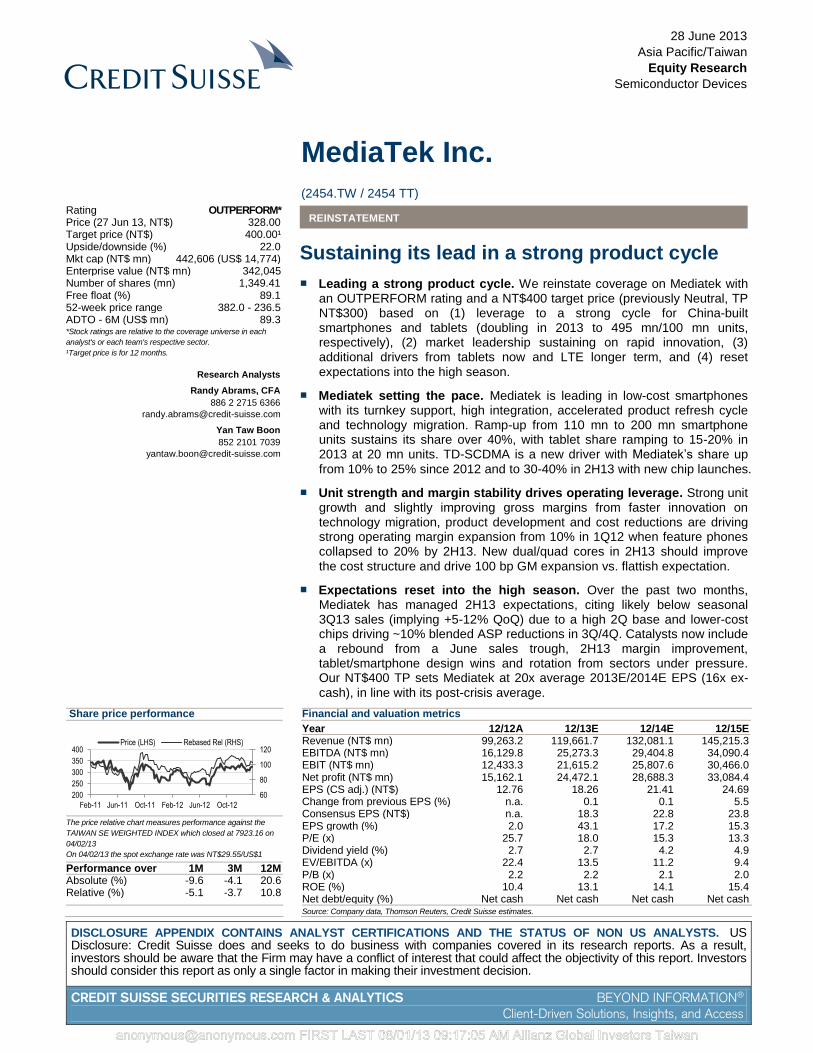

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 28 June 2013 Asia Pacific/Taiwan Equity Research Semiconductor Devices MediaTek Inc. (2454.TW / 2454 TT) REINSTATEMENT Sustaining its lead in a strong product cycle ■ Leading a strong product cycle. We reinstate coverage on Mediatek with an OUTPERFORM rating and a NT$400 target price (previously Neutral, TP NT$300) based on (1) leverage to a strong cycle for China-built smartphones and tablets (doubling in 2013 to 495 mn/100 mn units, respectively), (2) market leadership sustaining on rapid innovation, (3) additional drivers from tablets now and LTE longer term, and (4) reset expectations into the high season. ■ Mediatek setting the pace. Mediatek is leading in low-cost smartphones with its turnkey support, high integration, accelerated product refresh cycle and technology migration. Ramp-up from 110 mn to 200 mn smartphone units sustains its share over 40%, with tablet share ramping to 15-20% in 2013 at 20 mn units. TD-SCDMA is a new driver with Mediatek’s share up from 10% to 25% since 2012 and to 30-40% in 2H13 with new chip launches. ■ Unit strength and margin stability drives operating leverage. Strong unit growth and slightly improving gross margins from faster innovation on technology migration, product development and cost reductions are driving strong operating margin expansion from 10% in 1Q12 when feature phones collapsed to 20% by 2H13. New dual/quad cores in 2H13 should improve the cost structure and drive 100 bp GM expansion vs. flattish expectation. ■ Expectations reset into the high season. Over the past two months, Mediatek has managed 2H13 expectations, citing likely below seasonal 3Q13 sales (implying +5-12% QoQ) due to a high 2Q base and lower-cost chips driving ~10% blended ASP reductions in 3Q/4Q. Catalysts now include a rebound from a June sales trough, 2H13 margin improvement, tablet/smartphone design wins and rotation from sectors under pressure. Our NT$400 TP sets Mediatek at 20x average 2013E/2014E EPS (16x ex- cash), in line with its post-crisis average. Share price performance 60 80 100 120 200 250 300 350 400 Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12 Price (LHS) Rebased Rel (RHS) The price relative chart measures performance against the TAIWAN SE WEIGHTED INDEX which closed at 7923.16 on 04/02/13 On 04/02/13 the spot exchange rate was NT$29.55/US$1 Performance over 1M 3M 12M Absolute (%) -9.6 -4.1 20.6 Relative (%) -5.1 -3.7 10.8 Financial and valuation metrics Year 12/12A 12/13E 12/14E 12/15E Revenue (NT$ mn) 99,263.2 119,661.7 132,081.1 145,215.3 EBITDA (NT$ mn) 16,129.8 25,273.3 29,404.8 34,090.4 EBIT (NT$ mn) 12,433.3 21,615.2 25,807.6 30,466.0 Net profit (NT$ mn) 15,162.1 24,472.1 28,688.3 33,084.4 EPS (CS adj.) (NT$) 12.76 18.26 21.41 24.69 Change from previous EPS (%) n.a. 0.1 0.1 5.5 Consensus EPS (NT$) n.a. 18.3 22.8 23.8 EPS growth (%) 2.0 43.1 17.2 15.3 P/E (x) 25.7 18.0 15.3 13.3 Dividend yield (%) 2.7 2.7 4.2 4.9 EV/EBITDA (x) 22.4 13.5 11.2 9.4 P/B (x) 2.2 2.2 2.1 2.0 ROE (%) 10.4 13.1 14.1 15.4 Net debt/equity (%) Net cash Net cash Net cash Net cash Source: Company data, Thomson Reuters, Credit Suisse estimates. Rating OUTPERFORM* Price (27 Jun 13, NT$) 328.00 Target price (NT$) 400.00¹ Upside/downside (%) 22.0 Mkt cap (NT$ mn) 442,606 (US$ 14,774) Enterprise value (NT$ mn) 342,045 Number of shares (mn) 1,349.41 Free float (%) 89.1 52-week price range 382.0 - 236.5 ADTO - 6M (US$ mn) 89.3 *Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months. Research Analysts Randy Abrams, CFA 886 2 2715 6366 [email protected] Yan Taw Boon 852 2101 7039 [email protected] [email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

20130627 mtk sustaining its lead in a strong product cycle cs.pdf

Jun 24, 2015

Mediatek Analysis report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

28 June 2013

Asia Pacific/Taiwan

Equity Research

Semiconductor Devices

MediaTek Inc.

(2454.TW / 2454 TT) REINSTATEMENT

Sustaining its lead in a strong product cycle

■ Leading a strong product cycle. We reinstate coverage on Mediatek with an OUTPERFORM rating and a NT$400 target price (previously Neutral, TP NT$300) based on (1) leverage to a strong cycle for China-built smartphones and tablets (doubling in 2013 to 495 mn/100 mn units, respectively), (2) market leadership sustaining on rapid innovation, (3) additional drivers from tablets now and LTE longer term, and (4) reset

expectations into the high season.

■ Mediatek setting the pace. Mediatek is leading in low-cost smartphones with its turnkey support, high integration, accelerated product refresh cycle and technology migration. Ramp-up from 110 mn to 200 mn smartphone units sustains its share over 40%, with tablet share ramping to 15-20% in 2013 at 20 mn units. TD-SCDMA is a new driver with Mediatek’s share up

from 10% to 25% since 2012 and to 30-40% in 2H13 with new chip launches.

■ Unit strength and margin stability drives operating leverage. Strong unit growth and slightly improving gross margins from faster innovation on technology migration, product development and cost reductions are driving strong operating margin expansion from 10% in 1Q12 when feature phones collapsed to 20% by 2H13. New dual/quad cores in 2H13 should improve

the cost structure and drive 100 bp GM expansion vs. flattish expectation.

■ Expectations reset into the high season. Over the past two months, Mediatek has managed 2H13 expectations, citing likely below seasonal 3Q13 sales (implying +5-12% QoQ) due to a high 2Q base and lower-cost chips driving ~10% blended ASP reductions in 3Q/4Q. Catalysts now include a rebound from a June sales trough, 2H13 margin improvement, tablet/smartphone design wins and rotation from sectors under pressure. Our NT$400 TP sets Mediatek at 20x average 2013E/2014E EPS (16x ex-

cash), in line with its post-crisis average.

Share price performance

60

80

100

120

200

250

300

350

400

Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

TAIWAN SE WEIGHTED INDEX which closed at 7923.16 on

04/02/13

On 04/02/13 the spot exchange rate was NT$29.55/US$1

Performance over 1M 3M 12M Absolute (%) -9.6 -4.1 20.6 Relative (%) -5.1 -3.7 10.8

Financial and valuation metrics

Year 12/12A 12/13E 12/14E 12/15E Revenue (NT$ mn) 99,263.2 119,661.7 132,081.1 145,215.3 EBITDA (NT$ mn) 16,129.8 25,273.3 29,404.8 34,090.4 EBIT (NT$ mn) 12,433.3 21,615.2 25,807.6 30,466.0 Net profit (NT$ mn) 15,162.1 24,472.1 28,688.3 33,084.4 EPS (CS adj.) (NT$) 12.76 18.26 21.41 24.69 Change from previous EPS (%) n.a. 0.1 0.1 5.5 Consensus EPS (NT$) n.a. 18.3 22.8 23.8 EPS growth (%) 2.0 43.1 17.2 15.3 P/E (x) 25.7 18.0 15.3 13.3 Dividend yield (%) 2.7 2.7 4.2 4.9 EV/EBITDA (x) 22.4 13.5 11.2 9.4 P/B (x) 2.2 2.2 2.1 2.0 ROE (%) 10.4 13.1 14.1 15.4 Net debt/equity (%) Net cash Net cash Net cash Net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* Price (27 Jun 13, NT$) 328.00 Target price (NT$) 400.00¹ Upside/downside (%) 22.0 Mkt cap (NT$ mn) 442,606 (US$ 14,774) Enterprise value (NT$ mn) 342,045 Number of shares (mn) 1,349.41 Free float (%) 89.1 52-week price range 382.0 - 236.5 ADTO - 6M (US$ mn) 89.3

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Randy Abrams, CFA

886 2 2715 6366

Yan Taw Boon

852 2101 7039

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 2

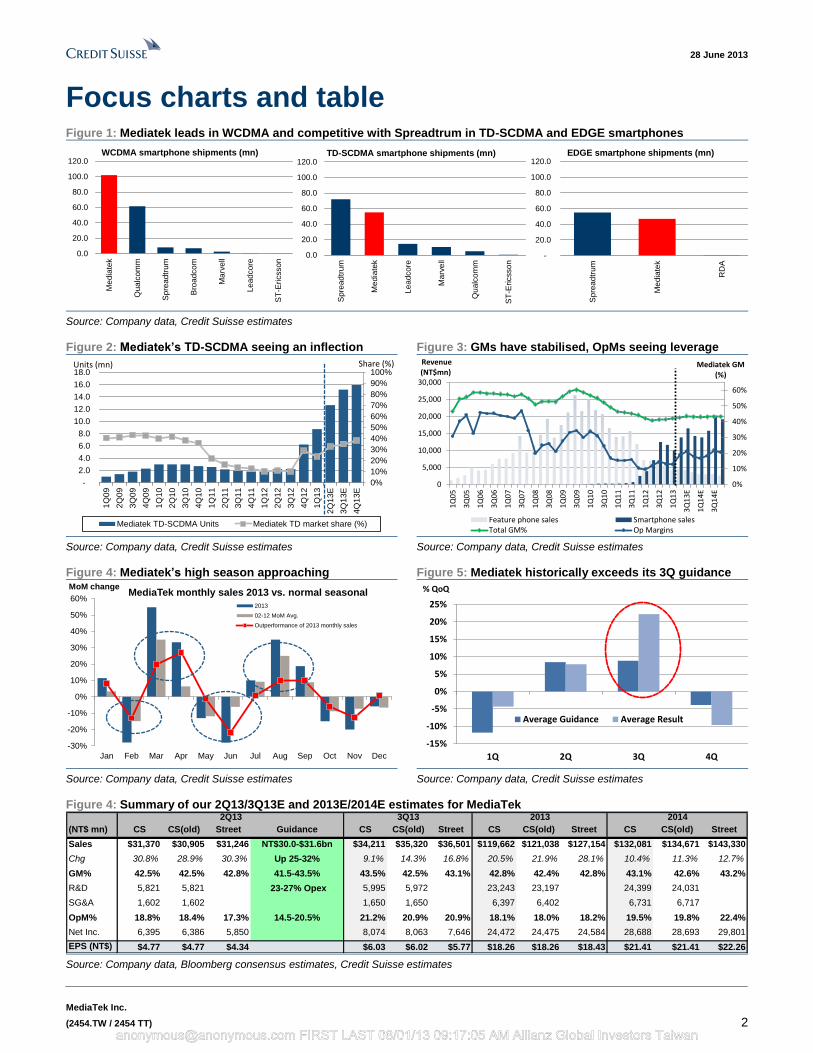

Focus charts and table Figure 1: Mediatek leads in WCDMA and competitive with Spreadtrum in TD-SCDMA and EDGE smartphones

-

20.0

40.0

60.0

80.0

100.0

120.0

Sp

rea

dtr

um

Me

dia

tek

RD

A

EDGE smartphone shipments (mn)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Me

dia

tek

Qu

alc

om

m

Sp

rea

dtr

um

Bro

adco

m

Ma

rve

ll

Le

adco

re

ST

-Ericsso

n

WCDMA smartphone shipments (mn)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Sp

rea

dtr

um

Me

dia

tek

Le

adco

re

Ma

rve

ll

Qu

alc

om

m

ST

-Ericsso

n

TD-SCDMA smartphone shipments (mn)

Source: Company data, Credit Suisse estimates

Figure 2: Mediatek’s TD-SCDMA seeing an inflection Figure 3: GMs have stabilised, OpMs seeing leverage

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

E

3Q

13

E

4Q

13

E

Mediatek TD-SCDMA Units Mediatek TD market share (%)

Units (mn) Share (%)

0%

10%

20%

30%

40%

50%

60%

0

5,000

10,000

15,000

20,000

25,000

30,000

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

E

1Q

14

E

3Q

14

E

Mediatek GM (%)

Revenue (NT$mn)

Feature phone sales Smartphone salesTotal GM% Op Margins

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 4: Mediatek’s high season approaching Figure 5: Mediatek historically exceeds its 3Q guidance

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MoM changeMediaTek monthly sales 2013 vs. normal seasonal

2013

02-12 MoM Avg.

Outperformance of 2013 monthly sales

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1Q 2Q 3Q 4Q

Average Guidance Average Result

% QoQ

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 4: Summary of our 2Q13/3Q13E and 2013E/2014E estimates for MediaTek 2Q13 3Q13 2013 2014

(NT$ mn) CS CS(old) Street Guidance CS CS(old) Street CS CS(old) Street CS CS(old) Street

Sales $31,370 $30,905 $31,246 NT$30.0-$31.6bn $34,211 $35,320 $36,501 $119,662 $121,038 $127,154 $132,081 $134,671 $143,330

Chg 30.8% 28.9% 30.3% Up 25-32% 9.1% 14.3% 16.8% 20.5% 21.9% 28.1% 10.4% 11.3% 12.7%

GM% 42.5% 42.5% 42.8% 41.5-43.5% 43.5% 42.5% 43.1% 42.8% 42.4% 42.8% 43.1% 42.6% 43.2%

R&D 5,821 5,821 23-27% Opex 5,995 5,972 23,243 23,197 24,399 24,031

SG&A 1,602 1,602 1,650 1,650 6,397 6,402 6,731 6,717

OpM% 18.8% 18.4% 17.3% 14.5-20.5% 21.2% 20.9% 20.9% 18.1% 18.0% 18.2% 19.5% 19.8% 22.4%

Net Inc. 6,395 6,386 5,850 8,074 8,063 7,646 24,472 24,475 24,584 28,688 28,693 29,801

EPS (NT$) $4.77 $4.77 $4.34 $6.03 $6.02 $5.77 $18.26 $18.26 $18.43 $21.41 $21.41 $22.26 Source: Company data, Bloomberg consensus estimates, Credit Suisse estimates

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 3

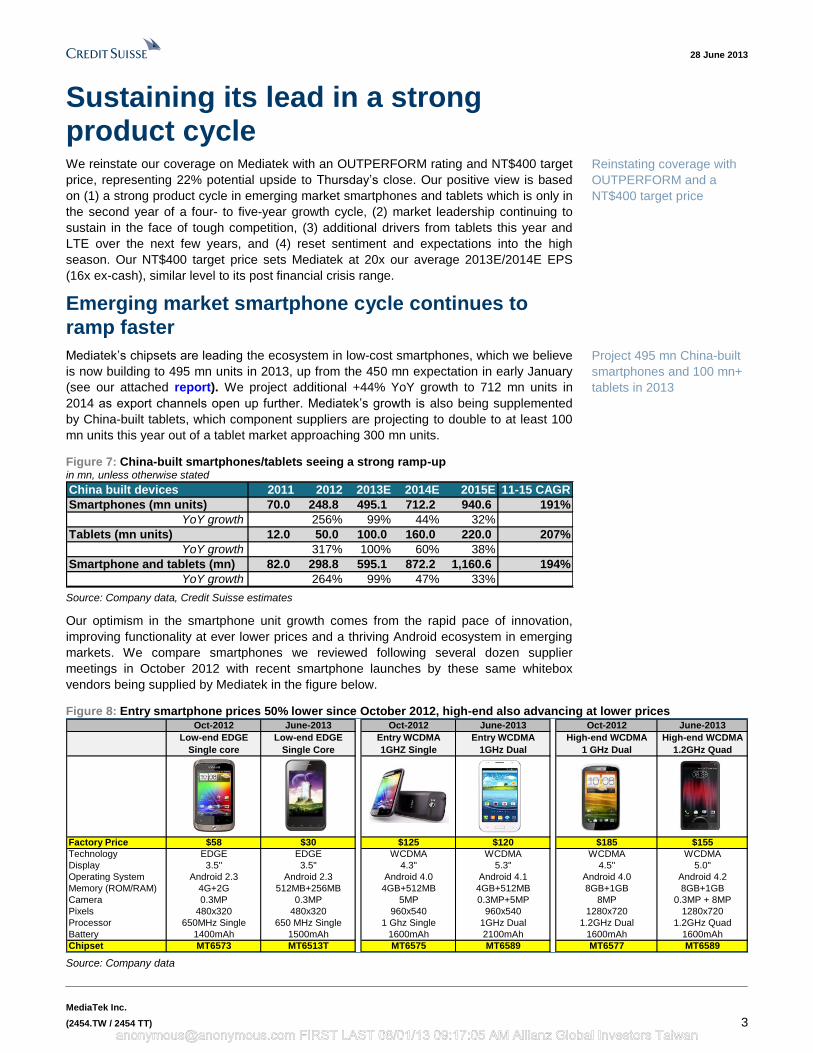

Sustaining its lead in a strong product cycle We reinstate our coverage on Mediatek with an OUTPERFORM rating and NT$400 target

price, representing 22% potential upside to Thursday’s close. Our positive view is based

on (1) a strong product cycle in emerging market smartphones and tablets which is only in

the second year of a four- to five-year growth cycle, (2) market leadership continuing to

sustain in the face of tough competition, (3) additional drivers from tablets this year and

LTE over the next few years, and (4) reset sentiment and expectations into the high

season. Our NT$400 target price sets Mediatek at 20x our average 2013E/2014E EPS

(16x ex-cash), similar level to its post financial crisis range.

Emerging market smartphone cycle continues to

ramp faster

Mediatek’s chipsets are leading the ecosystem in low-cost smartphones, which we believe

is now building to 495 mn units in 2013, up from the 450 mn expectation in early January

(see our attached report). We project additional +44% YoY growth to 712 mn units in

2014 as export channels open up further. Mediatek’s growth is also being supplemented

by China-built tablets, which component suppliers are projecting to double to at least 100

mn units this year out of a tablet market approaching 300 mn units.

Figure 7: China-built smartphones/tablets seeing a strong ramp-up in mn, unless otherwise stated

China built devices 2011 2012 2013E 2014E 2015E 11-15 CAGR

Smartphones (mn units) 70.0 248.8 495.1 712.2 940.6 191%

YoY growth 256% 99% 44% 32%

Tablets (mn units) 12.0 50.0 100.0 160.0 220.0 207%

YoY growth 317% 100% 60% 38%

Smartphone and tablets (mn) 82.0 298.8 595.1 872.2 1,160.6 194%

YoY growth 264% 99% 47% 33% Source: Company data, Credit Suisse estimates

Our optimism in the smartphone unit growth comes from the rapid pace of innovation,

improving functionality at ever lower prices and a thriving Android ecosystem in emerging

markets. We compare smartphones we reviewed following several dozen supplier

meetings in October 2012 with recent smartphone launches by these same whitebox

vendors being supplied by Mediatek in the figure below.

Figure 8: Entry smartphone prices 50% lower since October 2012, high-end also advancing at lower prices Oct-2012 June-2013 Oct-2012 June-2013 Oct-2012 June-2013

Low-end EDGE Low-end EDGE Entry WCDMA Entry WCDMA High-end WCDMA High-end WCDMA

Single core Single Core 1GHZ Single 1GHz Dual 1 GHz Dual 1.2GHz Quad

Factory Price $58 $30 $125 $120 $185 $155

Technology EDGE EDGE WCDMA WCDMA WCDMA WCDMA

Display 3.5" 3.5" 4.3" 5.3" 4.5" 5.0"

Operating System Android 2.3 Android 2.3 Android 4.0 Android 4.1 Android 4.0 Android 4.2

Memory (ROM/RAM) 4G+2G 512MB+256MB 4GB+512MB 4GB+512MB 8GB+1GB 8GB+1GB

Camera 0.3MP 0.3MP 5MP 0.3MP+5MP 8MP 0.3MP + 8MP

Pixels 480x320 480x320 960x540 960x540 1280x720 1280x720

Processor 650MHz Single 650 MHz Single 1 Ghz Single 1GHz Dual 1.2GHz Dual 1.2GHz Quad

Battery 1400mAh 1500mAh 1600mAh 2100mAh 1600mAh 1600mAh

Chipset MT6573 MT6513T MT6575 MT6589 MT6577 MT6589 Source: Company data

Reinstating coverage with

OUTPERFORM and a

NT$400 target price

Project 495 mn China-built

smartphones and 100 mn+

tablets in 2013

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 4

A few notable trends in the device migration since last fall:

1. Entry pricing getting lower. Factory prices for the entry level 3.5” EDGE Android

smartphones have dropped almost half in about a year from US$58 to US$30. The

prevalence of low-cost EDGE smartphones have opened up the export channel in

developing countries over the past year and allowed price elasticity to accelerate unit

growth.

2. Mid-tier whitebox phones getting much better. For a mid-tier US$120 factory price,

screen sizes have migrated from 4-4.5” up to 5-5.5”, rear cameras now scale up to 5-8

MP and are joined by front cameras, and 1 GHz dual core (versus single core last fall)

power a snappier user interface running Android 4.1 or 4.2.

3. High-tier with better screens resolution and lighter form factor. The upper tier

has allowed a US$150 factory price for 5” Android phone with 8GB memory, 8MP

camera, 1280x720 high resolution screen and quad core processor with vendors also

promoting slim brands and GS4 clone versions.

A combination of higher specs and lower price points is driving elasticity faster than

feature phones. Asian chipset suppliers have now reached 100 mn units just two years

into the ramp, a level that took almost four years during the feature phone ramp from

2005-09.

Price points for the entry level single core chipset are now less than US$5, a level that saw

Asian feature phone chips reach 160 mn units per quarter, suggesting room for continued

fast growth over the next few quarters.

Figure 9: Smartphones outpaced feature phones in ’05-09 Figure 10: $5 chipset drove 160 mn/qtr China feat. phones

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

50

100

150

200

250

3Q

11

/1Q

05

1Q

12

/3Q

05

3Q

12

/1Q

06

1Q

13

/3Q

06

3Q

13

/1Q

07

1Q

14

/3Q

07

3Q

14

/1Q

08

1Q

15

/3Q

08

3Q

15

/1Q

09

1Q

16

/3Q

09

3Q

16

/1Q

10

1Q

17

/3Q

10

3Q

17

/1Q

11

1Q

18

/3Q

11

Asian Feature phone units Asian Smartphone units FF Asian share (%)

Qtrly shipments (mn) Asian share (mn)

$0

$3

$6

$9

$12

$15

$18

$21

0

40

80

120

160

200

240

280

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

E

3Q

13

E

1Q

14E

3Q

14

E

1Q

15

E

3Q

15

E

Feature phone units Smartphones units

Feature phone ASPs Smartphone ASPs

Chipset units (mn) ASPs (US$)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Mediatek still setting the pace

Mediatek has regained the leadership position it held in emerging market feature phones

through a combination of benefits that scale beyond the raw chipset specifications:

■ Turnkey support. Mediatek’s turnkey solutions include manufacturing-ready

reference design kits and software support, with over 1,000 field applications

engineers in China supporting customers in various key locations (Shenzhen,

Shanghai and Beijing). The turnkey support Mediatek provides addresses whitebox

handset makers’ needs, lowers the entry barrier for suppliers, and vastly shortens

time-to-market. Despite the aggressive push by overseas vendors led by Qualcomm,

Mediatek is still leading in its understanding of the market and relationships with the

customers after working closely with them for seven to eight years.

■ High level of integration. Mediatek is enabling its customers to cut down costs faster

through integrating external components on chip. The company’s MT6572 integrates

an internal 32K clock, a SAW-less filter, and single antenna to also reduce external

Mediatek’s customers are

enabled for substantially

lower entry price points and

higher quality at similar

prices relative to last

October

US$5 chipset price on

feature phones enabled 160

mn units/quarter China-built

feature phone volumes

Mediatek’s model for

turnkey support still leads

competitor efforts,

integration, fast refreshes

and now aggressive leading

edge push steps up its

competitiveness

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 5

BOM costs and allows for simplified four-layer PCB. The company has also created a

high degree of flexibility for customers to source local low-cost suppliers, support

multiple mobile DRAM suppliers and scale up pixel count on photos to advertise a

higher megapixel count for the phone.

■ Fast product refreshes. Mediatek is quick in providing new software patches and

churning out optimised chips to help improve customers’ competitiveness. For

example, MT6589A is an optimised version of the 6589 enabling its customers to

improve clock speed performance and the MT6589M and MT6582 represent two

lower-cost chipsets within two quarters of the initial quad core launch which strip out

redundant non-core features, thus lowering prices.

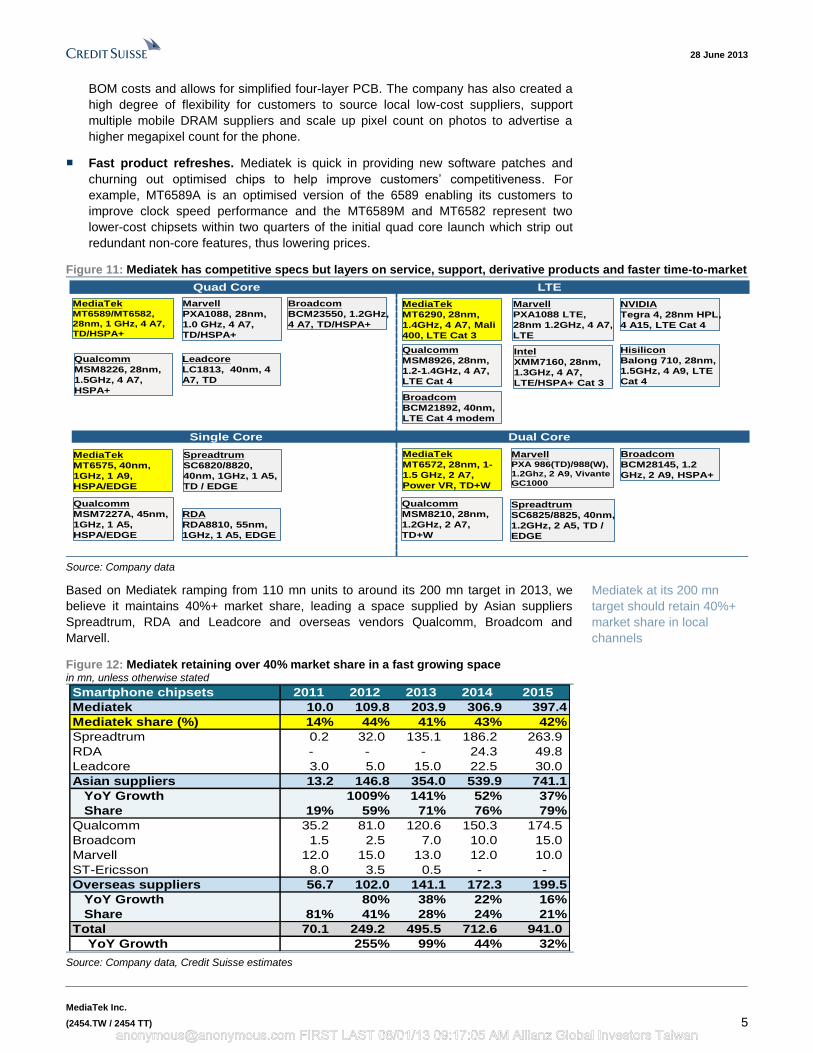

Figure 11: Mediatek has competitive specs but layers on service, support, derivative products and faster time-to-market

Quad Core LTE

Single Core Dual Core

MediaTekMT6589/MT6582,

28nm, 1 GHz, 4 A7,

TD/HSPA+

Qualcomm

MSM8226, 28nm,

1.5GHz, 4 A7,

HSPA+

NVIDIA

Tegra 4, 28nm HPL,

4 A15, LTE Cat 4

MediaTek

MT6572, 28nm, 1-

1.5 GHz, 2 A7,

Power VR, TD+W

Spreadtrum

SC6825/8825, 40nm,

1.2GHz, 2 A5, TD /

EDGE

Qualcomm

MSM8926, 28nm,

1.2-1.4GHz, 4 A7,

LTE Cat 4

Qualcomm

MSM8210, 28nm,

1.2GHz, 2 A7,

TD+W

Marvell

PXA1088, 28nm,

1.0 GHz, 4 A7,

TD/HSPA+

Spreadtrum

SC6820/8820,

40nm, 1GHz, 1 A5,

TD / EDGE

MediaTek

MT6575, 40nm,

1GHz, 1 A9,

HSPA/EDGE

Intel

XMM7160, 28nm,

1.3GHz, 4 A7,

LTE/HSPA+ Cat 3

MediaTek

MT6290, 28nm,

1.4GHz, 4 A7, Mali

400, LTE Cat 3

Leadcore

LC1813, 40nm, 4

A7, TD

Hisilicon

Balong 710, 28nm,

1.5GHz, 4 A9, LTE

Cat 4

Qualcomm

MSM7227A, 45nm,

1GHz, 1 A5,

HSPA/EDGE

MarvellPXA 986(TD)/988(W),

1.2Ghz, 2 A9, Vivante

GC1000

Marvell

PXA1088 LTE,

28nm 1.2GHz, 4 A7,

LTE

Broadcom

BCM23550, 1.2GHz,

4 A7, TD/HSPA+

Broadcom

BCM21892, 40nm,

LTE Cat 4 modem

Broadcom

BCM28145, 1.2

GHz, 2 A9, HSPA+

RDA

RDA8810, 55nm,

1GHz, 1 A5, EDGE

Source: Company data

Based on Mediatek ramping from 110 mn units to around its 200 mn target in 2013, we

believe it maintains 40%+ market share, leading a space supplied by Asian suppliers

Spreadtrum, RDA and Leadcore and overseas vendors Qualcomm, Broadcom and

Marvell.

Figure 12: Mediatek retaining over 40% market share in a fast growing space in mn, unless otherwise stated

Smartphone chipsets 2011 2012 2013 2014 2015

Mediatek 10.0 109.8 203.9 306.9 397.4

Mediatek share (%) 14% 44% 41% 43% 42%

Spreadtrum 0.2 32.0 135.1 186.2 263.9

RDA - - - 24.3 49.8

Leadcore 3.0 5.0 15.0 22.5 30.0

Asian suppliers 13.2 146.8 354.0 539.9 741.1

YoY Growth 1009% 141% 52% 37%

Share 19% 59% 71% 76% 79%

Qualcomm 35.2 81.0 120.6 150.3 174.5

Broadcom 1.5 2.5 7.0 10.0 15.0

Marvell 12.0 15.0 13.0 12.0 10.0

ST-Ericsson 8.0 3.5 0.5 - -

Overseas suppliers 56.7 102.0 141.1 172.3 199.5

YoY Growth 80% 38% 22% 16%

Share 81% 41% 28% 24% 21%

Total 70.1 249.2 495.5 712.6 941.0

YoY Growth 255% 99% 44% 32% Source: Company data, Credit Suisse estimates

Mediatek at its 200 mn

target should retain 40%+

market share in local

channels

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 6

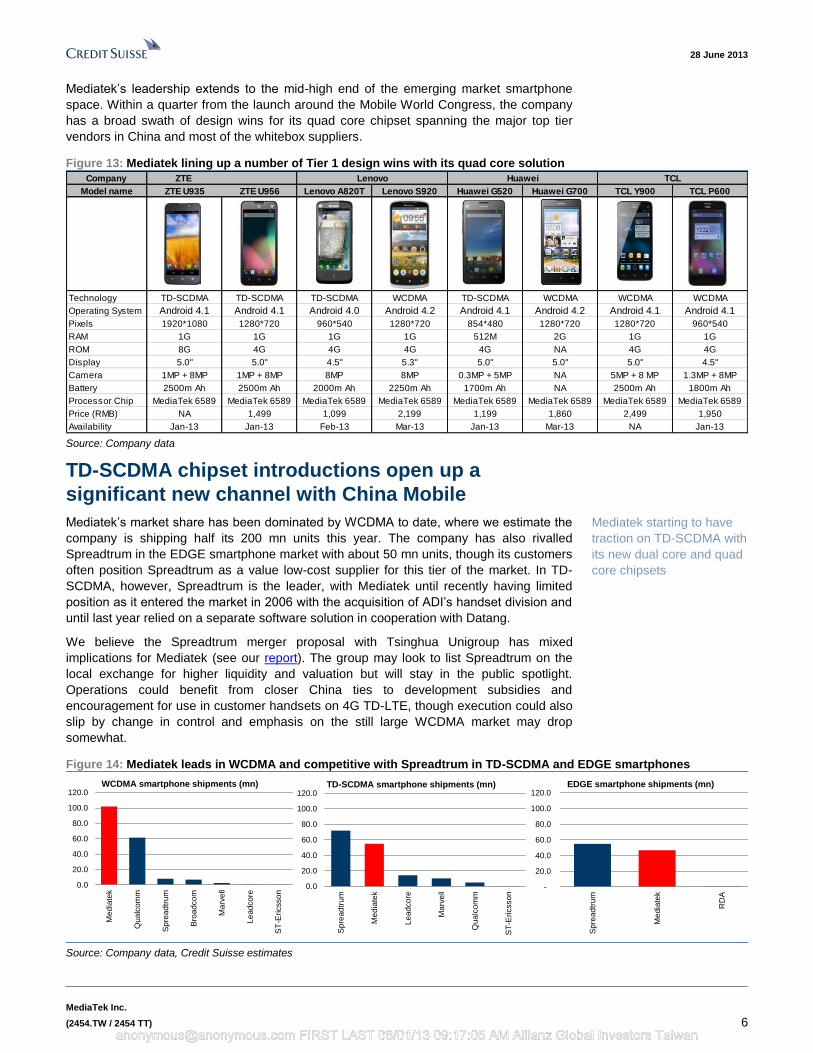

Mediatek’s leadership extends to the mid-high end of the emerging market smartphone

space. Within a quarter from the launch around the Mobile World Congress, the company

has a broad swath of design wins for its quad core chipset spanning the major top tier

vendors in China and most of the whitebox suppliers.

Figure 13: Mediatek lining up a number of Tier 1 design wins with its quad core solution

Company ZTE

Model name ZTE U935 ZTE U956 Lenovo A820T Lenovo S920 Huawei G520 Huawei G700 TCL Y900 TCL P600

Technology TD-SCDMA TD-SCDMA TD-SCDMA WCDMA TD-SCDMA WCDMA WCDMA WCDMA

Operating System Android 4.1 Android 4.1 Android 4.0 Android 4.2 Android 4.1 Android 4.2 Android 4.1 Android 4.1

Pixels 1920*1080 1280*720 960*540 1280*720 854*480 1280*720 1280*720 960*540

RAM 1G 1G 1G 1G 512M 2G 1G 1G

ROM 8G 4G 4G 4G 4G NA 4G 4G

Display 5.0" 5.0" 4.5" 5.3" 5.0" 5.0" 5.0" 4.5"

Camera 1MP + 8MP 1MP + 8MP 8MP 8MP 0.3MP + 5MP NA 5MP + 8 MP 1.3MP + 8MP

Battery 2500m Ah 2500m Ah 2000m Ah 2250m Ah 1700m Ah NA 2500m Ah 1800m Ah

Processor Chip MediaTek 6589 MediaTek 6589 MediaTek 6589 MediaTek 6589 MediaTek 6589 MediaTek 6589 MediaTek 6589 MediaTek 6589

Price (RMB) NA 1,499 1,099 2,199 1,199 1,860 2,499 1,950

Availability Jan-13 Jan-13 Feb-13 Mar-13 Jan-13 Mar-13 NA Jan-13

Lenovo Huawei TCL

Source: Company data

TD-SCDMA chipset introductions open up a

significant new channel with China Mobile

Mediatek’s market share has been dominated by WCDMA to date, where we estimate the

company is shipping half its 200 mn units this year. The company has also rivalled

Spreadtrum in the EDGE smartphone market with about 50 mn units, though its customers

often position Spreadtrum as a value low-cost supplier for this tier of the market. In TD-

SCDMA, however, Spreadtrum is the leader, with Mediatek until recently having limited

position as it entered the market in 2006 with the acquisition of ADI’s handset division and

until last year relied on a separate software solution in cooperation with Datang.

We believe the Spreadtrum merger proposal with Tsinghua Unigroup has mixed

implications for Mediatek (see our report). The group may look to list Spreadtrum on the

local exchange for higher liquidity and valuation but will stay in the public spotlight.

Operations could benefit from closer China ties to development subsidies and

encouragement for use in customer handsets on 4G TD-LTE, though execution could also

slip by change in control and emphasis on the still large WCDMA market may drop

somewhat.

Figure 14: Mediatek leads in WCDMA and competitive with Spreadtrum in TD-SCDMA and EDGE smartphones

-

20.0

40.0

60.0

80.0

100.0

120.0

Sp

rea

dtr

um

Me

dia

tek

RD

A

EDGE smartphone shipments (mn)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Me

dia

tek

Qu

alc

om

m

Sp

rea

dtr

um

Bro

adco

m

Ma

rve

ll

Le

adco

re

ST

-Ericsso

n

WCDMA smartphone shipments (mn)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Sp

rea

dtr

um

Me

dia

tek

Le

adco

re

Ma

rve

ll

Qu

alc

om

m

ST

-Ericsso

n

TD-SCDMA smartphone shipments (mn)

Source: Company data, Credit Suisse estimates

Mediatek starting to have

traction on TD-SCDMA with

its new dual core and quad

core chipsets

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 7

The untapped opportunity for Mediatek in TD-SCDMA is still mostly upside even if

Spreadtrum gains closer cooperation with China Mobile. Mediatek originally was strong in

China Mobile’s vast channel in 2G helping drive penetration of feature phones by the local

brands. China Mobile built the largest subscriber base among carriers globally at over 700

mn but is only 15% penetrated on 3G versus 45% penetration for China Telecom and 35%

for China Unicom.

Figure 15: China Mobile now leading in 3G adds Figure 16: China Mobile has the lowest 3G penetration

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

China Mobile China Unicom China Telecom

0%5%10%15%20%25%30%35%40%45%50%

0

100

200

300

400

500

600

700

800

Ma

y-1

0

Jul-1

0

Sep-1

0

No

v-1

0

Jan-1

1

Ma

r-1

1

Ma

y-1

1

Jul-1

1

Sep-1

1

No

v-1

1

Jan-1

2

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Sep-1

2

No

v-1

2

Jan-1

3

Ma

r-1

3

Mobile subscribers Unicom subscribers Telecom subscribers

Mobile penetration Unicom penetration Telecom penetration

Subscriber base (mn) 3G penetration %

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Mediatek is finally better addressing the market with its chipsets providing multi network

support for WCDMA and TD-SCDMA, with MT6589/MT8389 quad core processor for

smartphones/tablets and MT6572 dual core processor for mid-tier smartphones now

supporting TD-SCDMA. Mediatek’s market share has already rebounded from a trough of

10% in mid-2012 to 25% in 1H13 and may reach 35% in 2H13, giving it a new leg of

growth for its smartphone business as it ramps up the new TD products.

Figure 17: Mediatek’s new products integrate TD-SCDMA Figure 18: Mediatek’s TD-SCDMA seeing an inflection

Tablet processor MT8589 MT6572

Multi-core Quad-core Dual-core

CPU ARM Cortex-A7 ARM Cortex-A7

Clock speed 1.2GHz 1GHz

Graphics ARM Mali-400 ARM Mali-400

Process node 28nm 28nm

Foundry TSMC TSMC

Availability 1Q13 2Q13

Note

Multi-network support

(WCDMA, TD-SCDMA,

EDGE)

Multi-network support

- WCDMA: online

- TD: MT6572TD

(end of 2Q13)

- EDGE: MT6572E

- Quad-core: MT6589

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13E

3Q

13

E

4Q

13

E

Mediatek TD-SCDMA Units Mediatek TD market share (%)

Units (mn) Share (%)

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse estimates

China Mobile is a relatively

untapped opportunity at

over 700 mn subscribers

and 15% 3G penetration

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 8

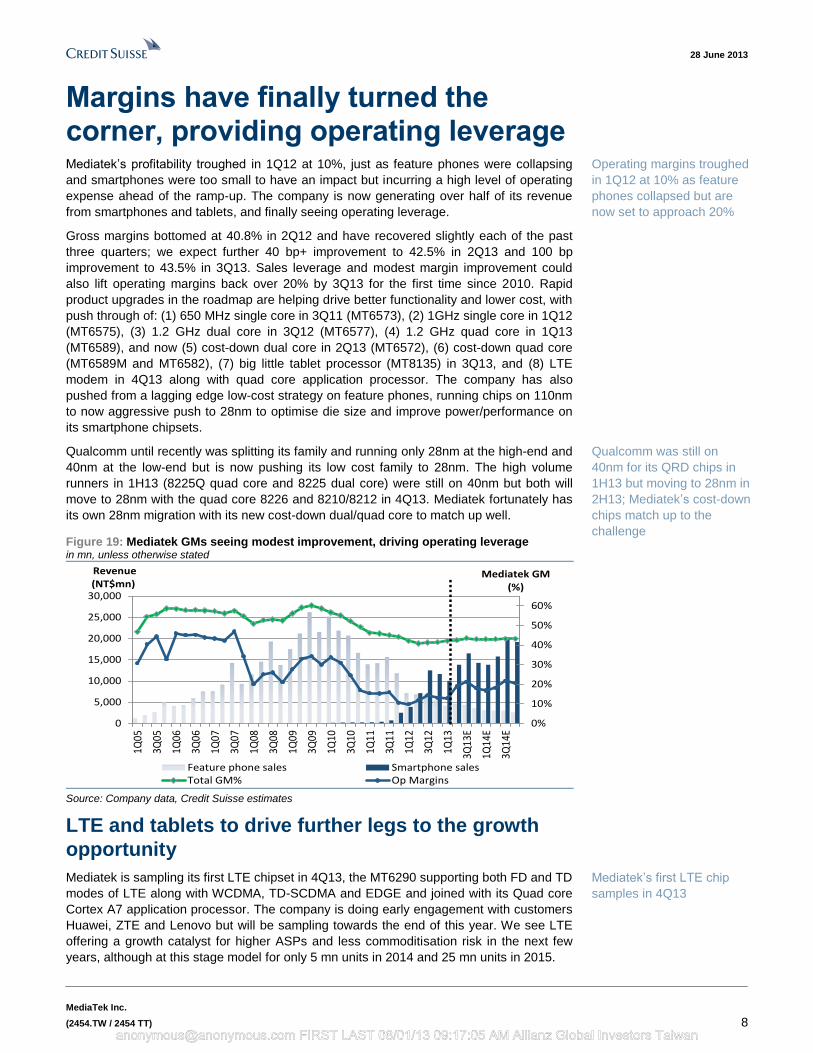

Margins have finally turned the corner, providing operating leverage Mediatek’s profitability troughed in 1Q12 at 10%, just as feature phones were collapsing

and smartphones were too small to have an impact but incurring a high level of operating

expense ahead of the ramp-up. The company is now generating over half of its revenue

from smartphones and tablets, and finally seeing operating leverage.

Gross margins bottomed at 40.8% in 2Q12 and have recovered slightly each of the past

three quarters; we expect further 40 bp+ improvement to 42.5% in 2Q13 and 100 bp

improvement to 43.5% in 3Q13. Sales leverage and modest margin improvement could

also lift operating margins back over 20% by 3Q13 for the first time since 2010. Rapid

product upgrades in the roadmap are helping drive better functionality and lower cost, with

push through of: (1) 650 MHz single core in 3Q11 (MT6573), (2) 1GHz single core in 1Q12

(MT6575), (3) 1.2 GHz dual core in 3Q12 (MT6577), (4) 1.2 GHz quad core in 1Q13

(MT6589), and now (5) cost-down dual core in 2Q13 (MT6572), (6) cost-down quad core

(MT6589M and MT6582), (7) big little tablet processor (MT8135) in 3Q13, and (8) LTE

modem in 4Q13 along with quad core application processor. The company has also

pushed from a lagging edge low-cost strategy on feature phones, running chips on 110nm

to now aggressive push to 28nm to optimise die size and improve power/performance on

its smartphone chipsets.

Qualcomm until recently was splitting its family and running only 28nm at the high-end and

40nm at the low-end but is now pushing its low cost family to 28nm. The high volume

runners in 1H13 (8225Q quad core and 8225 dual core) were still on 40nm but both will

move to 28nm with the quad core 8226 and 8210/8212 in 4Q13. Mediatek fortunately has

its own 28nm migration with its new cost-down dual/quad core to match up well.

Figure 19: Mediatek GMs seeing modest improvement, driving operating leverage in mn, unless otherwise stated

0%

10%

20%

30%

40%

50%

60%

0

5,000

10,000

15,000

20,000

25,000

30,000

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

E

1Q14

E

3Q14

E

Mediatek GM (%)

Revenue (NT$mn)

Feature phone sales Smartphone salesTotal GM% Op Margins

Source: Company data, Credit Suisse estimates

LTE and tablets to drive further legs to the growth

opportunity

Mediatek is sampling its first LTE chipset in 4Q13, the MT6290 supporting both FD and TD

modes of LTE along with WCDMA, TD-SCDMA and EDGE and joined with its Quad core

Cortex A7 application processor. The company is doing early engagement with customers

Huawei, ZTE and Lenovo but will be sampling towards the end of this year. We see LTE

offering a growth catalyst for higher ASPs and less commoditisation risk in the next few

years, although at this stage model for only 5 mn units in 2014 and 25 mn units in 2015.

Operating margins troughed

in 1Q12 at 10% as feature

phones collapsed but are

now set to approach 20%

Qualcomm was still on

40nm for its QRD chips in

1H13 but moving to 28nm in

2H13; Mediatek’s cost-down

chips match up to the

challenge

Mediatek’s first LTE chip

samples in 4Q13

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 9

Qualcomm will have the inside track on LTE having launched solutions at Tier 1 global

vendors. Qualcomm is also introducing LTE reference designs (QRD) for Chinese

handset-makers and has enabled K-Touch and Hisense to launch entry level LTE

smartphones targeting the export market for production starting from 3Q13 using its 8926

chipset on 28nm LP. Despite Qualcomm’s early lead, China should develop LTE gradually

in 2014 due to normal requirement to build out enough coverage before subsidising

higher-priced handsets. We estimate subscriber ramp in China from 2 mn in 2013 to 23

mn in 2014 and 61 mn in 2015 (out of a base of 800 mn emerging market smartphones).

We would note from the exhibits below that 3G China brands and Tier 2/3 brands saw a

bigger inflection only once Mediatek’s chipset was available even though Qualcomm,

Broadcom, ST-Ericsson and Marvell were already supplying Chinese brands with 3G

solutions. This implies that the Chinese branded channel may wait for Mediatek’s

readiness to see a material inflection. Mediatek’s sampling in 4Q13 should put it ready for

an emerging market inflection in 2015 as China Mobile targets 350,000 LTE base stations

by end-2014 and reaches 80% coverage at 400,000 base stations.

Figure 20: Mediatek’s ramp-up enabled the Tier 2 brands Figure 21: China brands gained share after MTK’s entry

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13

Mediatek Smartphone Units China brands

Tier one's Local brand share

Thousand (units) Local brand share (%)

0%

5%

10%

15%

20%

25%

30%

0

10,000

20,000

30,000

40,000

50,000

60,000

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Chinese brands Mediatek Smartphone Units Chinese brand global share

Share % / MTK units (mn)Units (thousands)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Whitebox tablet opportunity tracking to upside

The tablet market is accelerating as functionality greatly improves in the US$40-200 price

range and Chinese makers export to emerging markets with low PC penetration (see our

report). Usage centers on entertainment (games, movies and music) but is expanding to

education and productivity as keyboard attachments and Android apps proliferate. High-

end tablets with Chinese-sourced components have advanced substantially, with 9.7”

retina displays, quad core chipsets (Actions, Allwinner, Rockchip and Mediatek), 802.11

WiFi chipset (Realtek), 4:1 connectivity (Wifi, GPS, Bluetooth, FM) and up to 5MP rear

cameras, 16GB NAND + 2GB DDR3 DRAM, running Android 4.1.1, at FOB prices around

US$140-160.

Figure 22: Whitebox tablets supplement branded tablets Figure 23: Tablet pace faster than smartphone/handsets

-40%

-20%

0%

20%

40%

60%

80%

100%

0

20,000

40,000

60,000

80,000

100,000

120,000

Jun

-10

Se

p-1

0

De

c-1

0

Ma

r-1

1

Jun

-11

Se

p-1

1

De

c-1

1

Ma

r-1

2

Jun

-12

Sep-1

2

De

c-1

3

Ma

r-1

3

Jun

-13E

Se

pt-

13

E

De

c-1

3E

Branded tablets Whitebox tablets QoQ growth

Units ('000) QoQ growth

0

200

400

600

800

1000

1200

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Tablets Feature phones (re-based from 1995)

Smartphones (re-based from 2005)

Mn (units)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Qualcomm the substantial

early leader, now pushing

QRD designs to Chinese

customers

Mediatek has time on LTE–

broad China Mobile

coverage targeted for end-

2014 for 2015 ramp; 3G in

China inflected once

Mediatek was ready

Tablets pushing US$40-

$200 price points initially for

entertainment but expanding

into education and

productivity uses

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 10

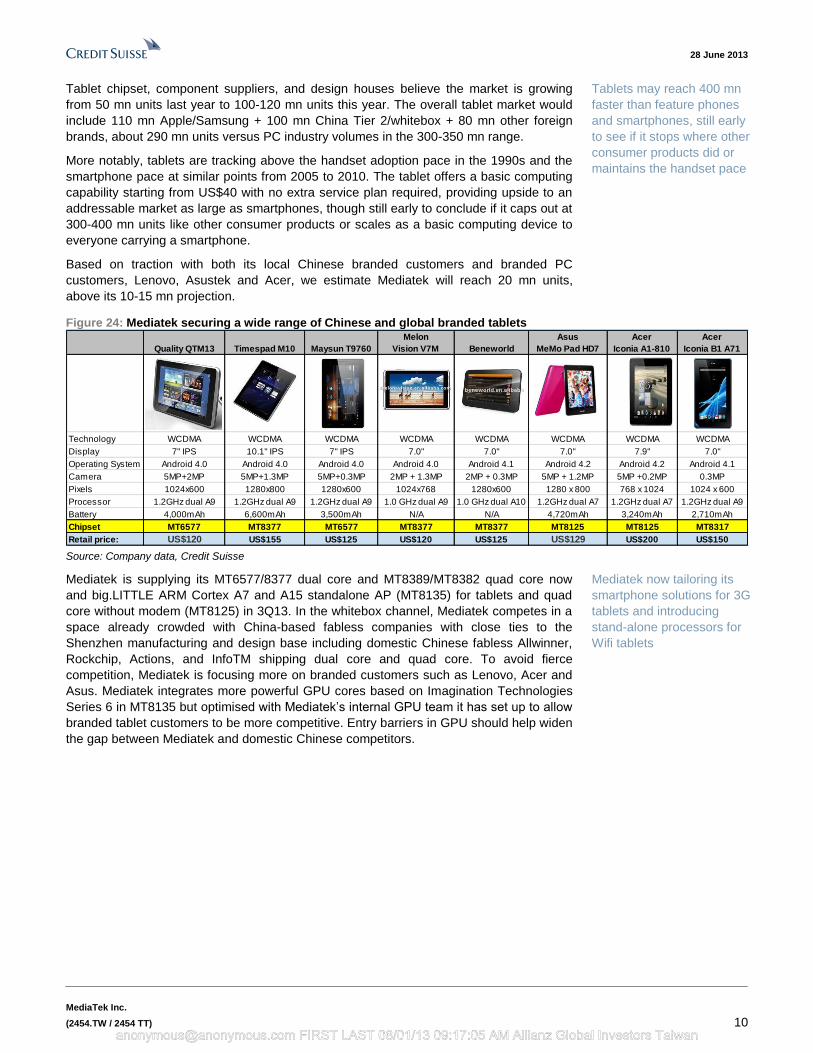

Tablet chipset, component suppliers, and design houses believe the market is growing

from 50 mn units last year to 100-120 mn units this year. The overall tablet market would

include 110 mn Apple/Samsung + 100 mn China Tier 2/whitebox + 80 mn other foreign

brands, about 290 mn units versus PC industry volumes in the 300-350 mn range.

More notably, tablets are tracking above the handset adoption pace in the 1990s and the

smartphone pace at similar points from 2005 to 2010. The tablet offers a basic computing

capability starting from US$40 with no extra service plan required, providing upside to an

addressable market as large as smartphones, though still early to conclude if it caps out at

300-400 mn units like other consumer products or scales as a basic computing device to

everyone carrying a smartphone.

Based on traction with both its local Chinese branded customers and branded PC

customers, Lenovo, Asustek and Acer, we estimate Mediatek will reach 20 mn units,

above its 10-15 mn projection.

Figure 24: Mediatek securing a wide range of Chinese and global branded tablets

Quality QTM13 Timespad M10 Maysun T9760

Melon

Vision V7M Beneworld

Asus

MeMo Pad HD7

Acer

Iconia A1-810

Acer

Iconia B1 A71

Technology WCDMA WCDMA WCDMA WCDMA WCDMA WCDMA WCDMA WCDMA

Display 7" IPS 10.1" IPS 7" IPS 7.0" 7.0" 7.0" 7.9" 7.0"

Operating System Android 4.0 Android 4.0 Android 4.0 Android 4.0 Android 4.1 Android 4.2 Android 4.2 Android 4.1

Camera 5MP+2MP 5MP+1.3MP 5MP+0.3MP 2MP + 1.3MP 2MP + 0.3MP 5MP + 1.2MP 5MP +0.2MP 0.3MP

Pixels 1024x600 1280x800 1280x600 1024x768 1280x600 1280 x 800 768 x 1024 1024 x 600

Processor 1.2GHz dual A9 1.2GHz dual A9 1.2GHz dual A9 1.0 GHz dual A9 1.0 GHz dual A10 1.2GHz dual A7 1.2GHz dual A7 1.2GHz dual A9

Battery 4,000mAh 6,600mAh 3,500mAh N/A N/A 4,720mAh 3,240mAh 2,710mAh

Chipset MT6577 MT8377 MT6577 MT8377 MT8377 MT8125 MT8125 MT8317

Retail price: US$120 US$155 US$125 US$120 US$125 US$129 US$200 US$150 Source: Company data, Credit Suisse

Mediatek is supplying its MT6577/8377 dual core and MT8389/MT8382 quad core now

and big.LITTLE ARM Cortex A7 and A15 standalone AP (MT8135) for tablets and quad

core without modem (MT8125) in 3Q13. In the whitebox channel, Mediatek competes in a

space already crowded with China-based fabless companies with close ties to the

Shenzhen manufacturing and design base including domestic Chinese fabless Allwinner,

Rockchip, Actions, and InfoTM shipping dual core and quad core. To avoid fierce

competition, Mediatek is focusing more on branded customers such as Lenovo, Acer and

Asus. Mediatek integrates more powerful GPU cores based on Imagination Technologies

Series 6 in MT8135 but optimised with Mediatek’s internal GPU team it has set up to allow

branded tablet customers to be more competitive. Entry barriers in GPU should help widen

the gap between Mediatek and domestic Chinese competitors.

Tablets may reach 400 mn

faster than feature phones

and smartphones, still early

to see if it stops where other

consumer products did or

maintains the handset pace

Mediatek now tailoring its

smartphone solutions for 3G

tablets and introducing

stand-alone processors for

Wifi tablets

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 11

Expectations getting reset into the high season Mediatek has been proactive resetting 2H13 expectations since right after its 2Q13 results,

noting that 2Q13 growth is substantially above seasonal at +31% QoQ versus normal +5-

10% QoQ growth so sets up a high base. The company at its recent AGM also highlighted

to expect sub-seasonal growth implying mid-single digit to low-teen QoQ growth versus

normal +20-25% QoQ growth.

We would highlight that Mediatek’s average guidance since 2003 is for +8% QoQ growth

but average result is +22% QoQ. Visibility is traditionally lower in July due to inventory

digesting after the May holiday for two months (as it did this year) before resuming build in

August-September, resulting in better chance for more frequent upside surprises in 3Q13.

Figure 25: Mediatek 3Q high season strength normal Figure 26: Mediatek historically exceeds its 3Q guidance

-25%

-15%

-5%

5%

15%

25%

35%

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Revenue Guidance Revenue Result

Revenue Growth QoQ (%)Revenue Growth QoQ (%)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1Q 2Q 3Q 4Q

Average Guidance Average Result

% QoQ

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

Sales to date this year are tracking Mediatek’s normal pattern, with hyper seasonality, with

a more-than-normal correction from November to February clearing out the channel, a

stronger-than-normal recovery in March-April and a slowdown from May through early

July, setting up potential for a rebound into the high-season ahead of the October China

holiday as Mediatek also ramps its new cost-down dual core (MT6582), quad core

(6589M/6582) and big.LITTLE (MT8135), providing a catalyst for the sales rebound from a

short-term trough near NT$8 bn sales in June.

Figure 27: Share price normally tracks monthly sales Figure 28: Mediatek’s high season approaching

- 50

100 150 200 250 300 350 400 450 500 550 600 650 700

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

20

13/1

22

01

3/0

72

01

3/0

22

01

2/0

92

01

2/0

42

01

1/1

12

01

1/0

62

01

1/0

12

01

0/0

82

01

0/0

32

00

9/1

02

00

9/0

52

00

8/1

22

00

8/0

72

00

8/0

22

00

7/0

92

00

7/0

42

00

6/1

12

00

6/0

62

00

6/0

12

00

5/0

82

00

5/0

32

00

4/1

02

00

4/0

52

00

3/1

22

00

3/0

72

00

3/0

22

00

2/0

92

00

2/0

42

00

1/1

1

Stock Price(NT$)

Monthly sales (NT$mn)

Mo. sales (000)

Stock price

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MoM changeMediaTek monthly sales 2013 vs. normal seasonal

2013

02-12 MoM Avg.

Outperformance of 2013 monthly sales

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Mediatek has consistently

noted to expect sub-

seasonal 3Q13 so should be

in expectations now

3Q has traditionally been

guided conservatively and

upsided significantly

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 12

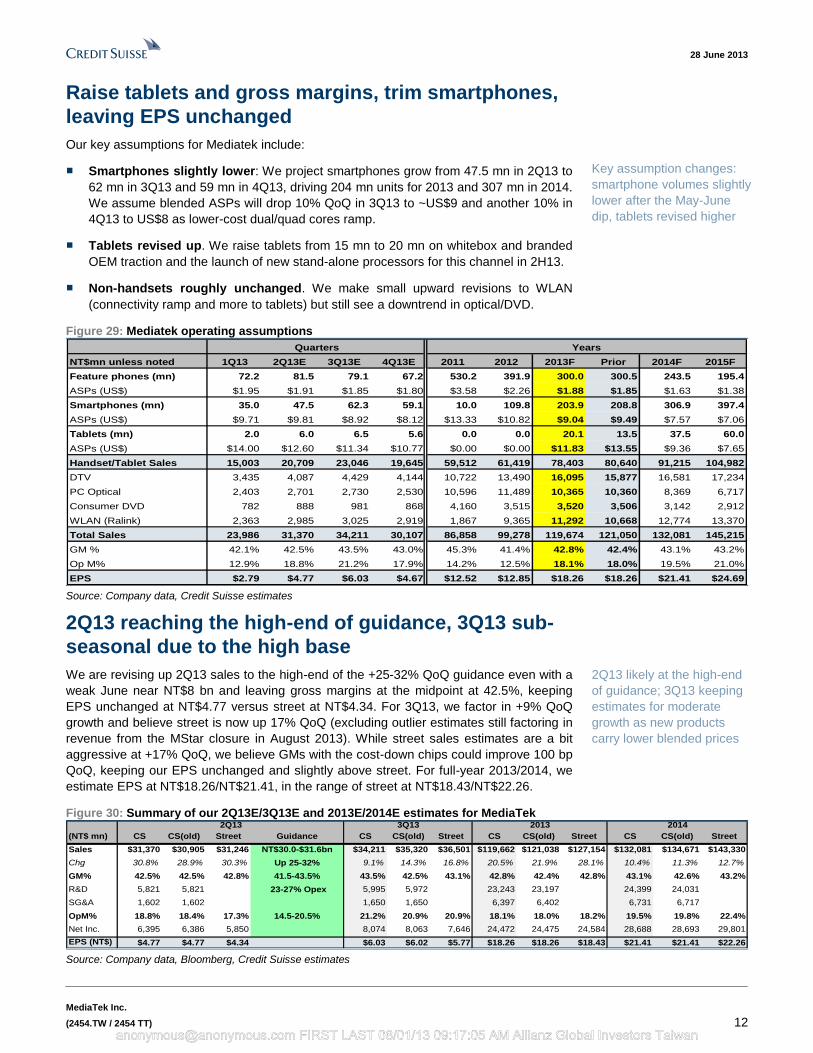

Raise tablets and gross margins, trim smartphones,

leaving EPS unchanged

Our key assumptions for Mediatek include:

■ Smartphones slightly lower: We project smartphones grow from 47.5 mn in 2Q13 to

62 mn in 3Q13 and 59 mn in 4Q13, driving 204 mn units for 2013 and 307 mn in 2014.

We assume blended ASPs will drop 10% QoQ in 3Q13 to ~US$9 and another 10% in

4Q13 to US$8 as lower-cost dual/quad cores ramp.

■ Tablets revised up. We raise tablets from 15 mn to 20 mn on whitebox and branded

OEM traction and the launch of new stand-alone processors for this channel in 2H13.

■ Non-handsets roughly unchanged. We make small upward revisions to WLAN

(connectivity ramp and more to tablets) but still see a downtrend in optical/DVD.

Figure 29: Mediatek operating assumptions

Quarters Years

NT$mn unless noted 1Q13 2Q13E 3Q13E 4Q13E 2011 2012 2013F Prior 2014F 2015F

Feature phones (mn) 72.2 81.5 79.1 67.2 530.2 391.9 300.0 300.5 243.5 195.4

ASPs (US$) $1.95 $1.91 $1.85 $1.80 $3.58 $2.26 $1.88 $1.85 $1.63 $1.38

Smartphones (mn) 35.0 47.5 62.3 59.1 10.0 109.8 203.9 208.8 306.9 397.4

ASPs (US$) $9.71 $9.81 $8.92 $8.12 $13.33 $10.82 $9.04 $9.49 $7.57 $7.06

Tablets (mn) 2.0 6.0 6.5 5.6 0.0 0.0 20.1 13.5 37.5 60.0

ASPs (US$) $14.00 $12.60 $11.34 $10.77 $0.00 $0.00 $11.83 $13.55 $9.36 $7.65

Handset/Tablet Sales 15,003 20,709 23,046 19,645 59,512 61,419 78,403 80,640 91,215 104,982

DTV 3,435 4,087 4,429 4,144 10,722 13,490 16,095 15,877 16,581 17,234

PC Optical 2,403 2,701 2,730 2,530 10,596 11,489 10,365 10,360 8,369 6,717

Consumer DVD 782 888 981 868 4,160 3,515 3,520 3,506 3,142 2,912

WLAN (Ralink) 2,363 2,985 3,025 2,919 1,867 9,365 11,292 10,668 12,774 13,370

Total Sales 23,986 31,370 34,211 30,107 86,858 99,278 119,674 121,050 132,081 145,215

GM % 42.1% 42.5% 43.5% 43.0% 45.3% 41.4% 42.8% 42.4% 43.1% 43.2%

Op M% 12.9% 18.8% 21.2% 17.9% 14.2% 12.5% 18.1% 18.0% 19.5% 21.0%

EPS $2.79 $4.77 $6.03 $4.67 $12.52 $12.85 $18.26 $18.26 $21.41 $24.69 Source: Company data, Credit Suisse estimates

2Q13 reaching the high-end of guidance, 3Q13 sub-

seasonal due to the high base

We are revising up 2Q13 sales to the high-end of the +25-32% QoQ guidance even with a

weak June near NT$8 bn and leaving gross margins at the midpoint at 42.5%, keeping

EPS unchanged at NT$4.77 versus street at NT$4.34. For 3Q13, we factor in +9% QoQ

growth and believe street is now up 17% QoQ (excluding outlier estimates still factoring in

revenue from the MStar closure in August 2013). While street sales estimates are a bit

aggressive at +17% QoQ, we believe GMs with the cost-down chips could improve 100 bp

QoQ, keeping our EPS unchanged and slightly above street. For full-year 2013/2014, we

estimate EPS at NT$18.26/NT$21.41, in the range of street at NT$18.43/NT$22.26.

Figure 30: Summary of our 2Q13E/3Q13E and 2013E/2014E estimates for MediaTek 2Q13 3Q13 2013 2014

(NT$ mn) CS CS(old) Street Guidance CS CS(old) Street CS CS(old) Street CS CS(old) Street

Sales $31,370 $30,905 $31,246 NT$30.0-$31.6bn $34,211 $35,320 $36,501 $119,662 $121,038 $127,154 $132,081 $134,671 $143,330

Chg 30.8% 28.9% 30.3% Up 25-32% 9.1% 14.3% 16.8% 20.5% 21.9% 28.1% 10.4% 11.3% 12.7%

GM% 42.5% 42.5% 42.8% 41.5-43.5% 43.5% 42.5% 43.1% 42.8% 42.4% 42.8% 43.1% 42.6% 43.2%

R&D 5,821 5,821 23-27% Opex 5,995 5,972 23,243 23,197 24,399 24,031

SG&A 1,602 1,602 1,650 1,650 6,397 6,402 6,731 6,717

OpM% 18.8% 18.4% 17.3% 14.5-20.5% 21.2% 20.9% 20.9% 18.1% 18.0% 18.2% 19.5% 19.8% 22.4%

Net Inc. 6,395 6,386 5,850 8,074 8,063 7,646 24,472 24,475 24,584 28,688 28,693 29,801

EPS (NT$) $4.77 $4.77 $4.34 $6.03 $6.02 $5.77 $18.26 $18.26 $18.43 $21.41 $21.41 $22.26 Source: Company data, Bloomberg, Credit Suisse estimates

Key assumption changes:

smartphone volumes slightly

lower after the May-June

dip, tablets revised higher

2Q13 likely at the high-end

of guidance; 3Q13 keeping

estimates for moderate

growth as new products

carry lower blended prices

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 13

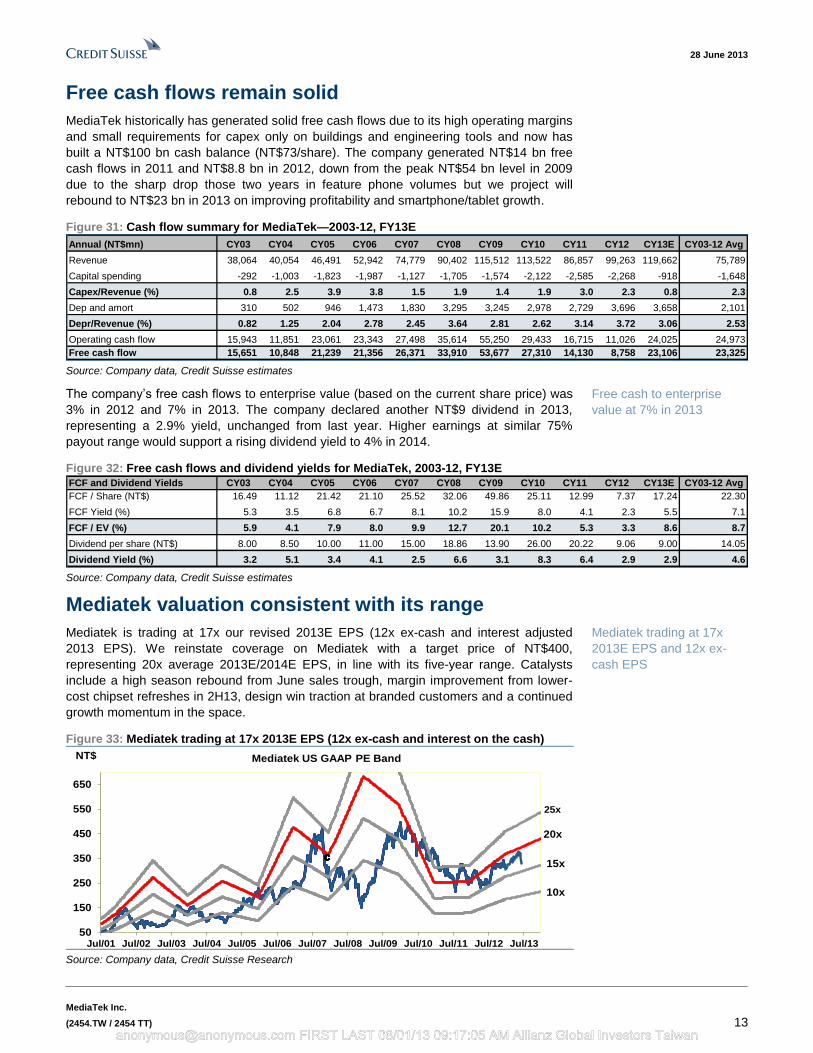

Free cash flows remain solid

MediaTek historically has generated solid free cash flows due to its high operating margins

and small requirements for capex only on buildings and engineering tools and now has

built a NT$100 bn cash balance (NT$73/share). The company generated NT$14 bn free

cash flows in 2011 and NT$8.8 bn in 2012, down from the peak NT$54 bn level in 2009

due to the sharp drop those two years in feature phone volumes but we project will

rebound to NT$23 bn in 2013 on improving profitability and smartphone/tablet growth.

Figure 31: Cash flow summary for MediaTek—2003-12, FY13E

Annual (NT$mn) CY03 CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13E CY03-12 Avg

Revenue 38,064 40,054 46,491 52,942 74,779 90,402 115,512 113,522 86,857 99,263 119,662 75,789

Capital spending -292 -1,003 -1,823 -1,987 -1,127 -1,705 -1,574 -2,122 -2,585 -2,268 -918 -1,648

Capex/Revenue (%) 0.8 2.5 3.9 3.8 1.5 1.9 1.4 1.9 3.0 2.3 0.8 2.3

Dep and amort 310 502 946 1,473 1,830 3,295 3,245 2,978 2,729 3,696 3,658 2,101

Depr/Revenue (%) 0.82 1.25 2.04 2.78 2.45 3.64 2.81 2.62 3.14 3.72 3.06 2.53

Operating cash flow 15,943 11,851 23,061 23,343 27,498 35,614 55,250 29,433 16,715 11,026 24,025 24,973

Free cash flow 15,651 10,848 21,239 21,356 26,371 33,910 53,677 27,310 14,130 8,758 23,106 23,325 Source: Company data, Credit Suisse estimates

The company’s free cash flows to enterprise value (based on the current share price) was

3% in 2012 and 7% in 2013. The company declared another NT$9 dividend in 2013,

representing a 2.9% yield, unchanged from last year. Higher earnings at similar 75%

payout range would support a rising dividend yield to 4% in 2014.

Figure 32: Free cash flows and dividend yields for MediaTek, 2003-12, FY13E FCF and Dividend Yields CY03 CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13E CY03-12 Avg

FCF / Share (NT$) 16.49 11.12 21.42 21.10 25.52 32.06 49.86 25.11 12.99 7.37 17.24 22.30

FCF Yield (%) 5.3 3.5 6.8 6.7 8.1 10.2 15.9 8.0 4.1 2.3 5.5 7.1

FCF / EV (%) 5.9 4.1 7.9 8.0 9.9 12.7 20.1 10.2 5.3 3.3 8.6 8.7

Dividend per share (NT$) 8.00 8.50 10.00 11.00 15.00 18.86 13.90 26.00 20.22 9.06 9.00 14.05

Dividend Yield (%) 3.2 5.1 3.4 4.1 2.5 6.6 3.1 8.3 6.4 2.9 2.9 4.6 Source: Company data, Credit Suisse estimates

Mediatek valuation consistent with its range

Mediatek is trading at 17x our revised 2013E EPS (12x ex-cash and interest adjusted

2013 EPS). We reinstate coverage on Mediatek with a target price of NT$400,

representing 20x average 2013E/2014E EPS, in line with its five-year range. Catalysts

include a high season rebound from June sales trough, margin improvement from lower-

cost chipset refreshes in 2H13, design win traction at branded customers and a continued

growth momentum in the space.

Figure 33: Mediatek trading at 17x 2013E EPS (12x ex-cash and interest on the cash)

10x

15x

20x

50

150

250

350

450

550

650

Jul/01 Jul/02 Jul/03 Jul/04 Jul/05 Jul/06 Jul/07 Jul/08 Jul/09 Jul/10 Jul/11 Jul/12 Jul/13

NT$ Mediatek US GAAP PE Band

ccccccccccccccccccccccc

25x

Source: Company data, Credit Suisse Research

Free cash to enterprise

value at 7% in 2013

Mediatek trading at 17x

2013E EPS and 12x ex-

cash EPS

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 14

Investor sentiment is not over-optimistic on Mediatek, with QFII holdings at 50%, sixth

highest among Taiwan tech and below the 61% peak in 2011, and with TSMC and Delta

well over 70%. Our Taiwan strategist Chung Hsu notes that fund flows are in the mid-

range for relative ownership in the IC design sector and points out that IC design is the

second most preferred sector for retail long margin balances in Taiwan after hardware

components at a 12% weighting of long margin vs. a 4% MSCI weighting (see our report).

Retail optimism following the favourable capital gains tax revision could flow into the sector

and Mediatek if retail investment preferences fall in line with history.

Figure 34: Mediatek – QFII ownership still not stretched Figure 35: MTK’s QFII is in the mid-range of its tech peers

0

100

200

300

400

500

600

700

0

10

20

30

40

50

60

70

Jul-0

1

Jan

-02

Jul-0

2

Jan

-03

Jul-0

3

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

Jan

-06

Jul-0

6

Jan

-07

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

Jan

-11

Jul-1

1

Jan

-12

Jul-1

2

Jan

-13

Share Price (NT$)QFII Holding (%)

MTK Stock Price (NT$) MTK QFII Holding (%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

TS

MC

De

lta

AS

E

Asu

ste

k

Co

mpa

l

Me

dia

tek

Ho

n H

ai

UM

C

Qu

an

ta

HT

C

Ca

tch

er

QFII (%)

Source: TEJ, Company data, Credit Suisse research Source: TEJ, Company data, Credit Suisse research

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 15

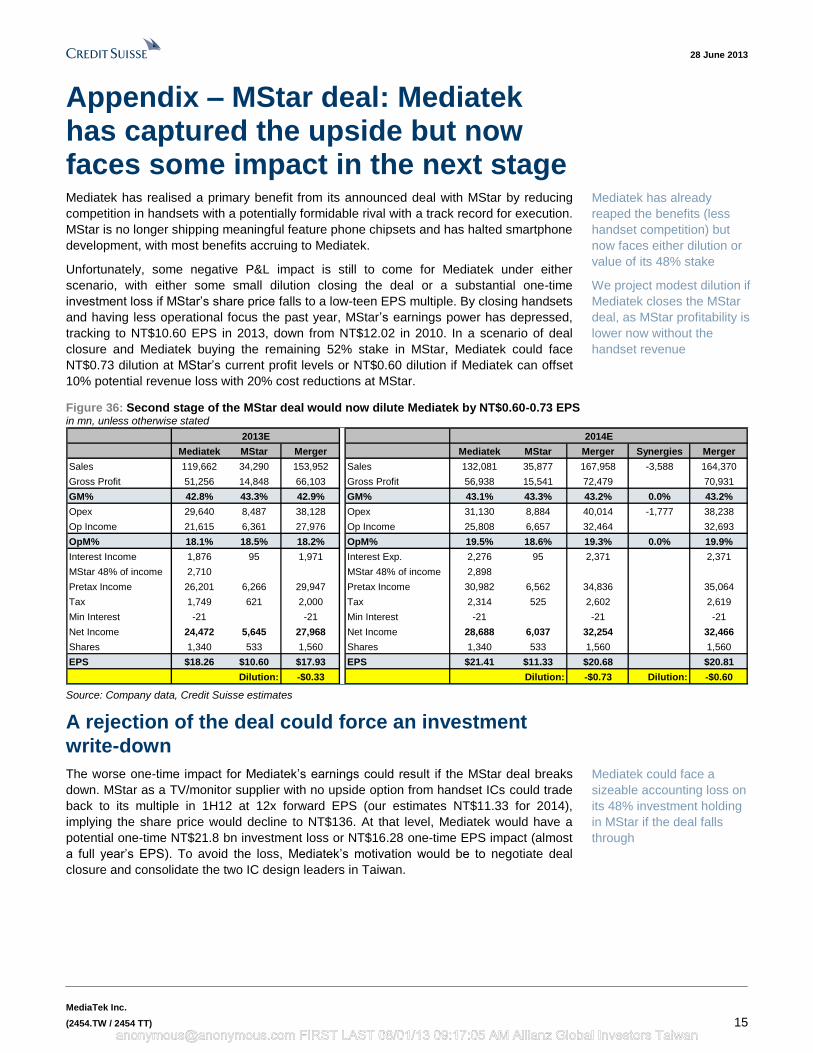

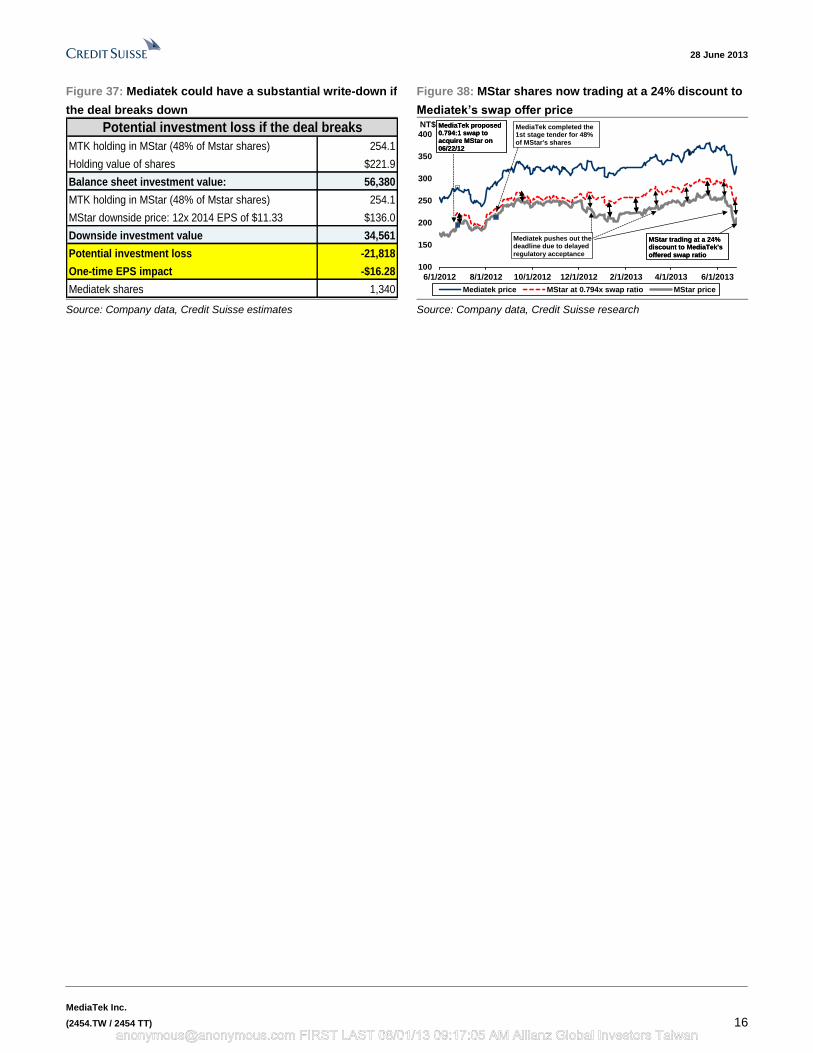

Appendix – MStar deal: Mediatek has captured the upside but now faces some impact in the next stage Mediatek has realised a primary benefit from its announced deal with MStar by reducing

competition in handsets with a potentially formidable rival with a track record for execution.

MStar is no longer shipping meaningful feature phone chipsets and has halted smartphone

development, with most benefits accruing to Mediatek.

Unfortunately, some negative P&L impact is still to come for Mediatek under either

scenario, with either some small dilution closing the deal or a substantial one-time

investment loss if MStar’s share price falls to a low-teen EPS multiple. By closing handsets

and having less operational focus the past year, MStar’s earnings power has depressed,

tracking to NT$10.60 EPS in 2013, down from NT$12.02 in 2010. In a scenario of deal

closure and Mediatek buying the remaining 52% stake in MStar, Mediatek could face

NT$0.73 dilution at MStar’s current profit levels or NT$0.60 dilution if Mediatek can offset

10% potential revenue loss with 20% cost reductions at MStar.

Figure 36: Second stage of the MStar deal would now dilute Mediatek by NT$0.60-0.73 EPS in mn, unless otherwise stated

2013E 2014E Potential investment loss if the deal breaks

Mediatek MStar Merger Mediatek MStar Merger Synergies Merger

Sales 119,662 34,290 153,952 Sales 132,081 35,877 167,958 -3,588 164,370

Gross Profit 51,256 14,848 66,103 Gross Profit 56,938 15,541 72,479 70,931

GM% 42.8% 43.3% 42.9% GM% 43.1% 43.3% 43.2% 0.0% 43.2%

Opex 29,640 8,487 38,128 Opex 31,130 8,884 40,014 -1,777 38,238

Op Income 21,615 6,361 27,976 Op Income 25,808 6,657 32,464 32,693

OpM% 18.1% 18.5% 18.2% OpM% 19.5% 18.6% 19.3% 0.0% 19.9%

Interest Income 1,876 95 1,971 Interest Exp. 2,276 95 2,371 2,371

MStar 48% of income 2,710 MStar 48% of income 2,898

Pretax Income 26,201 6,266 29,947 Pretax Income 30,982 6,562 34,836 35,064

Tax 1,749 621 2,000 Tax 2,314 525 2,602 2,619

Min Interest -21 -21 Min Interest -21 -21 -21

Net Income 24,472 5,645 27,968 Net Income 28,688 6,037 32,254 32,466

Shares 1,340 533 1,560 Shares 1,340 533 1,560 1,560

EPS $18.26 $10.60 $17.93 EPS $21.41 $11.33 $20.68 $20.81

Dilution: -$0.33 Dilution: -$0.73 Dilution: -$0.60 Source: Company data, Credit Suisse estimates

A rejection of the deal could force an investment

write-down

The worse one-time impact for Mediatek’s earnings could result if the MStar deal breaks

down. MStar as a TV/monitor supplier with no upside option from handset ICs could trade

back to its multiple in 1H12 at 12x forward EPS (our estimates NT$11.33 for 2014),

implying the share price would decline to NT$136. At that level, Mediatek would have a

potential one-time NT$21.8 bn investment loss or NT$16.28 one-time EPS impact (almost

a full year’s EPS). To avoid the loss, Mediatek’s motivation would be to negotiate deal

closure and consolidate the two IC design leaders in Taiwan.

Mediatek has already

reaped the benefits (less

handset competition) but

now faces either dilution or

value of its 48% stake

We project modest dilution if

Mediatek closes the MStar

deal, as MStar profitability is

lower now without the

handset revenue

Mediatek could face a

sizeable accounting loss on

its 48% investment holding

in MStar if the deal falls

through

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 16

Figure 37: Mediatek could have a substantial write-down if

the deal breaks down

Figure 38: MStar shares now trading at a 24% discount to

Mediatek’s swap offer price

Potential investment loss if the deal breaks

MTK holding in MStar (48% of Mstar shares) 254.1

Holding value of shares $221.9

Balance sheet investment value: 56,380

MTK holding in MStar (48% of Mstar shares) 254.1

MStar downside price: 12x 2014 EPS of $11.33 $136.0

Downside investment value 34,561

Potential investment loss -21,818

One-time EPS impact -$16.28

Mediatek shares 1,340

100

150

200

250

300

350

400

6/1/2012 8/1/2012 10/1/2012 12/1/2012 2/1/2013 4/1/2013 6/1/2013

NT$

Mediatek price MStar at 0.794x swap ratio MStar price

MStar trading at a 24% discount to MediaTek's offered swap ratio

MediaTek proposed 0.794:1 swap to acquire MStar on 06/22/12

MediaTek completed the 1st stage tender for 48% of MStar's shares

MStar trading at a 24% discount to MediaTek's offered swap ratio

MediaTek proposed 0.794:1 swap to acquire MStar on 06/22/12

Mediatek pushes out the deadline due to delayed regulatory acceptance

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse research

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 17

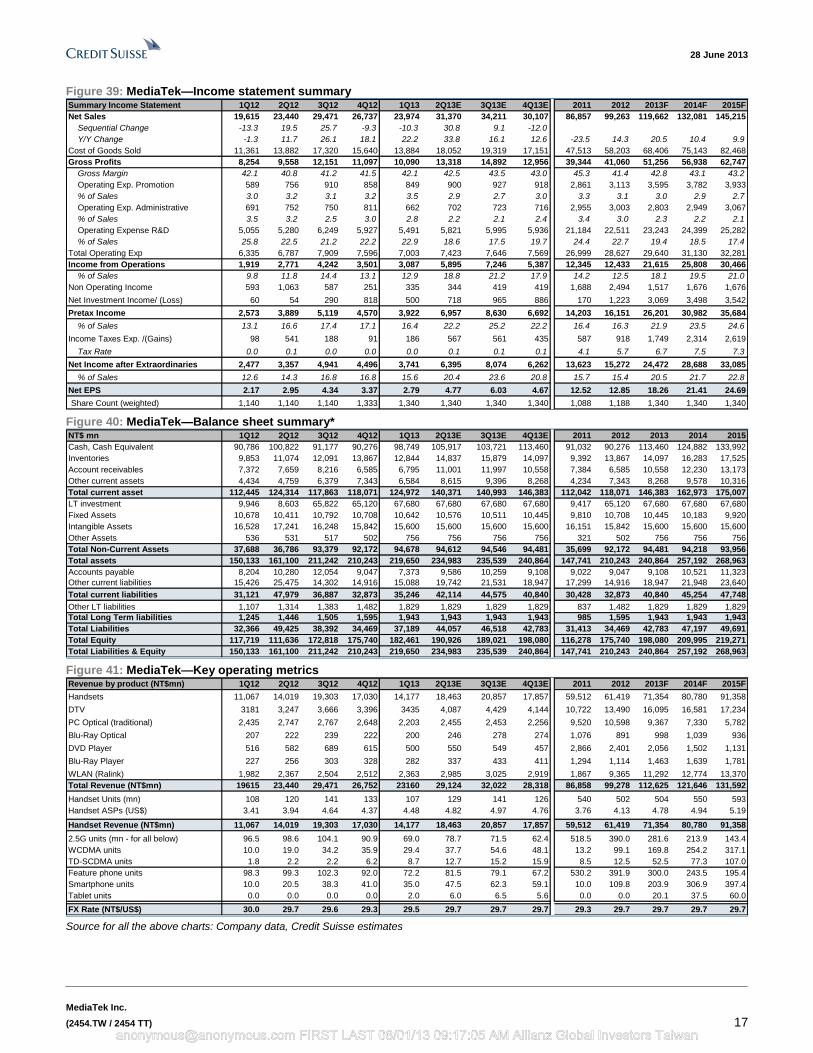

Figure 39: MediaTek—Income statement summary Summary Income Statement 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13E 3Q13E 4Q13E 2011 2012 2013F 2014F 2015F

Net Sales 19,615 23,440 29,471 26,737 23,974 31,370 34,211 30,107 86,857 99,263 119,662 132,081 145,215

Sequential Change -13.3 19.5 25.7 -9.3 -10.3 30.8 9.1 -12.0

Y/Y Change -1.3 11.7 26.1 18.1 22.2 33.8 16.1 12.6 -23.5 14.3 20.5 10.4 9.9

Cost of Goods Sold 11,361 13,882 17,320 15,640 13,884 18,052 19,319 17,151 47,513 58,203 68,406 75,143 82,468

Gross Profits 8,254 9,558 12,151 11,097 10,090 13,318 14,892 12,956 39,344 41,060 51,256 56,938 62,747

Gross Margin 42.1 40.8 41.2 41.5 42.1 42.5 43.5 43.0 45.3 41.4 42.8 43.1 43.2

Operating Exp. Promotion 589 756 910 858 849 900 927 918 2,861 3,113 3,595 3,782 3,933

% of Sales 3.0 3.2 3.1 3.2 3.5 2.9 2.7 3.0 3.3 3.1 3.0 2.9 2.7

Operating Exp. Administrative 691 752 750 811 662 702 723 716 2,955 3,003 2,803 2,949 3,067

% of Sales 3.5 3.2 2.5 3.0 2.8 2.2 2.1 2.4 3.4 3.0 2.3 2.2 2.1

Operating Expense R&D 5,055 5,280 6,249 5,927 5,491 5,821 5,995 5,936 21,184 22,511 23,243 24,399 25,282

% of Sales 25.8 22.5 21.2 22.2 22.9 18.6 17.5 19.7 24.4 22.7 19.4 18.5 17.4

Total Operating Exp 6,335 6,787 7,909 7,596 7,003 7,423 7,646 7,569 26,999 28,627 29,640 31,130 32,281

Income from Operations 1,919 2,771 4,242 3,501 3,087 5,895 7,246 5,387 12,345 12,433 21,615 25,808 30,466

% of Sales 9.8 11.8 14.4 13.1 12.9 18.8 21.2 17.9 14.2 12.5 18.1 19.5 21.0

Non Operating Income 593 1,063 587 251 335 344 419 419 1,688 2,494 1,517 1,676 1,676

Net Investment Income/ (Loss) 60 54 290 818 500 718 965 886 170 1,223 3,069 3,498 3,542

Pretax Income 2,573 3,889 5,119 4,570 3,922 6,957 8,630 6,692 14,203 16,151 26,201 30,982 35,684

% of Sales 13.1 16.6 17.4 17.1 16.4 22.2 25.2 22.2 16.4 16.3 21.9 23.5 24.6

Income Taxes Exp. /(Gains) 98 541 188 91 186 567 561 435 587 918 1,749 2,314 2,619

Tax Rate 0.0 0.1 0.0 0.0 0.0 0.1 0.1 0.1 4.1 5.7 6.7 7.5 7.3

Net Income after Extraordinaries 2,477 3,357 4,941 4,496 3,741 6,395 8,074 6,262 13,623 15,272 24,472 28,688 33,085

% of Sales 12.6 14.3 16.8 16.8 15.6 20.4 23.6 20.8 15.7 15.4 20.5 21.7 22.8

Net EPS 2.17 2.95 4.34 3.37 2.79 4.77 6.03 4.67 12.52 12.85 18.26 21.41 24.69

Share Count (weighted) 1,140 1,140 1,140 1,333 1,340 1,340 1,340 1,340 1,088 1,188 1,340 1,340 1,340

Figure 40: MediaTek—Balance sheet summary* NT$ mn 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13E 3Q13E 4Q13E 2011 2012 2013 2014 2015

Cash, Cash Equivalent 90,786 100,822 91,177 90,276 98,749 105,917 103,721 113,460 91,032 90,276 113,460 124,882 133,992

Inventories 9,853 11,074 12,091 13,867 12,844 14,837 15,879 14,097 9,392 13,867 14,097 16,283 17,525

Account receivables 7,372 7,659 8,216 6,585 6,795 11,001 11,997 10,558 7,384 6,585 10,558 12,230 13,173

Other current assets 4,434 4,759 6,379 7,343 6,584 8,615 9,396 8,268 4,234 7,343 8,268 9,578 10,316

Total current asset 112,445 124,314 117,863 118,071 124,972 140,371 140,993 146,383 112,042 118,071 146,383 162,973 175,007

LT investment 9,946 8,603 65,822 65,120 67,680 67,680 67,680 67,680 9,417 65,120 67,680 67,680 67,680

Fixed Assets 10,678 10,411 10,792 10,708 10,642 10,576 10,511 10,445 9,810 10,708 10,445 10,183 9,920

Intangible Assets 16,528 17,241 16,248 15,842 15,600 15,600 15,600 15,600 16,151 15,842 15,600 15,600 15,600

Other Assets 536 531 517 502 756 756 756 756 321 502 756 756 756

Total Non-Current Assets 37,688 36,786 93,379 92,172 94,678 94,612 94,546 94,481 35,699 92,172 94,481 94,218 93,956

Total assets 150,133 161,100 211,242 210,243 219,650 234,983 235,539 240,864 147,741 210,243 240,864 257,192 268,963

Accounts payable 8,204 10,280 12,054 9,047 7,373 9,586 10,259 9,108 9,022 9,047 9,108 10,521 11,323

Other current liabilities 15,426 25,475 14,302 14,916 15,088 19,742 21,531 18,947 17,299 14,916 18,947 21,948 23,640

Total current liabilities 31,121 47,979 36,887 32,873 35,246 42,114 44,575 40,840 30,428 32,873 40,840 45,254 47,748

Other LT liabilities 1,107 1,314 1,383 1,482 1,829 1,829 1,829 1,829 837 1,482 1,829 1,829 1,829

Total Long Term liabilities 1,245 1,446 1,505 1,595 1,943 1,943 1,943 1,943 985 1,595 1,943 1,943 1,943

Total Liabilities 32,366 49,425 38,392 34,469 37,189 44,057 46,518 42,783 31,413 34,469 42,783 47,197 49,691

Total Equity 117,719 111,636 172,818 175,740 182,461 190,926 189,021 198,080 116,278 175,740 198,080 209,995 219,271

Total Liabilities & Equity 150,133 161,100 211,242 210,243 219,650 234,983 235,539 240,864 147,741 210,243 240,864 257,192 268,963

Figure 41: MediaTek—Key operating metrics Revenue by product (NT$mn) 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13E 3Q13E 4Q13E 2011 2012 2013F 2014F 2015F

Handsets 11,067 14,019 19,303 17,030 14,177 18,463 20,857 17,857 59,512 61,419 71,354 80,780 91,358

DTV 3181 3,247 3,666 3,396 3435 4,087 4,429 4,144 10,722 13,490 16,095 16,581 17,234

PC Optical (traditional) 2,435 2,747 2,767 2,648 2,203 2,455 2,453 2,256 9,520 10,598 9,367 7,330 5,782

Blu-Ray Optical 207 222 239 222 200 246 278 274 1,076 891 998 1,039 936

DVD Player 516 582 689 615 500 550 549 457 2,866 2,401 2,056 1,502 1,131

Blu-Ray Player 227 256 303 328 282 337 433 411 1,294 1,114 1,463 1,639 1,781

WLAN (Ralink) 1,982 2,367 2,504 2,512 2,363 2,985 3,025 2,919 1,867 9,365 11,292 12,774 13,370

Total Revenue (NT$mn) 19615 23,440 29,471 26,752 23160 29,124 32,022 28,318 86,858 99,278 112,625 121,646 131,592

Handset Units (mn) 108 120 141 133 107 129 141 126 540 502 504 550 593

Handset ASPs (US$) 3.41 3.94 4.64 4.37 4.48 4.82 4.97 4.76 3.76 4.13 4.78 4.94 5.19

Handset Revenue (NT$mn) 11,067 14,019 19,303 17,030 14,177 18,463 20,857 17,857 59,512 61,419 71,354 80,780 91,358

2.5G units (mn - for all below) 96.5 98.6 104.1 90.9 69.0 78.7 71.5 62.4 518.5 390.0 281.6 213.9 143.4

WCDMA units 10.0 19.0 34.2 35.9 29.4 37.7 54.6 48.1 13.2 99.1 169.8 254.2 317.1

TD-SCDMA units 1.8 2.2 2.2 6.2 8.7 12.7 15.2 15.9 8.5 12.5 52.5 77.3 107.0

Feature phone units 98.3 99.3 102.3 92.0 72.2 81.5 79.1 67.2 530.2 391.9 300.0 243.5 195.4

Smartphone units 10.0 20.5 38.3 41.0 35.0 47.5 62.3 59.1 10.0 109.8 203.9 306.9 397.4

Tablet units 0.0 0.0 0.0 0.0 2.0 6.0 6.5 5.6 0.0 0.0 20.1 37.5 60.0

FX Rate (NT$/US$) 30.0 29.7 29.6 29.3 29.5 29.7 29.7 29.7 29.3 29.7 29.7 29.7 29.7 Source for all the above charts: Company data, Credit Suisse estimates

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 18

Companies Mentioned (Price as of 27-Jun-2013)

ARM Holdings (ARM.L, 795.0p) Acer Group (2353.TW, NT$21.4) Actions (ACTS.OQ, $2.9) Apple Inc (AAPL.OQ, $398.07) Asustek (2357.TW, NT$272.5) Broadcom Corp. (BRCM.OQ, $33.87) China Mobile Limited (0941.HK, HK$77.85) China Telecom (0728.HK, HK$3.7) China Unicom Hong Kong Ltd (0762.HK, HK$10.06) Datang International Power Generation Co. Ltd. (0991.HK, HK$3.01) Google, Inc. (GOOG.OQ, $873.65) HiSilicon (Unlisted) Hisense Kelon (0921.HK, HK$4.1) Huawei Tech (002502.SZ, Rmb8.36) Imagination Technologies (IMG.L, 295.5p) Intel Corp. (INTC.OQ, $24.01) Lenovo Group Ltd (0992.HK, HK$7.02) Marvell Technology Group Ltd. (MRVL.OQ, $11.73) MediaTek Inc. (2454.TW, NT$328.0, OUTPERFORM, TP NT$400.0) NVIDIA (NVDA.OQ, $14.14) QUALCOMM Inc. (QCOM.OQ, $61.27) RDA Microelectronics (RDA.OQ, $11.65) Realtek Semiconductor (2379.TW, NT$68.5) ST-Ericsson (Unlisted) Samsung Electronics (005930.KS, W1,339,000) Spreadtrum Communication (SPRD.OQ, $26.25) TCL Comm (2618.HK, HK$3.53) ZTE Corporation (0763.HK, HK$12.56)

Disclosure Appendix

Important Global Disclosures

I, Randy Abrams, CFA, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for MediaTek Inc. (2454.TW)

2454.TW Closing Price Target Price

Date (NT$) (NT$) Rating

02-Jul-10 424.65 475.00 N

28-Jul-10 442.00 440.00

07-Sep-10 472.00 475.00

06-Oct-10 412.50 370.00 U

02-Nov-10 387.50 350.00

08-Mar-11 341.00 315.00

19-Apr-11 309.00 295.00

02-May-11 316.50 315.00 N

23-May-11 310.00 300.00

07-Jun-11 313.50 280.00 U

28-Jul-11 266.00 255.00

07-Sep-11 282.50 260.00

31-Oct-11 318.00 306.00

06-Jan-12 278.50 270.00

04-Apr-12 277.00 300.00 N

30-Apr-12 253.00 260.00

25-Jun-12 280.50 300.00

29-Jun-12 273.00 R

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

U N D ERPERFO RM

REST RICT ED

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

[email protected] FIRST LAST 08/01/13 09:17:05 AM Allianz Global Investors Taiwan

28 June 2013

MediaTek Inc.

(2454.TW / 2454 TT) 19

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s tota l return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractiv e, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin Ame rican and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; Australia, New Zealand are, and prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, 12 -month rolling yield is incorporated in the absolute total return calculation and a 15% and a 7.5% threshold replace the 10-15% level in the Outperform and Underperform stock rating definitions, respectively. The 15% and 7.5% thresholds replace the +10-15% and -10-15% levels in the Neutral stock rating definition, respectively. Prior to 10th December 2012, Japanese ratings we re based on a stock’s total return relative to the average total return of the relevant country or regional benchmark.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.