2013 and 2014 Income and Estate Tax Issues January 14, 2014 J C. Hobbs - Assistant Extension Specialist OSU Department of Agricultural Economics

2013 and 2014 Income and Estate Tax Issues January 14, 2014 J C. Hobbs - Assistant Extension Specialist OSU Department of Agricultural Economics.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2013 and 2014 Income and Estate Tax Issues

January 14, 2014

J C. Hobbs - Assistant Extension SpecialistOSU Department of Agricultural Economics

2013 & 2014 Income Tax Rates

• 2013 and the future rates are to be: 10, 15, 25, 28, 33, 35, and 39.6 percent.

• 39.6% rate applies to:– Single Filers with TI > $400,000

($406,750)– Married Filers with TI > $450,000

($457,600)– Head of Household Filers with TI >

$425,000– Married Filing Separate with TI >

$225,000

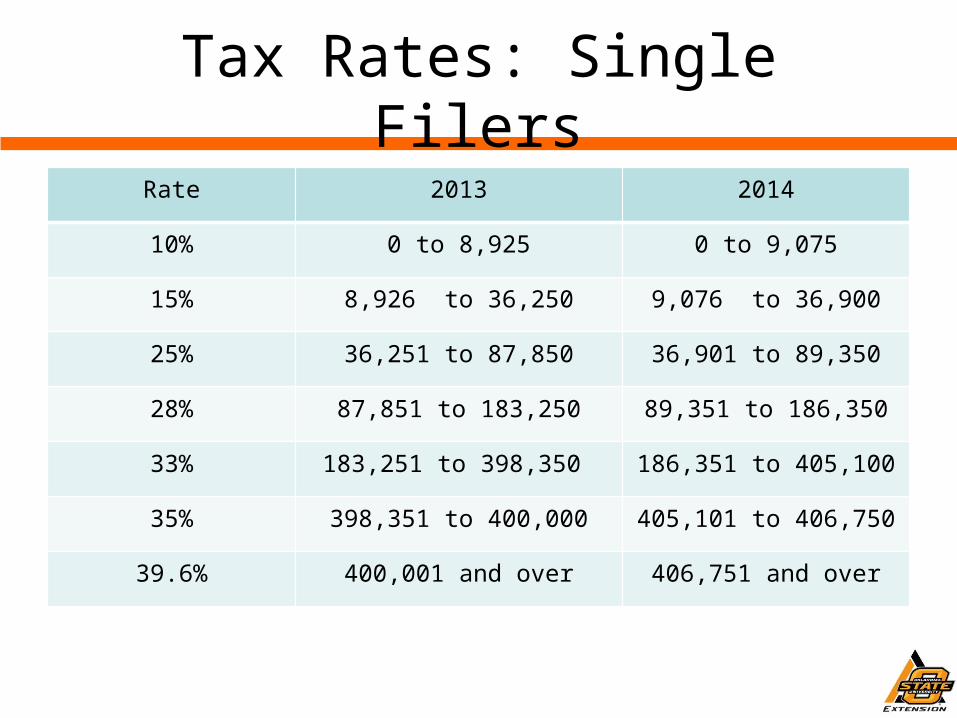

Tax Rates: Single FilersRate 2013 2014

10% 0 to 8,925 0 to 9,075

15% 8,926 to 36,250 9,076 to 36,900

25% 36,251 to 87,850 36,901 to 89,350

28% 87,851 to 183,250 89,351 to 186,350

33% 183,251 to 398,350 186,351 to 405,100

35% 398,351 to 400,000 405,101 to 406,750

39.6% 400,001 and over 406,751 and over

Tax Rates: Married Filing Joint

Rate 2013 2014

10% 0 to 17,850 0 to 18,150

15% 17,851 to 72,500 18,151 to 73,800

25% 72,501 to 146,400 73,801 to 148,850

28% 146,401 to 223,050 148,851 to 226,850

33% 223,051 to 398,350 226,851 to 405,100

35% 398,351 to 450,000 405,101 to 457,600

39.6% 450,001 and over 457,601 and over

Net Investment Income Taxbeginning in 2013

• Net Investment Income Tax on unearned income at a 3.8% rate if modified adjusted gross income exceeds $250,000 for married filing joint or $200,000 all others.

• Net investment income - applies to interest, dividends, annuities, royalties and rent (unless it is from business activities).

• Net income from the sale of capital investments including stock and real estate (unless it is from the sale of business property).

Net Investment Income Taxafter Dec. 31, 2012

• Does not include wages, social security, self-employment income, alimony, unemployment, tax exempt interest, distributions from qualified retirement plans, etc.

• Does not apply to the exclusion allowed on the sale of a principal residence of $250,000 for individuals or $500,000 on a joint return.

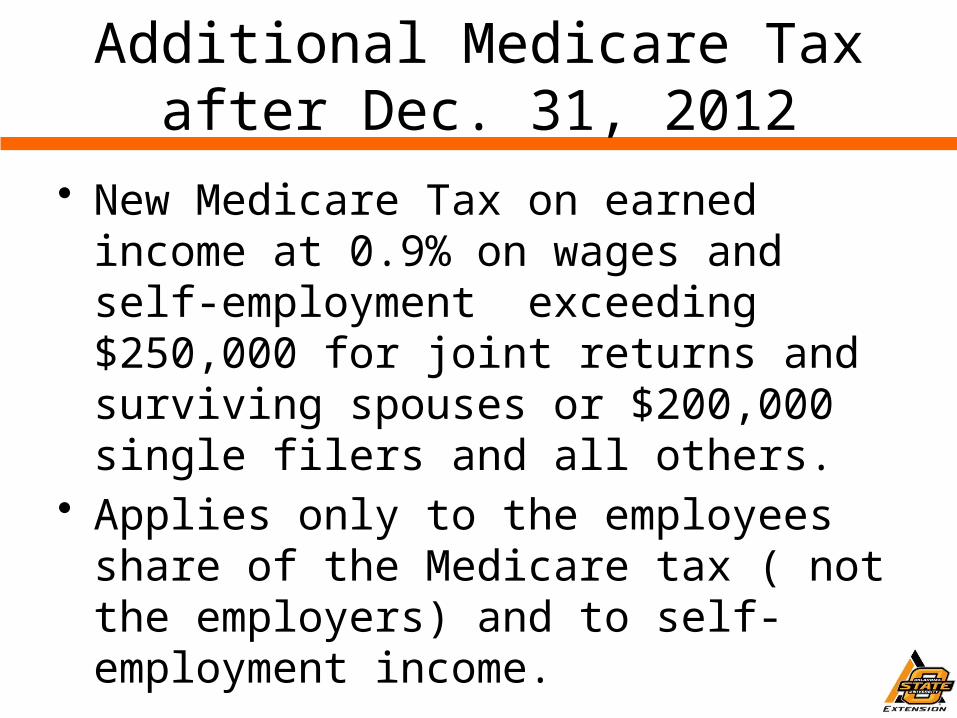

Additional Medicare Taxafter Dec. 31, 2012

• New Medicare Tax on earned income at 0.9% on wages and self-employment exceeding $250,000 for joint returns and surviving spouses or $200,000 single filers and all others.

• Applies only to the employees share of the Medicare tax ( not the employers) and to self-employment income.

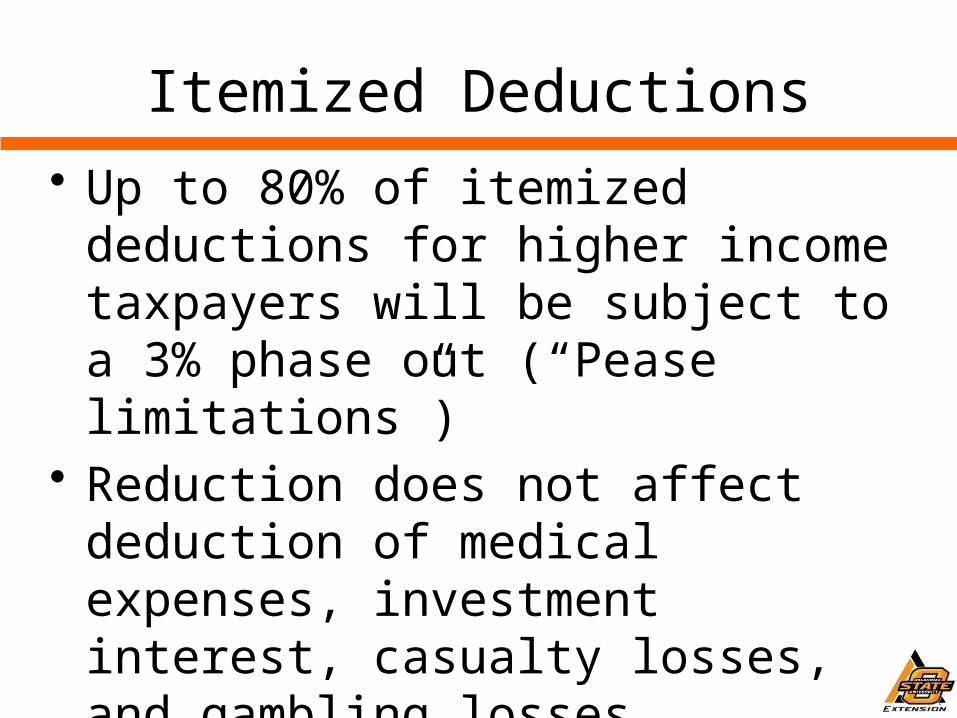

Itemized Deductions• Up to 80% of itemized deductions

for higher income taxpayers will be subject to a 3% phase out (“Pease limitations”)

• Reduction does not affect deduction of medical expenses, investment interest, casualty losses, and gambling losses

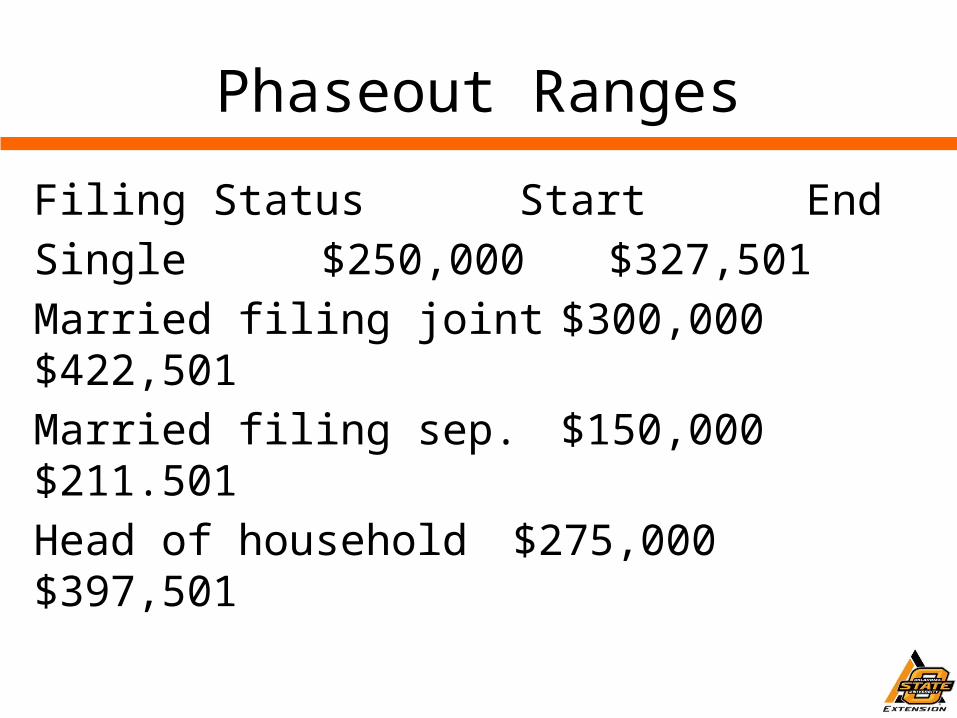

Phaseout Ranges

Filing Status Start EndSingle $250,000$327,501Married filing joint $300,000$422,501Married filing sep.$150,000$211.501Head of household $275,000$397,501

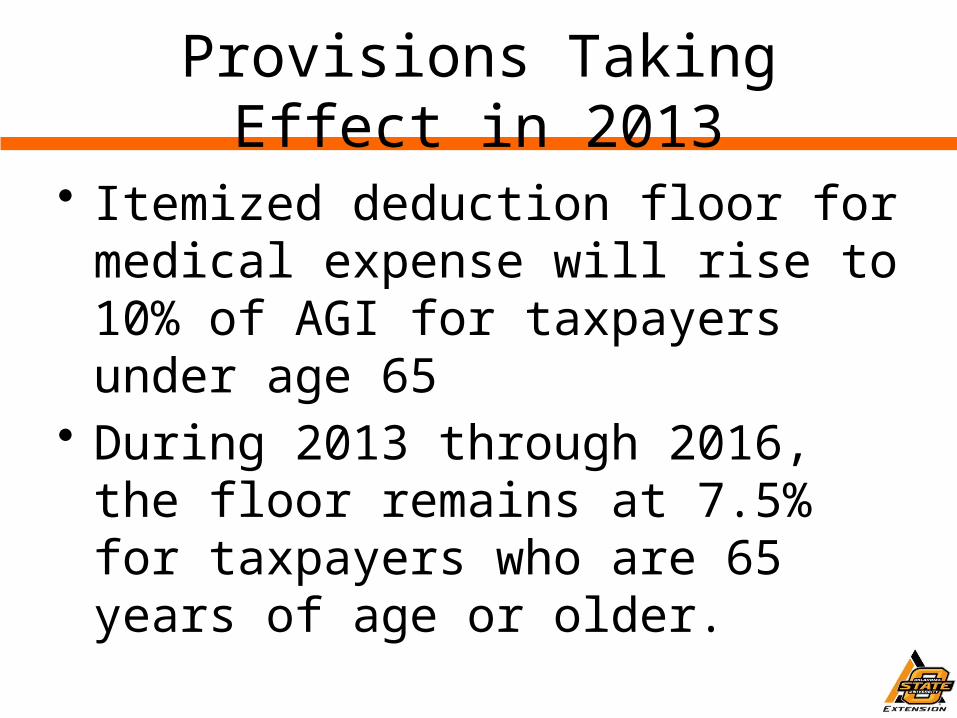

Provisions Taking Effect in 2013

• Itemized deduction floor for medical expense will rise to 10% of AGI for taxpayers under age 65

• During 2013 through 2016, the floor remains at 7.5% for taxpayers who are 65 years of age or older.

Capital Gain Rates

• Capital gains for 2013 and 2014– Net capital gain is taxed at the 0% rate

for taxpayers in the 10% and 15% income tax brackets.

– Net capital gain is taxed at the 15% rate for taxpayers in the 25%, 28%, 33%, and 35% income tax brackets.

– Net capital gain is taxed at the 20% rate for taxpayers in the 39.6% income tax bracket.

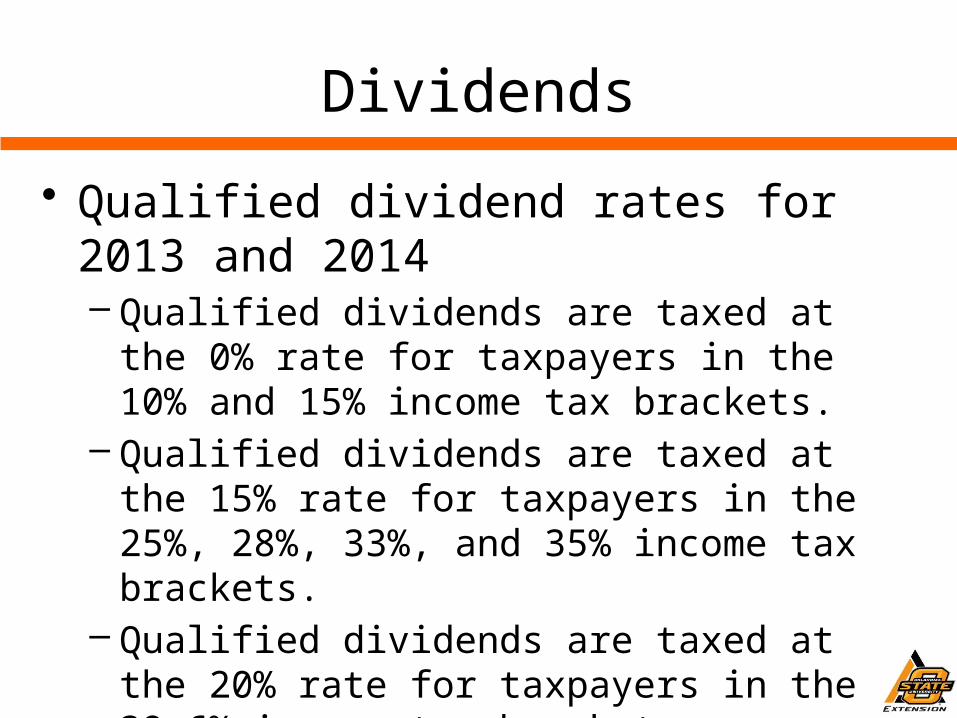

Dividends

• Qualified dividend rates for 2013 and 2014– Qualified dividends are taxed at the 0%

rate for taxpayers in the 10% and 15% income tax brackets.

– Qualified dividends are taxed at the 15% rate for taxpayers in the 25%, 28%, 33%, and 35% income tax brackets.

– Qualified dividends are taxed at the 20% rate for taxpayers in the 39.6% income tax bracket.

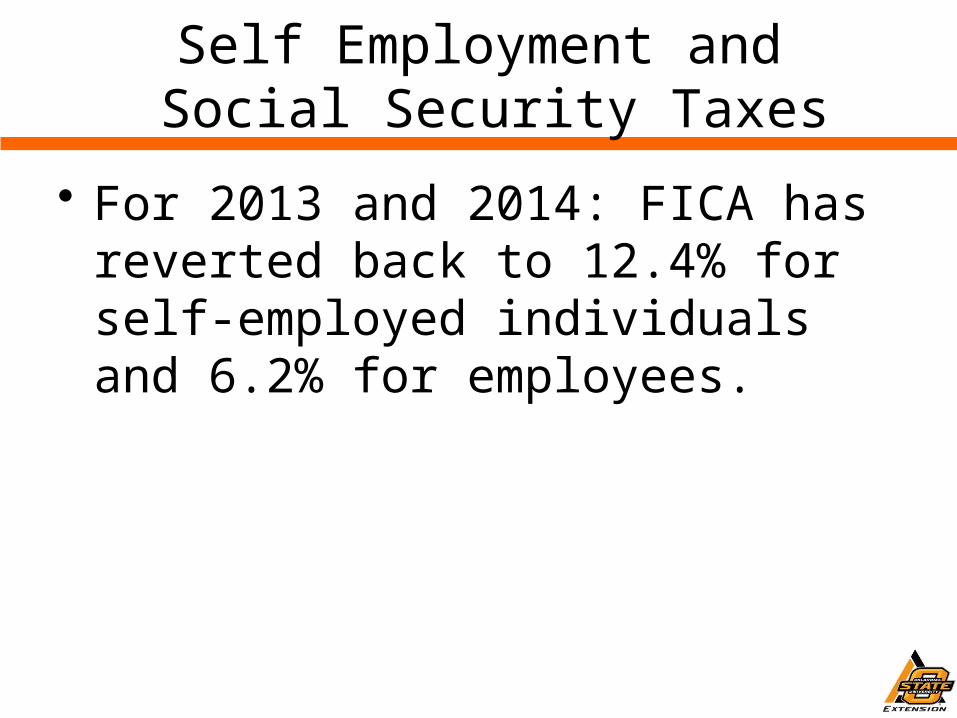

Self Employment and Social Security Taxes

• For 2013 and 2014: FICA has reverted back to 12.4% for self-employed individuals and 6.2% for employees.

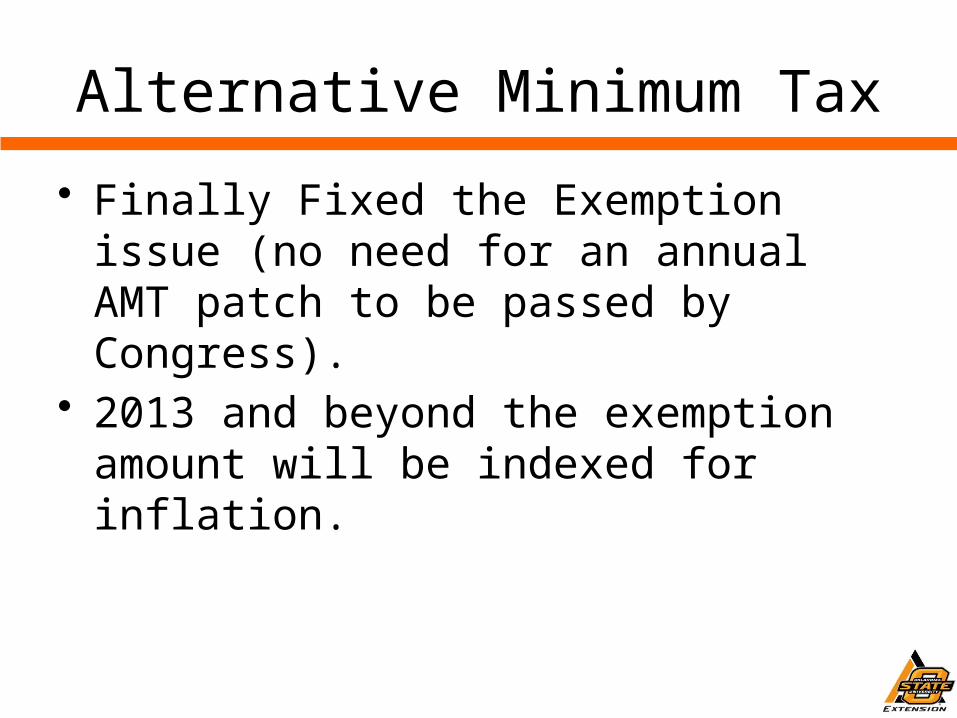

Alternative Minimum Tax

• Finally Fixed the Exemption issue (no need for an annual AMT patch to be passed by Congress).

• 2013 and beyond the exemption amount will be indexed for inflation.

Credits

• Adoption credit has been made permanent

• The $1,000 child tax credit for children under 17 has been made permanent

• Dependent care credit has been made permanent

• The simplified Earned Income credit has been made permanent

• American Opportunity (education) credit has been extended through 2018

Estate Taxes

• Rates:– 2013 & 2014 maximum rate is 40

percent• Exemption amount:

– 2013 exemption amount is $5.25 million

– 2014 exemption amount is $5.34 million

• The exemption amount is indexed for annual inflation.

Estate Taxes

• Portability between spouses made permanent– Husband and wife can transfer $10.68

million of assets free of estate taxation.– The unused estate tax exemption ($5.34

million) can be transferred from the deceased spouse and thus can be used by the surviving spouse when he/she passes.

Gift Taxes• Federal Gift Tax Exclusion (annual)

– 2013 & 2014 exclusion is $14,000 per person ($28,000 husband & wife using gift splitting)

• Gift Tax Rates:– 2013 & 2014 maximum rate is 40

percent • Exemption Amount (lifetime)

– 2013 exemption amount is $5.25 million – 2014 exemption amount is $5.34 million

• Indexed for inflation annually

Section 179 Expensing

• Purchased capital assets that are depreciable (new or used).

• 2013 was $250,000 with a $500,000 investment limit

• 2014 reverted back to $25,000 with a $200,000 investment limit. (Will Congress enact new legislation to modify this?)

Additional First-Year Depreciation

• 2013: 50% Additional First-Year Depreciation is allowed for qualifying property placed in service through 12/31/2013.

• Expired effective January 1, 2014

Contact Information

J C. [email protected]

580-237-7677

Oklahoma Cooperative Extension Service

Oklahoma State University

Related Documents