion in different areas at the end of the reporting period

Loan proportion for different guarantees at the end of the reporting period

Loans for top 10 customers at the end of the reporting period

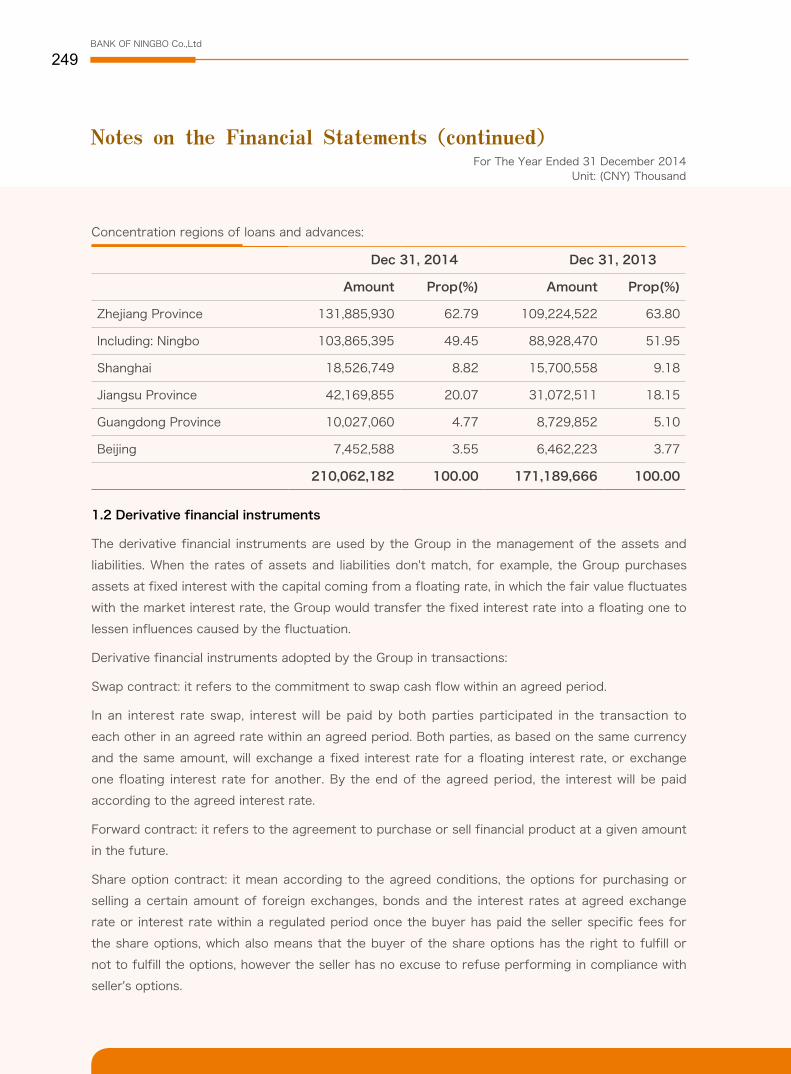

Region 31 Dec. 2014

Amount Proportion

Zhejiang Province 131,885,930 62.79%

Including: Ningbo 103,865,395 49.45%

Shanghai 18,526,749 8.82%

Jiangsu Province 42,169,855 20.07%

Guangdong Province 10,027,060 4.77%

Beijing 7,452,588 3.55%

Total amount of loans and advances 210,062,182 100.00%

Guarantee type 31 Dec. 2014

Amount Proportion

Credit Loan 60,609,001 28.85%

Guarantee loan 56,585,732 26.94%

Mortgage loan 77,827,511 37.05%

Pledge loan 15,039,938 7.16%

Total amount of loans and advances 210,062,182 100.00%

Industry Loan Balance Proportion to net capital

Public administration, social security and social organization

1,071,200 2.56%

Loans for real estate development 600,000 1.43%

Water resource, environment and public facilities management

520,409 1.24%

Mining 519,600 1.24%

Water resource, environment and public facilities management

510,000 1.22%

Leasing and commercial service 485,000 1.16%

Loans for real estate development 409,332 0.98%

Construction 401,500 0.96%

Leasing and commercial service 400,000 0.96%

Leasing and commercial service 398,000 0.95%

Total 5,315,041 12.70%

Net capital 41,844,020

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

39

Unit: (RMB) Thousand

Unit: (RMB) Thousand

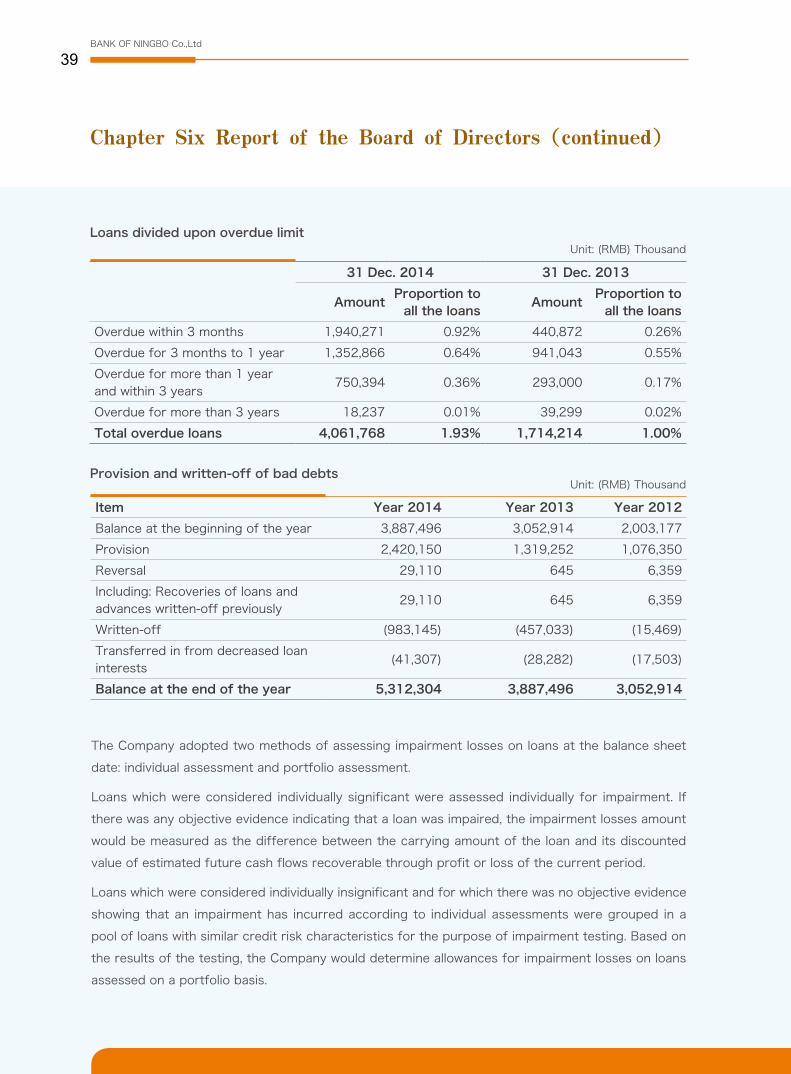

Loans divided upon overdue limit

Provision and written-off of bad debts

The Company adopted two methods of assessing impairment losses on loans at the balance sheet

date: individual assessment and portfolio assessment.

Loans which were considered individually significant were assessed individually for impairment. If

there was any objective evidence indicating that a loan was impaired, the impairment losses amount

would be measured as the difference between the carrying amount of the loan and its discounted

value of estimated future cash flows recoverable through profit or loss of the current period.

Loans which were considered individually insignificant and for which there was no objective evidence

showing that an impairment has incurred according to individual assessments were grouped in a

pool of loans with similar credit risk characteristics for the purpose of impairment testing. Based on

the results of the testing, the Company would determine allowances for impairment losses on loans

assessed on a portfolio basis.

31 Dec. 2014 31 Dec. 2013

AmountProportion to

all the loansAmount

Proportion to all the loans

Overdue within 3 months 1,940,271 0.92% 440,872 0.26%

Overdue for 3 months to 1 year 1,352,866 0.64% 941,043 0.55%

Overdue for more than 1 year and within 3 years

750,394 0.36% 293,000 0.17%

Overdue for more than 3 years 18,237 0.01% 39,299 0.02%

Total overdue loans 4,061,768 1.93% 1,714,214 1.00%

Item Year 2014 Year 2013 Year 2012

Balance at the beginning of the year 3,887,496 3,052,914 2,003,177

Provision 2,420,150 1,319,252 1,076,350

Reversal 29,110 645 6,359

Including: Recoveries of loans and advances written-off previously

29,110 645 6,359

Written-off (983,145) (457,033) (15,469)

Transferred in from decreased loan interests

(41,307) (28,282) (17,503)

Balance at the end of the year 5,312,304 3,887,496 3,052,914

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

40

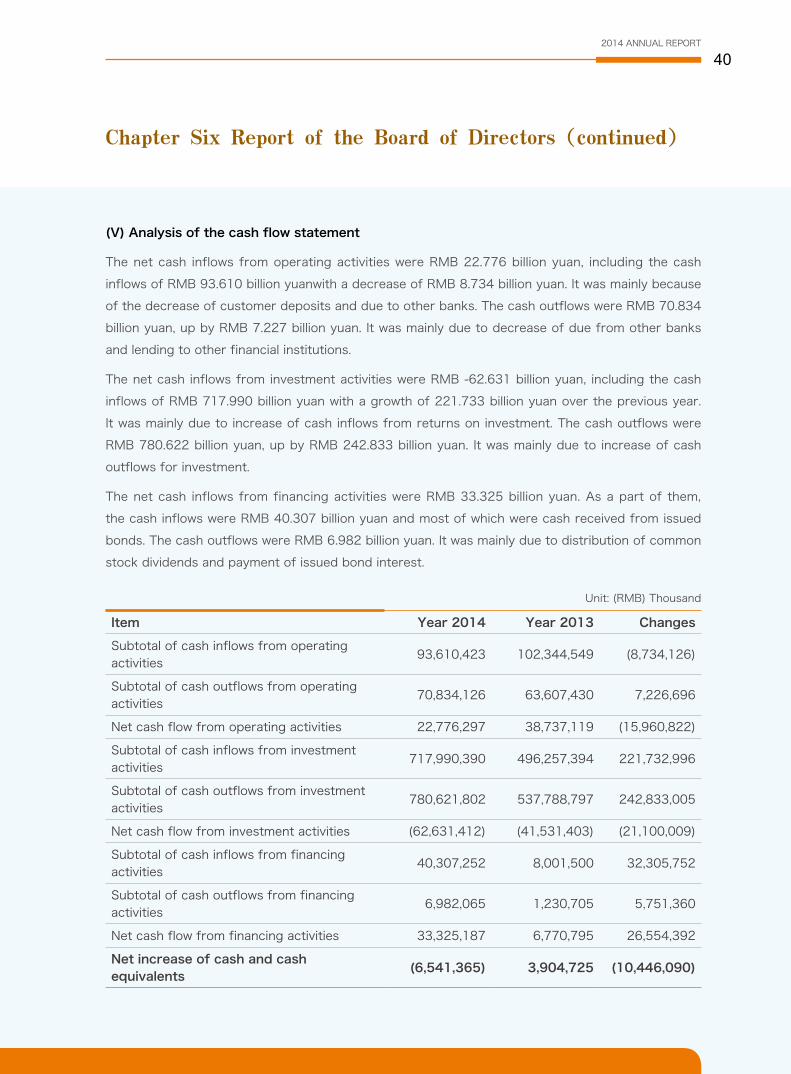

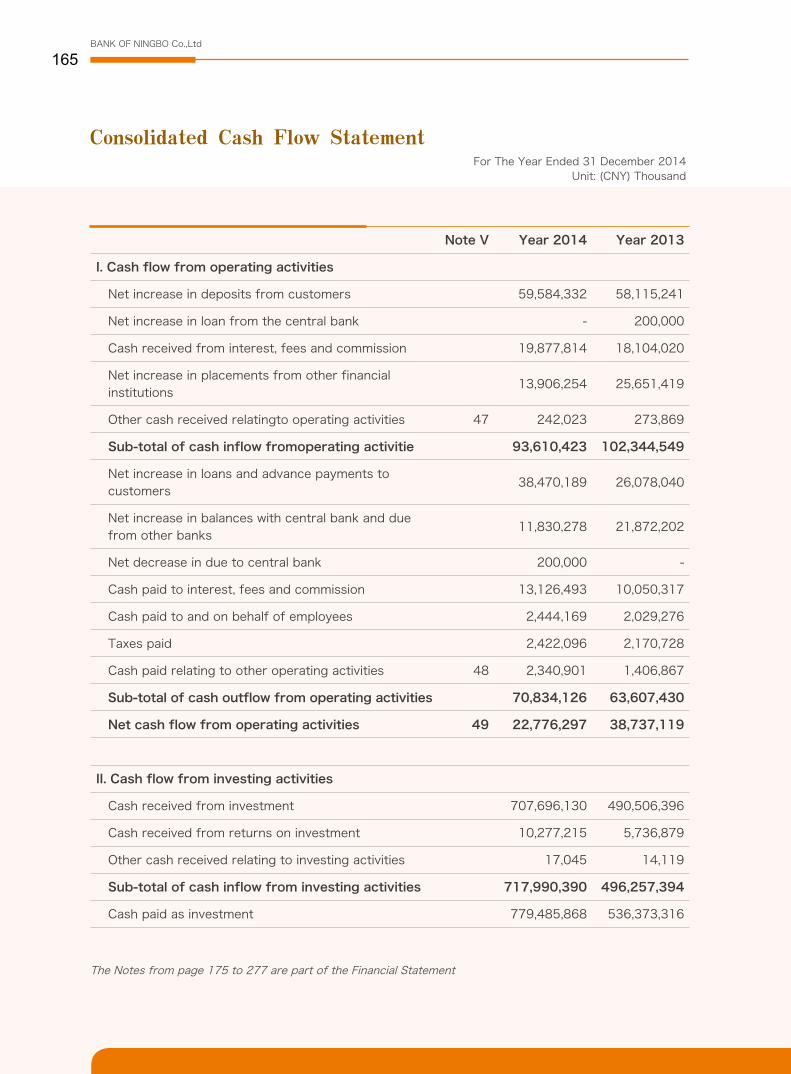

(V) Analysis of the cash flow statement

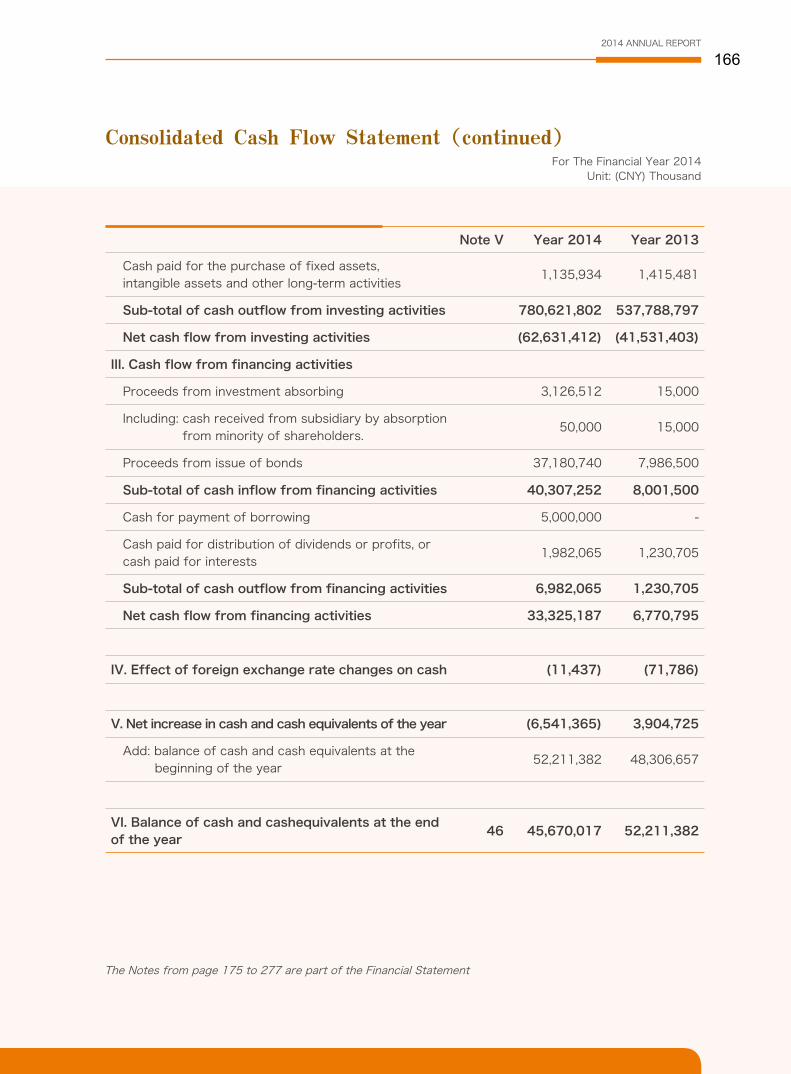

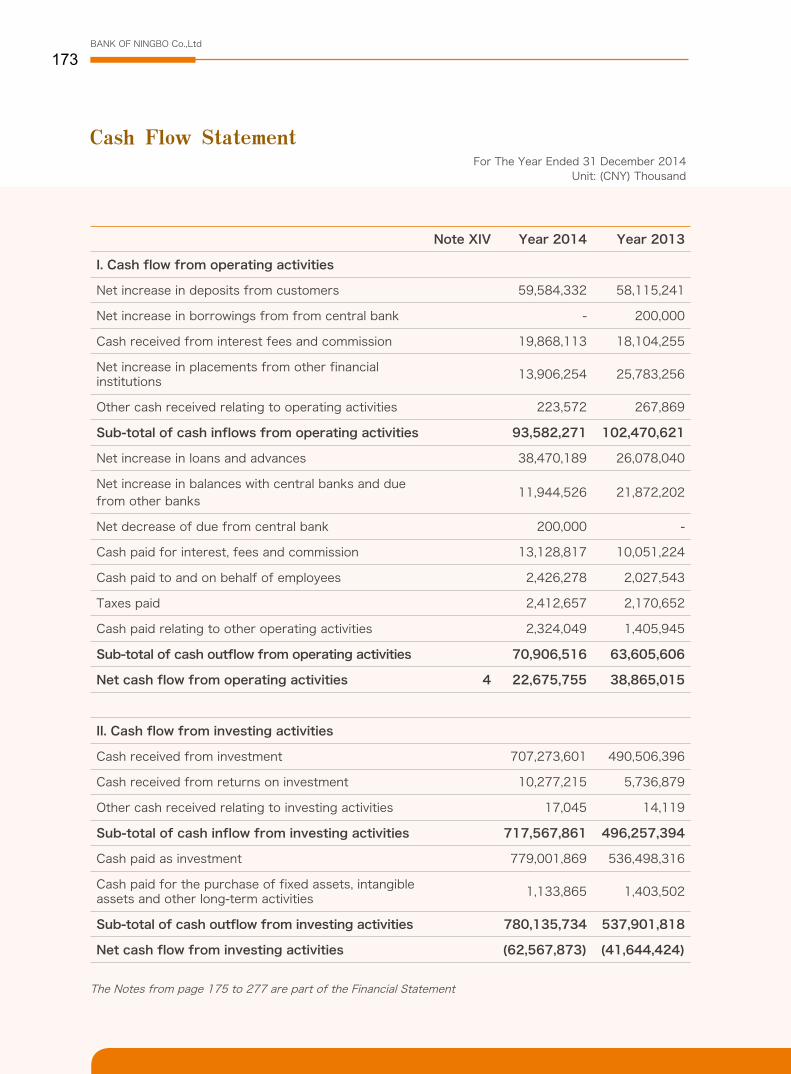

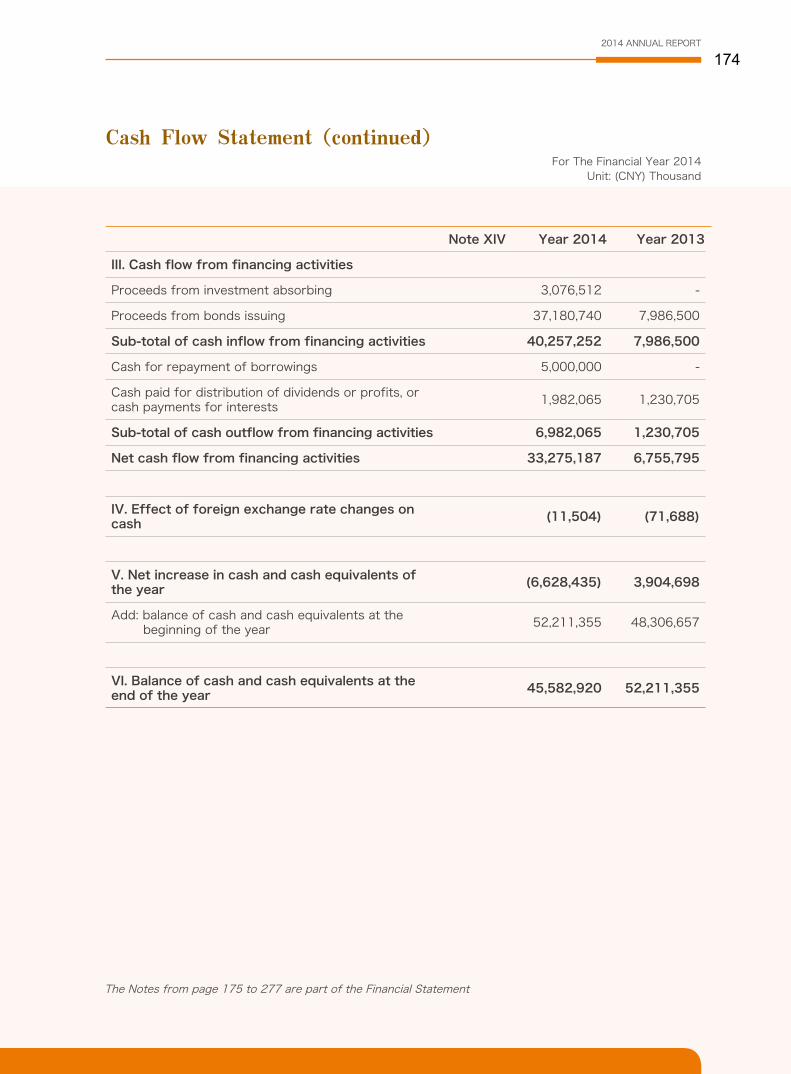

The net cash inflows from operating activities were RMB 22.776 billion yuan, including the cash

inflows of RMB 93.610 billion yuanwith a decrease of RMB 8.734 billion yuan. It was mainly because

of the decrease of customer deposits and due to other banks. The cash outflows were RMB 70.834

billion yuan, up by RMB 7.227 billion yuan. It was mainly due to decrease of due from other banks

and lending to other financial institutions.

The net cash inflows from investment activities were RMB -62.631 billion yuan, including the cash

inflows of RMB 717.990 billion yuan with a growth of 221.733 billion yuan over the previous year.

It was mainly due to increase of cash inflows from returns on investment. The cash outflows were

RMB 780.622 billion yuan, up by RMB 242.833 billion yuan. It was mainly due to increase of cash

outflows for investment.

The net cash inflows from financing activities were RMB 33.325 billion yuan. As a part of them,

the cash inflows were RMB 40.307 billion yuan and most of which were cash received from issued

bonds. The cash outflows were RMB 6.982 billion yuan. It was mainly due to distribution of common

stock dividends and payment of issued bond interest.

Unit: (RMB) Thousand

Item Year 2014 Year 2013 Changes

Subtotal of cash inflows from operating activities

93,610,423 102,344,549 (8,734,126)

Subtotal of cash outflows from operating activities

70,834,126 63,607,430 7,226,696

Net cash flow from operating activities 22,776,297 38,737,119 (15,960,822)

Subtotal of cash inflows from investment activities

717,990,390 496,257,394 221,732,996

Subtotal of cash outflows from investment activities

780,621,802 537,788,797 242,833,005

Net cash flow from investment activities (62,631,412) (41,531,403) (21,100,009)

Subtotal of cash inflows from financing activities

40,307,252 8,001,500 32,305,752

Subtotal of cash outflows from financing activities

6,982,065 1,230,705 5,751,360

Net cash flow from financing activities 33,325,187 6,770,795 26,554,392

Net increase of cash and cash equivalents

(6,541,365) 3,904,725 (10,446,090)

Chapter Six Report of the Board of Directors(continued)

BANK OF NINGBO Co.,Ltd

41

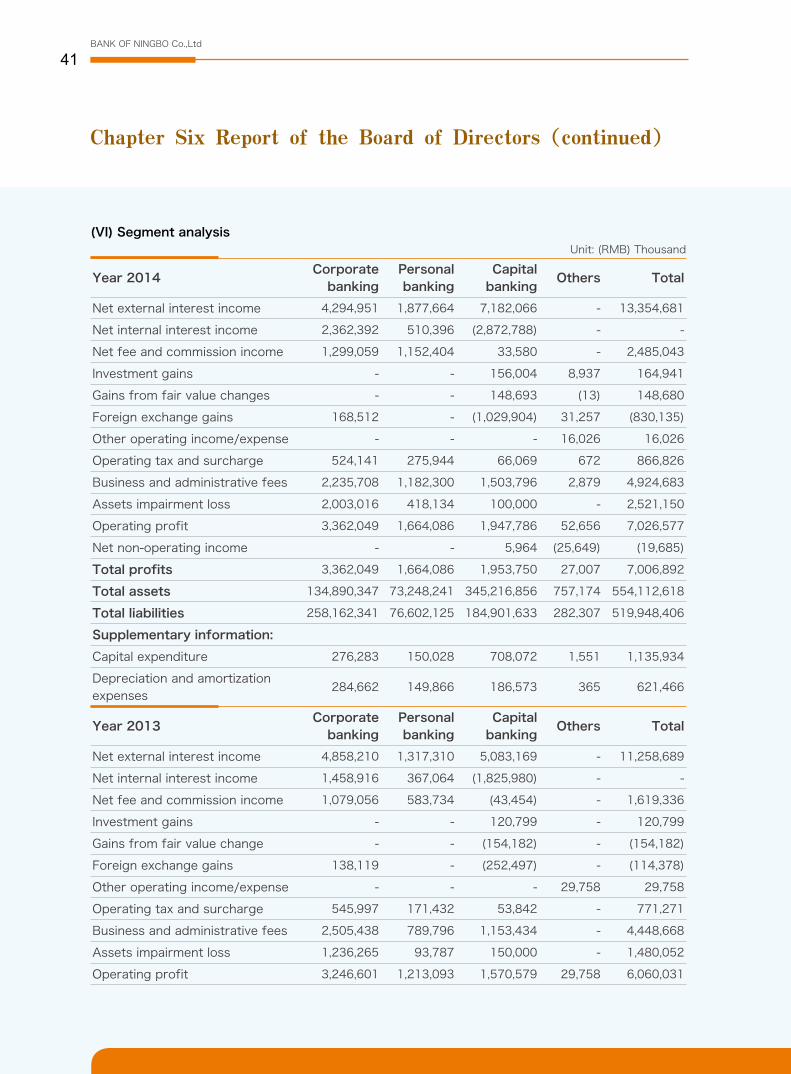

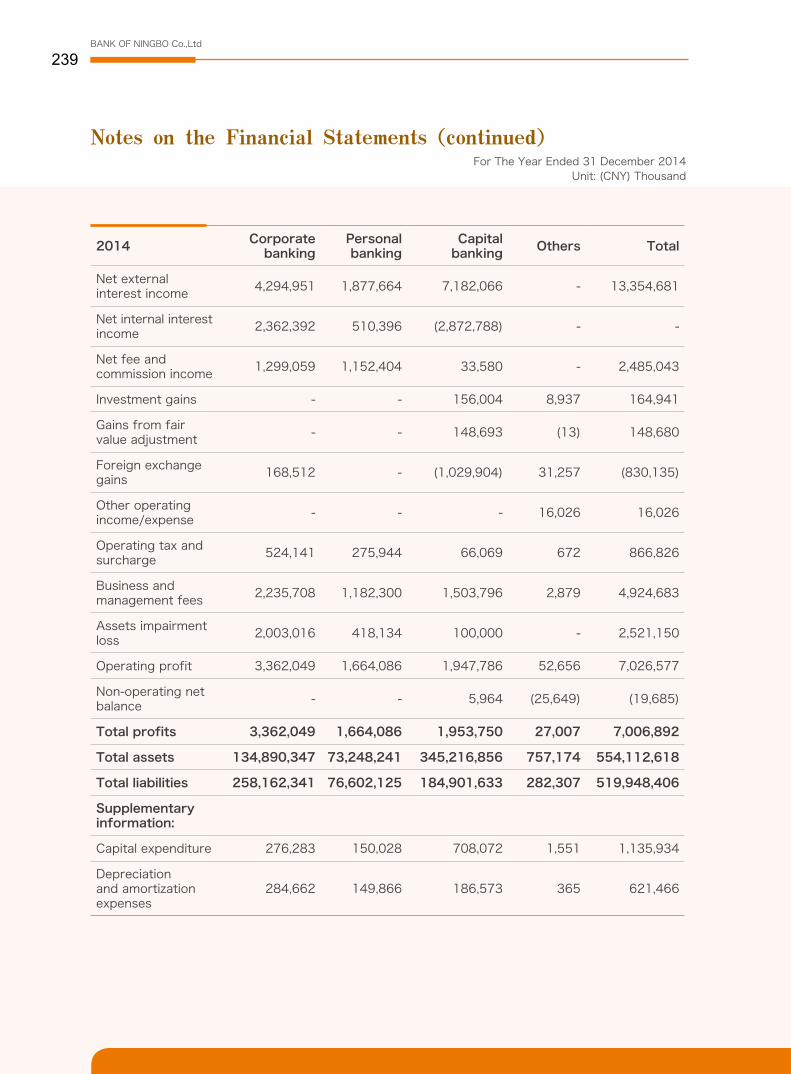

(VI) Segment analysisUnit: (RMB) Thousand

Year 2014Corporate

bankingPersonal banking

Capital banking

Others Total

Net external interest income 4,294,951 1,877,664 7,182,066 - 13,354,681

Net internal interest income 2,362,392 510,396 (2,872,788) - -

Net fee and commission income 1,299,059 1,152,404 33,580 - 2,485,043

Investment gains - - 156,004 8,937 164,941

Gains from fair value changes - - 148,693 (13) 148,680

Foreign exchange gains 168,512 - (1,029,904) 31,257 (830,135)

Other operating income/expense - - - 16,026 16,026

Operating tax and surcharge 524,141 275,944 66,069 672 866,826

Business and administrative fees 2,235,708 1,182,300 1,503,796 2,879 4,924,683

Assets impairment loss 2,003,016 418,134 100,000 - 2,521,150

Operating profit 3,362,049 1,664,086 1,947,786 52,656 7,026,577

Net non-operating income - - 5,964 (25,649) (19,685)

Total profits 3,362,049 1,664,086 1,953,750 27,007 7,006,892

Total assets 134,890,347 73,248,241 345,216,856 757,174 554,112,618

Total liabilities 258,162,341 76,602,125 184,901,633 282,307 519,948,406

Supplementary information:

Capital expenditure 276,283 150,028 708,072 1,551 1,135,934

Depreciation and amortization expenses

284,662 149,866 186,573 365 621,466

Year 2013Corporate

bankingPersonal banking

Capital banking

Others Total

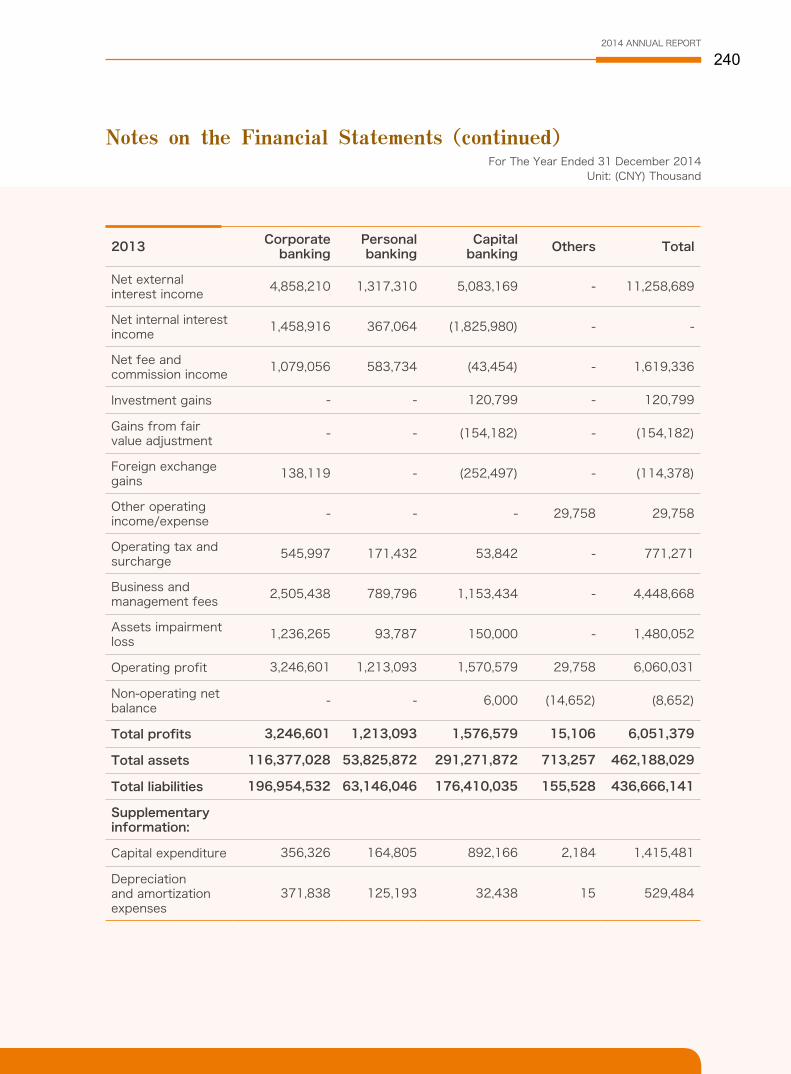

Net external interest income 4,858,210 1,317,310 5,083,169 - 11,258,689

Net internal interest income 1,458,916 367,064 (1,825,980) - -

Net fee and commission income 1,079,056 583,734 (43,454) - 1,619,336

Investment gains - - 120,799 - 120,799

Gains from fair value change - - (154,182) - (154,182)

Foreign exchange gains 138,119 - (252,497) - (114,378)

Other operating income/expense - - - 29,758 29,758

Operating tax and surcharge 545,997 171,432 53,842 - 771,271

Business and administrative fees 2,505,438 789,796 1,153,434 - 4,448,668

Assets impairment loss 1,236,265 93,787 150,000 - 1,480,052

Operating profit 3,246,601 1,213,093 1,570,579 29,758 6,060,031

Chapter Six Report of the Board of Directors(continued)

2014 ANNUAL REPORT

42

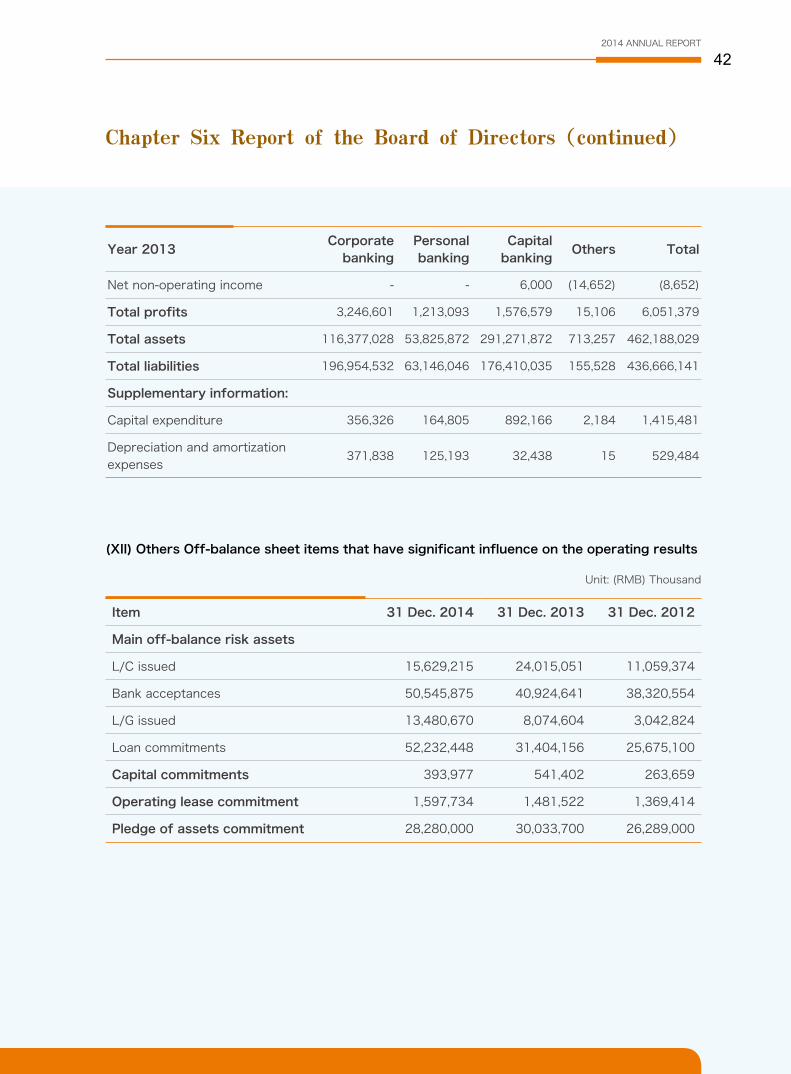

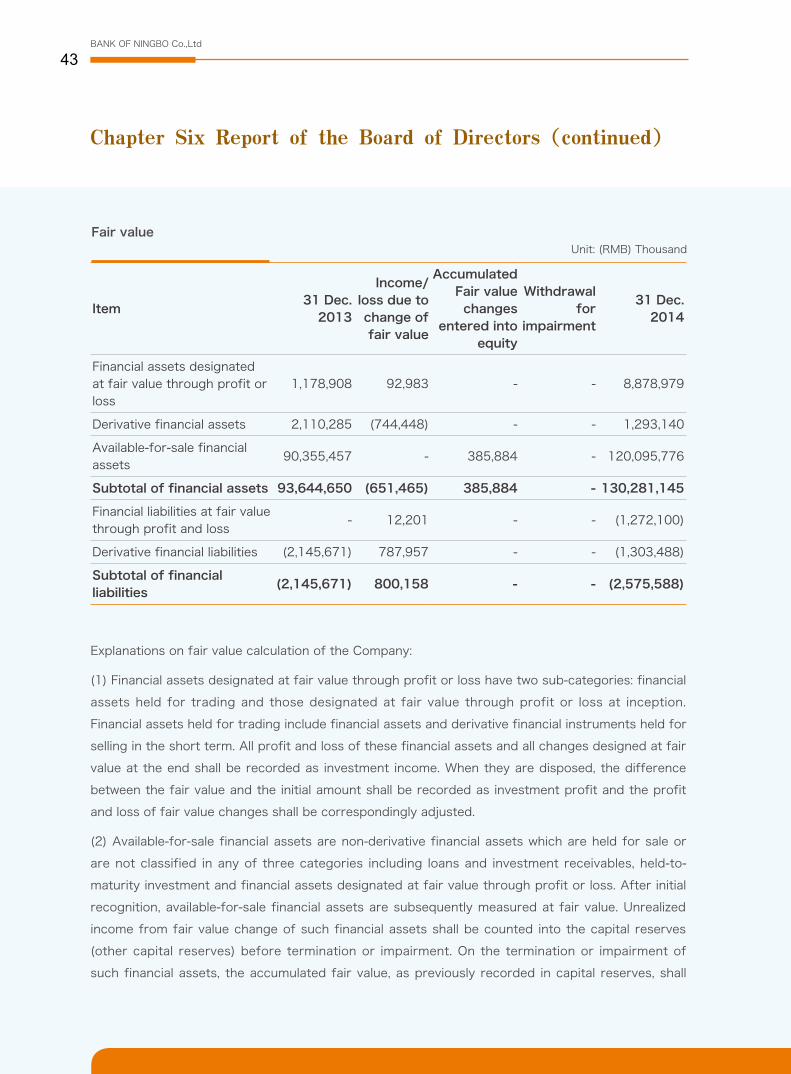

(XII) Others Off-balance sheet items that have significant influence on the operating results

Unit: (RMB) Thousand

Year 2013Corporate

bankingPersonal banking

Capital banking

Others Total