INTERNATIONALBUSINESSFINANCE FINS3616 Tutorial Week 2 Chapters 3 + 5

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 1/17

INTERNATIONALBUSINESSFINANCE

FINS3616

Tutorial

Week

2Chapters 3 + 5

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 2/17

Your Tutor

&

Tutor

‐in

‐Charge:

Peter Andersen

2

CONTACTDETAILS

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 3/17

Q. If the

spot

exchange

rate

of

the

yen

relative

to

the

dollar

is

¥105.75,

and

the

90‐day forward rate is ¥103.25/$, is the dollar at a forward premium or

discount? Express the premium or discount as a percentage per annum for a

360‐

day

year?

A. The dollar is at a discount as one $ is worth less for trading in 90 days time than

at today’s spot rate.

3

CHAPTER3— PROBLEM1

¥103.25/$ ¥105.75/$ 360100

¥105.75/$ 90

d/f d/f

n 0

d/f

0

F S 360100

S n

f

f

9.46%

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 4/17

Q. As a foreign

exchange

trader

for

JPMorgan

Chase,

you

have

just

called

a

trader at UBS to get quotes for the British pound for the spot, 30‐day, 60‐day,

and 90‐day forward rates. Your UBS counterpart stated, “We trade sterling at

$1.7745‐

50,

47/44,

88/81,

125/115.”

What

cash

flows

would

you

pay

and

receive if you do a forward foreign exchange swap in which you swap into

£5,000,000 at the 30‐day rate and out of £5,000,000 at the 90‐day rate? What

must be the relationship between dollar interest rates and pound sterling

interest rates?

A. Because the forward points are bigger/smaller, we subtract them from the spot

rate in order for the bid‐ask spread to widen as maturity lengthens.

4

CHAPTER3— PROBLEM3

$/£

0S $1.7745-50 / £

$/£

30F $1.7698-1.7706 / £

$/£

90F $1.7620-35 / £

Buy £5m at $1.7706/£

Sell £5m at $1.7620/£

= Pay $8,853,000 in 30d

= Receive $8,810,000 in 90d

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 5/17

Q. Consider the

following

spot

and

forward

rates

for

the

yen–euro

(¥/€)

exchange rates:

Is the euro at a forward premium or discount? What are the magnitudes of

the forward premiums or discounts when quoted in percentage per annum

for

a

360‐

day

year?A. Discount!

5

CHAPTER3— PROBLEM4

Spot 30 days 60 days 90 days 180 days 360 days

146.30 145.75 145.15 144.75 143.37 137.85

€

30 f

¥/€ ¥/€

n 0

¥/€0

F S 360100

S n

¥145.75/€ ¥146.30/€ 360100

¥146.30/€ 30

4.51%

€

90 f

¥144.75/€ ¥146.30/€ 360100

¥146.30/€ 90

4.24%

€

360 f

¥137.85/€ ¥146.30/€ 360

100¥146.30/€ 360

5.78%

i.e. not 365 days/year

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 6/17

Q. As a currency

trader,

you

see

the

following

quotes

on

your

computer

screen:

What are the outright forward bid and ask quotes for the USD/EUR at the 3‐

month maturity?

A.

Because the bid points are LESS THAN the ask points, we ADD them to the spot

rate.

6

CHAPTER3— PROBLEM5

Exch. Rate Spot 1‐month 2‐month 3‐month 6‐month

USD/EUR 1.0435/45 20/25 52/62 75/90 97/115

JPY/USD 98.75/85 12/10 20/16 25/19 45/35

USD/GBP 1.6623/33 30/35 62/75 95/110 120/130

$/€

0S $1.0435-45 / €

$/€

3F $1.0510-35 / €

Forward points = 75/90

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 7/17

Q. As a currency

trader,

you

see

the

following

quotes

on

your

computer

screen:

If one of your corporate customers calls you and wants to buy pounds with

dollars in 6 months, what price would you quote?

A.

As the customer wishes to purchase pounds and the quotes are given in terms

of $ price per pound, you would quote the higher ask rate of…

$1.6763/£

7

CHAPTER3— PROBLEM5

$/£0S $1.6623-33 / £

$/£6F $1.6743-63 / £

Exch. Rate Spot 1‐month 2‐month 3‐month 6‐month

USD/EUR 1.0435/45 20/25 52/62 75/90 97/115

JPY/USD 98.75/85 12/10 20/16 25/19 45/35

USD/GBP 1.6623/33 30/35 62/75 95/110 120/130

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 8/17

Q. Intel is

scheduled

to

receive

a payment

of

¥100,000,000

in

90

days

from

Sony

in connection with a shipment of computer chips that Sony is purchasing

from Intel. Suppose that the current exchange rate is ¥103/$, that analysts

are

forecasting

that

the

dollar

will

weaken

by

1%

over

the

next

90

days,

and

that the standard deviation of 90‐day forecasts of the percentage rate of

depreciation of the dollar relative to the yen is 4%.

Provide a qualitative description of Intel’s transaction exchange risk.

A. Intel is a U.S. company, and it is scheduled to receive yen in the future. A

weakening of the yen versus the dollar causes a given amount of yen to

convert to

fewer

dollars

in

the

future.

This loss of value could be severe if the yen depreciates by a significant

amount.

8

CHAPTER3— PROBLEM6

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 9/17

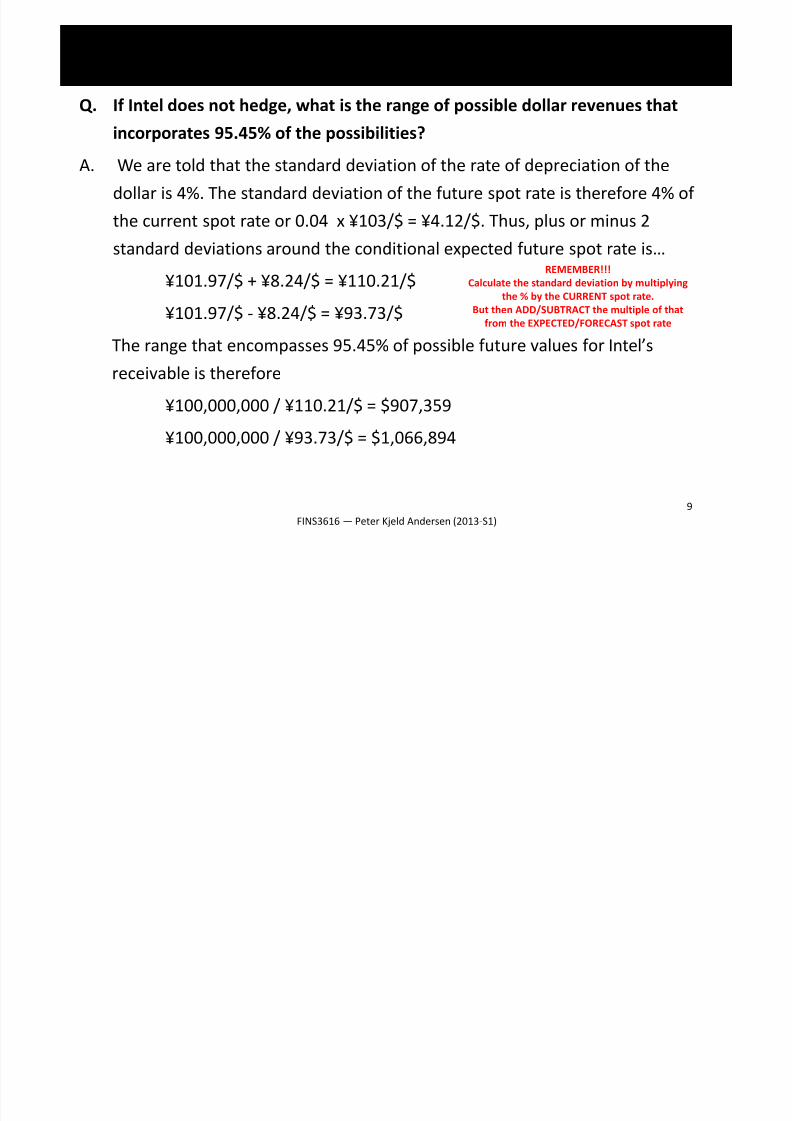

Q. If Intel

does

not

hedge,

what

is

the

range

of

possible

dollar

revenues

that

incorporates 95.45% of the possibilities?

A. We are told that the standard deviation of the rate of depreciation of the

dollar is

4%.

The

standard

deviation

of

the

future

spot

rate

is

therefore

4%

of

the current spot rate or 0.04 x ¥103/$ = ¥4.12/$. Thus, plus or minus 2

standard deviations around the conditional expected future spot rate is…

¥101.97/$ + ¥8.24/$ = ¥110.21/$

¥101.97/$ ‐ ¥8.24/$ = ¥93.73/$

The range that encompasses 95.45% of possible future values for Intel’s

receivable is therefore

¥100,000,000 / ¥110.21/$ = $907,359

¥100,000,000 / ¥93.73/$ = $1,066,894

9

CHAPTER3— PROBLEM6

REMEMBER!!!

Calculate the standard deviation by multiplying

the %

by

the

CURRENT

spot

rate.

But then ADD/SUBTRACT the multiple of that

from the EXPECTED/FORECAST spot rate

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 10/17

Q. How can

you

quantify

currency

risk

in

a floating

exchange

rate

system?

A. To characterize the risk of a currency position, you must try to characterize the

conditional distribution of the future exchange rate changes.

With floating exchange rates, historical information on standard deviations

provides useful information about this distribution.

The higher this volatility, the riskier are positions in this currency.

Finally, we

should

point

out

that

volatility

is

an

adequate

indicator

of

risk

when

exchange rate changes are approximately normally distributed.

In reality, the distribution of exchange rate changes displays fat tails, even in

floating exchange

rate

systems,

and

this

increases

the

risk

of

currency

positions.

10

CHAPTER5— QUESTION1

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 11/17

Q. Why might

it

be

hard

to

quantify

currency

risk

in

a target

zone

system

or

a

pegged exchange rate system?

A. If the

peg

or

target

zone

holds

for

a long

time,

historical

volatility

appears

to

be

zero or very limited, but this may not accurately reflect underlying tensions

that may ultimately result in a devaluation or revaluation of the currency.

Hence, the true currency risk does not show up in day‐to‐day fluctuations of

the exchange rate. It is hard to quantify this “latent volatility.”

11

CHAPTER5— QUESTION2

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 12/17

Q. What is

the

effect

of

a foreign

exchange

intervention

on

the

money

supply?

How can a central bank offset this effect and still hope to influence the

exchange rate?

A. When a central

bank

buys

(sells)

foreign

currency,

its

international

reserves

increase (decrease), and the money supply increases (decreases)

simultaneously.

To offset

the

effect

on

the

money

supply,

the

foreign

exchange

intervention

can

be sterilized; that is, the central bank can perform an open market operation

that counteracts the effect on the money supply of the original foreign

exchange intervention.

12

CHAPTER5— QUESTION7

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 13/17

Q. What is

the

effect

of

a foreign

exchange

intervention

on

the

money

supply?

How can a central bank offset this effect and still hope to influence the

exchange rate?

A. Continued…..

The direct effects of a sterilized intervention are two‐fold:

• First, it forces a portfolio shift on private investors, by replacing foreign bonds

with domestic

bonds

(or

vice

versa).

This

may

affect

expectations

and

prices.

• Second, the actions of the central bank in the foreign exchange markets, while

very small relative to the nominal trading volumes, may still manage to squeeze

foreign exchange inventories at dealer banks and generate pricing effects.

There is no consensus on how effective sterilized interventions are in affecting

the level and volatility of exchange rates.

13

CHAPTER5— QUESTION7

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 14/17

Q. Describe two

channels

through

which

foreign

exchange

interventions

may

affect

the value of the exchange rate.

A. There is a direct and an indirect channel.

The direct effect of forex purchases or sales is likely small, because trading volumes

are so large in the forex market.

The indirect channel refers to the fact that an intervention can alter peoples’

expectations and affect their investments, thus helping to push the exchange rate

in

the

direction

the

central

bank

desires.An intervention may be a signal to the public of the central bank’s monetary policy

intentions, or it may signal the central banks inside information about future

market fundamentals, or it may signal to investors that a currency’s exchange rate is

deviating too

far

from

its

long

‐run

equilibrium

value.

The signal is costly and therefore potentially more credible, because if the central

bank is wrong and, for example, buys an “undervalued” currency, which keeps

depreciating, the intervention will lose money.

14

CHAPTER5— QUESTION9

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 15/17

Q. How do

developing

countries

typically

manage

to

keep

currencies

pegged

at

values that are too high? Who benefits from such an overvalued currency? Who

is hurt by an overvalued currency?

A. Such a situation is difficult to maintain, because if the exchange rate overvalues the

local currency on the foreign exchange markets, there will be an excess supply of

the local currency—everybody will want to turn in local currency to the central

bank, receive foreign currencies, and invest them abroad.

If this

situation

persists,

the

central

bank’s

foreign

reserves

will

dwindle

quite

fast.

The only way to sustain such a system is to impose exchange controls.

The central bank of the developing country must ration the use of foreign

exchange, manage who gets access to it, and restrict capital flows; in short, it must

strictly control

financial

transactions

involving

foreign

currencies.

That currencies of developing countries are primarily traded by the central bank of

the country or by a number of financial institutions with strict controls on their use

of foreign currency (i.e. the currencies are inconvertible), is helpful to maintain

such a system.

15

CHAPTER5— QUESTION11

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 16/17

Q. How do

developing

countries

typically

manage

to

keep

currencies

pegged

at

values that are too high? Who benefits from such an overvalued currency?

Who is hurt by an overvalued currency?

A. It is

clear

who

benefits

and

who

loses

from

this

situation.

The fixed exchange rate undervalues the foreign currency and overvalues the

domestic currency, thereby subsidizing buyers of foreign currency (such as

importers

and

those

investing

abroad)

and

taxing

sellers

of

foreign

exchange

(such as exporters and foreign buyers of domestic assets).

Not surprisingly, one main reason for the popularity of over‐valued exchange

rates is that such situations increase the external purchasing power of the

political elite.

16

CHAPTER5— QUESTION11

FINS3616 — Peter Kjeld Andersen (2013‐S1)

7/27/2019 (2013-S1) - FINS3616 - Tutorial Slides - Week 03 - Forward Rates + Exchange Rate Systems

http://slidepdf.com/reader/full/2013-s1-fins3616-tutorial-slides-week-03-forward-rates-exchange 17/17

Q. Describe two

different

currency

systems

that

have

been

introduced

in

countries such as Hong Kong and Ecuador to improve the credibility of

pegged exchange rate systems.

A. Hong Kong

has

a currency

board

system.

A currency board is a monetary institution that issues base money (notes and

coins, and required reserves of financial institutions) that is fully backed by a

foreign

reserve

currency

and

fully

convertible

into

the

reserve

currency

at

a

fixed rate and on demand.

Hence, the domestic currency monetary base is 100% backed by assets payable

in the reserve currency. In practical terms, this requirement bars the currency

board from extending credit to either the government or the banking sector.

Ecuador instead has officially adopted the U.S. dollar as its currency. This is an

example of (“Official”) dollarization, which occurs when a foreign currency has

exclusive or

predominant

status

as

full

legal

tender

in

a particular

country. 17

CHAPTER5— QUESTION13

FINS3616 — Peter Kjeld Andersen (2013‐S1)

Related Documents