2014 ABCs of School Choice Paul DiPerna [email protected] International School Choice and Reform Academic Conference January 18, 2014 Ft. Lauderdale, FL

2014 ABCs of School Choice: Comparative Views on Choice in Districts and States (2014)

Jul 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2014 ABCs of School Choice

Paul DiPerna

International School Choice

and Reform Academic Conference

January 18, 2014

Ft. Lauderdale, FL

About the Friedman Foundation

edchoice.org

• Est. in 1996 by Milton & Rose Friedman

• Based Indianapolis, IN

• Annual Activities/Services in 30+ states

• 501(c)(3) / Nonpartisan / Nonprofit

• What do we do?

Outreach ~ Education

Research ~ Data Analysis

Advocacy ~ Marketing

Overview

1. Defining school choice, program types

2. Data challenges/limitations

3. National snapshots

4. Program indicators and comparisons

= eligibility, participation, funding, regulations

≠ academic outcomes; fiscal/financial outcomes; civic outcomes

5. Takeaways

What we mean by “school choice”

• Separate the public education funding

mechanism from the administration and

operation of schools, and minimize the inherent

conflict of interest in such arrangements.

• The direction and flow of education funding

should follow the student to whichever school –

public or private – that family feels is best to meet

the child’s needs and priorities.

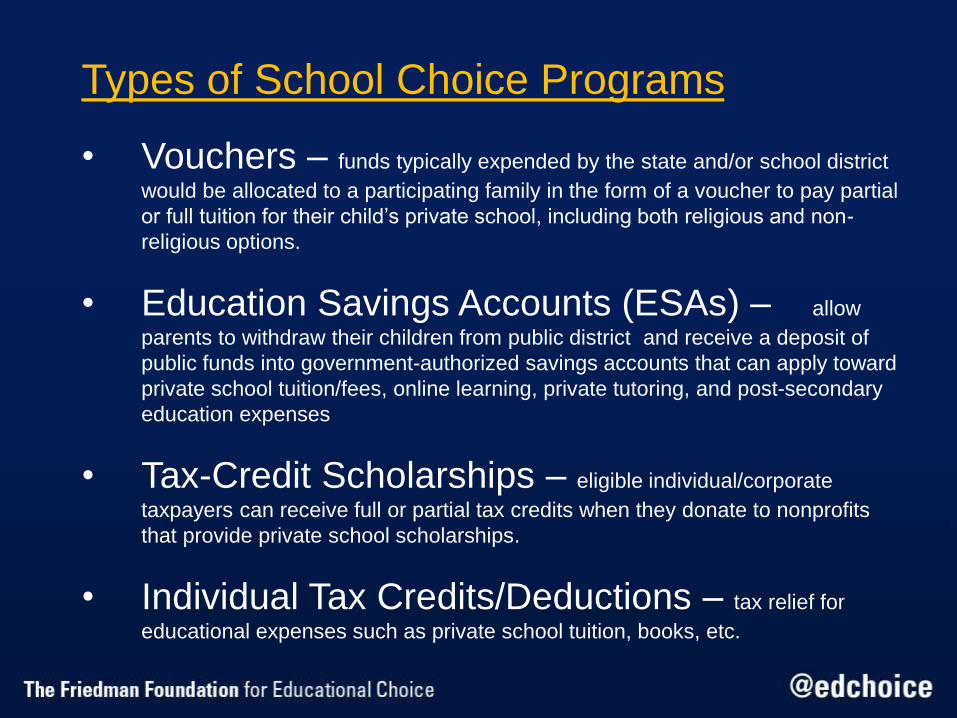

Types of School Choice Programs

• Vouchers – funds typically expended by the state and/or school district

would be allocated to a participating family in the form of a voucher to pay partial

or full tuition for their child’s private school, including both religious and non-

religious options.

• Education Savings Accounts (ESAs) – allow

parents to withdraw their children from public district and receive a deposit of

public funds into government-authorized savings accounts that can apply toward

private school tuition/fees, online learning, private tutoring, and post-secondary

education expenses

• Tax-Credit Scholarships – eligible individual/corporate

taxpayers can receive full or partial tax credits when they donate to nonprofits

that provide private school scholarships.

• Individual Tax Credits/Deductions – tax relief for

educational expenses such as private school tuition, books, etc.

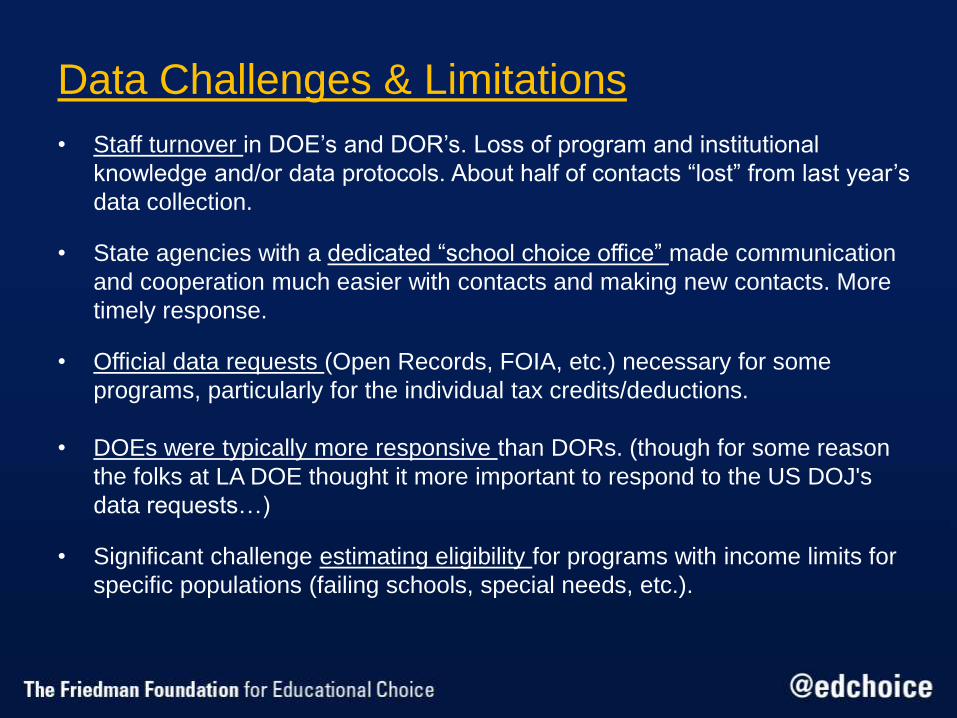

Data Challenges & Limitations

• Staff turnover in DOE’s and DOR’s. Loss of program and institutional

knowledge and/or data protocols. About half of contacts “lost” from last year’s

data collection.

• State agencies with a dedicated “school choice office” made communication

and cooperation much easier with contacts and making new contacts. More

timely response.

• Official data requests (Open Records, FOIA, etc.) necessary for some

programs, particularly for the individual tax credits/deductions.

• DOEs were typically more responsive than DORs. (though for some reason

the folks at LA DOE thought it more important to respond to the US DOJ's

data requests…)

• Significant challenge estimating eligibility for programs with income limits for

specific populations (failing schools, special needs, etc.).

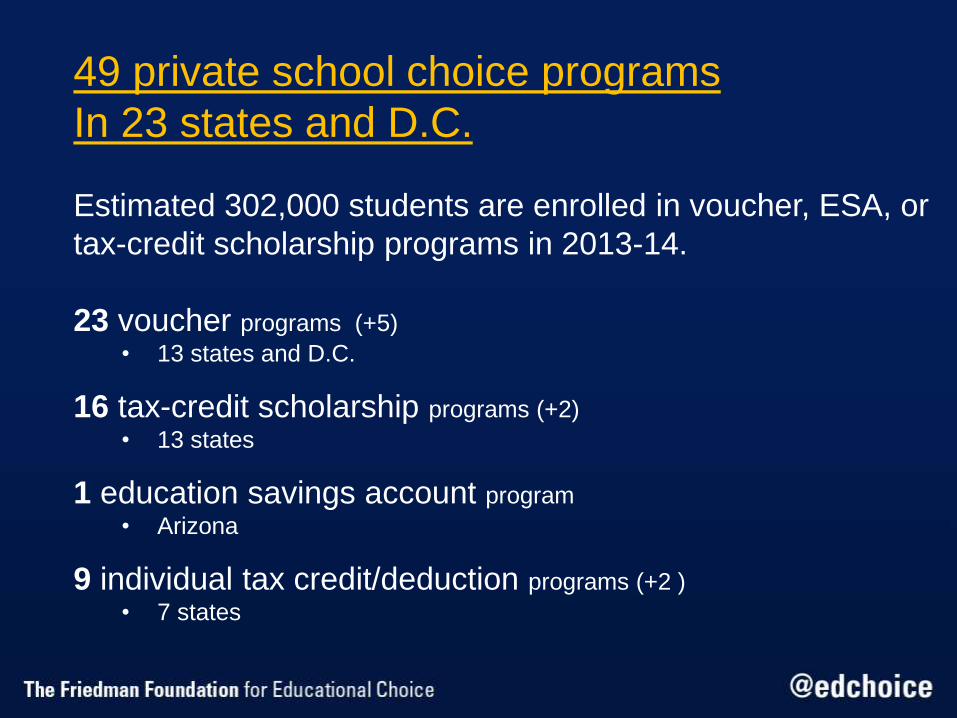

49 private school choice programs

In 23 states and D.C.

Estimated 302,000 students are enrolled in voucher, ESA, or

tax-credit scholarship programs in 2013-14.

23 voucher programs (+5)

• 13 states and D.C.

16 tax-credit scholarship programs (+2)

• 13 states

1 education savings account program

• Arizona

9 individual tax credit/deduction programs (+2 )

• 7 states

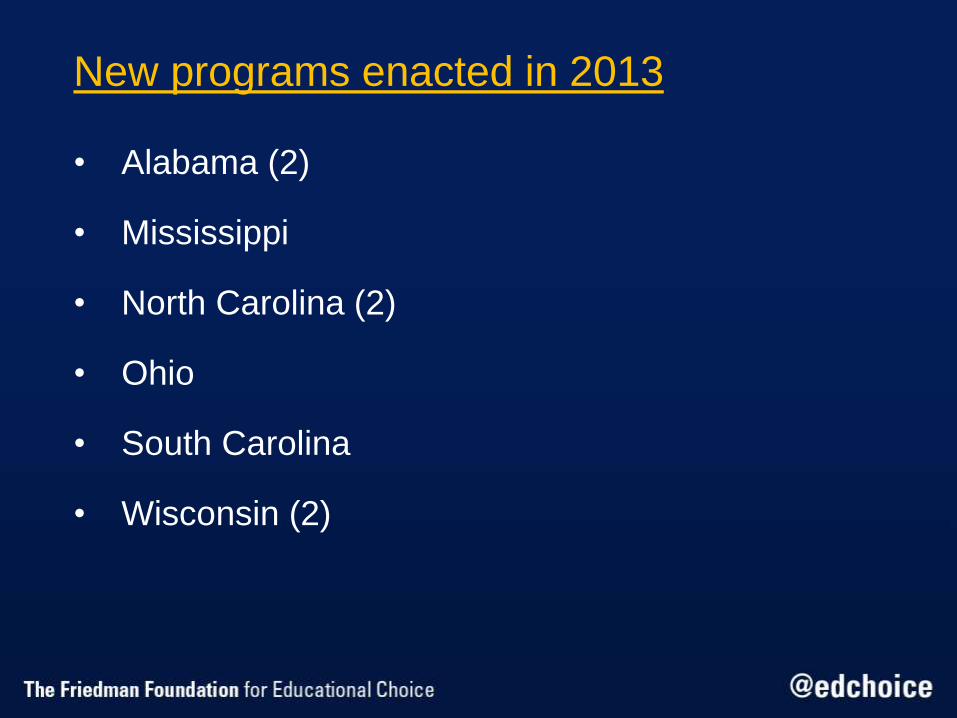

New programs enacted in 2013

• Alabama (2)

• Mississippi

• North Carolina (2)

• Ohio

• South Carolina

• Wisconsin (2)

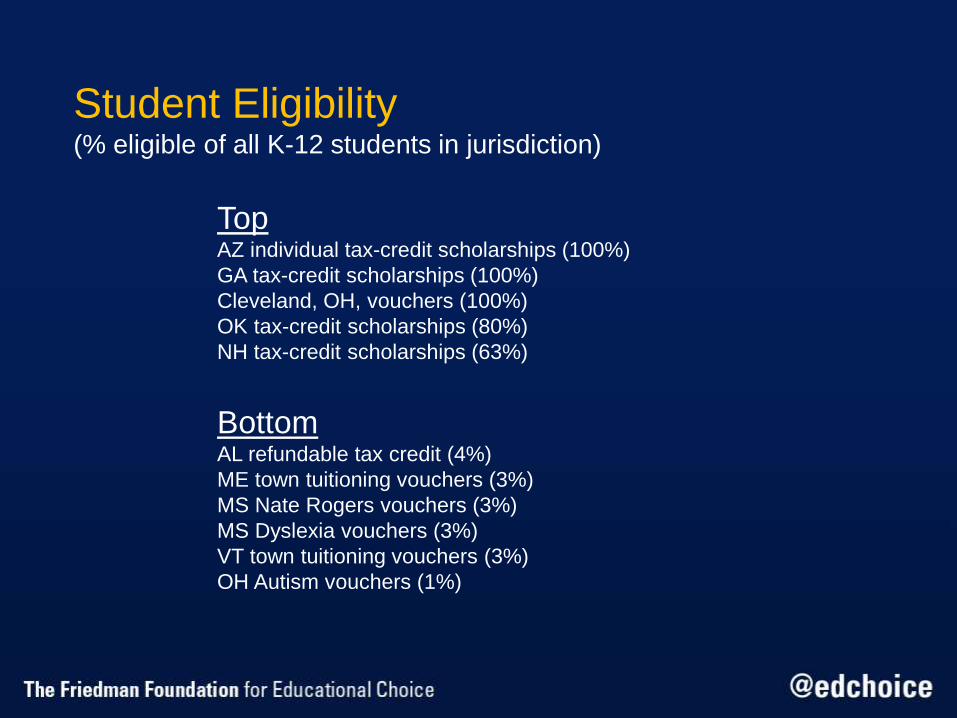

Student Eligibility (% eligible of all K-12 students in jurisdiction)

TopAZ individual tax-credit scholarships (100%)

GA tax-credit scholarships (100%)

Cleveland, OH, vouchers (100%)

OK tax-credit scholarships (80%)

NH tax-credit scholarships (63%)

BottomAL refundable tax credit (4%)

ME town tuitioning vouchers (3%)

MS Nate Rogers vouchers (3%)

MS Dyslexia vouchers (3%)

VT town tuitioning vouchers (3%)

OH Autism vouchers (1%)

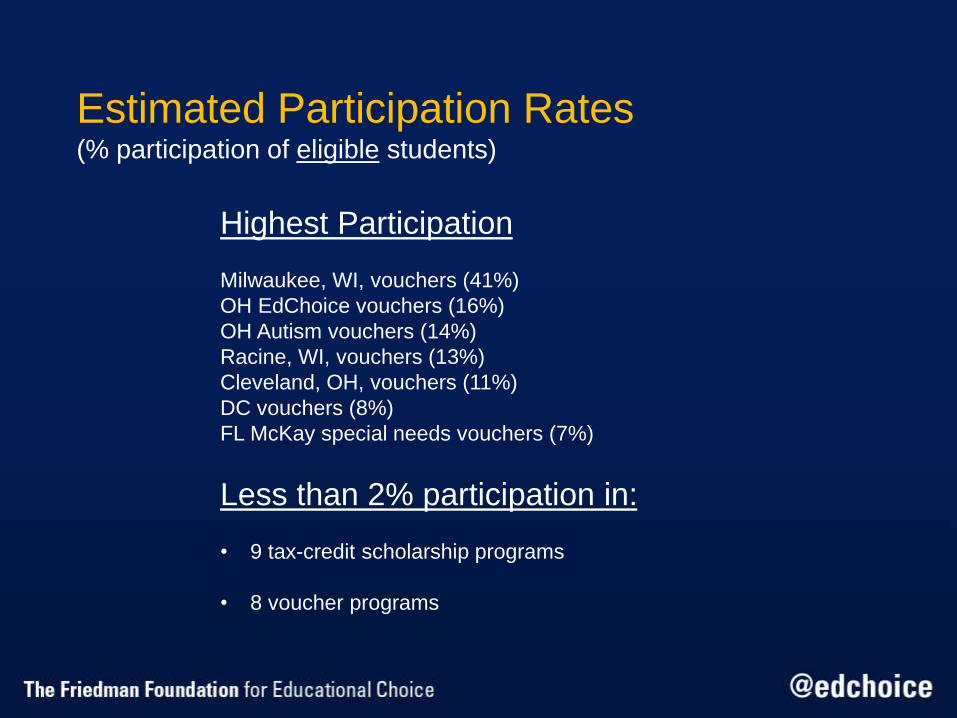

Estimated Participation Rates(% participation of eligible students)

Highest Participation

Milwaukee, WI, vouchers (41%)

OH EdChoice vouchers (16%)

OH Autism vouchers (14%)

Racine, WI, vouchers (13%)

Cleveland, OH, vouchers (11%)

DC vouchers (8%)

FL McKay special needs vouchers (7%)

Less than 2% participation in:

• 9 tax-credit scholarship programs

• 8 voucher programs

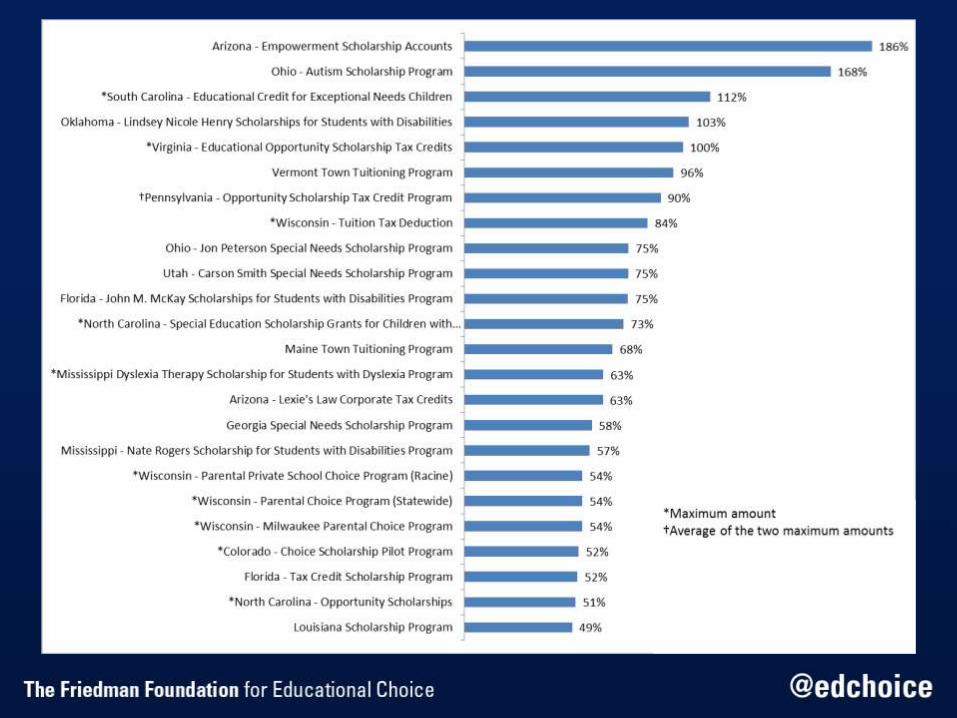

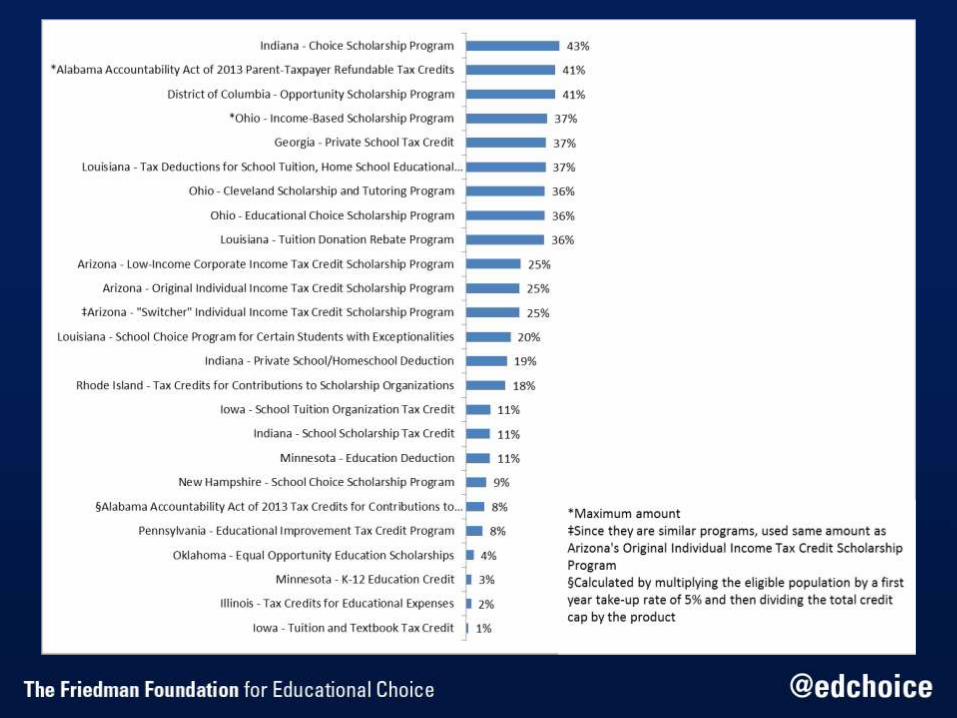

Student Funding(considering the average voucher/scholarship value

as percentage of state’s total per-student spending)

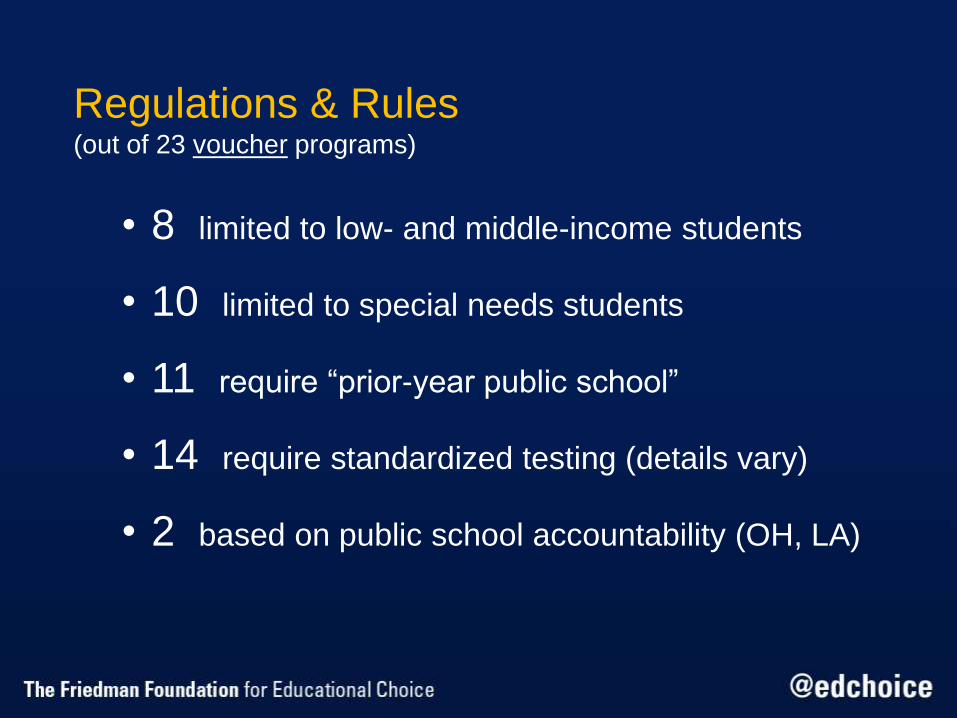

Regulations & Rules(out of 23 voucher programs)

• 8 limited to low- and middle-income students

• 10 limited to special needs students

• 11 require “prior-year public school”

• 14 require standardized testing (details vary)

• 2 based on public school accountability (OH, LA)

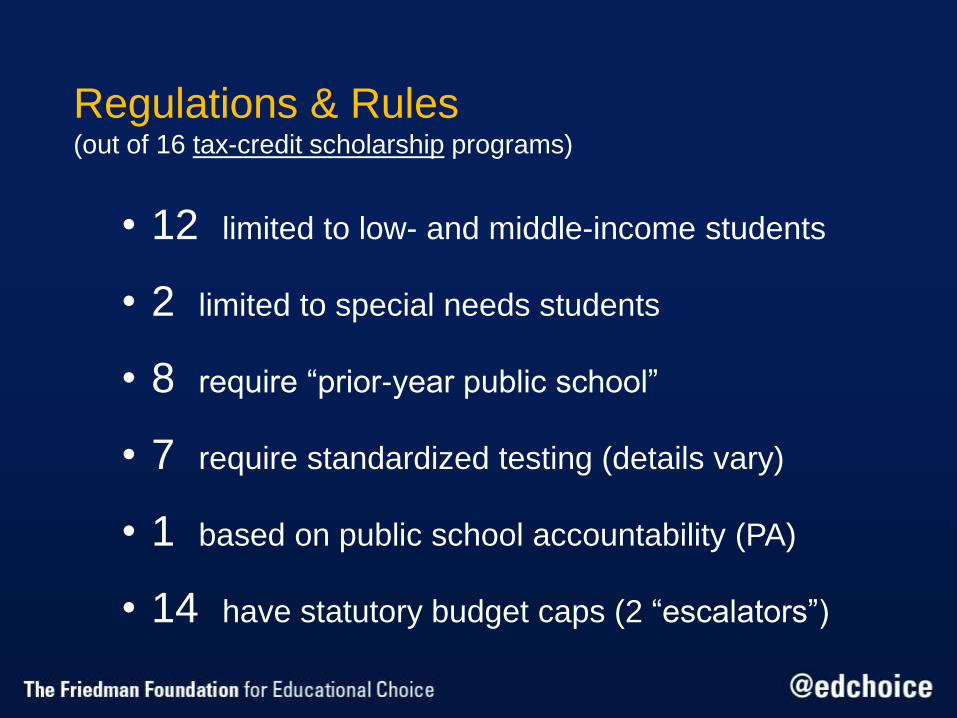

Regulations & Rules(out of 16 tax-credit scholarship programs)

• 12 limited to low- and middle-income students

• 2 limited to special needs students

• 8 require “prior-year public school”

• 7 require standardized testing (details vary)

• 1 based on public school accountability (PA)

• 14 have statutory budget caps (2 “escalators”)

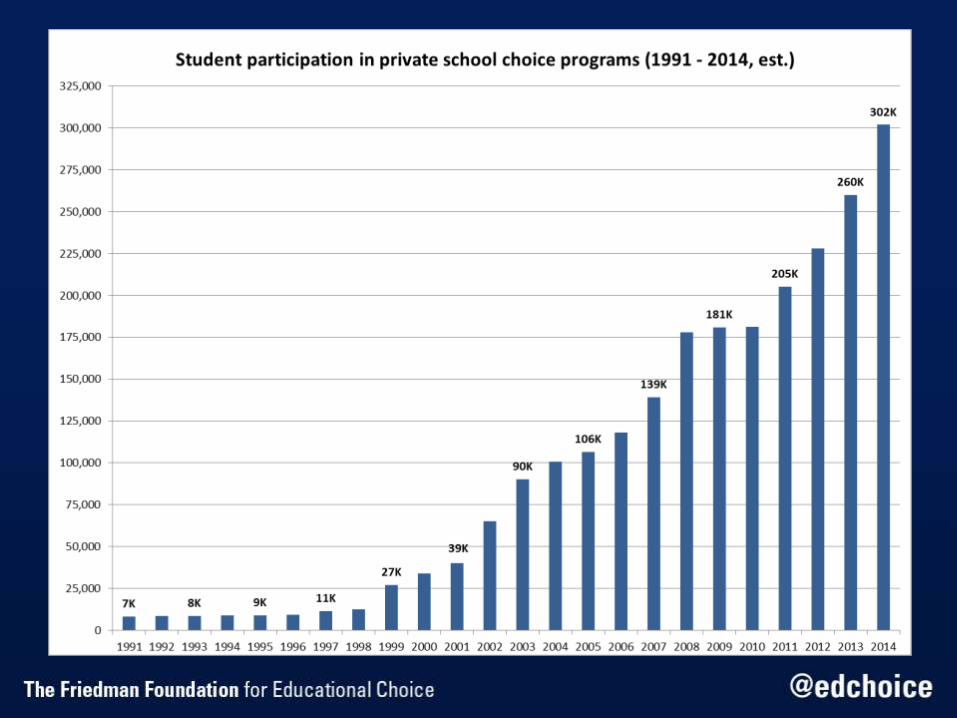

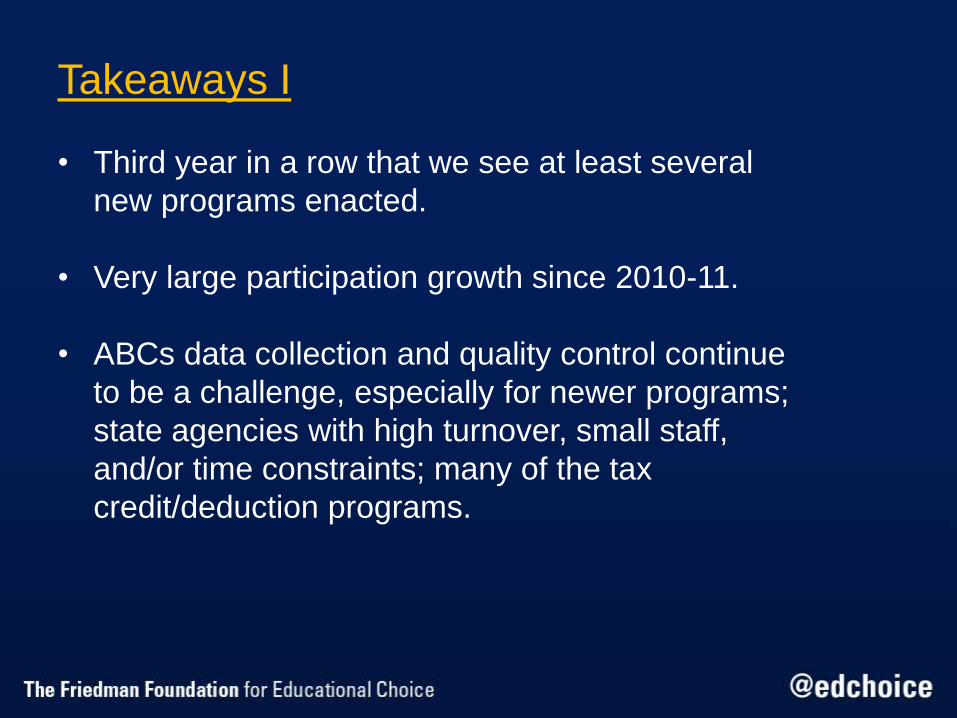

Takeaways I

• Third year in a row that we see at least several

new programs enacted.

• Very large participation growth since 2010-11.

• ABCs data collection and quality control continue

to be a challenge, especially for newer programs;

state agencies with high turnover, small staff,

and/or time constraints; many of the tax

credit/deduction programs.

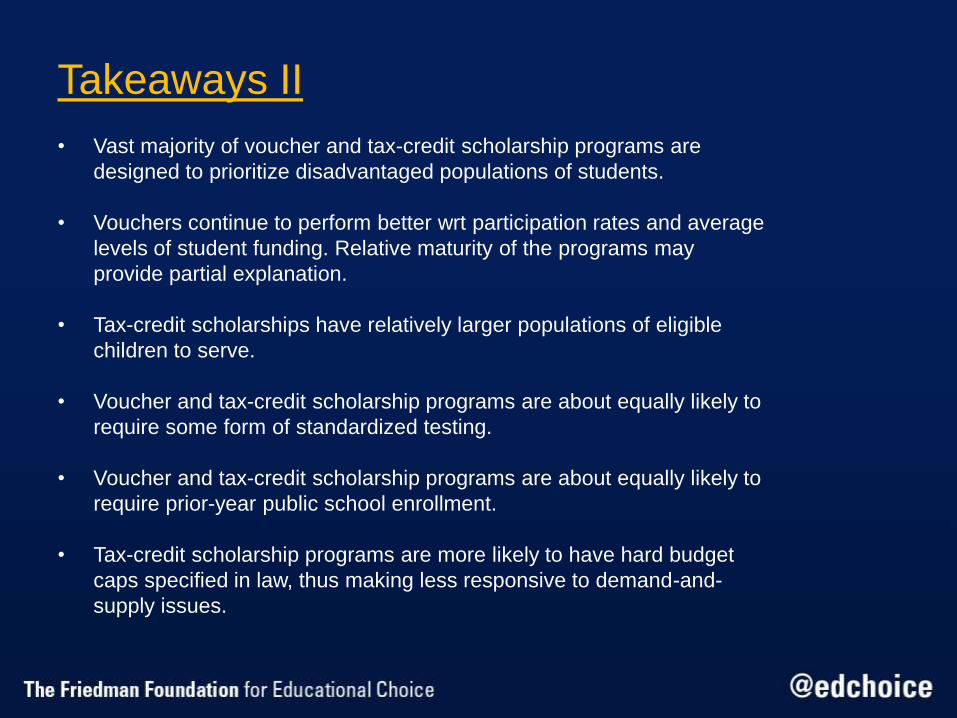

Takeaways II

• Vast majority of voucher and tax-credit scholarship programs are

designed to prioritize disadvantaged populations of students.

• Vouchers continue to perform better wrt participation rates and average

levels of student funding. Relative maturity of the programs may

provide partial explanation.

• Tax-credit scholarships have relatively larger populations of eligible

children to serve.

• Voucher and tax-credit scholarship programs are about equally likely to

require some form of standardized testing.

• Voucher and tax-credit scholarship programs are about equally likely to

require prior-year public school enrollment.

• Tax-credit scholarship programs are more likely to have hard budget

caps specified in law, thus making less responsive to demand-and-

supply issues.

Related Documents