©2012, College for Financial Planning, all rights reserved. Module 9 Life and Health Insurance Foundations In Financial Planning SM Professional Education Program

©2012, College for Financial Planning, all rights reserved. Module 9 Life and Health Insurance Foundations In Financial Planning SM Professional Education.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

©2012, College for Financial Planning, all rights reserved.

Module 9Life and Health Insurance

Foundations In Financial PlanningSM Professional Education Program

Learning Objectives

9–1: Identify a type or use of group or individual life insurance.

9–2: Identify a feature or provision of a life insurance policy.

9–3: Calculate the amount of life insurance needed for a client’s financial situation.

9–4: Describe features of group, major medical, or comprehensive major medical insurance, including managed care plans.

9–5: Calculate expenses that may be incurred under group, major medical, or comprehensive major medical insurance coverage.

9–6: Explain features and terms of disability income insurance.

9–7: Explain features and terms of long-term care insurance.

9–8: Identify definitions or characteristics of an annuity.5-2

Questions To Get Us Warmed Up

9-3

Coverage in the Event of Death• Social Security• Group Life Insurance

o four types of coverageo no evidence of insurability (usually)

9-4

Basic Types of Individual Life Insurance

• Term• Whole Life• Universal• Variable• Variable Universal

9-5

Term Life Insurance

• Temporary coverage• Annual renewable term• Level premium term• Decreasing term

9-6

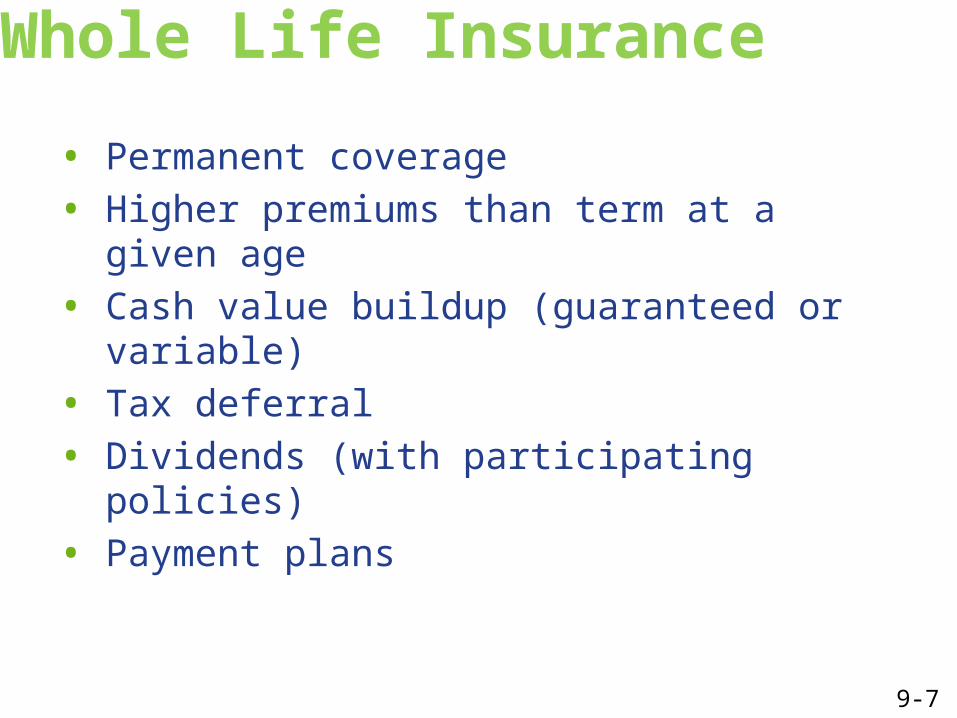

Whole Life Insurance

• Permanent coverage• Higher premiums than term at a given

age• Cash value buildup (guaranteed or

variable)• Tax deferral• Dividends (with participating policies)• Payment plans

9-7

Universal Life Insurance

Flexibility• Premium• Face amount of coverage• Cash value

Fluctuating interest rate• Danger of lapsing• Potential benefit of higher cash value

9-8

Variable Life Insurance

9-9

Life Insurance Features & Provisions

• Ten standard provisions• Other common provisions• Dividends

o taken in casho accumulate at interesto reduce premiumso paid-up additionso purchase one-year term

(5th dividend option)

9-10

Amounts of Life Insurance Coverage

Income-based method (human value)

• Estimate future average annual earnings

• Subtract expenses

• Determine number of productive years left

• Set discount rate

• Compute the present value

Needs-based method

• Determine needs (five categories)

• Determine available assets

• Needs – assets = insurance amount

9-11

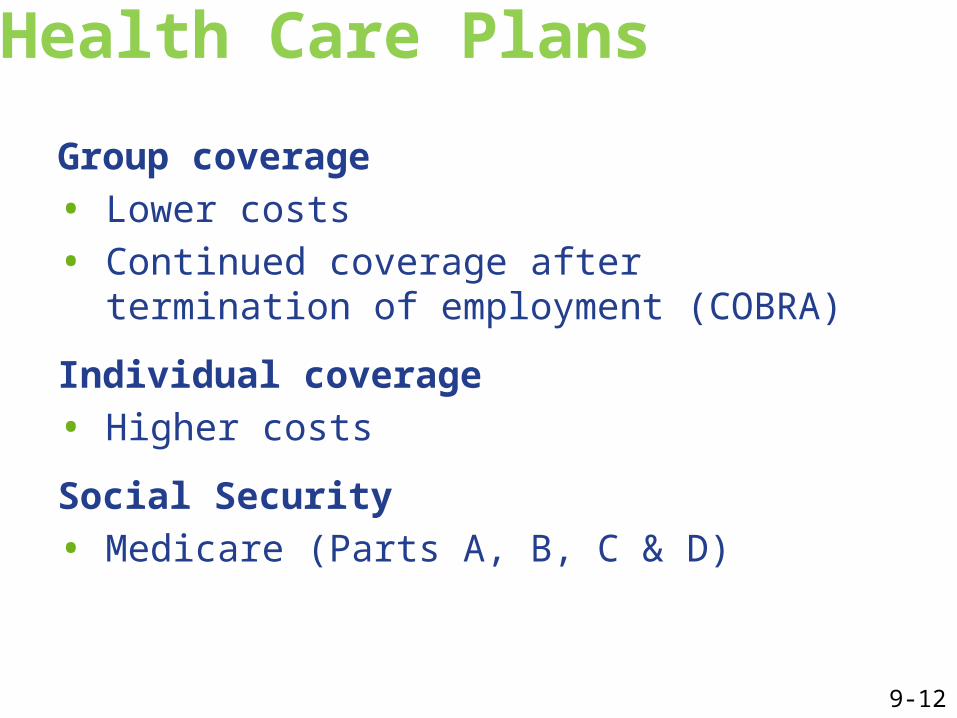

Health Care Plans

Group coverage• Lower costs• Continued coverage after termination of

employment (COBRA)

Individual coverage• Higher costs

Social Security• Medicare (Parts A, B, C & D)

9-12

Medical Expense Policies

• Major medicalo deductibleo coinsuranceo stop-loss limit

provision• Comprehensive major medical (combined

base plan and major medical): what most people think of when discussing major medical coverage

9-13

HMO, PPO & POS Plans

Health maintenance organizations • Preventive care emphasized• Gatekeeper concept

Preferred provider organizations• May or may not use a gatekeeper

Point of service plans• Greater flexibility• Benefits vary by the type

of service chosen

9-14

Coverage Decisions

• Costso deductibleo coinsurance

• Coordination of benefits• Level of benefits

o flexibility of doctor selectiono types of services neededo access to specialists

9-15

Disability CoverageSocial Security• Four requirements

o under age 65o disabled (or

expected to be) for 12 months

o filed an application for benefits

o has necessary quarters of coverage

• Definition (strict)• Waiting period

Workers’ Compensationo Coverage without

determination of fault

9-16

Other Types of Disability Coverage

• Group coverageo short termo long termo maximum monthly benefitso waiting periods

• Individual policieso COLA riders

9-17

Disability Income Terms

• Benefit amount

• Benefit period

• Elimination period

• Definitiono at any occupationo modified any occupation for which the

person might be qualified based on education, experience, or training

o own occupation

9-18

Disability Coverage Amounts• Insurance limitations• Monthly expenses• Cost of coverage• Business continuation• Business overhead expense

9-19

Long-Term Care

• Medicare (very limited benefit)o requires stay in

approved facilityo provides some home

care• Medicaid

• Individual policieso daily benefito elimination periodo benefit periodo activities of daily

living (ADLs)

9-20

Classifications of Annuities

9-21

Question 1

Which one of the following types of insurance should be used to provide insurance protection for a mortgage?a. term life insuranceb. paid up life insurancec. variable life insuranced. universal life insurance

9-22

Question 2

In seeking needed life insurance coverage in which participants can invest in broader investment markets such as equity or fixed income, you would suggest that a client consider which type of insurance?a. term life insuranceb. whole life insurancec. variable life insuranced. universal life insurance

9-23

Question 3

Which one of the following disability income categories would one be likely to find an insurance agent?a. blue collarb. white collarc. professionald. certified

9-24

Question 4

Which disability income insurance policy guarantees policy renewability, but has rates that can be changed; however, only for an entire rate class?a. cancellableb. noncancellablec. conditionally renewabled. guaranteed renewable

9-25

Question 5

Which one of the following is not an ADL (activity of daily living) in the standardized definition as put forth by HIPAA for policy qualification?a. eatingb. hearingc. bathingd. transferring

9-26

Question 6

An annuity that begins payments to the annuitant within 30 days of receipt must be which one of the following?a. deferred annuityb. refund annuityc. single premium annuityd. joint and survivor annuity

9-27

©2012, College for Financial Planning, all rights reserved.

Module 9End of Slides

Foundations In Financial PlanningSM Professional Education Program

Related Documents